Abstract

Quality education is fundamental for achieving sustainable development, yet its success is heavily dependent on the availability of resources. Financial sustainability plays a critical role in this context, as it ensures local governments have the necessary capacity to allocate and manage resources effectively. Therefore, this research has analysed how municipal financial sustainability and contextual conditions relate to the fulfilment of SDG 4 on quality education. To this end, the research draws on contingency theory, distinguishing between internal financial capacities and external socio-economic and institutional factors, and on institutional theory to capture the social, political and regulatory pressures under which municipalities operate. Our work indicates a nuanced relationship: while lower indebtedness supports higher educational outcomes, a higher average payment period (APP) is also associated with better results, highlighting the complex interplay between short-term liquidity and long-term financial burdens. Additionally, citizen income, current transfers, and the presence of social institutions positively affect educational quality, whereas higher tax burdens have a negative impact. Our results are aligned with contingency theory, demonstrating that financial conditions impact local government performance based on the alignment between internal resources and external pressures. Furthermore, the study supports institutional theory, emphasising how external socio-economic and regulatory pressures shape local government actions and influence educational outcomes. The findings offer practical insights for local governments by identifying the conditions under which financial and socio-institutional factors can foster progress toward SDG 4, while also contributing to the academic understanding of how fiscal dynamics affect sustainable development.

Plain Language Summary

Quality education is a cornerstone for achieving sustainable development, which is why Sustainable Development Goal (SDG) 4 on Quality Education in the 2030 Agenda serves as a pathway to accomplish the other 16 goals. Local governments, being closest to citizens, play a critical role in this process, although they face resource constraints that must be managed to maintain financial sustainability. This study analyses how the financial sustainability of municipalities, alongside other socio-economic and institutional factors, influences the achievement of SDG 4. The results indicate a nuanced relationship: while lower indebtedness supports higher educational outcomes, a higher average payment period (APP) is also associated with better results, highlighting the complex interplay between short-term liquidity and long-term financial burdens. Additionally, citizen income, current transfers, and the presence of social institutions positively affect educational quality, whereas higher tax burdens have a negative impact. These findings provide empirical evidence relevant for local policy design and academic research in sustainable development.

Introduction

The public sector plays a fundamental role in countries' economic development, whether by promoting innovation, providing necessary services to citizens, or ensuring social, environmental, and economic sustainability (Baa & Chattoraj, 2022; Bisogno et al., 2023). However, the financial soundness of public administrations is an essential requirement for sustaining these functions, meaning that situations of fiscal instability can compromise their capacity for action (Lopez-Hernandez et al., 2012; López Subires & Rodríguez Bolívar, 2017). In this regard, the 2008 financial crisis, which led to a marked deterioration in public accounts and a significant increase in debt, prompted the European Union to establish a stricter regulatory framework geared towards sustainable growth (European Union, 2012).

Spain was one of the countries most affected by this crisis, which led to the approval of the Organic Law on Budgetary Stability and Financial Sustainability in compliance with European requirements (Organic Law 2/2012). Local governments were particularly affected, with high levels of debt compromising the sustainability of public services (Lara-Rubio et al., 2017). Consequently, the new regulations introduced an explicit definition of financial sustainability, understood as the ability to finance present and future spending commitments within the limits established by law (Organic Law 2/2012). In line with contingency theory, the financial conditions of municipalities act as a critical internal factor that determines their ability to align their actions with external demands (Sajid et al., 2023), making financial sustainability crucial in enabling local governments to adapt and meet the expectations necessary to achieve quality public services.

The principle of financial sustainability was mainly implemented through the limitation of public debt and the payment period to suppliers (Organic Law 2/2012). Specifically, the spending rule was introduced, which restricts local authorities from incurring debt exceeding 110% of current settled or accrued income (Royal Legislative Decree 2/2004). Likewise, the average payment period (APP) to suppliers was consolidated as a key indicator in the economic and financial analysis of local governments, with a maximum limit of 30 days being established (Organic Law 2/2012; Rebollo, 2017). However, despite these reforms, local governments have shown mixed results, largely due to their different administrative traditions (Rodríguez Bolívar et al., 2021). Currently, debt levels in Spain, especially at the municipal level, remain among the highest in the European Union, posing risks to the continuity and quality of public services (Lara-Rubio et al., 2022; López Subires & Rodríguez Bolívar, 2017).

The financial sustainability of local governments is therefore an important factor in achieving the Sustainable Development Goals (SDGs), as it can compromise the provision of public services (Lara-Rubio et al., 2022). The SDGs, established in the United Nations 2030 Agenda in 2015, constitute a global framework for advancing towards balanced development in its three dimensions: economic, social and environmental (United Nations, 2015). Within this framework, local governments, due to their proximity to citizens, are in a privileged position to identify needs, establish partnerships and implement actions that contribute to the achievement of these goals (Benito et al., 2023; Sánchez de Madariaga et al., 2020;). Their responsibilities cover areas such as education, health, food security, urban mobility and waste management, making local authorities strategic actors in sustainable development (Bisogno et al., 2023; Guarini et al., 2022). As a result, many of the targets set out in the SDGs are relevant at the local level (Sánchez de Madariaga et al., 2020), and local governments must adapt their actions to the expectations and pressures of their environment. Institutional theory shows that these responsibilities are shaped by social, political and regulatory demands that encourage municipalities to adopt practices perceived as legitimate (Rana et al., 2022), which further underscores the relevance of examining how local conditions affect progress toward SDG 4.

Among the SDGs, Goal 4 on Quality Education stands out for its dual nature: it is both an aim in itself and a means to achieve the other goals (Unterhalter, 2019). Lack of education has a negative impact on social and economic indicators such as poverty, crime and economic growth (Arcaro, 2024). Conversely, quality education equips people with the knowledge, skills and values to integrate into society and contribute to collective progress (Baral, 2023). In Spain, local governments perform important functions in the field of education, such as maintaining schools, collaborating in the planning of education policies, monitoring compliance with compulsory schooling and even creating their own schools (Law 7/1985; Organic Law 3/2020; Royal Decree 2274/1993).

Although education constitutes a fundamental pillar for any society, Spain has experienced a significant increase in social inequalities, which has weakened the traditional role of education as a mechanism for social mobility (Soria Espín, 2022). The Spanish Government has acknowledged this situation and stressed the need to promote policies that ensure equal educational opportunities (Government of Spain, 2021), in a context where public investment in education has historically been below the international average (Hernando, 2025). However, the capacity of local governments to address these disparities is strongly conditioned by their financial situation (Lopez-Hernandez et al., 2012). Limited fiscal space can restrict their ability to maintain infrastructure, support vulnerable populations or invest in programmes that promote educational inclusion, factors that directly affect progress toward sustainable development (Homsy & Warner, 2015; Lopez-Hernandez et al., 2012; Navarro Arredondo, 2021). This scenario reinforces the relevance of analysing how the financial sustainability of local governments may influence progress towards SDG 4.

Recent literature has explored the interrelationships between financial sustainability and sustainable development from different perspectives: the influence of GDP on SDG financing (Ziolo et al., 2018), the impact of the implementation of the 2030 Agenda on fiscal sustainability (Benito et al., 2023), and the relationship between efficiency in public service delivery and achievements in the social dimension of development (Ríos et al., 2022). In a similar vein, the study by Bisogno et al. (2023) examines how budgetary balance, together with other economic and political variables, affects the implementation of the SDGs. Other factors also influence the capacity of local governments to implement the SDGs, such as institutional and management constraints (Bardal et al., 2021), the income level of the population and the resulting tax revenue (Lubell et al., 2009; Martínez-Córdoba et al., 2020), transfers from higher levels of government (Ferrera et al., 2022), and the quality of the built environment (Grum & Grum, 2020).

Despite the relevance of SDG 4 and the importance of local finances in its fulfilment, a significant knowledge gap remains. Existing studies have analysed the relationship between the economic situation and the general implementation of the 2030 Agenda or other SDGs (Benito et al., 2023; Ríos et al., 2022; Ziolo et al., 2018;; Bisogno et al., 2023), but research that specifically links financial indicators to the quality of education is still an unexplored field. Studies examining the relationship between economic resources and educational quality have focused mainly on the macroeconomic level, concluding that economic growth substantially improves education and that education, in turn, promotes economic growth (Kanval et al., 2024; Li et al., 2024; Odhiambo, 2021). However, these analyses do not consider the financial conditions of governments, which determine the capacity of local authorities to plan, fund and sustain education-related policies. Therefore, the objective of this study is to analyse the relationship between financial sustainability—operationalised through the level of indebtedness and the APP—and the degree of compliance with SDG 4 in Spanish municipalities. Complementarily, the effect of other explanatory variables will be examined, such as management capacity, citizens' income, the existence of social institutions, tax burden and current transfers received.

We believe that this research could be extremely relevant given the scarcity of studies in this field and the importance of achieving quality education. Through this work, we can contribute to the understanding of the importance of sustainable development, specifically SDG 4 on quality education. Furthermore, this study makes a dual contribution, both theoretical and practical. From a theoretical perspective, it advances the literature on sustainable development by providing empirical evidence on how municipal financial sustainability and local socioeconomic and institutional factors are associated with progress toward SDG 4, based on contingency and institutional theory. From a practical perspective, the findings offer useful insights for local and national policymakers by identifying which financial and contextual conditions support better educational outcomes, helping them design more effective strategies aligned with the 2030 Agenda.

Determinants of Quality Education

Achieving SDG 4 on Quality Education depends on a combination of financial, structural and social conditions that shape the capacity of local governments to act effectively in this area (Bisogno et al., 2023; Grum & Grum, 2020; Martínez-Córdoba et al., 2020). Understanding how these conditions interact requires considering not only the resources available to municipalities, but also the broader context in which they operate.

The analysis of these determinants can be understood through contingency theory, which argues that organisational performance depends on the fit between internal capabilities and the external environment in which public bodies operate (Fiirst and Beuren, 2021). In the case of local governments, previous research shows that their capacity to provide public services is conditioned by their financial situation (López-Hernández et al., 2012), the availability of administrative and human resources (Alonso-Morales, Sáez-Martín & Haro-de-Rosario, 2025) and the socio-economic context, determined by external factors such as citizen demands, income levels, tax capacity, or dependence on intergovernmental transfers (Farmer, 2022; Lubell et al., 2009; Martínez-Córdoba et al., 2020). These elements reflect the internal and external contingency factors highlighted in recent applications of the theory to the public sector, which emphasise that local performance varies according to the pressures, constraints and opportunities of the environment (Hadiyanti et al., 2024; Shonhadji & Maulidi, 2022).

In parallel, institutional theory highlights that public organisations operate under political, social and regulatory pressures that shape their behaviour and influence the adoption of practices aimed at reinforcing legitimacy and accountability (Greenwood & Hinings, 1996). Evidence shows that sound financial management and robust governance improve the credibility and stability of public organisations, which promotes more effective service delivery (Sajid et al., 2023; van Duuren et al., 2020), while local governments adjust their structures and processes in response to the expectations of citizens, regulators, and other stakeholders (Rana et al., 2022). Taken together, both theories offer a coherent framework for analysing the determinants of SDG 4 at the municipal level. Within this theoretical and empirical background, the following sections examine the main determinants considered in this study.

Financial Sustainability

Following the perspective of contingency theory, the literature has highlighted financial conditions as an essential element for the implementation of sustainability policies (Homsy & Warner, 2015; Zahran et al., 2008). The implementation of these policies requires financial, material and human resources, so the existence of fiscal deficits becomes a limiting factor (Navarro Arredondo, 2021). Consequently, the economic situation of municipalities acts as an internal constraint by directly affecting their capacity to provide public services, which significantly reduces their room for manoeuvre in contexts of financial difficulties (López-Hernández et al., 2012).

In this vein, Gutiérrez Ponce et al. (2018) demonstrate a strong link between budgetary stability and the sustainability of social welfare. Similarly, Ríos et al. (2022) emphasise the need for local governments to adopt policies consistent with the SDGs without losing sight of economic efficiency. Thus, maintaining balanced public finances is essential for advancing the 2030 Agenda (Benito et al., 2023). However, it has also been argued that, in situations of financial stress, it may be logical for governments to exceed their available resources in order to sustain essential services such as education (Zabalza, 2021).

To operationalise financial sustainability in this study, two indicators derived from the criteria of the regulatory framework have been selected: the average payment period (APP) and the level of indebtedness (Organic Law, 2/2012). Both have been used previously in the literature, albeit with different results. For example, Benito et al. (2023) incorporated both the APP and indebtedness as dependent variables, concluding that only the former showed a significant and negative relationship with SDG compliance. Ajili and Ayoub (2020), on the other hand, considered indebtedness as an independent variable, finding a negative and significant association with the population's quality of life.

Based on this background, the following hypothesis is proposed:

Personnel Expenditure Intensity

For an organisation to effectively fulfil its responsibilities, it is not enough to have sound finances; it is also essential to have adequate institutional capacity (Wang et al., 2012). Through contingency theory, personnel resources are a fundamental internal contingency, as local governments need sufficient human capacity to respond to changes and contingencies, adapt their internal management processes, meet citizens’ needs, obtain the necessary resources and define clear objectives (Satterthwaite, 2016; Wang et al., 2012). However, public administrations often face difficulties in investing in the recruitment and training of their staff, both of which are fundamental for the proper adoption and implementation of policies (McNab et al., 2003; Park & Matkin, 2021).

Several studies have shown that a lack of staff significantly limits the actions of local governments. For example, Bardal et al. (2021), through surveys and interviews with municipal officials in Norway, identified a shortage of resources and insufficient staff capacity as the main obstacles to progress on the 2030 Agenda. This problem is exacerbated in small municipalities, where one or two employees are responsible for planning, which often leads to replicating models from larger cities without adapting them to their local context.

Likewise, the literature shows mixed results on the relationship between staff capacity and sustainability. Wang et al. (2012) show that greater management capacity in US city governments has a positive effect on sustainability. In this line, the study of Alonso-Morales, Sáez-Martín & Haro-de-Rosario (2025) shows a positive relationship between human capital and social SDG. However, subsequent studies by Liao et al. (2019, 2020) indicate that the presence of staff dedicated to sustainability does not necessarily guarantee a greater number of actions aimed at social equity.

Based on this evidence, the following hypothesis emerges:

Socio-economic Environment

The socio-economic environment in which local governments operate has a decisive impact on their ability to implement SDG-oriented policies. Factors such as the population’s income level, tax revenues and transfers received from other levels of government shape the available resource framework and, at the same time, citizens’ expectations regarding the quality of public services (Farmer, 2022; Martínez-Córdoba et al., 2020).

Firstly, various studies have highlighted the importance of citizens' income levels in the efficiency of public service delivery. Higher income levels translate into larger local budgets, which in line with contingency theory, constitutes an external contextual factor that could facilitate investment in infrastructure and other areas (Hadiyanti et al., 2024; Martínez-Córdoba et al., 2020). Thus, having more resources increases the likelihood that an organisation will meet its objectives and generate prosperity for stakeholders (Mutiarani & Siswantoro, 2020). To achieve sustainable development, it is crucial to improve resource conditions through their full and efficient use (Zhao et al., 2021).

Likewise, a higher level of income not only increases the resources available within local governments, but also has direct implications on the educational opportunities of the population. It has been shown that some children may be conditioned in their decision to continue with post-compulsory education by economic constraints (Chevalier et al., 2013). At the same time, citizens with higher incomes tend to demand higher quality public services in line with their standard of living, which is aligned with institutional theory's premises, as it puts external social pressure on policymakers to manage more efficiently and improve the provision of such services (Martínez-Córdoba et al., 2020).

Empirical evidence confirms the existence of positive relationships between income and the achievement of the SDGs. Mutiarani and Siswantoro (2020) concluded that local own-source revenues improve SDG compliance. Martínez-Córdoba et al. (2020) found a significant effect between per capita household income and the achievement of SDG 6, while Puertas and Martí (2023) observed similar results for the SDGs as a whole, although limited to Italian municipalities.

Because local income levels shape both the resource base and the contextual pressures under which municipalities operate (Martínez-Córdoba et al., 2020), higher income may strengthen their ability to support educational outcomes. Taking the above into account, we propose the following hypothesis:

Based on the contingency theory, citizens’ income is a key external factor, as citizens' income translates into revenue for local governments through taxation, facilitating the alignment between internal capacities and external expectations (Hadiyanti et al., 2024). Collective goods sustained by tax collection are an essential pillar for the functioning of society, given that the revenue obtained is redistributed for the benefit of the population as a whole (Bird & Davis-Nozemack, 2018).

In this regard, an increase in the tax burden may encourage citizens to demand higher quality public services; however, it also carries the risk that local governments will manage these resources inefficiently or irresponsibly (Martínez-Córdoba et al., 2020). Following the premise of institutional theory, taxpayers can exert pressure to seek a balance between the tax burden they bear and the benefits they receive in return (Sajid et al., 2023), exerting social pressure on local authorities to improve efficiency and ensure collective well-being (Mutiarani & Siswantoro, 2020).

The literature has shown that a robust tax system contributes to sustainable development. Lubell et al. (2009) argue that higher per capita taxes can strengthen municipal planning and support sustainability. Some studies warn that when tax bases are small, local governments can enter a vicious circle in which limited fiscal capacity restricts their scope for action and hinders the adoption of innovative and sustainable policies (Homsy & Warner, 2015). In fact, without an effective tax system, it is unfeasible to finance essential services, including public education (Bird & Davis-Nozemack, 2018). The study by Gutiérrez Ponce et al. (2018) demonstrated this relationship empirically, specifically showing that an increase in tax pressure is associated with greater social advancement. However, Farmer (2022) found no significant relationship.

In view of the above, we propose the following hypothesis:

In relation with the above, municipal financing does not depend solely on its own tax revenues, but also on transfers from other levels of government, the origin of which influences spending policies and social responsibility (Gutiérrez Ponce et al., 2018). From the perspective of contingency theory, this situation reflects the dynamic relationship between internal resources and external pressures, where these transfers are crucial for covering current expenditure and ensuring the financial sufficiency of municipalities (Ferrera et al., 2022). These transfers can also encourage more sustainable behaviour on the part of municipalities by reducing uncertainty and reinforcing the credibility of their commitment to public policy guidelines and objectives (Farmer, 2022; Lubell et al., 2009).

In line with institutional theory standpoint, these financial dynamics also reflect broader social, political, and regulatory pressures. The transfers from central governments can act as a form of external legitimacy, reinforcing the credibility of local governments' policies and their alignment with national public policy goals (Farmer, 2022; Lubell et al., 2009). However, there is a risk that transfers will create dependence on central government, limiting local governments’ autonomy and ability to design their own policies (Wirt, 1985). From this perspective, having greater control over their own financial resources allows local governments to respond to citizens’ demands through public spending and, consequently, to offer a higher level of well-being through their services (Farmer, 2022). Likewise, having their own resources increases the flexibility of municipalities to implement initiatives aimed at fulfilling the 2030 Agenda (Mutiarani and Siswantoro, 2020).

The study by Gutiérrez Ponce et al. (2018) concludes that per capita transfers promote greater social sustainability. Similarly, Farmer (2022) showed that state support enables municipalities to undertake sustainability initiatives. Since transfers act simultaneously as an external contingency factor and as an institutional mechanism that shapes local governments’ incentives and their alignment with broader policy expectations, we propose the following hypothesis:

Social Institutions

Social equity is closely linked to the built environment, where organisations respond to pressure from their environments and adopt structures and practices that are considered legitimate and socially acceptable by other organisations in their field, following the premise of institutional theory (Pina et al., 2022). Therefore, social infrastructure is a fundamental component in ensuring that services are accessible to the entire population (Dempsey et al., 2011). In addition, high-quality social institutions improve the quality of life in urban environments and, as a result, contribute significantly to social sustainability (Grum & Grum, 2020). Similarly, following contingency theory, social institutions can be understood as a key contextual feature that determines the range of organisational responses available to support education, as a denser social infrastructure expands the resources and channels through which local governments can adapt to collaborative problem-solving (Alonso-Morales, Gil-García, Sáez-Martín & Caba-Pérez, 2025).

In this line, social institutions are crucial elements of the social and normative environment, shaping how local governments respond to community needs and expectations (Rana et al., 2022). These institutions not only address fundamental social needs but also promote cultural development and enhance the social value placed on education (Latham & Layton, 2019). Moreover, the efficient design and management of social infrastructure not only ensures the safety of the population but also strengthens intergenerational cohesion and promotes social stability (Grum & Grum, 2020). Although social infrastructure alone cannot solve problems such as social polarisation, the vulnerability of certain groups, or the exclusion of marginalised people, it is essential for effectively addressing these challenges (Klinenberg, 2018).

Taking as a reference the study by Grum and Grum (2020), which shows the direct relationship between social infrastructure and social sustainability, the following hypothesis is proposed:

Methodology

Model and Variables

To test the research hypotheses (H1–H6), a linear regression model was estimated using Ordinary Least Squares with heteroskedasticity-robust standard errors. Robust standard errors ensure consistent inference in the presence of heteroskedasticity, thereby strengthening the reliability of the hypothesis tests (Cameron & Miller, 2015). Statistical calculations were performed using STATA software version 15. The estimated model is defined by the following expression:

In this expression, α represents the constant term, βj the coefficients to be estimated, and µ the random error, which is assumed to be independent and identically distributed with mean zero.

Regarding the dependent variable, municipal educational quality is measured through the level of compliance with SDG 4, as reported in The SDGs in 100 Spanish Cities, published by the Spanish Network for Sustainable Development (SNSD) in 2020. In this report, which has already been validated and widely used in the literature (Alonso-Morales, Gil-García, Sáez-Martín & Caba-Pérez, 2025; Alonso-Morales, Sáez-Martín & Haro-de-Rosario, 2025; Bisogno et al., 2023), SDG 4 is calculated as the arithmetic mean of six indicators previously normalised on a 0–100 scale, where higher values indicate better performance (Sánchez de Madariaga et al., 2020). These indicators are related to the official SDG 4 targets, reflecting both access to education and educational attainment. Specifically, indicator 4.1 reflects the proportion of the population enrolled in higher education; 4.2, expenditure on education; 4.3, access to preschool education services; and indicators 4.4, 4.5, and 4.6 reflect the population with a maximum educational level in secondary, upper secondary and tertiary education, respectively (Sánchez de Madariaga et al., 2020). The use of these indicators allows the SDG 4 measure to capture municipal progress on the main components of the goal.

The explanatory variables include financial, socio-economic and institutional factors. Financial sustainability is measured by the average payment period to suppliers (APP), expressed in days and obtained from the Ministry of Finance, corresponding to the last published month of 2020, and indebtedness (IND), calculated as the ratio between consolidated outstanding debt and consolidated current revenue. Personnel expenditure intensity (PEI) is approximated by the ratio between expenditure on civil servants, contained in Article 12 of the expenditure budget, and the municipality's total budget. All data relating to budgets come from the 2020 municipal budgets of local councils.

Three variables are included in the socio-economic environment. Gross income (GI) represents the average gross income of the municipality in euros and is obtained from the National Statistics Institute. Tax burden (TAX) is measured as the ratio between the sum of revenue from direct taxes (chapter 1) and indirect taxes (chapter 2) and the population. Likewise, current transfers received (TRAN) are calculated as the ratio between chapter 4 of current transfer income and the total budget of the local council. Finally, social institutions (SIN) are collected through the ratio between the number of social institutions and the population of each municipality.

Sample

The analysis was carried out using a sample of Spanish local governments, given that they face significant difficulties in ensuring financial sustainability (Lara-Rubio et al., 2022). At the same time, local governments play an essential role in achieving sustainable development. In fact, the United Nations has emphasised that cities are key players in promoting sustainability and that their active involvement is essential to achieving the goals of the 2030 Agenda (United Nations, 2019). In this regard, it will not be possible to achieve these goals without the participation of municipalities, which justifies the choice of our study sample.

Specifically, the selected sample corresponds to the municipalities included in the SNSD report, that is, those with more than 80,000 inhabitants and provincial capitals (Sánchez de Madariaga et al., 2020). This group of municipalities represents approximately 50% of the Spanish population, according to data from the INE (2021). In addition, localities with larger populations tend to have more extensive resources, which favours the impact of sustainability analysis (Navarro-Galera et al., 2016).

Results and Discussion

Descriptive Analysis

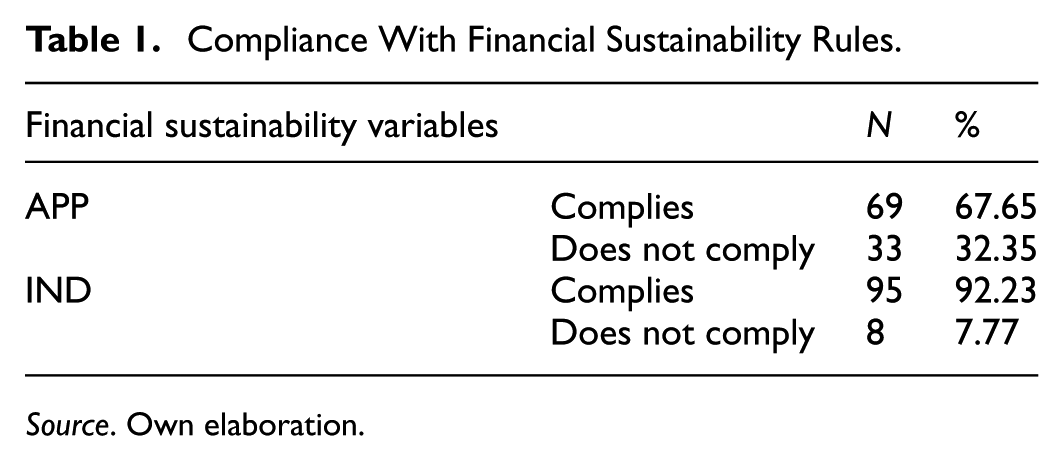

Before conducting the explanatory analysis, a descriptive analysis was carried out to examine the current situation of the municipalities. Table 1 shows the number of local councils that comply with or fail to comply with the financial sustainability rules. The results show that 95 municipalities comply with the maximum debt limit of 110%, compared to only 8 that exceed it. In contrast, compliance with the maximum 30-day APP is less favourable: 69 municipalities comply, while 33 do not. These data indicate that, although most municipalities maintain prudent management in terms of indebtedness, liquidity difficulties persist in a significant proportion of them, which is a cause for concern.

Compliance With Financial Sustainability Rules.

Source. Own elaboration.

Table 2 shows the results of the descriptive analysis of the variables. With regard to the dependent variable, compliance with SDG 4 of quality education is particularly problematic, as the average stands at 43.10%, that is, less than half the target, reaching minimum values in some municipalities. This situation compromises progress towards all sustainability goals, as SDG 4 constitutes a link between the economic, social and environmental dimensions of sustainable development by ensuring inclusive, equitable and quality education (Ferguson & Roofe, 2020).

Descriptive Statistics.

Source. Own elaboration.

With regard to the independent variables, the APP is noteworthy, with an average of 47.89 days, which is above the legal limit of 30 days. However, this result can be explained by the fact that, although most municipalities comply with the limit, those that do not exceed the established maximum by far, reaching up to 624.34 days in extreme cases. In contrast, the level of indebtedness has an average of 46.99%, significantly below the legal threshold, although the maximum value recorded (438.00%) shows that some municipalities far exceed this limit.

As for the remaining variables, local councils allocate an average of 17.18% of their budget to civil service personnel expenditure, with relatively low dispersion. The same is not true of gross income, which ranges from €18,904.00 to €82,188.00, with an average of €29,137.05, or of the tax burden, which averages €827.67 per inhabitant, but with notable differences between municipalities (standard deviation of €256.78 per inhabitant). In the case of social institutions, the average is 0.018%, which is equivalent to 1.8 institutions per 10,000 inhabitants, with values ranging from 0.002% to 0.061%. Finally, current transfers represent, on average, 29.60% of municipal budgets, although with considerable heterogeneity: in some municipalities they finance more than 60% of expenditure, while in others they barely reach 8%.

Empirical Analysis

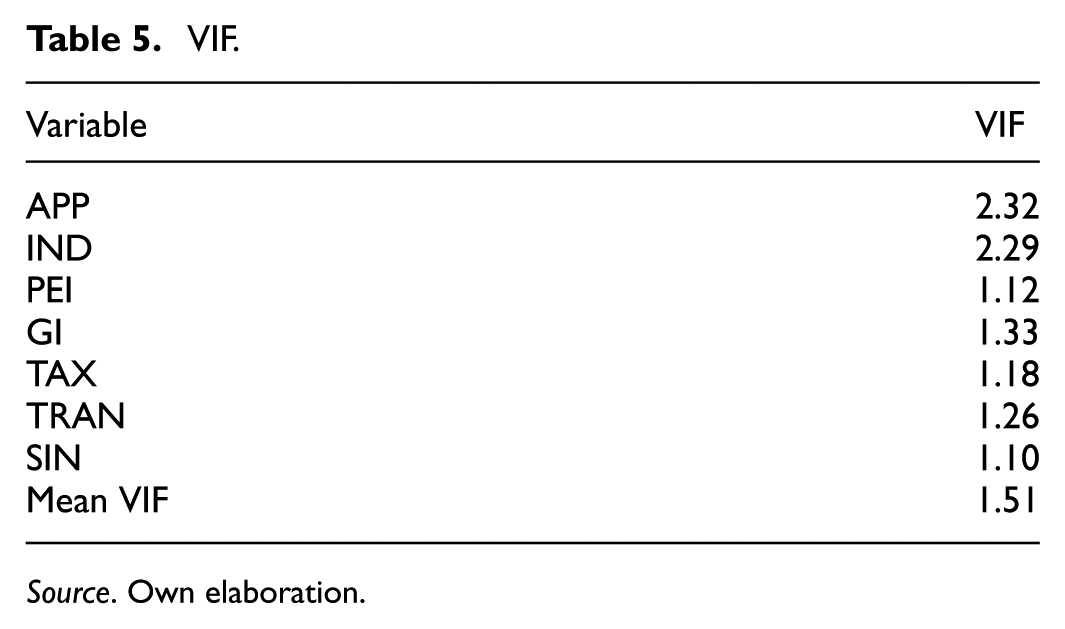

Before proceeding with the explanatory analysis, the absence of significant dependence between the independent variables was verified using Pearson's correlation matrix (Table 3). Although some significant correlations are observed, such as between the APP and indebtedness, they are all low, below 0.8. Therefore, according to Neter et al. (1996), these correlations do not suggest problems of multicollinearity and do not compromise the validity of the regression model. In addition, we calculated the Variance Inflation Factors (VIF) for all independent variables, which range from 1.10 to 1.43, further confirming that multicollinearity is not a concern as it is lower than the threshold of 10 (Wooldridge, 2016).

Correlations Between Independent Variables.

Significant correlation at the 0.10 level. **Significant correlation at the 0.05 level. ***Significant correlation at the 0.01 level.

Source. Own elaboration.

Next, explanatory analysis was performed using multiple linear regression, the results of which are shown in Table 4. The resulting model is statistically significant, indicating that it is capable of explaining how different factors are associated with quality education. Its linearity is also validated using Fisher’s F-test. Consequently, this model forms the core of the present study. It should be noted that most of the independent variables showed a significant association with the fulfilment of SDG 4, with the exception of personnel expenditure intensity, which did not reach statistical significance.

Determinants of Quality Education.

Source. Own elaboration.

Significant correlation at the 0.10 level. **Significant correlation at the 0.05 level. ***Significant correlation at the 0.01 level.

Although the aim of this study is to analyse whether financial sustainability influences quality education, it is also possible that educational outcomes influence local financial performance. To address this concern, we estimated a two-stage regression (2SLS) using the one-year lag of the key financial sustainability indicators (APP and indebtedness) as instruments, following previous sustainability research (Benito et al., 2023). As shown in Table 5, the 2SLS coefficients are almost identical to those obtained with robust OLS in both magnitude and statistical significance. In addition, potential endogeneity was formally assessed using the Wu–Hausman test, whose lack of significance indicates no evidence of endogeneity (Ullah et al., 2021). Therefore, consistent with Papies et al. (2017), when variables suspected of being endogenous are in fact exogenous, OLS remains the preferred estimator due to its greater efficiency.

VIF.

Source. Own elaboration.

To further assess the robustness of the findings, several additional analyses were conducted, including alternative bias corrections for the robust variance estimator (HC2 and HC3), resampling estimators (nonparametric bootstrap and jackknife), and penalised regression methods. In all cases, the results remained stable and consistent with the robust OLS regression, with the only exception being the tax burden variable, which already showed the lowest level of significance in the main model. Therefore, the significance of this variable should be interpreted with caution.

Once the robustness of our study has been confirmed, our results confirm the aim of this study where quality educational performance emerges from the interaction between internal capabilities and external socio-economic and institutional pressures, which is consistent with the central premises of contingency and institutional theory. By showing how these internal and external factors jointly shape progress toward SDG 4, the analysis directly addresses the research objective of identifying the determinants of educational quality at the local level and demonstrates the usefulness of combining contingency and institutional perspectives to understand the financial, socio-economic and institutional drivers of sustainable development in education.

From a contingency theory perspective, the results for the internal financial variables reveal a differentiated pattern between short-term liquidity pressures and long-term structural constraints. The APP shows a positive and statistically significant association with the achievement of SDG 4, which contradicts the initial hypothesis and suggests that longer payment periods are linked to better educational performance. This finding diverges from Benito et al. (2023), who argue that greater progress on the SDGs should be accompanied by shorter payment periods, but it can be interpreted as evidence that municipalities facing intense demands to expand or improve educational services may temporarily relax their payment discipline in order to reallocate resources to priority programmes (Zabalza, 2021). Under contingency theory, this behaviour reflects an attempt to adjust internal financial management to external educational pressures, accepting higher short-term liquidity stress to maintain or enhance the provision of quality education (Sajid et al., 2023; Zabalza, 2021).

In contrast, the level of indebtedness presents a negative and significant relationship with SDG 4, partially confirming the hypothesis and reinforcing the idea that structural financial burdens hinder the capacity of local governments to adapt effectively to their environment. Lower municipal indebtedness appears to favour the achievement of educational objectives, in line with Ajili and Ayoub (2020), who show that excessive debt can undermine quality of life. Unlike the APP, which captures temporary liquidity tensions, indebtedness reflects long-term commitments that absorb a substantial share of municipal resources and reduce the room for manoeuvre needed to respond to changing educational demands (Lopez-Hernandez et al., 2012; Organic Law, 2/2012). From a contingency standpoint, high debt levels weaken the fit between internal financial capabilities and the external requirement to advance towards SDG 4, thus explaining their negative association with educational performance (López-Hernández et al., 2012; Sajid et al., 2023).

Regarding personnel expenditure intensity, the results indicate that this internal resource does not play a decisive role in explaining progress towards SDG 4, leading to the rejection of the corresponding hypothesis. This result contrasts with contributions such as Wang et al. (2012) and Bardal et al. (2021), which stress the importance of adequate human resources for advancing sustainability policies and achieving the SDGs. However, it aligns with the evidence reported by Liao et al. (2019, 2020), who found that the mere presence of staff dedicated to sustainability does not necessarily translate into a greater number of actions aimed at social equity. Although investment in staff recruitment and training is essential for the effective implementation of public policies as an internal capacity (McNab et al., 2003; Park & Matkin, 2021), its actual influence on educational outcomes may be contingent upon other contextual factors, such as the availability of financial resources, community demands or the strength of the local social infrastructure (Ferrera et al., 2022; Grum & Grum, 2020; Mutiarani & Siswantoro, 2020). Future research should therefore consider alternative measures of personnel capacity that capture qualitative aspects, such as staff qualifications, technical expertise, or the presence of specific units dedicated to education, rather than relying solely on expenditure intensity.

Turning to the external variables, the positive association between average municipal gross income and SDG 4 confirms the proposed hypothesis and underscores the role of the socio-economic context as a key external contingency factor. Municipalities with higher income levels tend to achieve better educational outcomes, in line with Martínez-Córdoba et al. (2020), Mutiarani and Siswantoro (2020), and Puertas and Martí (2023) who document positive links between income, local own-source revenue and SDG performance. From a contingency perspective, higher income expands the resource base available to local governments and households, facilitating the alignment between internal capacities and external expectations regarding education (Hadiyanti et al., 2024; Martínez-Córdoba et al., 2020). At the same time, institutional theory helps to explain why richer contexts may generate stronger social pressures for quality education, as more affluent citizens typically demand higher standards in public services (Martínez-Córdoba et al., 2020).

The evidence for the tax burden points in the opposite direction. The negative and significant relationship between tax burden and SDG 4, contrary to expectations, suggests that higher levels of taxation are associated with worse educational performance. This finding does not coincide with Gutiérrez Ponce et al. (2018), who observed that higher tax burden was associated with greater social advancement, nor with Farmer (2022), who found no significant effects. As an external contingency factor, an excessive tax burden may restrict households’ disposable income and limit their ability to bear the costs of education (Terrell, 1986). From an institutional theory standpoint, high tax pressure can intensify tensions between local governments and citizens, eroding perceptions of fairness and legitimacy if taxpayers do not clearly perceive improvements in services (Sajid et al., 2023).

Current transfers received by municipalities exhibit a positive and significant association with SDG 4, thus supporting the corresponding hypothesis and highlighting their dual role as an external contingency factor and an institutional mechanism, consistent with the findings of Farmer (2022) and Gutiérrez Ponce et al. (2018). On the one hand, greater transfers expand the financial resources available to local governments and reduce uncertainty about funding for current expenditure, which facilitates the implementation of educational policies (Farmer, 2022; Ferrera et al., 2022). On the other hand, intergovernmental transfers can shape local spending policies and social responsibility, so through these channels, higher-level governments can exert pressures that encourage municipalities to align their actions with the SDGs, including SDG 4 ( Farmer, 2022; Gutiérrez Ponce et al., 2018).

Finally, the positive and significant relationship between social institutions and SDG 4 indicates that a higher density of social institutions is associated with better municipal educational performance. This finding is in line with the arguments of Grum and Grum (2020) regarding the importance of social infrastructure for social sustainability and community well-being. As an external contingency factor, these institutions contribute to the development of a quality built environment, which has a positive impact on people’s quality of life and promotes long-term sustainability (Grum and Grum, 2020). At the same time, institutional theory highlights that these organisations help shape the cultural environment in which local governments operate, articulating community expectations and strengthening the social value attached to education (Latham and Layton, 2019).

Conclusions

The 2030 Agenda is a global call to eradicate poverty, protect the environment and promote more just and peaceful societies (Adams, 2017). Its fulfilment requires the active involvement of all levels of government, particularly municipalities, due to their proximity to citizens and their ability to act directly on local needs (Benito et al., 2023; Sánchez de Madariaga et al., 2020). However, this work may be at risk if local governments do not have sufficient financial resources, as a fiscal deficit significantly reduces their scope for action (Navarro Arredondo, 2021). Therefore, this research has analysed how municipal financial sustainability and contextual conditions relate to the fulfilment of SDG 4 on quality education. To this end, the research draws on contingency theory, distinguishing between internal financial capacities and external socio-economic and institutional factors, and on institutional theory to capture the social, political and regulatory pressures under which municipalities operate.

The results show that there are currently marked inequalities in educational quality between municipalities, making it a priority to ensure equitable and quality education throughout the territory. In addition, many local councils still do not fully comply with the principles of financial sustainability, which highlights the need to make joint progress in both improving education systems and strengthening local financial management.

Furthermore, the results also show that the relationship between financial sustainability and education is more complex than expected. Based on contingency theory, these findings indicate that municipal performance in education depends on how different internal financial dimensions are combined to respond to external educational demands. Counterintuitively, a higher APP—which reflects short-term liquidity pressures—is associated with better performance on SDG 4. In contrast, lower indebtedness—an indicator of long-term sustainability—does favour educational attainment. This apparent contradiction can be explained by the nature of each variable: while debt structurally limits the ability of municipalities to allocate resources to educational and social policies, the APP may reflect a higher level of spending on services which, although it generates short-term payment delays, has a positive impact on education. These findings suggest that municipalities with high levels of indebtedness should prioritise long-term fiscal consolidation, whereas those experiencing short-term liquidity pressures may still advance educational outcomes if expenditure is strategically allocated. This multidimensional dynamic fits with contingency theory, whereby performance depends on how internal financial conditions align with external demands over different time horizons.

Beyond internal finances, the results confirm that external socio-economic and institutional conditions are decisive, in line with contingency theory. Municipalities with higher average income, more social institutions, higher current transfers received and lower tax burden tend to show better educational levels. At the same time, from an institutional theory perspective, these results indicate that citizen income, tax arrangements, transfers and social institutions operate as channels of political, social and regulatory pressures that shape local priorities and legitimise education as a central policy area, pushing municipalities to align their actions with the expectations of quality education. This underlines the importance of addressing quality education from a multidimensional perspective, where both the economic capacity of local councils and households and the way in which these resources are obtained have an influence.

Consequently, municipalities where citizens have lower income levels will need to make a deliberate effort to guarantee that their residents enjoy the same opportunities for quality education as those in wealthier territories. This involves designing and negotiating targeted transfer agreements with higher levels of government that explicitly prioritise investment in education, such as early childhood services or support programmes for disadvantaged students, while avoiding tax increases that could exacerbate inequality. In parallel, local governments should adopt prudent debt management strategies that protect fiscal sustainability but allow room for productive educational investment, and actively develop social infrastructure that reinforce community cohesion and provide accessible learning opportunities beyond the classroom, particularly in low-income municipalities.

Taken together, these results meet the objectives of the study by identifying which internal financial conditions and external socio-economic and institutional pressures most strongly influence the achievement of SDG 4 at the municipal level, thereby providing a theoretically grounded explanation of why some local governments are better positioned than others to advance quality education. In particular, we offer valuable information to local governments on the factors they should consider when implementing quality education in their respective territories, helping them to make more informed and effective decisions. Complementarily, this analysis may also be useful for central and regional governments, as it provides evidence on how they can support and guide local administrations to promote more sustainable practices consistent with the 2030 Agenda. Specifically, higher-level governments could provide financial support to municipalities with lower income levels or higher debt burdens through differentiated and compensatory funding schemes. They should also avoid reforms that increase local tax burden in economically vulnerable municipalities and reinforce local social infrastructure. Finally, a regulatory framework allowing greater flexibility to protect educational investment, even during periods of fiscal adjustment, would help safeguard progress toward SDG 4.

From an academic standpoint, the study contributes to the literature on sustainable development by providing empirical evidence that links municipal financial sustainability, socio-economic context and institutional environment with progress toward SDG 4, filling a current gap in the literature. The results offer joint support for contingency and institutional theory in the local-government sphere, showing that educational outcomes emerge from the interaction between internal financial conditions and external pressures rather than from isolated factors. Additionally, it establishes a conceptual and methodological framework that can serve as a basis for future research on other SDGs, different levels of government or national contexts, strengthening academic understanding of the factors that affect the implementation of the 2030 Agenda.

Despite the important contributions of this study, it is essential to recognise its limitations. First, the analysis focuses only on municipalities with more than 80,000 inhabitants and provincial capitals in Spain, which means that it does not consider the entire population or the situation of smaller localities. This leaves unexplored possible differentiated dynamics in smaller municipalities. Second, the operationalisation of SDG 4 relies on a composite index of six indicators; while robust, this measure may not fully capture qualitative aspects of education such as student competencies or learning outcomes. Third, the study uses data from a single year, which limits the ability to observe temporal dynamics. Given that the achievement of sustainable development goals requires a long time horizon, the analysis of a single year may not reflect medium- and long-term trends. Furthermore, we emphasise that the cross-sectional nature of the analysis does not allow for causal inference.

Future studies could build on these findings by incorporating longitudinal or panel data to analyse how financial sustainability and educational outcomes evolve together over time and to enable stronger causal claims. It would also be valuable to explore alternative indicators of institutional capacity, such as staff qualifications, technical expertise, organisational structures or the presence of specialised education units. In addition, further research could examine the mechanisms through which APP and indebtedness affect educational performance, distinguishing between different types of debt or investment patterns. Finally, future analyses could expand the geographic scope to include smaller municipalities or cross-country comparisons to enhance generalisability.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research has been supported by the Mediterranean Research Center for Economics and Sustainable Development (CIMEDES). Natalia Alonso Morales reports financial support was provided by Ministry of Science, Innovation and Universities, Spanish Government (FPU 2023). Pedro Gil García reports financial support was provided by University of Almeria (FPI 2023).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available on request.