Abstract

Accounting strategic management to competitiveness and financial performance, including business operations of construction business organizations. This study aimed to investigate whether accounting strategic management remains a significant factor in sustainable construction business organizations through interviews with 30 Key informants, and the causal factors relationship to impact accounting strategic management in sustainable construction business organizations through a survey by questionnaire with 330 samples data in construction business organizations, Thailand. The findings of strategic accounting management on the factors include corporate and management accounting strategies, management accountants’ role, accounting information systems, and effective organizational performance, which are the impact of direct and indirect influences in sustainable construction business organizations. The effect of accounting strategic management on achieving business goals and objectives plays an important role in impacting the efficient financial operations of sustainable construction business organizations.

Plain Language Summary

This study explores how knowledge is shared and exchanged among groups involved in accounting strategic management in construction business organizations projects. These projects often require collaboration between stakeholders, such as construction businesses, researchers, business entrepreneurs, and chief accountants, to create new and improved. The research identifies four key factors that influence how well these groups can share knowledge of corporate and management accounting strategies, management accountants’ role, accounting information systems, and effective organizational performance in sustainable construction business Organizations.

Introduction

Accounting information represents business operations, enabling entrepreneurs to know business performance, financial status, and effective competitiveness to be used as analytical tools and the benefit of strategic management to strengthen performance effectiveness (Sasong & Wingwon, 2016). Therefore, the business operators and accounting system of the parties in the business organization to the professional worker is important, because the organization will know whether the operation to profitable (Alafeef, 2015). Effective business performance is to be managed strategically in the accounting process by standards and suitability. Accounting information is also a tool that allows entrepreneurs to know the problems that arise with business operations to be able to problems promptly (Pakdee, 2021). Accounting strategic management is an important part of the success of business organizations, and business entrepreneurs because it supports the management of the organizations in various issues, for example, planning by accounting systems provides information about the results of the operations that can be used to make estimates and predictions of information to should occur in the future to meet the goals and objectives of business operations (Alabdullah, 2019). Communicating information from the goals of business operations to what employees have to do in the form of a master budget in various aspects, including raw material procurement planning, operating expense planning, and cash of working capital planning (Alamri, 2019). Business executives or entrepreneurs must have accounting strategic management from the assignment, and distribute plans according to the duties of each department must help each other to achieve success so that operators can operate conveniently and smoothly, problem-solving in leading to the overall success of the business operation of the organizations.

While, the management accountant’s role in the critical business world because under competitive conditions more serious and the economic environment and various macro factors as rapid change, where the management of capital resources, investment of capital resources, monitoring of the efficiency of capital utilization, and controlling the achievement of business growth goals, including, growth in operating value to sustainable business operations are important (Gomes et al., 2022). Tracking and evaluating employee performance to be by the duties and responsibilities to achieve the objectives and goals of the organization in accounting strategic management to reflect the overall business performance of the organizations. Accounting management of business owners, and business operators, is critical in supporting and driving business organizations to have accurate accounting and financial reporting that is useful for decision-making economically throughout the corporate and management accounting strategies, management accountants’ role, accounting information system, and organizational performance (Keskin et al., 2021). Accounting management including corporate and management accounting strategies, management accountants’ role, and accounting information systems to considered to be important in communicating the financial information of an entity’s financial position, and results on the operation of business enterprises (Kocyigit & Tabak, 2020) Financial information produces reports for management accounting, which are prepared to meet the needs of executives and business operators in their respective roles and functions.

However, business executives and entrepreneurs facing highly competitive conditions will need financial and non-financial information for decision-making, and in highly competitive costing systems, performance appraisal systems that essential for the survival of the business and its successful performance. This study analyzes accounting strategic management in sustainable construction business organizations and the causal factors relationship impact accounting strategic management in sustainable construction business organizations plays a crucial role in enhancing organizational performance by integrating finances to support strategic decision-making and accounting that aligns with strategic objectives for competitiveness and financial performance in sustainable construction business organizations in a case study of Chiang Rai Province, Thailand.

Literature Reviews

Accounting information represents the progress of a business and helps entrepreneurs know their performance, and financial position, can be used as a tool for forecasting analysis or for the benefit of business management. Therefore, an accountant is a professional practitioner who is very important to the business because the organization will know whether the performance of their organization is profitable—loss, good or bad performance will be the accounting must be made to know and must be made by the specified accounting standards (YahiaMarzouk & Jin, 2022). Determining the strategy of the business, and investing in high accounting systems to be used to increase the value of the business. Because it focuses on the decision-making process that requires the understanding of accountants and executives to determine business strategies. Accounting is the key to management and applying accounting information presented by accountants to planning, decision-making, controlling, and directing management in an organization it plays a very important role in the preparation of the financial statements of the entity (Panjaitan et al., 2018). Financial information and financial strategies are used as management tools for corporate strategy to monitor and plan for the company to operate efficiently (Chaichok & Kasorn, 2023). Thus, accounting information management accountants of business organizations are of great importance today as they oversee and drive financial strategies through infrastructure in the accounting of the business as uniqueness in the career and income of the sustainability. Accounting strategic management has a wide scope by users of strategic management accounting data to be correlated with success such as accounting information systems, management accountants’ role, corporate strategy, strategic management accounting, and organizational performance (Ojra et al., 2021). The formulation of accounting strategies and the implementation of strategic management accounting by the nature of the data that is essential to strategic management by the outcome is accounting innovation. As the accountant participates in strategic decisions, the results are rarely seen immediately but gradually. Immerse yourself in the cost estimation principle of the development of a strategic management accounting system that relates to the operating costs of a business organization (Phornlaphatrachakorn & Na-Kalasindhu, 2020). Accounting strategic management for used in developing and monitoring business strategies that enhance organizations’ operational efficiency and success. While, accounting strategic management enables executives to fulfill their strategic decision-making, capabilities and the provision of information for the strategic decision-making process (Wajdi & Arsjah, 2019). Forecasting future events to shape sustainability in a business.

However, this study focuses on accounting strategic management in the conceptual context of providing essential information with direct and indirect impacts on sustainable construction business organizations and envisages long-term business operations to support strategic decision-making, increasing competitiveness and sustainability of business. Accounting strategic management of accountants in decision-making using strategic management accounting strategies that play a larger role than performance-based strategic management processes, and further adjusting strategies by integrating customer, HR, and financial processes into corporate and management accounting strategies, management accountants’ role, accounting information system, and organizational performance (Saqib & Zhang, 2021). Under the conditions in the accounting perspective by evaluating from competitors who have shown the accounting model according to the set goals. Accounting strategic management is the management and analysis of a company’s financial data, competitor costs, competitor competence, cost structure, and auditing of corporate and competitor strategies in the marketplace (Stocker et al., 2021), and service-oriented management. Therefore, the challenges to impact accounting strategic management in sustainable construction business organizations to use of accounting information within an organization is used as a tool by management and business operators to assist in decision-making, planning, control, and comprehensive evaluation including corporate and management accounting strategies, management accountants’ role, accounting information system, and effectiveness organizational performance (Ojra et al., 2021; Phornlaphatrachakorn & Na-Kalasindhu, 2020; Saqib & Zhang, 2021; Stocker et al., 2021), which the frameworks to investigate whether accounting strategic management remains a significant factor in sustainable construction business organizations, and the causal factors’ relationship to impact accounting strategic management in sustainable construction business organizations in Chiang Rai Province, Thailand as leading the questions as follows:

(1) What is the accounting strategic management of the factors to indicators in sustainable construction business organizations?

(2) How is the causal factors relationship to impact accounting strategic management in sustainable construction business organizations with empirical data?

Methodology and Conducting

Research design as a mixed method research adopted for this research involves both qualitative and quantitative data to combine participatory action learning to multi-contextual and cultural perspectives for the research to complete and provide the explanations and conclusions based on the research results of the study on the accounting strategic management in sustainable construction business organizations and the causal factors relationship to impact accounting strategic management in sustainable construction business organizations. The spatial studies took place in the area of 10 construction business organizations in Chiang Rai Province, Thailand. Concerning the research participants and tools, the study involved 30 key informants from business entrepreneurs and chief accountants, they were selected through purposive sampling and focus group. Additionally, 330 samples from accounting officers, and operational personnel, respectively were involved under the selection technique of multi-stage cluster sampling.

The research instruments used for data collection included: (1) Structured interview addressed to leading the organization with accounting strategic management, it consisted of four interview topics all concerned with the corporate and management accounting strategies, management accountants’ role, accounting information system, and effectiveness of organizational performance of structure, it contained questions like—What is the accounting strategic management of the factors to indicators in sustainable construction business organizations? (2) A semi-structured questionnaire addressed to leading the organization with causal factors relationship to impact accounting strategic management in sustainable construction business organizations, aimed to explore the causal factors relationship from the perceptions of the sample. It consisted of five rating scales divided into five parts and each part addresses questions on a specific causal factors relationship as follows, part 1; general information, part 2; the question of corporate and management accounting strategies, part 3; the question of management accountants’ role, part 4; the question of accounting information system, part 5; the question of effectiveness of organizational performance. The whole questionnaire included open-ended suggestions with a reliability value of .89.

Data was collected throughout a synthesis of the literature, in-depth interviews with key informants, including business entrepreneurs and chief accountants of 30 people, from notes and tape recordings of interviews were conducted to study accounting strategic management on factors and indicators in sustainable construction business organizations. A survey of 330 operational accounting officers and officers was undertaken to examine the causal factor relationship to impact accounting strategic management in sustainable construction business organizations.

Data analysis in accounting strategic management on factors and indicators is a qualitative data analysis that relies on six steps: (1) data collection, (2) transcription, (3) identifying themes, (4) categorizing data, (5) data interpretation, and (6) conclusion. The causal factor relationship to impact accounting strategic management in sustainable construction business organizations is a quantitative data analysis by finding percentages, means, standard deviations, skewness, kurtosis, correlation coefficients, including structural equation models. For the statistical values and the level of acceptance to check the fit of the measurement model and the structural equation model with the empirical data, the model will be fit with the empirical data if it consists of a Chi-square value (χ2) not significant (p-value ≥ .05) or a proportion value/dfχ2 ≤ 4.00, CFI, TLI values ≥ .90, SRMR, RMSEA values < .08 (Bollen, 1986).

Results and Discussion

The results of accounting strategic management in sustainable construction business organizations and the causal factors related to the impact of accounting strategic management in sustainable construction business organizations were followed.

Accounting Strategic Management in Sustainable Construction Business Organizations

The significance of accounting strategic management in sustainable construction business organizations on four factors such as (1) the corporate and management accounting strategies to four sub-factors (1.1) defender strategic and analysis strategic, (1.2) prospector and responsive strategies, (1.3) strategic costing and planning and control, (1.4) strategic decision-making, competitors accounting, and customer accounting usage, (2) management accountants’ role to 3 sub-factors (2.1) financial accounting and fund management, (2.2) tax planning management and information system management, (2.3) financial and accounting risk control, (3) accounting information system to 3 sub-factors (3.1) timeliness and understandability, (3.2) accurate and completeness, (3.3) verifiability, (4) effectiveness of organizational performance to 4 sub-factors (4.1) financial perspective, (4.2) customer perspective, (4.3) internal process perspective, (4.4) learning and growth perspective are 14 indicators as shown in Table 1.

The 4 Factors, 14 Sub-Factors, and 14 Indicators of Accounting Strategic Management.

Source. Own compilation.

From the results on the factors of accounting strategic management in sustainable construction business organizations as (1) corporate and management accounting strategies to sub-factors of defender strategic and analysis strategic, prospector and responsive strategies, strategic costing and planning and control, strategic decision making, competitors accounting, and customer accounting usage, (2) management accountants’ role to sub-factors of financial accounting and fund management, tax planning management and information system management, financial, and accounting risk control, (3) accounting information system to sub-factors of timeliness and understandability, accurate, completeness, verifiability, and (4) effectiveness organizational performance to sub-factors of financial perspective, customer perspective, internal process perspective, learning, and growth perspective. Because the service-oriented management, trying to protect market share and offering superior quality services at competitive prices, creating strategies to take advantage of opportunities that arise to remove organization weaknesses, for example, taking advantage of the opportunity comes from the growth of internet technology to shorten the work process (Sugiyarti & Asmilia, 2020; Sukumar et al., 2020). The determining the ability of the service system with quickness, the entire process of delivering products to customers with reliability, flexible work system to allow the organization to meet the needs of customers, focusing the allocation of resources to limited, focusing market penetration with customers to suit the target market to create satisfaction in the markets to more than competitors (Intharaprasit, 2020). The advantages of production and operating costs per unit are low, managing different resources, and organizational operations as economical and efficient, the ability to sell goods and services at lower prices than competitors, planning to start from each division in activities of a business, accounting for budget of each division, bring together a total financial plan of the business to control the budget and finances of organization to maximize profits (Thapayom, 2021). Meanwhile, business financial structuring involves financing the business needs, working capital allocation, debt reduction, debt repayment extension, policy formulation, financial structure, and short-term and long-term planning (Guilding et al., 2000). Operation of the entity by rapidly the changing environment, new management methods on total quality control management, activity-based costing, activity-based management, competitive strategy planning to enhance the ability to anticipate the movements, and reactions of competitors to other companies’ offensive actions, structured competitor analysis to future goals, current strategies, assumption, competitor capabilities, collecting customer details, customer profiles, requirements, creating highest satisfaction to customers with quality, price and delivery of products, taking in account to value and diversity of customers that will bring financial returns and market share (Bansal & Bashir, 2023). Thus, accounting strategic management in sustainable construction business organizations is crucial for improving organizational performance and achieving sustainable business outcomes, enhancing organizational performance by integrating finances to support strategic decision-making, and strategic management to competitiveness and financial performance.

Causal Factors are Related to the Impact of Accounting Strategic Management in Sustainable Construction Business Organizations

The causal factors are related to the impact of accounting strategic management in sustainable construction business organizations on four variables of corporate and management accounting strategies (CMAS), management accountants’ role (MAR), accounting information system (AIS), and effectiveness of organizational performance (EOP) of the results were followed:

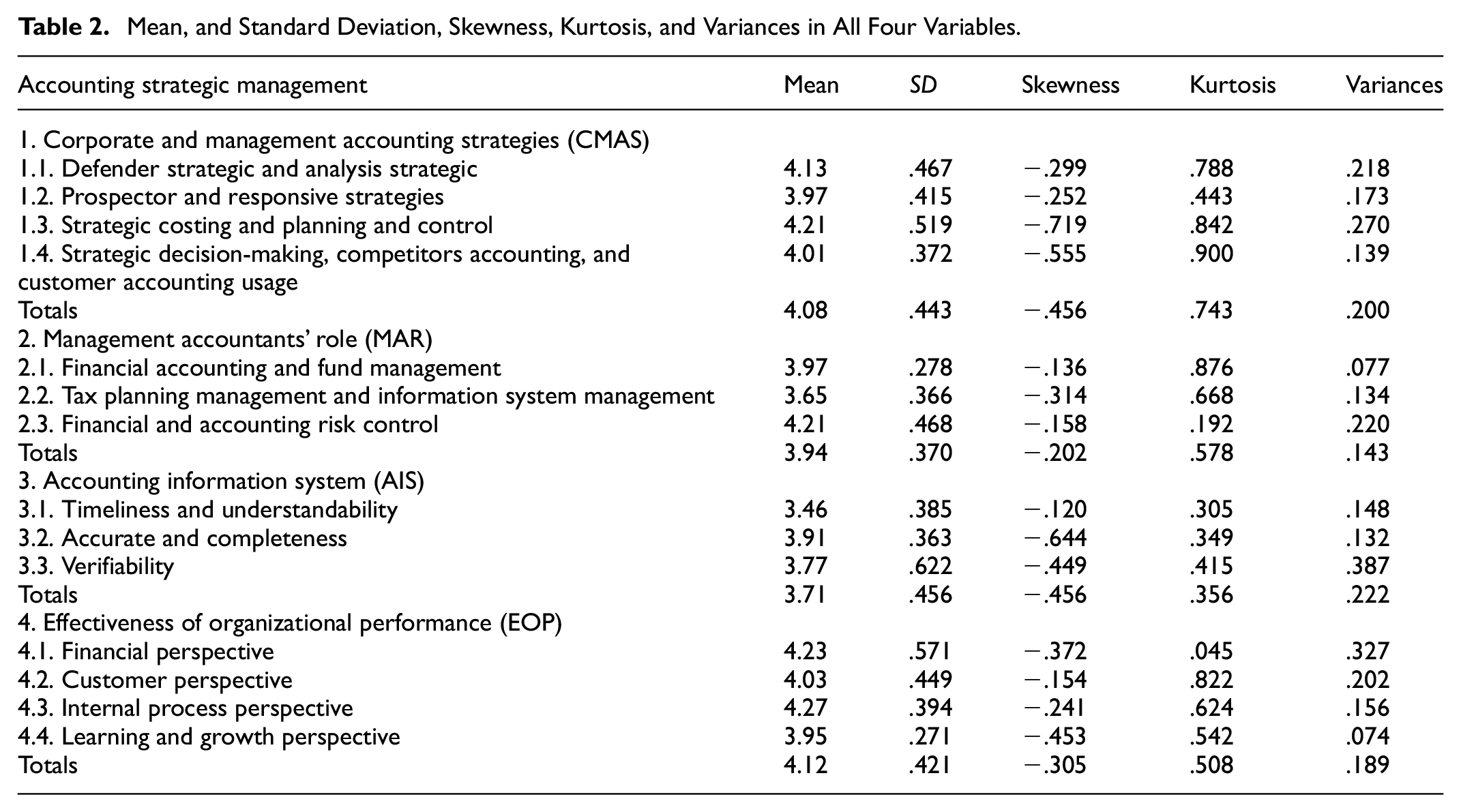

Which, is the level of accounting strategic management in sustainable construction business organizations in all five variables at high levels (Mean of 3.96), when considering each variable separately, it was found that the variable with the highest average value was the effectiveness of organizational performance (Mean of 4.12), next in lines such as corporate and management accounting strategies (Mean of 4.08), management accountants’ role (Mean of 3.94), the part with the lowest average value was accounting information system (Mean of 3.71), respectively. So, the skewness to a negative value is between −.022 to −.456, and kurtosis to a value is between .356 and .743, as shown in Table 2.

Mean, and Standard Deviation, Skewness, Kurtosis, and Variances in All Four Variables.

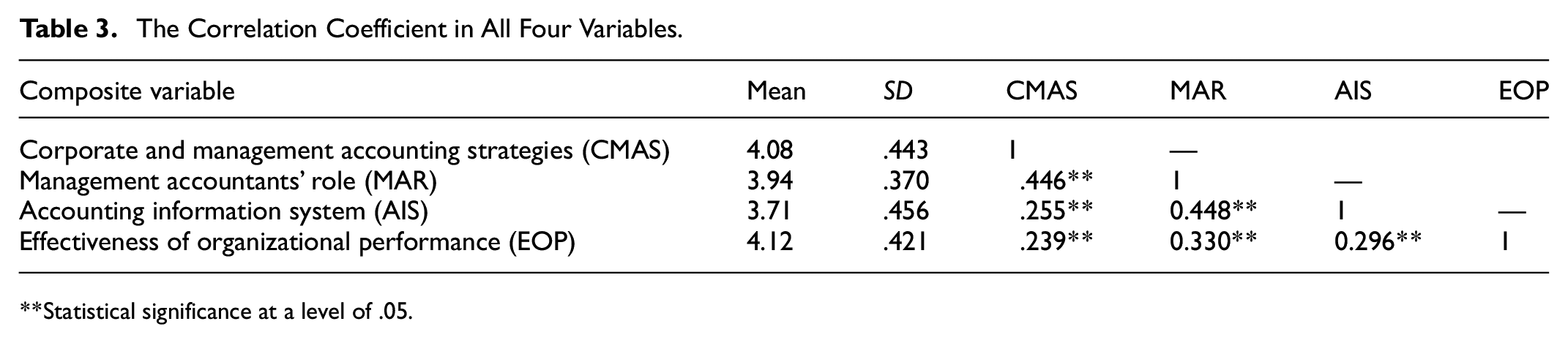

While the causal factors relationship to impact accounting strategic management in sustainable construction business organizations of all four variables are consistent with empirical data, considering the fit index values that passed the acceptance criteria (Chi-square of 148.69, df of 748, RMR of .023, AGFI of .92, RMSEA of .047), with both direct and indirect influences being positive to consistent the empirical data at statistical significance a level of .05, as shown in Tables 3 and 4, Figure 1.

The Correlation Coefficient in All Four Variables.

Statistical significance at a level of .05.

Direct Influence: DE, Indirect Influence: IE, and Total Influence: TE in all Four Variables.

Statistical significance at a level of .05.

The model of causal factors relationship to impact accounting strategic management in sustainable construction business organizations.

Regarding the causal factors related to the impact of accounting strategic management in sustainable construction business organizations on corporate and management accounting strategies (CMAS), management accountants’ role (MAR), and accounting information system (AIS) with both direct and indirect influences being positive to the effectiveness of organizational performance (EOP) in consistent the empirical data at statistical significance at a level of .05. In addition, the impact of accounting strategic management is the importance of accounting information should be emphasized in business management in terms of planning, controlling, directing, and decision-making, because accounting information reflects operations, and can be used to forecast the future (Adamu & Haruna, 2020). Proper cost management of the business, will lead to achieving the organization’s goals effectively. The assignment of accounting workload must be clear for the accountant to work effectively and efficiently, monitoring and evaluating accounting performance on a continuous and systematic basis, so that the evaluation system is an objective approach system (Correia et al., 2021; Hair et al., 2019). The operational efficiency of a business by profit is one of the financial measures and can be measured by customer sales growth, revenue share from new customers, employee revenue, costs relative to competitors, rate reduction of investment and development costs as well as return on investment (Valdiansyah & Augustine, 2021). Also, the organizational performance and accounting meet to needs of customers on efficient merchandise management, short cycle times, public relations advertising, modern operating systems and tools using modern technology of incentives with customers who have come to buy products continuously to obtain product quality at a fair and appropriate price in line with the needs of customers (Hossain et al., 2022). Ability to improve internal procedures, improve the organization’s internal operations, increase operational efficiency, solve problems from internal work processes, work efficiency, work on information systems, delivery time, and cost management (Dalwai & Salehi, 2021). Accounting strategic management significantly impacts organizations by aligning financial information with strategic objectives, thereby facilitating informed decision-making. Which enhances organizational competitiveness and financial performance. Thus, the impact of accounting strategic management to evident across various industries, including manufacturing, where it facilitates informed decision-making and sustainable performance. Business entrepreneurs and accounting executives of accounting information should be emphasized in business management in terms of planning, controlling, directing, and decision-making, because accounting information reflects operations, and, can be used to forecast the future to achieve sustainable construction business organizations.

Conclusion

The accounting strategic management in sustainable construction business organizations on corporate and management accounting strategies into defender strategic and analysis strategic, prospector and responsive strategies, strategic costing and planning and control, strategic decision making, competitors accounting and customer accounting usage, management accountants’ role on financial accounting and fund management, tax planning management and information system management, financial and accounting risk control, accounting information system of timeliness and understandability, accurate and completeness, verifiability, and effectiveness of organizational performance as financial perspective, customer perspective, internal process perspective, learning, and growth perspective. Meanwhile, the causal factors related to the impact of accounting strategic management on corporate and management accounting strategies, management accountants’ role, and accounting information systems with both direct and indirect influences being positive to the effectiveness of organizational performance inconsistent with the empirical data at statistical significance at a level of .05. However, the development of employee knowledge and competence, employee satisfaction, morale of employees, development of systems to facilitate work, working the environment, and skills, modern information systems towards sustainable construction business organizations.

Implementation

Thus, effective implementation of accounting strategic management in sustainable construction business organizations for improving organizational performance and achieving sustainable business outcomes. Which, accounting strategic management plays a crucial role in enhancing organizational performance by integrating financial information to support strategic decision-making, and providing tools and techniques that align with strategic objectives to improve competitiveness and financial performance. The impact of accounting strategic management, where it facilitates informed decision-making and sustainable performance. For business entrepreneurs and accounting executives to importance of accounting information should be emphasized in business management in terms of planning, controlling, directing, and decision-making, because accounting information reflects operations, and, can be used to forecast the future. Accounting executives should have formal and informal two-way communication that will result in a thorough awareness and understanding of the objectives and guidelines set. This will lead to achieving the organization’s goals effectively.

Footnotes

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.