Abstract

The intensification of carbon emissions poses a critical challenge to global ecological stability. This study employs panel quantile regression techniques alongside extensive preliminary diagnostics and robustness analyses to identify the principal determinants of consumption-based carbon emissions across 38 Organisation for Economic Cooperation and Development (OECD) members. Empirical findings reveal that demographic scale, economic output, international trade, and technological advancement significantly influence emission levels, lending support to both the trade-adjusted environmental Kuznets curve and the stochastic impacts by regression on population, affluence, and technology hypotheses. Furthermore, policy instruments such as environmental taxation and green finance play substantive roles in emission mitigation, with green finance demonstrating particular efficacy. This study makes a significant contribution to the current literature on ecological economics by shedding light on the pivotal factors of carbon emissions across various quantiles and cross-sections.

Introduction

Climate change is no longer a distant threat; rather, it is a present and escalating crisis, with carbon emissions at its core. Every year, the Earth’s atmosphere absorbs over 30 billion metric tons of carbon-dioxide (

The academic literature on carbon emissions has expanded considerably over the past three decades, providing valuable insights into the underlying mechanisms of environmental degradation. Ehrlich and Holdren (1971) first proposed the environmental effects of population, affluence, and technology (IPAT) hypothesis, which was later extended by Dietz and Rosa (1994) to the stochastic effects of regression on population, affluence and technology (STIRPAT) hypothesis. These hypotheses essentially capture the effects on the environment of human impact on the planet. Grossman and Krueger (1995) introduced the environmental Kuznets curve (EKC) hypothesis, proposing an inverted-U relationship between income and environmental damage. Antweiler et al. (2001) examined the environmental implications of international trade by identifying the scale, technology, and composition effects. Stern (2004) and Cole and Neumayer (2004) integrated technological efficiency and governance factors, thereby emphasizing their significance in decoupling emissions from growth. More recently, studies have incorporated institutional and financial variables, such as energy productivity, green finance and environmental taxation, into emissions models, recognizing the growing relevance of regulatory and market-based tools (Metcalf, 2018; Taghizadeh-Hesary & Yoshino, 2019; Zeqiraj et al., 2020). While these contributions have deepened our understanding of the causes of emissions, inconsistencies remain, particularly in how these factors interact across country contexts and emissions levels. This underscores the necessity for more sophisticated analyses that take into account the inherent complexities and variations in the data.

Understanding the determinants of carbon emissions is not merely an academic endeavor; it has become a political, economic, and moral imperative. The contemporary global landscape presents a paradox, meaning that countries must stimulate economic recovery and development while simultaneously reducing their environmental footprints (Edwards, 2021; Zhang et al., 2024). This challenge is amplified by the interdependencies of modern economies, where trade, investment, and energy systems are globally intertwined (Desha et al., 2010; Van de Graaf & Sovacool, 2020). At the same time, policies such as carbon taxes, subsidies for renewables, or trade-based environmental regulations are not universally effective and often face political resistance (Fan et al., 2021; Keohane & Raustiala, 2008). Therefore, the path forward lies in adopting data-driven frameworks that recognize heterogeneity across countries and emission levels, and in developing tailored policy responses that balance economic growth with environmental sustainability.

This paper aims to investigate the key drivers of the consumption-based carbon emissions. We envisage a threefold contribution. First, utilizing panel data for 38 OECD countries from 1994 to 2021, we conduct a comprehensive empirical analysis incorporating advanced econometric techniques. Recognizing the limitations of mean-based estimators in skewed distributions, we implement a panel quantile regression (PQR) approach to uncover the distributional effects of emissions drivers. The objective of this methodology is to offer a more granular perspective that supports the design of flexible, context-sensitive policies. The motivation stems from the urgent need to move beyond one-size-fits-all models and uncover the distributional realities of environmental drivers. Second, we extend the EKC and STIRPAT hypotheses to include international trade indicators and measures of energy efficiency, thereby capturing both domestic and global environmental impacts. Third, this paper simultaneously evaluates the effectiveness of environmental taxation and green finance, which are policy tools often studied in isolation, thus providing a more holistic view of carbon mitigation strategies.

The OECD members merit particular consideration. Given their status as both historically high emitters and industrial leaders, they shoulder a disproportionate responsibility for cumulative carbon emissions. Concurrently, these countries have also pioneered a plethora of regulatory, financial, and technological instruments intended to curtail emissions. The richness of their data, the maturity of their institutions, and the diversity of their policies all serve to position them as optimal candidates for the identification of both entrenched challenges and emerging best practices. Furthermore, the emissions trajectory of OECD countries exerts considerable influence on the realization of global climate objectives, particularly within the context of the Paris Agreement (Salman et al., 2022).

The findings of this paper carry relevance for a wide spectrum of stakeholders. For policymakers, the differentiated impacts of emission drivers across quantiles can inform better-targeted interventions, such as stricter regulations for high-emitting economies and incentive-based mechanisms for those closer to decoupling. Financial institutions and investors can leverage these insights to optimize the allocation of green capital and assess climate-related risks. Development agencies and civil society organizations can leverage this evidence to advocate for equitable climate action, ensuring that environmental strategies are aligned with socioeconomic priorities. In summary, the present study proposes a framework that links empirical rigor with practical relevance. This framework contributes to both scientific understanding and policymaking.

This study employs advanced panel econometric techniques to examine the determinants of carbon emissions. Following comprehensive preliminary diagnostics, we implement the panel quantile regression (PQR) methodology developed by Koenker and Bassett Jr (1978). This approach offers the distinct advantage of capturing heterogeneous effects of explanatory variables across different points in the conditional distribution of the dependent variable, rather than estimating average effects alone. Specifically, PQR enables the estimation of the marginal effects of covariates at various quantiles (e.g., lower, median, and upper) of the emissions distribution, thus providing a more nuanced understanding of the data structure. This technique is particularly well-suited for environmental data, which often exhibit non-normal distributions, skewness, and outliers. Moreover, the PQR framework controls for unobserved heterogeneity across countries, thereby accommodating time-varying structural differences in macroeconomic, demographic, and institutional conditions. To ensure the robustness of our empirical results, we supplement the PQR analysis with the generalized method of moments (GMM), which addresses endogeneity concerns and reinforces the validity of our findings.

The paper is organized as follows. Section 2 presents the theoretical framework. Section 3 details the data and empirical methodology. Section 4 discusses empirical findings, followed by concluding remarks in Section 5.

Theoretical Framework

This section constructs a theoretical model linking consumption-based carbon dioxide (

The theoretical mechanism based on STIRPAT and EKC clarifies how people, prosperity, and the technologies that power prosperity jointly write the carbon story. The population scales activity, that is, scale effect. Rising income initially intensifies resource throughout before structural upgrading and regulation bend the curve, that is, the composition and technique effects. Technology shifts emissions intensity across the distribution of outcomes (Dietz & Rosa, 1994; Grossman & Krueger, 1995; Stern, 2004). Within this scaffold, trade reweights sectoral composition, meaning that imports can embed foreign emissions while exports may reflect cleaner, efficiency-led specializations. Energy productivity captures the technique channel directly (Metcalf, 2018).

We extend STIRPAT by embedding explicit policy channels for environmental taxation and green finance. Taxes operate primarily through relative price effects that raise the user cost of carbon-intensive inputs, thereby improving energy productivity, reweighting sectoral composition toward cleaner activities, and moderating scale. Green finance lowers the cost of capital for low-carbon technologies and infrastructure, accelerating diffusion and shifting composition. Both instruments also act through embodied-trade channels by altering import and export bundles. This extended framework yields testable predictions: (i) direct negative effects of taxes and green finance on consumption-based emissions; (ii) indirect effects mediated by energy productivity; and (iii) complementary effects with larger elasticities in the upper tail of the emissions distribution.

Recent evidence across OECD economies converges on three points. First, green finance is not decorative capital, it measurably lowers emissions, especially when paired with innovation (Jin et al., 2023). Second, carbon pricing works, but coverage and price levels still lag what’s needed: an OECD systematic review of ex-post evaluations finds robust, economy-wide emission cuts from higher carbon taxes and Emission Trade Systems (ETS) prices (OECD, 2025b). Third, the drivers of OECD emissions are increasingly demand-side and structural. Updated OECD footprint accounts show most OECD countries remain net importers of embodied greenhouse gases, so trade composition, energy productivity, and sectoral mix shape consumption-based emissions even as territorial totals fall. Complementing these patterns, new OECD-wide studies report that well-designed environmental taxes reduce emissions over the long run, though effects are heterogeneous at low baseline emission levels, underscoring the importance of policy sequencing with innovation and renewable uptake (Murad et al., 2025). These findings justify our emphasis on green finance and innovation complementarities, credible and comprehensive carbon pricing, and demand-based diagnostics when interpreting OECD decarbonization trajectories. Taken together, our extended STIRPAT posits with plausible complementarities, for example, taxes that sharpen market signals and green finance that accelerates adoption.

As for methodological formulation, the general representation of STIRPAT model is as follows:

where I, P, A, and T stand for environmental impact, population size, affluence, and technology, respectively. θ denotes the constant term, β, γ, and ρ stand for the elasticity parameters of I with respect to P, A, and T.

When Equation (1) is rearranged in accordance with the objective of this paper, territory-based

Considering the aforementioned explanations, and dynamic nature of the empirical analysis with the cross-sections, we arrive at the Equation (2).

The relevant literature provides a priori information regarding the relationship among the variables. Within the EKC framework, early-stage industrialization and globalization typically result in increased energy consumption and emissions, suggesting a positive relationship between economic growth and carbon emissions (Zhang et al., 2023). Similarly, imports are expected to exhibit a positive elasticity, as they often include carbon-intensive goods consumed domestically (Hassan et al., 2022). Exports, by contrast, may yield a negative effect in some contexts, particularly when emission-intensive industries are offshored (Iqbal et al., 2021). Energy productivity is anticipated to exert a mitigating effect on emissions, as greater output is achieved with less energy input (Xie et al., 2021). Environmental taxation is theorized to induce behavioral changes among producers and consumers by increasing the cost of high-carbon activities, thereby encouraging cleaner alternatives (Rafique et al., 2022). Likewise, green finance mechanisms serve to alleviate capital constraints for renewable energy projects and sustainable innovations, thus promoting a structural shift toward lower emissions (Sun et al., 2022).

Data and Methodology

The Data

This study employs a panel data set comprising annual observations for 38 OECD members over the period 1994 to 2021. The selected countries are listed in the Appendix. The temporal scope is determined by the availability of consistent and reliable data, particularly for environmental taxation (available from 1994 onward) and green finance (available until 2021). All variables are sourced from the World Bank and OECD statistical databases, ensuring international comparability and data integrity.

The study incorporates a set of explanatory variables that are substantiated by both theoretical frameworks based on STIRPAT and EKC hypotheses, and empirical literature. We proxy the scale and affluence channels with population and gross domestic product, while the technique and composition channels are captured through energy productivity and trade structure, which jointly shape embodied emissions and sectoral mix (Patterson, 1996; Peters & Hertwich, 2008; York et al., 2003). Moreover, environmental taxes are a standard proxy for effective carbon pricing signals across energy and transport bases; green finance captures the cost-of-capital channel that accelerates diffusion of low-carbon technologies (Metcalf & Stock, 2023).

The population count (POP) is based on all residents, irrespective of their legal status or citizenship. The population estimates are typically derived from national population censuses. Gross domestic product (GDP) reflects the aggregate economic output, including the sum of value added by resident producers, product taxes, and subsidies. Exports (EX) and imports (IM) represent the total value of goods and services sold to or purchased from other countries, respectively. These variables capture the environmental consequences of global trade. Energy productivity (EP) is defined as the ratio of GDP to total energy consumption. It measures the economic efficiency of energy use and is a proxy for technological advancement and decoupling potential. Environmental taxes (ET) include taxes levied on products and activities that negatively impact the environment, such as taxes on vehicle fuels, emissions, and environmentally harmful products. Green finance (GF) captures public sector investments in energy-related research, development, demonstration, and deployment, reflecting the role of fiscal tools in supporting renewable energy transitions. All variables are transformed into natural logarithms to facilitate elasticity interpretation and mitigate heteroscedasticity.

Empirical Methodology

Figure 1 presents the estimation process applied in this empirical investigation.

Estimation process.

We begin with a series of diagnostic tests to evaluate the statistical properties of the data. The Doornik and Hansen (2008) test assesses multivariate normality based on skewness and kurtosis. Given the likelihood of non-normal data distributions in environmental and economic variables, this step helps justify the use of robust estimators. Next, we evaluate two essential features of the panel structure: cross-sectional dependence (CD) and slope coefficient heterogeneity (SCH). CD arises when unobserved shocks affect multiple countries simultaneously, while SCH indicates variation in regression slopes across cross-sections (Breitung, 2005). These issues, if unaddressed, may bias parameter estimates. The Pesaran (2021) CD test and Pesaran and Yamagata (2008) SCH test are employed to detect these properties.

To address the issue of non-stationarity in panel time series, we employ the cross-sectionally Augmented IPS (CIPS) test proposed by Pesaran (2007), which incorporates cross-sectional means and their lags to account for common factors across countries. This test is particularly suitable for panels with potential CD issue. To assess the existence of a long-run equilibrium relationship among the variables, we implement the Westerlund (2007) cointegration test. This approach employs an error correction framework and provides both group-mean and panel-level test statistics, allowing for heterogeneity across cross-sections.

Given the non-normality and possible heteroskedasticity in the dependent variable, this study adopts the panel quantile regression (PQR) approach, originally developed by Koenker and Bassett Jr (1978). This method allows for the estimation of conditional quantile functions rather than conditional means, capturing the effects of independent variables at different points of the carbon emissions distribution (e.g., low-emitting vs. high-emitting countries). Moreover, this approach is particularly well-suited for environmental data, which frequently exhibit skewed distributions and outliers (Koenker & Hallock, 2001).

The general quantile regression model is specified as:

To further validate the robustness of our results and address potential endogeneity concerns, we estimate a dynamic panel model using the generalized method of moments (GMM), as introduced by Hansen (1982). GMM controls for omitted variable bias, reverse causality, and unobserved heterogeneity. It also allows for autocorrelation and heteroskedasticity within panel units. The validity of the instruments used in GMM estimation is assessed through the Hansen J-test for over-identifying restrictions. A failure to reject the null hypothesis confirms that the instruments are valid and not correlated with the error term.

Empirical Findings

Preliminary Analysis

This subsection presents the results of diagnostic tests conducted to evaluate the distributional properties, cross-sectional dependence, and slope heterogeneity of the panel dataset. Table 1 reports the results of the Doornik and Hansen (2008) test for normality, which rejects the null hypothesis of multivariate normality at conventional significance levels for all variables except GDP. This confirms that the dataset does not conform to a normal distribution and justifies the use of quantile-based estimation techniques. The slope heterogeneity test developed by Pesaran and Yamagata (2008) indicates significant heterogeneity across countries, rejecting the null hypothesis of slope homogeneity at the 1% level. This suggests that the impact of explanatory variables on carbon emissions differs across countries and justifies the use of models that allow for parameter heterogeneity. Furthermore, the results of the cross-sectional dependence test proposed by Pesaran (2021) confirm statistically significant interdependencies among the OECD countries in the sample. The presence of CD suggests that common shocks or spillovers (e.g., trade or environmental agreements) affect multiple countries simultaneously, reinforcing the need for estimators that account for such dynamics.

Preliminary tests.

Note.***, **, and * represent a significance level of 1%, 5%, and 10%, respectively.

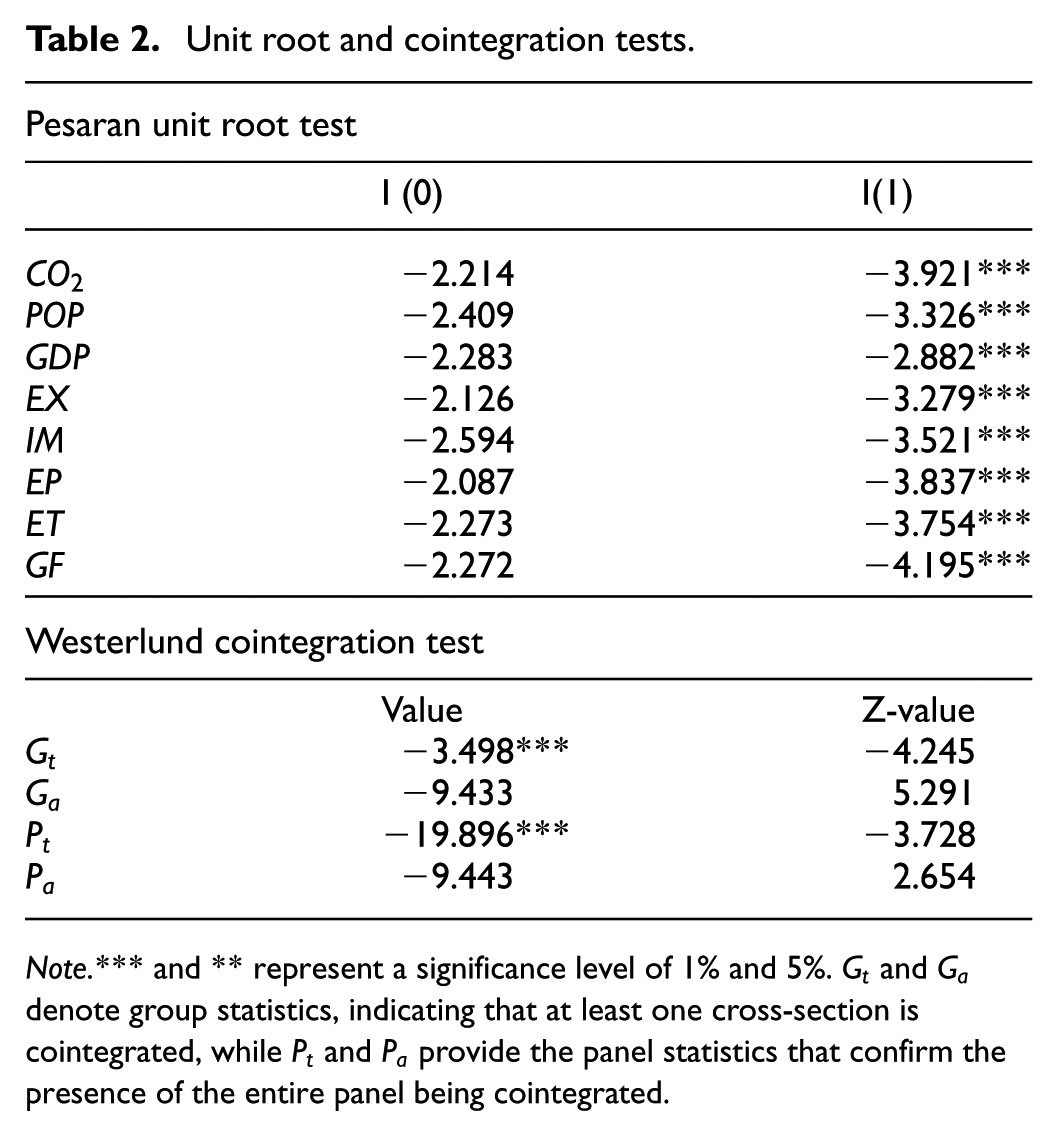

Unit-Root and Cointegration Tests

Table 2 presents the outcomes of the second-generation unit root test developed by Pesaran (2007), which accounts for cross-sectional dependence. The results reveal that all variables are integrated of order one, that is, non-stationary at levels but stationary at first differences. This necessitates cointegration testing to determine whether a stable long-term relationship exists among the variables. Using the Westerlund (2007) error correction-based panel cointegration test, we find robust evidence of long-run equilibrium relationships among the variables. Both group-mean and panel statistics are significant at the 1% level, thereby confirming cointegration. These results validate the estimation of long-run parameters via quantile regression and other cointegration-consistent methods.

Unit root and cointegration tests.

Note.*** and ** represent a significance level of 1% and 5%.

PQR Analysis

Table 3 reports the estimates from the panel quantile regression model, capturing the distributional heterogeneity in the determinants of consumption-based

QR estimation results.

Note.*** and ** represent a significance level of 1% and 5%, respectively. Standard errors are in parentheses.

The empirical results indicate that economic output and international trade exert statistically significant and consistent effects on carbon emissions across nearly all quantiles of the emissions distribution. These results are aligned with prior studies, such as Ali and Kirikkaleli (2022), and lend empirical support to the EKC hypothesis, which posits a non-linear relationship between income levels and environmental degradation. In lower-income countries, reduced emissions levels appear to be associated with lower consumption of final goods and services. In contrast, higher-income countries tend to display increased sensitivity to carbon-intensive consumption patterns. Emerging economies, often characterized by rapid industrialization and limited environmental regulations, exhibit elevated emissions levels due to their developmental trajectory and lower responsiveness to carbon externalities. Furthermore, the findings suggest that increased imports of energy and goods tend to elevate domestic carbon emissions, particularly in countries with limited clean energy infrastructure. By contrast, advanced economies demonstrate some emissions mitigation through the offshoring of energy-intensive production to other countries. Technological advancements and shifts toward carbon-neutral products also play a critical role in reducing emissions. Thus, the promotion of exports from carbon-intensive sectors and the adoption of low-carbon technologies are key strategies for enhancing environmental sustainability.

Table 3 provides further evidence of the effectiveness of emissions mitigation strategies, particularly environmental taxation and green finance mechanisms. The analysis reveals that both instruments significantly contribute to emissions reduction across all quantiles of the distribution, although green finance appears to yield greater marginal impacts. The efficacy of environmental taxation varies across the emissions spectrum. At lower emission levels, the deterrent effect of carbon taxes is relatively limited. However, as both emissions and tax rates increase, the disincentive effect intensifies, imposing higher costs on carbon-intensive sectors and thereby promoting a shift toward cleaner alternatives. These findings are consistent with those of Chien et al. (2021), who underscore the importance of targeted fiscal instruments in environmental policy. Green finance, in particular, is found to be robustly significant across all quantiles, indicating its capacity to stimulate investment in low-carbon technologies and renewable energy infrastructure. As shown in Shen et al. (2021), such financial mechanisms not only reduce dependence on fossil fuels but also catalyze systemic shifts in energy production and consumption. By lowering the capital costs associated with green innovation, green finance serves as both an economic incentive and a regulatory complement to achieve long-term sustainability goals.

To ground our panel results, we sketch three representative trajectories. Sweden illustrates the price-and-innovate path. An early, broad-based carbon tax catalyzed sustained emissions decline in taxed sectors while preserving growth, a pattern consistent with the strong negative elasticities we find for environmental taxes at higher emission quantiles (Andersson, 2019). Poland exemplifies the coal-to-clean transition. A power system still anchored in hard coal is pivoting toward solar, offshore wind, and nuclear; in such upper-quantile, carbon-intensive settings, our estimates predict large payoffs to price signals and green-capital de-risking as abundant low-cost abatement is unlocked (IEA, 2022). Türkiye represents an emerging decarbonizer within the OECD. Explicit economy-wide carbon pricing remains limited, implying that improvements in energy productivity and targeted green-finance programs may currently carry more weight, precisely the channels our quantile results elevate at lower to median emission quantiles (OECD, 2025a). For contrast, Germany’s Energiewende shows how stable, credible policy packages can shift the composition and technique margins over time, aligning with the increasingly negative effects of energy-productivity proxies (Rechsteiner, 2021). These country portraits translate our econometrics into practice: where carbon intensity is high, price signals and green finance bite hardest; where the system is already cleaner, composition and efficiency do the heavy lifting.

Across the OECD, heterogeneity in energy mixes, industrial structures, and policy maturity helps explain the quantile patterns we uncover. Economies earlier in the decarbonization journey, typically with higher fossil shares and heavier manufacturing, sit in the upper tail of the emissions distribution, where environmental taxes and green finance exhibit stronger mitigation elasticities because marginal abatement options are plentiful and directed technical change is more easily unlocked (Aghion et al., 2016; Metcalf & Stock, 2023). By contrast, countries already specialized in services and cleaner generation tend to occupy lower quantiles, where energy productivity and sectoral composition adjustments dominate incremental progress (Stern, 2004; Van de Graaf & Sovacool, 2020). Trade exposures add a further layer: where exports are cleaner than imports, openness lowers domestic footprints; where imported intermediates are carbon-heavy, the opposite can obtain (Antweiler et al., 2001; Peters & Hertwich, 2008). Reading our coefficients through this lens clarifies the policy script: stronger carbon pricing with revenue recycling and targeted green-capital de-risking should be prioritized in coal- and industry-intensive settings, while advanced decarbonizers should double down on efficiency, electrification, and supply-chain standards to capture the remaining, thinner margin of abatement.

Robustness Checks

To validate the consistency and robustness of the quantile regression results, a dynamic panel estimation using the generalized method of moments (GMM) is conducted. Table 4 summarizes the findings. The GMM estimates confirm the direction and significance of the relationships observed in the PQR model. Population, output, and imports remain positively associated with carbon emissions, while exports, energy productivity, environmental taxes, and green finance maintain their negative effects. The GMM estimator effectively addresses potential endogeneity and autocorrelation issues and accounts for unobserved country-specific effects. Importantly, the Hansen J-test for over-identifying restrictions does not reject the null hypothesis, indicating that the instruments used in the GMM specification are valid and not correlated with the error term. This further supports the robustness of the findings and enhances the credibility of the policy implications derived from the model.

GMM estimation results.

Note. *** and ** represent a significance level of 1% and 5%, respectively. Robust standard errors are in parentheses.

Concluding Remarks

This study investigates the principal determinants of consumption-based carbon dioxide emissions within the context of 38 OECD members, covering the period 1994 to 2021. In contrast to the majority of prior research that focuses on production-based emissions, this paper emphasizes a consumption-based perspective, which more accurately reflects the environmental burden associated with domestic demand, regardless of the location of production. Drawing on a comprehensive empirical strategy, including PQR and robustness testing via the GMM, the analysis incorporates a broad set of variables grounded in the STIRPAT and EKC frameworks. These include population size, economic output, international trade flows, energy productivity, environmental taxation, and green finance.

The results indicate that population, output, and imports are positively associated with carbon emissions, highlighting their roles as amplifiers of environmental degradation. These relationships persist across the emissions distribution, suggesting that both low- and high-emitting countries experience similar pressures from economic and demographic drivers. In contrast, exports, energy productivity, environmental taxes, and green finance are shown to reduce emissions. Notably, green finance emerges as a particularly effective instrument, with a stronger and more consistent mitigating impact than environmental taxation.

The empirical results yielded several potential policy recommendations. First, to reduce the environmental footprint of population and output, national education systems should emphasize environmental awareness and promote carbon-conscious behavior among consumers and producers. Second, the substitution of the carbon-intensive industries with low-emission alternatives and fostering cleaner production technologies will be crucial in achieving long-term sustainability. Third, enhancing energy productivity through investments in energy-efficient technologies, process optimization, and renewable energy systems, such as solar and wind, can help decouple economic growth from emissions. Four, carbon taxes should be calibrated according to emission intensity, with differentiated rates that incentivize high-emitting sectors to adopt cleaner technologies. For instance, a 10% increase in environmental taxes could lead to a reduction of approximately 810 million metric tons of CO2 in OECD countries. Five, increased allocation of public energy budgets toward renewable investments can substantially reduce emissions. A 10% shift in public energy expenditures toward green initiatives could lower CO2 emissions by approximately 2.9 billion metric tons. Financial institutions also play a critical role by adjusting their risk assessments and capital allocation in favor of low-carbon investments. Last but not least, non-governmental organizations and advocacy groups must work to build public support for carbon taxation and sustainable finance mechanisms. Their role in raising awareness and shaping public discourse on environmental policy is essential to long-term climate action.

Specifically, we propose a two-track policy framework. For economies in the upper quantiles of the emissions distribution, characterized by high carbon intensity, establish a rising carbon-price floor consistent with the High-Level Commission on Carbon Prices, recycle at least half of revenues to households, and allocate the remainder to de-risking low-carbon investment through credit guarantees, first-loss facilities, and carbon contracts for difference for hard-to-abate sectors, thereby aligning price signals with lower financing costs. For economies in the lower quantiles with relatively cleaner systems, prioritize standards and system upgrades, such as zero-emission vehicle and building codes, accelerated grid expansion and permitting reform, and green public procurement, to deepen technique and composition gains already underway. Across all contexts, earmark a visible share of carbon revenues for place-based transition support and competitive clean-innovation grants, measures shown to strengthen public acceptance and dynamic efficiency.

Like most studies, this study has some limitations. Firstly, the scope is restricted to OECD countries and ends in 2021, owing to data availability constraints. Secondly, the use of a single-equation panel model also limits the ability to account for institutional, cultural, and political heterogeneity across countries. Future research should aim to incorporate longer time spans, expand the country sample to include non-OECD economies, and apply alternative econometric techniques, such as dynamic spatial models or panel vector autoregressions. Moreover, beyond GMM, the empirical findings can be expanded by using Common Correlated Effects estimators to soak up unobserved global shocks and policy cycles, and fixed-effects OLS with Driscoll–Kraay standard errors to guard against serial correlation, heteroskedasticity, and cross-sectional dependence. Additionally, micro-level and sectoral analyses would complement the present macro-level findings and allow for more granular policy recommendations. We are constrained by proxy quality, potential spatial spillovers, and the inability to observe firm- or household-level adjustments directly. Priority extensions include linking policy exposure to installation/firm emissions, matching green-bond and credit issuance to emitter balance sheets, and building consumption footprints by merging Household Budget Surveys with MRIO/ICIO tables.

Footnotes

Appendix

List of the countries.

| Australia | Greece | Norway |

|---|---|---|

| Austria | Hungary | Poland |

| Belgium | Iceland | Portugal |

| Canada | Ireland | Slovak Republic |

| Chile | Israel | Slovenia |

| Colombia | Italy | South Korea |

| Costa Rica | Japan | Spain |

| Czechia | Latvia | Sweden |

| Denmark | Lithuania | Switzerland |

| Estonia | Luxembourg | Türkiye |

| Finland | Mexico | United Kingdom |

| France | Netherlands | United States |

| Germany | New Zealand |

Ethical Considerations

This study uses publicly available data. Therefore, ethical approval is not required.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data are available upon request from the corresponding author.