Abstract

The rising popularity of environmental, social, and governance (ESG) investing is prompting private and public sectors to enhance their ESG performance and achieve financial stability. Urging the importance, past research has revealed how stakeholders gradually rely on firms’ ESG disclosures to assess performance and make well-informed financial decisions, yet understanding the nexus between ESG performance and financial stability remains scattered. Unlike previous reviews, this paper thoroughly investigates the relationship by synthesizing 140 articles published between 2011 and 2023. In doing so, this review maps out the scholarly contributions of almost 200 researchers across 40 countries, with about 40% of the studies featuring cross-country analyses. The review identifies that no past studies rely on a single theory to outline ESG disclosure; instead, they mostly underpin multiple theoretical bases, including agency theory, legitimacy theory, stakeholder theory, signaling theory, resource-based view, risk management theory, institutional theory, etc. Also, it points out diverse critical factors influencing ESG performance, such as environmental uncertainty, political and legal environments, ownership structures, board characteristics, and investment efficiency. Contributing to the growing body of ESG literature, this review offers valuable insights into deepening our understanding of ESG performance and financial stability, facilitating future improvements in ESG reporting frameworks. Moreover, it outlines notable future research directions to enrich this evolving research field.

Keywords

Introduction

Over the past decade, many financial organizations have consistently emphasized reducing the risk associated with Environmental, Social, and Governance (ESG) practices, prioritizing these practices while making critical business decisions. ESG principles help organizations mitigate potential risks and positively impact their long-term environmental and social well-being (L. Wang & Yang, 2023). Given that, globally, scholars have urged taking rapid action and prioritizing ESG-related considerations in line with ESG principles (Abdul Razak et al., 2023). Businesses can enhance long-term financial stability toward more sustainable practices, prioritizing ESG performance by considering their value-creation activities with the Sustainable Development Goals, and integrating ESG issues under consideration (Alfalih, 2023; Danisman & Tarazi, 2024). Highlighting this importance, firms’ higher management is recommended to provide sufficient information about ESG opportunities and risks so that stakeholders can make well-informed investment choices (Landi & Sciarelli, 2019).

In recent times, the world has seen a surge of awareness regarding sustainability and ethical business practices, with substantial attention to ESG performance (Barros et al., 2024). Evidence proves that integrating ESG principles into corporate strategies significantly improves organizational reputation and financial performance (Pérez-Cornejo & de Quevedo-Puente, 2023). For instance, companies with strong ESG performance often show strong stock liquidity (Meng-tao et al., 2023), superior financial results (Ben Ali & Chouaibi, 2024), and increased shareholder wealth (Parikh et al., 2023). However, global challenges like social inequality, climate change, and governance ethics become more demanding and push stakeholders (e.g., firms, governments, and investors) to realize and comply with the factors influencing ESG performance (Sharma et al., 2020). While prior research has established a broad association between ESG performance and financial stability, a deeper examination of how individual ESG components, environmental (E), social (S), and governance (G) distinctly influence financial resilience remains underexplored (Z. Chen et al., 2024; Saharti et al., 2024). For instance, environmental stewardship (E) may mitigate regulatory and physical climate risks, thereby reducing long-term volatility in cash flows, whereas robust social practices (S) can enhance customer loyalty and employee productivity, indirectly stabilizing earnings. Meanwhile, effective governance (G), through transparency and accountability, may lower financing costs by attracting risk-averse investors (Chowdhury et al., 2023). This paper’s bibliometric analysis not only maps the evolution of this interdisciplinary field but also highlights thematic clusters that dissect these granular linkages, such as studies connecting carbon emissions to credit risk or board diversity to bankruptcy probability, offering a more nuanced understanding of ESG’s role in safeguarding financial systems. Hence, firms must take into account the significance of ESG issues in their strategic business frameworks to warranty a long-term corporate sustainability.

A significant amount of prior literature has underscored valuable insights into ESG performance (Galletta et al., 2022; Jain & Tripathi, 2023; S. S. Senadheera et al., 2022). For example, M. Saini et al. (2023) performed a thorough examination using bibliometric techniques to investigate the correlation between ESG practices and economic performance. Khan (2022) applied bibliometric and meta-analysis methods to explore the connection between ESG disclosure and firm financial performance. Similarly, Seow (2024) and Del Gesso and Lodhi (2024) conducted a thorough literature review to detect emerging trends in ESG performance, highlighting the contribution of sustainability reporting in corporate strategy and long-term performance across various sectors. However, Khaw et al. (2024) investigated the significant determinants of ESG considerations, including a bibliometric analysis and systematic literature review, highlighting the potential research gaps and future research directions. In most of these previous reviews, ESG considerations have been viewed mainly from a financial performance, risk-taking behavior, and sustainable perspective, neglecting the association between ESG performance and financial stability (Ding et al., 2025; Lokuwaduge & Heenetigala, 2017; Naeem et al., 2022). Furthermore, ESG practices connecting with corporate finance vary from financial and non-financial institutions, which also requires a deep understanding, as the current body of knowledge is still fragmented. Additionally, there is a lack of information in existing research about the impact of investment efficiency and ESG issues on company capital regulation, risk, and performance in developing and developed nations, which also requires further investigation.

To address these gaps, this review aims to bridge the gap by thoroughly navigating the relevant existing literature and mapping out the influence of ESG practices on financial stability. To accomplish this, a systematic review of 140 selected studies on ESG performance published between 2011 and 2023 was carried out. The results reveal a diverse range of widely recognized and less conventional theoretical approaches that inform ESG performance, thereby providing a foundation for future scholarly inquiry. Specifically, the findings of this review address the following questions:

This study contributes valuable insights into existing literature on sustainable corporate finance areas. Through a comprehensive scientometric analysis, it has successfully identified the key authors, different types of journals, institutions, and countries. The study meticulously explored the conceptual frameworks of the field, identifying key research streams and highlighting the crucial relationship between (1) ESG performance and firm performance, (2) ESG performance and firm risk, (3) ESG performance and investment efficiency, (4) ESG performance and cost of capital, (5) ESG performance and innovation efficiency, (6) firm-specific characteristics and ESG performance, and (7) corporate governance and ESG performance. Furthermore, the study conducted a comprehensive meta-analysis, pinpointing research gaps, outlining future research directions, and summarizing empirical findings from earlier literature. Ultimately, the study presents a robust research framework designed to significantly benefit researchers in sustainable corporate finance. Moreover, the outcomes may guide enterprises to navigate the compatible scenery of corporate sustainability and financial stability, contributing to well-being and long-term sustainability for all stakeholders.

The rest of the study is structured as follows: Section “Theoretical framework” shapes the methodology, Section “Research methods” presents the bibliometric analysis, Section “Bibliometric analysis” explains the meta-analysis, Section “META analysis” discusses future research guidelines according to the most recent literature, and Section “Future research directions” displays the conclusion.

Theoretical Framework

This section explores the fundamental theories that form the substance of the theoretical framework in the literature of sustainable finance. Sustainable finance is grounded in several key concepts that explain how ESG performance influences financial decision-making, firm performance, and long-term sustainability. These relevant theories are as follows:

Stakeholder Theory

Stakeholder theory, primarily proposed by Edward Freeman in 1984, highlights that firms must ensure the interests of the stakeholders, including investors, customers, suppliers, employees, communities, and society as a whole. Stakeholder theory suggests that companies should highlight sustainability and positive, robust ESG performance, which can decrease the information asymmetry between management and shareholders. According to sustainable business performance, stakeholders are classified as individuals and groups who can impact or be impacted by a firm’s performance (Freeman, 1984). The theory confirms that prioritizing ESG performance in companies’ strategic decision-making helps in meeting regulatory demands, increasing the firm’s reputation, reducing environmental risks, and ultimately improving financial performance. Providing valuable insights, the theory states that ESG performance influences firms’ risk-taking and financial stability, complying with regulatory requirements and expectations of environmentally aware stakeholders, especially in the financial sector (Zahid et al., 2023).

An effective management strategy provides some competitive advantages, highlighting ESG performance, which ensures stakeholders’ satisfaction and trust in firms’ commitment to sustainable business practices. It reduces firm capital costs, offering less risky and favorable rates to potential investors (Fandella et al., 2023). Alfalih (2023) conducted a study on ESG disclosure and financial performance and found that the firms concentrate on sustainable business practices, getting positive feedback, and investors’ trust. Similarly, S. Chen et al. (2023) and Z. Wang and Sarkis (2017) demonstrate that superior ESG performance is related to better financial and market outcomes, while Sassen et al. (2016) highlight that high ESG performance reduces operational risks and improves a company’s resilience against market fluctuations. Moreover, strong ESG practices meet stakeholder expectations and ensure sustainable business success, reducing overall costs and risk-taking behavior (DasGupta & Roy, 2023; Ding et al., 2024; C. Zhao et al., 2018).

ESG practices have been gaining traction in most developed and developing countries to boost firm performance and improve overall financial stability (Atellu & Muriu, 2022; Ramzan et al., 2021). Indeed, most of the recent literature has extensively investigated the consequences of ESG performance in reflecting how well a company meets the needs and prospects of its stakeholders in case of the association between ESG performance and firm risk-taking (Izcan & Bektas, 2022), creditworthiness (Kanno, 2023), cost of capital (Y. Chen et al., 2023), green innovation (F. Zhang et al., 2020), innovation efficiency (Wan et al., 2024), firm value (Aydoğmuş et al., 2022), and firm financial performance (El Khoury et al., 2023; Xie et al., 2019). However, stakeholder theory highlights the significance of ESG performance with firm capital efficiency, cost efficiency, and investment efficiency. It also did not highlight the connection between ESG performance and capital regulation, which plays an important role in maximizing the organization’s profit.

Legitimacy Theory

Legitimacy theory, first articulated by organizational theorists Max Weber and later expanded by scholars like Suchman (1995) and Dowling and Pfeffer (1975), posits that organizations seek to support their operations with societal values and norms to be perceived as legitimate by their stakeholders. Legitimacy theory states that institutions should maintain a commitment to stakeholders by doing environment-friendly business operations (Naeem et al., 2022; Xie et al., 2019). Trust is paramount in the financial sector, confirming accountability and transparency, which satisfy the stakeholders’ demands and community development. Legitimacy theory offers valuable insights into understanding the comprehensive structure to investigate the association between ESG factors, risk-taking, and financial performance (J. Chouaibi et al., 2024; Y. Liu et al., 2021). According to the theory, financial institutions should maintain ethical labor behavior, adopt diversity, engage in community development, and enhance customer satisfaction by creating a public image, attracting customer loyalty, and sustainable business performance (Ersoy et al., 2022; Hwang et al., 2021; Imperiale et al., 2023).

ESG performance establishes organizational legitimacy, which in turn ensures investment and capital efficiency, reducing financial and external environmental risk (N. Zhang et al., 2023; Zhou et al., 2023). Many studies were conducted in financial and non-financial sectors considering corporate governance and sustainable environmental practices, reducing carbon emissions, and implementing different types of green projects (Galletta et al., 2023). However, some initiatives ensure fair labor practices, community participation, and engagement with local communities, creating more resilient and socially responsible businesses (Trinh et al., 2023). Moreover, robust ESG performance and governance frameworks, emphasizing transparency, accountability, and ethical conduct to encounter governance-related issues like fraud, scandals, and regulatory penalties, help to significantly mitigate operational and compliance risks (Di Tommaso & Thornton, 2020; S.-P. Lee & Isa, 2024). Legitimacy theory is significant in understanding the alignment of financial practices and societal expectations to promote sustainable long-term success between ESG performance, firm risk-taking, and financial performance.

Agency Theory

Agency theory, first developed by Meckling and Jensen (1976), highlights the potential conflict of interest between agents (management) and principals (shareholders) within the organization, which discusses the existence of agency problems because of the ownership and separation of control in different companies. The theory underscores that managers wish to prioritize their demands over those of shareholders, causing agency costs, consisting of bonding, monitoring, and residual losses (H.-M. Chen et al., 2022). These costs are borne by shareholders, resulting from pursuing actions that benefit themselves at the cost of shareholders’ wealth maximization (Elmghaamez et al., 2024). This dynamic highlights the significant relationship between the two parties to reduce agency costs, ensuring sustainable managerial decisions to achieve shareholders’ objectives.

In agency theory, moral hazard is another key concept that occurs when more information to the agent (management) than to the principal (shareholders) due to information asymmetry (Ellili, 2022; Zamir et al., 2022). Overall, agency theory demonstrates a valuable understanding of the branches of corporate governance and the potential challenges of integrating shareholders’ and managers’ interests, particularly sustainable business performance and long-term value creation (W. Luo et al., 2023). Sometimes management emphasizes short-term profit maximization to increase their interest, but shareholders expect long-term value creation, which may create conflict between them (Zheng et al., 2023). The agency theory remains the dominant framework in governance and corporate finance, highlighting the accountability of management to satisfy the shareholders’ interests. This theory has also been criticized for its narrow emphasis on economic and financial sustainability, neglecting broader concerns such as ESG performance that are becoming dominant in modern corporate performance assessments (Al-Hiyari et al., 2023; D. Liu et al., 2023).

Resource-Based View (RBV)

RBV theory originated from “The Theory of the Growth of the Firm” (1959) and was developed by Jay Barney, offering valuable insights about non-substitutable resources to achieve competitive advantages within companies to reduce external uncertainties. According to the theory, financial organizations adopt ESG performance with the strategic resources that ensure corporate reputation and operational efficiency for sustainable corporate investment (Weber, 2017). Strong ESG practices make an organization suitable for investment opportunities from its competitors, offering valuable resources that are difficult to replicate (Azmi et al., 2021).

Furthermore, robust ESG performance allows business organizations to utilize their intangible assets to enhance sustainability, reducing reputational risks that ultimately confirm overall financial stability (Forgione et al., 2020; Y. Liu et al., 2022). ESG practices in financial and non-financial institutions safeguard against environmental uncertainties and global pandemic crises, mitigating risk and ensuring financial stability (H.-M. Chen et al., 2022). Establishing strong ESG performance, based on the RBV theory, provides a valuable understanding of the relationship between ESG practices and firm financial risk and performance (Alfalih, 2023; N. Saini et al., 2022). Ultimately, organizations legitimate their operations, leveraging valuable resources, mitigating operational risks, and achieving a sustainable competitive advantage in the industry (Azmi et al., 2021). Moreover, the national circumstances could affect how firms in each country leverage their ESG performance to improve investment efficiency and financial performance in response to crises like COVID-19.

Institutional Theory

Institutional theory, proposed by Selznick (1949) and was later expanded by DiMaggio and Powell (1983) in their persuasive paper “The Iron Cage Revisited.” The theory posits how norms, rules, and institutional pressure shape the adoption of the institutional environment. However, institutional environments are different in different countries in terms of regulatory frameworks, cultural norms, and societal expectations. This theory confirms that institutional pressure is significant for gaining legitimacy and securing resources. Based on ESG performance, financial and non-financial institutions are influenced by regulatory frameworks, industry policy, and societal values to adopt sustainability practices (Forgione et al., 2020; Paltrinieri et al., 2020).

Considering environmental uncertainties, financial and non-financial institutions integrate institutional norms, leverage unique resources, and enhance legitimacy, reducing reputational risks, increasing stakeholder trust, and improving overall economic stability. However, strong ESG performance safeguards against environmental uncertainties, significantly influencing (Y. Liu et al., 2022). ESG performance affects risk and performance, offering a comprehensive framework for understanding the institutional theory, legitimizing their operations, leveraging valuable resources, conforming to institutional norms, reducing risk exposure, and enhancing their financial outcomes, thereby achieving a sustainable competitive advantage in the industry (Ahmad et al., 2021; Nirino et al., 2022). These differences present a theoretical gap in understanding how institutional pressures ensure financial stability, with the effects of environmental volatility and external threats.

Signaling Theory

Signaling theory, introduced by Michael (1973) in “Job Market Signaling,” underscores how institutions promote quality and intentions to stakeholders using signals. Considering ESG performance, financial and non-financial organizations utilize these signals to ensure commitment to business ethics and long-term sustainability (Wan et al., 2024). Reducing information asymmetry, these signals influence stakeholders’ views and build trust to establish ESG performance, which confirms competitive advantages, attracting customers, investors, and other stakeholders, prioritizing efficient decision-making (S. Chen et al., 2023; Maji & Lohia, 2023).

The theory, also called disclosure theory, allows an organization to be efficient in communicating to stakeholders about its commitment to corporate sustainability and ESG performance. The theory orders information disclosure, promoting sustainable performance to meet legal obligations and sustainable business finance for long-term success. Healy and Palepu (2001) argue that optional reporting can enhance statutory financial reporting by offering further insights into a company’s expected financial performance. However, Grinblatt and Hwang (1989) suggest that these signaling tools may act as substitutes, implying a negative link between voluntary disclosures and the use of mandatory financial reports as signals. Furthermore, Meng-tao et al. (2023) provide new insights that promote ESG performance through a comprehensive understanding of signaling theory, organizations inspire good signals to potential investors, and improve public image in emerging economies.

Research Methods

Database, Keywords, and Filtering Criteria

To fulfill the research objectives, the authors examined all studies that investigated the relationship between ESG performance and financial stability, selecting an unbiased and reliable source for data extraction. To do that, the authors have selected the Scopus database, which is a trusted tool for Meta-analysis and bibliometrics because of its wide-ranging coverage of publishers and its neutrality toward any specific publisher (Galletta et al., 2022; Gao et al., 2021; Jain & Tripathi, 2023; Khan, 2022). Khan (2022) further demonstrated the superiority of Scopus and offered additional evidence, providing its broader coverage of titles in Oncological journals compared to the Web of Science (WOS).

In the next phase, the authors adopted the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) approach. The approach helps reviewers systematically conduct well-structured and focused literature reviews (S. Senadheera et al., 2024). In this research, the PRISMA review process was carried out in line with its four guiding steps: (1) identification, (2) screening, (3) eligibility, and (4) inclusion (see Figure 1).

PRISMA flow chart (Authors’ creation) 2250 × 3250 (300 dpi).

Using sustainable finance, the authors conducted a wide-ranging literature review and identified a particular set of keywords, including “ESG,”“ESG performance,”“ESG disclosure,”“ESG score,”“ESG ratings,”“Environmental, social and governance,”“Environmental, social and governance performance,”“CSR,”“Corporate social responsibility disclosure,” and “CSR disclosure,” and “firm performance” or “risk” to search for relevant articles. The search using these keywords yielded 1,501 articles published until 2023. This is because recently published articles (e.g., after 2023) require more citations to assess their authenticity and academic impact (Khan, 2022). Given that, the authors deliberately excluded articles published after the year 2024. It is essential to note that this research encompasses only published articles related to English in the fields of Accounting, Management, Business, Econometrics, Economics, and Finance.

After conducting an initial exploration, the authors have successfully extracted 1,105 papers published from 2011 to 2023, excluding the articles that are not journal articles, not related to the subject areas, and not published in English. The authors have established rigorous inclusion and exclusion criteria to sort these documents efficiently, following the past review studies (Khan, 2022; Khaw et al., 2024). Also, the authors have specifically chosen the standard followed by the EU policy, a widely recognized and respected definition of sustainable finance provided by Khan (2022), who states, “Sustainable finance is understood as finance to support economic growth while reducing pressure on the environment and also taking into account social and governance aspects as well.”

This study utilized all available ESG rating documents to comprehensively analyze firm-specific performance indicators. Studies focusing on sustainable and responsible investment (SRI) mutual funds and portfolios were deliberately excluded from the research to ensure that only those analyzing firm-level performance indicators were considered. The final dataset of 396 articles was chosen for bibliometric analysis, as labeled in Table 1 and Figure 1. For bibliometric analysis, Donthu et al. (2021) argued that there is no specific sample recommendation. However, Rogers et al. (2020) suggested a minimum sample of 200 articles. From this point, our review’s sample for bibliometric analysis surpasses the recommended threshold. To ensure the quality review, the authors used the Journal Guide list of the Australian Business Dean Council and selected articles from journals rated A or above. Given many documents, the authors screened for articles relating to sustainable business finance based on the abstract readings, resulting in 140 articles being retrieved and reviewed for meta-analysis.

Search Measures and Results

Analysis and Synthesis Methods

The first step in this process involves conducting a bibliometric analysis, which utilizes a scientometric examination of published papers and citations to effectively assess their impact (De Giuli et al., 2024; Khan, 2022). This approach is rapidly emerging in the field of corporate finance (Baker et al., 2021), enabling researchers to achieve a deeper grasp of the prominent patterns in recent literature and identify the most significant authors and journals. By analyzing the conceptual structure literature, researchers can effectively identify the most important themes and ideas currently driving research in this field. Based on previous literature (Akomea-Frimpong et al., 2022; Del Gesso & Lodhi, 2024; Khan, 2022; M. Saini et al., 2023; Seow, 2024), the authors have conducted a comprehensive bibliometric analysis using widely accepted tools such as VOSviewer. The analysis was conducted across four aspects: bibliometric citation investigation, bibliometric co-authorship investigation, keyword investigation, and bibliographic coupling with content analysis (Kalia & Gill, 2023; Khaw et al., 2024).

In the second part, a meta-analysis was conducted for each research direction recognized by bibliographic connection. It is widely accepted that meta-analyses are essential in economics and finance, especially in controversial areas (Guerrero-Villegas et al., 2018; Khan, 2022). For instance, earlier studies mainly focused on the ESG disclosure-financial performance and CSR-firm risk nexus (Khan, 2022; Orlitzky & Benjamin, 2001), sustainability and financial Performance (Atz et al., 2023), factors influencing ESG performance (Khaw et al., 2024), ESG-risk nexus (De Giuli et al., 2024), Corporate governance and risk management (Kalia & Gill, 2023), and ESG-financial variables nexus (M. Saini et al., 2023). The meta-analysis provides generalized findings from these conflicting results, which are instrumental in guiding policy decisions and future research.

Bibliometric Analysis

This part presents the results of the bibliometric analysis. Bibliometric analysis is a part of the quantitative research method for analyzing a field of study, incorporating diverse techniques such as citation, co-citation, bibliographic coupling, co-author, and co-word analyses (F. Luo et al., 2022). These techniques have been applied to identify influential research works in diverse fields, such as economic development and construction safety (F. Luo et al., 2022) and AI-based customer relationship management (Ozay et al., 2024). Furthermore, the meta-analysis effectively determined each cluster’s research gaps and future directions.

Number of Publications

Figure 2 clearly illustrates a steady increase in publications discussing ESG scores as a reliable measure of sustainability. It’s worth emphasizing that sustainability was a fairly new concept, with only two articles published in 2011. Still, it has since gained notable attention following the implementation of EU Directive 2014/95, which made it a legal requirement for large companies to reveal non-financial information publicly (Khan, 2022). The article explores the development of environmental indicators aligned with social and governance measures to evaluate ESG performance, a crucial aspect of evaluating a firm’s financial stability.

Growth of the journal.

Literature Co-Authorship Analysis

Co-authorship by Authors

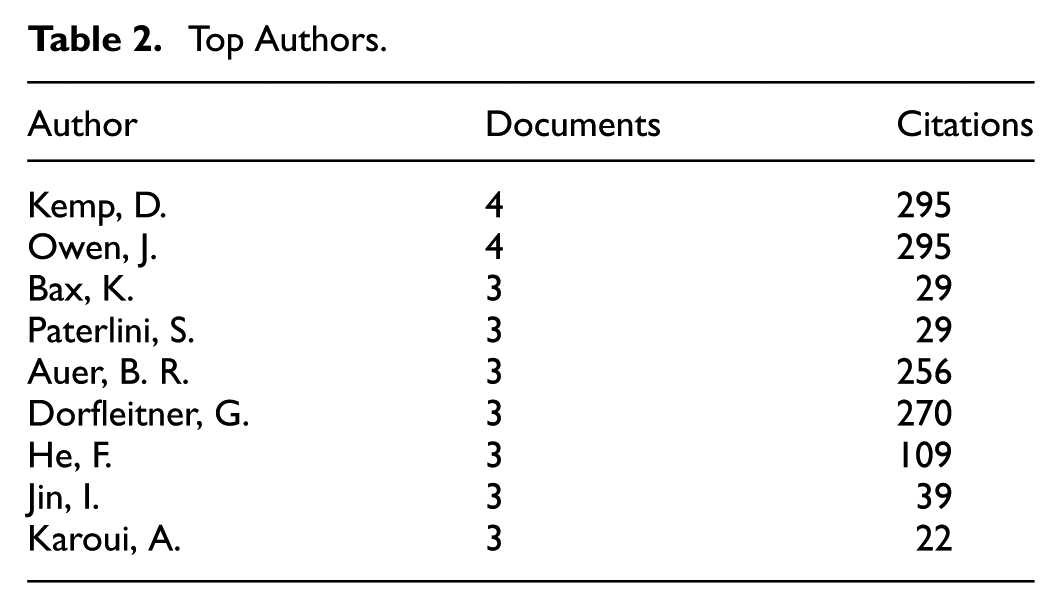

Table 2 lists the top nine authors who have contributed the most to writing ESG-related articles. Kemp, D., and Owen, J. are positioned at rank number one with four documents under their name. After that, contributions from Dorfleitner, G., Auer, B. R., He, F., Jin, I., Bax, K., Paterlini, S., and Karoui, A. have three articles, as all the authors have gathered under the top nine productive authors through total citations. Figure 3 visualizes the networks of researchers working on ESG indicators, as highlighted through VOSviewer.

Top Authors.

Science mapping of co-authors by authors.

Affiliation by Organizations

Ten of the 21 research affiliations by different organizations are presented according to several articles and citations. The School of Finance of “Capital University of Economics and Business” has the most articles (Documents 5). In contrast, the International School, Vietnam National University, and Stern School of Business at New York University in New York are the top institutions based on the citation (Citations 208 and 183; see Table 3 and Figure 4).

Top Affiliation by Organizations.

Science mapping of affiliation by organizations.

Co-Author by Countries

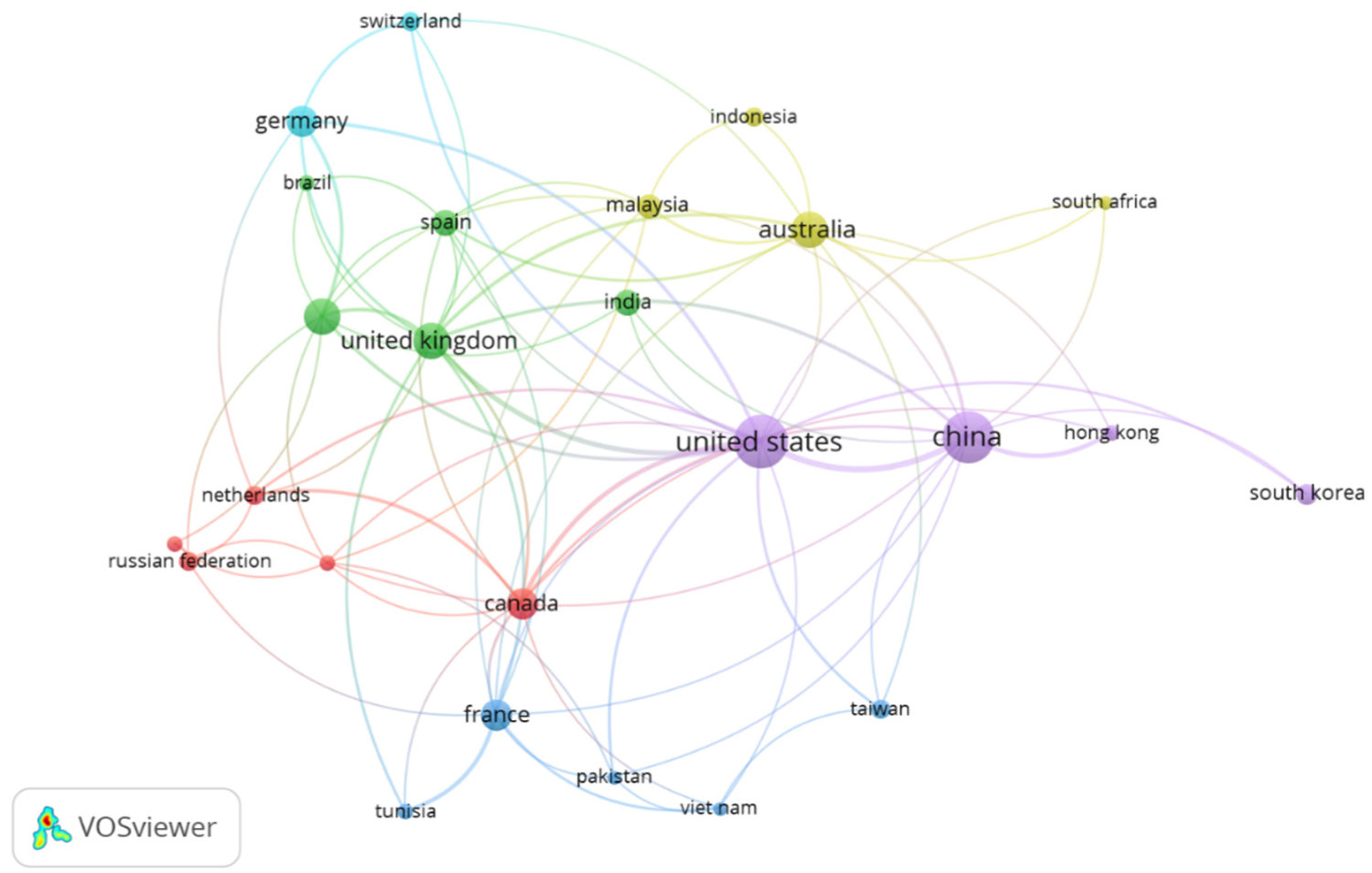

Table 4 lists countries studying ESG investing as a proxy of corporate business sustainability and its impact based on related papers. The list includes EU member countries, with notable contributions from Italy, France, Germany, and Spain. The United States leads the list of 72 articles. Among the Asian countries, China and India have made significant contributions to the literature. Some countries, such as Canada and Australia, have produced few articles but have a high average citation count, indicating strong influence.

Active Countries for ESG Literature.

Figure 5 visualizes the countries’ networks in this particular research field. The analytic requirements were strict, necessitating that each country produce a minimum of three publications, each of which had to have at least 25 citations. Out of the 25 countries evaluated, only ten met these rigorous requirements.

Red cluster: Canada, Netherlands, and the Russian Federation

Green cluster: United Kingdom, India, Spain, and Italy

Blue cluster: Germany and Switzerland

Yellow cluster: Malaysia, Australia, South Africa, and Indonesia

Purple cluster: China, South Korea, Hong Kong, and the United States

Science mapping of co-authors by countries.

Co-Occurrence of Keywords

To understand the thematic evolution of sustainability-related literature, the authors conducted a new network visualization inquiry of high-rate keywords, setting the minimum existence criterion to three. This analysis, shown in Figure 6 and Table 5, helps identify key research topics within the field (Khan, 2022). The literature commonly features the keywords “corporate social responsibility” (115 times), “ESG” (80 times), and “sustainability” (33 times). This suggests that the literature often uses ESG indicators or ratings to proxy for CSR or sustainability. “Environment” and “Social” occurred 18 and 13 times, respectively, while the word “Governance” occurred 12 times.

Most Repeated Keywords.

Science mapping of co-occurrence by keywords.

Citations of Articles

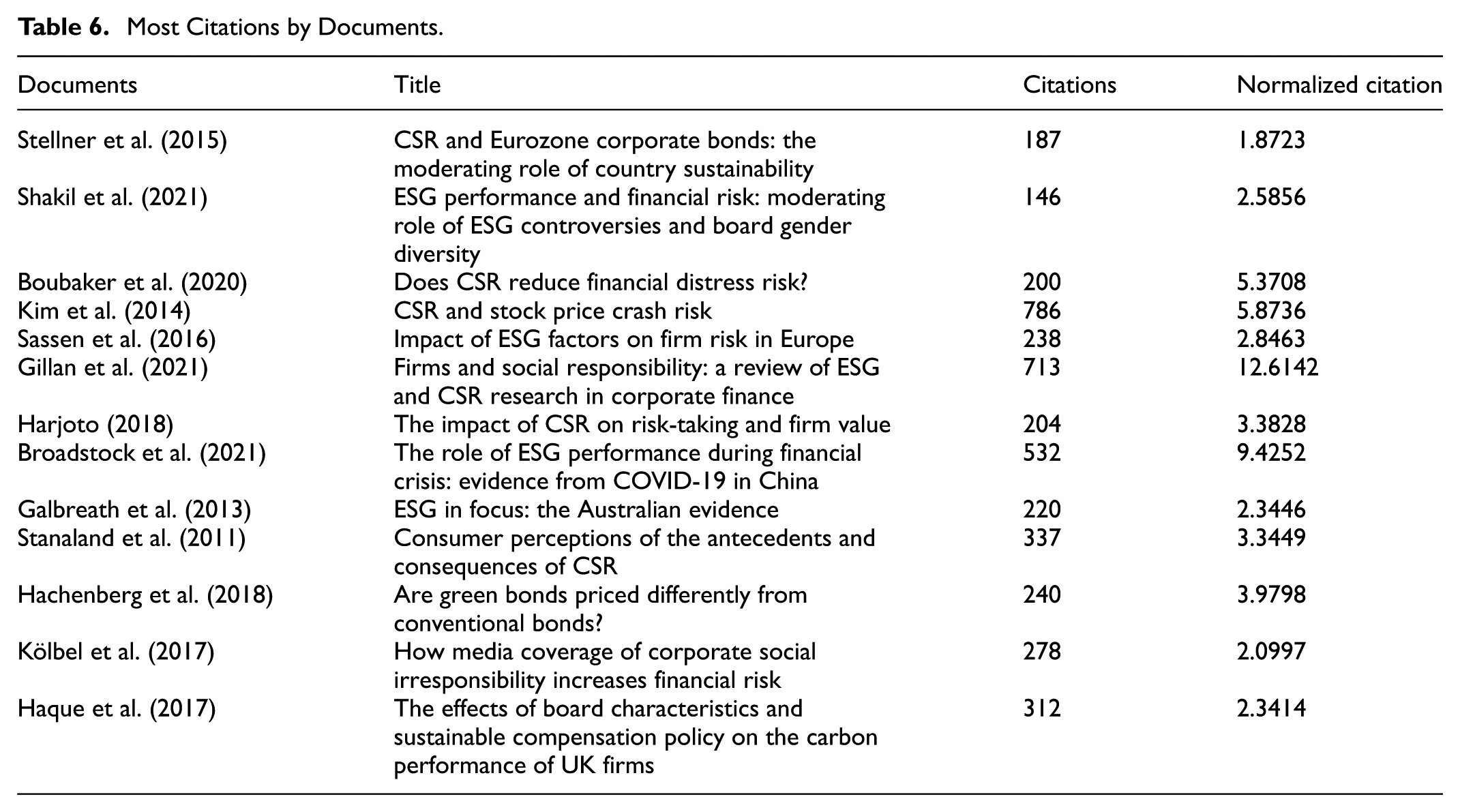

The citation analysis highlights the most important articles on the topic of ESG, which are discussed in this section. Table 6 and Figure 7 list the fourteen most influential articles that were found when the minimum citation requirement was set to 187 in VOSviewer. A synopsis of these top 14 most-cited papers is provided below.

Most Citations by Documents.

Science mapping of co-occurrence by documents.

Bibliographic Coupling by Sources

“CSR and Environmental Management,”“Journal of Business Ethics,”“Finance Research Letters,”“Journal of Cleaner Production,” and “Journal of Sustainable Finance and Investment” are the leading five journals where various literature reviews on the elements of ESG are found in Table 7 and Figure 8.

Top Articles With the Most Documents.

Science mapping of bibliographic coupling by sources.

META Analysis

In this step, the authors examined each research trend found by bibliographic coupling. In finance and economics, meta-analysis is particularly prevalent in controversial areas (Khan, 2022; Zigraiova & Havranek, 2016). Previous research on the meta-analysis focused mostly on subjects such as the correlation between firm competition and the financial stability nexus in the financial sector (Zigraiova & Havranek, 2016). These studies with conflicting results are synthesized through meta-analysis to extract generalized findings. The authors followed Khan (2022) to examine the highlighted study stream.

After analyzing the existing literature, a comprehensive examination was conducted to evaluate and identify the key research findings in ESG performance and sustainable business performance. Through careful evaluation of the selected articles, a wide range of research scopes has been identified. These selected papers were then classified into several streams, such as primary research and sub-stream research, based on the specific thematic focus. This study included relevant information and a similar research trend for the analysis provided in the existing literature. Seven key research streams emerged: (1) ESG performance and firm performance, (2) ESG performance and firm risk, (3) ESG performance and investment efficiency, (4) ESG performance and cost of capital, (5) ESG performance and green innovation, (6) firm-specific characteristics and ESG performance, (7) Corporate governance and ESG performance. The findings from each of these streams are outlined below.

ESG Performance and Firm Performance

The association between ESG performance and firm performance can be explored through various theoretical frameworks. Stakeholder theory posits that ESG initiatives enhance relationships with stakeholders like customers and employees, improving financial performance through increased loyalty and satisfaction (Duque-Grisales & Aguilera-Caracuel, 2021; Elmghaamez et al., 2024; Erol et al., 2023; Ruan & Liu, 2021). Agency theory highlights how strong governance practices reduce agency costs and improve managerial decision-making, directly benefiting firm financial performance (Bătae et al., 2021; S. Chen et al., 2023; Esteban-Sanchez et al., 2017; Weber, 2017). RBV considers ESG practices as strategic resources that provide competitive advantages, such as enhanced reputation and operational efficiencies (Azmi et al., 2021; Cavaco & Crifo, 2014; Garcia & Orsato, 2020). Legitimacy theory underscores the importance of societal approval, where ESG practices increase legitimacy, leading to greater customer and investor confidence (Duque-Grisales & Aguilera-Caracuel, 2021; Rao et al., 2023; Xie et al., 2019). Signaling theory highlights that companies inspire potential investors by confirming ESG practices and signaling their commitment to sustainable and long-term business decisions in financial sectors (Khamisu et al., 2024; Maji & Lohia, 2023; Menicucci & Paolucci, 2023). Finally, institutional theory demonstrates significant insights into the adoption of ESG performance, improving corporate governance and financial stability (Ahmad et al., 2021; Bahadır & Akarsu, 2024; Bahadori et al., 2021). Therefore, these theories provide comprehensive frameworks to understand the significant impacts of ESG practices on firm financial stability.

Most of the previous research highlighted the significant positive relationship between ESG practices and financial performance in different economic and non-financial institutions (Baran et al., 2022; M. T. Lee & Suh, 2022; N. Saini et al., 2022). Environmental sustainability practices can reduce capital costs and regulatory fines, which in turn increases investment efficiency. Robust ESG performance and corporate governance ensure sustainable decision-making by increasing customer loyalty, investor confidence, and employee satisfaction and reducing firm risk-taking (Baldi & Lambertides, 2024; Tang et al., 2024).

ESG Performance and Firm Risk

The relationship between ESG practices and firm risk-taking has been comprehensively examined with different theoretical frameworks. Stakeholder theory analyzes the stakeholder interests by addressing ESG performance to reduce probable risks and create a supportive environment (He et al., 2023; Naseer et al., 2024). Agency theory underscores the significance of robust corporate governance in reducing conflict of interest between principal and agent, thereby lowering overall financial risk (J. Chouaibi et al., 2024; D. Liu et al., 2023). Legitimacy theory highlights that ESG performance enhances legitimacy, increasing reputational risks, and establishing regulatory frameworks (J. Chouaibi et al., 2024; Izcan & Bektas, 2022). Signaling theory elucidates that ESG performance confirms transparency with the organizational commitment to sustainability, signals investor confidence, and reduces risk-taking behavior (Izcan & Bektas, 2022; Suttipun, 2023). Risk management theory supports financial and non-financial institutions using ESG practices to mitigate perceived risks, ensuring firms’ long-term sustainability (Neitzert & Petras, 2022; Sassen et al., 2016). These theories collectively demonstrate a significant framework for understanding the relationship between ESG disclosure and firm risk-taking.

ESG Performance and Investment Efficiency

The relationship between ESG performance and investment efficiency has been analyzed using some theoretical support. Stakeholder theory underscores that implementing ESG practices builds loyalty and trust among investors, customers, and employees, enhancing efficient capital allocation (Al-Hiyari et al., 2023; Benlemlih & Bitar, 2018; Samet & Jarboui, 2017). Legitimacy theory highlights that companies comply with corporate governance, which reduces conflicts of interest and legitimate enterprise decision-making systems (Al-Hiyari et al., 2023; Zamir et al., 2022). Agency theory is another important theory that explains the countries’ regulatory pressure and society’s demands directing companies to adopt ESG performance, influencing investment strategies (Al-Hiyari et al., 2023; Ellili, 2022; Zamir et al., 2022). Finally, information asymmetry theory highlights valuable insights that companies’ ESG performance signals accountability and quality to stakeholders and prioritizes the risk-return trade-off for long-term efficient investment (Bilyay-Erdogan et al., 2024; Ullah et al., 2020).

These theories provide an inclusive understanding of the association between ESG performance and investment efficiency is a very significant topic among researchers. Researchers demonstrated that ESG practices ensure investment efficiency by mitigating overall risks and confirming long-term investment growth (Cajias et al., 2011; Cook et al., 2019; Lin et al., 2023). Environmental performance decreases operational and regulatory risks, corporate social responsibility inspires stakeholder trust and customer loyalty, and corporate governance establishes better decision-making and ensures accountability, ultimately confirming organizational investment efficiency (Z. Chen et al., 2024; Zahid et al., 2023).

ESG Performance and Cost of Capital

The correlation between ESG factors and the cost of capital can be explained using different theoretical perspectives. Stakeholder theory examines how ESG performance builds stakeholder trust, mitigating operational risks that minimize the cost of capital and ensuring stable cash flows (Khanchel & Lassoued, 2022; Priem & Gabellone, 2024). Recent studies demonstrate that companies with strong ESG issues get better credit ratings, tend to have lower credit spreads, and ensure risk management and reliability (Bhuiyan & Nguyen, 2020; Y. Chouaibi & Zouari, 2023). Agency theory explains the importance of corporate governance that reduces conflict of interest between management and shareholders, which in turn lowers the cost of capital and agency costs (Y. Chen et al., 2023; Khanchel & Lassoued, 2022). Companies with robust ESG performance enhance operational efficiency and financial performance, leading to a minimum cost of capital (Fandella et al., 2023; La Rosa & Bernini, 2022).

However, signaling theory and information asymmetry theory underscore that robust ESG performance ensures quality and reduces environmental uncertainty, leading to the mitigation of the cost of capital. ESG practices send positive signals to stakeholders about the firm’s decision-making quality and potential investment opportunities, thereby reducing the information asymmetry (Abu Afifa et al., 2023; Khanchel & Lassoued, 2022). Legitimacy theory highlights that external shocks and society’s demands drive firms to adopt ESG performance to attract legitimacy and social expectations, which can significantly impact investor perceptions and corporate reputation (Y. Chouaibi & Zouari, 2023; Khanchel & Lassoued, 2022). Finally, these theories provide a comprehensive understanding of the effect of ESG performance on the cost of capital, enhancing the significance of sustainable business practices in corporate finance (Y. Chen et al., 2023; Khanchel & Lassoued, 2022).

ESG Performance and Green Innovation

The association between ESG practices and green innovation is complex, emphasizing different theoretical perceptions. Green innovation inspires companies to make decisions about eco-friendly innovation for long-term sustainability. Stakeholder theory recommends that companies consider ESG performance for establishing trust and attracting sustainable investment, creating a collaborative environment that promotes green innovation with valuable insights (H. Liu & Lyu, 2022; Xue et al., 2023). Institutional theory and legitimacy theory provide valuable insights that companies should accommodate green innovation to satisfy environmental and external shocks. Institutional theory prioritizes regulatory and society’s demands to adopt ESG performance for meeting environmental and societal expectations to ensure green innovation (H. Liu & Lyu, 2022; Yuan & Cao, 2022).

Similarly, legitimacy theory discusses that organizational practices with ESG performance secure legitimacy and social favor. Institutions can invest in eco-friendly industries and products deserving of corporate reputation, which provide competitive advantages (H. Liu & Lyu, 2022). The RBV also provides valuable insights to companies that perform environmentally friendly services to the stakeholders, which in turn ensures corporate green innovation, giving them competitive advantages (Yuan & Cao, 2022; Zhai et al., 2022). Signaling theory complements that strong ESG performance signals a company’s dedication to sustainability, drawing in environmentally aware customers and investors (Long et al., 2023; Xue et al., 2023).

Firm-Specific Characteristics and ESG Performance

The association between firm-level characteristics and ESG disclosure is explored with several theoretical perspectives, emphasizing key determinants like firm size, firm age, leverage, liquidity, growth, capital adequacy ratio, and firm risk (Abdul Razak et al., 2023; Anwer et al., 2023; DasGupta & Roy, 2023; Yu & Xiao, 2022). Stakeholder theory posits that more profitable and larger firms are more likely to adopt comprehensive ESG issues to meet stakeholder expectations. The RBV approach highlights how firm-specific resources, such as financial and human capital, enable superior ESG performance. Agency theory provides insights that ownership structure, particularly institutional investors, can drive better ESG performance by aligning managerial actions with long-term value creation. Institutional theory explains how the industrial sector and regulatory pressures on ESG practices compel firms in high-impact industries to adhere to stringent ESG standards. Signaling theory explains that companies leverage ownership structure and profitability to signal their dedication to corporate sustainability, thereby improving ESG performance. Legitimacy theory highlights that companies promote ESG practices to enhance legitimacy (Naeem et al., 2022). These theories collectively provide a comprehensive framework for how firm-specific characteristics impact ESG performance. Future research should focus on standardizing ESG metrics and exploring the dynamic interactions between firm-specific characteristics and ESG performance across different contexts and periods.

Corporate Governance Issues and ESG Performance

The ESG-related literature highlights corporate governance issues as a powerful mechanism of sustainability (S. Chen et al., 2023; Z. Wang & Sarkis, 2017). Agency theory analyzes that a robust governance structure, such as board oversight and performance-based executive compensation, aligns managerial actions with stakeholder interests, enhancing ESG performance (Tang, 2022; J. Wang et al., 2023). Stakeholder theory highlights that diverse, independent boards promote robust ESG initiatives by addressing varied stakeholder needs (Broadstock et al., 2020; Zhai et al., 2022). From the resource-based view, effective governance serves as a critical resource that supports superior ESG practices (Yuan & Cao, 2022; Zhai et al., 2022). Legitimacy theory highlights that ensuring governance in a transparent way makes reporting accountable and trustworthy, thereby developing ESG outcomes and legitimacy (H. Liu & Lyu, 2022; Wu et al., 2025). Finally, institutional theory underscores valuable insights into regulatory and society’s demands to ensure the governance of an organization, with the adoption of ESG standards following institutional norms (H. Liu & Lyu, 2022; Tan & Zhu, 2022). This theoretical perspective provides a complete structure for understanding the relationship between ESG practices and corporate governance.

Corporate governance is generally characterized by board diversity, accountability, and transparent disclosure, which in turn improve ESG performance. Independent members of the board of directors are highly motivated to establish sustainable business practices (Lin et al., 2023). Women directors are instrumental in advancing social initiatives within boardrooms. More female member participation in the board of directors promotes board gender diversity and organizational transparency, which ensures sustainable corporate practices (Abdelkader et al., 2024; Brinette et al., 2023). However, content analysis reveals that some articles report insignificant relationships between female board representation and sustainability outcomes (Al-Shaer et al., 2024; Yadav & Prashar, 2023).

CEO power is found to have a negative but insignificant effect on ESG practice. While Al-Shaer et al. (2024) reported a positive relationship, Velte (2020) and Y. Zhao et al. (2023) found a negative association. In contrast, board size has a positive and statistically significant effect on ESG performance (Suttipun, 2021, 2023; Treepongkaruna et al., 2024).

Board independence significantly affects ESG performance (Al Amosh & Khatib, 2022; Brinette et al., 2023). Additionally, a CSR committee is a key body of sustainable behavior, consistently positively influencing CSR performance across various studies. This research stream boasts a larger dataset and consistent effect sizes across studies.

In conclusion, the research stream on corporate governance and ESG reveals a significant gap, particularly in the generalizability of findings for global policy implications. Most studies rely on small sample sizes, mainly from China, the US, and Europe. To address these gaps, future research should utilize larger datasets that cover a broader range of geographical contexts, thereby improving the generalizability of the results. Moreover, it would benefit regulators and policymakers to investigate the specific attributes of integrated reporting, such as connectedness or a forward-looking perspective, that are particularly relevant for improving ESG outcomes.

Future Research Directions

This research maps out notable research gaps based on existing literature and offers future research directions based on the authors’ understanding (refer to Table 8). The emergence of ESG ratings in business sustainability has become an important and growing research area. Identifying dominant research trends and proposing a framework for potential future research based on identified gaps can offer valuable insights for academic researchers and the business community.

Future Research Directions.

Effect of ESG Implementation on Theoretical Frameworks

Despite the expanding body of literature on the relationship between ESG disclosure and firm risk-taking and performance, several areas remain unexplored for future research. A vital gap is the need for longitudinal studies that examine the long-term impacts of ESG issues on financial and non-financial outcomes. Most existing research relies on short-term data, which may not fully capture the sustainable benefits or risks associated with ESG initiatives. Longitudinal studies would provide deeper insights into how ESG strategies influence firm risk-taking and performance over time and across different economic cycles.

Contextually related studies display a significant research opportunity, especially in emerging economies. Recent literature highlights the relationship between ESG performance and risk-taking in developed countries, but it remains unexplored in developing countries. Regulatory environment, stakeholder expectations, and economic conditions are there in developing economies, which shape the perceptions and effectiveness of ESG practices. Comprehensive investigations needed in diverse contexts will provide a deeper understanding to uncover unique opportunities and challenges within the financial and non-financial sectors.

Future research can also be explored with interactions between ESG performance and the combined influence on firm performance and risk-taking behavior. Some studies have been conducted on those issues separately, they may have compound impacts on profitability and financial stability.

Future research should also be conducted using financial technology and financial innovation to improve the relationship between ESG performance and firm risk-taking behavior. Technological developments, such as artificial intelligence, blockchain, and big data analytics, enhance new insights for reporting and improving ESG performance. These studies can be leveraged to investigate ESG practices, reduce firm risk-taking, and improve overall performance, which will provide an invaluable understanding of sustainable and efficient corporate practices.

Finally, future studies should investigate the impact of regulatory frameworks and government policies on the correlation between ESG performance, risk-taking, and firm performance. The study can explore the impact of regulations that may inspire companies to adopt ESG performance, which in turn enhances financial stability and firm financial performance.

Considering the overall understanding of the correlation between ESG performance and financial stability, future research should highlight long-term impacts, context-specific analyses, standardization of metrics, qualitative insights, interactions between ESG performance, the role of technology, and regulatory implications. The future research directions will motivate academics and researchers to provide valuable insights to explore the impact of sustainable and efficient business operations. Moreover, integrating different theories with the study of ESG factors and firm risk-taking and performance also provides a robust understanding of firms’ operations and their deeper impact on stakeholders.

Effect of ESG Implementation on Firm Performance

Most of the previous literature discussed ESG practices and sustainability and their impacts on financial performance, but several significant research gaps remain unexplored. One important gap is the inconsistent findings concerning the financial outcomes of ESG disclosure in different industries. The majority of studies indicate that robust ESG performance can have a significant impact on financial performance and risk-taking behavior, but other literature finds insignificant or even negative effects. These discrepancies underscore the necessity for more thorough research using alternative methodologies and techniques in terms of different contexts, measurement approaches, and timeframes. Furthermore, longitudinal research can also be conducted to investigate the long-term impacts of ESG performance on firm performance using cross-sectional data, especially between developed and emerging economies.

Another significant research gap concerns the varying ESG practices and the impact of the environmental regulatory framework in shaping them. Most literature focuses on large institutions, smaller enterprises remain unexplored. Moreover, ESG performance reporting standards and their impact on stakeholder intentions and financial performance remain underinvestigated. Environmental uncertainties and global pandemic crises are also important determinants of ESG performance, and the affiliation between ESG issues and financial performance is still unexplored. Many ESG-related studies examine the relationship between environmental aspects and firm performance. Still, the components of ESG practices, such as social and governance, are often underexplored and need to be examined for the overall impact on firm financial performance.

Effect of ESG Implementation on Firm Risk

Several studies investigated the correlation between ESG performance and firm risk-taking, but many significant research gaps remain unexplored. One of the important gaps is the partial empirical evidence about how ESG performance impacts firm risk-taking, credit risk, market risk, and liquidity risk. Some studies suggested inconsistent findings that robust ESG performance can mitigate risks, considering risk management and shareholder trust. More in-depth studies are needed to explore the individual effects of ESG factors on different types of risk. This comprehensive analysis can offer more valuable insights to explore the effect of ESG performance on firm risk-taking, especially in the banking sector.

Most existing studies are cross-sectional, offering only a snapshot view and failing to capture the dynamic nature of risk management and ESG integration over time. The role of the regulatory environment in influencing the relationship also remains unexplored. Comparative studies across regulatory frameworks could highlight how varying regulations impact risk outcomes. Moreover, while environmental risks have been relatively well-studied, the governance and social dimensions, like community engagement, employee welfare, and governance structures, require more attention to understand how holistic ESG practices contribute to reducing overall firm risk.

Effect of ESG Implementation on Investment Efficiency

The correlation between ESG disclosure and investment efficiency is an emerging study area with several research gaps. One significant gap is the inconsistent findings regarding how ESG impacts investment efficiency across different sectors and regions. While some studies indicate that strong ESG performance improves resource allocation, reduces costs, and enhances innovation, others suggest minimal or mixed effects. These inconsistencies highlight the need for more sector-specific and region-specific research considering the unique operational market conditions. Furthermore, standardized metrics and methodologies must be used to measure ESG performance and investment efficiency, complicating comparisons across studies and industries.

Another critical research gap pertains to the role of specific ESG dimensions in driving investment efficiency. Most existing research tends to treat ESG performance as a composite index, failing to disaggregate individual components and their unique influences. Additionally, the absence of longitudinal studies restricts understanding of the long-run effects of ESG practices, as most research is cross-sectional and only captures a snapshot. There is also a need for more research on how ESG performance influences investment efficiency through better stakeholder relationships, enhanced innovation capabilities, or better risk management. Addressing these gaps can provide deeper insights for companies and investors integrating ESG disclosure into their strategies.

Effect of ESG Implementation on Cost of Capital

Despite growing interest in the correlation between ESG disclosure and the cost of capital, significant research gaps persist. Notably, there’s a lack of empirical findings regarding how ESG performance influences the cost of debt and equity. While some studies recommend that strong ESG performance leads to a lower cost of capital by reducing perceived risk and enhancing corporate reputation, others show mixed results. More rigorous research is to be conducted to explore the influence of ESG performance on the cost of capital, considering industry-specific and contextual differences. A comparative study can also be conducted between developed and developing economies, such as China and the USA. Another critical research gap pertains to treating ESG performance as a composite index, but the influence of individual components of ESG performance on the cost of capital is underexplored.

Effect of ESG Implementation on Green Innovation

The association between ESG disclosure and green innovation is an emerging study area with several research gaps. One significant gap is the inconsistent findings regarding how ESG impacts green innovation across different sectors and regions, especially in the financial sector. While some studies indicate that strong ESG disclosure stimulates green innovation by confirming stakeholder engagement and mitigating operational risks, others suggest minimal or mixed effects. These inconsistencies highlight the need for more sector-specific and region-specific research considering the unique environmental challenges. Furthermore, standardized metrics and methodologies must be used to explore the correlation between ESG disclosure and green innovation, complicating comparisons across studies and industries. One significant gap is that most of the research shows the ESG composite index on green innovation, while the specific effects of its components on green innovation are underexplored. Moreover, there is limited longitudinal research on the long-term impacts of ESG practices on green innovation, as most studies are cross-sectional and provide only a snapshot. Furthermore, the mechanisms through which ESG performance facilitates green innovation, such as enhancing corporate reputation and improving stakeholder trust, also need to be better understood. Addressing these gaps will provide deeper insights and more actionable guidance for companies to integrate ESG issues into their innovation strategies, fostering sustainable development and competitive advantage.

Conclusion

This review performed a comprehensive assessment of existing literature, including an analysis of scientific publications, to investigate important areas of the research field. Along with bibliometric analysis, a meta-analysis was conducted to examine the most prominent research trends. A total of 140 articles were analyzed from the database (Scopus), which used ESG ratings as sustainability indicators. Initially, scientometric analysis was done using the VOSviewer text mining-related software to identify the most influential documents, journals, authors, countries, and frequently used keywords. This review determines the contexts of ESG and financial stability using a scientometric analysis and a comprehensive review. The research in this discipline can be broadly categorized into two primary domains: firm risk-taking and financial performance, specifically focusing on the impact of capital efficiency and cost efficiency. This study examined a meta-analysis of the research trends to emphasize the impact of investment efficiency and environmental uncertainty, as well as the direction of connection for each variable.

However, most previous research was conducted on single-country or cross-country analyses of ESG issues and firm-level characteristics, resulting in a lack of awareness regarding the comparison between developed and developing countries. This cross-country analysis receives greater attention from regulators, governments, and researchers in the case of ESG performance due to its significance to the economy (Yu & Xiao, 2022). It would be attractive for policymakers and investors to show the correlation between ESG efficiency, green innovation, and firm financial stability. More specifically, the focus should be given to considering the variables management efficiency, capital structure, capital regulation, interest coverage ratio, Basel III leverage ratio, and institutional quality index that influence ESG performance.

Another important yet underexplored variable is the capital regulation, which refers to the regulatory requirements that determine the minimum capital levels banks must uphold to ensure financial stability and mitigate risk. Despite the importance of sustainability in financial and non-financial institutions, there needs to be more understanding of how capital regulation influences sustainability and the combination of ESG practices into firm activities. Further research in these areas could provide insights into the association between capital regulation, ESG performance, and sustainability practices within the banking sector.

The literature has identified profitability, risk-taking, and leverage profile as firm-level variables influencing firm risk-taking and performance in terms of ESG disclosure and investment efficiency. However, the role of ESG performance in influencing firm risk and investment efficiency is an area that has yet to receive much attention in the literature. Moreover, firms with strong ESG performance may experience reduced risk and improved investment efficiency due to enhanced reputation, stakeholder trust, and operational efficiencies. Additionally, the role of intangible assets, like brand reputation and customer relationships, and human capital, including employee expertise and commitment to sustainability, should be considered critical factors in understanding how ESG performance affects firm risk and investment efficiency.

The current body of research on corporate governance has predominantly concentrated on various crucial factors such as gender board diversity, board size, audit committee, board independence, audit tenure, CEO duality, female CEO, and independent director (Hammami & Hendijani Zadeh, 2020; Y. Zhao et al., 2023). Most of these studies have been conducted primarily in China, the US and Europe (Bătae et al., 2021; J. Chouaibi et al., 2024; Habib & Mourad, 2023; Sandberg et al., 2023). Future research should explore how corporate governance practices vary across different institutional settings to enhance our understanding of corporate governance further. This could involve analyzing the impact of regulatory frameworks, legal environments, a country’s enforcement of sustainability scores, and the country’s institutional factors that influence the firm’s performance, such as government effectiveness, political bias, and the rule of law. These factors could provide valuable insights into how these moderating factors influence an organization’s decision-making.

The addition of directors’ religious backgrounds as a variable in corporate governance research could offer an exciting perspective. Religion often serves as a code of conduct and can significantly influence ethical behavior within organizations. By comparing the ethical behavior shaped by different religions, researchers could gain valuable insights into how religious beliefs impact corporate governance practices and decision-making processes.

Studying the impact of ESG profiles in energy, real estate, and bank settings could offer valuable findings into how the market values ESG performance and its implications for efficient capital allocation. If the market values ESG considerations, it may impact the decision-making processes of higher ESG performers differently from their counterparts. The outcomes of such a study could significantly impact decisions related to capital structure. Specifically, the energy and real estate sectors are directly related to ESG issues, whereas the financial sectors are indirectly related to sustainable business finance. So, these three industries are greatly affected by ESG disclosure, making this an important area for further research.

Regarding the financial aspects, no research has been conducted on the correlation between ESG efficiency and firm capitalization. Exploring which characteristics of firm capitalization and ESG performance, such as connectivity or future-focused, are more relevant could be valuable for regulators and policymakers.

The relationship between firm performance, risk, and ESG practices is bidirectional, appearing in models that examine both ESG and firm financial performance (Menicucci & Paolucci, 2023). These outcomes have two important theoretical and organizational policy implications. Firstly, companies with high profits are typically more solvent and have fewer short-term existence concerns. This allows them to invest in corporate social responsibility projects that create long-term value, integrating with stakeholder and agency theories. Second, the role of systematic risk suggests that industries sensitive to such risks tend to show stronger ESG performance (Saci et al., 2024).

This study is also not free from limitations. Data was exclusively sourced solely from the Scopus-based database, which, while the largest and most reliable, could potentially be enhanced by including other databases such as Google Scholar, Dimension, Web of Science, and EBSCO. Additionally, the authors excluded articles from 2024 for analysis, assuming that these papers still need more citations to validate their contribution to the academic field of ESG-related literature. Although the review outlines several noteworthy aspects of ESG and financial stability, focusing on more underexplored aspects of ESG, such as greenwashing, sustainability assurance, integrated reporting, and the inside-out versus outside-in paradigms, could add value to the extant literature. Exploring these issues would enhance the relevance and depth of the paper.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.