Abstract

The severe acute respiratory syndrome coronavirus 2 (COVID-19) has significantly impacted the global economy. Presently, societies and businesses are facing unprecedented environmental shifts, with the sports industry being caught in this tumultuous tide. COVID-19 has affected all sectors of the global economy, suggesting an urgent need for most enterprises to reconsider their business models. This study investigates the advantages of corporate social responsibility (CSR) engagement during the negative external events of the COVID-19 pandemic, focusing specifically on the relationship between sports CSR and corporate financial performance and risk. Its objective is to provide empirical evidence on how sports CSR activities influence firm value, especially when facing systemic risks, and determine whether engaging in sports CSR serves as an effective protective tool against stock price decline. Methodologically, this study targets 159 companies that have received the Taiwan’s iSport Corporate Award over the years, employing the event study method and regression modeling to analyze the insurance effect of executing sports CSR on corporate financial performance during the COVID-19 pandemic. By offering empirical evidence on the relationship between CSR implementation and financial performance, this study contributes to a deeper understanding of the interconnectedness between sports CSR engagement and corporate financial outcomes, further enriching research in the realm of sports finance.

Keywords

Introduction

The severe acute respiratory syndrome coronavirus 2 (COVID-19) has emerged as the most significant event affecting the global economy since the Great Depression of the 1930s (Euronews, 2020). Owing to the widespread lockdowns and quarantine measures implemented across countries, both nations and individuals are grappling with the profound impact of the COVID-19 pandemic. Presently, societies and corporations are confronting unparalleled environmental shifts, and the sports industry is not immune to this upheaval (Parnell et al., 2022; Ratten, 2020a). With the progression of the United Nations’ Sustainable Development Goals (SDGs), corporate actions are pivotal for achieving the objectives set for 2030. The ramifications of COVID-19 will persistently be reflected in the capability of countries worldwide to meet these SDG targets (Shulla et al., 2021). As the COVID-19 crisis endures, posing threats globally, it has placed marginalized societal groups in numerous insurmountable predicaments. Organizations are significantly downsizing, leading to heightened unemployment rates, further exacerbating the economic crisis. These challenges have profound implications for the practice of corporate social responsibility (CSR) concepts in the future (He & Harris, 2020).

For sustainable enterprises, as the world is riddled with issues concerning natural disasters, climate change, food security, and waste pollution that adversely impact Earth, the actualization of CSR has become even more crucial. Similarly, the COVID-19 pandemic offers businesses the prime opportunity to manifest their environmental, social, and governance (ESG) principles, particularly the social dimension, to alleviate the crisis and address inequalities through their business models (Al Amosh & Khatib, 2023).

The manner in which a business constructs its model in alignment with social and environmental ethics is closely associated with stakeholder interests (Lins et al., 2017). Businesses are obligated to fulfill their social responsibilities in addition to bearing economic and legal responsibilities. Operational success can be achieved through a genuine commitment to economic, social, and environmental responsibilities and meeting the expectations of both internal shareholders and other stakeholders (Sexty, 2010, p. 139). In other words, for a business to thrive and develop, it should focus on the interests of all stakeholders, ensuring that its activities are legitimized, thereby maintaining alignment between societal and corporate objectives. When CSR initiatives genuinely cater to stakeholders and environmental needs, firm value increases correspondingly (Frynas & Yamahaki, 2016).

Under regular circumstances, research consistently posits that CSR investments augment firm value, subscribing to the belief that “doing good is good for business.” Similarly, after the COVID-19 crisis, both academia and the professional sphere have shifted their focus to the efficacy of CSR in safeguarding shareholders’ wealth. The crux of the discussions predominantly revolves around whether CSR engagement can maintain the resilience of firm value amid external systemic risks (Albuquerque et al., 2020). Due to the market collapse triggered by COVID-19, both market investors and business operators may intensify their attention and demand for CSR. This offers an avenue for examining whether businesses that invest in sports CSR activities can mitigate the negative effects under tremendous systemic risks. The COVID-19 crisis provides a distinct opportunity to validate the efficacy of CSR in shielding stock prices of companies.

Sports occupy a unique socioeconomic domain characterized by a large participating population, high media accessibility, and diverse attributes such as mass utility (Chadwick, 2009). Concurrently, sports embody vast societal functions including attracting younger participants, promoting a healthy image, enhancing social interactions and cultural exchanges, and strengthening environmental and sustainable management awareness. As such, any enterprise is aptly positioned to engage in CSR activities through a sports platform (Walters, 2009). The United Nations Office on Sports for Development and Peace (UNOSDP) underscores the multifaceted role of sports in individual and societal development. These roles encompass “personal development,”“health promotion and disease prevention,”“promotion of gender equality,”“social integration and development of social capital,”“conflict prevention and peace-building,”“mediating post-trauma or disaster recovery,”“economic development,” and “communication and societal mobilization.” Sports have long been recognized as a pivotal catalyst for sustainable development (Jadon, 2017), which resonates deeply with the core values of CSR. It means that the multidimensional nature of CSR, including economic, legal, ethical, and discretionary responsibilities might influence public perceptions of CSR activities conducted by sports organizations (Thormann & Wicker, 2021).

Similarly, the “Sport i Taiwan” initiative, promoted by the Ministry of Education, Sports Administration of Taiwan, offers enterprises the opportunity to actualize their CSR through sports, be it by embedding sport culture, expanding sport knowledge, propagating sport fundamentals, or promoting sport cities (Ministry of Education, Sports Administration, 2015). Notably, from 2016 to 2022, the continuous implementation of the Taiwan iSport Corporate Award was championed through collaboration between the government and businesses in support of the sports industry’s development. This program accentuates corporations’ sports engagement, underscores their commitment to healthy human resources and brand value, and encourages companies to actively instill regular exercise habits among their employees, thus actualizing the principle of caring for employees through sports CSR.

Currently, CSR is universally acknowledged as a vital tool for sustainable development, and its significance has gradually surfaced in sports management research. Numerous studies have underscored the importance of sports organizations fulfilling their sports CSR and showcased successful instances (Plewa & Quester, 2011; Smith & Westerbeek, 2007). Although M. Gao and Geng (2024) have indicated that ESG contributes to corporate resilience during crises, providing more solid data to support the conclusion that ESG improves corporate resilience, research on CSR and corporate value still reveals mixed perspectives. While some argue that CSR boosts company image (Song et al., 2017), enhances stakeholder trust, and reduces risk (Albuquerque et al., 2019), others view it as an agency cost where management might prioritize personal gains, thereby hurting firm value (Xiao et al., 2020). Therefore, topics concerning corporate entities actualizing sports CSR, establishing social capital, and interrelations with corporate financial performance (CFP) require more extensive research for validation. This study will fill the research gap observed in past sports management studies on CSR. Especially during the COVID-19 pandemic, extending the discussion on corporate participation in sports, CSR, and CFP has become indispensable.

As the COVID-19 crisis has affected all sectors of the global economy, most businesses are urgently rethinking their business models in response to significant shifts. This study primarily seeks elucidates the advantages of businesses engaging in sports CSR during the external negative events precipitated by COVID-19. It provides empirical evidence by examining the effects of sports CSR-related performance on CFP, corporate value, and market risk. It clarifies whether corporate engagement in sports CSR can protect companies against crises, especially in the face of negative macro-level events.

Literature Review

COVID-19 Crisis and the New Normal in Corporate Management

COVID-19 has instigated significant uncertainties in daily life, prompting concerns about a global economic crisis and recession (Nicola et al., 2020). Societal activities have been affected by the pandemic due to novel social behaviors, such as social distancing and self-isolation. These unprecedented phenomena starkly contrast with past policies promoting the globalization of the sports industry. The pandemic has severely affected companies, compelling them to reconsider appropriate business models (Ratten, 2020a). Consequently, advocating for an open style of business engagement with stakeholders, such as service-orientation, digitalization (F. Almeida et al., 2020; Juergensen et al., 2020), and corporate collaborations (Crick & Crick, 2020), constitutes the “new normal” in current business operations in the face of the COVID-19 crisis (Ratten, 2020b).

With the COVID-19 outbreak, research on its impact on business operations has expanded. Topics range from impact assessments on specific industries, such as tourism, food, and finance (Akinwale, 2020; Shahzad et al., 2022), crisis and risk management strategies (Chen et al., 2021), to the pandemic’s effects on business performance and stock returns (Bose et al., 2021; Fahlenbrach et al., 2020). Topics concerning CSR activities and business performance have also been fervently discussed during the pandemic (Bae et al., 2021; Bose et al., 2021; Demers et al., 2021; Shin et al., 2021). In the real world, businesses participated globally in various CSR activities during the COVID-19 crisis, including monetary and product donations, personal protective equipment production, unlimited mobile data offerings to customers, reduced insurance rates, and adjusted working hours for healthcare personnel during the pandemic (He & Harris, 2020).

Similarly, discussions about the COVID-19’s impact on sports have increased. For instance, Parnell et al. (2022) analyzed the COVID-19’s effect on sporting event crowds. Whether COVID-19 will fundamentally change the operation modes of related sport industries in the future requires further research evidence to bridge the gap.

Social capital perspective of CSR

Social capital, a form of capital, is characterized by its use in achieving instrumental or expressive objectives through social networks and the reciprocity and trust norms formed on this foundation (Bourdieu, 1986). The concept of social capital has continually garnered attention in both academic and practical fields, with applications in various domains (Putnam, 2000). According to the World Bank’s operational definition, social capital refers to the institutions, relationships, attitudes, and values that govern interactions among people and contribute to economic and social development (Grootaert & van Bastelaer, 2002). Academically, the social capital’s essence encompasses a broad and intricate domain, including individual psychology, culture, social interaction, and coexistence (Vveinhardt et al., 2014). Scrivens and Smith (2013) proposed that social capital can be segmented into four dimensions: personal relationships, social network support, civic participation, and trust and cooperation norms.

Civic participation within social capital denotes proactive contributions to the community through agents (e.g., by volunteering, political participation, and donations) (Guiso et al., 2011; Scrivens & Smith, 2013). Such participation can foster reciprocal actions based on trust and cooperative norms. From these measurement perspectives, social capital is seen as a driver of collective action and collaboration, yielding positive economic growth and performance by reducing transaction costs and allocating resources more efficiently (Bueno et al., 2004). Sacconi and Antoni (2011) emphasized the significant impact of well-implemented CSR on employees’ social capital. Gupta and Krishnamurti (2018) suggested that CSR performance contributes to establishing moral and exchange capital, aiding companies facing financial bankruptcy. As CSR can be considered as a mechanism of moral norms in society and markets formed by the will and expectations of civil society rather than institutional power, there is an intrinsic relationship between CSR and social capital. This means that enhancing social capital can positively impact CSR, and CSR practices can boost the accumulation of social capital (Vveinhardt et al., 2014).

Although Sapienza et al. (2013) argued that it might be impossible to gage a company’s comprehensive social capital through a single CSR investment level, CSR can at least be seen as a core indicator for measuring social capital, and it often elicits superior accounting performance (Flammer, 2015). Guiso et al. (2004, 2008) emphasized that higher degrees of social capital trust lead to greater stock market participation, thus substantiating the critical impact of social capital and trust on CFP from a macroeconomic viewpoint.

CSR can be viewed as a corporate commitment that contributes to sustainable development, mainly concerning the societal impacts of corporate behavior. Corporate decision-makers are responsible for ensuring that business activities cater to stakeholder interests and overall augment societal welfare (Carroll & Buchholtz, 2011). At the operational level, business managers commonly believe that CSR initiatives foster the establishment of social capital, amplify trust, and encourage collaboration with high CSR entities (Eccles et al., 2014). Hence, CSR can also become a competitive advantage for enterprises (Porter & Kramer, 2006, 2011), reducing the potential for short-term managerial speculative behavior by reinforcing stakeholder involvement (F. Gao et al., 2014). Over the decades, CSR research has covered a wide range of topics, each with its focal points, including the relationship between CSR and CEO’s risk-taking decisions (Dunbar et al., 2020), how CSR influences uncertainties pertaining to mergers and acquisitions (Arouri et al., 2019). Such focal points also include the impact of CSR on corporate financing and capital costs (H. Gao et al., 2021), effect of cause-related marketing on sales and growth (Lev et al., 2010), and association of CSR with labor productivity and financial performance optimization (Flammer, 2015).

Sport organizations can cultivate public trust and accumulate social capital. This not only meets public demand for sports and leisure activities but also assists governments in promoting national sports and implementing sports policies, further serving as a bridge between governments and international organizations (Tacon, 2014). Zhou and Kaplanidou (2018) empirically found that participatory sporting events can yield stable positive social capital for local communities, including supportive attitudes and behaviors, positive influences on others, prosocial actions, and increased daily social activities. Douvis and Kyriakis (2022) integrated the concept of CSR with sports management, stressing transparency, accountability, and interactions with stakeholders as indispensable elements for sports organizations to actualize CSR. Therefore, given the nature of social capital, whether businesses can fulfill CSR while simultaneously balancing the maximization of shareholder value and stakeholder interests requires further research to elucidate the connection between financial performance and CSR practices.

Relationship of CSR, CFP, and Market Risk Under Negative Events

The perpetual debate within the realm of financial management revolves around whether a company’s ultimate objective is to maximize shareholder value or stakeholder welfare (Krüger, 2015). The crux of this debate is the relationship between sports CSR activities and corporate performance (Arouri et al., 2019; Dunbar et al., 2020; Flammer, 2015), particularly under the influence of negative external events. For instance, the global economic downturn triggered by the U.S. subprime mortgage crisis between 2008 and 2009 severely impacted businesses and the entire economic sector (Dekimpe & Deleersnyder, 2018). As CSR is often perceived as a peripheral business activity, companies may adjust its input depending on operational costs (Aguinis & Glavas, 2013). Consequently, during severe market downturns, CSR might be deemed an “unaffordable luxury,” leading to recommendations that businesses reduce CSR investment and concentrate exclusively on core operational activities to prevent a decline in profitability (Franklin, 2008).

A retrospective view of capital market reactions reveals that during the early stages of the COVID-19 pandemic in the first quarter of 2020, global capital markets plummeted. The market generally referred to ESG as a “stock vaccine” against crash induced by the pandemic (Willis, 2020). However, by the latter half of 2020, the market began to question whether ESG truly served as an effective protective shield during the COVID-19 crisis. By early 2021, critics opposing this narrative had begun to advocate that ESG was an outdated concept (Steffen, 2021).

In terms of defensive efficacy of CSR against negative events, fulfilling CSR has been proven to offer insurance-like protective measures that benefit company operations during challenging times. Having good social relations and practicing CSR are akin to purchasing insurance for long-term corporate profits and image, which can mitigate the impact of negative events on CFP (Jia et al., 2020; Lins et al., 2017).

From a risk management standpoint, Koh et al. (2014) articulated that exemplary corporate social performance (CSP) could serve as a valuable ex-ante insurance mechanism to augment corporate value during rare environmental disasters or social mishaps. Value generation through CSP hinges on whether a company attains pragmatic legitimacy among its stakeholders and moral legitimacy. Albuquerque et al. (2019) suggested that companies with a higher sense of social responsibility face lower demand price elasticity. Socially conscious consumers tend to be highly loyal, implying that cash flows would exhibit fewer fluctuations throughout business cycles. Consequently, companies with high CSR experience fewer losses during business downturns and lower gains during recovery phases. Liu et al. (2020) used a sample of lawsuits filed in U.S. federal courts to investigate how a company’s CSR reputation and environmental lobbying efforts can protect shareholder wealth during adverse environmental litigation events. However, they also found that companies with a strong CSR reputation face more severe market reactions to environmental allegations. Ding et al. (2021) studied the stock price variations of multinational corporations practising CSR before 2020 during the COVID-19 pandemic. They revealed that companies with a high degree of CSR exhibited better stock performance.

Some recent studies provide valuable insights into the application of resilience theory in the realm of financial performance, offering a nuanced understanding of how resilience impacts corporate and entrepreneurial success (Alshebami & Murad, 2022; Zhang et al., 2023). Similarly, the view that CSR activities improve stock price resilience during crises is based on the belief that such activities help build social capital and trust in businesses, motivate stakeholders, and assist companies in overcoming the challenges posed by crises. CSR can protect against stock price decline during crises (Albuquerque et al., 2020; Ding et al., 2021; Jia et al., 2020). This effect is akin to the argument emphasized by Lins et al. (2017) during the 2008 to 2009 global financial crisis, who posited that building social capital and trust enables businesses to be more resilient under tumultuous market conditions. However, Berkman et al. (2021) provided evidence from the global financial crisis, countering the claims of Lins et al. (2017) and suggesting that CSR might not be applicable to alternative investments or to non-U.S. firms. Demers et al. (2021) also refuted the significance of ESG in explaining U.S. stock returns during the COVID-19 pandemic. Many critics argue that CSR activities divert excessive resources outside the core business; besides, there is a lack of effective oversight on the motivations of corporate management in executing CSR, potentially leading to severe agency problems and preventing the transfer of CSP to CFP. Community-based CSR practices do not benefit shareholder equity significantly. Hence, recent studies underscore inconsistent views on the value and stock resilience of companies practising CSR during different crises.

Sports organizations are closely linked to general business activities, and both can produce societal benefits, serving as a bridge between stakeholders’ social and economic interests (Smith & Westerbeek, 2004). Smith and Westerbeek (2007) pointed out that sports have a unique and superior influence on promoting health consciousness, youth education, and community relations management, highlighting the potential to develop a distinct “sport corporate responsibility” model. The sports sector possesses managerial advantages due to close stakeholder relations and has a unique impact in promoting health awareness, youth education, and community relations. However, the effects of practising any kind of sports CSR activities on businesses or sports organizations during the negative environment of the COVID-19 pandemic deserve ongoing attention and tracking by further studies.

Hypothesis Development

Although a substantial body of literature has explored the impact of trust and social capital on economic life, numerous studies have confirmed that having strong social relationships and practising CSR can offer protective measures akin to insurance, enabling companies to navigate crises (Gupta & Krishnamurti, 2018; Lins et al., 2017). In particular, during negative external events such as financial crises, the importance of social capital in market operations and financial stability becomes even more pronounced (Lins et al., 2017). Although Guiso et al. (2004, 2008) suggested that trust derived from social capital fosters increased stock market participation, the extent of the influence of social capital and trust on CFP remains relatively underexplored.

CSR proponents assert that investing in CSR helps companies build social capital and establish trust toward a firm. They believe that responsible corporate behavior toward society and the environment results in essential connections between a company and its stakeholders. Moreover, such benevolent actions are particularly rewarded during a crisis. This “risk management” perspective on CSR presumes that CSR investments can function as an insurance-like mechanism to hedge against stock market downturn risks (Albuquerque et al., 2020; Ding et al., 2021; Jia et al., 2020). Hence, we propose the following hypothesis:

Hypothesis 1: During the stock market crash induced by COVID-19, the abnormal returns of Taiwan’s iSport Corporate Award winners outperformed those of the overall stock market.

According to a comprehensive review by Friede et al. (2015), which aggregated findings from over 2,000 empirical studies, a positive relationship exists between ESG factors and financial performance. Multiple studies further argued that CSR can mitigate tensions from negative events, reduce risks, and promote a favorable image of corporate entities in the market (Albuquerque et al., 2019; Ding et al., 2021; Gupta & Krishnamurti, 2018; Jia et al., 2020; Koh et al., 2014; Lins et al., 2017). However, the principles of social exchange remain relatively uncertain, particularly when confronted with conflicting interests of shareholders and other stakeholders. The existing literature on CSR has yet to reach a consistent conclusion.

In essence, when a firm receives the Taiwan’s iSport Corporate Award, it signifies that its involvement in sports CSR has garnered multifaceted trust and commitment from stakeholders, such as the government, the general public, company employees, and their families. This trust can potentially alleviate the negative impacts on CFP during stock market crashes induced by macro-level negative events, and might even shield the firm’s value, reducing market risks. Hence, we propose the following hypotheses:

Hypothesis 2: During the stock market crash caused by COVID-19, a significant positive relationship existed between the CSR scores of Taiwan’s iSport Corporate Award winners and their CFP.

Hypothesis 3: During the stock market crash triggered by COVID-19, a marked positive correlation existed between the CSR scores of Taiwan’s iSport Corporate Award winners and firm value indicators.

Hypothesis 4: Amidst the stock market downturn due to the COVID-19 outbreak, the higher the CSR scores of Taiwan’s iSport Corporate Award winners was, the lower the market risk they had to bear.

Methodology

To assess the protective effect of corporate engagement in sports CSR activities during the stock market crash triggered by COVID-19, a two-phase approach was adopted to validate the aforementioned hypotheses.

In the first phase, an event study method was employed to preliminarily estimate and test the abnormal returns of stocks belonging to Taiwan’s iSport Corporate Award winners during the COVID-19 crisis. These returns were, then, compared with the abnormal returns of the overall Taiwanese stock market during the crash. This was done to determine whether portfolios comprising Taiwan’s iSport Corporate Award winners yielded relatively higher abnormal returns than the overall market.

In the second phase, regression models were formulated to explore the relationship among various CFP metrics, firm value indicators, and market risks with the CSR performance of sports enterprises during the stock market crash induced by COVID-19.

Event Study Method

As Shin et al. (2021) pointed out, changes in market value following announcements of events, such as new corporate social initiatives, can serve as an estimate of the impact of such initiatives. The use of the econometric event study methodology for estimating changes in corporate market value has matured in modern marketing, finance, and economics research. The functional application of the event study methodology in sports management should also be evident (Lei et al., 2010; Samitas et al., 2008). This methodology is based on the basic principles of the efficient market hypothesis, assuming that a firm’s market value is fully reflected in its stock price, which means that any relevant information in the market is reflected in CFP.

Selection of Event and Estimation Windows

Given the need for a sample data period that covers both the event and estimation windows, our study aligns with the fluctuations of Taiwan’s stock market induced by COVID-19. Due to the COVID-19 outbreak, the first crash of Taiwan’s stock market began on 20 January 2020, the day when the Central Epidemic Command Center was established and opened at the third level. Signs of escalation in Taiwan’s COVID-19 situation started to appear from that day. The downturn persisted until 21 March 2020, when the stock market began to rebound, lasting for a total of 61 days. Similarly, the second crash of Taiwan’s stock market began on 23 April 2021, when China Airlines formally reported that a cargo plane’s pilot was infected. The Taiwanese situation continued to worsen. However, when the daily increase in locally transmitted cases began to decline, the stock market started to rebound after 23 May 2021, lasting for a total of 31 days. Therefore, we chose two stock market crash periods triggered by COVID-19 as event windows: 20 January 2020 to 21 March 2020 and 23 April 2021 to 23 May 2021. The market-adjusted stock return rate was used to measure daily stock market returns. To avoid overlap between the estimation and event windows, we set 100 stock market trading days before 20 January 2020 and 23 April 2021 as the estimation windows.

Moreover, if the sample companies’ stock prices were affected by COVID-19, the variance in stock returns during the event window might have significantly increased (event-induced variance). Using information from the estimation window to estimate the abnormal return variance during the event window might be meaningless (Brown & Warner, 1985). Thus, we considered ignoring the residual information of the estimation window, calculating the variance of abnormal returns during the event window based on individual sample companies, and assumed that individual abnormal returns between different sample companies are unrelated, that is,

Considering the research event’s impact, the COVID-19 pandemic can be seen as an external event affecting the entire stock market. As the event day for all certified company samples is the same calendar date, and considering that the daily stock price data used may deviate from the norm, our study employs the GARCH (1, 1) method of the market risk adjustment model to estimate the expected return of the sample companies’ stock prices (Bollerslev et al., 1992) before testing the abnormal returns. The return estimation model is as follows:

Here,

Calculation of Abnormal Returns

The individual stock return rate of a sample company is defined by equation (2):

where

where

Using equation (4), we calculate the cross-sectional cumulative abnormal returns (CAR) of companies recognized for sports certification and all listed companies during the stock market crash caused by COVID-19. Then, we test whether companies recognized for sports certification have a significantly smaller negative CAR than all listed companies.

Measurement of Variables and Regression Model

Variable Measurement

To comprehensively examine the impact of the CSR-related performance of companies that obtained sports enterprise certification during the second stock market crash caused by COVID-19 on CFP, corporate value, and risk, we measure CFP based on the models of H. Almeida et al. (2012) and Harford et al. (2014). The measurement uses accounting-based indicators such as return on assets (ROA), return on equity (ROE), and earnings per share (EPS) to evaluate the CFP of the sample companies. Corporate value is measured using the market-based value indicator, Tobin’s Q. For the risk variable, the market risk (BETA) during the two stock market crashes is estimated using the event study method. CSR performance during the stock market crash is measured using three variables: the sports CSR rating score (SCSR) of the sample companies, cumulative number of Taiwan’s iSport Corporate Award obtained from 2016 to 2022 (SCA), and total annual ESG activity score (TESG) of the sample companies.

Furthermore, considering that the CSR performance of companies that have obtained sports enterprise certification during the COVID-19 pandemic might be affected by the omission of important variables, making the CFP not attributable to CSR itself, the regression model includes variables that may affect the CFP, value, and risk of the sample companies during the COVID-19 pandemic as control variables. These include the size of a sample company (LnScale), debt ratio (DEBR), R&D expense ratio (RD) (Morck et al., 1988), price-to-book ratio (PB) (Goss & Roberts, 2011), board size (BOARD), management shareholding ratio (MHO), institutional shareholding ratio (IHO) (Yermack, 1996), stock price momentum factor (MOM) (Bae et al., 2021), and the four major industry categories (measured by dummy variables). Table 1 provides the names and definition/measurement indicators of each variable.

Variable Definitions and Measurement.

Regression Model

To understand how CSR-related indicators influence the financial performance, company value, and market risk of the sample companies during the COVID-19 crisis, we establish a cross-sectional regression model for the sample companies during the two stock market crashes, as shown in equation (5).

where

Data Selection

The sample selection predominantly focused on companies that were recipients of the Taiwan iSport Corporate Award announced by the Sports Administration of the Ministry of Education between 2016 and 2022. This included a total of 574 private enterprises, some of which were awarded multiple times. Subsequently, these award-winning enterprises were classified based on whether they were publicly listed or traded on the over-the-counter market. If a Taiwan’s iSport Corporate Award winner was not publicly listed during the research period, it was excluded due to the challenges in obtaining financial data and concerns over its authenticity. Consequently, a total of 159 valid sample companies were selected to ensure consistency in the quantitative analysis. The secondary data on the financial performance, stock market transactions, and Corporate Social Responsibility (CSR) performance scores of these sports companies primarily utilize daily data, extracted from the Taiwan Economic Journal (TEJ) database. The measurement and extraction of each data point are based on the descriptions in Section 3.2.1, as referenced in Table 1. The data period will fully encompass the two crashes in Taiwan’s overall stock market during the COVID-19 pandemic from 2020 to 2021.

Results and Discussion

Abnormal Stock Returns of Taiwan’s iSport Corporate Award Winners During the Stock Market Crashes

During the two stock market crashes triggered by COVID-19, the cross-sectional stock price CAR for both Taiwan’s iSport Corporate Award winners and the entire set of publicly listed companies was computed using the event study method. Although both showed statistically significant negative CARs, the CAR for Taiwan’s iSport Corporate Award-winning companies (159 in number) during these two crash periods was notably higher than that for all listed companies (1,677 in number), as illustrated in Figures 1 and 2. In these two periods, the average CAR for the sample of Taiwan’s iSport Corporate Award winners was −5.274% and −3.34%, respectively, both of which exceeded the CAR of the entire set of publicly listed companies of −8.594% and −5.735%, respectively.

Comparison of CAR between Taiwan’s iSport Corporate Award winners and all listed companies during the 2020 stock market crash.

Comparison of CAR between Taiwan’s iSport Corporate Award winners and all listed companies during the 2021 stock market crash.

Further T-test analysis, as presented in Table 2, revealed that Taiwan’s iSport Corporate Award winners had a significantly smaller negative CAR compared to all listed companies. This finding suggests that, when impacted by external macro negative events, the abnormal stock returns of Taiwan’s iSport Corporate Award-winning companies outperformed those of the overall stock market. Consequently, Hypothesis 1 is supported.

Analysis of CAR Differences Between Taiwan’s iSport Corporate Award Winners and All Listed Companies Across Different Stock Market Crashes.

p < .01.

Correlation Analysis and Regression Estimation Results

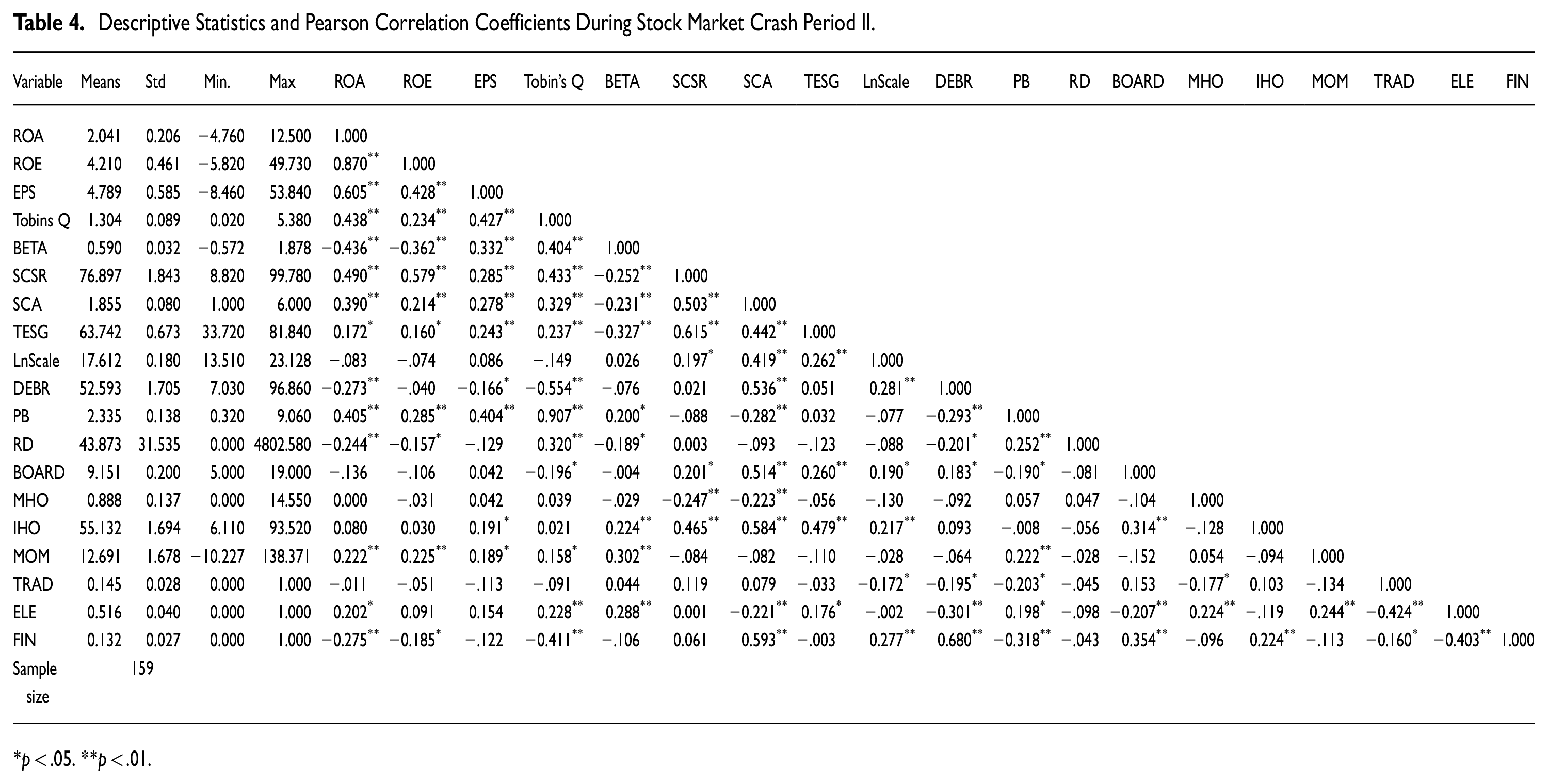

The Pearson correlation matrix across the two stock market crash periods shows that the CSR-related performance variables are predominantly and significantly positively correlated with CFP and company value, and significantly negatively correlated with market risk, as shown in Tables 3 and 4. This suggests that companies with better CSR-related performance tend to display better financial performance and higher company values, and take lower market risks when faced with macro-level negative events, such as the COVID-19 pandemic.

Descriptive Statistics and Pearson Correlation Coefficients During Stock Market Crash Period I.

p < .05. **p < .01.

Descriptive Statistics and Pearson Correlation Coefficients During Stock Market Crash Period II.

p < .05. **p < .01.

The regression results in Table 5 indicate that the estimated coefficients for the three CSR-related performance variables—SCSR, SCA, and TESG—are significantly positive. This suggests that sample companies with higher sports CSR scores, more accumulations of Taiwan’s iSport Corporate Awards, or higher annual ESG event overall scores tend to have relatively higher ROA, ROE, and EPS, indicating better CFP. Similarly, these three CSR-related performance measures have a positive relationship with the company value indicator (Tobin’s Q). This highlights that, even under the impact of external macro-negative events, CSR-related performance can positively influence company value. Consequently, these findings support Hypotheses 2 and 3. Furthermore, from the estimation results of the risk variable (BETA), the coefficients for all three CSR-related performances are significantly negative, suggesting that if the sample companies have better CSR-related performance, they face lower market risk, thus supporting Hypothesis 4.

Regression Estimates of CSR-Related Performance on CFP, Firm Value, and Market Risk During the Two Stock Market Crash Periods.

Note. The t values of the estimated coefficients are in brackets.

p < .05. **p < .01.

Discussion

The empirical results show that when the stock market crashed due to the panic induced by COVID-19, companies that had received sports enterprise certification had a lower degree of negative stock price CAR than all listed companies. This phenomenon resonates with the findings of Jia et al. (2020), who found that market investors show lesser short-selling interest in companies with better CSR performance. This finding suggests that a lower negative stock price CAR can be attributed to the insurance effect of CSR-related performances.

Hence, in the face of macro-level negative events, a company’s actions and performances related to CSR help establish a more robust performance insurance and risk mitigation mechanism compared to that of the overall market. Market investors can select companies with commendable sports CSR outcomes as an investment portfolio to buffer stock price returns and mitigate negative impacts, thereby reducing investment losses. This aligns with Friede et al. (2015), who emphasized that ESG-related investment strategies generally do not lead to inferior financial performance. Especially under external macro-negative events, sports CSR can predict positive risk-adjusted performance, offering an insurance effect on company value. Investors should consider the role of CSR performance in their investment strategy, as it is a risk management tool and a potential driver of performance.

Meanwhile, companies with better sports CSR performance build a good image and trust, thus accumulating reputational capital in the financial market. When negative external events occur, the social capital built through CSR participation can act as a buffer against negative financial impacts, resulting in companies bearing lesser market risks. This is consistent with prior studies emphasizing the social capital perspective (e.g., Gupta & Krishnamurti, 2018; Jia et al., 2020; Lins et al., 2017; Minor & Morgan, 2011). This finding highlights that companies with better sports CSR performance gain an additional layer of social capital and trust in stakeholder evaluations. Even when facing negative external events, the general public’s willingness to trust companies with superior CSR performance ensures that the impact on the financial performance of these companies is relatively low, providing a protective effect on company value.

Conclusions

Empirical Findings

Past research on CSR has largely focused on the impact of CSR engagement on firm performance, with limited empirical investigation into the insurance effect of sports CSR implementation during specific periods. This study considers the stock market crash caused by COVID-19 in Taiwan as a significant negative event. It explores the effects of sports CSR-related performance on CFP and market risk among 159 firms.

The empirical results indicate that while companies committed to sports CSR cannot be entirely immune to the stock market crash triggered by the COVID-19 outbreak, their performance is notably more resilient than that of the overall stock market. Many firms in this study were non-sports organizations. Despite the significant resources and costs associated with engaging in sports CSR, these investments align with government policy incentives and also fulfill contemporary corporate management objectives of maximizing stakeholder benefits. These findings provide evidence supporting recent claims in the literature that proactive CSR engagement facilitates sustainable corporate development, enhances firm value, and offers performance insurance under adverse conditions.

This study’s results encourage corporate management to recognize that obtaining the Taiwan’s iSport Corporate Award is a manifestation of the implementation of sports CSR. This aligns with various aspects, such as sustainable business operations, workplace environment, and employee welfare, fulfilling the policy objectives set by the Taiwanese government to integrate sports elements to foster a friendly and healthy environment for businesses and their employees. In the long run, engaging in sports CSR helps build a firm’s healthy human capital, brand value, and image, providing insurance against shocks from macro-negative events, such as the COVID-19 pandemic. Therefore, a company’s management should base its operations on winning stakeholders’ trust and support. Fulfilling sports CSR responsibilities ensures financial advantages for firms, especially in the face of macro negative events, where strong CSR performance can serve as a protective mechanism for CFP.

Managerial Implications

By incorporating financial metric methods in this study, the empirical findings suggest that Taiwanese firms’ participation in sports CSR positively affects their financial performance and provides an insurance function. This is consistent with most previous CSR research perspectives. The empirical data highlight a significant positive reaction to financial performance during macro-negative events when firms engage in sports CSR activities. This implies that companies with good sports CSR outcomes can be considered low-risk investment portfolios.

Amid the rapid advancement of global SDGs initiatives, there is no doubt that the future will bring new standards and requirements for sports organizations’ CSR activities. Companies will also have to deal with pressure and increased market awareness from investors and consumers. The development of sports CSR in Taiwan is becoming an increasingly important commercial practice and academic topic. Through an empirical analysis, this study reveals the pattern of Taiwanese firms’ engagement in sports CSR during the COVID-19 pandemic, reflecting abnormal stock returns, CFP, and market risks. This confirms the positive relationship between the promotion of the Taiwan iSport Corporate Award and corporate CFP. The methodologies and results presented should guide future organizational practices in sports CSR and sustainable development. This study also aids investors by revealing the impact of sports CSR practices on stock market performance, helping them strategise their investment portfolios.

Research Limitations and Further Studies

This study validates the insurance effect of Taiwanese companies practising sports CSR on their financial performance. However, due to sample size constraints and the availability of specific corporate financial data, this study did not differentiate or quantitatively include the performance of the sample companies across various stakeholder groups. Aspects such as environmental impacts, employee rights, relationships with consumers and the supply chain, information disclosure, and corporate governance were not evaluated.

This makes it challenging to assess which of these areas predominantly represent the insurance function of CSR performance. The research model did not compare the differences in CSR engagement between sports and non-sports organizations, nor did it specifically pinpoint the impact of ESG-related activities by sports industries on their CFP during the research period. Future studies could consider expanding the sample size, collecting long-term data, or employing case studies to delve deeper into the motivations and processes behind sports CSR and reveal its philosophical connections with organizational performance. This will serve as a robust foundation for sports enterprises to develop ESG strategies or guide investors in market portfolio allocations.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Science and Technology Council under Grant MOST 111-2410-H-156-004.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.