Abstract

This research examines the influence of financial development on sustainable growth in 16 Asia-Pacific countries from 2000 to 2022. Employing advanced econometric techniques, such as multiple fixed effects and quantile regression, the research demonstrates a positive linkage between financial development and sustainability outcomes. Investments in education, research and development (R&D), and government expenditure are also identified as key contributors promoting sustainable development. Robust tests and quantile regression are performed to further validate these results. Empirical results indicate that financial development exerts a more pronounced effect in countries with lower SDG scores. The findings suggest tailored policy recommendations, highlighting the need to balance short- and long-term financing strategies, encourage environmentally focused financing, and strengthen financial literacy initiatives to foster sustainable development.

Introduction

Financial development supports economic growth by directing resources to productive enterprises; however, its contribution to sustainable development—encompassing economic, social, and environmental dimensions—has not been fully studied, especially in the Asia-Pacific region. This region characterizes by rapid urbanization and including 13 of the 30 countries most vulnerable to climate change; therefore, it offers a critical context for assessing the role of financial institutions in advancing the United Nations’ Sustainable Development Goals (SDGs). Using quantile regression on data set of 16 Asia-Pacific countries from 2000 to 2022, this study provide insights on the effects of financial development on sustainability that are more relevant to the region’s unique challenges.

Notwithstanding recent economic expansion, the Asia-Pacific region has several obstacles in attaining sustainable development. Since 2000, 70% of worldwide natural catastrophes have transpired in the area, impacting 1.6 billion individuals. The United Nations Economic and Social Commission for Asia and the Pacific (2025) report indicates that the Asia-Pacific region is lagging in achieving the Sustainable Development Goals, with most goals stalled or not on track. This situation poses a challenge and a request for governments in Asia-Pacific countries to balance economic growth and sustainable development (World Economic Forum, 2018). This study diverges from prior research that concentrates on developed economies or isolated issues like carbon emissions (Tamazian et al., 2009) by investigating the influence of financial institutions and markets on economic stability, social equity, and environmental health in Asia-Pacific region, a region impacted by extensive urbanization, climate vulnerability, and inequitable access to finance.

The literature highlights the role of financial systems on facilitating economic progress and possesses the capacity to promote the Sustainable Development Goals (SDGs), such as diminishing inequality, enhancing governance, and safeguarding the environment (World Economic Forum, 2012). Financial development influences sustainability via three primary mechanisms. Primarily, effective capital allocation fosters innovation and infrastructure, hence facilitating economic growth. In the Asia-Pacific region, finance is pivotal in the transition from an export-driven to a domestic consumption-driven paradigm, supporting investment-led advancement (Xu, 2000; Gurley & Shaw, 1995). Second, access to credit enhances opportunities, alleviating poverty and inequality, as evidenced by the influence of microfinance on small enterprises in Indonesia (Demirgüç-Kunt & Levine, 2008). Third, adequate capital may facilitate ecologically sustainable projects, shown as the green bond market in Singapore. An robust financial system enhances productivity by fostering innovation and facilitating access to capital (Levine, 2005). Nonetheless, if unregulated, financial development may also facilitate toxic enterprises, as seen in certain regions of China (Jalil & Feridun, 2011). This study emphasizes the distinctive context of the region, characterized by recurrent natural catastrophes, densely populated metropolitan areas, and economic inequalities, distinguishing it from prior assessments in developed economies or on a worldwide scale.

While a growing body of research has explored the relationship between financial development and sustainable development, most of it has focused on advanced economies or on narrowly defined sustainability outcomes (environmental degradation or income inequality). Furthermore, existing findings remain fragmented and contradictory, with studies reporting both positive and negative impacts depending on countries with various stages of development, institutional quality, and financial structures. Some analyses highlight the benefits of financial development in promoting inclusive growth and green investment, such as finance fosters green innovation, shown by the funding of solar farms in Thailand (Lundgren, 2003). Meanwhile, others highlight risks such as financial instability or inefficient capital allocation (Stiglitz & Weiss, 1981). Specifically, Vo et al. (2023) find that financial development can increase income inequality in Asia-Pacific countries, especially where the regulatory framework is weak. Similarly, Zhang and Liang (2023) argue that uncontrolled financial expansion, coupled with unsustainable exploitation of natural resources, can undermine environmental goals. Nevertheless, obstacles such as competition for financing among small enterprises, undeveloped bond markets, and tight banking rules impede growth. The dependence on short-term bank credit in several Asia-Pacific nations poses further challenges for sustainable growth. Financial intermediaries frequently emphasize short-term loans and limit assistance for long-term initiatives, such as renewable energy or financial inclusion programs in rural regions. This potentially worsens environmental degradation and inequality. These contradictions in empirical results highlight the need for further empirical clarification, especially in the diverse economic contexts of Asia-Pacific countries. This study addresses these gaps by providing a more comprehensive and context-sensitive analysis.

Empirical research on the relationship between financial development and sustainable growth yields inconclusive results. Certain studies indicate that, whilst others demonstrate that financial development may bolster ecologically detrimental sectors, as observed in certain regions of China. In the Asia-Pacific region, nations like Malaysia are compelled to attain GDP development while confronting environmental issues. With the middle class projected to comprise two-thirds of the global population by 2030, the area must spend significantly on infrastructure and renewable technology.

This study examines the influence of financial development on sustainable development in 16 Asia-Pacific nations from 2000 to 2022. It aims to address the question of how financial institutions foster sustainability in a fast-developing region that confronts substantial climate risks. The study used quantile regression, bivariate clustering, and fixed effects to evaluate the disparities in fiscal impact between nations with high and poor Sustainable Development Goal (SDG) development, exemplified by Japan and Laos. The research advocates measures tailored to regional requirements, including enhancing financial education in rural regions and broadening green bond markets to foster sustainable growth.

This study presents several advantages. It first offers sophisticated statistics on how finances might aid a nation with social inequality, urbanization, and environmental degradation. Second, it attains noteworthy results by integrating various financial data using advanced econometric methods. Third, it offers practical advice on several topics, including the diversification of financial markets and support for small enterprises. The research enables policymakers to implement budgetary strategies that promote equitable, sustainable development by addressing these issues.

The paper is structured as follows. Studies on financial growth and sustainability are the subject of Section “Literature review and hypotheses development.” The methodology is delineated in Section “Methodology and data,” which employs data from 16 Asia-Pacific nations. Empirical data is presented in Section “Research Results and Discussion,” and Section “Conclusion and Policy Implications” concludes with policy recommendations.

Literature Review and Hypotheses Development

Understanding the relationship between financial development and sustainable development has become an increasingly important and urgent research topic at the national, regional, and global levels. Sustainable development, as enshrined in the United Nations 2030 Agenda, aims to eradicate poverty, protect the environment, and promote inclusive prosperity across all member states. Achieving these goals requires efficient mobilization and allocation of financial resources to support economic growth, reduce inequality, and promote environmental sustainability.

This study adopts a multidimensional perspective in the concept of financial development, incorporating both financial institutions (e.g., banking system) and financial markets (e.g., equity and bond markets), in line with the IMF Financial Development Index. We argue that financial development plays a key role in enhancing sustainable development outcomes by improving capital allocation, increasing access to finance for disadvantaged groups, and supporting the mobilization of green and socially responsible investments. These financial functions are linked to the three pillars of the Sustainable Development Goals (SDGs) of economic prosperity, social inclusion, and environmental protection. By highlighting these linkages, the study provides a more integrated understanding of how financial systems contribute to sustainable development across different development contexts.

Financial Development

Levine (2005) conceptualizes financial development as the enhancement of the financial system’s core functions, which encompass the mobilization of savings, the allocation of capital to viable investment opportunities, the oversight and management of investment risks, the diversification of risks, the facilitation of trade, and the provision of financial services.

Financial markets and financial institutions are the two primary parts of a financial system. Each part has a unique role in providing lenders, investors, and borrowers with a variety of financial services and facilities (Adnan, 2011). Even though commercial banks, the biggest category of financial institutions, are often seen as essential for addressing financial needs, the roles of non-commercial bank financial institutions, such as investment banks, mutual funds, insurance companies, and pension funds, are becoming more and more important in the modern world (Svirydzenka, 2016). In the meanwhile, financial markets—which comprise the stock and bond markets—are significant sectors of the economy in numerous nations, offering businesses and individuals ways to diversify their investments and raise capital. In general, the financial system monitors financial activities and facilitates the accumulation and mobilization of funds for both surplus and deficit families (Fase & Abma, 2003).

Financial development, according to Fase and Abma (2003), can assist in resolving the knowledge asymmetry between lenders and borrowers, leading to a more effective and fruitful deployment of funds. From this perspective, a more sophisticated financial system is seen to raise living standards and increase economic efficiency. Furthermore, there is another way in which finance influences society and the economy. For instance, Sahay et al. (2015) expand on this topic by emphasizing how financial expansion contributes to diversified risk, consequently increasing the capability of enterprises and households to withstand economic shocks.

Measuring financial development poses challenges due to the multifaceted roles of the financial system, which encompass the mobilization of savings, the facilitation of investments, the execution of transactions, the diversification of risks, and the oversight of financial activities. To conceptualize financial development, this study uses the framework put forth by Čihák et al. (2012) and World Bank (2019). It focuses on three main aspects: (1) the stability and depth of financial markets; (2) the accessibility of financial services and infrastructure; and (3) the effectiveness of financial service delivery at sustainable costs while guaranteeing long-term revenue stability.

Sustainable Development

The notion of sustainable development was solidified and expanded during the 2002 World Summit on Sustainable Development, building on its initial endorsement at the 1992 Earth Summit on Environment and Development. The United Nations emphasizes that all countries should work toward achieving the Sustainable Development Goals (SDGs) by 2030 to ensure development while preserving resources for future generations. The 17 Sustainable Development Goals (SDGs) aim to address a number of global issues, including reduce poverty and hunger, improve health and well-being, ensure access to high-quality education, support gender equality, provide clean water and sanitation, make energy accessible and sustainable, support decent work and economic growth, foster innovation and infrastructure, reduce inequality, build sustainable infrastructure, encourage responsible consumption and production, prevent climate change, protect marine and terrestrial ecosystems, and strengthen governance and institutions (Nilsson et al., 2016; Sachs et al., 2019).

Three aspects of sustainable development are identified in the literature: the environmental, social, and economic aspects (Strezov et al., 2017). Sustainable economic growth aims to achieve wealth and economic stability without diminishing natural resources or having detrimental long-term consequences (Rashed & Shah, 2003). A sustainable society enhances community participation, guaranteeing that everyone has access to education, healthcare, and employment opportunities within a stable and equitable society. Sustainable environmental practices focus on protecting and conserving the environment for the future, including minimizing pollution, preserving biodiversity, and using natural resources efficiently.

Financial Development and Sustainable Development

Financial Development and Economic Achievement

First, the relationship between financial development and economic growth plays a significant role and has attracted the interest of many researchers (Levine, 1997; Mallick, 2014). One of the first scholars to mention the role of finance as a driver of economic development is Schumpeter and Opie (1934); their perspective has since been validated by many researchers, such as Gurley and Shaw (1995), McKinnon (1973), and Shaw (1973).

Pioneering research has demonstrated that financial market development contributes favorably to economic growth by: (1) encouraging the accumulation of savings, (2) directing resources toward productive investments, (3) minimizing costs associated with information, transactions, and oversight, (4) spreading risks, and (5) supporting the exchange of goods and services. These mechanisms enhance the efficiency of resource distribution, accelerate the buildup of physical and human capital, and foster advancements in science and technology. Specifically, Schumpeter and Opie (1934) pointed out the financial market’s role in funding innovative and productive development, which in turn promotes economic progress. Patrik (1966) developed the idea of “supply leading” and “demand following” in financial market development. Financial institutions are responsible for transferring resources from outdated to modern sectors and directing funds toward profitable operations. This idea was endorsed by Gurley and Shaw (1995), who attributed that financial market development boosts economic growth by enabling savings to be used to finance effective investments. More recently, Xu (2000) discovered compelling evidence that financial development has a positive impact on growth, mostly through investment channels. Similarly, McKinnon (1973) and Shaw (1973)’s studies shown common financial regulations, such as: interest rate caps and reserve requirements have hindered investment decisions, particularly in emerging nations. They emphasized that financial liberalization, through removing interest rate caps, leads to increased borrowing, and more efficient capital allocation.

Nonetheless, a number of researchers have recently demonstrated the non-linear link between the growth and development of financial markets. Cecchetti and Kharroubi (2012) discovered that the development of the financial market becomes an obstacle to economic expansion when banks loan to the private sector surpasses 90% of GDP. Notably, the financial sector competes with the rest of the economy for resources (including financial resources and excellent human resources), hence its explosive expansion may be harmful to the whole economy. Using both national and sectoral data, Arcand et al. (2012) demonstrated that when the private credit to GDP ratio for high-income nations was above 110%, there was a negative correlation between growth and finance.

In addition, studies have shown the relationship between financial market and economic growth depends on the level of economic development. Based on data from 119 developed and developing countries, Deidda and Fattouh (2002) demonstrated that financial development positively affects economic growth in developed countries, but it is not a driver of growth in developing countries. Similarly, Rioja and Valev (2004) demonstrated that positive and statistically significant impact of financial development to growth in high-income countries, whereas this relationship is not statistically significant in low-income countries.

Additionally, Loayza and Ranciere (2006) found differing short-term and long-term impacts of financial market development to economic growth. Using data from 75 countries over the period 1960 to 2000, researchers found the positive and statistically significant long-term relationship between growth and financial development, whereas the short-term relationship is negative and statistically significant. To explain, researchers attributed the negative short-term impact could result from strong business cycle fluctuations and the heterogeneity among countries.

Research on financial market development and economic sustainability shows a non-linear relationship between two variables. On the one hand, some studies indicate that financial development positively impacts financial sustainability. For example, Denizer et al. (2000) argued that countries with well-developed financial sector have lower fluctuation in output, consumption, and investment growth. This suggests that the level of private credit can best explain economic fluctuation. Comparable results were found in studies by Aghion et al. (2005) and Beck et al. (2014). Aghion et al. (2005) developed a macroeconomic theoretical model showing that countries with underdeveloped financial markets tend to have low economic stability and growth rate. They pointed out that low financial development and the separation of savers from investors lead to shortages in the economy, causing it to converge around its sustainable growth trajectory in a cyclical manner. Conversely, in developed financial markets, economies tend to converge toward a stable growth path, where fluctuations are driven primarily by external shocks.

In addition, studies have shown that the relationship between financial markets and economic growth depends on the level of economic development. While classical theories emphasize the positive contributions of financial development to economic growth and resource allocation (Schumpeter & Opie, 1934; King & Levine, 1993), critical studies from the post-Keynesian and ecological economic literature highlight the potential downsides of overexpansion of the financial sector. For example, Cecchetti and Kharroubi (2012) argue that beyond a certain threshold, financial development can become a drag on economic growth, especially when the financial sector grows faster than the real economy and diverts resources, especially human capital, and credit, away from productive sectors. Similarly, Arcand et al. (2015) provide empirical evidence of a threshold effect in the finance-growth nexus. Using cross-country data, they find that when credit to the private sector exceeds 100% to 110% of GDP, the impact of private credit on economic growth turns significantly negative. These studies argue that excessive financialization can increase economic volatility (Beck et al., 2006, Denizer et al., 2000), encourage speculative lending, and exacerbate inequality.

Financial Development and Social Welfare

In terms of social dimensions, several studies have noted that financial development creates welfare and social care, tackles social injustice, boosts economic growth, and lowers poverty (Beck et al., 2007; Jalilian & Kirkpatrick, 2002; Jeanneney & Kpodar, 2011). The mechanism underlying the connection between social benefits and financial development may be identified by robust economic growth. Financial growth, according to Demirgüç-Kunt and Levine (2008), influences the economy, labor demand, and the accessibility and utilization of money by individuals. This immediately enhances opportunities for the poor and indirectly creates extra job possibilities during periods of heightened economic growth in a nation. Ng et al. (2020) argued that financial development facilitates social welfare activities in securing funding to address various social issues such as poverty, inequality, health care, and food insecurity. In other words, capital not only advances social concerns but also propels economic development (Alam et al., 2015).

Furthermore, financial development plays an essential role in addressing social problems such as poverty and inequality by expanding access to financial services for vulnerable populations (Chung & Lin, 2023). When disadvantaged groups gain access to credit and other financial services, their incomes are likely to improve, thereby improving their living conditions and reducing poverty (Jalilian & Kirkpatrick, 2002). Empirical evidence from developing economies shows that improved access to credit helps households increase their investment in education, health care, and productive assets, contributing to sustainable welfare (Demirgüç-Kunt & Klapper, 2013). One of the ways that financial development supports this process is through reducing information asymmetries. Tools such as credit scoring, financial disclosure requirements, and digital finance platforms help banks and financial markets more accurately assess borrower risk, thereby allocating capital more efficiently, especially to small and medium-sized enterprises and underserved groups (Beck et al., 2007). In addition, the equitable allocation of financial resources for science and technological development in areas such as health, transportation, and telecommunications is also an effective way to narrow the social gap.

Financial Development and Environmental Performance

Technological advancement and financial assistance are seen as two essential factors in tackling environmental sustainability challenges (Kumbaroğlu et al., 2008). Facilitated access to funding enables enterprises to concentrate on R&D (Switzer, 1984), which pertains to innovative solutions for environmental challenges. The financial sector, as noted by Tadesse (2005), is crucial for its function in promoting risk dispersion and capital accumulation. Financial development promotes technical improvement and innovation in the green sector, thereby mitigating pollution. Specifically, financial development facilitates the global adoption of new technologies in many activities, including green technology in sustainable materials (Abbasi & Riaz 2016; Charfeddine & Khediri 2016; Shahbaz et al., 2016). The extensive accessibility of low-cost funds has facilitated the funding of ecologically sustainable initiatives, as noted by Tamazian et al. (2009). Additionally, researchers have empirically examined the connection between environmental sustainability and financial progress. Their findings have demonstrated that financial development affects environmental quality in a number of nations, including BRIC nations (Tamazian et al., 2009) and transnational economies (Tamazian & Rao, 2010). This suggests that a strong financial system encourages research and development, which is crucial in lowering environmental problems. Financial development makes it easier for businesses to obtain financing at reduced rates, allowing them to purchase pollution control machinery that is necessary for creating eco-friendly goods (Lundgreen, 2003).

However, technology is suspected of causing harm since the increased use of technological equipment leads to higher energy demand (Sadorsky, 2010). They found that inefficient energy use degrades the level of environmental quality in Pakistan. Yuxiang and Chen (2011) studied Chinese provinces between 1999 and 2006 and found that industrial SO2 emissions rose with R&D intensity, particularly for energy-intensive technology. According to their research, low-cost, simple access to financing speeds up the expansion of China’s capital-intensive businesses, which raises pollution emissions. According to Zhang’s (2011) empirical findings, there is a positive correlation between environmental deterioration and financial development in China. In their analysis of 23 European nations between 1990 and 2013, Al-Mulali et al. (2015a, b) found a similar outcome, concluding that funding non-environmental initiatives might make environmental issues worse.

Financial development provides enterprises and individuals with accessible capital at lower risk and lower borrowing costs. This encourages the purchasing and investment behavior of entities in society. More consumption and investment increase production supply, creating a risk of causing more negative impacts on the environment during production through higher energy consumption and increased emissions (Birdsall & Wheeler, 1993). For instance, energy consumption is necessary for economic activities like investment and consumption, which raises Europe’s electrical usage (Al-Mulali et al., 2015a, b). According to empirical data presented by Sehrawat et al. (2015), financing increases economic activity in India, which in turn raises CO2 emissions per capita.

An advanced financial system can render a nation more appealing to foreign direct investment (FDI). Increased foreign company presence can facilitate the introduction and implementation of low-carbon production techniques and procedures in host countries (Eskeland & Harrison, 2003), which will result in a reduction in CO2 emissions (Kumbaroğlu et al., 2008). Jalil and Feridun (2011) discovered that, in the case of China, financial development is essential to lowering environmental pollution.

The difference in the impact of banking system development compared to financial market development on sustainable development can be explained primarily by the structural characteristics and operating mechanisms of each financial channel. The banking system with an operating model based on credit relations and prioritizing risk management through collateral assets is often oriented towards short-term and medium-term credit. This can lead to a tendency toward “short-termism” when banks prioritize projects with quick payback and low risk, consequently limiting the financing of long-term sustainable projects such as renewable energy infrastructure or large-scale social development programs (Rajan & Zingales, 2003).

In contrast, financial markets based on stocks and bonds, with a key role through pricing mechanisms based on information and pressure from the investor community, are better able to support long-term investments. Market financial instruments such as green bonds and ESG-linked securities create incentives to align investors’ financial interests with sustainable development goals (Mathew & Sivaprasad, 2023). In addition, increasing transparency in information disclosure and investor pressure play a role in motivating organizations to develop sustainable investment strategies to improve their reputation and avoid legal risks (Dasgupta et al., 2001; Dasgupta et al, 2006; Fan et al., 2023). Therefore, considering these operational features, it becomes evident that each financial system exhibits distinct capacity and effectiveness in promoting sustainable development.

To summary, studies demonstrate that financial development promotes economic growth (Xu, 2000), reduces social inequalities (Beck et al., 2005), and has diverse environmental effects, capable of facilitating both sustainable investment and pollution-heavy growth (Tamazian et al., 2009; Yuxiang & Chen, 2011). Nonetheless, its comprehensive impact on sustainable development, including economic, social, and environmental aspects, is still inadequately examined. Based on the literature reviews, this paper proposes the following hypothesis:

Financial development arises from the growth of two key components: financial markets and financial institutions. As financial institutions and markets offer distinct mechanisms (Duisenberg, 2001), we expect both to positively influence sustainable development, with varying impacts.

Methodology and Data

Data

This research examines data from 16 Asia-Pacific countries, spanning the years 2000 to 2022. This area represents a range of economies with differing income levels, financial structures, and advancements toward the Sustainable Development Goals (SDGs). The data is retrieved from reliable sources, including the Sustainable Development Report (SDR), the International Financial Statistics (IFS), and the World Development Indicators (WDI). These sources were chosen as their consistent coverage and reliability in the fields of finance and sustainability research.

To measure the dependent variable, sustainable development, we utilize the SDG scores, which is sourced from the Sustainable Development Report (SDR). This index tracks annual progress on the 17 SDGs established by 193 UN Member States. These ratings provide a comprehensive instrument for cross-country comparisons on sustainability, taking into account economic, social, and environmental factors.

The IMF’s financial development index is employed to capture financial development. This index encompasses all facets of financial development (efficacy, productivity, and accessibility) in two components of financial structure, financial institutions, and financial markets. This index’s construction aligns with the framework for financial system features put forward by Svirydzenka (2016) and Čihák et al. (2012).

For other control variables, we include economic development, educational attainment, R&D spending, and government expenditure, which similar to existing literature (Li et al., 2024; Ng et al., 2020; Vo et al., 2023). Although some studies employ GDP per capita as a metric for economic development, this variable is frequently strongly correlated with financial development, as countries with higher GDP per capita tend to have higher levels of financial development. Thus, this study employs the economic growth rate as a control variable instead of GDP per capita to mitigate multicollinearity. Educational attainment reflects human capital’s role in sustainability, while R&D and government expenditure capture innovation and policy support, respectively (Table 1).

Variables Measurement.

To address the potential influence of outliers, the study applied winsorization at the 1st and 99th percentiles for all variables.

Econometric Methods

To analyze the impact of financial development on the sustainable development of Asian countries, the econometric model is proposed as follows:

Where:

The research adopts multiple fixed effects and a two-way clustering method to perform the analysis. Specifically, a country’s fixed effect is included to control for time-invariant unobservable characteristics, such as cultural or institutional factors. Meanwhile, the two-way clustering method, accounting for clustering by both country and year, are implemented to mitigate the potential biases arising from heteroscedasticity and autocorrelation in panel data (Peterson, 2008).

To ensure the robustness of research result, this study adopt two alternative measures, the Financial Institutions Index (FinII) and the Financial Markets Index (FinMI), to proxy for financial development. Besides, Prais-Winsten estimation method and the Newey-West procedure are utilized in the robustness check to further reinforce the validity of the results.

Potential endogeneity, such as reverse causality between financial development and SDG scores, is noted as a concern. However, due to data constraints limiting instrumental variable approaches, robustness checks, including alternative model specifications, are employed to ensure reliable findings.

Research Results and Discussion

Descriptive Statistical Analysis

Table 2 provides an overview of the descriptive statistics for the dataset analyzed in this study. During the period from 2000 to 2022, the Sustainable Development Goals (SDG) index for Asian countries averaged 66.314, with a standard deviation of 7.213. The index ranged from a low of 49.361 to a high of 78.804, illustrating considerable variation in sustainable development levels across the region.

Descriptive Statistics.

Source. Author’s calculations.

The Financial Development Index (FinDI) recorded an average score of 0.478 over the same period, with values spanning from 0.071 to 0.950 and a standard deviation of 0.264. This substantial range underscores significant disparities in financial development among nations. Countries such as Australia and Japan exhibited notably elevated levels of financial development, whereas others, including Laos, Cambodia, and Myanmar, were characterized by much lower scores.

A similar trend was observed for the Financial Institutions Index (FinII) and the Financial Markets Index (FinMI), where marked differences were evident across the region. Nations such as Japan, Australia, and South Korea emerged as regional leaders in both institutional and market financial development, reflecting robust and advanced financial systems. Conversely, countries like Laos, Cambodia, and Myanmar consistently ranked at the lower end of these measures.

The secondary school enrollment ratio (Human) for Asian countries during the study period averaged 85.127%, with the lowest recorded value at 24.696% and the highest at 153.576%. In terms of economic growth (GDP), the average annual growth rate was 4.748%, with a standard deviation of 3.642%. Thailand experienced the lowest growth rate (–6.067%) in 2020, while Myanmar achieved the highest growth rate (13.844%) in 2003.

Regarding research and development (R&D) expenditure, the countries in the sample allocated an average of 1.452% of GDP to R&D activities. South Korea stood out as the highest investor in R&D, while Brunei was at the opposite end of the spectrum. Government expenditure, measured as a percentage of GDP, also varied significantly, with an average of 13.791%, ranging from a minimum of 4.807% to a maximum of 26.223%.

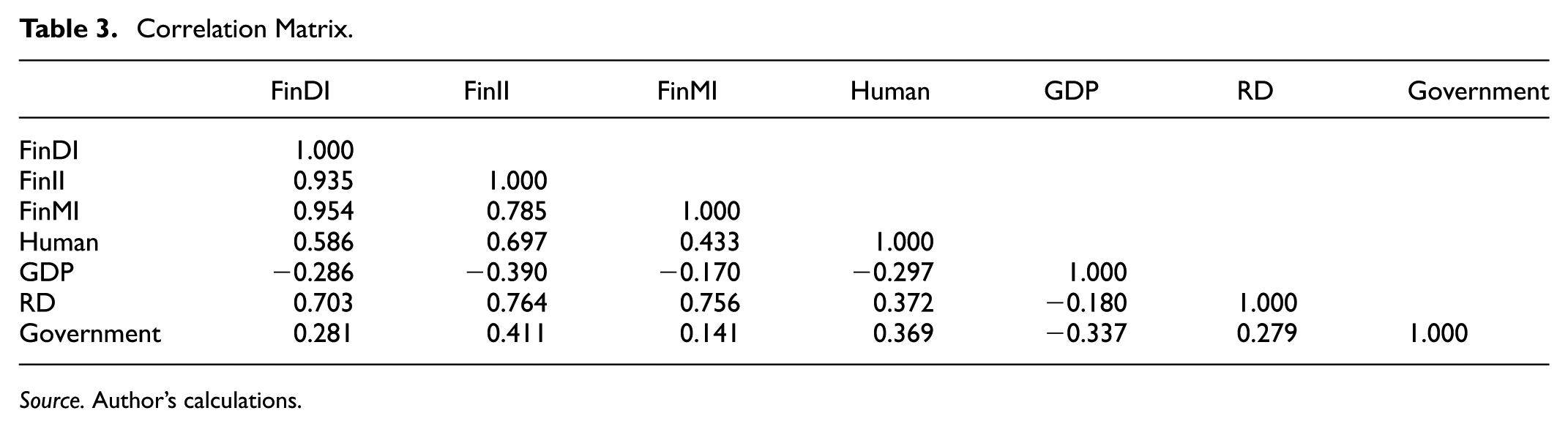

Table 3 shows the correlation coefficients among the independent variables. The findings indicate that these coefficients are below 80%, suggesting low correlations between the variables. This confirms the absence of multicollinearity, making the variables suitable for regression analysis (Judge et al., 1985; Hair et al., 2006).

Correlation Matrix.

Source. Author’s calculations.

The Im-Pesaran-Shin uni root test performed reveals that all variables are stationary at I(1), except for FinMI and GDP, which are stationary at I(0) (Appendix 2). The long-run relationship between the key variables, financial development, GDP growth, and sustainable development, was confirmed at the 5% significance level using Pedroni cointegration test (Appendix 3). However, due to missing data, a full cointegration tests for all control variables could not performed, which may constrain the generalizability of long-run inferences across all model components.

The Impact of Financial Development on Sustainable Development

Table 4 presents the regression results on the impact of financial development (FinDI) on sustainable development (SDG) in Asian countries. The baseline model (1) conducts a univariate regression between financial development (FinDI) and sustainable development (SDG) to test the direct relationship between these two variables. The main model (2) incorporates control variables into the regression to enhance the explanatory power of the research framework. These control variables include: (i) secondary school enrollment ratio (Human), (ii) GDP growth rate (GDP), (iii) research and development expenditure (RD), and (iv) government expenditure (Government).

Estimation Results.

Note: Table 4 presents the regression results on the impact of financial development (FinDI) on sustainable development (SDG) in Asian countries. The dataset was adjusted to exclude outliers at the 1% and 99% levels to minimize noise and ensure robust estimates. Coefficients are reported in their original unit. It represents the estimated change in the SDG score associated with a one unit increase in the corresponding explanatory, ceteris paribus. Adjusted standard errors are reported in parentheses. Symbols *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

Source. Author’s calculations.

Additionally, the study employs the Prais-Winsten regression method to address potential autocorrelation issues in model (3) and the Newey-West regression method to produce consistent estimates in the presence of autocorrelation and heteroscedasticity in model (4). Across all four models, the results consistently demonstrate the robustness and suitability of the research framework under different econometric approaches. Consequently, the research team opted to use the results from the main model (2) as the primary findings of the study.

Table 4 reveals that financial development, as measured by the Financial Development Index, exerts a positive and statistically significant influence on sustainable development. These results confirm our hypothesis and align with prior research (Alam et al., 2015; Ho & Njindan Lyke, 2007), which highlights the contribution of finance to advancing sustainability. This is consistent with Schumpeter’s (1961) theory of innovation, which posits that finance facilitates transformative investments, thereby assisting social initiatives and environmental projects. Notably, the quantile regressions show that the impact of financial development is more pronoun in countries with lower SDG quantiles. This finding implies that financial development serves as a catalyst for nations with low sustainability scores (like Cambodia and Laos).

The findings further indicate that human capital (as proxied by the secondary school enrollment rate) positively and significantly impacts sustainable development in Asian countries, with statistical significance at the 1% level. This finding is comparable to those of Barua (2021) and Payab et al (2023), implying that sustainable development outcomes are improved by higher-quality human capital. Workers who have received a higher level of education are more competent at utilizing sophisticated technologies and managing resources efficiently, which in turn improves the quality of production and productivity. Additionally, competent workers frequently demonstrate critical thinking skills and actively engage in the decision-making and problem-solving processes of their communities, such as issues of inequality or environmental degradation.

For economic growth (GDP), the results reveal a negative relationship with sustainable development. This implies that nations undergoing fast economic expansion may exhibit less efficacy in sustainable development. Neglecting concerns like income distribution, environmental preservation, and social equity in pursuit of GDP growth might lead to unsustainable development practices (Eisenmenger et al, 2020; Aldieri et al, 2022).

The study reveals a significant positive association between sustainable development and research and development expenditure in Asian countries. This conclusion aligns with Aldieri et al. (2022), which illustrates that augmented R&D investment enhances sustainable development outcomes. These technological developments possess the capacity to improve production efficiency, preserve resources, and reduce environmental repercussions. Thus, it contributes to the sustainable development of countries.

Similarly, the results highlight that government expenditure positively influences sustainable development in Asian countries. Government spending can be directed toward investments in sustainable infrastructure, such as eco-friendly transportation, renewable energy, wastewater treatment, and green technology (Osuji & Nwani, 2020). Investments in sustainable infrastructure yield long-term benefits for the environment and society, including reduced pollution, resource conservation, improved quality of life, and the promotion of sustainable economic growth.

Robustness Check and Quantile Regression Results

To ensure the robustness of the results, the study employs alternative proxies for financial development. Specifically, the Financial Institutions Index (FinII) and the Financial Markets Index (FinMI) are used as substitutes. The detailed robustness testing equations are as follows:

The study employs multiple fixed effects models, combined with the two-way clustering method, to perform Equations (2) and (3). The results of the analysis are presented in Table 5.

Alternative Measure of Financial Development Index.

Note: Table 5 displays the regression results regarding the influence of the financial institution index (FinII) and the financial market index (FinMI) on sustainable development (SDG) across Asian countries. The dataset is winsorized to eliminate outliers at the 1% and 99% thresholds, aiming to reduce noise and achieve reliable estimates. Standard errors that have been adjusted are presented within parentheses. Symbols *, **, and *** indicate levels of statistical significance at 10%, 5%, and 1%, respectively.

Source. Author’s calculations.

Table 5 displays the results examining the impact of the financial institution index (FinII) and the financial market index (FinMI) on sustainable development (SDG) across Asian countries (Model 2). This table serves as a robustness check for the main finding presented in Table 4, which aims to validate whether the observed relationship between financial development and SDG remains unchanged across different dimensions of the financial system. Both models demonstrate positive connections between sustainable development and the expansion of financial institutions and markets, with statistical significance at the 1% level. This implies that a well-developed financial system in an economy encourages savings and investments by both individuals and corporations, which in turn increases the national investment and savings rates. Consequently, they generate substantial funds for development projects and foster long-term, sustainable economic growth. Additionally, an effective financial system offers the requisite resources to facilitate economic expansion. Banks and other financial institutions may contribute to the creation of jobs, the increase in income, and the promotion of sustainable development in the nation by lending money, supporting infrastructure projects, and assisting companies in their operations.

The study results also reveal that financial institutions exert a greater influence on sustainable development than financial markets. In the Asia-Pacific region, where many nations’ financial system depends on bank loans, financial institutions are the main channel for supplying financing to small and medium-sized firms (SMEs). These firms, which account for over 98% of the number of enterprises, significantly contribute to poverty alleviation and employment generation, both crucial components of the Sustainable Development Goals (SDGs). Furthermore, financial markets, particularly bond markets, in the Asia-Pacific region, are in their infancy. This results in FinMI exerting a weaker influence on sustainable development, since financial markets currently lack the capacity to offer sufficient finance sources for sustainable initiatives like renewable energy or green infrastructure.

The researcher employs quantile regression to assess whether the impact of financial development on sustainable development differs across various levels of SDG scores. Traditional regression methods, such as ordinary least squares (OLS), typically rely on the mean value of the sample, with the assumption of a normal distribution of error term. However, when the sample shows heterogeneity or having outlier, relying on OLS might not yield the most accurate conclusions. In contrast, quantile regression allows for examining different points in the distribution of the data, providing a more nuanced understanding. Moreover, quantile regression does not assume that the errors are evenly distributed across all levels of sustainable development (Tables 6–8).

Quantile Regression Results.

Source. Author’s calculations.

p < 0.01. **p < 0.05. *p < 0.1.

Sub-Group Analysis.

Source. Author’s calculations.

Robust standard errors in parentheses.

p < .01. **p < .05. *p < 0.1.

Instrumental Variables Regression Result.

Source. Author’s calculations.

p < 0.01.

The quantile regression results reinforce the outcomes of the primary regression model, affirming a positive association between financial development and sustainable development. Specifically, the analysis reveals variations in the effect of financial development on sustainable development across different quantiles. Unlike traditional Ordinary Least Squares (OLS) regression, which estimates the average effect of the independent variable on the dependent variable, quantile regression allows for an examination of the relationship at different points in the conditional distribution of the outcome variable. As a result, it provides a more comprehensive and nuanced understanding of the heterogeneity in effects across the distribution, rather than focusing solely on the mean. Specifically, the impact of financial development on sustainable development is most pronounced in countries with SDG scores at the 50th percentile or below, and then gradually decreases as the SDG score increases. The highest impact (at the 50th percentile—12.9) is 2.8 times higher than the lowest impact (at the 90th percentile—4.5). This suggests that financial development helps Asian countries with lower SDG scores improve their sustainable development capacity more effectively than those with higher SDG scores. In summary, the results from quantile regression reaffirm the consistency of the study’s findings. Furthermore, the research demonstrates that financial development not only influences sustainable development at the average value but also has varying impacts at different quantiles of sustainable development. In countries with lower SDG scores, financial systems play a key role in improving capital allocation by directing credit and investment to underfunded sectors such as rural infrastructure, education, and health. This supports inclusive growth and poverty reduction. Furthermore, bank-dominated systems in these countries often have geographic, informational, and relationship proximity to borrowers, making the banking system more effective in reaching underserved communities and SMEs, thereby promoting financial inclusion. On the other hand, in countries with higher SDG performance, although financial development remains important, the marginal benefits may decline due to saturation effects or structural inefficiencies. These findings imply that policy interventions aimed at expanding access to finance and further developing financial markets may be significantly more effective in countries with lower SDG baseline outcomes (Figure 1). Therefore, financial sector reforms need to be tailored to each country’s specific development context to maximize the contribution of financial development to sustainable development.

Marginal effect of financial development on SDG across quantiles.

The subgroup analysis confirms the presence of heterogeneous effects across income levels. Specifically, the regression results reveal that financial development has a statistically significant and positive impact on sustainable development in low to medium income countries. In contrast, the effect is statistically insignificant in high-income countries. This finding suggests that financial development plays a more critical role in advancing sustainability outcomes in less developed economies, where financial access and resource allocation remain more constrained.

To address endogeneity concerns, we employ a two-stage least squares (2SLS) regression using the financial openness (Chinn-Ito index) and internet penetration as an instrument for financial development (FinDI). Chinn-Ito index (KAOPEN) captures cross-border capital account openness, a policy variable that strongly influences financial sector development, but is plausibly exogenous to domestic sustainable development outcomes (Chinn & Ito, 2006). Additionally, internet penetration (number of individuals using the internet as of % of population) is also used due to its empirically documented role in facilitating digital financial services and inclusion (Asongu & Nwachukwu, 2019; Haini & Pang, 2022). The underidentification test (Kleibergen–Paap LM statistic: 161.487 with p value <.05) confirms that the model is properly identified. The Cragg–Donald Wald F-statistic (286/753) exceeds the Stock–Yogo critical values at all maximal IV size thresholds. It indicates that the instrument is sufficiently strong. Hansen J Statistic p value is 0.8467, which is larger than 0.05, indicating that the instrumental variables used are valid. The coefficient on FinDI remains positive and statistically significant, confirming a robust positive impact of financial development on sustainable development after accounting for endogeneity. This finding reinforces the baseline results and highlights the importance of financial sector liberalization in advancing SDG performance across Asian economies.

To further validate the robustness of our results, we estimate the IV regression under alternative specifications. Specifically, we run the extended instrumental variables model both with and without two-way clustering at the country and year levels. In both cases, the result remains unchanged. Moreover, we estimate a fixed-effects instrumental variables model to account for time-invariant unobserved heterogeneity at the country level. The estimation method that differs assumes strict exogeneity of instruments within panel fixed-effects structure. The consistency across model specifications strengthens the credibility of causal inference. We also include additional control variables, including trade openness and institutional quality, as part of a robustness check (see Appendix 1). The results remain consistent, indicating that our main findings are not sensitive to the inclusion of these variables.

Conclusion and Policy Implications

The findings of this research establish that financial development significantly contributes to enhancing the attainment of national sustainable development objectives. Financial resources play a particularly key role in boosting and supporting businesses, governments in developing plans, strategies, and transformation projects aimed at stable development. These findings are further verified by robustness tests and quantile regression analyses. In addition to financial development, key variables such as investment in education, research and development, and government spending are also important for promoting sustainable growth.

This research advances the current body of knowledge in multiple ways. First, it offers an in-depth analysis of sustainable development by assessing the influence of financial development on its various dimensions, encompassing economic growth, social well-being, and environmental sustainability. Second, it utilizes advanced econometric methods, including multiple fixed effects models, two-way clustering, and quantile regression, to ensure the reliability and robustness of the results. Third, it proposes tailored policy recommendations for Asia-Pacific area to promote sustainable development across many economic contexts.

By bridging gaps in the literature, offering robust empirical evidence, and providing practical policy recommendations, this study advances the understanding of the financial development-sustainability nexus, particularly in the context of the Asia-Pacific region.

To stimulate the development of the financial market, several recommendations can be implemented as follows:

After three recent crises—the global financial crisis, the debt crisis, and the Covid-19 pandemic, one of the major risks that developing and emerging countries are currently facing is the tightening of external financial conditions, with rising financial costs and reducing international individual capital flows (Ocampo, 2022). Accordingly, in terms of recommendations for financial market development, countries need to develop the balance and the diversity between the banking system and the stock market, as well as formulate policies that encourage medium- and long-term credit structures to promote sustainable economic development. On the other hand, improving the quality of information disclosure and market transparency is essential. Besides, the stronger and more consistent effect of the financial institution index suggests that bank-based financial systems remain more effective in promoting sustainable development, especially in low- and middle-income countries. Therefore, targeted interventions such as improving SME access to credit, expanding branch networks in underserved areas, and supporting inclusive banking initiatives should be prioritized. Targeted measures such as simplified loan procedures, credit guarantees, and digital microfinance platforms can help bridge financing gaps for small businesses and stimulate local development. In addition, policymakers should encourage banks to integrate environmental, social, and governance (ESG) criteria into lending decisions, develop green credit products, and enhance climate-related financial disclosures. Such efforts can directly enhance the developmental role of financial institutions, particularly in mobilizing capital for clean energy, poverty reduction, and inclusive growth.

Second, on the demand side, implementing financial education programs enhances awareness and access to financial services for people, thereby aiming at sustainable development. The observed stronger impact of financial development in countries with lower SDG performance supports the prioritization of foundational policies such as financial education. Financial education is crucial in improving awareness and usage of formal financial services, particularly in vulnerable and underserved populations. These policies help amplify the benefits of financial development in settings where baseline sustainability performance is relatively weak. Countries need to build a systematic, diversified, and appropriate financial education system for different audiences, conduct annual evaluations of population’s financial literacy as a basis for designing suitable financial education programs. At the same time, financial education should be integrated into school curricula at various levels, enabling individuals to access financial knowledge foundation from a young age.

Third, diversifying sustainable financial resources and attracting the participation of businesses. For example, sustainable financial resources is still primarily green credit, while the issuance of green bonds remains limited. To attract greener financial resources and stimulate the private sector to participate in sustainable financial market, it is essential to establish a suitable sustainable financial mechanism to foster motivation and demand for green financial resources. Accordingly, several directions for implementation include: (1) promoting the development of green transition roadmaps for businesses for two directions: voluntarily and mandatorily (for certain industries with specific characteristics), (2) enhancing businesses’ ability to self-assess their environmental efficiency, (3) increasing requirements for transparency and information disclosure related to listed businesses’ environment, and (4) supporting the private sector in developing criteria for determining environmental quality in specific sectors and business industries. Besides, one possible policy tool is to create blended finance platforms that combine public and private capital, de-risking investments through partial guarantees or concessional co-financing. For example, Indonesia’s “SDG Indonesia One” program has proven effective in mobilizing private green finance. At the same time, governments can support companies in self-assessment by providing standardized ESG reporting templates, benchmarking tools, and ESG training and education programs, as has been done in pilot programs in Korea and Malaysia.

Policymakers also need to be aware of the potential negative impacts of excessive financial expansion. If not effectively managed, excessive financial sector growth can lead to misallocation of resources, encourage speculative activities and increase systemic risk, thereby compromising sustainable development goals. Therefore, policies to promote sustainable finance need to be accompanied by appropriate legal safeguards and oversight to ensure that financial development is consistent with realistic economic and social objectives.

While this study provides valuable insights into the relationship between financial development and sustainable development in the Asia-Pacific region, it also has certain limitations that should be acknowledged. First, the study primarily relies on macro-level data, which may not fully capture country-specific institutional and regulatory factors that influence financial development and sustainability outcomes. Future research could incorporate case studies or micro-level data to provide a more detailed analysis of how financial policies impact sustainable development at the firm or household level.

Second, although the study employs robust econometric techniques, including fixed effects, two-way clustering, and quantile regression, it does not fully account for potential endogeneity issues arising from bidirectional causality between financial development and sustainable development. Future studies could apply instrumental variable (IV) approaches or dynamic panel models (e.g., Generalized Method of Moments—GMM) to address this concern and enhance causal inference.

Third, while this research examines the overall impact of financial development on sustainable development, it does not delve deeply into specific financial instruments such as green bonds, impact investing, or sustainable banking. Future research could explore the effectiveness of different financial instruments and policies in promoting sustainable development, particularly in emerging markets.

Additionally, this study focuses on 16 Asia-Pacific countries, which, while diverse, may not fully represent global trends. Expanding the geographical scope to include Africa, Latin America, or the Middle East could provide comparative insights into how different financial structures and policy environments affect sustainability outcomes.

Finally, future research could explore the long-term effects of financial crises and external shocks (e.g., the COVID-19 pandemic, climate-related financial risks) on sustainable development. Understanding how financial resilience influences sustainability during crises would provide policymakers with critical insights into designing more adaptive and shock-resistant financial systems.

By addressing these limitations, future studies can further refine the understanding of how financial development interacts with sustainability goals, ultimately contributing to more effective financial policies and strategies for long-term sustainable growth.

Footnotes

Appendix

Pedroni Cointegration Test.

| Panel | Group | |

|---|---|---|

| V | −0.2312 | . |

| Rho | −0.962 | 1.094 |

| t-stat | −3.007 | −1.326 |

| Adf | −1.765 | −1.953 |

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author gratefully acknowledge the financial support from the Banking Academy of Vietnam

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

This study uses secondary data that are publicly available from https://databank.worldbank.org/source/world-development-indicators#; https://dashboards.sdgindex.org/ and ![]() .

.