Abstract

Despite the positively significant evidence of the sustainability performance (SP)-financial performance (FP) association across various sectors, the empirical results from the banking industry are still inconclusive. This study, therefore, seeks to investigate the SP-Islamic banks’ FP relationship over a sample of 32 Islamic banks drawn from nine key jurisdictions in Islamic finance industry for the period from 2016 to 2021 using GMM estimator. We collected SP data by applying weighted content analysis method on the sustainability indicators developed by the GRI framework for the financial services sector index. This standard provides relevant items which helps measure financial institutions’ economic, social and environmental sustainability impact. Our results underline the existence of significantly negative impact of overall sustainability performance, social and environmental sustainability scores on Islamic banks’ FP. Moreover, the results show that the establishment of sustainability committee, experience of sustainability disclosure, and Islamic banks’ adherence to sustainable finance networks’ specifications do not significantly moderate the SP-Islamic banks’ profitability relationship. A key implication of this study is the imperative to establish effective Islamic banks-policymakers’ collaborations. This may ultimately create a conducive environment for better governance of Islamic banks’ sustainability strategies and better management of their various stakeholders’ interests. This, in turn, may help Islamic banks leverage their sustainability experience, better align their strategies with other sectors’ sustainability guidelines, and consistently steer their financial resources towards more sustainable projects, which may ultimately trigger a positive SP-FP relationship.

Keywords

Introduction

Banks are key players in the transition towards a sustainable economic system. With their intermediary role in the economy, and their capacity to create money and allocate credit to various economic sectors, banks can steer significant financial resources towards climate-resilient investments and mitigate systemic risk exposure of financial stability to climate and environmental shifts (Campiglio, 2016; Sustainalytics Thematic Research, 2014; Zimmermann, 2019). Banks can, therefore, leverage their position as intermediaries to reduce the sustainable finance (SF) gap (Campiglio, 2016), and exercise their power as advisors, and institutional investors to impel their clients to integrate sustainability criteria into their operational systems and business strategies (Dong et al., 2020; Z. M. Islam et al., 2012; Jo et al., 2015). As such, banks are constantly subject to supervisory control to show greater stewardship commitment to their borrowers’ environmental impact and substantive involvement in community development (Bose et al., 2018; Campiglio, 2016; Jo et al., 2015; Nizam et al., 2019).

At corporate level, borrowers’ unsustainable corporate conduct may undermine bank stability. Their linear business model which is more likely to increase their vulnerability and exposure to climate and environmental shocks may expose banks to insolvency risks due to extensive write-off of loan losses; negatively influence banks’ asset quality due to the loss of their ability to meet their financial obligations and collateral damage; decrease banks’ financial performance due to substantial counterparty risks, significant regulatory constraints and non-compliance fines; and increase the likelihood of bank runs due to substantial borrowers’ applications for new loans to reestablish their productive assets (Jo et al., 2015; Klomp, 2014). On top of that, banks may find themselves liable for their borrowers’ negative environmental impacts (liability risk; Jo et al., 2015). Accordingly, banks hold considerable reasons to manage and mitigate their sustainability risk exposure and integrate sustainability criteria into their credit allocation policy (Z. M. Islam et al., 2012; Jo et al., 2015).

Banks’ motives to integrate sustainability credentials into their corporate conduct and promote sustainable business models, therefore, vary considerably and range from strategic choice to regulatory compliance, social legitimacy, business stability and profitability to name few (Bose et al., 2018; Wu & Shen, 2013). SP and banks’ FP association, in particular, is an old yet a controvertible topic (Orlitzky et al., 2003; Wu & Shen, 2013) that is, the empirical results are, so far, controversial and inconclusive (Nizam et al., 2019). Prior studies report positive (Albertini, 2013; Bose et al., 2021; Dixon-Fowler et al., 2013; Torre Olmo et al., 2021; Weber & Chowdury, 2020), negative (Zhou et al., 2021), and non-linear (El Khoury et al., 2023; Trumpp & Guenther, 2017) relationship between SP and banks’ FP. Moreover, other publications control for several moderators namely, corporate governance structures (Adu, 2022; Jan, Marimuthu, & Hassan, 2019), quality of institutions (Khattak, 2021), and financial stability (Saadaoui & Ben Salah, 2023) and examine whether they may positively influence this relationship. It is noticeable, however, that past literature did not account for moderators that may determine and strengthen banks’ SP, and thenceforth, positively impact their FP.

Therefore, this paper aims to examine the impact of SP on Islamic banks’ FP across key jurisdictions in Islamic finance industry in light of good management, stakeholders, and institutional theories. It seeks specifically to identify whether the establishment of sustainability committee, experience of sustainability disclosure and Islamic banks’ membership in local and/or international SF initiatives may positively moderate the influence of SP on Islamic banks’ profitability. Their integration may help identify how SP flows towards Islamic banks’ FP. This may broaden the range of testable hypotheses and provide additional perspectives that may further help understand the dynamics of the SP-FP relationship.

Thus, this study adds to the body of knowledge on the impact of SP on Islamic banks’ FP by investigating whether sustainability committees, experience of sustainability disclosure, and Islamic banks’ membership in local and/or international SF initiatives may positively moderate this association. To the best of our knowledge, this is the first study to introduce such variables and examine their significance as moderators on the relationship between SP and FP. The recent development in the institutional environment of Islamic banks across the selected jurisdictions (i.e., the introduction of specific regulatory guidelines to strengthen banks’ sustainability disclosure, reinforce their environmental and social impacts, better manage their social and environmental risks, and set conducive framework for effective peer pressure outcomes) may improve Islamic banks’ sustainability practices, enhance their SP and therefore, positively influence their profitability.

Consistent with this, we introduce experience of sustainability disclosure as a potential moderator because it is a typical outcome of institutional pressures, that is, regulators’ mandatory requirements for financial institutions to report on their sustainability impacts and strengthen their SP. Better banks’ sustainability expertise may increase their management efficiency and boost their asset quality, and therefore, positively impact their FP. Similarly, the establishment of local professional networks and Islamic banks’ commitment to international sustainability certifications as a normative process may create strategic platforms for effective collaboration and better synchronisation of business focus with sustainability at local, national, and international levels. This will result in optimal resource allocation, better Islamic banks-policymakers’ collaboration, coordination and discussions and better management of implementation strategies (BNM, 2018; Kawabata, 2019). Hence, this normative isomorphism structure may positively moderate the relationship between SP and FP. The establishment of a sustainability committee, on the other hand, demonstrates Islamic banks’ shift towards more stakeholders’ perspectives of value creation. It exhibits the boards’ commitment to integrate, oversee, and monitor their sustainability impacts (Elmaghrabi, 2021). Moreover, SC increases the likelihood of board proactive involvement in sustainability issues, assists management in the development of relevant sustainability strategies, ensures effective implementation of sustainability strategies and practices, translates sustainability commitments, strategies, and guidelines into corporates’ key performance indicators, develops a relevant framework for effective social and environmental risk management, advises boards of directors on the appropriate measures for better alignment with regulatory stipulations (Homroy & Slechten, 2019; Maybank, 2021; Ricart et al., 2005; Shaukat et al., 2016), and therefore boost Islamic banks’ FP that may flow from better SP.

This paper, therefore, consists of four chapters in addition to the introductory one. Section 2 describes the theoretical background and set the testable hypotheses. Section 3 provides a description of data and empirical methodology. Section 4 outlines the study’s results and discusses their implications in line with our theoretical frameworks, whereas section 5 concludes the study and provides recommendations for Islamic banks and policymakers.

Literature Review and Hypothesis Development

Theoretical Framework

Prior studies made use of various theoretical frameworks to investigate the SP-FP association. These theoretical underpinnings seek to identify both the impact of the relationship and the direction of causality. Waddock and Graves (1997) report that the direction of causality is subject to the fundamentals of two major theoretical perspectives: (1) slack resource theory and (2) good management theory. The slack resource theory underlines that firms’ better FP is more likely to generate spare or additional resources that firms may allocate to improve their SP. Alternatively, Good Management theory establishes that good management practices have a positive correlation with FP. This is because organisations’ close attention to their social and environmental impacts may help their boards better manage their relationships with their major stakeholder categories, uphold their reputation and definitely generate better FP (Preston & O’Bannon, 1997).

As for impact, Vance’s trade-off hypothesis (1975) and the negative synergy theory suggest a negative SP-FP association (Jo et al., 2015). They argue that organisations’ responsible conduct may produce additional costs they might otherwise avoid or externalise in order to maintain their competitive advantage. This is in line with Friedman’s (1970) and neoclassical economists’ philosophy: the substantial expenses firms may incur as a result of integrating sustainability criteria into their business strategy is not consistent with the readily/instantly measurable financial and economic returns (Waddock & Graves, 1997). Stakeholders’ theory, on the other hand, assumes that SP has a positive impact on firms’ profitability. It claims that better incorporation of sustainability criteria into organisations’ business decisions indicates that they take their stakeholders’ interests into account in their management processes from both strategic and normative perspectives (Esteban-Sanchez et al., 2017).

Relationship Between Sustainability Performance and Banks’ Financial Performance

In line with stakeholders’ theory, Simpson and Kohers (2002) examine the impact of social SP on the FP of 385 banks in the US. Their OLS estimates document a positive relationship. On the same note, Esteban-Sanchez et al. (2017) investigate whether banks laid down a proactive approach to corporate social sustainability (CSP) and the extent to which this strategy mitigates the impact of the financial crisis of 2007 to 2008 on the decrease of banks’ FP. The determinants the authors use to measure banks’ social sustainability score include employee relations, community relations and product responsibility. Moreover, they introduce additional criteria to account for banks’ corporate governance (CG) structures. Their analysis spans 6 years (2005–2010) and includes 154 financial institutions from 22 countries. They discover that banks with superior CG practices and better employee relationships yield higher FP. Nonetheless, the introduction of ‘crisis’ as a moderator turns the effect to become negative for the former. This suggests a potential failure of banks’ CG structures. Furthermore, the research, in contrast to authors’ hypothesis, documents an insignificant or negatively significant relationship between product responsibility and banks’ FP.

Specific to environmental SP and its potential influence on FP in the financial services industry, Jo et al. (2015) report that better management of environmental sustainability may reinforce firms’ FP. This positive impact may result from investments in effective processes, mechanisms and tools that may ultimately help financial institutions minimise their environmental costs. Their analysis establishes that the reduction of environmental costs takes at least 1 or 2 years, whereupon firms can increase their return on equity. Moreover, they report that the decrease in environmental expenses has an immediate and significant influence on the profitability of financial institutions. This impact is more perceptible in sophisticated financial markets than less-developed financial systems.

In a similar vein, and in a more specific institutional context, Bose et al. (2021) examine the influence of environmental sustainability performance on banks’ FP in Bangladesh after the introduction of green banking regulatory guidelines by the central bank. The authors’ results show a significantly positive impact of environmental sustainability on banks’ profitability. More specifically, the study reports that cost efficiency is the key driver of this relationship.

Nizam et al. (2019), on the other hand, investigate the impact of social sustainability and environmental sustainability scores on corporate FP of 713 banks from 75 countries from 2013 to 2015. Their cross-sectional linear analysis, which controls for both bank-specific characteristics and macroeconomic variables indicates that access to finance – a proxy to social SP – has a significantly positive impact on banks’ FP in most estimates. Furthermore, their results document that management quality and loan growth are the channels through which positive value flows from access to finance to banks’ FP. As for environmental sustainability-banks’ FP relationship, the results show an insignificant or positively significant impact across their various estimates. Unlike access to finance, the environmental sustainability positive impact on banks’ profitability flows from loan growth only.

Torre Olmo et al. (2021) move the analysis a step forward and seek to examine how sustainability practices influence banks’ profitability and banks’ financial stability (insolvency risk) given the customers’ sceptical attitude towards banks after the global financial crisis of 2007 to 2008. They also investigate how and whether banks’ commitment to sustainability criteria defines the impact of market power and efficiency on banks’ FP. The authors find out first that sustainable banks generate higher profits relative to conventional banks. Moreover, they report that sustainable banks do not leverage their market power to increase their FP. Rather, they tend to boost their profitability by means of better reputation, different business culture, and effective stakeholders’ management. Finally, in accordance with the efficiency hypothesis, the results document that cost scale efficiency positively influences banks’ profitability for both sustainable and conventional banks regardless of the additional costs the former may incur in order to strike a balanced interplay of environmental and social sustainability and economic prosperity. In this respect, Bassen et al. (2006) and Clarkson et al. (2011) claim that the effective integration and implementation of sustainability strategies may boost sustainable banks’ reputation, which may in turn, reduce their cost of funds, on one hand, and uphold the industry’s sustainability standards/practices (normative pressures) on the other, which may definitely increase the competitors’ costs.

In light of legitimacy theory, Weber and Chowdury (2020) investigate the impact of the introduction of Environmental and Social Risk Management Guidelines in Bangladesh in 2011 on the SP-banks’ profitability association. The Granger causality test indicates a unidirectional causal effect that runs from SP to FP and not the other way around. Accordingly, the authors conclude that banks in Bangladesh are reactive to institutional pressures that require financial institutions to account for regulators’ sustainability guidelines. In other words, banks do not cultivate proactive conduct, that is, they do not strategically incorporate sustainability standards into their core business activities and do not steer part of their slack resources to enhance their SP.

Yin et al. (2021), on the other hand, apply the GMM method to 20 banks with various ownership structures from 2011 to 2018 to investigate the impact of green credit allocation on banks’ financial performance in China after the introduction of green credit policy in 2007 and green credit guidelines in 2012. Consistent with good management theory, the authors report that the green credit ratio positively influences banks’ FP.

Trumpp and Guenther (2017) contend that the main reason for the lack of a conclusive theoretical framework that may explain the controversial results of SP-FP associations is the dominance of linear models in previous studies. In line with this claim, El Khoury et al. (2023) conjecture that the influence of SP on banks’ FP follows a non-linear relationship. Their study covers the period 2007 to 2019 and their sample consists of 46 banks from Middle East, North Africa and Turkey (MENAT) region. Their results document that the impact of overall SP, social and environmental SP on banks’ FP is non-linear.

As for Islamic banks, literature that examines the SP-FP association is scant. Jan, Marimuthu, Bin Mohd, and Isa (2019) investigate the SP-FP relationship of Islamic banks in Malaysia over a 10-year period (2008–2017) in accordance with stakeholders’ theory. Commensurate with Platonova et al. (2018), Jan, Marimuthu, Bin Mohd, and Isa (2019) show that SP has a significantly positive impact on Islamic banks’ FP from both shareholders and management perspectives. However, this association does not hold true from the market perspective. Interestingly, Jan, Marimuthu, and Hassan (2019) replicate the same econometric model, but they posit that Shari’a governance and managerial ownership may positively moderate the relationship between SP and FP. Prior to the introduction of moderators, the results were similar to their previous study. Noteworthily, the insignificant SP-Islamic banks’ FP association from the market stakeholders’ perspective becomes significantly positive after the introduction of moderator variables. The effective involvement of Shari’a Supervisory Boards (SSB) in monitoring banks’ sustainable business practices may provide positive indicators or signals to market stakeholders. This may mitigate their reluctance and increase their confidence in Islamic banks’ ability to generate competitive financial returns via socially responsible conduct.

In this regard, Muhmad et al. (2021) provide evidence that Islamic banks with larger SSB show greater commitment to sustainability practices in comparison with their counterparts. Hence, they clearly corroborate the role of SSB in improving Islamic banks’ accountability towards sustainability impacts. Last but not least, Mallin et al. (2014) investigate the CSR-Islamic Banks’ FP relationship of 90 Islamic banks across 13 countries from different jurisdictions. Their three-stage least square estimation documents a unidirectional causality that runs from banks’ profitability to sustainability disclosure practices. This is more consistent with slack resource theory.

Keeping that in mind and in line with Stakeholder, good Management and Stewardship theories, we formulate our hypotheses as follows:

H1: Overall sustainability performance has a positive and significant impact on Islamic banks’ financial performance.

H2: Economic sustainability performance has a positive and significant impact on Islamic banks’ financial performance.

H3: Social sustainability performance has a positive and significant impact on Islamic banks’ financial performance.

H4: Environmental sustainability performance has a positive and significant impact on Islamic banks’ financial performance.

Moderator Variables

The Establishment of Sustainability Committee

SC as a board structure may moderate the relationship between SP and Islamic banks’ FP. The introduction of SC at board-level shows organisations’ commitment and accountability towards their various stakeholders’ demands, or rather, their willingness to allocate resources for better stakeholder management (Elmaghrabi, 2021; Ricart et al., 2005; Velte, 2016), their dedication to balance the interplay of financial, social and environmental sustainability (Liao et al., 2015; Velte & Stawinoga, 2020), and their due diligence to set effective communication processes and networks to better discuss sustainability issues with their stakeholders (Cui et al., 2018; Ricart et al., 2005). Moreover, The SC helps establish a company-wide sustainability governance structure; integrate sustainability criteria into business practices; develop, execute, monitor, and assess organisations’ sustainability strategies, guidelines, and policies; establish sustainability risk management control systems that will govern organisations’ management of environmental, climate and social risks; facilitate organisations’ alignment with regulatory ecosystem development; and oversee, manage, and report on their sustainability performance (Maybank, 2021). Bearing this in mind, the effectiveness of SC may strengthen Islamic banks’ reputation, establish and reinforce their corporate image, and uphold their customers’ loyalty, and thus, contribute to boosting their FP. On account of this, and in accordance with stewardship and resource dependence theories, we may conjecture that SC may positively moderate the relationship between SP and Islamic banks’ profitability. Therefore, our fifth testable hypothesis (H5) related to the moderating effect of SC is as follows:

H5: SC positively moderates the relationship between SP and Islamic banks’ FP.

Islamic Banks’ Experience of Sustainability Disclosure

Consistent with institutional theory, Li (2020) claims that organisations with more experience of sustainability disclosure are more aware of their sustainability impacts, show better transparency of their corporate sustainability practices, and they are more able to identify their purpose statements in relation to sustainable development. Moreover, more years of sustainability disclosure may enable corporates’ managers to better figure out, respond and manage their various stakeholders’ interests, help boards of directors consistently take sustainability issues into consideration in their discussions, and derive relevant data about how to better integrate sustainability criteria into their business strategies. This may ultimately reinforce their SP (Jia & Li, 2020), which in turn may spur their FP. Profitability in this respect may result from organisations’ cost-scale efficiency (Torre Olmo et al., 2021), a decrease of their exposure to environmental and climate risks/costs (Jo et al., 2015), and income that may flow from environmental and climate-resilient investments. Accordingly, we expect the experience of sustainability disclosure to moderate the SP-Islamic banks’ FP association positively; thus, our sixth hypothesis is set as follows:

H6: Experience of sustainability disclosure positively moderates the relationship between SP and Islamic banks’ FP.

Islamic Banks’ Membership in Sustainable Finance Networks

Sustainable finance networks (SFN) act as catalysts that may reinforce organisations’ SP. Kawabata (2019) documents a positive and statistically significant impact of financial institutions’ involvement in SFN on their commitment to mobilising additional financial resources towards climate-resilient investments. In addition, other studies (Bose et al., 2018; Contreras et al., 2019) report that peer pressure or normative isomorphism is an effective mechanism that may increase banks’ willingness to improve their sustainability disclosure or performance and enhance their self-governance or rather self-regulation with respect to responsible investments. SFN help banks strengthen their institutional capacities in relation to sustainability practices, better integrate sustainability criteria into their business strategies and set appropriate control systems to better assess banks’ progress in their implementation process of SF guidelines. Moreover, they provide financial institutions, FI, with appropriate prospects for policy alignment with sustainable and responsible finance guidelines. Specifically, they can unite financial institutions with policymakers to better discuss their sustainability transition, improve their sustainability practices, and contribute to developing relevant or applicable sustainability policies and regulations (Kawabata, 2019; Setyowati, 2023). Islamic banks can leverage on this policy alignment to minimise their transaction costs, maintain and uphold their regulatory legitimacy/compliance, reinforce their resilience to climate and environmental shocks, sustain their social legitimacy and ultimately, reinforce their FP. Hence, our seventh hypothesis related to Islamic banks’ membership in SFN is as follows:

H7: Membership in SFN positively moderates the relationship between SP and Islamic banks’ FP.

Data and Empirical Methodology

Empirical Strategy

To estimate our model and examine the impact of SP on Islamic banks’ FP, we apply a two-step system Generalised Method of Moments estimator. Our empirical specifications for the dynamic panel data analysis are as follows:

where i, j and t indicate Islamic bank, country, and time, respectively; Y is the Islamic bank’s financial performance; SP denotes Islamic banks’ sustainability performance. It includes the overall sustainability score and its components, that is, economic, social and environmental SP; B and M are vectors of bank-specific and country-level control variables that may determine Islamic banks’ profitability. Bank-specific determinants consist of capitalisation, asset quality, management efficiency, liquidity, bank size and business model, whereas country-specific variables include GDP Growth, inflation, and concentration.

Two Step System GMM

The underlying reasons to apply the dynamic system GMM estimator in our empirical analysis are threefold. First, to account for banks’ profitability persistence over time and overcome the endogeneity bias problem. Berger et al. (2000) document that the persistence of banks’ FP may stem from imperfect market competition, informational opacity and regional/macroeconomic shocks. Accordingly, Blundell and Bond (1998) propose to introduce the lagged dependent variable as a regressor to help control for both issues. Second, several determinants of banks’ profitability (e.g., capitalisation) are endogenous variables (Athanasoglou et al., 2008). Unlike other alternative estimation methods, the system GMM approach enables researchers to instrument for endogenous determinants, and thus, produce consistent estimates. Moreover, this method is ideally set to control for the endogeneity bias that may result from the short macro panel data that may, in turn, create inconsistency issues to the estimates (Lee & Hsieh, 2013). Finally, since other alternative estimation methods are vulnerable to omitted variable bias, should the model fail to introduce some important determinants of Islamic banks’ FP into the vector of explanatory variables, the system GMM technique is more reliable. This method is robust, and therefore, helps avoid this problem (Hesse & Poghosyan, 2016).

Data

Our study examines the SP-FP association of 32 Islamic banks from key jurisdictions in the Islamic finance industry from 2016 to 2021. Refinitiv’s assessment of the global Islamic finance industry performance across key indicators or parameters (quantitative development, knowledge, governance, awareness, and CSR) reveals that the selected jurisdictions hold their positions in the top 15 countries throughout the research period (Refinitiv, 2021). Furthermore, they account for around 67% ($2.3 out of 3.4 trillion) of Islamic finance assets in 2020 (IFDI, 2021). Table 1 below shows the list of jurisdictions, the sample of Islamic banks and the number of observations across the study period. Our sample consists of 192 bank-year observations for 32 Islamic banks drawn from nine jurisdictions from 2016 to 2021.

sample of Islamic Banks by Country.

Dependent Variable

Banks’ survival, business continuity, expansion and market competitiveness are dependent on their ability to yield competitive returns on their assets and capital. For the purpose of this study, we use return on average equity (ROAE) as our primary metric for Islamic banks’ FP since sustainability considerations (particularly environmental and climate risks) are more relevant to shareholders and investors (Kawabata, 2019).

Independent Variables

To collect sustainability data, we apply the Weighted Content Analysis Method (WCAM) to the GRI financial services sector index across Islamic banks’ annual and sustainability reports. This technique provides a wider range of dummy codes that extends beyond a typical [0 1] interval, allowing for a more accurate assessment of Islamic banks’ SP. Commensurate with (Jan, Marimuthu, Bin Mohd, & Isa, 2019; Jan, Marimuthu, & Hassan, 2019), we apply a dummy interval of [0 2] whereby we allocate a dummy code of ‘0’ to an item if a bank does not report on it, ‘1’ if a bank shows a partial disclosure of an item, or ‘2’ if a bank’s disclosure exhibits a measurable impact on its SP (monetary, weight, volume etc.).

Jan, Marimuthu, Bin Mohd, and Isa (2019), Jan, Marimuthu, and Hassan (2019) introduced several Islamic banks’ specific characteristics into the GRI financial services sector index to make it more relevant to their business operations. This index involves 65 items divided into four dimensions, namely, integrated sustainability strategies (7 items), economic sustainability (10 items), social sustainability (36 items) and environmental sustainability (12 items). Our investigation will disregard the first dimension and consider closely the other three pillars (Table 2).

Definition of Variables and Sources of Data.

Control Variables

Bank-Specific Variables

Capitalisation

Capitalisation measures banks’ ability to manage, or rather, absorb shocks or losses on their balance sheets that could otherwise increase their exposure to insolvency that is, raise their risk of bankruptcy. Prior studies are inconclusive and do not provide unequivocal results in relation to capitalisation-banks’ FP association. Better capitalisation may indicate lower banks’ risk exposure (Bourke, 1989; Demirguc-Kunt & Huizinga, 1998), better protection of banks’ equity (Milne & Whalley, 1998), and access to cheaper sources of funds (Bourke, 1989), and so banks are more likely to reduce their cost of capital and improve their FP (Pasiouras & Kosmidou, 2007; Revell, 1980). Moreover, market participants may interpret banks’ higher capital buffers as an indicator of boards’ willingness to use banks’ own funds to expand their capacity and/or modernise or streamline their facilities/infrastructure to become more efficient, reinforce their competitive position, and thus, increase their profitability. Conservative banks, on the other hand, may underutilise their funds due to their risk-averse behaviour (Dietrich & Wanzenried, 2011), incur additional costs (Milne & Whalley, 1998), and hence, negatively affect their FP. Accordingly, we cannot predict the impact of capitalisation on Islamic banks’ FP. Capital ratio is measured as the ratio of common equity to total assets.

Asset Quality

Asset quality assesses banks’ exposure to specific risks relevant to their borrowers’ financial health, creditworthiness and FP, that is, it measures banks’ credit quality. We use NPL over Gross Loans as a proxy of asset Quality. Banks with higher exposure to credit risk that is, weaker asset quality, should increase their provisions for bad debts (M. Islam & Rana, 2017). This may have a detrimental influence on banks’ capital, reduce loanable resources and accessible credit limits and hence, reduce their FP (Brock & Rojas Suarez, 2000; García-Herrero et al., 2009; sIslam & Rana, 2017). Therefore, the smaller the NPL, the better the banks’ asset quality, and the more profitable the banks are.

Management Efficiency

Our proxy to Islamic banks’ management efficiency is the cost-to-income ratio. The lower the ratio, the more efficiently banks utilise their resources, and the better their FP (Athanasoglou et al., 2008; Hesse & Poghosyan, 2016). Thus, we expect an inverse relationship between Islamic banks’ inefficiency and their FP.

Liquidity

To assess the liquidity of our sample of Islamic banks, we use the ratio of liquid assets over deposits and short-term funds. It demonstrates whether banks can manage the risk of unexpected withdrawals from a significant number of depositors and investors or the risk of bank runs. Liquidity-banks’ profitability relationship is inconclusive (Ben Lahouel et al., 2024). On the one hand, the more liquid the banks are, the better their liquidity management control system, and therefore, the better their FP (Hesse & Poghosyan, 2016). Moreover, Berger et al. (1995) claim that banks with substantial liquid assets can leverage on the positive perception they may gain from participants in fund markets to reduce their cost of funds, and therefore, increase their profitability. On the other hand, highly liquid banks may experience opportunity costs due to the relatively lower liquidity premium of their liquid assets. In other words, higher banks’ liquidity may have adverse impact on banks’ interest margins, and hence, negatively influence their profitability (Ben Lahouel et al., 2024). As a result, we cannot set a clear prior expectation of liquidity and Islamic banks’ profitability association.

Bank Size

Size is a common determinant of banks’ profitability. Several studies claim that the larger the banks, the more they can leverage economies of scale (they can collect and process relevant information to banks’ business strategy at lower costs due to better operational efficiency); the more they can diversify their loans across various sectors and regions and differentiate their products (i.e., they are more able to reduce their exposure to liquidity shocks) and thus, the more profitable they are (Regehr & Sengupta, 2016). Product differentiation, market diversification and relatively lower risks may enable banks exercise their power and reinforce – in line with the relative market power (RMP) hypothesis – the transmission mechanism from market structure (more market concentration) to FP. Specific to Islamic banks, several studies document a positive relationship between bank size and Islamic banks’ FP (Alharbi, 2017; Alharthi, 2016; Bashir, 2003; Čihák & Hesse, 2010; Haron, 1996). Hence, we may anticipate this positive correlation to persist.

Business Model

We introduce business model to control for the impact of revenue diversification on banks’ profitability and account for economic heterogeneity across the country. Banks’ income/revenue consists of traditional or interest income that includes gross interest revenues and investment securities; and non-traditional or non-interest income that comprises ‘fees and commissions revenues from credit derivatives, custody and administration of securities, underwriting operations, placement of securities and financial structure consultancy services, and asset management’ to name a few (Brighi & Venturelli, 2016). Previous works demonstrate that banks’ diversification into non-interest income may reinforce their stability and profitability (Ahamed, 2017; Junttila et al., 2021; Köhler, 2015; Mergaerts & Vander Vennet, 2016). Albertazzi and Gambacorta (2010) and Bolívar et al. (2023) claim that internationalisation strategies, the development of fintech, regulatory changes and demand composition have reinforced competition and reduced the interest margins and spurred banks to diversify their sources of revenues and strengthen their efficiency in production and distribution. Consistent with prior studies, we use the ratio of non-interest income over total operating income as a proxy for banks’ business model.

Country-Specific Variables

GDP Growth

Banks’ profitability fluctuates over the business cycle. Therefore, it is crucial to control for banks’ exposure to economic activity and introduce GDP growth in our model. Companies in stages of cyclical booms or expansion are more likely to increase their demands for banks’ credit. Banks can therefore expand their portfolio and leverage on the rise of interest rates with less probability of default rates to enhance their profitability (Athanasoglou et al., 2008). As a result, several studies report a significantly positive impact of GDP growth on FP (Albertazzi & Gambacorta, 2009; Dietrich & Wanzenried, 2011; Pasiouras & Kosmidou, 2007). Alternatively, in periods of contraction and downturns, banks may experience a deterioration of their credit quality, and thus, negatively influence their FP. Moreover, Albertazzi and Gambacorta (2009) claim that macroeconomic shocks and financial crises influence banks’ profitability. They underline that banks’ FP is procyclical because GDP affects both interest income and loan loss provisions.

Concentration

Bank concentration in accordance with the World Bank definition is the fraction of bank assets held by the three largest commercial banks in a country. Concentration and banks’ profitability relationships are complex and subject to various factors, such as bank size and the competitive environment in which banks operate (particularly the barriers to entry) (Gilbert, 1984) to name a few. Commensurate with the RMP hypothesis, higher concentration can lead to a significant increase in the FP of largest banks. This is because larger banks can leverage economies of scale and scope in their operations, and therefore, they can exercise their market power, drive their interest rates up and thus earn supernormal profits (Demirguc-Kunt & Huizinga, 1998; Nizam et al., 2019). As for competition, studies report inconsistent results. While Mirzaei et al. (2013) claim that higher market concentration may have a negative impact on market competition, and hence, drive banks’ profitability up, other studies (Heggestad & Mingo, 1976) report that, with consistent increase in market concentration, competition will decrease, banks’ levels of services will drop and thus, negatively affect banks’ FP.

Inflation

Demirguc-Kunt et al. (2004) report that inflation exerts a robust positive impact on banks’ cost of financial intermediation. Moreover, several studies (Albertazzi & Gambacorta, 2009; Bourke, 1989; Molyneux & Thornton, 1992; Pasiouras & Kosmidou, 2007) document a significantly positive impact of nominal inflation rates on banks’ FP, that is, increase in banks’ income with inflation outpace banks’ costs. However, this impact is dependent on banks’ perfect prediction of inflation dynamics. Banks’ better expectation of inflation movement results in an effective anticipation of the interest rates margins, and therefore, maintain/sustain banks’ real profits (Perry, 1992). In other words, banks’ failure to [fully] anticipate inflationary environments creates a delay in interest rate adjustment, and hence, negatively influences banks’ profits.

Descriptive Statistics

Table 3 exhibits the descriptive statistics of dependent, independent, and control variables across the 192 bank-year observations.

Descriptive Statistics.

Table 3 below shows that Islamic banks’ profitability ratio (ROAE) ranges from a minimum value of −15.17% to a maximum value of 32.66% with a standard deviation of 7.22 and a sample mean profitability ratio of 13.08%. As for sustainability performance, it is noticeable that the variability or the variance of the environmental sustainability score is the greatest, and its mean score is the lowest. Moreover, it can be clearly seen that the mean overall, social, and environmental sustainability scores, that is, 0.38, 0.33, and 0.28, are rather or somewhat low. This indicates that Islamic banks should develop their sustainability roadmap and better integrate sustainability criteria into their business strategy.

With respect to bank-specific control variables, Table 3 indicates that the sample mean capitalisation, Asset quality, management efficiency, liquidity and business model are 10.04, 3.15, 44.56, 13.94 and 19.42, respectively. Islamic banks’ size ranges from US$1.35bn to US$165.96bn with a mean value of US$12.88bn. As for country-level variables, we can observe that the average GDP growth across jurisdictions is 1.98% whereas the mean concentration and inflation rates are 63.5% and 1.48%, respectively.

Correlation Matrix

To test whether a multicollinearity issue exists in our dynamic regression model, we derive a correlation matrix of our explanatory variables. As Table 4 below shows, our Pearson correlation coefficients between predictor variables are small (the highest is .584 between INF and GDP growth), that is, they are not equivalent to or higher than .8 (Akoglu, 2018), and therefore, the test fails to detect the existence of a multicollinearity problem in our model.

Correlation Matrix.

Note:***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

Empirical Results and Discussion of Findings

The Impact of SP on Islamic Banks’ Profitability

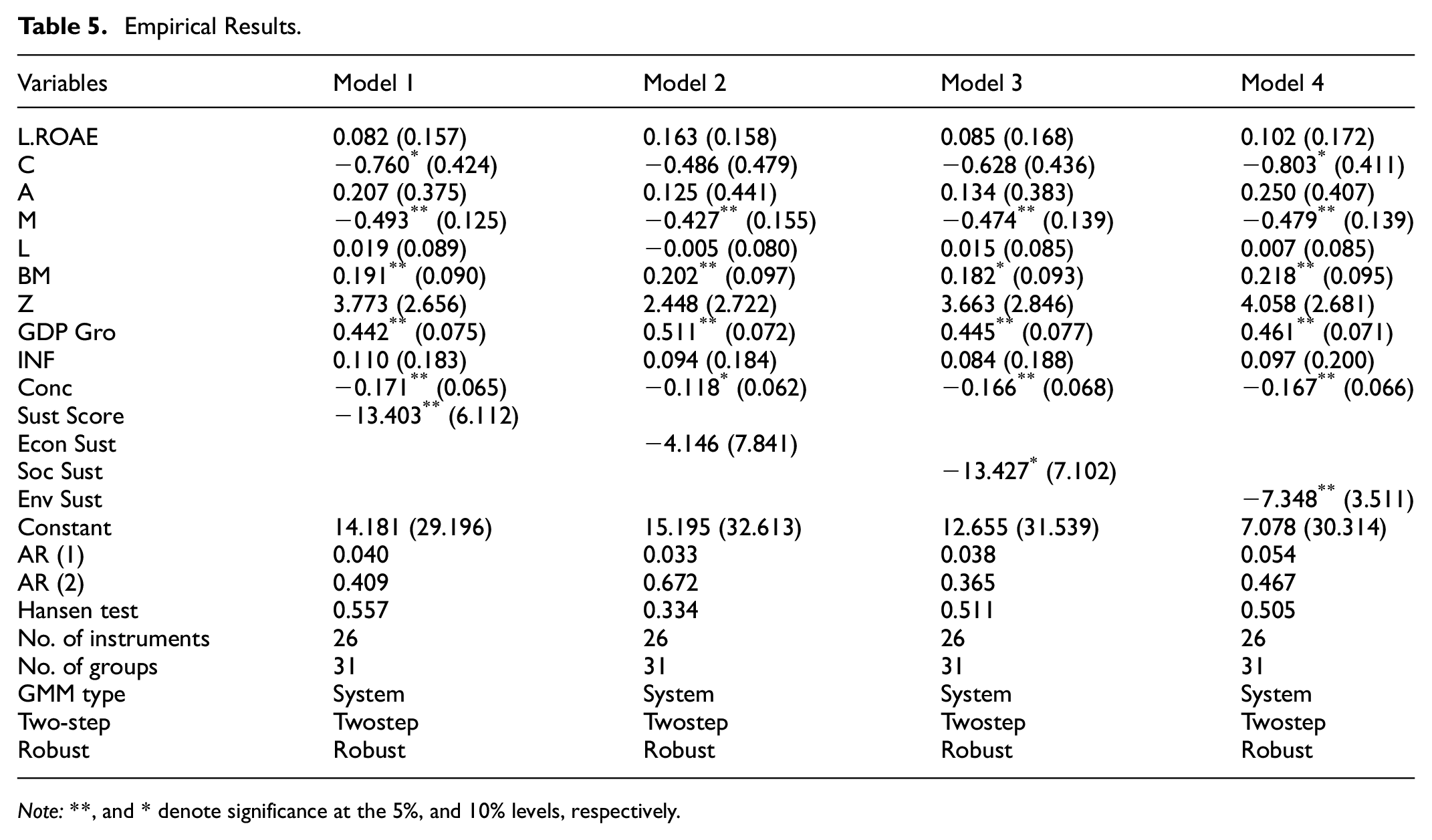

Table 5 below shows that overall sustainability, social sustainability and environmental SP – in contrast to our expectations – are statistically significant but negatively related to Islamic banks’ FP (consistent with Lin et al., 2019; López et al., 2007; Moore, 2001; inconsistent with Platonova et al., 2018). Therefore, we do not find support for H1, H2, H3 and H4.

Empirical Results.

Note:**, and * denote significance at the 5%, and 10% levels, respectively.

Our results trigger several courses of interpretation. First, it reinforces the trade-off and negative synergy predictions of a negative SP-FP association. Moreover, it lines up with the neo-classical economists’ perspective of value creation, which underlines that socially dependable conduct at corporate level may generate additional and substantial costs that will ultimately offset or diminish the foreseen financial and economic benefits (Lin et al., 2019; Waddock & Graves, 1997). This hypothesis sides with Friedman’s (1970) position and supports Vance’s (1975) and Moore’s (2001) results in which they report that organisations with better sustainability credentials experience a downward pattern of stock prices and profitability in comparison to market averages.

Second, consistent with our results, that is, low mean environmental and social sustainability scores, Trumpp and Guenther (2017) indicate that companies with low SP, particularly environmental sustainability scores, experience a negative SP-FP relationship. Conversely, they document a positive environmental SP-FP association for organisations that were able to show notable environmental sustainability scores. With better experience of sustainability management, more exposure to sustainability networks’ certifications and effective integration of SC into their CG structures, Islamic banks can improve their SP, and therefore, positively influence their FP.

Finally, the integration of sustainability criteria into Islamic banks’ strategies is more likely to produce changes in their company-wide governance structures and management systems, which may ultimately cause a reallocation of available resources in their capacity as intermediaries, advisors, head of supply chain, and institutional investors (López et al., 2007) and may, therefore, negatively affect their FP in the short-run. In other words, Islamic banks need a transition period to lay down their purpose or mission statement in relation to sustainability transition (identify the most relevant sustainability criteria to which they will pay more attention), set effective internal policies to better respond to their institutional and SF frameworks and guidelines, promote and/or hire relevant people to better monitor the transition towards better sustainability practices, develop marketable financial instruments for sustainable development, closely monitor other sectors’ shift towards more responsible investments, and manage or reconcile the possible mismatch in stakeholders’ interest in the short-term (Lin et al., 2019). This transformation and its positive implications on Islamic banks’ operating efficiency requires significant upfront costs that could lead to short-term financial losses.

As for bank-specific control variables, while management efficiency is significantly and negatively related to Islamic banks’ profitability across the four models, business model has a positive and statistically significant impact on Islamic banks’ FP across the four models too. Capitalisation on the other hand, shows a negative and statistically significant association with Islamic banks’ profitability in models 1 and 4. However, Islamic banks’ asset quality, liquidity, and size are positive but statistically insignificant. In relation to country-specific indicators, results in Table 5 document a significantly positive impact of GDP growth on Islamic banks’ profitability across the four models, whereas concentration is negatively associated with Islamic banks’ FP. Finally, our estimates report that inflation does not determine Islamic banks’ FP.

Moderating Effect

The specification for models 1, 2, 3 and 4 in Tables 6 to 8 are the same except that we introduce SC, Islamic banks’ membership in international and/or local SF initiatives and Islamic banks’ experience of sustainability disclosure into our equation to test whether they may positively moderate the SP-FP association. Our dynamic estimation results in Tables 6 to 8 show that the establishment of SC, Islamic banks’ commitment to SF Networks’ certifications and Islamic banks’ experience of sustainability disclosure do not significantly moderate the relationship between SP and Islamic banks’ profitability. Accordingly, we do not find support for H5, H6 and H7.

The Moderating Effect of Sustainability Committee.

Note:**, and * denote significance at the 5%, and 10% levels, respectively.

The Moderating Effect of Islamic Banks’ Experience of Sustainability Disclosure.

Note:**, and * denote significance at the 5%, and 10% levels, respectively.

The Moderating Effect of Professional Networks.

Note:**, and * denote significance at the 5%, and 10% levels, respectively.

Consistent with Kashi et al. (2024) who reveal a significantly positive impact of SC and better experience of sustainability disclosure on firms’ SP; and in line with Trumpp and Guenther’s (2017) affirmations, we may offer a couple of policy and managerial implications. Policymakers in Islamic finance jurisdictions should enhance their sustainability and SF-specific regulatory ecosystem to streamline sustainability practices, establish relevant SP matrix or impact metrics, standardise Islamic banks’ disclosure structures and practices (better to comply with international industry standards) and constantly assess banks’ progress towards better sustainability disclosure. In addition, more regulatory incentives for Islamic banks to subject their business operations to global SF networks’ specifications; and regulators’ commitment to establish effective local sustainability/SF initiatives may – ultimately – have positive impact on Islamic banks’ SP. Both measures will help better monitor Islamic banks’ shift towards more sustainable business conduct, increase Islamic banks’ experience of sustainability disclosure and strengthen the effectiveness of their sustainability control management systems, and hence, help their boards perform better from the financial point of view.

From the managerial perspective, Islamic banks’ boards – particularly in GCC countries – should establish an SC and integrate it in their organisational and CG structures. They should define clear fit and proper criteria for effective selection of its members; grant more authority to SC to develop, oversee and monitor banks’ sustainability strategies; allocate the necessary resources to better fulfil their responsibilities/obligations (this includes resources for continuous development of their expertise, knowledge and exposure to sustainability and SF issues); and assess whether it diligently exercises its authority/power and effectively employs corporate’s resources to strengthen Islamic banks’ SP, and thus, their FP.

Robustness Check

To test the robustness of our results, we introduce an alternative measure for Islamic banks’ FP and re-estimate our dynamic panel data model. This robustness analysis supports our results and reinforces their reliability. Table 9 above provides a summary of the results of our alternative analysis across the four models.

Robustness Check – Alternative Measure of Islamic banks’ profitability.

Note:**, and * denote significance at the 5%, and 10% levels, respectively.

The use of ROAA as an alternative measure to Islamic banks’ FP provides support to our previous results. To illustrate, – similar to our results in Table 5 overall sustainability, social sustainability, and environmental sustainability scores have a significantly negative impact on Islamic banks’ profitability.

Conclusion

This study investigates the SP-Islamic banks’ FP association across key jurisdictions in Islamic finance industry. Previous studies failed to integrate the determinants of SP and investigate whether they may positively moderate the relationship between SP and Islamic banks’ profitability. Therefore, we seek to better figure out the dynamics of this association and expand the range of testable hypotheses in this respect.

In order to achieve the study’s objectives, we use a system GMM estimator and account for both bank-specific variables and country-specific or macroeconomic indicators. Moreover, we gradually introduce moderators into our model to potentially acquire additional perceptions about this association.

We can categorise our results into two main parts. First, it is clearly evident that SP, specifically overall sustainability score, social sustainability, and environmental SP are statistically significant and negatively related to Islamic banks’ FP. This is consistent with the trade-off hypothesis and negative synergy theory. In addition, low mean environmental and social sustainability scores of our sample of Islamic banks may also explain this negative association (consistent with Trumpp & Guenther, 2017). On top of that, in line with Jo et al. (2015), better integration of sustainability criteria into financial institutions’ business strategies requires time and resources that could trigger negative FP in the short run.

Second, with the introduction of sustainability committee, Islamic banks’ commitment to sustainability/SF networks’ specifications, and their experience of sustainability disclosure as potential moderators, the relationship between SP and Islamic banks’ FP became positive but statistically insignificant. In other words, countries’ institutional factors and CG structures are yet to moderate the SP-FP association for Islamic banks.

The study’s results have implications for Islamic banks, and policymakers across the selected jurisdictions. Islamic banks should set their purpose statements and clearly identify their contribution to sustainability transition; embed relevant processes that will ensure better identification, assessment, measurement, deliberation, mitigation or promotion of their positive and negative impacts; establish effective company-wide sustainability governance structures, particularly, the establishment of SC to better manage, oversee and monitor their sustainability frameworks; develop appropriate guidelines to determine, assess, deliberate, and mitigate their own and borrowers’ sustainability risks; equip Islamic banks’ staff, that is, boards of directors, executive management, Shari’a boards, and others, with relevant knowledge, capacities, and expertise to better drive banks’ sustainability transformation; develop marketable financial instruments that will promote their sustainability impacts; closely monitor and adapt to non-financial sectors’ shifts towards sustainable and responsible conduct that is, develop or inspect specific sector guides; and develop performance matrix and impact metrics consistent with international industry standards (this will ultimately enhance their expertise and experience of sustainability disclosure.

Regulators, on the other hand, should consistently develop the SF ecosystem and account for Islamic banks’ gradual integration of sustainability criteria into their credit allocation policies. This requires strategic coordination and collaboration between Islamic banks and policymakers. Moreover, it may help avoid any inadvertent consequences of counter-productive policies and regulations (Nizam et al., 2019). On top of that, they should set appropriate macroprudential regulations and monetary policies that may incentivise Islamic banks to decarbonise their balance sheets and spur their involvement in climate-resilient investments (Campiglio, 2016; D’Orazio and Popoyan, 2019; Esposito et al., 2019).

Islamic banks-policymakers effective collaboration may ultimately create a conducive environment for better governance of Islamic banks’ sustainability strategies and better management of their various stakeholders’ interests. This may help Islamic banks reduce their costs of sustainability transformation, leverage their sustainability experience, better align their strategies with other sectors’ sustainability guidelines and consistently steer their financial resources towards more sustainable projects, which may ultimately trigger a positive SP-FP relationship.

Notwithstanding the contribution of the study to literature, future studies can tackle a few noteworthy limitations, providing further insights into the dynamics of SP-FP associations. First, the lack or rather the unavailability of sustainability data in some jurisdictions, specifically, Oman and Indonesia and the small sample size. The recent development of institutional framework in Oman and the enhancement of sustainability disclosure in Indonesia and other key Islamic finance jurisdictions may help overcome this shortfall, increase the number of banks subject to analysis and ultimately generate more robust and generalisable results as to the impact of SP on Islamic banks’ FP. Second, several Islamic finance jurisdictions lack active local SF initiatives, and few Islamic banks show commitment to the specifications of international SF networks. Accordingly, our results on whether Islamic banks’ adherence to local and international SF networks’ specifications can positively moderate the relationship between SP and their profitability is inconclusive. With more involvement of Islamic banks in global sustainability certifications and their commitment to establishing more effective local networks, this normative structure may have a positive moderating effect on the relationship between SP and FP. Finally, several Islamic banks claim in their sustainability reports that digitalisation has become a major determinant of their sustainability credentials. However, data available – so far – on their digitalisation levels is relatively scarce. Hence, future research can leverage on greater disclosure in this respect and investigate its moderation effect on the relationship between SP and their profitability.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors extend their appreciation to the Deanship of Scientific Research, King Faisal University for funding this research work through project number KFU252649.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analysed during the current study.