Abstract

The social norm of “high savings, low consumption” has traditionally constrained the consumption ability of Chinese families. However, life insurance has become an essential component of household financial planning due to the increasing unpredictability of economic growth and rising demand for financial security. This study utilizes PLS-SEM and ANN models, grounded in an expanded Theory of Planned Behavior (TPB), to analyze the impact of life insurance on household consumption expenditures. Based on a survey of 505 Chinese families, the results indicate that life insurance provides both financial and psychological stability. This stability reduces households’ cautious saving tendencies, thereby promoting an increase in consumption expenditures.

Introduction

Chinese households exhibit a notably high savings rate, with the economy characterized by “high growth,”“high savings,” and “low consumption” (Tang et al., 2022). According to the World Bank (2023), China’s total savings rate stands at 46%, ranking it among the highest globally and first among the top 10 economies (see Figure 1). While this high savings rate supports domestic investment, it limits the growth of household consumption expenditures. As a result, the economy remains excessively dependent on exports and investment, hindering the shift from an investment-driven to a consumption-driven model. In the post-pandemic era, widespread uncertainty stemming from COVID-19 and the slowing of China’s economic growth have heightened households’ preference for savings, further suppressing consumption. In this environment, life insurance has emerged as a crucial component of household financial planning and asset allocation strategies (Li et al., 2023). Unlike other financial instruments, life insurance combines protection and savings, with a specified cash value in the contract. Therefore, the allocation of life insurance can probably influence household consumption behavior.

Saving rates for the world’s top 10 economies in 2023.

To investigate the impact of life insurance on household consumption behavior, this study analyzes data from a survey of 505 Chinese households regarding their consumption habits and life insurance allocation. Using the extended Theory of Planned Behavior (TPB) and Artificial Neural Network (ANN) models, the research examines the relationship between life insurance policies and household consumption expenditures. Specifically, it focus on households’ attitudes, subjective norms, and perceived behavioral control regarding life insurance allocation and its impact on consumption. By systematically analyzing the connection between life insurance and household consumption, this study highlights the role of insurance in household financial management. It provides theoretical and empirical support for the role of life insurance in boosting consumption, contributing to China’s shift from an investment-driven to a consumption-driven economy. Additionally, the findings may offer valuable insights for other countries facing similar challenges, such as low domestic demand, and provide practical recommendations for addressing these issues.

In conclusion, this study employs the PLS-SEM and ANN models to examine the mechanisms by which life insurance influences household consumption behavior, as derived from the extended TPB. Exploring the association between Risk Management Instruments (e.g., life insurance) and consumer behavior helps improve social consumption levels and promote sustainable economic growth globally.

Review of Literature, Theoretical Constructs

Influences Affecting Household Spending

The scale and structure of household consumption expenditures are key indicators of living standards, economic vitality, and social well-being. There are many factors that affect these expenses, with financial investment behavior emerging as a significant driver of consumption growth. The development of financial markets has increased household participation in financial investments, raising the proportion of financial assets in their portfolios. This shift has significantly boosted households’ propensity to consume and overall consumption levels. However, households holding risky assets may reduce consumption during periods of significant volatility in asset prices. Meanwhile, commercial insurance, as part of the financial investment sector, reflects households’ precautionary saving motives. It promotes consumption by diversifying risks and reducing uncertainty, particularly among urban households (Peltonen et al., 2012).

The age structure of a household significantly impacts consumption expenditure. The child-rearing ratio and old-age support ratio play a dual role in shaping household consumption. While some scholars disagree, it is generally accepted that an increase in the child-rearing ratio tends to boost consumption, whereas an aging population may reduce it (Bonham & Wiemer, 2013). The influence of age structure is evident in shifting consumption patterns, as expenditures on healthcare, food, transport, education, and entertainment vary with the proportion of elderly individuals in a household.

Household income volatility and leverage are also crucial factors affecting consumption. Income volatility influences borrowing decisions, while high leverage amplifies the impact of income fluctuations, leading households to cut non-essential spending due to debt-related stress (Ogawa & Wan, 2007). During economic downturns, households with high debt are more sensitive to income changes, which further reduces their consumption expenditure (Song, 2020).

Factors Influencing Life Insurance Allocation Behavior

Life insurance is a crucial component of the modern financial system, serving as an essential tool for individual and family risk management. It also complements the social safety net by mitigating the financial burdens from accidents, illnesses, and longevity. Yaari (1965) was the first to suggest that life insurance can reduce the impact of longevity uncertainty on personal financial planning. Subsequent studies have explored the various factors influencing life insurance demand, including household economic characteristics, education levels, social security systems, and overall economic development (Segodi & Sibindi, 2022; Shieh et al., 2020).

In China, the demand for life insurance has evolved alongside rapid economic growth and social changes. Segodi and Sibindi (2022) found that income levels, insurance market development, and marketization impact life insurance demand. However, the response to inflation shows distinct characteristics, as residents’ living standards have not been significantly affected by severe inflation during periods of high economic growth.

Chinese residents face multiple factors when allocating life insurance. First, demographic shifts, such as changes in family size and population aging, influence insurance demand (Nebolsina, 2020). Second, social factors like rising dependency ratios and increased life expectancy have prompted residents to focus more on life insurance to cover potential pension and healthcare expenses (Zhang et al., 2023). The evolving socio-economic environment requires a thorough understanding of life insurance needs and timely adjustments to address the growing demand for protection and to enhance the social security system.

TPB Model and Residents’ Consumption Intention

TPB developed by Fishbein and Ajzen (1972), builds on the Theory of Reasoned Action (TRA) and is widely recognized for predicting behavior. It analyzes and forecasts the motivational framework underlying individual actions. The theory suggests that behavioral intentions directly influence actions and are shaped by three key components: behavioral attitudes (emotional evaluation of the behavior), subjective norms (perceived social pressures from others), and perceived behavioral control (self-assessment of the ability to execute the behavior). These components are interconnected and collectively form a robust system for predicting behavior (Hassan et al., 2016).

Household consumption intention is a critical element of economic and social activities, reflecting the attitudes, preferences, and expectations of family members in their consumption decisions. This intention directly influences the allocation and use of household resources (Al Mamun et al., 2018). The decision-making process is complex and involves emotional responses to consumption objects, as well as various influences from the household’s internal and external social environment. Factors such as individual preferences, perceptions of economic status, socio-cultural norms, and access to information and resources significantly affect purchasing decisions.

Life Insurance Allocation and Household Consumption

Since Richard (1975) introduced life insurance into Merton’s optimal consumption and portfolio model, scholarly interest in the distribution of life insurance and its impact on household consumption has grown. Duarte et al. (2011) expanded this framework to include multiple high-risk assets, advancing the understanding of life insurance allocation strategies. Striani (2023) used a Constant Relative Risk-Utility (CRRU) function to analyze the significant effect of life insurance purchases on Italian households’ overall consumption expenditure.

Life insurance is not only a means of financial protection but also a key component of household risk management. Kolukuluri (2023), using longitudinal data from the Indonesian Household Life Survey, found that households without insurance faced a 1.3% point decrease in food consumption and a 2% point drop in non-food consumption when experiencing severe health shocks. Conversely, households with Askeskin insurance had sufficient coverage for both food and medical expenses. Life insurance helps families manage costly healthcare expenses and maintain child support during health crises (Wang et al., 2018). Thus, life insurance is essential for providing financial stability and reducing the financial risks associated with unexpected events like illness or accidents. This protection allows households to allocate additional precautionary savings, improves their sense of future security, and increases their willingness to spend on consumption rather than saving for potential risks.

Gaps in Prior Literature

The literature review of this study mainly focuses on the influencing factors of household consumption, residents’ life insurance allocation behavior, the role of TPB in shaping consumption intention, and the impact of life insurance allocation on household consumption.

However, existing studies still have the following shortcomings. First, there is a lack of in-depth discussion on how life insurance indirectly affects consumption behavior through psychological factors (such as attitude, subjective norms, and perceived behavioral control). Most of the previous studies analyzed the impact of life insurance on family consumption behavior from the perspective of economics, ignoring the psychological decision-making process of consumers (Li et al., 2023). In fact, buying life insurance is not only an economic act but also a decision-making process, which is affected by psychological factors. Based on the extended TPB, this study explores how life insurance affects family members’ psychological factors, which in turn indirectly affects consumption behavior.

Second, the existing literature research method is single, and lacks innovation. Previous studies on life insurance and consumer behavior mostly relied on economic models and rarely used more complex behavioral analysis tools. In this study, the PLS-SEM model and ANN model were comprehensively used to analyze the causal path and prediction ability of variables. This approach fully reveals the linear and non-linear relationship between life insurance and household consumption expenditure, making up for the limitations of traditional statistical methods.

Third, previous studies have failed to provide theoretical support for the consumption behavior of Chinese households. Most of the existing studies are based on data from Western countries, and the high savings rate and relatively conservative consumption pattern of Chinese households may not be fully applicable to the existing research conclusions.

Hypothesis Development

Impact of the TPB Model on Household Consumption Intention

Although life insurance has been widely discussed in the academic circle, its research direction mainly focuses on the allocation strategy of life insurance, the impact mechanism of life insurance allocation on specific daily necessities, and the consumption demand of life insurance. However, there is a lack of exploration on the impact mechanism of life insurance policy and the overall household consumption expenditure. In addition, in terms of research methods, traditional research often adopts microeconomic models to study consumption decisions, ignoring the impact of cognitive and psychological factors on new consumption decisions. This gap limits the understanding and prediction of consumer behavior. In fact, individuals are not entirely rational in their decision-making and are always able to make utility-maximizing choices.

In order to clarify the family’s consumption intention and its influence on consumption behavior, applying the TPB model to household consumption intention is helpful in exploring the psychological mechanism affecting household consumption decision-making (Paul et al., 2016). Based on this theory, family consumption decision-making behavior can be attributed to the three drives of its psychological mechanism: attitude, as the core cognitive dimension, reflects the family’s utility evaluation and emotional tendency toward insurance consumption, and directly affects the orientation of consumption intention. Subjective norms are internalized into social reference standards for decision-making through internal and external family social pressures, strengthening or weakening consumption motivation. Perceived behavioral control further measures households’ ability to evaluate their own consumption. If perceived resources are sufficient and behavioral paths are clear, consumption intentions are more likely to be translated into actual behaviors (Yadav et al., 2016). These three factors form the psychological framework of consumption decision through dynamic interaction, while the external situation may regulate the transformation efficiency.

The TPB model chosen in this study is a theoretical response to the complexity of insurance consumption decision-making under the background of theoretical innovation of behavioral economics: Through three dimensions of attitude, subjective norms and perceived behavior control, the model constructs a framework for comprehensive analysis of residents’ consumption intention, which not only makes up for the defect of traditional economics ignoring psychological authenticity, but also provides a key analytical tool for solving the saving-consumption paradox and insufficient security in Chinese household finance through an operable measurement system. At the same time, by revealing the key psychological factors affecting decision-making and their interactions, the model provides empirical support for the strategy design of promoting healthy consumption patterns and improving household consumption intention. Based on this, the following hypotheses are proposed in this paper.H1: Attitude positively and significantly affects household consumption intention.

The Influence of Life Insurance Allocation on Household Consumption

Life insurance is essential to provide financial stability and reduce financial risk associated with unexpected events such as illness or accidents. This protection enables households to allocate additional precautionary savings, increasing their sense of security about the future and improving their willingness to spend rather than save for potential risks (Papanicolas et al., 2018).

Life insurance releases the consumption willingness of households through the risk buffer effect. Risk buffering occurs when insurance reduces future uncertainty, enhances economic security, and encourages current consumption by reducing the need for precautionary savings. This path is driven by the behavioral attitudes and perceptual control of TPB (Peijnenburg et al., 2017). At the same time, life insurance products have the function of long-term savings and wealth appreciation, transforming short-term income into long-term cash flow through the compulsory savings mechanism. This intertemporal allocation optimizes the household financial structure and enables consumers to maintain stable consumption power in different stages of the life cycle (Alhassan & Biekpe, 2016). In addition, in the cycle of inflation or economic downturn, the hedging function of life insurance can partly hedge the risk of currency depreciation. Consumers are more willing to invest liquid funds in consumption rather than low-yielding savings because of increased asset safety.

Therefore, on the basis of the previous analysis of household consumption intention, this study intends to take life insurance as a new variable to further explore the analysis of household consumption behavior. In this context, the following hypothesis is proposed.

Methodology

Measurement Statistics

This study employs a hybrid approach for hypothesis testing, combining Partial Least Squares-Structural Equation Modeling (PLS-SEM) with machine learning techniques. PLS-SEM is a statistical method used to develop and evaluate theoretical models. It is particularly suited for analyzing and predicting complex interactions between variables in data sets with limited sample sizes (Leguina, 2015). The ANN is a computational system with numerous basic processing units (neurons) that can assess the quality and reliability of PLS-SEM data (Goodfellow et al., 2016).

The empirical data analysis was structured into three distinct stages. First, SPSSv27 statistical software was used to perform Confirmatory Factor Analysis (CFA) on the questionnaire data, ensuring the accuracy and reliability of the measurement model. Second, Smart-PLS software was used to conduct correlation path analysis to validate the hypotheses. Finally, ANN machine learning was applied to verify the PLS-SEM results, ensuring the precision of the test outcomes. Figure 2 outlines the detailed research procedures.

The framework of research design.

Survey Instruments and Data Collection

The data-gathering process for this study was divided into three phases. In the first phase, the study analyzed the motivation, intention, and consumption psychology of Chinese families when purchasing life insurance, based on existing research.

In the second phase, the questionnaire content was developed using semi-structured interviews. Participants included an insurance broker from Mingya Insurance Broking Company, two insurance consumers, an insurance product manager, and a university lecturer specializing in insurance research. Each interview lasted over 45 min. Further details can be found in Table 1.

Profile of Semi-Structured Interviewees.

In the third phase, the survey questionnaire was created and made available online, using insights from relevant scientific literature and the initial interviews. To ensure broad coverage of households across China and improve efficiency, an online format was used. The survey was distributed via China’s largest online survey platform, “Questionnaire Star” (Xu et al., 2019). To enhance the efficiency of data collection, the research team actively disseminated questionnaire links through WeChat, a free instant messaging application for smart terminals launched by Tencent on January 21, 2011, and invited participants to complete the survey online. After data collection was completed, this study conducted a background analysis of participants’ response durations and manually reviewed the questionnaire results. Responses falling outside a reasonable time range, incomplete submissions, and inconsistent answers were identified as anomalous data and subsequently removed.

Hair et al. (2010) suggest a minimum sample size of 10:1 for the number of independent variables. To minimize random error and sample bias and to improve statistical effectiveness, the study distributed 709 questionnaires for the four independent variables: attitude, subjective norms, perceived behavioral control, and life insurance allocation behaviors. Among them, 505 valid responses were collected, resulting in a valid response rate of 71.2%. This meets the sample size requirements for the study.

Furthermore, because the survey data was mostly based on self-reported replies from participants, there was a possibility of social desirability bias, in which respondents were more likely to offer socially acceptable answers. To minimize this bias, this study implemented the following measures in questionnaire design and data collection. First, In terms of question design, a Likert scale was used for questions related to psychological factors to minimize extreme response tendencies (Jebb et al., 2021). Additionally, all questions concerning personal background information were presented in an objective manner, avoiding any leading wording. Finally, the questionnaire contained randomized questions to prevent respondents from modifying their responses in accordance with previous inquiries, thereby guaranteeing response independence (Paulhus & Vazire, 2007). Regarding respondent selection, one individual per household was designated to complete the questionnaire. To improve the accuracy of their responses, participants were required to provide responses that were based on the financial situation of their household. Before completing the survey, respondents in married households were advised to consult with their spouses regarding financial decisions.

Data Analysis

Descriptive Analysis

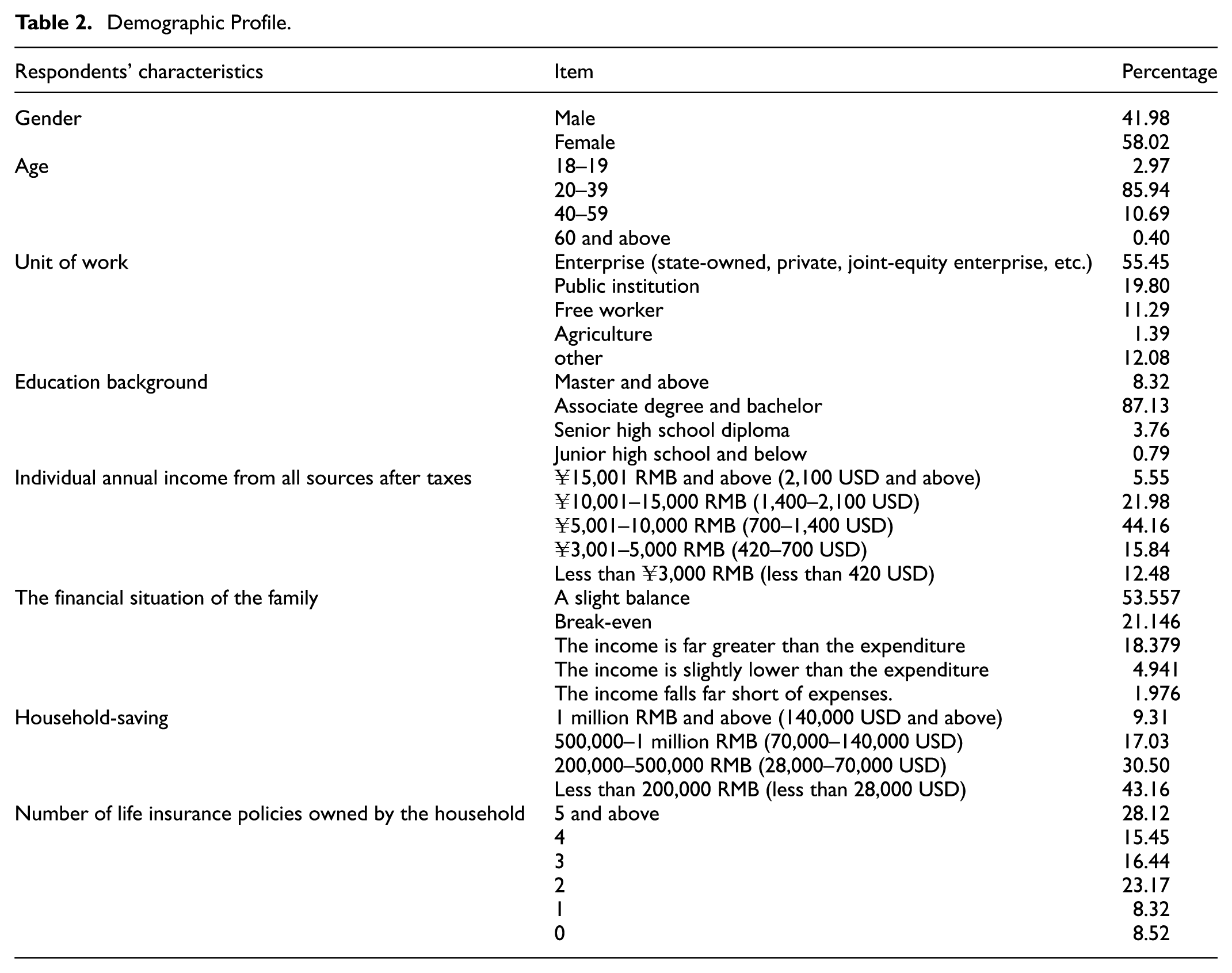

Table 2 provides the characteristics of the respondents. The analysis of the gender and age distribution of respondents shows a relatively balanced gender ratio, with women making up 58.02% and men 41.98%. This balance helps prevent potential data bias due to gender disparities. Additionally, all participants were 18 years or older, enhancing the validity and accuracy of the survey results.

Demographic Profile.

A thorough examination of the sample reveals that 93% of Chinese households have incomes equal to or exceeding their total expenditure. Among the respondents, 21.14% possess balancing household income and expenditure, 53.56% have a small surplus, and 18.28% have incomes significantly higher than their spending. This suggests that most Chinese households are in a stable financial state and have substantial capacity for insurance-related expenditures.

Furthermore, the data indicates that 56.83% of households hold deposits exceeding RMB 200,000, suggesting the majority of survey participants belong to the middle class or above (Gan et al., 2014). Of these, 30.50% have deposits ranging between RMB 200,000 and RMB 500,000.

Regarding life insurance distribution, 91.49% of households surveyed hold life policies. Within these households, 28.12% have five or more life insurance policies, while 15.45%, 16.44%, 23.17%, and 8.32% hold four, three, two, and one life insurance policies, respectively. This indicates that a significant portion of Chinese households retain an in-depth awareness of insurance.

Overall, the survey sample includes participants from various age groups, genders, professions, and economic backgrounds, making it a suitable sample for empirical study.

Measurement Model

Design of Questionnaires and Measurement of Variables

This study developed a questionnaire with three primary modules addressing four independent factors and two dependent variables. The first module gathers basic information about the respondents’ families, such as age, education level, profession, and annual income. The second module covers attitudes, subjective norms, perceived behavioral control, consumption intentions, and consumption practices. The third module examines the allocation of family life insurance policies and their impact on consumption behavior. The content design is based on the expertise of relevant scholars. For instance, questions on subjective norms and perceived behavioral control are derived from the research of Bao et al. (2020) and Xu et al. (2019), while those on family life insurance policy are based on Brown and Finkelstein (2011).

To ensure the reliability and accuracy of the questionnaire, questions were formulated to cover multiple dimensions for each variable (Chong, 2013). A Likert scale was used to assess respondents’ attitudes and opinions, ranging from 1 (“strongly disagree”) to 7 (“strongly agree”). Likert scales are widely used to measure complex cognitive concepts, enhancing the reliability and validity of the evaluation tool (Jebb et al., 2021).

Factor Analysis and Construct Reliability

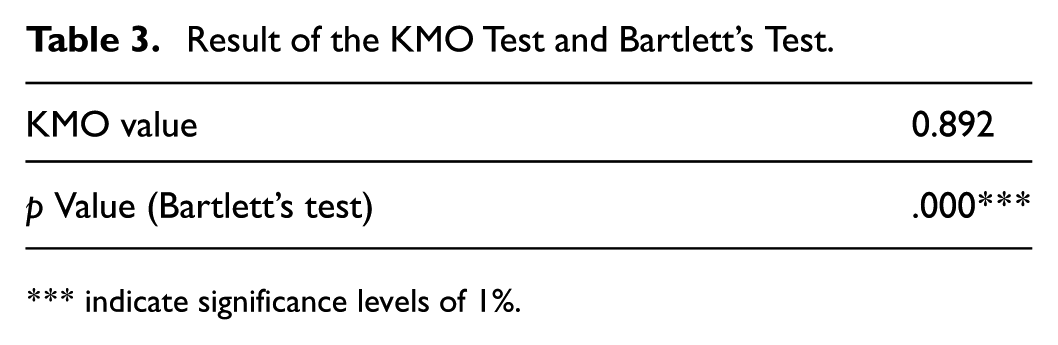

Before conducting Confirmatory Factor Analysis (CFA), the Kaiser-Meyer-Olkin (KMO) test and Bartlett’s test of sphericity are performed to assess data suitability for factor analysis. Kaiser (1970) and Hair et al. (2010) suggest that a KMO value above 0.5 and a Bartlett’s test p-value below the significance level indicate data suitability. Table 3 shows a KMO value of 0.892 and Bartlett’s test p-value of .000***, statistically significant at the 1% level, indicating high suitability for factor analysis.

Result of the KMO Test and Bartlett’s Test.

indicate significance levels of 1%.

Following these tests, CFA is conducted to assess the validity of the theoretical model. The factor loadings (FL) of all questionnaire items exceed 0.7, demonstrating that the items adequately represent the variables. Additionally, the R1 values for willingness and behavior related to household consumption exceed 0.7, indicating a strong model fit (Field, 2013; Hair et al., 2010). The six components exhibit composite reliability (CR) ranging from 0.766 to 0.879, surpassing 0.7, demonstrating strong internal consistency. The average variance extracted (AVE) for each variable exceeds 0.5, ranging from 0.663 to 0.721, indicating good convergence (Henseler et al., 2015). All Cronbach’s alpha values for behavior, attitude, perceived behavioral control, subjective norms, willingness to consume, and attitudes toward life insurance exceed .8, confirming internal consistency and reliability (Cronbach, 1951; DeVellis, 2016). Table 4 elaborates on these quantitative findings.

Reliability and Validity Assessment.

Note. FL = factor loadings; R2 = coefficient of determination; CR = composite reliability; AVE = average variance extracted; α = Cronbach’s alpha.

Discriminant validity is assessed using the cross-loading approach. Chin (1998) suggest that a questionnaire has good discriminant validity when the factor loading of each item is higher with its corresponding factor than with other factors. Table 5 shows that all items in this study exhibit a higher loading on their respective factors than on others, validating the questionnaire’s discriminant validity.

Criterion of Discriminant Validity.

Note. ATT = attitude; PBC = perceived behavioral control; SN = subject norm; BALI = behavior of allocating the life insurance; PI = intention to increase household expenses; PB = behavior of increasing household expenses. Bold values indicate that the indicator’s loading on its associated construct is higher than its cross-loadings on other constructs.

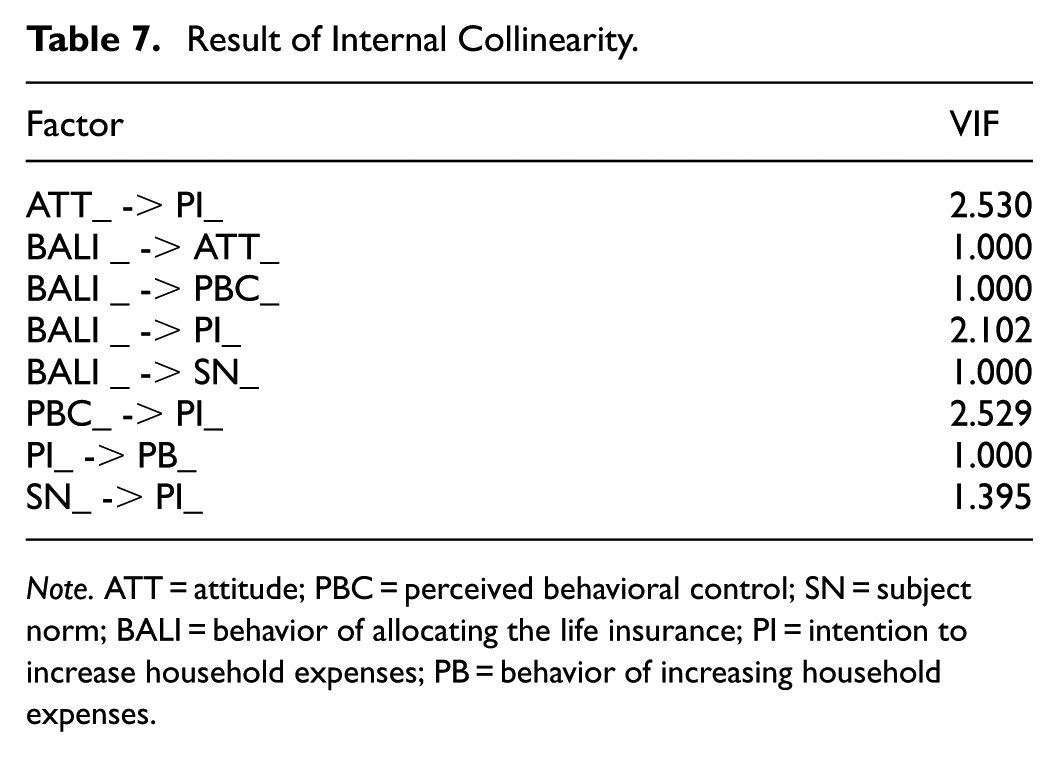

To mitigate the risk of covariance affecting the interpretability and predictive accuracy of the model (Chin, 1998), both internal and external covariance tests are conducted. The variance inflation factor (VIF) is used to assess multicollinearity, with lower VIF values indicating less covariance. While some researchers use a VIF threshold of 10 (Field et al., 2012; Kutner et al., 2005), Hair et al. (2010) recommend a threshold of less than 5. This study adopts a VIF threshold of five to ensure reliability and robustness in the model findings, minimizing the effects of multicollinearity. The obtained VIF values range from 1.483 to 2.726, all below the threshold of 5, indicating minimal multicollinearity among variables. Internal covariance VIF values range from 1.000 to 2.53, further confirming minimal multicollinearity and good model accuracy. Specific results are presented in Tables 6 and 7.

Result of External Collinearity.

Note. ATT = attitude; PBC = perceived behavioral control; SN = subject norm; BALI = behavior of allocating the life insurance; PI = intention to increase household expenses; PB = behavior of increasing household expenses.

Result of Internal Collinearity.

Note. ATT = attitude; PBC = perceived behavioral control; SN = subject norm; BALI = behavior of allocating the life insurance; PI = intention to increase household expenses; PB = behavior of increasing household expenses.

Structural Model PLS Results

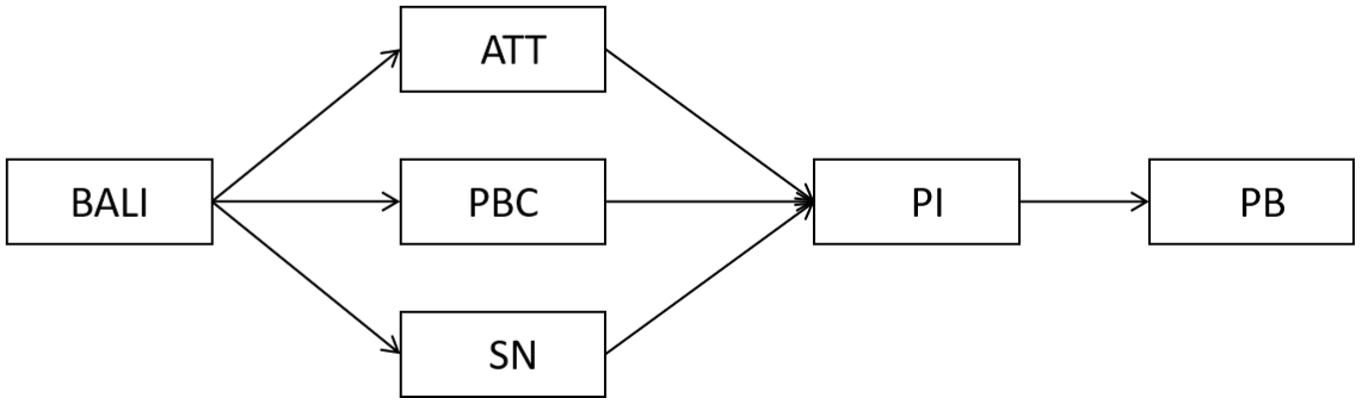

The study employs factor analysis to assess the appropriateness of questionnaire data for PLS-SEM. Following this, path analysis is used to examine relationships among the components. The results in Table 8 show that the path coefficients for all eight hypotheses are positive and statistically significant at the 99% confidence level. Figure 3, Tables 8 and 9 present the statistical outcomes of the extended TPB model, including path coefficients for hypothesis testing, T-statistics, and overall impact effects.

Structural Model Results.

Note. STDEV = standard deviation; ATT = attitude; PBC = perceived behavioral control; SN = subject norm; BALI = behavior of allocating the life insurance; PI = intention to increase household expenses; PB = behavior of increasing household expenses.

Represents that it is significant at the significance level of .01.

The proposed extended TPB model.

Total Effects from the PLS-SEM Analysis.

Note. STDEV = standard deviation; ATT = attitude; PBC = perceived behavioral control; SN = subject norm; BALI = behavior of allocating the life insurance; PI = intention to increase household expenses; PB = behavior of increasing household expenses.

Represents that it is significant at the significance level of .01.

The Effect of Attitudes, Social Norms, and Perceived Behavioral Control on Household Consumption Intentions

Analysis of the determinants of consumption intention and behavior indicates that Attitude, Subjective Norm, and Perceived Behavioral Control significantly influence consumption intention. Specifically, the path coefficient of attitudes on consumption intention is 0.246 (t = 4.166, p < .01), indicating that a positive household consumption attitude significantly enhances consumption intention. The path coefficient of subjective norms is 0.190 (t = 14.85, p < .01), suggesting that the opinions of family members and social networks positively impact consumption intentions. Similarly, the path coefficient of perceived behavioral control is 0.315 (t = 19.887, p < .01), which reveals greater household confidence in financial capability is associated with stronger consumption intentions. This underscores the critical role of attitudes, subjective norms, and perceived behavioral control in shaping consumption intentions (Xu et al., 2019).

The Effect of Life Insurance on Household Consumption Attitudes, Social Norms, Perceived Behavioral Control, and Consumption Intentions

Regarding life insurance, its impact on attitude, subjective norms, perceived behavioral control, and consumption intention is positive. Among them, life insurance exerts the strongest influence on perceived behavioral control (path coefficient = 0.645, t = 49.21, p < .01) and consumption attitudes (path coefficient = 0.631, t = 14.037, p < .01). This implies that life insurance significantly boosts behavioral control and consumption attitudes, leading to higher expenditures. However, its influence on subjective norms (path coefficient = 0.502, t = 6.619, p < .01) and consumption intention (path coefficient = 0.267, t = 5.802, p < .01) is weaker.

Although the direct effect of life insurance on household consumption intentions is weak, its total effect is significantly higher (total effect = 0.72, t = 29.016, p < .01), as shown in Table 9. Life insurance primarily enhances consumption intentions through mediating variables rather than directly influencing consumption by reducing future uncertainty and increasing financial security.

The Impact of Consumption Intentions on Consumption Behavior

This study conducts a statistical analysis of the total effects of various independent variables on consumption behavior. Analyzing total effects is crucial for comprehensively understanding the relationships between variables, facilitating a better interpretation of research phenomena and prediction of outcomes (Sarstedt et al., 2017).

The path coefficient between household consumption intention and actual consumption behavior is notably high (path coefficient = 0.862, t = 5.524, p < .01), indicating that household consumption intention is a key driver of consumption expenditure.

Attitude, perceived behavioral control, and subjective norms also exert comparable influences on consumption behavior, with values of 0.212, 0.271, and 0.164, respectively. In terms of the impact of life insurance, life insurance exhibits the strongest indirect effect on consumption behavior (total effect = 0.621, t = 23.206, p < .01). It indicates that financial security tools like life insurance significantly shape household consumption decisions, potentially outweighing short-term influences such as attitude, subjective norms, and perceived behavioral control.

Artificial Neural Network Analysis

The ANN model replicates the structure and function of neural networks found in the human brain. It can learn, recognize patterns, and make predictions from complex input data (Patel et al., 2015). In the analysis of variable importance, ANN primarily evaluates the direct contribution of input variables to output variables through neuron connection weights (Hiran & Dadhich, 2024). The specific pathway is as follows:

where N represents a mediating variable or hidden layer, X denotes the independent variable, and Y refers to the dependent variable.

To ensure the accuracy and reliability of the findings, this study proposes an ANN model based on partial least squares. Before training the model, this study first conducted a multicollinearity test on the input variables to prevent potential impacts on predictive capabilities. Although a multicollinearity check have already been performed prior to using the PLS-SEM model, an additional assessment was conducted at this stage due to structural and estimation differences in the ANN model. This step aims to further enhance the performance of the ANN model. As shown in Table 10, the Variance Inflation Factor (VIF) values for attitude, perceived behavioral control, behavior of allocating life insurance, subject norm, and purchase intention are all below the threshold (VIF = 5), showing that multicollinearity among the input variables is minimal (Hair et al., 2010).

Multicollinearity Test for Independent Variables in the ANN Model.

Note. ATT = attitude; PBC = perceived behavioral control; SN = subjective norm; BALI = behavior of allocating life insurance; PI = intention to increase household expenses.

Moreover, to enhance the model’s learning capability, all input data was normalized by scaling it to a range of 0 to 1 before training. This helps achieve a more even distribution of the input data, preventing discrepancies in variable scales from affecting model training. (Liébana-Cabanillas et al., 2017).

After data pre-processing, the ANN model was built using SPSS v27 software. The model includes input, output, and hidden layers. The input layer contains five variables (ATT, PBC, SN, BALI, and PI), while the output layer has one variable (PB). The model also includes two hidden layers, with the number of neurons automatically determined by SPSS. The Sigmoid function was applied to both input and output layers to capture nonlinear relationships and adapted to complex data structures (Bishop, 1995; Rumelhart et al., 1986). Additionally, this function helps prevent vanishing or exploding gradient issues (Goodfellow et al., 2016). Detailed information is provided in Figure 4.

The map of neural network architecture.

As overfitting could still occur(Goodfellow et al., 2016), the study used a 10-fold cross-validation method, with 70% of the data for training and 30% for testing (Yadav et al., 2016). The model’s performance was evaluated using the Root Mean Square Error (RMSE), where lower RMSE values indicated better predictive accuracy (Liébana-Cabanillas et al., 2017; Tan et al., 2014). The formula for computing Root Mean Square Error (RMSE) is:

where

Training and Testing Criterion.

Note. SD = standard deviation; N1 = number of training samples, N2 = number of testing samples; N1 + N2 = 505; SSE = sum square of errors.

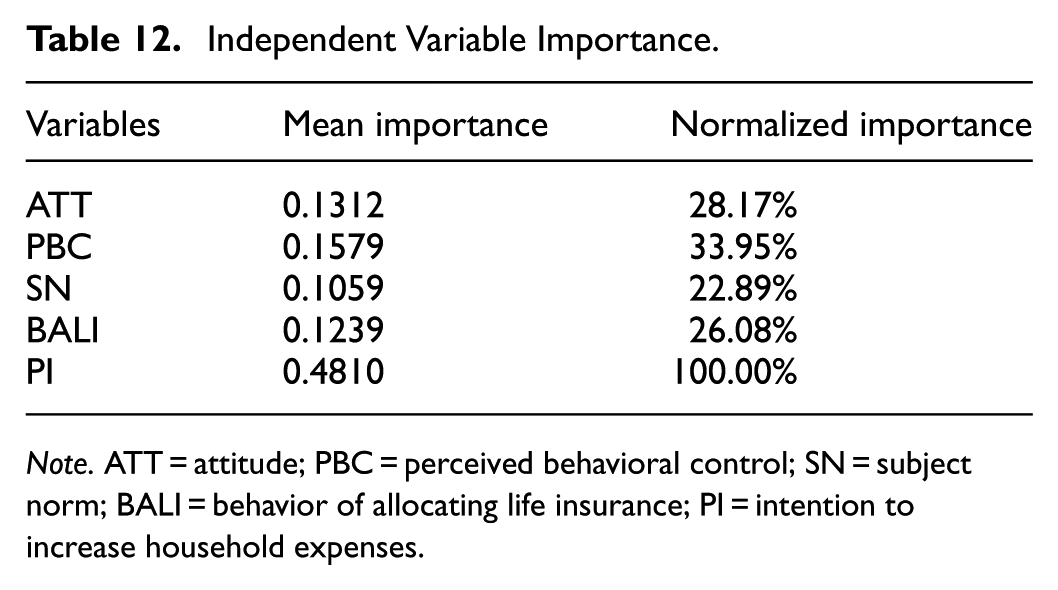

Following the successful testing of the ANN model, this study analyzes the predictive impact of five variables (ATT, PBC, SN, BALI, PI) on PB. Intention to Increase Household Expenses (PI) emerged as the strongest predictor of Consumption Behavior (PB), followed by Perceived Behavioral Control (PBC) at 33.95%, Attitude (ATT) at 28.17%, Life Insurance Allocation Behavior (BALI) at 26.08%, and Subjective Norms (SN) at 22.89%. The detailed results are presented in Table 12.

Independent Variable Importance.

Note. ATT = attitude; PBC = perceived behavioral control; SN = subject norm; BALI = behavior of allocating life insurance; PI = intention to increase household expenses.

Comparison of ANN and PLS-SEM Model Results

As shown in Table 13, when comparing the results of the ANN model with PLS-SEM, the predictive importance (normalized) and overall impact of consumption intention, perceived behavioral control, attitudes, and subjective norms on household consumption expenditures were consistent. However, differences were noted regarding the significance of life insurance purchasing behavior. The ANN model assigns less importance to life insurance purchasing behavior in predicting household consumption expenditure, while PLS-SEM indicates a greater overall effect, ranking it second only to consumption intention.

Comparison of the Results Between the PLS-SEM Model and ANN Model.

Note. STDEV = standard deviation; ATT = attitude; PBC = perceived behavioral control; SN = subject norm; BALI = behavior of allocating the life insurance; PI = intention to increase household expenses; PB = behavior of increasing household expenses.

Represents that it is significant at the significance level of .01.

Discussion

Overall Effect of Life Insurance Allocation on Household Consumption Spending

Path Analysis of Household Consumption Behavior Using the Extended Tpb

This research examines the relationship between life insurance allocation behavior and household consumption expenditure in China.

Life insurance significantly influences attitudes toward increased consumption expenditure, primarily by providing households with a relatively stable cash flow and personal life security. Due to its substantial cash value, life insurance is considered an effective family financial planning tool compared to other financial products (Brown, 2008; Williams et al., 1998). By acquiring life insurance, families can strategically plan for future cash flow, reducing concerns about financial uncertainty and promoting a higher propensity to increase consumer expenditure rather than just saving. Moreover, life insurance provides psychological security, as the payout after the insured’s death can help families manage unexpected financial burdens. Thus, assuming a stable income, families with life insurance policies are more confident in increasing household consumption spending. Overall, life insurance allocation significantly enhances a household’s financial resilience, strengthening both consumer confidence and attitudes toward consumption.

Life insurance also significantly affects perceived behavioral control. By purchasing life insurance, household members not only gain financial security but also feel more in control of future concerns. This leads to a more optimistic assessment of the household’s financial outlook and greater confidence in consumption decisions. Therefore, under the premise of constant total income, households with life insurance policies exhibit greater confidence in increasing their proportion of consumption expenditure.

Life insurance also significantly affects subjective norms. In some socio-cultural contexts, purchasing life insurance is viewed as a prudent and rational financial decision. After obtaining life insurance, household members perceive greater recognition and expectation from friends, colleagues, and others regarding their financial responsibility. This, in turn, reinforces the influence of subjective norms, encouraging them to plan household consumption expenditures more rationally rather than solely focusing on savings. However, the complex terminology of insurance contracts and deficiencies in the Chinese insurance market are likely to reduce households’ trust in life insurance plans, negatively affecting their propensity to consume. Additionally, since most life insurance policies restrict cash value withdrawal for a specified period, some households may face reduced short-term liquidity after purchasing a policy. This could contribute to the lower path coefficient observed for life policies’ impact on consumption expenditures.

Life insurance positively impacts the propensity to increase consumption expenditure, although its path coefficient is lower than that of attitudes, perceived behavioral control, and subjective norms. This may be because the substantial cash value of life insurance eventually exceeds the total premiums paid over time (Black et al., 2000). Policyholders can access the cash value by surrendering the policy, using the funds to enhance consumption. Unlike other financial products, such as banking, the cash value of life insurance is typically fixed in the contract (Rejda & McNamara, 2014), and the insurance company cannot adjust it after the policy is sold. As a result, the savings function of life insurance may encourage households to take a more assertive approach to consumption.

In terms of behaviors that increase consumption, attitudes, perceived behavioral control, subjective norms, willingness, and life insurance all have a strong positive effect on consumption expenditure. Willingness to consume has the greatest overall influence on increasing household consumption, consistent with the findings of previous studies (Bao et al., 2020; Xu et al., 2019). The overall impact of life insurance on consumption expenditure is 0.621, surpassing the influence of attitudes, subjective norms, and perceived behavioral control, ranking second. This suggests that a household’s decision to acquire life insurance policies can significantly impact future expenditures.

Comparative Analysis of ANN Model Results and PLS-SEM Model Results

This study employs both the PLS-SEM model and the ANN model to provide a more comprehensive explanation. The results indicate that although both models confirm the significant positive impact of attitudes, subjective norms, perceived behavioral control, and life insurance allocation behavior on household consumption behavior, there are notable differences in the ranking of variable importance.

This discrepancy can be attributed to structural differences and variable weight calculations between the two models. From a structural perspective, PLS-SEM is based on linear assumptions, making it more inclined to analyze linear relationships or causal connections between variables. As a result, PLS-SEM may struggle to capture nonlinear interactions among variables. Conversely, ANN allows for nonlinear mappings, enabling it to detect more complex nonlinear interactions among variables (Hiran & Dadhich, 2024). For instance, the impact of life insurance on household consumption expenditure may be influenced by external factors such as policy environment, cognitive biases, and financial capability. These nonlinear interaction effects can be captured by ANN instead of PLS-SEM, reducing the predictive significance of life insurance in this model. In contrast, PLS-SEM fails to reveal these nonlinear interaction effects, potentially overestimating the importance of life insurance.

Regarding the calculation method of variable weights, the direct effect of life insurance on household consumption intention is relatively weak. Instead, its impact is primarily mediated through attitudes, subjective norms, perceived behavioral control, and consumption intention, exerting a stronger total effect, which in turn influences household consumption behavior. As depicted in Figure 5, compared to attitudes, subjective norms, and perceived behavioral control, life insurance influences consumption behavior through a more complex mediation pathway. This intricate mediation mechanism may weaken the predictive capability of life insurance on household consumption behavior.

Simplified path network of PB.

Theoretical and Practical Implication

This study examines the impact pathways and magnitude of life insurance allocation behavior on household consumption expenditure, thoroughly examining how life insurance indirectly influences consumption behavior through psychological mechanisms. Additionally, to enhance the robustness of the findings, this study integrates PLS-SEM with ANN to strengthen the study’s reliability and explanatory power.

Theoretical Implication

This study extends the traditional TPB by examining the influence of external factors, such as life insurance, on household consumption. This extension strengthens the theoretical foundation of consumption behavior and provides a new perspective on how financial decisions influence household consumption through psychological factors. Unlike previous studies, this research finds that life insurance has a relatively limited direct impact on household consumption behavior. Instead, in most cases, its impact is mediated by psychological factors, indirectly shaping household consumption decisions.

Second, the study attempts to introduce an innovative methodology that integrates SEM with ANN learning. While existing research predominantly relies on a single SEM approach to explore the relationship between consumption intention and consumption behavior, this study innovates by incorporating ANN to validate SEM results, thereby strengthening the understanding of complex behavioral patterns. Additionally, this integration provides a more robust theoretical framework for studying the impact of insurance on consumption behavior.

This study also contributes to the body of research on precautionary savings theory by examining how life insurance influences household consumption expenditure. This provides both empirical evidence and a theoretical foundation for the further development of precautionary savings theory. The research on precautionary savings theory has traditionally focused on cash savings and investments, paying less attention to life insurance as a factor in household consumption and savings decisions. This study demonstrates that life insurance policies with high cash value can, to some extent, serve as a substitute for traditional cash-saving tools. When life insurance is adequate, households may reduce their need for precautionary savings and reallocate some resources to consumption. Additionally, the protective function of life insurance can assist in reducing the inclination to accumulate excessive savings, encouraging households to increase their consumption.

Practical Implication

This research offers valuable insights into the financial planning and risk management of households, with a particular emphasis on the role of life insurance in assuring financial security and stabilizing consumption. Not only does life insurance offer long-term financial protection, but it also assists households in maintaining their consumption levels during periods of income uncertainty, due to its substantial cash value. In response to financial instability, conventional risk management theories propose that consumers tend to decrease expenditure and increase savings. Nevertheless, this research demonstrates that life insurance reduces income volatility and improves household financial stability, thus helping families maintain or even increase their consumption levels during economic downturns or uncertain income periods.

Stabilizing family consumption expenditures serves to sustain society’s total consumption demand and contributes to economic development. Life insurance fosters consumer confidence and prevents the widespread consumption repression caused by economic instability. Therefore, insurance-based financial strategies have important implications for macroeconomic policies, and this study can provide references and inspiration for government policies to stabilize consumption and promote economic recovery in the context of global economic uncertainty.

Conclusions and Future Research

Conclusion

Chinese society is undergoing significant changes in its economic development and consumption patterns. Due to the global economic downturn and the cautious spending habits of Chinese citizens, China’s export-driven economy faces major challenges, leading to rising unemployment and increased social tensions. Therefore, examining how life insurance affects household consumption is crucial for improving consumption levels and promoting economic growth.

This study investigates the impact of life insurance on household consumption using data from 505 nationwide household surveys and employing the TPB, PLS-SEM, and ANN models. The key findings are as follows:

Attitude, subjective norms, and perceived behavioral control significantly affect consumption intention, consistent with prior research. The influence of consumption intention on consumption behavior is also strong, confirming the findings of Xu et al. (2019). This study, while acknowledging previous research, innovatively incorporates artificial neural networks to explore how attitudes, subjective norms, and perceived behavioral control influence consumption willingness. It also contrasts these findings with PLS-SEM results, offering a new perspective on the TPB.

Life insurance significantly impacts the consumption attitudes, subjective norms, perceived behavioral control, and consumption intentions of Chinese households. The allocation behavior of life insurance encourages changes in family consumption habits and increases household spending. While there has been extensive discussion about the savings features of life insurance, current research lacks quantitative analysis and empirical examination of its effects on household finances. Many studies overlook the critical role of household financial status and actual consumption capacity in raising overall consumption levels.

Indeed, among the 505 households surveyed, more than half (56.8%) have savings exceeding 200,000 RMB (28,000 USD), and about 71.9% report that their daily income exceeds their expenses. This suggests that the consumption potential of Chinese households is underutilized, likely influenced by their expectations of future economic growth. Over 30% of respondents are not optimistic about China’s economic future. However, life insurance can act as a financial tool to enhance household consumption potential and stimulate economic vitality. These policies shape attitudes, subjective norms, perceived behavioral control, and willingness to consume, thereby indirectly influencing consumption capacity.

The results are consistently confirmed by both economic models (PLS-SEM and ANN). While the magnitude of the factors’ influence on consumption behavior differs between the models, both affirm the positive effect of life insurance on consumption behavior, enhancing the study’s reliability.

Suggestions

Initially, from a familial standpoint, a comprehensive financial strategy should be developed, with life insurance as a key component. In creating this strategy, families must carefully assess factors such as the age, occupation, and health status of family members, as well as their financial situation, to choose appropriate life insurance products. Families should also regularly review and adjust their financial plans to ensure that life insurance policies’ coverage remains suitable for their needs. By fully utilizing the cash value of life insurance for financial planning, families can achieve asset preservation and growth while maintaining their purchasing power.

Secondly, insurance companies must improve the training and management of their sales staff to ensure they have a thorough understanding of insurance products and adhere to high ethical standards. Sales personnel should be able to assess customers’ needs and risk tolerance accurately, provide tailored insurance solutions, and clearly explain the terms and coverage of insurance products. Additionally, insurers should streamline the claims process and improve claims management efficiency to ensure clients receive timely payouts, which will help reduce skepticism toward insurance providers.

Thirdly, from the government’s perspective, it should strengthen its oversight of the insurance market to ensure that companies operate in compliance with regulations. The government should also implement policies that encourage insurance companies to innovate their products and services to meet diverse family needs. For example, tax incentives or subsidies could be provided to lower life insurance costs, stimulate market activity, and encourage families to engage in preventive savings. This would support China’s strategic goal of expanding domestic demand and improving consumer quality. Additionally, the government ought to improve the distribution of insurance-related information and education to elevate public understanding of insurance as well as risk management.

Limitations and Future Research

The limitations of this study may stem from inherent boundaries of methodology and theoretical frameworks. First, the ANN and PLS-SEM approaches exhibit irreconcilable methodological disparities in capturing nonlinear relationships and latent causal pathways. ANN excels at identifying complex interaction effects but cannot directly deconstruct rational decision-making mechanisms in social behaviors, whereas PLS-SEM’s theory-driven path analysis may overlook dynamic stochasticity in real-world contexts. Such differences reflect fundamental conflicts between statistical paradigms (data-driven vs. theory-driven), which cannot be fully resolved by expanding sample sizes or optimizing variable selection. Nevertheless, future research could still consider incorporating additional mediating or moderating variables, such as financial literacy, household income, and dependency ratio, to further explore the mechanisms.

Furthermore, the cross-cultural applicability of findings is constrained by the non-reproducibility of socio-economic systems. Systemic variations in social safety nets, cultural norms of household risk aversion, and accessibility of consumer credit across countries (e.g., high savings traditions in East Asian families vs. credit dependency in Western households) may embed the “consumption-smoothing effect” of life insurance within specific institutional and cultural path dependencies.

Additionally, this study collects data through an online survey, which may introduce sampling bias. As a result, the sample is more likely to consist of individuals with a certain level of digital literacy, such as middle-class or younger households. Therefore, future research could consider employing a combination of online and offline surveys to further examine variations in responses to life insurance and consumption behavior across different demographic groups. Since self-reported measures of insurance and spending habits could have social choice bias, using actual customer data from insurance companies could make the study more objective and correct.

Footnotes

Ethical Considerations

Our study did not require further ethics committee approval as it did not involve animal or human clinical trials and was not unethical.

Consent to Participate

In accordance with the ethical principles outlined in the Declaration of Helsinki, all participants provided informed consent before participating in the study. The anonymity and confidentiality of the participants were guaranteed, and participation was completely voluntary.

Author Contributions

Minghao Chen: Conceptualization, Writing-Reviewing and Editing, Visualization, Investigation; Yueling Xu: Conceptualization, Methodology, Software; Jiafeng Chen: Writing-Original draft preparation, Software, Validation.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by the Hangzhou Philosophy and Social Science Planning Regular Project (No. Z24YD046) and A Project Supported by Scientific Research Fund of Zhejiang Provincial Education Department (No. Y202455848).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.