Abstract

Over the past decade, mobile money services have rapidly expanded in developing economies, yet research on their adoption by petty traders remains limited. This study investigates the factors influencing the intention to use MTN Mobile Money (MTN MoMo) among Makola traders in Ghana. Using a two-stage PLS-SEM artificial neural network (ANN) predictive analytic approach, the study first applied PLS-SEM to test hypotheses, followed by ANN to detect nonlinear effects. A total of 945 questionnaires were collected, revealing that performance expectancy, effort expectancy, social influence, price value, and trust significantly influence traders’ intentions to use MTN MoMo. Additionally, both intention to use and facilitating conditions significantly predict the actual usage of MTN MoMo. Model B indicates differences in the ranking of price value, trust, and intention to use between the PLS-SEM and ANN models, suggesting hidden attributes may influence these relationships. These findings benefit policymakers and service providers committed to advancing digital financial inclusion and economic development. Theoretically, the study extends UTAUT2 in the context of MoMo, a neglected research area. Methodologically, it is the first to apply the UTAUT2 model using the hybrid PLS-SEM-ANN approach in Ghana.

Introduction

Monetary transactions are the essence of international business, fostering economic connectivity across nations and driving socio-economic progress. This global movement is essential in emerging markets, where it is interrelated with local financial ecosystems, impacting economic opportunities. However, in many developing economies, low financial inclusion hinders opportunities for individuals, particularly those within the informal sector (Narteh et al., 2017; Osei-Assibey, 2015). Limited access to traditional financial institutions poses a significant constraint to socio-economic well-being, prompting the development of innovative solutions such as mobile money (MoMo; Rahman et al., 2020).

MoMo platforms, designed for inclusivity, empower unbanked and underbanked populations to conduct financial transactions, store value, and access credit, bridging the financial gap, especially in regions lacking traditional banking infrastructure (Mattern, 2018; Shapshak, 2018). These platforms have facilitated improved financial behaviors and outcomes, such as increased savings rates and improved access to credit among low-income earners. Despite widespread adoption in countries like Ghana, specific segments of the population, particularly those engaged in petty trade, continue to experience limited benefits from MoMo services (Akolgo, 2023; Duho et al., 2022; GSMA, 2016).

The Ghanaian government has actively promoted a cashless society, evident in initiatives such as the Bank of Ghana’s 2008 “Guidelines for Branchless Banking,” which fostered collaboration between telecommunications giants and banks, laying the foundation for the current MoMo ecosystem (Duho et al., 2022). This policy revolution reflects regulatory and economic shifts influencing digital finance. However, a significant challenge persists within the Ghanaian economy, as nearly 89% of employed Ghanaians work in the informal sector, requiring efficient financial tools to manage their cash-flow-dependent businesses (Baah-Boateng & Vanek, 2020). Hence, to explore this critical area further, the study focuses on the practical usage of MoMo among Makola traders in Ghana, entrenched within the informal economy.

Despite high rates of phone ownership and MoMo registration, there is a notable discrepancy in actual usage, with concerns regarding safety, system complexity, and compatibility with existing merchant systems contributing to this gap (Akomea-Frimpong et al., 2019). Moreover, recent policy measures such as introducing the E-levy on MoMo transfers have raised affordability concerns, casting doubt on the overall value proposition of MoMo services (Anyidoho et al., 2023; Nyabor, 2022).

Service providers in Ghana, particularly telecom giants like MTN, are proactively implementing initiatives to stimulate MoMo adoption and usage among critical demographics such as Makola traders (GSMA, 2022). These efforts are crucial in addressing the identified challenges, aiming to align the technological solutions with the real needs of the users. However, underlying challenges threaten to undermine the effectiveness of these efforts. While existing studies have enhanced the understanding of the main predictors of MoMo adoption in Ghana, there remains a notable gap in the literature regarding the specific adoption patterns of MTN MoMo, the predominant network provider in Ghana’s mobile money market (Kwateng et al., 2019; Kwofie & Adjei, 2019).

To address these gaps, this research examines the adoption patterns of MTN MoMo among Makola traders in Ghana. By analyzing the factors influencing MoMo adoption rates, mainly focusing on MTN and the effectiveness of current initiatives in bridging the observed usage gap, this research seeks to reconcile divergent perspectives and contribute to the ongoing discourse on digital financial inclusion and economic development in the region. The study employs the Unified Theory of Acceptance and Use of Technology 2 (UTAUT2) model as a framework to pursue these objectives. Building upon the work of Alalwan et al. (2017), this study explores the relationship between trust and performance expectancy, proposing that trust in the mobile money service influences the traders’ belief in its overall effectiveness. This theoretical extension offers novel insights into the dynamics of technology adoption within the unique socio-economic contexts of developing economies. The study utilizes a novel hybrid method, combining Partial Least Squares Structural Equation Modeling (PLS-SEM) with Artificial Neural Networks (ANN), to comprehensively analyze MoMo adoption behavior among Makola traders. The anticipated outcomes of this study will provide valuable insights for policymakers and service providers committed to advancing digital financial inclusion and economic development in Ghana and similar contexts.

The remainder of this article is structured as follows: Section 2 reviews the literature; Section 3 outlines the theoretical framework; Section 4 presents the hypotheses; Section 5 describes the methodology; Section 6 reports the results; and Section 7 provides the discussion, implications, limitations, and conclusions.

Literature Review

MTN Mobile Money (MoMo)

The market leader MTN introduced MTN Mobile Money in July 2009, gaining an early advantage in the industry. By the end of 2013, all major telephone network operators had adopted electronic money transactions, with MTN reporting a substantial customer base, particularly in the Greater Accra Region (Flika, 2022). MTN MoMo offered a convenient and accessible alternative to traditional banking systems, promoting financial inclusion, especially among the unbanked population (Mattern, 2018). This widespread network facilitates access to MoMo services, even in remote areas. This aligns with the goals of the Bank of Ghana’s 2008 regulations, which established a framework for a bank-led, many-to-many MoMo model (Duho et al., 2022). As part of the GSMA’s Connected Women Commitment Initiative, MTN MoMo has committed to increasing the proportion of women in their MoMo Pay customer base to 40% by 2023. Additionally, MTN MoMo actively promotes financial literacy and targets specific demographics, such as women in informal markets (GSMA, 2022). These efforts contribute to MTN MoMo’s role in driving financial inclusion and transforming financial transactions in Ghana.

Studies on Mobile Money (MoMo)

Ghana’s growing mobile money (MoMo) landscape has attracted significant scholarly attention, with several studies exploring the determinants of MoMo adoption and usage patterns. Studies by Narteh et al. (2017) and Osei-Assibey (2015) employed frameworks like Innovation Diffusion Theory (IDT) and the Technology Adoption Model (TAM) to understand user intentions and motivations. Osei-Assibey (2015) focused on factors influencing MoMo adoption among market traders and susu collectors, highlighting perceived risk, education level, and relative advantage as significant determinants. Narteh et al. (2017) used Structural Equation Modeling (SEM) to reveal that perceived ease of use, usefulness, trust, and cost significantly influence adoption, with social influence playing an additional role. Subsequent studies extended the Unified Theory of Acceptance and Use of Technology (UTAUT2) to the mobile money context. Kwofie and Adjei (2019) incorporated trust into the model and examined gender as a moderating variable, finding differences in how performance expectancy and facilitating conditions influenced adoption across gender lines. Similarly, Penney et al. (2021) also adopted UTAUT2, integrating moderators such as age, education, and experience, and identified habit, price value, and trust as key drivers of adoption. Kwateng et al. (2019) confirmed the UTAUT2 model’s applicability to m-banking in Ghana, emphasizing the role of individual differences in adoption behavior. Recent literature has expanded the analytical scope, incorporating regional trends, policy implications, and macro-level impacts. Grzybowski et al. (2023), using a two-stage model with survey and geospatial data from nine Sub-Saharan African countries, showed that mobile phone network coverage and handset ownership influence usage patterns, particularly among younger and wealthier users for remittances, and among older, low-income users for receiving transfers. Complementing this, Asongu and le Roux (2023) employed quantile regression on panel data to reveal that mobile money innovations significantly promote self-employment among women, especially at higher entrepreneurial levels. At the intersection of financial innovation and inclusion, Avom et al. (2023) used both parametric and nonparametric methods on panel data from 50 African countries and found that mobile money adoption enhances financial inclusion, a result reinforced by Ahmad et al. (2023), who extended the Solow growth model to incorporate ICT and mobile money’s contribution to growth. These studies emphasize Africa’s distinct digital financial trajectory in comparison to the rest of the world. However, broader challenges and contextual disparities are increasingly acknowledged. Osabutey and Jackson (2024) conducted a thematic review highlighting ongoing barriers such as data privacy issues, weak infrastructure, and unequal benefits, particularly among the poorest communities. Seck-Sarr (2024), drawing on innovation and strategy frameworks, affirmed mobile money’s African roots but cautioned against exclusion risks linked to AI-based enhancements and geopolitical shifts. Social, environmental, and sectoral impacts of mobile money have also gained prominence. Ky (2025), using logit models, found that rural farmers, especially women and the less educated, utilize mobile money for remittances, borrowing, and savings. Eshun and Kočenda (2025) linked financial inclusion to green sustainability outcomes across African countries, uncovering a nonlinear (inverted-U) relationship. Franke et al. (2025), using a mixed-methods approach, documented how mobile money, enabled cash transfers boosted healthcare utilization in humanitarian settings in Madagascar. Azamuke et al. (2025) developed a synthetic mobile money transaction dataset to support fraud detection and machine learning research. These emerging African-based studies provide context-specific evidence that validates and extends the UTAUT2 framework in mobile money research. Despite these advancements, a notable gap persists regarding provider-specific adoption patterns. There is limited empirical research focused on MTN MoMo, the dominant service provider in Ghana’s mobile money landscape. Addressing this gap, the present study examines MTN MoMo adoption among Makola traders in Accra, employing a hybrid methodological approach that combines Partial Least Squares Structural Equation Modeling (PLS-SEM) with Artificial Neural Networks (ANN) to offer a nuanced understanding of the determinants of MoMo adoption in an informal economy.

Theoretical Foundation and Conceptual Framework

Theoretical Foundation

The Unified Theory of Acceptance and Use of Technology (UTAUT2) is a framework widely used to understand user adoption of new technologies (Venkatesh et al., 2003). It combines existing theories into a single model, focusing on how users form the intention to adopt and then actually use the technology (Venkatesh et al., 2003). UTAUT2 identifies four key factors influencing this intention, which include users’ belief in the technology’s effectiveness (performance expectancy), perceived ease of use (effort expectancy), social pressure to adopt (social influence), and the availability of necessary resources (facilitating conditions; Venkatesh et al., 2003). These factors directly influence a user’s intention to adopt a technology, which then translates into actual usage. Additionally, factors like age, gender, and experience can moderate these relationships.

Later, the UTAUT2 model was developed, adding three new constructs: Hedonic Motivation (HM), Price Value (PV), and Habit (HT). These additions significantly enhanced the model’s explanatory power, leading to a more nuanced understanding of behavioral intention and technology adoption (Venkatesh et al., 2012). This extended model suggests that these additional factors, along with the original four, influence both user intention and actual usage.

Despite its widespread application in various contexts, such as mobile banking (Kwateng et al., 2019), online shopping (Tandon et al., 2016), and mobile marketing (Eneizan et al., 2019), UTAUT2 has seen limited use in studying mobile technology like MoMo Africa. However, recent African-based studies provide robust justification for revisiting and extending this framework. For example, trust in digital services has emerged as a critical factor influencing adoption across various contexts in Sub-Saharan Africa (Osabutey & Jackson, 2024; Penney et al., 2021). Facilitating conditions, such as access to mobile agents and infrastructure, have also been identified as key enablers (Grzybowski et al., 2023). Furthermore, Asongu and le Roux (2023) emphasize that self-efficacy and effort expectancy significantly shape mobile money adoption among women entrepreneurs, while Ky (2025) and Franke et al. (2025) illustrate the role of perceived usability and real-world service outcomes. These emerging African-based studies provide context-specific evidence that validates and extends the UTAUT2 framework in mobile money research. To capture these contextual dynamics, this study employs UTAUT2 as a reference model and extends it by including trust as a direct driver of behavioral intention. Additionally, the research examines the relationship between trust and performance expectancy. The decision to include trust stems from its recognized importance in influencing user confidence and behavioral intention, particularly in mobile financial environments characterized by risk and uncertainty (Alalwan et al., 2015). Given these regional insights and theoretical gaps, the extension enhances the model’s (Figure 1) contextual fit for petty traders in Ghana.

Conceptual diagram of the extended structural model (ESR) based on UTAUT2 with Trust.

Methodologically, this study adopts a novel hybrid approach combining Partial Least Squares Structural Equation Modeling (PLS-SEM) with Artificial Neural Networks (ANN) to analyze both linear and nonlinear relationships. The choice is supported by calls in recent digital finance research to adopt models capable of uncovering complex, nonlinear patterns in user behavior (Singh et al., 2023; Wang et al., 2022). This dual-stage approach strengthens the model’s predictive accuracy and offers deeper insights into the determinants of MoMo adoption in informal market environments.

Conceptual Framework

The conceptual framework for this study is anchored in the UTAUT2 model and extended to include trust as a key construct, based on its prominence in recent African mobile money studies. The framework posits that performance expectancy, effort expectancy, social influence, facilitating conditions, price value, and trust influence traders’ intention to use MTN MoMo, which in turn predicts actual usage behavior. Trust is also modeled as an antecedent of performance expectancy, capturing the idea that users who trust a platform are more likely to perceive it as useful. This structure reflects insights from recent Sub-Saharan African research, which has highlighted the importance of contextual factors such as digital literacy, infrastructure, and social capital in shaping mobile money adoption. By incorporating trust and using a dual-stage PLS-SEM and ANN approach, the framework enables both explanatory power and predictive accuracy in understanding adoption behavior among Ghanaian market traders. The Extended Structural Model (ESR) model is presented in Figure 1. It captures both the cognitive and contextual drivers of mobile money adoption, particularly relevant in informal market settings like Makola. Given the complexity of user behavior and the possibility of nonlinear relationships among constructs, this study adopts a two-stage hybrid modeling approach. PLS-SEM is first used to estimate the linear relationships and test hypotheses. To complement this, an Artificial Neural Network (ANN) analysis follows, allowing for the detection of complex, nonlinear interactions and the ranking of predictor importance. This dual-stage approach ensures both explanatory insight and predictive robustness, in line with best practices in digital finance modeling.

Hypotheses Development

Effort Expectancy (EE)

EE refers to the perceived ease of using new technology (Venkatesh et al., 2003). This is similar to the concept of perceived ease of use in the Technology Acceptance Model (TAM) and the complexity factor in Innovation Diffusion Theory (IDT; Venkatesh et al., 2003). For the uptake of MTN MoMo, traders’ perceptions of the effort required or the difficulty encountered in using the service are crucial. In the vibrant and busy market atmosphere of Makola, cash payments are often perceived as quicker and simpler than mobile money. In this aspect, EE includes a simple registration process and ease of making payments during transactions. Additionally, the availability of MTN MoMo agents and compatible mobile devices contributes to EE. Thus, the accessibility of MTN MoMo with minimal effort, whether physical or mental, will increase traders’ intention to use (IU). More so, several studies suggest a positive relationship between effort expectancy (EE) and performance expectancy (PE; Al-Okaily et al., 2020; Davis, 1993; Djimesah et al., 2022; Makanyeza, 2017; Narteh et al., 2017; Osei-Assibey, 2015; Penney et al., 2021). When users perceive technology as easy to use, they are more likely to anticipate achieving the expected performance benefits (Martins et al., 2014; Mutlu & Der, 2017). Based on this, we propose the following:

Performance Expectancy (PE)

PE refers to the degree to which users believe a specific technology will improve their ability to perform certain tasks (Venkatesh et al., 2012). It captures their perception of the benefits they will gain from using the technology. This concept is similar to “perceived usefulness” in other models like the Technology Acceptance Model (TAM) and “relative advantage” in Innovation Diffusion Theory (IDT; Venkatesh et al., 2003). In this context, PE reflects traders’ belief in how MTN MoMo will enhance their financial transactions. This includes perceived benefits like convenience, faster and safer transactions, and overall effectiveness of the service. Research by Al-Okaily et al. (2020), Dzisi et al. (2023), Koenig-Lewis et al. (2015), and Penney et al. (2021) support this notion, showing a positive correlation between perceived usefulness (which aligns with PE) and the intention to use mobile payments. Traders are more likely to use MTN MoMo if they believe it will improve their financial activities. Therefore, we hypothesize:

Social Influence (SI)

SI refers to the importance users place on the opinions of their close social circle regarding the adoption of a specific technology (Venkatesh et al., 2003). This concept aligns with the subjective norm in the Theory of Reasoned Action (Venkatesh et al., 2003). SI captures the influence of environmental factors, such as the viewpoints of a user’s relatives, friends, and supervisors, on user behavior (Baptista & Oliveira, 2015; Eneizan et al., 2019; Makanyeza, 2017). In this context, it represents the trader’s perception of whether significant others, such as family and friends, believe they should use MTN MoMo. Consequently, friends and families of traders who use and promote MTN MoMo are critical to driving uptake (Alalwan et al., 2016; Narteh et al., 2017). Studies by Dzisi et al. (2023) and Penney et al. (2021) further highlight the influence of important social circles like family, friends, and colleagues on individual technology adoption decisions. Often, people are more likely to adopt MoMo if their social network members are already using it. Therefore, we hypothesize:

Price Value (PV)

PV reflects the mental trade-off users make between the perceived benefits of technology and the associated monetary costs (Dodds et al., 1991; Venkatesh et al., 2012). The manner in which prices and costs are structured significantly impacts consumers’ technology adoption behaviors. Users are more likely to adopt the technology when the perceived value outweighs the cost. Therefore, the perceived benefits and usefulness should exceed the financial costs involved (Alalwan et al., 2017; Kwateng et al., 2019). In the uptake of MTN MoMo, traders are more likely to use the service if the fees and costs associated with using MTN MoMo services are considered reasonable (Al-Okaily et al., 2020; Eneizan et al., 2019; Kwofie & Adjei, 2019). Therefore, traders have a stronger propensity to utilize the service when the perceived value exceeds the monetary cost. Thus, we hypothesize:

Trust (TR)

Trust embodies an individual’s sense of security, confidence, and willingness to consistently rely on a system, service, or product to meet their expectations without failure (Kim et al., 2011; Koksal, 2016). Cultivating trust among individuals is crucial as it alleviates consumer fears and uncertainties, enhancing adoption intentions (Ooi & Tan, 2016; Sharma & Sharma, 2019). Therefore, traders’ confidence in MTN MoMo’s ability to safeguard them from fraud and hacking significantly influences their adoption and usage of the service. Studies have shown that trust is a critical predictor of user intention to utilize any technology (Kwateng et al., 2019; Kwofie & Adjei, 2019). Building on the work of Gefen et al. (2003), trust is posited to exert a direct impact on traders’ intention to adopt mobile payment, or it could indirectly influence behavioral intention (BI) by enhancing the role of performance expectancy. This suggests that trust in MoMo acts as a facilitator, strengthening the user’s belief in the performance benefits of the service. Consequently, this study puts forth the following hypotheses:

Facilitating Condition (FC)

FC represents consumers’ confidence in the availability of resources and support systems necessary to utilize new technologies (Martins et al., 2014; Venkatesh et al., 2003). Similar to the “perceived behavioral control” concept in the Theory of Planned Behavior (Zhou et al., 2010), FC indicates the accessibility of resources that encourage adopting a specific behavior. These resources give users a sense of control, influencing their willingness to adopt (Nel et al., 2012). In this case, traders are required to possess certain fundamental skills, such as operating mobile phones and sending/receiving text messages (Alalwan et al., 2017; Kiconco et al., 2019). Additionally, traders rely on FCs like functional mobile service connections and the availability of MTN MoMo transfer agents to render services to users. The lack of these essential operational skills and financial resources impedes their usage of MTN MoMo (UoM). Therefore, we propose the following hypothesis:

Intention to Use (IU)

IU has consistently emerged as a significant factor in the literature on Information Technology, with numerous studies emphasizing its pivotal role in shaping the actual usage of new technologies (Ajzen, 1991; Venkatesh et al., 2012). Therefore, this study assumes that the actual usage of MTN MoMo (UoM) can largely be predicted by traders’ willingness to adopt such systems. This assertion is supported by extensive evidence from various studies, including the works of Cheung and To (2017), Sharifzadeh et al. (2017), and Wang et al. (2022), among others. Consequently, this study posits the following hypothesis:

Methodology

Population and Sample

Our study targeted the diverse population of traders within Makola Market, Accra’s largest open-air market. A stratified two-stage cluster sampling approach was employed to achieve a representative sample. We collaborated with market authorities to obtain a current list of registered traders stratified by merchandise category (fresh produce, manufactured goods, imported goods). Market maps guided the random selection of trader-concentrated clusters within each category, utilizing Probability Proportional to Size (PPS) sampling. A power analysis determined the optimal sample size for the entire study and for each stratum. Systematic random sampling was implemented within each chosen cluster to ensure all traders had an equal chance of selection. This approach ensured a representative sample reflecting the market’s composition. Finally, a random sample of 945 traders was selected.

Ethical Considerations

This study involved human participants and was carefully designed to avoid any potential harm. The survey focused on general questions related to mobile money usage, as outlined in the questionnaire, and did not collect sensitive or personally identifying information. The potential benefits of the study, such as improving mobile money services and promoting financial inclusion, were considered to outweigh any minimal risks. Since the study was conducted in a market environment, verbal informed consent was obtained with the assistance of local market authorities and participating traders, and participation was entirely voluntary. Participants were informed of their right to decline or withdraw from the study at any time.

Measures

The unit of analysis for this study was the individual trader. Their opinions were captured through a questionnaire to assess the direct determinants, intention to use (IU), and actual usage of MTN MoMo (UoM) for trade, aligning with the proposed conceptual framework. Since every trader possesses a personal mobile money account, they were considered the whole entity under study, encompassing relevant factors influencing behavior change. As a group, the traders formed the unit of observation. Following Venkatesh et al. (2012), measurement items were adapted from related studies utilizing the UTAUT model. To measure user behavior aspects of MTN MoMo adoption for trade, constructs were carefully adapted from the UTAUT model, related mobile money adoption studies, and gaps identified in the literature review (Malinga & Maiga, 2020; Osei-Assibey, 2015). The established validity and acceptability of Venkatesh et al. (2012) instrument for the adoption model construct justified its adoption in this research. Additionally, the questionnaire incorporated demographic factors (gender, age, and education), merchandise types traded, business duration, and sales volume. A 5-point Likert scale was used, ranging from 1 (strongly disagree) to 5 (strongly agree).

Data Collection Method

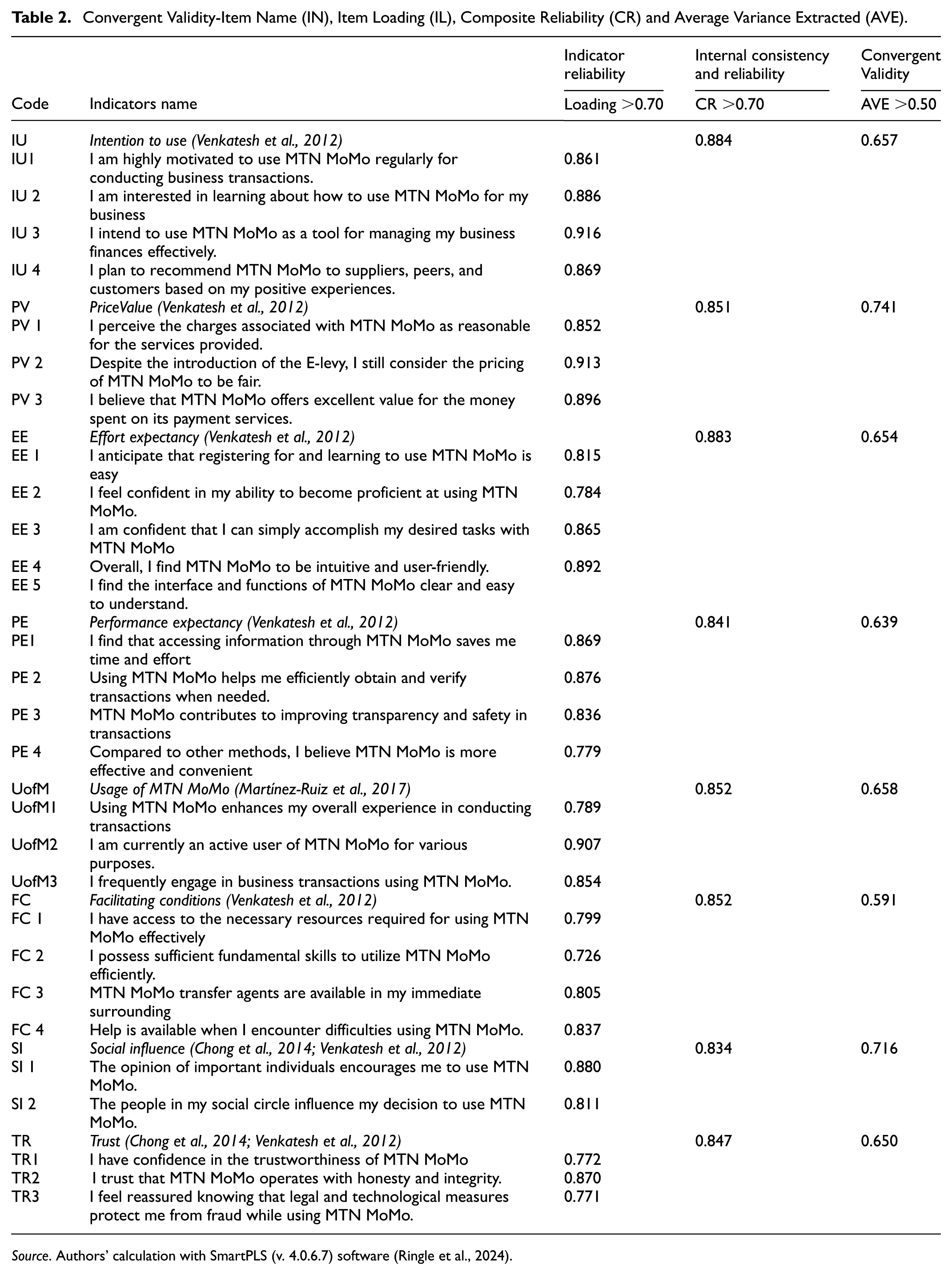

This study employed a mixed-methods approach, incorporating both qualitative and quantitative data collection methods. A structured questionnaire and a key informant checklist were utilized to capture the factors influencing MTN MoMo adoption among Makola Market traders. Recognizing the predominance of Twi among Ghanaian traders, the questionnaire was meticulously translated into this local language. Research assistants underwent comprehensive training before data collection to ensure consistent and accurate data collection procedures. A pilot study was conducted to assess the instrument’s validity and reliability. Based on the pilot test findings, the trained research assistants refined the questionnaires before administering them to the Makola traders. The questionnaire distribution in August 2023 yielded 1,014 questionnaires, with a high valid response rate of 93.2% (n = 945). The sample demographics revealed a majority of female respondents (83.8%) and a dominance of traders with below-tertiary education (760; Table 1). The questionnaire’s reliability was confirmed through Cronbach’s alpha values, all exceeding the acceptable threshold of .7 for all constructs (Table 2). This indicates a high level of internal consistency within the questionnaire, strengthening the reliability of the collected data.

Demographic Characteristics of the Respondents.

Source. Authors’ computation with SPSS (26) software. Exchange rate: Bank of Ghana (2024).

Convergent Validity-Item Name (IN), Item Loading (IL), Composite Reliability (CR) and Average Variance Extracted (AVE).

Source. Authors’ calculation with SmartPLS (v. 4.0.6.7) software (Ringle et al., 2024).

Analysis and Findings

A two-stage PLS-SEM-ANN simulation technique is utilized in this study to evaluate the collected data. In the first stage, the PLS-SEM analysis uses SmartPLS 4 to forecast the suggested model with multidimensional constructs (Purohit et al., 2023). PLS-SEM is effective for identifying linear relationships among constructs, but its variance-based approach has limitations, particularly in capturing nonlinear interactions between variables (Albahri et al., 2022). To address this gap, the study integrates ANN in the second stage of the analysis to explore and model the potential nonlinear relationships that PLS-SEM cannot capture effectively.

While PLS-SEM provides a solid foundation for understanding the linear structural relationships between constructs, ANN complements this by offering a more flexible approach that can identify non-linear patterns in the data. ANN’s ability to model relationships between input and output variables without requiring explicit specification of these relationships adds robustness to the analysis (Leong et al., 2020). As reported by Wang et al. (2022), the ANN is a model composed of neurons distributed across the input, hidden and output layers inside a complex network, and researchers can utilize the ANN without needing to comprehend the hidden correlations among variables being examined.

However, despite its advantages, ANN is often criticized for its “black box” nature, where the internal workings of the model are not easily interpretable, making it challenging to directly test specific hypotheses. This limitation, alongside PLS-SEM’s inability to handle nonlinearities effectively, justifies the use of the combined PLS-SEM-ANN approach in this study. By integrating these two methods, we can leverage the strengths of both: PLS-SEM for its clarity in hypothesis testing and ANN for its capacity to uncover nonlinear relationships. Hence, this hybrid methodology addresses the respective limitations of each individual technique.

Assessment of the Measurement Model

The validity and reliability of the reflective measurement model for latent variables (LVs) are assessed as part of the evaluation process (Cepeda-Carrion et al., 2019). This means looking at the links between the LVs and the items to which they are linked. Two significant coefficients that are frequently used to assess internal consistency reliability and convergence validity are composite reliability (CR) and extracted average variance (AVE).

This study’s measurement model was based on eight constructs: PE, EE, IU, SI, PV, TR, FC, and UofM. To determine how reliable the model is, there is a need to determine and compare the loading of each indicator on its LVs to a threshold. In general, the loading is considered satisfactory if the reliability of the indication is more than 0.70 (Lin et al., 2020). Table 2 reveals that each of the indicator loadings on their respective LVs was greater than 0.70. For internal consistency, the CR coefficient must be higher than 0.70 (Cepeda-Carrion et al., 2019; Lin et al., 2020). Table 2 shows that for all LVs in the PLS path model, the CR for each data set was greater than 0.70. These results show that the measuring model is reliable for the model assessment.

By looking at both convergent and discriminant validity, the researcher can ensure the validity of the constructs (Bayonne et al., 2020). The AVE of LVs must be greater than 0.5, according to Hair, Matthews et al. (2017), for convergent validity to be demonstrated. Table 2 shows that the AVE of each construct was more than 0.5.

The degree to which one LV differs from other model constructs determines the extent of discriminant validity (Hair, Hult et al., 2017). The heterotrait-monotrait (HTMT) ratio has been chosen as a better way to determine if a test is valid (Henseler et al., 2015). Researchers have indicated 0.85 and 0.90 as limits for determining whether the HTMT criteria are robust (Henseler et al., 2015). This study uses the more conservative 0.90 criterion to measure discriminant validity (HTMT.90). All of the HTMT results in Table 3 are below the 0.90 criterion, which shows that the test is discriminant.

Discriminant Validity—Heterotrait-Monotrait (HTMT) Criterion.

Source. Authors’ calculation with SmartPLS (v. 4.0.6.7) software.

Assessment of the Structural Model

First, the analysis addressed potential multicollinearity among predictor constructs by examining their Tolerance (VIF) values in Table 4. All VIF values fell comfortably between 0.2 and 5, indicating no significant concerns about collinearity that might distort the model’s results.

Result of Hypothesis Testing.

Source. Authors’ calculation with SmartPLS (v. 4.0.6.7) software.

Note. Cohen (1988), 0.02 small effect size, 0.15 medium effect size, 0.3 large effect.

Second, path coefficients were then employed to assess the hypothesized relationships. All hypotheses (H1-H9) received support. A statistically significant and positive association was found between Effort Expectancy (EE) and both Intention to Use (IU; β = .251, p = .000) and Performance Expectancy (PE; β = .781, p = .000). Similarly, PE demonstrated a positive and significant relationship with IU (β = .672, p = .000). The influence of Social Influence (SI; β = .041, p = .007), Performance Expectancy (PE; β = .028, p = .027), and Trust (β = .038, p = .004) on IU were also statistically significant and positive. Additionally, Trust exhibited a positive and significant relationship with PE (β = .142, p = .000). Facilitating Conditions (FC) demonstrated a positive and significant impact on the Usage of Mobile Money (UofM; β = .038, p = .004). The hypothesized link between IU and UofM (β = .603, p = .000) was also confirmed using a bootstrapping procedure with a minimum of 9,999 samples and a significance level of at least 5% (p < .05). Detailed findings are presented in Table 4 and Figure 2.

Final Structural model.

In the third stage, the determination coefficient (R 2) is assessed, which indicates the amount of variability in an endogenous latent variable that several exogenous latent variables can clarify. R 2 value evaluation is highly reliant on the particular research topic (Cepeda-Carrion et al., 2019; Lin et al., 2020). Hair, Matthews et al. (2017) proposed an interpretation of R-squared values: R-squared above .67 indicates a robust model, .67 to .33 indicates an average model, .33 to .19 indicates a weak model, and below .19 is considered unsatisfactory. Figure 2 and Table 5 show that the proposed model demonstrates adequate explanatory power. The R 2 values for Intention to Use (IU; R 2 = .905), Performance Expectancy (PE; R 2 = .714), and Usage of Mobile Money (UofM; R 2 = .645) all fall within the acceptable range, indicating that the model effectively explains a substantial portion of the variance in these variables.

R 2 and Q 2.

Source. Authors’ calculation with SmartPLS (v. 4.0.6.7) software.

Table 4 presents the results of hypothesis testing. Cohen (1988) defined small impact size as falling between 0.02 and 0.15, medium impact range as 0.15 to 0.30, and large impacts are greater than 0.30. PC has no effect size on IU, PE has a medium effect size on IU (H3), EE has a high effect size on PE, and IU has a large effect size on UofM, as indicated by the f 2 coefficients. The final and most important statistic is predictive validity (Q 2). The cross-redundancy values in the model of the present study are greater than zero, indicating that it has predictive value (Hair, Matthews et al., 2017). In Table 5, Q 2 scores for IU, PE, and UofM were 0.586, 0.452, and 0.418, indicating a significant tendency for foresight. These results indicate that the test model can be used to make predictions.

ANN Analysis

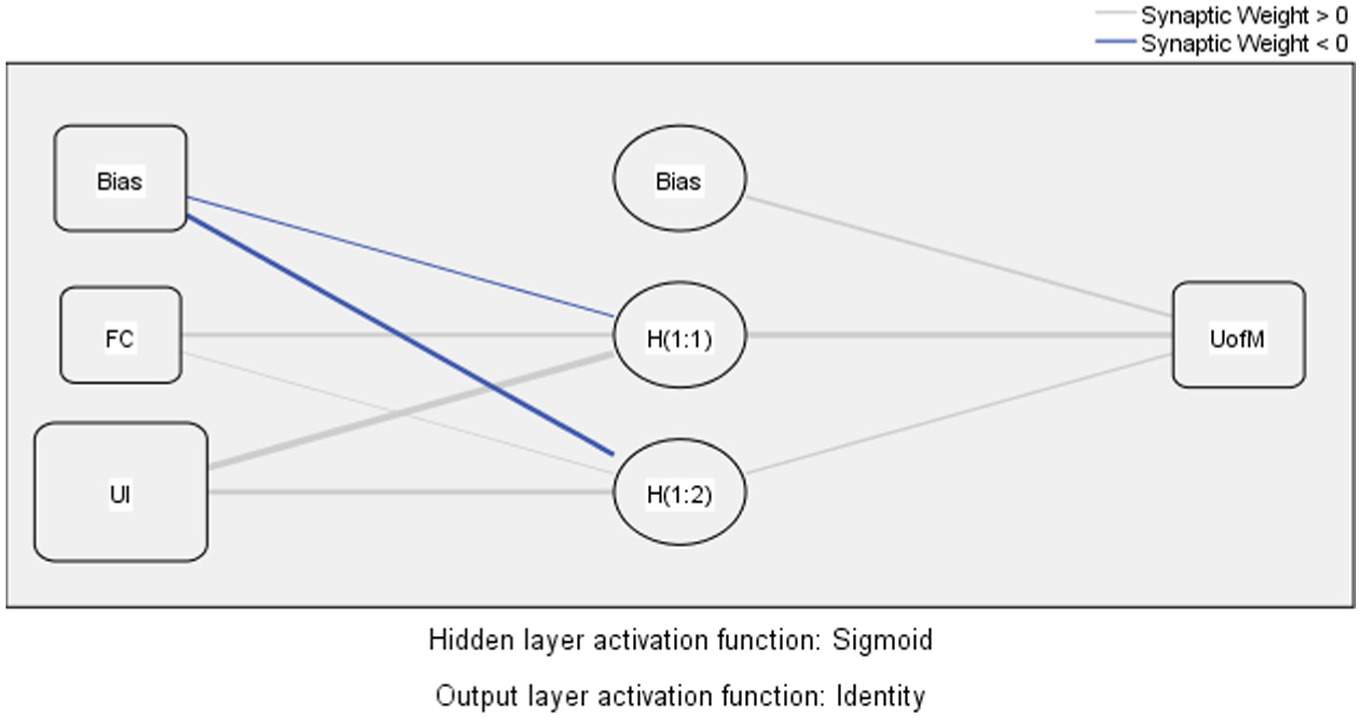

For the ANN model, a similar procedure used by Singh et al. (2023) was applied in this study. The significant determinants observed from the SEM-PLS path analysis were used as input neurons, as presented in Figures 3 to 5. Artificial neural networks have the ability to capture nonlinear structures well in high dimensions of the data. However, linear methods are needed to identify the most crucial variable and simplify the data before applying ANNs, as some of the structures detected by ANNs may not appear linear. Predictions and classifications are more accurate using ANNs because they capture patterns that a linear method could not detect. The linear approach explored the data at earlier stages to ensure that all the variables were relevant before applying the ANNs. ANN was used in cases where data is not normally distributed, and nonlinear structures are evident between the exogenous and endogenous determinants (Wang et al., 2022). They are also robust against outliers, the noise of the data, and small sample populations (Yin et al., 2023). Additionally, the model can be used in the non-compensatory domain of compensatory models, where an increase in one determinant is not needed to compensate for the decrease in another determinant (Yin et al., 2023).

Model A.

Model B.

Model C.

This study used IBM’s SPSS neural network module to implement the ANN analysis. The ANN algorithm was used through the feed-forward-backward-propagation (FFBP) algorithm, whereby data were fed forward to get prediction outcomes and then fed backward to check the errors (Purohit et al., 2023). The input layers were connected to a hidden layer, and a multilayer perceptron was utilized to develop the neural network model since it efficiently fits the sigmoid activation function. After several learning processes, errors were minimized, and the accuracy of predictions was increased. 90% of the samples were allocated for the training process, and the rest were used in testing, according to Leong et al. (2020) and Singh et al. (2023). This study used the root mean square error for the accuracy of the ANN model through a tenfold cross-validation method to prevent overfitting (Alkawsi et al., 2021). The RMSE process of training data, the processing of testing data, and the standard deviation were conducted to determine the precise predictions of the model, as shown in Figures 3 to 5. As seen in Table 6, the RMSE values of the training process and testing process range between 0.0303 and 0.2168, indicating relatively low error margins and the strength of the model (Singh et al., 2023; Wong et al., 2020).

RMSE Values.

Note. RMSE = root mean squared error; SSE = sum square of errors; SD = standard deviation; N = sample.

Additionally, a sensitivity analysis was conducted to check the prediction capability of input neurons, and their normalized importance was calculated by dividing the relative importance by the maximum importance and presenting it in a percentage value. Hence, the sensitivity analysis was conducted following Singh et al. (2023) and Wang et al. (2022). According to Table 7, ANN Model A, results show that PE has the highest probability of accuracy, while the normalized importance is 100%, followed by EE at 12%, PV and SI both having 11%, and Trust at 10%. Regarding ANN Model B, EE (100%) holds significant importance to PE (25%), while Trust is the second most influential predictor of PE. Lastly, in the ANN model C, the most important predictor of UofM is IU (100%), followed by FC (69%). This study also compares the rankings for PLS-SEM and ANN, focusing on the path coefficients and normalized relative importance. The results indicate consistency between PLS-SEM and ANN for Models B and C; except for Model A in the ANN analysis (see Table 8).

Sensitivity Analysis Results.

Note. EE = effort expectation; PE = performance expectations; T = trust; SI = social influence; FC = facilitating conditions; PV = price value; IU = intention to use; UoM = usage of mobile money.

Comparison of PLS-SEM and ANN Findings.

Discussion and Conclusions

Discussion of Results

This study investigated the factors influencing the adoption of MTN MoMo among traders in Makola Market using a dual-stage PLS-SEM and ANN approach. The results offer robust empirical support for most of the hypothesized relationships based on the extended UTAUT2 model, with meaningful implications for both theory and practice. Effort Expectancy (EE) significantly influenced both Intention to Use (IU) and Performance Expectancy (PE) (H1 and H2). Traders who perceived MTN MoMo as easy to use were more likely to adopt it and believe it would benefit their business operations. This confirms previous findings by Davis et al. (1989) who noted that perceived ease of use enhances perceived usefulness and aligns with mobile money studies by Alalwan et al. (2017), Djimesah et al. (2022), and Penney et al. (2021). This underscores the need for MTN MoMo to improve adoption by focusing on easy-to-use features, simple steps for using the service, and helpful customer support.

Performance Expectancy (PE) also strongly predicted Intention to Use (H3), suggesting that traders evaluate mobile money platforms based on practical advantages, such as faster transactions, safe storage of funds, and easier access to financial services. These findings are consistent with studies by Al-Okaily et al. (2020), Dzisi et al. (2023), and Venkatesh et al. (2003). Communicating the functional value of MTN MoMo, particularly for small-scale business operations, can enhance its perceived utility and encourage continued use.

Social Influence (SI) significantly impacted IU (H4), showing that peer recommendations, social norms, and community perceptions shape traders’ decisions to adopt MTN MoMo. This mirrors insights from Alalwan et al. (2016), Makanyeza (2017), and Narteh et al. (2017). In the close-knit environment of Makola Market, word-of-mouth and community trust play a vital role. However, the mixed findings in Kwofie and Adjei (2019) suggest SI may be context-specific, indicating the importance of localized outreach strategies.

Price Value (PV) had a significant positive influence on Intention to Use (IU), supporting Hypothesis 5 and reinforcing the notion that users assess mobile money services based on the balance between perceived benefits and financial costs. While transaction fees can pose a barrier, the findings indicate that traders still perceive MTN MoMo as offering strong value, evidenced by the sharp rise in MoMo transactions following the removal of the E-Levy in Ghana (Effah, 2025). This result is consistent with prior research by Alalwan et al. (2018), Al-Okaily et al. (2020), and Kwateng et al. (2019), who all identified that price positively affects behavioral intention.

Trust (TR) was a strong determinant of both PE and IU (H6 and H7), emphasizing that perceived security, reliability, and fraud protection are central to adoption decisions. This supports findings by Alalwan et al. (2017), Kwateng et al. (2019), and Kwofie and Adjei (2019). Traders’ trust in MTN’s systems significantly influences the willingness to adopt the MoMo service. It also shapes perceptions of the platform’s usefulness, highlighting the importance of visible security features and targeted consumer education.

Facilitating Conditions (FC) significantly influenced Use of MTN MoMo (UoM) (H8), indicating that technical infrastructure, such as phones, stable networks, and support services, are essential for usage. This reinforces earlier research by Alalwan et al. (2017), Kiconco et al. (2019), and Venkatesh et al. (2012). For mobile money to thrive in informal economies, service providers must ensure users have the practical means to participate. Finally, Intention to Use (IU) was a strong predictor of actual usage of MTN MoMo (UoM) (H9), in line with the original UTAUT2 model Venkatesh et al. (2012) and empirical studies by Cheung and To (2017), Sharifzadeh et al. (2017), and Wang et al. (2022). This confirms that once traders form strong positive intentions, based on value, trust, and ease of use, they are more likely to engage in sustained usage behavior.

Theoretical and Practical Implications

This study contributes novel theoretical insights into mobile money adoption in developing contexts by applying a modified UTAUT2 model (Akasreku, 2020). This version incorporates trust, a critical but often underexplored factor in digital financial services adoption (Kwofie & Adjei, 2019). By focusing specifically on Makola Market traders in Ghana, the study extends prior research (Kwateng et al., 2019; Narteh et al., 2017; Osei-Assibey, 2015), which typically addressed mobile money or banking adoption at the general population level without isolating provider-specific dynamics. Building on Alalwan et al. (2017), this research deepens the UTAUT2 model by empirically integrating trust alongside traditional constructs.

Methodologically, it advances existing literature by applying a two-stage hybrid approach, PLS-SEM and ANN, to overcome linearity constraints inherent in SEM (Al-Okaily et al., 2020; Dzisi et al., 2023). The ANN model captures complex, nonlinear relationships that better reflect real-world adoption behavior. This is particularly useful in unpacking how traders’ perceptions of ease of use and trust in MTN MoMo jointly shape performance expectancy. By introducing these new causal paths, effort expectancy and trust on performance expectancy, the study offers a refined lens for understanding mobile money usage in informal markets and contributes to theory-building in digital finance adoption.

From a practical standpoint, this study offers actionable insights for MTN, financial institutions, and policymakers aiming to expand mobile money adoption among informal traders in Ghana. The findings highlight key behavioral drivers, intention to use, performance, effort expectancy, social influence, facilitating conditions, price value, and trust as critical to influencing uptake of the MoMo service.

To improve adoption, MTN should simplify onboarding procedures and payment processes, especially for traders with limited technical expertise. Improving user experience through a simple interface, clear instructions, and responsive customer support will be essential to encouraging adoption. Traders’ concerns about security and fraud can be addressed through visible trust-building measures, such as fraud alerts, scam awareness pop-ups, and collaboration with regulators on consumer protection campaigns. Real-life success stories from Makola traders who have benefited from MTN MoMo should be actively shared to boost peer influence in this community-driven environment.

Financial institutions can develop microcredit products linked to mobile money usage, targeting traders who trust the platform but lack capital. Meanwhile, policymakers like the Bank of Ghana and local market authorities should support the ecosystem by expanding agent networks, enforcing service quality standards, and investing in digital literacy campaigns. Furthermore, small-scale fee exemptions or subsidies should be considered, particularly given the deterrent effects previously associated with the E-levy. Its removal led to a record GHC365 billion in mobile money transactions in April 2025, demonstrating how affordability is central to sustaining usage (Effah, 2025).

Finally, trust-building efforts should be community-based and culturally grounded, delivered in local languages like Twi, to close knowledge gaps and enhance long-term confidence in the MTN MoMo platform.

Limitations and Future Research Directions

The study focused on MTN MoMo adoption among Makola Market, Accra, Ghana traders. The findings may not directly apply to other developing countries due to potential cultural and economic differences. Future research could explore MoMo adoption across a broader geographical scope or within specific industry segments to deepen insights into how individuals utilize MoMo in diverse contexts. Further, future studies could explore additional variables such as perceived security or risk aversion on MoMo adoption behavior.

Conclusions

The rapidly growing MoMo platform in Ghana presents significant opportunities for increased adoption among traders. The study addresses this by examining the factors influencing MTN MoMo adoption among traders in Makola Market. This fills a gap in the literature, as few studies on mobile money in Ghana exist. Additionally, there was a need to select a theoretical foundation that captures the key aspects associated with MTN MoMo adoption by Makola traders in Ghana. Therefore, we selected Venkatesh et al. (2012) UTUAT2 to propose the conceptual model of this study. We included trust as an external factor, given its widely recognized importance as a predictor of individuals’ intention to use mobile payments. The main statistical results supported the predictive validity of the conceptual model, explaining about 90.5% of the variance in the intention of Makola traders to use MTN MoMo. Our findings show that performance expectancy, effort expectancy, social influence, price value, and trust significantly influence traders’ intention to use MTN MoMo. Additionally, both intention to use and facilitating conditions were significant factors predicting actual usage of MTN MoMo, explaining about 64.5% of its variance. These findings can guide strategies to promote MTN MoMo adoption among traders in Makola Market and potentially contribute to Ghana’s more inclusive financial ecosystem.

Footnotes

Ethical Considerations

This study involved human participants and was carefully designed to avoid any potential harm. The survey focused on general questions related to mobile money usage, as outlined in the questionnaire, and did not collect sensitive or personally identifying information. The potential benefits of the study, such as improving mobile money services and promoting financial inclusion, were considered to outweigh any minimal risks. Since the study was conducted in a market environment, verbal informed consent was obtained with the assistance of local market authorities and participating traders, and participation was entirely voluntary. Participants were informed of their right to decline or withdraw from the study at any time.

Author Contributions

Regina Naa Amua Dodoo: Conceptualization, Writing – Original draft, Fu Xin: Conceptualization, Reviewing and Editing, Tinashe Mangudhla: Methodology, Reviewing and Editing, Validation, Emmanuel Bosompem Boadi: Data curation, Methodology, Formal Analysis; Levente Dimen: Writing—Original draft, Data curation; Alina Cristina Nuta: Conceptualization, Writing—Original draft; Reviewing and Editing, Supervision. All authors read and approved the final manuscript.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be available on request.