Abstract

Integrated Reporting (IR) is a relatively new concept that is considered one of the most recent trends in corporate reporting; it is still an emerging research area in different parts of the world. Malaysia is an appropriate emerging economy to investigate IR adoption. Large Malaysian public listed companies (PLCs) are encouraged by the Malaysian Code on Corporate Governance (MCCG) of 2017 to adopt IR based on the international IR framework. By combining the stakeholder theory and the agency theory, this article proposes a conceptual framework to explore the moderating effect of sustainability reporting on the relationship between corporate governance mechanisms and IR disclosure level for the Malaysian PLCs. To obtain the data related to IR and the other variables, the study suggests using a content analysis method on the annual reports of the top 100 Malaysian PLCs based on their market capitalization. The proposed conceptual framework could be very useful; it can assist PLCs having sustainability practices to adopt the IR framework, reduce information asymmetries, increase information transparency, and create value. This study contributes to the literature by investigating the IR practices and their determinants in Malaysia after the introduction of MCCG 2017.

Keywords

Introduction

The external business environment has significantly changed and has become more complex, while traditional corporate financial reporting is unable to face these changes due to its several limitations and drawbacks, such as absence of nonfinancial information (e.g., social, health, carbon emissions, and labor rights), short-termism, lack of coherence, and complexity (Haji & Ghazali, 2013; Silvestri et al., 2017). To overcome these limitations, Integrated Reporting (IR) has gained significant attention in recent years as an emerging approach to corporate communication (Camodeca et al., 2018).

IR could accomplish stakeholders’ demand by improving the quality of the information provided to them as well as enhancing accountability and stewardship (Haji & Hossain, 2016). IR improves the resource allocation in the decision-making process (Frías-Aceituno et al., 2013) and promotes a more cohesive, concise, and efficient corporate reporting approach, showing how organizations can create value over time (International Integrated Reporting Council [IIRC], 2013b).

IR represents the most recent improvement of the corporate reporting movement (Pistoni et al., 2018). For many countries, the shift toward IR is already a reality; the majority of large companies worldwide integrate financial and nonfinancial disclosures in their annual reports (KPMG, 2017). According to the International Integrated Reporting Council (IIRC) database, more than 1,600 organizations in more than 70 countries globally depend on the International Integrated Reporting Framework (IIRF) to support their strategy and reporting process (IIRC, 2019); this is a meaningful step in building significant momentum toward global IR adoption. Accordingly, IR has recently attracted the attention of many academics and practitioners as the next evolution of corporate reporting (Velte & Stawinoga, 2017); moreover, the discussion about IR adoption level, and its benefits and determinants to meet stakeholders’ needs, is still in progress.

The main objective of this article is to provide a conceptual framework to examine the moderating effect of sustainability reporting (SR) on the relationship between some corporate governance mechanisms and IR disclosure level for the Malaysian public listed companies (PLCs). The authors choose to develop this framework for application in Malaysia for the following reasons: Malaysia is different from other developing countries around the world, it is considered one of the most rapidly growing and emerging economies in Asia, and its status is heading toward being a developed economy (Zahid et al., 2019)

Recently, Malaysian companies have been rapidly increasing various types of voluntary disclosures; as a result, several terms related to nonfinancial information were mentioned, such as the Triple Bottom Line reporting (3BL), Corporate Social Responsibility (CSR), and SR. However, IR is the most recent reporting technique that appeared in Malaysia. For instance, in December 2014, the Malaysian Institute of Accountants (MIA) established the Integrated Reporting Steering Committee (IRSC). This committee focuses on raising awareness on and boosting IR adoption in Malaysia, and engages various stakeholders in shaping the continued development of IR (MIA, 2016).

In 2016, MIA and ACCA (2016) conducted an IR survey among many stakeholders in the value chain of corporate reporting. The survey demonstrated that the knowledge and awareness of IR in Malaysia are relatively low. However, in April 2017, as part of the Malaysian Code on Corporate Governance (MCCG), large Malaysian firms were called on to adopt IR based on the international IR framework (SCM, 2017). Furthermore, Bursa Malaysia encouraged PLCs to adopt IR in their annual reports. Besides, to encourage Malaysian firms to adopt IR in their annual reports, the National Annual Corporate Report Award (NACRA) introduced a new prize known as the Integrated Reporting Award in 2017.

Accordingly, 100 Malaysian PLCs adopted IR in 2018. In total, 28 of them were large companies, 10 companies were mid-capital companies, and the remaining 62 were small-capital companies (SCM, 2019). Therefore, Malaysia is considered not only one of the countries with regulatory signs or compliance with IR principles, but is also leading the path for IR adoption along with Brazil, China, India, Japan, Luxemburg, New Zealand, and the United Kingdom (IIRC, 2019).

Corporate governance (CG) has become a vital issue in Asia, especially after the corporate failures and the Asian financial crisis of 1997 (Akhtaruddin et al., 2009). CG aims to enhance stewardship and transparency and plays a significant role in bridging the information expectation gap between organizations and stockholders in countries such as Japan, South Africa, and Malaysia (IIRC, 2019). These benefits of CG are achieved through putting pressure on firms for doing more voluntary disclosures. IR is viewed as an indicator for effective CG, which is vital in attracting investors (KPMG, 2017). At the same time, governance disclosures are one of the essential components in the structure of IR content presentation (IIRC, 2013b). Furthermore, a firm’s CG structure has a significant impact on voluntary disclosure and IR adoption (Velte & Stawinoga, 2017).

Concurrently, due to its nature in providing nonfinancial disclosures related to the impact of a firm’s activities on the economic, social, and environmental issues, SR is viewed as an intrinsic element of IR; hence, it is an essential and vital step toward IR adoption (Silvestri et al., 2017; Stubbs & Higgins, 2014). Furthermore, according to Bursa Malaysia requirements, Malaysian PLCs should adopt SR guidelines; currently, most of the Malaysian firms are interested in sustainability activities and issue a separate sustainability report. Therefore, SR could play a significant role in the IR adoption process among Malaysian PLCs, and CG and SR could have a significant impact on increasing IR disclosures.

Despite growing interest in IR around the world, there are a few studies, such as MIA and ACCA (2016), Jamal and Ghani (2016), Wen and Heong (2017), and Abdullah et al. (2018), that examined IR adoption in Malaysia. Some of these studies measured the adherence of Malaysian firms to IIRC framework content elements. However, all of these studies were conducted before the MCCG 2017 call to adopt IR. Motivated by the research gap found in the prior IR-related studies in Malaysia, the present study aims to contribute to IR literature and respond to several calls for research on IR implementation (Dumay et al., 2016; García-Sánchez & Noguera-Gámez, 2018; Haji & Anifowose, 2016b; Pistoni et al., 2018) in three ways: first, it investigates IR disclosure in its earliest application stage in Malaysia; second, this study provides a conceptual framework that examines the impact of the MCCG 2017 call, board of directors, and SR on the IR disclosure level; and, finally, it conceptualizes the moderating effect of SR on the relationship between CG and IR.

This article has been structured in the following way: The next section provides the underpinning theories, followed by the inclusion of the literature review and propositions development, the presentation of the conceptual framework, and description of the research methodology. Finally, the conclusions and directions for future research are provided.

Theory

Stakeholder Theory

According to stakeholder theory, companies can maintain a strong relationship with stakeholders by achieving their objectives; this relationship can also improve the company’s reputation and have a positive impact on firm performance (Bose et al., 2017). Moreover, responding to the demands of stakeholders leads to competitive advantage and sustainability (Needles et al., 2016). This theory also states that the expectations of shareholders and the ability to meet their demands are crucial in maintaining a firm’s legitimacy and achieving sustainable performance (Ferri et al., 2016). In this regard, Oshika and Saka (2017) concluded that the main reason behind why Japanese firms were considered more sustainable was that management adopted the philosophy of “Providing satisfaction to stakeholders” for business success, and they disclosed it in their sustainability reports.

Following the global financial crisis of 2008, shareholders, regulators, and other stakeholders took a closer look at the long-term viability and sustainability of companies (S. Adams & Simnett, 2011). Therefore, they demand more nonfinancial information and require companies to disclose more information on governance, social issues, environmental issues, and sustainability in their annual reports (Camilleri, 2018; Needles et al., 2016; Velte & Stawinoga, 2017). Sustainability disclosure is in line with the aim of IR, which emphasizes providing stakeholders with high-quality, holistic, and concise information (Naynar et al., 2018). Besides, IR reduces the number of reports to avoid dispersion of stakeholders. Therefore, investors and other stakeholders depend on integrated reports as an exact representation of an organization’s social, environmental, and ethical activities (Flower, 2014).

According to the IR framework, although the primary purpose of the integrated report is directed at financial capital providers, it also benefits all stakeholders interested in the company’s value creation over time; these stakeholders include customers, suppliers, employees, business partners, legislators, regulators, local communities, and policy makers (IIRC, 2013). IR should explain and include a disclosure about value-added distribution for the firms’ stakeholders, to achieve their satisfaction (Oshika & Saka, 2017). This added value can be used as a practical and efficient reporting tool (Haller & van Staden, 2014) that makes stakeholders more interested in IR. Whereas, for stakeholders’ engagement by IR, the company reflects rational maximization of value (Parrot & Tierney, 2012). Consequently, to satisfy stakeholders’ requirements and create value over time, many firms around the world adhere to IR adoption by issuing a separate integrated report or including IR framework content elements in their annual reports.

Agency Theory

Despite the persistent attempts by companies to publish more information about their performance, there is still a noteworthy information asymmetry between stockholders and management; it is considered a major challenge in the reporting process (Briem & Wald, 2018). Information asymmetry is a situation, often between management (Agent) and shareholders (Principle), where one party has more information than the other. To alleviate this problem, an important objective is to reduce information asymmetry between managers and stockholders, causing a high level of corporate transparency that allows stockholders to evaluate the firm’s behavior in detail (Jensen & Berg, 2012).

In the corporate reporting process, transparency means the extent of information available about an organization that allows external parties to monitor internal activity and performance (Grimmelikhuijsen et al., 2013). Agency theory and legitimacy theory provide a comprehensive approach to support the assumption that transparency is an essential and critical factor in improving public accountability (Stefanescu et al., 2016). There are many ways to increase and enhance transparency in reporting, one of them being voluntary disclosure. Voluntary disclosure provides relevant information about a firm that helps to decrease the level of information asymmetry and reduce the agency problem; it is also an indicator of the increase in operations’ quality and makes the economy more efficient (Sehar & Tufail, 2013). That is because, according to agency theory, the narrow view of performance provided by traditional financial statements is insufficient to overcome the information asymmetry problem (Ruiz-Lozano & Tirado-Valencia, 2016).

The recent trends toward IR are more focused toward information connectivity, and a firm’s value creation process may further assist in overcoming the lack of transparency, avoiding information asymmetries and meeting stockholders’ requirements (IIRC, 2013; Ruiz-Lozano & Tirado-Valencia, 2016). Pavlopoulos et al. (2017) also highlighted that companies with a high level of IR disclosure quality display lower agency costs than those with a low level of IR disclosure quality. García-Sánchez and Noguera-Gámez (2017) also confirm that there is a negative association between disclosure of an integrated report and information asymmetry, indicating that using this disclosure tool to inform can help alleviate agency problems, facilitate firm decision making, and improve information quality among stockholders.

Literature Review and Propositions Development

Integrated Reporting Disclosure Practice

Until now, the adoption of IR was considered a voluntary practice all over the world except in South Africa and Brazil. However, it had global acceptance and launched in certain countries and organizations. For instance, according to a KPMG (2017) survey, the number of companies that adopted the IR framework and issued integrated reports significantly increased from the year 2015 to 2017 in many countries. In Japan, adoption increased from 21 companies in 2015 to 42 companies in 2017; in Brazil, it increased by 16 companies; the same increase occurred in Mexico by 16 companies; and increased in South Korea by seven companies. In Malaysia, based on the present study analysis, the large PLCs that issued a full integrated report increased from two companies in 2015 to 11 companies in 2017.

The advantages and benefits of applying IR are highlighted by various studies. For instance, IR improves information quality by connecting previously disconnected pieces of financial and sustainability information (Baboukardos & Rimmel, 2016). Furthermore, in firms dealing with a complex operating and informational environment, IR decreases information processing costs (Lee & Yeo, 2016). Moreover, it could eventually assist many organizations in reducing the reporting burden and information asymmetries (IIRC, 2013b). Also, companies that adopt IR voluntarily are associated with higher earnings quality (Obeng et al., 2020) and also increase the quality of their earnings per share (Cortesi & Vena, 2019). According to Vena et al. (2019), IR adopting companies have seen a decline in their cost of capital. Besides, IR plays a significant role in minimizing regulatory risk by providing information required from the capital markets and adopting a standard structure that could be generally accepted shortly (Pavlopoulos et al., 2017).

Recently, IR disclosure practices and their determinants have become a highly researched area. There are several studies (see Haji & Ghazali, 2013; Lee & Yeo, 2016; Pistoni et al., 2018; Rivera-Arrubla et al., 2017) seeking to answer the question of how to measure or evaluate IR disclosure level as a voluntary disclosure. For instance, to assess the quality of something, an assessment tool is needed. Previous studies developed a checklist or index as a measurement tool to evaluate the IR disclosure quality according to South Africa’s King Code III and the IIRC framework.

In the Southeast Asian region, IR is still in an early stage. However, some countries such as Malaysia, Indonesia, and Singapore have made noteworthy attempts to adopt IR. These countries have already started their IR journey after issuance of the IIRC framework (Abdullah et al., 2018; Dragu & Tiron-Tudor, 2013; Setiawan, 2016). In this regard, using a sample of Malaysian and Singaporean PLCs, Abdullah et al. (2018) proposed an IR checklist based on the IIRC framework to determine the presence of IR-related elements in companies’ annual reports; they found that some IR elements are included in the companies’ annual reports for both countries; moreover, each country focuses on different IR elements.

Another study by Wen and Heong (2017) used the IR index to measure the IR disclosure for the top 50 Malaysian PLCs from 2012 to 2015. They confirmed that Malaysian PLCs reported more than 50% for every content element. Jamal and Ghani (2016) also examined the extent of IR practices among listed property companies in Malaysia. The results showed that these companies should work more to achieve an adequate level of IR practices.

However, to answer the question of what are the factors affecting the production of integrated reports, a series of studies highlighted the determinants of IR disclosure level and the factors affecting it. Jensen and Berg (2012) examined various IR determinants and empirically showed that the financial system, cultural system, economic system, and educational and labor systems of a country play a significant role in IR adoption. Consistent with that, from an institutional perspective, Dragu and Tiron-Tudor (2013) argued that the cultural, political, and economic factors are the main emerging determinants of voluntary IR.

The recent literature has also tested the effect of a firm’s characteristics such as firm size, profitability, and the industry as a determinant of IR quality. For example, Frias-Aceituno et al. (2014) confirmed that firm size and profitability have a positive impact on the issuance of the integrated report; however, industry and growth opportunities are not significant in this respect. Also, Iredele (2019) confirmed that firm profitability positively influences the IR, but no significant impact was found for leverage. For Malaysia, Jamal and Ghani (2016) confirmed that the company size plays an important role in the extent of IR practices. The results of Ghani et al. (2018) showed that for real property companies in Malaysia, company size and audit firm size have a positive impact on IR disclosure. However, Vaz et al. (2016) empirically tested the impact of some firm features on the adoption of the IR and found no effect for firm size, industry, and sustainability assurance on IR.

To sum up, without empirical evidence, De Villiers et al. (2017) developed a conceptual model of IR development; they classified the determinants of IR into organizational features (e.g., size, profitability, growth, ownership structure, managerial motivations, disclosure costs, and nonfinancial performance) and external factors (e.g., stakeholder pressure, industrial sector, regulators, cultural dimensions, and geographical location).

Corporate Governance and Integrated Reporting

The relationship between CG and firm’s voluntary disclosure has gained importance in recent years and become widely researched. IR is still a voluntary disclosure practice in all countries except South Africa. A research trend is focusing on the relationship between some of the CG variables and IR adoption. For instance, some studies (see Frias-Aceituno et al., 2012; Hurghiş, 2017; Velte & Stawinoga, 2017) tested the impact of board of directors size, independence, diversity, and activity; these studies found a significant positive influence for some of the board characteristics on IR adoption. According to Haji and Anifowose (2016a), the audit committee effectiveness, activity, and authority have a strong positive impact on the quality and extent of IR practice, but there is no effect to audit committee independence and financial expertise. Moreover, concerning the ownership structure, Gunarathne and Senaratne (2017) confirm that the primary users of integrated reports are institutional investors. Therefore, they may have an influence and pressure on the firm’s management to adopt IR. The following section focuses mainly on evidence regarding the impact of the MCCG and the board of directors on IR disclosure level.

Malaysian Code on Corporate Governance (MCCG) 2017

According to stakeholder theory, the firm’s management should enhance communication with stakeholders. For this reason, in April 2017, as part of the MCCG launched by the Securities Commission Malaysia (SCM) in Practice 11.2, large Malaysian firms were called on to adopt IR based on the global IR framework (SCM, 2017). The integrated report was defined as “the main report from which all other detailed information flows, such as annual financial statements, governance, and sustainability reports.”

The IIRC accepted this call. It was considered a transformation in the reporting process to embrace IR. Moreover, the IR adopting motivations for Malaysian companies, the application steps, and the expected outcome are identified by the third edition of Corporate Governance Guide. It was issued by Bursa Malaysia in 2017 for users to gain a better understanding of CG practices inserted in the governance code (Bursa Malaysia, 2017). In this context, Bursa Malaysia started to develop a strategic corporate reporting approach by adopting the IR in its annual report in 2016. It enhanced IR disclosures in its 2017 annual report and introduced its first annual integrated report for the financial year 2018. This journey is considered as a guide to encourage other Malaysian firms to adopt the IR.

To the best of our knowledge, there is no prior literature highlighting this IR call. Therefore, the main motivation of this study is Practice 11.2 of the MCCG 2017. We argue that all Malaysian PLCs should follow the requirements of this code to enhance their transparency, accountability, and long-term sustainability. In response to the Practice 11.2 IR call, large Malaysian PLCs should follow the IR framework and increase IR disclosure in their annual reports or issue a full integrated report. Based on all the above, we suggest the following proposition:

Board of directors and Integrated Reporting

The board of directors (BOD) is a group of executive and nonexecutive directors that is responsible for protecting shareholder’s wealth and ensuring that various stakeholders’ requirements are met (García-Sánchez & Noguera-Gámez, 2018). It has a vital role as an internal CG mechanism in monitoring and supervising operations inside the firm. It enhances the transparency of reporting, reduces risks, agency costs, and private managerial interest (Bueno et al., 2018; Sartawi et al., 2014). Besides, a stronger BOD has a greater interest in satisfying stakeholders’ requirements for relevant information (García-Sánchez et al., 2018).

The BOD composition is the main legitimacy aspect of an appropriate CG structure (Velte & Stawinoga, 2017). According to Stakeholder Theory, there is a broad range of parties such as shareholders, government agencies, auditors, and creditors who are interested in companies’ attitudes toward nonfinancial information, for instance, CSR, governance, and sustainability (Needles et al., 2016). The BOD plays a critical role in good practices of CSR, implementing policies of stakeholder engagement, including processes to achieve holistic transparency (Frias-Aceituno et al., 2012). In addition, it ensures that shareholders receive relevant, balanced, and instructive information on the strategy, development model, nonfinancial policy, and long-term prospects of the company (IFA, 2017). Therefore, BOD strength has a positive effect on the transparency of a company to reduce information asymmetries. Consequently, the board plays a principle role in determining a firm’s disclosure practices.

In the context of the relationship between board characteristics (such as board independence, board size, activity, and board diversity) and voluntary disclosure, most of the prior studies confirmed that the board characteristics have a positive influence on the extent of voluntary disclosure of information. They suggest that a large number of members on the board makes it much easier to become involved with all disclosure matters, due to the different expertise in different fields, such as financial, social, and environmental (Fuente et al., 2017). Also, more independent nonexecutive directors on boards ask for more accountability and transparency. Besides, the board of directors’ members that meet regularly have more effective control. Furthermore, board diversity promotes problem-solving related to social performance (Fasan & Mio, 2017). Therefore, the board could seek to achieve the stakeholder’s requirements and protect their interests by encouraging management to provide more social and environmental information besides financial information to ensure the quality of information and increase transparency.

In Malaysia, there is some evidence (Akhtaruddin et al., 2009; Said et al., 2009; Sallehuddin, 2016), consistent with the literature, of a positive correlation between board size, independent nonexecutive directors, and voluntary disclosure. It is also important to mention that so far, IR disclosure is mandatory only in South Africa. Therefore, IR is considered a voluntary disclosure in all other countries, including Malaysia.

The MCCG 2017 increased board responsibilities to ensure the best governance practices and long-term sustainability. The BOD should understand and incorporate the new reporting dimensions (i.e., economic, environmental, and social responsibilities) into their decision to ensure that firms operate successfully and experience sustainable growth.

There are some other responsibilities related to IR that boards should bear on their shoulders, as identified by the French Institute of Directors (IFA 2017). First, boards should directly involve management in the process of IR preparation. Second, boards should commission established committees to conduct frequent monitoring during this process. Third, boards should have effective participation to identify the basic strategic guidelines. These responsibilities may interpret the expected impact of the BOD on the IR disclosure.

Previous studies highlighted different arguments related to the correlation between board characteristics and IR disclosure. For instance, using a sample of 15 countries, Frias-Aceituno et al. (2012) examined the influence of certain BOD features on the degree of information integration presented by leading nonfinancial multinational firms. They confirmed that firm size, growth opportunities, and board gender diversity are the most critical variables in the integration of information. Furthermore, greater board size and diversity, rather than increasing communication problems among board members, positively influenced the integration of corporate information (García-Sánchez et al., 2018).

That is consistent with Hurghiş (2017), who found a direct but weak relation between board size and the extent to which integrated reports were issued following the IIRC framework. Also, Fasan and Mio (2017) showed that the main determinants of materiality disclosure in integrated reports are firm industry, BOD size, and diversity. They claimed that large board size has a different mix of expertise to safeguard a wider scope of stakeholder’s rights. At the same time, IR aims to provide comprehensive information to a wider range of stakeholders on different issues; it requires a complex work. Therefore, larger boards are more likely to engage and enhance IR disclosure. This result is in line with a study by Iredele (2019), which shows that companies with a large number of board members have higher IR mean scores, an indicator of a positive association between board size and IR quality. The same is the case for gender diversity.

In contrast, Iredele (2019) found no significant impact of the board chairman on IR improvement. From another point of view, Pavlopoulos et al. (2017) examined the influence of IR disclosure quality as an independent variable in some CG mechanisms and found that IR disclosure quality is positively associated with CG variables, that is, a higher number of independent and nonexecutive board members results in higher IR disclosure quality.

Following the above argument, this research assumes that firms with strong governance, represented by an independent, large, and more diverse BOD, could put more pressure on management to maximize shareholder value over time, while protecting other stakeholders’ interests. Also, this situation will satisfy stakeholders’ needs and requirements by reducing information asymmetry and agency costs through increasing nonfinancial disclosure and by adopting the IIRC framework in the reporting process. Therefore, to examine the relationship between board characteristics and IR disclosure, we suggest the following propositions:

Sustainability Reporting

In an environment that has suffered from overpopulation, climate change, pollution, and resources depletion, sustainability is one of the most crucial and imperative issues (Ruiz-Lozano & Tirado-Valencia, 2016). It has become an increasingly relevant area of research, capturing wide attention (Hahn & Kühnen, 2013). Sustainability refers to the ability of all types of firms to safeguard limited resources for future generations, while supplying and maintaining value for the current generation (James, 2014). It consists of three different dimensions, namely, economic, environmental, and social issues; thus, any organization adopting the sustainability approach must take these three dimensions into account (Jensen & Berg, 2012).

SR aims to provide information about a firm’s activities, aspirations, and public image regarding environmental and social issues (Kılıç & Kuzey, 2018). It offers entities the chance to share their values, performance, and actions with the overarching goal of sustainable development by engaging stakeholders toward achieving this objective (Brusca et al., 2018). It has been promoted significantly in some firms, which issue a separate report on their CSR activities, while other firms choose to devote only a section of their annual report to sustainability activities (Abdullah et al., 2018).

The most widely accepted SR standards are called “GRI Sustainability Reporting Standards.” The responsibility for setting these standards rests with the Global Sustainability Standards Board (GSSB), which is an independent operating body under the Global Reporting Initiative (GRI) umbrella. GRI is an independent international organization responsible for GRI SR standards and its guidelines, which are known as “G4 Guidelines.” These standards aim to assist organizations to enhance their transparency and report their positive and negative effects on sustainable development. By adopting these standards, firms can determine risks and opportunities, improve the strategic decision-making process, reduce risks, and build strong relationships with stakeholders. It is fit for all organizations regardless of type, size, sector, and country. These standards are divided into two parts. First, universal standards contain foundation, general disclosures, and management approach standards. Second, the top specific standards relate to economic, environmental, and social standards. For reporting purposes, organizations are free to use all these standards or select any part to disclose specific information. According to a survey conducted by KPMG (2017), so far, GRI is the most widely adopted standard for corporate responsibility reporting among large firms in more than 100 countries.

In Malaysia, since 2010, listed companies are called by Bursa Malaysia to integrate sustainability elements into their strategies. These elements should include material economic, social, and environmental risks and opportunities of an organization (MIA & ACCA, 2016). Now, all listed companies in Bursa Malaysia Securities Berhad are required to prepare a “sustainability statement” under the Main Market Listing Requirements in Paragraph 6.1 and 6.2, including all sustainability matters related to economic, social, and environmental risks and opportunities (Bursa Malaysia, 2017). Furthermore, the Malaysian government has launched policies and incentives to ensure sustainable industrialization and cleaner production (Qureshi et al., 2019). Also, to motivate Malaysian firms to integrate sustainability practice in their annual reports, some organizations introduced awards related to the best sustainability reports, such as the National Annual Corporate Report Award (NACRA).

As highlighted by Bursa Malaysia (2018), there are varied benefits to embedding sustainability in business, which should encourage Malaysian companies to increase their sustainability practices. These benefits include enhancing risk management, encouraging innovation and attracting more clients, increasing productivity and cost reduction, enhancing reputation and brand value, and maintaining an operating permit.

Consequently, based on a KPMG (2017) survey, about 97% of the top 100 Malaysian companies by revenue had a corporate sustainability performance disclosure, compared with 72% as the global average. Also, 93% of these Malaysian companies embedded Corporate Responsibility (CR) disclosures into their annual financial reports. This ranked Malaysia as the second-highest country after India in the CR global ranking, comprised of 49 countries. In fact, Zahid et al. (2019) reported on great improvements in SR practices in the last 10 years in Malaysian companies. Also, some variables play a significant role in increasing these practices, such as firm size, age and profitability, GRI framework, and sustainability awards.

To measure sustainability practices, this study suggests using the corporate sustainability disclosure index adopted by Zahid et al. (2019). This index corresponds to the SR guide issued by Bursa Malaysia and GRI standards using content analysis and the scoring method to collect and measure data related to the four dimensions of sustainability practices in Malaysian companies, namely, economic, social, environmental, and workplace sustainability practices.

Sustainability Reporting and Integrated Reporting

Recently, corporate reporting has undergone an enormous transformation globally. SR and IR are the latest ways in which large companies practiced better communications with their stakeholders. According to KPMG (2017), the majority of large companies in 49 countries around the world have incorporated SR practices. Also, there is a noticeable increase in the number of companies that issue integrated reports in these countries. Particularly in the United States, around 395 companies of the 500 large companies listed on Standard & Poor’s (S&P) 500 stock exchange index issued sustainability reports in 2018. Also, in the same year, the number of IR reporters in the United States doubled since 2013 (IRRCI, 2018).

In fact, there is often uncertainty as to whether sustainability reports and integrated reports vary. Both are communication and reporting tools to deliver the firm’s activities and results. However, Bastian Buck (director, Reporting Standards) of GRI mentioned that “It is important to recognize that there are different audiences and purposes of reports. Just because you are producing an integrated report, it does not mean that you should stop producing a sustainability report” (GRI, 2016). This means the two types of reporting are not identical and have many differences. Thus, several organizations tend to provide a stand-alone sustainability report, besides their integrated report (Kılıç & Kuzey, 2018).

To understand these differences and highlight the similarities between them, Table 1 provides a comprehensive comparison between SR and IR in many varied aspects. Information has been extracted from the IR framework, GRI standards, and KPMG survey (GRI, 2013; IIRC, 2013; KPMG, 2017).

Comparison Between SR and IR.

Source: Adapted from (IIRC, 2013; GRI, 2013; KPMG, 2017).

The purpose of sustainability and IR differ in their main focus, between a focus on showing the organization’s impact on the environment, society, and the economy to a wide range of stakeholders, compared with a focus on shareholders and the value creation process. IR not only combines financial and nonfinancial information in one report but also shows the links and connectivity between different forms of capital, and how value is created clearly and concisely. That is not provided by SR, which tends to focus less on these issues. Despite these differences, IR and SR could provide a way for organizations to communicate how they sustainably and ethically generate financial value.

To highlight the relationship between sustainability and IR, although they could have some differences, as mentioned in Table 1, GRI considers a firm’s SR as the basic engine to provide the data required for IR. Also, SR is a necessary condition for effective IR; we suggest that IR assists companies in using a multistakeholder strategy to combine appropriate financial and sustainability information (GRI, 2013). While SR provides valuable nonfinancial information to investors and other stakeholders (Camodeca et al., 2018), integrated reporters could depend on SR bases and disclosures in the preparation of their integrated report.

In other words, GRI plays a crucial role in the further development of the concept of IR (Camilleri, 2018). The GRI guidelines provide Key Performance Indicators (KPIs) for the reporting process. Therefore, many IR firms adopt the GRI’s guidelines on preparing an integrated report (Oshika & Saka, 2017). As mentioned by the G4 guidelines, firms that issue integrated reports depend on SR basics and disclosure in preparing their integrated reports. The reason is that SR is considered a significant element of IR, and it is fundamental to a company’s integrated thinking and reporting process on its material issues, strategic objectives, and the assessment of its ability to achieve those objectives and create value over time (GRI, 2013).

As stated above, SR and nonfinancial disclosures could be considered a part of IR. Furthermore (Silvestri & Veltri, 2019) mentioned that IR evolved from SR as a tool to overcome the limitations and shortage of SR, such as disconnection with financial activities, and low trust and reliability from stockholders. Therefore, SR was a critical step forward on the road to IR (Stubbs & Higgins, 2014).

Some of the previous literature proposed a relationship between SR and IR. For example, Kılıç and Kuzey (2018) empirically examined the influence of some corporate sustainability features on the adherence level of the company to the IIRC framework’s eight content elements. They found that firms that adopt the GRI guidelines and issue a separate sustainability report are adhering more to IR framework content elements. Also, the existence of a sustainability committee has a significant positive impact on IR disclosure.

In their study, Lueg et al. (2016) conducted a case study of one company in Denmark, investigating the impact of SR guidelines and standards on IR. They confirmed that SR practices could assist firms in successfully implementing IR adoption. In addition, Mervelskemper and Streit (2017) proposed that there is a strong motivation to switch immediately to adopt IR for firms that are already producing a sustainability report. This is consistent with Setiawan (2016), who mentioned that firms that won the Indonesian SR Award are ready to issue an integrated report with only a few modifications, which adds value to their reports.

In Malaysia, based on the MIA and ACCA (2016) IR survey, approximately 50% of the respondents believe that SR is considered a subcategory of IR. Besides, these two approaches are not ideal substitutes, but they are overlapping. Also, just 3% of the respondents think that SR is enough without IR.

Based on the above argument, this study supposes that companies interested in sustainability issues and that produce sustainability reports are more likely to include the IR disclosures in their annual report or issue an integrated report. Consistent with that, we suggest the following proposition:

The moderating role of sustainability reporting

Generally, a moderator is a qualitative or quantitative variable that influences the direction and/or strength of the relationship between an independent and dependent variable (Baron & Kenny, 1986). It is a third variable that affects positively or negatively the correlation of the other two variables. Recently, SR has attracted a notable interest among researchers, however, very few studies exist highlighting the moderator role of SR in various situations. Utama and Mirhard (2016), for example, examined the moderating impact of SR disclosure on the relationship between intellectual capital and the company’s performance in Indonesia. The result shows that intellectual capital and SR have a significant positive effect on the company’s Return on Assets (ROA) as a proxy of the company’s performance. Also, SR positively moderates the relationship between intellectual capital and the company’s ROA.

Similar for the oil and gas industry in Malaysia, Shad et al. (2019) suggested that SR and enterprise risk management could have a positive impact on the company’s performance measured by economic value-added. Furthermore, SR may positively moderate the relationship between enterprise risk management and the company’s economic value-added. Moreover, using a sample from different industries in Finland, Ukko et al. (2019) confirmed that sustainability strategy has a moderator role as a promoter variable in the relationship between operational capability and firm financial performance.

As mentioned earlier, SR contains the three types of nonfinancial disclosures, economic, social, and environmental. Haladu (2018) empirically investigated the moderating influence of social sustainability on the relationship between some of the firm’s characteristics (e.g., Firm age, Audit firm) and environmental sustainability disclosure. The results confirmed a significant positive influence. However, to the best of our knowledge, no study used SR as a moderator for the relationship between CG and IR disclosure so far.

In unison with the legitimacy theory, SR has been considered a useful tool to enhance the firms’ reputation and legitimacy and to engage stakeholders (Brusca et al., 2018). Whereas stakeholder theory concentrates on how a firm interacts with particular stakeholders, legitimacy theory takes into account interactions with “society” as a whole (Stefanescu et al., 2016). Society and social disclosure are not only considered a significant part of SR, but they are also one of the dimensions of IR represented in social capital disclosures. Therefore, organizations could provide SR and IR to maintain and improve their legitimacy with their stakeholders (De Villiers et al., 2017)

Regarding capital disclosures, SR is commonly seen as the reporting practice on a firm’s impact on the society (which is generally equivalent to social and relationship capital and some of the human capital aspects), environment (which is generally equivalent to natural capital), and the economy (IIRC, 2013a). A firm that applies IR should provide disclosures to show its impact on the various six forms of capital (Financial, Manufactured, Intellectual, Human, Social and relationship, and Natural Capital). Some elements of SR and IR overlap and have other conflicts. Therefore, if a firm engaged with SR, it has made a significant step on the road to applying IR in terms of capital disclosures.

Moreover, SR is essential to an enterprise’s reporting and integrated thinking process in providing the input that assists in identifying the material issues, long-term objectives, and the evaluation of the ability to achieve objectives and creating value over time (GRI, 2013). Therefore, according to Camodeca et al. (2018), most of the firm’s success in the IR journey was motivated by the concentration on sustainability disclosure. Also, SR could be the natural development in the IR journey (IIRC, 2013a). To prove that, according to the KPMG (2017) survey, the growth in IR disclosure in Mexico was partly driven by the overall rise in sustainability disclosures.

Based on the previous discussion, due to the nature of sustainability disclosure, SR could influence the firm’s ability to generate IR. In Malaysia, according to MCCG 2017, “An integrated report is the main report from which all other detailed information flows; such as annual financial statements, governance and sustainability reports” (SCM, 2017). This means the information in sustainability reports is considered a significant portion of the IR practice, like financial and governance disclosures. Therefore, this study argues that the impact of MCCG Practice 11.2 on the IR disclosures level could be stronger in the Malaysian firms that have started their SR journey and issued sustainability reports. We suggest that companies with higher SR disclosures already have experience in dealing with nonfinancial and voluntary disclosure; hence, they could be faster in responding to the requirement of MCCG’s call to adopt IR.

While the relationship between the BOD and IR has attracted attention among scholars, and the board plays a vital role in business sustainability (Bueno et al., 2018), there might be a moderate effect to SR on this relationship. The sustainability report may work as a moderator to the extent that it accounts for the relation between BOD and IR, suggesting that board characteristics may affect the IR disclosures level most strongly for high levels of sustainability disclosures.

Based on the above, this study claims that the relationship between CG and IR may be strengthened with SR. Consistent with that, we suggest the following propositions:

Conceptual Framework

A conceptual framework is a visual or written output that explains the key factors, concepts, or variables, and the presumed relationships between them (Roberts, 2000), to be studied. Global corporate reporting standards have undergone considerable changes and improvements. The firm’s orientation and transformation to sustainability and IR have become a fact in many countries. C. A. Adams (2015) called on academics to engage and conduct more research related to these new forms of reporting.

In October 2018, the IIRC saw significant progress in its strategic direction, moving from the breakthrough phase to momentum phase. In this phase, the IIRC plans to engage with global markets and gain significant regulatory endorsement until 2021, when this transitional stage shifts toward the next “Global Adoption Phase” in 2021–2026 (IIRC, 2019). In response to the transition to IR, and because of the theoretical arguments mentioned earlier, a framework must be developed to not only shed light on the importance of IR transition to Malaysian companies but also to provide insights about the role of CG and SR in this transition.

This proposed conceptual framework aims to provide a better understanding of the relationship between governance and IR and the effect of sustainability on this relationship. It incorporates three main variables: (a) the independent variable is CG, which includes the MCCG 2017 and board of directors’ characteristics; (b) the dependent variable is IR disclosure level; and, finally, (c) SR is the variable that moderates the relationship between these two, as shown in Figure 1.

Conceptual framework linking corporate governance, sustainability reporting, and integrated reporting disclosure.

The framework supposes that among the influencers on IR, CG mechanisms, including code adherence and BOD, are considered extremely important, as the decisions about IR scope and quality start at the boardroom. Consist with that, IIRC and the South African King III Report on Governance confirmed the CG role in producing a high-quality, integrated report and establishing a suitable credibility-enhancing process (Wang et al., 2019). Alongside that, firms with long involvement and experience in SR are in a better position to adopt IR. The required systems, assurance processes, and internal controls have been established to assure top management that high-quality, nonfinancial information to support the preparation of an integrated report is readily available (Bursa Malaysia, 2017).

Based on the above consideration, this study argues that the relationship between applying the MCCG Practice 11.2 and IR disclosure level could be stronger in firms that follow GRI standards and issue sustainability reports. Also, the influence of the board of directors’ characteristics on IR disclosures could be better in the firms with higher SR. In other words, the effectiveness of the BOD in enhancing and putting pressure on the firm’s management to increase the IR disclosure could be stronger if a firm has SR in place. According to Ngu and Amran (2019), adopting SR will assist corporate boards to fulfill their governance duties and responsibilities, and to create and maintain the trust in their work.

The practical implications of the proposed conceptual framework outlined in this study are very useful to Malaysian companies. Companies that already have SR can be motivated to follow the IR framework, which increases transparency and reduces information asymmetries. This method could also be helpful for practitioners to identify the transitions in corporate reporting among Malaysian companies. Finally, this study is compatible with the Malaysian government 2030 agenda in achieving the UN sustainable development goals because IR disclosures are in line with achieving these goals.

Method

This article provides a conceptual framework to set a base for future research to empirically examine the moderating effect of SR on the relationship between MCCG 2017, the BOD, and IR disclosure level. The target research population consists of the 841 PLCs in the main market of Bursa Malaysia. However, the research sample comprises the top 100 companies based on their market capitalization (RM2 billion or more) in the Financial Times Stock Exchange (FTSE) Bursa Malaysia for two reasons: (a) the MCCG identifies certain practices and reporting expectations that only apply to those companies; (b) Practice 11.2 encouraged only large companies to adopt IR. Therefore, the aforementioned top 100 companies are more likely to respond to the MCCG and Bursa Malaysia requirements regarding the adoption of IR.

For future researchers, the best method to collect data in this type of research is the content analysis method, which assists the collection and analyses of the secondary hand-collected data from the company’s annual reports. The study proposes to collect data for 5 years over the period 2015–2019 because this period will cover 2 years before the issuance of MCCG 2017 call of IR and 2 years after.

Furthermore, to measure the variables and empirically investigate the relationships in the proposed framework, this study proposes to assess the IR disclosure practices level of Malaysian PLCs using IR disclosure index. This index should follow the IIRC framework and reflects various studies (see Haji & Anifowose, 2016b; Pistoni et al., 2018; Rivera-Arrubla et al., 2017). Also, to measure SR, this study suggests using the Zahid et al. (2019) sustainability disclosure index because it was adopted according to GRI standards and Bursa Malaysia SR guidelines. Furthermore, the quantitative methodology within the positivist framework may be used to examine the relationships between variables using the regression analysis.

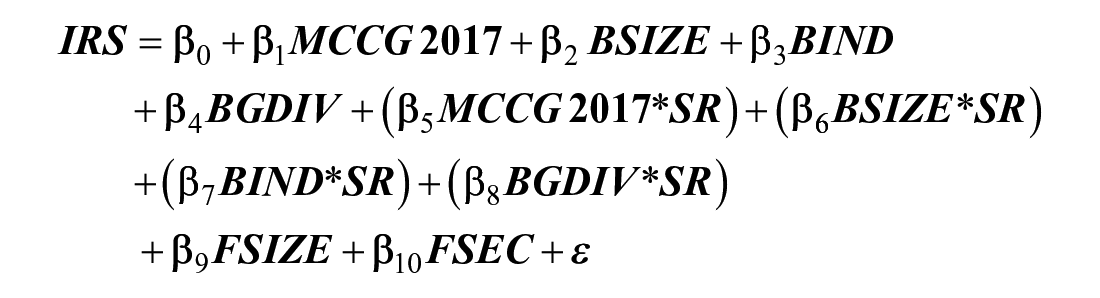

The research framework has two main relationships. Therefore, two regression models are proposed in this article to investigate the impact of CG and SR on the level of IR disclosure of the Malaysian PLCs. The study suggests using the following ordinary least squares (OLS) regression model:

To investigate the moderating effect of SR on the relationship between CG and the level of IR disclosure of the Malaysian PLCs, the study suggests using the following OLS model:

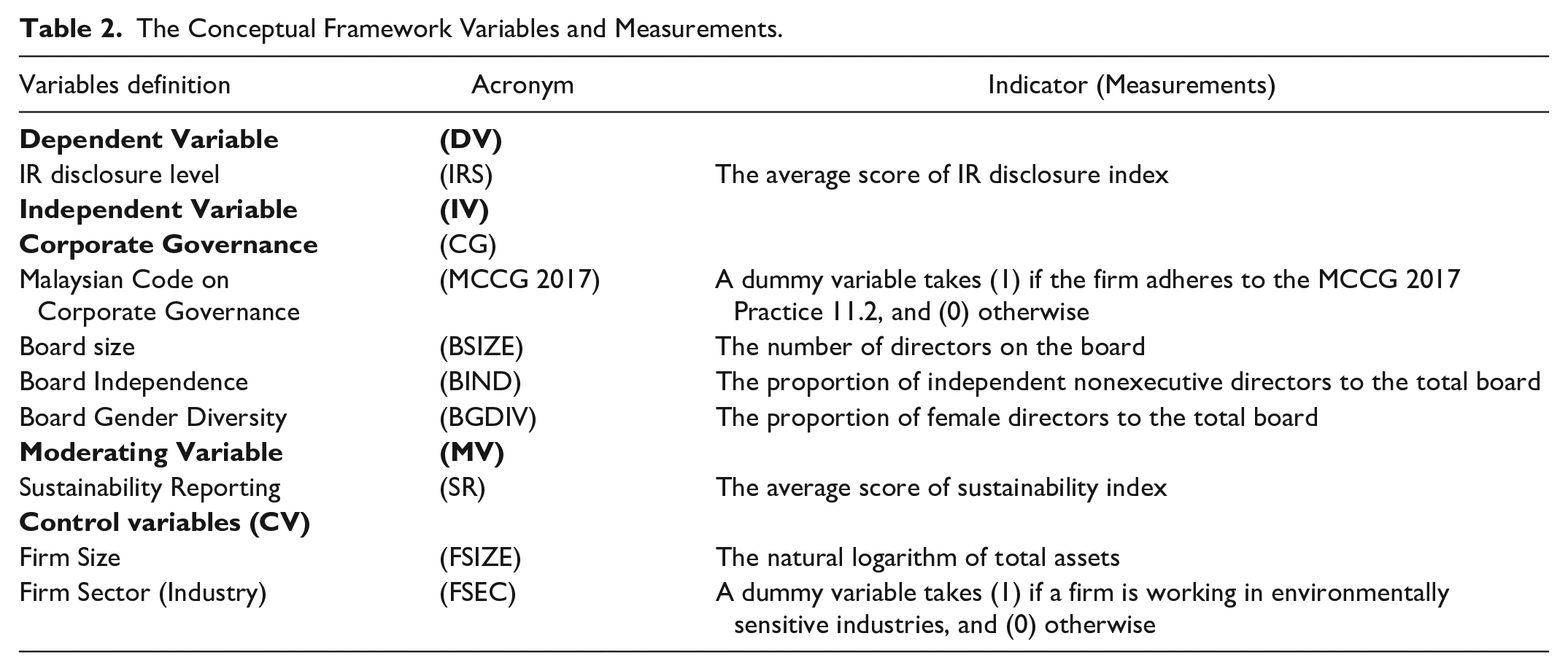

The operationalization of dependent, independent, moderating, and control variables and their indicators are given in Table 2.

The Conceptual Framework Variables and Measurements.

Conclusion and Future Research

Corporate reporting is considered the primary tool that shows how firms can create value over time. Producing separate financial and nonfinancial reporting has become insufficient to describe how an organization can create value over time. IR is a new disclosure technique that gives a holistic picture of a firm’s activities by including comprehensive information covering economic, social, environmental, and governance issues in one report. It shows how firms create value through business models, which helps stakeholders to understand the firm well and make better decisions. Therefore, the value creation process is the most essential concept of IR. According to this process, organizations should make their reporting wider to contain all the key resources and capital used to generate their business activities.

Malaysia is among the most rapidly growing and emerging economies in Asia; it is considered a distinctive country in comparison with other developing countries, and its status is close to becoming a developed country. Recently, Malaysian companies have rapidly increased their various types of voluntary disclosures. SR and IR are the most recent reporting techniques that appeared in Malaysia. Also, these two reporting styles grabbed the attention of various professional institutions and government organizations in Malaysia; therefore, to study them became imperative.

To set a base for future empirical research, this study proposes a conceptual framework to empirically examine the moderating effect of SR on the relationship between the MCCG 2017 call and BOD on the IR disclosure level for the Malaysian PLCs. Prior studies provided some shreds of evidence on the positive consequences and advantages of SR and IR. For instance, the adoption of these approaches will lead to improving information quality, relevance, and transparency; moreover, they can be helpful in reducing information asymmetry and regulatory risk, enhancing reputation and brand value, and finally increasing the organization value and market position.

The implication of the proposed framework is not only to provide a better understanding of the relationship between CG and IR, but also insights to academics and practitioners about the role of CG and SR in the transition to IR. We hypothesize that the impact of CG proxies on the IR disclosures level could be stronger in firms that follow GRI standards and issue sustainability reports. IR could be very useful for Malaysian PLCs. We propose that companies that already have SR follow the IR framework, which increases transparency and reduces information asymmetries.

IR is still a researchable area; future research can empirically test and validate this study’s proposed conceptual framework. Moreover, the impact of other factors such as ownership structure, audit committee, and risk committee on the level of IR disclosure can also be investigated. Last but not least, a comparison between IR disclosure practices in Malaysia and other Asian countries, such as Singapore and Indonesia, can also be conducted by using the proposed framework.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by the Universiti Teknologi PETRONAS, Malaysia, under the Graduate Assistantship Scheme for the first author.