Abstract

The present study revisits the relationship between earnings management (EM) and firm performance, employing a nonlinear threshold approach and introducing national governance quality (NGQ) as a potential threshold variable. This study demonstrates how NGQ at the country level influences the impact of EM on firms’ performance at the micro level. Utilizing dynamic frameworks with data encompassing 52 firm samples across nine sub-Saharan African countries spanning from 2007 to 2019, the study reveals that the beneficial impact of EM on performance materializes when NGQ falls below a certain threshold. Beyond this threshold, the influence of EM becomes marginal or occasionally adverse on firm performance. As a result, we suggest that policymakers in Africa and other emerging and developing economies consider the estimated nonlinear relationship between EM and firm performance, as well as the NGQ threshold, when devising governance strategies. It is also imperative to consider institutional quality when making investment decisions and to promote rigorous standards for earnings management and institutional issues.

Plain language summary

Earnings management practices of firms have been widely observed to have devastating consequences on firm value or performance, which ultimately threatens the survival of businesses. Our present study however observes that, the performance effect of firms’ earnings management practices may be contingent of some external factors which have the capacity to moderate the devastating effects of earnings management practices. Our study demonstrates how country-level national governance quality (NGQ) is able to alter the micro-level effect of earnings management on firms’ performance at a defined threshold level. We find that, within the NGQ threshold of 0.446, the effect of earnings management on performance is favorable or value-enhancing. However, beyond this threshold, the performance effect of earnings management is negligible or occasionally adverse. We have therefore recommended some proactive actionable steps that capital market policy makers and managers can take to maintain NGQ at optimal levels to encourage efficient earnings management.

Keywords

Introduction

Earnings management (EM) is a natural financial reporting phenomenon facilitating capital market operations (Beneish, 2001). Firm’s earnings have become an effective channel for measuring managers’ success by shareholders. Firms with increasing earnings growth are considered successful, while those with low reported earnings are perceived to be less profitable and unattractive to investors (Mahrani & Soewarno, 2018). It is also becoming a cliché that managers use accounting discretion to influence earnings and maximize their utilities (Jensen, 1993; Schipper, 1989). As per Healy and Wahlen (1999), earnings management refers to the practice where managers exercise discretion in financial reporting and structuring transactions to modify financial statements, either to deceive certain stakeholders regarding the true economic performance of the company or to impact contractual results dependent on reported accounting figures. EM practices are carried out within or without the boundaries of accounting standards for various intents and purposes, including signaling capital market participants of firms’ financial health and growth prospects. By its nature, EM may be deployed either for opportunistic purposes (Giroux, 2004; Nasir et al., 2018) or for efficient or informative purposes (Deegan, 2009; Lin et al., 2016). Scholars typically attribute opportunistic intentions to cases where earnings management (EM) leads to negative effects on performance, or efficiency-driven intentions to instances where EM positively influences performance (Boachie & Mensah, 2022; Elkalla, 2017; Rezaei & Roshani, 2012). Recent investigations into EM practices have gained prominence due to their acclaimed role in accounting scandals and corporate failures. As already indicated, EM has been noted to affect firm performance, with the literature recognizing some of the transmission mechanisms through which EM can affect firm performance to include: insider trading (Osma et al., 2020), fraud (Nasir et al., 2018), internal control (Gong et al., 2023), management control systems (Osma et al., 2022), investment efficiency (Dinh et al., 2019; X. Jiang & Xin, 2022), common institutional ownership (Ramalingegowda et al., 2021), as well as corporate governance quality (Boachie & Mensah, 2022; Duong et al., 2022). The EM – firm performance nexus has occupied the attention of researchers because investors are usually interested in the bottom-line profits of a business as it reflects financial performance and prospects of growth (Akram et al., 2015; Walker, 2013). Hence, efforts to contribute toward firm performance enhancements, including EM practices that can result in efficient outcomes, are worth studying.

Previous research indicates that there are various reasons why both individuals and companies engage in earnings manipulation (Scott & O’Brien, 2020). For instance, managers employ accounting discretion to meet specific earnings targets (Burgstahler & Dichev, 1997), enhance bonus payouts (Guidry et al., 1999; Healy, 1985), secure job stability (Dechow & Skinner, 2000; Matsunaga & Park, 2001), meet expectations of the stock market and shareholders (Jiraporn et al., 2008), among other reasons. Signal theory suggests that earnings management can be beneficial when it communicates private information about a company’s future prospects (Al-Shattarat et al., 2018; Gul et al., 2003). Therefore, earnings management is viewed from two opposing perspectives: ‘opportunistic earnings management’, while the other is ‘signaling earnings management’. In this context, we highlight a strong association between earnings management and profitability, which confirms the neoclassical idea that managers have a single obligation to maximize shareholders’ profit and welfare (Friedman, 2007).

Some earlier studies have investigated how earnings management impacts company performance (Boachie & Mensah, 2022; Nguyen & Duong, 2022). Nevertheless, the empirical results remain inconclusive. While some scholars (Bouaziz et al., 2020; Vorst, 2016) validate the presence of a negative impact, others suggest a positive influence (Al-Shattarat et al., 2018; Gunny & Zhang, 2014). We expect that the threshold effect of governance quality, particularly within the African context, will lead to significant variations in the influence of earnings management on firm performance. Consequently, it is imperative to enrich the existing body of literature by examining the impact of a threshold variable, such as national governance quality, within this relationship.

Recent research has highlighted the significance of macroeconomic factors and national governance structures in explaining earnings management (EM) practices and its consequent effect on firm performance (Abdou et al., 2021; Alghemary et al., 2023; Elkalla, 2017; Filip & Raffournier, 2014; Lei & Wang, 2019; Mensah et al., 2023). For instance, Abdou et al. (2021) demonstrated that efforts to combat corruption had a considerable latent impact on the EM behaviors of firms in both Egypt and the United Kingdom. Daniel et al. (2011) developed a theoretical framework linking a nation’s institutional framework (encompassing regulatory quality, rule of law, government effectiveness, and corruption mitigation) to international corporate governance practices, earnings management strategies, and firm disclosure policies. The current study acknowledges the limitations of previous studies of the EM – performance or governance nexus, which generally considers EM independently or in interaction with isolated national governance variables, thus implying a linear relationship (Abdou et al., 2021; Boachie & Mensah, 2022; Duong et al., 2022; Osma et al., 2022). As a result, most previous research tends to overlook the indirect channels through which EM gets transmitted, particularly concerning performance. Few researchers have examined the link between EM and other variables using a nonlinear method (Costa et al., 2018; Guo et al., 2019; Mazumder, 2017; Mensah et al., 2023; Wu, 2014). The current study seeks to re-examine the EM – performance nexus utilizing a nonlinear threshold regression approach with national governance quality (NGQ) as the threshold variable.

The study adopts agency and signaling theories to understand how complex EM and national governance quality can enhance firm performance and increase wealth. The agency theory describes a situation where individuals act opportunistically to maximize their wealth at the detriment of shareholders. However, EM can be used as a signaling device through discretionary accruals to signal future positive changes in earnings which can be beneficial for overall firm performance.

This study contributes to the literature in a variety of ways. First, it directs its inquiry toward the distinct setting of sub-Saharan African businesses, an area often overlooked in studies of this nature (see, Callao et al., 2014a). In their comprehensive survey of earnings management research in reputable accounting and finance journals, Callao et al. (2014a, 2014b) discovered an absence of studies from Africa, despite the acknowledgment of the prevalence of this phenomenon in all capital markets (Beneish, 2001). Besides, recent emerging studies from Africa depict a notable scarcity of panel cross-country investigations into earnings management within the African context. This situation provides an opportunity to shed insights into this phenomenon by employing cross-country panel samples of firms operating in the distinctive sub-Saharan African context, whose governance systems are very different from those of the West from where most earnings management investigations emanate. Second, the study introduces and demonstrates how NGQ can change the EM – performance relationship from a dynamic nonlinear threshold framework that previous research has not looked at. Third, the study’s use of NGQ as measured through a rotated principal component analysis of Government Effectiveness, Regulatory Quality, and Rule of Law (Kaufmann et al., 2011) to capture the influence of national governance and institutional quality on EM and firms’ performance, allows for a more nuanced analysis of diverse governance factors examined in a unified framework. Fourth, it is among the first multi-country studies to examine the EM – performance nexus from a nonlinear threshold perspective, with NGQ used as a threshold variable. Fifth, the study’s findings extend the traditional agency theory by showing that EM’s performance effect depends on the country-level governance structures in which businesses are embedded. Finally, our research is relevant to stakeholders, particularly policymakers and standard setters, who must establish several standards to improve national governance quality and minimize earnings management.

The remainder of the paper is structured as follows: The next section provides a concise overview of the theoretical and empirical discussions concerning how national governance systems could influence the relationship between earnings management and firm performance, thereby laying the foundation for the study’s hypotheses. The following section then outlines the data and its origins, and discusses the analytical methods employed to examine the study’s hypotheses. The subsequent section presents the study’s findings. Finally, the last section concludes the study, addressing its limitations and offering recommendations.

Literature Review and Hypothesis Development

Signaling Theory

A significant body of evidence indicates that companies employ earnings management as a signaling mechanism, with managers using discretionary accruals to communicate future positive changes in cash flows or earnings (Holthausen & Leftwich, 1983). Koerniadi (2007), for example, has long offered evidence to support the claim that managers utilize discretionary accruals and dividend increases to convey confidential information about their firm’s future value. Linck et al. (2013) proposed and tested the idea that financially constrained companies with crucial projects use discretionary accruals to reliably indicate favorable prospects, allowing them to raise funds for investment. As a result, their findings prove that using discretionary accruals can assist constrained companies with worthwhile projects and boost firm value. In a recent study on the signaling effect of discretionary accruals, Pham et al. (2019) discovered that discretionary accruals are insignificantly connected to contemporaneous stock returns. However, they discover that income-increasing discretionary accruals of GAAP-compliant growth firms are strongly and positively correlated with contemporaneous stock returns. They also demonstrated that this favorable effect is larger for companies with better corporate governance processes. Cudia and Dela Cruz (2018) also discovered that managers use earnings management efficiently to signal confidential information to stakeholders.

Agency Theory

The agency theory put forth by Jensen and Meckling (1976), along with the positive accounting theory developed by Watts and Zimmerman (1978), acknowledges that individuals will consistently act in self-serving ways to enhance their financial gains. When decision-making authority has been delegated, it can lead to some loss of efficiency and, consequently costs; agency costs. While agency cost is a fundamental problem in corporate governance, researchers have sought ways to minimize it and pursue value maximization (Man, 2019). The main problem with the delegation of duties is conflicts of interest. Agency theory posits that the rift between the shareholders’ and managers’ interests will lead to new managerial problems, such as managerial mischief (Nyberg et al., 2010). Because all individuals are driven by self-interest, the interest of one may conflict with the interest of the other. The separation of control and ownership, and the conflicts of interest, lie at the base of the agency theory. From the shareholder’s perspective, the main goal would be to maximize the firm’s value by generating higher profitability for the corporation. However, the agency theory explains that the agents will act opportunistically to maximize their rewards. Hence, the interests of shareholders conflict with the interests of the agents. Organizations employ mechanisms to align the interests of the agents and the principals to reduce the opportunistic behavior of managers. Contracts, for example, are used to ensure that all parties, acting in their self-interest, are simultaneously motivated toward maximizing the organization’s value (Deegan & Unerman, 2006, p. 215). These mechanisms, however, are only sometimes effective in avoiding earnings management by managers. Demski and Feltham (1978) demonstrated that agency theory uses employment contracts differently to influence financial information based on the firm’s situation in the labor market and the firm’s standards. The empirical results of this study regarding earnings management and performance support the age-old agency problem of conflict of interests and how the quality of governance standards serves to address it.

The quality of governance at the national level is often a pointer to economic and political stability. Improvements in government’s effectiveness, regulatory quality, and the rule of law of a country are attractive signals to investors who usually look for stable political, governance and business environments. Robust governance systems such as strong investor protection mechanisms and effective internal monitoring systems are expected to limit opportunistic behavior and deliver decent returns on investors’ funds. Therefore, a solid national governance system is expected to affect firm performance positively. EM practices in weaker governance environments are expected to be opportunistic as managers would have more room to abuse their discretion in disregarding other stakeholders. On the contrary, efficient EM practices are expected in robust governance environments as unscrupulous behavior would be subjected to dire consequences such as strict legal enforcement of investor protection laws. The agency theory’s prediction regarding governance and EM is that an inverse relationship would ordinarily exist, with causality running from governance to EM. Prior empirical studies have largely demonstrated a favorable link between national governance or institutional quality and firm performance (Borges Junior et al., 2023; Chang, 2023; Ngobo & Fouda, 2012). In addition, a positive association is predicted between governance and firm performance by the agency theory, with causality flowing from governance to performance. We, therefore, hypothesize as follows:

H1. The level of NGQ in a country is positively related to its firms’ performance.

Research findings concerning the correlation between a nation’s degree of national governance quality and the extent of EM within its corporations have yielded conflicting results (Abdou et al., 2021; Duong et al., 2022; Elkalla, 2017). Investigating the influence of earnings management on corporate performance, Duong et al. (2022) found that internal governance constrains EM more efficiently than external governance. Moreover, they noted that internal governance exerts a more pronounced effect on earnings manipulation in countries characterized by deficient external governance mechanisms. Their findings show that effective inside governance mechanisms serve as a substitute rather than a complement to an outside governance system. In a weaker external governance environment, internal governance systems appear to be more effective in restricting EM behaviors and improving firm performance (Wu, 2021). Elkalla (2017) provides evidence of a favorable relationship between the national governance index and discretionary accruals. Abdou et al. (2021) investigated the link between EM and corporate governance in a sample of British and Egyptian firms. They discovered that governance quality (i.e., corruption control) had an apparent hidden effect on EM. They emphasized that regulators and policymakers can dissuade EM by regulating the level of corruption in their respective countries. Aslan and Kumar (2014) previously asserted that the quality of national governance significantly affects agency-principal dynamics within companies. Consequently, the performance of a company is shaped by various factors including industry conditions, corporate governance protocols, other firm-specific variables, and the quality of governance within the country (Anderson & Gupta, 2009; Ngobo & Fouda, 2012; Wu, 2021). Moreover, Lei and Wang (2019) illustrated the impact of China’s governmental anti-corruption efforts in mitigating accrual earnings management behaviors among businesses. Over the period from 2008 to 2017, the researchers examined a sample of A-share listed firms and investigated how anti-corruption measures influenced the substitution effect of earnings management, using 2013 as the pivotal year for categorizing anti-corruption events. Overall, the emerging body of literature underscores the significant role that national-level governance factors play in shaping micro-level corporate behaviors, such as firms’ earnings management practices, and consequently, their performance. We therefore hypothesize that:

H2. The relationship between EM and firm performance is nonlinear and may be contingent on the level of NGQ

Clearly, alterations in governance factors at the country level appear to impact the practices of EM within individual firms and subsequently affect their performance. Nevertheless, conflicting pieces of evidence suggest the need for further investigations. Moreover, many prior studies have tended to rely on linear frameworks with stringent assumptions. Therefore, this current study aims to introduce a fresh approach to examining the relationship between EM and firm performance using a nonlinear threshold framework. The study posits that the variable representing national governance quality (NGQ) could modify the relationship between EM and performance. Thus, NGQ is considered a threshold variable capable of influencing the performance implications of EM and other explanatory variables. Additionally, the study hypothesizes a non-monotonic relationship between EM and performance, contingent upon NGQ. Specifically, it suggests that as NGQ increases, firms should adopt more efficient EM practices, whereas decreasing NGQ levels may lead to opportunistic EM practices. The following hypotheses will therefore be tested:

H3. There exists an NGQ threshold over which the performance effects of EM change from opportunistic to efficient.

Data and Method

The study’s dataset consists of 52 publicly traded companies obtained from the stock exchanges of nine Sub-Saharan African nations spanning from 2007 to 2019. The selection of both the sample and the study period (2007–2019) was based on the availability of annual reports and financial data. Financial institutions and banks were excluded from the sample due to significant differences in their financial accounting methods compared to non-financial firms, which complicates the calculation of discretionary accruals for such entities (see also Dittmar & Mahrt-Smith, 2007; Schultz et al., 2010). This limitation in the sample suggests that caution should be exercised when generalizing the study’s findings to firms operating in the financial services sector, such as banks and insurance companies.

Annual reports and financial statement data for non-financial firms from the nine selected countries were obtained from the Library of African Markets, AfricanFinancials, MachameRatios, and country Stock Exchanges. There were a total of 107 annual reports data on our study’s targeted non-financial firms covering nine countries which could be sourced from the databases we consulted. These databases provide annual reports data on listed firms in Africa on an as-available-basis. The annual reports data on firms collected comprised the following: 5 from Ghana, 11 from Kenya, 2 from Malawi, 5 from Mauritius, 2 from Namibia, 40 from Nigeria, 35 from South Africa, 3 from Tanzania, and 4 from Zambia, all making a total of 107. Of the 107 firms whose annual reports data were collected, 55 had missing and inadequate data covering to the study period of 2007 to 2019; hence these were dropped from the study sample. Consequently, only 52 firms’ data comprising 5 from Ghana, 6 from Kenya, 2 from Malawi, 2 from Mauritius, 2 from Namibia, 13 from Nigeria, 17 from South Africa, 3 from Tanzania and 2 from Zambia were retained and used in the study’s analysis which required a balanced panel. The study meticulously reviewed and filtered the collected annual reports data by cross-referencing them with the websites of the sampled firms. This was done to ensure the reliability of the data and minimize any missing values. Data pertaining to variables specific to each firm were extracted from their annual reports, while information regarding national governance quality was sourced from the World Bank’s Worldwide Governance Indicators (Kaufmann et al., 2011). Kaufmann et al. (2011) delineated six facets of national governance quality, including voice and accountability, political stability, government effectiveness, regulatory quality, rule of law, and corruption control. However, in line with the approach advocated by Knudsen (2011), Nguyen et al. (2015), and van Essen et al. (2013), the study focused on the most pertinent indicators of governance quality at the national level concerning business operations. Consequently, three indices of national governance were selected: Government Effectiveness, Regulatory Quality, and Rule of Law.

Description of Study Variables

The study utilizes return on assets (ROA) as its key measure of firm performance (PERF) because it reflects a firm’s gains generated for all its capital providers. For robustness checks, the return generated for only equity providers of finance (i.e., ROE), and Tobin’s Q (i.e., TOBQ) are used as alternative measures of firm performance in the study’s estimations. These firm performance measures which are used as dependent variables in the current study’s models have been utilized severally and justified in the literature (see e.g., Sow & Tozo, 2019; Zhou et al., 2017).

The main independent variable of interest in the current study; earnings management, can be measured in several ways. The commonly utilized metrics for examining earnings management across different countries in the literature encompass various approaches, including aggregate accruals methods (Dechow et al., 1995; Jones, 1991; Pae, 2005), discretionary revenues models (Stubben, 2010), earnings distribution methods (Bissessur, 2008; McNichols, 2000), and real activities methods (Kuo et al., 2014; Roychowdhury, 2006; Zamri et al., 2013). In this study, the aggregate accruals model proposed by Pae (2005) was chosen as the proxy for accrual earnings management in the analysis. This decision was based on its demonstrated superior predictive capability when applied to the dataset under examination.

The study utilized the national governance quality index, a key variable, which was derived through rotated principal component analysis incorporating three dimensions from Kaufmann et al.’s (2011) six dimensions of national governance quality. These three dimensions have been identified as particularly pertinent to assessing governance quality at the country level with respect to firm operations (Nguyen et al., 2015). Previous research has established associations between national governance and both firm performance (Bruno & Claessens, 2010; Wu, 2021) and earnings management (Abdou et al., 2021), as well as between earnings management and firm performance (Boachie & Mensah, 2022; Gunawan et al., 2015). These findings provide a basis for the present study to explore the interaction of these variables within a fresh methodological framework.

In addition to earnings management, the study incorporates controls for various factors known to influence firm performance based on prior research evidence. These factors include firm size (Zhou et al., 2017), growth opportunities (Kothari et al., 2002), leverage (Pham et al., 2015), firm age (Lin & Fu, 2017), asset tangibility (Boachie & Mensah, 2022), IFRS adoption (Key & Kim, 2020), and corporate governance quality (Asiedu & Mensah, 2023) in its analyses. These variables and their measurements are summarized in Table 1.

The Study’s Variable Measurement.

Source. Authors’ compilation, 2022.

Dynamic Panel Threshold Regression Model

In this paper, we employ the dynamic panel threshold regression model to explore the potential nonlinear correlation between earnings management and firm performance. Traditional panel data models often employ quadratic, polynomial, or piecewise specifications to investigate nonlinearity. However, these methods have certain limitations that the threshold model can overcome. Polynomial regression models impose the order of the polynomial function on the relationship between variables, assuming all firms share an identical earnings management – firm performance relationship once the model is identified. This can be misleading as managerial earnings management evolves alongside the internal and external monitoring mechanisms of firms, meaning high and low earnings management may not have the same impact on firm performance. In piecewise regression, the selection of earnings management levels is subjective, leading to results and conclusions that are sensitive to this choice.

Panel threshold models, such as those proposed by Hansen (1999), Seo and Shin (2016), and Seo et al. (2019), allow for the asymmetric effect of exogenous variables based on whether the threshold variable is above or below an unknown threshold. The threshold variable is typically determined by the economic model, and in our study, we choose the quality of governance at the national level (NGQ) as the threshold variable. Firms can transition between groups over time depending on changes in this variable. Estimated coefficients vary among firms and over time, addressing firm heterogeneity and the time instability of coefficients. Compared to polynomial and piecewise regression models, threshold models offer more flexibility and consistency as they estimate the threshold level either from an endogenous explanatory variable or, in our case, an exogenous variable to the model (i.e., NGQ). This enables us to examine the impact of our variable of interest, namely earnings management, on firm performance both above and below the threshold level.

Panel threshold models, initially introduced by Hansen (1999) and subsequently refined by Seo and Shin (2016), Seo et al. (2019), and Miao et al. (2020), have found widespread application in exploring nonlinear relationships across various domains, including macroeconomics (Ben Cheikh & Ben Zaied, 2020; Khue & Lai, 2020), energy economics (Apergis, 2019; Chiu, 2017), finance (Kadilli, 2015; Namouri et al., 2018), and more recently, governance (Gharbi & Othmani, 2022; Hu et al., 2022). In this study, we adopt the threshold model proposed by Seo et al. (2019), which employs first-differenced generalized method of moments (GMM) estimators and the corresponding asymptotic variance estimator introduced by Seo and Shin (2016). Additionally, the model incorporates linearity testing to assess the presence of a threshold effect. Moreover, our model introduces a computationally more efficient bootstrap algorithm for implementing the linearity test compared to the nonparametric independent and identically distributed bootstrap originally suggested by Seo and Shin (2016). Furthermore, the model includes a constrained GMM estimator that accounts for the kink restriction, a technique that has gained popularity in recent years, as evidenced by studies such as Zhang et al. (2017), along with its asymptotic variance formula and a consistent estimator.

Models Specification and Estimations

For the analysis in this study, the following models are defined. Firstly, linear dynamic models are specified, and their estimation is carried out using traditional techniques such as fixed effect (FE), ordinary least squares (OLS), system generalized method of moments (SGMM), and difference generalized method of moments (DGMM). These estimators were selected based on diagnostic tests conducted in the study to determine suitable panel data estimators.

Where

In terms of diagnostics, the Durbin-Wu-Hausman (DWH) test was employed to assess the endogeneity of regressors, operating under the null hypothesis that endogenous regressors could be regarded as exogenous variables (Baum et al., 2007). Each potential endogenous regressor underwent testing, with test statistics following a Chi-squared (Chi-sq) distribution with one degree of freedom for each regressor. Following Schultz et al. (2010), the test was conducted based on the firm performance equation (in levels), with 1-year lagged changes of each regressor used as instrumental variables. A combined endogeneity test was also conducted, employing eight degrees of freedom, corresponding to the number of potential endogenous regressors (EM, CGQ, NGQ, SIZE, GROP, LEV, IFRS, and AT). Endogeneity tests were separately conducted for each variable in the study, with only firm age considered exogenous across all test specifications, while the remaining variables were treated as endogenous.

Results indicated that the null hypothesis could not be accepted for one of the individual endogeneity tests, specifically for leverage [i.e., χ2(1) = 7.34401, p = .0067)], nor for the combined endogeneity test encompassing all variables [i.e., χ2(8) = 16.5569, p = .0351)], suggesting the presence of endogeneity in the explanatory variables. Consequently, the study adjusted for the endogeneity of the leverage variable in its threshold estimations.

To explore potential nonlinearities in the relationship between earnings management (EM) and firm performance, the study employed a threshold model and estimated it utilizing the dynamic panel threshold regression approach via the generalized method of moments (GMM). This method is adept at revealing potential shifts in all explanatory variables, including the EM variable (Seo et al., 2019). For this analysis, the Stata community contributed command ‘xthenreg’, developed by Seo et al. (2019), was utilized. The analysis proceeded in three steps, following the model outlined below.

Where

Moreover, apart from conducting dynamic panel threshold regression estimation, which inherently includes a lagged dependent variable as an additional explanatory variable, a static restriction was applied to assess potential significant changes in results. Furthermore, although the threshold model typically suggests a discontinuity in the regression function, it might imply the presence of a kink rather than a jump if

Where the variable definitions and measurements are as previously described. Once more,

The final steps in the study’s estimations involved three distinct specifications: 1) The dynamic panel threshold model was specified without any specific classification of endogenous and exogenous variables; 2) The model was specified with the direct inclusion of an ad hoc lag leverage variable to address endogeneity concerns; 3) The model was formulated with explicit classifications for exogenous and endogenous variables.

Across all these specifications, the bootstrap p-value for the linearity test was zero, indicating confirmation of the presence of nonlinearity or a non-monotonic relationship between firm performance and the included explanatory variables. The number of moment conditions for the first and second dynamic model specifications remained consistent at 165, while that for the third specification was 231. A distinct NGQ threshold estimate was determined (i.e., r = .0113, 1.082***, and 0.446***, respectively) in each case.

A simulation test was conducted with the grid number set at grid(15) and the trim rate at trim_rate(0.1), resulting in nearly identical parameter estimates for almost all explanatory variables, yet yielding another threshold estimate of r = .525***. The results of the study’s sequential estimations of its baseline and robustness test models are presented and discussed in the next section.

Results and Discussion of Findings

Descriptive Statistics

Tables 2 and 3 summarize the descriptive statistics and correlation diagnostics for the variables in the study. The mean Return on Assets (ROA) stands at 8.03%, suggesting comparable returns earned by financiers to companies in Sub-Saharan Africa during the sample period to those reported in other countries (Elkalla, 2017). The Corporate Governance Quality (CGQ) and National Governance Quality (NGQ) indices exhibit means of −0.209 and 0.0267, respectively, on a scale ranging from −1.294 to +2.334. These aggregate governance indices for sampled companies in Sub-Saharan Africa indicate low levels, reflecting minimal progress in developing national and corporate governance institutions within the African subregion.

Descriptive Statistics of the Study’s Variables.

Note. This table reports descriptive statistics based on a balanced sample with 676 observations. The variables are as defined in Table 1. For interpretation purposes, the descriptive statistics are calculated on the basis of levels with the exception of IFRS Adoption which was computed from a dummy scale, CGQ and NGQ which were calculated as indices from normalized rotated principal component analysis, and Firm Size, Age and Leverage which were calculated on the basis of logarithmic form to normalize their histogram distributions for a meaningful statistical analysis. The ROA, being the dependent variable in our model, was not transformed but allowed to retain its original form for 1) ease of interpretations, 2) because its histogram distribution appears normal.

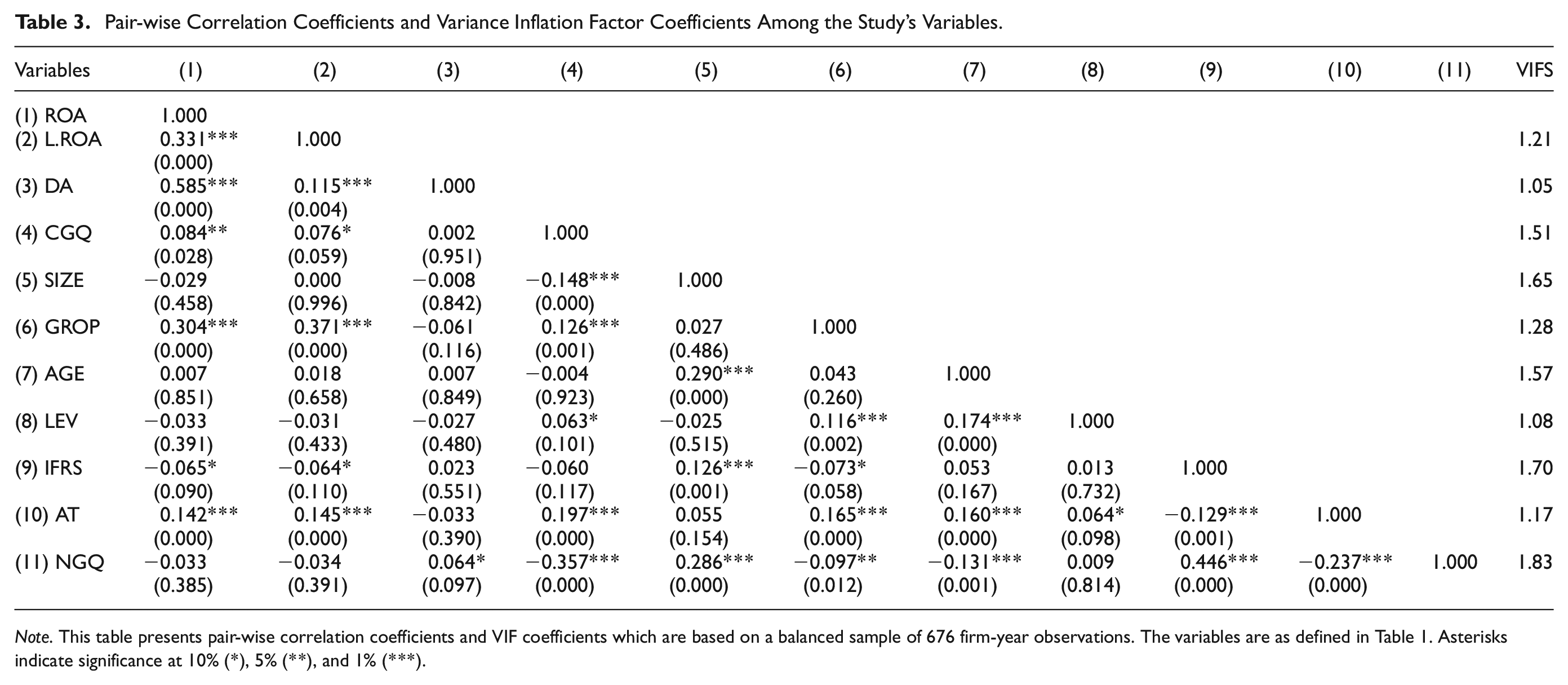

Pair-wise Correlation Coefficients and Variance Inflation Factor Coefficients Among the Study’s Variables.

Note. This table presents pair-wise correlation coefficients and VIF coefficients which are based on a balanced sample of 676 firm-year observations. The variables are as defined in Table 1. Asterisks indicate significance at 10% (*), 5% (**), and 1% (***).

The average amount of discretionary accruals, or the proportion of managed earnings for sampled companies, was approximately 0.020, comparable to figures reported in other emerging economies (Tang & Chang, 2015; Zimon et al., 2021), and suggest the prevalence of earnings management practices among firms in Sub-Saharan Africa. The average firm size, expressed logarithmically, was 5.29, with a standard deviation of 0.72, while the average leverage was 3.81, with a standard deviation of 0.69. These metrics, presented in logarithmic form so as to normalize their histogram distributions for meaningful statistical analysis, indicate moderate firm sizes and a balanced mix of equity and debt in the surveyed companies’ capital structure.

With a mean market-to-book ratio of 3.72 and a standard deviation of 5.62, the sampled firms displayed moderately strong growth opportunities with occasional erratic surges in growth. Additionally, 36% of the sampled firm’s assets were tangible, and about 84.6% of the sample firm-year observations indicated the adoption of International Financial Reporting Standards (IFRS). IFRS adoption is believed to enhance the information environment, improve earnings quality, and enhance performance measurement ratios (Abdullah & Tursoy, 2021; Abiodun & Asamu, 2018). Finally, the average business age, approximately 55 years or 3.80 when expressed logarithmically, suggests that many sampled firms are still maturing within their respective industries.

Table 3 indicates that the majority of the firm-specific variables postulated in the literature to be associated with performance (Khan et al., 2017; Kim et al., 2021) hold true in the African context. None of the correlation coefficients among the independent variables exceeds .80, indicating that the empirical regression analysis is devoid of multicollinearity concerns (Gujarati, 2004). This is further corroborated by the Variance Inflation Factor (VIF) coefficients presented in the final column of Table 3.

Multiple Regression Results and Analysis

The current study employs a combination of linear and nonlinear threshold regression models to investigate its hypotheses. Initially, the study fits a dynamic multiple linear regression model (Equation 1) and estimates it using various estimation techniques including fixed effect, Ordinary Least Squares (OLS) with Driscoll-Kraay standard error estimators, and system and difference Generalized Method of Moments (GMM). The classical Hausman test was conducted to determine the appropriate econometric estimation method, selecting the fixed effect estimator. Furthermore, the Breusch and Pagan Lagrangian multiplier test confirms var(u) = 0, allowing the use of the pooled OLS estimator for comparison. These estimations are then performed using Driscoll-Kraay standard errors due to the independently distributed residuals of the variables (i.e., χ2(2) = 4.20, p = .1224 on the joint test of normality of residuals). It has been observed that even in the presence of heteroscedastic residuals, standard errors derived from this estimator remain consistent (Driscoll & Kraay, 1998). Additionally, GMM estimators are utilized as acceptable dynamic panel data estimators for their acclaimed ability to address endogeneity (Arellano & Bond, 1991; Blundell & Bond, 1998). The results of the study’s multiple linear regression analyses conducted from a dynamic perspective are presented in Table 4.

Linear Regression Results of the EM - Performance Nexus using OLS, SGMM, FE, and DGMM Estimators From a Dynamic Approach.

Note. This table reports empirical results from estimating Equation 1 through the use of OLS and FE with Driscoll-Kraay Standard Errors Estimators from a dynamic approach. As typical Dynamic Panel Estimators, the SGMM and DGMM were also utilized in estimating Equation 1. Asterisks indicate significance at 10% (*), 5% (**), and 1% (***). The notations in all the regression tables are as defined in Table 1.

The study reveals that while earnings management (EM) consistently shows a positive correlation with performance, this relationship does not reach statistical significance when using dynamic Generalized Method of Moments (GMM) estimators. Additionally, the National Governance Quality (NGQ) variable appears to be an insignificant predictor of firm performance on its own. This inconclusive evidence regarding the EM – performance relationship and the apparent lack of significance of NGQ concerning firm performance, contrary to theoretical predictions, prompted the study to explore nonlinear threshold models to reassess the EM – performance connection.

Thus, the study estimated dynamic threshold models outlined in Equations 2 and 3 to re-examine the EM – performance relationship, under the assumption that there might be a sudden change or a shift in the EM – performance association, possibly dependent on an NGQ transmission mechanism suggested in emerging literature. The results of these estimations are provided in Tables 5 to 8. They confirm the study’s hypothesis that the EM – performance relationship is contingent on national institutional factors, particularly NGQ.

Test of the Dynamic Threshold Effects of NGQ on the EM – Firm Performance Relationship With No Lags Used for Any Endogenous Explanatory Variables.

Note. This table reports empirical results from estimating a dynamic GMM panel threshold regression model (i.e., Equation 2) with ROA as the dependent variable, NGQ as the threshold variable, and all the other explanatory variables as region variables. In addition, a kink restriction is introduced in the model for further investigation of a possible kink in the relationship (i.e., Equation 3). Again, a static restriction is imposed in each of these models to observe changes. These regression estimations were executed via the community contributed Stata command “xthenreg.” Asterisks indicate significance at 10% (*), 5% (**), and 1% (***). The notations in all the regression tables are as defined in Table 1. The parameter estimates with designation (_b) are below the threshold whereas the parameter estimates with designation (_d) are above the threshold.

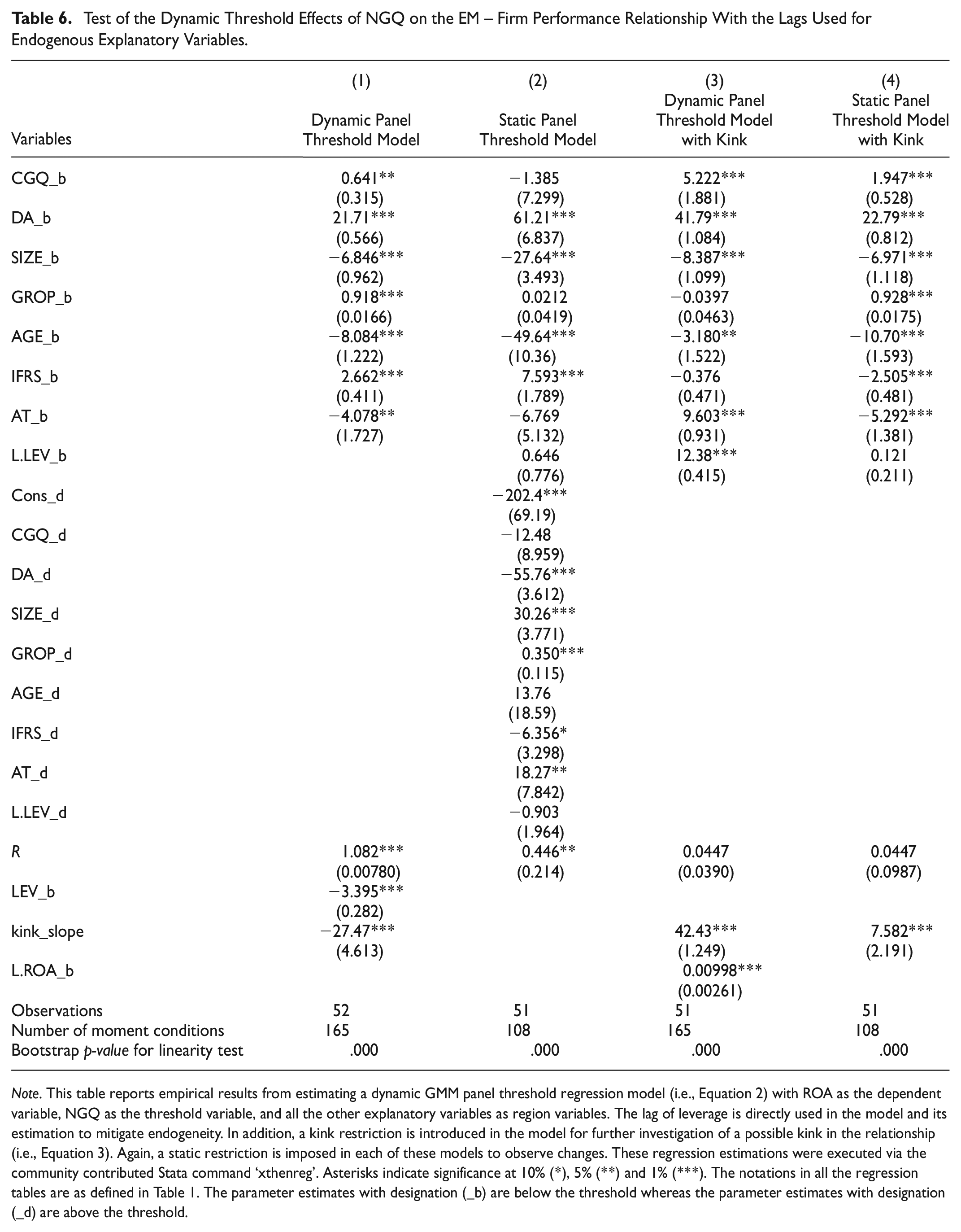

Test of the Dynamic Threshold Effects of NGQ on the EM – Firm Performance Relationship With the Lags Used for Endogenous Explanatory Variables.

Note. This table reports empirical results from estimating a dynamic GMM panel threshold regression model (i.e., Equation 2) with ROA as the dependent variable, NGQ as the threshold variable, and all the other explanatory variables as region variables. The lag of leverage is directly used in the model and its estimation to mitigate endogeneity. In addition, a kink restriction is introduced in the model for further investigation of a possible kink in the relationship (i.e., Equation 3). Again, a static restriction is imposed in each of these models to observe changes. These regression estimations were executed via the community contributed Stata command ‘xthenreg’. Asterisks indicate significance at 10% (*), 5% (**) and 1% (***). The notations in all the regression tables are as defined in Table 1. The parameter estimates with designation (_b) are below the threshold whereas the parameter estimates with designation (_d) are above the threshold.

Test of the Dynamic Threshold Effects of NGQ on the EM – Firm Performance Relationship With Specification of Endogenous and Exogenous Variables in the Model.

Note. This table reports empirical results from estimating a dynamic GMM panel threshold regression model (i.e., Equation 2) with ROA as the dependent variable, NGQ as the threshold variable, and all the other explanatory variables as region variables. The model specifies endogenous and exogenous variables. In addition, a kink restriction is introduced in the model for further investigation of a possible kink in the relationship (i.e., Equation 3). Again, a static restriction is imposed in each of these models to observe changes. These regression estimations were executed via the community contributed Stata command ‘xthenreg’. Asterisks indicate significance at 10% (*), 5% (**), and 1% (***). The notations in all the regression tables are as defined in Table 1. The parameter estimates with designation (_b) are below the threshold whereas the parameter estimates with designation (_d) are above the threshold.

Further Simulation Test of the Dynamic Threshold Effects of NGQ on the EM – Firm Performance Relationship (Using a Different Grid Number & Trim Rate).

Note. This table reports simulation test results from estimating the dynamic GMM panel threshold regression model (i.e., Equation 2) using a different grid number and trim rate. The models clearly specified endogenous and exogenous variables where the lag of endogenous variables was used as instruments in the estimation although the endogenous variables maintained their original forms in the respective models. These regression estimations were executed via the community contributed Stata command ‘xthenreg’. Asterisks indicate significance at 10% (*), 5% (**), and 1% (***). The notations in all the regression tables are as defined in Table 1. The parameter estimates with designation (_b) are below the threshold whereas the parameter estimates with designation (_d) are above the threshold.

The findings further suggest that the impact of earnings management (EM) on performance varies depending on the estimated National Governance Quality (NGQ) threshold. Below this threshold, EM has a positive effect on performance, whereas above it, the effect of EM on performance is either insignificant or occasionally negative. In a simulation analysis conducted with different trim rates and grid numbers, the threshold estimation yields nearly identical parameter estimates for most explanatory variables but slightly alters the threshold estimate, denoted as ‘r’ (refer to Table 8). These results imply that below the optimal NGQ threshold, EM tends to reflect efficiency-driven motives or outcomes, while above this threshold, opportunistic motives of EM become apparent. The subsequent tables: Tables 9 to 11 present results of the study’s additional robustness tests.

Robustness Test of the Dynamic Threshold Effects of NGQ on the EM – Firm Performance Relationship Using an Alternative Performance Indicator (ROE).

Note. This table reports robustness test results from estimating the dynamic GMM panel threshold regression model (i.e., Equation 2) using alternative performance indicators (i.e., ROE). The models clearly specified endogenous and exogenous variables where the lag of endogenous variables was used as instruments in the estimation although the endogenous variables maintained their original forms in the respective models. These regression estimations were executed via the community contributed Stata command ‘xthenreg’. Asterisks indicate significance at 10% (*), 5% (**), and 1% (***). The notations in all the regression tables are as defined in Table 1. The parameter estimates with designation (_b) are below the threshold whereas the parameter estimates with designation (_d) are above the threshold.

Robustness Test of the Dynamic Threshold Effects of NGQ on the EM – Firm Performance Relationship Using an Alternative Performance Indicator (Tobin’s Q).

Note. This table reports robustness test results from estimating the dynamic GMM panel threshold regression model (i.e., Equation 2) using alternative performance indicators (i.e., TOB_Q). The models clearly specified endogenous and exogenous variables where the lag of endogenous variables was used as instruments in the estimation although the endogenous variables maintained their original forms in the respective models. These regression estimations were executed via the community contributed Stata command ‘xthenreg’. Asterisks indicate significance at 10% (*), 5% (**) and 1% (***). The notations in all the regression tables are as defined in Table 1. The parameter estimates with designation (_b) are below the threshold whereas the parameter estimates with designation (_d) are above the threshold.

Robustness Test of the Dynamic Threshold Effects of NGQ on the EM – Firm Performance Relationship Using an Alternative NGQ Measurement.

Note. This table reports robustness test results from estimating the dynamic GMM panel threshold regression model (i.e., Equation 2) using alternative national governance indicator [i.e., NGQ(a)]. The models clearly specified endogenous and exogenous variables where the lag of endogenous variables was used as instruments in the estimation although the endogenous variables maintained their original forms in the respective models. These regression estimations were executed via the community contributed Stata command ‘xthenreg’. Asterisks indicate significance at 10% (*), 5% (**), and 1% (***). The notations in all the regression tables are as defined in Table 1. The parameter estimates with designation (_b) are below the threshold whereas the parameter estimates with designation (_d) are above the threshold.

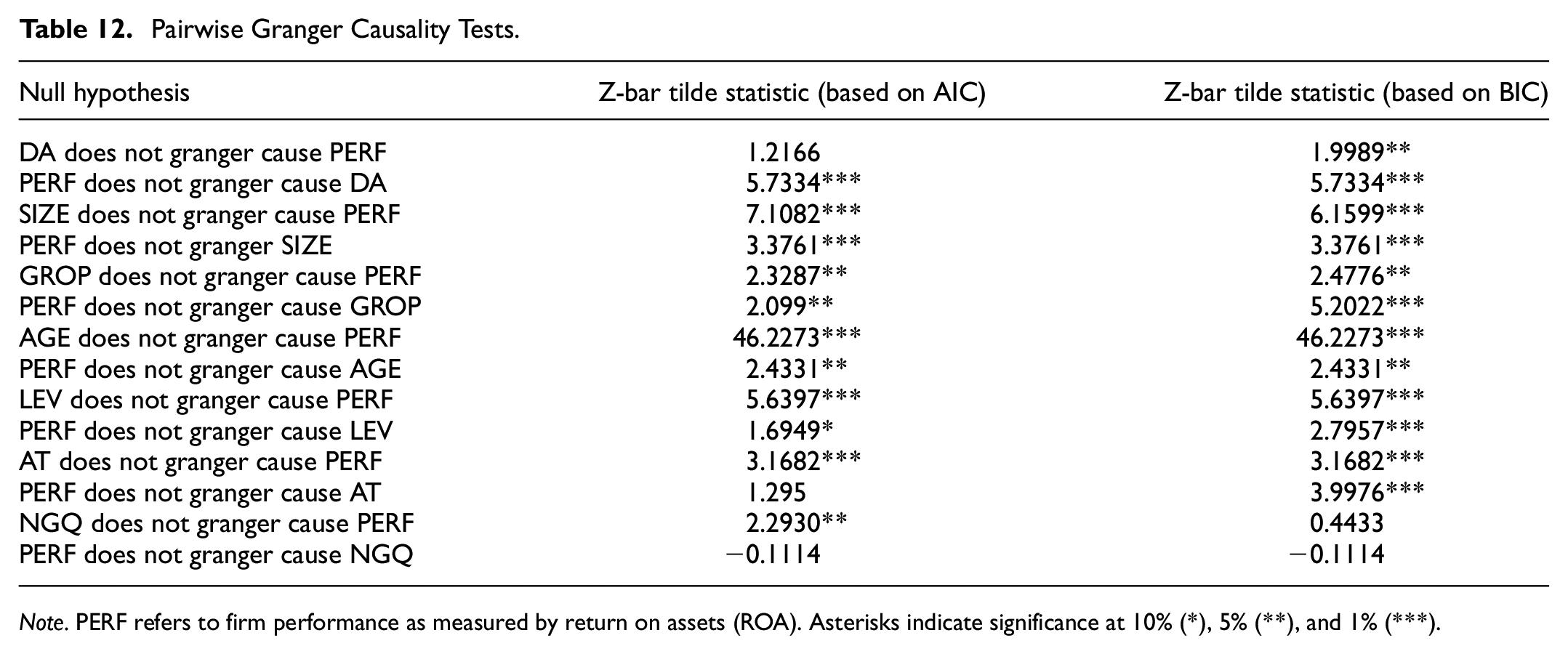

The additional test results remain consistent and robust when different performance indicators (such as Return on Equity [ROE] and Tobin’s Q) and alternative measures of National Governance Quality (NGQ) are employed in the estimation. Additionally, the study observes from its Granger causality tests (see Table 12) that NGQ has a causal relationship with performance, providing further support for the significant role that NGQ plays in influencing the dynamic effects of the study’s explanatory variables across its threshold. These original empirical insights serve as the study’s contribution to this ongoing discussion.

Pairwise Granger Causality Tests.

Note. PERF refers to firm performance as measured by return on assets (ROA). Asterisks indicate significance at 10% (*), 5% (**), and 1% (***).

Discussion of Findings and Implications

The present study acknowledges that firm-level dynamics are influenced by national institutional factors that shape corporate operations within their respective jurisdictions. Hence, it aimed to investigate whether National Governance Quality (NGQ) factors can modify the relationship between earnings management (EM) and firm performance, thereby contributing to our comprehension of this association. By utilizing NGQ as a threshold variable to analyze the EM – firm performance relationship, the study discovered that the impact of EM depends on an optimal NGQ threshold of 0.446***. Below this threshold, EM positively affects performance. However, above the optimal NGQ threshold, the impact of EM on firm performance becomes insignificant or occasionally negative. This suggests a direct correlation between the quality of national governance and the performance-enhancing aspects of EM practices, up to a certain threshold. Beyond this threshold, firms appear to become divisive in their EM practices, possibly in response to a more tightened governance environment, hence culminating in opportunistic outcomes of EM cementing the agency theory. Our research backs up the underlying theories of earlier studies that discovered a connection between NGQ and other variables. It supports the idea of considering NGQ, which is a crucial threshold determinant of EM, and consequently, firm performance.

Our results corroborate those of Abdou et al. (2021), who found that, for Egyptian companies, the national governance variable (control of corruption) moderates the relationship between two corporate governance mechanisms—independent outside directors and female directors—and earnings management negatively. Likewise, our results also agree with Bruno and Claessens (2010) as well as Wu (2021) whose paper demonstrated the moderating effect of country governance on the relationship between firm-level governance and firm performance. Bruno and Claessens (2010) research highlighted the interplay between company-level corporate governance practices and country-level legal investor protection in influencing company performance, suggesting the existence of a threshold level. Above this threshold, stronger regulation could have either negative effects on company outcomes (when the company is well governed) or neutral effects (when the company is poorly governed). In contrast, Elkalla (2017) found contradictory evidence regarding the impact of their study’s composite national governance index on discretionary accruals and firm performance.

When analyzing the results of the SGMM estimator in our study, IFRS adoption was significantly negatively correlated with firm performance. This finding contradicts the results of Abdullah and Tursoy (2021) and Li et al. (2017). This discrepancy may be attributed to the fact that IFRS requires extensive disclosure, leading firms to incur additional costs for technology and logistics to produce the required financial and non-financial information, thus affecting firm performance.

Furthermore, the identified nonlinear effect of EM on firm performance and the NGQ threshold can serve as benchmarks for Africa and other emerging and developing countries in assessing their situations. These findings have significant implications for national governments and their agencies regarding how governance should be conducted to elicit favorable firm-level responses, particularly in terms of promoting efficient EM practices. Additionally, investors typically favor destinations that assure the protection of their capital, demonstrate investor-friendly governance systems, and maintain less corrupt business environments, thus aligning with the signaling theory. Therefore, although a robust national governance environment is healthy, the question of how robust a nation’s governance system should be so as not to deter cross-border investments comes to the fore. A ‘too much stringent or restrictive governance environment’ may be counterproductive for developing nations and their businesses as they seek to attract cross-border investor capital for growth. Therefore, countries should be able to strike a delicate balance between having a more tightened governance environment that invariably elicits opportunistic responses from local business players while also deterring cross-border investments.

Apart from EM, the dynamic threshold models indicate that the control variables (such as corporate governance quality [CGQ], firm size, growth opportunities [GROP], firm age [AGE], leverage [LEV], asset tangibility [AT], and International Financial Reporting Standards [IFRS] adoption) also appear to undergo changes across the NGQ threshold level. Additionally, the study observes from its Granger causality tests that nearly all explanatory variables demonstrate bidirectional causality with the performance variable. The results suggest that corporate governance quality, firm size, age, leverage, asset tangibility, and IFRS adoption are significant determinants of firm performance, which aligns with prior research findings (refer to Boachie & Mensah, 2022; Khan et al., 2017; Kim et al., 2021). Furthermore, their impact may be contingent on the quality of governance at the national level. The positive correlation between CGQ and firm performance indicates that improvements in internal governance quality enhance the ability to monitor managerial opportunism, thereby contributing positively to firm performance. Likewise, firm-age and growth opportunities also exhibit a positive relationship with performance which indicates that, as a firm grows and advances in age, it gains a certain level of legitimacy and credibility with its varying stakeholders which allows it to continue to survive and stay profitable. The proportion of tangible assets in a firm’s asset base also dictates the level of flexibility it has to manipulate earnings and consequently affect the performance of the firm. Hence, higher asset tangibility lowers managerial flexibility with earnings management which usefully reflects in enhanced performance. On the other hand, firm-size, leverage and IFRS adoption negatively relate performance. We attribute these observations largely to cost considerations regarding maintenance of a large firm, servicing interest obligations, and the necessary technology and infrastructure required to be able to comply with complex reporting and disclosures under IFRS regime. Our threshold model however showcases varying changes in these results across the identified threshold. The application of different estimation approaches, the variations in measurements of the study’s variables of interest, and the robustness of the study’s findings address any possible endogeneity concerns.

The findings make a significant theoretical contribution to the literature because there has been little study on the relationship between EM and performance utilizing NGQ or institutional quality indicators as potential threshold variables. The study therefore enhances our understanding of some identified mechanisms via which EM is transmitted to performance. Additionally, based on the results from its SGMM estimator, the study observes that corporate governance quality, asset tangibility, and firm growth opportunities all demonstrated a significant positive relationship with performance. These findings align with the results of Boachie and Mensah (2022). However, firm age, despite having a positive correlation with performance, was found to be statistically insignificant, while leverage exhibited a significantly negative correlation with performance, consistent with the findings of Zimon et al. (2021) and Tang and Chang (2015). Furthermore, firm size was significantly and adversely associated with performance, whereas discretionary accruals were found to be statistically insignificant, despite showing a favorable relationship with performance.

These findings indicate that good national governance regimes can benefit businesses if it does not become overly restrictive to elicit devious behavioral responses such as opportunistic EM behavior. The findings support the idea and emergent stream of research on the role and interface between national governance systems and firm-level characteristics in contributing to performance enhancements. By and large, by employing dynamic panel threshold regression techniques, the research reveals that the impact of earnings management on firm performance is not linear but instead characterized by distinct thresholds. The study highlights the dynamic nature of the governance cum earnings management – firm performance nexus. It identifies specific thresholds or tipping points in NGQ beyond which the beneficial effects of firm earnings management practices become significantly attenuated. It unearths how variations in governance quality thresholds influence the performance outcomes of firms’ earnings management behavior. By delineating threshold effects, the study provides policymakers and managers with actionable insights for enhancing governance practices and mitigating earnings management risks. It underscores the importance of maintaining NGQ at optimal levels to foster transparent and efficient corporate behavior. Moreover, the dynamic panel threshold regression application where NGQ is used as a threshold variable represents a methodological innovation in examining the earnings management – firm performance nexus. By incorporating time-varying thresholds, the study offers a more nuanced understanding of the complex interplay between governance quality dynamics and earnings management strategies. The study contributes to the literature on corporate governance, earnings management, and firm performance by advancing our understanding of these domains’ non-linear relationships and threshold effects. It fills a significant gap in research by offering novel empirical evidence and methodological advancements.

Conclusions and Limitations

Our main objective was to empirically investigate the existence of threshold effects in the relationship between EM and firm performance. Samples were collected from sub-Saharan Africa spanning from 2007 to 2019, with the NGQ level serving as the threshold variable. To our knowledge, this study is the first to utilize the dynamic panel threshold approach to analyze the EM – performance relationship while considering macro-level factors like NGQ as threshold indicators. Additional analyses have confirmed our findings and appear to be robust and unbiased.

The findings indicate that, NGQ has no significant direct impact on firm performance, thus refuting our first hypothesis (H1). However, a causal relationship was identified, suggesting the relevance of including the national governance variable in our model analysis. The relationship between EM and firm performance is nonlinear, displaying shifts at specific transmission mechanisms such as NGQ thresholds. Hence, our second hypothesis (H2) is supported, indicating that the EM – performance connection may depend on macro-level governance factors like NGQ. Additionally, there exists a distinct threshold beyond which the performance impact of EM transitions from beneficial to opportunistic. This however contradicts the study’s third hypothesis (H3). Below the NGQ threshold, EM’s effect on performance is positive, reflecting efficiency motives or outcomes, while above this threshold, EM’s effect becomes negative. Thus, EM has a non-monotonic influence on firm performance, contingent on NGQ levels. Overall, the findings confirm that the performance-enhancing effect of EM, reflecting efficiency-driven motives, is only realized when NGQ is systematically improved up to an optimal threshold level. Beyond this threshold, EM’s impact on performance may become detrimental. Our study provides a significant theoretical contribution by elucidating an underlying mechanism through which EM may affect firm performance. Our study also holds significant implications for practice, research, and society.

In terms of its practical implications, the study’s findings suggest that policymakers and corporate managers would need to work at maintaining NGQ at optimal levels to encourage efficient earnings management behavior and consequently improve firm performance. Some concrete steps which policymakers and managers in developing and emerging economies can take to maintain NGQ at optimal levels include: (1) Targeted Governance Reforms: Prioritize governance reforms aimed at addressing specific weaknesses or vulnerabilities identified through diagnostic assessments or empirical research. Targeted reforms can help enhance NGQ in areas critical to mitigating opportunistic earnings management while fostering an environment conducive to efficient earnings management. (2) Capacity Building and Training: Invest in capacity building and training programs to enhance the skills, knowledge, and expertise of policymakers, regulators, corporate leaders, and other stakeholders involved in governance-related activities. Building institutional capacity is essential for implementing and enforcing governance reforms effectively. (3) Stakeholder Engagement and Participation: Foster stakeholder engagement and participation in governance processes to ensure that reforms are responsive to the needs and priorities of diverse stakeholders, including investors, businesses, civil society, and government agencies. Engaging stakeholders can help build consensus around reform initiatives and promote their effective implementation. (4) Continuous Monitoring and Evaluation: Implement robust mechanisms for monitoring and evaluating NGQ on an ongoing basis. This includes regularly assessing the effectiveness of governance policies and practices, identifying areas for improvement, and adjusting strategies accordingly. (5) Legal and Regulatory Frameworks: Strengthen legal and regulatory frameworks governing corporate governance, financial reporting, and disclosure practices to align with international best practices and standards. This includes enacting laws and regulations that promote transparency, accountability, and integrity in corporate decision-making processes. (6) Independent Oversight and Enforcement: Enhance the independence, authority, and effectiveness of regulatory bodies responsible for overseeing corporate governance and financial reporting practices. Empowering regulatory authorities to enforce compliance with governance standards and impose sanctions for misconduct is critical for maintaining NGQ at optimal levels. (7) Promotion of Ethical Culture: Promote a culture of ethics, integrity, and accountability within organizations and across the business community. This can be achieved through awareness campaigns, ethics training programs, and recognition of ethical leadership practices that prioritize long-term value creation over short-term gains. (8) International Collaboration and Benchmarking: Engage in international collaboration and benchmarking efforts to learn from experiences of other countries and leverage global expertise in governance reform initiatives. Collaborating with international organizations, peer countries, and multilateral institutions can provide valuable insights and technical assistance to support NGQ improvement efforts. (9) Incentives for Good Governance Practices: Introduce incentives, such as tax incentives, regulatory rewards, or access to financing, to encourage companies to adopt and maintain good governance practices voluntarily. Positive reinforcement mechanisms can complement regulatory enforcement efforts and encourage proactive compliance with governance standards. (10) Public Awareness and Advocacy: Raise public awareness about the importance of good governance for economic development, investor confidence, and sustainable business growth. Advocacy campaigns and public education initiatives can mobilize support for governance reforms and create pressure for change among policymakers and corporate leaders. By implementing these concrete steps, policymakers and managers in developing and emerging economies can work toward maintaining NGQ at optimal levels, thereby promoting efficient earnings management practices that contribute to sustainable economic growth and enhanced firm performance.

Besides its practical significance, our study would also benefit academic researchers as it contributes to the literature in this area through theoretical and empirical exploration. Specifically, we expand the discourse on the relationship between earnings management and firm performance by introducing NGQ as a threshold variable. Through this, we contribute toward the understanding and comprehension of how organizations are able to improve their financial performance despite the touted negative impacts of earnings management, thus laying the groundwork for future empirical research endeavors. Lastly, our study aims to influence public perception of governance and earnings management, and how these can contribute to the quality of life in general. Active engagement of stakeholders in governance at national levels profoundly impacts societal well-being and facilitates the sense of ownership and belongingness which is crucial for the collective realization of desirable governance outcomes including efficient earnings management practices, and also, the UN’s sustainable development goal related to peaceful and inclusive societies (i.e., SDG 16).

Like any other research, this study has its limitations. Firstly, it relied on audited annual reports from 52 listed companies across 9 sub-Saharan countries. Therefore, the findings should be understood and interpreted within this specific context. As highlighted by Leuz (2018), the primary challenge hindering the advancement of more comprehensive and impactful policy-related research is the scarcity of data. This same challenge frequently constrains accounting and financial market researchers, preventing them from establishing causal relationships. To overcome this obstacle, Leuz (2018) proposes an active involvement of businesses and regulators in data generation. Specifically, the author recommends the proactive collection of data pertaining to financial reporting and the enforcement of auditing regulations. This collected data can then be shared with researchers for thorough analysis and post-implementation assessments of auditing rules. We recommend for future studies to aim at verifying the findings of the current research by utilizing a more extensive panel dataset once additional data becomes accessible. Subsequent studies should explore samples from developed and other emerging economies to modestly validate the current study’s results using other nonlinear frameworks such as panel smooth transition regression. Furthermore, future research, especially from other emerging market contexts, can build on this study by for example, examining how national governance quality thresholds in their several unique contexts alter the earnings management – firm performance dynamics. Again, it would be interesting to examine how other macro-economic variables such as economic growth, inflation rate, unemployment rate and political stability, or an aggregate measure of these variables such as Okun’s misery index influences the earnings management firm performance dynamics. Arguably, a country’s overall economic growth rate can affect firms’ earnings management decisions. In periods of economic expansion, firms may face less pressure to manipulate earnings to meet expectations. In contrast, there may be more significant incentives to manage earnings to avoid adverse outcomes during economic downturns. Besides, inflation can impact earnings management by affecting the valuation of assets, liabilities, and revenues. High inflation rates may lead firms to engage in income-increasing earnings management techniques to offset the erosion of real value, while low inflation rates may reduce the need for such actions. Furthermore, the stability of the political environment can impact investor confidence, business sentiment, and economic activity. Firms operating in politically unstable countries may face more significant uncertainty and pressure to manage earnings to mitigate risks or appease stakeholders. All these areas present avenues for future inquiry.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability

Data for the study is obtained from publicly available sources and can also be made available upon request.