Abstract

Related party transactions (RPTs) enhance firm value by reducing transaction costs under incomplete information but may harm firm value when used as an instrument for expropriating a firm’s wealth. Focusing on the worsening of agency problems due to political connection, we explore how the effects of RPTs on firm performance differ across firms based on their level of political connection. Using manually collected data on RPTs and the political connections of Indonesian listed firms from 2007 to 2018, we find that, on average, financial RPTs are negatively associated with accounting performance but positively associated with stock returns. This reflects the mixed evidence from prior studies that RPTs have both positive and negative consequences on firm value. We further examine whether politically connected firms are more likely to commit to value-destroying RPTs. We find that RPTs are negatively associated with stock returns specifically when a firm is closely tied to politicians or government officials. Overall, our findings suggest that political connection may facilitate value-destroying RPTs, muting their positive effects on firm value.

Plain Language Summary

This study explores how related party transactions (RPTs)—business deals between companies with shared ownership—affect the performance of Indonesian firms. The researchers analyzed data from companies listed in Indonesia between 2007 and 2018. They found that while RPTs often harm a company’s financial health (accounting performance), they can also lead to higher stock returns. However, in politically connected firms, RPTs tend to destroy value, significantly reducing stock returns. These findings suggest that political connections may enable the misuse of RPTs for personal gain, underscoring the need for strong corporate governance to protect minority shareholders and promote fair business practices in emerging markets like Indonesia.

Introduction

Related party transactions (RPTs) are transactions between two related entities, such as firms and their shareholders, board of directors, or affiliated companies. The effects of RPTs on firm value are so far unclear and inconclusive. On the one hand, RPTs may destroy firm value when used to control shareholders and managers to expropriate firm resources at the expense of minority shareholders (Chang & Hong, 2000; Johnson et al., 2000; Shin & Park, 1999). On the other hand, RPTs can enhance value as transactions among related parties reduce information asymmetry and incur fewer transaction costs (Khanna & Palepu, 1997; Williamson, 1975). In emerging markets with weak investor protection, minority shareholders are likely to suffer from the detrimental effects of RPTs (e.g., tunneling that refers to the transfer of resources out of a company to its controlling shareholder) more severely than in developed markets (Gao & Kling, 2008; Johnson et al., 2000). Hence, it is important to examine the impact of RPTs on firm performance and shareholder values in the context of emerging markets.

The effects of RPTs on firm value may depend on a firm’s governance structure (Abigail & Dharmastuti, 2022; Kang et al., 2014; Ma et al., 2013; Wong et al., 2015; Yeh et al., 2012), such as political connection that critically determines a firm’s behaviours and performance (Habib et al., 2017a, 2017b; La Rocca et al., 2022; Sun & Zou, 2021; L. Wang, 2015). Prior studies suggest that politically connected firms likely engage in value-destroying RPTs, facilitating the tunneling of resources (Ma et al., 2013). Politicians may use RPTs to transfer value from firms to their pockets or use firm resources to establish social relationships and build reputation (Ma et al., 2013; L. Wang, 2015). In Indonesia, where political connections in business are prevalent, RPTs can be driven by opportunistic managers or controlling shareholders and thus detrimentally affect firm value (Habib et al., 2017a, 2017b). This is because politically connected firms often receive preferential treatment, including government subsidies, bailouts, and easier access to financing. Research indicates that politically connected firms often receive significant benefits, such as preferential access to resources and favorable regulatory treatment (Faccio, 2006). These advantages can enhance the power and influence of the managers within these firms (Faccio et al., 2006). As a result, powerful managers, who are difficult to challenge or replace, may exploit their positions to conduct related party transactions that serve their interests, rather than those of the firm and its shareholders.

Our study examines the relationships among RPTs, political connections, and firm performance, focusing on Indonesian listed firms. Indonesia provides an interesting setting to examine these relationships, particularly given the increasing attention from global investors toward emerging markets. As global investors continue to expand their portfolios into emerging markets to capture higher growth opportunities and diversification benefits (Reuters, 2024), understanding the determinants of firm value in countries like Indonesia has become increasingly important. First, Indonesian firms have a concentrated ownership structure. Around 67% of the listed firms in Indonesia are family-controlled and have a large control-ownership wedge (Claessens et al., 1999, 2000; Darmadi, 2016). Severe agency problems between principal and minority shareholders are likely to result in value-destroying RPTs (Claessens et al., 1999; Kang et al., 2014). Second, Indonesia has many large conglomerates that actively engage in RPTs within affiliated groups (Al-Fadhat & Al-Fadhat, 2019; Brown, 2007). Although Indonesian firms often commit to RPTs for efficiency purposes (C. A. Utama & Utama, 2014), there still is a possibility that principal shareholders tunnel the wealth of minority shareholders, especially in firms with weak corporate governance (Claessens et al., 2000; Gupta & Maheshwari, 2022). Lastly, after the Suharto regime, which lasted for 32 years, many government-connected entrepreneurs became politicians (Habib et al., 2017a, 2017b). Politically connected managers significantly influence corporate strategy and firm decisions, increasing firms’ possibility of committing to RPTs for rent extraction. Collectively, the unique institutional features of the Indonesian market, combined with the growing global interest in emerging markets, provide a powerful setting to examine the combined effect of RPTs and political connection on firm performance. Our study aims to offer valuable insights not only for policymakers and practitioners in Indonesia but also for global investors seeking to better understand corporate governance risks and opportunities in emerging markets.

On one hand, the result of our study demonstrates that RPTs are negatively associated with accounting performance, measured by the return on assets, which reflects prior studies on RPTs as a means of tunnelling profits, undermining the firm’s operational efficiency (Cheung et al., 2009; Gupta & Maheshwari, 2022; H. D. Wang et al., 2019). On the other hand, we find that RPTs are positively associated with stock returns. This finding is consistent with Wong et al. (2015), who document that RPTs, on average, increase firm value.

Mixed findings on the relationship between RPTs and firm performance can be attributed to the failure to consider firm-specific circumstances (Abigail & Dharmastuti, 2022; Bona-Sánchez et al., 2017; Hendratama & Barokah, 2020). While some RPTs may have efficient contracting, other transactions may arise from agency problems under weak monitoring (Gupta & Maheshwari, 2022; Kang et al., 2014; Wong et al., 2015; Yeh et al., 2012). Managers or controlling shareholders in politically connected firms have the power to expropriate the wealth of minority shareholders (Ma et al., 2013; L. Wang, 2015). Since politically connected firms enjoy favorable regulatory treatment and government support (Faccio et al., 2006; Li et al., 2006; Sun & Zou, 2021), there are more opportunities to tunnel resources and profits without strong resistance from minority shareholders.

We find that the interaction term between RPTs and political connection has significant negative effects on stock returns. A sum of coefficients test reveals that the positive effect of RPTs on stock returns in the main test disappears when a firm is politically connected. This finding is consistent with Wong et al. (2015), that RPTs, on average, increase firm value, but such positive effects disappear when corporate governance is weak. Furthermore, this finding reflects investors voting with their feet by selling or refusing to buy the stocks of politically connected firms since these firms are likely to engage in value-destroying RPTs (Kohlbeck & Mayhew, 2010).

Our study contributes to the studies on the effect of RPTs on firm value and performance (Abigail & Dharmastuti, 2022; Hendratama & Barokah, 2020; Kohlbeck & Mayhew, 2010; Wong et al., 2015). While RPTs can be used for efficient contracting to enhance firm value, they can also tunnel and prop up firms with weak corporate governance (Cheung et al., 2009; Wong et al., 2015). Focusing on the political connections that increase the probability that top management and principal shareholders seek rent through RPTs, our results suggest that RPTs are perceived as value-destroying by investors when the firms are politically connected.

We also add to the studies on political connection and firm value (Akey, 2015; Faccio & Parsley, 2009; Ma et al., 2013). Political connection is a double-edged sword for minority shareholders. Firms can obtain better access to resources via political networks; however, connecting board members or managers may create agency problems (Ma et al., 2013). Our results reconcile these two opposing stances on political connection by showing that political connection itself has positive effects on accounting performance but simultaneously is detrimental to stock prices when it is likely to induce value-destroying RPTs.

We also contribute to the wider debate on corporate governance in emerging markets. The abuse of minority shareholders by controlling shareholders is more common in emerging markets with relatively weak investor protection from legal institutions compared to developed markets (Gao & Kling, 2008; Johnson et al., 2000). Moreover, the links between politics and business are deep-rooted in countries such as China and Indonesia. Our findings suggest that political connection can facilitate value-destroying RPTs at the expense of minority shareholders.

The remainder of our study proceeds as follows. Section II provides the institutional background of the Indonesian stock market. In Section III, we review the related literature and develop our hypotheses. Section IV describes the data sources, sample selection, and research design. Section V reports the empirical results, and Section VI concludes the paper.

Institutional Background

Corporate Governance in Indonesia

A concentrated ownership structure is commonplace in Asian countries (Claessens et al., 2000), including Indonesia, with around 67% of listed firms identifying as family-controlled (Claessens et al., 1999; Darmadi, 2016). Concentrated ownership can cause agency problems since controlling shareholders own a large stake of a company’s outstanding shares and influence firm decisions significantly. Claessens et al. (2000) document that the sizeable control-ownership wedge in Indonesia results in the expropriation of minority shareholders by controlling shareholders.

Indonesian firms have two-tier board systems. The directors are divided into two segments: the board of directors serves as top management, and the board of commissioners supervises the board of directors (Leuz & Oberholzer-Gee, 2006). The board of directors plays a central role in determining corporate strategies and investments. Considering its strategic importance, firms carefully select candidates for this position. As cited by Mulyani et al. (2016), the Asian Development Bank (2000) found that about 85% of controlling shareholders assign their family members to the board and management team. However, the regulatory body (i.e., Bapepam-LK) requires listed companies to employ at least one independent commissioner external to the firm who does not hold firm shares and does not have direct or indirect business relationships. The board of commissioners exercises significant influence on firm behavior as they monitor the corporate board and give strategic advice to the directors (Agrawal & Knoeber, 2001). Indonesian firms often bring in politically connected people as directors or commissioners (Leuz & Oberholzer-Gee, 2006).

Many Indonesian firms are large conglomerates and actively engage in RPTs within their affiliated groups (Brown, 2007; Darmadi, 2016). According to the Indonesian Financial Accounting Standards (Pernyataan Standar Akuntasi Keuangan or PSAK), which follow International Accounting Standards (IAS), No. 24, a related party transaction is defined as a transfer of resources, services, or obligations between related parties, regardless of whether a price is charged. Related parties refer to (1) when the entity and the reporting entity are members of the same group, (2) individuals (or close family members) with either direct or indirect voting rights for the reporting entity who have significant influence and control, (3) key employees or people who have the authority and responsibility for planning, leading, and controlling firm activities, (4) an entity that is a parent, subsidiary, associate, or joint venture of the reporting entity, or (5) an entity that is substantially owned by a person who is described as a related party, as mentioned above.

The regulatory body in Indonesia, Bapepam-LK, imposes several regulations to protect the interests of minority shareholders to mitigate expropriation and the negative impact of RPTs. Since 2000, listed companies have been required to disclose RPT information in financial statements, including assets, liabilities, sales, purchases that involve RPTs, pricing policies, transaction requirements, and reasons and assumptions for doubtful accounts of RPT receivables (Bapepam Rule VIII.G.7; S. Utama et al., 2010). In addition, if the transaction amount of an RPT account exceeds one billion Rupiahs (approximately US $110,000), the firm should disclose the amounts or balances separately and reveal the identity of the related party and their relation to the firm.

The Political Environment in Indonesia

Indonesia has been facing an interesting political environment since the Suharto regime (1966–1998), called the New Order era. The Suharto regime undertook large-scale development of natural resources, giving birth to economic oligarchies that emerged from the close relationship with the ruling regime. One of these is the Salim Group, Indonesia’s biggest conglomerate whose owner is a close ally of Suharto (Al-Fadhat & Al-Fadhat, 2019; Brown, 2007). Even after Indonesia shifted to reformation era, the economic oligarchies from the Suharto regime still exist even after the regime change. Leuz and Oberholzer-Gee (2006) find that the firm performance of politically connected firms depends on their connections to the government. For example, the Salim group obtained the exclusive right to do business in the western region, representing 80% of the domestic flour market. Comprising only three companies in 1957, the Salim Group grew to 427 companies in the early 1990s (IDEAS, 2020).

Before 2004 when Indonesia held its first direct presidential election, presidential roles were selected by the People’s Consultative Assembly (MPR), a legislative body of Indonesia. During their regime, many entrepreneurs became members of parliament who had significant power to appoint top bureaucrats, chiefs of the army and police, determine the budget (Habib et al., 2017a; Mietzner 2006), and assist firms in winning contracts from the government (Fukuoka, 2013). This power led to mutual relationships between political elites and business firms by appointing members of parliament to corporate boards. Politicians rely on businesses for donations to their parties, and the companies expect the parties to grant them government contracts or favorable policy treatment.

In sum, the Indonesian capital market features weaker protection for minority shareholders and firms engaging in frequent RPTs with affiliated groups. These unique characteristics give rise to potentially severe agency problems between controlling and minority shareholders. Controlling shareholders tunnel other investors’ wealth through RPTs, destroying firm value. Indonesian firms’ strong connection to politics, rising from the unique political history, as well as the prevalent tunneling renders an ideal setting to examine the interactive effects of political connection and RPTs on firm value.

Literature Review and Hypotheses Development

Related Party Transactions and Firm Performance

Two competing perspectives help explain firms’ commitment to RPTs. First, RPTs can be efficient contracting tools in an incomplete information environment (Ryngaert & Thomas, 2012; Williamson, 1979). Especially in less developed markets in emerging economies, transactions through market mechanisms may incur high transaction costs due to the less transparent information environment and weak legal institutions. In poor external markets, internal markets serve as efficient alternatives since related parties have less information asymmetry (Coase, 1937; Khanna & Palepu, 1997). For example, Indonesian firms often rely on related lending or borrowing that provides a lower cost of debt compared to external loans (Habib et al., 2017a, 2017b). According to this view, RPTs may improve firm efficiency, stabilize business relations, and thus reduce firm risks (Bona-Sánchez et al., 2017; Cook, 1977; Khanna & Yafeh, 2007). Supporting this notion, Wong et al. (2015) found that RPTs positively correlate with firm value.

On the other hand, RPTs can be used to tunnel resources from a firm to related parties (Johnson et al., 2000). In several emerging markets, where controlling shareholders exercise significant influence on firm decisions beyond their cashflow rights, controlling shareholders may use RPTs to siphon firm profits for personal benefit (Bae et al., 2002; Bertrand et al., 2002). Furthermore, in countries with large business conglomerates, such as Korea, firms may use RPTs to prop up underperforming affiliates (Bae et al., 2002; Cheung et al., 2009; Gupta & Maheshwari, 2022). Using RPTs to tunnel and prop is considered value-destroying as these transactions are not driven by economic reasons (Cheung et al., 2009), contributing to the empirical evidence that supports RPTs harming firm performance and value (Berkman et al., 2009; Cheung et al., 2009; Jiang et al., 2010; La Porta et al., 2003; H. D. Wang et al., 2019).

In this sense, predictions and empirical evidence on the relationship between RPTs and firm value (or performance) are inconclusive. Minority shareholders are subject to expropriation through tunneling but also gain from propping, implying that countervailing forces work together to determine RPTs’ effects on firm performance and value (Cheung et al., 2009). We develop our hypotheses in a null form:

Political Connection and Related Party Transactions

Some studies suggest that mixed findings on the effects of RPTs on firm value can be attributed to firms’ specific circumstances, such as corporate governance. The negative impact of RPTs on firm value is more pronounced with weak governance, such as a control-ownership wedge or government connections (Abigail & Dharmastuti, 2022; Kang et al., 2014; Ma et al., 2013; Wong et al., 2015; Yeh et al., 2012). In emerging markets, firms’ political connections are an important dimension of corporate governance that determine corporate strategy and investment decisions (Habib et al., 2017a, 2017b; La Rocca et al., 2022; Sun & Zou, 2021; L. Wang, 2015). In the Indonesian context, with broad political networks among businesses (Habib et al., 2017a, 2017b), we expect that political connection will significantly influence firms’ motives to engage in RPTs.

Although political connection provides benefits, such as preferential access to loans from state-owned banks or favorable regulatory and legal treatment (Faccio et al., 2006; Leuz & Oberholzer-Gee, 2006; Li et al., 2006), it may aggravate the misuse of RPTs. Political connection worsens controlling shareholders’ expropriation of minority shareholders (Cheung et al., 2006) because politicians may use RPTs to transfer value from firms to entities they own or use firm resources to establish social relationships (Ma et al., 2013; L. Wang, 2015). Controlling shareholders can exercise their power to extract rents without disruption when linked to government officials or politicians. For controlling shareholders and connected managers, RPTs provide a tractable channel to tunnel resources for personal benefit. Consistent with this notion, Habib et al. (2017b) found that politically connected firms in Indonesia engage in RPTs to a greater extent than their non-connected counterparts. Other articles also suggest that politically connected firms are likely to commit to value-destroying RPTs (Ma et al., 2013; L. Wang, 2015).

We expect that using RPTs to tunnel and prop up will be more pronounced with political connection, destroying a firm’s accounting performance. In addition, external investors (e.g., minority shareholders) will respond negatively to these tunneling activities under political connection by selling and refusing to buy these firms’ stocks (Kohlbeck & Mayhew, 2010).

Methodology

Sample Selection and Data Sources

We use data from Indonesian-listed firms from 2007 to 2018. Our sample period begins in 2007 as there is little information related to RPTs before 2007. The sample period encompasses two terms of the first directly elected president, Susilo Bambang Yudhoyono (SBY), who served from 2004 to 2014, and one term of the next elected president, Joko Widodo (Jokowi), who served from 2015 to 2019. The financial year 2019 is excluded from the analysis due to a change in the political regime with the election of a new government. In addition, starting in 2020, the Financial Services Authority of Indonesia, known as OJK (Otoritas Jasa Keuangan), implemented regulatory changes aimed at enhancing corporate governance, particularly concerning related party transactions. Here are some key aspects of these regulations. First, the regulation expands the definition of Affiliate Transactions to include any activity or transaction conducted by a public company or its controlled company with affiliates of the public company or affiliates of members of the board of directors, board of commissioners, major shareholders, or controllers, including transactions conducted for the benefit of these affiliates. Second, public companies are required to have adequate procedures to ensure that Affiliate Transactions are conducted according to generally accepted business practices. Third, financial institutions, under certain conditions, that engage in Affiliate Transactions or Conflict of Interest Transactions are exempt from the obligation to disclose information to the public but must still report to OJK. Last, public or controlled companies must follow Conflict of Interest (COI) procedures for transactions that are not Affiliate Transactions or COI Transactions but could disrupt the business continuity of the public company (OJK, 2020). Therefore, we chose 2018 as the end of the sample period as the relationships among RPT, political connection, and firm performance may be significantly different after 2019.

We manually collected financial RPT information (i.e., RP lending and borrowing) from firms’ audited financial reports. We retrieved the financial reports from the Indonesian Stock Exchange (http://www.idx.co.id/index-En.html) and supplemented this with the reports disclosed on each firm’s website, if available. We obtained financial statement and stock price information from Thomson Reuters Datastream and Worldscope databases.

We also hand-collected information on political connections. Following Habib et al. (2017a, 2017b), we define politically connected firms as firms with at least one large shareholder (controlling at least 10% of the votes directly or indirectly), board member, or commissioner who is: (1) a current or former member of parliament, (2) a minister or head of local government, or (3) closely related to a politician or party (spouse, child, or other intimate relatives). We collected the names of parliament members from the Indonesia House of Representatives (http://www.dpr.go.id/id/anggota/) and the names of government officials in the Cabinet Secretariat—the central government of Indonesia—from the Cabinet Secretariat of the Republic of Indonesia (http://setkab.go.id/en/profil-kabinet.html). The heads of local governments were compiled from Kementerian Dalam Negeri—the Ministry of Home Affairs in Indonesia (http://www.kemendagri.go.id/staff-directory/gubernur-dan-wakil-gubernur). We obtained information on family members or relatives by searching related news articles. With the collected data, we matched the names of parliament and cabinet members, and the heads of local governments, with the names of board members, commissioners, and controlling shareholders.

We initially began with firm-year observations of active firms listed on the Indonesian Stock Exchange from 2007 to 2018. We excluded observations without information on RPTs and financial statement variables. We further deleted the observations missing information on stock prices, leading to a final sample of 1,749 firm-year observations. Panel A of Table 1 exhibits the sample selection procedure. Panel B and C describe the sample distribution across industries and years, respectively. As shown in Panel B, the number of firms that disclose information on RPTs gradually increases. Panel C shows that some industries have more firms that disclose RPTs. We mitigate the concern that certain industries or years drive our results by including firm and year-fixed effects in our regressions.

Sample Selection.

Model Specification and Variable Measurement

To mitigate concerns that unobservable firm-specific characteristics endogenously determine political connection and firm performance, we employ firm fixed effect regressions (Wooldridge, 2010). To test hypothesis H1a on the relationship between RPTs and firms’ accounting performances, we estimate the following fixed effects regression, equation (1). We omit the intercept in the fixed effects regressions since firm fixed effects replaces the constant term:

where the dependent variable, ROA, is the return on assets, defined as earnings before interest, depreciation and amortization, and taxes divided by total assets. Following prior studies that measure the extent of RPTs with the sum of all RPT transactions (Kang et al., 2014; Kim et al., 2015), we define RPT as the sum of RP lending and borrowing scaled by total assets. We do not assign a signed prediction on the coefficient of γ1 since RPT can positively or negatively affect firm performance.

PCON is an indicator variable that takes 1 if a firm has politically connected board members, commissioners, and controlling shareholders in a year and 0 otherwise. We further control for time-varying firm characteristics that may influence accounting performance, such as financial leverage (Leverage), growth opportunities measured by market value of equity over book value of equity (MTB), firm size measured by natural logarithm of total assets (Size), audit quality (Audit_Quality), or ownership structures, including ownership concentration measured by the percentage of total shares owned by the five largest shareholders (OCON), government ownership (Gov_Own), and foreign ownership (Foreign_Own). Detailed definitions of variables are in Appendix A.

We regress equation (1) using the abnormal amount of RPTs (Abn_RP) that are not explained by economic and governance structures instead of total RPTs. Since RPTs can increase naturally in business, we expect that the “abnormal” portion of RPTs is more likely to be driven by opportunism than the predicted level of RPTs. To calculate the Abn_RP, we take the residuals from the estimation of the following equation (2). We estimate equation (2) under the assumption that the firms in a market share similar functions in determining the optimal level of RPTs. We allow different intercepts across industries and years by including industry fixed effects and year fixed effects:

To test H2a on the interrelation among RPTs, political connection, and accounting performance, we estimate the following fixed effects regression:

Since political connection increases the possibility that firms commit to value-destroying RPTs, we expect the coefficient of γ2 to be negative. Definitions of other variables are the same as explained above.

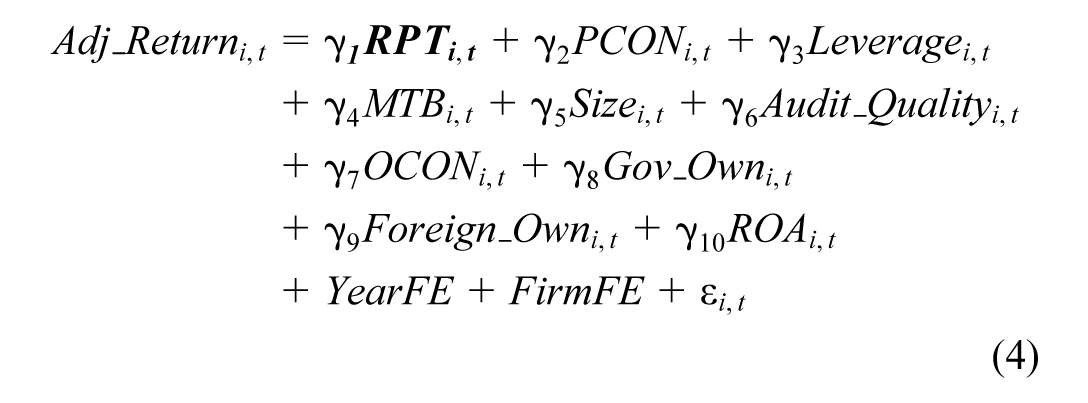

To test hypothesis H1b on the relationship between RPTs and stock returns, we regress the following fixed effects model:

The dependent variable Adj_Return is the industry-adjusted annual stock returns. We define the annual stock returns of a firm as {(stock price at year-end t + dividend per share)/stock price at year-end t−1}−1. We subtract the average stock returns of the same industry (excluding the focal firm’s stock returns) from the calculated stock returns. Since RPT can both positively and negatively affect firm value, we do not assign a signed prediction to γ1. We further control for the accounting performance (ROA) in the model since the market reacts to surprises in accounting performance.

Finally, to test H2b on the interrelation among RPTs, political connection, and stock returns, we estimate the following fixed effects regression:

Since politically connected firms are likely to commit to value-destroying RPTs, we expect the coefficient for γ2 to be negative.

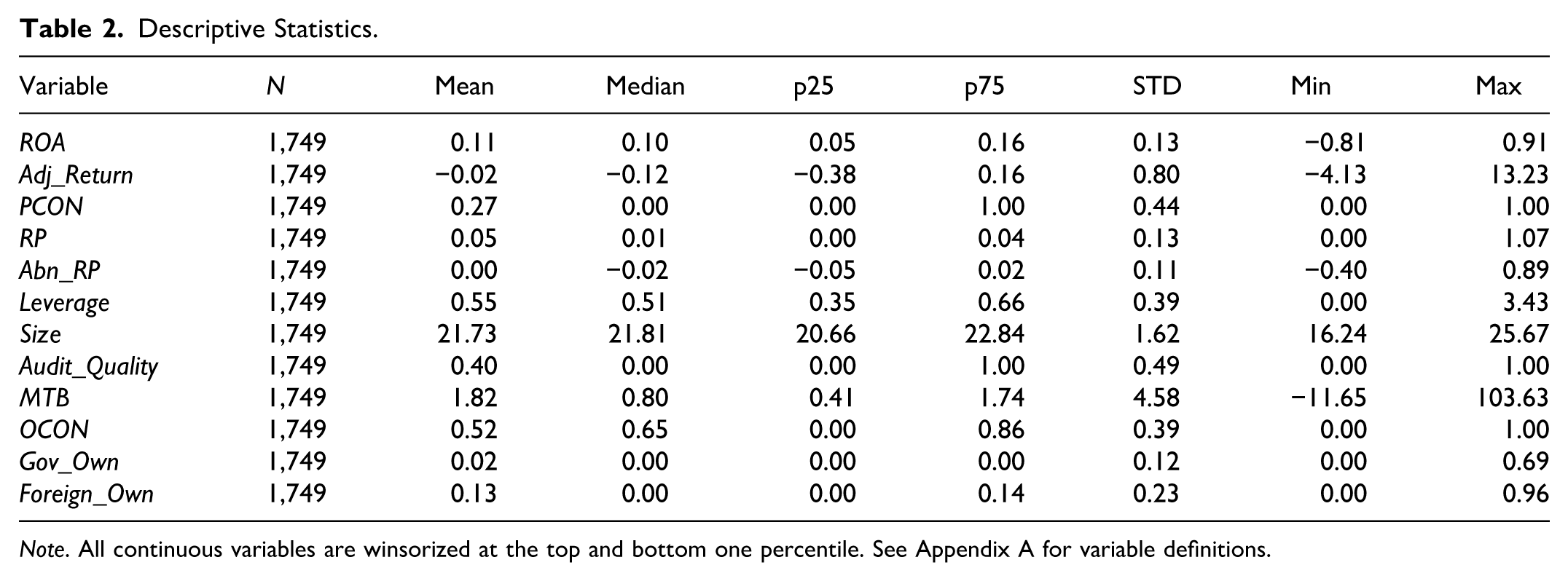

Table 2 shows the descriptive statistics for our variables. The mean return on assets is 11% for our sample observations, and the average industry-adjusted stock return is −0.02. In total, 27% of our sample observations have political connections. On average, (financial) RPTs account for 5% of total assets. The mean value of financial leverage is 0.55. Forty percent of our sample is audited by Big 4 auditors. Top-five shareholders of each firm hold about 52% of the total shares outstanding. The central government of Indonesia owns 2% of the total shares of each firm, on average. Foreign shareholders hold 13% of the shares.

Descriptive Statistics.

Note. All continuous variables are winsorized at the top and bottom one percentile. See Appendix A for variable definitions.

Table 3 exhibits the Pearson correlation coefficients among our variables. RPT negatively correlates with ROA and insignificantly correlates with Adj_Return. Abn_RPT negatively correlates with both ROA and Adj_Return.

Pearson Correlation Coefficients.

Note. Bolded are significant at the 5% level. This table presents Pearson correlations in the lower diagonal. All continuous variables are winsorized at the top and bottom one percentile. See Appendix A for variable definitions.

Empirical Results

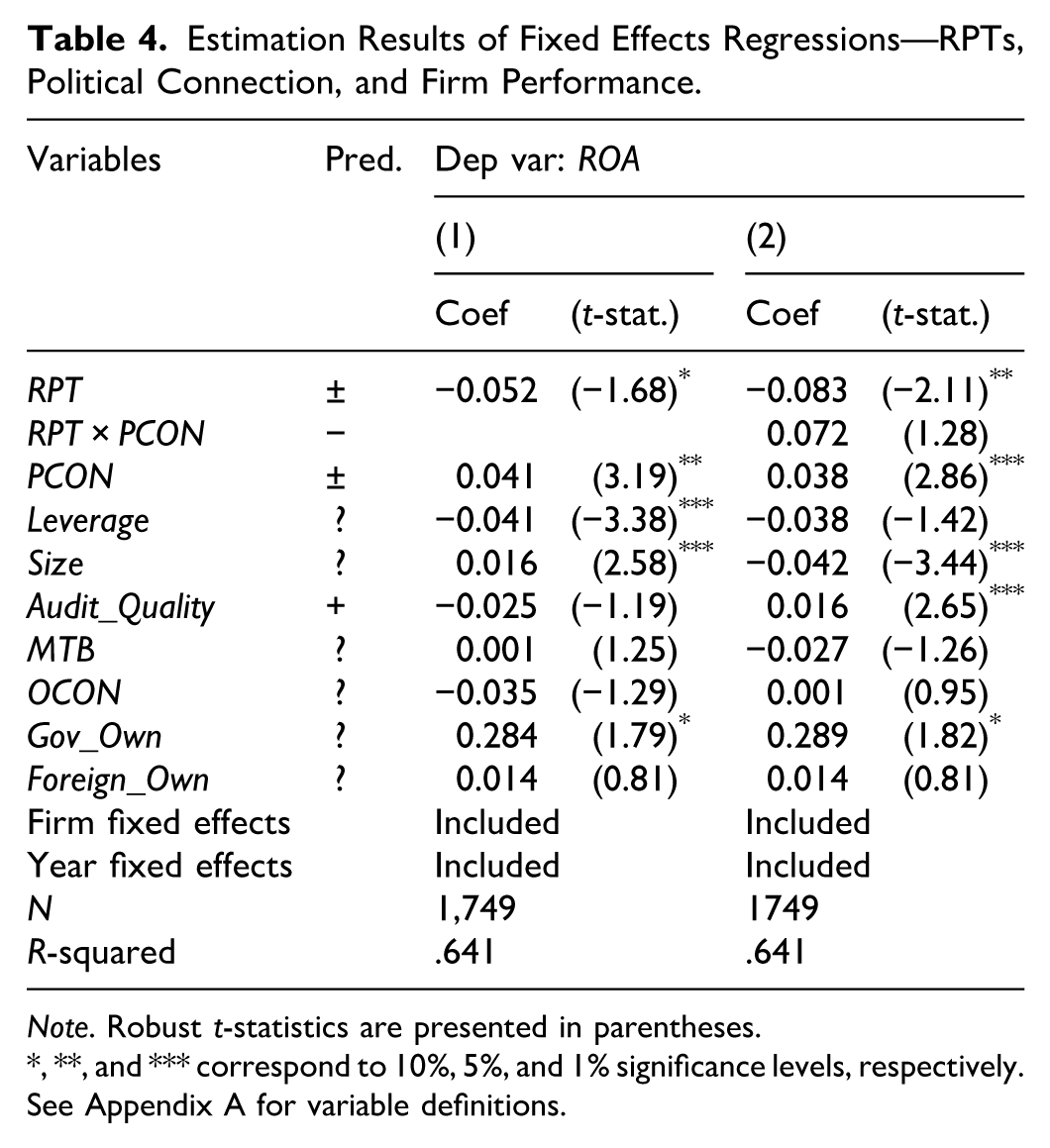

This section reports our empirical results. Table 4 shows the fixed effects regression results of equations (1) and (3). The dependent variable in both columns is the return on assets (ROA). We find that the coefficients of RPT are significantly negative in both columns, suggesting that the firm’s operating performance deteriorates as RPTs increase. In terms of economic significance, the coefficient on RPT is −0.052 (p < .1) in column (1), indicating that the increase in RPTs by 1% of total assets is associated with a decrease in average ROA by −0.052%, all other variables held constant. While RPTs may have positive and negative effects on firm performance, Table 4 suggests negative effects dominate accounting performance. This rejects the null hypothesis (H1a) that related party transactions are not associated with accounting performance. The finding is consistent with the prior studies that RPTs destroy firm value when used to control shareholders and managers to expropriate firm resources at the expense of minority shareholders (Chang & Hong, 2000; Johnson et al., 2000; Shin & Park, 1999).

Estimation Results of Fixed Effects Regressions—RPTs, Political Connection, and Firm Performance.

Note. Robust t-statistics are presented in parentheses.

, **, and *** correspond to 10%, 5%, and 1% significance levels, respectively. See Appendix A for variable definitions.

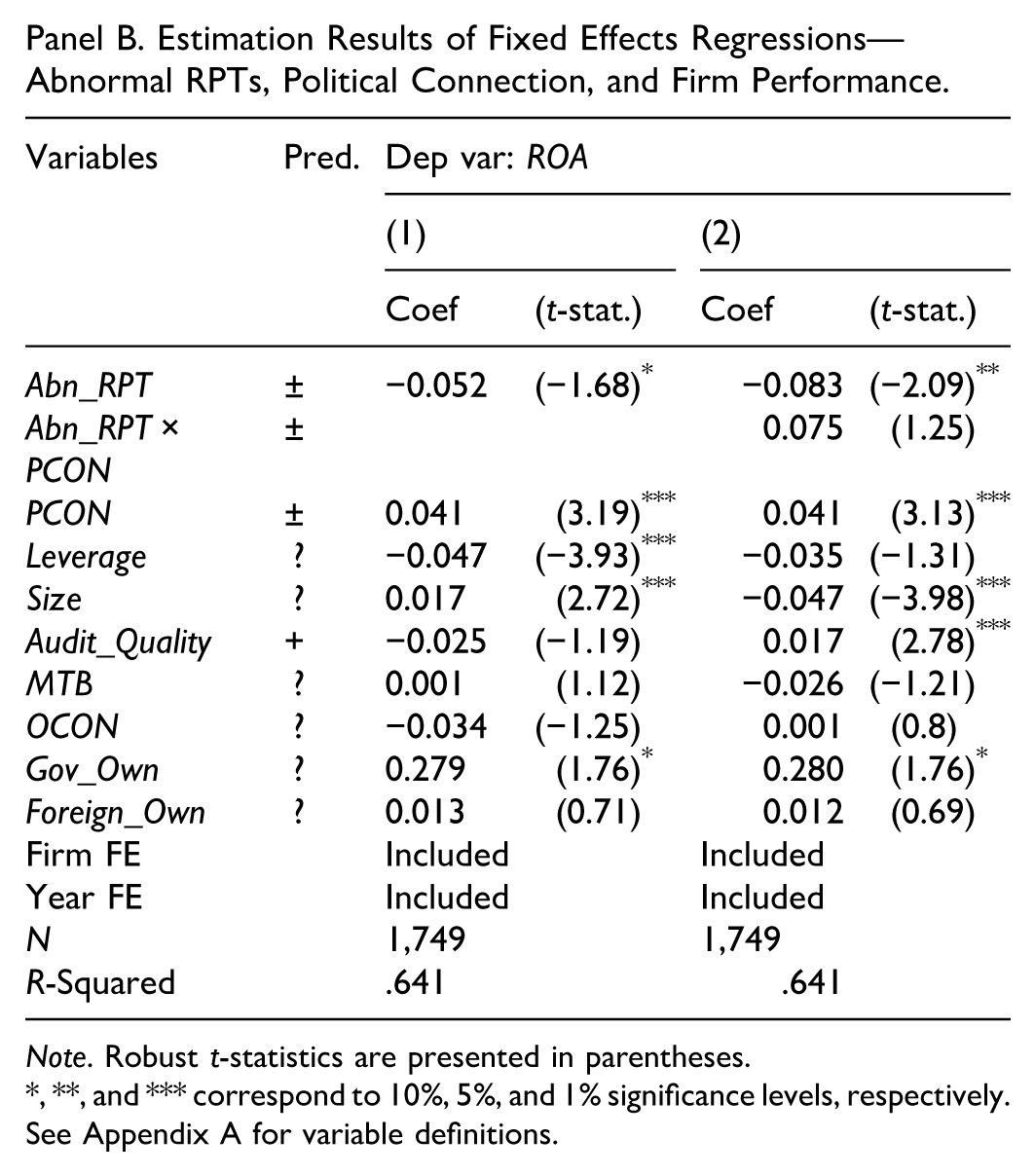

In Column (2), we find insignificant effects of the interaction term RPT × PCON on accounting performance, suggesting that the negative impacts of RPTs on accounting performance do not become aggravated or muted by political connection. One potential explanation for this is that political connections may have a more pronounced impact on long-term aspects of a firm’s performance rather than on short-term metrics like return on assets (ROA). Political connections might influence future profitability expectations, which are often reflected in stock returns rather than immediate accounting measures. Another possible reason for the insignificant interaction effect is that the total measure of RPTs includes both “good” and “bad” RPTs. “Good” RPTs may be economically justified and beneficial for the firm, while “bad” RPTs are likely driven by the personal interests of politically connected managers, potentially leading to value destruction. It is the “bad” or abnormal RPTs, those not justified by economic reasoning, that are more likely to have a negative impact on accounting performance through the political connection. To further explore this issue, Table 5 employs a determinant model of RPTs to separate abnormal RPTs from normal ones.

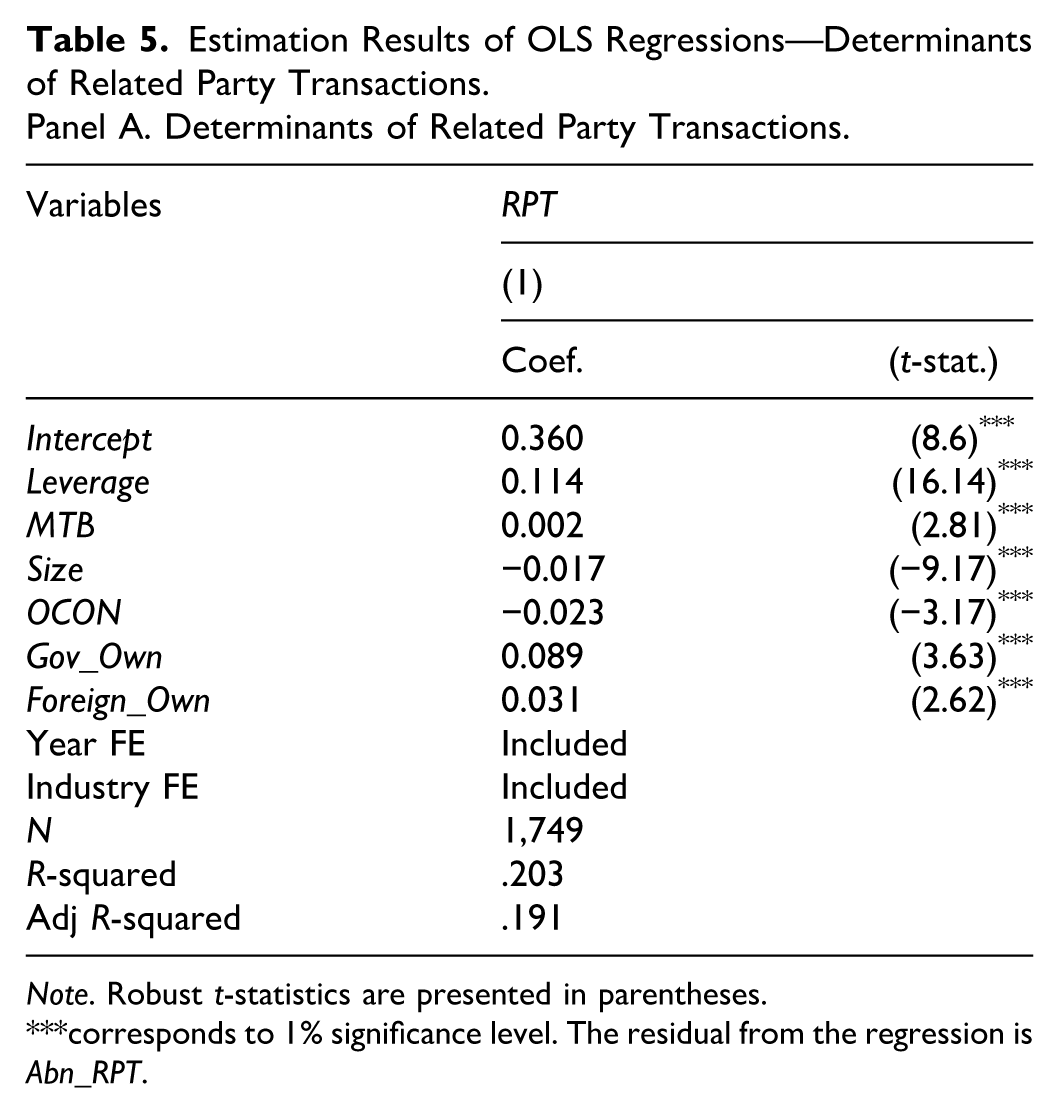

Estimation Results of OLS Regressions—Determinants of Related Party Transactions.

Panel A. Determinants of Related Party Transactions.

Note. Robust t-statistics are presented in parentheses.

corresponds to 1% significance level. The residual from the regression is Abn_RPT.

Panel B. Estimation Results of Fixed Effects Regressions—Abnormal RPTs, Political Connection, and Firm Performance.

Note. Robust t-statistics are presented in parentheses.

, **, and *** correspond to 10%, 5%, and 1% significance levels, respectively. See Appendix A for variable definitions.

Table 5 shows the results using abnormal RPTs instead of total RPTs. Since RPTs can be a natural part of business, the unexplained amount of RPTs should more precisely capture agency problems. To calculate the abnormal RPTs, we estimate equation (2), which includes firms’ fundamental characteristics. Panel A shows the estimation results of equation (2), and the residuals are the abnormal RPTs (Abn_RPT). Panel B reports the estimation results of equations (1) and (3) using Abn_RPT instead of RPT. We find similar results in Table 4. The analysis in Table 5, despite using abnormal related party transactions (Abn_RPT) to isolate the economically unjustified portion of RPTs, still does not reveal a significant moderating effect of political connections on the relationship between Abn_RPT and accounting performance (ROA). Political connections may exert a more significant influence on long-term strategic outcomes rather than short-term financial metrics. While ROA captures the immediate financial health of a company, it might not fully reflect the future risks and inefficiencies introduced by politically motivated RPTs (Bona-Sánchez et al., 2017; Wong et al., 2015). This could mean that political connections impact future profitability and risk, which might be more visible in metrics like stock returns rather than in current accounting performance.

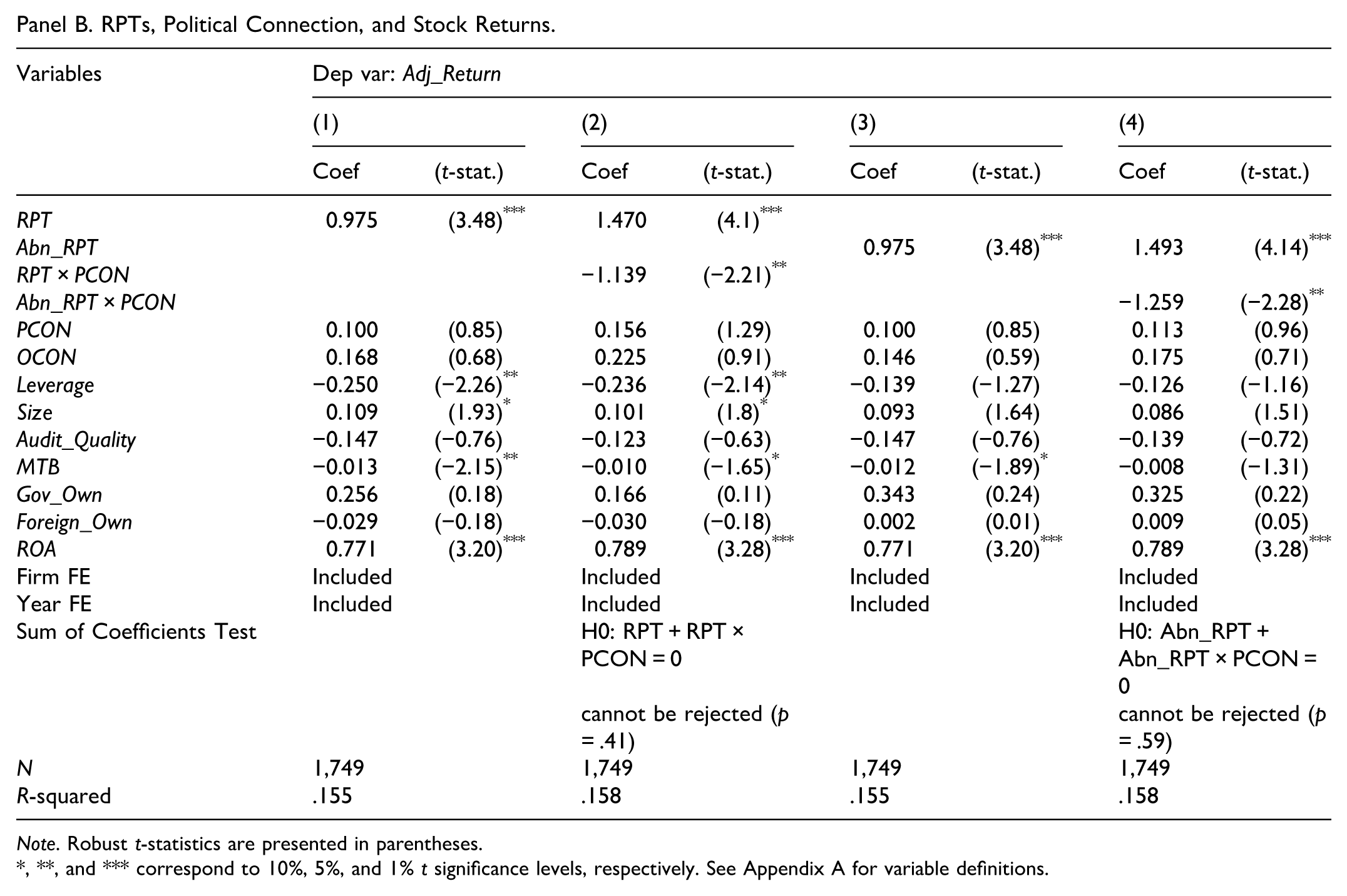

Table 6 reports the results of the empirical tests on the effects of RPTs on stock returns. In Panel A, we compare the stock returns of high and low RPT groups and divide each sample into politically connected versus non-connected firms. In the central column of panel A, we observe that high RPT groups exhibit higher industry-adjusted returns (−0.01 for high RPT groups and −0.04 for low RPT groups), implying that, on average, investors perceive RPTs as efficiency-improving transactions. There appears to be a perception that RPTs can be beneficial, possibly because they reduce transaction costs, stabilize business operations, or provide favorable financing conditions. This aligns with the theoretical perspective that RPTs can serve as efficient contracting mechanisms, especially in environments with incomplete information or high transaction costs (Bona-Sánchez et al., 2017; Cook, 1977; Khanna & Yafeh, 2007; Wong et al., 2015).

Related Party Transactions, Political Connection, and Stock Returns.

Panel A. Univariate Comparison of Stock Returns.

Panel B. RPTs, Political Connection, and Stock Returns.

Note. Robust t-statistics are presented in parentheses.

, **, and *** correspond to 10%, 5%, and 1% t significance levels, respectively. See Appendix A for variable definitions.

However, we find more interesting results when we divide the samples depending on political connection. High RPTs combined with political connection are associated with the most negative stock returns (average Adj_Return is −0.09 for the high RPT and political connection group), implying that investors perceive RPTs as most detrimental when the firms are politically connected. The stark contrast in stock returns between politically connected and non-connected firms with high RPTs suggests that investors do not view all RPTs equally. In politically connected firms, RPTs are more likely to be viewed as “bad” transactions, driven by personal interests rather than corporate benefit. This is likely due to the perceived lack of checks and balances that political connections might engender, allowing for more unchecked managerial or shareholder opportunism.

Regression-based tests exhibit similar results. Panel B shows the estimation results of equations (4) and (5) with a dependent variable of industry-adjusted annual stock returns (Adj_Return). We find that RPT is positively associated with Adj_Return in columns (1) through (4). This finding is consistent with Wong et al. (2015) that, on average, RPTs are value-enhancing.

However, the joint effects of RPTs and political connection are negative. For example, in column (2), the interaction term RPT×PCON is significantly negative (−1.139, p < .05). The sum of the coefficient tests reveals that the effects of RPT on Adj_Return when PCON = 1 are not different from zero (thus, it cannot reject the null H0: RPT + RPT×PCON = 0, p = .41). In other words, investors’ positive valuation of RPTs disappears when firms are politically connected. This result supports the notion that politically connected firms are likely to engage in value-destroying RPTs, tunneling the firms’ resources to minority shareholders, causing investors to vote with their feet, refusing to buy or sell such stocks.

Overall, the empirical results in Tables 4 through 6 suggest that RPTs may or may not be value-enhancing on average, as shown by their opposing effects on accounting performance and stock returns. However, when RPTs are combined with political connection, investors view them as value-destroying due to potential tunneling of resources and abuse of minority shareholders by controlling shareholders. However, our analyses of stock returns suggest that investors are wary of politically connected firms engaging in RPTs, viewing them as more likely to engage in value-destroying activities, such as tunneling—where controlling shareholders or managers divert resources from the firm to benefit themselves at the expense of minority shareholders. This negative perception leads investors to “vote with their feet,” meaning they may avoid investing in such firms or choose to sell off their shares, thus depressing the stock price.

Additional Analysis

Since politicians or government officials do not randomly select the firms they work for, there may be omitted factors that drive our results. In our main analyses, we mitigate this concern by controlling for firm fixed effects in every regression. However, some concern remains that politically connected firms differ from other firms, and these unique characteristics drive our results. For example, politically connected firms are riskier than non-connected firms, increasing the firm’s incentives to seek political support and decreasing stock returns simultaneously.

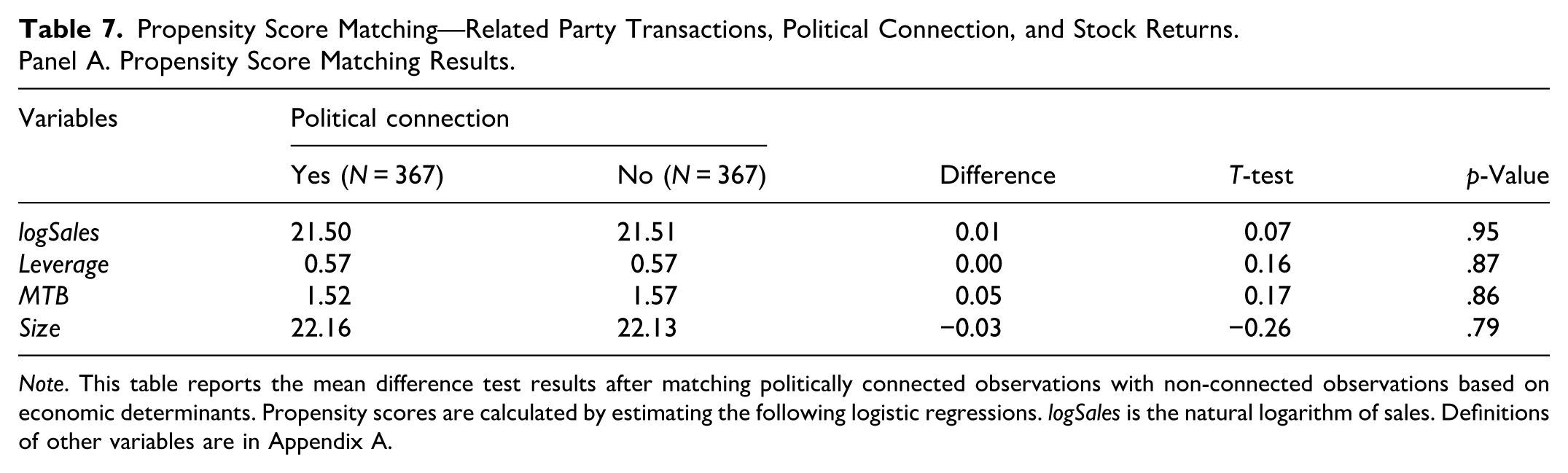

Hence, we conduct propensity score matching based on underlying risk factors influencing stock returns, such as financial leverage, market-to-book, size, and sales. We regress the logistic regression of the probability of political connection (PCON=1) on logSales, Leverage, Size, and MTB. Panel A of Table 7 shows the mean differences of matching variables between the politically connected and non-connected groups within the matched sample. The mean values of all the matching variables are not statistically different between the two groups.

Propensity Score Matching—Related Party Transactions, Political Connection, and Stock Returns.

Panel A. Propensity Score Matching Results.

Note. This table reports the mean difference test results after matching politically connected observations with non-connected observations based on economic determinants. Propensity scores are calculated by estimating the following logistic regressions. logSales is the natural logarithm of sales. Definitions of other variables are in Appendix A.

Panel B. Matched Sample—RPTs, Political Connection, and Stock Returns.

Note. Robust t-statistics are presented in parentheses.

, **, and *** correspond to 10%, 5%, and 1% significance levels, respectively. This table shows the estimation results of equations (4) and (5) using matched sample. See Appendix A for variable definitions.

Panel B reports the results of replicating Panel B of Table 6 with a matched sample (N = 734). We find qualitatively similar results in Table 6, mitigating concerns that underlying risk factors simultaneously drive stock returns and political connection.

We use the caliper distance of 0.01 and one-to-one matching without replacement.

Discussion

Our study examines the relationship between RPTs and firm performance, focusing on Indonesian listed firms. We show how the relationship between RPTs and performance differs depending on firms’ political connections. Using manually collected RPT and political connection data of Indonesian listed firms from 2007 to 2018, we document the following key findings. We first find that RPTs are negatively associated with accounting performance but positively associated with stock returns. Opposing effects on accounting and price performance reflect the prior studies that indicate that RPTs have either positive or negative effects on firm value (Chang & Hong, 2000; Johnson et al., 2000; Khanna & Palepu, 1997; Shin & Park, 1999; Wong et al., 2015).

Building upon studies that focus on firm-specific circumstances influencing the underlying motives of firms committing to RPTs (Kang et al., 2014; Ma et al., 2013; Wong et al., 2015; Yeh et al., 2012), we suggest that political connection influences how investors perceive RPTs. Our results show that investors react more negatively to RPTs in firms with political connections. This reflects that political connection gives controlling shareholders more opportunities to expropriate rent from minority shareholders without strong resistance when backed by political support (Ma et al., 2013; L. Wang, 2015).

Emerging economies often have weak protection for minority shareholders and strong links between politics and business. Weak corporate governance, combined with political connection, can significantly limit the positive functions of related transactions. Our study suggests an important implication that RPTs can be more value-adding when top management is independent of political influence and has less power to abuse minority shareholders.

This study investigates the effects of related party transactions (RPTs) and political connections on firm performance among Indonesian listed firms. The literature presents two contrasting views on RPTs: they can either enhance firm value by reducing transaction costs and information asymmetry or harm it by facilitating the expropriation of firm resources by controlling shareholders, especially in politically connected firms. Our findings align with these mixed perspectives, showing that RPTs negatively impact accounting performance but positively influence stock returns.

The paper extends the existing literature by focusing on the moderating role of political connections in the relationship between RPTs and firm performance. While previous studies have highlighted the potential for politically connected firms to engage in value-destroying RPTs, our research provides empirical evidence from Indonesia, a market characterized by strong political-business links and weak minority shareholder protections. We find that the presence of political connections exacerbates the negative effects of RPTs on stock returns, suggesting that investors are particularly wary of the governance risks associated with these firms.

Conclusion

Theoretically, this study contributes to the ongoing debate on the dual role of RPTs. It underscores that while RPTs can serve as efficient contracting mechanisms, they also pose significant risks of resource tunneling and value destruction, particularly in politically connected firms. This highlights the complex interplay between corporate governance, political connections, and firm behavior in emerging markets.

For practitioners and policymakers, our findings emphasize the need for robust corporate governance mechanisms to mitigate the risks associated with RPTs, especially in firms with political ties. Enhanced transparency, stricter oversight, and stronger regulatory frameworks are crucial to protect minority shareholders and maintain investor confidence. Firms should implement policies that ensure independent board oversight of RPTs and enhance the disclosure of such transactions.

Limitations

Despite its contributions, this study has several limitations. First, politicians or government officials do not randomly select the firms they become associated with. This non-random selection may introduce omitted variables that influence both political connection and firm performance. Although we include firm fixed effects to mitigate this issue, unobserved heterogeneity may still bias the results. Second, the study is based on data from Indonesian listed firms, whose political and institutional environment may not be representative of other countries. This limits the external validity of our findings. Third, the analysis depends on manually collected data on related party transactions and political connections from financial reports. These disclosures may be incomplete or inconsistently reported, potentially affecting the reliability of our measures. Fourth, our dataset covers the period from 2007 to 2018. Political and economic developments in Indonesia since then may reduce the contemporaneous relevance of our results. Finally, the low R¹ values reported in models such as Table 6 suggest that a substantial portion of firm performance remains unexplained, indicating that other omitted variables—such as macroeconomic shocks, industry dynamics, or internal governance mechanisms—may play a critical role.

Directions for Future Research

Future research could examine the impact of related party transactions (RPTs) and political connections in other emerging markets and developed countries to see if the findings from Indonesia are applicable more broadly. Comparing results across different political and regulatory environments could provide a deeper understanding of how these factors influence firm performance. Future studies could also differentiate between various types of RPTs (e.g., loans, asset sales, service agreements) to determine if certain types of transactions are more likely to be beneficial or detrimental to firm performance. To address the low R¹ problem, future research should explore additional variables, such as macroeconomic conditions, industry-specific factors, and firm-specific characteristics, to better understand the drivers of stock returns in politically connected firms. Finally, investigating the role of corporate governance mechanisms in mitigating the adverse effects of RPTs in politically connected firms could provide insights into how firms can protect minority shareholders and improve overall performance.

Footnotes

Appendix

Variable Definitions.

| Variables | Definition |

|---|---|

| ROA | ROA = EBITDA/total assets |

| Adj_Return | Annual stock returns—industry average annual stock returns (excluding the focal firm’s stock returns when calculating the average stock returns), where annual stock returns = {(stock price at year-end t + dividend per share)/stock price at year-end t−1}−1. |

| PCON | An indicator of 1 if a firm is politically connected. A firm is politically connected if at least one large shareholder (controlling at least 10% of the votes directly or indirectly), board member, or commissioner is (1) a current or former member of parliament, (2) a minister or head of local government, or (3) closely related to a politician or political party (spouse, child, or other immediate family). |

| RPT | (Loans to related parties + borrowings from related parties)/total assets |

| Abn_RP | Residuals from the regression of Eq(1) using RPT as the dependent variable |

| Leverage | Total liabilities/total assets |

| Size | Firm size, measured by natural logarithm of total assets |

| Audit_Quality | An indicator that takes 1 if a firm is audited by BIG 4 auditors (PwC, EY, KPMG, Deloitte) and 0 otherwise |

| MTB | Growth opportunities, measured by market value of equity/book value of equity |

| OCON | Ownership concentration, measured by percentage of total shares owned by the five largest shareholders |

| Gov_Own | Percentage of total shares owned by the central government |

| Foreign_Own | Percentage of total shares owned by foreign shareholders |

Ethical Considerations

This study does not involve any human subjects or biological participants. As such, ethical considerations pertaining to human subjects, confidentiality, informed consent, or potential harm do not apply to this research.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by 2025 Hongik University Research Fund.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data used in this study were manually collected from publicly available financial statements and disclosures of Indonesian listed firms from 2007 to 2018. The processed dataset compiled by the authors is not publicly available; however, it may be shared upon reasonable request to the corresponding author.