Abstract

The purpose of this empirical study is to undertake a comparative analysis of the South Asian and Western food companies based on their corporate social responsibility (CSR) adoption and impact on firm performance. We conducted a survey of 24 South Asian and 20 Western companies. Later, we performed independent samples t-tests and ordinary least squares (OLS) regression. Furthermore, we applied Kingdon’s agenda and green consumer theories to explain how CSR in Western food companies could be advanced than the food companies in South Asia. Based on the aforementioned tests, the Western food companies obtained better scores than their counterparts in South Asia. This result was obvious as the West has a developed CSR management system compared to South Asia. However, this is interesting that we found a weak CSR performance link between the Western and the South Asian food companies. The lower CSR adoption levels of South Asian food companies show their greedy nature as these companies are hesitant to spend the portion of their profits on promoting CSR. South Asian governments with a vested interest in improving CSR performance provide tax breaks and other motivations for increasing CSR adoption among food companies. These findings have theoretical and practical implication for future research.

Introduction

During the last two decades, increased adoption of corporate social responsibility (CSR) was witnessed in various private and public corporations. Contrary to past practices, the corporate world is currently focusing on various environmental, economic, and social impacts and issues caused by business operations. Different companies, that is, Coca-Cola, KFC, and Nestle, have taken voluntary initiatives to address the aforementioned issues (S. Kim & Choi, 2018; R. Kiran & Sharma, 2011; Seele & Lock, 2015). Besides, the national governments and international standard organizations have introduced stringent policies at country and global levels, respectively. The purpose is to put more efforts by the corporate world to resolve aforementioned issues. CSR enables us to learn how the corporate world manages and implements business practices to create a positive effect on society (Y. C. Chen et al., 2018). The active involvement in resolving the issues and contributing to reducing the negative effects of business operations elicit remarkable advantages to the corporation as well. The adaption of CSR offers advantages in the management system, cost saving, firm value, client, and investor association. CSR is gaining increasing acceptance in the corporate world (Ding et al., 2016). Many organizations have adopted CSR as an essential element of their business plan and management. However, an effective integrated management system (IMS) approach is also required to address the requirement of CSR adaption.

Despite the fact that the participation of CSR in different fields provides a value addition for society, still the major pillar has been ignored, which is the food industry even though in the recent perspective of CSR, the Asian region has attracted larger interest from the corporate world (Chapple & Moon, 2005). Countries in the South Asian region such as India, Bangladesh, and Pakistan are among the vibrant and economically progressing regions that have attracted the attention of the world’s renowned multinational companies for investment and business. This is observed through increased investment in various industrial sectors; foreign investment in these regions had increased to almost 500 times higher than in the 1990s when economic liberalization was started in these countries (United Nations Conference on Trade and Development, 2016). For example, there are plentiful franchises of KFC, McDonald, and Burger King operational in South Asia. However, little is known about their contribution to society. Moreover, the rise in external investments from South Asian regions are also observed as several multinationals companies especially in the food industry due to global sharing of taste and extreme adoption of multicultural rituals have started global operations (Khilji, 2012). This interest has companies to adapt circumstantial attitudes to management that include philosophy, religious conviction, and establishments in developing CSR (Azizi & Jamali, 2016).

CSR finds significant application in the food industry as this industry has a major influence and substantial impact on the economy, environment, and society, and it is the emerging sector across the world contributing 25% to the global gross domestic product (GDP). Simultaneously, the food industry is experiencing various challenges for several reasons. First, the food sector highly depends on different natural assets (Silva et al., 2009). Second, food is a primary human need, and human beings are always concerned about the food they eat. This concern results in diverse requirements in the food industry ranging from the procurement of the best raw items (meat, grains, etc.) to the environmental effect (energy resource and water usage; waste management) and community situations as well as the worth, physical condition, and safety of the finished goods (Maloni & Brown, 2006). Finally, the food industry has a distinctive and multidimensional arrangement. Small and big companies have different approaches to CSR adaption; this indicates possible conflicts in CSR implementation in the food industry, whereas the cross-border changing taste is also a major hurdle. Although the various aspects of food production, processing, and distribution, as well as quality and safety, have been a focus of research in the Western world, no or lack of research has been done in this regard for the South Asian region, while various researchers regressed to come up with an inclusive definition, which merely shows the basic CSR characteristics. The study is particularly desirable to evaluate the adaption of CSR management system with its due course, and a comparison of this adaption is also desired with already adapted CSR management practices in the Western world.

Assessment of CSR performance in business ethics, food industry, and financial perspective seems to have a lack of systematic and logical bases for quantitative studies. Undoubtedly, various researchers draw special attention toward the concept and partially defined the basis of shallow studies rather than a systematic and scientific consensus to measure the CSR performance in the food industry. Moreover, the wide-ranging contemporary CSR performance related to food industry requires a substantial assessment to measure CSR performance to ensure quality food. Conceptually, it is important to understand that what would the empirical estimation yielded while after adaption of CSR Management System in Food Industry rather than to measure the common basis CSR performance. For a corporation to be able to produce favorable long-term consequences, the organizations need to conduct its performance assessment for the satisfaction of shareholders, customers, society, and other stakeholders. However, unfortunately, it is not easy to measure the quantitative aspects considering the multidimensional aspects and varying opinions of a company’s end-consumers while evaluated quantitative facts lead toward a certain and reliable decision making. To address this problem, we have conducted an empirical assessment of CSR performance holistically.

The quantitative study is conducted in four food industries of the South Asian Region, that is, India and Pakistan. A survey comprising a questionnaire for evaluating CSR management system is prepared for shareholder groups such as personnel, clients, stockholders, community, natural environment, and sellers. A robust framework of the research hypotheses is formulated and based on the collected information; statistical tools are used to accept or reject the proposed hypotheses to assess CSR management system adaption.

The purpose of this empirical study is to undertake a comparative analysis of the South Asian and Western food companies based on their CSR adoption and impact on firm performance. The specific objectives of this research are as follows:

To assess the state-of-art in CSR management system in the food industry.

To compare the adoption of CSR in South Asia and Western food industries.

To figure out the framework of problems in the implementation of CSR management system and provide a suggestion for better adaption.

The organization of this article is structured as follows. The “Introduction” section provides the background information of the study, the problem statement, research aim, and the specific objectives. A review of the available literature regarding CSR management in the food industry and the development of the hypothesis was presented in the second section of the research. The detailed survey of CSR and CSR management system, research methodology, data sources, and data tools are provided in the third section. Data analysis results and discussions based on statistical method were conducted and comparison with the Western companies made in the fourth section. Finally, section “Conclusion and Policy Implication” presents the conclusions and recommendations drawn with policy implication.

Literature Review

CSR

The idea of CSR was first introduced by Bowen as the social commitment to adopt policies and procedures that are valuable to society (Bowen, 2013). That commitment to society led to further exploration of CSR in almost every field. During the last decade, a growing trend is witnessed in the adaption of CSR in public as well as private sector companies of all types and sizes (Mark-Herbert & Schantz, 2007; Millon, 2015). Although the concept of CSR has been discussed for the past 65 years, the last decade produced more research on this topic than ever. The significant contribution in CSR literature is presented in the following paragraph.

Dhaliwal et al. (2011) studied the possible advantages related to the adaption of CSR practices in the corporations and revealed that the corporations with the adaption of CSR initiative experienced reduction in the cost of equity as compared to previous years. Y. Kim et al. (2012) studied whether corporations practice CSR act similarly or differently from other corporations in business reporting and found that CSR corporations do not believe in (a) income from discretionary accruals, (b) influencing business operations, and (c) involvement of activities prone to regulatory investigations. Moser and Martin (2012) considered two major perceptions of CSR: (a) firms should only practice CSR in situations where stock values are increased and (b) firms should also practice CSR for improvement of society even it results in a reduction of stock values. Gao et al. (2014)studied about the involvement of senior officials of CSR practicing firms in informed trading. The study revealed that senior officials of CSR practicing firms are not often involved in insider trades as compared to non-CSR practicing firms. It was also revealed that there exists a negative relationship between insider trade benefit and CSR practice if senior officials have personal interests similar to the corporate interest. Lys et al. (2015) studied the relationship between CSR expenditures and corporate performance and noted that adoption of CSR reduces the organizational cost. Servaes and Tamayo (2013) studied the linkage between CSR and corporation worth specifically, in a way when CSR has a significant impact on corporation worth. It was found that the CSR adaption and adaption publicity in the market results in enhancement of corporation worth. However, in the case of CSR-related incidents, this publicity can also defame corporation growth and decrease its worth. Eccles and Serafeim (2013) explored various communal and ecological concerns caused by the adaption of CSR in corporations and studied how CSR influences managerial practices and organizational achievements. It was found that the growth and sustainability of big corporations is a virtue of efforts by higher ups such as members of the governing body, and their incentives are normally associated with growth rate. It was also found that big corporations with significant growth rate considerably leave behind their opponents in the long term, with respect to shareholders and financial achievement. Van der Laan Smith et al. (2010) studied the effect of CSR on investment activities in the United States, Japan, and two European countries considering investor theory as the fundamental basis. It was revealed that CSR has a significant effect on investment activities in all the above-mentioned regions and that their investors’ inclination marks the level of this effect. Taneja et al. (2011) examined the research work in CSR from 1970s to the following 40 years in prominent technical periodicals to evaluate the various research areas in CSR. Malik (2015) also presented a literature study aimed to highlight the CSR effect in increasing corporation value, presented in the renowned academic Journal of Business Ethics, besides other periodicals that focused on CSR theory.

CSR Management System

The central part of CSR management is to make the stakeholder’s requirements for an integrated part of the business strategy (Castka et al., 2004). For an organization to be successful with CSR, the whole organization should take an active part (Castka et al., 2004). It starts at the top where the board should take responsibility for the strategic direction and put up measurable CSR objectives. Then organizations need to put CSR structures and processes into place to make a meaningful contribution toward sustainable development (Asif et al., 2010; Klettner et al., 2014). These CSR structures have to be integrated through every level of the organization and be aligned with the strategic direction of the company (Asif et al., 2013). For CSR to be implemented effectively in an organization, CSR has to be a part of the strategic planning process and the organization’s IMS (Asif et al., 2013).

A management system is a function-specific system intended to support the overall business. There are several management systems for different areas that can be a base for organizations’ IMSs (Asif et al., 2009; Zutshi & Sohal, 2005).

The International Organization for Standardization (ISO) is a standard body that is used among organizations globally with high credibility (Castka et al., 2004). The management systems most relevant to CSR are the environmental management system (EMS) ISO 14001, the occupational health and safety management system (OHSMS) OHSAS 18001, the energy management system (EnMS) ISO 50001, the social accountability system SA 8000, and the quality management system (QMS) ISO 9001 (Ikram, Mahmoudi, et al., 2019). Since the release of such management systems, organizations in both the private and public sector have replaced old rigid “command and control” procedures with management systems that are more flexible and open. The management systems fulfill various stakeholder requirements based on the Deming cycle of “Plan-Do-Check-Act” for continuous improvements (Asif et al., 2009; Zutshi & Sohal, 2005). When organizations get certifications for management systems by an external auditor that gives stakeholders verified the evidence of the organization’s performance in the specific areas (Asif et al., 2009).

In 2010, ISO developed guidance on social responsibility, ISO 26000. Considering the popularity of the EMS ISO 14001, ISO 26000 might be widely accepted (Ranängen et al., 2014). The overarching objective for ISO 26000 is to make all types of organizations to participate in viable progress (British Standards Institution [BSI], 2010). ISO 26000 offers direction to organizations to follow seven principles and to define how organizations can work with seven fundamental topics (BSI, 2010). The guidelines of ISO 26000 could be used to evaluate and improve a company’s CSR performance to make CSR successful in an organization (Ranängen et al., 2014). In operations management literature, there are two schools of thought regarding IMS’s. One school of thought says that an IMS is one kind of a performance improvement program that only will lead to better operational performance. According to this school of thought, there is no link between an IMS and corporate strategy.

Conversely, the second school of thought means that performance improvement practices do depend on the larger organizational context. The second school of thought indicates that IMS is not about combining procedures. An IMS implementation should be aligned with an organizational strategy to improve the strategic performance of an organization (Asif et al., 2009).

An IMS builds on the integration of individual management systems that address specific needs of stakeholders, and the similarity between an IMS and CSR is that both concepts are engaging stakeholders (Asif et al., 2013). When taking CSR into account in an IMS, a sustainability management system (SMS) is created. Organizations have to decide and clarify what social responsibility means for the organization itself for an SMS to continuously contribute to sustainable development (ISO 26000).

CSR is an umbrella issue (Garcia de Madariaga & Valor, 2007) and pointed out an overlap of the essential themes in ISO 26000 and the objectives of some management systems for CSR, as shown in Figure 2. One way for organizations to take stakeholder requirements into account using a systematic and planned approach is thus to create an IMS based on the management systems ISO 14001, ISO 9001, ISO 500001, OHSAS 18001, and SA 8000 (Ranängen, 2013). Organizations that are certified to the management systems in Figure 1 fulfill the requirements for following five of seven essential themes in ISO 26000: human rights, labor practices, environment, customer issues, and organizational governance (Ranängen, 2013).

The overlap of ISO 26000’s essential themes and relevant management systems for CSR.

CSR in the Food Industry

The adaption of CSR is gradually observed in the food industry as well indicated by their regularly published CSR bulletins. Jones et al. (2006) showed that CSR is an essential part of British food companies and also supported by local stores. Anselmsson and Johansson (2007) also suggested that there exist a significant relationship between CSR and buying food items. Li et al. (2010) studied CSR practice in big food companies and found that food companies with consistent CSR practices have progressed well as compared to companies with poor CSR practice. Hartmann (2011) studied CSR in the food sector and also suggested future research directions in this domain. Assiouras et al. (2013) studied the effect of CSR on the goods-harm disaster in the food sector and suggested that CSR should be adapted not only to increase product sale but also to handle incidents (e.g., goods-harm disaster). Bilinelli (2016) examined the application of CSR in the Australian food industry. It was found that CSR is an intrinsic element in the Australian corporate world. Business corporations are embracing CSR as an integral business part and also promoting their practices in their reports and websites. However, this practice was not due to the efforts of any government agency or regulatory body. Therefore, in this regard, it was suggested that the Australian government should take an active part. Y. Kim (2017) studied customer reactions to the food sector’s environmental CSR practice and product rate as CSR tradeoffs. The study showed that encouraging buying response of consumers was found from companies with CSR program. More recently, Zhang et al. (2018) examined the relationship between CSR and safety in the food sector. They considered two groups in the food sector, first with reported safety violations in the past and other without any violation record. The study revealed that there exists a relationship between CSR and safety in the food sector. Both groups showed a positive attitude to CSR. However, the first group showed a growing obligation to CSR.

Numerous studies are concerned with the measurement of CSR performance but provide a partial view of the CSR performance. These studies lack the empirical clarity in terms of exact facts and figure even though they provide inclusive definitions. Furthermore, such studies had a narrow scope. For instance, Sharif and Rashid (2014) conducted such a study only for Pakistan, while Mishra and Suar (2010) undertook for India only. However, the rapidly changing environment/parameters/needs of the world demand a rigorous analysis to measure the performance of CSR. Therefore, this article is an attempt to fill the research gap and provide an assessment of adaption of CSR management system in the food industry.

The interests in South Asian Countries are influenced by the emergence of contextual approaches to management which have been used to reveal the role of religion and culture in shaping CSR in the area (Azizi & Jamali, 2016).

Specific Strategies Adopted by Food Companies

Little is known about various strategies adopted by food companies in the globe. However, some previous researchers have attempted to illustrate the various types of activities that are commonly included regarding key strategies used by food companies to protect their products (Lerro et al., 2018). The first strategy is the use of public relations campaigns and public statements to state companies concerns about the health of respective populations and customers at large. For example, big tobacco invested heavily into public relations efforts to deflecting consumer criticism where claims were made that cigarette companies never encouraged abuse of the product, but provide choice and recommendations for moderate consumption (Y. H. Chen et al., 2016).

Another notable strategy is the tactical campaign emphasizing freedom of choice and personal responsibility to encourage consumers to oppose regulation of the industry. Such initiatives emphasize self-control while holding people accountable for what they purchase and consume (Y. Kim, 2017). A good example of the utilization of this strategy is the highlighting of individual responsibilities by the Big Food Company through messages of moderation printed on the packaging such as the “Be Treat Wise” words printed on the exterior of food products by Mondelez International that have high sugar contents.

The third strategy is the adoption of a lobbying tactic. Large Corporations have made huge investments in the lobbying approach to create influence on politicians while blocking or stalling regulatory efforts (Lerro et al., 2018). For example, Philip Morris campaigned heavily on contributions to politicians’ pet causes in the bid of attaining good political mileage concerning federal and state levels. Furthermore, the study observed the possibility of lobbying activities via industry-funded front groups. A good example of the utilization of such a lobbying activity is by the Big Food funds groups that work in a manner of opposing regulation of marketing to children, front-of-pack nutrition labeling, and taxing of unhealthy foods.

The fourth strategy is the use of co-opting policy makers as well as health professionals. For instance, the Big Food promoted partnership with health experts and professionals to undermine public health interventions and policies (Y. Kim & Zapata Ramos, 2018).

The fifth strategy included funding research and development. It is argued that research generates data that supports the food industry’s position. For example, some researchers have focused on the roles of CSR initiatives in promoting products, brands, and industries to the community members (Ikram, Zhou, et al., 2019).

Hypothesis Development and Research Method

Hypothesis Development

The topic of this study involves both the (a) effectiveness and (b) adoption of CSR management systems in the respective food industries of companies in South Asia and the West. Hypotheses related to the topic can be developed on the basis of past findings and theoretical frameworks. First, there is a consensus in the existing literature (Chernev & Blair, 2015; DiSegni et al., 2015; Schrempf-Stirling et al., 2016) that CSR first emerged from North America and Western Europe as the result of (a) the historical strength of grassroots environmentalist movements, (b) the rise of so-called green consumers who demanded CSR in the marketplace, and (c) the commitment of governments to improved ecological stewardship. There is a concomitant consensus in the literature that in South Asia in particular (Anisul Huq et al., 2014; Dhanesh, 2015; Iqbal et al., 2012), CSR has been adopted at a later stage and at a lower intensity than in the West.

Perry and Kingdon (1985) agenda theory and green consumer theory (DiSegni et al., 2015) constitute the conceptual framework for the study. Kingdon’s theory explains broad social interest in CSR which would translate into higher levels of CSR among Western food companies, as citizen preferences for CSR would have led to government support for CSR (Biswas & Roy, 2015). In a global context of CSR, South Asia has made the greater attraction of interest among business leaders, academics alike, and politicians (Herrera, 2015). This is because the region has recorded some of the most dynamic and fast-growing figures when compared to the rest of the world, making many multinationals to view it as an important strategic growth market for expansion. However, the adoption of CSR management systems by food companies in South Asia faces significant challenges when compared to the West. According to Visser et al. (2010), businesses in South Asia face great interference from religion and religion institutions which play a key role in CSR development. Also, strategic CSR in South Asia is primarily practiced by multinationals and multilateral organizations and relatively larger domestic conglomerates and corporations leaving the majority averaged sized and small- and medium-sized enterprises (SMEs) behind. Apparently, multinationals in South Asia act as initiators and influencers of CSR in the region. Hence, we hypothesized the following:

Next, there is a consensus (Flammer, 2012; Theodoulidis et al., 2017; Wang & Sarkis, 2017) in the literature that, after controlling for other relevant factors, there is a positive relationship between CSR and financial performance. There are many available measures of financial performance; one common measure of financial performance in the food industry is net profit margin (NPM; Kafetzopoulos & Gotzamani, 2014). Green consumer theory is more of a market-driven explanation of why CSR is higher among Western companies. The theory also explains why there should be a positive link between CSR and financial performance. According to S. Kiran et al. (2015), the overall performance of an organization is majorly dependent on the ethical business activities as well as activities related to social and environmental gains. Such activities enable organizations to sustain their reputations and goodwill. The argument implies that CSR, which is concerned with practices that relate to procedures and policies that focus on improving social conditions, rights, protections of the environment, and the interests of all the stockholders, results in an improvement in the financial performance of organizations among other forms of performance.

Hence, we hypothesized the following:

However, claims have been made that South Asian companies are both later and shallower CSR adopters (Dhanesh, 2015) in comparison to Western companies. Studies in CSR and financial performance have been subjected to debates because of varying results concerning several variables. According to Hermawan and Mulyawan (2014), the effect of CSR on financial performance varies across countries and industries. It was argued that in developing countries, listed companies, regardless of being aware of the importance of CSR on financial performance, record lower CSR-related benefits than in developed countries. In relation to the above assertions, the following hypothesis can be added:

Data were collected through a simple random sampling of South Asian and Western companies that were either fast food companies or food suppliers to point-of-sale companies. A questionnaire survey was sent to 44 companies through email: 24 from South Asia and 20 from the United States and the United Kingdom combined. All the 44 respondents filled the questionnaire.

The methodology adopted for this study was multivariate ordinary least squares (OLS) regression. The CSR variable was a measure of CSR adoption specific for the industry, based on a combination of food industry–specific CSR scale and more general scale items derived from ISO 14001, ISO 9001, ISO 500001, OHSAS 18001, and SA 8000 (Pino et al., 2016). The resulting 30-item scale was based on a 7-point Likert-type scale, with a spectrum of scores from 30 to 210. In this scale, lower scores represented lower levels of CSR adoption, and higher scores represented higher scores of CSR adoption. Scores were calculated by adding the respondent entries for each question on the scale. Cronbach’s Alpha of the scale was .84, indicating a sufficiently high level of internal reliability.

In H1, the independent variable was company location (South Asia vs. the West), and the dependent variable was CSR adoption. In H2, the independent variable was CSR adoption, the dependent variable was NPM, and the control variables were (a) revenue (in USD) and (b) industry subtype (fast food, restaurant chain, and supplier). In H3, the independent variable was CSR adoption, the dependent variable was NPM, and the control variables were (a) revenue (in USD), (b) industry subtype (fast food vs. supplier), and (c) company location (South Asia vs. the West).

Research Method

The study adopted a quantitative research method implying that numerical data were gathered, analyzed, and conclusions made based on the analysis results. Unlike the alternative method, a qualitative research method, a quantitative approach was considered because of numerous advantages related to the current study. First, quantitative research enabled the collection of the large data set which enhanced the generalization of the results to the larger population. Second, the adopted approach allowed the use of statistical tools and techniques which increased the reliability of the research process. Furthermore, quantitative research was considered more appropriate than the mixed research method due to its simplicity.

Conversely, the study adopted a descriptive research design where the CSR management systems adopted by the selected food companies in South Asian Region, that is, India and Pakistan, as well as the selected food companies in the Western region were investigated based on the natural occurrences and not by manipulating any of the variables. The design was advantageous because it presented the true picture regarding the adoption of CSR in South Asia and the Western Food Companies. The quantitative study is conducted in four food industries of the South Asian Region, that is, India and Pakistan, as well as four food industries in the Western region. A survey comprising a questionnaire for evaluating CSR management system is prepared for shareholder groups such as personnel, clients, stockholders, community, natural environment, and sellers. The questionnaire is availed in the Appendix.

CSR adoption was measured using a 30-item scale that reflected the business roles toward different stakeholders with respect to economic performance. The 30 items were all measured on a scale of 1–10 with 1 showing low and 10 showing high level, respectively. The CSR score was the total value obtained as the score for each of the 30 items. Hence, the highest possible CSR score was 300 and was only observable if a responded provided a score of 10 for all the 30 items. The scale was validated by several authors (Hermawan & Mulyawan, 2014; S. Kiran et al., 2015). The NPM was measured using the income statement where the cost of goods sold, operating expenses, and other expenses and interests on debts were subtracted from the received revenue and divided by revenue. The value was then converted into percentage scores by multiplying by 100.

The concept of supplier was considered as an important variable which was set as a control variable. According to Hermawan and Mulyawan (2014), being a supplier was associated with reduced NPM. Also, industry subtype was believed to influence the NPM as different products attracted different types of clients with varying demographic characteristics, including salary. Above all, revenue was an important factor in the determination of NPM. It was argued that many of the companies that end up receiving high amounts of revenue can benefit from economies of scale resulting in higher NPM (S. Kiran et al., 2015). The analysis involved both descriptive and inferential statistics. For the descriptive statistics, the study computed measures of central tendency as well as measures of dispersion to describe the various characteristics of the sample. For the inferential statistics, a robust framework of the research hypotheses was formulated and based on the collected information; statistical tools were used to accept or reject the proposed hypotheses to assess CSR management system adaption. Assessment of the state of art in CSR management system, particularly in the food industry, is provided by using multiple OLSs regression model on 24 south Asian and 20 Western food companies across three subtypes. After the assessment of CSR adaption in South Asia, enriched comparative analysis has been provided between the Western food industries to provide complete understanding at the global level. The researcher ensured that all the necessary ethical requirements were met. First, senior management of the selected companies was requested to sign informed consent forms showing that the management was aware of the study and that they agreed to participate. Also, the researcher ensured that the data were handled with great confidentiality where the questionnaires were only sent to the researcher via a private email address. Above all, the researcher ensured that there was anonymity in the way participants’ information was gathered. No question in the questionnaire requested identifying information such as company name or address.

Results and Discussions

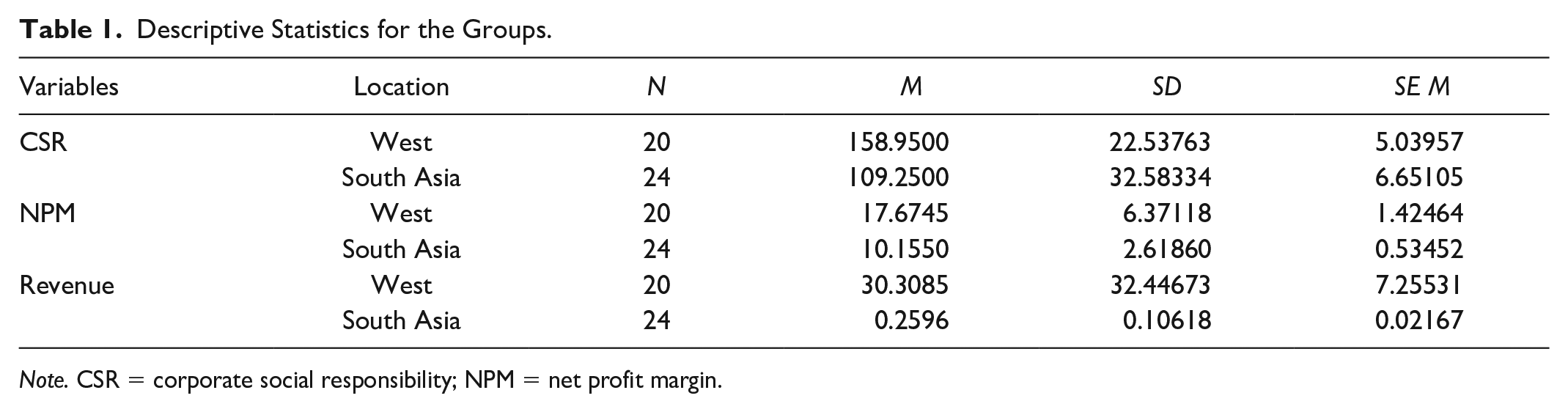

Descriptive Statistics

The results of the descriptive statistics showed that the sampled companies presented significant variations across the various variables for the two locations, which are presented in Table 1. The CSR score for the companies from the West had a mean value of 158.95 with a standard deviation of 22.54, while the companies from South Asia had a mean value of 109.25 with a standard deviation of 32.58. However, the NPM for the sampled companies from the West averaged at 17.67 with a standard deviation of 6.37, while the companies from South Asia averaged at 10.16 with a standard deviation of 2.62. Furthermore, the revenue of the sampled companies from the West averaged at 30.31 with a standard deviation of 32.45, while that of companies from South Asia averaged at 0.26 with a standard deviation of 0.106. It was noted that the companies from the West recorded better average scores than the companies from South Asia for the three variables.

Descriptive Statistics for the Groups.

Note. CSR = corporate social responsibility; NPM = net profit margin.

The distribution of the CSR score was assessed using a frequency histogram. According to the graph presented in Figure 2, a majority of sampled companies from both the West and South Asia had CSR scores around the mean as the bars at the center were taller than bars at the sides resulting in bell-shaped curves. However, more short bars were observed in the left-hand side than in the right-hand side for the histogram representing the companies from the West leading to figure that had a slightly longer tail toward the left. Hence, a conclusion was made that while the CSR score was normally distributed, there was evidence of slight negative skewness among the companies from the West. The results implied that a majority of the sampled companies from the West had CSR scores less than the average value of the sample. The two sampled groups had almost equal variances, although the values for the West companies were generally higher than those for the South Asian companies.

Frequency histogram for the CSR score.

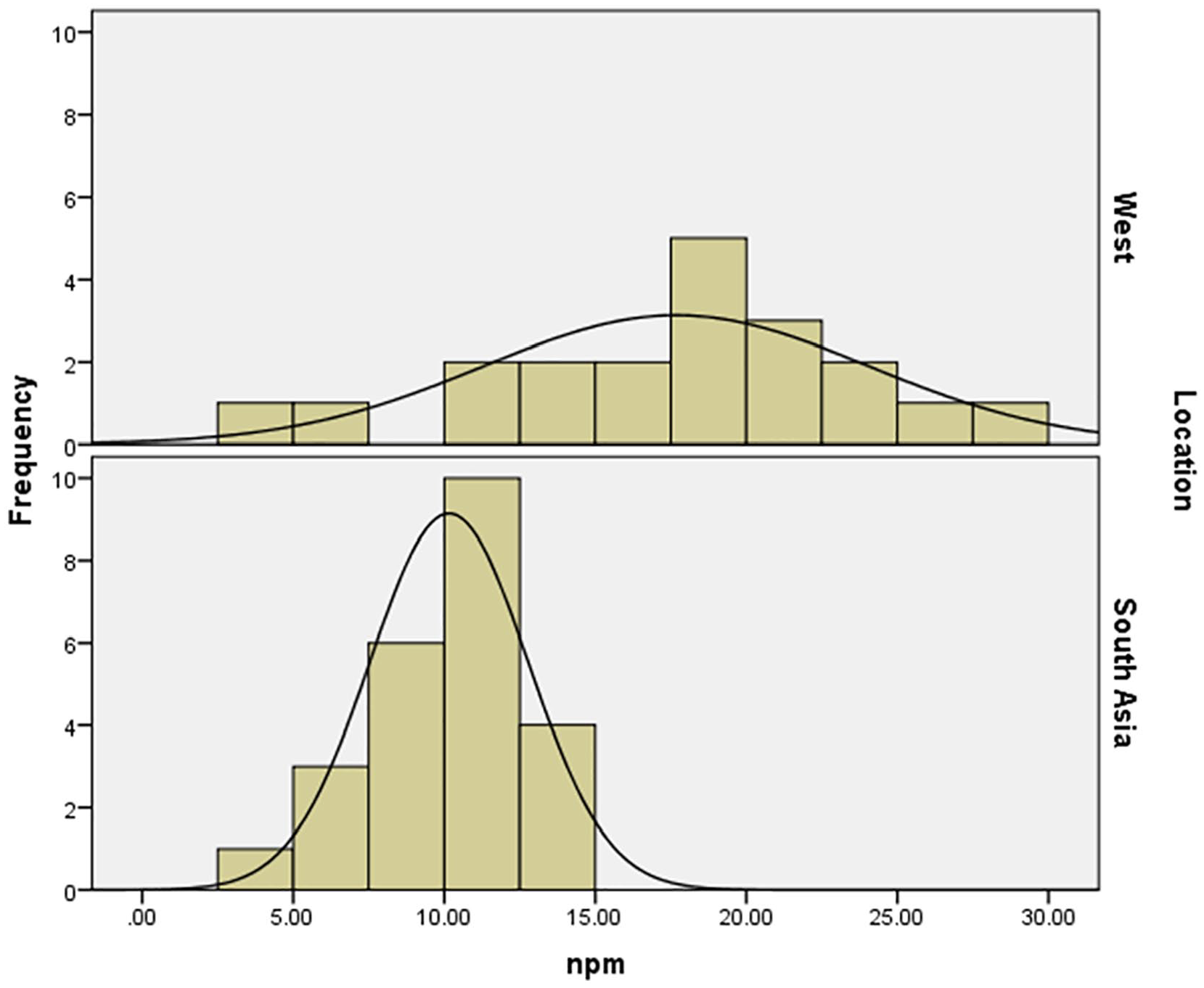

Also, the distribution of the NPM score was assessed using a frequency histogram. According to the graph, a majority of sampled companies had CSR scores around the mean as the bars at the center were taller than bars at the sides resulting in a bell-shaped curve. The two sample groups had different variances where the companies from the West varied more than companies from South Asia. In general, the companies from the West had higher NPM values than those for the South Asian companies as shown in Figure 3.

Frequency histogram for the NPM score.

Furthermore, the distribution of the revenue was assessed using a frequency histogram in Figure 4. According to the graph, a majority of sampled companies from the two locations had had low revenue values leading to a histogram whose shape was not similar to that of a bell. A conclusion was made that the revenue of the sampled companies was not normally distributed. There was evidence that the data were significantly skewed to the right.

Frequency histogram for the revenue.

The distribution of the sample across the subtype for the two locations was assessed using a cross-tabulation presented in Table 2. According to the analysis results, a majority of the sampled companies from the West belonged to the supplier subtype with a frequency of 11, while the rest, with a frequency of 9, belonged to the fast food subtype. Similarly, a majority of the sampled companies from South Asia belonged to the supplier subtype with a frequency of 18, while the rest, with a frequency of 6, belonged to the fast food subtype.

Subtype and Location Cross-Tabulation Count.

Similarly, the distribution of the sample across the company location was assessed using a frequency distribution. According to the analysis results, a majority of the sampled companies were from South Asia with a frequency of 24 (54.5%), while the rest, with a frequency of 20 (45.5%), were from the West.

Inferential Statistics

The results of the study have been presented separately for each of the hypotheses.

H1 results

Hypothesis 1 was as follows: CSR adoption is not as advanced in the South Asian food companies as compared to Western food companies. Figure 5 contains the strip plot of these data.

Strip plot, CSR by location.

The OLS result revealed that the food companies located in West had an increased CSR score of 49.70 points (b = 49.70, SE = 8.62, t = 5.76, p < .0001). The mean CSR score for South Asian food companies (M = 109.25, SD = 32.58) was significantly less than the mean CSR score for Western food companies (M = 158.95, SD = 22.54), t(42) = −5.76, p < .0001. To validate these findings, a Shapiro–Wilk (Shapiro & Wilk, 2006) test of normality was conducted on the dependent variable of CSR score. In the absence of normality, the parametric independent t-test findings could be triangulated through a Mann–Whitney (Mann & Whitney, 1947) U test. The Shapiro–Wilk test indicated that the dependent variable of CSR score was distributed normally, W = 0.97, z = 0.34, p = .37. A comparative kernel density plot of the distributions of CSR by location appears in Figure 6.

Kernel density plot, CSR by location.

H2 results

Hypothesis 2 was as follows: There is a positive relationship between CSR and the NPM among all food companies. The first step in analyzing these data was to visualize them in the form of a scatter plot, which is presented in Figure 7. The scatter plot includes the OLS line of best fit as well as the 95% confidence interval for this fit.

Scatter plot, NPM as a function of CSR.

The scatter plot suggests a positive relationship between CSR score and NPM. The OLS regression indicated that the regression of net profit margin on CSR score was significant, F(1, 42) = 7.92, p = .0074. The coefficient of determination of this OLS model was 0.1587, which indicated that 15.87% of the variation in the dependent variable of NPM was attributed to CSR performance. The predictor variable of CSR performance was significant (b = 0.06, SE = 0.02, t = 2.81, p = .007). Thus, for every one-point increase in CSR performance on the CSR scale utilized in this study, food companies experienced a NPM increase of 0.06%:

The quality of the OLS finding for H2 was tested using a Breusch–Pagan Cook–Weisberg (Breusch & Pagan, 2006; Cook & Weisberg, 1983) test of heteroskedasticity. The errors in the regression for H2 were found to exhibit constant variance, χ2 = 2.52, p = .1122. Therefore, no robust standard errors alternative to the OLS regression model was applied for H2.

The H2 results are shown in Table 3 and were re-evaluated after the addition of the control variables of industry subtype and revenue. In the revised model, the explanatory power of CSR on NPM declined as (b = 0.04, SE = 0.02, t = 1.83, p = .074) revenue was a significant and positive predictor of NPM (b = 0.07, SE = 0.03, t = 2.04, p = .048) and being a supplier (b = −3.10, SE = 1.83, t = −1.69, p = .099) was associated with reduced NPM.

H2 Model.

Note. NPM = net profit margin; CSR = corporate social responsibility.

H3 results

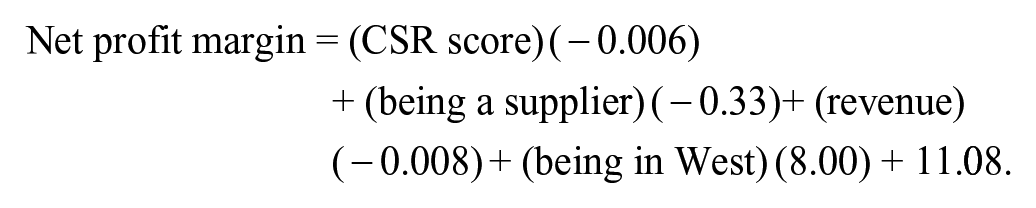

Hypothesis 3 stated that the positive CSR–NPM relationship is stronger for the Western than for the South Asian food companies. The first step in analyzing this hypothesis was to plot the NPM as a function of CSR separately for the Western and the South Asian companies (see Figure 8). In terms of analysis, the same multiple OLS model applied in H2 was reapplied to H3 with the addition of geographic location as a covariate. The b value and associated statistical significance of the predictor of the geographic location were then utilized to test H3.

Scatter plot, NPM as a function of CSR, sorted by location.

In Table 4, the OLS results for H3 indicated that once location was added as a covariate, the variables of CSR performance (b = −0.006, SE = 0.03, t = −0.23, p = .818), revenue (b = −0.008, SE = 0.04, t = −0.19, p = .849), and being a supplier (b = −0.33, SE = 1.89, t = −0.18, p = .862) were all insignificant and only location remained as a significant predictor (b = 8.00, SE = 2.59, t = 3.09, p = .004) of NPM.

H3 Model.

Note. NPM = net profit margin; CSR = corporate social responsibility.

One means of interpreting these findings is that the CSR–performance link does not exist for either the Western or the South Asian companies. Rather, the CSR–performance link is itself a spurious finding whose significance disappears when the location is a predictor variable, meaning that financial performance is a function of where a company is headquartered, not of a company’s CSR levels.

The findings of the study can be discussed in reference to the studies utilized for hypothesis-building as well as relevant theories. The absence of a correlation between CSR and financial performance was at odds with previous findings (Choi et al., 2010; Eberl & Schwaiger, 2005; Rose & Thomsen, 2004; Wang & Sarkis, 2017) suggesting this positive correlation. The findings are in line with theories of corporate advantage based in the privileged position of companies in the Global North (Albrecht et al., 2015) in terms of access to innovation, protection by high-quality governmental institutions, and other advantages. For South Asian food companies, one possible implication of this finding is that there is a reduced need to attempt to improve CSR as a driver of profitability. While there are other reasons to adopt CSR related to environmental stewardship, good corporate citizenship, and, possibly, competitive advantage rooted in the creation of a green premium. In addition, it does not appear as if profitability is a sequel of CSR adoption for the food industry, subject to the limitations of this study. However, another perspective on this interpretation is that, in both South Asia and the West, green consumers have not necessarily exerted market power in the food industry; should consumers demand higher levels of CSR, they might disproportionately frequent food companies in line with these values. Therefore, although no CSR–financial profitability relationship appears to exist for South Asian food companies, such a relationship might exist in the future.

Conclusion and Policy Implication

The purpose of this empirical study was to compare the South Asian with the Western food companies based on CSR adoption and CSR adoption–performance link. The comparison would, in turn, reveal whether the adoption of CSR systems had significant impacts on financial performance or not. In addition, the analysis aimed at revealing the state-of-art in CSR management systems in the food industry. Besides, the study would be able to figure out the framework of problems in the implementation of CSR management system and provide suggestions for better adoption.

Conclusion

The study, through the descriptive analysis, showed that the food companies varied significantly across the various variables, including CSR score, NPM, and revenue. Also, the study observed that the sample was balanced with respect to subtype and location where both the studied subtypes and the locations were fairly presented. However, it was revealed that Western food companies showed higher CSR performance than Asian food companies. As further observation was made that Western food companies recorded significantly higher NPM, an implication was made that CSR systems had significant effects on the financial performance of food companies. Also, through the scatter plot diagram, the study concluded that a positive relationship exists between CSR score and NPM. The coefficient of determination of this OLS model was 0.1587, which indicated that 15.87% of the variation in the dependent variable of NPM was attributed to CSR performance. The results for the model parameters suggested that for every 1-point increase in CSR performance on the CSR scale utilized in this study, food companies experienced a NPM increase of 0.06%. Moreover, it was revealed that with the addition of the control variables of industry subtype and revenue, the explanatory power of CSR on NPM declined. The company’s revenue was a significant and positive predictor of NPM while being a supplier was associated with reduced NPM.

Furthermore, after the location was added as a covariate, the variables of CSR performance, including revenue and being a supplier, were all insignificant, and only the location remained as a significant predictor of NPM. The analysis led to a conclusion that the CSR–performance link does not exist for either the Western or the South Asian companies. Rather, the CSR–performance link is itself a spurious finding whose significance disappears when the location is a predictor variable, meaning that financial performance is a function of where a company is headquartered, not of a company’s CSR levels. The study further concluded that governments have, to some extent, vested interests in improving CSR because as stewards of the environment for current and future citizens, they are responsible for maintaining the kinds of standards that are encoded within CSR.

Recommendations and Policy Implications

Governments should have a vested interest in improving CSR because as stewards of the environment for current and future citizens, they are responsible for maintaining the kinds of standards that are encoded within CSR. With this responsibility in mind, the governments, particularly in South Asia, could consider creating economic incentives for food companies and other corporations to increase their adoption of CSR. If there is no intrinsic financial advantage to be derived from higher CSR, then governments could create an extrinsic advantage through subsidies, tax breaks, and other incentives designed to reward food companies that demonstrate higher levels of CSR adoption and commitment.

Corporations should implement and adopt the policies and strategies of CSR as a priority to put off negative publicities in the future such as zero emissions operations during production and development of green parks and footpath. The development of industry standards gained an industry competitive approach which may produce higher emission barriers to achieve higher return and ensure competitive advantage. Therefore, it is necessary for corporations to maintain the pace of economic benefits and environmental concern. The development of industry standards is necessary because standards of environmental protection are fundamental for industry standards and the establishment of these standards should be legal such as the European Union passed Waste Electrical and Electronic Equipment standards to protect the environment.

However, the findings are limited and therefore propose some future research directions. The study had numerous limitations. We used only two covariates revenue and industry subtype, so other variables can be added in future research. The cross-sectional approach to analysis meant that longitudinal trends could not be identified. The sample size of the study (n = 44) was also small, and non-response bias suggests that the results of the study might not be generalizable to the population of food companies in South Asia and the West. Future researchers should consider studying the reciprocal links between CSR adoption, CSR effectiveness, and financial performance in a longitudinal manner. It is possible that financial performance benefits from CSR over time, in which case an approach based on vector auto-regression or an autoregressive distributed lag model might be an appropriate analytical strategy. Future researchers working with either cross-sectional or longitudinal models should add covariates to their analyses to obtain greater explanatory scope, precision, and power. In addition, future researchers should attempt to draw larger and more statistically representative samples.

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are grateful for the financial support provided by the National Natural Science Foundation of China, Grant/Award Number: 71572115; Major Program of Social Science Foundation of Guangdong, Grant/Award Number: 2016WZDXM005; and Natural Science Foundation of SZU, Grant/Award Number: 836.