Abstract

State-owned enterprises (SOEs) are the leading force in the national economy. The main goal of mixed-ownership reform is to enhance the SOEs’ independent innovation capability, thereby bringing high-quality development of the national economy. Based on the baseline regression and mediation effect model, this study explores the impact of mixed-ownership reform on exploratory innovation of SOEs from ownership structure adjustment and control rights allocation. The results show that the diversity of mixed shareholders, the depth of mixed equity, and the control of mixed equity significantly increase the SOEs’ exploratory innovation investment. And the shareholding ratio of heterogeneous shareholders has a differentiated influence on exploratory innovation. The mediation effect test indicates that the promotion effect of mixed-ownership reform of SOEs in the ownership structure dimension is achieved by reducing the second-type agency conflict and easing the financing constraints. In contrast, the promotion effect in the control rights allocation dimension is achieved by lowering the first-type agency conflict. The findings demonstrate that the mixed-ownership reform have positive effect on the SOEs’ exploratory innovation investment, and the different dimensions of mixed-ownership reform have disparate function routes to exploratory innovation. This study provides guidance for SOEs on how drive national innovation development through mixed-ownership reform. SOEs should guarantee the rights of non-state-owned capital to hold shares and appoint directors, improve internal governance mechanisms, so as to accelerate the development of exploratory innovation activities.

Introduction

Exploratory innovation is an effective approach for enterprises to cultivate and maintain core competitiveness (J. P. Wang, 2020). The concepts of “exploratory” and “exploitation” put forward by March (March, 1991) have aroused wide attention in the academic circles and become a hot topic in the innovation field. At present, China is in a critical period of economic transformation and upgrading. As the micro-entity of innovation activities, enterprises need to use the existing technology and market to stabilize income and constantly explore new technology and market to propel basic research and achieve new interest growth points. The 13th 5-year Plan on Technology and Innovation points out that the breakthrough progress in basic research and strategic high-tech field, the continuous raising of original innovation ability and international competitiveness are important manifestation of the obvious improvement of national independent innovation capability. The 14th 5-Year Plan also emphasizes the demand to consistently strengthen basic research, encourage free exploration, formulate and implement long-term action plans for basic research, and increase the proportion of basic research investment in total R&D investment to more than 8%. Therefore, adjusting the resource allocation of innovation strategy, enlarging the capital investment of exploratory innovation, breaking through the existing technology and knowledge trajectory to shape the core competitiveness has become crucial in ensuring the sustainable development of enterprise, and building an innovation-oriented country.

The study of the antecedent elements of exploratory innovation mostly starts from the perspective of results output, focusing on internal factors such as organizational learning (Jin & Chen, 2015), executive background (Z. Yang et al., 2017), and resource base (C. Y.Wang et al., 2014), as well as external factors such as network location (D. Ma et al., 2020), environmental dynamics (Y. Li et al., 2008), and institutional capital (Xiao et al., 2018). Existing research has explored the influencing factors of exploratory innovation performance from both internal and external aspects but has not sought motivation from the resource input. Reasonable allocation and effective use of resource elements are strong guarantees for promoting exploratory innovation (Su et al., 2007). The institutional background impacts significantly on the resource acquisition of innovation activities. There are evident distinctions in the types and quantities of resources owned by enterprises with different property rights (S. B. Choi et al., 2011). SOEs are an important pillar of the socialist economy with Chinese characteristics. Compared with other enterprises, they are of great significance in boosting the development and growth of the socialist public economy, maintaining national economic security, and driving national basic innovation. However, SOEs have policy-oriented operation objectives and single access to resources, and cannot support the acquisition of scarce resources through the market trading system. As a result, they can only adopt a conservative innovation strategy, which fundamentally limits the rational allocation of innovation resources and the implementation of high-risk exploratory innovation.

As an important way for the new round of SOE reform, mixed-ownership reform introduces non-state-owned strategic investors, establishes a marketization management system, and effectively uses marketization power to realize rational allocation of resources, which provides a realistic soil for the exploratory innovation activities of SOEs. This institutional reform requires SOEs transfer part of state-owned equity and share the ability to participate in governance. It is embodied in allowing non-state-owned shareholders to hold shares to obtain the transferred state-owned equity, giving them the right to appoint personnel, and exerting influence on innovation decisions. Meanwhile, exploratory innovation helps SOEs to innovate in the basic field and improve their innovation capability, which is consistent with the goal of mixed-ownership reform. Therefore, both equity and control rights should be included in the research scope to explore how mixed-ownership reform has an impact on exploratory innovation. However, the existing studies are mostly carried out around the ownership structure change. It is believed that non-state shareholders release innovative resources by reducing political pressure or suppressing management’s rent-seeking motives (W. G. Li & Yu, 2015; Y. W. Wang & Chen, 2017), which does not pay attention to exploratory innovation conducive to the formation of competitive advantage of enterprises, and also ignores the impact and path of equity and control rights reconstruction caused by mixed-ownership reform on these innovation activities.

Sufficient funds and effective governance mechanism are strong supports for exploratory innovation. The former originates from the expansion of financing channels by non-state-owned shareholders to ease the financing constraints, while the latter originates from the establishment of an effective supervision and balance mechanism to alleviate agency conflicts of SOEs. And other governance paths (Feng et al., 2021; Li & Li, 2022) are mostly realized on the premise of solving the agency problems and increasing the capital source for the enterprise. Therefore, this paper takes agency conflicts and financing constraints as the main perspectives to explain the impact of mixed-ownership reform on SOEs’ innovation decisions. On the one hand, the dynamic adjustment of the ownership structure has changed SOEs’ resource endowment and governance structure (X. Q. Yang & Yin, 2018). While restraining the capital occupation of major shareholders, it has obtained multiple financing channels from external strategic investors (Luo et al., 2019), alleviating the enterprises’ financing constraints, and bringing more resource support for the exploratory innovation with large capital demand. On the other hand, the control rights reallocation improves the voice of non-state-owned shareholders in innovation decisions. It enables SOEs to effectively utilize resources for basic research and development through the supervision of original executives by appointed directors. It can be seen that the dual dimensions of mixed-ownership reform may act on exploratory innovation through different paths.

Based on this, taking A-share state-owned listed companies as the research sample, this paper studies the impact of SOEs’ mixed-ownership reform on exploratory innovation and its mechanism from ownership structure adjustment and control rights allocation. There are three major contributions including: (1) It enriches the relevant research on the economic consequences of mixed-ownership reform. The existing works of literature concentrate on the function of mixed-ownership reform on SOEs’ investment decision (X. Q. Yang et al., 2020), financing cost (P. Wang et al., 2015), dividend distribution (Lu & Jiang, 2018), risk-taking (M. Y. Wang et al., 2020), policy burden (W. H. Zhang et al., 2021), enterprise value (L. F. Ma et al., 2015), and total factor productivity (L. Chen, 2018), while neglecting the impact on enterprises innovation investment assignment. This paper is the first to investigate the governance effect of mixed-ownership reform from the perspective of exploratory innovation, which provides a scientific basis for the quantitative evaluation of this policy reform effect. (2) It expands the research territory of influencing factors of exploratory innovation. At present, scholars mainly study the driving factors of enterprise exploratory innovation output from the internal and external resource base, seldom consider the effect of the reconfiguration of the SOE’s internal shareholder power and board power caused by the mixed-ownership reform. This paper considers equity and control rights at the same time to explore whether the mixed-ownership reform can promote exploratory innovation. Furthermore, the distinctions in the influence of different types of non-state-owned shareholders on exploratory innovation is analyzed to provide empirical evidence for the priority selection of heterogeneous non-state-owned shareholders in SOEs. (3) It reveals the mechanism of SOEs’ mixed-ownership reform on exploratory innovation. From agency conflicts and financing constraints, this paper dissects the specific path of the mixed-ownership reform affecting exploratory innovation, finds that the ownership structure adjustment and the control rights allocation play a role in exploratory innovation through different routes, breaking the previous limitations of paying attention to a single agency problem (Feng et al., 2021; Zhu et al., 2019). It explains the governance logic of non-state shareholders and their appointed directors in detail, which offers a beneficial complement to the related research on the governance path of SOEs’ mixed-ownership reform.

Theoretical Analysis and Hypothesis Development

The exploratory innovation of enterprises refers to subverting the existing organizational structure and knowledge system, fundamentally changing the original technological track, conducting research and development based on new knowledge and technology, and bringing unique, novel, and advanced products or services. It meets the needs of emerging markets and customers, forms a long-term competitive advantage through breakthrough revolution, and enables enterprises to obtain excess returns. However, investment activities are highly uncertain and have a long investment recovery cycle (Calantone & Rubera, 2012; Levinthal & March, 1993), which requires diversified knowledge, advanced technology level, abundant capital sources, and comprehensive market information of enterprises to support (Zhou & Wu, 2010). We can conclude that the technology research and development and innovation ability are closely related to the enterprise resources and capital input (Faber & Hesen, 2004), and the amount of investment directly determines the formulation of enterprise innovation strategies (Hewitt-Dundas, 2006). Therefore, investigating how to increase the exploratory innovation investment and the independent innovation ability of enterprises and even the country will be the research emphasis of this paper.

Agency conflicts and financing constraints are the main reasons for the inefficiency of corporate investment and the irrational allocation of resources (Bertrand & Mullainathan, 2003; Jensen & Meckling, 1976; Yu et al., 2014). This phenomenon is particularly obvious in the SOEs with “owner absence” and “government intervention,” which seriously hinders the tilt of SOEs’ resources to exploratory innovation. The mixed-ownership reform achieves cross-shareholding, mutual integration, and mutual restriction of heterogeneous capital by introducing external strategic investors, which significantly impacts the reconfiguration and reintegration of enterprise resource elements, and solves the above problems well. The SOEs’ mixed-ownership reform is mainly carried out through two channels. One is the continuous introduction of non-state-owned shareholders. It causes ownership structure change of SOEs, including the diversity of mixed shareholders formed by the cross-holding of heterogeneous shareholders and the depth of mixed equity formed by the perpetual accumulation of non-state-owned shareholders equity. The increasing types and proportion of non-state-owned shareholders can produce restriction and supervision on the state-owned controlling shareholders, raise the financing channels and financing ability, and achieve the complementary advantages of heterogeneous resources. The other is the control of mixed equity structured by non-state shareholders appointing directors, supervisors, and executives to obtain certain control rights. It impacts the SOEs’ operating decisions and brings down the possibility of the government-appointed executives making decisions that deviate from the interests of the enterprise. Thus, the mixed-ownership reform in imparity dimensions may affect the resource allocation of exploratory innovation activities through different paths. In summary, from the agency conflicts and financing constraints, this paper explores how the mixed-ownership reform promotes the SOEs’ exploratory innovation, which has certain theoretical and practical significance.

Mixed-Ownership Reform and Exploratory Innovation of SOEs

Shareholders of different property in SOEs have their target preferences. State-owned controlling shareholders are more concerned about policy tasks, while non-state-owned shareholders emphasize their own interests (Cronqvist & Fahlenbrach, 2009). Due to the discrepancies in interest demands, risk preferences, and information costs of heterogeneous shareholders, when there are multiple shareholders of different property in the enterprise simultaneously, the supervision motivation of a single shareholder is stronger, which helps heterogeneous shareholders restrict and supervise each other in the decision-making process (Bennedsen & Wolfenzon, 2000). Most SOEs that the government fully controls conduct innovation activities based on original products and markets to maintain the current operating conditions. The mixed-ownership reform has brought heterogeneous non-state capital to SOEs. The abundant property rights subjects can reduce the government’s control (Wu & Li, 2005), allowing heterogeneous shareholders to rationally allocate their resources, and incline resources toward exploratory innovation. The higher the degree of mixed-ownership reform, the more dispersed the ownership structure and the higher the level of ownership diversification (B. Zhang et al., 2019). C. D. Liu (2019) pointed out that the entry of non-state-owned shareholders has a certain extent of checks and balances on state-owned shareholders and tends to make collective decisions with the improvement of the diversity of mixed shareholders, to weaken the capital occupation behavior of state-owned controlling shareholders, and provide a capital source for exploratory innovation. In addition, on account of the resource dependence theory, multiple heterogeneous shareholders have brought different resource elements to SOEs. The increase in the diversity of mixed shareholders subjoins the financing channels, provides large amounts of funds for enterprises, and guarantees the development of exploratory innovation activities (Luo et al., 2019). Meanwhile, the introduction of multiple shareholders conveys to investors the good news that the state has policy support for the SOEs’ mixed-ownership reform, which makes it easier for enterprises to obtain external investment. Therefore, the diversity of mixed shareholders can have a positive impact on the exploratory innovation investment.

Given the above analysis, this paper puts forward the following hypothesis:

H1a: The higher the diversity of mixed shareholders, the stronger the promotion effect on SOEs’ exploratory innovation investment.

Although the diversity of mixed shareholders can affect the exploratory innovation, the impact will also vary due to the disparity in the depth of mixed equity. In the case of an imperfect external governance mechanism, the corporate equity controlled by the state or family is highly concentrated; and the ultimate controlling shareholder’s ownership is far higher than its cash-flow right, which is likely to infringe the interests of minority shareholders (Porta et al., 1999). Z. Q. Li et al. (2004) found that the degree of controlling shareholders’ capital occupation is significantly negatively correlated with the proportion of non-state-owned shareholders. The continuous increase in the shares held by non-state-owned shareholders has enabled the simultaneous existence of multiple large shareholders in SOEs, which can effectively restrain the state-owned controlling shareholders’ tunneling behavior, and the decentralized ownership structure can also lessen the supervision costs of other shareholders (Pagano & Röell, 1998). The decrease of the tunneling behavior of state-owned controlling shareholders and the reduction of the supervision cost of non-state-owned shareholders avoid the waste of resources, improve the risk-taking capacity, and enable SOEs to carry out exploratory innovation. Besides, the increase in the proportion of shares held by non-state-owned shareholders has gradually perfected the equity structure of SOEs, which can balance the interests of state-owned and non-state-owned shareholders when making investment decisions, form a reasonable innovation investment plan, and reflect the demands of non-state-owned shareholders in the innovation strategy (Y. Chen et al., 2017). Due to the strict market expenditure control and government marketing behavior regulation of SOEs, a large proportion of state-owned shareholders will negatively impact product innovation. At the same time, non-state-owned enterprises have high enthusiasm for new product development and market expansion (Wu & Li, 2005). Compared with state-owned shareholders, non-state-owned shareholders are more concerned about obtaining stable and lasting competitive advantages (L. F. Ma et al., 2015). Exploratory innovation generally conducts subversive research, and its innovation ability is more prominent, which is more favored by non-state-owned shareholders. Consequently, the heighten in the depth of mixed equity can play a role in the exploratory innovation investment of SOEs.

Based on the above analysis, this paper proposes the following hypothesis:

H1b: The higher the depth of mixed equity, the stronger the promotion effect on SOEs’ exploratory innovation investment.

The implementation of exploratory innovation requires enterprises to master comprehensive market information and accurately predict and identify emerging opportunities (Xiao et al., 2018). The original executives of SOEs are generally directly appointed by the superior government. Guided by the non-market incentive system based on government performance appraisal, they pursue the maximization of political performance within the service period rather than the maximization of enterprise economic benefits in operation (Bennedsen & Wolfenzon, 2000), to evade innovation activities with large uncertainty, long investment recovery cycle, and no obvious profit during their tenure. Richardson (2006) also remarked that for the innovation activities that require executives to pay for a long time, executives can only get a small amount of income according to the regulations. At this time, they will not spend much effort on exploratory innovation. As the undertakers of innovation risks, executives are confronted with the possibility of being dismissed due to innovation failure. They will have aversion to innovation risks for their inherent positions and reputation (Aghion et al., 2013) and select a more conservative innovation strategy. The traits of exploratory innovation technology’s research and development with high uncertainty and inability to be observed in practice also provide intentions for executives to manipulate R&D investment (Sun & Zhang, 2019). Non-state-owned shareholders attach more importance to economic goals (Cai et al., 2018). In the process of mixed-ownership reform, they have the motive to appoint directors to SOEs for their interests, fully participate in the internal governance, obtain sufficient information and discourse power, truly exert their supervisory and governance action, restrain the short-term behavior of SOEs’ management (Y. G. Liu et al., 2016), and provide financial support for exploratory innovation. Moreover, employees of non-state-owned enterprises are more sensitive to market demands and tend to establish long-term and stable cooperative relationships with enterprises through technology research and development (H. M. Choi et al., 2012). Therefore, executives appointed by non-state-owned shareholders can better identify opportunities for exploratory innovation. Meanwhile, as the performers of innovation activities, they make non-state shareholders understand to a large extent the management’s contribution and the risks assumed to innovation activities, lower the probability of the executives being fired, and facilitate them to wage exploratory innovation more actively.

In reliance on the above analysis, this paper suggests the following hypothesis:

H1c: The stronger the control of mixed equity, the more obvious the promotion effect on SOEs’ exploratory innovation investment.

The Mediation Effect of Agency Conflicts

The actual state-owned property rights functions are performed by the managers appointed by the government in SOEs. There is a deviation between the interest demand of managers and the actual property rights subjects. In the absence of a sound incentive and regulatory mechanism, managers may engage in opportunistic behaviors such as perquisite consumption and inefficient investment in the course of business operations, resulting in the first-type agency conflict. On the other hand, since state-owned controlling shareholders occupy a dominant position in the company, they appoint their profit-making relationship personnel to the board. SOEs’ operating decisions are made with the desires of them. They are likely to use their power and information advantages to turn innovation resources into their profit-making tools through tunneling behavior, connected transaction, asset transformation, thus damaging the interests of other shareholders and creating the second-type agency conflict (S. Li et al., 2018). These two types of agency problems decrease the enterprises’ resources through transfer and encroachment and hinder exploratory innovation activities.

After entering the SOEs, the non-state-owned shareholders can participate in the enterprise innovation decisions through exercising the voting rights of the shareholders meeting and the board meeting. Firstly, if non-state shareholders acquire voting rights on the board, they will sustain innovation strategies that conform to their interest preference. Most non-state shareholders are individuals or institutions, concerned about the long-term benefits and investment returns of enterprises. The higher the control of mixed equity, the more likely it is to form a supervision mechanism and availably ameliorate the resource efficiency loss caused by SOEs’ supervision invalidation. The improvement of the discourse power of non-state-owned shareholders in the board has strengthened the SOEs’ internal governance mechanism. It establishes reasonable incentive and restraint mechanisms such as manager’s compensation incentives (Hao & Gong, 2017), inhibits the manager’s opportunistic behavior and moral hazard from obtaining hidden welfares, reduces the first-type agency cost (Li & Li, 2022), and provides abundant free cash flow for exploratory innovation. Secondly, with the augment of the diversity of mixed shareholders, there are multiple heterogeneous shareholders in the SOEs, and the supervisory effect among shareholders has enhanced. Most SOEs adhere to the voting principle of “one-share, one-vote.” The shareholding ratio of non-state-owned shareholders represents their power in the shareholders meeting. The enlargement in the depth of mixed equity enables non-state shareholders to influence the decision-making of the shareholders meeting. It raises the cost of embezzlement, avoids connected transactions and other phenomena that alter the fund uses of innovation investment, subsides the second-type agency cost owing to the benefit expropriation (Zhu et al., 2019), and offers opportunities for the occurrence of exploratory innovation. This paper argues that the mixed-ownership reform in the dimension of control rights allocation plays a role by weakening the first-type agency conflict, and in the ownership structure dimension is through declining the second-type agency conflict.

In the light of the above analysis, this paper forms the following hypotheses:

H2a: The first-type agency conflict plays a mediation effect in the relationship between the control of mixed equity and exploratory innovation investment.

H2b: The second-type agency conflict plays a mediation effect in the relationship between the diversity of mixed shareholders, the depth of mixed equity, and exploratory innovation investment.

The Mediation Effect of Financing Constraints

Insufficient financing is an important factor restricting innovation (Hottenrott & Peters, 2012). Although SOEs are supported by national policies and can more easily gain funds from state-owned banks, the financing channels of SOEs are relatively simple (Luo et al., 2019), which limits the resource acquisition of exploratory innovation. The augment of heterogeneous shareholder categories enriches the resource support available to SOEs, which is reflected in the diversity of mixed shareholders adding the enterprise financing channels. SOEs introduce four types of non-state-owned shareholders by issuing new shares and acquire their original financing channels, to furnish capitals for the enterprise exploratory innovation. The non-state-owned shareholders’ shareholding is equivalent to bringing equity financing for the SOEs. The increase in their shareholding ratio means that they have bought more SOEs’ shares, and SOEs have obtained more equity financing. In addition, owing to its high complexity and risk (Danneels, 2002), exploratory innovation involves too many core technical secrets in the process of sustained development of new products, so enterprises tend to hide relevant information and subject them to stricter external financing constraints. The strengthening of the funding sources of SOEs will have a more obvious boost to them. The control of mixed equity mainly affects the internal governance structure through participation in operating decisions, has no substantial impact on external financing modes, and cannot directly act on the SOEs’ financing ability. This paper considers that the mixed-ownership reform in the dimension of ownership structure plays a role through financing constraints. That is to say, the diversity of mixed shareholders and the depth of mixed equity urge enterprises to ease their financing constraints by broadening financing channels and heightening financing levels, which further stimulate variations in exploratory innovation investment.

According to the above analysis, this paper proposes the following hypothesis:

H3: The financing constraints play a mediation effect in the relationship between the diversity of mixed shareholders, the depth of mixed equity and exploratory innovation investment.

Research Design

Sample Selection and Data Sources

In order to select state-owned listed companies of different scales as sample observations in different years during the investigation period, we use the unbalanced panel data of state-owned listed companies from 2013 to 2018 to explore the impact of mixed-ownership reform on exploratory innovation. Considering that there is a certain time lag in the governance effect of non-state shareholders on exploratory innovation, the sample interval of the explained variable is forwarded by one-period from 2014 to 2018, and explanatory variables and control variables are the current period from 2013 to 2017. In line with the demands of the research problem, the sample selection procedure is as follows: (1) Excluding ST, *ST, financial listed companies; (2) Sample observations with negative or greater than 100% financial leverage ratio are removed; (3) Eliminating firms with missing financial characteristics. After the above sample screening, 4,530 firm-year observations are finally retained. In addition, as there are new listed or withdrawn SOEs every year, the sample of eligible state-owned listed companies is not exactly the same from year to year. There were 876 samples in 2013, 887 samples in 2014, 896 samples in 2015, 920 samples in 2016, and 951 samples in 2017.

The basic data of mixed-ownership reform is mainly obtained by querying the annual reports and related information websites of state-owned listed companies. Other financial data and special company indicators are mainly from the CSMAR database. The industry classification comes from the WIND database. Data processing and empirical testing are completed through the software of STATA.14.0. All continuous variables are winsorized at 1% and 99% quantiles to eliminate the influence of outliers.

Variable Definition and Model Construction

This paper draws on the practice of Sun and Zhang (2019) to construct the following regression model to be tested:

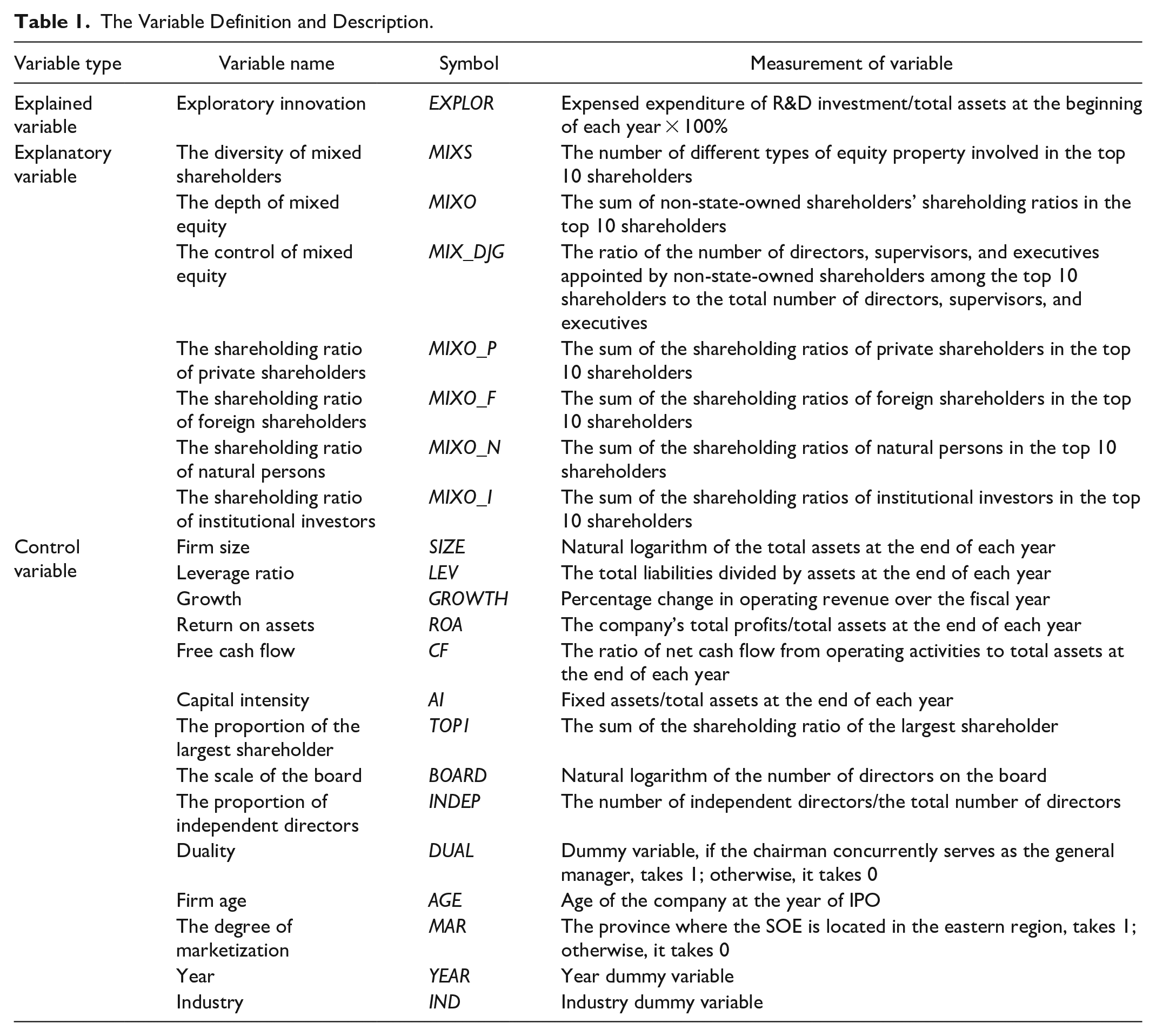

Where i and t represent the firm and year, and ε is the random error term of the regression model. Explained variable EXPLORi,t + 1 delegates the exploratory innovation investment of firm i in year t + 1. The explanatory variable MIX is the degree of SOEs’ mixed-ownership reform. The specific construction method of each index is shown below.

The explained variable is the exploratory innovation, EXPLOR. According to the classification of intangible assets in the “Accounting Standards for Business Enterprises No. 6-Intangible Assets,” the R&D investment of enterprises is divided into two stages: research and development. The research and development expenditures in the research phase are expensed, and in the development phase are capitalized. Exploratory innovation aims to implement basic research and development to produce subversive revolutions. The investment in the research phase has higher risks and uncertainties than that in the development phase, and it is more inclined to exploratory expenditure. Thence, in reference to the research of Bi et al. (2017), this paper measures exploratory innovation with the ratio of the expensed expenditure of R&D investment to the total assets at the beginning of the year.

The explanatory variable is the degree of SOEs’ mixed-ownership reform, MIX. Non-state-owned shareholders exert substantial influence on the operating decisions by acquiring equity and appointing personnel to participate in the governance of SOEs. In terms of ownership structure adjustment, considering the number and shareholding proportion of heterogeneous shareholders among the top 10 shareholders of SOEs, the following two indicators are constructed: The diversity of mixed shareholders (MIXS), the number of different types of equity property involved in the top 10 shareholders (L. F. Ma et al., 2015). When there is only one type of shareholder among the top 10 shareholders, MIXS takes a value of 1, and when there are two types of shareholders, the value is 2. By analogy, when there are five different types of shareholders, the value is 5. The depth of mixed equity (MIXO), the sum of non-state-owned shareholders’ shareholding ratios in the top 10 shareholders (Liang et al., 2020). For control rights allocation, since the appointment of personnel to supervise and vote can better reflect the governance role of non-state-owned shareholders, referring to the practice of Cai et al. (2018), the ratio of the number of directors, supervisors, and executives appointed by non-state-owned shareholders among the top 10 shareholders to the total number of directors, supervisors, and executives is used to measure the control of mixed equity (MIX_DJG). Moreover, this paper also sums up the shares held by each type of non-state-owned shareholders among the top 10 shareholders (Lu & Jiang, 2018). It analyzes the distinctions in the impact of each type of shareholder’s shareholding ratio on the exploratory innovation of SOEs. Based on existing research (Porta et al., 1999; X. Q. Yang & Yin, 2018), we divide the property of heterogeneous shareholders into six types: state-owned, private, foreign, natural persons, institutional investors, and others. The number and shareholding ratio of other shareholders are very few, which are not the research objects of this paper.

To control for many factors that may potentially affect enterprises’ exploratory innovation, we selected firm-level and governance-level controls in our study, including: firm size (SIZE), leverage ratio (LEV), growth (GROWTH), return on assets (ROA), free cash flow (CF), capital intensity (AI), the proportion of the largest shareholder (TOP1), the scale of the board (BOARD), and the proportion of independent directors (INDEP), duality (DUAL), firm age (AGE), and the degree of marketization(MAR). Meanwhile, this paper also sets up the year (YEAR) and industry (IND) dummy variables, the definition, and description of the variables are shown in Table 1:

The Variable Definition and Description.

Results and Discussion

Summary Statistics

Table 2 reports the results of the summary statistics of the main variables. The mean value of exploratory innovation investment in total assets (EXPLOR) is 0.011, and the standard deviation is 0.016, indicating that the proportion of exploratory innovation investment in SOEs is relatively low, and there is a large gap among SOEs. The intensity of enterprises’ exploratory innovation activities is uneven. The mean value of mixed shareholder diversity (MIXS) is 2.921, and there are three types of heterogeneous shareholders in SOEs. The mean value of mixed equity depth (MIXO) is 0.114, manifesting that the average share participation ratio of non-state-owned shareholders is 11.4%. The mean value of mixed equity control (MIX_DJG) is 0.021, showing that the average number of directors, supervisors, and executives appointed by non-state-owned shareholders accounts for 2.1% of the total number of directors, supervisors, and executives. It can be seen that although the mixed-ownership reform has achieved initial results, the discourse power of non-state-owned shareholders needs to be further enhanced. The mean value of private shareholder’s shareholding ratio (MIXO_P) is 0.028, the standard deviation is 0.064. The mean value of foreign shareholder’s shareholding ratio (MIXO_F) is 0.025, the standard deviation is 0.073. The mean value of natural person shareholders’ shareholding ratio (MIXO_N) is 0.020, the standard deviation is 0.036. The mean value of institutional investors shareholders’ shareholding ratio (MIXO_I) is 0.039, the standard deviation is 0.042. It is observed that heterogeneous non-state-owned capital has a certain shareholder power in SOEs at present. However, the shareholding ratio is not high enough, and the degree of mixed-ownership reform still has great room for improvement.

Summary Statistics of Main Variables.

Correlation Analysis

Table 3 lists the results of the correlation analysis between the main variables. We find that the diversity of mixed shareholders (MIXS) and exploratory innovation investment (EXPLOR) are positively correlated but not significantly. The depth of mixed equity (MIXO) and the control of mixed equity (MIX_DJG) and exploratory innovation investment (EXPLOR) have a significant positive correlation. The above results preliminarily state that the mixed-ownership reform of SOEs may impact exploratory innovation. Still, the specific impact degree and path need to be further verified. For control variables, growth (GROWTH), return on assets (ROA), and exploratory innovation (EXPLOR) are significantly positively correlated. Firm size (SIZE), leverage ratio (LEV), capital intensity (AI), the proportion of the largest shareholder (TOP1), the scale of the board (BOARD), firm age (AGE), the degree of marketization (MAR) are negatively correlated with exploratory innovation (EXPLOR). Moreover, the correlation coefficients between the variables are all less than 0.6, and there is no multicollinearity problem in equation (1).

Correlation Analysis of Main Variables.

Note. *, **, and *** designate statistical significance at the 10%, 5%, and 1% level, respectively.

The Baseline Results of Mixed-Ownership Reform and Exploratory Innovation of SOEs

Table 4 presents the regression results of the impact of mixed-ownership reform on exploratory innovation of SOEs. There is a significant positive correlation between the diversity of mixed shareholders (MIXS) and exploratory innovation investment (EXPLOR) (α = 0.074, p < 0.01), indicating that the more types of heterogeneous shareholders introduced by SOEs’ mixed-ownership reform, the higher the level of exploratory innovation investment. The depth of mixed equity (MIXO) and exploratory innovation investment (EXPLOR) are significantly positively correlated (α = 0.577, p < 0.01). It demonstrates that the higher the proportion of shares held by non-state-owned shareholders, the more inclined SOEs in mixed-ownership reform are to increase exploratory innovation investment. The control of mixed equity (MIX_DJG) has a significant positive correlation with exploratory innovation investment (α = 2.202, p < 0.01). It declares that the higher the proportion of directors, supervisors, and executives appointed by non-state-owned shareholders, the stronger the positive impact on exploratory innovation. Hypothesis 1a, 1b, and 1c pass the verification. These findings extend earlier findings which shows that the mixed-ownership reform positively influences innovation investment (Cheng & Chen, 2021; C. Y. Wang et al., 2020; X. Q. Zhang et al., 2020). We refine the impact of mixed-ownership reform on innovation investment decisions to the allocation of resources among innovation activities, indicating that mixed-ownership reform of SOEs tends to increase investment in exploratory activities, which is helpful to drive the basic innovation development of enterprises.

Regression Results of the Impact of Mixed-Ownership Reform on Exploratory Innovation of SOEs.

Note. The t-statistics are reported in parentheses.

, **, and *** designate statistical significance at the 10%, 5%, and 1% level, respectively.

Table 5 further dissects the disparate impact of each type of shareholder’s shareholding ratio on exploratory innovation. Column (1) shows that the relationship between private shareholder’s shareholding ratio and exploratory innovation investment is not significant (α = −0.962, p > 0.1). Column (2) reveals that the foreign shareholder’s shareholding ratio is significantly positively correlated with exploratory innovation investment (α = 0.830, p < 0.01). Column (3) displays that the natural person shareholder’s shareholding ratio is significantly positively correlated with the exploratory innovation investment (α = 1.273, p < 0.05). Column (4) shows that there is a significant positive correlation between institutional investors shareholder’s shareholding ratio and SOEs’ exploratory innovation (α = 1.295, p < 0.05). The reasons for the consequences are as follows: First, the equity of private shareholders has not reached their expectations, which unable to produce effective restrictions on state-owned shareholders, so it does not have a substantive effect on the exploratory innovation of SOEs. Second, the entry of foreign shareholders brings the advantages of knowledge, technology, management experience, etc., for enterprises. They have higher innovation consciousness and ability, which furnishes conditions for the development of exploratory innovation activities. Third, the natural persons in the top 10 shareholders join the SOEs as owners. To aggrandize their wealth, they maximize the enterprise’s economic benefits as the operation objective and prefer exploratory innovation that can bring excess returns. Last, institutional investors exert an effective supervisory effect on state-owned controlling shareholders, lessen the embezzlement behavior of major shareholders to promote exploratory innovation.

Regression Results of the Impact of Heterogeneous Shareholders’ Shareholding Ratio on Exploratory Innovation of SOEs.

Note. . The t-statistics are reported in parentheses.

, **, and *** designate statistical significance at the 10%, 5%, and 1% level, respectively.

Mediation Effect Test Results

This paper constructs a mediation effect model from agency conflicts and financing constraints to further examine the specific path of the impact of the mixed-ownership reform on exploratory innovation in the two dimensions of ownership structure adjustment and control rights allocation. It discusses how the mixed-ownership reform affects exploratory innovation. Based on the practice of Wen et al. (2004), this paper is mainly divided into three steps for analysis. The first step is to explore the impact of mixed-ownership reform on exploratory innovation investment, verified by the above equation (1). The second step is to explore the impact of mixed-ownership reform on mediators, verified by equations (2) and (4). The third step is to explore the impact of mixed-ownership reform on exploratory innovation investment after adding mediators, verified by equations (3) and (5).

Mechanism test of agency conflicts

In SOEs, there are dual agency problems between shareholders and managers and between state-owned controlling shareholders and non-state shareholders. Through supervision and restriction, the non-state-owned shareholders and their appointed directors, supervisors and executives can reduce the two types of agency costs and provide capital flow for exploratory innovation. Therefore, the two dimensions of the SOEs’ mixed-ownership reform will affect the exploratory innovation investment by intervening in different agency conflicts. Equation (2) represents the impact of the mixed-ownership reform on the two types of agency costs, and equation (3) is the impact of the mixed-ownership reform on exploratory innovation while controlling the agency costs.

According to the research of Hong and Yuan (2019), the first-type agency cost (AGENCY_1) is measured by the proportion of administrative expenses to operating income. The second-type agency cost (AGENCY_2) draws on the study of G. Jiang et al. (2010) and K. J. Chen (2019), and uses the proportion of other receivables in total assets to measure.

Table 6 lists the regression results of agency conflicts mechanism test. Among them, panel A analyzes the mediation effect of the first-type agency cost. The results reveal that the diversity of mixed shareholders and the depth of mixed equity are not related to the first-type agency cost, illustrating that the mixed-ownership reform in the dimension of ownership structure adjustment cannot significantly alleviate the first-type agency conflict to heighten the exploratory innovation investment. And the mediation effect of the first-type agency cost does not exist. There is a significant negative correlation between the control of mixed equity and the first-type agency cost. After adding the first-type agency cost, the control of mixed equity is still significantly positively correlated with exploratory innovation. The regression coefficient is decreased from 2.202 to 2.156, which explains that the first-type agency cost plays a partial mediation in the dimension of control rights allocation. Hypothesis 2a passes the verification. These findings are inconsistent with the previous research findings (Feng et al., 2021) that non-state shareholders appoint directors to improve innovation investment by alleviating the second-type agency cost. It shows that non-state-owned shareholders have actual control rights to supervise and restrain managers more effectively, which makes the R&D investment of SOEs inclined to exploratory innovation.

Regression Results of Agency Conflicts Mechanism Test.

Note. The t-statistics are reported in parentheses.

, **, and *** designate statistical significance at the 10%, 5%, and 1% level, respectively.

Panel B inquires into the mediation effect of the second-type agency cost. The results demonstrate that the diversity of mixed shareholders and the depth of mixed equity are negatively correlated with the second-type agency cost. Under the control of the second-type agency cost, the diversity of mixed shareholders and the depth of mixed equity still have significant positive correlations with exploratory innovation. The regression coefficients are dropped from 0.074 and 0.577 to 0.069 and 0.528, manifesting that the second-type agency cost plays a partial mediation role in the dimension of ownership structure adjustment. The control of mixed equity has no significant correlation with the second-type agency cost, which means that the mixed-ownership reform in the dimension of control rights allocation cannot elevate the exploratory innovation investment by mitigating the second-type agency conflict. Now the mediation effect of second-type agency cost does not exist, and hypothesis 2b passes the verification. These findings enrich previous findings (Y. J. Yang et al., 2020), which explore how mixed-ownership reform in different dimensions act on exploratory innovation by alleviating different agency problems.

Mechanism test of financing constraints

There is a relatively single financing method in SOEs, which is very restrictive for exploratory innovation that requires a large number of funds. The increase in the types and proportion of non-state-owned shareholders can significantly ease financing constraints and maintain a loose capital stock within SOEs to cope with the exploratory innovation. Therefore, the mixed-ownership reform may act on exploratory innovation investment through financing constraint paths. Equation (4) represents the influence of mixed-ownership reform on financing constraints, and equation (5) is the influence of mixed-ownership reform on exploratory innovation while controlling financing constraints.

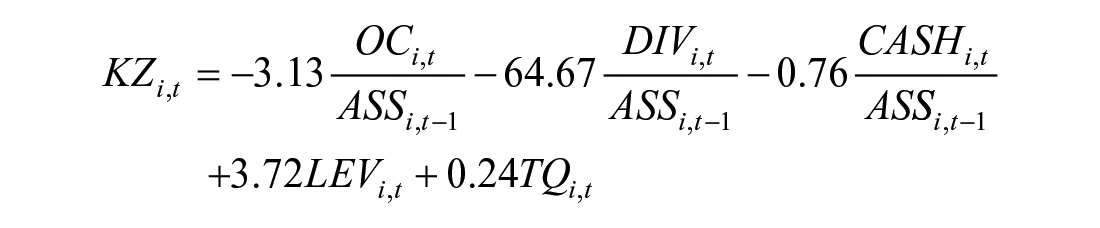

Financing constraint (KZ), referring to the research of Kaplan and Zingales (1997) and Lamont et al. (2001), takes China’s state-owned listed companies as samples to construct the corresponding financing constraint model:

OC stands for net cash flow from operating activities, DIV stands for total cash dividends, CASH stands for total monetary funds, LEV stands for asset-liability ratio, TQ stands for Tobin’s Q value, and ASS stands for total assets. The KZ index of the degree of financing constraints of each listed state-owned enterprise can be calculated from this model. The larger the KZ index, the higher the financing constraints of SOEs.

Table 7 lists the regression results of financing constraints mechanism test. It can be seen that the diversity of mixed shareholders and the depth of mixed equity have significant negative correlations with financing constraints. There have the same results while controlling the financing constraints, the regression coefficients decrease from 0.074 and 0.577 to 0.072 and 0.559, which indicates that financing constraints have a partial mediation in the relationship between the SOEs’ mixed-ownership reform and exploratory innovation investment in the dimension of ownership structure adjustment. There is no significant correlation between the control of mixed equity and financing constraints, which claims that the mixed-ownership reform in the dimension of control rights allocation cannot affect exploratory innovation investment by easing the financing constraints. In this case, the mediation effect of financing constraints does not exist, and hypothesis 3 is verified. These findings are contrary to the early findings that the increase of non-state-owned shareholders’ shareholding will improve the financing constraint level of SOEs (L. Y. Chen et al., 2021). It declares that the participation of non-state-owned shareholders widens the enterprises financing channels, which provides research results from different viewpoints.

Regression Results of Financing Constraints Mechanism Test.

Note. The t-statistics are reported in parentheses.

, **, and *** designate statistical significance at the 10%, 5%, and 1% level, respectively.

Robustness Test

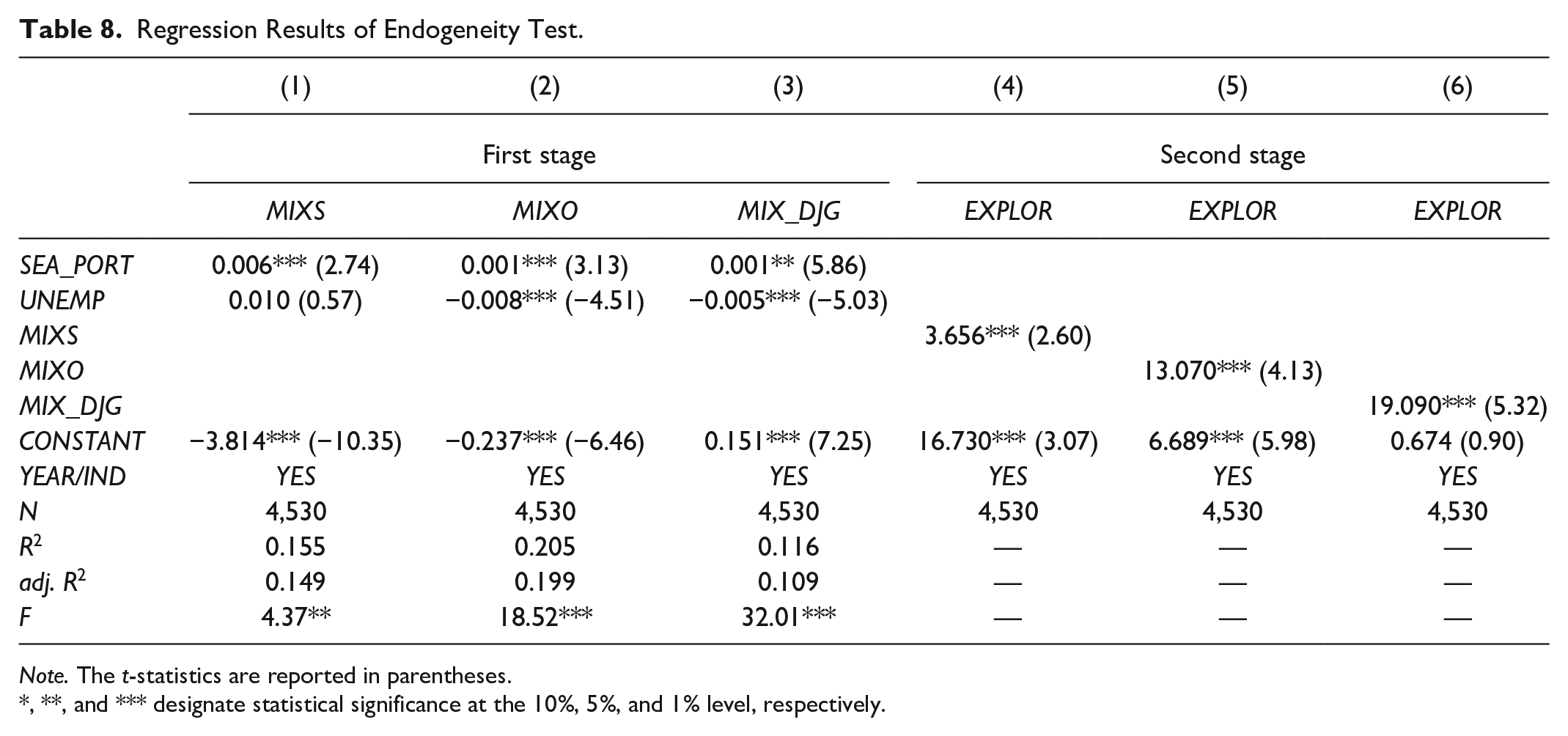

Endogenous Test

Since there may be some unobservable factors in equation (1) that affect the degree of SOEs’ mixed-ownership reform and exploratory innovation investment at the same time, resulting in endogenous problems caused by omitted variables. Therefore, this paper consults with the research of Fan et al. (2013) and Tang et al. (2020), and selects the number of coastal ports (SEA_PORT) and the unemployment rates (UNEMP) in each province as the instrumental variables of the degree of SOEs’ mixed-ownership reform, and uses the two-stage least square method (IV-2SLS) for regression. Since exploratory innovation activities are the operating decisions of SOEs, the number of coastal ports and unemployment rates in each province will not directly affect them, which conforms to the exogenous standard of instrumental variables. Table 8 describes the research results of two-stage regression, and further confirms that the improvement of the diversity of mixed shareholders, the depth of mixed equity, and the control of mixed equity can promote the exploratory innovation investment under the control of endogenous problems.

Regression Results of Endogeneity Test.

Note. The t-statistics are reported in parentheses.

, **, and *** designate statistical significance at the 10%, 5%, and 1% level, respectively.

Other Robustness Tests

For ensuring the robustness of the main regression conclusion, this paper adopts three methods of the robustness test: replacing the exploratory innovation measurement index, replacing the degree of SOEs’ mixed-ownership reform measurement index and changing the regression model.

Alternative measurement index of the exploratory innovation

For exploratory innovation, this paper standardizes expensed expenditure of R&D investment using the operating income of the previous period (EXPLOR1) (Sun & Zhang, 2019). The test findings are exhibited in columns (1) to (3) of Table 9. Moreover, considering innovation output, we use the natural logarithm of the number of invention patent applications in period t + 1 plus 1 to measure exploratory innovation (EXPLOR2) (Xiong et al., 2021). The results are shown in columns (4) to (6) of Table 9. The diversity of mixed shareholders (MIXS), the depth of mixed equity (MIXO), and the control of mixed equity (MIX_DJG) are significantly positively correlated with exploratory innovation (EXPLOR1/EXPLOR2) under the two alternative methods, and the consequences are consistent with the previous above.

Regression Results of Other Robustness Test.

Note. The t-statistics are reported in parentheses.

, **, and *** designate statistical significance at the 10%, 5%, and 1% level, respectively.

Alternative measurement index of the degree of SOEs’ mixed-ownership reform

To exclude the influence of indicator selection on the research conclusions, after replacing the measurement index of the explained variable, we also replace the explanatory variable. Regarding the research of Lu and Jiang (2018), this paper uses the Herfindahl index of shareholder categories (

Alternative regression model

Exploratory innovation is non-negative and continuous value censored variable, which has zero censoring problem. Therefore, using the method of X. Y. Jiang (2016) for reference, the Tobit model is applied for estimation. The regression results are shown in columns (10) to (12) of Table 9. The diversity of mixed shareholders (MIXS), the depth of mixed equity (MIXO), and the control of mixed equity (MIX_DJG) have significant positive correlations with exploratory innovation (EXPLOR), and the results are consistent with the previous one.

Conclusions

This study investigates how mixed-ownership reform affects exploratory innovation using an unbalanced panel data of state-owned listed companies from 2013 to 2018. The following empirical results are found: (1) The mixed-ownership reform will indeed affect the exploratory innovation, which is reflected in the diversity of mixed shareholders, the depth of mixed equity and the control of mixed equity have a significant promotion effect on the exploratory innovation investment. What’s more, the control of mixed equity has a stronger driving function, indicating that the mixed-ownership reform, which is carried out in-depth to the control right level, has a more obvious governance effect on improving enterprise independent innovation ability and is conducive to realizing China’s innovation-driven development. (2) There are differences in the impact of heterogeneous non-state-owned shareholders’ shareholding ratio on exploratory innovation. The augment in the proportion of shares held by foreign shareholders, natural person shareholders, and institutional investor shareholders enhance the exploratory innovation investment of SOEs. In contrast, the private shareholders who fail to reach their expected shareholding level have no impact on exploratory innovation. (3) The two dimensions of the SOEs’ mixed-ownership reform act on exploratory innovation through disparate routes. The mixed-ownership reform in the dimension of ownership structure plays a pivotal role in exploratory innovation by restraining the tunneling behavior of state-owned controlling shareholders and alleviating financing constraints. While in the dimension of control rights it impacts the exploratory innovation through the formation of supervision function on management.

According to the above research conclusions, the following suggestions are put forward to heighten the exploratory innovation investment level and speed up the marketization process of SOEs. First, considering the “breadth” and “depth” of the SOEs’ mixed-ownership reform, we should introduce diversified non-state-owned strategic investors and ensure that their shareholding attains a certain depth, so as to give full play to the unique advantages of non-state-owned shareholders and release the enterprise innovation resources. Second, establish a supporting guarantee system for non-state shareholders to appoint directors, give them the right to nominate and appoint directors, supervisors, and executives, drill the SOEs’ mixed-ownership reform into the control right level, and protect the discourse power of non-state shareholders in innovation decisions. Third, SOEs with mixed-ownership reform needs to consummate the governance and incentive mechanism, perfect the fault-tolerant system of managers for innovation failure, reduce restrictions on profit distribution, attract the active entry of non-state-owned strategic investors, then weaken the agency conflicts and financing constraints, and afford funds safeguard for the SOEs’ exploratory innovation.

Our conclusions have two important theoretical and practical implications. Firstly, in a theoretical sense, this study deepens the mixed-ownership reform of SOEs to the actual control rights level, discusses the impact of non-state-owned shareholder governance on exploratory innovation investment, and reveals multiple possible paths between them, which has a certain reference value for constructing the research framework between mixed-ownership reform and exploratory innovation. Secondly, in a practical sense, the conclusions of this paper show that the implementation of mixed-ownership reform has optimized the allocation of innovation resources of SOEs. It provides practical guidance for deepening the mixed-ownership reform, improving the internal governance mechanism, and leading state-owned listed companies to actively carry out exploratory innovation activities.

Although this study expands the literature and draws relatively reliable conclusions, there are still some limitations to be improved. In terms of index measurement, the paper uses expensed expenditure of R&D investment to measure exploratory innovation from a financial perspective, which provides convenience for data acquisition. However, this method is difficult to more accurately reflect the overview of exploratory innovation and further subdivide exploratory innovation. In the future, we can consider taking the big data method of information mining to measure exploratory innovation and its subdivision types, so as to enhance the accuracy and comprehensiveness of measurement. In terms of sample selection, we focus on the empirical analysis of large samples and obtain regular statistical results, but it is unable to further analyze the internal logic of the mixed-ownership reform affecting the exploratory innovation. In the future research, we can concentrate on the typical SOEs implementing mixed-ownership reform, obtain first-hand data based on field investigation, interview, and other methods, and dissect the formation process of the innovation behaviors of this single enterprise.

Footnotes

Acknowledgements

We wish to thank the editor and anonymous referees for valuable comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by the major research project of humanities and social science research of Hebei education department (grant number ZD201904).

Ethics statement

Not applicable.