Abstract

Promoting budget performance management reform in-depth is a crucial tool for the long-term enhancement of fiscal governance efficacy, as well as a way to break the structural solidification of fiscal resources and waste of money. Using a Multi-Period Difference-in-Differences model based on panel data from 31 Chinese provinces, autonomous regions, and municipalities between 2001 and 2021, the study empirically examines the effect of this reform on local fiscal resilience. According to the study, budget performance management reform increases local fiscal resilience, and its mechanisms of influence are related to the structure, risk, and efficiency of fiscal expenditures. The impact of this reform varies depending on fiscal decentralization, tax competition, and regional dispersion. The study’s conclusions provide more insight into how this reform impacts local fiscal resilience and offer policy recommendations for averting and reducing local fiscal risks.

Keywords

Introduction

The 20th CPC Central Committee’s Third Plenary Session adopted “the Decision of the CPC Central Committee on Further Comprehensively Deepening Reforms and Promoting Chinese-style Modernization” (Communist Party of China [CPC], 2024), which makes it abundantly evident that strengthening the coordination of fiscal resources and budgets and improving the budgetary system are essential for supporting and preserving key national strategies and fundamental means of subsistence. As a novel form of budgetary system, budget performance management has been crucial in enhancing both the effectiveness of fiscal resource allocation and budgetary management throughout time. Through its own quality and efficiency improvement, it advocates for improving the tax and fiscal systems to release stronger system execution and governance efficiency. This offers crucial assistance for preventing and addressing fiscal issues as well as for further controlling and effectively using the government’s “money bag.” The CPC Central Committee’s policy deployment to further reform the tax and fiscal system has led to the gradual emergence of China’s budget management’s legalization, standardization, and transparency. Apart from that, a budget performance management path with Chinese characteristics has been formed by the completion of the “all-around, whole process and full coverage” system from the national to local governments. To provide detailed guidance for the budget performance management reform, China has released several rules and regulations, operating procedures, and other instructions in the area of policy practice. Scholars in the field of theoretical study have studied in detail the meaning, process, and mechanism of budget performance management as well as how it affects fiscal pressure, fiscal expenditure, and fiscal sustainability. The goal is to investigate how budget performance management, a novel approach to budget management, might help address the current tight fiscal balance.

Fiscal resilience has steadily emerged as a crucial metric for assessing a nation’s or region’s capacity for sustainable development and economic health because of the close integration of economic globalization and integration (Salignac et al., 2022). The disparity between fiscal revenue and spending in different regions has gotten worse, particularly after the 2020 novel coronavirus epidemic outbreak, and fiscal resilience has drawn a lot of attention. Currently, in the field of fiscal resilience research, existing literature has formed a three-dimensional research framework of “Concept-Influencing Factors-Measurement,” but there are still significant gaps in research.

First, from the perspective of conceptual evolution, since Christopherson et al. (2010) expanded regional economic resilience to a “economic-social-policy” composite dimension, Bristow and Healy (2014) revealed the decisive role of subject behavior and policy choices in resilience, Hochrainer-Stigler et al. (2015) and Mechler et al. (2016) limit fiscal resilience to financing sustainability and system recovery capacity in disaster response scenarios. However, this theoretical transfer has obvious limitations. Noy (2019) emphasizes the importance of rapid recovery of fiscal revenue and expenditure after a disaster, but this does not fully cover the need to build resilience in normal fiscal governance. The regional resilience differences identified by Susan et al. (2010) and the revenue-expenditure balancing mechanism proposed by Afonso and Jalles (2014) have not been effectively linked to the policy tools of fiscal and tax system reform. Secondly, at the methodological level, the shortcomings of existing research are exposed in multiple dimensions. Research on fiscal resilience remains confined to crisis response measures such as risk management strategies and financing mechanisms, lacking theoretical connections to budgetary reform (Hochrainer-Stigler et al., 2024). The measurement methods used by Gong (2023) do not incorporate policy intervention variables, making it difficult to identify the impact of institutional factors. There is insufficient research on the normalized resilience mechanism of fiscal balance in the context of economic globalization (Chen & Sun, 2024). Most importantly, there has been no empirical testing of the causal relationship between budget performance management—a core reform tool—and fiscal resilience in terms of policy linkage. This research gap makes it impossible to assess the substantive impact of fiscal and tax system reforms on fiscal sustainability and hinders the establishment of a routine resilience enhancement mechanism from a policy tool perspective, such as the issue of missing implementation pathways for the growth capacity dimension proposed by Kamble et al. (2025) in policy scenarios. Finally, from the perspective of the causal chain, existing research limits fiscal resilience to disaster response scenarios and fails to explain the differentiated resilience characteristics exhibited by local finances in the context of China’s “comprehensive, full-process, full-coverage” budget performance management system in the face of shocks such as the COVID-19 pandemic (Zhou & Ren, 2020). This disconnect between theory and practice makes it difficult for the academic community to analyze the formation mechanism of fiscal resilience from the perspective of budget management system innovation, thereby limiting the comprehensive assessment of the effectiveness of fiscal and tax system reforms and the theoretical support for local fiscal governance. Therefore, conducting an in-depth analysis of the intrinsic link between budget performance management reform and local fiscal resilience is of great significance for promoting theoretical development and practical progress in the field of finance.

Given this, this article addresses the shortcomings of existing research, which emphasizes crisis response over institutional coordination. On the one hand, by reconstructing the concept of fiscal resilience, it constructs a dynamic resilience index comprising four dimensions—response, recovery, growth, and governance—in the measurement system, which is suitable for routine governance scenarios. By introducing policy relevance, Doran and Fingleton (2016) upgraded their micro-resilience framework to a linked system of “Policy Tools-Institutional Environment-Economic Entities.” Based on Pratt and Hyder’s theory of system adaptability (Pratt & Hyder, 2016), they proposed a theoretical hypothesis that budget performance management can enhance fiscal resilience through a three-dimensional mechanism of “Resource Allocation-Risk Prevention-Control-Structural Optimization,” breaking through the limitations of traditional crisis response research. On the other hand, this paper uses panel data from 31 provinces, autonomous regions, and municipalities in China from 2001 to 2021 and applies a multi-point difference-in-differences model. It incorporates budget system variables based on the spatial resilience research proposed by Fingleton and Palombi (2013). This echoes the proposition of “fiscal policy flexibility” put forward by Chen and Sun (2024), which focuses on the impact of budget performance management reform on local fiscal resilience, its mechanism of action, and its heterogeneous characteristics, achieving multidimensional innovation in methodology. Finally, the study found that budget performance management reforms have a significant positive effect on local fiscal resilience, and this conclusion remains reliable after undergoing various robustness tests. Mechanism testing shows that this reform mainly enhances the resilience of local finances through improving the efficiency of local fiscal expenditure, reducing fiscal risks, and optimizing the structure of fiscal expenditure. Heterogeneity analysis shows that the effectiveness of reforms in enhancing local fiscal resilience varies significantly in terms of spatial distribution, degree of tax competition, and level of fiscal decentralization.

Overall, this article systematically argues for the role of budget performance management reform in local fiscal resilience and its heterogeneous characteristics by deeply deconstructing the theoretical gaps and methodological shortcomings of existing research. It fills a research gap while achieving dual innovation in academic theory and policy practice. This not only expands the scope of research on fiscal resilience but also provides empirical evidence with both theoretical depth and practical value for deepening fiscal and tax system reform.

Theoretical Analysis and Research Hypothesis

Government finance is dealing with issues like sluggish tax growth, rising social security spending, rising government debt risk, and mounting demand to lower taxes and fees in the new economic normal. Further reform of the tax and fiscal systems is urgently needed. Enhancing the efficiency of fiscal finances and ensuring the sensible distribution of resources are key components of budget performance management reform. Systematic coupling necessitates that this reform considers how different components of the fiscal system interact, addresses the issue of wasteful finances through incentive limitations and performance management, encourages effective resource allocation, and improves fiscal sustainability. The complete implementation of budget performance management guarantees the fiscal system’s resilience and ongoing improvement in a changing environment, and its dynamic management and supervision mechanism offers a solid foundation for enhancing the system’s adaptability and resilience. This is crucial for enhancing the effectiveness of fiscal governance and supporting the economy’s stability and long-term growth.

Budget Performance Management Reform and Local Fiscal Resilience

The main goal of budget performance management, a result-oriented approach to budget management, is to increase the effectiveness and efficiency of public resource allocation through careful budget preparation, rigorous budget implementation, and efficient oversight mechanisms. The results-oriented budget performance management system influences the internal operations of departments and agencies to increase the organizational effectiveness of government agencies (Sterck & Scheers, 2006) and contributes to the improvement of government service efficiency (Kong, 2005). This guarantees that the anticipated economic, social, and environmental advantages of investment may be realized (Frost & Rooney, 2021). By encouraging cross-sectorial coordination and collaboration to accomplish sustainable development goals, this reform helps the government integrate resources more successfully (Hu, 2023). It pushes the government to give long-term interests more consideration when allocating fiscal resources and integrates sustainable development goals into the framework of performance indicators (Kantabutra, 2024). Fiscal resilience is further improved, and the compliant use of fiscal funds is ensured by strengthening fiscal monitoring and accountability measures (Jiang & Chi, 2024). On the one hand, fiscal resilience calls on the fiscal system to manage risks quickly, recover and rebuild effectively following external shocks such as natural disasters, public health emergencies, and fiscal crises, and allocate funds sensibly in the face of these occurrences. Reforming budget performance management also increases the fiscal system’s capacity for self-regulation and adaptation, fosters fiscal resilience, and improves the effectiveness of the use of fiscal funds and the accuracy of fiscal expenditures. On the other hand, the reform helps improve the transparency of budget performance information and management quality, as well as the trust of all societal sectors in fiscal performance, by increasing the transparency of performance objectives and assessment results and actively accepting public supervision. Enhancing the fiscal system’s capacity for external oversight and self-correction, as well as its internal management level and capacity for risk prevention and control, is beneficial. The article suggests Hypothesis 1, considering this.

Budget Performance Management Reform, Fiscal Expenditure Efficiency and Local Fiscal Resilience

By incorporating performance data into the budgeting process, budget performance management helps government agencies operate more efficiently and save money (Curristine, 2005). Performance budgeting clarifies the relationship between the type and distribution of government spending by including efficiency data from government actions in the budget process (Ferreira & Otley, 2009). The budget performance management reform promotes the effective distribution and use of budget funds by altering budget regulations or procedures (Shaw, 2016). Establishing precise performance targets and metrics, allocating fiscal money scientifically and reasonably, and modifying budget rules or procedures to promote effective allocation and usage of budget funds, reduces budget slack behavior (Feng et al., 2023). Additionally, increased fiscal expenditure efficiency improves fiscal sustainability by enabling the government to offer more public services without adding to the fiscal burden (Afonso & Alves, 2023). On the one hand, fiscal resilience refers to the fiscal system’s ability to adjust and withstand shocks from the outside world, societal shifts, and economic fluctuations. These skills can be strengthened by increasing the efficiency of fiscal expenditures, which can effectively assist economic recovery and preserve fiscal stability, particularly when faced with external shocks. However, increasing the effectiveness of fiscal spending, ensuring that resources are used efficiently, encouraging economic expansion, and giving the fiscal system more leeway to handle possible fiscal and economic risks are all crucial for enhancing fiscal resilience. The article suggests Hypothesis 2, considering this.

Budget Performance Management Reform, Fiscal Risk, and Local Fiscal Resilience

Budget performance management can monitor fiscal risks in real-time, comprehensively, and dynamically by building and optimizing the fiscal risk early warning index system. This helps the government assess and respond to fiscal risks quickly and effectively, and it also improves the government’s capacity to manage a variety of risks and stop and manage the spread of fiscal risks. By improving the structure of government spending, budget performance management reform can lower fiscal risk, which will unavoidably impact the overall resilience and health of the fiscal system. Ho and Im (2015) established a reasonable norm of “spending money to buy results” by developing a framework for examining the institutional space of budget performance management reform. This norm helps to optimize the structure of government expenditure, reduce ineffective and inefficient expenditure, and lower fiscal risks. According to Kamble and Gunasekaran (2020), a strong framework for performance management can guarantee that government departments’ actions align with the government’s overarching objectives, encourage collaboration and coordination between departments, prevent resource waste and reinvestment, and lower fiscal risks. Nonetheless, one of the most important elements in improving fiscal resilience is the control of fiscal risks. The government can better respond to crises and changes in the economy by recognizing and controlling fiscal risks. The government can lessen budget uncertainty by managing fiscal risk (Mechler et al., 2016). As a result, improving budget performance management lowers fiscal risks and promotes a more robust and sustainable local fiscal system. The article suggests Hypothesis 3, considering this.

Budget Performance Management Reform, Fiscal Expenditure Structure and Local Fiscal Resilience

Reforming budget performance management is a crucial step in maximizing the fiscal spending structure. First, during the entire budget performance management process, make sure that money is allocated to the most critical areas, cut down on wasteful spending, and increase the amount of public funds allocated to important regions and livelihood programs. Second, by promoting the adoption of innovative budget management techniques by government agencies, such as zero-based budgeting, a departure from the conventional fiscal spending model, and a more effective use of fiscal money. Enhancing fiscal resilience is largely dependent on the fiscal spending structure, which includes the stability of fiscal revenue, the efficacy of fiscal expenditure, and the coordination of intergovernmental fiscal interactions. On the one hand, the counter-cyclical adjustment function of fiscal policy is realized through the optimization of the fiscal expenditure structure. It smooths economic swings by boosting economic growth during a recession by raising government spending and preventing economic overheating during a period of economic overheating by cutting spending (Aizenman et al., 2019). To promote sustainable economic development and improve the long-term resilience of finance, it is beneficial to optimize the structure of fiscal expenditure, which also entails making effective use of limited fiscal resources and reducing waste and inefficient expenditure (Zhao & He, 2024). However, by lowering fiscal investment in general competitive fields, more money is allocated to public sectors like environmental protection and social security, which can not only address social needs but also prevent wasteful use of fiscal resources, lower fiscal risks, and improve fiscal sustainability (Liu, 2020). The construction of flood control facilities and the development of renewable energy sources are two examples of climate change adaptation strategies that can be implemented by optimizing the fiscal spending structure to increase fiscal resilience and adaptability (Boitan, 2023). Therefore, the stability and resilience of the fiscal system in the face of social and economic shocks are enhanced by an appropriate, balanced, and flexible fiscal expenditure structure. The article suggests Hypothesis 4, considering this.

Research Design

Sample Selection and Data Sources

Budget performance management reform in China’s provinces and municipalities is concentrated in the period 2004 to 2018. To comprehensively track and assess the effect of budget performance management reform on local fiscal resilience, limited to data availability, the article selects unbalanced panel data of 31 provinces, autonomous regions and municipalities directly under the central government from 2001 to 2021. The data selection stems from two points. First, the time of implementation of budget performance management reform policies was collected through the web pages of the Chinese Ministry of Finance and local finance departments. Second, collect other data through China’s provincial statistical yearbooks, China’s fiscal and tax databases, China’s regional economic databases, provincial government work reports, and databases such as the China Economic Network.

In addition, the data processing operation of the article is as follows. (1) Removes samples that are seriously missing the values of the main variables. (2) The missing values of individual samples are completed by the linear interpolation method. (3) Logarithmic processing of non-ratio-related variables. (4) All variable values were tailed at 1% and 99% quantiles to exclude extreme values in the sample. After the screening, 558 valid observations were retained.

Variable Selection

Explained Variable

According to the fiscal emergency governance and evolution perspective, the article evaluates the degree of local fiscal resilience from four dimensions: fiscal responsiveness to external shocks, fiscal resilience, fiscal growth potential, and fiscal governance effectiveness. The efficiency assessment model (Banker-Charnes-Cooper [BCC]) in Data Envelopment Analysis (DEA) is then combined with the panel entropy weighting method to determine the fiscal resilience of each region. The article chose local fiscal resilience (Resit) as an explanatory variable; the greater the Resit, the better the region’s fiscal resilience.

About fiscal responsiveness. The fiscal strength of local governments is gauged by the ratio of fiscal revenue to fiscal spending. The ability of local governments to employ their fiscal resources to implement macroeconomic control and maintain fiscal stability is positively connected with fiscal self-sufficiency. The growth rate of fiscal expenditure indicates the short-term response capacity of local finance to external shocks, whereas the fiscal deficit rate indicates the degree to which the current obligations of the local government are converted into possible hazards. About the capacity for fiscal recovery. The quality of the local fiscal revenue structure is shown by the ratio of tax and non-tax revenue to GDP, and the growth rate of public budget revenue indicates the local fiscal revenue scale’s capability for expansion. About the ability of fiscal expansion. The ratio of the fiscal revenue growth rate to GDP growth rate, which indicates whether the national income distribution is rational and scientific, is used to calculate the elasticity of fiscal revenue. The ratio of the growth rate of fiscal expenditure to the GDP growth rate is a measure of the elasticity of fiscal expenditure, and the ratio of people’s livelihood expenditure to fiscal expenditure is a measure of the structure of fiscal expenditure, which reflects the objective of government governance and the impact of stabilizing the economy through expenditure. About the ability to regulate finances. The input of fiscal monies and the output of public services are reflected in the DEA’s calculation of fiscal expenditure efficiency. The GDP growth rate indicates how much economic activity has increased or decreased over a given period; the Gini coefficient is used to quantify how unequally people’s incomes are distributed. The gap between residents’ affluent and the poor is measured by comparing the difference between the actual income distribution and the fully equal distribution. The ability of fiscal funds to leverage social capital investment is measured by the ratio of total fixed assets to GDP, which reflects the distribution of fiscal resources.

Core Explanatory Variable

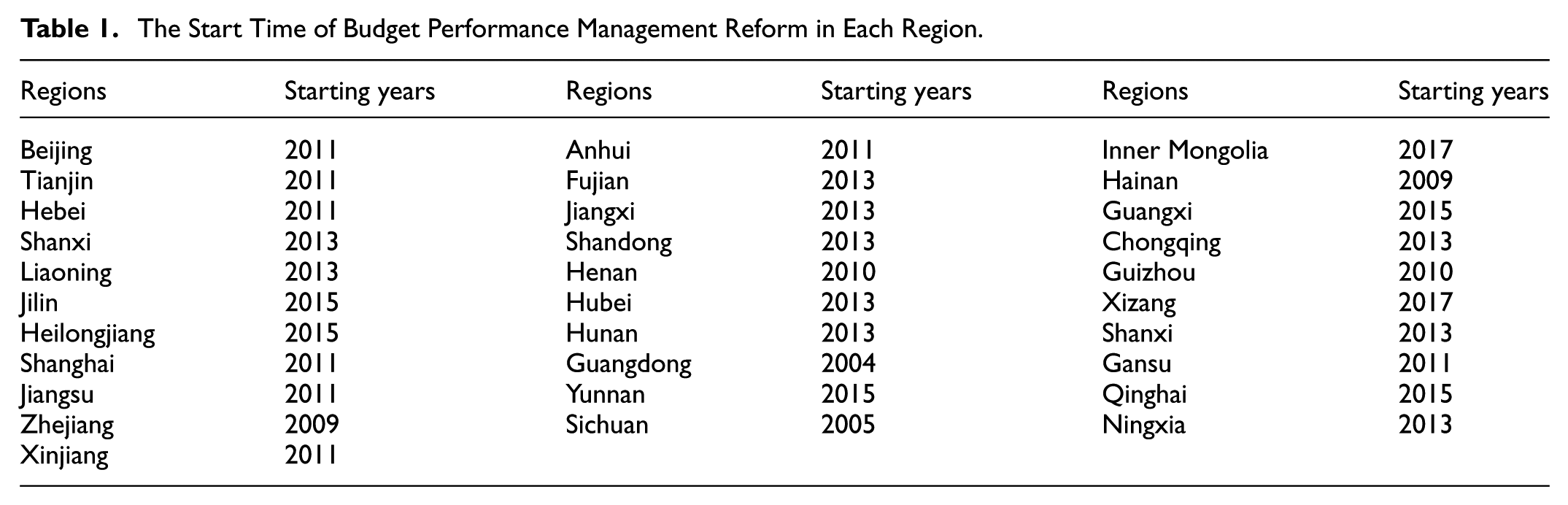

The dummy variable Reformit is used to indicate whether the area i has implemented the reform measures in the year t. If it is implemented, the value of the year after the year is 1, and vice versa is 0. The essential content of the policy remains the same, and matching institutional mechanisms have been established in conjunction with the local areas. In China, local governments have been introducing normative papers for budget performance management reform gradually, following the central policies. The specific implementation time is shown in Table 1.

The Start Time of Budget Performance Management Reform in Each Region.

Control Variables

To ensure the accuracy of the estimation results, the article refers to the literature of Chen et al. (2022), and Jiang and Chi (2024), and selects the level of economic development (Pgdp), urbanization level (Urban), education level (Edu), expenditure structure bias (Fiexp), unemployment rate (Unemp), human capital level (Cap), infrastructure construction (Infd), and aging level (Age) as control variables that affect local fiscal resilience. The definition of each variable is shown in Table 2.

Definition of Variables.

Model Design

China’s provinces and municipalities have been progressively investigating budget performance management reform since 2004. This is a quasi-natural experiment with several shocks because the policy pilot locations and times are different. Referring to the related research content and ideas of Callaway and Sant’Anna (2021) and Wing et al. (2018), the article adopts the Multi-Period Dual Difference Model (Multi-Period DID). Through this model, it gives full play to its advantages of stronger ability to deal with dynamic effects, reliability of causal inference, and flexibility of model setting, and effectively controls time trends and individual heterogeneity by setting up treatment and control groups at multiple points in time, accurately identifies the causal impact of budget performance management reforms on dynamic changes in the toughness of local budgets, and provides a scientific basis for the assessment of policy effects.

In Equation 1, the explained variable Resit denotes the local fiscal resilience of region i in year t; the core explanatory variable Reformit denotes whether region i implemented budget performance management reform in year t. If region i implemented the reform policy in year t, the year after that year is assigned a value of 1, which represents the observed individuals as the experimental group, and vice versa is assigned a value of 0, which represents the observed individuals as the control group; Controlsit represents a set of control variables that affect local fiscal resilience; Prov and Year represent individual and time fixed effects, respectively; εit represents a random disturbance term that affects local fiscal resilience; α is the intercept; and β1 greater than 0 indicates the presence of a positive effect, and vice versa for a negative one.

Empirical Results and Analysis

Descriptive Statistics and Correlation Analysis

Based on the results in Table 3, the mean value of local fiscal resilience (Resit) is .379, indicating that the overall fiscal resilience of local governments is low; the minimum value is .185, and the maximum value is .731, indicating that there is a large difference in the level of fiscal resilience of various localities.

Descriptive Statistics Results.

Secondly, to avoid the reliability of empirical results being affected by excessive correlation between variables, this study first analyzed the correlation between variables using Pearson’s correlation coefficient. The results are shown in Table 4. The explanatory variable Res is significantly positively correlated with Reform, and its correlation with variables such as Urban and Edu also reaches statistical significance, consistent with the theoretical framework of “factor synergy promoting growth” in development economics.

Correlation Analysis Results.

Note.***, **, * are significant at the 1%, 5%, and 10% confidence levels, respectively.

However, the high correlation between Pgdp and Cap suggests a potential risk of collinearity. Therefore, this study tested for multicollinearity using the variance inflation factor (VIF). The results are shown in Table 5. The overall average VIF value is 3.63, and the VIF value of the core explanatory variable, Reform, is 2.80, indicating that it is relatively independent. The VIF for Pgdp is 9.43, close to the critical value of 10, reflecting the systemic characteristics of regional development: economic growth is usually accompanied by capital accumulation and urbanization. This correlation is consistent with development economics theory and does not interfere with the estimation of Reform. The low VIF value of the explanatory variable Reform is consistent with theoretical expectations, supporting the scientific validity of the model setting. Therefore, the model passes the test.

Results of Multicollinearity Tests.

Unit Root Test

Given the characteristics of geographical adjacency among cross-sectional units in non-balanced panels, this paper first verifies cross-sectional independence using the Friedman test. The results indicate that the test statistic is 11.490 with a p-value of .9991. Therefore, we do not reject the null hypothesis of “cross-sectional independence,” confirming that the data exhibits no cross-sectional correlation issues. Secondly, given the significant cross-sectional variation in the time dimension of this study’s non-equilibrium panel data, the efficiency of the Levin, Lin & Chu (LLC) and Im, Pesaran & Shin (IPS) tests is susceptible to impairment. Therefore, this paper employs the combined ADF-Fisher (Fisher Augmented Dickey–Fuller) and Fisher Phillips–Perron (PP-Fisher) tests, which are robust to missing observations and adaptable to heterogeneous time series lengths, to rigorously assess variable stationarity and effectively mitigate the risk of spurious regression. The test results are shown in Table 6. Except for the variable Reform, all other variables became stationary after differencing.

Unit Root Test Results.

Note. The value in parentheses is the p-value. “Δ” represent first-order difference sequences.

, **, * are significant at the 1%, 5%, and 10% confidence levels, respectively.

Among these, as a binary virtual variable, the core explanatory variable, Reform, is essentially an exogenous policy shock, which is itself a “0–1” discrete stationary sequence. Furthermore, unit root tests apply to continuous economic variables, and the test results for binary variables lack economic significance. The core objective of variable Reform is the timing and impact of policy shocks. Therefore, the effects of policies should be tested by constructing a multi-period DID model, rather than verifying stability. In addition, the remaining variables are all first-order unit-root series. Based on co-integration theory, this paper uses the two-step EG method (Engle–Granger) to prove that a co-integration relationship does indeed exist, and that subsequent empirical analysis can be conducted using the original series. At this point, both the ADF and PP tests have been passed, ruling out single-method bias and ensuring the accuracy of subsequent regression analysis.

Benchmark Regression

The article uses the benchmark regression model for preliminary estimation to fully disclose the precise effect of budget performance management reform on local governments’ budgetary resilience. Table 7 displays the regression findings.

Benchmark Regression Results.

Note. Standard errors are represented by the values in parentheses. To mitigate the effects of time-series correlation in the difference-in-differences model, regression analysis employs the robust standard error of clustering at the regional level. The other tables are identical.

, **, * are significant at the 1%, 5%, and 10% confidence levels, respectively.

According to the findings, the budget performance management reform has increased local fiscal resilience, as evidenced by the estimated coefficients before and after the addition of control variables, which are .0712 and .0642, respectively, and both are positively significant at the 1% level. Hypothesis 1 is correct.

Parallel Trend Test

To demonstrate the validity of the benchmark regression results, the Multi-Period DID model’s effective estimation must meet the common trend assumption. Thus, this study examines the dynamic change characteristics in the budget performance management reform policy’s implementation process and performs a parallel trend test on the research sample. This article uses the implementation year of the budget performance management reform pilot policy as a reference point because of the potential time lag effect of policy implementation. Figure 1 displays the test findings.

Parallel trend test results.

The findings demonstrate that the experimental group’s and the control group’s regression coefficients in each period before the reform’s implementation are not significant, but the coefficients following the implementation are significantly positive. This suggests that there was no discernible difference between the pilot and non-pilot areas before the policy’s implementation, which is consistent with the parallel trend test hypothesis and the effectiveness of the benchmark regression results. Regarding dynamic effects, the coefficients from the first period following policy implementation to the 11th period following policy implementation are positive and significant, suggesting that the positive effect has been steadily reinforced over the 11 years following policy implementation and has not diminished over time. The estimation was favorable in the 13th year and beyond, but the significance started to wane in the 12th year following the policy, suggesting that the policy’s impact needed to be reinforced right away. Feng and Bilinski (2024) similarly point out that the dynamic effects of policy implementation need to be tracked over time, and the range of data chosen in this paper is largely adequate for analyzing this situation.

Placebo Test

Although endogenous issues are tentatively eliminated by the aforementioned test, issues like random factors and variable omission may still have an impact on robustness. Considering that the choice of districts to implement budget performance management is not completely randomized, referring to the research methodology of Cao et al. (2021), the article adopts the constructed interaction term methodology to conduct a placebo test on the results of the benchmark regression by creating a dummy variable for randomized policy implementation year, reconstructing the interaction term, and conducting 500 repetitions of the experimental cycle to avoid chance error (Figure 2).

Placebo test results.

Repeated experiments reveal that the estimated coefficients are concentrated around 0 and that the majority of the p-values are greater than 0.1. This suggests that neither random variables nor missing variables can interfere with the benchmark regression and that the effectiveness of the budget performance management reform in boosting local fiscal resilience has been confirmed.

Robustness Tests

This article uses Tobit parameter estimation, varying sample intervals, and lagging explanatory factors to evaluate the resilience of the original econometric model to confirm the robustness of the core explanatory variables to the explanatory variables based on the original econometric model.

Tobit Parameter Estimation

The article uses Tobit regression to verify its robustness since the observed value of the explained variable, Res, in the sample data is restricted between positive and zero values, and some samples contain missing and censored data. Table 8’s columns (1) and (2) display the findings. Before and following the addition of control variables, the budget performance management reform regression coefficients were .1450 and .0913, respectively. Both are statistically significant at the 1% level. The empirical findings are strong, and the conclusion that reforming budget performance management helps to increase local fiscal resilience is still relevant today.

Robustness Test Results.

Note.***, **, * are significant at the 1%, 5%, and 10% confidence levels, respectively.

Change the Sample Interval

The world economy has been severely hit by the new coronavirus outbreak. This research evaluates the effect of budget performance management reform on local fiscal resilience once more, removing data from 2020 to prevent data contamination. The empirical results are robust, as evidenced by the estimated coefficients of .0746 and .0683, respectively, which are significant at the 1% level and are displayed in columns (3) and (4) of Table 8.

Lag One Phase Explanatory Variables

The article will re-run the benchmark regression under the double fixed effect after the explanatory variable lags one period to circumvent the reform policy’s time lag for estimating the bias of the benchmark regression results of the original model. Table 8’s columns (5) and (6) display the findings. The empirical results are robust, and the promotion effect of the reform on local fiscal resilience remains positive and significant even after removing the effect of time lag, as indicated by the regression coefficients before and after adding control variables, which are .0812 and .0731, respectively, and both significant at the 1% level.

Mechanism Tests

Fiscal Expenditure Efficiency

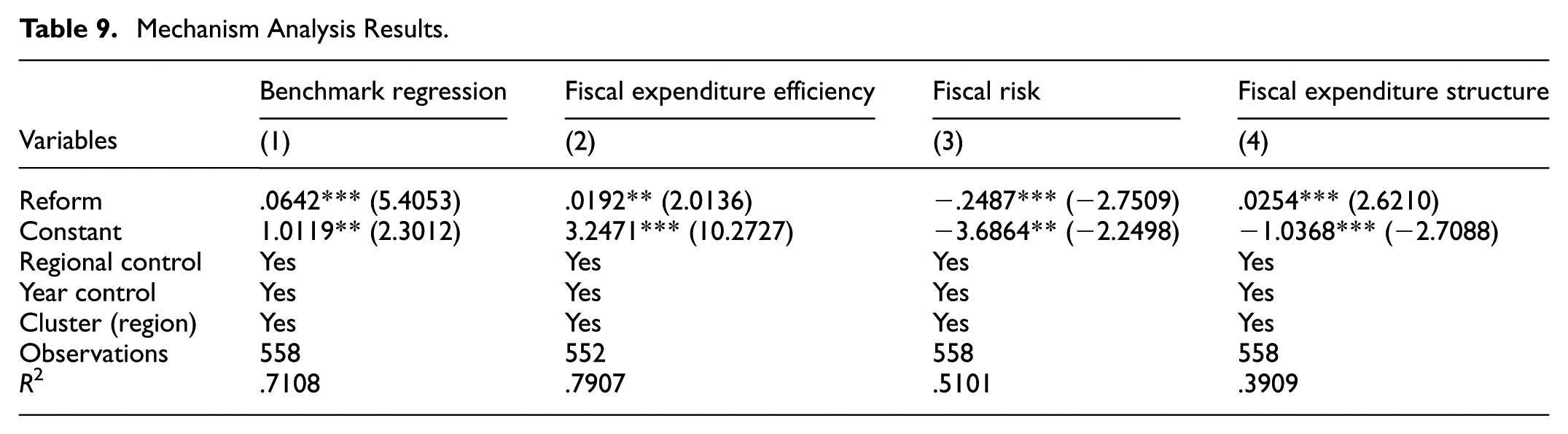

Improving local fiscal expenditure efficiency is a good method to reduce the disparity between fiscal revenue and expenditure in the setting of decreasing economic growth. The DEA-BCC model considers the features of variable returns to scale local fiscal expenditure, eliminates issues brought on by subjective bias or model assumptions, and focuses on how to maximize output under specific input conditions. To measure the effectiveness of fiscal expenditure, this article uses the input-oriented BCC model, uses the per capita fiscal expenditure (in billions) as the input index, and chooses the corresponding output index from the three dimensions of social stability, economic development, and improvement of people’s livelihoods. Among these, the per capita GDP is used to gauge economic development; the urban-rural divide and employment are used to gauge social stability; and education, health, infrastructure, and living standards are used to gauge the advancement of people’s livelihoods. The exact output indicators are no longer included because of the article’s length. According to Table 9’s results in Column (2), budget performance management reform helps to improve the efficiency of fiscal expenditure. Upon analysis, the implementation of active fiscal policy with added strength and efficiency, and the improvement of fiscal expenditure efficiency by focusing on the main business, expanding domestic demand, innovation and leading and livelihood protection can better bring the effectiveness of fiscal policy into play and achieve stable economic growth. Rashied et al. (2024) state that budget performance management reforms are effective in improving the efficiency of local government budgets through the introduction of transparent performance assessment mechanisms and accountability systems. And improving the efficiency of fiscal spending can help governments allocate funds more efficiently to respond to emergencies with limited financial resources, or to be able to deploy resources more quickly to respond and recover after an emergency (Sadler et al., 2024). This will help to provide strong financial support for stable economic growth, enhance market confidence and thus stabilize the finances. Therefore, by implementing reforms to improve the efficiency of fiscal expenditures, local governments can make efficient use of financial resources and improve the adaptability and resilience of their fiscal systems. That is, improving the efficiency of fiscal spending is important for enhancing fiscal sustainability and resilience. Hypothesis 2 is confirmed.

Mechanism Analysis Results.

Fiscal Risk

The rise in fiscal risk could impact the macroeconomic stability of the nation and cause economic volatility. Long-term and significant budget deficits may pose increased fiscal concerns, even though they may temporarily stimulate the economy. Therefore, the article is measured by fiscal deficit, that is, fiscal deficit = (fiscal expenditure − fiscal revenue)/total number of people. According to Table 9’s results in Column (3), budget performance management reforms help to reduce fiscal risks. Budget performance management reform reduces fiscal risks by strengthening budgetary constraints and optimizing resource allocation. Currently, local governments in China may face the risk of contingent and hidden debt, which may inhibit the ability of fiscal sustainability, and need to avoid the waste and abuse of fiscal resources by strengthening budget performance management, thus reducing fiscal risks. Hochrainer-Stigler et al. (2024) argue that fiscal buffers need to be built up in advance to effectively cope with declining revenues and rising spending pressures, which can help mitigate short-term recessionary shocks and long-term fiscal fatigue, thereby reducing fiscal risks (Wang, 2023).In addition, Australia’s experience in establishing transparent fiscal rules and a multi-level risk-sharing mechanism suggests that risk reduction can improve the ability to cope with external shocks and fiscal resilience (OECD/The World Bank, 2019). Thus, budget performance management reforms can enhance local fiscal resilience by reducing fiscal risks. Hypothesis 3 has been confirmed.

Fiscal Expenditure Structure

An appropriate fiscal spending structure facilitates effective resource allocation and raises the general economy’s and society’s operational efficiency. Among them, the fiscal expenditure structure = (health care + education + science and technology + social security and employment expenditure)/fiscal expenditure. According to the results of Table 9’s Column (4), budget performance management reforms have helped to increase the proportion of livelihood-related expenditures and optimize the structure of fiscal expenditures. Zhou and Ren (2020) similarly point out that the optimization of the fiscal expenditure structure can enhance the stability and growth potential of the economy by promoting industrial upgrading and coordinated regional development, for example, the increase in health and social security expenditures not only improves the living standards of the residents, but also stimulates the vitality of the labor market, thus providing a more stable source of fiscal revenue. Duan and Soh (2024) showed that by optimizing the structure of expenditures, fiscal resources can support economic activities more efficiently and reduce fiscal volatility. This means that the Government can be more flexible in adjusting the direction and scale of expenditure in times of economic fluctuations, thus enhancing its fiscal responsiveness. Therefore, optimizing the structure of fiscal spending not only improves fiscal efficiency and sustainability but also enhances the stability and growth potential of the economy, thereby effectively increasing fiscal resilience. In summary, budget performance management reform can enhance local financial resilience by optimizing the structure of fiscal expenditures. Hypothesis 4 has been confirmed.

Heterogeneity Analysis

The aforementioned descriptive statistical findings demonstrate that there is a significant difference between the highest and lowest levels of local fiscal resilience. This study uses group regression to better understand how budget performance management reform affects local fiscal resilience from three angles: Tax competition, fiscal decentralization, and spatial distribution.

Spatial Distribution

The eastern part of the region has a reasonably balanced fiscal revenue structure and a solid economic base. For instance, Jiangsu, Zhejiang, Shandong, and other provinces have comprehensive fiscal scales above 1.5 trillion yuan, whereas the central and western areas have low levels of economic development and a fiscal revenue structure that is more reliant on federal subsidies. It can still demonstrate the possibility of fiscal revenue increase, nevertheless, in some circumstances. To deeply analyze the impact of budget performance management reforms on local fiscal resilience in each region, this paper divides the country into two regions, the East and the Midwest, and conducts group regressions. Table 10 displays the estimated outcomes.

Spatial Distribution-Group Regression.

Note.***, **, * are significant at the 1%, 5%, and 10% confidence levels, respectively.

The results show that the reforms are more effective in raising the level of fiscal resilience in the central and western regions. After analyzing, the budget performance management reform in the central and western regions started late, the economic development is relatively lagging, and the overall economic activities show a relatively rough development stage. However, the eastern region, where the reform was introduced earlier, has benefited from higher levels of economic development and productivity, and its financial resources have been invested more abundantly and efficiently in public services. Combined with the principle of diminishing marginal benefits, when the economic development of a region reaches a certain stage, the marginal benefits of fiscal resource inputs will gradually decrease. Jiang and Chi (2024) similarly argue that the eastern region may have a faster rate of diminishing marginal benefits of financial resource inputs due to its higher level of economic development and abundant and efficient financial resources. Thus, while budget performance management reforms can improve the efficient use of financial resources, they may not produce extremely significant results in the eastern region. On the contrary, reforms in the central and western regions have been more effective, suggesting that reforms have greater potential in regions with relatively weak economic development, and Dzigbede et al. (2023) also point out that reforms in regions with weak budgetary systems can significantly improve the efficiency of the allocation of financial resources, and thus better cope with economic crises. Therefore, reforms should be more oriented towards economically weak regions to achieve balanced regional development.

Tax Competition

The significant fiscal challenges that are currently being faced in the restructuring of the Chinese government system have made it more difficult for the economy to run steadily. Inequitable distribution of resources and fiscal revenue in different regions continues to cause societal difficulties. When it comes to tax competition, local governments will act strategically by changing tax rates to draw in investment. The issue of uneven regional economic development grew as a result of different regions implementing different tax policies to draw in capital and businesses. This widened the economic divide between regions and could result in disparities in the fiscal quality of developed and underdeveloped areas (Tamai, 2022; Tao et al., 2023). Nonetheless, the resilience of fiscal revenue can be increased by tax structure optimization, tax source diversification, and increased tax collection and management effectiveness (Li & Yang, 2024). As a result, the average tax burden of other regions outside the province is used to build a dummy variable of tax competition in this paper. Table 11 displays the results of the grouping regression.

Tax Competition-Group Regression.

Note. Regional tax burden is measured by macro tax burden, that is, regional tax revenue/GDP. ***, **, * are significant at the 1%, 5%, and 10% confidence levels, respectively.

The results suggest that the reforms have a more pronounced effect on fiscal resilience in areas with low tax competition. The analysis shows that, because regions with low tax competition have stable tax sources and less competitive pressure, fiscal funds are used more efficiently, and the response to reform policies is better. And Cai and Treisman (2005) similarly point out that in areas with lower tax competition, local governments are more inclined to maintain competitiveness and increase economic resilience through more efficient use of fiscal funds. Tax competition may lead some regions to become overly dependent on tax incentives, while others maintain competitiveness through more efficient use of fiscal funds (Bucovetsky & Wildasin, 1989). Local governments will lower taxes and increase the supply of public goods to attract residents and capital, and over-reliance on policies such as tax incentives to attract investment in areas with strong tax competition will result in lower tax revenues (Zodrow et al., 1986). Under the implementation of reforms focusing on the quality and effectiveness of tax policies, local governments need to maintain a balance between tax incentives and improved efficiency in the use of fiscal resources. Therefore, implementing budget performance management reforms in areas with low tax competition can be more effective in improving fiscal resilience.

Fiscal Decentralization

Fiscal decentralization has greatly accelerated economic growth since the 1994 tax-sharing reform, but it is also a major contributor to economic volatility. This is because it could result in an unequal allocation of resources and fiscal income among areas, which would then have an impact on regional economic development (Nirola et al., 2022). The budget performance management reform helps to standardize and scientificize the fiscal behavior of local governments and enhances the effectiveness and efficiency of the use of fiscal funds under the fiscal decentralization system. The essay uses regional fiscal revenue and spending decentralization as metrics for fiscal decentralization. Table 12 displays the results of the grouping regression.

Fiscal Decentralization-Group Regression.

Note. Fiscal revenue (expenditure) decentralization = provincial per capita fiscal revenue (expenditure)/central per capita fiscal revenue (expenditure). ***, **, * are significant at the 1%, 5%, and 10% confidence levels, respectively.

The results show that reforms are significantly more effective in regions with low levels of fiscal revenues and higher levels of decentralized fiscal spending. Among them, local governments in regions with higher levels of fiscal decentralized spending have greater autonomy and flexibility in the allocation of financial resources, enhancing fiscal resilience by responding more effectively to economic fluctuations and external shocks. Xia et al. (2022) argue that local governments in regions with high levels of fiscal decentralized spending have greater autonomy and flexibility in the allocation of financial resources and are better able to balance economic development and environmental governance, while low-spending regions face greater challenges. Zhan et al. (2022) point out that regions with high fiscal decentralization expenditures are more fiscally resilient and better able to cope with economic fluctuations due to sufficient resources. Fiscal imbalances in regions with low fiscal decentralized revenues and high decentralized expenditures are prone to fiscal deficits or debt problems, and reforms are needed to improve the efficiency of the use of fiscal funds to cope with fiscal imbalances (Cai & Treisman, 2005). As budget performance management reforms are more likely to lead to accurate allocation of resources in areas with relatively tight financial resources, fiscal deficits can be mitigated, and systemic risks can be avoided. As a result, the effects of reform implementation are more pronounced in this type of area.

These findings have important implications for international policy. First, for other developing or emerging economies, budget performance management reforms should be implemented differently according to the level of economic development and fiscal situation of the region. Second, policymakers should focus on the impact of tax competition on fiscal resilience, avoiding over-reliance on tax incentives to attract investment and instead enhancing competitiveness by improving the efficiency of the use of fiscal funds. Thirdly, the implementation of fiscal decentralization policies should take full account of regional fiscal revenue and expenditure situations, giving more autonomy and flexibility to regions with high levels of decentralized fiscal expenditure, while providing the necessary policy support to regions with low levels of decentralized fiscal expenditure, to achieve an overall increase in fiscal resilience.

Conclusions and Revelations

Based on provincial panel data from China from 2001 to 2021, this article uses a multi-point DID model to empirically investigate the impact of budget performance management reform on local fiscal resilience and its mechanism of action. The study confirms that this reform has significantly enhanced local fiscal resilience by improving fiscal expenditure efficiency, reducing fiscal risks, and optimizing expenditure structure. It also shows heterogeneity in terms of spatial distribution, tax competition, and fiscal decentralization. However, although budget performance management reform has achieved significant results, it still faces issues such as uneven development and incomplete implementation. It is imperative to accelerate the construction of a new development pattern and the process of high-quality development. The research findings not only provide empirical support for the integration of fiscal resilience and budget management theory but also offer key references for deepening reform practices.

Based on the research findings, this article proposes three policy recommendations. First, accelerate the digital transformation of budget performance management, use big data and artificial intelligence technology to achieve dynamic monitoring of the entire fiscal fund process, strengthen source governance, improve the fiscal risk early warning system, adhere to the principle of “guaranteeing the basics and maintaining the bottom line,” and strictly adhere to the debt safety bottom line. Second, strengthen regional coordination and governance mechanisms, adhere to the principle of “adapting to local conditions,” formulate differentiated reform plans for central and western regions, and ensure that the “pie” is both enlarged and distributed fairly. At the same time, improve the financial and accounting supervision system, increase the coordination of fiscal funds and the adjustment of expenditure structures, and narrow regional fiscal resilience gaps through dynamic monitoring and targeted policies. Third, improve the government regulatory accountability system, give full play to the government’s macro-control role, eliminate misalignment, overreach, and neglect, while strengthening tax competition regulations and fiscal information disclosure, promoting public participation in the performance management process, and continuously improving government credibility and public service levels to drive the transformation of performance management from “focusing on input” to “focusing on results.”

Overall, this article expands the theoretical dimension of combining fiscal resilience with budget management tools and provides empirical experience for deepening budget performance management reform. It is conducive to further improving top-level policy design, helping local governments implement precise policies, and pointing the way forward for subsequent exploration. On the one hand, it can further validate the dynamic regulatory role of budget performance management reform in responding to economic fluctuations and sudden public events, providing experience for improving national governance efficiency. On the other hand, it is possible to broaden the scope of international comparison, learn from the experience of developed countries in fiscal performance management, and optimize the overall design of the country’s fiscal system. However, despite the rigorous design of the data and methods used in this article, certain limitations remain. At the data level, due to restrictions on public information, the absence of certain key variables, such as implicit debt and real-time budget execution data, may affect the accuracy of estimates. Future research could explore data innovation and technological breakthroughs to address this gap. In terms of scope, this article focuses solely on the provincial level, making it difficult to reflect the complex mechanisms at play in reform practices at the municipal and county levels. This provides a starting point for in-depth analysis of the micro-level pathways through which policies are transmitted. In theoretical analysis, the role of non-economic factors such as the political environment and institutional change has not been sufficiently explored. Further research is urgently needed to apply an interdisciplinary perspective and construct a more explanatory theoretical framework.

Therefore, in future research, it is possible to conduct an in-depth analysis of the micro-mechanisms and macro-effects of budget performance management reform by integrating multi-source data, further constructing a multi-level analytical framework, and incorporating institutional economics theory. This will not only help to improve the theoretical framework of fiscal resilience but also provide more targeted theoretical and practical guidance for the modernization of the fiscal system. We will continue to pay close attention to the latest developments in this field and look forward to more scholars engaging in in-depth discussion and innovative exploration in this area.

Footnotes

Acknowledgements

We sincerely thank our colleagues, mentors, and industry experts for their invaluable insights and guidance, which have been pivotal in advancing this research. Their commitment and constructive feedback have been essential to our study’s development.

Ethical Considerations

There were no animal and human studies being applied in this manuscript. Ethics Approval is no need.

Consent to Participate

There were no animal and human studies being applied in this manuscript. Informed consent is no need.

Author Contributions

Each author has made substantial contributions to the research: this includes conceptualization and methodology design, development of the search strategy, data curation, results presentation (visualization), and discussion. The drafting of the original manuscript was primarily undertaken by Anli Xu, Xiaoqi Zhang was responsible for sorting out the literature, while Shujun Jiang provided critical review and editing. All authors have reviewed and approved the final version of this article.

Funding

The authors disclosed receipt of the following fiscal support for the research, authorship, and/or publication of this article: Support Program for Innovative Talents of Philosophy and Social Sciences in Colleges and Universities in Henan Province of China (2025-CXRC-30).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.