Abstract

Since 2016, the Malaysian Stock Exchange has mandated sustainability reporting for publicly listed firms, requiring them to disclose their environmental impact and sustainability efforts. However, to meet these expectations, some firms may overstate their achievements to gain a competitive edge, a practice known as greenwashing. This highlights the critical role of corporate governance, particularly the board of directors, in ensuring transparency and accountability. This study aims to examine the impact of corporate governance on greenwashing and examines whether political connections and environmentally sensitive industries moderate this relationship. Using an unbalanced panel dataset of 988 firm-year observations from 2016 to 2023, the study employs a fixed effects model to analyse the data. The findings indicate that board independence and gender diversity are the most significant governance factors in curbing greenwashing. Additionally, political connections and industry sensitivity partially moderate the governance-greenwashing relationship. By investigating the interaction of corporate governance and greenwashing in an emerging market, this study provides novel insights into corporate sustainability. It also provides valuable implications for managers and policymakers, highlighting the need for stronger governance frameworks to mitigate greenwashing risks.

Plain language summary

This study looks at how corporate governance impacts greenwashing and investigates whether political ties and industry types have an impact on the governance-greenwashing relationship. The study analyses 988 firm-year observations between 2016 and 2023 using a fixed effects model. The results show that having an independent board and gender diversity are the most important factors in reducing greenwashing. The study also found that political connections and firms operating in environmentally sensitive industries play a partial role in influencing how corporate governance affects greenwashing. By exploring how governance and greenwashing interact in an emerging market, this research provides new insights into corporate sustainability. It also offers important lessons for managers and policymakers, emphasising the need for stronger governance to reduce the risks of greenwashing.

Introduction

The 2030 Agenda for the UN’s Sustainable Development Goals (SDGs), established in 2015, provides a blueprint for the well-being of people and the environment, both now and in the future. The blueprint contains 17 SDGs that address environmental issues such as biodiversity, water, CO2, and energy, along with social problems like inequalities, education, and children. The promulgation of SDGs has led firms to engage in their environmental and social sustainability activities in their daily business operation. Recognising that all countries face climate issues, regulators require firms to take responsibility for their operations’ environmental impact (Kyaw et al., 2022). Firms are required to state environmental and social sustainability performance in their sustainability reports in their business strategies (Albitar et al., 2022). Firms convey their environmental responsibilities through disclosure to stakeholders. However, as alluded to by Marquis et al. (2016) and Ghitti et al. (2024), when firms give more prominence to the disclosure of sustainability performance, they face the risk of practising greenwashing. Elements of greenwashing exist when firms over-emphasise sustainability disclosure and communicate aggressively their commitment to reducing environmental footprint; however, the communication is not accompanied by actual environmental efforts. Greenwashing gives the false impression to consumers that the firm is environmentally friendly and misleads consumers to think they are buying sustainable products, which undermines real environmentally friendly firms. Firms doing this could face legal action, including penalties, fines, and lawsuits from investors and consumers who feel being misled.

W. Li et al. (2023) mention that greenwashing practices can be observed from the way firms disclose their sustainability practices, often in the form of elaborate sustainability strategies. This is where firms overclaim sustainability practices that are not commensurate with actual practices; in other words, green communication exceeds green practices (E. H. Kim & Lyon, 2015). Cormier and Magnan (2015) and S. Kim (2019) state that firms engage in greenwashing as a strategy to improve firm value, legitimacy, and environmental reputation. Despite the growing interest, Hora and Subramanian (2019) and Torelli et al. (2020) state that studies on greenwashing are still in its initial stages. Lyon and Montgomery (2015) and Torelli et al. (2020) state the need for further research, particularly on greenwashing. This is because existing studies seem to focus on the impact of greenwashing on firm value (Testa et al., 2018; Yu et al., 2020), while factors affecting greenwashing behaviour remain largely unexplored. These studies find that greenwashing leads to scepticism towards environmental claims and negatively influences firm value. It also harms firms that are genuinely dedicated to environmental responsibility because investors and consumers start doubting all green-environment claims. This is where corporate governance, particularly the board, plays a crucial role in determining whether firms are genuinely practising green practices.

Prior studies have established relations between corporate governance and sustainability issues (e.g., Al-Mamun & Seamer, 2021; Lee, 2023). Hence, it is plausible that a relationship exists between corporate governance and greenwashing. To provide a clearer indication of the relationships, Testa et al. (2018) call for more studies on the influence of corporate governance on greenwashing. Corporate governance is the framework of practices, processes and rules by which firms are controlled and directed. The boards of directors are responsible for ensuring effective governance and accountability of their firms (Jain & Jamali, 2016). Previous studies commonly use different variables to measure corporate governance, such as CEO non-duality (De Villiers et al., 2011; Y. Li et al., 2018), independent board members (Pekovic & Vogt, 2021), board size (Ntim & Soobaroyen, 2013), and board’s gender diversity (Ghitti et al., 2024; Glass et al., 2016) to capture key aspects of how firms are governed. However, research on corporate governance and greenwashing is limited, and the available evidence is inconsistent, suggesting a lack of consensus and a gap in the current understanding. This situation opens the debate regarding the board’s role in greenwashing. Our study aims to provide new evidence on the influence of corporate governance and greenwashing, using four board elements mentioned above: board independence, board size, CEO non-duality, and board gender diversity. According to Kyere and Ausloos (2021), these board elements represent good corporate governance.

Further, despite some studies focusing on greenwashing in developed countries (Ghitti et al., 2024; Hora & Subramanian, 2019), its implications in emerging markets remain underexplored, representing a significant gap in the current literature. This highlights the need for further investigation into greenwashing in emerging markets, such as Malaysia. Malaysia started its industrialisation strategies aggressively in the 1970s, which has played a significant role in the country’s economic growth. However, the industrialisation process simultaneously has negative effects on the environment (Chin et al., 2019). To reduce these negative impacts, Malaysia has taken steps to develop sustainability frameworks to help firms engage in environmentally responsible practices. In 2021, the Securities Commission Malaysia revised the Malaysian Code on Corporate Governance (MCCG), placing greater emphasis on the board’s role in addressing sustainability issues. Additionally, the Malaysian Stock Exchange has mandated sustainability reporting requirements for publicly listed companies since 2016. Consequently, firms need to disclose their environmental footprint and sustainability efforts. However, some firms might become encouraged to overstate their sustainability achievements, highlighting the critical role of corporate governance in mitigating greenwashing.

Our study focuses on the relationship between corporate governance and greenwashing. Additionally, we extend previous work by considering how political connection and sensitive industries moderate this link. Tee (2020) highlights that Malaysian corporate behaviour is likely to be affected by political connections. The initiation of the New Economic Policy (1971–1990) and the New Development Policy (1991–2000) by the Malaysian government created a space for governmental intervention in the corporate environment (Gomez & Jomo, 1999). As a result, corporations can have commercial benefits via their connections with politics. According to Wong and Hooy (2018), Malaysia has the greatest number of politically connected firms (PCFs) among Southeast Asian countries. However, being a PCF has its advantages and disadvantages. Wong and Hooy (2018) document that political connections led to better board effectiveness and subsequently better performance. However, Isa and Lee (2016) find the opposite, that is, government-linked companies (GLCs) perform worse than their non-GLC counterparts. The impact of political connections on PLCs’ greenwashing is still unexplored. A recent study by Ren et al. (2024) finds that political connections reduce Chinese firms’ greenwashing behaviour. This is because PCFs are more likely to receive government support and subsidies for green initiatives, which boosts environmentally responsible activities (Akcigit et al., 2023). Against this backdrop, it would therefore be interesting to see if PCFs are better behaved in terms of their greenwashing behaviour.

Additionally, firms behave differently if they are operating in environmentally sensitive industrial sectors as opposed to in non-sensitive sectors. Sensitive sectors are those that involve elements of controversy in their operations, products, and/or services, such as tobacco, oil and gas, pharmaceuticals, gaming, weaponry, etc. T. F. Zhang et al. (2022) and Ruiz-Blanco et al. (2022) find that firms operating in environmentally sensitive industries greenwash less than those in other industries. This could be due to firms in sensitive industries being under greater scrutiny from external stakeholders and being more likely to avoid greenwashing. However, there is a lack of research on how political connections and sensitive industries moderate the relationship between corporate governance and greenwashing.

Against the above background, our study addresses the pressing issue of greenwashing, where firms overstate sustainability efforts, which undermines market trust and stakeholder interests. By investigating whether key corporate governance mechanisms (board size, board independence, CEO non-duality, and gender diversity) mitigate such behaviour, and whether political connections and industry sensitivity shape this effect, this study aims to provide a nuanced understanding of how internal and external governance contexts influence sustainability integrity.

Theories and Hypotheses

Theoretical Framework

In modern organisations, ownership and managerial control are often separated, creating a potential conflict of interest between shareholders and managers, known as the agency problem (Jensen & Meckling, 1976). According to agency theory, managers may prioritise their benefits over the interests of stakeholders, leading to governance challenges. To address this, corporate governance mechanisms are implemented to regulate and oversee managerial activities. Fama and Jensen (1983) suggest that a well-structured corporate governance system can help mitigate agency costs. Research indicates that agency conflicts can arise in corporate social responsibility (CSR) activities, sometimes leading managers to engage in greenwashing (Masulis & Reza, 2015). However, studies by Naciti (2019) and Dyck et al. (2023) suggest that strong corporate governance practices can mitigate agency problems and enhance environmental performance, potentially reducing the risk of greenwashing. Despite this, evidence on the relationship between corporate governance and greenwashing remains limited. While Frendy et al. (2024) and Ghitti et al. (2024) indicate that corporate governance is ineffective in curbing greenwashing, more studies are needed to clarify this relationship.

According to Freeman (1994), managers must consider the social objectives of their stakeholders to achieve profit maximisation. Stakeholder theory suggests that managerial decisions are driven not by managers for personal gain but by the interests of all stakeholders. This theory integrates stakeholders into business strategy, emphasising that they can both influence and be influenced by managerial decisions, including corporate governance. Social and environmental responsibility activities serve as mechanisms for firms to build and maintain trust with their stakeholders. Additionally, previous studies have linked stakeholder theory to resource dependence theory, which views board composition as a valuable resource for firms (Mukherjee et al., 2013). Pfeffer (1972) argues that a board with more members who have professional qualifications enhances expertise and strengthens the firm’s resource base. Research by Kyaw et al. (2017) and Chen and Dagestani (2023) suggests that board diversity and political connections provide unique resources that can influence environmental performance. A well-diversified board is better positioned to actively monitor management decisions and ensure they align with stakeholder expectations. This, in turn, can reduce the risk of greenwashing and promote genuine sustainability efforts.

Legitimacy theory suggests that firms must continuously ensure they are perceived as operating within societal norms (Deegan, 2009). This theory posits that companies, especially those in environmentally sensitive industries, partake in environmental responsibility activities to bolster their legitimacy. For example, energy companies invest in renewable energy technologies to align with societal expectations. Ruiz-Blanco et al. (2022) state that environmentally sustainable actions can help improve a firm’s image and perceived legitimacy. However, some firms may use sustainability communications to present an environmentally responsible image that does not reflect their actual performance, thereby misleading stakeholders (Emma & Jennifer, 2021). Conversely, firms in sensitive industries may engage in genuine environmental initiatives as a way to strengthen stakeholder relationships and improve their reputation (Cai et al., 2012). Arena et al. (2015) find that the environmental disclosures by U.S. oil and gas companies were primarily aimed at increasing transparency rather than manipulating corporate image. The study argues that firms in environmentally sensitive industries are more likely to undertake genuine environmental actions to legitimise their existence. Engaging in greenwashing can severely damage a firm’s reputation, potentially resulting in significant financial losses. Additionally, regulatory bodies often impose fines on firms that fail to meet legal and ethical standards, further impacting their financial performance. These theories collectively frame the scientific problem by highlighting that without robust governance, firms may exploit sustainability reporting to engage in greenwashing. Therefore, evaluating how specific governance characteristics influence this behaviour, especially under politically and environmentally sensitive conditions, is central to addressing the identified gap.

Hypotheses Development

Firms are organisations with systems, regulations and rules by which they are managed, directed, and controlled. This controlling mechanism is usually referred to as corporate governance. Corporate governance also ensures connectivity between firms and stakeholders, including employees, customers, and shareholders. A key element of corporate governance is the board of directors. The board is the highest decision-making body in a firm. Its main function is to provide strategic direction to the companies and determine policies and strategies to facilitate achieving the strategic goals. As evidenced by the work of Manning et al. (2019) and Lee (2023), corporate governance is found to have a significant impact on firms’ sustainable practices. Additionally, Gracia-Torea et al. (2016) and Pekovic and Vogt (2021) find that the effectiveness of the board is determined by its advisory and monitoring roles. Related to this study, Naciti (2019) and Dyck et al. (2023) document that the board’s functions can influence firms’ environmental performances. Unfortunately, previous studies do not focus specifically on greenwashing activities. Because of this, it is felt that this study provides an important contribution by linking board functions and firms’ greenwashing practices. Specifically, our study proposes including board features: CEO non-duality, board independence, board size, and gender diversity in the model.

CEO Non-duality

An effective organisational structure requires collaboration between the board and management to achieve corporate goals. The board represents stakeholders, particularly shareholders, and has a fiduciary duty to oversee management. The CEO holds significant authority over operations, including firms’ environmental and social policies (Aguinis & Glavas, 2012; Y. Li et al., 2018). Good governance maintains separation between the board and management, but some firms adopt a “duality” leadership, where one person serves as both CEO and Chairman. This compromises the board’s oversight function, eliminating checks and balances and increasing the risk of agency problems (De Villiers et al., 2011). The Malaysian Code on Corporate Governance (MCCG, 2017) discourages dual leadership to strengthen the board oversight function. Lu and Wang (2021) support this, finding that non-duality enhances governance and sustainability performance. According to best practices and agency theory, non-duality should also reduce greenwashing. Hence, we formulate H1 below:

H1: Firms practicing CEO non-duality are expected to have lower greenwashing activities than firms practicing duality.

Board Independence

Ferrell et al. (2016) highlight board independence as key to effective governance, typically measured by the proportion of independent directors. These directors enhance oversight, reduce agency conflicts, and prioritise stakeholder interests (Kassinis & Vafeas, 2002; Mallin & Michelon, 2011). Masud et al. (2018) find that more independent board members would enhance the monitoring of environmental strategies, boosting sustainability performance. In greenwashing cases, independent boards are expected to mitigate such practices. Freeman (1994) stakeholder theory suggests that companies should consider all stakeholders, not just shareholders. Liao et al. (2015) and Haque (2017) suggest that independent boards enhance expertise, representation, and stakeholder interests. Unbound by financial incentives, independent directors can better monitor managerial actions (De Villiers et al., 2011) and promote strong environmental policies. In line with this, the MCCG (2017) encourages Malaysian firms to have a majority of independent directors. Based on these discussions, we hypothesise that:

H2: Board independence is inversely related to greenwashing activities.

Board Size

The impact of board size on firm performance is debatable. One view supports large boards for their diverse expertise, skills, and stakeholder representation (Ntim & Soobaroyen, 2013; Said et al., 2009), thereby aligning with stakeholder theory. The opposing view favours small boards for better communication, coordination, and decision-making (De Andres et al., 2005; Kiel & Nicholson, 2003). Large boards may suffer from coordination issues (Eisenberg et al., 1998), while small boards may lack the resources and expertise for effective monitoring. Researchers link board size positively to corporate environmental performance, for example, Walls et al. (2012) and Lu and Wang (2021); suggesting that board size has a negative relationship to greenwashing. Ghitti et al. (2024) confirm that larger boards, with their diverse expertise, enhance oversight and reduce greenwashing risks. Based on these discussions, we hypothesise that:

H3: Board size is inversely related to greenwashing practices.

Gender Diversity

Gender diversity, operationalised as the percentage of female directors, reflects inclusivity and leverages gender-based strengths that postulate that women excel in intuition and relationship-building, while men are more task-oriented. According to Cucari et al. (2018) and Qureshi et al. (2020), gender diversity is a key factor in determining board effectiveness. Agency theory views that more female directors enhance board monitoring and curb managerial opportunism (Hillman & Dalziel, 2003). Female directors also promote corporate environmental responsibility and discourage negative decisions (Arfken et al., 2004). Legitimacy and stakeholder theories indicate that women strengthen stakeholder relationships (Glass et al., 2016; Mallin & Michelon, 2011). Post et al. (2011) find that at least three female directors are needed to significantly influence environmental policies, as women naturally foster strong stakeholder relationships, enhancing sustainability. Supporting this, Naciti (2019) and Lu and Wang (2021) report a positive link between female board representation and corporate social responsibility. Thus, H4 is proposed as below:

H4: Gender diversity in the board is inversely related to greenwashing activities.

Political Connection

Politically connected firms (PCFs) are those owned by the government (L. Zhang et al., 2019), government-linked companies (Isa & Lee, 2016), or whose top officers or shareholders have ties to high-ranking politicians (Gul, 2006; Tee, 2018). PCFs may obtain benefits for their businesses from favourable regulations, subsidies, and government contracts, allowing them to influence policy and economic environments to their advantage. Research on PCFs largely focuses on their impact on firm value (Hassan et al., 2012; Wong & Hooy, 2018). Resource dependence theory suggests that political ties provide external resources, boosting firm value (Wu et al., 2012; L. Zhang et al., 2019). However, PCFs also face risks like falling into corruption and inefficiencies, leading to poor financial performance (Amin & Cumming, 2023). Isa and Lee (2016) found that in Malaysia, government-linked companies (GLCs) underperform compared to non-GLCs. Studies generally link PCFs to better environmental performance. Wang et al. (2018) and L. Zhang et al. (2019) find that PCFs engage more in social and environmental responsibility due to political incentives. Wang et al. (2018) extend the resource dependence theory, arguing that PCFs secure resources in exchange for meeting government goals, such as emissions reduction and renewable energy use. They also suggest that politically connected boards align with government priorities, making PCFs potential catalysts for mitigating greenwashing. Therefore, we hypothesise that:

H5: Political connection moderates the relationship between corporate governance and greenwashing activities.

Sensitive Industries

The second moderating variable of our study is environmentally sensitive industries (SIN). Firms in these industries face public scrutiny due to their products or operations that may harm the environment or society (Cai et al., 2012; Garcia et al., 2017). These industries, such as pharmaceuticals, oil & gas, mining, chemicals, and tobacco, are subject to criticism, encouraging them to adopt responsible practices to maintain a positive image (Heal, 2008). Firms in these sectors often engage in environmental or CSR activities to reinforce their reputation (Dhandhania & O’Higgins, 2022; Sharma & Song, 2018). According to legitimacy theory, firms adopt social and environmental initiatives to align with societal norms and stakeholder expectations (Suchman, 1995). Given their heightened visibility and regulatory scrutiny, firms in SIN must actively manage their image by enhancing sustainability efforts (Garcia et al., 2017; Marquis et al., 2016). Ruiz-Blanco et al. (2022) note that these firms undergo stricter environmental monitoring, making them less likely to engage in greenwashing. Therefore, we propose that firms in SIN influence the corporate governance–greenwashing relationship, leading to the following hypothesis:

H6: Environmentally sensitive industries moderate the relationship between corporate governance and greenwashing activities.

The research framework of our study is summarised in Figure 1.

Research framework and research hypothesis.

Data and Methodology

Data

Data for this study were obtained from the Refinitiv Workspace database, which provides the necessary information to calculate firms’ green communication and green practice indices. This study uses non-financial Malaysian firms over the period 2016 to 2022. This period was selected based on data availability. Financial firms and firms with significant missing data are excluded from our study. Financial firms are dropped because financial regulations may influence firms’ environmental disclosure and their greenwashing activities. As of the end of 2022, the database included 346 listed Malaysian firms. The final unbalanced panel dataset consists of 988 company-year observations from 300 firms. Information on board characteristics was also extracted from the same database. Data on firms’ financial and corporate information is obtained from the Datastream. The data is deemed suitable for our analysis because it has the necessary information to calculate all the variables needed. We use all available Malaysian data in the database that fulfils our criteria in providing specific information on the items related to green practice and communication for our computation of the greenwashing index.

Measurement of Variables

Our study employs a methodological approach consistent with previous studies (W. Li et al., 2023; Testa et al., 2018), which measures greenwashing by analysing the difference between a firm’s green communication and green practices. Green communication includes green vision, environmental profile and initiatives, and stakeholder communication that are conveyed in firms’ annual reports. Green practices are actual conduct, such as green product development, environmental spending, green supply chain management, and pollution prevention. Greenwashing is defined as the difference between the green communication index (GCI) and green practices index (GPI; W. Li et al., 2023). The bigger the gap between GCI and GPI, the more greenwashing activities are taking place.

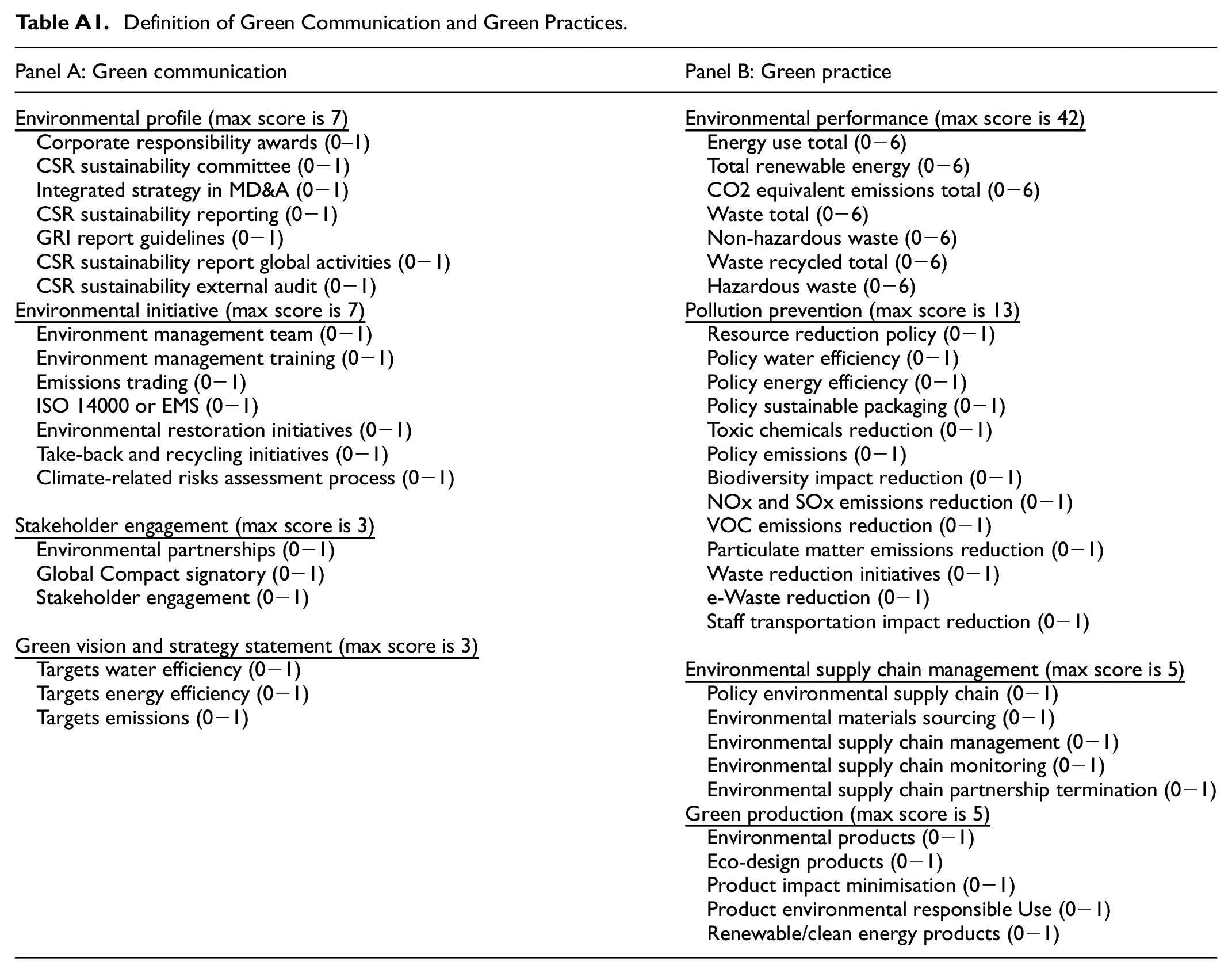

To compute the GCI and GPI, the environmental items obtained from the Eikon database are coded as a binary scale for all the items involved, except a few; for these few items in the green practices section, the items are assigned numbers on a sliding scale according to the intensity of the involvement. The final set of code includes 4 categories of green practices, comprising 40 items and 4 categories of green communication with 20 items. The items used for the green communication and practice key performance indicators in the firm’s day-to-day decision-making processes are adopted from Testa et al. (2018) and W. Li et al. (2023). The categories, individual items, and definitions are presented in Appendix A, Table A1. The GCI and GPI scores were computed by averaging the scores of items of green communication and green practices, respectively.

The greenwashing index (GWI) is obtained by calculating the difference between standardised GCI and standardised GPI. Following Testa et al. (2018) and W. Li et al. (2023), the standardisation is done by dividing the score’s deviation from its mean by its standard deviation. The GWI score is computed as follows:

where

Our independent variable is corporate governance. We use four board characteristics to represent corporate governance. These are:

(i) CEO non-duality (Nonduality), indicated by a dummy variable where 1 denotes separate individuals holding the CEO and board chairman roles, and 0 otherwise,

(ii) Board independence (BInd) is calculated as the percentage of independent members on the board,

(iii) Board size (BSiz), is the number of directors on the board, and

(iv) Gender diversity (GDiv) is computed as the percentage of female board members.

In this study, we proposed two moderating variables. The first moderating variable is political connection firm (PCF), which is a dummy variable equal to 1 if the company is politically connected and 0 if it is not. Following Tee (2018), and Wong and Hooy (2018) a firm is assigned as PCF if it is a government-linked company (GLC), or one of its top officers or controlling shareholders is connected to any of the following: a top politician or a cabinet minister, a head of state, or a parliament member.

The second moderating variable is environmentally sensitive industries (SIN), which is a dummy variable that equals 1 for firms belonging to environmentally sensitive industries and 0 otherwise. The classification of firms belonging to sensitive industries is based on Ruiz-Blanco et al. (2022).

Consistent with previous literature, we include control variables for the firm-specific characteristics that may influence greenwashing practices (Ghitti et al., 2024; W. Li et al., 2023). This variable is company profitability, computed as total net income scaled by total assets (ROA); leverage is calculated as total debt over total assets; current ratio is estimated as current assets over current liabilities, and firm size is calculated as the natural logarithm of total assets.

Data Analysis Tools and Techniques

We test our hypotheses by running panel regressions. To select an appropriate econometric model to analyse the panel data, this study conducts the Hausman test. This study employs the Hausman test to assess the most suitable econometric model for our panel data analysis. To rigorously test the alignment between governance structures and greenwashing behaviour as framed in our research problem, this study employs a fixed effects panel regression model. This method is chosen to control for firm-specific heterogeneity, which is essential for isolating the causal influence of governance on the divergence between green disclosure and practice.

First, we test Equation 1 below to investigate the effect of corporate governance on greenwashing activities. This regression tests hypotheses 1 to 4.

where GWI is the greenwashing index, Nondual is a dummy variable with 1 representing CEO non-duality and 0 otherwise, BInd is the percentage of independent directors, BSiz is the total number of directors, GDiv is the percentage of female directors, and Control is the set of firm-specific control variables and εi,t denotes the error term for company i at time t. Non-binary variables are lagged by one fiscal year to reduce possible endogeneity concerns.

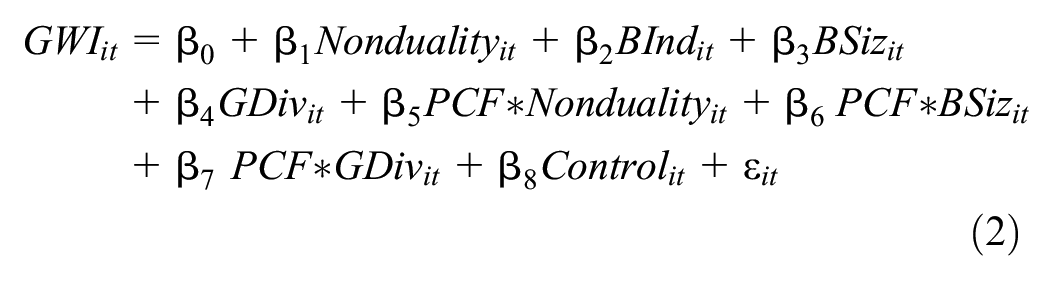

Second, we investigate the moderating effect of political connections on the corporate governance and greenwashing relation. Accordingly, we incorporate the interaction terms of corporate governance and political connection dummy (PCF) in Equation 1 to become Equation 2, as follows. Equation 2 is used to test Hypothesis 5.

where PCFs is a dummy variable equal to 1 if the firm has political connections and 0 otherwise. Equation 2 includes the interaction terms to examine the moderating role of PCF on the governance-greenwashing relation.

Third, we examine the role of sensitive industries in moderating the link between corporate governance and greenwashing. Accordingly, we include the interaction terms of corporate governance and sensitive industries dummy (SIN) in Equation 1 to test Hypothesis 6. After incorporating SIN and its interaction terms in Equation 1, it became Equation 3 as follows:

Results and Discussions

Descriptive and Correlation Analysis

Table 1 presents the summary statistics of the dependent and independent variables. The mean value of GWI is −0.02, and the minimum and maximum are −2.44 and 2.53, showing that the extent of greenwashing of the firms varies quite significantly. CEO non-duality occurs in about 83% of the total sample firms. The high percentage of non-duality is very encouraging, as it seems that these companies are moving towards good governance practices. The average proportion of independent directors on the board is more than half at 50.46%, which is consistent with the recommendation of the MCCG (2017), which advocates that a minimum of 50% of board members should be independent. The board of directors was composed of eight members on average during the study period. The mean for gender diversity (percentage of female directors) is 22.04%, which is less than a third as recommended by the MCCG (2017). The descriptive statistics for the firm-specific control variables show that the average total assets (firm size) is RM8.87 billion. The mean for the ROA is 6.15%, with values ranging from 65.66% to −36.79%. The mean for leverage, estimated as the total debt scale by total assets, is 23.58%. The mean value of the liquidity ratio is 2.37. The means for the moderating variables of politically connected firms and sensitive industries are 0.23 and 0.28, respectively. This means nearly a quarter of the firms are politically connected, and a little over a quarter are in sensitive industries.

Descriptive Statistics.

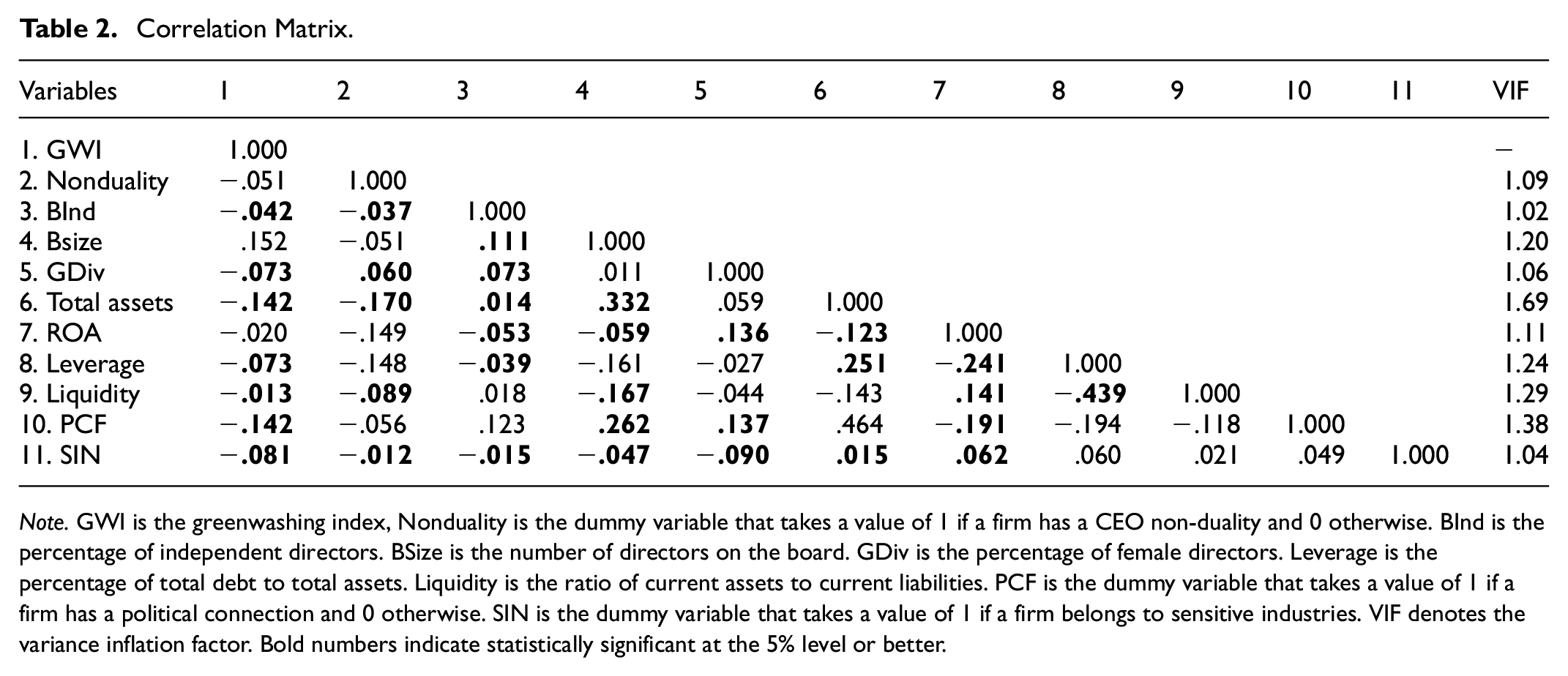

Table 2 reports the pairwise Pearson correlation coefficients of the variables to check whether there are issues of multicollinearity. In general, the correlation coefficients are moderately low. The multicollinearity diagnostic test, which is the variance inflation factor (VIF), suggests that there is no multicollinearity issue in our model.

Correlation Matrix.

Note. GWI is the greenwashing index, Nonduality is the dummy variable that takes a value of 1 if a firm has a CEO non-duality and 0 otherwise. BInd is the percentage of independent directors. BSize is the number of directors on the board. GDiv is the percentage of female directors. Leverage is the percentage of total debt to total assets. Liquidity is the ratio of current assets to current liabilities. PCF is the dummy variable that takes a value of 1 if a firm has a political connection and 0 otherwise. SIN is the dummy variable that takes a value of 1 if a firm belongs to sensitive industries. VIF denotes the variance inflation factor. Bold numbers indicate statistically significant at the 5% level or better.

Regression Results

Determining the Regression Model

For regression analysis, we consider three different panel estimation methods: (i) pooled ordinary least squares (POLS), (ii) fixed effect model (FEM), and (iii) random effect model (REM). Following Sandberg et al. (2023), we perform two-level tests to identify the best model for our analysis. First, we use the poolability test to determine the best model between POLS and FEM. The H0 (null hypothesis) for this test is the POLS model. The test result in Table 3 suggests that the p-value is .000, which is significant at the 5% level. Therefore, the FEM is preferred. We then use the Hausman test to decide between FEM and REM. In this test, the H0 is the REM. If the p-value is less than .05, the H0 is rejected in favour of the alternative. The result of this test, as shown in Table 3, indicates the p-value is .000. Therefore, the test rejects the REM in favour of the FEM. Hence, we use a robust FEM to analyse the impact of corporate governance on greenwashing. Besides, we also control for time-fixed effects to mitigate the effects on the regression results (Chen & Dagestani, 2023).

Results of the GWI Regressions for Determining the Best Model.

Note. Figures in parentheses are t-statistics.

,**, and * indicate statistical significance at the 1%, 5%, and 10% levels.

Corporate Governance and Greenwashing (H1–H4)

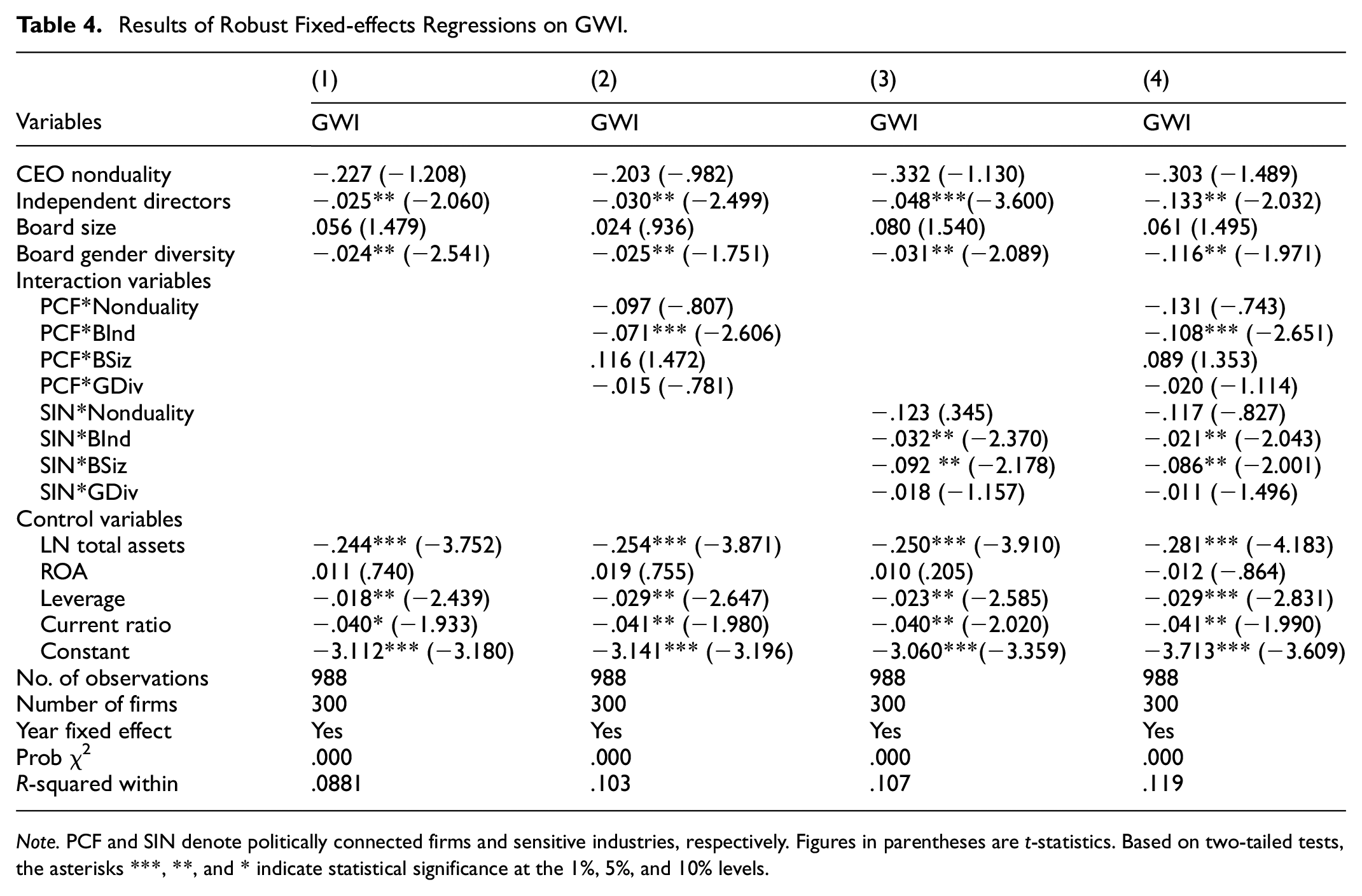

The first aim of our study is to analyse the impact of corporate governance (board characteristics) on greenwashing. Table 4 reports the results of the robust fixed-effects regression model (FEM). In this section, our focus is on Column 1, which shows results for the basic model, Equation 1. The results show that among the four governance variables tested, two have negative coefficients while the other two are insignificant. The results indicate that independent directors and gender diversity have a negative influence on firms’ greenwashing activities. This is consistent with our arguments that independent directors would bring more objectivity to board decisions, which in turn would lead to better monitoring and a lower likelihood of firms engaging in greenwashing activities. Similar arguments apply to having more female members (gender diversity) on a corporate board. This result suggests that more female directors are associated with a lower greenwashing index. Hence, Hypotheses 2 and 4 are supported by our results. Our findings regarding independent directors align with previous research suggesting that external directors are more attentive to the environmental sustainability practices of companies and less likely to participate in greenwashing (Post et al., 2011; Webb, 2004). The results align with agency theory research on board composition and CSR relationship, indicating that boards with a greater proportion of independent directors provide superior governance (Dahyaa & McConnell, 2004). This is because independent directors can monitor the behaviours of managers and intervene when managers behave opportunistically, which reduces the chances of engaging in greenwashing. In contrast to external directors, internal directors may prioritise their personal interests over their duties to shareholders. Independent directors are more focused on firms being good corporate citizens, while non-independent directors are more concerned with the dollars and cents performance of their operations.

Results of Robust Fixed-effects Regressions on GWI.

Note. PCF and SIN denote politically connected firms and sensitive industries, respectively. Figures in parentheses are t-statistics. Based on two-tailed tests, the asterisks ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels.

For female directors, our findings are consistent with Post et al. (2011) and Chen and Dagestani (2023). This indicates female directors are more stakeholder-oriented and promote green practices rather than greenwashing. Post et al. (2011) mention that prior studies argue that women’s more protective attitude toward the environment stems from a closer identification with nature because of their reproductive role. Although Hayes (2001) documents no significant gender differences in environmental attitudes, the majority of prior research suggests that women tend to exhibit greater concern for environmental issues compared to men (Diamantopoulos et al., 2003).

The two insignificant governance variables are the CEO non-duality and board size. For CEO non-duality, our results indicate that it does not influence greenwashing. Its coefficient, although having a negative sign, yet insignificant. Therefore, Hypothesis 1 is not supported by our results. It seems that firms having non-duality leadership are not associated with reduced greenwashing activities. This result is somewhat disappointing given the serious attention from the MCCG (2017) on requiring firms to practice non-duality leadership, which is shown by the high percentage of non-duality firms in our sample. This might suggest that CEO non-duality is often seen as a mechanism for improved governance, but it does not automatically translate into ethical leadership. Even in non-duality leadership, a CEO may not prioritise environmental sustainability practices, making them less likely to impact greenwashing.

As for board size, we have discussed earlier that it may be difficult to argue that the number of directors would have a negative or positive impact on greenwashing. However, previous studies suggest that a larger board size may positively influence performance, thereby indirectly reducing greenwashing. Our results, however, indicate that board size, with an insignificant coefficient, is a non-issue as far as greenwashing is concerned. Hypothesis 3 is therefore not supported. This evidence on board size aligned with Yu et al. (2020). Incidentally, Jensen (1993) mentions that boards greater than eight directors are less likely to function effectively, which is in line with the 8.16 average board size of our sample. Some prior studies state that large boards entail larger agency costs, due to inefficiencies in the interactions of insiders with outsider board members (Raheja, 2005). On the other hand, Lu and Wang (2021) find that larger boards enhance environmental performance. This suggests that to benefit from the board size increase, the firms might aim to appoint directors who are experts in environmental sustainability, which could mitigate greenwashing risk.

The Moderating Effects of Political Connection (H5) and Sensitive Industries (H6)

The second objective of our study is to analyse the moderating role of political connections and sensitive industries on the link between governance and greenwashing. Column 2 of Table 4 presents results on regression Equation 2 with political connection (PCF) as the moderating variable. The focus here is on the interaction variables involving PCF and governance variables. For the PCF moderating variable, we find only one interaction variable with a negatively significant coefficient, that is, independent directors (PCF*BInd). We have seen earlier that independent directors are negatively related to greenwashing in the basic relation (Column 1). A negative coefficient for the interaction variable (PCF*BInd) means that the basic negative relationship is more intensified for companies with political connections. This means political connections will strengthen the influence of independent directors on greenwashing. All the other governance interaction variables (PCF*nonduality, PCF*BSiz, and PCF*GDiv) are insignificant. We conclude that Hypothesis 5 is partially supported. Malaysian regulators have consistently updated the MCCG to ensure good corporate governance practices of firms. The MCCG also emphasises the board’s responsibility in managing sustainability issues; thus, the political connections might not be influential enough to moderate the relationship between corporate governance and greenwashing. Our result suggests that political connections further strengthen the role of independent directors in reducing greenwashing. This may be because of independent directors’ ability to leverage political relationships, thus acting as a more powerful governance mechanism, consequently reducing greenwashing.

Column 3 of Table 4 shows results for Equation 3 with sensitive industries (SIN) as the moderating variable. The results show two negatively significant interaction variables, that is, independent directors (SIN*BInd) and board size (SIN*BSiz). This means that for firms operating in sensitive industrial sectors, board independence will have an enhanced negative impact on its already negative relationship with greenwashing, thereby greatly reducing greenwashing activities. As for board size, it is insignificant in the direct relationship but becomes significant in the interaction variable (SIN*BSiz). This means that for firms in sensitive industries, larger boards are associated with lower greenwashing activities. Our results align with stakeholder and legitimacy theories and suggest that sensitive industries serve as a moderating force, pushing independent directors to reduce greenwashing. The possible reason is that firms in sensitive industries are under intense scrutiny from stakeholders (i.e., regulators, activists, local communities, and investors), which increases the pressure on independent directors to engage in actual environmentally responsible practices to avoid the reputational damage that could result from greenwashing.

The coefficients for the interaction variables of SIN*nonduality and SIN*GDiv are insignificant. This means that industry type does not influence the negative relations between gender diversity and greenwashing. Similarly, the insignificance of non-duality in the basic relationship is also not affected by the SIN moderating variable. Our results indicate that Hypothesis 6 is partially supported. In Column 4, we combine both the moderating variables into one regression. The results are qualitatively similar to those seen in the first three columns.

Conclusion

This study responds to the critical challenge of greenwashing in emerging markets, particularly within Malaysia’s regulatory environment. It investigates whether corporate governance mechanisms – specifically CEO duality, board independence, board size, and gender diversity – can mitigate the misalignment between a firm’s environmental communication and actual practices. Additionally, the study explores whether the presence of political connections and operation within environmentally sensitive industries moderates these relationships. Using a fixed-effects panel regression on Malaysian listed firms between 2016 and 2022, the analysis offers novel empirical evidence.

The findings reveal that board independence and gender diversity significantly reduce the extent of greenwashing, aligned with the expectations of stakeholder and agency theories. However, CEO non-duality and board size do not show a direct significant effect. Furthermore, both political connections and industry sensitivity partially moderate the governance and greenwashing link. These insights affirm that while corporate governance can serve as a powerful tool for promoting authentic sustainability practices, its effectiveness depends on external institutional and industry factors.

This study contributes to the literature by directly addressing the scientific problem of how firms may exploit sustainability reporting frameworks to project a misleading image of environmental responsibility. By integrating governance indicators with contextual moderators, the study bridges theoretical propositions with observed corporate behaviour, especially in under-researched emerging market settings.

From a practical perspective, the findings underscore the need to strengthen board governance, particularly in increasing the presence of female and independent directors. Although Malaysian firms largely comply with governance codes, there remains room to enhance the depth of board diversity. The evidence also suggests political connections can either reinforce or undermine governance effectiveness, depending on how these relationships are managed. Firms with political ties must ensure transparency to avoid the risks of perceived favouritism or misrepresentation. Likewise, firms in environmentally sensitive industries should leverage their heightened visibility to implement substantive sustainability initiatives rather than symbolic disclosures.

Despite this study offering significant insights, it has certain limitations. The focus on a single country–Malaysia – may restrict generalizability to broader contexts. Additionally, the relatively recent enforcement of ESG disclosure requirements limits the available data scope. Nonetheless, this controlled context provides a unique opportunity to isolate governance effects. Future research should expand to cross-country studies and consider other ESG dimensions, such as social responsibility, to build a more comprehensive understanding of corporate sustainability behaviour. As ESG expectations evolve, continued scrutiny of the relationship between governance and greenwashing remains essential to ensuring firms do not misuse sustainability narratives at the expense of genuine impact.

Footnotes

Appendix A

Definition of Green Communication and Green Practices.

| Panel A: Green communication | Panel B: Green practice |

|---|---|

|

|

|

| Corporate responsibility awards (0–1) | Energy use total (0−6) |

| CSR sustainability committee (0−1) | Total renewable energy (0−6) |

| Integrated strategy in MD&A (0−1) | CO2 equivalent emissions total (0−6) |

| CSR sustainability reporting (0−1) | Waste total (0−6) |

| GRI report guidelines (0−1) | Non-hazardous waste (0−6) |

| CSR sustainability report global activities (0−1) | Waste recycled total (0−6) |

| CSR sustainability external audit (0−1) | Hazardous waste (0−6) |

|

|

|

| Environment management team (0−1) | Resource reduction policy (0−1) |

| Environment management training (0−1) | Policy water efficiency (0−1) |

| Emissions trading (0−1) | Policy energy efficiency (0−1) |

| ISO 14000 or EMS (0−1) | Policy sustainable packaging (0−1) |

| Environmental restoration initiatives (0−1) | Toxic chemicals reduction (0−1) |

| Take-back and recycling initiatives (0−1) | Policy emissions (0−1) |

| Climate-related risks assessment process (0−1) | Biodiversity impact reduction (0−1) |

| NOx and SOx emissions reduction (0−1) | |

|

|

VOC emissions reduction (0−1) |

| Environmental partnerships (0−1) | Particulate matter emissions reduction (0−1) |

| Global Compact signatory (0−1) | Waste reduction initiatives (0−1) |

| Stakeholder engagement (0−1) | e-Waste reduction (0−1) |

| Staff transportation impact reduction (0−1) | |

|

|

|

| Targets water efficiency (0−1) |

|

| Targets energy efficiency (0−1) | Policy environmental supply chain (0−1) |

| Targets emissions (0−1) | Environmental materials sourcing (0−1) |

| Environmental supply chain management (0−1) | |

| Environmental supply chain monitoring (0−1) | |

| Environmental supply chain partnership termination (0−1) | |

|

|

|

| Environmental products (0−1) | |

| Eco-design products (0−1) | |

| Product impact minimisation (0−1) | |

| Product environmental responsible Use (0−1) | |

| Renewable/clean energy products (0−1) |

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors would like to acknowledge the financial support from Universiti Tunku Abdul Rahman (Grant No. 2023-C2/L06).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available upon request through the corresponding author.