Abstract

Shariah governance is the mechanism to monitor and implicate shariah compliance in Islamic banks. The study’s goal of exploring the Islamic bank’s governance attributes and credit scores or rating relationship in the presence of shariah board attributes as moderators. The study collected time-variant data from 22 Asian banks (286 observations) from 2006 to 2018. Applied descriptive statistics, correlations, Likelihood Ratio (LR) test and the Ordered Logistic Regression model, a suitable technique for the ordinal dependent variable. The study findings provide evidence of shariah governance’s moderating role in the relationship between corporate governance attributes and credit rating. Moreover, shariah board characteristics strengthen the association between the corporate board and credit worthiness nexus. This research recommends that credit score evaluating agencies consider the shariah governance characteristics in evaluating Ib’s credit rating. The shariah governance attributes as part of credit rating can be an appropriate method for investors to measure the shariah compliance level of Ibs. Accordingly, Ibs can gain the confidence of investors or sukuk investors by improving shariah compliance and can access competitive fund sources. The study’s uniqueness is in determining the impact of shariah governance attributes as moderators on the board-rating nexus. This study suggested that credit rating agencies revise or amend their assessment procedures for Ibs. Abundant literature is available from the owner’s point of view. Nonetheless, this research explores governance and shariah governance attributes concerning Sukuk holders.

Introduction

Amid the economic collapse of 2008, Islamic bank credit and assets surpassed conventional banking because the attributes of the Islamic business framework adopted by Ibs helped control the losses (Hasan & Dridi, 2011). During the last four decades, the shariah-compliant finance industry has significantly progressed and experienced the fastest growth. Today, this industry’s size range is over $2.5 trillion, which is a direct output of its development at a quicker pace (Mirza, 2022). According to the Malaysia Islamic Financial Centre (MIFC) and Ernst & Young, the projected growth in late 2018 will be $3.4 trillion (Naveed, 2015). In light of the shariah-compliance financial sector growth, evaluating agencies focus on their Islamic Financial Institutions (IFIS) assessment methodologies, where they make specific adjustments and improve and revise parameters (Hassoune, 2009; Howladar, 2015).

In any organization, the high-ranking governing body is the corporate Board. Its primary duty is to safeguard the interests of sukuk holders and shareholders without adversely affecting the interest of other stakeholders (Kennon, 2020). Literature suggests that the independence of Board, foreign and women members, reputed and accounting-finance (A/F) knowledge-based board members, and the size of the Board is essential for highly performed Ibs (Grassa & Matoussi, 2014; Mansoor et al., 2019; Nomran et al., 2018).

In Ibs, another layer exists explicitly, known as the shariah board, which is missing in the case of conventional or non-shariah-compliant banks (Nomran et al., 2018). Furthermore, the Ib’s governance mechanism could be divided into two layers, that is, the Board of directors is responsible for the legal perspective and the shariah board members are responsible for confirming moral philosophy (Abdelsalam & El-Komi, 2016; Shibani & De Fuentes, 2017). Compared with Conventional Banks, no shariah governance layer is required due to the non-shariah compliant banks. However, Investors prefer investments in Islamic banks over conventional banks due to shariah compliance. Therefore the Islamic banks’ lack of implementation of shariah-guided rule and regulations have distracted depositors confronting high business risk, low profitability and poor financial stability (Hamza, 2013; Nomran et al., 2017). One of the reasons behind the high business risk of Ibs is poor shariah compliance, which leads to dissatisfied customers and a lack of access to a pool of funds (Alnasser & Muhammed, 2012; Grassa, 2016).

Problem Statement

The concept of profit and loss distribution in the Ib framework distinguishes it from conventional banks in terms of operations and financing structure. Islamic banking experiences several operational risks that affect its operations (Masood et al., 2011; Radzi & Lonik, 2016). The Ibs is based on the foundation of shariah’s injunctions, while the conventional banks do not consider the Islamic-guided rules and regulations in their policies. However, the commitment level to compliance with shariah rules and regulation differs in Ibs (Radzi & Lonik, 2016). Ideally, credit rating agencies must consider shariah compliance in the credit evaluation policy and procedures (Radzi & Lonik, 2016). A shariah scholar oversees compliance with shariah principles and certifies the standard of compliance in Islamic banking.

Standard and Poor’s, Fitch, and Moody’s are the topmost market leaders and large credit rating companies. Still, all these ratings evaluating firms have the same procedures and policies for all conventional and Islamic banks (Mansoor, Ellahi, Hassan, et al., 2020). Islamic and conventional banks use the same credit rating standards, procedures, or methodology because they all deal with intermediate cash flows and share the same risk classes (Radzi & Lonik, 2016). Moody’s also has the same credit evaluation criteria for both types of banks, claiming that the methodology is a flexible global corporation that fits Islamic and conventional banks (Howladar, 2015).

According to Fitch, the analytical structure for conventional and Islamic banking is the same when examining financing and lending policy, and risk curtailing or management strategies are the same (Fitch, 2007). A crucial point is Standard & Poor’s (S&P), Moody’s (Moody’s), and Fitch, respectively, hold 40%, 40%, and 15% of the World Credit Rating Assessment shares (IDBG, 2016). The remaining 5% of the credit rating market share belongs to other global rating organizations. Islamic banking is based on shariah injunctions and fundamentals, and additionally, the shariah board is liable for overseeing all its services and operations.

The three major credit evaluation market leaders use the same approach for conventional and Ibs, which is controversial. The distinctive characteristics of Ibs are less focused or undervalued, resulting in an inaccurate and biased credit worthiness evaluation of Ibs. Same as, shariah governance characteristics affecting the relationship between corporate board characteristics attributes and credit rating are inconclusive. The involvement of an effective shariah board should ideally be able to strengthen the board credit rating nexus. This research focuses solely on identifying the shariah governance characteristics that must be focused on when assessing Islamic banks’ creditworthiness. This proposed attribute would enforce Ibs to make greater efforts to improve the commitment level with shariah rules and regulations.

The study focused on the Islamic banks’ credit ratings, which were affected by Board of director and Chief Executive Officer (CEO) characteristics, Islamic bank attributes, and shariah governance characteristics. The study found scarce literature on shariah governance and credit rating from Asian countries’ perspectives. Corporate board attributes and shariah board Attributes significantly affect the credit rating in Islamic countries (Grassa, 2016; Mansoor, Ellahi, Hassan, et al., 2020). Corporate and shariah governance attributes have association in Pakistan’s Ibs (Mansoor et al., 2019; Mansoor, Ellahi, & Malik, 2020). It is found that Ibs in Pakistan have a strong governance system, which enhances credit ratings (Salman et al., 2022). Literature suggests that studies including (Ashbaugh-Skaife et al., 2006; Mansoor et al., 2019; Mansoor, Ellahi, Hassan, et al., 2020; Mansoor, Ellahi, & Malik, 2020; Salman et al., 2022) and (Grassa, 2016) explored the corporate aboard attributes, shariah board attributes and credit rating relationship but without considering any moderating variable (Mansoor, Ellahi, & Malik, 2020). This may be the first research to directly understand and take the shariah board attributes into account as a moderator. These shariah board characteristics also influence the link between corporate board characteristics and credit rating. The study will recommend that global credit evaluation services providers make necessary adjustments in existing policies for Ibs or develop the policy or procedure by considering the shariah governance attributes. The conclusion also suggests the shariah governance factors that credit evaluation agencies may consider to improve their methodologies and procedures.

Limited investigations were found in the literature that explored the impact of Ibs governance characteristics on credit scores (Alali et al., 2012; Aman & Nguyen, 2013; Ashbaugh-Skaife et al., 2006), and no study discussed in the literature that addressed the responsiveness of credit rating with corporate governance in Ibs perspective (Grassa, 2016). This research objective is to analyze Asian Islamic banks and provide evidence of how the Ibs and shariah board characteristics influence credit rating.

Literature Review and Hypothesis Development

The resource dependence theory (RDT) explains how an organization’s external resources influence it. RDT argues that the board members are highly interconnected with the organization’s external environment, increasing the firm’s access to various resources and enhancing the organization’s performance. Steward’s theory explains that managers are highly motivated and honest with corporates and accomplish their tasks efficiently and effectively. Therefore many firms prefer to small board because the presence of a large board may cause monitoring the operations, increase the cost of the firm and decrease the organizational (Kalsie & Shrivastav, 2016). Freeman (1984) presented “Stakeholder theory,” which argues the number of BODs expanded, more stakeholders will be represented, and no single stakeholder community will have a dominant on-board debate (Ghayad, 2008). The shariah board can improve the interpretations and enhance problem-solving ability and efficiency by appointing diverse shariah scholars from different backgrounds, fiqah, knowledge and skills (Hamza, 2013). Moreover, resource dependence theory explains that the presence of a large Board can access more resources. Hence, we anticipate that having a larger number of shariah scholars on the shariah board would help the Board to clarify issues and improve performance in terms of improved credit ranking. The large corporate board size enhances the mechanism of accountableness, innovation and transparency due to the effective monitoring function performed (Malik et al., 2014).

H1a: The corporate board size positively affects the Islamic bank credit rating

H1b: The shariah board size is positively associated with the Islamic banks’ credit rating

H1c: The large shariah board positively strengthen the link between the large corporate size board and the credit rating of Islamic bank.

Board Interlock and Shariah Board Interlock

In markets with a lot of competition, companies are more likely to use their external capital than their rivals. The government controls many resources, either directly or indirectly. As a result, people who serve as directors in different organizations are important and can influence or gain access to key policymakers. Ribeiro and Colauto (2016), Grassa (2016), Willems et al. (2015), Santos et al. (2012), and Ashbaugh-Skaife et al. (2006) extensively discussed and highlighted the issue of reputed directors or board interlock. The shariah scholar’s trend of offering services in more than one Islamic financial institution is found in Ibs. The trend of high board interlocking of shariah scholars found in gulf countries. That is, Unal and Ley (2009) reported that three shariah scholars in the GCC countries hold 26% of all shariah boards, with the 10 leading scholars securing 253 places in the shariah board, implying that each has 25.3 positions.

The interlocked shariah scholars are experts because they observe shariah compliance in various cultural contexts and deal with multiple Islamic financial institution scenarios. As a result, they are more effective than other scholars at interpreting, developing new shariah-compliant products, and overseeing management. Moreover, the resource dependence theory supports that the organization can access more crucial resources in the presence of directors linked to the Board of directors’ network (Caiazza et al., 2023).

H2a: The percentage of reputed directors (Board interlock) on the Board positively affects the Credit rating of Islamic banks.

H2b: The percentage of shariah board members who held positions in other shariah boards (shariah board interlock) positively associated with Islamic banks’ credit rating.

H2c: The more shariah board members interlock positively enhance the relationship between the reputed board of directors and the firm credit rating.

Board Members and Shariah Board Members Accounting and Finance Knowledge

The lack of financial experts on the corporate Board causes the firm’s failure. The Board of directors with financial degrees could perform their duties better than the other directors (Erin et al., 2019). High-profiled corporates’ failure causes uncertainty, and it is suggested to investigate the corporate Board’s financial expertise. Currently, Corporates making their boards more effective through diversification without considering financial knowledge. The board members with good accounting and finance knowledge could understand the factors that affect the firm, improve the firm’s value, and further anticipate the Board’s decision’s strategic outcome (Cossin, 2020). The firms are lucky and have no “bored” board of directors during the discussion on financial issues; therefore, the firm must have financial experts on the Board (Milton, 2017). One of the essential responsibilities of board members is to enhance the quality of financial reporting. Shariah scholars must be well-versed in Islamic law and have strong theoretical business backgrounds (Levy & Rezgui, 2015).

Henceforth, the study suggests that accounting and finance knowledge is essential for the Board of directors. It enhances the Board’s anticipation about board decisions’ strategic outcome and can provide understandable, credible and accurate financial reports to the stakeholders.

Hence, if the shariah board members have a business background or knowledge, they will investigate in-depth financial issues or financial services using shariah guidelines. As a result, performance in terms of credit rating has improved.

H3a: The percentage of Accounting and Finance knowledge of Board members positively associated with the Credit rating of Ibs.

H3b: The percentage of Accounting and Finance knowledge of shariah board members is positively associated with credit rating.

H3c: The presence of business background or Accounting and finance knowledge shariah scholars on the Board positively strengthen the link between AF knowledge of BODs and credit rating Islamic banks

Foreign Board Members and Shariah Scholars

The foreign board members in the Board positively impact the organizational performance (Bremholm, 2015). Choi et al. (2012) concluded that independent foreign board directors could enhance the expertise and monitoring of management. The resource dependence theory explains that the corporate Board arranges resources for the corporation. The ratio of investment in research and development can be increased by increasing foreign directorship (Bremholm, 2015; Okere et al., 2019).

The firms with foreign directors engaged in international financial misreporting pay high compensation to the CEO, showing laziness in replacing the poor performer CEO (Masulis et al., 2012). The Board’s national and foreign diversity negatively affects its monitoring function since the foreign directors have low attendance and lack company-specific information due to limited informal networks (Rehman et al., 2018). The firm with foreign directors was found to possess complex communication and reporting procedures due to language problems and high costs associated with the foreign directorship on the Board (Masulis et al., 2012).

Therefore, the current study predicts that the Board’s foreign directors engaged in international financial misreporting increased the cost, lack of firm-specific information and foreign directors’ presence makes the communication channels more complicated, adversely affecting the Board’s monitoring function. The ineffective monitoring system enhances the probability of misuse of funds and defaults, resulting in low credit ratings. Since the shariah foreign scholars are also unable to attend the shariah board meetings regularly due to money and time limitations, leasing to poor shariah compliance and hence too low credit rating.

H4a: The national board diversity adversely affects the Islamic bank credit rating.

H4b: The presence of foreign scholars in the shariah board is adversely associated with credit rating.

H4c: The presence of foreign members in the shariah board negatively moderates the relationship between the Board of directors’ regional diversity and credit rating.

Women’s Presence in the Corporate Board and Shariah Board

The have also confronted the dilemma of the scarcity of scholars. In 2013, Pakistan had 1.5% female representation on organizational boards, compared to 1.6% in Japan, 6.7% in India, 10.7% in China, 16% in Kazakhstan, 10.9% in Malaysia, 7.9% in Singapore, and 6.6% in Turkey, while Norway had a high of 39.7% (Yi, 2011). In the Asia Pacific region, female board members have an education background in accounting and law, while male board members have an education background in science or engineering (Yi, 2011). Gender diversity has been debated in the literature, and results suggest that there is no connection between gender diversity and business performance (Reguera Alvarado et al., 2011). Despite all, Adams and Ferreira (2009) found that male directors have more attendance issues than women directors, and the boards with female members have high attendance ratio of board members. According to Liu et al. (2014), increasing the proportion of women on boards of directors improves performance as measured by ROE.

From psychological aspects, women prefer teamwork while men prefer hierarchy (Nossel, 2016), and two or more female board members in Board are more suitable than others (Qian, 2016). Further, the boards have women board members reporting higher attendance (Ferreira, 2010), and adversely the over-monitoring system is the result of more female members on the Board (Pathan & Faff, 2013). There is no evidence found in literature from Gulf and Asian Ibs which addressed the role of women directors on the Board from debt holder perspective (Grassa, 2016). Further, the resource dependence theory explains that the Board with gender diversity has a positive effect on financial outcomes (Reddy & Jadhav, 2019).

Therefore, this study predicts that if a woman is elected to the Board, it will positively influence board members’ behaviors by attending more board meetings. Board functions will be improved due to high attendance and regularity. This positively affects Ib’s credit scores. Secondly, women’s directors prefer teamwork, and the attendance ratio is higher than men’s, resulting in improved monitoring. High team spirit and a better monitoring mechanism would be encouraged, and misrepresentation or misuse of resources would reduce creditors’ unrest and enhance credit ratings. Third, Ibs confront the shortage of shariah scholars, which could be addressed by increasing the percentage of female shariah scholars on the Board.

H5a: The women members on the Board positively affect Islamic banks’ credit rating.

H5b: The shariah women scholars on the shariah board are positively associated with credit rating.

H5c: The female shariah scholars on the shariah board would strengthen the link between the female on the corporate Board and the credit scores of Islamic banks.

Independent Directors and Shariah Supervisory Board

The objective of outside director’s appointments is to minimize agency problems. The outside director is also termed an independent director. Independent directors with more authority will improve organizational performance (Wang et al., 2015). Credit rating and independent directors have a strong link (Ashbaugh-Skaife et al., 2006; Grassa, 2016). Agency theory explains that the primary function of a separate Board is to mitigate the principal-agents conflicts. As a result, the study predicts that if outsiders or independent directors are present, controlling management functions will improve, and fund misallocation will be minimized, resulting in improved credit rating scores. Hence, financial institutions will have more trust in the Ibs, and the risk of default will be reduced.

Currently, Ibs have various shariah boards, such as shariah advisory boards and shariah committees. The advisory shariah board role is limited to advice and suggestions. The executives can approve or deny acting on this advice or suggestions, preventing the shariah board from achieving its goal of shariah enforcement (Grassa & Matoussi, 2014). Furthermore, a study shows that shariah supervisory board negatively impacts credit scores (Grassa, 2016). The resource dependence theory predicts that the Board of directors is responsible for arranging resources for the organization; normally, independent directors perform this function (Hillman et al., 2000). Resource dependence theory also explains the U-shaped relationship between the Board independence and benefit means Independence can be beneficial to a certain level. After that, the independence cost increases more than the benefit because the firm is over monitored and bears financial loss (Bertoni et al., 2023). Therefore, the Ibs required a shariah supervisory board to improve shariah compliance. This study predicts that a strong shariah board or supervisory shariah board enhances shariah compliance and strengthens the association between the board’s independence and credit rating.

H6a: The percentage of independent directors on the Board positively affects the Islamic bank credit rating.

H6b: The presence of the shariah supervisory board positively affects the credit rating of the Islamic bank.

H6c: The supervisory shariah board’s presence enhances the relationship between an Islamic bank’s independent Board and credit rating.

CEO Power and Credit Rating

The most debatable topic in the current decade is CEO power. Liu and Jiraporn (2010) found that credit ratings are lower in companies where the CEO has more decision-making authority. Han et al. (2016) also recommended that strong CEOs perform worse than non-powerful CEOs. The main cause of demanding high-interest or profit rates from bondholders or sukuk holders is the inability to monitor corporate CEOs. Hence, the firms that have more powerful CEOs have a high cost of debt financing due the bondholders considers to be at high risk. CEO tenure, CEO Duality and CEO founder or founding family factors used to measure the powerfulness of CEO.

CEO Duality

When the CEO holds two positions, that is, CEO position and Chairman Position is called CEO duality. Agency theory rejects the CEO duality because, due to poor monitoring, the chances of principal-agent conflict increase, which results in high agency costs and organization performance decreases (Duru et al., 2016).

Since stewardship theory focuses on non-financial causes, it demonstrates that CEO duality and firm performance are linked. It argues that respect, appreciation, and prestige empower the CEO to use unity of command to create more value for equity holders or owners. In 1978, Pfeifer and Salanik explains resource dependency theory endorsed the impact of external resources on corporations. They explained if the CEO has duality, they can make quick decisions and react quickly to the changing market situations, resulting in more firm value creation. While in the literature, the aspect of CEO duality with reference to agency theory evidence was also found (Jensen, 1993; Armstrong et al., 2014; Duru et al., 2016). As a result, we anticipated that if the CEO holds two offices, the oversight mechanism will be opaque, potentially leading to abuse or resource mismanagement (debt, etc.) and Ibs credit ratings suffering.

H7: A negative association exists between the CEO duality link and Ibs’ credit scores.

CEO Tenure

According to Karlsson et al. (2008), CEO tenure in the European country has decreased to 5.7 years. Lucier et al. (2006) described that CEO demand has increased, resulting in shareholders not being hesitant to replace the CEO when performance is poor or fails to fulfil investor expectations. As per Grassa (2016), there is a negative correlation between CEO tenure and credit ranking.

From the discussion, the CEO has a long tenure, and the study anticipates a negative relationship between CEO tenure and firm success. The long-tenure CEO is more powerful and can dominate the Board or influence the decision of the Board. When CEO tenure is long in a dynamic setting, it restricts knowledge flow and increases adherence to an outdated model, resulting in poor credit scores.

H8: The long CEO tenure is negatively associated with credit rating.

CEO Founder

According to the related transaction hypothesis, the founder CEOs’ primary goal is to improve the controlling family rather than the business (Ullah & Zhang, 2016). Cohen et al. (2013) found that a founder with higher abilities could positively affect the company’s future return compared to the non-founder manager. Villalonga and Amit (2006) also concluded a study and found that the founder CEO performs better in developed countries than a non-founder CEO. According to the Chinese business approach, the higher the CEO ownership, the more highly concentrated ownership and decision-making in a few hands will enhance the performance (Tan et al., 2001). A CEO with high stock can influence the Board and dominate decision-making (Finkelstein, 1992).

As a result, the study predicts that the founder CEO will not improve the firm’s credit rating because he works to control private family interests. Resource mismanagement will lead to default, resulting in low creditworthiness or scores.

H9: A negative relationship exists between the CEO founder or cofounder, CEO ownership and Islamic bank credit rating.

Methodology

Data Description

This study’s population includes the Ibs in the Asian region, and the sample is selected, consisting of 20 % of all Ibs for the Asian part. In literature, Ausat (2018) explored the Ibs performance by considering 60 observations, Grassa (2016) analyzed the conventional and shariah governance attributes concerning the credit rating of Ibs through 94 observations, Aslam and Haron (2020) considered 129 and I. Khan et al. (2018) analyze the 192 observations from the shariah governance perspective of Ibs.

This study selects a sample of 80 Ibs, and 41 banks are excluded due to offering Islamic windows. Further, 17 banks are excluded based on the unavailability of data. Thus, the final sample size included 22 banks bank for the period ranging from 2006 to 2018, that is, 13 years (286 observations), with annual frequency. The Credit rating agencies’ market leaders, including Standard & Poors (S&P) and Moody and Fitch’s data, are used for analysis (260 observations). Moreover, the data of Pacra and Crisl credit rating agencies were used to consider the remaining credit agencies (26 observations).

Data Sources

Data is collected from 2006 through 2018 and from the official websites of Ibs, Bloomberg (Islamicmarket.com), that is, the database of 955 shariah scholars, Forbes, Zawya and annual reports of the Ibs. Table 1 shows the selected Asian countries and sample composition

List of the Number of Countries and Islamic Banks Included in the Sample.

Note. The above table explains the number of countries and the number of Ibs form each country included in the sample.

Variables and Measures

The study adopted the credit scale used by Grassa (2016) and Ashbaugh-Skaife et al. (2006), which is used to rank Ibs. A higher credit rating is rated 19, and the lowest credit rating is 1. For more in-depth analysis, each category is given different ratings. Table 2 below explains the credit rating, the score assigned to each category and grade. Table 3 explained the definitions and descriptions of different attributes of corporate governance, shariah governance and firm characteristics.

Credit Rating Classifications.

Source. The rating methods procedure adapted from Grassa (2016) and Mansoor, Ellahi, and Malik (2020).

Note. The above table describes the ranking of credit rating and the assigned scores.

Corporate Governance, Shariah Governance Attributes.

Note. Table 3 explains the dependent, independent, and control variables and definitions in practice. The directors and shariah foreign scholars who have any degree or diploma in business study or accounting and finance, member of Any International Accounting body, that is, AAOFI considered financially knowledgeable persons (Grassa, 2016).

Data Analysis Technique

The ordered logistic regression model is appropriate when the outcome variable has three or more ordinal categories. The ordered logistic regression resembles multinomial regression. However, the key difference lies in the fact that order logistic regression is for meaningful ordinal categories and multinomial regressions are used for unordered categories of the criterion variable. When the variable’s response is in the ordinal form, it is advisable to use a specific model called the ordered Logit Model (Grilli & Rampichini, 2014). Henceforth, the study applied the ordered logistic model since this current analysis’s dependent variable is in ranked scale, which violates the Ordinary least square (OLS) assumption. Further, the Ordered Logit Model is preferred on the multinomial regression since the order of the dependent variable is in an ordered form.

Estimable Models

The research analysis investigated whether the Ibs’ credit rating is the function of corporate governance attributes, including corporate board attributes, CEO attributes, and shariah board attributes. The study might be able to prove that the Moderating role of shariah governance could improve the credit rating of Ibs. Henceforth, the estimable models of the study are the following:

Econometric Models

The analysis’s primary purpose is to find evidence of the moderating role of shariah governance between the board attributes and credit rating. The study adopted equations (1) and (2) from Ashbaugh-Skaife et al. (2006) and Grassa (2016) with the addition variables. Further, the rest of the models explain the moderating relationship this study developed through the critical literature review. Additionally, the study used a generally specific approach to determine the relationship between corporate governance, shariah governance and credit rating, as Grassa (2016) used. Hence, the current study developed the logical models from the literature and introduced the moderating role of shariah governance between conventional governance and credit rating. Further, the econometric models or equations are following:

Equations (1) and (2) tests hypothesis H1a, H1b, H2a, H2b, H3a, H3b, H4a, H4b, H5a, H5b, H6a, and H6b:

In the above equation, the terms stand for,

Corporate board Attributes (CBA)

Shariah board Attributes (SBA)

Corporate General Characteristics (CGC)

Result and Discussion

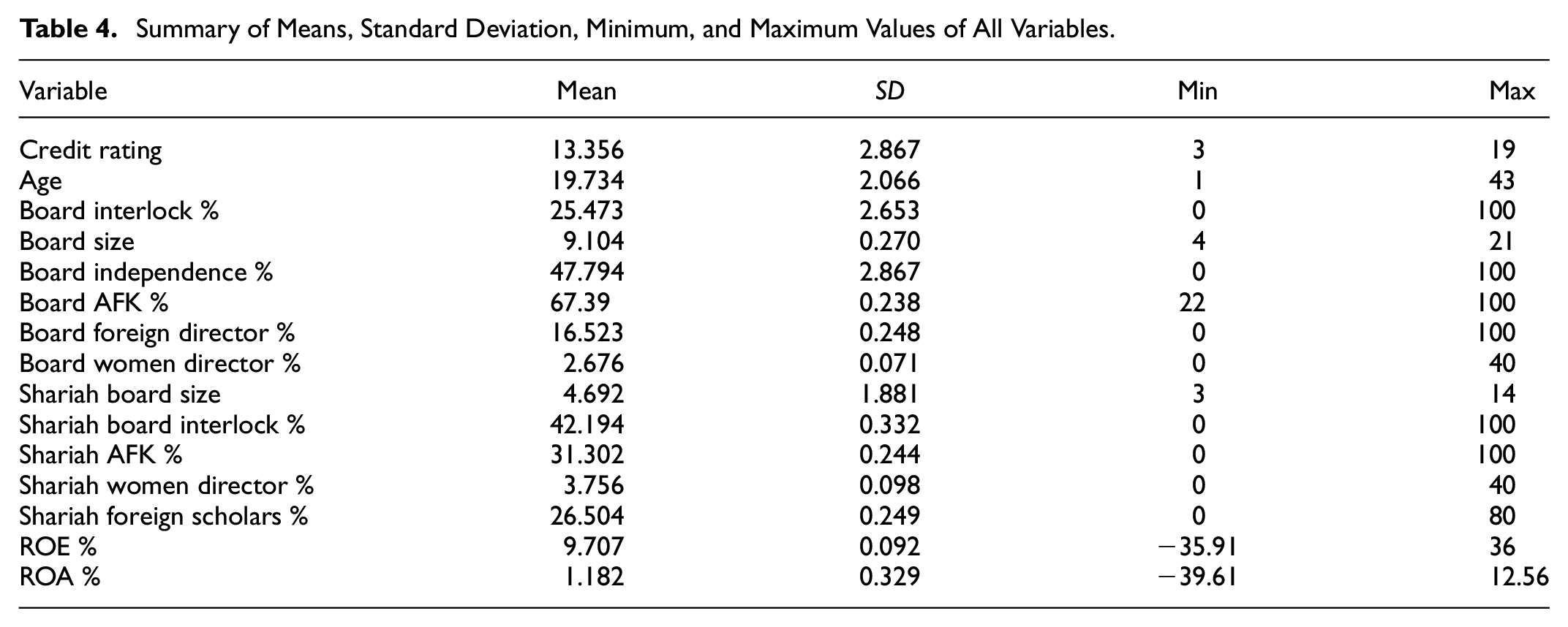

Table 4 explains the general characteristics of data and variables. Table 5 explains the correlations between the independent variables.

Summary of Means, Standard Deviation, Minimum, and Maximum Values of All Variables.

Correlation Matrix and Variance Inflation Factor (VIF).

The Pearson correlations results suggest that all the correlation coefficients are less than .8, therefore no multicollinearity issue (Aslam & Haron, 2020; Gujarati & Porter, 2009). Besides, the study applied the variance inflation factor (VIF) to detect multicollinearity. Table 5 shows all the values VIF for all explanatory variables are less than 10, confirming no multicollinearity (Aslam & Haron, 2020).

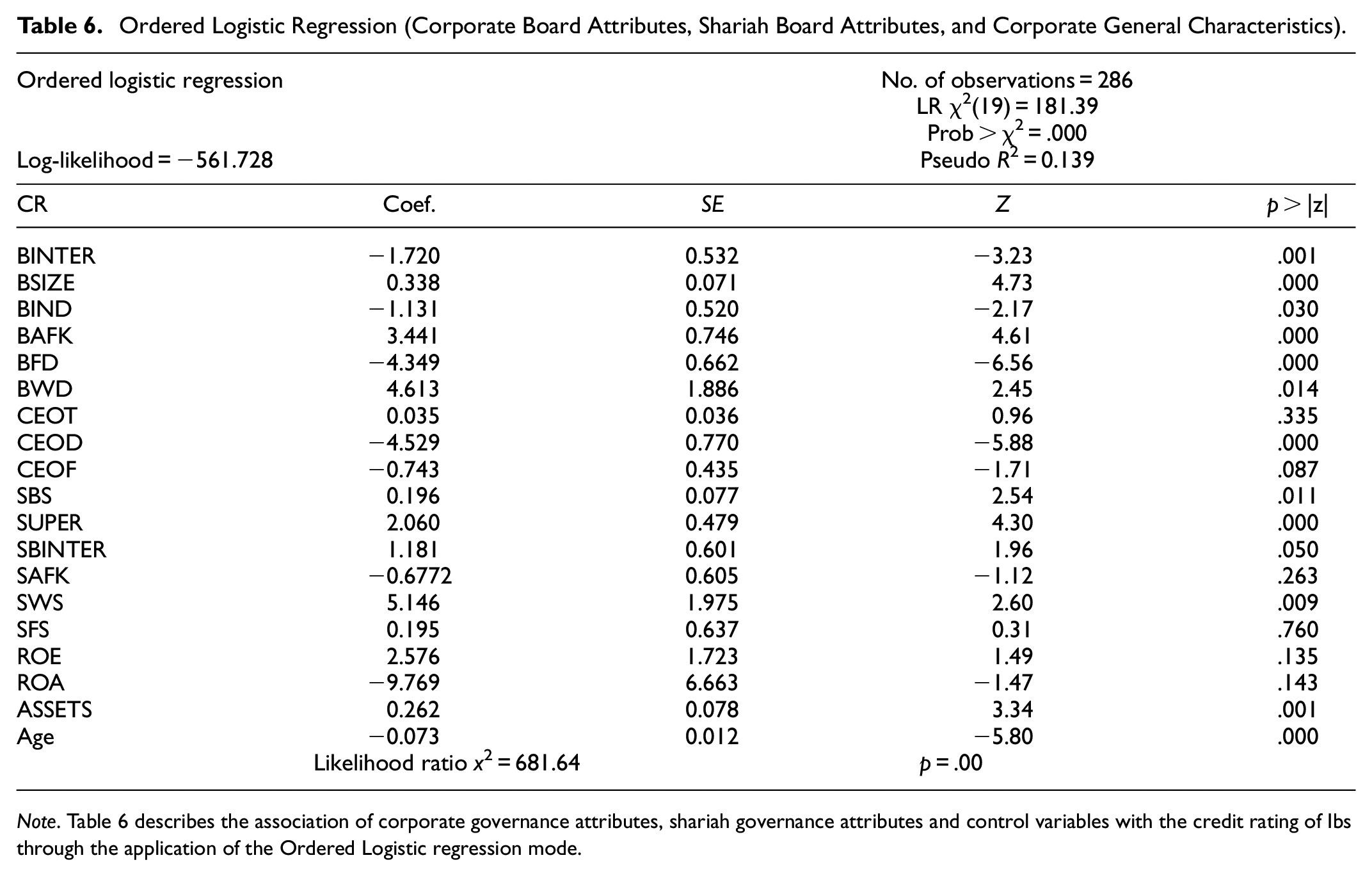

In Tables 6 and 7 the Assets (Log of total assets) is used as a proxy of the firm’s size. The findings show that the firm’s size significantly affects the firm’s credit rating, and the coefficient is positive. The positive coefficient explains the credit rating improves with the increasing size of the Ibs. Our results supported (Ashbaugh-Skaife et al., 2006; Grassa, 2016; Majumdar, 1997) proposed that larger firms are more productive, can access more resources and have more negotiation power than small firms. This study also provides evidence in favor of the resource dependence theory that Ibs can access more external resources in the presence of a large board.

Ordered Logistic Regression (Corporate Board Attributes, Shariah Board Attributes, and Corporate General Characteristics).

Note. Table 6 describes the association of corporate governance attributes, shariah governance attributes and control variables with the credit rating of Ibs through the application of the Ordered Logistic regression mode.

Ordered Logistic Regression (Corporate Board Attributes, Shariah Board Attributes).

Note. Table 7 describes the relationship between the independent variables, that is, corporate governance attributes and shariah governance attributes, with the dependent variable credit rating. The relationship results got through the application of the ordered logistic regression model.

The positive relationship between the Ibs size and credit rating supports the economies of scale hypothesis and is consistent with prior studies (Penrose, 1959; Pervan & Višić, 2012). Current analysis suggests that larger firms attain economies of scale to reduce cost and that high negotiating power provides more favorable financing conditions. The study also explained that the one-unit increase in the Ibs age caused a decrease in odd logs and 0.07 in credit rating, given that all the other variables held constant. The findings also indicate that the Ibs age significantly negatively affects credit rating. The negative sign explains that with the increase in age, the Ibs are prone to corporate inertia and fossilized bureaucratic style, which results in the aged Ibs being unable to quickly respond to the dynamic environment compared to young Ibs.

Hence, this study contradicts the learning-by-doing hypothesis of Grassa (2016) but supports Pervan et al. (2017) argued that old-age firm inertia overcomes the old-age firm benefits included in customer relations, supply channels, human capital and technology. Further Results explain that board interlock significantly and negatively affects credit rating. The negative sign indicates that the number of interlocks increases; the firm credit rating decreases. The negative sign confirms the busyness hypothesis, which explains that the number of board members offering services to various organizations results in compromised governance quality (Pandey et al., 2019). Therefore, the negative relationship between board interlocks and credit rating explains that the board members may be unable to give proper attention to Ibs operation due to busyness in other organizations, which may cause poor governance and low credit ratings.

Tables 6 and 7 explain that board size positively and significantly affects the company’s credit rating. The positive sign supports the resource dependence theory, which states that the Ibs large size board enhances the credit rating. Tables 6 and 7 also explain that a large shariah board size-positive significantly affects the Ibs credit rating. The positive coefficients clarify that the existence of a large board means the Board consists of scholars with different experiences, knowledge, skills, and different fiqh of schools, which results in better interpretation of products and shariah compliance operations.

Hence, the presence of a large shariah board gains the confidence of investors whose operations are conducted according to shariah compliance, resulting in access to optimum and low-cost funds.

Results described a significant negative relationship between board independence and credit rating. The negative sign is indicative of the fact that the presence of distracted independent directors on the Board. Due to this distraction, the independent directors cannot attend the Ibs meeting regularly, or the level of attendance reduces. Distracted independent directors allocate less time to Ibs and less attention to Ibs (Masulis & Zhang, 2019). The independent director depends on the executives for information, so the proper monitoring process remains incomplete due to a lack of time and attention. Another justification in its favor is that Independent directors are professionals serving in various firms simultaneously, and they depend on management for information. As a result, due to lack of time, workload and dependency on management for information, there is a limit to the role of independent directors in Ibs.

Accounting and finance knowledge positively and significantly explained that directors with accounting and finance backgrounds could bitterly understand the financial statements and effectively evaluate Ibs financial policies. The positive sign indicates that directors with an accounting and finance background could provide Ibs with a more effective internal control system. The more effective control systems mean appropriate use of resources and fewer frauds, leading to appropriating funds available for Ibs to pay their debt timely

Tables 6 and 7 explain that foreign directors on the Board are significantly and negatively associated with the Islamic banking credit rating. The significant and negative coefficients of foreign directors with credit scores explained that foreign directors usually attend fewer Ibs meetings due to the geographical distance between foreign directors and Ibs head offices compared to local directors. The firms with foreign directors engaged in international financial misreporting and paid high compensation to the CEO, showing laziness in replacing the poor performer CEO (Masulis et al., 2012).

The results show a significant positive relationship between the women on the Board, the shariah board and credit rating. The findings also support that the presence of female directors creates the firms’ financial value. These current study findings support that the attendance of women directors is comparatively more than men’s, and women prefer teamwork. The Ibs with women directors on the Board have high credit ratings because the high team spirit in the Board and high attendance ratio improve the monitoring system.

Moreover, the study suggests a shortage of shariah scholars facing Ibs, so this deficiency could be overcome by increasing the percentage of women shariah scholars on the Board. Tables 6 and 7 results described a significant positive relationship between the shariah board interlock and credit rating. The positive sign indicates that scholars with interlock having more knowledge and experience, could be done their job in a better way. Due to high expertise and experience, Islamic products’ innovation and performance are enhanced, which positively affects the credit rating.

Other research, such as Grassa (2016), has found that shariah board qualities and corporate board characteristics impact credit ratings. Given that all other factors in the model were unchanged, our findings show that a one-unit increase in CEO duality, board interlock, independent board members and foreign board members might reduce log odds of a 1.4, 1.4, 5.20, and 3.90 credit rating. Given that all other factors in the model were unchanged, the log odds for the credit rating of Ibs increased to 0.267, 2, 42, and 5.24 for board size, accounting and finance knowledge, and women board members, respectively. If the number of members on the Board, supervision, board members cross organization service, and proportion of women increased by one unit on the shariah board. As a result, we estimate a rise in the log odds for Ibs credit ratings of 0.22, 1.5, 1.4, and 6.8, respectively.

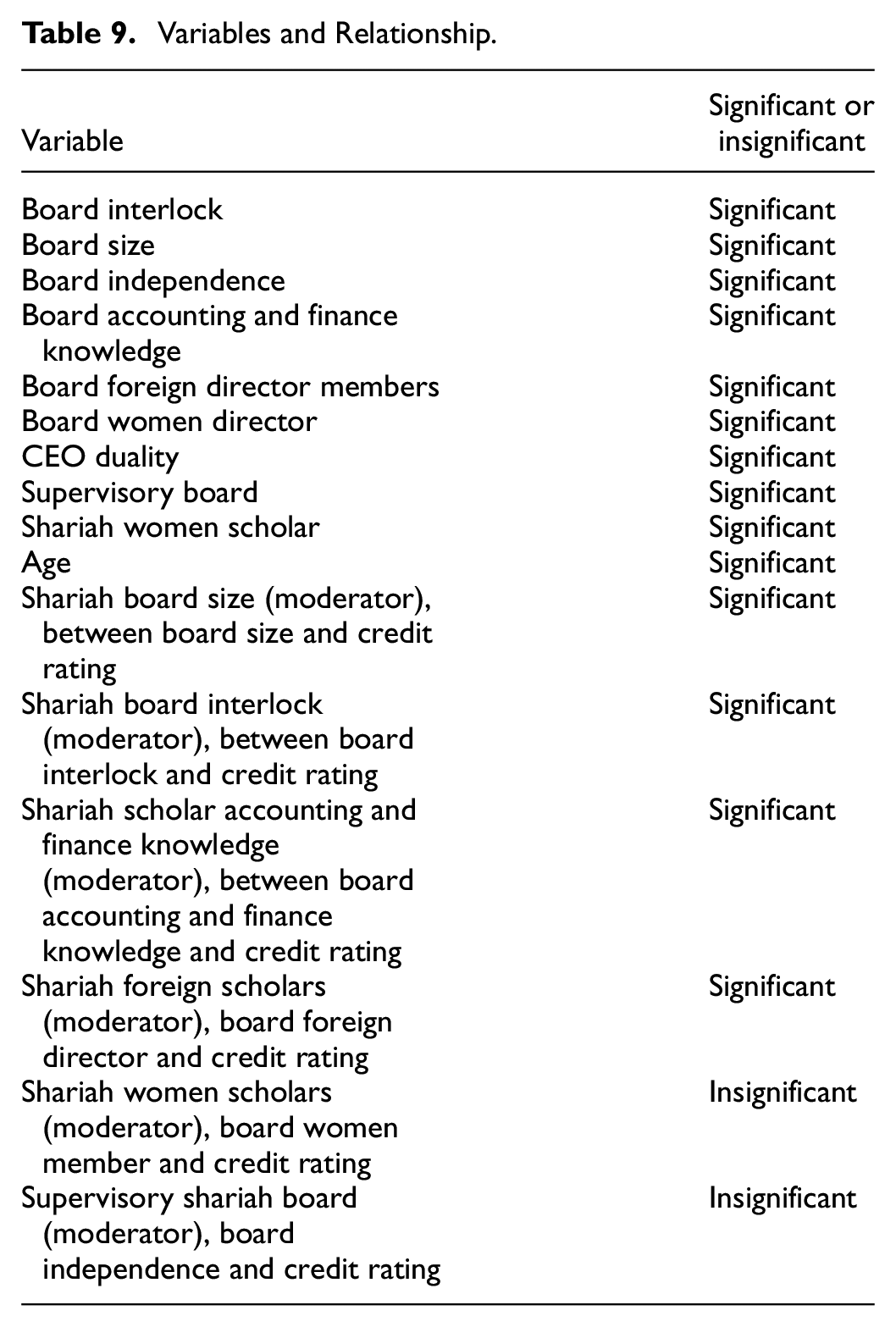

Table 8 shows that the interaction term (board size and shariah board size) positively impact the Ibs credit rating and provides evidence of Moderation. The findings suggest that the presence of a large board enhances the monitoring efficiency of management. A large shariah board also improves monitoring of the operations and transactions according to shariah-compliant principles (Table 9).

Ordered Logistic Regression Moderation.

Note. Table 8 describes the effect of Moderator Shariah Governance attributes on the relationship between corporate board attributes and credit ratings and results obtained through the ordered logistic regression model. The bold values shows that P-Value less then 0.05 which indicates the significant relationship between the Independent, Moderator and dependent variables.

Variables and Relationship.

Results depict that the term BAFK significantly affects the credit rating with coefficients of 3.441 and 2.422, respectively. When the shariah board AFK applied as a moderator between the BAFK and Credit rating, the interaction term BAFKSBAFK significantly positively affects the credit rating at a 1% significance level. Furthermore, the coefficients also improved by 7.103951 and 6.767816 in Table 8, respectively. Hence, the study suggests that the board accounting and finance knowledge could strongly affect the Ibs credit rating in the presence of shariah scholars with a business background.

Findings explained that the relationship of shariah foreign scholars (SFS) is as a moderator between the Board’s foreign directors and credit rating. In Tables 6 and 7, the board of foreign directors (BFD) significantly and negatively affect the Ibs credit rating with coefficients −4.349 and −5.237, respectively, at p = .000. When the shariah foreign scholars (SFS) are used as a moderator between the board of foreign directors and credit rating, the interaction term significantly negatively affects the credit rating at a 1% significance level with coefficients −7.382 and −5.785 in Table 8 respectively. So the improved value of coefficients in 8 is −7.382, and −5.785 represents that the relationship between Board foreign directors and credit rating (CR) is stronger in the presence of a shariah foreign scholar (SFS) as moderator. Henceforth, the study suggests that Ibs must consider the appointment of not only corporate directors but also shariah scholars who must prefer local nominations. The reason is that foreign directors lack firm-specific information, and due to lack of attendance, they cannot actively participate in monitoring or decision-making processes.

Conclusion

The study confirms that shariah board attributes and corporate attributes significantly affect the credit rating, and shariah governance strengthens the corporate governance-rating nexus. The findings suggested that Asian Ibs with large board sizes have better credit ratings, enhancing transparency, accountability and provision of access to more external resources.

Further, Ibs with large shariah boards can accommodate more scholars from different fiqahs, ultimately leading to a good understanding of shariah products. In addition to the above, a part of the conclusion confirms the RDT that the shariah board size positively moderates the relationship between the board sizes and credit rating, which is indicative of the overall monitoring and reviewing process on management to be more effective in the presence of a large shariah board. The current findings suggest that shariah scholars with business backgrounds positively moderate or strengthen the relationship between the corporate Board’s accounting and finance knowledge and credit rating. Therefore, Ibs can improve their credit rating efficiently through reputed directors in the presence of more qualified, well-informed, and eminent shariah scholars. Besides, the study found that foreign directors’ existence negatively affects credit ratings due to money and time limitations. Foreign directors are lazy to change the CEO and are found to be engaged in international financial misreporting. The study recommended that women’s participation be increased in the corporate Board and shariah board because women have fewer attendance concerns and prefer to work in groups. The Board’s monitoring role is improved.

Further, the study supports “the relevant transaction hypothesis” that discourages the CEO founder or belongs to the founding family. It argued that the CEO founder’s or founding family’s principal goal is to create value for founding families rather than maximize shareholder wealth. The study also confirms the economies of scale hypothesis that larger firms behave more optimally with high productivity, access more resources, and have more negotiation power than small firms.

The study first confronted the lack of literature on Islamic financial institutions’ corporate governance and credit rating. Therefore, this limitation creates difficulties in the development of the conceptual model. Secondly, the study found limitations in the availability of data. One of the data limitations is the case of Iran, where a council of ministers acts as a central shariah committee for all Islamic commercial banks. The same council is responsible for defining the products offered by Ibs. As a result, the absence of a separate shariah board is another limitation for including banks in the sample. As discussed in the case of Iran. Notwithstanding these limitations, the study has provided several pieces of evidence that fulfil the research purpose, meet objectives, and provides the answers to the research questions under investigation.

Future research could also compare the central shariah governance system (as practised in Iran) and Ibs individual shariah governance system. In line with the current or other previous studies, future research may focus on how stakeholders’ interests can affect the presence of both board and shariah board attributes. In sum, research in this field can expand generalizability by incorporating other countries’ financial institutions to provide a better relationship between corporate, shariah attributes, and credit rating. The future research also focuses on the qualitative analysis of improving the shariah governance in Ibs by conducting interviews with shariah scholars and stakeholders.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of the study are available on request from the Corresponding author.