Abstract

The tax system provides the necessary financial resources to a country’s administration to use the collected resources for the welfare of the general public and the development of general infrastructure. Therefore, compliance with the prevailing tax system is necessary for a country’s political and administrative system to survive. The current study aims to explore the intention to comply and the compliance behavior toward the tax system among Malaysian taxpayers. The data were collected using the survey method, and quantitative data were analyzed using the dual-stage methods of partial least squares structural equation modeling (PLS-SEM) and artificial neural network (ANN). The analysis results showed that the perceived fairness of the tax system, tax penalties, and tax awareness were significantly related to the intention to comply with the tax rules and regulations. Furthermore, the intention to comply with the tax system significantly influenced tax compliance behavior. The ANN analysis confirms that tax awareness, tax penalties, and fairness perception are the three most important factors influencing tax compliance. The tax authorities need to build the taxpayers’ confidence in the prevailing tax system and streamline the tax system to reduce tax complexity. Consequently, the taxpayers will start paying the correct and timely tax liabilities. The study’s limitations and future research avenues are documented at the end of this paper.

Introduction

A country’s economic development and growth reflect the efficacy of the prevailing tax system in that country (Noor Azmi et al., 2020). Active taxpayers complying with the prevailing tax regulations bring the necessary monetary resources needed to pursue the development and redistribution of resources collected by the tax authorities (Ghani et al., 2020). On the other hand, non-compliance with the tax system is common around the globe (Evans & Tran-Nam, 2014). Individuals are reluctant to comply with the tax rules and regulations, which has established barriers to an effective tax system (Brockmann et al., 2016).

The primary purpose of a tax system is to generate revenue for the government to perform administrative activities (Palil & Mustapha, 2011). Thus, the tax revenue system helps generate financial resources to develop the economic conditions and redistribute the resources from the rich to the poor (Ghani et al., 2020). Nevertheless, most prospective and existing taxpayers are avoiding tax payments in one way or another (Loo, 2016). Therefore, tax authorities need to raise the tax rates or impose multiple tax types to increase the government revenue (Rahmayanti et al., 2020). Taxpayers’ compliance with the tax rules and procedures is vital for the progress of a nation and the government’s effort to provide social support to the poor of the country (Musimenta, 2020).

The Malaysian tax administration replaced the official self-assessment system (SAS) with the self-assessment system (SAS) in 2001 (Remali et al., 2018). SAS was a significant reform since the enforcement of the Income Tax Act (ITA) 1967. Tax complexity has reduced with the introduction of SAS (Palil & Mustapha, 2011). The SAS facilitates the taxpayers, and fewer supporting documents are required to establish the taxpayers’ income.

Non-compliance with the tax system is the biggest obstacle to the effectiveness and success of the tax collection capacity of the tax system (Remali et al., 2018). The non-compliance with the tax system leads to the imposition of tax penalties and tax audit fees to the taxpayers (Ghani et al., 2020). Nonetheless, the non-compliance with the tax system increases over time as taxpayers use every opportunity to pay lower taxes (Saad, 2012). Non-compliance with tax legislation refers to behavior that fails to comply with the requirements the tax authorities have stipulated (Richardson, 2006). Non-compliance with the tax system has significant consequences for tax collection and efficiency (Hamid et al., 2022). There were two million active taxpayers in Malaysia, with about 80,000 prospective taxpayers who needed registration, while the Malaysian tax authorities lost approximately RM 2,000 million of tax collection in 2019 (Noor Azmi et al., 2020).

The Malaysian tax authorities are making attempts to improve compliance with the tax system and encourage Malaysian taxpayers to pay the entire tax liability to achieve the growth of Malaysia (Sapiei et al., 2014). Certain individuals make every effort to evade the tax liability or understate the income earned in a tax year (Youde & Lim, 2019). Human behavior plays a significant role in the compliance and avoidance behavior toward tax systems internationally and specifically in Malaysia (Rashid et al., 2021). A tax payer’s decision to engage or evade the tax payment is complex and requires multiple perspectives to explore the tax compliance behavior (Coita et al., 2021). Tax avoidance is described as the taxpayer’s behavior to reduce tax obligation using the rules and regulations of the prevailing tax system (Zandi et al., 2016). Non-compliance with the tax system is a global phenomenon and shows the lack of robustness of the prevailing tax system in a country (Jaffar et al., 2021; Remali et al., 2018).

In this context, it is necessary to explore the taxpayers’ intention to comply and the compliance behavior toward the tax system in Malaysia with regard to the taxpayers’ perception of the tax system attributes. The current study aims to explicate the influence of tax awareness, morals, complexity, penalties, and tax fairness on the intention to comply with the tax system. The intention to comply with the tax system instigates the tax compliance behavior. To explain tax compliance intention and behavior, the current study first used a dual analytical technique based on PLS-SEM and ANN analysis. The study adds to the body of knowledge by explaining tax system attributes and deterrence toward the tax system, thereby influencing tax compliance intention and later compliance behavior. The current work provides empirical evidence for the implication of deterrence and the framework explains tax compliance behavior.

The following section offers a detailed discussion about the relevant literature and the hypotheses development. Next, the research methodology adopted in the current research is described, followed by the data analysis and discussion sections. Finally, this paper ends with the conclusion section.

Literature Review

Theoretical Foundation

Tax compliance is necessary for the development of both rich and emerging countries. However, tax non-compliance is motivated by the desire to reduce the tax liabilities of an individual or a firm (Noor Azmi et al., 2020). Tax compliance represents the degree to which a taxpayer complies with the prevailing tax rules and regulations (Youde & Lim, 2019). Deterrence theory is utilized as the central theoretical framework to depict tax compliance (Taofeeq, 2018). The deterrence approach suggests that taxpayers make a cost-benefit analysis to decide their tax compliance behavior. Tax penalties and tax sanctions determine individual tax compliance and the implementation of tax laws and tax sanction levels (Devos, 2007). Tax compliance is a deterrence based on tax awareness, tax penalties, tax audits, and tax rates. Paying tax liabilities based on deterrence outperforms avoiding tax audits, penalties, or compliance due to fear (Noor Azmi et al., 2020).

On the other hand, the attribution theory is defined as finding what motivates or restricts a person from taking action (Kamil, 2015). Attributes are the causes that influence human behavior, and individuals use these factors to explain their actions. Internal and external factors surrounding the taxpayer influence their tax compliance behavior. The tax system’s attributes facilitate and suggest the importance of promptly taxing the liabilities fully to support the country’s development. Nevertheless, specific tax system attributes undermine the tax system’s positive attitude, and individuals do not pay taxes on time or pay the total amount. Perceived factors of tax compliance are tax awareness, tax morale, and tax fairness perception, while the external factors are tax penalties and tax complexity.

Hypotheses Development

Fairness perception

Perception of fairness relates to the provision of justice, equality, and impartiality toward any system. It defines taxpayers’ feelings toward the tax system’s imposition of fair tax liabilities according to the taxpayers’ abilities (Azmi et al., 2016). The fairness perception in the tax system depicts that the tax system has justice and impartial rules and procedures that offer a sense of equality and reduce the misconception that decreases compliance behavior (Richardson, 2006). The perception of tax fairness is described at the horizontal and vertical levels. Horizontal fairness relates to taxpayers and perceives that all taxpayers with the same economic conditions need to pay the same tax (Saad, 2012).

Meanwhile, vertical fairness is described as the perception among the taxpayers having different economic needs to pay accordingly. Azmi et al. (2016) have postulated that the perception of fairness leads to the intention to comply with the tax system. Therefore, in the current study, the following hypothesis is proposed:

Hypothesis (H1): Tax fairness perception is positively related to the intention to comply with the tax system among individual taxpayers in Malaysia.

Tax penalty

Paying tax on time is the personal duty of every taxpayer. A tax penalty is a punishment for not complying with the implemented tax rules and regulations (Saad, 2012). It is a disciplinary measure to impose a monetary or non-monetary fee for non-compliance exhibited by an individual (Taofeeq, 2018). Tax penalty promotes the attitude to comply with implemented tax laws and procedures for tax collection (Brockmann et al., 2016). Tax compliance can involve administering the tax laws and dealing with violations (Rahmayanti et al., 2020). Tax penalty promotes tax awareness and harnesses tax compliance forcefully (Palil & Mustapha, 2011). Furthermore, the tax penalty acts as an attribute of the tax system to consider the enforcement of the tax system and the likelihood that non-compliance may result in a penalty to tackle tax evasion in a monetary aspect or via imprisonment (Kamil, 2015). Thus, this hypothesis is proposed:

Hypothesis (H2): Tax penalty is positively related to the intention to comply with the tax system among individual taxpayers in Malaysia.

Tax morale

Confidence in the tax system harnesses the intention to comply with the tax system. Tax morale signifies the tax system’s attitude whereby tax morale is described as the intrinsic motivation to promptly pay tax (Alasfour et al., 2016). Moreover, tax morale fulfills the civic duty to pay the right amount of tax on time since paying tax is a national duty. The collected tax is utilized for the development of society (Youde & Lim, 2019). Thus, tax morale depicts the individual’s tax compliance motive and understanding that the tax framework is an acceptable norm of collecting money utilized for public welfare (Luttmer & Singhal, 2014). Ghani et al. (2020) postulated that tax morale significantly impacted the intention to comply with the tax system. Hence, the following hypothesis is proposed in this study:

Hypothesis (H3): Tax morale is positively related to the intention to comply with the tax system among individual taxpayers in Malaysia.

Tax awareness

Tax awareness depicts an individual’s understanding of the importance of the tax system (Youde & Lim, 2019). Individual-level tax awareness shows the recognition of tax mechanisms and prevailing tax laws (Taofeeq, 2018). Tax awareness indicates the importance of the tax system for public welfare (Savitri & Musfialdy, 2016). A thorough understanding of tax awareness suggests a possible link with tax compliance (Zandi et al., 2016). Tax awareness makes the taxpayers conscious of paying taxes and promotes public wellbeing (Rahmayanti et al., 2020). As such, this study proposes the following hypothesis:

Hypothesis (H4): Tax awareness is positively related to the intention to comply with the tax system among individual taxpayers in Malaysia.

Tax complexity

Tax complexity represents the perception of difficulty or strain at the taxpayers’ end (Coita & Mare, 2021). The associated tax complexity was acknowledged at the tax instrument and tax laws levels (Taofeeq, 2018). Tax complexity directs the difficulty perceived by the taxpayers toward the tax system that encourages tax non-compliance (Kamil, 2015). Besides, tax complexity shows the non-understanding of the tax rules and procedures that leads to tax non-compliance (Ghani et al., 2020). Hence, the following hypothesis is proposed in this study:

Hypothesis (H5): Tax complexity is negatively related to the intention to comply with the tax system among individual taxpayers in Malaysia.

Intention to comply with the tax system and tax compliance

The intention to behave in a particular manner significantly represents the behavior. Tax compliance is the taxpayers’ decision to comply with the prevailing tax laws and regulations to pay tax accurately and on time (Swee Kiow et al., 2021). The intention to comply with the tax rules instigates compliance behavior (Rahmayanti et al., 2020). Therefore, the following hypothesis is proposed in this current study:

Hypothesis (H6): Intention to comply with the tax system positively influences tax compliance among individual taxpayers in Malaysia.

Research Methodology

Research Design

In the current study, a cross-sectional and quantitative approach were employed to explain the influence of the factors impacting the intention to comply and the compliance behavior among Malaysian taxpayers. In this explanatory study, data were collected in a cross-sectional fashion. The causal-predict data analysis technique, partial least squares structural equation modeling (PLS-SEM), and artificial neural network (ANN), were utilized for the hypothesis testing.

Population and Sample

The target population of the current study was the Malaysian taxpayers. The sample size calculation was performed with G-Power 3.1 with a power of 0.95 and an effect size of 0.15 with seven predictors. The required sample size was 84 (Faul et al., 2007). However, a minimum of 200 samples is suggested for PLS-SEM (Hair et al., 2019). Hence, this study employed the second-generation statistical analysis technique of structural equation modeling, whereby data from 500 respondents were collected.

Survey Instrument

The survey instrument used in this study was a structured questionnaire. All the question items were taken from earlier studies with minor modifications. To gauge tax morale, five items were taken from Alasfour et al. (2016), while for fairness perception, the questions were adapted from the work of Taofeeq (2018). Next, tax awareness was estimated with six question items taken from Noor Azmi et al. (2020), whereas tax complexity was assessed with five items from Sapiei et al. (2014) and Saad (2012). Lastly, the tax penalty was estimated using five items from Loo (2016). In this study, a five-point Likert scale (not important, slightly not important, neutral, slightly important, and very important) was used to measure the variables.

Common Method Bias (CMB)

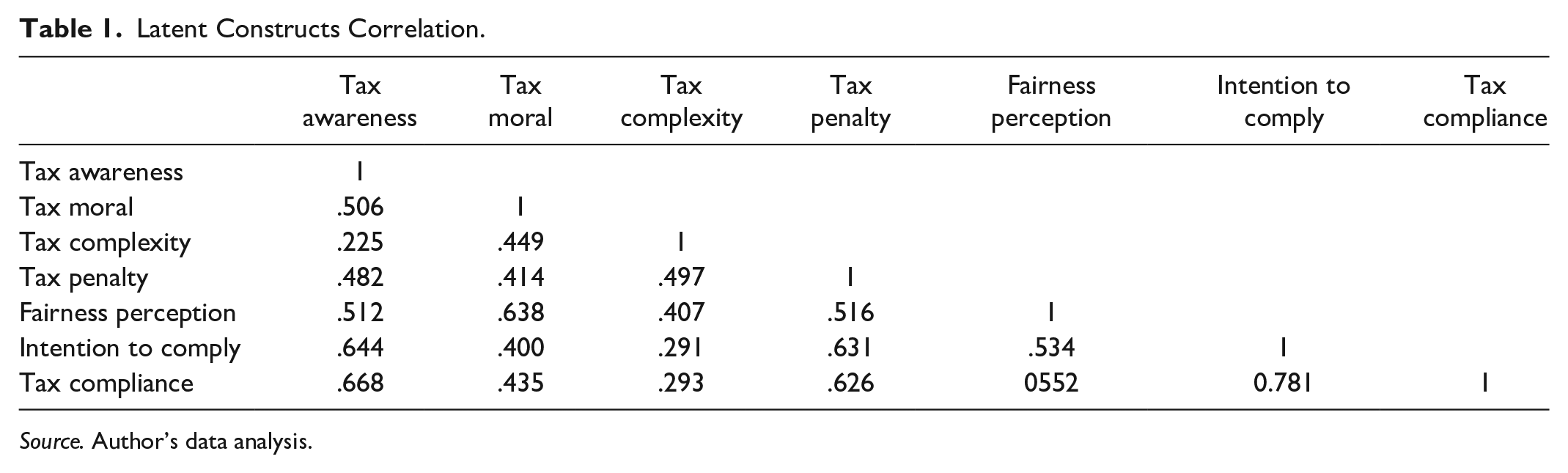

Cross-sectional studies are commonly associated with common method bias; CMB was assessed using multiple methodological and statistical tools (Podsakoff et al., 2012). The current study applied Harman’s one-factor test to determine CMB’s effect as a diagnostic technique. The single factor accounted for 25.9%, which was below the recommended threshold of 40.0% in Harman’s one-factor test, thus, confirming the inconsequential influence of CMB on this study (Podsakoff et al., 2012). Latent factors correlation also showed no issue of CMB among the study constructs, whereby the correlation among the latent constructs was less than .90 (Podsakoff et al., 2012). The results are listed in Table 1.

Latent Constructs Correlation.

Source. Author’s data analysis.

Multivariate Normality

Hair et al. (2019) have suggested evaluating the multivariate data normality before using SmartPLS. Therefore, multivariate normality for the study data was assessed with the Web Power online tool (source: https://webpower.psychstat.org/wiki/tools/index). The calculated Mardia’s multivariate p-value revealed that the study data had a non-normality issue because the p-values were below 0.05 (Cain et al., 2017).

Data Analysis Method

Partial Least Squares Structural Equation Modeling (PLS-SEM)

Due to the existence of multivariate non-normality in the dataset, this study used PLS-SEM. Hair et al. (2019) have recommended adopting variance-based structural equation modeling to analyze the exploratory nature and non-normality issues in-depth in the structural equation model’s dependent constructs. The Smart-PLS 3.1 programme was employed to analyze the data collected in the current study. PLS-SEM is a multivariate exploratory method for analyzing integrated latent constructs’ paths (Hair et al., 2019). It empowers researchers to work well with non-normal data when they have a small dataset. Furthermore, PLS-SEM is a casual-predictive analytical tool to execute complex models with composites and has no specific assumption of the goodness-of-fit static requirements (Chin, 2010). PLS-SEM analysis is performed in two phases. The first step deals with model estimation, where the constructs’ reliability and validity are evaluated (Hair et al., 2019). Phase two deals with evaluating the correlations of the models and the systematic testing of the study path model (Chin, 2010). The analysis performed with r2, Q2, and effect size f2 can explain the endogenous construct’s change caused by the exogenous constructs (Hair et al., 2019).

Artificial Neural Network (ANN) Analysis

ANN analysis is a non-compensatory analytical approach built on three levels, namely the input, output, and hidden layers (Gbongli et al., 2019). The hidden layer links the input and output neurons. Besides, the hidden layer functions like the human brain’s block-box (Hayat et al., 2020). The data is divided into three sections: training, testing, and hold-out sample. The predictive score is determined using the training and tested data’s root mean square errors (RMSE) (Gbongli et al., 2019). The more significant the gap between the RSME scores of training and tested data, the greater the predictive accuracy (Hayat et al., 2021). A sensitivity analysis was executed to determine the relative impact of each exogenous component. The normalized relevance of each exogenous component indicates the effect on the endogenous structure (Leong et al., 2020). Following that, the average synaptic weights aided in understanding the contribution of the input and hidden layers on the output (Hayat et al., 2020).

Data Analysis

Demographic Profile

48.4% were men, and 51.6% were women among the study respondents. Next, 60.9% of the study respondents were single, while 36.4% were married, 2.0% were divorced, and the rest were widowed. The respondents were divided into five age groups, that is, 18 to 25 (39.2%), 26 to 35 (45.5%), 36 to 45 (10.3%), 46 to 55 (4.5%), and 56 to 65 (0.5%) years old. Among the 1,061 respondents, 6.2% had secondary school level education, 10.7% had a diploma certificate level education, 60.0% had a bachelor degree-level education, 20.5% had a master-level education, and the remaining had a doctoral-level education. Meanwhile, 69.3% were full-time employees, 13.4% worked part-time, and the rest were seeking employment opportunities. Besides, 41.2% of the respondents had a monthly income of less than or up to RM 2,500, 22.0% had between RM 2,501 and RM 5,000, 17.6% had between RM 5,001 and RM 7,500, and 10.8% had between RM 7,501 to RM 10,000. Respondents working in the upper management level comprised 12.6%, while 32.1% worked in the middle management level, and 38.3% at the junior management level. The remaining respondents were working in self-employed settings. The results are provided in Table 2.

Demographic Characteristics.

Reliability and Validity

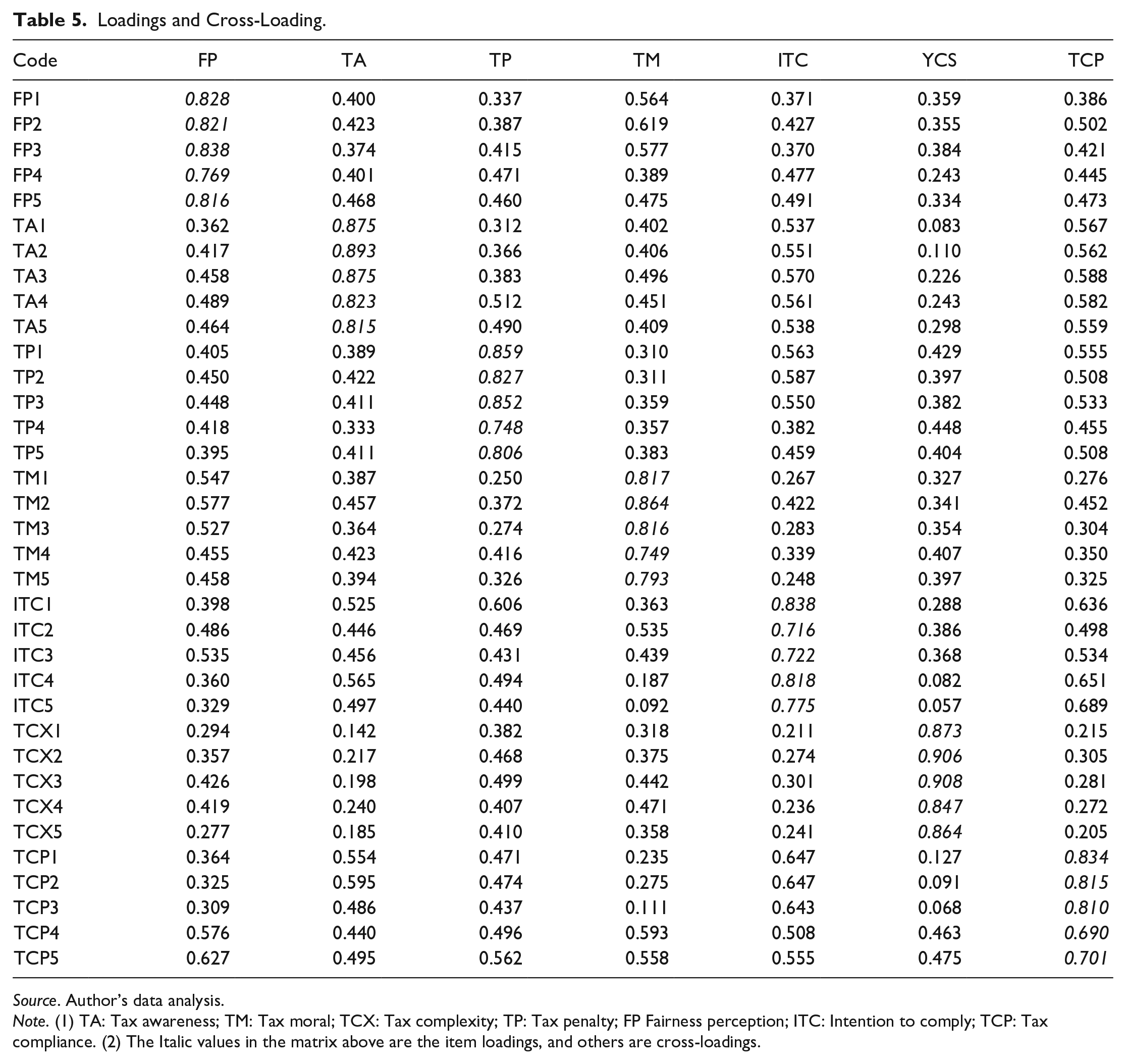

Based on Hair et al. (2019), the study’s latent constructs’ reliabilities were attained and appraised using Cronbach’s alpha (CA), DG rho, and composite reliability (CR). Cronbach’s alpha value for each construct was well above the threshold of 0.70, and the minimum Cronbach’s alpha value was 0.830 (Hair et al., 2019). The results are presented in Table 3. All the DG rho values of the study’s constructs were also well above the threshold of 0.70, where the minimum value of DG rho was 0.838 (Hair et al., 2019). Moreover, the CR values were higher than the threshold of 0.70, where the lowest CR value was 0.880 (Chin, 2010). These outcomes postulate that the latent constructs have achieved appropriate reliabilities and would perform well in the later analysis stages. The average value extracted (AVE) for all the items for each construct must be above the score of 0.50 to establish an adequate convergent validity to support the uni-dimensionality concept for each construct (Hair et al., 2019). Thus, the items showed that the constructs had adequate convergent validity (see Table 3). Additionally, all the value inflation factor (VIF) values for each construct were well below the threshold of 3.3, revealing no issue of multicollinearity (Chin, 2010). The item loading and cross-loading reported confirming the constructs’ discriminant validity are described in Tables 3 and 4, respectively.

Reliability and Validity.

Source. Author’s data analysis.

Note. TA= tax awareness; TM= tax moral; TCX= tax complexity; TP = tax penalty; FP= fairness perception; ITC= intention to comply; TCP= tax compliance; SD= Standard Deviation; CA= Cronbach’s alpha; DG= rho—Dillon-Goldstein’s rho; CR—COMPOSITE reliability; AVE = average variance extracted; VIF= variance inflation Factor.s

Discriminant Validities.

Source. Author’s data analysis.

Note. TA = tax awareness; TM = tax moral; TCX = tax complexity; TP = tax penalty; FP = fairness perception; ITC intention to comply; TCP = tax compliance.

The study’s constructs had fitting discriminant validities (see Table 4). Moreover, the Fornell and Larcker (1981) criterion was utilized to determine the discriminant validity of each construct. The Fornell-Larcker criterion was calculated with the square root of a construct’s AVE, and the AVE’s square root for the construct must be higher than the correlation among the study’s other constructs (Hair et al., 2019).

Another suggested test for discriminant validity is the Heterotrait-Monotrait (HTMT) ratio. The HTMT values must be 0.90 or less to establish discriminant validity (Hair et al., 2019). The results in Table 4 demonstrate that the study has no evidence of the lack of discriminant validity. Tables 4 and 5 show that the study has sufficient discriminant validity for each construct.

Loadings and Cross-Loading.

Source. Author’s data analysis.

Note. (1) TA: Tax awareness; TM: Tax moral; TCX: Tax complexity; TP: Tax penalty; FP Fairness perception; ITC: Intention to comply; TCP: Tax compliance. (2) The Italic values in the matrix above are the item loadings, and others are cross-loadings.

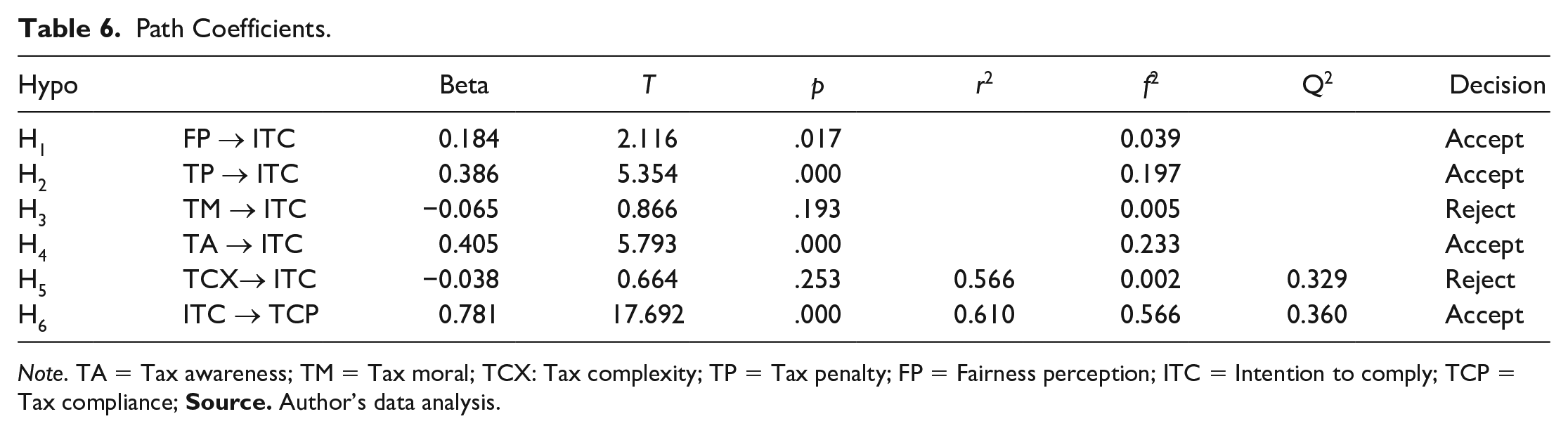

Path Analysis

After gaining satisfactory reliabilities and validities from the structural assessment of the study model, the study’s hypotheses were evaluated. The adjusted r2 value for the five exogenous constructs (i.e., tax awareness, tax morale, tax complexity, tax penalty, and fairness perception) elucidated 55.7% of the change in the intention to comply with the tax system. The predictive relevance (Q2) value for the part of the model was 0.329, demonstrating a medium predictive relevance (Hair et al., 2019). Meanwhile, the adjusted r2 value for the intention to comply as the exogenous construct on tax compliance explained 60.9% of the change in tax compliance among the study samples. The predictive relevance (Q2) value for the part of the model was 0.360, signifying a large predictive relevance (Chin, 2010).

Model standardized path values, t-values, and significance levels are listed in Table 6. The path coefficient between FP and ITC (β = .184, t = 2.116, p = .017) indicated a significant and positive effect of fairness perception on the intention to comply with the tax system. This result formed significant statistical support for H1. Next, the path between TP and ITC (β = .386, t = 5.354, p = .000), which illustrated the influence of tax penalty on the intention to comply with the tax system, was positive and significant; this delivered the support to accept H2. The path value for the TM and ITC (β = –0.065, t = 0.866, p = .193) showed that tax morale insignificantly impacted the intention to comply with the tax system, and this offered no statistical support for H3. The path coefficient for TA and ITC (β = .405, t = 5.793, p = .000) represented a positive and significant effect; it offered support for the argument that tax awareness influenced the intention to comply and thus the acceptance of H4. On the other hand, the path from TCX to ITC (β = −0.038, t = 0.664, p = .253), illustrating the influence of tax complexity on the intention to comply, was negative and insignificant. Hence, H5 was rejected. The path from ITC to TCP (β = .781, t = 17.692, p = .000), which illustrated the intention to comply and tax compliance, was positive and significant; it delivered the support to accept H6.

Path Coefficients.

Note. TA = Tax awareness; TM = Tax moral; TCX: Tax complexity; TP = Tax penalty; FP = Fairness perception; ITC = Intention to comply; TCP = Tax compliance;

ANN Findings

Model 1

In this study, the deep multi-layer perception (MLP) ANN, consisting of four layers, that is, one input, two hidden, and one output was applied (Gbongli et al., 2019). The feed-forward-back propagation (FFBP) with MLP ANN was utilized in this study. The ten-fold ANN model in the SPSS neural network algorithm (Hayat et al., 2021) was used to address over-fitting. Seventy percent of data was utilized for training, 20% for testing, and the remaining were put on hold. The prediction accuracy was assessed with the RMSE score of the model (Leong et al., 2020). The results are depicted in Table 7. High predictive accuracy was displayed as the RMSE values of the training and testing data segments were close (Figure 1).

RMSE for Training and Testing of ANN Model.

ANN made 1.

The results also indicated that the ANN model achieved better data fitting and predictive accuracy (Hayat et al., 2020).Next, sensitivity analysis was employed to evaluate the contribution of each input variable in the model to the intention of complying with the tax system (Gbongli et al., 2019). Normalized importance for every input of the constructs was gauged by the percentage fraction of the relative importance of each input neuron divided by the highest relative importance (Leong et al., 2020). Table 8 presents the evaluation results. The findings showed that tax awareness was the most significant contributing factor, followed by tax penalties and fairness perception.

Sensitivity analysis.

Source. Author’s data analysis.

Note. TA = tax awareness; TM = tax moral; TCX = tax complexity; TP = tax penalty; FP = fairness perception; ITC = intention to comply; TCP = tax compliance.

Finally, the average synaptic weights were estimated for the input layer and hidden layers (Hayat et al., 2021). The results showed that the three most contributing factors were tax awareness (100%), tax penalties (92.55%), and fairness perception (62.82%). Tax complexity and tax morals, on the other hand, are the least influential factors on the intention to comply with the tax system. The first hidden layer contributory neuron was H (1.2), while the inhibiting neuron was H (1:3). Meanwhile, the most contributing hidden outer neuron was H (2:2), and the most inhibiting hidden neuron was H (2.1) (Table 9).

Average synaptic weights of the input and hidden neurons in the ten-fold ANN.

Source. Author’s data analysis.

Note. TA: Tax awareness; TM: Tax moral; TCX: Tax complexity; TP: Tax penalty; FP Fairness perception; ITC: Intention to comply; TCP: Tax compliance.

Model 2

The prediction accuracy for model 2 (Figure 2) was assessed with the RMSE score of model 2 (Hayat et al., 2021). Results are listed in Table 10, and high predictive accuracy is shown since the RMSE values of training and testing are close (Leong et al., 2020).

ANN Model 2.

RMSE for training and testing of ANN model.

It also represented the ANN model’s data fitting and higher predictive accuracy. The ANN model 2 can predict the overall tax compliance behavior by 24.8% by the goodness of fit (Table 11).

Average Synaptic Weights of the Input and Hidden Neurons in the Ten-Fold ANN.

Source. Author’s data analysis.

Note. TA = Tax awareness; TM = Tax moral; TCX = Tax complexity; TP = Tax penalty; FP = Fairness perception; ITC = Intention to comply; TCP = Tax compliance.

Discussion

The current study examined the intention to comply and tax compliance among individual Malaysian taxpayers. This study’s result has established support for the argument that the perception of fairness promotes the intention to comply with the tax rules and regulations. The PLS-SEM and ANN model 1 confirmed that the perception of fairness promoted the intention to comply with the tax regulations. Furthermore, the study’s findings coincided with the results in Richardson (2006) that the perception of tax fairness harnessed the taxpayers’ intention to comply with the tax rules and regulations. Thus, tax fairness promotes the perception of quality and fairness in the tax system. Perception of tax system fairness develops the perception of prevailing justice of the tax system and appropriately influences the intention to comply (Guzel et al., 2019). Hence, promoting the perception of fairness is necessary to promote tax compliance.

Besides that, tax awareness significantly harnessed the intention to comply with the tax rules and regulations. The current study’s finding concurred with the outcome in Taofeeq (2018), whereby the intention to comply increased when there was an awareness that the tax collected would be utilized for the public’s welfare and that the general public conditions had improved. Additionally, tax awareness improves the taxpayers’ knowledge and the necessity to pay tax on time and feel more comfortable paying the tax in full (Rahmayanti et al., 2020).

Next, the perception of tax penalty endorsed complying with the tax rules and regulations. Thus, the perception of the tax penalty promotes a positive attitude toward paying tax on time and complying with tax regulations. The result coincided with the outcome reported by Taofeeq (2018) that the tax penalty system harnessed the attitude toward complying with the tax rules and tax compliance. The tax penalty is critical to follow the tax rules and regulations to avoid unnecessary tax payments. It shows that strict rules and regulations are necessary for a tax system to achieve the tax collection target (Gambo et al., 2014). Nevertheless, the tax penalty acts as an astringent strategy to promote the intended tax compliance.

Furthermore, the current study determined no significant association between tax morale and the intention to comply with the tax rules and regulations. The result showed that the taxpayers in Malaysia were not morally inclined to follow the tax regulations. It depicts the lack of perceived civic duty and that Malaysians are not comfortable paying taxes on time and in full. This result coincided with the findings in Youde and Lim (2019) that developing countries’ taxpayers had less tax morale to comply with the tax rules and regulations. Generally, developing countries have low civic mindfulness and a lower level of responsibility to pay tax liabilities on time (Luttmer & Singhal, 2014).

Tax complexity insignificantly influenced the intention to comply with the tax rules and regulations. This result did not match Taofeeq’s (2018) finding that tax complexity reduced the intention to pay tax. Nevertheless, Musimenta (2020) postulates that tax complexity motivates the taxpayers to engage in tax evasion as the tax system is perceived as complex, and compliance is challenging to follow. Tax complexity needs attention, and the tax system must be streamlined to reduce the perceived perception of complexity. A simple, innovative, and easy-to-use tax system promotes the perception of fairness and promotes compliance (Youde & Lim, 2019).

The analysis outcome supported that the intention to comply with the tax rules and regulations significantly promoted tax compliance. This finding coincided with the result in Youde and Lim (2019). The intention to comply with the tax rules by deterrence seems less effective than by the attributes of the prevailing tax system. However, intention significantly leads to tax compliance behavior.

Policy and Practical Implications

The current work offers several policy and practical implications. Tax collection is the most vital source of government revenue, and tax compliance is necessary to increase government resources (Remali et al., 2018). Malaysian taxpayers are not morally inclined to conform to the tax rules and regulations. Thus, the tax authorities need to inform the taxpayers why paying the enforced tax fully and on time is necessary. Communication is crucial to highlight the importance of paying tax and utilizing the collected tax appropriately. Taxpayers’ morale and awareness are essential to enhancing government revenue (Taofeeq, 2018). Tax fairness and tax morale can improve tax payment on time and the total amount.

Tax complexity reduces the intention to comply with the tax rules and regulations (Zandi et al., 2016). The tax system needs to streamline the tax payment procedures and advocate the benefits of paying tax for individuals and the nation. Furthermore, the tax authorities need to include tax accountants, individual taxpayers, and corporate taxpayers to formulate more sustainable tax policies to increase the tax collection at the national level (Luttmer & Singhal, 2014). The government also needs to improve the public trust in the tax system and transparently perform the disbursement of public funds and only utilize it for public welfare.

The current study has three limitations. First, the study concentrated on explaining tax compliance intention and behavior among individuals with limited factors. As such, the inclusion of relevant factors, acquiring data from tax accountants, and enforcing tax laws may offer sufficient exploration of tax compliance intention and behavior. Second, the data were collected in a self-report manner and in a single time frame, having limited generalization, and the study results must be carefully interpreted. Therefore, it would be good to collect the data longitudinally and explore taxpayer compliance intention and behavior. Lastly, the current study gathered data from only Malaysian samples. Future studies may include samples from neighboring countries and explore the countries’ national culture factors of trust in the government, governance effectiveness, and perception of corruption affecting the tax compliance intention and behavior.

Conclusion

The current work aimed to explore and explain the tax compliance intention and compliance with the tax system factors via the dual methods of PLS-SEM and deep ANN analysis. Tax awareness, tax penalty, and perception of fairness promoted the intention to comply with the tax rules and regulations. However, significant efforts are required to uplift the tax morale and reduce the tax complexity. A thorough system-level change requires simplifying the tax complexity and harnessing the tax morale among the people in general. The role of the government is vital to improve tax compliance by reducing the wastage of public money on unnecessary developmental spending. The public spending in infrastructure, human capital, and uplifting the civic lifestyle promotes public confidence in the government and the perception that the tax money is utilized prudently.

Footnotes

Institutional Review Board Statement

Local ethics committee (Universiti Malaysia Kelantan, Malaysia) ruled that no formal ethics approval was required in this particular case as this research did not collect any medical information, there was no known risk involved, did not intend to publish anyone’s personal information, and did not collect data from underaged people. This study has been performed in accordance with the Declaration of Helsinki.

Informed Consent Statement

Informed consent for participation was obtained from respondents who participated in the survey. For the respondents who participated the survey online (using google form), they were asked to read the ethical statement posted on the top of the form (There is no compensation for responding nor is there any known risk. In order to ensure that all information will remain confidential, please do not include your name. Participation is strictly voluntary and you may refuse to participate at any time) and proceed only if they agree. No data was collected from anyone under 18 years old.

Availability of Data and Materials

All data will be available after acceptance for publication

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.