Abstract

Sustainability certifications have been introduced for the palm oil industry to ensure its sustainable operation and the production of highly demanded palm oil. At present, there are several sustainability certifications in the market, namely the Roundtable on Sustainable Palm Oil (RSPO), the Malaysian Sustainable Palm Oil (MSPO), and the Indonesian Sustainable Palm Oil (ISPO) certifications. As the crude palm oil (CPO) becomes the largest product been produced and exported in the palm oil industry, it is assumed that the major CPO producers would adhere to the call for sustainability practices by producing certified palm oil. However, the additional cost of acquiring sustainability certification might hinder them from doing so. Besides, it is unclear on the effect of these certifications on firm profitability since there are very few studies have provided quantitative evidence empirical research focuses specifically on the sustainability certification in palm oil industry context. Thus, this intends to fill this gap by examining the effect of local, that is, MSPO or ISPO and international, that is, RSPO certifications on the financial profitability of the world’s top 20 CPO producers which comprises of the leading global palm oil companies based in Malaysia and Indonesia for the period of 2013 to 2018. General Least Regression is employed due to the problems of non-normality of data, heteroscedasticity, and autocorrelation. The main variable under investigation in this study is RSPO, MSPO, and ISPO, proxied by dummy variable. The results showed no significant difference in profitability of locally certified and non-certified CPO producers. Meanwhile, CPO producers with international certification, that is, RSPO recorded reduced profitability of 5% compared to locally certified producers. Hence, the adverse effect of sustainability certifications calls for intervention from both Malaysian and Indonesian governments as well as palm oil authorities in the respective countries, for example, introduction of tax incentives and/or subsidies to compensate for the reduced profitability and the cost of certification.

Introduction

The palm oil global market is forecasted to exceed 85 million metric tons by 2024. The surge of demand for palm oil is driven by the increasing consumption for foodstuff and biodiesel production (Mutombo, 2018). In 2018, palm oil dominated global vegetable oil consumption at 40.7%, outranking soybean, sunflower, rapeseed, and other vegetable oils (Malaysian Palm Oil Board, MPOB, 2020a). Oil palm grows best in stable-warm areas with sufficient soil moisture all year round. The optimal temperatures for the cultivation of oil palm are 30 to 32°C for 80 days minimum. The ideal combination of soil, temperature, and rainfall frequency like in Indonesia and Malaysia make them the best place to grow the crop (Nambiappan et al., 2018). Palm oil is processed from fresh fruit bunch which turned into CPO, palm kernel oil, and palm crude kernel oil. CPO becomes the largest product been produced and exported in palm oil industry. Thus, CPO significantly contributes toward economic growth of producers’ countries. For instance, palm oil industry becomes the third largest contributor for Malaysian economy worth USD15.47 billion in 2019 (MPOB, 2020b).

The world’s largest palm oil producing countries are Indonesia (57%), Malaysia (27.7%), Africa (3.7%), and Thailand (3.2%) (Ganling, 2019). Meanwhile, in 2019, the top-three palm oil consuming countries are Indonesia, India, and the European Union (EU), making up approximately 19, 13, and 11%, of the world’s oil consumption, respectively (MPOB, 2020c). The aggressively increasing demand for palm oil has led to the massive development of palm oil producing countries which generated extensive positive social and economic benefits (Acosta & Curt, 2019). At present, there is an increasing demand for certified (sustainable) palm oil (CSPO) specifically from the EU (Chin, 2014; Lim, 2014; Noor et al., 2017; Teo, 2019). CSPO refers to palm oil that is operated and produced sustainably from the cultivation process up to the end products and certified by sustainability certification, for example, RSPO. For instance, CPET (2017) reported that in 2015, UK purchase of palm oil supported by RSPO certification have tripled since 2009—a rise of nearly 302,294 metric tons. Thus, this trend provides great advantages for certified palm oil producing countries like Indonesia and Malaysia exporting to the EU.

It is imperative for palm oil producers to fulfill the demand for certified palm oil to sustain their business as well keeping up with global sustainable development agenda, that is, Sustainable Development Goals (SDG). This is because sustainability certification emerges new governance model planning to promote sustainable in social, environment, and economic aspects. It helps to ensure the protection and conservation of wildlife as well as flora and fauna. The certification ensures palm oil industry use the sources efficiently; value added in labor benefits; reduce risk and strong corporate reputation. The need for sustainable palm oil is high since it can fulfill the increasing global food demand and poverty alleviation as well as safeguard the social interest and protect the environment and wildlife. As a result, not-for-profit organizations (NGOs), for example, RSPO and government agencies in Indonesia and Malaysia have taken actions by developing standards for the palm oil industry that address the legal, economic, ecological, and social requirements to produce certified palm oil, known as sustainability certifications (Brandi et al., 2013; Glasbergen, 2011). If properly applied, these certifications can help to minimize the negative impact of palm oil cultivation on the environment and communities in palm oil-producing regions.

There are several sustainability certifications in the palm oil industry. RSPO (2007) was the world’s first certification established as an actor to arrange and improve the condition of production in November 2007. RSPO supervises its members to comply with eight (8) principles and fulfill the criteria of certification. The potential benefits from RSPO include increasing the profits of its members, as certified palm oil will be sold at a higher price and thus enhance productions and sales (Preusser, 2015). Meanwhile, as the largest global palm oil producers, Indonesia and Malaysia have developed the ISPO and MSPO certifications correspondingly to signify good sustainable practices in their palm oil industries in line with the global standard of RSPO. The ISPO and MSPO certifications were introduced in 2011 and 2013 by the governments of Indonesia and Malaysia consecutively.

Based on the above discussion, it is assumed that the major CPO producers would adhere to the call to implement sustainability practices by producing certified palm oil. However, this condition puts pressure on CPO producers. Despite the high demand for certified palm oil from Western countries, there are additional costs that the CPO producers must account for to comply with sustainability certification. For example, the cost to obtain RSPO certification for plantation areas ranges from USD720 to USD900 per hectare (Ganeshwaran, 2017; RSPO, 2015). Altogether, the cost to maintain this certification is equal to USD204 million (Yusof & Yew, 2016). In the context of Malaysian sustainable certification, the range of total cost to obtain MSPO is from USD5,330 to USD278,591 (Ganeshwaran, 2017). The detail costs of MSPO are illustrated in Table 1 below:

The Costs of MSPO.

Source. Ganeshwaran (2017).

Note. The current exchange based on 11 March 2022 from MYR to USD.

Besides, certifying the palm oil produced is only a means to circumvent the pressure from the EU. Moreover, The Star (2019) reported that only half of the 13.6 million metric tons of certified palm oil was sold in April 2019. Concern among CPO producers arises because it is unclear whether these certifications will result in increased or decreased firm profitability. Therefore, this study aims to examine the effect of local (MSPO/ISPO) and international (RSPO) sustainability certifications on the profitability of the world’s top 20 CPO producing companies. This study will provide evidence on the adoption of local and international sustainable certifications in the palm oil industry. The study frames its analysis on the world’s top 20 CPO producing companies in 2018 which were the leading global palm oil manufacturers and exporters.

Even though there are a lot of studies on firm profitability and sustainable practices (Chen et al., 2016; Hafizuddin-Syah et al., 2018; Jafari et al., 2017; Lee et al., 2017; Tang et al., 2016), however there are only a few studies on profitability and sustainable practices in the context of sustainability certifications for the palm oil industry. In addition, the existing studies applied qualitative approach. Hence, this study fills the gap by empirically examining the effect of palm oil sustainability certification on the profitability of the world’s top 20 CPO producers.

This paper is organized as follows: Section 2 presents a review of relevant literature regarding the differences between ISPO and MSPO, the effects of sustainability certification on firm profitability, and the attributes of profitability. Section 3 discusses the methodology of this study including research design, empirical methods, sample size, and source of data. Section 4 discusses the empirical findings and, finally, Section 5 concludes this study.

Literature Review

MSPO and ISPO

There are five (5) themes for sustainable practices in agriculture industry namely, land management, waste management, advance technology, economic empowerment, and social inclusion (Abas et al., 2021). The study found that sustainability certification and its underlying principles is one of the methods to achieve all five themes of sustainability practices. As the largest global palm oil producers, Indonesia and Malaysia have developed the ISPO and MSPO certifications correspondingly to signify good sustainable practices in their palm oil industries in line with the global standard of RSPO. The sustainable certifications demonstrate the countries commitment toward safeguarding and enhancing the reputation of the palm oil industry by establishing national standards (Wijaya & Glasbergen, 2016).

The ISPO certification was first launched in March 2011 by the government of Indonesia (Staff, 2019) and Malaysia follow suit with the introduction of MSPO certification in November 2013. Both certifications are standards and legal frameworks developed by the government and are exclusive of any profit-earned purposes. ISPO is governed by the Ministry of Agriculture, the State Ministry for the Environment, the Ministry of Forestry, and the National Land Agency of Indonesia. Meanwhile, the Ministry of Primary Industries Malaysia is responsible for regulating matters regarding MSPO. ISPO is mandatory for all producer companies and smallholders in Indonesia (Indonesia Palm Oil Platform [InPoP], 2015) although requirements for each vary. Large producers were required to comply with the standard by 2014, or face penalty and risk losing their license to operate. Meanwhile, MSPO is also mandatory for the entire palm oil supply chain such as oil palm groups and stakeholders including small, medium, and large growers in Malaysia (Hemananthani, 2017).

Both certifications include seven (7) general principles with specific criteria and indicators that are used as a determinant of the compliance of its members. Any members that are unable to meet the requirements of the ISPO and MSPO through these principles will have their certifications suspended. The MSPO principles underline economically viable, socially acceptable, and environmentally sound practices. MSPO emphasizes more on sustainability through palm oil supply chains which are from the smallholders up to palm oil-based product producers (Kamaruddin, 2020; Mclnnes, 2017). For instance, MSPO adopts good agricultural practices (GAP) as a realistic approach in achieving environment sustainability. The palm oil players especially the smallholders will be exposed on how to use suitable fertilizers, proper harvesting technique, managing cost of production as well as track records (Senawi et al., 2019). This certificate will protect the oil palm cultivation and processing and help small Malaysian farmers to operate sustainably. Therefore, the establishment of MSPO is subjected to counter the negative perceptions from EU country on this traded commodity (Balu et al., 2018; Kushairi et al., 2018).

Meanwhile, the principles of ISPO appear to provide the least stringent overall protection for biodiversity (Hidayat et al., 2018). Owing to the newness of the ISPO and MSPO certificates in the market, some critics have been leveled at them. When looking from a transparency aspect, MSPO presents a low level of transparency; it hides the online complaints and the status updates of cases affecting the public (Benjamin, 2018). Besides that, the credibility of ISPO has been questioned since the government is perceived as having vested interests in the palm oil industry. Ivancic and Koh (2016) therefore suggested ISPO appoint a third party to prevent and conflict of interest.

The Relevance of Sustainability Certification to Firm Profitability

Garriga and Mele (2004) suggested that Stakeholders theory is a relevant theory for over decades to explain firm’s profitability and environment sustainability. This theory also becomes one of the most widely used theory to theoretically address the relationship between firm’s profits and its corporate social responsibility (Horisch et al., 2014; Mutti et al., 2012; Pfajfar et al., 2022). The theory suggests firms should taking into consideration the social issues in maximizing their profits (Freeman, 1984). This theory states that firm does not only focus on the shareholder’s wealth but also considers the “stakeholders” (Freeman, 1984). Freeman (1984) defines stakeholders as shareholders, employees, managers, society, customers, suppliers, media, and government. In short, firm should earn profits without ignores the value, quality, satisfaction, ethical, and moral actions demanded by the stakeholders (Florea & Florea, 2013). For instance, the shareholders desire to maximize their profits. The society need clean environment for their health and good life. The customers demand for certified sustainably products, while employees claim for high self-reward and benefits. Firms and stakeholder have interest affect each other. Business operations affect interests of multiple parties having stake in a business. Therefore, firms should not ignore the stakeholders’ expectation from their planning and policies (Murray & Vogel, 1997). Hence firms should maximize the profits in and improve their sustainability practices to achieve sustainability in a long-run motivation.

As there are numerous sustainability certifications in the market, a firm should choose the best scheme that would provide a return in investment and retain profitability (Benjamin, 2018), as profitability is a crucial point that shareholders and managers use to evaluate companies. Dangelico and Pontrandolfo (2015) asserted that firms that implemented environmental actions significantly improved their image and performance. For example, Palmer and Truong (2017) found that firms leveraging on green technology new product introduction (NPI) not only minimized environmental impact but also increased profitability. Chen et al. (2016), Hafizuddin-Syah et al. (2018), Lee et al. (2017), Saswattecha et al. (2017), Tang et al. (2016), and Tey et al. (2019) also support this finding. Meanwhile, a study by Tey et al. (2020) find interesting result where the timing of adopting a sustainable certification has a significant in affecting the palm oil companies’ performance in Malaysia. Palm oil companies that adopted RSPO certification at the beginning of its introduction obtained more financial advantage. This is because CPO’s premium price and its demand is higher during the early-stage introduction of RSPO. However, late adopter companies seem faced lower premium price of CPO and higher implementation costs.

Besides, firms with sustainability certification could enjoy many benefits. Based on a study by Gijs et al. (2015), firms with a Forest Stewardship Council certification received significant benefits such as tax incentives, research grants, and support from the government to directly increase their profits. A recent study by Preusser (2015) found a positive correlation between CSPO-certified plantation area and CPO price. Specifically, firms with at least 40% of plantation areas certified by RSPO had higher CPO prices compared to firms with 20% or less certified areas. This premium price helped offset the incurred costs of the certification (Rival et al., 2016). Moreover, the companies with sustainability certification signal that they are investing on sustainability certification for their sustainable practices. Ahmad et al. (2019) found that environmental disclosure that provide credible information to the investors tend to boost firm profitability. However, Pichler (2013) found that RSPO certification benefited only for export-oriented palm oil companies rather than plantation worker and smallholders.

In contrast, Noorhayati et al. (2016) discovered that compliance with palm oil sustainability certifications negatively affected a firm’s profitability, especially among exporter companies. The study found that certified palm oil was sold at the same price of non-certified palm oil. Thus, there was no extra profit to cover the additional costs of complying with sustainability certification. The adoption of environmentally sustainable supply chain management (SSCM) was found to not necessarily improve cost performance. Esfahbodi et al. (2016) found that SSCM positively increased environmental performance but not cost performance. Moreover, Yusof and Yew (2016) revealed that the subscription to RSPO certification adversely affected the economy due to the high cost incurred, lukewarm demand, and low sales from customers. Besides, a study by Asche et al. (2015) disclosed that consumers had a low interest to pay for certified food; they even questioned the credibility of the Marine Stewardship Council (MSC). Jafari et al. (2017) opined that there would be only small impacts on the major environment-economic variables in Indonesia under a scenario of moderate reduction in EU import demand, for example, due to sustainability concerns. It can, therefore, be concluded that, although ISPO has initiated a process of change, it has not yet developed its full potential. The main reason is that ISPO has a rather loose problem definition, a weak enforcement authority, and a reliability that is too low to convince (parts) of the global market (Hidayat et al., 2018).

Meanwhile, a study by Segarra-Oña et al. (2012) found that the economic performance of rural hotels in Spain was not impacted at all by the hotel sustainability certification, namely ISO 14001. This is because their environmental awareness was already at a high level compared to urban and beach hotels. Hotels in natural surroundings are essentially forced to respect the environment as part of their core concept. This study is supported by Vogelpohl (2021), Shahida et al. (2018), Nor et al. (2016), Morley, 2015, and Rahman et al. (2009). The studies emphasized that the government endorsed environment sustainability certification to meet domestic regulatory requirement that emphasizing sustainability in environment and social. Sarumpaet (2005) also found that the financial performance of Indonesian companies with excellent sustainability ratings was not significantly associated with their environmental performance. Green products or services are usually more expensive and are not favored by Indonesian consumers and this could affect a company’s financial performance since there are no incentives provided by the government. Besides, Fisher et al. (2017) opined that sustainability certification was not enough to serve as a ticket to tap the EU market. Sustainability certification was not developed for economic reasons but simply out of concern for the environment (Van Kooten et al., 2005). Nor et al. (2016), Rahman et al. (2009), and Shahida et al. (2018) discovered the same results.

Other Factors Affecting Firm Profitability

According to Adams and Buckle (2003), financial leverage indicates the ability of firms to manage their economic exposure to unexpected losses. A study on the impact of capital structure on the performance of firms by Ogebe et al. (2013) found that leverage had a negative and statistically significant relationship with firm performance. The study suggested that firms should use more equity than debt to finance business activities, also supported by Bayyurt and Orhunbilge (2007) and Chen et al. (2008). However, Ramasamy et al. (2005) found that leverage had a positive relationship with the financial performance of Malaysian palm oil companies because the firms expected to earn more than the cost of debt capital. A study by Ding and Sha (2011) and Zhang (2010) found that leverage could bring tax-sheltered benefit that would improve firm governance and firm performance.

Jose et al. (2010) used current ratio to analyze the efficiency of Chinese ports and found that a high current ratio indicated the good condition of the firm, as it shows that the firm could meet its liquid liabilities. Adlina (2015) explored the determinants of profitability of Malaysian public listed companies during financial crises and found similar results, that is, liquidity positively affected the profitability of companies during financial crisis. However, Wei (2012) found that liquidity had no effect on the financial performance of listed agricultural companies in China because agricultural firms were not as effective at paying back short-term debt compared to long-term debt.

According to Salim and Yadav (2012), larger companies have more extensive abilities and enjoy economies of scale that are good for their profitability. Meanwhile, smaller companies have limited sources of financing and prefer internal financing over external debts due to its higher associated cost and risk (Abor & Biekpe, 2009). This result is supported by the trade-off theory that suggests that larger firms tend to borrow more due to their ability to diversify risk. Muritala (2012), Wang (2013), and Rahim (2013) also obtained the same result, finding that firm size had a positive relationship with firm profitability. However, Ramasamy et al. (2005) found that firm size was less significant and had a negative correlation with profitability because larger firms are generally more difficult to manage and have decreased organizational effectiveness.

Companies with a high growth rate could also be in high debt (Tian, 2007), so banks would be willing to lend money to companies with a good growth rate (Rahim, 2013). Large firms with a low growth rate have better opportunities to borrow long-term debt because they are deemed to be a less risky option (Barclay & Smith, 1995). Ramasamy et al. (2005) revealed that growth rate had a positive correlation with the profitability of palm oil companies because a growth rate will increase the good impression toward the firm, a result that is also supported by Yolanda and Soekarno (2012).

The annual average CPO price has a positive relationship with profitability since it is externally determined by the world market and would, therefore, affect the performance of the firms, where the higher the price, the higher the profits (Ramasamy et al., 2005). Meanwhile, fluctuations in price will improve business risk and reduce tax charges (Deng & Luo, 2009). Some studies have applied the consumer price index (CPI) to measure inflation. Booth et al. (2001) showed that a high inflation rate (high CPI) caused the firm performance to, increase because of the low debt level of the firm.

Based on the above discussion, it is apparent that most of past studies centered on the effect of sustainability certifications of other than palm oil industry (Esfahbodi et al., 2016; Ferron, 2012; Gijs et al., 2015; Segarra-Ona et al., 2012; Yusof & Yew, 2016). There is no empirical evidence on the effect of palm oil sustainability certification on firm profitability which the present study expect to fill in the research gap.

Methodology

Data Analysis Method

This study aims to examine the effect of local and international palm oil sustainability certifications on the profitability of the world’s top 20 CPO producing companies. According to Gogtay et al. (2017), to evaluate relationship between dependent an independent variable, a regression analysis is the best statistical tool. Since the study has more than one independent variables, a multiple regression analysis is conducted in this research to analyze the effect of local and international sustainable certification on the financial profitability of the world’s top 20 CPO producers. A panel data model was employed as the Ordinary Least Squares (OLS) might be irrelevant for panel data analysis due to the problem of non-normally distributed data, heteroscedasticity, and autocorrelation (Gujarati, 2003). Therefore, the White test and the Wooldridge test were conducted to detect the problems of heteroscedasticity and autocorrelation subsequently. Accordingly, the study used a quantitative approach and adopted the base regression model by Noorzaleha (2011) and Ramasamy et al. (2005), which also studied the profitability of palm oil companies. These previous studies appointed return on assets (ROA) as a proxy for financial profitability that also served as the dependent variable of each model. ROA has been widely used as a variable to measure profitability (Azhagaiah & Deepa, 2012; Bayyurt & Orhunbilge, 2007; Wei, 2012). ROA is measured by dividing earnings before interest (EBIT) with total assets. EBIT is more relevant as a nominator since the sample size consists of foreign shareholders (Myšková & Hájek, 2017; Strouhal et al., 2018). This ratio allows firms to measure operating efficiency in earning profit from their assets. This is because the nominator of EBIT ignores tax burden and interest expenses. This ratio also represents a pure measure of true ROA (Damadaran, 2001). Therefore, the firms will be able to determine whether they are using the assets effectively as compared to before.

Specifically, the study develops a regression model to identify the effect of local and international sustainable certifications on the profitability of the world’s top 20 CPO producing companies obtained from Palm Oil Analytics (2018). Palm Oil Analytics is an independent publisher of palm and lauric oil price, news, data, and analytics covering major origin and destination markets. Based on model by Ramasamy et al. (2005) and Noorzaleha (2011), this study introduces new variables, that is, LCERT and ICERT. LCERT variable represents local sustainability certification which is MSPO or ISPO. Meanwhile, the variable of ICERT refers to international sustainability certifications which is ISPO. The local and international sustainability certifications are represented by a dummy variable, which takes the value of 1 if the world’s top 20 CPO producers companies adopted MSPO, ISPO, and RSPO, otherwise 0.

The other independent variables are leverage (LEV), liquidity (LIQ), firm size (SIZE), sales growth (GRO), and CPO price (P). These variables serve as control variables, as the study aims to control the exogenous and endogenous influences of the variables that have an impact on firm profitability (Atinc et al., 2012; Carlson & Wu, 2012; Spector & Brannick, 2011). The regression model of the study is outlined in the following paragraphs.

where,

Data Collection Method

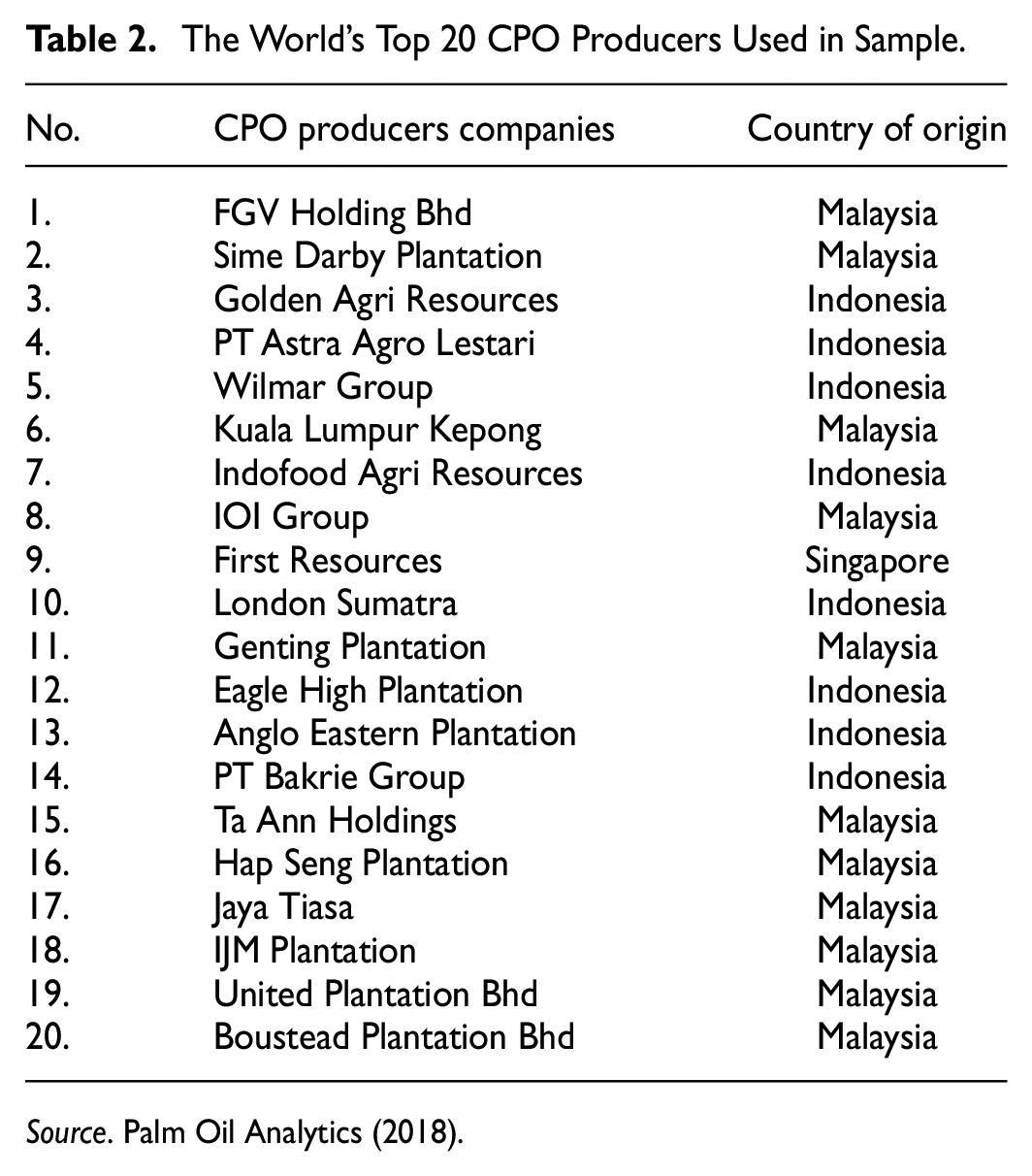

The sample consist of the world’s top 20 CPO producing companies in 2018, which comprises of the leading global palm oil manufacturers and exporters. Most of the companies are based in Indonesia and Malaysia. Indonesia remains to be the world’s largest producer and consumer of palm oil in which, central to Indonesian economy. Meanwhile, as the world’s second-largest producer and exporter of the palm oil and palm oil products, Malaysia plays a vital role in achieving the rising global need for oils and fats (Council of Palm Oil Producing Countries [CPOPC], 2022). The study only focused on the top 20 companies due to availability of data (refer Table 2). Besides, CPO is the largest product been produced and exported in palm oil industry as compared to palm kernel oil, processed palm oil, and crude palm kernel oil. The period of study is from 2013 to 2018 (6 years), as ISPO and MSPO was introduced in Indonesian and Malaysian palm oil industry in 2011 and 2013 respectively. The secondary financial data of ROA, leverage, liquidity, firm’s size, and sale’s growth were obtained from (then) Thompson Reuters Datastream database. Currently the database is known as Refinitiv Datastream™. Meanwhile, the list of the world’s top 20 CPO producers was obtained from Palm Oil Analytics. Table 2 shows the list of world’s top 20 CPO companies. The membership of MSPO and RSPO were obtained from the respective websites while the ISPO membership was retrieved from the annual report and sustainability report of the companies.

The World’s Top 20 CPO Producers Used in Sample.

Source. Palm Oil Analytics (2018).

Empirical Findings

Descriptive Statistics

The White-test and the Wooldridge test were conducted to detect heteroscedasticity and autocorrelation problems. The results of the White test in Table 3 (χ2: 62.81; p-value: 0.0013) showed that the χ2 was significant at 5% significance level. Therefore, this study rejected the null hypothesis that indicates a heteroscedasticity problem. In other words, the data in this study has an autocorrelation problem. Based on Table 4, the results of the Wooldridge test (F-stat: 43.93, p-value: 0.0000) were significant at the 1% level, demonstrating the presence of autocorrelation. Therefore, this study employed the Generalised Least Square (GLS) estimation as remedy for the problems, as suggested by Atanlogun et al. (2014) and Wooldridge (2002).

White-Test.

Wooldridge-Test.

Next, Table 5 presents the mean, standard deviation, skewness, and kurtosis of the study. Data is considered as normally distributed if the skewness is close to 0, and the kurtosis value is close to 3 as suggested by Park (2015). Results in Table 5 shows that only variables of LCERT, ICERT, SIZE, and P were normally distributed, as their skewness and kurtosis values were close to 0 and 3, respectively. It is important to have normality data distribution as it allows for reliable explanation and inference (Razali & Wah, 2011), otherwise, serious bias and less meaningful findings will result (Van et al., 2012). Since the assumption of normality data distribution in this study was violated, the OLS estimation method will not be able to produce reliable results. Therefore, the GLS method was found more appropriate for application in this study (Gujarati, 2003; Hsiao, 2007; Wooldridge, 2002). Hence, this study used the GLS estimation to cater to the non-normality of data.

Descriptive Statistics.

Pearson Correlation Matrix

As the study has many independent variables, that is, SUSC, SUSC2, LEV, LIQ, SIZE, GRO, and P, a multicollinearity problem may exist. The problem of multicollinearity presents when the independent variables are severely related to each other. The presence of multicollinearity violates the assumptions of OLS and will lead to a coefficient estimation bias. The estimation for the standard error of the regression coefficient could be increased and the sign of the relationship for the variables might be incorrect and underestimated (Yoo et al., 2014). The Pearson’s correlation result is shown in Table 6 below. The correlation coefficient of each variable was well below 0.8, indicating the absence of a severe multicollinearity problem. Thus, all the independent variables in this study were included in the regression, that is, no variables were omitted.

Pearson’s Correlation.

Regression Results

This study investigated the effect of local and international palm oil sustainability certification on the profitability of the world’s top 20 CPO producers. A regression model was developed to meet the objectives of the study. The model was regressed using GLS estimations due to the problems of non-normality of data, heteroscedasticity, and autocorrelation inherent in this study. Table 7 below reports the GLS estimation result that examined the effect of local (ISPO or/and MSPO) and international (RSPO) sustainability certifications.

The GLS Estimation Result.

Note. Value in the parentheses is the standard errors (SE).

Significant level at 1%, ** at 5%, and * at 10% respectively.

In GLS estimation, the goodness of fit was measured by employing the Wald test (Magee, 1990). In Table 7, the results of the Wald test shows that χ2 was significant at the 1% level (χ2 = 43.63, p-value = 0.0000), demonstrating that all the variables should be included in the model. The regression result showed that there was no significant difference in the profitability between locally certified and non-certified producers after controlling LEV, LIQ, SIZE, GRO, and P. Surprisingly, ICERT was negatively correlated to ROA at 5% significance level, after controlling LEV, LIQ, SIZE, GROWTH, and P. This result indicates that the world’s top 20 CPO producers that are certified with RSPO bear 5% losses compared to non-certified producers. Meanwhile, although LEV is highly significant, its effect on ROA was rather minimal, only 0.08%. LIQ was positively significant, indicating that if the producers increased their liquidity ratio by 1%, their profit would increase by 2.3%. The variable of SIZE showed a positive relationship with the profitability of the world’s top 20 CPO producers, signifying that a 1% increase in size will increase ROA by around 0.9%.

The result above reveals that the local sustainability certifications of MSPO and ISPO had no significant effect on the profitability of the world’s top 20 CPO producers. In this regard, the finding is consistent with that of Nor et al. (2016), Rahman et al. (2009), and Shahida et al. (2018), which revealed that sustainability certification did not significantly affect firm profitability. This is because MSPO and ISPO are developed to meet domestic regulatory requirement that emphasizing sustainability in environment, social, and legal perspectives (Morley, 2015; Vogelpohl, 2021). In this case, the world’s top 20 CPO producers become socially and environmentally responsible by adopting ISPO or/and MSPO due to the legal pressure exerted by the government (Daddi et al., 2011; Hinkes, 2020; Sarkar, 2008). Moreover, both certifications, that is, ISPO and MSPO are mandatory for palm oil players that operate only in Indonesia and Malaysia. The reason for this action is to guarantee that palm oil and its related products are sustainably produced. The certification also acts as a tool for countering the negative perception toward the palm oil industry (Palmer & Truong, 2017; Preusser, 2015) especially among European market (Aziz et al., 2021; Kushairi et al., 2018). The non-adoption of these certifications will incur penalties and will subsequently affect the firm’s reputation. Thus, it is crucial for the world’s top 20 CPO producers to adopt ISPO and/or MSPO for the sake of preserving their good image and reputation (Naidu & Moorthy, 2021).

Meanwhile, international sustainability certification, that is, RSPO is significantly reduces the profitability of the world’s top 20 CPO producers. It was found that these producers had to bear 5% losses when they complied with the RSPO principles. This finding is consistent with that of Noorhayati et al. (2016), who also discovered that the certification of palm oil had a negative effect on the profitability of exporter companies. The world’s top 20 CPO producers were unable to make profits due to the high costs of complying with RSPO and the lukewarm sales from consumers (Asche et al., 2015; Yusof & Yew, 2016), owing to the premium price of certified palm oil, higher than that of non-certified palm oil. The high price is not favored by consumers especially Indonesians, so the CPO producers’ financial profitability is greatly affected (Sarumpaet, 2005; Yusof & Yew, 2016). Moreover, RSPO only helps improve environmental performance but not cost performance (Esfahbodi et al., 2016). Only the EU requires certified palm oil and no other countries (Jafari et al., 2017). Thus, the world’s top 20 producers can seek out other alternatives to sustain their profits. For instance, they could channel their palm oil supply to other importer countries that do not demand certified palm oil. In fact, sustainability certification was developed to respond to the pressure of environmental concerns and not for economic reasons (Van Kooten et al., 2005). Thus, complying with RSPO principles only serves to encourage CPO producers to take environmentally sustainable actions.

Leverage showed a significant and positive relationship with firm profitability. A high leverage ratio correlated to the ability of a firm to manage its economic exposure to unexpected losses. This study is consistent with that of Ding and Sha (2011) and Zhang (2010), who also found that leverage could bring tax-sheltered benefit, which, in turn, improved firm governance and firm performance, that is, when the firm expects to earn more than the cost of debt capital, the firm’s venture into borrowing capital will increase. Based on the trade-off theory, high leverage could drive the firms to bankruptcy, overruling the tax benefit gained from debts. Thus, managers are advised to balance the source of capital from equity and debt. Meanwhile, the Pecking theory by Myers (1977) suggests utilizing internal financing more than external financing due to the high cost of issuing higher external financing.

As liquidity has a positive relationship with profitability, it is important for the world’s top 20 CPO producers to have more cash to increase financial performance. A shortage of cash could result in the companies’ inability to pay for their obligations such as debt and operational costs (Velnampy, 2005). Thus, the more cash held by companies, the better their ability to meet their liabilities (Ablanedo-Rosas et al., 2010). Liquidity is also an important indicator of a firm’s cash flow. A low liquidity ratio signals financial distress and bankruptcy risk (Shafaai & Masih, 2013).

The control variable of SIZE, which represents the firm size, was significant and positively related to the profitability of the world’s top 20 CPO producers. Salim and Yadav (2012), Muritala (2012), Rahim (2013) and Wang (2013) reported consistent findings to that of this study. A large firm is assumed to have more resources (Capon et al., 1990). Larger firms are also able to provide superior technology and enlist the help of the best professionals and experts (Mule et al., 2015). Larger firms gain easier access to acquiring funds from debt (Sahudin et al., 2011). These companies are therefore recommended to invest more in tangible assets such as land and equipment due to the lesser cost of funding these assets compared to intangible assets (Sahudin et al., 2011). Hence, the world’s top 20 CPO producers should increase their assets to enjoy the benefits of credibility, making it easier for them to obtain more capital.

Conclusion

This study examined the effect of local (ISPO and/or MSPO) and international (RSPO) sustainability certification on the profitability of the world’s top 20 CPO producers. This study obtained yearly data from 2013 to 2018 and employed a GLS regression due to non-normally distributed data, heteroscedasticity, and autocorrelation problems. This study provides current knowledge related to profitability and sustainability certifications in the palm oil industry with a focus on the RSPO, ISPO, and MSPO certifications. This study addressed the lack of empirical studies related to these certifications and contributes additional knowledge to the field. In conclusion, ISPO and MSPO local certifications had no significant effect on the profitability of the world’s top 20 CPO producers. On the other hand, the study found that the world’s top 20 CPO producers with RSPO bore 5% losses compared to non-certified producers. The high costs in complying with RSPO and the lukewarm sales from the consumers were among the factors that caused these producers to not make higher profits. Sustainability certifications tend to play a more supportive role, namely in mitigating pressure from anti-palm oil lobbyists and in safeguarding the reputation of the industry.

This study highlights the need for the government to play a more effective role by endorsing RSPO and MSPO/ISPO to all palm oil industry players. This is because the certification plays an important role in protecting nature and environment; value added to the social living and improved corporate reputation. Therefore, tax incentives and subsidies should be introduced by government for the CPO producers to cover the cost of certifications. These incentives have the potential to reduce the burden in complying with sustainability certification, especially RSPO. This is because CPO producers are in a dilemma whether they should adopt the certification since it will increase their operational cost. Hence, by introducing relevant tax benefits and financial incentives, the firms would more likely comply with the RSPO, ISPO, and MSPO standards. Besides, the implementation of RSPO, ISPO, and MSPO from time to time will provide competitive advantages and promote certified palm oil products worldwide. The authorities should ensure a transparent implementation mechanism to generate consumer trust. The government should also promote more sustainability certifications through awareness campaigns to the community, so they are able to gain more information about the benefits of these practices and will be more willing to buy green products. The campaign can be done through seminars, mass media, and publications. Due to the limited data on available CPO producers, this study could not measure the effect of CSPO on all palm oil producers. Further study could be conducted to test the effect of sustainability certification on all the CPO producers in the world. Besides, future work could extend this study by continuing the period of study from the year 2018 as a replacement for the earlier period because the price data of palm oil is not static. Future studies could also contribute to increasing the number of empirical studies on sustainability issues.

Footnotes

Acknowledgements

We thank our colleagues from UKM and MPOB whom provided insights and expertise that greatly assisted the research, although they may not agree with all the interpretations/conclusions of this paper. We are also immensely grateful to the reviewers for their comments on an earlier version of the manuscript, although any errors are our own and should not tarnish the reputations of these esteemed persons.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the MPOB-UKM Endowment Chair Research Grant (EP-2017-062).

Ethics Statement

This article does not contain any studies involving human participants performed by any of the authors.

Consent

This empirical study only involved secondary data of companies retrieved from online open sources.