Abstract

Enterprise environmental, social, and governance (ESG) performance and digital transformation are of great value for enhancing firm performance. Based on data from A-share listed companies in China from 2016 to 2022, a regression model was constructed to verify the influence of ESG performance on company performance under digital transformation. Research suggests that ESG performance enhances firm performance and that enterprise innovation has an intermediary effect, which is adjusted by digital transformation. Digital transformation provides “big data technology” and other means to effectively and intelligently promote enterprise innovation and enhance the role of ESG performance in promoting enterprise performance. Heterogeneity indicates that, compared to state-owned, high-tech, and heavily polluting firms, the ESG performance of non-state-owned, high-tech, and non-heavily polluting enterprises has a stronger effect on firm performance. These conclusions are of significant importance to the ESG performance, digital transformation, and sustainable and high-quality development of enterprises.

Plain language summary

Based on data from A-share listed companies in China from 2016 to 2022, we constructed a regression model to verify the influence of environmental, social, and governance (ESG) performance on company performance under digital transformation. First, the benchmark regression model verified that ESG performance can directly improve firm performance. Second, through a test of the intermediary scheme, we found that promoting enterprise ESG performance to enhance firm performance can also be achieved by promoting enterprise innovation, which plays a partial intermediary role between the two. Additionally, we built a regulated intermediary test model and showed that digital transformation can positively regulate ESG performance and promote firm performance by enhancing enterprises’ innovation ability. Finally, we divided the research sample into groups and discussed the heterogeneity of ESG performance on enterprise performance under different property rights and industry attributes. This research provides significant guidance for ESG development in China and the digital transformation of enterprises.

Keywords

Introduction

Environmental, social, and governance (ESG), also known as environmental, social, and corporate governance, assesses the sustainability of enterprise production and operations, as well as their impact on societal values based on three dimensions: environmental protection, social responsibility, and corporate governance (Eccles et al., 2020). With the goals of peak carbon and carbon neutrality being put forward, China has been paying increased attention to enterprise ESG performance. The Dual Carbon policy has become an important tool for promoting ESG performance in China, and it has also become the main impetus for high-quality development among Chinese companies. ESG is highly compatible with the five development concepts of innovation, coordination, green, openness, and sharing, and it provides an efficient tool for economic and social transformation and high-quality development. Enterprises require more information to cooperate in the growth process, which also requires them to improve the quality and level of the information they disclose to maintain their development (Eccles et al., 2011). ESG maintains a company’s sustainability characteristics, which can enhance its reputation and create a distinctive brand, thereby winning the trust of external investors and leading to higher resource availability and performance (S. Chen et al., 2023). When companies face economic and environmental risks, it is important to reduce costs by improving environmental management and information disclosure. Providing comprehensive environmental information to external entities also improves a company’s productivity and profitability (Dagestani & Qing, 2022). ESG performance, as non-financial information, is used in conjunction with financial information by corporate managers and stakeholders to achieve corporate profitability and sustainable development (Lokuwaduge & Heenetigala, 2017). The economic and social benefits of ESG for enterprises and society are becoming increasingly prominent. It is of great significance to realize the sustainable and high-quality development of Chinese enterprises by continuously improving firm performance and social value (Alsayegh et al., 2020; Попов & Макеева, 2022). However, some listed companies still face many problems with information disclosure, financial fraud, environmental pollution, and so on. In addition, enterprises’ ESG performance, as a non-financial information indicator, has become a “gimmick” used to cover up their malpractices and mislead investors when making judgments (X. Wu & Hąbek, 2021). Therefore, exploring the effects of enterprise ESG performance on firm performance can help enterprises use financial results to standardize corporate behavior, guide the accurate disclosure of information, actively assume social responsibility, and fully understand the contributions of ESG to the enterprise (Alareeni & Hamdan, 2020; Koroleva et al., 2020).

A report by the 20th Party Congress notes that it is necessary to “accelerate the development of the digital economy, promote deep integration of the digital and real economies, and create an internationally competitive digital industry cluster.” Digital transformation emphasizes the appropriate reform of enterprises in the information age; this involves integrating the Internet of Things, big data, digital technology, artificial intelligence, and other means into product development, production, sales, service innovation, and other processes, and continuously promoting operational efficiency and total factor distribution efficiency, thus achieving a higher input–output ratio. Digital transformation is important for enterprises to achieve high-quality development and improve performance (Yudong et al., 2021). Accordingly, companies should keep up with the development of the digital economy by prioritizing digital transformation. Digital transformation breaks through the barrier of time–space communication within enterprises by utilizing digital technology, continuously promoting internal cooperation, improving competitive advantage (Song et al., 2021), and driving business model innovation by building a new value exchange mechanism, which points to a new direction for improving enterprise performance (DaSilva, 2018). Digital transformation can not only create enterprise development plans for enterprise production and improve the quality of products and services, but also promote the flattening of the enterprise organizational structure, thus providing more transparent and efficient information flow and sharing and helping enterprise managers optimize decision-making (Nguyen et al., 2018). The information advantage that digital transformation brings to enterprises strengthens the interconnectivity between government and enterprise departments, R&D departments, and other industries, as well as the public, which helps enterprises integrate differentiated and large amounts of knowledge and capabilities, tap into their own innovation potential, and enhance their self-innovation capabilities and firm performance by optimizing factor allocation (Yang et al., 2023). Digital transformation empowers enterprise production-line intelligence, improves production efficiency, promotes enterprise models and product innovation, and mitigates business risks caused by information asymmetry. Thus, it is important for managers to govern companies, improve firm performance, and ensure high-quality development.

Academic research on the effects of ESG performance and digital transformation on firm performance is quite rich, and most of the existing literature believes that both are helpful for improving firm performance. However, research on the mechanisms between ESG performance, enterprise performance, and enterprise digital transformation are still lacking. In particular, the regulatory role of digital transformation in the influence of ESG performance on firm performance has not attracted much academic attention. Here, we argue that digital transformation plays an active regulatory role in the relationship between ESG and firm performance, and that its mechanism requires empirical testing. Innovation is the internal driving force for improving firm performance, and improving enterprise innovation ability is indispensable for maintaining the core competitiveness and strengths of an enterprise. Therefore, this study considers enterprise innovation as an intermediary factor for exploring the influence of enterprise ESG performance on firm performance and the regulatory mechanism of digital transformation.

This paper focuses on three questions:

Q1: How does enterprise ESG performance affect firm performance?

Q2: How does digital transformation regulate ESG performance and firm performance?

Q3: What are the effects of ESG performance on the performance of different enterprises?

The main contributions of this study are reflected in three aspects. First, the study brings digital transformation into the influence of enterprise ESG performance on firm performance and clarifies that digital transformation plays an active regulatory role in promoting enterprise ESG performance. The results expand the existing research on the effect of ESG performance on firm performance. Second, this study analyzes the regulatory mechanism of digital transformation on the impact of ESG performance on firm performance. In other words, when the degree of digital transformation is high, the effect of ESG performance on firm performance is further enhanced, which manifests in a more obvious promotion of enterprise innovation. This conclusion provides dynamic support for the promotion of ESG development and digital transformation. Third, listed companies in China are classified according to different property rights and industries, and the heterogeneity of ESG performance on firm performance is understood from different perspectives to help the government and relevant departments or staff cope with the improvement and management of different firm performances.

Literature Review and Hypothesis Development

Enterprise ESG Performance and Firm Performance

An enterprise’s ESG performance involves maintaining social balance and promoting social progress while pursuing its own profits, thereby achieving its own goals while working towards those of society (Gao & Han, 2022). Since ancient times, China has been deeply influenced by Confucianism and has accepted the idea of harmonious coexistence. ESG performance is a core element of business ethics. Enterprises that perform well in terms of ESG tend to exhibit better firm performance (Aboud & Diab, 2019). By analyzing more than 200 related documents, Clark found that 88% of the papers revealed a positive correlation between ESG performance and financial performance (Clark et al., 2014), and that environmentally conscious firms had a higher level of financial performance (Kjetil, 2006). Bhagat found that the governance index, shareholdings of board members, separation of the CEO and chairperson, and firm performance showed a significant positive relationship (Sanjai & Bolton, 2008). In the agricultural and forestry industries, ESG performance can also positively contribute to the growth of firm performance, especially because the influence of corporate governance dimensions on firm performance is more obvious. The higher the ESG rating, the more favorable the improvement in firm performance (Zeng & Jiang, 2023).

ESG performance reduces information asymmetry (Kim & Park, 2023), improves corporate information transparency, enhances organizational information disclosure mechanisms (Chao Li et al., 2022), and boosts financing abilities. First, ESG reduces information asymmetry (Kim & Park, 2023) by providing investors with a more transparent channel to understand the company and displaying more information about all aspects of the company (Ryan, 2021), which improves investment efficiency (Lin et al., 2023). Second, when company information in the bond market is more transparent, it is easier for enterprises to obtain development funds, and banks impose fewer contract restrictions (Chy & Kyung, 2023). Third, business analysts focus more on companies with good ESG performance (Jiandong Chen et al., 2016), motivating enterprises to standardize their business activities under external supervision and improve the quality of their financial reports, thus reducing the uncertainty of investors’ investments (Xianzhong et al., 2017). In addition, a high-quality level of information disclosure is not necessarily detrimental to the enterprise, but in some aspects, it means that the managers and relevant stakeholders may request a higher level of review, and they will always be aware of the strengths and weaknesses of adjusting the enterprise’s policies and optimizing its decision-making. This will also enable enterprises to obtain better business advice and ultimately improve their performance (Shen et al., 2016; Shive & Forster, 2020). In other words, ESG performance can improve enterprises’ information transparency, which is conducive to improving their operational efficiency.

Enterprises’ ESG performance can satisfy relevant stakeholders (shareholders, managers, employees, customers, suppliers, and society; Harrison & Freeman, 1999) by establishing a good brand image, improving corporate reputation, promoting the vitality of human resources, and improving the total factor productivity and corporate performance (Deng et al., 2023). First, an enterprise with good ESG performance has a management system that is well equipped to cope with risks, and shareholders and managers engage in more legal and compliant behaviors (Yue Zhang et al., 2023). Enterprises with good ESG performance can resist risks and maintain a stable development environment by restraining the risk of stock price collapse (W. Luo et al., 2024). High-quality ESG performance can also restrain managers’ misconduct, improve their transaction efficiency and management quality, and reduce the principal-agent risk to enterprises (He et al., 2022). Second, enterprises with better ESG performance can signal that they can manage and develop social talent, fully tap employees’ potential, and attract more high-quality talent, thus equipping them with sufficient human capital for development (Branco & Rodrigues, 2006). Enterprises with good ESG performance can not only provide employees with a better working environment but also recognize their work achievements, enhance their sense of accomplishment and organizational identity (Ge et al., 2022), and retain high-quality and highly skilled talents to generate ideal economic benefits (Ferrero-Ferrero et al., 2016; Garsaa & Paulet, 2022). Third, companies with good ESG performance send positive signals of a good brand image and reputation to customers and suppliers (Meng et al., 2023), which makes it easier for them to gain customers and suppliers’ trust and realize long-term cooperation and development (Kramer & Porter, 2006). Friedman (2007) believes that focusing on social responsibility can improve corporate profits (Friedman, 2007). If the public recognizes enterprises’ social responsibility, environmental protection, and corporate governance activities, the consumption level of corresponding products and services will improve, brining benefits to enterprises (Z. Li et al., 2020).

H1: Enterprise ESG performance can actively affect firm performance.

Enterprise ESG Performance, Enterprise Innovation, and Firm Performance

Organizational innovation is an important management method for improving the level of knowledge exchange and the quality of products and services in enterprises; it is also a necessary means for improving workflow efficiency and enhancing the level of corporate performance (Fang & Chen, 2020). ESG performance plays a positive role in promoting the innovation and sustainable development performance of enterprises (Zhou et al., 2023), and enterprises’ innovation ability is enhanced with the improvement of ESG performance, thus boosting their performance (Pavelin & Porter, 2008).

From the perspective of corporate environmental performance, to reduce long-term environmental costs, companies actively disclose ESG information to build investors’ trust, strengthen public recognition of corporate environmental awareness (Xiang et al., 2020), promote sustainable green innovation and development, and enhance corporate performance (Humphrey et al., 2012). In addition, the substitution effect between good environmental performance and the intensity of environmental regulation can reduce the binding nature of mandatory government environmental regulation, help enterprises achieve a relaxed external environment for their own development (F. Wang & Sun, 2022), and concentrate available resources on product innovation. It is worth noting that higher awareness of environmental protections is more conducive to enterprises gaining the trust and support of the government, attracting more capital injection, easing financing constraints, and realizing innovation (Jian et al., 2021). In the context of “double carbon” emissions in China, such awareness is not only in line with the needs of the government and the market for companies to actively undertake environmental responsibilities but also motivates enterprises to actively use technical means to improve resource utilization, accelerate improvements in innovation output and innovation efficiency, and promote their long-term development (Xiaohong et al., 2024).

From the CSR perspective, firms can promote innovation in their products and production processes and enhance their innovative abilities to improve their performance (Cegarra-Navarro et al., 2016; McWilliams et al., 2006). As a result, enterprises can actively fulfill their social responsibilities to protect stakeholders’ interests, gain external resources, share information more easily, shape new thinking, strengthen their innovation ability (X. Luo & Du, 2015), and build core competitive advantages. A good sense of social responsibility also means that companies can retain high-quality innovative talent by improving their incentive systems, providing human and technological resources for enterprise innovation, and promoting the flow and sharing of knowledge (Fatemi et al., 2017). Consequently, they are more likely to create valuable knowledge integration systems, improve production technology and service levels, enhance market competitiveness (Ortas et al., 2015), and provide long-term motivation for sustainable development. Additionally, a higher level of social responsibility is conducive to shaping a good corporate image, enhancing corporate reputation (Ge et al., 2022), gaining support from external innovation funds (Barnett & Salomon, 2012; Buallay, 2019), easing financing constraints, reducing equity capital, and improving corporate performance (Yonghuai Chen et al., 2023).

From the perspective of corporate governance, good ESG performance means that an enterprise’s corporate management system is relatively perfect, which can alleviate the short-sighted behavior of management and reduce the internal constraints on innovative behavior (Amore & Bennedsen, 2016; D. Li & Shen, 2021). The fulfillment of ESG responsibility strengthens firms’ internal management mechanism, urges them to actively improve the disclosure quality of ESG information, reduces the cost of principal agents, and improves the rate of resource allocation. In turn, they increase their R&D efforts (Zhong & Gao, 2017), reduce the disadvantages of information asymmetry, and enable investors’ to pay attention to and grasp more complete information (Tan & Zhu, 2022). Investors tend to invest in the R&D of companies with excellent ESG performance, which not only ensures the safety of investors’ funds, but also promotes firms’ sustainable development (Tang, 2022). High-quality disclosure of non-financial information helps investors increase their risk tolerance and accept looser budget constraints as they have a more complete grasp of company information (Z. Chen & Xie, 2022), thus attracting investors’ capital injection and improving enterprises’ innovative investment and performance.

H2: Enterprise innovation can mediate the relationship between ESG performance and firm performance.

Moderating Role of Digital Transformation

Digital transformation can be a catalyst through which ESG performance improves firm performance, and it can positively adjust the relationship between them. On the one hand, digital transformation plays a positive role in improving the information transmission mode and efficiency and can improve the signal strength and influence effect of ESG to a certain extent. Digital transformation reduces information asymmetry, inhibits corrupt behavior among company managers, standardizes business activities (Yao Zhang & Guo, 2022), and catalyzes further improvement of ESG information disclosure quality. Digital transformation can collect real-time information about customers through new systems, equipment, and platforms (Yubo Chen & Wang, 2019), so that enterprises can comprehend and adapt to the complex characteristics of the market environment and make scientific, rational, and accurate decisions (Jahangir & Walter, 2015; Nylén & Holmström, 2015). Digital transformation empowers existing products and services to undergo intelligent transformation and development (Brynjolfsson & Mitchell, 2017; Chunqing Li et al., 2018); efficiently integrates, configures, and utilizes existing resources; overcomes time and space constraints; and acquires a large amount of external market information (Sungtk, 2018). Enterprises with a high degree of digital transformation have more advanced digital technology, which is more suitable for developing intelligent information systems that combine production factors to improve the efficiency of data observation, collection, analysis, and prediction and realize timely and predictable enterprise production. Moreover, it is more conducive to the integration of ESG practice activities and digital technology (Junlong Chen et al., 2020). The combination of digital transformation and a company’s production process develops its operational potential, leads to innovation in business models, improves total factor productivity (N. Li et al., 2022), and brings about additional benefits (Mikalef et al., 2019). Digital transformation improves the efficiency of internal communications, reduces internal communication costs, and accelerates the flow of information across departments and levels (Loureiro et al., 2021). Digital transformation can indirectly enhance ESG performance by reducing production and operational costs (Mikalef et al., 2020; Selander & Jarvenpaa, 2016; D. Wang et al., 2023).

By contrast, digital transformation introduces digital technology into production and operations, improves resource utilization (Vial, 2019), and promotes persistent R&D and innovation. The digital transformation drives the new business system, helps enterprises reshape their business model to boost efficiency, changes the way they obtain resources and innovate, and enables them to seize business opportunities so that they can swiftly adapt to market changes (F. Li, 2020; D. Y. Liu et al., 2011; Warner & Wäger, 2019). Digital technology not only improves the speed of data processing but also mines more available information, empowers the authenticity of ESG performance, strengthens the innovation of production technology and management modes (Mann, 2015), and improves enterprise performance. During the process of ESG performance promoting enterprise innovation, digital transformation helps enterprises record production and operation information efficiently (Lynn et al., 2019), capture and intelligently apply massive data, broaden the channels for them to build competitive advantages (Gualdani, 2021; Y. Liu et al., 2022), and enhance their innovation ability (Svahn et al., 2017) and core competitive advantage (Virginia et al., 2018). Further, it boosts enterprises’ anti-risk ability, empowers their ESG performance, promotes their innovation value chain, and enables them to develop products and services more conveniently (Butollo et al., 2022). In addition, digital transformation means that enterprises place more emphasis on intelligent production (Porter & Heppelmann, 2014), which, through big data technology can accurately determine customer needs and future trends (Erevelles et al., 2016; Fernández-Rovira et al., 2021; Suoniemi et al., 2020) and achieve high-quality personalized services and enterprise products (Abrell et al., 2016; Dalenogare et al., 2018; Yoo et al., 2010). Driven by digital transformation, automated production will also learn independently, search for optimal production paths, and improve the utilization efficiency of enterprise assets (Ji et al., 2018). On the whole, digital transformation serves enterprises’ strategic objectives, responds to the uncertainty of the external environment and the dilemma of internal operations (Barykin et al., 2021), builds their core competitive advantage, enhances their innovation ability, and leads to high-quality development (Fichman et al., 2014).

H3: Digital transformation positively regulates the relationship between ESG performance and firm performance.

Methods

Sample and Data Collection

Using the CSMAR (China Stock Market and Accounting Research Database) database (https://cn-gtadata-com-s.ytu.yitlink.com:443) as the data source, this study selected data from A-share listed companies in China from 2016 to 2022 as the test sample, and processed them using four steps (J. Wang et al., 2023). First, the ST, PT, and *ST samples were excluded. Second, we eliminated financial industry samples. Third, samples with missing data were excluded. Finally, continuous variables were shrunk-tailed to the upper and lower 1% quartiles. In this study, 21,064 samples were analyzed.

Variable Definitions

Explained Variable

In this study, return on assets (ROA) was used as an explained variable (Guo & Xu, 2021; Velte, 2017). Then, return on assets (ROE) was used as a proxy variable in the subsequent robustness test (Hongtao et al., 2022). ROA is an essential factor for measuring an enterprise’s competitiveness and future ability, as it reflects a company’s comprehensive level and asset utilization efficiency. ROE represents the income level of all shareholders, and measures the ability and efficiency of a company to use its own capital.

Interpretative Variable

In this study, the interpretative variable was ESG performance. Drawing on other studies, Huazheng ESG ratings were selected to measure ESG performance. This system is a reference for the mainstream international ESG evaluation system and is suitable for the Chinese market. The rating is characterized by high data availability, high update frequency, and wide coverage (Jinglin et al., 2021). This index has been widely recognized and applied by academics and industry professionals. The nine ESG performance grades “C, CC, …, AAA” are ranked as “1, 2, …, 9” in descending order of corporate ESG performance in this paper (Bo & Maojia, 2022; Linlin et al., 2022; Zeng & Jiang, 2023).

Intermediary Variable

Studies have measured enterprise innovation mainly based on R&D inputs and outputs. The former is a basic guarantee that enterprises conduct innovation activities. It is the most direct index for measuring enterprise innovation. However, because R&D inputs do not represent the success of innovation activities, R&D outputs are more intuitive and accurate. Examples include the number of patents applied for or granted by an enterprise and the number of products developed. Of these, patents are considered a more suitable variable to represent a firm’s R&D output. Therefore, we measured a company’s innovation ability based on its number of patent applications, including utility model, invention, and design patents (Jinglin et al., 2021).

Moderator Variable

Digital transformation involves the application of new technologies to realize major business transformations and model innovations. In this study, the frequencies of the following five key words in the annual reports of listed companies were counted: “big data technology,”“digital technology application,”“artificial intelligence,”“blockchain,” and “cloud computing” (F. Wu et al., 2021). The frequency of these five key words were then logarithmized by adding 1 (Fei et al., 2021). Finally, we obtained a quantitative index of digital transformation.

Controlling Variables

To improve accuracy, and referring to relevant basic research, Lev, Cashflow, Growth, Indep, and Mfee were included as control variables in the regression analysis, and industry and time effects were fixed. The variable definitions are shown in Table 1.

Variable Definitions.

Model Setting

As shown in Model (1), this study fixed the year and industry effects in a regression that sets the influence of enterprise ESG performance on company performance (Hong & Linxiao, 2023).

where

We built Models (2) and (3) according to Wen and Ye’s mediation effect test (Zhonglin & Baojuan, 2014).

In Model (2), the influence of ESG on company innovation is tested using enterprise innovation RD as an explanatory variable to indicate the innovation level of enterprise i in period t. Model (3) tests the effect of ESG performance and enterprise innovation on firm performance simultaneously. When the product of

To observe the moderating effect of digital transformation, this study developed Model (4), as follows:

We refer to Edwards and Lambert (2007) for moderated regression in this study. This approach integrates moderation and path analysis. If the coefficient

Results

Descriptive Statistical Analysis

Table 2 shows the descriptive statistics of the relevant variables. Among them, the maximum value for ESG performance is 6 and the minimal is 1, indicating a large gap in ESG performance among firms. In addition, the mean value of 4.106 shows that the average enterprise ESG rating is above grade “B.” The maximum value for enterprise innovation is 6.874, the minimum is 0, and the mean value is 2.906, indicating that there is also a significant difference in innovation ability among enterprises, which needs to be paid attention to and improved upon. Similarly, the maximum and minimum values for digital transformation were 5 and 0, respectively, and the average value was 1.406, indicating a clear gap in digital transformation among enterprise and showing that the overall transformation degree was low. To avoid multicollinearity, a VIF test was performed on the existing variables; each variable had a VIF value of less than two, indicating that there was no obvious multicollinearity issue in the data.

Variable Descriptive Statistics.

Relevance Analysis

Table 3 presents the relevance analysis results. A significantly positive relationship between ESG performance and firm performance implies that when a company has high levels of ESG performance, its performance will also improve (Peng & Isa, 2020; Yoon et al., 2018). The positive relationship among enterprise innovation, ESG performance, and firm performance also shows that ESG can promote enterprise innovation, thereby improving firm performance (C. Zhang et al., 2020). However, digital transformation was negatively correlated with corporate performance, which may be related to the large costs and resources involved in the early stages of digital transformation and the lag in output (L. Li, 2022). These results offer preliminary support for H1 and H2. Among the control variables, the estimated effects of cash flow and growth on firm performance were significant at the 1% level, whereas Lev, Indep, and Mfee were negatively correlated with corporate performance.

Relevance Analysis.

p < .1. ***p < .01.

Baseline Regression

The baseline regression results for ESG and firm performance are presented in Table 4. As per Model (1), a distributed regression was performed. In Column (1), only the firm and ESG performance variables were added, and the time and industry effects were fixed. The ESG coefficient was found to be significantly positive at the 1% level (α = .006, p < .01). When the control variables are added in Column (2), the estimation coefficient of ESG performance is 0.002 (α = .002, p < .01), which means that the standard deviation of enterprise ESG performance has increased by 1%, and the average value of enterprise performance has increased by 5.83%. These results show that good ESG performance is conducive to improving enterprise image, reducing information asymmetry, and improving firm performance. Thus, H1 is supported. This research supports previous conclusions regarding the influence of ESG performance on firm performance (Brogi & Lagasio, 2019; Koroleva et al., 2020; Y. Li et al., 2018).

Baseline Regression Results.

p < .01.

Robustness Tests

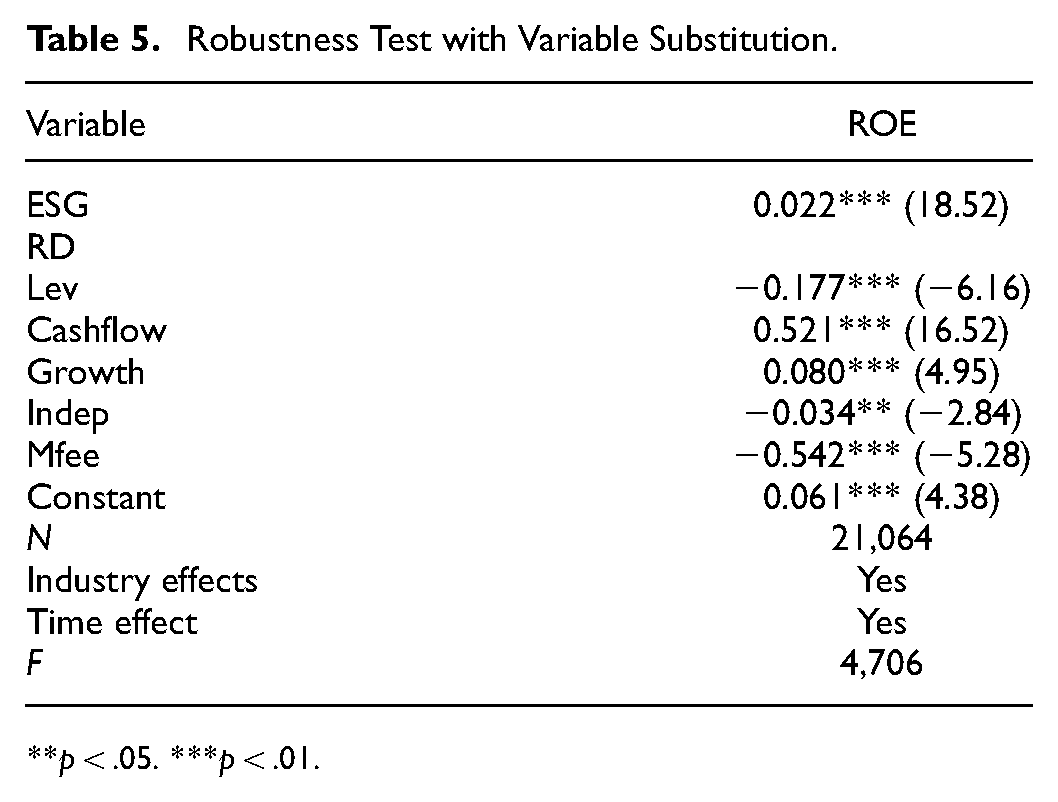

To test the robustness of the results, we replaced the explained variable ROA with ROE and found that ESG performance remained significantly positive at the 1% level (α = .002, p < .01; Table 5), which is consistent with the benchmark regression test (Fan & Hong-xia, 2019). The verification results demonstrate the robustness of the conclusion that ESG performance positively promotes corporate performance.

Robustness Test with Variable Substitution.

p < .05. ***p < .01.

Treatment of Endogeneity Issues

To solve endogeneity problems such as bidirectional causality, we tested the reliability of the results with lag effects and the two-stage least square (2SLS) test. First, we examined the three-phase lag effects of the explanatory variables. As shown in Table 6, lagged ESG performance still has a favorable influence on firm performance, indicating the reliability of the positive effect between them. Second, we used ESGAVG, the average value of ESG performance in various industries and years, as a tool variable, and tested the regression results using the 2SLS method (Table 7; Hong & Linxiao, 2023). From the estimation results of the first stage in the table, the regression results of the instrumental variables and endogenous explanatory variables are significant at the 1% level, with a p value of 0, and the unidentifiable test rejects the original hypothesis. The value of F is 517.76, which is significantly higher than the critical value of 10% (16.38), indicating a strong correlation between the instrumental and endogenous variables and no weak instrumental variable. In addition, the number of exogenous and instrumental variables is equal; thus, there is no overidentification problem. In the second stage, the estimation results show that after considering the above endogenous effects, the estimation coefficient of enterprise ESG performance remains positive, indicating that the effect of the promotion of enterprise ESG performance on enterprise performance remains unchanged.

Testing for Lagged Effects.

p < .1. ***p < .01.

2SLS Test.

p < .05. ***p < .01.

Mechanism Test

An empirical test was conducted based on Model (2). As shown in Column (1) of Table 8, the ESG estimation coefficient was significantly positive at the 1% level (γ = .068, p < .01), suggesting that ESG performance can improve firm performance by promoting enterprise innovation. ESG performance can increase the trust of external investors and improve governors’ awareness of environmental management, thereby promoting enterprise innovation. Positive ESG activities can also promote the formation of innovation-related mechanisms to facilitate R&D activities, thereby enhancing innovation capabilities. We continued the test in Model (3). As shown in Column (2), the product of the

Mechanism Test.

p < .05. ***p < .01.

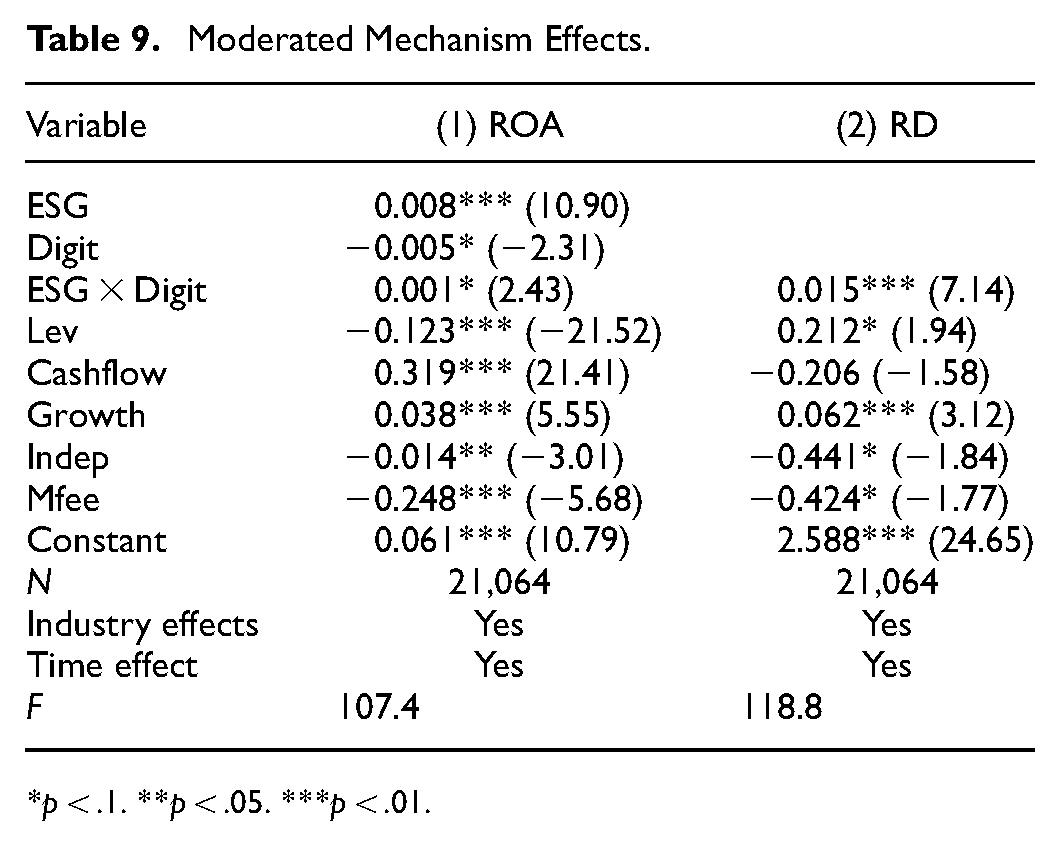

Based on the previous analysis, digital transformation may positively affect the influence of ESG performance on firm performance, and its moderating role is supported by Model (2). As shown in Table 9, Column (1) shows, there is a negative correlation between digital transformation and enterprise performance, which is consistent with the results in Table (3), indicating that the cost of early digital transformation of the enterprise is high and the output is lagging, which has a certain negative impact on enterprise performance. Currently, the digital transformation of domestic enterprises is in an early stage; therefore, the estimation coefficient of digital transformation is negative. However, the interaction coefficient between ESG and digital transformation is 0.001, which is significantly positive at the 1% level, indicating that although previous digital transformation cannot directly improve enterprise performance, it can positively adjust the positive impact of ESG performance on enterprise performance. Column (2) shows that the coefficient of ESG × Digit is obviously positive (0.015 > 0.001). In other words, the process by which ESG performance promotes enterprise innovation is positively regulated by digital transformation, which improves enterprise performance. Digital transformation makes enterprise products more intelligent. During innovation and R&D activities, digital transformation helps enterprises to quickly process the large amounts of data needed for innovation and apply them intelligently, accelerate the completion of innovation R&D, and enhance sustainable competitiveness and high-performance returns (Mann, 2015). Digital transformation can shorten the cycle of product development and business operations, forcing enterprises to accelerate innovation and improve their corporate performance. Thus, Hypothesis 3 is supported, which is consistent with other people’s research results (Fu & Li, 2023).

Moderated Mechanism Effects.

p < .1. **p < .05. ***p < .01.

Further Analysis

Heterogeneity of Property Rights

Enterprises are divided into state-owned (SOEs) and non-state-owned enterprises (NSOEs) according to ownership type, and the regulatory role of firms’ ownership in the relationship between ESG performance and firm performance is discussed below. As shown in Table 10, the ESG performance of the two types of firm has a positive effect on firm performance. The estimated coefficient of ESG performance is positive at the 1% level, further highlighting the positive correlation between ESG performance and firm performance. The ESG performance of non-state-owned enterprises improved significantly. SOEs are more likely to acquire financial support for R&D and face less market pressure, while non-SOEs can only attract external investors by improving ESG performance, easing financial pressure to enhance innovation, and improving firm performance. NSOEs have clear ownership structures and improved management mechanisms. They are also more sensitive to information on public opinion. Therefore, they are more concerned about ESG performance than SOEs (Hong & Linxiao, 2023).

Heterogeneity of Industry Characteristics

Dividing the panel into high-tech and non-high-tech industries, and non-heavily polluting and heavily polluting industries (Jinglin et al., 2021) allows us to further examine whether the impact of ESG performance on firm performance differs across industries. As shown in Table 10, enterprise ESG performance enhances all firm performance. Thus, H1 was validated. Notably, the ESG performance of enterprises in high-tech and non-heavily polluting industries also increases firm performance. Owing to its characteristics, the high-tech industry pays more attention to the development and use of new technologies and sustainable development, and the stakeholders of enterprises in this industry actively seek to improve ESG performance when making decisions (Wenjing & Hongxing, 2022). In non-heavily polluting industries, enterprises have relatively low environmental pollution and pay attention to ecological mitigation; therefore, they bear more environmental protection responsibilities, have higher environmental awareness, and are more sensitive to their ESG performance rating coefficient (Ruibo et al., 2023). However, it is natural for heavily polluting industries to improve their production environment to improve ESG performance, and their ESG performance signals are easy to ignore and interrupt, and cannot play their corresponding role.

Heterogeneity Analysis.

p < .05 ***p < .01.

Discussion

China’s high-quality economic development has entered a new stage, leading enterprises to achieve high-quality, high-efficiency, fair, sustainable development. ESG is a new concept of sustainable development encompassing three dimensions—environment, society, and corporate governance—and an important starting point for achieving high-quality economic development.

Our results illustrate three main issues. First, what is the relationship between ESG performance and enterprise performance and its influencing mechanism? As can be seen from Tables 3 and 4, enterprise ESG performance improves enterprise performance, which supports H1 in this paper. It is worth noting that the results in Table 6 show that the positive, lasting impact of ESG performance on enterprise performance continuing into the third year and beyond. Table 8 clearly shows that enterprise ESG performance can be improved by promoting enterprise innovation, which supports H2 in this paper. For example, positive ESG performance conveys an enterprise’s strong sustainable development capability, which helps it cultivate a positive reputation, attract more attention from external investors, and thus acquire more development resources and support for enterprise innovation (Meng et al., 2023). Good ESG performance improves the transparency of corporate information, inhibits illegal financial activities, and reduces the risk of damage to a company’s reputation (Yuan et al., 2022). ESG performance optimizes the quality of information disclosure so that managers and investors can fully and accurately understand production and business trends (C. Li et al., 2022), thereby optimizing decision-making quality and improving enterprise performance.

Second, what is the regulatory mechanism of digital transformation between ESG and corporate performance? Table 9 shows that digital transformation can positively regulate the influence of enterprise ESG performance on enterprise performance and that their relationship can be mediated by improving the influence of enterprise innovation. Digital transformation uses big data technology and artificial intelligence to provide a technical means for ESG performance to influence enterprise performance. Specifically, digital transformation facilitates more efficient and more intelligent enterprise innovation. When digital technology enters the operation process of enterprises, it greatly shortens the distance between enterprises and customers, helps collect customer information, identifies customer needs, improves enterprises’ innovation ability and efficiency, and further strengthens the promotion of enterprise ESG performance (Lynn et al., 2019).

Finally, what are the effects of the ESG performance of different enterprises on enterprise performance? We study sample grouping and further analyze the influence of ESG performance on enterprise performance. Table 10 shows that the improvement in enterprises’ ESG performance varies with the type of enterprise property rights and the nature of the industry. First, influenced by the nature of property rights, the ESG implementation of SOEs tends to be a mandatory requirement for policies and systems, whereas the ESG implementation of non-SOEs can better reflect their strong sense of sustainable development. Therefore, the ESG performance estimation coefficient for non-SOEs is higher than that for SOEs. Second, high-tech industries have high product barriers and long return periods on investment, which is conducive to improving firms’ long-term performance. High-tech industries face greater market competition and financing constraints; therefore, they are more sensitive to ESG performance than non-high-tech industries. Finally, the estimation coefficient of ESG performance in non-heavily polluting industries is higher than that in heavily polluting industries, which may be because heavily polluting industries are subject to stricter environmental regulations in the production process, and the cost of green innovation is higher than that in non-heavily polluting industries. However, as a long-term investment, ESG does not provide short-term benefits to enterprises. Therefore, heavily polluting industries are less sensitive to ESG performance than non-heavily polluting industries.

Conclusions

Enterprises’ ESG performance and digital transformation are of great value for enhancing firm performance. Using CSMAR as the data source, we selected data from A-share listed companies in China between 2016 and 2022 as the observation sample and obtained 21,064 valid observations. We constructed a main effects regression, mediation effects, and mechanism adjustment model to explore the relationship between enterprise ESG performance and firm performance. We also conducted relevant robustness and endogeneity tests using substitution variables, a lagged effects test, and a 2SLS test. The results showed that enterprises’ ESG performance significantly improves their performance levels and enterprise innovation plays a partial intermediary role between them. Moreover, the digital transformation of enterprises enhances the influence of ESG performance on enterprise performance. The specific mechanism is that digital transformation enables enterprises to innovate more efficiently and intelligently. In addition, we found that the ESG performance of non-SOEs, high-tech industries, and non-heavily polluting industries clearly promotes enterprise performance.

We use listed companies in China as the research object and proved through empirical analysis that ESG performance positively impacts enterprise performance. Digital transformation can positively promote the influence of ESG performance on enterprise performance by improving enterprises’ innovation ability, which expands the existing literature on the relationship between ESG and enterprise performance and makes theoretical contributions. China, which is currently the world’s largest developing country, has issued a series of national policies and standards on ESG practice and is constantly moving toward the goal of “carbon dioxide emissions peaking and carbon neutrality.” However, research on ESG in China began relatively late, and many domestic enterprises have paid insufficient attention to ESG performance and concealed their related information. Similarly, some enterprises have pursued short-term profits and neglected sustainable development, which has caused a series of ESG problems. For example, high-pollution industries have excessive emissions, chaotic internal governance, frequent accidents in production safety and issue false financial reports (Bao et al., 2023; Cong et al., 2022). However, Chinese enterprises’ ESG practices can still improve their market scale. Therefore, this study is of great significance for the development of ESG in China.

These results are essential for the sustainable development of Chinese enterprises. The results show that ESG performance positively impacts enterprise performance, especially for enterprises with a high degree of digital transformation. Therefore, enterprises should pay attention to ESG performance and digital transformation and take the initiative to incorporate them into future development plans and corporate culture. They should also promote enterprise innovation and digital technology application reform and seek to optimize management and development decisions to achieve sustainable and high-quality development goals.

Moreover, the research results of the heterogeneity analysis can help the government realize the need to pay attention to state-owned, non-high-tech, and heavily polluting industries; avoid ignoring the signals transmitted by the ESG performance of relevant enterprises; correctly guide enterprises to improve ESG performance and information disclosure quality; and urge non-SOEs, high-tech industries, and heavily polluting industries to play a leading role.

Finally, the research results show that ESG performance and digital transformation have a positive impact on enterprise performance, which encourages stakeholders to pay more attention to ESG performance and digital transformation and exert a good supervisory effect to urge enterprise managers to improve ESG performance and implement digital transformation.

This study also has several limitations to indicate need for improvement or further study. ESG consists of three dimensions: environmental protection, social responsibility, and corporate governance. This study examines the influence of ESG performance as a whole, but fails to consider the individual effects of these dimensions. For example, digital transformation mainly affects a company’s production, operations, and information acquisition through technical means. However, whether this has a positive moderating effect on environmental protection and social responsibility remains unknown. For some firms, the cost of fulfilling their social responsibility is higher than their income; therefore, social responsibility may inhibit corporate performance. Therefore, to further analyze the moderating effect of digital transformation on the relationship between ESG performance and firm performance, future research should examine each of the three ESG dimensions separately.

Footnotes

Acknowledgements

We are grateful to all the people involved in the investigation for their active cooperation.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.