Abstract

This study examines the impact of mixed-ownership reform on total factor productivity (TFP) of Chinese state-owned enterprises (SOEs), based on panel data of 1,211 firms from 1998 to 2007. The analysis identifies two primary reform pathways: reducing the share of state-owned capital and removing the SOE identity. Results reveal that eliminating SOE identity significantly improves TFP, while merely reducing the state-owned capital share exerts a negative effect. The positive impact of identity removal is linked to reductions in agency costs and policy burdens, whereas the adverse effect of ownership dilution may stem from alternative mechanisms unrelated to governance improvement.

Introduction

State-Owned enterprises (SOEs) are firms in which the government holds a substantial ownership stake, either wholly or partially, and exerts significant control over their operations (Lin et al., 2020). These entities are typically established to pursue both economic and social objectives and are concentrated in strategic sectors such as energy, transportation, and public services (Gershman & Thurner, 2016). Economists frequently regard SOEs as less efficient than their private-sector counterparts, citing agency problems, and political burdens as primary concerns (Jensen & Meckling, 1976; Clò et al., 2023; Lin & Tan, 1999).

Over the years, policymakers have introduced various reforms to improve SOE performance. In China, home to the world’s largest number of SOEs, reforms have included contract-based management systems, profit retention schemes, and, more recently, mixed-ownership reforms (Lin, 2021). Although introducing private capital into SOEs through mixed-ownership reform is widely considered a potential solution to inefficiency, its actual effectiveness remains under debate.

A growing body of literature has examined the relationship between state ownership and firm performance. Sun and Tong (2003) reported a negative impact of state ownership on firm performance, while Chen et al. (2009) argued that SOEs can be more efficient than private firms. Li et al. (2023) analyzed 826 Chinese firms and found a negative association between government ownership and firm value. Other studies have highlighted the adverse effects of separating control and ownership rights on shareholder value (Gompers et al., 2010; Nguyen et al., 2020), though some have reported exceptions, for instance, Sanjaya (2011) found that separation of rights can benefit controlling shareholders in Indonesia. Konijn et al. (2011) noted a negative effect of such measures on U.S. firms. Zhang et al. (2020) observed that mixed-ownership reform enhances innovation capacity in SOEs.

Despite these efforts, few studies have distinguished between different types of mixed-ownership reform. This may partly explain the inconsistency in empirical findings. To address this gap, this study disaggregates mixed-ownership reform into two types based on preliminary descriptive statistics.

First, data from China’s Industrial Enterprise Database reveal that joint ventures frequently maintain state ownership at or near 50%. According to Chinese regulatory definitions, enterprises retaining at least 50% state ownership are still classified as SOEs. We thus identify two reform pathways: (1) reducing the proportion of state-owned capital below 50%, resulting in the loss of SOE identity; and (2) introducing non-state capital while keeping state ownership above 50%, thereby retaining SOE status. The latter approach is three times more common than the former.

Due to missing values for key variables after 2007, our analysis focuses on the 1998 to 2007 period using Chinese SOE joint venture data. We employ the random forest method to estimate the causal impact of mixed-ownership reforms on TFP. The baseline and robustness checks indicate that eliminating the SOE identity significantly increases TFP, while merely reducing the share of state capital, without changing SOE status, reduces TFP.

Mechanism analysis reveals that removing SOE identity improves productivity by lowering agency costs and policy burdens. Conversely, reducing state capital without fully eliminating state control yields the opposite effect. Heterogeneity analysis shows that the positive impact of SOE identity removal is significant in eastern, labor- and technology-intensive regions, while the negative impact of reducing state capital is more pronounced in western, capital-intensive regions. Moreover, removing SOE identity is associated with lower employment levels but higher wages, while reducing state capital results in higher employment but lower wages.

This study makes several key contributions: First, this is the first study to classify mixed-ownership reform into distinct categories based on statistical evidence and evaluate their differential impacts on firm-level TFP. This approach helps clarify the divergent findings in the existing literature. Second, to address concerns about endogeneity and model overfitting that often plague panel fixed-effects models, we adopt a nonlinear random forest approach. This method effectively handles high-dimensional data and mitigates estimation bias. We further enhance the robustness of our analysis by employing propensity score matching (PSM) and a difference-in-differences (DID) design. Third, given China’s large number of SOEs, our findings offer valuable insights into the effectiveness of mixed-ownership reforms in other developing and emerging economies seeking to improve state sector performance.

The remainder of this study is organized as follows. Section “Literature Review and Hypotheses Development” reviews the relevant literature and develops the research hypotheses. Section “Research Design” describes the research design. Section “Stylized Fact Analysis” presents the stylized facts. Section “Empirical Results” reports the empirical results. Section “Further Analysis” conducts further analyses and heterogeneity checks. Section “Conclusion” concludes with a summary and policy implications.

Literature Review and Hypotheses Development

SOEs possess distinct characteristics that differentiate them from non-state-owned enterprises (non-SOEs), which are privately owned and operated with minimal or no government ownership or control. While SOEs often pursue a combination of economic and social objectives, non-SOEs are primarily driven by profit maximization and operate independently from government influence. Private enterprises vary widely in scale, ranging from small family-owned businesses to large multinational corporations.

SOEs are frequently subject to substantial policy burdens, including employment mandates, taxation requirements, and obligations to maintain macroeconomic stability (Wang et al., 2022). These responsibilities often conflict with commercial goals, compelling managers to prioritize social welfare over operational efficiency and productivity. Under the political championship system, SOE executives may focus on short-term political or social objectives at the expense of long-term performance, ultimately exerting a negative influence on TFP (Terry, 2023).

Additionally, such policy constraints are associated with rigid budget constraints and heightened risk aversion (Peng et al., 2023), which limit the ability of SOEs to invest in long-term innovation activities such as research and development (R&D; Lin, 2021).

Beyond policy burdens, SOEs also face pronounced principal-agent problems. Misalignments between managers’ interests and those of the firm or shareholders can result in decisions that prioritize personal benefit over long-term value creation (Apriliyanti et al., 2023; Van Thiel et al., 2020). The centralized nature of ownership in SOEs may further aggravate these issues by enabling the appointment of directors based on political loyalty or rent-seeking motives, thereby undermining governance quality (Zhang et al., 2024). Government interference in board appointments has also been found to negatively impact firm performance (Jin et al., 2022).

Moreover, due to a lack of market-based incentives and effective supervisory mechanisms, SOE managers often exhibit hesitation in strategic decision-making. Short-term investment decisions are common, often driven by political or bureaucratic considerations. Furthermore, limited familiarity with operational realities and rapidly changing market dynamics restricts the ability of SOE executives to make rational and scientifically informed decisions (Leutert, 2016). Figure 1 presents the above mechanisms.

SOEs’ TFP is lower than non-SOEs’.

In light of the above considerations, we propose the following research hypothesis:

H1: The TFP of SOEs is lower than that of non-SOEs due to higher policy burdens and greater agency costs.

The removal of the state-owned identity enables SOEs to alleviate policy burdens, enhance internal governance, and redirect executive incentives toward profit maximization (Liu et al., 2024). This transformation facilitates the establishment of a more market-oriented operational framework and promotes strategic organizational changes. In particular, the introduction of non-state shareholders can increase the degree of external control over corporate decision-making (Ye et al., 2021), allowing these shareholders to appoint directors and participate directly in corporate governance. In contrast, in many SOEs that retain their state-owned status, the authority of executives and board members is often constrained, limiting their ability to implement effective strategic decisions.

Furthermore, the removal of the SOE identity can improve firm competitiveness and governance structures. Non-state shareholders often bring innovative thinking and entrepreneurial spirit, which can support SOEs in developing new products and identifying market opportunities, thereby enhancing their leadership in key industries (Sun et al., 2024). Their diversified investment experience also strengthens SOEs’ capabilities in information acquisition and risk management (Li et al., 2023). These advantages allow firms to respond more quickly to market dynamics and reduce operational uncertainty. Additionally, reducing policy burdens and mitigating principal-agent problems can significantly lower agency costs.

In contrast, reforms that merely reduce the proportion of state capital may fail to address the root causes of inefficiency. In such cases, productivity remains constrained by unresolved policy burdens. Moreover, reducing the state-owned capital ratio can trigger internal power struggles due to misalignment between ownership stakes and control rights. Non-state shareholders may find it difficult to obtain board representation proportional to their equity holdings, limiting their influence over corporate governance and strategic planning. Without sufficient access to decision-making authority or resources, their ability to support board-level initiatives remains weak. As a result, control effectiveness deteriorates. As argued by Liu et al. (2018), effective governance arrangements are more critical than ownership structure alone in realizing the intended benefits of mixed-ownership reform. Figures 2 and 3 present the above mechanisms.

Removing state identity improves TFP.

Reducing state capital ratio reduces TFP.

Based on this discussion, we propose the following research hypothesis:

H2a: Mixed-ownership reforms that involve the removal of state-owned enterprise identity are positively associated with improvements in firms’ TFP.

H2b: Mixed-ownership reforms that reduce the share of state-owned capital while retaining a state-owned identity are negatively associated with firms’ TFP.

Research Design

Data

The data used in this study are derived from the China Industrial Enterprise Database (CIED), compiled by the National Bureau of Statistics of China. This dataset is based on annual reports submitted by industrial firms to local statistical bureaus. Formally titled the Database of All State-Owned and Non-State-Owned Industrial Enterprises Above Designated Size, it includes all state-owned enterprises and non-state-owned industrial firms with annual main business revenue of 5 million RMB or more. The statistical unit of observation is the legal entity of the enterprise.

To measure TFP, we adopt the Levinsohn-Petrin (LP) and Wooldridge estimation methods, both of which require data on intermediate inputs. However, this variable is unavailable after 2007. Therefore, we restrict our analysis to the 1998 to 2007 period.

The raw dataset for 1998 to 2007 contains 2,226,933 firm-year observations. Following the filtering criteria outlined by Brandt et al. (2012), we implement the following steps: (1) we exclude 857,780 observations with missing values for key variables such as value-added, total sales, and total assets. (2) We remove 27,703 observations from firms with fewer than eight employees. (3) We eliminate 497 observations with implausible asset structures—for example, where total current assets or total fixed assets exceed total assets. (4) We exclude 243,777 observations with annual sales below 5 million RMB. (5) Based on the standard of Bai (2009), we remove 436,280 outlier observations. (6) Since our focus is on SOEs undergoing mixed-ownership reform, we exclude 559,645 observations of non-state-owned firms.

To construct a reliable panel, we follow the panel identification strategy of Brandt et al. (2012), using legal entity codes as the primary identifier. In cases of unmatched or duplicate legal entity codes, we match firms using legal names. If this still yields ambiguity, we adopt a composite identifier: “region (county) + legal representative’s name.” Unlike Brandt et al.’s (2012) original method—which may generate overly broad matches by using “postal code + industry code + main product + county name + year of establishment,” our approach minimizes misclassification by employing “regional code (county) + telephone number + year of establishment” as a more precise matching strategy.

After all processing steps, the final panel consists of 47,700 firms and 101,251 firm-year observations for the period 1998 to 2007 (see Table 1).

The Information of Data.

Random Forest Approach

Unlike traditional parametric methods, the random forest approach, as emphasized by Breiman (2001), does not rely on the assumption of a predetermined functional form.

Consider a sample of n independent observations (Xi, Yi, Wi), i = 1, 2, 3–n, where Xi represents the covariates, Yi∈R denotes the response variable, and Wi is the binary treatment indicator. Let Y(0)

i

and Y(1)

i

denote the potential outcomes under the control and treatment conditions, respectively. The individual treatment effect

Following Rosenbaum and Rubin (1983), we assume the conditional independence assumption holds:

Under this assumption, the treatment effect can be expressed as:

where e(x) is the propensity score, that is, the probability of receiving treatment conditional on x. An unbiased estimate of e(x) can be obtained once

To analyze the effect of removing the SOE identity on TFP, Yi denotes the TFP of firm i, and Wi is the treatment variable indicating SOE status. Firms with a state-owned capital share greater than or equal to 50% as assigned to the treatment group (Wi = 1), while others form the control (Wi = 0).

For the analysis of reducing the state-owned capital share, Wi = 1 denotes firms that experienced a reduction in the state-owned capital share while maintaining SOE identity. The control group (Wi = 0) includes SOEs whose state-owned capital share remained unchanged. To implement the random forest model, 70% of the sample is randomly selected to form the training dataset.

Variables

Total Factor Productivity

Given the unbalanced nature of our panel data, we employ the Levinsohn–Petrin (LP) method (Levinsohn & Petrin, 2003) to estimate firms’ TFP. Following existing studies, we calculate firm-level fixed capital stock using the China Industrial Enterprise Survey Database. Specifically, we adopt the total fixed assets indicator as a proxy for capital stock, as it comprehensively reflects a firm’s capital status by incorporating the original value of fixed assets, construction materials, asset liquidation, pending losses, and other relevant items, in accordance with standard accounting principles.

We estimate fixed asset investment using the following identity:

Where It is the investment in fixed assets in year t, Kt is the fixed asset value, and Dt denotes the depreciation of fixed assets. All nominal variables are deflated to constant prices using 1999 as the base year. Industrial value-added is deflated by the local producer price index (PPI) for industrial products, while the capital stock is deflated using the fixed asset investment price index for each province.

To ensure robustness, we also estimate TFP using the Wooldridge (2009) approach, which addresses potential endogeneity in intermediate input choices.

Control Variables

Drawing on prior studies, we include the following control variables in our regression models:

(1) Firm size: Larger firms may benefit from economies of scale, which enhance productivity (Steinbrunner, 2024). We use the natural logarithm of total assets to measure firm size (lnsize).

(2) Firm age: Older firms often accumulate experience and learning effects, contributing to productivity improvements (Cucculelli et al., 2014). Firm age is calculated as the natural logarithm of the difference between the statistical year and the year of establishment, plus one (lnage).

(3) Human capital: A more skilled workforce is positively associated with productivity (Abel et al., 2012). We use the natural logarithm of the number of employees to proxy human capital (lnlabor).

(4) Wage level: Wage per capita is measured as the natural logarithm of total wages payable divided by the number of employees (lnwage), reflecting labor cost and potential skill intensity.

(5) Firm leverage: Financial leverage may constrain investment and negatively affect productivity (Towo et al., 2019). Leverage is measured as the ratio of total liabilities to total assets.

(6) Capital stock: Capital stock per worker is a key determinant of labor productivity. It is calculated as the natural logarithm of paid-in capital divided by the number of employees (lncapital).

To mitigate the influence of outliers, all continuous variables are winsorized at the 1st and 99th percentiles

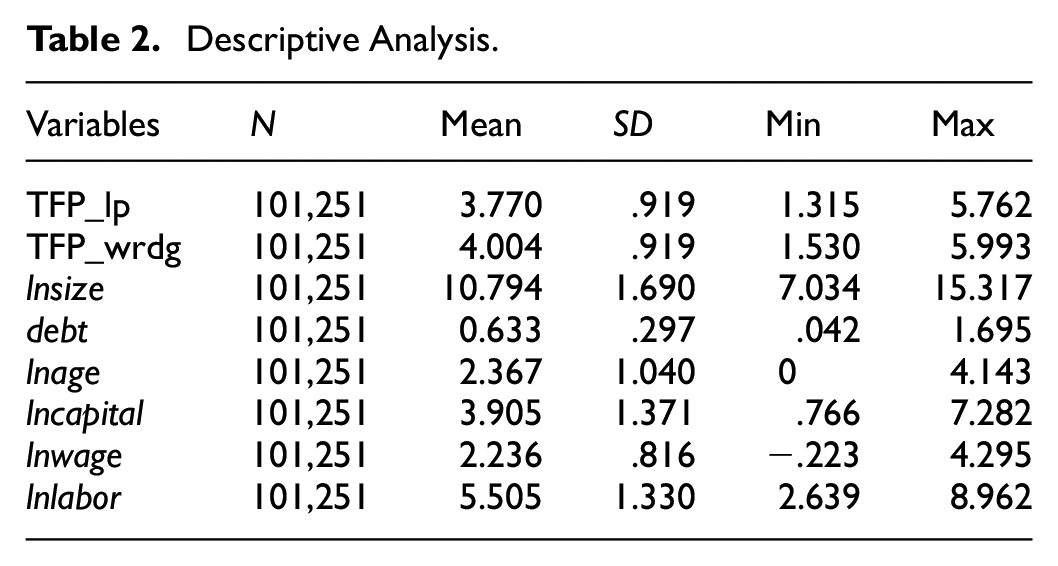

Description Statistics

Table 2 reports the results of the descriptive statistical analysis. The mean, standard deviation, maximum, and minimum values of TFP are 3.770, 0.919, 5.762, and 1.315, respectively, indicating substantial variation in TFP across firms. The descriptive statistics for the control variables are consistent with the findings of previous studies, suggesting the reliability and representativeness of the sample.

Descriptive Analysis.

Stylized Fact Analysis

Preferential Characterization of State Ownership of Joint Ventures

According to the prevailing institutional classification in China, firms with state-owned capital equal to or exceeding 50% are considered to possess a state-owned identity.

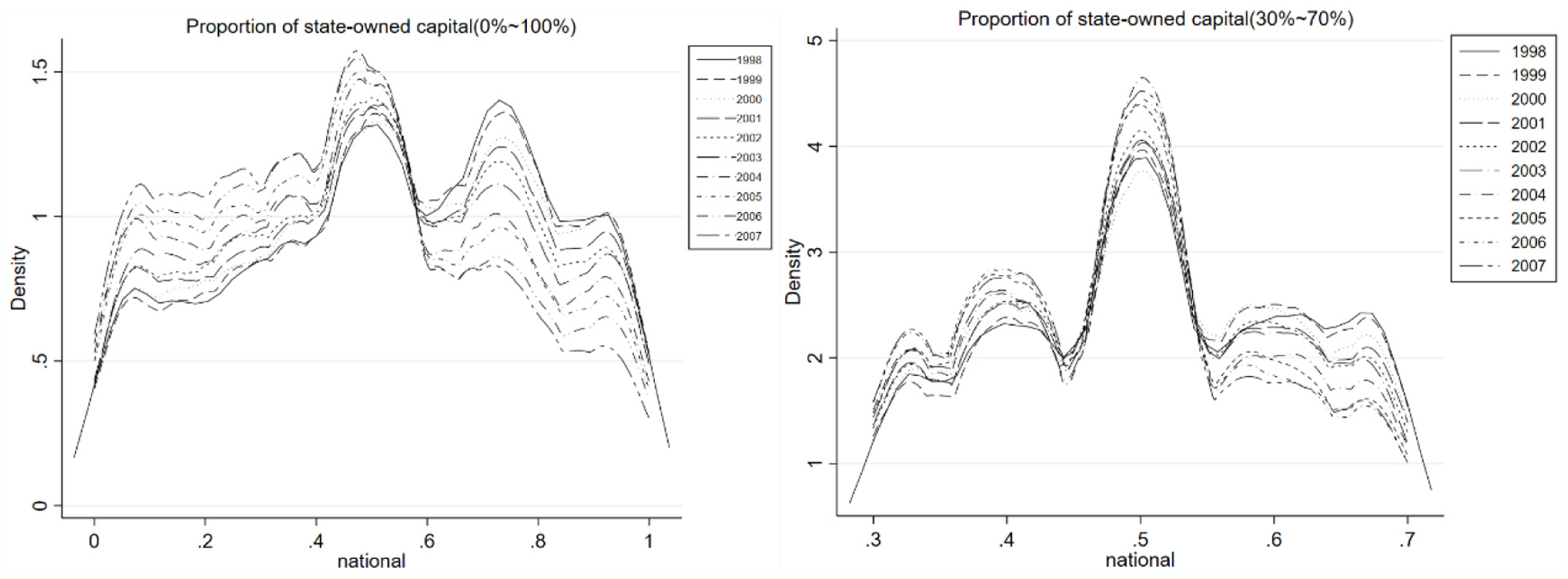

Among industrial joint ventures involving state-owned capital, the proportion of firms retaining state-owned identity was highest in 1999, reaching 58.33%. This figure gradually declined over the years, with only 42.55% of joint ventures retaining state-owned status by 2007.

As shown in Figure 4, many joint ventures appear to strategically adjust their state-owned capital ratio around the 50% threshold to maintain or obtain state-owned identity. Although some firms have transitioned away from state-owned status, a clear preference for retaining such identity remains evident within the joint venture group.

Kernel density plot of state capital share.

Additionally, we observe a sharp peak in the distribution of state-owned capital ratios at 75%. This is largely attributable to China’s policy that grants tax incentives to firms with at least 25% foreign equity participation. As a result, many enterprises adjust their equity structure to maintain foreign ownership just above this 25% threshold, leading to a concentration of state-owned capital ratios at 75%.

Characteristics of the Path of Mixed-Ownership Reform of SOEs

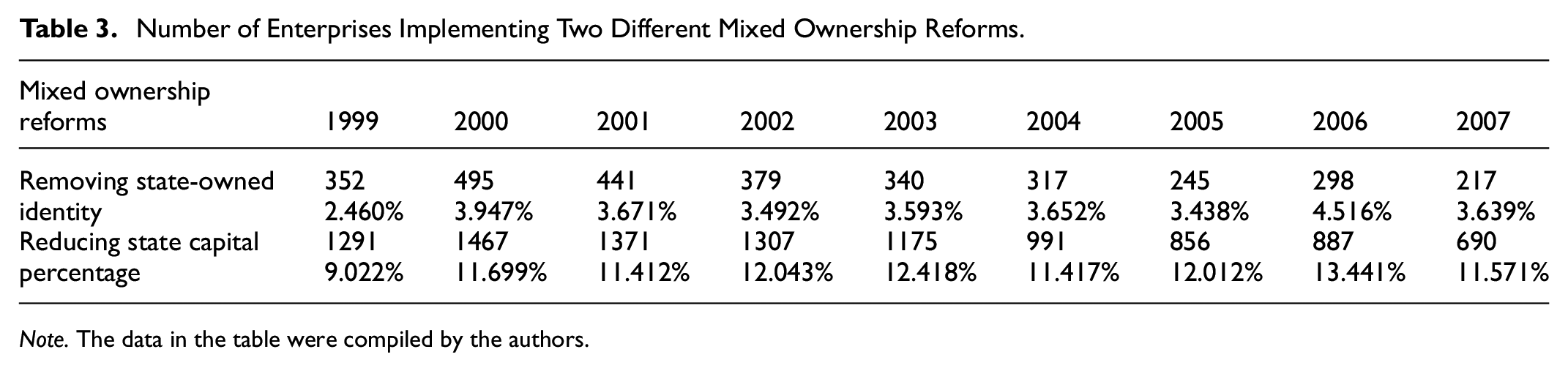

In China, mixed-ownership reform typically follows two main pathways: the removal of state-owned identity and the reduction of the state-owned capital share. As shown in Table 3, the number of firms that choose to reduce the proportion of state-owned capital without relinquishing their state-owned identity is approximately three times greater than the number of firms that fully remove their state-owned status. This pattern suggests a strong institutional preference among joint ventures to retain their state-owned identity, likely due to associated advantages such as regulatory benefits, access to resources, or political legitimacy.

Number of Enterprises Implementing Two Different Mixed Ownership Reforms.

Note. The data in the table were compiled by the authors.

Characteristics of the Relationship Between State Ownership and TFP

Table 4 compares TFP between joint ventures with and without state-owned identity. With the exception of 2007, joint ventures retaining state-owned identity consistently exhibit lower TFP than those without such identity. However, the average TFP growth rate for firms with state ownership is 2.31%, slightly higher than the 1.94% observed for their non-state-owned counterparts.

Comparison of TFP.

Note. Diff is the value of TFP minus TFP of firms on the left side of the identity breakpoint 50% of the firms on the right side of the breakpoint, and a negative value means that the right side of the breakpoint has a higher total factor productivity than the left side of the breakpoint.

These findings reveal two noteworthy patterns: (1) firms with state-owned identity tend to have lower TFP levels, and (2) their TFP growth rate is marginally higher. This contrast suggests that mixed-ownership reform may play a role in enhancing productivity within state-owned firms.

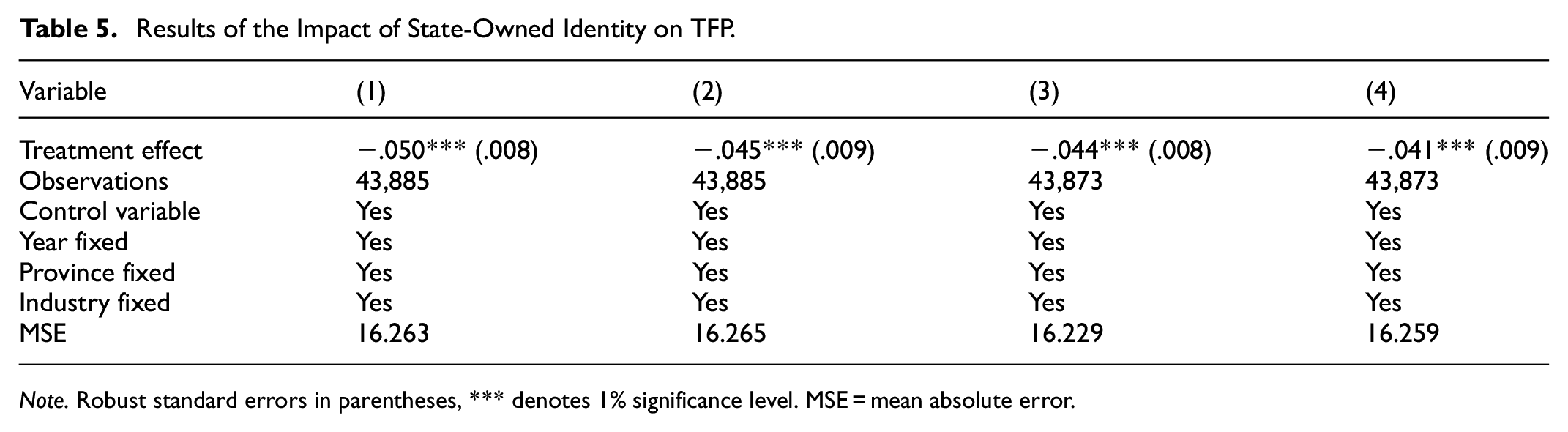

This section examines the impact of state-owned identity on firm productivity using a sample of joint ventures with a state-owned capital share ranging between 30% and 70%. Column (1) of Table 5 presents the results using the LP method to compute TFP, where firms are classified as having a state-owned identity if their state-owned capital share is greater than or equal to 50%. The estimated treatment effect is −.05 and is statistically significant at the 1% level, indicating that joint ventures with state-owned identity exhibit lower TFP.

Results of the Impact of State-Owned Identity on TFP.

Note. Robust standard errors in parentheses, *** denotes 1% significance level. MSE = mean absolute error.

In Column (2), we adopt an alternative identification criterion: a firm is classified as state-owned if the share of state-owned capital is the highest among all types of capital ownership. Under this alternative classification, the negative treatment effect remains statistically significant, suggesting the robustness of the result.

Columns (3) and (4) provide additional robustness checks. Column (3) reports results using the Wooldridge (2009) method for TFP estimation, while Column (4) applies the state-owned identity identification strategy proposed by Du et al. (2022). Both approaches yield consistent evidence of a significant negative impact of state-owned identity on firm productivity.

Figure 5 further illustrates the distribution of the estimated treatment effects of state-owned identity on firms’ TFP using a density plot. The probability mass is concentrated predominantly on the left side of the distribution, indicating that negative treatment effects are substantially more likely than positive ones. This visual evidence reinforces our earlier findings, suggesting that retaining a state-owned identity tends to reduce firms’ productivity.

Spectrogram of random forest treatment effect.

Although numerous studies have highlighted the inefficiency of SOEs, the specific mechanisms underlying this inefficiency remain insufficiently explained. Our baseline analysis identifies state-owned identity, not merely the presence of state capital, as a key factor contributing to lower TFP among firms.

To further explore the relationship between state ownership and productivity, we employ a panel fixed-effects model to examine the effect of the state-owned capital share on TFP. As shown in Table 6, the coefficients across all three model specifications are statistically insignificant. This suggests that the proportion of state-owned capital, in isolation, does not significantly impact firms’ productivity.

State Capital Share and Total Factor Productivity.

Note. Robust standard errors in parentheses, *, and *** denote 10% and 1% significance levels, respectively.

Taken together, these results indicate that it is the possession of a state-owned identity rather than the extent of state capital involvement that plays a decisive role in lowering firm-level TFP.

Empirical Results

Baseline Results

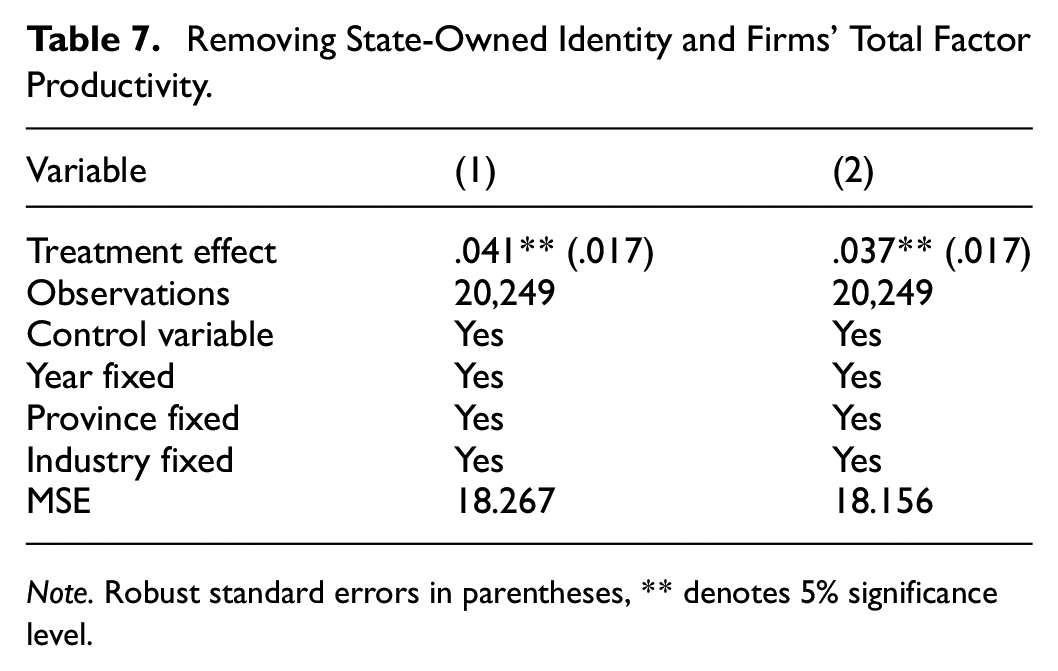

Table 7 presents the impact of removing state-owned identity on firms’ TFP. In Column (1), TFP is estimated using the LP method. The coefficient of the treatment effect is .041 and is statistically significant at the 5% level, indicating that firms that have removed their state-owned identity experience significantly higher TFP compared to those that retain it.

Removing State-Owned Identity and Firms’ Total Factor Productivity.

Note. Robust standard errors in parentheses, ** denotes 5% significance level.

In Column (2), TFP is estimated using the Wooldridge (2009) method. The results remain robust, confirming that the removal of state-owned identity has a positive and significant effect on firm productivity.

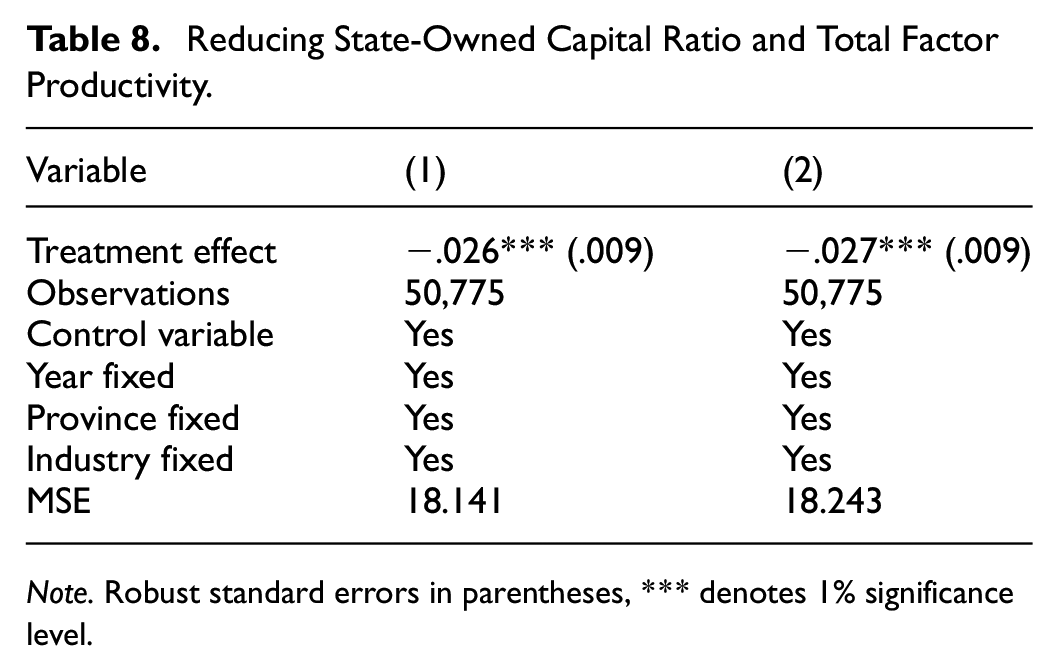

We now examine the impact of reducing the state-owned capital share on firms’ TFP. Column (1) of Table 8 reports the results using the LP method. The findings indicate that a reduction in the share of state-owned capital is associated with a further decline in firm-level TFP, suggesting a negative effect of partial ownership reform when state-owned identity is retained.

Reducing State-Owned Capital Ratio and Total Factor Productivity.

Note. Robust standard errors in parentheses, *** denotes 1% significance level.

In Column (2), we replace the TFP estimation method with the Wooldridge (2009) approach to test the robustness of the results. The negative relationship remains consistent, reinforcing the conclusion that the presence of state-owned identity is a key factor contributing to lower productivity in firms.

Moreover, Figure 6 reports the contribution of control variables in the above corresponding four different models. It indicates that wage, firm size, and leverage plays a great role in influencing TFP.

The contribution of control variables.

Robustness Tests

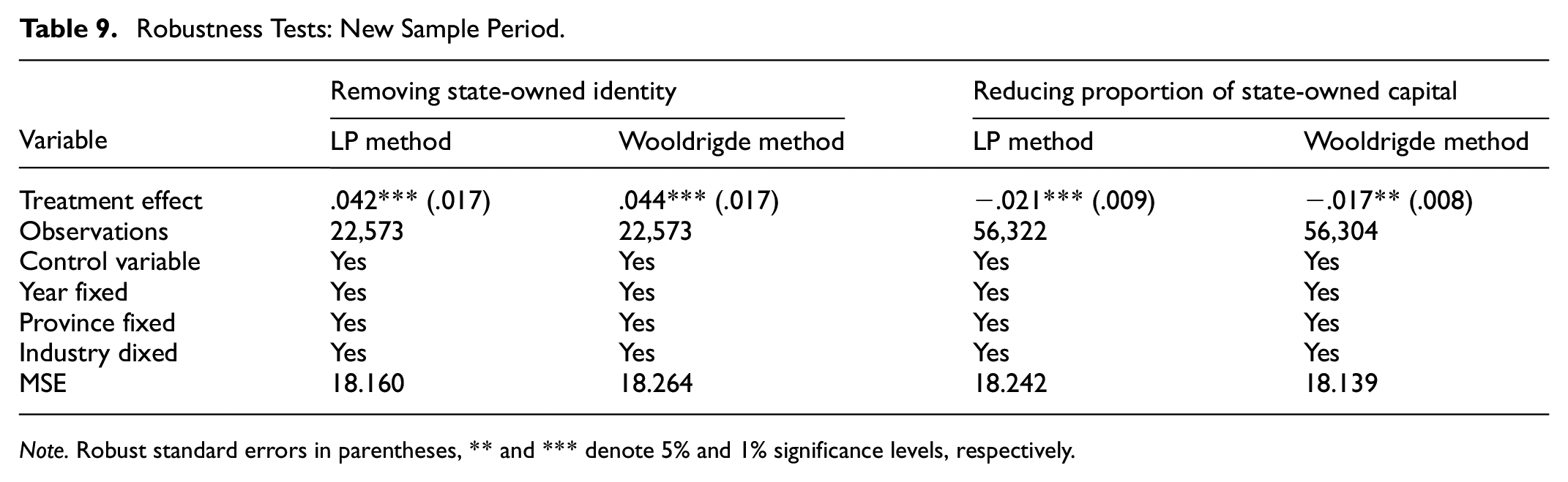

New Sample Period

We exclude the sample period from 2008 to 2010 due to missing key variables: the paid-in capital indicator is unavailable for 2009, and depreciation data are missing for all 3 years from 2008 to 2010. Accordingly, for the robustness analysis, we redefine the sample period as 1998 to 2013.

Given that the database lacks information on intermediate inputs after 2007, we employ the income approach to estimate industrial value-added. Intermediate inputs are approximated based on accounting standards, allowing us to construct a consistent TFP estimation framework for the extended sample.

Table 9 presents the results of the robustness tests. The coefficients on the treatment variables remain statistically significant at the 5% level or higher, confirming the reliability and consistency of the baseline findings.

Robustness Tests: New Sample Period.

Note. Robust standard errors in parentheses, ** and *** denote 5% and 1% significance levels, respectively.

New Sample: A-Share Listed Firms

In the baseline analysis, the study period was limited to 1998 to 2007 due to the unavailability of key variables, which restricted our ability to examine the long-term effects of mixed-ownership reforms on TFP. Moreover, Zhang et al. (2022) report a stagnation in TFP between 2008 and 2010, a trend that aligns with the global financial crisis during that period. In addition, the COVID-19 pandemic introduced significant distortions in capital markets and firm-level operations, further complicating data reliability for recent years.

To overcome these limitations and assess the long-term impact of mixed-ownership reform, we utilize data from Chinese A-share listed firms spanning 2011 to 2019. The results, presented in Table 10, indicate that removing state-owned identity continues to enhance TFP, whereas reducing the share of state-owned capita leads to a decline in TFP. These findings reaffirm the baseline conclusions and underscore the persistent effects of ownership structure on firm productivity over time.

Robustness Tests: New Sample Period.

Panel Fixed Model

As a robustness check, we employ a panel fixed-effects model to assess the impact of mixed-ownership reform on firms’ TFP. In this specification, the key independent variable is an interaction term between two dummy variables: Reform: A firm-level indicator that equals 1 if the enterprise has implemented a mixed-ownership reform, and 0 otherwise; Time: A time indicator that equals 1 for the year in which the reform is implemented and for all subsequent years, and 0 otherwise.

This model structure allows us to estimate the dynamic effect of reform adoption over time while controlling for firm-specific and time-invariant characteristics. The results, presented in Table 11, confirming that the removal of state-owned identity has a statistically significant effect on improving TFP.

Robustness Tests: New Model.

PSM–DID

To address potential selection bias, we conduct additional robustness checks using a propensity score matching combined with difference-in-differences (PSM–DID) model. The matching covariates include firm-level characteristics such as profitability, leverage, firm size, firm age, and capital stock. We adopt a 1:1 nearest-neighbor matching algorithm to construct a balanced treatment and control group.

Table 12 reports the results of the covariate balance test. The p-values for all matched covariates exceed the 5% threshold, indicating that the differences between the treatment and control groups are statistically insignificant after matching. This confirms that the matched sample satisfies the common support and balance requirements, ensuring the validity of subsequent regression analysis.

PSM Results.

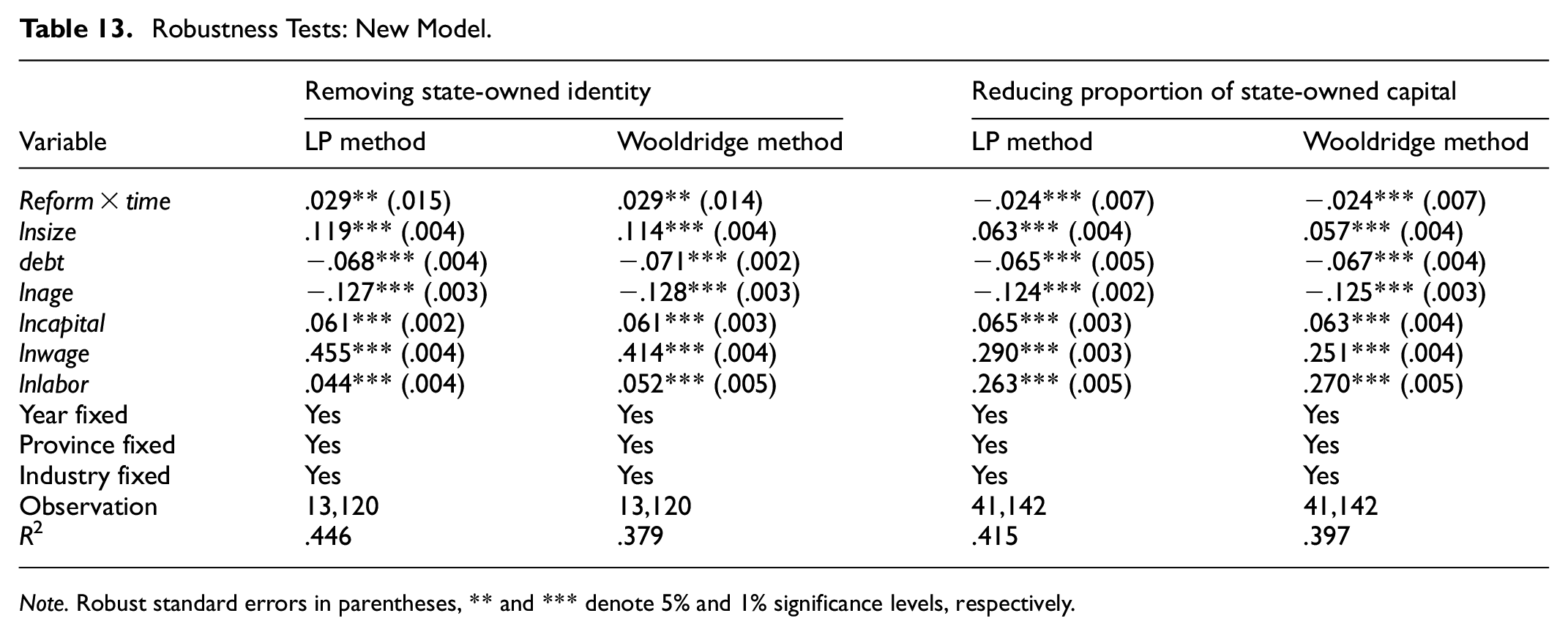

In the difference-in-difference (DID) model, the independent variable is the interaction term reform × time, where reform is a binary indicator equal to 1 if the firm has implemented a mixed-ownership reform, and 0 otherwise. The variable time takes the value of 1 for the year in which the reform was implemented and for all subsequent years, and 0 otherwise. The results reported in Table 13 are consistent with the baseline findings, further supporting the robustness of the main results.

Robustness Tests: New Model.

Note. Robust standard errors in parentheses, ** and *** denote 5% and 1% significance levels, respectively.

Comparison with Private Firms’ TFP

To further evaluate the impact of mixed-ownership reform on firm performance, we construct a new dependent variable: the absolute value of the TFP gap between SOEs undergoing mixed-ownership reform and private firms operating in the same industry. Given that private firms consistently exhibit higher TFP than SOEs within the same sector, a decline in this TFP gap would indicate that reform is contributing to productivity improvement.

Table 14 presents the results of this analysis. The findings show that, following the removal of state-owned identity, the TFP gap between SOEs and industry-matched private firms is significantly reduced. This suggests that such reform effectively narrows the productivity differential and enhances SOE efficiency.

Robustness Tests: Comparison with Private Firms’ TFP.

Note. Robust standard errors in parentheses, *** denotes 1% significance level.

In contrast, Columns (3) and (4) reveal that reducing the share of state-owned capital leads to a significant increase in the TFP gap. This result indicates that partial ownership reform not only fails to close the productivity gap with private firms but may further impair performance.

Internal Mechanism

First, according to principal-agent theory, higher agency costs in SOEs are associated with lower TFP. Following Ang et al. (2000), we measure agency costs using two indicators: the management expense ratio (management expenses divided by total revenue) and the asset turnover ratio (total industrial output value divided by total assets).

Second, based on the theory of benefit maximization, firms operating under resource constraints are expected to pursue profit maximization to achieve optimal resource allocation. However, SOEs often bear additional policy burdens which dilute their profit-driven objectives and result in higher risk aversion. This, in turn, reduces innovation incentives and leads to lower TFP compared to non-SOEs. Drawing on Ye et al. (2021), we quantify policy burden using the excess redundancy rate, calculated as:

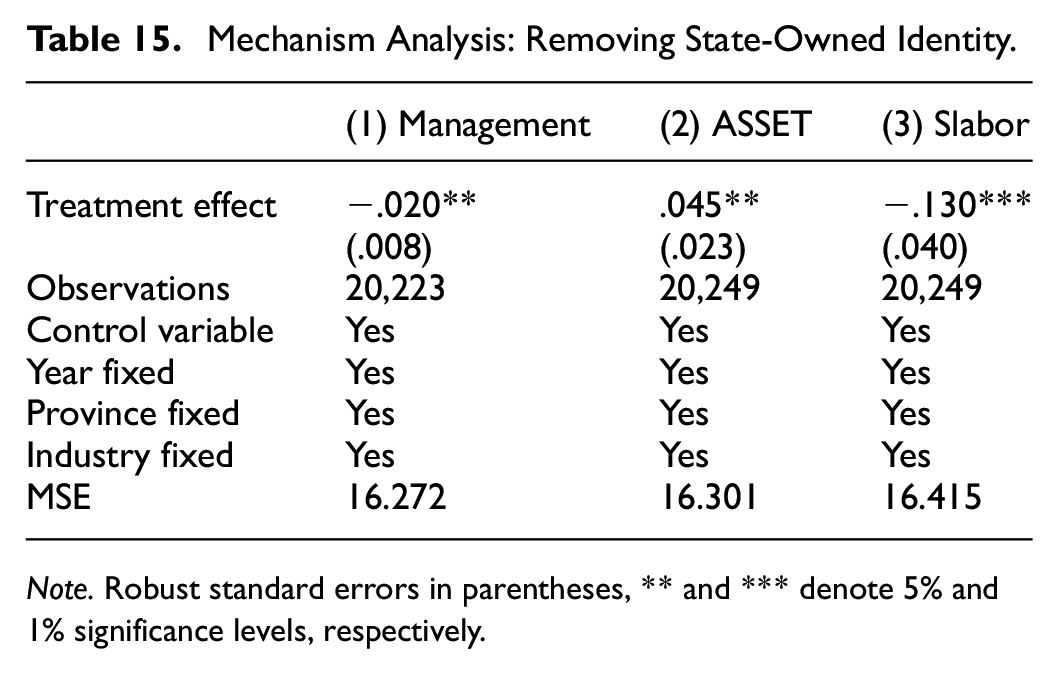

Table 15 presents the impact of removing state-owned identity on these mechanism variables. Columns (1) and (2) show that the treatment effect of identity removal is significantly negative for the management expense ratio and significantly positive for the asset turnover ratio. These findings suggest that removing the state-owned identity reduces agency costs. Column (3) further shows that identity removal significantly lowers the excess redundancy rate, indicating a reduction in policy burden.

Mechanism Analysis: Removing State-Owned Identity.

Note. Robust standard errors in parentheses, ** and *** denote 5% and 1% significance levels, respectively.

Taken together, these results support the hypothesis that eliminating the state-owned identity improves firms’ internal governance and operational efficiency by alleviating both agency problems and external administrative constraints.

Columns (1) and (2) of Table 16 show that reducing the share of state-owned capital significantly increases agency costs. Column (3) further indicates that such a reduction also raises firms’ policy burdens. These findings suggest that mixed-ownership reform, when implemented without the removal of state-owned identity, not only fails to alleviate internal inefficiencies but may in fact exacerbate them.

Mechanism Analysis: Reducing the Share of State-Owned Capital.

Note. Robust standard errors in parentheses, ** and *** denote 5% and 1% significance levels, respectively.

Specifically, the persistence of state ownership may hinder improvements in governance structures, thereby increasing managerial agency problems and sustaining or intensifying external policy constraints. As a result, management efficiency deteriorates, ultimately contributing to a decline in TFP.

Heterogeneity Tests

Central and Local SOEs

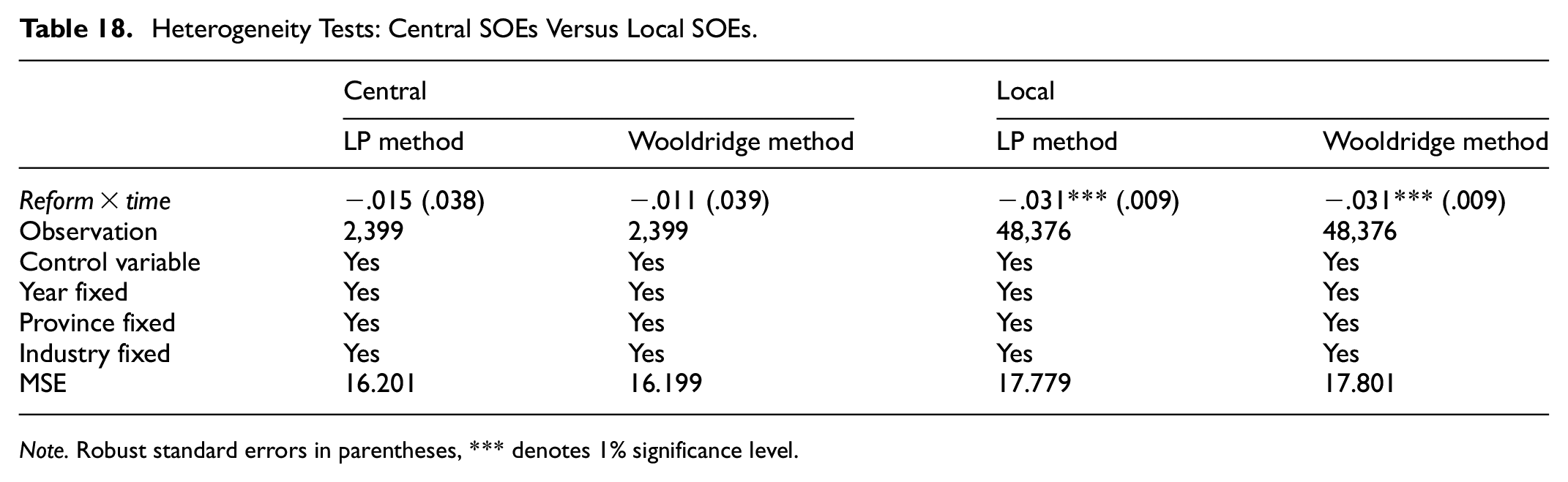

Due to differing business objectives and varying degrees of government intervention, there are substantial differences between centrally administered and local SOEs in the implementation of mixed-ownership reform. To examine this heterogeneity, we divide the sample into two subsamples: central SOEs and local SOEs.

Table 17 reports the differential effects of removing state-owned identity on firms’ TFP. The results show that the removal of state-owned identity has no statistically significant impact on the TFP of central SOEs. In contrast, it significantly improves the TFP of local SOEs.

Heterogeneity Tests: Central SOEs Versus Local SOEs.

Note. Robust standard errors in parentheses, ** denotes 5% significance level.

Several factors may explain this disparity. Central SOEs are typically large in scale and possess complex organizational structures, resulting in higher agency costs. Moreover, they often shoulder broader national policy responsibilities and are embedded in intricate networks of political and economic interests. These features make deep reform more difficult to execute effectively within central SOEs, thereby limiting the potential impact of mixed-ownership reform. By comparison, local SOEs operate in more decentralized governance environments and may respond more effectively to changes in ownership identity, thus realizing greater productivity gains.

Table 18 presents the heterogeneous effects of reducing the share of state-owned capital on firms’ TFP, disaggregated by ownership level. The results indicate that the reform leads to a statistically significant decline in TFP only among local SOEs. No significant effects are observed for centrally administered SOEs.

Heterogeneity Tests: Central SOEs Versus Local SOEs.

Note. Robust standard errors in parentheses, *** denotes 1% significance level.

This finding suggests that local SOEs may be more vulnerable to governance inefficiencies and institutional frictions when the share of state-owned capital is reduced without a corresponding adjustment in control mechanisms or corporate governance structures.

East, Center, and West Regions

Regional differences in economic development lead to variations in business environments, competitive intensity, and operational costs across firms. Following the regional classification established in China’s “Seventh Five-Year Plan” (1986), we divide the sample into three regions: eastern, central, and western China, based on the location of each firm.

Columns (1) to (3) of Table 19 report the effect of removing state-owned identity on TFP across these regions. The results indicate that this reform significantly enhances TFP only in the eastern region, while no statistically significant effects are found in the central or western regions. These findings remain robust when alternative TFP estimation methods are applied, as shown in the subsequent columns of Table 19.

Heterogeneity Tests: Central Versus Eastern Versus Western.

Note. Robust standard errors in parentheses, *** denotes 1% significance level.

Several factors may explain the regional variation. First, compared with the central and western regions, the eastern region offers a more favorable business environment and greater access to diverse resources including advanced technology, skilled labor, and capital which contribute to higher productivity. Second, the eastern region is characterized by more intense market competition. This heightened competition incentivizes firms to improve production efficiency and adopt more effective management practices. Moreover, competitive pressure helps reduce the opportunity for agency problems by aligning the interests of managers with those of the firm, thereby enhancing decision-making efficiency and overall firm performance.

Table 20 presents the regional heterogeneity in the impact of reducing the share of state-owned capital on firms’ TFP. Columns (1) to (3) report results for the eastern, central, and western regions, respectively. The findings reveal that reducing the state-owned capital share does not exert a statistically significant effect on TFP in either the eastern or central regions. However, a significant negative impact is observed in the western region.

Heterogeneity Tests: Central Versus Eastern Versus Western.

Note. Robust standard errors in parentheses, ** and *** denote 5% and 1% significance levels, respectively.

These results remain robust across different TFP estimation methods, indicating that the adverse effects of partial ownership reform are more pronounced in less-developed regions, where institutional environments and market mechanisms may be weaker.

Industry Heterogeneity

The industrial distribution of China’s SOEs is heavily concentrated in monopoly-dominated sectors such as public utilities, energy, telecommunications, military industries, and transportation. This structural concentration contributes to significant productivity disparities across industries. Based on the national industry classification system, we categorize firms into three groups: labor-intensive, capital-intensive, and technology-intensive industries.

Table 21 presents that mixed-ownership reforms involving the removal of state-owned identity significantly enhance TFP in labor-intensive and technology-intensive industries.

Industry Heterogeneity Tests.

Note. Robust standard errors in parentheses, ** and *** denote 5% and 1% significance levels, respectively.

This pattern can be explained by the nature of policy burdens in different sectors. In labor-intensive industries, SOEs often carry a strong policy mandate to preserve employment, resulting in labor redundancy and diminished productivity. The removal of state-owned identity reduces these social responsibilities, allowing firms to streamline employment structures and improve efficiency.

In technology-intensive industries, SOEs, particularly centrally administered ones, are frequently tasked with national R&D projects that are not necessarily driven by market efficiency. As a result, these enterprises often lag behind private firms in terms of technological innovation (Dong et al., 2014). Transitioning away from a state-owned identity enables SOEs in these sectors to adopt more market-oriented innovation strategies, thereby improving productivity.

Table 22 reveals that reducing the share of state-owned capital has a statistically significant negative impact on TFP in capital-intensive industries. However, the effect is not significant in labor-intensive or technology-intensive industries. These results suggest that the adverse consequences of reducing state capital are more pronounced in sectors where large-scale capital investment and state involvement may be more critical for operational stability and efficiency.

Industry Heterogeneity Tests.

Note. Robust standard errors in parentheses, *** denotes 1% significance level.

Further Analysis

In the previous sections, we examined whether and how two types of mixed-ownership reform affect firms’ TFP. However, for policymakers, enhancing TFP may not be the sole objective. Therefore, in this section, we further explore how mixed-ownership reform influences employment and wage levels, two key dimensions of firms’ social and economic performance.

First, we analyze the effect of mixed-ownership reform on employment. Removing state-owned identity helps alleviate policy burdens; however, increasing employment is often considered a form of social responsibility or burden for SOEs. Column (1) of Table 22 shows that removing state-owned identity significantly reduces employment levels, while reducing the proportion of state-owned capital significantly increases employment. This suggests that different types of reform have opposite effects on labor absorption.

Second, given the close relationship between wages and productivity (Strain, 2019), we examine how mixed-ownership reforms influence wage levels. Our findings indicate that removing the state-owned identity enhances firm productivity, leading to higher profitability. As shown in Column (2) of Table 23, this reform is associated with a significant increase in wage levels. In contrast, reducing the proportion of state-owned capital is found to lower TFP, and Column (4) of Table 23 demonstrates that this form of reform is linked to a reduction in wage levels.

Further Analysis.

Note. Robust standard errors in parentheses, ** and *** denote 5% and 1% significance levels, respectively.

These results highlight the differential social consequences of the two reform types and underscore the importance of tailoring reform strategies to both economic and social policy goals.

Conclusion

This study investigates the impact of mixed-ownership reform on TFP and explores the reasons behind inconsistent findings in the existing literature. Based on statistical classification, we identify two types of reform: (1) reducing the share of state-owned capital and (2) removing the state-owned identity. Our empirical analysis reveals that only the removal of state-owned identity leads to a significant improvement in TFP. In contrast, merely reducing the proportion of state-owned capital tends to reduce TFP.

From a mechanism perspective, the removal of state-owned identity alleviates agency problems and reduces policy burdens, thereby enhancing firm productivity. Conversely, reducing state capital may weaken governance arrangements and trigger internal power struggles, ultimately worsening efficiency.

We also find that the effects of reform are heterogeneous across regions and industries. The positive impact of removing state-owned identity is more pronounced in eastern China, particularly in labor- and technology-intensive industries. Meanwhile, the negative effect of reducing state capital is more significant in western regions dominated by capital-intensive sectors. Moreover, we observe that firms removing state-owned identity tend to reduce employment and increase wage levels, while those reducing state ownership alone show the opposite pattern, higher employment but lower wages, reflecting differences in labor allocation strategies.

Based on these findings, several policy recommendations can be drawn:

First, efforts to deepen mixed-ownership reform should prioritize establishing a fully market-oriented governance structure. The role of the state as a capital provider should be separated from managerial intervention. Strengthening capital market systems and creating a favorable external governance environment are crucial to this transformation.

Second, decision-makers in SOEs should pursue comprehensive and substantive mixed-ownership reforms. Non-state shareholders must be granted equal rights in corporate governance, particularly in board representation and voting rights. Such reforms can improve internal governance, enhance strategic decision-making, and promote alignment between firm objectives and market demands.

Third, a classification-based reform strategy should be adopted. Reform directions and governance standards should be tailored to the characteristics and functions of different types of SOEs. For instance, firms should choose reform paths that are compatible with their local institutional environment. In regions where economic development and fiscal revenue are highly dependent on SOEs, local government intervention should be minimized to prevent SOEs from being used as instruments for short-term political or economic goals.

Finally, for other developing countries with large state-owned sectors, the Chinese experience offers valuable insights. Mixed-ownership reforms can serve as an effective means to improve SOE performance, but such reforms must be carefully designed. A balance should be maintained between retaining state influence and incorporating private-sector dynamism. Rapid or poorly executed reforms may lead to unintended negative outcomes. Policymakers should focus on enhancing SOE autonomy, reducing administrative burdens, and customizing reform strategies to fit specific national contexts. For example, reforms that remove excessive state control while retaining partial state ownership may be more effective in certain strategic sectors than in others.

This study has several limitations that warrant consideration. First, the empirical analysis is restricted to Chinese state-owned enterprises (SOEs) during the period from 1998 to 2007. This temporal and geographical scope may constrain the generalizability of the findings to other national contexts or more recent timeframes. Future research could expand the scope by incorporating data from other developing or emerging economies, as well as more recent periods, to explore the broader implications of mixed-ownership reform on productivity across diverse institutional and economic environments. Cross-country comparative analyses may further enrich our understanding by identifying contextual conditions under which such reforms are more or less effective.

Second, the study does not explicitly examine heterogeneity in reform impacts across industries. Sector-specific factors—such as variations in capital intensity, labor structure, and market competitiveness—may shape how reforms influence firm performance. Future investigations could benefit from disaggregating results by industry to provide a more granular understanding of reform dynamics and to generate sector-specific policy insights.

Third, while the study establishes a relationship between mixed-ownership reform and productivity, it does not delve into the underlying mechanisms that drive this relationship. Labor allocation, managerial incentives, and technological innovation are potential channels through which reforms may exert their effects. Future studies could investigate these pathways more explicitly and consider how institutional settings and market structures condition the effectiveness of reform efforts in other developing country contexts.

Footnotes

Acknowledgements

We thank Chenchen Tian for her assistance in the initial data-collection phase.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article is supported by the National Social Science Fund of China (23BJL007).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.