Abstract

This study employs the perspectives of bounded rationality to examine how government attention affects corporate risk-taking. Additionally, it explores the moderating role of politically connected CEOs’ access to privileged information. A dataset of 1,995 Chinese A-share public firms for the period 2011 to 2020 is employed. The data were analyzed using fixed effect regression. The two-step system GMM estimator, an assessment for omitted variable bias, lagged variable tests, and alternative measures of key variables were used for the robustness test. The findings indicate that both direct and indirect government attention are inversely related to corporate risk-taking. However, this negative relationship is significantly lessened for firms led by politically connected CEOs. These CEOs appear to leverage their access to exclusive information to more effectively mitigate government regulations. This mitigating effect varies; it is most pronounced in two specific situations: (a) in firms with strong internal corporate governance, especially when they are under direct government scrutiny, and (b) in regions with weaker external institutional environments, where political connections act as a substitute for formal market structures. Furthermore, the mechanism analysis reveals that this relationship is channeled through agency costs and financial constraints. Practically, these findings assist companies in balancing the demands for risk-taking and the social duties of government, enabling them to develop effective risk strategies for utilizing these connections to attain a suitable level of risk for the company.

Keywords

Introduction

A centrally planned economy is one of the characteristics of the Chinese economy. There is a natural link between government and companies, with the former achieving social and development goals through firms and the latter accessing more valuable resources through a good connection with government (Cui & Jiang, 2012). Maintaining a strong connection with the government serves as a significant social asset for firms (Ling et al., 2016) to acquire valuable essential resources (Ahmed & McMillan, 2023), which allows for access to privileged information and better business development. Meanwhile, most studies of government and firms have focused on financial distress (Ho et al., 2021), firm performance (Y. Wang et al., 2019), and capital structure (C. Wang et al., 2023). These studies have used traditional theories such as trade-off theory, agency theory, and resource-based theory to explain these issues. Researchers suggest that firms with government attention have easy access to resources from authorities (Ho et al., 2021). This notion is based on the assumption of “perfect rationality,” which assumes that individuals make decisions by optimizing their utility functions in a consistent and flawless manner. However, the traditional economic model fails to capture the full scope of human behavior, as it overlooks the exploratory nature of human values and the imperfections in decision-making processes (McKenzie, 2010).

The concept of “attention” first began in psychological research and specifically refers to the individual’s mental behavior of allocating and focusing awareness on a specific issue with concentration and directionality (Posner & Rothbart, 2007). Simon (1947) introduced the concept of attention to the field of management, combining attention with decision theory and proposing the bounded rationality model. He argued that decision makers’ attention is a scarce resource that is restricted by a variety of costs. It is not possible to evenly allocate their attention to all aspects of decision-making at the same time and selectively attend to one aspect while indirectly ignoring others. In China, there are two ways for government attention: one is direct attention, also known as state ownership; the other is indirect attention, that is, institutional ownership. The majority of institutional investors in China are either owned or controlled by the government, including banks, trust companies, insurance firms, and securities companies (Lim et al., 2012; Y. Zhu & Ni, 2014).

Corporate risk-taking is a reflection of their propensity to pursue large profits while willingly accepting the associated risks (Lumpkin & Dess, 1996), as demonstrated by their deliberate selection of high-risk, high-return investment opportunities (Boyd & Solarino, 2016; Vo, 2018). Corporate risk-taking plays a critical component that influences the company’s development and sustainability in the current business environment (Chin et al., 2024; Zhai et al., 2017). Events like the COVID-19 pandemic in 2019 and the financial crisis of 2008 highlight businesses’ complex challenges when dealing with significant uncertainties.

Although there has been some research investigating the factors that impact corporate risk-taking, there are still challenges with both theory and practice. The theory of bounded rationality, from the perspective that rationality is limited, has the potential to fill the research gap. Additionally, politically connected CEOs as a communication bridge between firm-government linkage can provide significant advantages in terms of information access privileges, uncertainty reduction, and signaling effects. This study explores how government attention impacts corporate risk-taking while examining the moderating effect of politically connected CEOs on these relationships. The research discovered that government attention exerts a negative influence on corporate risk-taking. Additionally, indirect government attention has a stronger negative influence on corporate risk-taking than direct government attention. However, politically connected CEOs mitigate the negative impact of government attention on corporate risk-taking, especially for indirect government attention. Further, the moderating effect of politically connected CEOs tends to have a more prominent impact in firms with strong internal governance mechanisms and in regions with weak external institutional environments. The empirical results suggest that politically connected CEOs can compensate for the bounded rationality of government attention.

This study allows four significant contributions. First, there remains a notable gap in studies that specifically explore the moderating effect of politically connected CEOs on corporate risk-taking. Considering political connections and networking in Chinese terms, they are highly valued in business dealings and are considered essential to Chinese culture and society. Hence, this research attempts to fill this gap, which has not been explored in prior studies and it enriches the study on the moderating effect of politically connected CEOs on risk-taking by Chinese corporations. Second, explaining the relationship between government attention and corporate risk-taking from a psychological perspective breaks the assumption of “perfect rationality” using traditional theories. This research provides a more realistic model of decision-making by explaining it using the theory of bounded rationality. Third, this study expands on understanding how politically connected CEOs impact risk-taking in various settings. It provides strong evidence of the heterogeneous effect that political connections CEOs have as moderators within both internal and external governance environments. Finally, it also helps to illuminate how government attention and politically connected CEOs affect corporate risk-taking, providing helpful insights for corporate strategies.

The following sections relate to the literature review and hypotheses, the research method, the findings of the study, and the conclusion.

Literature Review and Hypotheses Development

Government Attention and Corporate Risk-Taking

According to the previous studies, government-owned firms face an agency problem stemming from the differing risk perceptions held by managers and shareholders, as noted by Jensen and Meckling (1976). While the government aims to achieve social and political goals through firms, managers prioritize their interests, such as occupational safety and personal reputation. In this context, these firms are more inclined to undertake high-risk projects when backed by governmental support (Farag & Mallin, 2018; W. Zhu & Yang, 2016). More specifically, managers are more likely to pursue risky projects that offer greater returns and economic advantages.

As medium for resource allocation (Chen et al., 2014), government-owned firms are more likely to receive preferential treatment in accessing valuable resources from the government through shareholding (Brandt & Li, 2003; Cui & Jiang, 2012). Government-owned firms are protected by the government from consequences in case their high-risk projects fail, as the government provides additional funding or directly subsidizes these firms when they face financial distress (Ho et al., 2021). If the project succeeds, it can enhance managers’ entrepreneurial reputations and help them establish their business empires, benefiting their political careers and positions within firms. Therefore, some studies (e.g., Zhai et al., 2017) observe that government-owned firms and corporate risk-taking are positively correlated.

However, according to bounded rationality theory, government selectively attend to one aspect while indirectly ignoring others (Simon, 1947). Government attention, as shareholders, needs to allocate it among numerous policy objectives and responsibilities. Government attention tends to be attracted to urgent public issues or strategic tasks, like maintaining employment stability, economic growth, achieving specific industrial policies, and promoting societal stability (Nguyen et al., 2020).

Government ownership in firms can lead to conservative risk-taking because the government may prioritize political objectives over profit maximization, leading to a more risk-averse stance in corporate decision-making (Uddin, 2016). When government attention focuses on particular policy objectives or social responsibilities, this may result in less attention being paid to firms’ development. Conversely, the government may require that firms collaborate with them to accomplish political objectives. To align with the strategic missions of the government, managers typically exhibit a more conservative approach toward decision-making and are less inclined to promote risk-taking behavior (Chong et al., 2018). Governments typically have a greater aversion to risk than private businesses, as they have a responsibility for the public and face more serious political consequences of failure (Biglaiser et al., 2023). Thus, our hypothesis 1 is formulated as follows:

Moderating Role of Politically Connected CEOs

The concept of corporate political connection has its origins in Pfeffer and Salancik’s resource dependence theory (1978; Chkir et al., 2020), which highlights the need for organizations to depend on external resources to meet their requirements and goals (Hillman, 2005). Political connections are valuable because they provide companies an advantage with greater flexibility and autonomy over other companies (Wu et al., 2012), such as access to market trust, regulatory relief, and more favorable financing terms (Piotroski & Zhang, 2014).

Politically connected CEOs are inclined to pursue investment opportunities that entail lower risk due to concerns over potential damage to their reputation and status in case of failure. For example, Farag and Dickinson (2020) report that companies with politically connected CEOs take fewer risks than those without connections. Similarly, strong CEO political connections are shown to lessen the sensitivity of corporate risk-taking, as demonstrated by Chong et al. (2018). In contrast, the policy support obtained through political connections helps mitigate uncertainty stemming from the external environment, potentially increasing the willingness of management to take on more risky projects (Chai & Mirza, 2019).

Politically connected CEOs are easier to obtain bank loans (Belghitar et al., 2019) with lower external risks (Mitchell & Joseph, 2010). Furthermore, local governments have the authority to provide additional government subsidies when they are financially distressed (Duchin & Sosyura, 2012), allowing them to make riskier managerial decisions. Similarly, findings of some previous studies (e.g., Awijen et al., 2024; Chai & Mirza, 2019; García-Gómez et al., 2023; Otchere et al., 2020) also suggest that firms with politically connected CEOs take more risks.

In the current environment of frequent government interventions in businesses, these CEOs are more likely to take on projects specified by the government than CEOs without political connections (Bertrand et al., 2018). Politically connected CEOs have access to privileged information that can reduce the constraints of government attention on corporate risk behavior, thereby encouraging them to take higher risks. Hence, this study presents the following hypothesis and Figure 1 illustrates the research framework:

Research Framework.

Research Method

Sample and Data

The sample consists of 1,995 listed companies in the China Stock Market and Accounting Research Database (CSMAR) and China Market Index Database from 2011 to 2020. This study excluded companies operating within the financial sector, ST and *ST type companies and firms that had incomplete or irrelevant data. Consequently, the final sample comprises 19,950 firm-year observations for a total of 1,995 firms.

Variable Definition

In this study, consistent with Tee et al. (2021), leverage is used as a proxy for measuring corporate risk-taking. Consistent with Ahmed and McMillan (2023), leverage is determined by calculating the total debt divided by the total assets. This study includes government attention as well. The government allocates its attention to firms through shareholding. Therefore, state ownership and institutional ownership are used as a proxy for measuring direct and indirect government attention. State ownership is calculated as the proportion of state shareholders’ shareholding to the total shares, consistent with Yao et al.’s (2018) studies. Additionally, institutional ownership is based on the proportion of shares held by institutional investors relative to the total shares (C. Wang et al., 2023).

Following Z. Wang et al.’s (2017) suggestion, the moderator variable, politically connected CEOs, is evaluated by whether a CEO is at present or has served in the government or military, a member of the Chinese People’s Political Consultative Conference (CPPCC) or the Chinese People’s Congress (CPC). Politically connected CEOs is a dummy variable. Specifically, it takes on a value of 1 if a company has a politically connected CEO, while it assumes a value of 0 if there is no such connection.

In addition, the following are the control variables: Firm size is measured by the logarithm of total assets (García-Gómez et al., 2023); Firm growth, which is the growth rate of total assets (Feng et al., 2020); Tangibility, which is fixed assets to total assets (Tee et al., 2021); Profitability, which is EBIT divided by total assets (Boateng et al., 2017); Non-debt tax shields, which is depreciation and amortization to total assets (C. Wang et al., 2023); Board size, which is the total number of board members (Chong et al., 2018); Director independence, which is the number of independent directors to the total number of board directors (Feng et al., 2020); CEO duality is a dummy variable, assigned a value of 1 if the CEO also serves as the chairman and 0 otherwise (Tarus & Ayabei, 2016); Board meeting refers to the total number of board meetings held annually (Lorca et al., 2010).

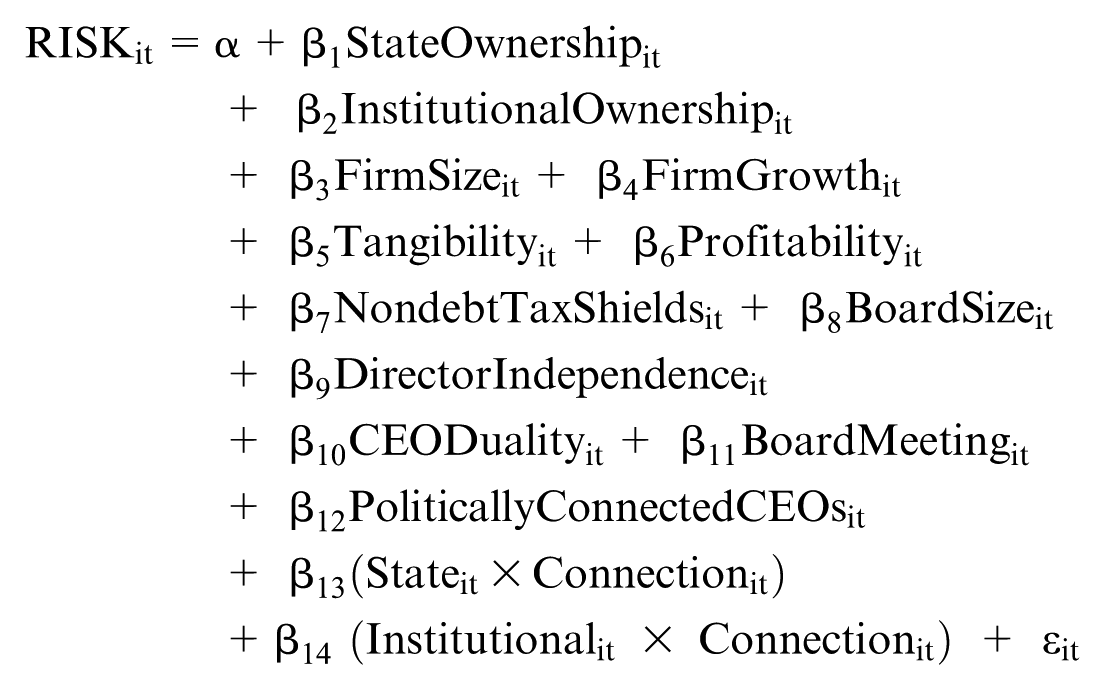

Model Design

A panel regression analysis model is employed to examine the influence of government attention on corporate risk-taking. Firm-level and board characteristics variables are controlled for in the analysis. Equation 1 represents the baseline regression model:

Among them,

Politically connected CEOs is the moderator variable, which is evaluated through Equation 2:

where

Empirical Results

Descriptive Statistics and Correlation Analysis

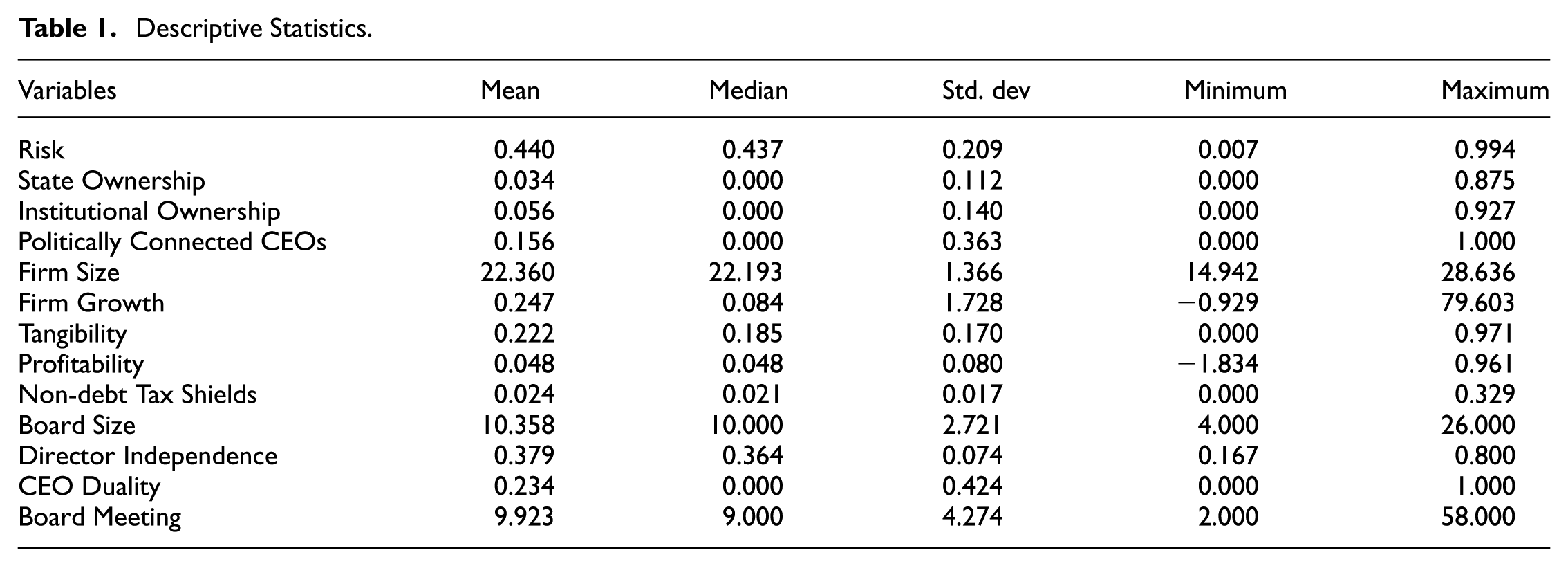

The variables’ descriptive statistics are presented in Table 1. The mean leverage value is 0.440, with a minimum of 0.007, a maximum of 0.994, and a standard deviation of 0.209, suggesting significant variations in the level of risk-taking among the different companies. The mean values of 0.034 and 0.056 for state and intuitional ownership, respectively, with standard deviations of 0.112 and 0.140, reveal that the allocation of government attention is more dispersed and that the government may play the role of mentor. However, the maximum values of 0.875 and 0.927 for state and institutional ownership indicate that government attention is more likely to be allocated to a specific type of firm.

Descriptive Statistics.

Table 2 reveals the results of correlation analysis. The correlation coefficients range from .720 to −.177, all below the maximum value of .8, which indicates that multicollinearity is not an issue for this research. Notably, the influence of state ownership on corporate risk-taking is positive at .094, which means that direct government attention tends to enhance corporate risk-taking. Conversely, institutional ownership is negatively linked with corporate risk-taking (−.103), revealing that indirect government attention generally reduces corporate risk-taking. Furthermore, there exists some relationship between risk-taking and some control variables.

Correlation Matrix

Significant at 10% level. **significant at 5% level. ***significant at 1% level.

Regression Analysis

Baseline Regression

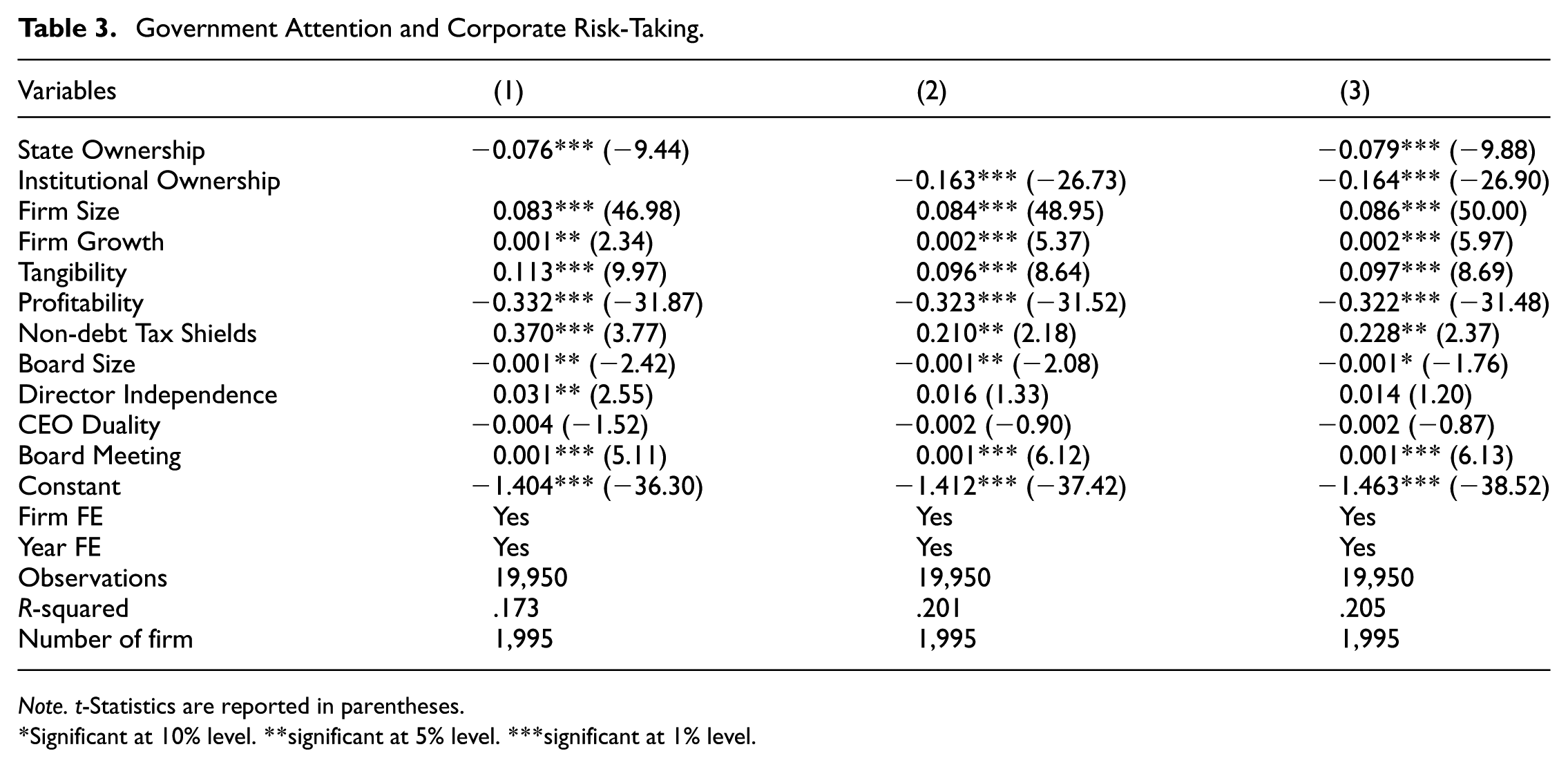

The study’s regression findings are shown in Table 3. There is a negative correlation between state ownership and corporate risk-taking, as seen in Column 1. At the same time, Column 2 of Table 3 also reveals that institutional ownership is negatively related to corporate risk-taking. The findings support H1, which claims that government attention negatively influences corporate risk-taking, regardless of direct or indirect government attention.

Government Attention and Corporate Risk-Taking.

Note. t-Statistics are reported in parentheses.

Significant at 10% level. **significant at 5% level. ***significant at 1% level.

From the perspective of bounded rationality, the government, as the decision-making authority, possesses limited cognitive capacity, information processing capabilities, and resource allocation capabilities. Faced with complex and multifaceted social issues, government attention is unable to make perfectly rational decisions and frequently lacks the capacity to evaluate all relevant information or perform infinite analyses. They are only able to choose the most appropriate option for achieving the decision goals among the decisions, in accordance with the principle of satisfaction. Therefore, government attention, as a scarce authoritative resource, is allocated through an inherently political process. Governments focus their attention on urgent public issues and strategic tasks, like maintaining employment stability, economic growth, and promoting societal stability (Nguyen et al., 2020). In contrast, the development of firms always remains on the periphery of government attention.

Under the constraints of bounded rationality, government attention usually functions as a “grabbing hand” (Opoku-Mensah et al., 2020; Shleifer & Vishny, 1998). This compels firms to shoulder political responsibilities, thereby constraining the resources and decision-making space needed for high-risk activities. Consequently, the core objective of corporate governance shifts from “maximizing shareholder value” to “fulfilling political mandates” (Bai & Lian, 2013). To safeguard their careers and align with government preferences, managers tend to abandon long-term, beneficial yet uncertain projects in favor of safer alternatives. This strategic shift toward safer investments ultimately diminishes the corporate risk-taking.

Further, Column 3 summarizes the regression study’s results, which reveal how the two types of government attention together impact corporate risk-taking. The findings are compatible with the findings reported in Columns 1 and 2. From another aspect, indirect government attention (β = −.164) has a stronger negative influence on corporate risk-taking than direct government attention (β = −.079). Compared to government attention through state ownership, institutional ownership is usually indirect shareholding, with the government participating in corporate decision-making through the institution as an agent. This leads to information asymmetry and the inability of managers to accurately identify the policy objectives of government. In this situation of greater uncertainty, decision-making tends to be more conservative.

Moreover, the control variables, firm size, firm growth, tangibility, non-debt tax shields and board meeting are positively linked with corporate risk-taking. By contrast, profitability and board size are negatively associated with corporate risk-taking.

The Moderating Role of Politically Connected CEOs

In terms of moderating effect of politically connected CEOs, Column 1 of Table 4 reveals a positive interaction impact between state ownership and politically connected CEOs (State × Connection). Meanwhile, Column 2 shows a positive interaction between institutional ownership and politically connected CEOs (Institutional × Connection). The results support H2, indicating that the negative effect of direct and indirect government attention on corporate risk-taking will be mitigated when companies hire politically connected CEOs.

Moderating Effect of Politically Connected CEOs.

Note. The two interaction terms are as follow: State × Connection = state ownership × politically connected CEOs. Institutional × Connection = institutional ownership × politically connected CEOs. t-Statistics are reported in parentheses.

Significant at 10% level. **significant at 5% level. ***significant at 1% level.

Consistent with resource dependence theory, politically connected CEOs constitute a critical resource for firms, serving to diminish external dependencies and alleviate uncertainty. Their close governmental affiliations grant them unique informational advantages, enabling them to effectively anticipate policy shifts (Piotroski & Zhang, 2014). This privileged position allows them to engage directly with authorities when faced with potential pressures, thereby securing enhanced managerial discretion and strategic flexibility for the firm (Wu et al., 2012).

Moreover, the appointment of politically connected CEOs serves as a potent signal of political alignment to the government, indicating the firm’s commitment to political objectives and thereby mitigating the intensity of the “grabbing hand.” In summary, politically connected CEOs alter the firm’s decision-making context. This encourages firms to undertake necessary risks within a more flexible environment, thereby weakening the negative influence of government attention on corporate risk-taking.

Further, the results of all the variables on corporate risk-taking in this study are revealed in Column 3, consistent with those shown in Columns 1 and 2.

Robustness Checks

Omitted Variables

There might be certain neglected variables for corporate risk-taking, even though this study is in control of many of its influencing factors. Omitting relevant variables can lead to estimation base issues, weakening the validity of empirical findings (Peng et al., 2022). Therefore, this research adds two supplementary variables into the foundational model to assess whether the findings undergo alterations.

Following Tian et al. (2022), this study adds firm age and cash ratio into the basic model. Firm age is defined as counting the years since its initial public offering (IPO) or listing, while the cash ratio is calculated by dividing cash by total assets. The two new variables are added one by one to the basic model. Table 5 shows that the results are consistent with those in Tables 3 and 4. As a result, this study demonstrates that the results of the basic model are robust to the addition of omitted variables.

Additional Control Variables.

Note. The two interaction terms are as follow: State × Connection = state ownership × politically connected CEOs. Institutional × Connection = institutional ownership × politically connected CEOs. t-Statistics are reported in parentheses.

Significant at 10% level. **significant at 5% level. ***significant at 1% level.

Lag Test

This study examines the lagged effects of government attention on corporate risk-taking. In particular, government attention in previous years may have a greater impact on a company’s current risk-taking. As a result, government attention is lagged by two periods in the basic model. The results are shown in Table 6, which observes that government attention remains negative with significance in all models.

Lag Test.

Note. t-Statistics are reported in parentheses.

Significant at 10% level. **significant at 5% level. ***significant at 1% level.

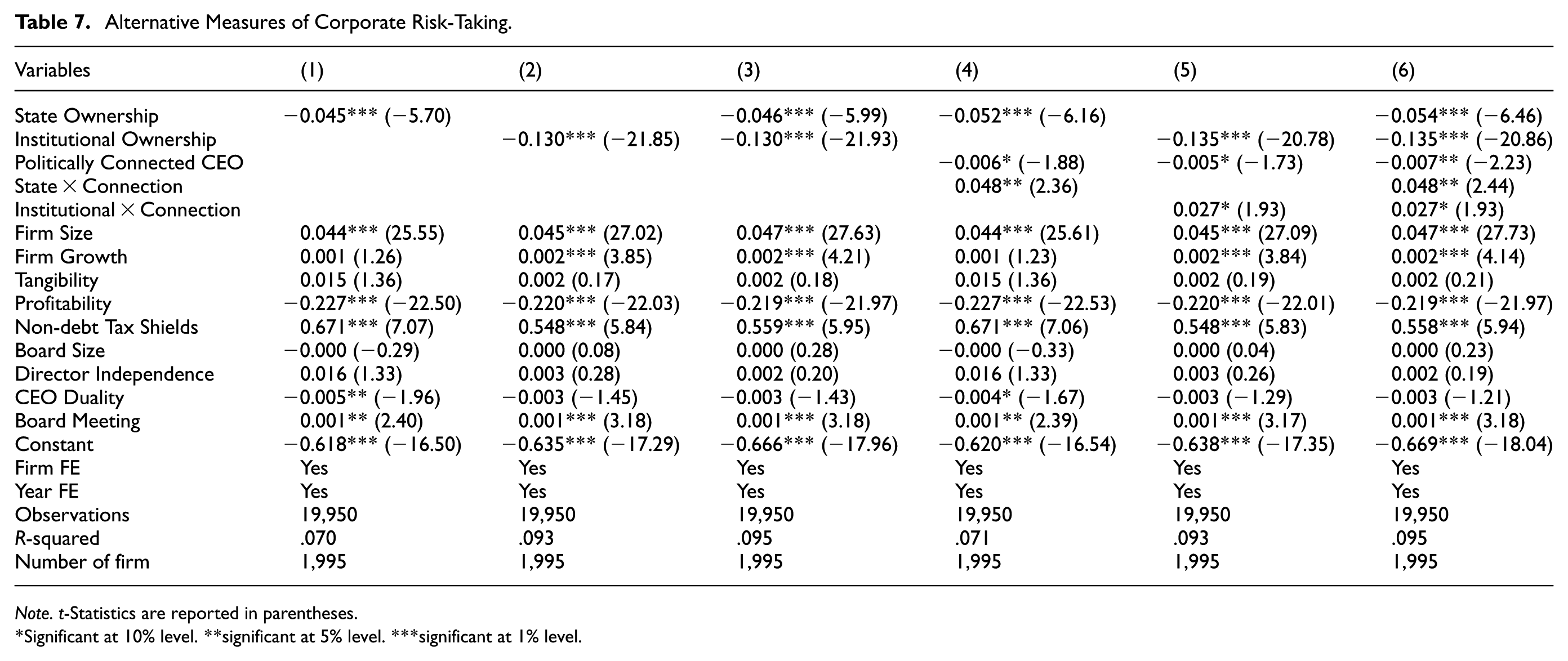

Alternative Measures of Corporate Risk-taking

An alternative variable is utilized to evaluate the stability of the regression findings, which is in line with the Feng et al. (2020) study. That is, total debt divided by total assets is substituted by short-term debt divided by total assets. Except for a few control variables, the regression findings, shown in Table 7 closely resemble those found in Table 3 and 4, which verifies that the regression analysis results for this study are reliable.

Alternative Measures of Corporate Risk-Taking.

Note. t-Statistics are reported in parentheses.

Significant at 10% level. **significant at 5% level. ***significant at 1% level.

Endogeneity Issues

Brown et al. (2011) highlighted that endogeneity can pose a significant challenge in the relationship between corporate governance and various accounting and financial variables. In light of the possibility that the findings would be impacted by the endogeneity issue caused by omitted variables or bi-directional causation, this study uses the system GMM estimation technique (Roodman, 2009). Table 8 presents the findings from the two-step system GMM analysis, which align with the results obtained from the FE result shown in Table 3 and 4.

Endogeneity Problems.

Note. The two interaction terms are as follow: State × Connection = state ownership × politically connected CEOs. Institutional × Connection = institutional ownership × politically connected CEOs. t-Statistics are reported in parentheses.

Significant at 10% level. **significant at 5% level. ***significant at 1% level.

Regarding the test results, the models show p-value below .10 for the AR(1) test and above .10 for the AR(2) test. This indicates rejection of the null hypothesis for AR(1) but non-rejection for AR(2), suggesting no evidence of second-order serial correlation in the residuals. Furthermore, all the p-values of the Hansen test are higher than .10. Therefore, the null hypothesis is not rejected, indicating that the model does not suffer from an over-identification issue and the instruments are valid. Moreover, all the p-values for the difference-in-Hansen test are greater than .10. Therefore, the null hypothesis is not rejected, implying that the subset of instruments used in the system GMM estimator is exogenous.

Mechanism Analysis

This study further identifies how government attention negatively impacts corporate risk-taking through two potential mechanisms. This study examines whether government attention restrains corporate risk-taking through agency costs and financial constraints. Following Deng et al. (2023), agency costs are measured by the ratio of overheads to total assets. Furthermore, this study introduces the FC index to proxy the corporate financial constraints (Farooq et al., 2022).

Table 9 reports the results. Government attention, regardless of direct or indirect government, is positively related to agency costs. Meanwhile, these agency costs are shown to suppress corporate risk-taking. This suggests that government attention exacerbates agency costs between management and shareholders, thereby reducing firms’ propensity to undertake risks.

Mechanism Analysis of Agency Costs.

Note. t-Statistics are reported in parentheses.

significant at 1% level.

Table 10 presents the mechanism concerning financial constraints. A positive relationship between government attention and financial constraints, which in turn are negatively linked with corporate risk-taking. This means that government attention diminishes corporate risk-taking through the mediating channel of financial constraints.

Mechanism Analysis of Financial Constraints.

Note. t-Statistics are reported in parentheses.

Significant at 10% level. ***significant at 1% level.

Heterogeneity Analysis

In addition, different factors may influence whether political connections have a dominant impact on firms, which includes the firm’s internal governance environment and the regional macroeconomic environment (Chkir et al., 2020). To more precisely assess the moderating effect of politically connected CEOs, the research analyses the impact of internal corporate governance mechanism and external institutional environment of firms.

The Effect of Internal Corporate Governance Mechanism

Using independent directors as a proxy for internal corporate governance mechanisms, the median proportion of independent directors on the board as the standard is used to divide the samples into high and low independent directors. Column 1 in Table 11 illustrates that the interaction effect of state ownership and politically connected CEOs is positive in firms with highly independent directors. Column 4, however, indicates that firms with low numbers of independent directors have no significant interaction effect between State and Connection. The findings indicate that politically connected CEOs are able to take on more risk in companies that have lower agency costs. Lower agency costs typically mean that the goals of management and shareholders are more closely aligned. CEOs with political connections can leverage their relationships to secure additional resources for the company without being hindered by challenges related to agency issues. This enables them to pursue riskier investments with greater confidence. Thus, the impact of politically connected CEOs is more pronounced in companies with strong internal corporate governance structures.

Grouping Regression Analysis of Independent Directors.

Note. The two interaction terms are as follow: State × Connection = state ownership × politically connected CEOs. Institutional × Connection = institutional ownership × politically connected CEOs. t-Statistics are reported in parentheses.

Significant at 10% level. ***significant at 1% level.

As shown in Columns 2 and 5, the positive moderating effect between Institutional and Connection is the same. The findings suggest that institutional ownership can substitute for board independence in reducing agency costs. Politically connected CEOs are able to obtain more policy support and resource security due to their strong ties with the government or other political forces, which enhances the firm’s ability to cope with risks. Even when board independence is weak, institutional ownership and politically connected executives can still reduce agency problems by strengthening internal corporate governance and the integration of external resources. Consequently, politically connected CEOs may take on greater risks in firms with indirect government attention regardless of board independence.

The Effect of External Institutional Environment

The unequal development of the country is one characteristic of China’s reform that is little understood (Wu et al., 2012). Less developed regions typically exhibit weak institutional environments, leading firms to rely more on “relationships.” Therefore, companies in less developed regions are compelled to rely more heavily on political connections to offset the limitations and challenges posed by institutional environments (He et al., 2014). This study uses the financial market maturity as a proxy for the external institutional environment. Financial market maturity is evaluated by the Financial Market Development Index, a proxy for financial market maturity at the provincial level in China. A higher index suggests that the financial market is more mature and has a more developed institutional environment in that region. The sample is divided into less and more mature financial markets by using the median of financial market maturity as the standard.

In Table 12, Columns 1, 2, and 3 show that for the sub-sample, the variable interactions (State × Connection and Institutional × Connection) are positive in provinces with low financial market maturity and insignificant in companies situated in areas with high financial market maturity. This suggests that political connections have a more prominent impact in areas with less mature financial markets (Borisova et al., 2015). Regions with weaker external institutional environments often have inadequate regulatory systems, lack enforcement, and experience increased unpredictability in policy development and execution. In such circumstances, CEOs with political connections may try to influence regulatory decisions and policies in their favor, ensuring that the policies benefit high-risk firm investments. Consequently, politically connected CEOs are likely to have a more significant impact in regions with weaker institutional environments compared to those with stronger institutional environments.

Grouping Regression Analysis of Financial Market Maturity.

Note. The two interaction terms are as follow: State × Connection = state ownership × politically connected CEOs. Institutional × Connection = institutional ownership × politically connected CEOs. t-Statistics are reported in parentheses.

significant at 5% level. ***significant at 1% level.

Conclusion

Main Conclusions

This study explores how government attention impacts corporate risk-taking while examining the moderating effect of politically connected CEOs on these relationships. Moreover, mechanism analysis reveals that government attention diminishes corporate risk-taking through two potential mechanisms. It further investigates the heterogeneous effect of the moderating role of political connections CEOs by classifying companies based on internal corporate governance mechanisms and external institutional environments. The key findings are as follows.

Firstly, based on the theory of bounded rationality, government attention negatively influences corporate risk-taking, whether direct or indirect government attention. This is because government attention is bounded rationality, which tends to be attracted to urgent public issues or strategic tasks, reducing focus on firms’ development. Government attention often functions as a “grabbing hand,” compelling firms to assume political responsibilities. This shifts corporate governance’s core objective from shareholder value maximization to fulfilling political mandates, limiting their risk-taking and preventing them from investing in risky programs. Moreover, indirect government attention has a stronger negative influence on corporate risk-taking than direct government attention. Indirect government attention is realized through the institution as an agent. This leads to information asymmetry and the inability of managers to accurately identify the policy objectives of government. In this situation of greater uncertainty, decision-making tends to be more conservative.

Secondly, politically connected CEOs mitigate the negative impact of direct and indirect government attention on corporate risk-taking, which is consistent with resource dependence theory. Politically connected CEOs can provide significant advantages in terms of information access privileges, uncertainty reduction, and signaling effects, which alter the firm’s decision-making context. This encourages firms to undertake necessary risks within a more flexible environment, thereby weakening the negative influence of government attention on corporate risk-taking.

Lastly, mechanism analysis identifies government attention negatively impacts corporate risk-taking through agency costs and financial constraints. Heterogeneity analysis reveals that the presence of an independent board increases the risk-taking tendencies of CEOs who have political connections within firms with direct government attention. However, this impact is not observed in indirect government attention due to the substitute effect of corporate governance. Additionally, political connections tend to have a more prominent impact in regions with weak institutional environments, regardless of direct or indirect government attention.

Practical Implications

The implications of this study are essential for both the Chinese government and companies. Firms should be aware of the bounded rationality of government attention and appropriately evaluate the role that government attention plays in companies. Moreover, companies with government attention can better understand how politically connected CEOs can help them balance the demands for risk-taking and the social duties of government. This research empowers companies to develop effective risk strategies for utilizing these connections to attain a suitable level of risk for the company.

Specifically, it is recommended that firms establish specialized government relations departments responsible for continuously interpreting policy dynamics and forecasting regulatory trends. This function should be integrated into the company’s strategic decision-making apparatus, thereby enabling the firm to maintain operational flexibility while concurrently discharging its political responsibilities. Furthermore, firms should establish institutionalized channels of communication with government authorities, engaging in regular dialogue to build trust and mitigate future uncertainties. Finally, for management incentives, firms should integrate both political mandate fulfillment and corporate development into executive performance evaluations. This balanced approach helps counteract excessive managerial risk aversion and ensures that long-term business growth is not neglected.

The study emphasizes institutional environments, which also improves the global relevance by highlighting the differential applicability between developed and developing economies. In developing economies, characterized by institutional weaknesses and high uncertainty, politically connected CEOs act as an informal institutional substitute. They leverage informational advantages and signaling effects to secure scarce resources. Therefore, regular communication is especially necessary in developing economies with weak institutional environments. Conversely, in developed economies with mature markets and legal systems, political connections are a less critical asset for success, as firms primarily depend on formal channels.

Research Limitations

This study has made numerous contributions. However, it is not without limitations. First, it examines only government attention through shareholding. Future studies can consider more direct measures of government attention using the policy text analysis method, such as the frequency of policy directives, government official site visits, or the inclusion of a firm in key government industrial plans. Secondly, this study does not take into account the proxy for corporate risk-taking comprehensively. Hence, it may be beneficial for future studies to employ additional measures of corporate risk-taking from a dynamic perspective, like the volatility of corporate earnings or investment volatility. Additionally, this study only examines the moderating role of politically connected CEOs. Future research could further explore CEO characteristics like CEO power and inventiveness to gain a more comprehensive perspective on this relationship.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: PhD Start-up Foundation of Baoshan University BSSK2408.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available on request from the corresponding author.