Abstract

The mixed ownership reform of China is a kind of further partial privatization for the listed state-owned enterprises (SOEs), and an opportunity for non-state-owned enterprises (non-SOEs) to expand their commerce boundaries. The purpose of this paper is to investigate the effect of heterogeneous blockholders on corporate innovation. Spanning the analysis with listed companies in China from 2007 to 2017, we find that heterogeneous blockholders have a significant positive effect on enterprise innovation. Lowering agency costs and improving corporate innovation efficiency are the two plausible mechanisms. From further research, we find that compared with non-SOEs, the positive effect of heterogeneous blockholders on enterprise innovation is more pronounced for SOEs, and the effect is more positive with the improvement of relative power balance between heterogeneous blockholders. The paper sheds light on the innovation effects of mixed-ownership reform in emerging and transitioning countries.

Keywords

Introduction

Equity structure is the foundation of the survival and development of an enterprise, and is also an extremely important governance mechanism, which is the core issue of China’s mixed-ownership reform. Researchers have concentrated attention on corporate governance, with a particular emphasis on the conflict between employed managers and dispersed shareholders (Morck et al., 1988). However, La Porta et al. (1999) point out that large shareholders are widespread around the world. Scholars have carried out lots of studies on the governance of large shareholders from different perspectives (Cai et al., 2015), Maury and Pajuste (2005) investigate the effects of multiple blockhoders on firm value, and Jiang et al. (2020) find firms with multiple blockholders usually have higher earnings management than others.

The mixed ownership reform of China is a kind of further partial privatization for the listed SOEs, and an opportunity for non-SOEs to expand commerce boundaries. The reform was formally proposed in 2013 in order to improve corporate governance and enhance the efficiency and competitiveness of SOEs (Guan et al., 2021; Xia et al., 2022). Simply changing the diversity of ownership structure can’t significantly affect the corporate governance (Xia et al., 2022), so the key to the reform lies in exploring the effective arrangement of a company’s equity structure among the different natures of property rights of large blockholders. In the paper, different natures of property rights refer to a company with state-owned and private property rights at the same time. In China, state-owned property right and private property right are located at both ends of the property right pedigree and are important components of listed companies. Each of the property rights has its unique advantages, but they have been considered separated artificially for a long time.

The mixed-ownership reform should focus not only on the formal mixing but also on the effective allocation and integration of different types of property rights. Most of the prior studies focus on the forms mixture of different property rights, Li et al. (2022) and Shang et al. (2022) find mixed-ownership reform can significantly restrain excessive perquisite consumption by executives. But the core of the reform is the rational allocation of heterogeneous property rights, which has remained untouched. The effective allocation of heterogeneous property rights means that large blockholders with different property rights can actively perform the functions of corporate governance (Guan et al., 2021), and Zhang et al. (2020) and Yuan et al. (2022) find the reform will improve SOE’s innovation, especially exploratory innovation of SOEs. The reform is continuing to advance from 2013 till now, and the effect should be fully tested.

It has been documented that blockholders are a common global phenomenon that has both positive and negative influences on corporate governance (La Porta et al., 1999). To overcome the defects of one single large blockholder, multiple large blockholders are the typical solution. The positive effect on corporate governance of multiple large blockholders has been argued by many scholars (Claessens et al., 2000; Shleifer & Vishny, 1997). According to the Company Law of the People’s Republic of China, shareholders with a stake of 10% or more can recommend directors and executives and has the right to propose an interim shareholders’ meeting. Hence, blockholders are important in corporate governance. However, the existing researches only pay attention to the number of large blockholders and the shareholding ratio, rather than to the governance effects of different property natures of large blockholders with 10% or more of the shares (Edmans, 2014).

Technological innovation is the most crucial driver of a country’s economic growth or a company’s value improvement (Porter, 1992). Studies on factors of enterprise innovation and the impact of equity structure on enterprise innovation are numerous (Gu et al., 2020; Kang et al., 2019; Z. W. Wang et al., 2022). In recent years, some new factors are focused on by literature, such as managerial ability (Salehi et al., 2018), supplier change (Zu & Zhang, 2022), digital economy (Li et al., 2022), executive shareholding (T. Wang &Cheng, 2022), intellectual and social capital (Salehi, Fahimi, et al., 2022), and top management team stability (Cao & Yu, 2023). Salehi, Ammar Ajel, and Zimon (2022) point that the expertise of the board and audit committee have a positive correlation with financial reporting transparency; Salehi and Alkhyyoon (2022) find there is a positive relationship among managerial entrenchment, social responsibility disclosure, and social responsibility growth; These will improve enterprise innovation. However, the effect of multiple large blockholders on enterprise innovation is under investigation. Occasionally, when scholars focus on heterogeneous blockholders, the ten large shareholders are usually selected, rather than the actual shareholding ratio as the basis for measuring the large shareholders. Hence, will heterogeneous blockholders with a share of 10% or more impact on enterprise innovation? Heterogeneous blockholders mean the coexistence of large state-owned blockholders and large private blockholders. It is interesting for us to study the influence of heterogeneous blockholders on enterprise innovation.

This study has implications for emerging countries and contributes to the existing literature in four ways. First, we study the influence of heterogeneous blockholders on enterprise innovation. Compared with equity balances, heterogeneous blockholders can both supervise and conspire with each other, and blockholders are active participants in corporate governance rather than hitchhikers. We find that heterogeneous blockholders have a significant positive effect on enterprise innovation. The study extends the prior research by focusing on heterogeneous blockholders rather than blockholders. Second, the influence of heterogeneous blockholders on enterprise innovation is a new perspective. Mixed-ownership reform is one of China’s important development strategies, and innovation is the key to measuring the quality of the reform. It is of significant value to study the relationship between heterogeneous blockholders and enterprise innovation. Third, we study the path of heterogeneous blockholders on enterprise innovation. It is found heterogeneous blockholders will reduce the tunneling occupation, obtain more financial subsidies, improve the efficiency of enterprise innovation, and so on, thus promoting enterprise innovation. The study supports the theory of corporate governance and the theory of resource dependence. Finally, this paper confirms the effectiveness of mixed-ownership reform and points out that equity structure arrangements with heterogeneous blockholders are the effective path of the reform. The study enhances our understanding of the mixed ownership reform and the heterogeneous blockholders which with different nature on property rights.

The rest of the paper is organized as follows. Section 2 discusses the related literature and hypotheses development. Section 3 presents the data and research design. Section 4 examines the influence of heterogeneous blockholders on enterprise innovation, and tests the path of heterogeneous blockholders on enterprise innovation. Section 5 is the robustness tests. Section 6 is the conclusions, implications, and limitations.

Relation to Existing Literature and Hypotheses Development

The first agency cost problem mainly focuses on the conflict of interest between shareholders and managers, while the second agency cost problem focuses on the encroachment of large shareholders on the interests of small and medium-sized shareholders. In the early days, scholars mainly focused on the former. In the late 1990s, research found that the latter was the most important issue in corporate governance (Shleifer & Vishny, 1997), especially for emerging countries. When the equity structure is highly concentrated, the controlling shareholder tends to encroach on the interests of other shareholders (Shleifer & Vishny, 1997). The coexistence of blockholders would inhibit the disadvantages associated with one single large blockholder. Large blockholders have the will and ability to participate in corporate governance (Shleifer & Vishny, 1997). Multiple large blockholders can supervise the behavior of controlling shareholders and reduce tunneling behavior. By the voting power, or exit threat, etc., large shareholders other than the controlling shareholder can participate in corporate governance (Edmans, 2009), which would reduce earnings management (Aharony et al., 2010), increase investment efficiency (Jiang et al., 2018), enhance risk-bearing level (Boubaker et al., 2016), reduce financing costs, enhance social responsibility (F. Cao et al., 2019), and increase the enterprise value (Maury & Pajuste, 2005).

However, empirical literature shows that there may be collusive behavior among multiple large blockholders, thus aggravating the encroachment on the interests of other shareholders (Maury & Pajuste, 2005). But collusion behavior requires certain conditions, Maury and Pajuste (2005) find when multiple blockholders are family-owned enterprises, collusion between each other can be more easily achieved; Cheng et al. (2013) point out that when there is a conspiracy plan among multiple blockholders, it is easier for blockholders to conspire. In addition, multiple blockholders may lower efficiency and reduce their supervisory capabilities (Fang et al., 2018), thereby exacerbating the agent problems.

According to the existing studies, the active supervision effect and collusion effect of multiple blockholders coexist. Why are there different views on the governance effects of multiple blockholders? Jiang et al. (2019) point out that the reason may be derived from the differences in ownership systems under varying institutional backgrounds. Though the literature about multiple large blockholders is numerous, there is a lack of literature on heterogeneous blockholders. And when the difference like property rights of large blockholders are ignored, the real effect of the mixed-ownership reform cannot be truly tested. The mixed-ownership reform should form effective balances among large blockholders and realize the true mixing of heterogeneous property rights, thus the mixing of heterogeneous shareholders can achieve complementary advantages and make up for the lack of marketization. The existence of heterogeneous blockholders will affect enterprises’ innovation, and the reasons are outlined in the following.

First, heterogeneous blockholders can affect the company’s decision-making and management strategy. Enterprise innovation relates to business decisions, strategies, operations, and innovation decision-making depends on the decision of senior executives. Firstly, blockholder has the right to propose candidates for director board and senior executives. By supervising the behavior of the senior executives, blockholder can affect the company’s strategy, including its innovation strategy (Xu et al., 2021). Secondly, through the exit threat, blockholder may not only increase the possibility of the senior executive being forced to change but also increase the possibility of a company being acquired (Parrino et al., 2003). Finally, a large blockholder is more interested in projects that can bring long-term benefits to the company, so he will actively support the company’s innovation strategy (Hill & Snell, 1988). Thus, it can influence the company’s decision-making, and innovation strategy is an important decision of the company.

Secondly, the theory of decentralized control is one of the theoretical foundations of the mixed ownership reform, the purpose of which is to form a competitive relationship among shareholders. Heterogeneous blockholders inhibit the basis of blockholder’s collusion. Shareholders with the same property nature have a relatively consistent objective function, and they have a good basis for collusion. However, the objective functions of heterogeneous blockholders are quite different. State-owned shareholders shoulder both political and economic goals, whereas non-state-owned shareholders are more concerned with economic goals. So, it is difficult to form a basis for collusion between them. And heterogeneous blockholders will pay more attention to the firm value. Therefore, heterogeneous blockholders will provide a basis for the scientific decision-making of corporate innovation, which can enhance the enterprise’s innovation capacity through incentive and constraint mechanisms (Xia & Zhou, 2022). Yuan et al. (2022) point out that the diversity of mixed shareholders will significantly increase the enterprise’s exploratory innovation investment. Based on the above arguments, the main research hypothesis H1 is as follows:

According to the theory of corporate governance, heterogeneous blockholders can promote corporate innovation by improving corporate governance (Yuan et al., 2022). Multiple blockholders can supervise the behavior of controlling shareholders, restrain related transactions, reduce the cost of equity, restrain job consumption and opportunistic behavior of senior executives, resolve agency problems, and restrain stock price synchronicity (Helling et al., 2020; W. Wang et al., 2021). In the absence of effective supervision, the controlling shareholder will encroach on the company’s resources through tunneling behavior, which is particularly prominent in emerging countries. Heterogeneous large blockholders can effectively prevent the tunneling behavior of the largest shareholder, ensure the demand for innovation funds, and improve the innovation output. Multiple blockholders can improve an enterprise’s risk-bearing capacity (Chen et al., 2019). The higher level of risk-bearing capacity is conducive to grasping investment opportunities such as innovation and increasing the long-term competitive advantage. At the same time, through exit threat, agency problems can be alleviated and innovation input and innovation output can be increased, to realize the long-term prosperity of the company (Helling et al., 2020). The active supervision of multiple large blockholders will provide a good institutional foundation for corporate innovation, the same conclusion is gotten by Shang et al. (2022). The research hypothesis H2 is proposed:

Based on the theory of resource dependence, heterogeneous blockholders can promote corporate innovation through resource advantages. Heterogeneous blockholders can ease financing constraints and take advantage of the natural benefits of different capitals (Yuan et al., 2022). For example, the state-owned shareholder has abundant financial resources, human resources, market resources, and political resources based on the nature of the ownership background (J. Cao et al., 2020), whereas private shareholder has acute market insight and can grasp market trends more effectively. Moreover, the coexistence of heterogeneous blockholders can use their advantages to seek more innovative resources for the enterprise, thus better promoting corporate innovation. At the same time, the mixed ownership reform is always conducted between the same industry, and peer effect will promote the innovation behavior of enterprises (Liu et al., 2022). The research hypothesis H3 is proposed:

Heterogeneous blockholders can improve innovation efficiency. The coexistence of heterogeneous blockholders can break down the barriers of industry boundaries for non-state capital and expand the business boundary of private capital. Heterogeneous blockholders can realize mutual assistance between different capitals, which not only enhances the market acumen of state-owned capital but also opens a wider development space for non-state-owned capital. There is no doubt heterogeneous blockholders will improve a company’s resource allocation efficiency, the quality of decision-making, and innovation efficiency and increase innovation output. Yuan et al. (2022) find that the mixed ownership reform can optimize the reasonable allocation of resources and can promote the green innovation of enterprises. The research hypothesis H4 is proposed:

Research Design

Data Source and Sample Selection

The paper uses the data of China’s A-share listed companies from 2007 to 2021 as the sample because the R&D investment and patent information of China’s listed companies has been disclosed since 2007. The paper excludes samples of the financial industry, newly listed companies that year, missing research data, and companies in an abnormal financial situation such as Special Treatment companies (ST and *ST). At the same time, because the multinational firms apply for patents from the headquarter, in this paper, we removed the sample of multinational corporations. And excluded the samples without two or more blockholders. A company with two or more large blockholders with 10% or more of the shares is selected as the sample. The data on the patents comes from the Chinese Research Data Services Platform, the data on the large blockholders’ equity nature comes from the SinoFin Financial Information China Center for Economic Research database, and other data are obtained from the China Stock Market Accounting Research database. To mitigate the outliers, all continuous variables are winsorized at 1% and 99%. Our final sample consists of 16,087 firm-year observations for 3,068 firms, including 4,682 SOEs and 11,405 non-SOEs observations.

Variable Selection

Dependent Variable

The dependent variable is enterprise innovation. Two methods are usually used to measure enterprise innovation, from the perspectives of innovation input and output. Taking innovation investment as an indicator of enterprise innovation can reflect an enterprise’s innovation willingness (Z. He & Wintoki, 2016), but due to the choice of corporate strategy and changes in accounting standards, the disclosure on innovation investment by enterprises is not in place to any significant degree, and it is difficult to obtain accurate enterprise innovation input data (J. J. He & Tian, 2013). And enterprise innovation is the comprehensive result of the input of many resources, such as capital, scientific research personnel, technical support, organization, and management, whereas innovation investment only measures enterprise innovation from the perspective of capital investment. Therefore, innovation investment cannot reflect the investments of other innovation resources, and it is not the most appropriate indicator of enterprise innovation (Aghion et al., 2013). Innovation output is the final result of various innovation inputs and corporate governance of an enterprise, it is a comprehensive indicator of enterprise innovation and is a more accurate indicator of enterprise innovation than innovation input (J. J. He & Tian, 2013), and which has become standard in the innovation articles (J. J. He & Tian, 2018). Enterprise innovation output is patent, which can be measured in terms of patent application, and patent authorization. And patents are divided into invention patents, utility model patents, and design patents. An invention patent has the highest value, utility model patent is the second, and design patent is the lowest. Therefore, we use the natural logarithm of the number of invention patents granted plus one (Igrant) as the enterprise innovation proxy and the natural logarithm of the number of invention patents applied plus one (Iapply) is used as the proxy of enterprise innovation output in robustness test.

Explanatory Variable

The explanatory variable is heterogeneous blockholders (Naturemulti). Regarding the definition of a blockholder, this article draws on La Porta et al. (1999), Attig et al. (2013), Ben-Nasr et al. (2015), using a shareholder with a 10% or more share as a blockholder. We divided a blockholder’s equity into state-owned and non-state-owned according to the nature of property rights. We use listed companies with two or more blockholders with 10% or more shares as the research samples and define the samples with both state-owned blockholder and non-state-owned blockholder as heterogeneous blockholders. When a sample with heterogeneous blockholders, Naturemulti is assigned a value of 1 and the others assign a value of 0.

Control Variables

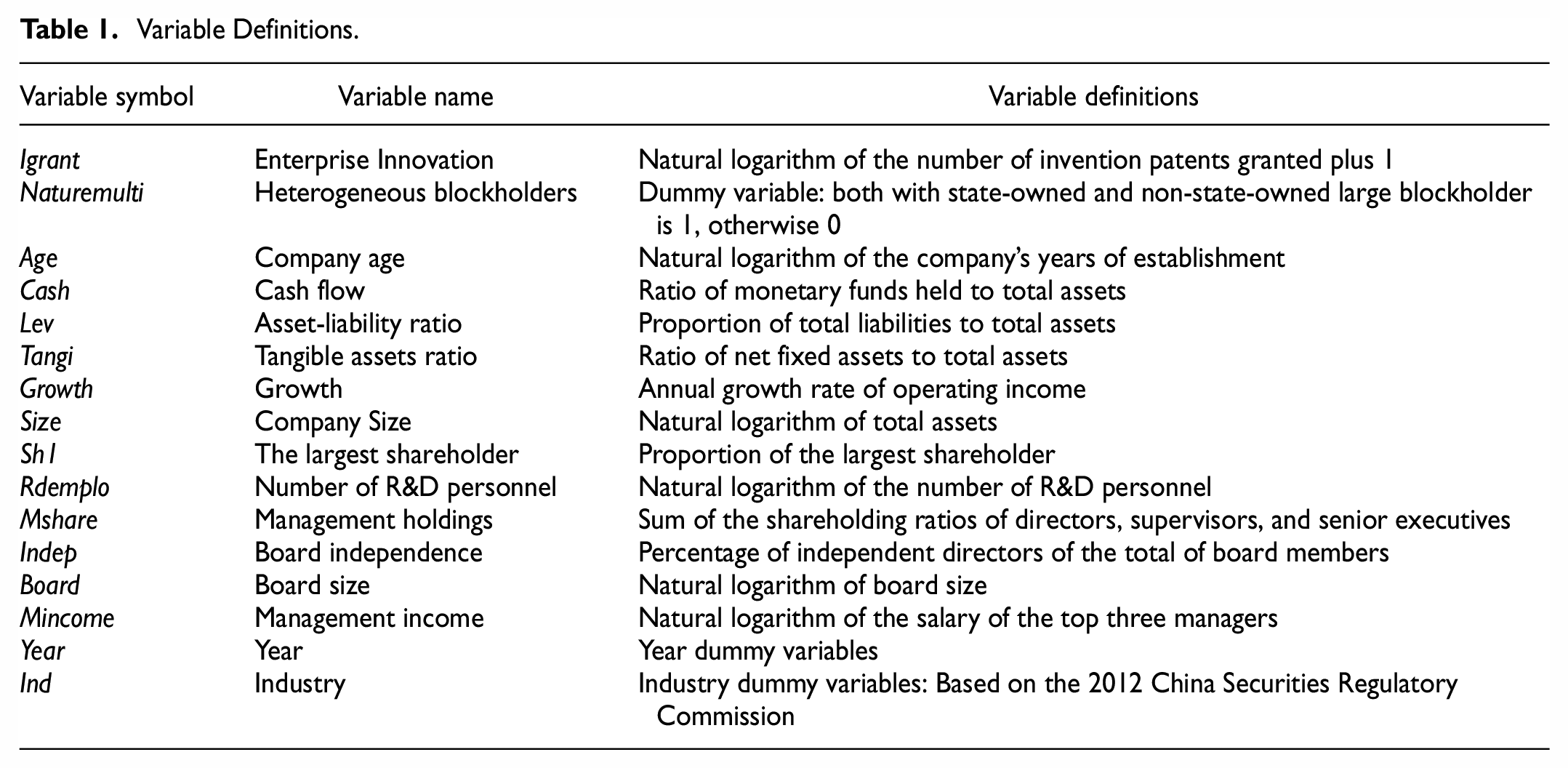

Following Balsmeier et al. (2017), the control variables include two categories: One is corporate governance variables, including the size of the board, the independence of the board, the share of the largest shareholder and the shares of executives, and the incentive variable of executive income. The other is the company’s characteristic variable, including company age, cash flow, asset-liability ratio, tangible asset ratio, company growth, company size, and the number of R&D personnel. We also control two dummy variables of year and industry. The definitions of variables are presented in Table 1.

Variable Definitions.

Model Design

The Tobit model is a kind of model that applies to the observation value with a positive probability value of 0 although the dependent variable is roughly continuously distributed in positive value. Because Igrant is a variable with a lower limit of 0, we follow the previous literature to conduct the Tobit regression (e.g., Gao & Chou, 2015). The Tobit model is shown in model (1).

In model (1), if α1 is significantly greater than 0, it indicates that heterogeneous blockholders are beneficial to enterprise innovation, and if α1 is significantly less than 0, it implies that it will hinder corporate innovation.

Empirical Analysis

Descriptive Statistical Analysis of Variables

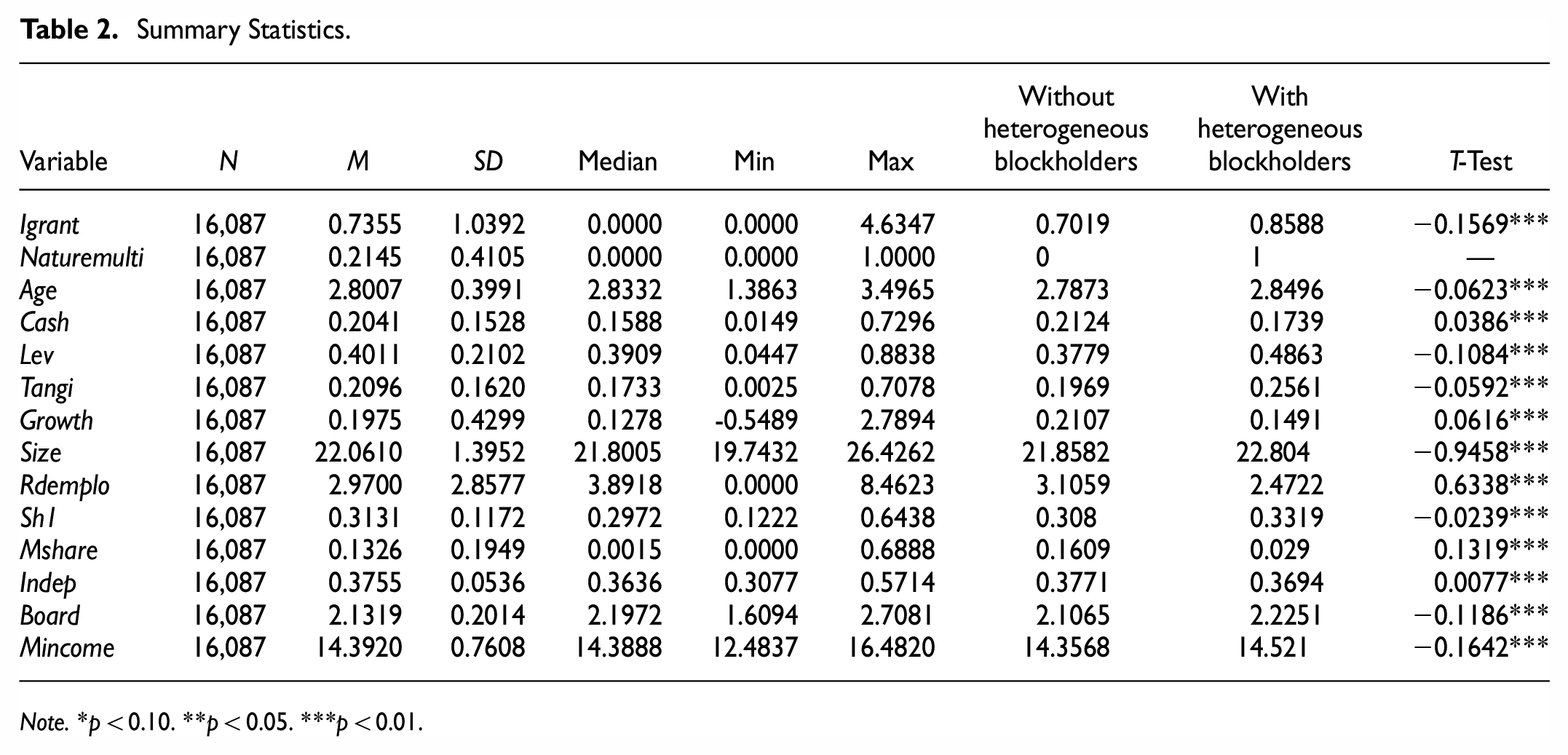

Table 2 reports the summary statistics of the variables. The mean number of Igrant is 0.7355 and the standard deviation is 1.0392, indicating that there are significant differences in innovation output among different enterprises. The average level of Naturemulti indicates 21.45% of the samples have heterogeneous blockholders. It also reports on the univariate test, which shows that the innovation output of the group without heterogeneous blockholders is significantly lower than the group with heterogeneous blockholders, which supports the research hypothesis, and there are significant differences between the other variables between the two groups, indicating that it is necessary to control these variables in the regression analysis.

Summary Statistics.

Note.*p < 0.10. **p < 0.05. ***p < 0.01.

Correlation Analysis

Table 3 reports the Pearson correlation coefficient between the main variables. The correlation coefficient between heterogeneous blockholders and innovation output is .062, which is significant at the level of 1%, showing that heterogeneous blockholders can significantly promote enterprise innovation. And the correlation coefficients between variables are lower than 0.53, indicating that there is no serious multi-collinearity problem between variables.

Analysis of the Correlation Between the Main Variables.

Note.*p < 0.10. **p < 0.05. ***p < 0.01.>

Basic Regression

The regression results of heterogeneous blockholders on enterprise innovation is shown in Table 4. Column (1) reports the impact of heterogeneous blockholders on enterprise innovation when only year and industry dummy variables are controlled, and the results show that the coefficient is .5433 and is positive and statistically significant at the 1% level. Column (2) reports that there is still a significant positive correlation between them when company characteristic variables, the year, and the industry variables are controlled. Column (3) shows the relationship when all control variables are controlled, and the results show there is a significant positive correlation at the 1% level, with a correlation coefficient of .2872, which means that the innovation output with heterogeneous blockholders is, on average, 28.72% higher than that of enterprises without heterogeneous blockholders. The results show that heterogeneous blockholders can significantly promote enterprise innovation. Thus, hypothesis H1 is proved.

Heterogeneous Blockholders and Enterprise Innovation.

Note. In order to save space, the results of control variables in the following tables are omitted and replaced by “controls.”*p < 0.10.

p < 0.05. ***p < 0.01.

Judging from the results of control variables, company size, compensation incentive, and board size are positively related to enterprise innovation, whereas the company’s age, asset-liability ratio, ratio of net fixed assets to total assets, and growth are negatively related to company innovation.

Plausible Underlying Mechanisms

Based on the above empirical results, there is a causal link between heterogeneous blockholders and enterprise innovation. In this section, we’ll explore plausible underlying mechanisms. We hypothesize heterogeneous blockholders encourage enterprise innovation through three possible mechanisms.

Mechanism Test: Based on the Perspective of Corporate Governance

To a certain extent, heterogeneous blockholders can avoid collision among blockholders with one single property nature and can play a supervisory function. The second agency cost (Cost2)—that is, the proportion of other receivables minus other receivables in total assets—is used to measure the tunneling behavior of blockholder. Using the method of mediation effect, we construct the following mediation effect regression models as (2), (3), and (4):

All continuous variables in the model (2), (3), and (4) were centrally processed, denoted by C_. Table 5 Column (2) shows heterogeneous blockholders are significantly negatively correlated with C_Cost2, which means that heterogeneous blockholders will reduce the tunneling effect of large blockholders. Column (3) shows heterogeneous blockholders are significantly positively correlated with enterprise innovation, whereas C_Cost2 is significantly negatively correlated with enterprise innovation, which means that the lower the C_Cost2, the higher the enterprise innovation. Comparing the regression coefficients of heterogeneous blockholders in columns (1) and (3), it can be found that heterogeneous blockholders will partly reduce agency costs to improve enterprise innovation. That is, there is a partial mediation effect. Thus, hypothesis H2 is proved.

Heterogeneous Large Blockholders and Enterprise Innovation Path Test.

Note.*p < 0.10. **p < 0.05. ***p < 0.01.

Mechanism Analysis: Based on Resource Dependence Theory

Enterprise innovation requires the input of multiple resources. Based on the previous analysis, heterogeneous blockholders can combine numerous resources for enterprise innovation. We take government subsidies as a variable of innovation resources to examine the mechanism of heterogeneous blockholders on enterprise innovation from the perspective of resource dependence theory. Here, the government subsidies are measured by the proportion of financial subsidies in total assets at the end of the period (Subsidy). Using the method of mediation effect, we construct the following mediation effect regression models as (5), (6), and (7). The test was also carried out with mediation effect regression models, and the results are provided in Table 5 column (4) and (5). These findings show that Subsidy plays a partial role in the mediating effect between heterogeneous blockholders and enterprise innovation. Thus, hypothesis H3 is proved.

Mechanism Test: Based on the Perspective of Enterprise Innovation Efficiency

The increase in enterprise innovation output may be due to improving innovation efficiency. We use the number of patent applications per unit of R&D investment (Rdef) as an indicator of innovation efficiency, the result of Table 5 column (6) shows that Naturemulti has a significant positive correlation with Rdef at 1% level, illustrating that heterogeneous blockholders will improve enterprise innovation efficiency. Thus, hypothesis H4 is proved.

Robustness Tests

Change the Dependent Proxy Variable to Conduct a Robustness Test

Replace the enterprise innovation variable in the basic regression with the natural logarithm of the number of invention patent applications plus 1 (Iapply). Regression results can be seen in Table 6 column (1). The results show that there is still a significant positive correlation between heterogeneous blockholders and enterprise innovation at the 1% level.

Change the Dependent Proxy Variable and Change Sample Period.

Note.*p < 0.10. **p < 0.05. ***p < 0.01.

Change the Sample Period to Conduct the Robustness Test

The Decision of the Central Committee on Major Issues of Comprehensive Deepening Reform issued in 2013 proposed to actively promote the reform of mixed ownership, and the Opinions of the State Council on the Development of mixed ownership economy of SOEs issued in 2015 provided measures to support the promotion of the mixed ownership reform of SOEs. So we take the mixed-ownership reform in 2013 and the introduction of specific measures for the mixed-ownership reform in 2015 as the starting point for the sample period and conduct the robustness test separately. The results are shown in Table 6. The findings show that they are still positively correlated at the 1% level after the change of sample period.

Robustness Test of Innovation Delayed Effect of Heterogeneous Large Blockholder

A patent from the beginning of research to success, from patent application to patent granted will take a long time. Whether heterogeneous blockholders impact enterprise innovation depends not only on the impact on the current innovation output but also on the innovation output in the next few years. We take the number of patent grants of a delay of 2 and 3 years as dependent variables to test the effect of heterogeneous blockholders on it. The results of Table 7 column (1) and (2) show that heterogeneous shareholders can significantly improve the later stage of enterprise innovation.

Innovation Delayed Effect of Heterogeneous Blockholders and Test by Fixed Effect Model.

Note.*p < 0.10. **p < 0.05. ***p < 0.01.

Fixed-Effect Model Test

Although control variables that may impact the relationship between heterogeneous blockholders and enterprise innovation are controlled in the basic regression, it is still possible to omit variables that do not change over time, thus affecting the regression results. So, we draw on the practices of Paligorova and Xu (2012) to control possible endo-existing problems using both corporate and time fixed-effect regression. Table 7 column (3) and (4) reports the impact of heterogeneous blockholders on enterprise innovation indicators, and the results show significant positive correlations between them at the 1% level.

Carry Out Robustness Test With PSM-DID

To further control for possible endogeneity, we take the samples with changed ownership of heterogeneous blockholders as the treatment group, take the samples without heterogeneous blockholders as the control group, and test by the PSM-DID method. First, 1 year before the nature of heterogeneous blockholders changed, all control variables in the model (1) are used as matching variables, and the control group sample that matched the treatment group 1:1 is selected through the nearest neighbor matching method of PSM; then we use DID method as shown in model (8) for testing.

In model (8), Treat is a dummy variable that indicates whether the nature of blockholders has changed. If Naturemulti has changed during the sample period, this variable is 1; otherwise, is 0. Post is a dummy variable that indicates before and after the change of Naturemulti, the value of the year before the change is 0, and the value of the year after the change is 1. Controls are the controlled variables listed in Table 1.

Specifically, there are two situations due to changes in Naturemulti from 0 to 1 and from 1 to 0. When conducting empirical testing, we also performed two cases separately. First, for the sample of Naturemulti from 0 to 1, the change sample is used as the treatment group and the sample without change during the sample period as the control group. Second, for the sample of Naturemulti from 1 to 0, we also take the change sample as the treatment group, and the sample without change as the control group. And we removed the samples with multiple changes in the nature of large blockholders and samples with only 1 year period before and after the change.

From column (1) of Table 8, it can be found that when multiple blockholders change from homogenous to heterogeneous, the effect is significant at the 5% level. Column (2) shows that when heterogeneous blockholders transformed into homogeneous blockholders, the effect is negatively significant at the 5% level. The result confirms that heterogeneous blockholders are beneficial for promoting enterprise innovation.

PSM-DID Robustness Test.

Note.*p < 0.10. **p < 0.05. ***p < 0.01.

Further Research

In this section, we’ll analyze the moderating effect of the nature of controlling property rights and the influence of the degree of relative power balance among heterogeneous blockholders.

The Moderating Effect of the Nature of Controlling Property Rights

The mixed ownership reform is a national strategy promoted by China and the focus is the ownership reform of SOEs. Here, we first test the impact of the difference in the nature of control property on enterprise innovation (Control). When a enterprise is SOE, control is taken as 1; otherwise, 0. The regression results are shown in Table 9 column (1). The result shows that the influence of control property on enterprise innovation of the whole samples are not significant. Then, the interaction variable Control×Naturemulti is used in column (2) of Table 9. And the results show that the interaction has a significant positive correlation at the level of 5%, indicating that heterogeneous blockholders can promote the innovation of SOEs. Next, according to whether or not the sample is SOE, the samples are grouped and regressed. The results are shown in columns (3) and (4). Compared with NSOEs, heterogeneous blockholders are found to have a significant effect on promoting the innovation of SOEs. The result not only supports the robustness of the basic regression but also confirms the effectiveness of the mixed-ownership reform of SOEs.

Tested According to the Nature of Holding Property Rights.

Note.*p < 0.10. **p < 0.05. ***p < 0.01.

The Relative Power of Heterogeneous Blockholders and Enterprise Innovation

In this section, We use the sum of the share ratios of blockholders with 10% or more with the same nature as the largest blockholder as the denominator, and the sum of the share ratios with different property rights as the numerator. The ratio of the two is used to measure the relative power balance of heterogeneous blockholders, expressed as Naturebalance. Table 10 column (1) and (2) show that the higher degree of Naturebalance, the more conducive to the promotion of enterprise innovation. Hence, the mixed ownership reform is not only a formal mix of different types of equity but also suggests the necessity to introduce blockholders with different property rights who hold 10% or more.

The Relative Power of Heterogeneous Blockholders and Innovation Efficiency.

Note.*p < 0.10. **p < 0.05. ***p < 0.01.

Conclusions and Implications

Conclusions

We used companies with two or more blockholders holding more than 10% of the shares in 2007 to 021 as the research samples to examine the impact of heterogeneous blockholders on enterprise innovation. The following conclusions are obtained.

Firstly, Heterogeneous blockholders can significantly promote enterprise innovation, and have a more significant role in promoting SOE’s innovation. In the past 45 years, various measures have been used to enhance the competitiveness of state-owned enterprises, but property rights have rarely been touched. Although these measures have achieved positive results, their marginal effects are constantly decreasing. The essence of mixed ownership reform is property rights reform, and it is achieved through the combination of different natures of property rights. The results confirm that mixed ownership reform can significantly improve the innovation ability of enterprises. Although both state-owned and non-state-owned enterprises can undergo mixed ownership reform, its promoting effect on innovation in state-owned enterprises is more significant.

Secondly, the higher degree of relative power balance among heterogeneous blockholders, the more conducive to enterprise innovation. The results indicate that the closer the shareholding ratio of heterogeneous major shareholders exceeds 10%, the more significant the promoting effect on corporate innovation. This tells us that the reform of mixed ownership must pay attention to the balancing effect between heterogeneous shareholders, to fully leverage the positive promoting effect of mixed ownership reform on enterprise innovation.

Thirdly, the mechanisms test shows that heterogeneous blockholders can significantly improve enterprises’ innovation efficiency. Finally, Heterogeneous blockholders promote enterprise innovation by reducing the tunneling behavior of large blockholders, and can obtain more innovation resources for enterprises. The results show that the mixed ownership reform has leveraged the comparative advantages of heterogeneous shareholders, provided more resources and information for enterprise innovation, and strengthened corporate governance, providing a good environment for enterprise innovation.

Implications

Our study verifies the effectiveness of heterogeneous blockholder. The findings of this paper have important implications for emerging countries’ governments and enterprises, especially those that focus on the transformation of state-owned enterprises.

First, it reveals that heterogeneous blockholder is an active and effective governance mechanism. The shareholders of state-owned property rights are held by government departments or held by state-owned enterprises on behalf of the government. In emerging countries, governments have the power to allocate resources in kinds of resources, such as financial resources, land resources, talent resources, and even industrial planning, and so on. Therefore, state-owned property rights can use the resources to serve the development of SOEs. Although non-state-owned property rights do not have advantages in these resources, they possess keen market insight and flexible market adaptability. The reform of mixed ownership can effectively combine state-owned and non-state-owned property rights, fully leveraging their comparative advantages. Therefore, the reform of mixed ownership is an optimization of the equity structure. The research results confirm that the reform of mixed ownership promotes enterprise innovation and enhances the core competitiveness of enterprises.

Second, we advocate that the mixed-ownership reform should focus on heterogeneous blockholders. There are various approaches to the reform of mixed ownership, including state-owned asset securitization, employee shareholding, and the introduction of strategic investors. The reform’s main realization path is to integrate heterogeneous shareholders. The reform of mixed ownership is a mixture of state-owned property rights and non-state-owned property rights. The manifestation is the diversified investment, cross shareholding, and integrated development of heterogeneous shareholders entity in an enterprise, which is essentially a redefinition of the enterprise’s property rights structure. So the reform of mixed ownership is no longer a formal combination of heterogeneous shareholders, but also a deep integration and organic combination of heterogeneous shareholders.

Third, heterogeneous shareholders can perform corporate governance functions through multiple mechanisms. The deep integration of state-owned and non-state-owned property rights can effectively leverage their comparative advantages. From the perspective of corporate governance, after the reform of mixed ownership, different types of property rights have the same goal of pursuing enterprise value appreciation while meeting social responsibility requirements. Therefore, the two types of property rights entities will not only strengthen supervision but also make scientific decisions to promote enterprise development. From the perspective of resources, after the reform of mixed ownership, it is possible to utilize financial resources, talent resources, industrial development,and other information resources with state-owned property rights, effectively grasp market information, enhance market sensitivity, and enhance market adaptability. These advantages are not possessed by individual state-owned and non-state-owned enterprises, achieving a 1 + 1 > 2 effect.

Therefore, substantial importance should be attached to the positive effect of the effective allocation of heterogeneous blockholders equity structure, and the next stage of mixed ownership reform should focus on the effective arrangement of heterogeneous large blockholders’ equity structure.

Limitations and Further Research

This article has the following limitations. There are significant differences between state-owned enterprises in China due to the different levels of government departments holding shares. There are central state-owned enterprises, provincial-level state-owned enterprises, municipal state-owned enterprises, and county-level state-owned enterprises. This article only analyzes the heterogeneous shareholders and enterprise innovation as a whole, without delving into the impact of mixed ownership reform of state-owned enterprises at different levels on enterprise innovation. This will also be the content of our future research. At the same time, there may be differences in the resources owned by state-owned enterprises at different levels, so their mechanisms of action on enterprise innovation will also vary, which requires further research in the future. So, how to effectively arrange the equity structure of different kinds of state-owned shareholders and non-state shareholders will be the focus of the next research in this field.

Footnotes

Acknowledgements

First of all, we would like to extend our sincere gratitude to Dr. Liu Feng and Yuan Di, for their instructive advice and useful suggestions on the paper. Second, we would like to express our gratitude to China National Social Science Fund, with the financial support we can complete the research.

Author Contributions

Shixian Ling conceived the study and were responsible for the design and development of the data analysis. Hui Xia and Zhanxin(Frank) Liu were responsible for data collection and analysis. Shixian Ling and Hui Xia were responsible for data interpretation. Shixian Ling wrote the first draft of the article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Shixian Ling acknowledges the funding support from China National Social Science Fund (No. 21BJY146).

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.