Abstract

With increasing global concerns about business continuity, societal welfare, and environmental degradation, corporate sustainability has gained significant academic attention. Big data analytics has emerged as a pivotal dynamic resource for enhancing sustainability, yet its adoption in Malaysia remains low, and research on its impact in emerging economies is limited. This study addresses this gap by examining the influence of big data analytics capability on sustainability performance and the mediating role of green supplier integration. Specifically, sustainability performance is divided into three dimensions: economic, social, and environmental. To provide a strategic roadmap for manufacturers and suggest targeted policies to policymakers to accelerate the industry’s transformation toward sustainability, a survey was administered to manufacturers. Using data from 245 manufacturing firms and partial least squares structural equation modeling, the findings reveal that both big data analytics capability and green supplier integration positively impact sustainability performance. Green supplier integration further mediates the relationship between big data analytics capability and sustainability, underscoring its critical role. The essence of this research is to dive into a compelling and pragmatic topic, offering insights to help enterprises understand the underlying mechanisms. It stands as one of the pioneering investigations that explores this influence through the lens of resource dependence theory within the realm of emerging technologies and sustainability requirements. Additionally, the present research offers theoretical insights into how big data analytics enhances sustainability and provides practical guidance for manufacturers to leverage external resources and foster supplier alliances for sustainable development.

Plain language summary

This research focusses on manufacturers in developing countries such as Malaysia, including firms of various sizes that are often underrepresented in studies. Despite successfully adopting the ISO certificate, these manufacturers have not yet achieved the same level of financial, social, and environmental success as their global counterparts. To explore the underlying reasons, this research investigates how a company’s ability to leverage big data can address these challenges, both directly and indirectly, through green supplier integration. By surveying 245 manufacturers in Malaysia and analyzing the data with PLS-SEM, the research demonstrates that strong big data capabilities significantly boost overall sustainability, supporting the resource dependence theory. In addition, close collaboration with environmentally conscious suppliers further strengthens these positive effects. The findings provide empirical evidence that contributes to existing knowledge and offers practical insight for businesses and policymakers striving to improve sustainability in the manufacturing sector.

Keywords

Introduction

In today’s rapidly evolving business landscape and growing technological advancements, sustainability has emerged as a critical focus for organizations across various sectors (Bilal et al., 2024). While the manufacturing sector remains a cornerstone of global economic development, especially as the global economy gradually recovers from the pandemic (Sasso et al., 2025), achieving sustainability in manufacturing has transitioned from a peripheral concern to a core strategic priority. With escalating concerns about economic instability, social inequality, and environmental degradation, the need for manufacturers to adopt sustainable practices has never been more pressing (Blandino & Montagna, 2025). Manufacturers are increasingly held accountable not only for their financial performance but also for their impact on the environment and society. This green shift is driven by stringent environmental regulations, the growing consumer demand for eco-friendly products, and the urgent need to conserve finite resources (Oubrahim & Sefiani, 2025). In this context, sustainability performance has become a significant determinant of long-term organizational success, influencing both corporate reputation and competitive advantage.

The adoption of environmental management systems, such as ISO14001 certification, has become a key strategy for Malaysian manufacturers looking to improve their sustainability practices (Cheng et al., 2025). ISO14001 provides a structured framework for integrating environmental management into business processes, ensuring compliance with regulations, and fostering continuous improvement (Arana-Landín et al., 2025). However, achieving enhanced sustainability performance requires more than just adherence to standards; it necessitates the effective integration of dynamic technologies and strategic capabilities that can drive substantial improvements in economic, social, and environmental outcomes.

One such technology is big data analytics, which was proposed as a powerful dynamic capability with transformative potential that helps companies improve supply chain transparency, optimize operations, make data-driven decisions, and improve sustainability efforts (Abdul Razak et al., 2024). Being a research hotspot in the field of sustainability, scholars have found that big data analytics is the computational process of analyzing vast datasets, allowing firms to extract meaningful insights, identify patterns, predict trends, and optimize processes (Rashid et al., 2025). Its application within the realm of corporate sustainability is particularly significant as it empowers organizations to drive more efficient resource use, reduce waste, and foster innovative solutions (Ogiemwonyi et al., 2023). Consequently, the capability to leverage big data analytics is widely recognized by many researchers as a transformative resource for addressing and overcoming sustainability challenges (Baig et al., 2023). While the potential of big data analytics capability (BDAC) in improving sustainability has been widely acknowledged, there remains a lack of research exploring the underlying mechanism through established theoretical lenses, particularly from the perspective of resource dependence theory.

Resource dependence theory (RDT) posits that organizations also need external resources to fulfill their operational needs. It provides a useful framework for understanding how organizations manage their relationships with external stakeholders, such as suppliers, to access the resources required for sustainability initiatives. Given the interconnected nature of modern supply chains, the ability to foster green partnerships with suppliers is instrumental in realizing the full potential of big data analytics and advancing sustainability goals (Rashid et al., 2025). By leveraging big data analytics, firms can improve communication and information exchange with their suppliers, allowing a more effective and efficient integration of sustainability initiatives throughout the supply chain. However, the enthusiasm and attention of scholars to supplier alliances are limited (Alkaraan et al., 2025). There is a lack of studies that extend the resource dependence theory by applying it to the context of emerging technologies and sustainability, demonstrating how firms can manage external dependencies through internal capabilities and strategic alliances.

However, manufacturers face significant challenges in Malaysia, including a decrease in their digital competitiveness (IMD, 2024), as depicted in Figure 1, and limited integration of sustainable practices into their supply chains (Abbas et al., 2022). Contributing factors to the decline in digital competitiveness include low digital literacy, high adoption costs, and infrastructure deficiencies (Zhu et al., 2022), all of which impede manufacturers’ ability to leverage technologies such as big data analytics (Cetindamar & Burdon, 2025). In parallel, common challenges related to the supply chain include limited awareness and commitment to sustainability, resource constraints for SMEs, supply chain complexity, regulatory compliance issues, data and metric limitations, and a skill gap (Kamali Saraji et al., 2023). These issues underscore the critical need for enhanced big data analytics capabilities and better integration of green supplier partnerships to promote sustainability within the sector. While prior studies have explored the roles of big data analytics and green supplier integration (GSI) separately, there is a notable gap in research examining their combined impact on sustainability, particularly in the Malaysian manufacturing context (Khattab et al., 2022)

Digital competitiveness ranking and factors from 2020 to 2024.

Given the array of challenges and prospects in the current context, this study revolves around a central research query: “How do manufacturing firms improve sustainability performance through big data analytics capability and green supplier integration?” To answer this question, the present research endeavors to pursue three key objectives.

Investigate the impact of big data analytics capability on green supplier integration and sustainability performance.

Explore the role of green supplier integration in improving sustainability performance.

Introduce green supplier integration as an intermediary variable and explore its role in the relationship between big data analytics capability and sustainability performance.

To achieve these objectives, this study draws on a survey of ISO14001-certified manufacturing firms in Malaysia, employing partial least squares structural equation modeling (PLS-SEM) to analyze the data. The findings of this research offer valuable insights for both practitioners and policymakers, suggesting strategic avenues to improve sustainability performance through the effective use of big data analytics and integration of green suppliers. Ultimately, this study contributes to the growing body of knowledge on sustainability practices in the context of emerging technologies, offering practical recommendations for organizations and industry stakeholders seeking to accelerate the transformation toward a more sustainable future.

Literature Review

Overview of Prior Studies

Over the years, a growing body of literature has explored strategies, practices, and technologies that manufacturing companies can adopt to improve sustainability outcomes. Early research primarily emphasized the role of governance structures and institutional frameworks in fostering sustainability. Although these macrolevel approaches were effective in addressing immediate challenges, they often lacked the depth required to drive long-term innovation-driven sustainability (Hussien et al., 2025). Subsequently, research related to traditional environmental management systems has entered a booming stage, with an emphasis on reducing environmental impacts such as energy consumption, waste generation and emissions (Arana-Landín et al., 2025). Many studies predominantly explored the adoption of green manufacturing practices and environmental management standards, such as ISO14001, with a primary concern for environmental sustainability (Oyelakin et al., 2025). Social and economic sustainability was often considered secondary, with much of the literature centered on environmental compliance and efficiency improvements through established practices (Benzidia et al., 2025). In contrast, the present study takes a more comprehensive approach, integrating not only environmental outcomes, but also economic and social sustainability dimensions.

As sustainability challenges became more complex, scholars began to explore the potential of technological innovations in driving sustainable practices, particularly in the areas of big data analytics, artificial intelligence, and digital tools (Al Halbusi et al., 2025). The emergence of big data analytics capability as a transformative resource marked a significant shift in this direction. This shift reflects a broader understanding of sustainability, one that emphasizes not only minimizing negative impacts but also creating positive environmental, social, and economic outcomes through innovative practices (Ertz et al., 2025). Similarly, green supply chain management has gained increasing attention, focusing on extending sustainability efforts beyond the firm’s boundaries to its entire supply chain (Farrukh Shahzad et al., 2025). However, research exploring how big data analytics capability can enhance green supplier integration and improve sustainability performance across all three dimensions, economic, social, and environmental, remains relatively novel.

In Malaysia, the evolution of sustainability research has mirrored the country’s development trajectory. Early efforts concentrated on macro-level strategies, such as fostering regional capital chains through comprehensive policy support (Hasan et al., 2024). These initiatives aimed to address immediate economic and environmental challenges by directing resources to key sectors. Although technology was not initially a central theme, the groundwork was laid for its integration into sustainability practices (Deli et al., 2024). Over time, the focus shifted from environmental protection and social equity to a broader, innovation-driven sustainability agenda. This shift involved aligning industrial chains with innovation chains and promoting technological advancements to boost performance (Yin & Zhao, 2024b). Despite these advances, challenges such as limited digital literacy, high implementation costs, and infrastructure deficiencies have impeded the widespread adoption of big data analytics capability and green supplier integration within the Malaysian manufacturing sector (Falahat et al., 2022). These unique challenges and opportunities in the Malaysian context have not been sufficiently explored, limiting the applicability of the findings to other regions or industries.

Despite progress in prior research, several significant gaps remain, underscoring the need for further investigation. First, previous studies have largely examined big data analytics capability and green supplier integration independently. It is urgent to test their synergistic impact, providing a more holistic understanding of how these elements interact to drive sustainability (Abbas et al., 2023). Second, the intermediate mechanism through which green supplier integration influences sustainability remains relatively unexplored, particularly in the Malaysian context (Harikannan et al., 2025). Understanding this mediation can reveal the underlying mechanisms that shape sustainability outcomes. Third, prior research often concentrates on specific dimensions of sustainability, rather than adopting a comprehensive approach that integrates economic, social, and environmental aspects (Yadegaridehkordi et al., 2023). What is also rarely considered is the influence of green supplier integration on each dimension of sustainability performance. Fourth, while international studies provide valuable insight, research tailored to the Malaysian manufacturing context is needed to account for local regulations, market conditions, and supply chain dynamics (Benzidia et al., 2023). While many prior studies have examined the impact of ISO14001 on environmental performance, fewer have explored how emerging technologies and green supply chain integration can enhance sustainability within certified firms (Oyelakin et al., 2025). Specifically focusing on ISO14001 manufacturing firms, this study addresses a critical gap in understanding the implementation of sustainability practices within certified systems. Fifth, existing research employs various methodologies to measure sustainability constructs (Damtoft et al., 2025). For instance, financial performance (FP) is typically evaluated using financial statements, social performance (SP) is measured via corporate social responsibility reports, and environmental performance (EP) is indicated by compliance with environmental regulations and standards. However, the reliability and generalization of these measures are limited as few studies have used questionnaires to gather primary data. Lastly, the practical implications of fostering big data analytics capability, green supplier integration, and sustainability in Malaysia’s manufacturing sector have not been thoroughly explored in prior studies (Al-Khatib, 2023). Insights into actionable strategies and recommendations for companies are needed to advance sustainability initiatives and achieve long-term success.

Theoretical Foundations and Framework

The theoretical framework illustrated in Figure 2 encompasses five constructs: big data analytics capability, green supplier integration, financial performance, social performance, and sustainability performance, all of which are rooted in the resource dependence theory. Resource dependence theory delves into the ways external resource dependencies of an organization shape its behavior and decisions (Hillman et al., 2009). The selection of resource dependence theory as the guiding framework for this study is purposeful, as it aligns closely with the research objectives and the phenomena under investigation. Resource dependence theory’s central focus on resource dependencies and inter-organizational relationships makes it particularly well-suited for examining the integration of green practices within a supply chain (Issah, 2025). This choice seamlessly harmonizes with the study’s overarching goals, which revolve around gaining insights into how manufacturing companies enhance their management of external dependencies, particularly with suppliers, to achieve enhanced performance outcomes. (Bag et al., 2022). When manufacturers embark on the path of integrating sustainability practices with their suppliers, their primary objective is to secure a reliable and environmentally responsible source of inputs (Ramanathan et al., 2025). In this context, resource dependence theory provides a robust framework for comprehending how manufacturers strategically manage their external dependencies. This involves allocating crucial resources, such as supplier relationships and big data analytics capability, to exert influence on their financial, social, and environmental performance. By cultivating robust in-house big data analytics capability, manufacturers can gain greater control over this pivotal resource, reducing their reliance on external sources of information. This aligns with resource dependence theory, which posits that organizations seek to manage dependencies on external resources by developing internal capabilities (Widjaja-Adhi & Soetjipto, 2025). In this context, big data analytics serves as an internal resource that enhances decision-making autonomy and reduces uncertainty, enabling firms to make well-informed decisions related to sustainability initiatives (Hazen et al., 2016). This dual approach, leveraging internal big data analytics capabilities and external green supplier integration, creates a synergistic effect, enhancing performance. Thus, resource dependence theory provides a robust framework for understanding how firms can balance internal and external resources to achieve sustainability goals. Furthermore, it is worth noting that previous studies within this field have predominantly leveraged resource dependence theory to explore similar phenomena. Given the ongoing need to advance and expand upon this body of knowledge, employing resource dependence theory in this research not only provides continuity, but also contributes to the existing literature. It allows for the building of established foundations and a deeper understanding of how external dependencies impact the sustainability efforts and overall performance of manufacturing companies.

Theoretical framework.

Terminologies and Hypothesis Development

Big Data Analytics Capability

Big data analytics capability refers to an organization’s capacity and readiness to effectively collect, process, analyze, and derive actionable findings from extensive and intricate datasets, frequently labeled as big data (Mikalef et al., 2018). This capability encompasses not only the technological infrastructure required but also the organizational skills, processes, and strategies required, to transform raw data into meaningful and strategic decisions. The rationale for this definition lies in its alignment with the multifaceted nature of big data analytics, which goes beyond technology to include human expertise, data-driven culture, and strategic alignment. In the age of big data, where businesses generate and collect extensive data from diverse origins, such as customer interactions, operational processes, social networks, and sensors, this capability becomes critical (Aldossari et al., 2023). A robust big data analytics capability enables organizations to identify patterns, predict trends, optimize operations, and improve decision-making, ultimately driving competitive advantage and sustainability performance.

Green Supplier Integration

Green supplier integration refers to the process through which an organization collaborates with its suppliers to incorporate environmentally sustainable practices and principles into their operations and relationships (Al-Khatib, 2023). It is the cornerstone of sustainable supply chain management, focusing on minimizing environmental impact and promoting sustainability. This includes setting environmental criteria, monitoring environmental metrics, mitigating risks, encouraging eco-friendly innovation and regulatory compliance, and balancing triple-bottom-line outcomes (Benatiya Andaloussi, 2024). The rationale for defining green supplier integration in this way lies in its comprehensive approach to sustainability. It goes beyond mere compliance with environmental regulations to include proactive measures such as setting environmental criteria for supplier selection, fostering close collaboration, monitoring environmental performance metrics, and mitigating supply chain risks.

Financial Performance

Financial performance refers to the evaluation of an organization’s ability to achieve its economic goals, such as reducing costs, increasing market share, improving sales and profits, and optimizing return on investment (Green et al., 2012). It serves as a critical metric to assess the general health and efficiency of an organization’s financial activities, providing insight into profitability, expense management, and resource allocation (Gangaraju et al., 2025). This multifaceted concept encompasses key indicators such as revenue growth, cash flow, liquidity, debt management, asset utilization, and market performance (Simmou et al., 2023). Strong financial performance is vital for long-term sustainability and growth of a manufacturer, as it attracts investors and allows reinvestment in operations, research and development, and expansion efforts. Monitoring and improving financial performance are key to effective financial management and strategic decision making.

Social Performance

Social performance refers to the evaluation of an organization’s societal impact and its ability to fulfill social responsibilities (Teraji, 2009). It focuses on interactions with key stakeholders, including employees, customers, and communities, and extends beyond financial metrics to include corporate social responsibility, employee well-being, and community engagement (Chliova et al., 2025). Manufacturers that prioritize social performance are perceived as responsible and ethical, foster trust among stakeholders, attract socially conscious investors, and make positive contributions to society.

Environmental Performance

Environmental performance refers to how effectively an organization manages its environmental impact and sustainability efforts (Brent & Labuschagne, 2004). It involves assessing practices and initiatives aimed at reducing ecological footprints and promoting environmentally responsible behavior (Khan et al., 2022). Key indicators of environmental performance include emissions reduction, energy efficiency, waste management, and regulatory compliance (Anderson et al., 2025). Manufacturers that prioritize environmental performance can achieve benefits such as lower operational costs, improved reputation, compliance with regulations, and alignment with environmentally conscious stakeholders. By focusing on environmental performance, organizations not only contribute to sustainability, but also strengthen their competitive positioning in an increasingly eco-aware market.

Big Data Analytics Capability and Financial Performance

Big data analytics enhances financial performance by enabling firms to manage external dependencies and optimize operations, aligning with resource dependence theory (Rashid et al., 2025). It improves efficiency by identifying bottlenecks, reducing downtime, and cutting operational costs while optimizing inventory management to boost cash flow and lower holding costs (Papadopoulos & Balta, 2022). From a resource-dependence perspective, data analytics also strengthens supply chains by reducing lead times and improving logistics, leading to fewer disruptions, timely material delivery, lower operational costs, and better financial health. By identifying cost-saving opportunities in procurement and maintenance, data analytics enable predictive maintenance, minimizing financial losses and safeguarding profitability (Riggs et al., 2023). These enhancements contribute to better financial performance, enhancing the competitiveness and sustainability of manufacturing companies.

Big Data Analytics Capability and Social Performance

Big data analytics enhances social performance by enabling firms to strengthen stakeholder relationships and reduce reputational risks, aligning with the resource dependence theory. It uncovers employment opportunities, facilitates favorable supplier contracts, safeguards social cohesion, and frees resources for social initiatives (Sahoo et al., 2023). Manufacturers use big data to identify opportunities for community participation, philanthropy, and environmental stewardship, fulfilling their social responsibilities. From a resource-dependence perspective, data analysis also promotes ethical governance and transparency by detecting irregularities and unethical behaviors, enhancing social trust and reputations (Dubey et al., 2019). As companies adopt big data analytics, their social performance is expected to improve, as evidenced by the subsequent hypothesis formulated.

Big Data Analytics Capability and Environmental Performance

Big data analytics identifies inefficiencies, reduces waste, and minimizes environmental footprints by fine-tuning machinery and optimizing energy use (Benzidia et al., 2023). It also supports regulatory compliance through real-time monitoring of emissions, reducing risks, and preserving reputation through early issue identification and prompt corrective action (Sahoo et al., 2023). From a resource-dependence perspective, big data analytics enables manufacturers to assess suppliers and logistics, choose eco-friendly partners, and optimize routes to reduce carbon emissions, mitigating reliance on unsustainable practices. This promotes sustainability, enhancing manufacturers’ environmental performance and encouraging greener practices among partners (Al-Khatib & Ramayah, 2023). Therefore, increased involvement in big data analytics is hypothesized to lead to improved environmental performance for the firm.

Big Data Analytics Capability and Green Supplier Integration

Big data analytics allows real-time assessment of suppliers’ environmental performance, identifying eco-friendly partners, and fostering integration with those prioritizing sustainability (Gallo et al., 2023). It also enables collaboration and knowledge sharing, encouraging suppliers to adopt greener practices and align with sustainability initiatives. (Bahrami et al., 2022). From a resource-dependence perspective, big data analytics ensures transparent tracking of green initiatives, monitors supplier sustainability and addresses environmental issues promptly (Al-Khatib & Ramayah, 2023). By driving innovation in green practices through supplier collaboration, big data analytics strengthens sustainability goals and reduces reliance on unsustainable external practices. This demonstrates how internal capabilities can mitigate external dependencies and promote sustainable supply chains.

Green Supplier Integration and Financial Performance

Green supplier integration reduces operating costs through eco-friendly practices, such as energy efficiency and waste reduction, directly improving profitability (Zainuddin et al., 2018). It also bolsters a firm’s reputation as socially and environmentally responsible, attracting consumers willing to pay more for sustainable products, thus increasing sales and revenue (Zhao & Liu, 2024). From a resource-dependence perspective, integration of green suppliers fosters innovation and efficiency by collaborating with green suppliers, leading to sustainable products and processes that provide a competitive edge. This allows premium pricing and higher profit margins, further enhancing financial performance (Kaliani Sundram et al., 2018). These factors collectively contribute to improved financial results, demonstrating how strategic alliances can drive profitability and sustainability. therefore, the following hypothesis was proposed.

Green Supplier Integration and Social Performance

Green supplier integration improves social performance by enabling firms to manage external dependencies and fulfill social responsibilities, aligning with resource dependence theory. It encourages collaboration with suppliers on ethical labor practices, safety, and fair wages, improving the social impact of the company (Huma et al., 2024). In addition, green supplier initiatives support community development projects, benefiting local communities and strengthening the firm’s social reputation (Kholaif & Ming, 2022). Transparency and accountability in meeting environmental and social standards further enhance social standards, trust, and stakeholder relationships (Kholaif et al., 2024). By prioritizing diverse suppliers, supplier integration also promotes equity and diversity within the supply chain, further improving social performance. Through these mechanisms, supplier integration enhances social impact as proposed in the hypothesis.

Green Supplier Integration and Environmental Performance

Green supplier integration fosters collaboration with suppliers to implement eco-friendly practices, such as energy-efficient processes, waste reduction, and sustainable material sourcing, significantly reducing environmental impact (Lee & Wu, 2023). It also emphasizes resource conservation and responsible management, further lowering the environmental footprint (Shin & Cho, 2023). From a resource-dependence perspective, the integration of green suppliers reduces the dependence on unsustainable practices by promoting energy efficient transportation and logistics, targeting greenhouse gas emissions, and minimizing carbon footprints (Zhang et al., 2023). By leveraging green supplier integration, firms can mitigate external environmental dependencies, improve resource efficiency, and improve environmental performance, as proposed in the hypothesis. Increased involvement in green supplier integration leads to higher environmental performance, suggesting the proposed hypothesis.

Big Data Analytics Capability, Green Supplier Integration, and Financial Performance

Big data analytics capability enables manufacturers to integrate green practices with suppliers by enhancing decision-making, transparency, risk management, and customized sustainability efforts, leading to a robust supplier integration strategy (Gallo et al., 2023). Green supplier integration, in turn, reduces costs, enhances reputation, and drives innovation, positively impacting financial performance (Zainuddin et al., 2018). Through the utilization of big data analytics, manufacturing firms can harness green supplier integration to enhance supply chain resilience, curtail expenses, elevate product quality, and guarantee adherence to regulations, thus fostering a greater level of financial performance. This means that big data analytics capability improves financial performance by enhancing green supplier integration. Meanwhile, the integration of green supplier carries the influence of big data analytics on financial performance, acting as an intermediate step in the causal pathway. Big data analytics capability serves as an internal capability that reduces dependency on external information sources, while green supplier integration represents a strategic alliance with green suppliers to access sustainability-related resources. A positive link was found between big data analytics capability and financial performance (Al-Khatib & Ramayah, 2023), between big data analytics capability and green supplier integration (Gallo et al., 2023), and between green supplier integration and financial performance (Zainuddin et al., 2018). When these positive causal relationships are present, the possibility of a mediating effect arises (Hayes & Preacher, 2014). This study suggests that green supplier integration mediates the link between big data analytics capability and financial performance, leading to the following hypothesis.

Big Data Analytics Capability, Green Supplier Integration, and Social Performance

Increasingly, there is evidence suggesting that green supplier integration serves as a mediator in the relationship between big data analytics capability and social performance. The ability to use big data analytics empowers manufacturers to make informed decisions about green supplier integration, allowing data-driven assessment, risk management, performance monitoring, and sustainability collaboration (Bahrami et al., 2022). Green supplier integration, in turn, enhances social performance by fostering ethical labor practices, community engagement, transparency, employee well-being, and supplier diversity (Huma et al., 2024). Green supplier integration clarifies the underlying mechanism or process linking big data analytics and social performance. In other words, it bridges the relationship between the predictor and the outcome, providing insight into how or why the relationship exists. By combining big data analytics with green supplier integration, manufacturing companies in Malaysia can enhance employee well-being, engage responsibly with their communities, and maintain ethical governance, contributing to positive social performance (Y. Xu et al., 2023). These improvements collectively contribute to positive social performance, bolstering the company’s reputation and relationships with stakeholders, and aligning the organization with societal values and expectations. These findings indicate the likelihood of a mediating effect within this relationship framework (Hayes & Preacher, 2014). Consequently, the following hypothesis is formulated.

Big Data Analytics Capability, Green Supplier Integration, and Environmental Performance

There is increasing evidence that big data analytics capability can improve environmental performance by leveraging green supplier integration as an intermediate mechanism. Big data analytics empowers manufacturers to make informed decisions, foster collaboration, ensure compliance, optimize resource utilization, and continuously improve sustainability efforts with green suppliers (de Assis Santos & Marques, 2022). The data-driven approach promotes the integration of green suppliers, which positively impacts environmental performance by fostering eco-friendly practices and resource-efficient processes throughout the supply chain. This contributes to reduced environmental impact, resource conservation, and emission reduction (Lee & Wu, 2023). Consequently, incorporating big data analytics capability and green supplier integration in Malaysian manufacturing firms enhances environmental performance by improving resource efficiency, proactive environmental management, and sustainable supply chain practices (Shin & Cho, 2023). This positions these companies as responsible and environmentally conscious entities in the industry, aligning with global sustainability goals. In other words, big data analytics capability provides the tools and insights needed to identify and collaborate with green suppliers, and these collaborations, in turn, drive improvements in environmental performance. Given the positive and causal links observed among the variables, it suggests that green supplier integration acts as a mediator between big data analytics capability and environmental performance (Hayes & Preacher, 2014). As a result, the following hypothesis is formulated.

Research and Data Methodology

This study employs a quantitative design to test 10 research hypotheses grounded in established theoretical frameworks. The research process is structured into three steps while implementing robust ethical safeguards. Initially, a comprehensive literature review is conducted to develop the conceptual framework, ensuring alignment with resource dependence theory and prior studies. This is followed by the collection of primary data through surveys, ensuring a robust data set for analysis. Ethical considerations remain paramount throughout this social science research, particularly as it involves questionnaire-based data collection, storage, and analysis. Risks of harm are minimized by using noninvasive survey questions and ensuring confidentiality and anonymity. No personally or organizationally identifiable data appear in any research outputs, including text, figures, and tables. The societal value of this research, including its contributions to advancing knowledge on sustainable practices and enhancing organizational performance, outweighs any minimal risks to participants. These benefits also extend to participants through potential applications of findings in their professional contexts. Moreover, informed consent was obtained from all participants, who received clear information about the purpose, procedures, and the rights of the study, including the option to withdraw at any time. Participation is contingent upon agreement to these terms, and submission of a completed questionnaire serves as confirmation of informed consent. The study design further ensures data integrity by accepting only fully completed surveys and permitting each participant to submit only one response. These measures collectively ensure the welfare of the participants and ethical research conduct while maintaining scientific rigor. Finally, the research hypotheses are tested using advanced statistical techniques, specifically PLS-SEM. It allows for the simultaneous examination of measurement models and structural models, ensuring a rigorous examination of the research objectives and enhancing the credibility of the findings.

Sampling

The research employed a quantitative approach rooted in the positivist paradigm, utilizing an inductive methodology to achieve its research objectives. Data collection involved surveying ISO14001 manufacturing firms in Malaysia as listed in the Federation of Malaysia Manufacturers Directory. This focus on Malaysian firms ensures that the sample captures the specific environmental and regulatory context of the country, which is essential to understand local sustainability practices. The directory is a reputable source, offering a comprehensive list of registered firms that enhance the sample’s reliability. In addition, the directory encompasses a variety of manufacturing sectors, providing a broad representation of different practices and challenges related to sustainability. By including firms of various sizes, the study also gains insights into how different scales of operation impact sustainability performance. A probability sampling technique was used to ensure diverse participation, with managers chosen as respondents due to their presumed deeper knowledge of their companies’ sustainable practices. Data were collected using an online questionnaire, employing a cross-sectional survey design to assess research hypotheses. Ethical approval was not required as it was an independent study. The research methodology adhered to ethical guidelines, ensuring the welfare, rights, and privacy of the participants. Confidentiality and anonymity were strictly maintained throughout the survey process, with no unethical activities occurring.

Measurement Instruments

The survey questionnaire was designed by incorporating items from prior studies in the field to ensure its reliability and adaptability across different contexts. Two academic experts specializing in sustainability performance provided valuable input to validate the items and refine the questionnaire, aligning it with the cultural nuances of Malaysia. A six-item scale was employed to gage the extent of big data analytics capability (Al-Khatib, 2023). A five-item scale was utilized to assess the level of green supplier integration (Al-Khatib, 2023). Three five-item scales were used to measure financial performance, social performance, and environmental performance accordingly (Khan & Quaddus, 2015).

Data Analysis and Results

Descriptive Analysis

After addressing various disturbance and excluding six invalid questionnaires, a total of 245 valid surveys remained for analysis. This equates to an effective response rate of 50.2% based on the initial surveys distributed. The analysis of descriptive statistics indicates that the manufacturers involved in this study come from various industrial sectors, including food and beverages (27%); chemicals (24%); plastics (13%); rubber products (11%); basic metals (6%); mineral products (5%); fabricated metals (4%); rubber (2%); and various other sectors (8%).

Assessment of Measurement Model

Before advancing to structural equation modeling, it is crucial to validate the measurement model (Shahzad et al., 2024). This validation process involves verifying two forms of validity: convergent validity and discriminant validity. To establish convergent validity, it is necessary to verify three criteria: (i) construct items have loadings of at least 0.70, (ii) the composite reliability (CR) is equal to or greater than 0.80, and (iii) the average variance extracted (AVE) should be equal to or greater than 0.50. All items had loadings of ≥0.70 except for BDA6, SP3 and ENP2. Therefore, these particular items were excluded from the analysis. The highest CR value, observed for financial performance, stands at 0.943, while the lowest CR value, which pertains to social performance, is 0.847. Correspondingly, the highest AVE value is 0.769, linked to financial performance, whereas the lowest AVE value, associated with social performance, is 0.581. For a more comprehensive overview of the results regarding measurement model convergent validity, please refer to Figure 3 and Table 1.

Measurement model comprises path coefficient and R2 values.

Construct Validity and Reliability.

Upon confirming the convergent validity in the measurement model, the next phase involves examining the discriminant validity (Xu et al., 2025), which is evaluated through two criteria: cross-loadings and the Heterotrait-Monotrait (HTMT) ratio. To assess the cross-loading criteria, it is important that the loading of each construct is greater than the loadings on other constructs. For instance, the loading values are 0.872 for business data analytics capability, 0.584 for environmental performance, and 0.390 for financial performance. Detailed values can be found in Table 2.

Cross Loadings.

To evaluate Heterotrait-Monotrait values, it is crucial to ensure that the correlation values between constructs do not surpass .90. As indicated in Table 3, all construct correlation values remain within an acceptable range, signifying the absence of any discriminant validity concerns. The next step involves performing an analysis of the structural model.

HTMT.

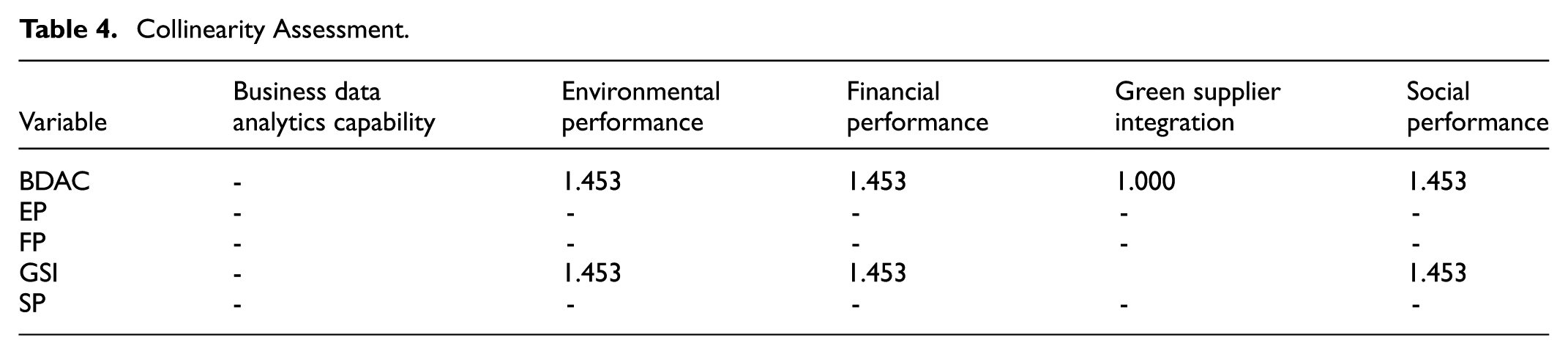

Before conducting the structural model analysis, it is essential to evaluate collinearity diagnostics (Ashraf et al., 2024). Multicollinearity was evaluated using the variance inflation factor (VIF) in Smart PLS. The variance inflation factor threshold to detect multicollinearity typically exists when the value of the individual endogenous construct exceeds 5. However, some scholars consider a more conservative level with a threshold of ≤2.5. In the present model, the value of the variance inflation factor for financial performance stood at 1.453. The results of the collinearity diagnostics, presented in Table 4, affirm the absence of any collinearity problems within the model.

Collinearity Assessment.

Assessment of Structural Model

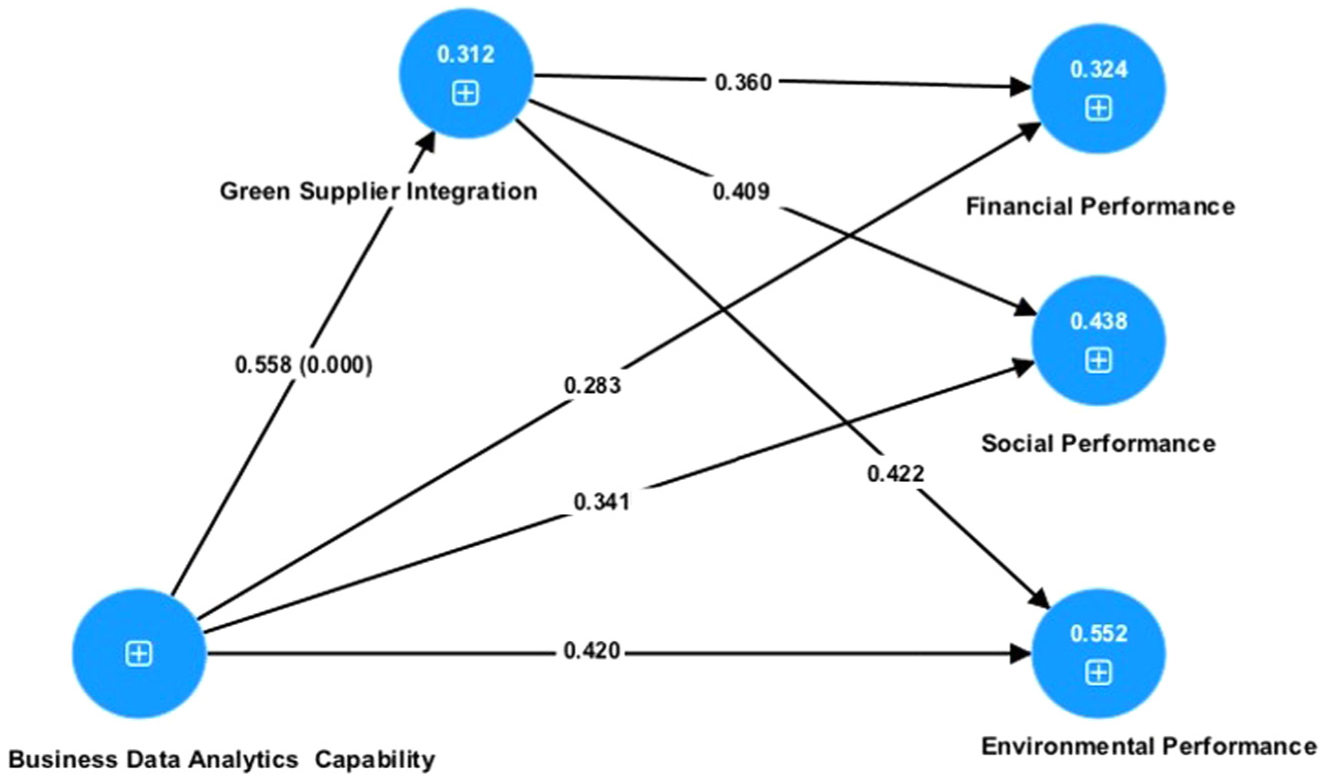

After establishing the validity of the measurement model, the next stage focused on analyzing the structural model. This phase aimed to investigate the suggested connections among exogenous, mediating, and endogenous variables, which included the evaluation of both direct and indirect effects. For instance, with regard to H1, it was found that big data analytics capability had a statistically significant positive impact on financial performance (b = 0.283, t = 3.655, p < .001). Similarly, in relation. to H2, the analysis showed that big data analytics capability had a significant positive effect on social performance (b = 0.341, t = 6.865, p < .001). The remaining hypotheses, including H3, H4, H5, H6, and H7, which confirm the direct effects, are also supported, as demonstrated in Figure 4 and Table 5.

Path coefficient and p values.

Direct Effects.

The next step of the analysis focused on assessing the indirect effects within the structural model. This was done to investigate the proposed indirect relationships among exogenous, mediating, and endogenous variables. As an example, H8 suggests that green supplier integration mediates the relationship between business data analytics capability and financial performance. The results show a mediation effect with a coefficient (b) of 0.201, a t-value of 4.370, and a p-value of less than 0.001. Similarly, for H9, which proposes that green supplier integration mediates the relationship between business data analytics capability and social performance, the results indicate a mediation effect with a coefficient (b) of 0.228, a t-value of 6.795, and a p-value of less than 0.001. The remaining hypotheses also find support, including H10, as indicated in Figure 5 and Table 6.

Path coefficient and T values.

Indirect Effects.

Assessment of Structural Model

The first hypothesis, suggesting a positive link between big data analytics capability and financial performance, is supported by the results (b = 0.283, t = 3.655, p < .001). The second hypothesis proposed a positive link between big data analytics capability and social performance and is confirmed by the results (b = 0.341, t = 6.865, p < .001). The third hypothesis proposed a positive link between big data analytics capability and environmental performance and is validated by the results (b = 0.420, t = 7.471, p < .001). The fourth hypothesis, suggesting a positive link between big data analytics capability and green supplier integration, is supported by the results (b = 0.558, t = 13.034, p < .001). The fifth hypothesis proposed a positive link between green supplier integration and financial performance and is validated by the results (b = 0.360, t = 5.194, p < .001). The sixth hypothesis proposed a positive link between green supplier integration and social performance and is confirmed by the results (b = 0.409, t = 8.657, p < .001). The seventh hypothesis suggested a positive link between green supplier integration and environmental performance and is supported by the results (b = 0.422, t = 8.304, p < .001). The eighth hypothesis, proposing that green supplier integration mediates the relationship between big data analytics capability and financial performance, is validated by the results (b = 0.201, t = 4.370, p < .001). The ninth hypothesis proposed that green supplier integration mediates the relationship between big data analytics capability and social performance. The results (b = 0.228, t = 6.795, p < .001) validate this hypothesis. The 10th hypothesis proposed that green supplier integration mediates the relationship between big data analytics capability and environmental performance. The results (b = 0.236, t = 6.333, p < .001) validate this hypothesis.

Conclusions, Implications, and Future Directions

Discussion

Responding to the need to fill research gaps, the main research question of this research is to explore how manufacturing firms enhance sustainability performance through big data analytics capability and green supplier integration. Malaysia’s evolving manufacturing industry serves as a solid basis for investigating this dynamic. Specifically, three research objectives were developed and a theoretical framework underpinned by the resource dependence theory was empirically tested using PLS-SEM.

The results addressing the first research objective, supported by hypotheses H1 to H4, confirm a positive correlation between big data analytics capability and green supplier integration, as well as between big data analytics capability and sustainability performance. Specifically, the findings of H1 to H3 validate the positive impact of big data analytics capability on financial, social, and environmental performance while H4 confirms the positive influence of the big data analytics capability on green supplier integration. These results are consistent with prior studies (Al-Khatib & Ramayah, 2023; Gallo et al., 2023), which highlight the importance of robust internal capabilities for corporate development. To leverage these findings, it is essential to promote the adoption of big data analytics among manufacturers through targeted strategies. In Malaysia, for instance, municipal efforts have prioritized the adoption of advanced technologies in the manufacturing sector, supported by significant advancements in infrastructure, employment opportunities, and regulatory frameworks. Other recommendations include: (1) fostering a culture of data-driven decision-making within organizations, (2) establishing key performance indicators to monitor and evaluate the impact of big data analytics, (3) allocating resources for research and development to explore innovative applications of big data analytics in sustainability, (4) encourage collaborations between governments, private companies, and research institutions to drive innovation in big data analytics, (5) develop training programs to upskill employees in data analytics (Kazancoglu et al., 2025; Tariq et al., 2025).

The results of H5 to H7 address the second research objective by confirming the significant role of green supplier integration in shaping sustainability performance, aligning with previous studies (Huma et al., 2024; Zainuddin et al., 2018). In Malaysia, the recovery of supportive supply chains after the pandemic has likely fostered trust, collaboration, and shared responsibility between suppliers, further enabling green integration. To improve the integration of green suppliers, manufacturers can (1) define and communicate sustainability standards for supplier selection and evaluation, (2) collaborate with suppliers on projects such as waste reduction, energy efficiency, and circular economy practices, (3) encourage suppliers to innovate and share best practices for sustainability through workshops, forums, or online platforms, (4) use digital platforms to track and share environmental performance metrics, ensuring accountability, and (5) conduct regular audits of supplier practices and provide constructive feedback to drive continuous improvement (Fahlevi et al., 2025; Onukwulu et al., 2025; Rashid et al., 2025).

The results of H8 to H10 confirm the mediating role of green supplier integration in the relationship between big data analytics capability and sustainability performance. These findings highlight the importance of green supplier integration, particularly in Malaysia, where manufacturers have demonstrated increased awareness of sustainability due to these active promotion of green practices by the government and the visible impact of supplier alliances. These results align with previous research, suggesting that advances in data analytics strengthen strategic collaborations with suppliers, ultimately improving financial, social, and environmental performance. To further strengthen the intermediate relationship, efforts can be directed toward (1) developing platforms for seamless data sharing between manufacturers and suppliers to improve transparency and coordination in sustainability initiatives, (2) using technologies such as IoT, AI, and blockchain to enhance supply chain visibility, traceability, and real-time monitoring of sustainability metrics, (3) organize workshops, seminars, and forums to share best practices and success stories, inspiring broader adoption of green and data-driven initiative, (4) working with industry associations and governments to advocate for policies and standards that support green supplier integration and data-driven sustainability, and (5) build trust-based long-term relationships with suppliers to ensure commitment to shared sustainability objectives (Al Mamun et al., 2025; Ertz et al., 2025; Farrukh Shahzad et al., 2025).

Furthermore, the study highlights challenge unique to Malaysia’s context that hinder its digital and sustainability progress. Despite industrial advances, Malaysia’s digital competitiveness has declined over the past 5 years (IMD, 2024), contrasting with global trends. This decline points to structural barriers, such as an overreliance on big data workshops and a lack of accessible, practical training programs, which limit the impact of government-led initiatives. Furthermore, the widespread retirement of the aging infrastructure poses a significant challenge, exacerbated by the limited investment of manufacturers in equipment upgrades and staff training for big data analytics (Chong et al., 2024; Vachkova et al., 2023). These issues not only slow technological adoption but also undermine Malaysia’s ability to compete globally. Addressing these challenges requires urgent, targeted interventions, such as increased investment in digital infrastructure, expanded training programs, and incentives for manufacturers to modernize their operations. Without such measures, Malaysia risks falling further behind in the global digital and sustainability landscape.

Conclusions

Under the global imperative for green business practices, sustainability performance has emerged as a critical driver of corporate development. Integrating sustainability principles into business management enables firms to optimize external resources and strategic alliances, fostering long-term success. In Malaysia, the evolving manufacturing landscape, shaped by sustainability challenges, demands an updated framework that goes beyond the traditional theory of resource dependence. This research addresses this need by exploring how big data analytics capability and green supplier integration enhance sustainability performance, offering a comprehensive understanding of resource dynamics in the context of emerging technologies and sustainability imperatives.

Focusing on manufacturers in Malaysia, this research addresses a critical gap in the literature, offering tailored insights for emerging economies. It is guided by the central research question: “How do manufacturing firms improve sustainability performance through big data analytics capability and green supplier integration?” Through empirical analysis of the BDAC-GSI-SP framework, this research not only expands traditional resource categories to include information and technology resources but also underscores the interconnected nature of resources and dependencies. This enhanced resource dependence theory for sustainable manufacturing underscores the interconnected nature of resources and dependencies, demonstrating how big data analytics capability influences green supplier integration and, in turn, drives sustainability.

By surveying 245 ISO14001 manufacturers and analyzing the primary data using PLS-SEM, this study provides quantitative findings that demonstrate how firms can leverage big data analytics capability to address sustainability challenges, both directly and indirectly through green supplier integration. Compared to industry benchmarks, the results highlight the critical role of digital resources, particularly big data, as essential dependencies for modern firms. Firms with a strong big data analytics capability achieve significantly higher overall sustainability performance, reinforcing the validity of resource dependence theory. Close collaboration with environmentally conscious suppliers further amplifies these positive effects, emphasizing the relevance of resource dependence theory in analyzing inter-organizational relationships and sustainability practices in Malaysia.

Furthermore, this research highlights the managerial significance of investing in data analytics capability and fostering eco-friendly supplier partnerships within the Malaysian manufacturing industry. Such investments lead to tangible improvements in financial performance, social reputation, and environmental impact. In addition, this study provides a strategic roadmap for companies and suggests targeted policies to policymakers to accelerate the industry’s transformation toward sustainability. By enhancing understanding of resource dynamics and its implications for sustainability, this research equips companies, policy makers, and scholars with the tools to make informed decisions and advance sustainable practices in the manufacturing sector. The collective effort of these stakeholders will be instrumental in fostering a more sustainable and prosperous future for Malaysia’s manufacturing landscape and beyond.

Theoretical Implications

This study extends the theory of resource dependence into the sustainability domain within manufacturing, demonstrating its adaptability to modern contexts. By integrating technological resources such as big data analytics capability and sustainability-related resources such as green supplier integration, it broadens the theory’s application and understanding of resource dependency. Second, this study bridges the gap between sustainability and the technology literature by examining how big data analytics capability influences green supplier integration and its subsequent effects on financial, social and environmental performance. This provides a comprehensive understanding of its interplay and highlights the mediating role of green supplier integration. Third, this study focuses on the Malaysian manufacturing industry, offering insight into how companies in emerging markets leverage technological capabilities to address sustainability challenges. It emphasizes that possessing resources such as the ability to perform big data analytics alone is insufficient; effective integration with external partners is critical for performance improvements. Lastly, it contributes to the triple-bottom-line literature by examining financial, social, and environmental performance separately, showing their interplay and potential synergies. The findings show that improvements in one dimension can positively influence others, reinforcing the importance of a holistic approach to sustainability.

Managerial Implications

This study highlights the strategic value of leveraging the ability to exploit big data analytics and fostering green supplier integration for Malaysian manufacturing managers. Managers should focus on utilizing big data analytics to optimize operations, reduce costs, and enhance decision-making. It is also important to collaborate with green suppliers to improve resource efficiency and sustainability outcomes. Adopting a comprehensive performance measurement framework that integrates financial, social, and environmental metrics is also important. Additionally, the study provides policymakers with information to develop targeted sustainability policies, allocate resources effectively, and create regulatory frameworks that promote innovation and competitiveness in the Malaysian manufacturing industry and beyond. Furthermore, the findings have a wider applicability across different sectors. For example, in the technology sector, big data analytics can drive innovation and efficiency, while green supplier integration can enhance supply chain sustainability. In the retail sector, these practices can improve inventory management and reduce environmental footprints. Similarly, in the energy sector, leveraging big data and green partnerships can optimize resource use and support the transition to renewable energy.

Practical Implications

This study offers actionable insights for manufacturing firms, particularly in Malaysia, to enhance sustainability performance through big data analytics capability and green supplier integration. Practitioners can develop in-house big data analytics capability to collect, process, and analyze data for optimizing operations, reducing costs, and improving decision-making. It is also important to use predictive analytics to identify sustainability risks and opportunities, such as energy efficiency improvements or waste reduction strategies. Moreover, manufacturers can collaborate with suppliers who prioritize green practices, establish joint sustainability goals, and share data to monitor progress and ensure alignment with environmental standards. Other recommendations include measuring performance using financial, social, and environmental metrics to ensure a balanced approach to sustainability, and regularly reporting sustainability achievements to stakeholders to build trust and enhance reputation. Finally, businesses can use big data analytics capability to identify cost-saving opportunities, such as optimizing supply chain logistics or reducing energy consumption, while investing in innovation and workforce training to create high-skilled jobs and improve competitiveness. By adopting these practices, firms can position themselves as leaders in sustainable manufacturing, attract investment, and foster long-term economic resilience. Policymakers can also use these findings to design incentives that encourage sustainable practices, further driving economic growth while addressing environmental and social challenges.

Limitations and Future Directions

This study has several limitations that should be acknowledged. First, the use of cross-sectional data limits the ability to capture dynamic changes over time. While this approach provides a snapshot of the relationships between variables, it does not allow for the examination of how these relationships evolve. Longitudinal data would be necessary to establish causality more definitively. Second, the reliance on survey-based data introduces the potential for measurement error and respondent bias, which may affect the accuracy of the findings. Third, the study focuses exclusively on the Malaysian manufacturing industry, which may limit the generalizability of the results to other countries or industries due to contextual differences. Finally, while the study examines mediation effects, the cross-sectional design prevents definitive conclusions about causality.

Future research endeavors should explore various avenues for investigation, with a particular emphasis on the critical role of digital technology in driving sustainability outcomes (Yin & Zhao, 2024a). Longitudinal studies would be invaluable for tracing how these relationships change over time, offering deeper insights into causality and the long-term impact of digital interventions (Liu, Yuan, & Lee, 2024). Cross-country or cross-regional comparisons may reveal contextual variations in the adoption and effectiveness of digital technologies, supporting the development of more broadly applicable theories (Khan et al., 2022). Additionally, experimental studies could evaluate the impact of specific interventions designed to enhance big data analytics capability and other digital capabilities, such as artificial intelligence, Internet of Things, and blockchain, in driving sustainability performance (Cheng et al., 2023; Liu, Liu, & Lee, 2024) and other digital technology related capabilities is a promising avenue for future research. Combining quantitative data with qualitative approaches, such as interviews and case studies, can yield a richer understanding of the dynamics and contextual factors influencing the adoption and implementation of digital technologies in sustainability practices (Farooq et al., 2022). Exploring moderating factors, such as industry-specific traits, firm size, or technological readiness, could add nuance to our understanding of how digital capabilities interact with organizational and environmental contexts to shape sustainability outcomes (Yin et al., 2024). Furthermore, assessing the effectiveness of policy interventions aimed at promoting the adoption of digital technologies for sustainability would offer valuable guidance for policymakers (Liu, Zheng, & Lee, 2024). Lastly, expanding research to encompass small and micro-sized enterprises, beyond those listed in the FMM directory, and examining broader supply chain dynamics, will offer a more holistic perspective on sustainability practices within the industry.

Footnotes

Author Note

The authors claimed that none of the material in the paper has been published or is under consideration for publication elsewhere.

Ethical Considerations

The authors claimed that this article does not contain any experiments with human bodies performed by any of the authors. This study was conducted in accordance with Sage’s ethical guidelines for social science research, with no occurrences of plagiarism and copyright infringement, duplicate publication, data fabrication and falsification, authorship disputes, and citation manipulation.

Consent to Participate

The survey commenced with an explanation of the study’s purpose and protocol. Participants had to read and agree to the terms before proceeding, with the option to withdraw at any point. Submission of a completed questionnaire was considered informed consent. No personally or organizationally identifiable data appear in any research outputs, including text, figures, and tables.

Author Contributions

Conceptualization, Investigation, and Writing, J.C.; Data collection, J.C.; Resources and Funding, N.S., Y.N.Z., K.B.L., and D.D.W.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We are profoundly thankful for the trust and investment placed in our research endeavors by the Ministry of Education Anhui, China. Its support not only helped in the execution of this study but also significantly contributed to the advancement of knowledge in corporate sustainability performance. This work was supported by: (1) Quality Engineering Project–Business English (Grant no. PX-255245811); (2) Talent Initiation Project of Huangshan University (Grant no. 2024xskq032); (3) Science Research Project (Philosophy and Social Sciences) of Higher Education in Anhui Province (Grant no. 2024AH052538); (4) Anhui Xinhua University First-Class Undergraduate Program Construction Project in Logistics Management (Grant no. 2020ylzyx06); (5) Humanities and Social Science Project of Anhui Provincial Education Department (Grant No. 2024AH052535).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.