Abstract

Empirical literature on the Ethiopian insurance sector has largely overlooked the impact of non-financial strategic orientations and the moderating effect of the legal environment on firm performance. This paper examines the impact of six orientations—customer focus, internal processes, learning, technology, diversification, and social and environmental issues—on stable performance. It investigates the moderating influence of the legal environment. With an explanatory design, information from 450 workers in 10 large Ethiopian insurance companies was analyzed using Partial Least Squares Structural Equation Modeling (PLS-SEM). The Findings indicate that all six orientations were significant predictors of stable performance, accounting for 62.4% of its variance (R2 = .624), with internal processes being the most critical predictor (β = .253). The legal environment moderated the effect of customer orientation and social/environmental issues positively, but did not affect the relations for technology, diversification, and learning and development. Moreover, stable performance in Ethiopia’s insurance industry is a matter of an integrated strategy. As a supportive legal environment is hypothesized to enhance customer-oriented and social strategies, internal motivation, such as technology, presently seems to be less regulation-dependent. This work introduces a tested performance framework that expands the balanced scorecard, dynamic capabilities, and contingency frameworks to the insurance sector in an emerging economy.

Plain Language Summary

Performance of insurance companies.

Keywords

Introduction

Insurance companies play a crucial role as catalysts in the economic development of developing countries, such as Ethiopia, by contributing to economic growth, efficient resource allocation, and financial stability (Baruti, 2022). According to Slayton (2023). These financial institutions act as essential intermediaries in the system, mobilizing savings from individuals and enterprises to be channeled into investments in productive areas of the economy, which are supportive not only of capital formation but also of entrepreneurial activity and job creation, all of which are necessary for economic growth. Insurance companies, furthermore, contribute to financial security through risk mitigation related to the uncertainty of unforeseen events, such as natural disasters, accidents, and health emergencies, which could put people, businesses, and entire communities at financial risk (Fan et al., 2024). Beyond this, they help to foster economic resilience through risk reduction and speedier recovery from adverse events (Biener & Eling, 2012).

Managerial and financial factors, such as firm size, capital adequacy, leverage, risk management, corporate governance, operational efficiency, and macroeconomic conditions, are closely linked to the performance of insurance companies (Farida & Setiawan, 2022). According to Z. Pan et al. (2021). Larger insurance firms are generally associated with more robust financial performance, hence, positive effects on profitability and efficiency. Meanwhile, for the company to remain profitable, implementing effective risk management is necessary; furthermore, robust corporate governance enhances returns on equity and assets (Abebe Zelalem et al., 2022). Additionally, operational efficiency supports competitiveness and consumer welfare, while external factors such as GDP growth and inflation also significantly impact profitability (Fabac, 2022).

In today’s rapidly evolving global economy, insurance companies must balance multiple dimensions of their operations to sustain performance (Le, 2019). The balanced scorecard framework provides a comprehensive approach to integrating and measuring the various dimensions. It focuses on four interrelated perspectives: financial, customer, internal processes, and learning and growth. Due to this, organizations translate strategic objectives into measurable outcomes (Agyeman et al., 2017). It has been further extended to encompass social and environmental factors, as well as product diversification, which have gained importance for the sustainability of a corporation and portfolio management, aligning with stakeholder expectations in the digital transformation and innovation era (Kaplan & Norton, 2012).

The BSC framework applied to the Ethiopian insurance companies emphasizes customer orientation, internal process efficiency, employee development, social and environmental responsibility, product diversification, and technology and digital transformation. These dimensions are crucial for fostering sustainable growth and competitiveness, particularly in developing economies like Ethiopia, where the insurance sector plays a significant role in economic development (Mengistu, 2015). In addition, Kebede and Tegegne (2018) have stated that focusing on customer-centricity, improving internal processes, investing in employee development, addressing social and environmental concerns, and diversifying products or services are essential priorities for Ethiopian insurance companies.

Although the BSC framework is emerging, the application of research in the Ethiopian insurance sector remains minimal and is, therefore, plagued by numerous challenges. For instance, existing studies tend to focus mainly on financial and managerial performance at the expense of other non-financial dimensions, including customer satisfaction, employee development, internal processes, social and environmental concerns, as well as product diversification and concerns related to technology and digital transformation. Under-investigated areas, such as regulatory constraints and low insurance penetration, are affecting BSC implementation. Important aspects, such as the regulatory framework, customer views, internal process efficiency, employee growth and development, integration of social and environmental considerations, and the effect of product diversification on performance within the BSC framework, are not discussed. There is also a scarcity of longitudinal studies and research on the role of technology and digital transformation. Despite the above methodological limitations, such as overreliance on quantitative or descriptive methods, this further hinders the generalizability of the findings.

The regulatory environment plays a crucial role as a moderating factor, affecting how various performance dimensions relate to organizational outcomes (Hughes & Mester, 2013). Regulatory frameworks can either support or hinder strategic initiatives such as digital transformation and innovation by influencing operational flexibility and compliance demands (Chen et al., 2015). Woldemariam Birru (2016) discovered that strong regulatory frameworks positively influence the connection between risk underwriting and company performance, leading to greater operational efficiencies and better financial results. Additionally, a review of the performance of life insurance companies reveals that regulatory factors have a significant impact on outcomes, underscoring the importance of effective governance structures, robust risk management processes, and ethical decision-making frameworks (Zinyoro & Aziakpono, 2023). Furthermore, Tsai et al. (2009) argue that grasping the relationship between regulatory conditions and performance drivers is vital for both academic research and practical implementation. Hence, this study aims to address these knowledge gaps by examining the relationships between customer orientation, internal process efficiency, employee development, social and environmental factors, product diversification, and digital transformation in the performance of Ethiopian insurance companies.

The study employs Smart PLS to identify factors influencing organizational performance, revealing a moderate-sized relationship between customer orientation and stable performance. Internal processes, learning, and technological innovation have a positive impact on the stability of insurance companies in Ethiopia. Moreover, the Smart-PLS moderation analysis yields mixed results for insurance companies, indicating that the legal environment hurts social and environmental perspectives, as well as customer orientation, but not on product diversification, technology, innovation, or learning and development. In addition, the study’s findings emphasize the importance of customer orientation, internal processes, education, and technological innovation in driving performance, highlighting the moderating effect of the legal environment.

Literature Review

Theoretical Literature Review

The Balanced Scorecard (BSC) is utilized in insurance firms as a strategic management tool for measuring and aligning performance (Sener & Ege, 2017). In the view of Gwangwava et al. (2013), BSC assimilates both financial and non-financial elements to provide comprehensive performance measurement across an organization. In an insurance firm, customer and financial viewpoints are emphasized and used for measuring performance (Pan et al., 2021). It integrates the best-worst method (BWM) with BSC to assess performance based on time, enabling managers to make more effective decisions. This approach is applied as a tool for knowledge management, where planning decisions merge with control ones using non-financial measures (Pietrzak et al., 2015). On average, the BSC is established as a tool for measuring performance, with a focus on vision and strategy.

The second theory mentioned in this study is dynamic capabilities theory (DCT). dynamic capabilities theory (DCT) is a framework that explains how organizations can adapt and reconfigure their competencies to respond to rapidly changing environments (Yaneva, 2021). In insurance companies, DCT is highly relevant in the context of digital transformation and changing market dynamics, enabling companies to adapt to technological changes and integrate new digital processes, thereby maintaining competitiveness (Bitencourt et al., 2020). According to Baía and Ferreira (2024), dynamic capabilities theory mediates the relationship between resources, knowledge, learning, and firm performance, with cultural and economic contexts potentially enhancing this relationship. In addition, factors such as resources, knowledge, learning, and alliances stimulate learning and adaptation, and effective resource management is crucial for enhancing performance and maintaining a competitive advantage (Tone et al., 2019).

The third theory is contingency theory, a framework that emphasizes the importance of an organization’s effectiveness about external environmental factors (Horvey & Odei-Mensah, 2024). According to S. H. Lee et al. (2020), this theory has been applied to various aspects of the insurance sector, including the impact of war on insurer safety, the transition to agile organizational structures, enterprise risk management (ERM), recruitment strategies, contingency planning, and leadership. Contingency theory also applies to studying the challenges that organizations, in this case, insurance companies, face when recruiting personnel. Additionally, benefits can be gained through contingency planning, as well as the role contingency management plays in leadership (Huang et al., 2023). Additionally, it has been employed to design scenarios for the insurance sector and to assess contingent life insurance products. Strategic initiatives aligned with contextual variables have the potential to enhance organizational performance and competitiveness within the insurance business (Pacheco-Cubillos et al., 2024).

Empirical Literature Review and Hypotheses Development

Customer Orientation and Stable Performance of Insurance Companies

Customer orientation has a positive impact on financial performance in service firms and insurance companies, with service innovativeness partially mediating this relationship (Businge et al., 2023; Pekovic & Rolland, 2012). According to Doligalski and Tomczyk (2018) and Mokhtaran and Komeilian (2016). Furthermore, a customer-oriented management approach fosters long-term client relationships and stabilizes performance (Islam & Zhe, 2022). However, empirical evidence suggests that excessive customer-centric initiatives can hurt operational efficiency or profitability (dos Santos et al., 2020; Guillem, 2020; Islam & Zhe, 2022; Mokhtaran & Komeilian, 2016). This highlights the need for a balanced approach to customer orientation. Hence, based on the above-listed empirical evidence, the study develops the following hypothesis to test the relationship between customer orientation and the performance of insurance companies in the Ethiopian context.

Internal Process and Stable Performance of Insurance Companies

Most studies reveal a positive relationship between internal processes and the performance of insurance companies (Huijiao, 2021; Jerr Jerry & Bran Hadianto, 2024; Weitlaner et al., 2012). Moreover, Gasiorkiewicz (2019) emphasizes the importance of environmental control, risk valuation, action control, information communication, and monitoring. Furthermore, the impact of management competence index and company growth rate on performance is vital (Eze et al., 2019). Additionally, empirical evidence suggests a negative correlation between internal processes, control defects, and enterprise performance (Ahmeti et al., 2022; Anderloni et al., 2020; Cao et al., 2022; Ogunwale et al., 2024). These findings contradict the following hypothesis, which is prepared to be further investigated in the Ethiopian context.

Learning and Development and Stable Performance of Insurance Companies

Studies show a strong correlation between employee development and the performance of insurance companies (Akanpaadgi & Binpimbu, 2021; Kajwang, 2022). On the other hand, a strong learning orientation fosters innovation and enhances firm performance (Ouma et al., 2017). Continuous employee training programs improve operational efficiency and customer satisfaction. Furthermore, investment in skill development leads to improved service delivery, increased profitability, and enhanced financial performance (Inkumsah et al., 2021; Klapkiv & Klapkiv, 2017). Moreover, prioritizing knowledge exchange and promoting digital literacy improves product development, customer satisfaction, productivity, and service quality, directly impacting financial outcomes (Nham et al., 2020; Ouma et al., 2017). However, contrary to the above, Singhal et al. (2020) suggest that employee development and learning orientation may not always improve insurance company performance. On the other hand, overemphasis on training without strategic goals can lead to inefficiencies and financial decline (Al-Mutairi et al., 2021; Azizi, 2017). Furthermore, Knowledge exchange and digital literacy initiatives may not guarantee improved outcomes due to organizational culture, resistance, and inadequate infrastructure (Choi & Jeong, 2022). Taking this conflict of findings, the researcher prepared the following hypothesis to test the relationship in the Ethiopian insurance market context.

Technology, Innovation, and Stable Performance of Insurance Companies

The integration of insurance technologies has significantly improved the performance of insurance companies by reducing financing constraints and optimizing resource allocation (J. Liu et al., 2023). According to Neale et al. (2024), digitalization strategies have also improved business performance by streamlining operations and enhancing customer experiences. However, insurance companies have not fully capitalized on these innovations, indicating potential areas for further development. Proactive involvement in technology development can yield substantial performance gains, as seen in the emergence of telematics and usage-based insurance models (Lanfranchi & Grassi, 2021; Xu & Hao, 2023) Zarifis and Cheng (2022) cites significant technologies and their particular applications with which these transformations are being propelled that is AI-based virtual assistants (chatbots), proactive loss presentation, prevention quicker underwriting, and improved claims processing. Moreover, Mavundla et al. (2024) prepared a manual for insurance carriers on how to apply machine learning technology to tap into untapped revenue within their current customers, offering both a high-performing predictive model and targeted customer characteristics to focus on growth. Moreover, technology is an essential building block of and an asset to trust. For insurance firms, explainable technology has to be employed in order to guarantee regulatory compliance, cultivate customer trust, and infuse ethical values into their automated decision-making (Owens et al., 2022). Based on these insights, the following hypothesis is proposed to test the relationship between the adoption and effective utilization of technologies and innovations and the performance of insurance companies, particularly in developing countries such as Ethiopia.

Product Diversification and Stable Performance of Insurance Companies

The empirical evidence on the effect of product diversification on the performance of insurance companies reveals a complex relationship, often characterized by trade-offs between risk and return (Rathnasiri & Buddhika, 2024). While diversification can mitigate specific risks, it frequently correlates with lower financial performance, particularly in specific contexts and company sizes (Hsieh et al., 2015; Iability et al., 2008). According to C. Y. Lee (2017), the impact of diversification varies significantly with company size. Hence, smaller insurers tend to experience more pronounced adverse effects on performance compared to larger firms, which may benefit from product diversification. However, studies indicate that product diversification often exhibits a negative correlation with financial performance, such as return on equity and return on assets (Septina, 2022). Based on these contradictions, the following hypothesis is prepared.

Social and Environmental Concern and Stable Performance of Insurance Companies

Research indicates that social and environmental factors (ESG) can improve the financial performance of insurance companies (Bressan, 2023; Wu et al., 2022). According to Chiaramonte et al. (2020), ESG factors drive sustainability and competitive advantage through sustainable financial principles and environmentally based service products. However, many studies lack direct evidence on the impact of social and environmental aspects on the performance of insurance companies, focusing on broader contexts like corporate environmental performance, sustainability, and corporate social performance in emerging economies (Cavero-Rubio & Amorós-Martínez, 2020; Galletta et al., 2021; Mahoney & Roberts, 2007). Some studies highlight the benefits of governance and social responsibility, while others focus on the role of insurance companies. More targeted research is needed to test the relationship between social and environmental factors. Considering this contradiction, the following hypothesis is designed to test the scenario about Ethiopian insurance services.

Moderating Role of Legal Environment

Empirical studies have demonstrated that the legal environment significantly moderates the relationship between strategic constructs, such as customer orientation, internal processes, learning and development, technology and innovation, product diversification, and social and environmental initiatives, and the performance of insurance companies (Arias et al., 2020; Pekovic & Rolland, 2016). For instance, customer orientation enhances organizational creativity and innovation capabilities, leading to improved financial performance, especially in markets with supportive legal frameworks (Racela & Thoumrungroje, 2020). On the other hand, efficient internal processes, when aligned with corporate sustainability practices, have a positive impact on organizational performance, with the legal environment influencing the extent of this effect (Makhdoom et al., 2023). Furthermore, investments in learning and development, particularly in technological innovation, are more effective in jurisdictions that foster a market-oriented approach and promote corporate performance (Ali, 2016). The adoption of advanced technology and innovation drives efficiency and customer engagement, with the legal environment playing a moderating role in this relationship. Product diversification strategies can enhance firm performance, with the legal environment influencing the success of these strategies (Su et al., 2013). Moreover, social and environmental initiatives, such as sustainable innovation, have been shown to improve organizational performance, particularly in contexts where environmental performance is emphasized (Islam & Zhe, 2022). Based on this empirical evidence, the following hypotheses were prepared

Conceptual Framework of the Study

Moreover, based on previous theories and empirical evidences which reflect the relationship between exogenous concept like customer orientation, internal process, learning and development, social and environmental concern product diversification and technology and innovation and endogenous constructs (stable performance) as well as moderating construct (legal environment), the following conceptual framework is prepared used for further understanding of relationships.

Figure 1 shows conceptual framework of the study.

Conceptual framework.

Materials and Methods

Sampling and Data Collection

The study participants were employees of 10 insurance companies in Ethiopia that had implemented a balanced scorecard management and accounting framework as a performance tool and had been in operation for at least 10 years in the insurance industry. These companies include Awash Insurance Company, established in 1994, which employs 1,100 people. Birhan Insurance Company, founded in 2010, has a workforce of 625 employees, while Nib Insurance Company, which started in 2002, employs 820 individuals. Lion Insurance Company, established in 2007, employs 750 staff members. The Ethiopian Insurance Corporation, one of the oldest, was established in 1976 and has a workforce of 1,500 employees. Nyala Insurance Company, founded in 1995, employs 614 staff members, while the National Insurance Company of Ethiopia, established in 1994, has 1,200 employees. United Insurance Company, founded in 1938, has a workforce of 620. Africa Insurance Company, established in 1994, employs 540 individuals, and Nile Insurance Company, also founded in 1994, employs 720 people. The total population of the study is 8,489 in general.

The study used Soper’s (2025) sample size formula for structural equation modeling to determine a sample size of 460 from a total population of 8,489. This calculation was based on an expected effect size of 0.23, a statistical power of 0.95, and a significance level of 0.05. A multi-stage sampling technique was implemented to ensure the research’s methodological rigor. The sample size is also noteworthy, as it meets the minimum sample size guidelines (Hair, 2023; Henseler et al., 2015). Proportional stratified sampling was utilized to achieve a balanced and representative distribution from each insurance company. Following this, systematic random sampling was used to select respondents within each stratum, which involved choosing participants at regular intervals from a pre-arranged list of respondents in each stratum.

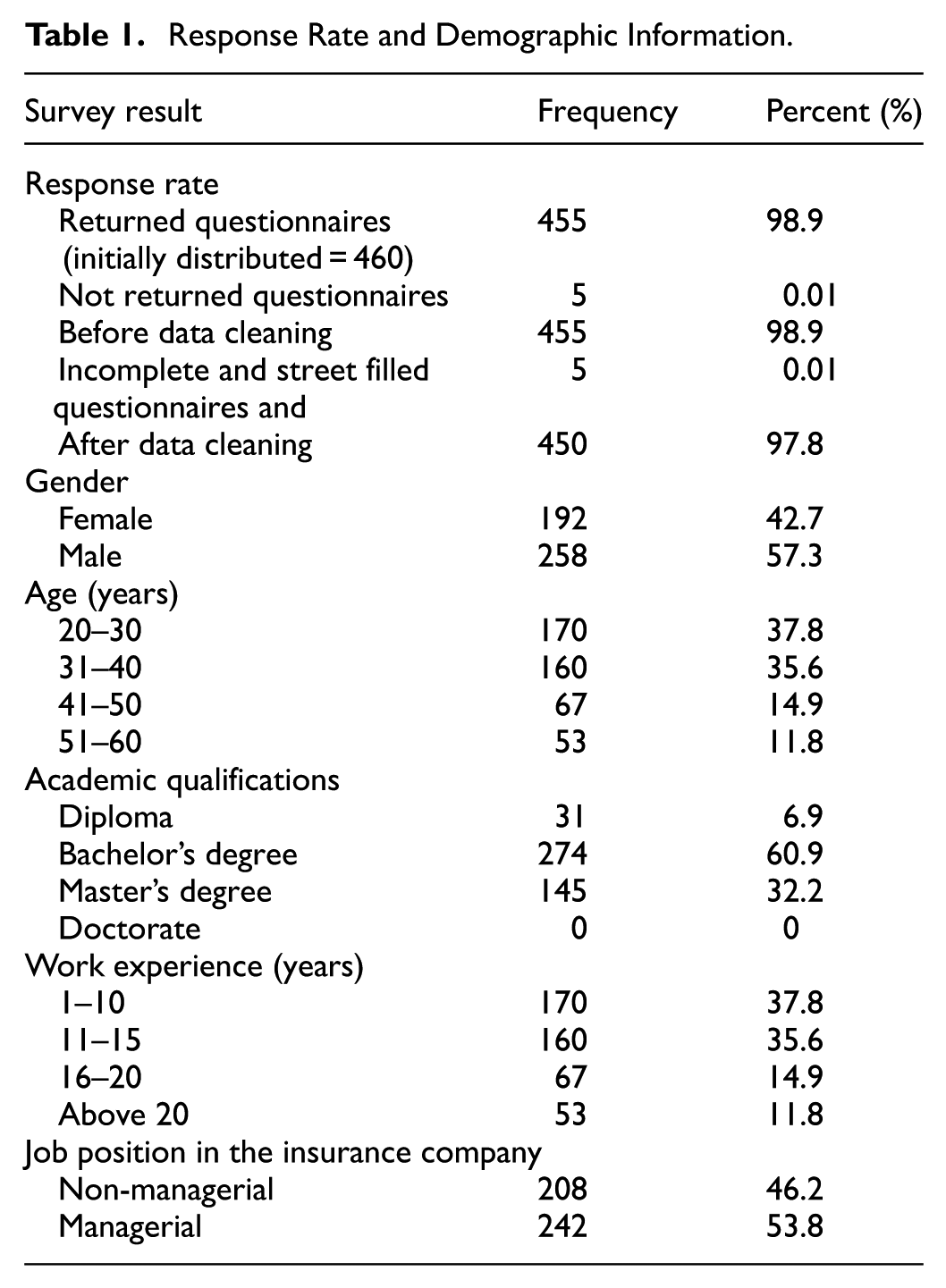

Data was gathered using a structured questionnaire developed within a cross-sectional framework. The questionnaire was distributed and collected in person. Out of 460 questionnaires sent out, all were returned. However, five respondents were excluded due to significant missing data, leaving 455 for initial review. After addressing issues such as undesirable response patterns, including straight-lining, and conducting further cleaning, 450 questionnaires were deemed valid for analysis, yielding a response rate of 97.8%.

Table 1 provides the demographic information of the study participants. The majority of respondents were male, accounting for 57.3%. In terms of age, the largest group (37.8%) consisted of respondents aged 20 to 30, totaling 170 individuals. This was followed by 35.6% of respondents (160 individuals) who were aged 31 to 40 years. Those in the 41- to 50-year age range made up 14.9% (67 respondents), while the smallest group, aged 51 to 60 years, accounted for 11.8% (53 respondents). Regarding education and training, most respondents held a bachelor’s degree, comprising 60.9% of the sample (274 respondents). This was followed by 32.2% (145 respondents) with a master’s degree and 6.9% (31 respondents) with a diploma. In terms of experience, 37.8% of respondents (170 individuals) had 1 to 10 years of experience, while 35.6% (160 respondents) reported having 11 to 15 years of experience. Those with 16 to 20 years of experience constituted 14.9% (67 individuals), and 11.8% (53 individuals) had 21 to 30 years of experience. Lastly, regarding job position, 46.2% of respondents (208 individuals) held non-managerial roles, while 53.8% (242 individuals) were in managerial positions.

Response Rate and Demographic Information.

Data and Data Analysis Method

This research examines the performance of insurance firms in Ethiopia, using customer focus, internal processes, learning and development, technology and innovation, social and environmental concerns, and product range as essential constructs. Stable performance is treated as an endogenous construct, and the legal environment is treated as a moderating variable. All measures for these constructs were surveyed on a Likert-type scale from 1 (strongly disagree) to 5 (strongly agree). For the sake of a sound theoretical foundation, all of the measurement items were taken from well-established, peer-reviewed scales. The particular sources of each construct’s items are summarized in Table 2. Furthermore, it was made clear to all participants that the results of this study would be published in an academic journal. During the informed consent, they consented to the publication of the anonymized and aggregated data. The authors hereby attest that no individual data or information identifiable by a person are included within this manuscript.

Measurement Indicators and Their Source.

Structural equation modeling (SEM) is a robust analytical method used to analyze and estimate complex relationships between different constructs (Hair et al., 2019). Among the various techniques of SEM, partial least squares structural equation modeling (PLS-SEM) is the most used in social science research. This approach is nonparametric and relies on bootstrapping to determine statistical significance and produce confidence intervals for parameter estimates, enabling valid statistical inference (Hair et al., 2019). Data analysis for this study was conducted using the PLS-SEM approach with Smart-PLS 4.0 software. This technique has proven to be very effective in managing multiple constructs and their related indicators, mostly in maximizing the explained variance of the endogenous constructs under study (Hair et al., 2022).

Result and Discussion

Exploratory Factor Analysis (EFA)

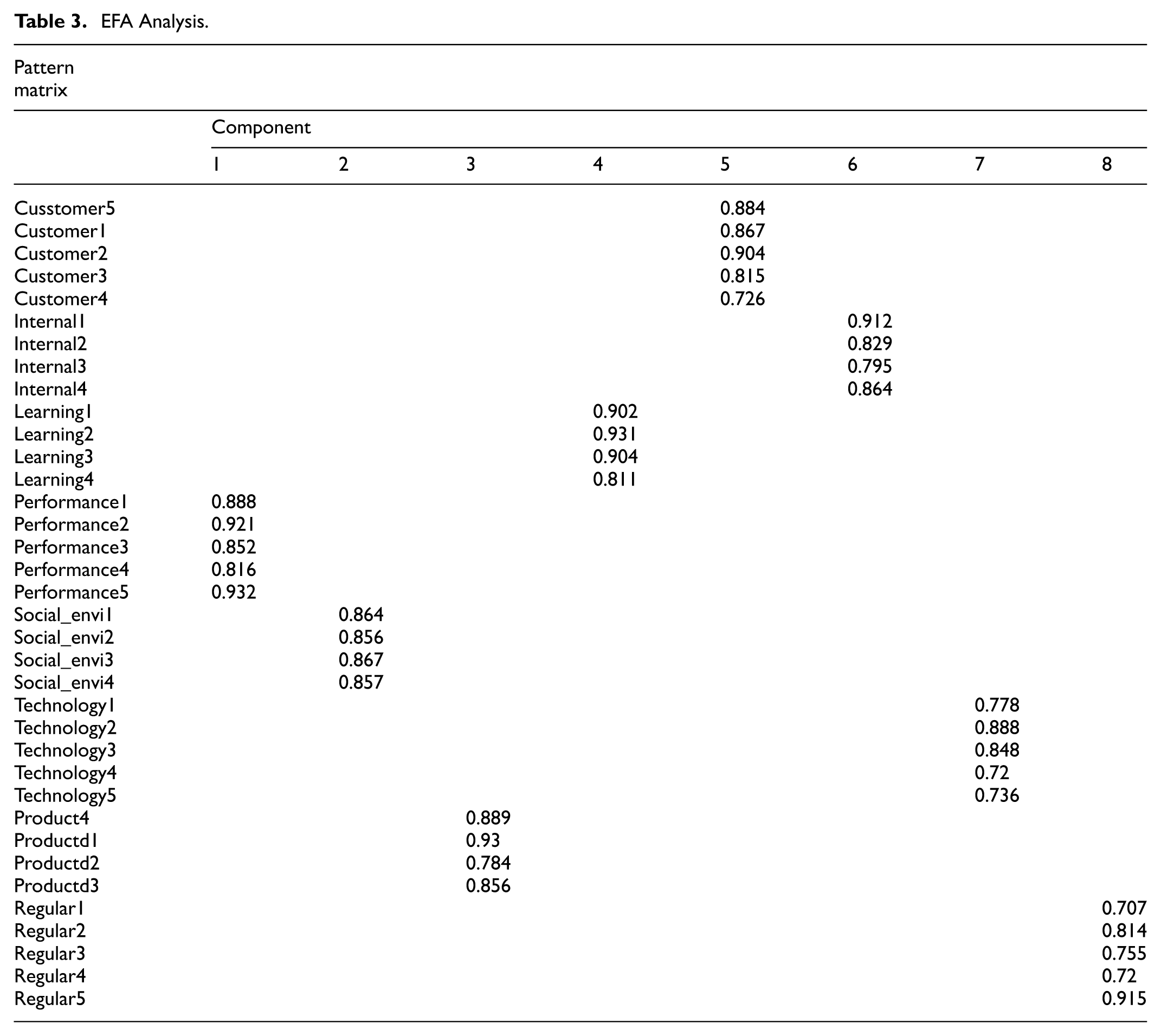

This report presents the results of an exploratory factor analysis (EFA) conducted to determine the latent underlying structure from a set of observed variables. The goal was to condense the variables into a reduced number of interpretable factors (Hair et al., 2018). An exploratory factor analysis (EFA) was conducted using principal component analysis (PCA) as the extraction technique. The produced pattern matrix indicates that an oblique rotation was employed, a procedure that allows the extracted factors to be correlated, which is often a more realistic assumption in social science studies (Costello & Osborne, 2005; Tabachnick & Fidell, 2019). Rotation converged successfully in eight iterations. For ease of readability and to highlight the most important relationships, factor loadings below some agreed cutoff (e.g., 0.40) were suppressed, a standard convention for reporting EFA findings (Stevens, 2002). As indicated in the Table 3, the exploratory factor analysis was highly successful with a clean and easily interpretable factor structure. The findings strongly support an eight-factor structure, and the high strength and clarity of the loadings indicate that the measurement instrument employed is reliable and has good construct validity (Hair et al., 2018).

EFA Analysis.

Measurement Model

First, consider the loadings of the indicator. When the loading is greater than 0.70, this indicates that more than 50% of the variance of the construct is explained by the relevant indicator (Byrne, 2005). From Table 4, it is evident that all indicator loadings exceed 0.70; therefore, there are no issues with the indicators. Furthermore, the internal consistency reliability is assessed via Cronbach’s alpha and composite reliability (CR). According to Bentler (2013), values between 0.70 and 0.95 are considered acceptable. As evident from Table 4, the values for Cronbach’s alpha and CR fall within the specified range. Therefore, the reliability data in this study are adequate. The next step in the measurement model assessment procedure is evaluating convergent validity. This is achieved by reviewing the AVE values, where, a threshold value of 0.50 or greater is required to be within acceptable limits (Hair et al., 2022). Table 4 indicates that all constructs have AVE values above 0.50, indicating no concern regarding convergent validity.

Outer Loading and Reliability.

The second important aspect of evaluating a measurement model is the degree to which a construct is distinct from other constructs within the structural model, a process known as assessing discriminant validity (Ketchen, 2013). This is typically evaluated using the Heterotrait-Monotrait (HTMT) ratio and the Fornell-Larcker criterion. According to Hair et al. (2022), the HTMT ratio should be below 0.850, while the Fornell-Larcker criterion requires that the square root of the average variance extracted for each construct (represented by the diagonal values) exceeds the correlations between that construct and the others. As presented in Table 5, the values appearing above the bold and underlined diagonal elements of the constructs were all less than 0.85, thus meeting the HTMT requirement. In addition, the inter-construct correlations as depicted by the values between the bold and underlined diagonal elements are consistently lower than the square root of the AVE (the values on the bold and underlined diagonal). This establishes that the Fornell-Larcker criterion is also satisfied.

Fornell and Larcker Criterion and the Heterotrait-Monotrait Ratio.

Note. The square root of the AVE (the bold diagonal value) for each construct should be greater than the highest correlation that construct has with any other construct.

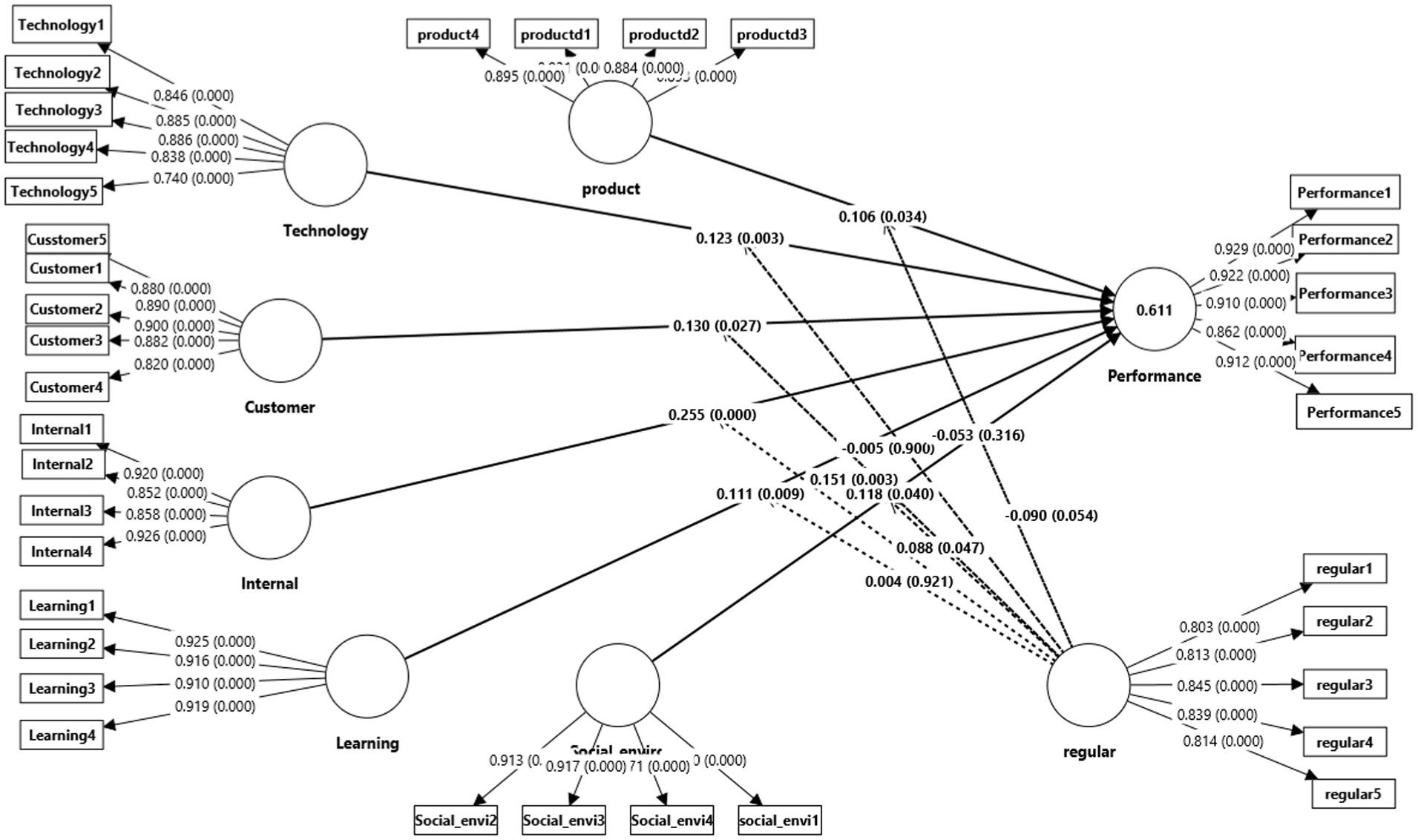

Structural Model

Once the data of the measurement model in PLS-SEM is verified to comply with the necessary criteria, the next step is to assess the structural model (shown in Figure 2). This evaluation starts with checking for potential collinearity. According to Hair et al. (2022), the variance inflation factor (VIF) values should have a desirable value of 3 or lower (Hair Jr, 2014). Table 6 shows that all values in the VIF construct are less than 3, and consequently, there is no collinearity among the predictor constructs. If collinearity is deemed not a concern, the next step is to evaluate the importance and relevance of the relations within the structural model through a bootstrapping process in PLS-SEM, based on 5,000 bootstrap subsamples. Structural model evaluation is conducted using typical measures, such as the coefficient of determination (R2), effect size (F2), and predictive relevance (Q2; Hair et al., 2019). As outlined in Table 6, the structural model accounts for 62.4% of the variance, demonstrating that the predictor variables significantly explain the outcome variables. The effect size (F2) analysis revealed varying levels of influence across constructs and scenarios. According to Hair et al. (2019), an effect size (F2) greater than 0.20 is considered satisfactory. From the results stated in Table 6, all value of F2 exceeds 0.20; hence, medium effect sizes were observed for all constructs.

PLS-SEM results.

Results of the Structural Mode Analysis.

In addition, due to the robustness of the PLS-SEM model in terms of all performance measures, the PLS-SEM model exhibits superior predictive performance (RMSE values that are either equal to or even better than those of the LM model). In addition, the relatively small MAE values indicate that PLS-SEM has systematically low prediction errors. In general, the findings confirm the appropriateness of PLS-SEM for predictive modeling in this application. In general, the findings reported in Table 6 demonstrate that the PLS-SEM model already possesses reliable predictive significance, suggesting it is a valuable tool for predictive modeling.

The last, but most crucial, is the assessment of the complete model fit status. According to Hair et al. (2019), the model fit is measured using the root mean square residual (SRMR) and normed fit index (NFI), with computed values of less than 0.05 and greater than or equal to 0.90, respectively. In this study, the SRMR value is 0.028, and the NFI calculated value is 0.901, which are within the threshold.

Hypothesis Testing

The research employed Smart PLS to identify the various dimensions that influence organizational Performance. Hypotheses are either supported or not supported using path coefficients, standard errors, T-statistics, and p-values in this section. Findings are therefore described as follows:

The first hypothesis is formulated to verify the relationship between customer orientation and Performance. As shown in Table 7, β = .129, T = 2.206, p = .027, and the F2 computed value is 0.28, revealing a medium-sized effect. Therefore, this means that customer-related factors have a meaningful influence on Performance, although not a very strong one. The finding is in line with the previous study findings (dos Santos et al., 2020; Guillem, 2020; Islam & Zhe, 2022; Mokhtaran & Komeilian, 2016).

Direct Relationships (Hypotheses).

On the other hand, this study on Table 7 revealed that internal processes demonstrated the highest influence on stable Performance of insurance companies (β = .253, T = 5.664, p < .001). The F2 value is 0.77, indicating a large effect size, which suggests that the performance improvement resulting from optimizing internal processes is highly significant. Similar findings were reported by Ahmeti et al. (2022), Anderloni et al. (2020), Cao et al. (2022), and Ogunwale et al. (2024), who indicated that streamlined operations play a key role in attaining strategic objectives. Furthermore, the learning and development dimension was positively linked to Performance (β = .111, T = 2.634, p = .078), as indicated in Table 7. A medium-sized effect has been observed, with an F2 value of 0.29, indicating that organizational learning and employee growth are significant factors. According to recent studies, knowledge-oriented abilities are considered the key drivers of stable organizational success (Al-Mutairi et al., 2021; Azizi, 2017; Choi & Jeong, 2022; Singhal et al., 2020).

Another intriguing hypothesis examined in this study is the correlation between Social and Environmental perspectives on the stable Performance of insurance companies. The results shown in Table 7 reveal β = .15, T = 3.035, p < .002, and F2 = 0.2. This implies that a growing emphasis on the role of sustainability and corporate social responsibility plays an important role in improving organizational outcomes. Studies by Alshadadi et al. (2024), Bressan (2023), Chiaramonte et al. (2020), Elshawarby (2018), N. C. Wang et al. (2022), and Wu et al. (2022) support this conclusion, advocating for the integration of social and environmental concerns into core business strategies. In addition, the study tried to see the relationship between technology and innovation in insurance companies and stable performance. According to Table 7, a significant positive effect on performance was recorded with β = .123, T = 2.97, p = .003, F2 = 0.21. This suggests that the role of technology adoption and digital transformation is essential in driving efficiency and competitive advantage. This result aligns with the findings of previous studies (Lanfranchi & Grassi, 2021; J. Liu et al., 2023; Neale et al., 2024; Xu & Hao, 2023).

Moreover, the factor of product diversification was found to have a significant and positive correlation with Performance, at β = .108, T = 2.123, p = .034, and F2 = 0.31. A broad range of products can significantly enhance Performance, as evidenced by Table 7. The finding is consistent with some recent studies by Cole and Karl (2016), C. Y. Lee (2017), Hsieh et al. (2015), Iability et al. (2008), Rathnasiri and Buddhika (2024), and Septina (2022), who emphasize the strategic role of diversification in managing risk and market exploitation.

Furthermore, according to Table 7, the R2 value is equal to .624, implying that the independent variables contained in the model explain 62.4% of the variability in the dependent variable. This which reflects a robust explanatory power for the, model as indicated by a close relationship between the variables under scrutiny. The findings thereby indicate that the proposed framework of study is well-structured and informative, particularly in revealing the nature of factors associated with the phenomenon under study.

Although the p-values establish statistical significance for these associations, examining the effect sizes (F2) provides greater insight into their practical significance. For example, Internal Process not only significantly impacted stable Performance (β = .253, p < .001), but it had the largest effect size (F2 = 0.77) in the model. Based on Cohen’s (1988) effect-size rules of thumb, this represents a huge effect, indicating that gains in internal process efficiency (e.g., claims processing and risk assessment) are not merely statistically significant but are a potent, primary driver of stable performance in the Ethiopian insurance environment. By contrast, although product diversification was significant (β = .108, p = .034), its medium effect size (F2 = 0.31) indicates that while good, it is less significant than core operational excellence. This enables managers to prioritize their strategic efforts more effectively more effectively.

Moderation Analysis

Smart-PLS moderation analysis in Table 8 yielded mixed results regarding the moderating effects of the regular environment construct on social/environmental, internal process, product, technology, learning and development, and customer perspectives on stable performance. Table 8 presents the results of the innovative PLS computing for the moderating variable in this analysis. Accordingly, the moderating role of legal environment between social/environmental perspective and stable performance of insurance companies is significant and positive at (β = .091, T = 2.005, p = .045), which is also like the customer orientation at (β = .118, T = 2.054, p = .040). This finding aligns with previous research findings (Etikan, 2024; Handoyo & Anas, 2024; Jung & Yoo, 2023). On the other hand, legal environment has a significant negative impact on the internal process interaction perspective facilitating the relationship between internal process and stable performance of insurance companies at (β = −.084, T = 1.903, p = .050) which is similar with the findings of (Siopi & Poufinas, 2023; Y. Pan et al., 2019). However, legal environment does not have moderating role in relationship of stable performance of insurance companies with product diversification (β = −.058, T = 0.994, p = .320); technology and innovation (β = −.007, T = 0.126, p = .900); and learning and development (β = .003, T = 0.099, p = .921). These findings are similar to those of previous research (J. Liu et al., 2023; Kihara, 2023; Rathnasiri and Buddhika, 2024).

Result of Moderation Analysis.

Note. SE = standard error.

An equally interesting finding is the non-significant moderation of the legal environment on the technology-innovation-stable performance relationship (p = .900). The implication of this result need not be that the legal environment is unimportant; indeed, it could imply several contextual realities in Ethiopia. The existing regulatory environment for Insurtech may remain in its infancy, neither significantly supporting nor strongly hindering innovation. Companies’ technological innovation might be more a function of internal strategic decisions and competitive forces rather than the existing legal environment. Likewise, the non-significant moderation of learning and development (p = .921) may indicate that these activities are primarily internal cultural processes, impervious to direct regulation at this time.

Results and Discussion

The study employs Smart PLS to identify the dimensions that influence organizational performance. The first hypothesis confirms the relationship between customer orientation and stable performance, with a medium-sized effect. On the other hand, Internal processes have the highest influence on the stable performance of insurance companies in Ethiopia, with streamlined operations playing a key role in achieving strategic objectives. Furthermore, the Learning and development dimension is positively linked to stable performance, with knowledge-oriented abilities being key drivers of stable organizational success. The study also examines the correlation between social and environmental perspectives on the stable performance of insurance companies, with a growing emphasis on sustainability and corporate social responsibility. In addition, innovative technology practices are essential for driving efficiency and competitive advantage, with a significant positive impact on the stable performance of insurance companies. Lastly, but not least, the findings of the study reveal that Product diversification has a significant and positive correlation with performance, with a broad range of products significantly enhancing stable performance. Moreover, as shown above, the study’s R2 value of .624 indicates that the independent variables explain 62.4% of the variability in the dependent variable, demonstrating strong explanatory power and a close relationship between the constructs in this research, thereby establishing a well-structured and informative framework.

Regarding the moderating role of the legal environment, the Smart-PLS moderation analysis yielded mixed results in insurance companies. The legal environment significantly moderates the relationship between social and environmental perspectives and customer orientation, while also affecting the interaction between internal process perspectives. However, it does not play a moderating role in the relationship between the stable performance of insurance companies and product diversification, technology and innovation, and learning and development, as per previous research.

Theoretical and Practical Implications of the Study

Theoretical Implications

The findings of this study bring significant theoretical implications for the BSC, DCT, and Contingency Theory. Since customer orientation and internal processes have been confirmed as critical dimensions influencing stable performance, this aligns with the emphasis of the BSC on integrating the customer, internal process, and learning perspectives in performance measurement. In addition, the impact of learning and development, as well as technology innovation, is that DCT remains relevant, demonstrating how organizations should adapt and leverage dynamic capabilities, including knowledge-oriented abilities and innovative practices, to attain a competitive advantage. Moreover, this research enhances Contingency Theory by proving that in an emerging economy, the external environment (in this instance, the legal environment) is not a uniform moderator across all strategy orientations. Its strong moderation on customer orientation, but lack of significant effect on technology, implies that the “contingency fit” is precise. This highlights a substantial conceptualization of the environment and suggests that the theory needs to account for the varying levels of maturity of different aspects of the institutional context. Additionally, by incorporating social and environmental concerns, our research extends the conventional balanced scorecard (BSC) framework to more clearly embed sustainability as a core dimension for long-term stable performance, as opposed to an ancillary view, which is especially essential for companies operating in developing economies with serious social issues.

Practical Implications

Additionally, the research has practical implications for managers, policymakers, and practitioners in the insurance industry. The findings reveal the following importance for customer orientation, internal processes, employee training, sustainability, technology innovation, and product diversification for the insurance industry. Furthermore, with its significant effect size (F2 = 0.77), its managers should first make investments in streamlining core internal processes. This involves introducing digital workflows for claims handling to decrease settlement time and leveraging more advanced data analytics for underwriting to enhance risk pricing precision. On the other hand, the strategic Adoption of Technology is necessary. That means instead of overall IT upgrades, companies need to concentrate on customer-oriented technologies such as mobile apps for policy access and simple claims submissions, capitalizing on the country’s high cell phone penetration to be more customer-centric. Moreover, policymakers and regulators (e.g., The National Bank of Ethiopia) should establish a Contemporary insurance Tech Architecture which enables overcoming the non-significant moderation effect of the legal environment on technology, policymakers need to develop a straightforward and conducive regulatory framework for digital insurance. This may involve the establishment of “regulatory sandboxes” to enable insurance providers to experiment with new technologies under controlled circumstances. Finally, to leverage the positive impact of social and environmental issues, the government may offer tax incentives or public recognition for insurance companies that introduce inclusive products for low-income individuals or invest in environmental projects.

Limitations and Future Research

Although this research provides a solid and practical framework for understanding stable performance in the Ethiopian insurance industry, it is worth noting that it has some limitations, which in turn present fertile ground for further research. First, the study’s cross-sectional design is a significant limitation. Although it establishes a good association between strategic orientations and stable performance at one point in time, it cannot positively infer causality. For example, more successful companies may be in a position to invest in learning and technology, and therefore, a possible bi-directional relationship exists. A longitudinal study would be highly valuable for future research, following these insurance organizations over numerous years to determine temporal precedence and observe how shifts in strategic orientations affect performance over time. Second, the use of employee percept data for all measures, including performance, is subject to a threat of common method bias and subjectivity. Subsequent studies may strengthen these findings by combining objective archival financial metrics (e.g., return on assets, market share, premium growth) with perceptual measures of performance to triangulate the measures. This might be further explored by employing a mixed-methods design, where qualitative in-depth interviews or case studies with high-level managers are used to reveal the subtle “how” and “why” underlying the statistical associations documented here. Third, the emphasis on the Ethiopian setting, though a central contribution, constrains the extensiveness of the generalizability of the results. The unique institutional and market conditions of Ethiopia can inform these relationships in distinctive terms. Comparative cross-country research can help validate the model’s validity in other emerging economies with dissimilar regulatory and competitive environments, thereby determining the comprehensive utility of the framework.

Footnotes

Acknowledgements

The researchers would like to thank employees and managers of insurance companies operating in Ethiopia for completing the distributed questionnaires.

Ethical Considerations

All procedures undertaken in this study with human subjects conformed to the ethical principles of the 1964 Helsinki Declaration and subsequent amendments or equivalent ethical standards. The study protocol was constructed to safeguard the anonymity and voluntary status of all participants. Since the study was conducted on a low-risk, non-invasive survey of professional personnel and did not gather sensitive personal information, it complied with the overall ethical principles for social science studies.

Consent to Participate

Informed consent was received from all individual participants that were part of the study. Each questionnaire had a cover letter describing the purposes of the research, that participation was voluntary, and that confidentiality and anonymity were guaranteed. Participants were assured that their answers would be aggregated and used solely for academic reasons, and that they could withdraw their participation at any time without consequence. The act of filling out and returning the questionnaire was taken as a sign of their agreement to take part.

Consent for Publication

It was made clear to all participants that the results of this study would be published in an academic journal. During the informed consent, they consented to the publication of the anonymized and aggregated data. The authors hereby attest that no individual data or information identifiable by a person are included within this manuscript.

Author Contributions

The article was drafted by a corresponding Author, who also did its conception, study design, data collection, analysis, and interpretation.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data is available as per required.