Abstract

The economic downturn has led to a variety of challenges for higher education institutions, including budget cuts and a heightened focus on efficiency and effectiveness. Performance-based budgeting is gaining traction as a means of more efficiently allocating resources, and Chinese public universities are not an exemption. The main purpose of this study was to look into the relationship between political influence, financial pressure, performance-based budgeting, and university performance in China. It also explored power dynamics in Chinese public universities. 271 participants were chosen using a purposive sampling technique. This study employed a multimethod approach combining necessary condition analysis (NCA), the PROCESS macro, and partial least squares structural equation modelling (PLS-SEM). Furthermore, this study employed a novel technique (the Johnson-Neyman technique) to show the exact scope of the moderation effect. The findings of the PLS-SEM showed that performance-based budgeting is positively related to university performance and acts as a mediator between selected variables, and it also indicated that the moderated mediation model is validated in Chinese public universities. The NCA results showed that performance-based budgeting, political influence, and financial pressure are all important necessary conditions for university performance. Meanwhile, the outcomes of PLS-SEM and NCA showed how researchers and practitioners can pinpoint key elements that affect university performance and produce the best outcomes. Overall, this study provides useful information about the implementation of performance-based budgeting in higher education institutions.

Plain Language Summary

The main purpose of this study was to look into the relationship between political influence, financial pressure, performance-based budgeting, and university performance in China. It also explored power dynamics in Chinese public universities. This study employed a multimethod approach combining necessary condition analysis (NCA), the PROCESS macro, and partial least squares structural equation modelling (PLS-SEM). Furthermore, this study employed a novel technique (the Johnson-Neyman technique) to show the exact scope of the moderation effect. The findings of the PLS-SEM showed that performance-based budgeting is positively related to university performance and acts as a mediator between selected variables, and it also indicated that the moderated mediation model is validated in Chinese public universities. The NCA results showed that performance-based budgeting, political influence, and financial pressure are all important necessary conditions for university performance. The outcomes of PLS-SEM and NCA showed how researchers and practitioners can pinpoint key elements that affect university performance and produce the best outcomes. Overall, this study provides useful information about the implementation of performance-based budgeting in higher education institutions. Limitations: Just focus on Chinese public universities.

Keywords

Introduction

Higher education institutions (HEIs) have faced profound changes in recent years (Hagerer, 2019), including a greater emphasis on effectiveness as well as efficiency, globalization, declining government funding, shifting societal expectations, and changing demands for higher education (Cheah et al., 2022). The university’s primary goal has shifted to realizing the effectiveness of the organization and improving its economic rationality (Bobe & Kober, 2018). Given this context, effectively allocating scarce public resources has become more complicated and the strategic goals of higher education have become increasingly difficult to achieve (Hamlin & Patel, 2017; Kenno et al., 2020). Universities must improve their level of accountability, evaluate their teaching and research performance, focus on increasing revenue, reduce their costs, improve efficiency, and ensure that the budget is met (Bobe & Kober, 2018; Su & Baird, 2017), which means doing the most with the least money. Various researchers agreed that budget plays a vital role in universities (Zha & Liu, 2019). As Leth et al. (2017) stated performance-based budgeting (PBB) is a public sector funding mechanism that strengthens the connection between funding and results through the methodical application of formal performance data.

Ho et al. (2019) stated that PBB integrates performance information and analysis into the budgetary process to enhance efficiency, effectiveness, and accountability in resource allocation toward policy goals. PBB, emphasizing output and outcomes over input, has garnered attention in public management research (Hyndman et al., 2014; Mauro et al., 2017). Amidst reduced public funding and increasing financial pressure in higher education, PBB ensures transparency, centralized spending control, and strategic expenditure management, holding universities accountable to stakeholders. Moreover, it incentivizes sustainable planning and offers financial benefits (Sangiumvibool & Chonglerttham, 2016), aligning with New Public Management principles (Heinicke & Guenther, 2019). Figure 1 shows the antecedents and consequences of PBB.

A multi-layered understanding of PBB.Source: Ho et al.(2019)

Several reasons explain the use of PBB in this study. Firstly, although there were a few studies (Aliabadi et al., 2019; Altundemir & Gungor-Goksu, 2017; de Vries et al., 2019; Habiburrochman & Rizki, 2020; Huber & Hillebrandt, 2019; Pratolo et al., 2020; Sangiumvibool & Chonglerttham, 2016) that address the importance of PBB in HEIs, none of them focused on China. Budget deficits, structural problems, increasing competition, globalization, political and social motivations, and taxpayers’ growing demand for university accountability all promote the implementation of PBB. Therefore, there is a need to conduct research on PBB in the context of China. For Chinese universities, it is first related to the construction of “double first-class” universities currently implemented (Zong & Zhang, 2017). Universities should focus on performance-oriented funding, rational resource allocation, and raising Chinese universities’ global reputation.

Second, PBB was first implemented in the United States and other developed countries. Its purpose was to improve the efficiency of government funds, albeit with unsatisfactory results (de Vries et al., 2019; Lu et al., 2015; Melkers & Willoughby, 2005). According to Lu et al. (2015), 27 factors affect the implementation of PBB, which are mainly divided into internal factors and external factors. Ho et al. (2019) believed that multi-level institutional and organizational factors are crucial to the implementation of PBB. Amirkhani et al. (2020) also emphasized the important role of the external environment, organization, and individual factors in the implementation of PBB, and believed that the synergy of multiple factors can optimize the implementation of PBB more than a single factor. Due to the many contextual factors, a “one-size-fits-all” strategy is impossible (Amirkhani et al., 2020). Previous studies had not reached a consensus on the choice of contextual factors, which were usually based on the specific conditions of the countries (Lu et al., 2015). For Chinese universities, culture, politics, economics, and human resources can have an important and far-reaching influence on the adoption of PBB. Chinese universities are under strong government control, so government policies play a very important role in universities. To obtain more financial appropriations, universities will actively respond to government policies. Many previous studies (Ahn et al., 2014; Alsharari et al., 2015; Burns, 2000; Carter & Mueller, 2006; Hiebl, 2018; Modell, 2012; Wu & Boateng, 2010; Xiao et al., 2004) examined the influence of political influence on management accounting changes, with fewer studies on PBB (Amirkhani et al., 2020; Hawke, 2012; Lu et al., 2015), none of which were in the higher education sector. PBB can link budget and performance to maximize resource utilization and can ease the financial pressure on universities (Lu et al., 2015). Therefore, there is a need to explore the Chinese context to see whether the implementation of PBB by the political and economic environment with Chinese characteristics would result in positive outcomes. Last, PBB has not yet been implemented at the central government level and has only been piloted in several provinces, such as Guangdong (Niu, 2016). Therefore, it is crucial to see its country-wide implementation. The findings from this research are anticipated to offer insight into how PBB will be implemented in public universities.

This study highlights the impact of political influence and financial pressure on university performance and the role of power in Chinese public universities, enriching literature by developing a new moderated mediation model discussing the role of PBB in HEIs. This study primarily used necessary condition analysis (NCA) and partial least squares-structural equation modelling (PLS-SEM) to analyze data from the survey questionnaire in order to respond to the research questions. This study adds to the body of knowledge in three ways. First of all, this study takes financial pressure as a new contextual factor affecting PBB implementation, no previous studies used this variable to explain the adoption of PBB and its impact on university performance. This study fills this research gap by adding financial pressure as a novel variable. Second, combining PLS-SEM and NCA has the possibility of contributing to theory building while also having practical consequences for both business practice and research (Richter et al., 2020). Richter et al. (2022) stated that multimethod is becoming more popular in management research, but they were rarely used in previous studies. This study will fill this research gap. Third, according to Carrillo et al. (2021) and Lu et al. (2015), previous PBB research has been primarily explanatory as well as descriptive, and most of them have no theoretical foundation. This study fills the gap in the theoretical framework by combining contingency theory and RDT, so as to provide a more solid theoretical foundation for the research of PBB in higher education institutions.

Theoretical Framework and Hypothesis Development

Contingency theory and resource dependency theory (RDT) are used in this study as the theoretical foundations to develop a moderated mediation model in order to test the relationship between the selected variables.

Political Influence, PBB, and University Performance

No budget reform, including PBB operated in a political vacuum. The logic of linking political influence and PBB in the proposed model is mainly based on Dawson (1994) and Pettigrew (1972). They stated that the PBB provides a power resource. Therefore, when studying PBB, research on the role of power and politics is indispensable. It may be used as a means to some political ends, such as redistribution of power among and within departments (Jones & McCaffery, 2005). There are some studies (Aidt et al., 2011; Amirkhani et al., 2020; Covaleski et al., 2013; Ferlie et al., 2008; Hawke, 2012; Lee & Wang, 2009; Lu et al., 2015; Phusavat et al., 2012) on the role of political influence on PBB. However, these studies mainly focus on the political influence of politicians, but not on the influence of government policies on the public sector that depends on government funding. Hiebl (2018) and Xiao et al. (2004) argued that political influence has a positive effect. Meanwhile, some studies have reached the opposite conclusion, Wu and Boateng (2010) argued that political influence has no influence. There were also some studies that did not demonstrate the relationship between them (Ahn et al., 2014; Alsharari et al., 2015; Carter & Mueller, 2006; Modell, 2012).

The Chinese public universities have certain administrative functions. This administrative feature of Chinese universities causes all university activities to be affected by political influence. In addition, the main source of revenue for Chinese universities is government financial appropriations. Universities are very dependent on financial appropriations. Chinese universities’ development is under continuous and strong government control. Without government financial appropriations, public universities cannot survive. Therefore, political influence is a very important factor. The Chinese government is currently vigorously promoting PBB. In order to adapt to this change, Chinese universities must change their management methods in order to obtain more financial appropriations. Based on this, this study postulates that the current policy will have a positive impact on the adoption of PBB in Chinese public universities. Thus, the following hypothesis is proposed:

H1: Political influence has a positive effect on PBB in Chinese public universities.

H2: Political influence has a positive effect on university performance in Chinese public universities.

Financial Pressure, PBB, and University Performance

Due to the coronavirus outbreak, universities face unprecedented financial pressure mainly manifesting in the loss of international students and the increase in the development cost of online courses. The balance of payments of universities is currently undergoing enormous challenges. Universities already faced tremendous financial pressure pre-pandemic with the increase in enrolment and the decrease in public funding. Under this pressure, universities must reduce costs, increase revenue, improve capital efficiency, and reasonably allocate limited resources. PBB connects budget and performance to allocate resources, thereby improving resource efficiency and enhancing accountability and transparency. Its implementation relieves financial pressure and avoids unnecessary expenditures. Given the current economic bust, resource efficiency, which is needed to achieve institutional goals, has become increasingly arduous (Hamlin & Patel, 2017; Kenno et al., 2020). To the best of our knowledge, no study has used financial pressure as an independent variable. This study therefore adds this novel variable following the actual situation of Chinese universities. Because previous studies in PBB have not used financial pressure as a contextual factor, this study fills this gap by identifying whether financial pressure influences university performance. So, the following hypothesis is tested in this study:

H3: Financial pressure has a positive effect on PBB in Chinese public universities.

H4: Financial pressure has a positive effect on university performance in Chinese public universities.

PBB and University Performance

As previously stated, the use of PBB may provide enhanced information to improve decision-making and reinforce better achievement of organizational goals, thereby improving its performance. There exists various literature on university performance. However, the literature on the variables affecting university performance and methods for improving university performance is still very limited. Different findings have been found in previous studies on the association between PBB and university performance (de Vries et al., 2019; Habiburrochman & Rizki, 2020; He & Ismail, 2023; Pratolo et al., 2020). de Vries et al. (2019) stated that PBB has varying (either positive or negative) effects in American universities in different states. Meanwhile, both Habiburrochman and Rizki (2020) and Pratolo et al. (2020) studied PBB in universities in Indonesia, Habiburrochman and Rizki (2020) found that PBB has no effect on university performance, and Pratolo et al. (2020) stated that PBB has a positive effect on university quality. In line with Pratolo et al. (2020), He and Ismail (2023) found the PBB positively impact on university performance.

The budget is an important tool in China for governance and management, negotiation and resource allocation, and government accountability. Similarly, among practitioners, this is a shared area where various stakeholders coexist. However due to great differences in culture, concepts, expectations, and professional norms, they usually cannot fully interact. As a result, budgeting and performance evaluation are frequently linked. Universities that do a good job get more government funding and, surprisingly, cut their budgets. The performance of higher education reflects the efficiency and effectiveness of public services, and social interests must guide universities. Overall, PBB is inextricably linked to university performance. Given the inconclusive relationship and the specific condition of Chinese universities, the following hypothesis is put to the test in this study:

H5: Performance-based budgeting has a positive effect on university performance in Chinese public universities.

The Mediating Role of PBB

Organizations differ in their characteristics and budget practices. Researchers conduct rigorous investigations inside of each organization to explain its accounting practices (Youssef et al., 2020). Some studies (Haldma & Lääts, 2002; Hammad et al., 2010; Hariyati & Tjahjadi, 2018; Hutahayan, 2020; Pasch, 2019; Youssef et al., 2020) believe that management accounting practices play a mediating role between the internal and external factors of the organization and organizational performance. Meanwhile, Hutahayan (2020) verifies the same relationship posited by Hariyati and Tjahjadi (2018) where the results showed the complete opposite: management accounting information systems, instead, have no mediating effect. Some studies are different from the above two results. Pasch (2019) studied the mediating role of management accounting systems between strategy and innovation, where results showed that management accounting is only partially mediated. For PBB, Pratolo et al. (2020) and He and Ismail (2023) demonstrated that PBB plays a mediating role in universities.

Universities are under a great deal of pressure as a result of the current economic crisis, which has forced them to make cost cuts, keep their budgets balanced, and actively contribute to economic growth. That is to say, the adoption of PBB depends on its capacity to raise revenues, cut costs, and boost fund efficiency. These functions will only benefit university performance if they are fully utilized. As a result, it is essential that the budget system act as an intermediary to assist in planning and control management. In other words, a budget system is a tool for organizing different organizational departments, monitoring and evaluating employee performance, inspiring staff members, and enhancing communication. PBB serves as an inspector in this process because the budget system is a vehicle through which culture, politics, economics, and human resources all influence how well universities perform. Because of its implementation, there is now an indirect relationship between contextual factors and university performance. As a result, the hypothesis that follows is suggested based on the preceding arguments:

H6 a: PBB serves as a mediator between political influence and university performance in Chinese public universities.

H6 b: PBB serves as a mediator between financial pressure and university performance in Chinese public universities.

The Moderating Role of Top Management Support

Top managers in Chinese universities wield absolute power. The allocation of resources primarily reflects the support of top managers. PBB implementation may fail if top management support is not present. On the other hand, the organization’s current inadequacy of other resources, however, can be supplemented or made up for by top management support, which can also promote PBB implementation (Hsu et al., 2019). All resources were under the control of top administrators in Chinese public universities. Therefore, it is important to look into how top management support affects PBB implementation and university performance. Ali et al. (2020), Hsu et al. (2019), and Islam et al. (2009) have examined top management support as a moderating variable, however, not all of them have been examined in higher education institutions. In this study, top management support is examined both at higher and lower levels in terms of its moderating effects. The following hypothesis is suggested in this study:

H7: The relationship between PBB and university performance in Chinese public universities is moderated by the level of top management support.

The testing of the seven hypotheses in this study is summarized in Figure 2 (research model).

Research model. A description of the relationship between variables in the present study.

Methodology

The aforementioned hypotheses were tested using a quantitative research design. This study used online questionnaire to collect data. In order to ensure that only participants with the necessary skills and knowledge were contacted, a purposive sampling strategy was used. G*Power 3.1 was used to determine the sample size. The estimated minimum sample size is N = 159. For this study, Wenjuanxing (https://www.wjx.cn) was utilized. It is a popular online survey platform in China. The survey was available for 4 weeks in May 2021. In addition, a representative sample of the pertinent population was gathered through the use of WeChat and QQ. The survey was entirely voluntary and anonymous, and participants were free to withdraw at any time. 271 responses were obtained overall after several rounds of follow-up; details are shown in Supplemental Appendix Table A1.

The sample consisted of 132 male accountants and 139 female accountants. In terms of age, nearly half of the respondents (47.6%) were aged over 45, with 27.3% falling between the ages of 26 and 35, and 25.1% between 36 and 45. Regarding educational background, the majority (53.1%) held a Bachelor’s degree, followed by 36.2% with a Master’s degree, and a small proportion (9.2%) with a doctoral degree. In terms of academic background, the majority (66.1%) were accounting majors, with most of the remaining respondents having majors related to accounting. Regarding positions, the majority (80.9%) were accounting staff from the financial department responsible for budget management. These findings suggest that all participants possessed the requisite professional knowledge to address issues related to PBB in Chinese public universities and provide informed perspectives.

In accordance with Churchill’s (1979) recommendations for developing a standardized survey instrument, this study meticulously chose the variable measurements according to the research context. Each measurement instrument had been modified from previous research and had proven to be long-term reliable. A 5-point Likert scale was used to ask respondents to rate the situation. The items of the proposed model are listed in Supplemental Appendix Table A2. The measurement of political influence was adapted from Gu et al. (2019), Wu and Boateng (2010), and Xiao et al. (2004). Gu et al. (2019) have provided a comprehensive definition of political influence, highlighting its impact at both the macro and micro levels. On the macro level, political influence stems from shifts in political power and alterations in regulations and policies. At the micro level, political influence assumes an even greater significance, influencing day-to-day operations, including aspects such as budget allocation, cost management, and performance evaluation within companies (Cohen et al., 2017). This study combines the actual situation of Chinese public universities and previous research and defines political influence as the impact of national-level policy on the implementation of PBB by universities, both in terms of published policies, the allocation of resources, and the designation of university leaders. The measurement of financial pressure was adapted from Huikku et al. (2018). According to Huikku et al. (2018), the financial pressure of a university refers to the degree of difficulty for the university to obtain funds from external or internal sources. In this study, financial pressure represents the level of difficulty of the university in obtaining external and internal resources. The reliability of this measure was found to be acceptable with high internal consistency (Cronbach’s alpha = .901). PBB establishes a connection between input costs and performance, aiming to enhance expenditure efficiency across various aspects by systematically tying funding to outcomes and leveraging performance data to accomplish this connection (de Vries et al., 2019). A survey instrument comprising ten items, originally devised by Pratolo et al. (2020), was adapted to assess PBB implementation in Chinese public universities. The scale demonstrated a reliability coefficient of .881. For university performance, the survey instrument created by Bobe and Kober (2018) served as the foundation for the scale. The scale was adjusted to fit the Chinese public university management construct as it was conceptualized in this study (based on input received on the pilot survey). The scale’s reliability was found to be .899. The concept of top management support was derived from Islam et al. (2009) and was employed as a moderating variable in this research. The reliability of this measure was found to be acceptable with high internal consistency (Cronbach’s alpha = .935).

Data Analysis and Results

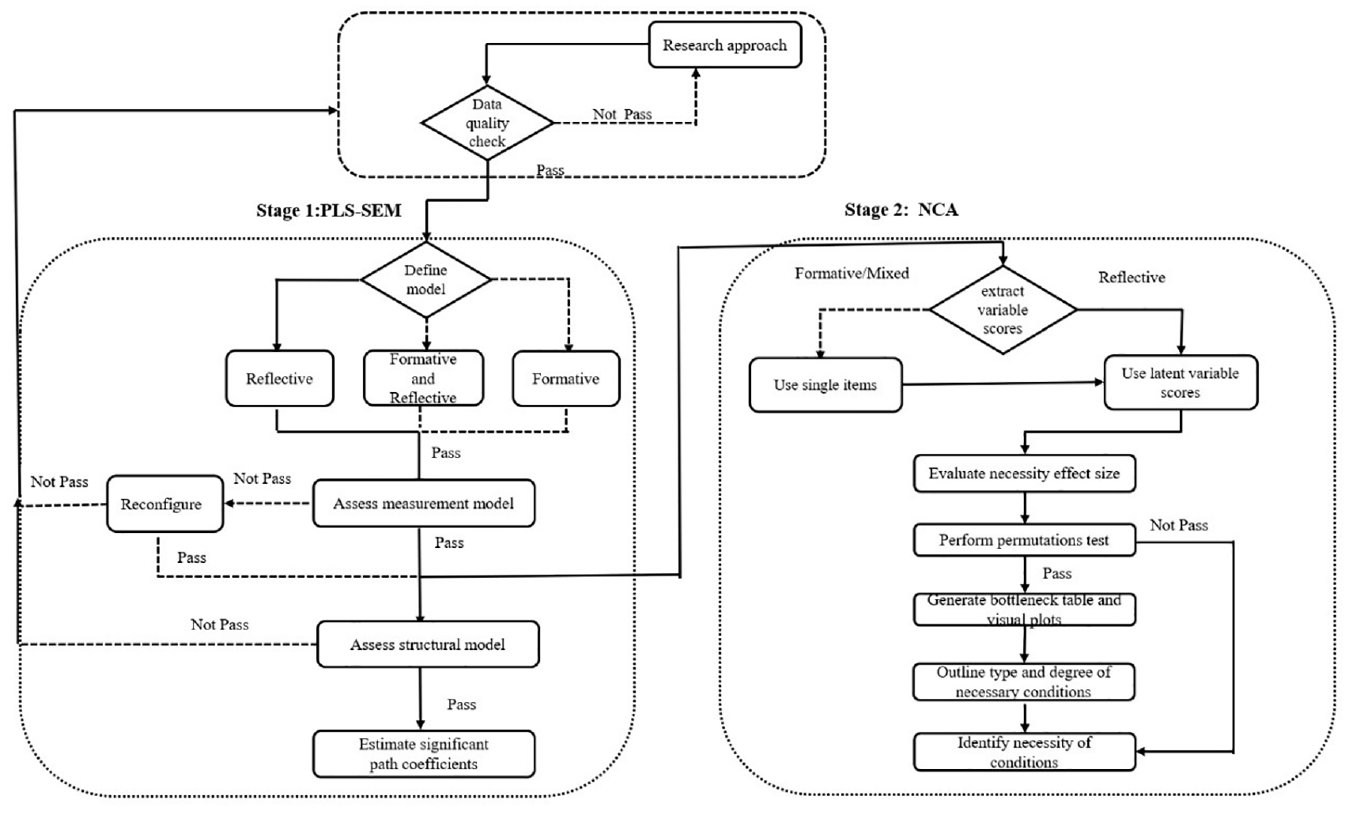

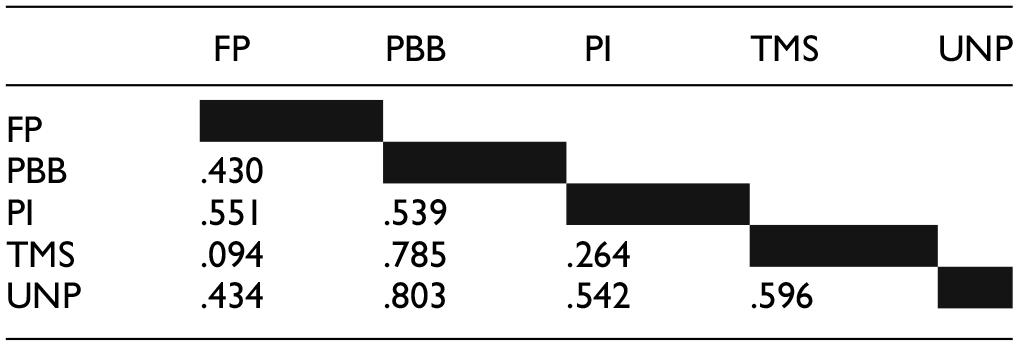

As for the theoretical model, the theoretical model used in this study includes both mediating and moderating variables. It is a relatively complex moderated mediation model as well as an exploratory model. PLS-SEM has been widely used to evaluate complex models (Hair et al., 2018). It is a causal-predictive approach used to develop path models that empirically validate the antecedents that lead to an outcome (Richter et al., 2020). Necessary condition analysis (NCA) is a new data analysis technique that enables researchers to look beyond the structural relationships between constructs and identify the necessary conditions in datasets (Dul et al., 2020). Thus, this study used a variety of methods, including SPSS, PLS-SEM, the PROCESS macro, and NCA. Figure 3 illustrates our analytical process, serving as a sequential guide. The descriptive statistical analysis was performed using SPSS version 26.0 software, and hypothesis testing was performed using Smart PLS and the PROCESS macro software. This study used SPSS for preliminary analysis. The findings included the mean, SD, square root of AVE across the variables in the model, and correlation coefficients calculated using Pearson’s r values (r). These findings are consistent with and provide preliminary support for our proposed hypotheses (for details see Supplemental Appendix Table A3).

A visualization of a combination of analytical methods.

Common Method Bias

According to Chin et al. (2012), Liang et al. (2007), and Podsakoff et al. (2003), two methods were used in this study to lessen the likelihood of common method bias (CMB). First, a Harman single-factor test could be used to test CMB (Podsakoff & Organ, 1986). Five factors were identified by the results of this test, with the highest possible level of covariance explained by one factor being 46.57%, which was less than the 50% threshold, suggesting that CMB had no impact on the questionnaire. Second, this study employed an ad hoc unmeasured latent marker construct (ULMC) approach based on Smart PLS to test CMB (Chin et al., 2012; Liang et al., 2007). The results showed that the average substantively explained variance of the indicators was .851, while the average method-based variance was .035, as shown in Supplemental Appendix Table A4. The substantive variance to method variance ratio was roughly 24:1. These findings demonstrated that CMB had no impact on the questionnaire.

Measurement Model Evaluation

The PLS-SEM method involves two stages: the measurement model and the structural model. The measurement model is used to assess the quality of the measurement instruments used to measure the latent variables. The measurement model can be evaluated using a variety of criteria, including convergent validity, discriminant validity, and reliability (Hair et al., 2018). This study used Cronbach’s alpha (CA), factor loadings, composite reliability (CR), average variance extracted (AVE), and heterotrait–monotrait (HTMT) to test the reliability and validity of the constructs. Tables 1 and 2 show the results of the evaluation. According to these results, all of the indicators were valid in terms of convergent validity, discriminant validity, and internal consistency.

Results of Reliability and Validity.

Results of HTMT.

Structural Model Evaluation

The following criteria are used in this study for the structural model evaluation: coefficients of determination (R2), effect size f2, and predictive relevance Q2 (Hair et al., 2018). The results of R2 indicated a moderate acceptance. The results of f2 showed that political influence and financial pressure have a minor impact on PBB and university performance. The Q2 values for PBB and university performance for predictive relevance are .143 and .409, respectively. This means that for PBB, there is a small predictive relevance, while for university performance, there is a medium predictive relevance (Figure 4).

Structural model evaluation.

Hypotheses Testing

Testing of the Direct Effects

This study used PLS to test hypotheses 1 to 6. Table 3 shows the results of the direct and indirect hypotheses. Following Table 3, for H1, results showed a significant and positive relationship between political influence and PBB (β = 0.317, p < .001), thus supporting H1. The results of H2 also showed a significant and positive relationship between political influence and university performance (β = 0.126, p < .01), thus supporting H2 as well. The results of the third hypothesis revealed a significant and positive relationship between financial pressure and PBB (β = 0.259, p < .001), indicating that H3 is supported. The fourth hypothesis was established to examine the relationship between financial pressure and university performance (β = 0.133, p < .01), thus supporting H4. For H5, results showed a significant and positive relationship between PBB and university performance (β = 0.511, p < .001), indicating that H5 is supported. Thus, all the direct hypotheses are supported.

Results of Direct and Mediation Effects.

Note. Standardized estimating of 5,000 bootstrap sample.

*p < .05. **p < .01. ***p < .001.

Testing of the Mediation Effects

This study explored the indirect relationship between political influence, financial pressure, PBB, and university performance after testing the direct hypotheses. This study followed the steps of Rasoolimanesh et al. (2021) and employed the mediation analysis technique that Zhao et al. (2010) have described. Table 3 shows the results of the mediation effect. The results revealed that PBB positively mediates the relationships between political influence and university performance (β = 0.162, t = 4.424, p < .001) and PBB also positively mediates the associations between financial pressure and university performance (β = 0.132, t = 3.748, p < .001). Given that both the direct and indirect effects were significant, it was likely that the mediation effect was a complementary mediation. So, H6 was supported.

Testing of the Moderated Mediation Effects

This study chose PROCESS (version 3.5 model 14) to test H7. The PROCESS established a multiple regression model for SPSS. The results are summarized in Table 4. As shown in Table 4, the findings showed that political influence positively impacted on PBB (β = 0.234, t = 3.609, p < .001), and political influence also positively impact on university performance (β = 0.217, t = 5.038, p < .001). PBB is positively impacted by financial pressure (β = 0.339, t = 6.612, p < .001), and university performance is also positively impacted by financial pressure (β = 0.212, t = 5.370, p < .001). There is a positive significant association between PBB and university performance (β = 1.223, t = 8.705, p < .001). These results coincide with the previous direct and mediation hypothesis test. Additionally, the relationship between PBB and university performance was negatively moderated by top management support for the moderation effect (TMS × PBB, β = −0.237, t = −6.509, p < .001). Thus, the moderated mediation model is validated in Chinese public universities.

Results of the Moderated Mediation Effect.

Note. Model = 14 of Hayes’ PROCESS macro; Bootstrapping samples = 5,000; β = unstandardized regression coefficient; SE = standard error; LLCI = lower limit confidence intervals; ULCI = upper limit confidence intervals; SD = standard deviation; and M = Mean.

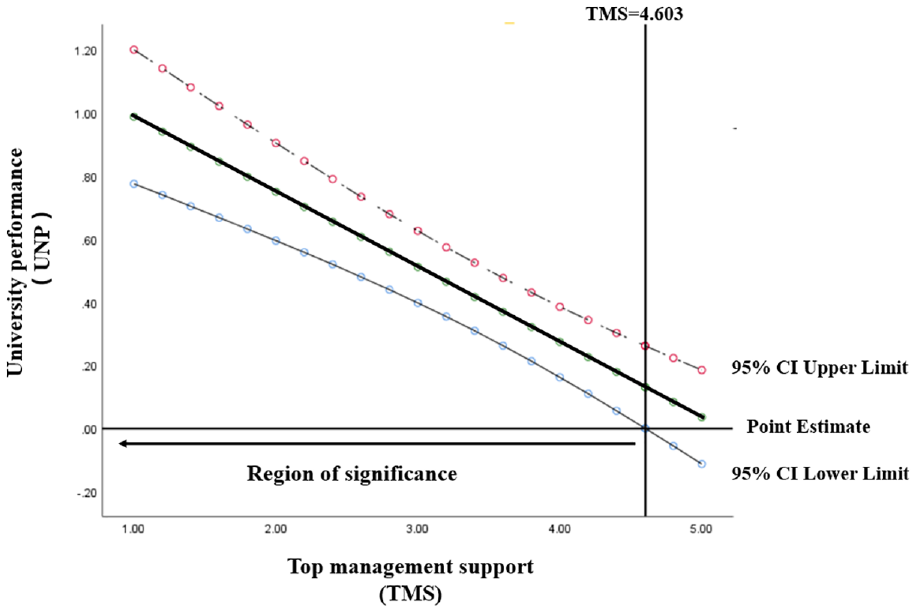

Additionally, this study implemented Finsaas and Goldstein’s (2021) recommendation in order to clearly explain the moderation effect. To determine the exact scope for moderation effect of top management support, it applied the Johnson-Neyman method. The Johnson-Neyman points were determined to be TMS = 4.603. When TMS was less than 4.603, there was a significant moderation effect. When TMS was greater than 4.603, there was no significant moderation effect. Figure 5 revealed the results of the Johnson-Neyman slope.

Moderation effect of TMS (Johnson–Neyman analysis).

Robustness Checks

According to Deb et al. (2022), researchers should do a robustness check in order to confirm the validity of the empirical model and research findings. In accordance with Hair et al. (2018, 2019) and Latan (2018), numerous complementary techniques have been put forth recently for the robustness check of PLS-SEM results. Followed by Hair et al. (2019) and Sarstedt et al. (2020), this study used confirmatory tetrad analysis (CTA-PLS) for the measurement model and nonlinear robustness check for the structural model. According to CTA-PLS results, our model is a reflective measurement model, and the nonlinear test results showed that the linear effects model was reliable (for details see Supplemental Appendix Tables A5, A6, and A7).

Additional Analysis—Necessary Condition Analysis (NCA)

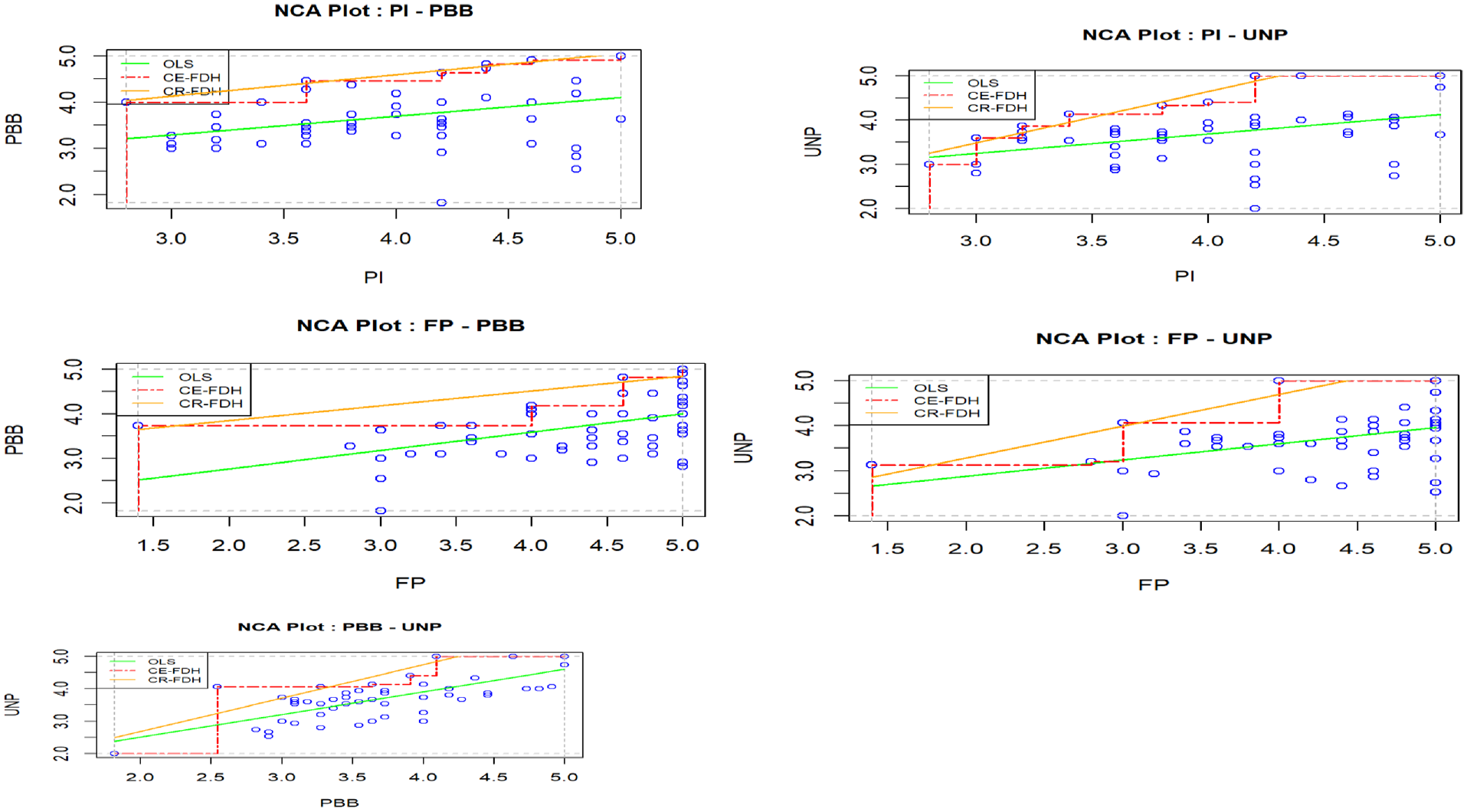

Necessary condition analysis (NCA) is used in this study to supplement the results of PLS. NCA is a novel data analysis method that identifies necessary conditions in sets of data (Dul, 2016). According to Richter et al. (2020, 2022), the aim of NCA is to identify the area pointing to the necessary conditions through the scatter plot, as opposed to the PLS, which is to analyze the causal relationship between variables, in order to determine whether the independent variable is a necessary condition for the dependent variable. After done the PLS analysis, this study examined whether political influence, financial pressure, and PBB were necessary conditions for university performance in accordance with the recommendations of Richter et al. (2020). R software was used to conduct the NCA analysis. Tables 5 and 6 as well as Figure 6 show the outcomes of the NCA analysis.

Analysis Results of Necessary Conditions for NCA (CE-FDH).

Note. 0 ≤ d < 0.1 means “low level”; 0.1 ≤ d < 0.3 means “medium level”; 0.3 ≤ d < 0.5 means “large level”; d ≥ 0.5 means “very large level”. p-Value represents the permutation test (permutation test, number of redraws = 10,000) in NCA analysis, the closer the p value is to 0, the more significant the impact.

p < .05; **p < .01; ***p < .001.

Bottleneck Table (in Percentages).

Note. CR-FDH bottleneck table and NN = not necessary.

NCA scatter plots.

Discussion

General Discussion

The objective of this study is to investigate the associations between political influence, financial pressure, PBB, and university performance in Chinese public universities. We created a moderated mediation model by combining two popular theories named contingency theory and RDT as our theoretical bases, and empirically tested the proposed hypotheses. The findings of this study are shown in Table 7.

Overview Findings of the Study.

These results led to the discovery of several intriguing findings. First, the findings demonstrated that political influence and financial pressure are required for PBB and university performance. PBB and university performance were both significantly influenced by political and financial pressure. The findings implied that in Chinese public universities, the implementation of a new system is inseparable from the support of policies and funds. Without these two items, the system will definitely not be implemented effectively. Second, in accordance with earlier studies by Pratolo et al. (2020) in Indonesia, our study demonstrated that political influence, financial pressure, and PBB are all necessary conditions, but PBB is the most crucial. Furthermore, PBB acted as a mediator between political influence, financial pressure, and university performance. The findings revealed the accuracy of our data. Meanwhile, this study also revealed that the moderated mediation model is validated in Chinese public universities. The impact of power cannot be ignored when implementing innovations.

Theoretical Contribution

The current study contributes to the body of knowledge in three ways. First, for influence factors, it adds a new contextual factor (financial pressure) to the previous theoretical model. When selecting the influencing factors, this study comprehensively considers politics, and economics in combination with Chinese unique national context. Based on the current situation, the economies of various countries have been greatly affected due to the pandemic, cascading its effects to universities with many international students (Bolton & Hubble, 2021). However, no study uses this variable to explain the adoption of PBB and its impact on university performance. By including financial pressure as a new variable, this study fills the knowledge gap in the management accounting area.

Second, for theoretical foundations, Carrillo et al. (2021) and Lu et al. (2015) recommended that the utilization of a unified theory has not been employed in prior research on PBB, with over 90% lacking a theoretical foundation. Meanwhile, de Vries et al. (2019) and Mauro et al. (2017) also stated that the development of PBB requires theoretical underpinning. In particular, this study seeks to respond to Mauro et al.’s (2017) call for more research in non-US countries and recommends integrating multiple subjects to encourage PBB execution. This study fills the knowledge gap by combining two related theories as its theoretical foundations. To further test the relationship between the chosen variables, this study developed a moderated mediation model based on the theoretical underpinnings, and the suggested model is validated in China. The findings are consistent with what is actually occurring in China.

Third, for data analysis, this study enriches the literature by using multimethod data analysis in accounting research. This study employed SPSS, PLS-SEM, PROCESS, and NCA. The multimethod is a recent development, which has yet to be explored in management research. According to Hauff et al. (2019) and Richter et al. (2020, 2022), NCA has gained considerable traction in this field, as demonstrated by its use in prior studies, and there need for more research that used this method. Meanwhile, as stated by Ghasemy et al. (2020) and Nitzl (2016, 2018), PLS remains a minority method in management research. Additionally, to extend the moderation analysis methodologies, this study used a novel data analysis technique to test the moderating effect, which is called the Johnson-Neyman technique.

Practical Implications

This study contributes to enhancing the efficiency of university funds by utilizing PBB, optimize resource allocation, and improving capital efficiency, which can improve the internal management and core competitiveness of universities. The study sheds light on the influence of contextual factors on PBB and university performance, which can serve as a useful reference for Chinese public universities. Moreover, the study offers practical guidance for institutions looking to implement PBB. By emphasizing the importance of result-oriented awareness in universities, the study can also provide ideas for applying PBB in universities and liberate them from the mundane tasks of daily reimbursements, allowing them to focus on other management tasks with greater efficiency.

Limitations and Further Research

Although this study contributes to the growing performance-based budgeting literature, it has sample limitations. Specifically, the sample under investigation was restricted to exclude participation from accounting academics, researchers, and senior executives within higher education institutions. Future research should consider stratifying the sample based on the administrative authority of universities. Additionally, future studies should conduct systematic literature reviews to understand why previous research on the relationship between PBB and university performance has yielded different or contradictory results. The reviews will provide a more comprehensive understanding of the subject and pave the way for more nuanced insights into the effectiveness of performance-based budgeting in higher education.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440241256637 – Supplemental material for How Political Influence and Financial Pressure Contribute to Performance-Based Budgeting and University Performance: Evidence fromSEM and NCA

Supplemental material, sj-docx-1-sgo-10.1177_21582440241256637 for How Political Influence and Financial Pressure Contribute to Performance-Based Budgeting and University Performance: Evidence fromSEM and NCA by He Liying and Zhang Mengying in SAGE Open

Footnotes

Acknowledgements

None.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

Ethical approval was obtained from the University Malaya Research Ethics Committee (UMREC). Reference Number is UM.TNC2/UMREC_1346.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.