Abstract

This study evaluates the impact of China’s Film Industry Promotion Law—the first industry-specific law in the cultural sector—on the financial and social performance of Chinese film enterprises. Using a Propensity Score Matching-Difference- in-Differences (PSM-DID) approach with data from A-share listed companies (2011–2019), the study finds that while the law improved social performance, it led to a decline in financial performance. However, overall corporate performance significantly improved. These results highlight the dual role of regulatory frameworks in balancing social benefits and economic outcomes. The study fills a research gap, introduces an innovative analytical framework, and enhances understanding of how institutional environments affect corporate performance, offering valuable insights for shaping film industry policies in developing countries.

Plain Language Summary

This study explores how China’s Film Industry Promotion Law, implemented in 2017, affects the performance of film companies. Using data from 2011 to 2019, the research employs a method that combines matching techniques with a difference-in-differences approach to compare the effects of the law on film companies and non-film companies. The results show that while the law led to a decline in the financial performance of film companies, it improved their social performance, particularly in corporate social responsibility (CSR) ratings. Overall, the companies’ performance improved when considering both financial and social aspects. This study is important because it shows the complex effects of government regulations, which aim to balance cultural and economic goals. The law helped film companies achieve social benefits, such as promoting cultural values, but also imposed financial challenges, highlighting a trade-off between economic success and societal contributions. The findings can help policymakers refine future regulations and guide other countries considering similar laws for their cultural sectors.

Keywords

Introduction

From the initiation of China’s film legislation process in 2003 (Cheng, 2021) to the submission of the draft to the National People’s Congress on October 30, 2015 (Shi & Liu, 2015), and its eventual approval on November 7, 2016 (The National People’s Congress of China, 2016), the Film Industry Promotion Law of the People’s Republic of China (hereafter referred to as the Film Law; Film Industry Promotion Law of the People’s Republic of China, 2016) marked a significant milestone in the evolution of the nation’s cultural policy framework. Officially implemented on March 1, 2017, the Film Law is the first industry-specific law in China’s cultural sector (Wu, 2019). Its promulgation is widely regarded as a watershed moment (Dong et al., 2017), signifying the institutionalization of China’s film reform policies (Guan, 2020) and laying a legal foundation for the industry’s sustainable development (Zhang, 2017).

The Film Law embodies the Chinese government’s perspective on the film industry, as explicitly stated in Article 3 of Chapter 1: film activities should “prioritize social benefits while achieving a synergy between social and economic benefits” (Film Industry Promotion Law of the People’s Republic of China, 2016). This principle underscores the government’s emphasis on the social value of the film industry, recognizing its role in fostering cultural cohesion and ideological dissemination. At the same time, it reflects an intent to maintain economic viability, striving for a balance where social objectives are achieved without compromising economic performance—particularly significant as China has become the world’s second-largest film market since 2012 (MPAA, 2012).

Despite its symbolic and regulatory importance, the empirical effects of the Film Law remain underexplored. Existing research has largely focused on legal interpretation or descriptive commentary, while systematic assessments of its impact on enterprise-level performance are limited. This absence of empirical evaluation not only impedes the refinement of cultural legislation but also restricts international understanding of how state-led interventions affect market-driven cultural industries.

This study addresses this gap by evaluating the impact of the Film Law on the financial and social performance of China’s film enterprises. Leveraging the law’s implementation as a quasi-natural experiment, we employ a Propensity Score Matching and Difference-in-Differences (PSM-DID) framework to analyze panel data from A—share listed firms between 2011 and 2019. This empirical design allows us to assess the policy’s causal effects while mitigating selection bias. Our treatment group consists of firms in the film industry, while the control group comprises matched firms from other sectors.

Beyond empirical identification, this study is theoretically motivated by perspectives from institutional theory and cultural political economy. The Film Law, by embedding social mandates into market operations, can be interpreted as a form of coercive institutional pressure (DiMaggio et al., 1983; Scott, 2013) that compels firms to reorient toward legitimacy-oriented social performance. Simultaneously, it reflects broader ideological ambitions in cultural governance, resonating with scholarship on cultural policy as a vehicle for symbolic regulation and value engineering (Hesmondhalgh, 2018; Hesmondhalgh & Pratt, 2005; Miller & Yúdice, 2002). These perspectives frame our interpretation of the observed trade-off between enhanced corporate social responsibility and declining financial returns.

This study makes three key contributions. First, it provides novel empirical evidence on how regulatory frameworks shape both financial and social outcomes in the cultural industries of developing economies. Second, it applies an integrated PSM-DID strategy to cultural policy analysis, offering a replicable model for future policy impact evaluations. Third, by situating China’s film regulation in broader theoretical discourse, it contributes to a more nuanced understanding of how institutional environments influence firm behavior in state-guided cultural markets.

Literature Review

Empirical Gaps in Film Policy Evaluation

Although the Film Industry Promotion Law represents a landmark in China’s cultural governance, empirical studies assessing its long-term effects remain scarce. Initial analyses following its 2017 enactment primarily focused on textual interpretation, policy goals, or doctrinal commentary (Gu, 2017; Lai, 2017; Zhu, 2017), offering limited insights into its implementation outcomes. Even subsequent literature has largely remained descriptive or focused on isolated case studies (Cheng, 2021; Hu & Chen, 2023; Wu, 2019), rarely addressing firm-level behavioral responses or organizational adaptation. Unlike environmental or industrial policy, cultural regulation lacks a mature empirical evaluation tradition, partly due to its ambiguous objectives, symbolic content, and multi-layered implementation.

This analytical gap has broader implications for cultural economics and policy analysis. International scholars increasingly argue that cultural policy must be understood as a structuring force in creative labor and symbolic production (O’Brien & Oakley, 2015; O’Connor, 2007). O’Connor (2007) emphasizes the need for empirical validation to complement normative policy models, while O’Brien and Oakley (2015) stresses the lived realities of creators under regulatory regimes. Yet in the Chinese context, these international perspectives remain underapplied, leaving a crucial gap in understanding how cultural policy shapes economic and symbolic outcomes at the organizational level.

Comparative Cultural Policy Models

Insights from international cases offer critical context for analyzing the Film Law. In South Korea, the Basic Law for Cultural Industry Promotion simultaneously enables government oversight and subsidizes content production to foster industrial competitiveness (Jin, 2023; Kwon & Kim, 2013). Singapore’s Infocomm Media Development Authority (IMDA) enforces ideological boundaries while offering generous support for local creators through training, grants, and international distribution mechanisms (Kim, 2022; Yu, 2008). These examples demonstrate that cultural governance can integrate normative regulation with capacity-building policies.

Such dual-track models suggest that state-led cultural policy need not choose between ideological coherence and market viability. Instead, as Miller and Yúdice (2002) argues, successful frameworks mobilize policy tools both as regulatory instruments and as development levers. For China, where symbolic legitimacy and industrial sustainability are intertwined policy goals, these international cases provide a conceptual and strategic benchmark for improving sectorial resilience without sacrificing ideological alignment.

Theoretical Anchors: Institutionalism and Cultural Political Economy

Understanding the Film Law’s impact requires engagement with theories that address both coercive regulation and symbolic governance. Institutional theory explains how policy instruments generate legitimacy pressures that shape organizational behavior (DiMaggio et al., 1983; Scott, 2013). In this framework, firms conform not only for economic survival, but to align with prevailing normative expectations. Such coercive isomorphism is well-documented in CSR literature, especially in politically embedded contexts (Marquis et al., 2011).

Meanwhile, cultural political economy examines how cultural production is embedded in ideological structures and policy rationalities. Garnham (2005) and Hesmondhalgh (2018) describe how regulation shapes not just outputs but also symbolic hierarchies and power asymmetries in creative industries. Miller and Yúdice (2002) introduces the notion of “cultural engineering,” highlighting how policy codifies national values into institutional expectations. These perspectives are particularly salient in China, where state-led cultural policy imposes normative content directives and influences market access, production incentives, and narrative framing.

Integrating these perspectives provides a dual-theoretical lens: institutional theory clarifies how firms adapt strategically to policy pressures, while cultural political economy situates those pressures within broader ideological agendas. This combined approach helps explain the simultaneous rise in CSR signaling and decline in ROA observed in this study—a dual outcome that reflects both symbolic compliance and operational constraint.

Methodological Advances in Cultural Policy Evaluation

Despite the rising popularity of quasi-experimental techniques in industrial policy analysis, such methods remain underutilized in cultural sectors. The Difference-in-Differences (DID) design has been effectively applied to examine policy effects on innovation, ESG metrics, and organizational adaptation (Gupta et al., 2021; Roth et al., 2023), yet few studies have adopted this method for cultural legislation. This gap persists partly because policy shocks in the cultural field are often qualitative, ideologically coded, and difficult to isolate temporally or structurally.

Emerging studies suggest that cultural regulation can induce observable behavioral shifts among firms, particularly in systems characterized by formalized approval procedures and symbolic performance metrics (De Man et al., 2025; Kwon & Kim, 2013). Yet, assessing these impacts poses methodological challenges, given the ideologically embedded and non-randomized nature of policy interventions. To address this complexity, the present study adopts a Propensity Score Matching combined with Difference-in-Differences (PSM-DID) framework. As foundational work on matching methods emphasizes, this design helps mitigate selection bias in observational settings (Stuart, 2010), and has been recognized as suitable for evaluating policy effects in complex institutional environments (Abadie et al., 2023).

Research Design

Following the identified research gaps in policy evaluation studies of China’s cultural industries, this section outlines the empirical strategy employed to assess the causal effects of the Film Law on firm-level performance. Given the quasi-experimental nature of regulatory implementation, the study adopts a Propensity Score Matching–Difference-in-Differences (PSM-DID) approach. This combined method addresses the challenges of non-random policy exposure and enhances causal identification. The following subsections describe the sample selection, model construction, variable design, and validity tests.

Core Principle of the DID Approach

The DID method is a widely used causal inference technique in economics and other social sciences, designed to evaluate the impact of a specific policy or event (Ashenfelter & Card, 1984; Atanassov, 2013; Gruber & Poterba, 1994; Rajan & Zingales, 1996). It achieves this by comparing the changes in outcomes before and after the policy implementation between a treatment group (affected by the policy) and a control group (unaffected by the policy; Abadie, 2005; Athey & Imbens, 2006; Görg & Strobl, 2007; Lach, 2002). In essence, the core principle of DID is to estimate the causal effect of a policy or intervention by examining the difference in changes between the treatment and control groups over time (Brown et al., 2013; Mukherjee et al., 2017). Compared to traditional regression analysis, DID effectively mitigates issues related to endogeneity caused by omitted variables (Abadie et al., 2023; Athey & Imbens, 2022; S. Wang, 2021). The core logic of the DID method can be illustrated in Table 1.

Core Principles of DID.

The main steps involved in implementing the DID approach are as follows:

(1) Data preparation: Collect data on the treatment and control groups before and after the policy implementation.

(2) Model specification: Construct a regression model incorporating time dummy variables, treatment group dummy variables, and their interaction term.

(3) Parameter estimation: Estimate the model parameters through regression analysis, with particular attention to the coefficient of the interaction term, which represents the policy effect.

(4) Parallel trend hypothesis test: The parallel trend hypothesis is a fundamental requirement of the DID method. It assumes that, in the absence of treatment, the outcome variables for both the treatment and control groups would follow a similar trend over time. This implies that prior to the intervention, the changes in outcome variables should be comparable between the two groups. Graphical analysis and statistical tests can be employed to verify whether the parallel trend hypothesis holds.

(5) Robustness checks: Conduct a series of robustness checks, such as placebo tests, to ensure the reliability of the results.

It is important to note that real-world policies are essentially non-randomized experiments (or quasi-natural experiments), making the DID method susceptible to self-selection bias. To address this issue, the Propensity Score Matching (PSM) method can be employed to match each treatment group sample with a specific control group sample, thereby approximating randomization in quasi-natural experiments (Rosenbaum & Rubin, 1983, 1985). This process involves selecting covariates, estimating propensity scores, and performing the PSM procedure. Further, the PSM-DID model integrates PSM with the DID approach to enhance estimation accuracy when the selection of treatment and control groups is non-random (Fowlie et al., 2012; Heckman, Ichimura, & Todd, 1998; Heckman, Ichimura, & Todd, 1997). By using PSM to select control groups with characteristics similar to those of the treatment group and subsequently applying the DID method, this combined approach effectively reduces selection bias, yielding more reliable estimates of policy effects (Böckerman & Ilmakunnas, 2009; Derrien & Kecskés, 2013; Heyman et al., 2007). Therefore, this study adopts the PSM-DID method to evaluate the impact of Film Law on China’s film industry.

Sample Selection

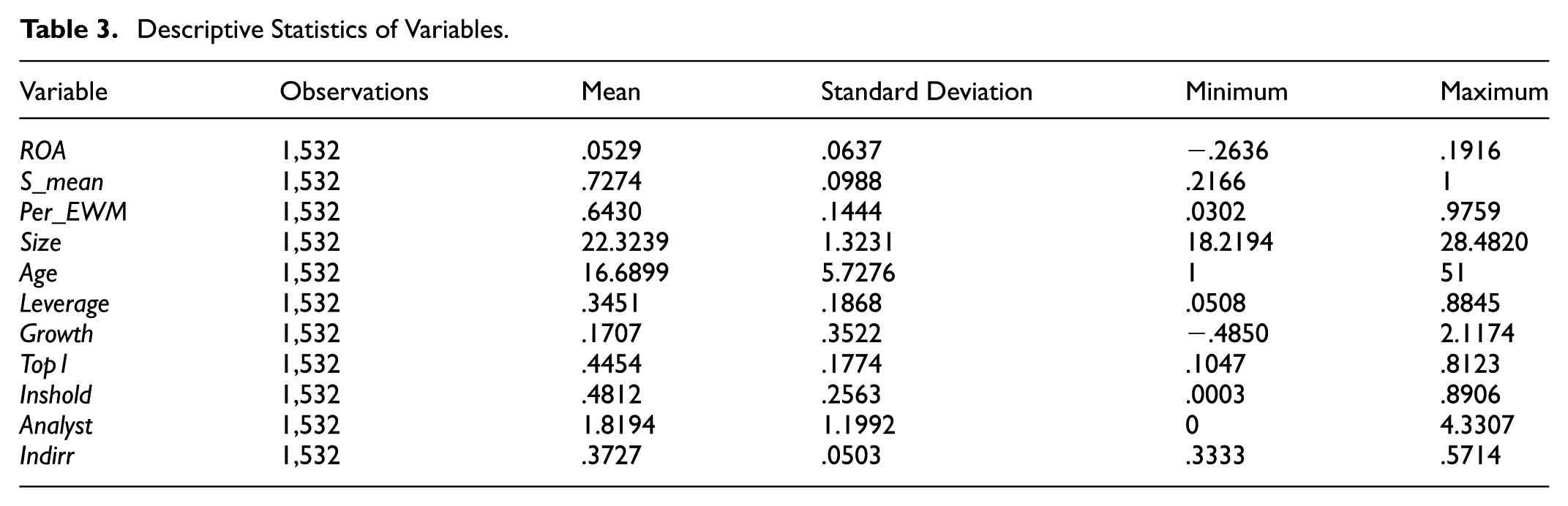

This study selects Chinese A-share listed companies from 2011 to 2019 as the research sample and uses the implementation of the Film Industry Promotion Law of the People’s Republic of China (hereinafter referred to as the Film Law ) as a quasi-natural experiment. The study employs the PSM-DID method to investigate the impact of the implementation of film industry policy on corporate performance. The treatment group comprises listed companies in the film industry, while the control group consists of non-film industry companies matched using the PSM method. Data on institutional ownership are obtained from the WIND database, corporate social responsibility (CSR) ratings are sourced from the Sino-Securities ESG Rating System, and other data are derived from the China Stock Market and Accounting Research (CSMAR) database. The data are processed as follows: (1) financial sector companies are excluded and (2) ST and *ST companies are excluded. Additionally, to mitigate the influence of extreme values, key continuous variables are Winsorized at the 1% and 99% levels.

The treatment group and the construction of the control group using the PSM method are defined as follows. According to the Guidelines for the Industry Classification of Listed Companies issued by the China Securities Regulatory Commission (2012 revision) and based on the scope of activities covered by the film industry, this study defines companies in four secondary industries within the culture, sports, and entertainment sector (R) as film industry companies. These industries include news and publishing (R85), broadcasting, television, film, and sound recording production (R86), cultural and artistic industries (R87), and entertainment industries (R89). These companies form the treatment group. Notably, the proportion of film industry companies within all China’s A-share listed companies is minimal, which increases the likelihood of endogeneity issues caused by omitted variables. To address potential endogeneity issues driven by observable factors, the PSM method is employed to match the treatment group with a control group. Specifically, a 1:6 nearest-neighbor matching approach is adopted to match film industry companies with non-film industry companies. The covariates selected include firm size (Size), firm age (Age), leverage ratio (Leverage), revenue growth rate (Growth), the shareholding ratio of the largest shareholder (Top1), institutional ownership ratio (Inshold), analyst coverage (Analyst), and the proportion of independent directors (Indirr). After applying the PSM method, the final sample includes 1,532 observations, comprising 59 treatment group companies (233 observations), and 898 control group companies (1,299 observations).

Model Specification and Variable Definitions

To examine the impact of film industry policies on corporate performance, this study adopts the PSM-DID method, drawing on the approach used by (S. Wang, 2021). After constructing the sample using the PSM method, a DID model is developed for empirical analysis. The regression equation is specified as follows:

The dependent variable in this study is corporate performance (Performance), which is divided into two dimensions: financial performance and social performance. Drawing on the indicator selection approaches of Chen and Miller (2007) and Xie et al. (2015), this study constructs a performance measurement framework. Financial performance is measured by return on assets (ROA), while social performance is measured using the social responsibility sub-score from the Sino-Securities ESG rating system. The Sino-Securities ESG ratings are released quarterly (four times per year) and provide nine levels of ratings, ranging from AAA to C, with scores ranging from 0 to 100. This study constructs the social performance indicator (S_mean) by taking the annual average of the social responsibility sub-score from the ESG ratings and dividing it by 100. Furthermore, inspired by the methodology of Li et al. (2011); Sahoo et al. (2017); Zou et al. (2006), who used the Entropy Weight Method (EWM) to construct composite indicators, this study employs EWM to create a comprehensive performance indicator (Per_EWM) to measure comprehensive corporate performance. EWM addresses the issue of assigning weights in multi-indicator assessments by eliminating bias from subjective weight assignments, thereby reducing the influence of human factors and improving the objectivity and accuracy of the evaluation results. At the same time, it retains the integrity of the original information. The steps for constructing the comprehensive performance indicator using EWM include: standardizing the financial performance (ROA) and social performance (S_mean) indicators, 1 calculating the weight of each indicator, computing the information entropy, determining the weights of the indicators, and calculating the comprehensive score. The result is the comprehensive corporate performance indicator (Per_EWM).

The independent variable of interest is the implementation of the film industry policy (Film Law), represented as an interaction term (Treat × Post). Treat is a dummy variable indicating whether a company belongs to the film industry. If the sample company is part of the film industry, Treat equals 1; otherwise, it equals 0. Post is a dummy variable for the policy implementation period. Since the Film Law came into effect on March 1, 2017, Post equals 1 for periods from 2017 onward, and 0 otherwise. Treat × Post is the interaction term between Treat and Post. By definition, for film industry companies in the post-2017 period, Treat × Post equals 1; otherwise, it equals 0. In the empirical regression, the coefficient (β) of the core explanatory variable Treat × Post and its significance level are the primary focus. If β is significantly positive, it indicates that the Film Law improved a specific type of performance for film industry companies. Conversely, if β is significantly negative, it suggests that the Film Law reduced a specific type of performance for film industry companies. Notably, the model also controls for individual fixed effects (δ i ) and year fixed effects (δ t ), which already capture Treat and Post that are eliminated in Equation 1 to avoid multicollinearity.

The control variables (Control) consist of firm-level indicators. Following the studies by F. Wang, Ma, and Liao (2024); S. Wang (2021), this study controls for variables including firm size (Size), firm age (Age), leverage ratio (Leverage), revenue growth rate (Growth), the shareholding ratio of the largest shareholder (Top1), institutional ownership ratio (Inshold), analyst coverage (Analyst), and the proportion of independent directors (Indirr). The specific definitions of all variables are presented in Table 2.

Variable Symbols and Definitions.

The descriptive statistics for the main variables are presented in Table 3. It can be observed that the average firm age is 17 years, the average institutional ownership ratio is 48.12%, the average shareholding ratio of the largest shareholder is 44.54%, and the average proportion of independent directors is 37.27%. Based on the standard deviations, there are varying degrees of differences among the sample companies in terms of financial performance, social performance, and size.

Descriptive Statistics of Variables.

Empirical Analysis

Main Empirical Results

To investigate the impact of film industry policies on comprehensive performance, this study applies the PSM-DID method and uses the OLS model to estimate Equation 1. The empirical results are presented in Table 4. Columns (1) to (3) correspond to regression results with ROA, S_mean, and Per_EWM as the dependent variables, respectively.

Film Industry Policies and Corporate Performance.

Note. Values in parentheses are standard errors clustered at the firm level.

, **, *** indicate significance levels at 10%, 5%, and 1%, respectively.

From Column (1), the coefficient of the interaction term Treat × Post is −.0530 and is significant at the 1% level. From Column (2), the coefficient of Treat × Post is .0349 and is significant at the 5% level. From Column (3), the coefficient of Treat × Post is .0364 and is also significant at the 5% level. These empirical results indicate that China’s film industry policies, as represented by the Film Law, have reduced the financial performance of listed companies but improved their social performance, thereby enhancing their overall performance. This suggests that after the implementation of the Film Law, the economic benefits of film industry companies declined, while their social benefits increased, leading to an improvement in their comprehensive performance. The decline in short-term ROA among treated firms may reflect the financial burden of adapting to the need for increased internal compliance capacity, as stipulated in Articles 15-20 of the Law. In contrast, the improvement in social performance is consistent with firms’ strategic efforts to align with the law’s emphasis on “social benefit” and “cultural responsibility.”

Parallel Trend Hypothesis Test

To test whether the treatment group and the control group exhibited similar trends prior to the official implementation of the film industry policy, this study follows the methodology of Han et al. (2024) and F. Wang et al. (2024). Based on whether the observation period corresponds to the year (2017) of implementation of the Film Law, the years before, or the years after, seven dummy variables (Pre4, Pre3, Pre2, Pre1, Cur, Post1, Post2) were created. These were interacted with Treat to construct interaction terms (Treat × Pre4, Treat × Pre3, Treat × Pre2, Treat × Pre1, Treat × Cur, Treat × Post1, Treat × Post2). These interaction terms were then introduced into Equation 1, replacing the original Treat × Post term, and the regression was re-estimated. To avoid potential interference caused by the year of policy implementation, the Treat × Cur term was excluded.

The results, presented in Table 5, show that when the dependent variables are ROA, S_mean, and Per_EWM, the coefficients of the interaction terms (Treat × Pre4, Treat × Pre3, Treat × Pre2, Treat × Pre1) are all insignificant. However, the coefficients of Treat × Post1 and Treat × Post2 are significant, and their signs are consistent with the baseline regression. These findings indicate that prior to the implementation of the Film Law, there were no significant differences between the treatment and control groups in terms of financial performance, social performance, or comprehensive performance. However, after the implementation of the Film Law, the financial performance of companies in the treatment group declined significantly relative to the control group, while their social and comprehensive performance improved significantly. Therefore, the parallel trend hypothesis is satisfied.

Parallel Trend Hypothesis Test.

Note. Values in parentheses are standard errors clustered at the firm level.

, **, *** indicate significance levels at 10%, 5%, and 1%, respectively.

Furthermore, this study presents a graphical illustration to more intuitively demonstrate the relationship between the film industry policy and corporate performance according to the results of Table 5. Figure 1 plots the coefficient estimates on the interactions between the policy dummies and corporate performance and the 95% confidence intervals. As shown in Figure 1, the coefficients of the interaction terms prior to the implementation of the Film Law are not significantly different from zero, indicating no significant differences between the treatment and control groups before the policy was implemented, which means there is no anticipated effects that companies adjust their behavior in advance of the policy implementation. This supports the validity of the parallel trend hypothesis. Starting 1 year after the implementation of the Film Law, the coefficients of the interaction terms become significantly negative when ROA is the dependent variable, and significantly positive when S_mean and Per_EWM are the dependent variables. These results suggest that the Film Law significantly reduced financial performance but improved social performance, ultimately enhancing comprehensive corporate performance, and the effects are sustainable.

Dynamic effects of Film Law. (a) Financial performance, (b) Social performance, and (c) Comprehensive performance.

Robustness Checks

To ensure the robustness of the main conclusions, this section conducts robustness checks from the following perspectives:

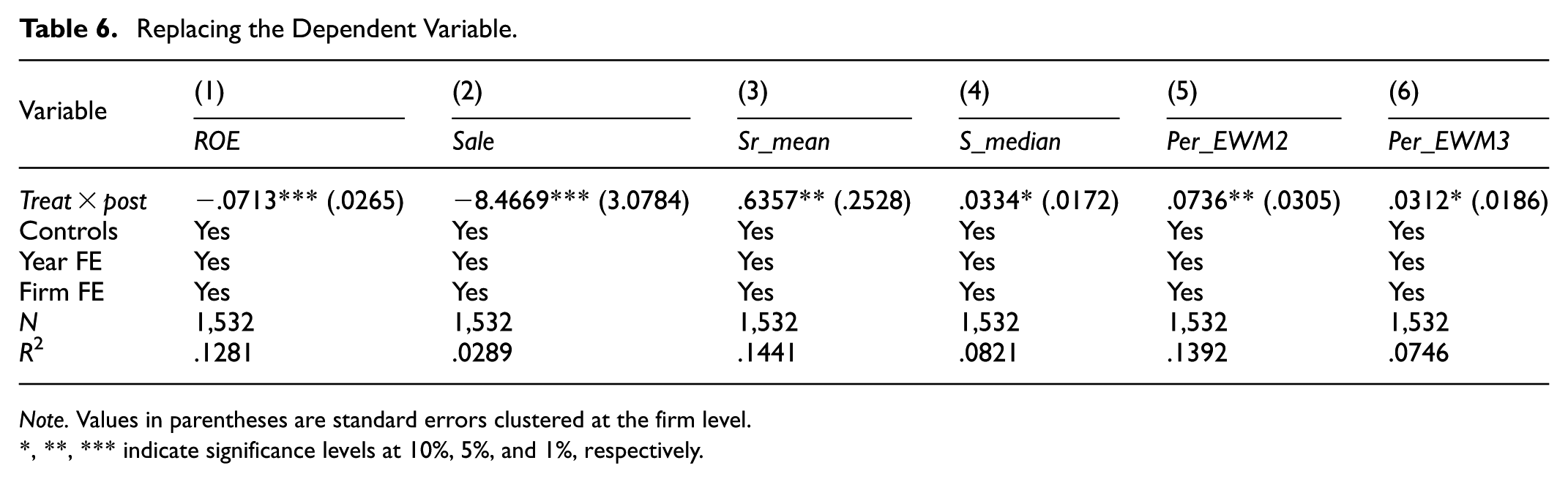

Replacing the Dependent Variable

First, for financial performance, prior research suggests that indicators such as Return on Equity (ROE; Howell, 2017) and operating revenue (F. Wang, Li, & Sun, 2019) can be used as proxies. Based on this, the study uses ROE and operating revenue (Sale, in billions of RMB) as alternative proxy variables for corporate financial performance and re-estimates Equation 1. The results are presented in Columns (1) to (2) of Table 6. Second, for social performance, prior studies recommend using scores ranging from 9 to 1 to represent the nine ESG social responsibility rating tiers (from AAA to C). Accordingly, this study uses the mean score of these ratings (Sr mean) as an alternative proxy for corporate social performance and re-estimates Equation 1. Additionally, the study replaces S_mean with the median of the four quarterly social responsibility ratings divided by 100 (S_median) and re-estimates Equation 1. The results are presented in Columns (3) to (4) of Table 6. Finally, for comprehensive performance, the study constructs two additional comprehensive performance indicators (Per_EWM2 and Per_EWM3) by applying the Entropy Weight Method (EWM) to two sets of indicators: ROA and Sr_mean, and ROA and S_median, respectively. Equation 1 is then re-estimated using these two comprehensive performance indicators. The results are shown in Columns (5) to (6) of Table 6. The findings in Table 6 further substantiate the research conclusions, providing stronger support for the robustness of the study’s results.

Replacing the Dependent Variable.

Note. Values in parentheses are standard errors clustered at the firm level.

, **, *** indicate significance levels at 10%, 5%, and 1%, respectively.

Adjusting Model Specification

To enhance the robustness of the analysis, the model is further adjusted by incorporating industry fixed effects into the regression of Equation 1. The results, presented in Table 7, reaffirm the findings of this study.

Robustness Checks: Adjusting Model Specification.

Note. Values in parentheses are standard errors clustered at the firm level.

, **, *** indicate significance levels at 10%, 5%, and 1%, respectively.

Excluding Samples from the Policy Implementation Year

To further ensure robustness, samples from the policy implementation year (2017) are excluded, and Equation 1 is re-estimated. The results, presented in Table 8, indicate that the main conclusions of this study remain robust.

Robustness Checks: Excluding Samples from the Policy Implementation Year.

Note. Values in parentheses are standard errors clustered at the firm level.

, **, *** indicate significance levels at 10%, 5%, and 1%, respectively.

Verifying that the Control Group is Unaffected by the Policy

This section aims to verify that non-film industry companies are unaffected by the Film Law, indirectly confirming that the policy impacts only the performance of film industry companies. To test this, a new policy dummy variable (TreatCon) is created, which equals 1 if a company belongs to the non-film industry, and 0 otherwise. The regression results, presented in Table 9, show that the coefficients of the interaction terms are all insignificant. This indicates that the Film Law did not affect the performance of non-film industry listed companies, thereby indirectly validating the robustness of the study’s main conclusions.

Robustness Checks: Verifying that the Control Group is Unaffected by the Policy.

Note. Values in parentheses are standard errors clustered at the firm level.

, **, *** indicate significance levels at 10%, 5%, and 1%, respectively.

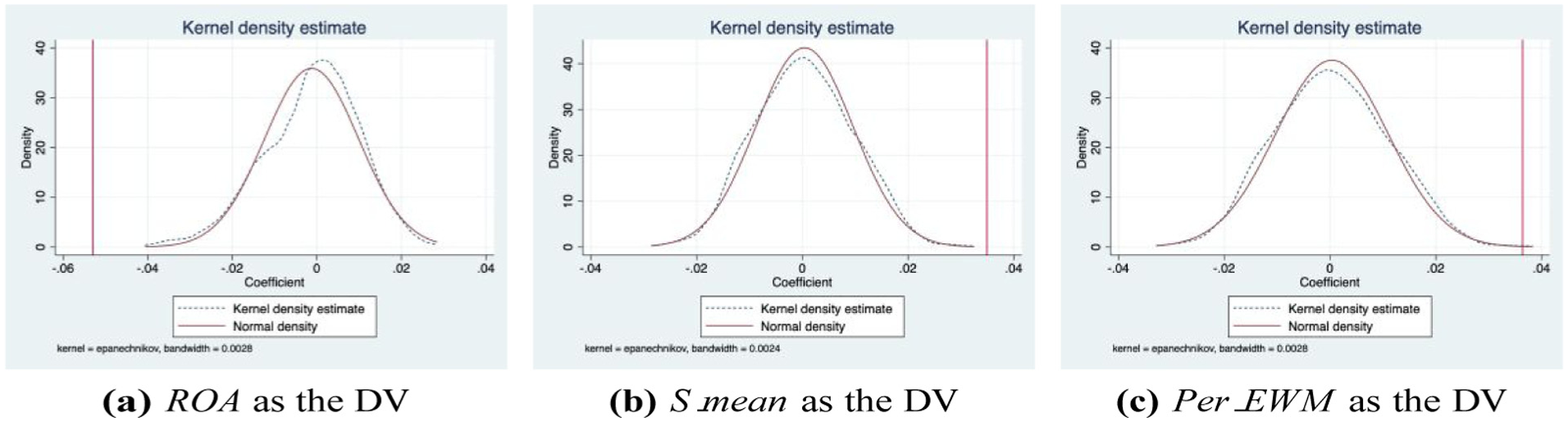

Placebo Test

Following the approach of Ferrara et al. (2012) and Liu and Lu (2015), this study conducts a placebo test by randomly generating treatment groups. The results are illustrated in Figure 2.

Placebo test with 500 iterations. (a) ROA as the DV, (b) S_mean as the DV, and (c) Per_EWM as the DV.

In this quasi-natural experiment, although we have controlled for firm and year fixed effects, there may still be unobservable differences between the treatment and control groups prior to the implementation of the Film Law. Due to data limitations, these differences cannot be directly observed and may potentially affect the evaluation of the policy’s effect, thereby threatening the validity of the identification assumption.

To address this issue, we adopt an indirect strategy to examine whether these potentially omitted characteristics might influence the estimation results. First, based on Equation 1, we derive the expression for

Here, c represents all control variables. If γ = 0, it implies that unobserved factors do not affect the estimated results, and the estimation is unbiased. However, it is not possible to directly test whether γ = 0.

We therefore consider an indirect approach: if we can find a variable to replace Treati × Posti,t, which, in theory, should have no true effect on the corresponding Performancei,t (i.e., β = 0), and the estimated coefficient is indeed zero, it would indicate that γ = 0.

To implement this, we randomize the treatment assignment (the impact of the Film Law on specific industry firms) using computer-generated random processes, and repeat this process 500 times. This randomization ensures that the placebo treatment has no actual effect on Performancei,t, that is, βrandom = 0. Under this condition, we compute the mean of the estimated placebo coefficients, and the distribution of all 500 placebo estimates is shown in Figure 2.

As shown in Figure 2, the estimated coefficients

Conclusion

This study investigates the effects of the Film Industry Promotion Law of the People’s Republic of China (Film Law) on the performance of A-share listed film enterprises. Using a Propensity Score Matching and Difference-in-Differences (PSM-DID) methodology, we identify a bifurcated impact: while firms experienced a decline in financial performance post-policy implementation, their social performance—as reflected in Corporate Social Responsibility (CSR) ratings—improved significantly. This divergence reflects the institutional logic of symbolic compliance, wherein firms adapt to normative expectations at the expense of market-oriented efficiency. The aggregated results, evaluated via the Entropy Weight Method, reveal a modest net positive effect. As the first sector-specific cultural law in China, the Film Law institutionalizes the dual policy goal of promoting social value while sustaining economic viability. This research not only fills an empirical gap in evaluating the law’s enterprise-level effects, but also provides a replicable quantitative framework for assessing state-led cultural policy interventions. Theoretically, it contributes to literature on institutional coercion and symbolic regulation within the cultural economy. These findings also point to the need for more responsive governance models that balance ideological guidance with sectorial sustainability.

Discussion

Navigating Symbolic Compliance: Empirical Findings

The empirical findings of this study reveal a distinct divergence in how cultural regulation affects different dimensions of firm performance. On one hand, the Film Law appears to have led to a measurable increase in corporate social responsibility (CSR) performance among treated firms. On the other hand, it is associated with a decline in financial performance, as measured by return on assets (ROA). This bifurcated outcome highlights a central tension faced by firms in the creative sector: the need to secure political legitimacy while maintaining market viability.

The increase in CSR scores suggests that film companies are actively responding to normative signals from the state. Through practices such as producing ideologically aligned content, participating in public-interest projects, and engaging in officially supported collaborations, firms appear to be pursuing symbolic legitimacy in line with institutional expectations (Aguilera et al., 2021; Scott, 2013). These adaptations reflect an emerging logic of compliance shaped more by political-ideological alignment than by market incentives.

At the same time, the observed decline in ROA points to the economic trade-offs of such symbolic compliance. Regulatory demands—ranging from content pre-approval to ideological vetting—impose additional costs and reduce operational flexibility. This is particularly burdensome for small and medium-sized enterprises (SMEs), which often lack the institutional resources to absorb these pressures. Together, these findings illustrate the dual demands embedded in cultural policy implementation: firms are expected to serve not only as economic actors, but also as ideological agents within a state-framed symbolic order.

Institutional Pressures and Ideological Standardization

To understand the dual shifts in CSR and ROA, it is necessary to examine the institutional environment in which the Film Law operates. From the perspective of institutional theory, regulatory interventions often exert coercive pressures that prompt organizations to conform not only to legal requirements but also to normative expectations embedded in state ideology (DiMaggio et al., 1983; Scott, 2013). In China’s cultural sector, this takes the form of symbolic compliance—actions taken not for direct economic gain but to align with political priorities and avoid regulatory risk.

In this context, CSR initiatives—such as producing educational content, promoting national values, or participating in government-endorsed campaigns—become instruments of legitimacy. Rather than responding solely to stakeholder pressures or market reputation concerns, firms engage in these practices to signal ideological alignment and secure access to approval channels, funding opportunities, or symbolic capital. This type of legitimacy-seeking behavior is consistent with findings from other highly regulated or politically embedded industries (Marquis et al., 2011).

At the same time, the Film Law functions as a normative standard-setting mechanism. It not only articulates the regulatory boundaries of acceptable content, but also conveys policy-endorsed cultural preferences—emphasizing themes such as national identity, social responsibility, and collective values. This standardization operates through both formal mechanisms (e.g., mandatory content review procedures 2 ) and informal guidelines (e.g., genre recommendations, thematic suggestions). As a result, firms do not merely respond to explicit prohibitions or approvals, but often internalize these normative expectations in the early stages of creative decision-making. The institutionalization of such expectations may contribute to resource reallocation, cautious innovation, and strategic conservatism—factors that help explain the observed decline in financial returns.

Structural Impacts on Creative Diversity and Market Composition

The institutional and ideological pressures described above do not operate in isolation; rather, they generate cumulative effects on the structural dynamics and creative potential of the film industry. One visible outcome is the increasing homogenization of cultural content. By consistently emphasizing themes such as “positive energy,” national pride, and moral integrity, the regulatory environment may unintentionally constrain the expressive latitude available to filmmakers. As these normative expectations become internalized within production logics, creative experimentation becomes more uncertain, giving way to risk-averse replication of preferred narrative formats.

This pattern raises concerns about the long-term vitality of the domestic film ecosystem. In an increasingly globalized cultural market, success is often contingent on genre diversity, storytelling originality, and the ability to resonate with heterogeneous audiences. The institutionalization of ideologically coded expectations may undermine these capacities, weakening the international competitiveness of Chinese film productions and limiting cultural pluralism at home.

Moreover, these constraints are unevenly distributed. Firms located outside major production centers—such as Beijing, Shanghai, or Hangzhou—often lack access to policy support, funding streams, and talent pools. Without compensatory mechanisms, such as regional development grants or quota-based broadcasting incentives, these structural disparities are likely to deepen. The risk is that a bifurcated industry may emerge, wherein a small number of politically connected firms dominate both regulatory access and narrative visibility, further concentrating symbolic and economic capital.

Theoretical Contributions to Institutional and Cultural Political Economy

This study makes two key theoretical contributions. First, it extends institutional theory by demonstrating how coercive isomorphism operates in the cultural sector under conditions of ideological governance. While prior studies have emphasized regulatory compliance in fields such as environmental or financial regulation, this study shows how symbolic conformity—through CSR signaling and content alignment—can emerge in response to politically encoded legitimacy demands. In doing so, it empirically substantiates the claim that organizational behavior is shaped not merely by market competition but also by the pursuit of state-sanctioned normative acceptance (DiMaggio et al., 1983; Scott, 2013).

Second, the findings engage with the tradition of cultural political economy by offering a quantitative framework for understanding how cultural policy translates ideological intent into organizational outcomes. Scholars such as Garnham (2005); Hesmondhalgh (2018); Miller and Yúdice (2002) have long argued that state intervention in cultural industries serves not only economic ends but also functions as a form of symbolic governance. This study operationalizes that insight: it traces how regulatory authority configures performance expectations, incentivizes symbolic behavior, and redistributes creative agency across firms with differing capacities for ideological compliance.

More broadly, the study advances a methodological proposition for future cultural policy research. By combining quasi-experimental identification strategies with institutional and critical theory, it demonstrates how empirical techniques can be harnessed to interrogate not just “whether” policies work, but “how” and “for whom.” This integrative approach opens a path for rethinking cultural governance not merely as an administrative process, but as a field of symbolic power, organizational adaptation, and contested legitimacy.

Rethinking Cultural Governance: Policy Implications

The dual impacts identified in this study—rising symbolic compliance alongside declining financial returns—underscore the limitations of uniform regulatory models in the cultural sector. While the Film Law has played a crucial role in institutionalizing standards and formalizing oversight procedures, its current framework imposes disproportionate burdens on firms with limited resources or political capital. A more adaptive governance model is needed—one that recognizes the heterogeneity of market actors and supports sectorial sustainability.

Policy refinement should begin with differentiated compliance structures. Regulators could adopt tiered frameworks that distinguish between large state-affiliated studios and smaller independent producers, with adjustments such as simplified administrative procedures, reduced compliance thresholds for low-risk content, and targeted funding schemes. Public support measures—such as regional development subsidies or improved access to distribution platforms—can help empower marginal producers without undermining core ideological objectives.

In parallel, investment in capacity-building programs would enhance the ability of firms to comply without sacrificing creativity. Professional development initiatives—focused on ethical content production, value-consistent storytelling, and audience engagement strategies—can bridge the gap between ideological expectations and creative autonomy, especially for new entrants and producers outside major media hubs.

Governance reform should also prioritize procedural transparency and inclusive participation. Mechanisms such as policy hearings, industry roundtables, and digital feedback platforms can help align regulatory design with industry realities and foster mutual accountability. Furthermore, performance evaluations should move beyond administrative compliance to include metrics that capture artistic innovation, audience diversity, and international resonance—thus encouraging both creative excellence and symbolic alignment.

Consistent with the view that cultural policy should serve not only as a regulatory instrument but also as an engine of industry development (Miller & Yúdice, 2002), these recommendations aim to balance symbolic authority with institutional flexibility. A responsive governance model—attuned to market diversity and grounded in participatory legitimacy—will be essential for building a pluralistic, competitive, and ideologically coherent cultural sector in transitional economies.

Limitations and Future Directions

This study offers empirical insight into the performance effects of the Film Law, yet several limitations should be acknowledged. First, the analysis relies on data from publicly listed film enterprises, excluding small-scale, privately held, or informally organized firms that constitute a substantial portion of China’s creative sector. As such, the findings may not fully generalize to the broader industry landscape, particularly in contexts where resource asymmetries and informal production practices are prevalent. Second, although the parallel trends test utilizes a 4-year pre-treatment period (2013–2016), the post-treatment window (2018–2019) is relatively short. This constraint arises from the outbreak of the COVID-19 pandemic in early 2020, which caused unprecedented disruptions to China’s film industry. Since it is difficult to disentangle the effects of the pandemic from those of the policy, we limited our analysis to data prior to 2020. Future studies with longer post-policy observation periods—once the market stabilizes—could better assess the long-term effects of the Film Law.

Third, while the robustness checks employ alternative outcome variables and model specifications to validate the empirical results, they follow a similar econometric logic and therefore may not constitute full methodological triangulation. Moreover, the study adopts a macro-level design and does not incorporate micro-level qualitative insights into how firms internally respond to regulatory changes or how policy goals are translated into organizational practice. Future research could strengthen both causal inference and interpretive depth by incorporating complementary approaches, such as in-depth interviews, case studies, or content-level analyses of policy implementation and corporate strategy.

Fourth, the measurement of social performance is based on CSR scores derived from public disclosures, which may reflect reporting practices rather than substantive social outcomes. Triangulating these scores with independent audits or qualitative assessments could enhance interpretive depth. Taken together, these limitations suggest that future research should incorporate more diverse organizational types, extend temporal coverage, and explore alternative indicators to more fully capture how cultural regulation shapes firm behavior over time.

Footnotes

Acknowledgements

We would like to express our gratitude for the support and resources provided during the course of this research.

Ethical Considerations

This research is not applicable.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Project of National Social Science Foundation of China (24CJL063).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting the findings of this study are obtained from licensed commercial databases (CSMAR, WIND, and Sino-Securities ESG Rating System), which are publicly accessible to registered users.