Abstract

This research investigates the moderation effect of strategic intent in the relationship between business respect, reciprocity, and loan repayment (LR) in microfinance. This study uses social exchange theory to relate business respect, reciprocity, strategic intent, and LR, improving our understanding of the theory in the context of microfinance and its scope of applicability in the business-to-business (B2B) context. Data was collected using a cross-sectional design and structured questionnaires from 603 respondents, and analyzed using the multiple regression analysis technique. Findings reveal that LR is influenced by the business relationship quality dimensions of respect and reciprocity. Strategic intent moderates the relationships between business respect, reciprocity, and LR. The research was conducted in developing nation, Tanzania. Hence, it opens an opportunity for cross-cultural validation in different countries to foster generalizability. By considering reciprocity norms when deciding loan factors such as interest rates and repayment schedules, microfinance institutions (MFIs) could achieve their social goal of improving societal well-being through the financial inclusion of trusted microenterprises that can obtain loans at reasonable rates and on a consistent basis. This study offers MFIs and policymakers helpful guidance on how to boost business respect, reciprocity, strategic intent, and consequently, LR, which is essential for MFI sustainability, poverty reduction, and socio-economic development in general.

Introduction

To alleviate poverty and promote entrepreneurship, microfinance institutions (MFIs) provide loans to self-employed individuals in low-income communities (microenterprises) who are often excluded by traditional financial institutions (Kasoga & Tegambwage, 2022). However, MFIs worldwide, particularly in developing countries like Tanzania, face significant challenges such as high loan default rates, institutional sustainability, and balancing financial performance with social impact (I. Ali et al., 2022; Kasoga & Tegambwage, 2021; Pellegrina et al., 2021; Tegambwage & Kasoga, 2025). Tanzanian microenterprises that obtain loans from MFIs often exhibit unfavorable behaviors such as multiple borrowings, excessive debt, dishonesty, and opportunism, which contribute to high loan default rates (Tegambwage & Kasoga, 2022b). Previous studies have identified various factors influencing loan repayment (LR) rates among microentreprises, particularly in developing countries like Tanzania. These factors can be categorized into supply and demand sides. The side of demand includes key factors like social cohesion, gender, marital status, age, education level, monthly income, household size, and business experience. Other challenges such as low enterprise returns, lack of profitable innovation, financial illiteracy, unfamiliarity with modern commercial practices, weak moral incentives, loan diversion, and the perceived cost of default also play a significant role (Kassegn & Endris, 2022; Makorere, 2014; Muhammad et al., 2019).

On the supply side, loan characteristics such as interest rates, loan size, and loan tenure are crucial determinants of repayment performance (Churchill & Halpern, 2001; Endris, 2022; Kiros, 2023; Makorere, 2014; Muhammad et al., 2019). Despite efforts to address the factors contributing to LR issues in Tanzania, LR remains a significant challenge for MFIs, impacting their sustainability, outreach, and, ultimately, their ability to alleviate poverty (Tegambwage & Kasoga, 2022a). As a result, both academics and policymakers are advocating for further research to improve LR rates (Ullah et al., 2019).

In developing economies like Tanzania, LR behavior in microfinance is largely driven by survival needs, social pressure, and informal enforcement mechanisms (Dubale & Beshir, 2020). Borrowers often rely on loans to meet basic necessities or sustain small informal businesses, making repayment highly sensitive to income shocks (Kasoga & Tegambwage, 2021). Group lending models and strong community ties play a key role, as peer pressure and the desire to maintain social reputation encourage timely repayment (Tegambwage, 2023). Limited access to formal legal or financial systems means trust, social cohesion, and local norms are central to repayment dynamics (Afolabi, 2013). In developed economies, on the other hand, LR behavior in microfinance is primarily influenced by borrowers’ goals of credit rehabilitation, personal advancement, and integration into the formal financial system (Carr & Tong, 2002). Factors such as access to credit scoring systems, legal consequences of default, availability of digital payment tools, and financial education play significant roles (Servon, 2006). Unlike in developing economies, social pressure is less central, and repayment is often driven by the desire to build credit history, improve future financial opportunities, and achieve economic mobility.

Since LR behavior in developing economies like Tanzania is mostly dependent on informal enforcement mechanisms, as mentioned earlier, business relational elements like reciprocity and respect can be very important in helping microentrepreneurs improve their LR because they strengthen the social bonds that underpin informal enforcement mechanisms (Tegambwage & Kasoga, 2025). Business respect and reciprocity are key relational factors that MFIs leverage to encourage microenterprise growth and add value addition (Hani et al., 2022). Business respect acknowledges the value and inherent worth of business partners (Bourassa et al., 2018), while business reciprocity encompasses norms that foster community support and information sharing (Hani et al., 2022). According to these scholars, MFIs that demonstrate respect and reciprocity foster stronger growth and financial rewards for microenterprises. This, in turn, can enhance LR. This argument aligns with Blau’s (1964) social exchange theory (SET), which suggests that when microenterprises experience significant business growth and financial benefits from an MFI that respects and reciprocates their efforts, they feel a reciprocal obligation to reward the MFI by repaying loans promptly, knowing that their behavior affects future access to credit and support.

Few researchers that investigated the associations between relationship quality and LR have reported mixed results. For example, Tegambwage and Kasoga (2022a) and Towo et al. (2022) found non-significant relationships, while Cornée et al. (2012), Mori and Ng’urah (2020), and Mori et al. (2024) found significant relationships. However, most of these studies focused on business-to-customer (B2C) relationships rather than business-to-business (B2B) relationships. Other empirical studies such as Hani et al. (2022) and Tegambwage and Kasoga (2025) linked business respect and reciprocity with value addition and customer loyalty, respectively. They did not establish a link between business relational factors and LR. To our knowledge, no prior research has empirically investigated the influence of relational factors, such as business respect and reciprocity on LR in the B2B context. Hence, the current study extends the aforementioned prior research by investigating the links between business respect, reciprocity, and LR in microfinance. Other relational factors such as trust, commitment, and satisfaction were excluded from this study because they are more relevant to individual (B2C) relationships, where such factors hold greater importance and sensitivity, unlike organizational (B2B) interactions (Tegambwage & Kasoga, 2025).

In addition, this study examines the moderating role of strategic intent, the microenterprise’s long-term vision and growth commitment (Johnson & Sohi, 2001), on the relationship between business respect, reciprocity, and loan repayment (LR). Based on social exchange theory (Blau, 1964), high strategic intent may strengthen the impact of strong MFI-microenterprise relationships on LR, as growth-oriented microenterprises view MFIs as strategic partners and repay loans loyally. Conversely, low strategic intent may weaken this effect, as short-term focused microenterprises may default despite good relationships. Other potential moderators like reputation, financial stability, and leadership were excluded, as they are closely tied to strategic intent (Johnson & Sohi, 2001). Johnson and Sohi (2001) examined the influence of strategic intent on reciprocity, contending that strategic intent is a prerequisite for reciprocity in social exchange interactions between organizations. Voss et al. (2019) integrated reciprocity and strategic intent in an inter-firm relational model. However, no empirical study has investigated the moderation effect of strategic intent on LR. Thus, including strategic intent to moderate the link between business respect, reciprocity, and LR provides a new theoretical explanation for the LR.

This research, therefore, investigates the moderation effect of strategic intent in the relationship between business respect, reciprocity, and loan repayment (LR) in microfinance. From a theoretical perspective, this study explicitly uses SET to relate business respect, reciprocity, strategic intent, and LR, improving our understanding of the theory in the context of microfinance as well as its scope of applicability in the B2B context. From a practical perspective, this study provides MFIs and policymakers with useful advice on effective strategies to build strong B2B relationships with microenterprises and enhance their strategic intent in order to boost LR in developing economies like Tanzania, which is crucial for MFI survival and, as a result, the achievement of the objectives of financial inclusion, poverty reduction, and socioeconomic development in general. Understanding these dynamics in Tanzania could offer lessons for adapting microfinance strategies to diverse cultural contexts, thereby improving microfinance practices, particularly in developing economies.

Literature and Hypotheses Development

Theoretical Framework

SET (Blau, 1964) postulates that, when people engage in an exchange, they gain social and financial benefits. According to SET, two parties, a seller and a buyer, can interact socially to exchange love, esteem, affection and acceptance, as well as products and services (Yoganathan, 2015). Social interaction, as opposed to strict economic exchange, frequently inspires sentiments of appreciation, obligation, and trust (Blau, 1964). As MFIs rely heavily on their customer relationships as collateral for loan approval (Hani et al., 2022), SET is highly pertinent to the context of our research.

The key principles of SET include reciprocity, equity, and maximization of rewards and minimization of costs, among others (Blau, 1968). These principles guide how individuals form and maintain relationships, make decisions, and assess their social environments based on rewards, costs, and expectations. It is founded on the idea that people stay together because they expect to enjoy social trade, which comprises a number of exchanges that result in commitment through reciprocal duties (Blau, 1964). As such, any benefits obtained result in debts that can only be paid off through reciprocation. As long as parties get enough social and financial incentives, they will remain partners. Accordingly, reciprocity can develop and boost LR. After receiving adequate reciprocal actions and respect from the MFI, microentrepreneurs will derive higher business value that leads to strong business growth and financial rewards (Hani et al., 2022) and therefore feel obliged to repay their loans promptly through reciprocal obligations. According to Cornée and Szafarz (2014), reciprocity can generate better repayment performance. SET emphasizes the connection between relational factors (business respect and reciprocity) and LR.

Additionally, drawing on SET, strategic intent can shape the extent to which relationship quality (characterized by respect and reciprocity) affects LR. When strategic intent is high, microenterprises focus on long-term growth and see the MFI as a key growth partner, which may enhance the positive impact of relationship quality on LR. Conversely, with low strategic intent, microenterprises tend to focus on short-term survival and neglect future funding prospects, increasing the risk of default, which may weaken the link between relationship quality and LR.

SET, institutional theory, and the resource-based view (RBV) are distinct theoretical frameworks used to understand organizational behavior, relationships, and strategies. While SET is more focused on the interactions between parties in exchange relationships (Blau, 1964), Institutional theory examines pressures from the external environment that shape organizational behavior (Hodgson, 2001; Peters, 1999), and RBV emphasizes the firm’s assets and capabilities as a foundation for competitive advantage (Barney, 1991). Each theory offers valuable insights into different aspects of organizational behavior, and depending on the context, they can complement each other in understanding how organizations develop strategies and manage relationships. However, SET is particularly effective in explaining how strategic intent moderates the relationship between relationship quality and LR, which is the primary focus of this study.

Business Respect and LR

According to S. H. S. Ali (2011), respect is a relationship in which one side responds appropriately to the other from a certain standpoint. Creating lasting positive interactions with clients is crucial (S. H. S. Ali et al., 2012). Hani et al. (2021) claim that relationships are strengthened when two people exchange respect, which is composed of recognition, responsibility, and empathy. Accordingly, this research defines respect in the context of microfinance as the acknowledgment, accountability, and empathy shown by the MFI to microenterprise (Hani et al., 2022). This implies that an MFI that respects its clients acknowledges their aspirations and ambitions, accepts responsibility for pursuing those goals, and shows empathy for them. Respect is a key factor affecting the business relationships between MFIs and microentrepreneurs (Hani et al., 2022; Tegambwage & Kasoga, 2025). Thus, an MFI that respects microentrepreneurs by supporting them in achieving their goals and making decisions considering their feelings and thoughts will positively influence their decision making and set expectations of reciprocation (Pai, 2015), which may boost LR. Drawing on SET, microentrepreneurs who are respected by the MFI in such a way that their aspirations and ambitions are acknowledged by the MFI, their pursuit of their goals is supported by loans granted by the MFI, and who are treated with empathy by the MFI feel obligated to reciprocate by repaying their loans promptly. Previous studies (Cornée et al., 2012) show that robust relationships with customers help financial institutions mitigate moral hazards and LR problems. However, this previous study did not study relationship quality at a dimensional level. Given the above debate, the following proposition is stated:

H1: Business respect has a positive and significant effect on LR

Business Reciprocity and LR

Reciprocity strengthens ties between exchange partners and builds a high-quality relationship (Hoppner et al., 2015). Through holding weekly community meetings in a physical location, an MFI builds reciprocity norms among borrowers in order to build social capital and forge relationships (Hani et al., 2022; Tegambwage & Kasoga, 2025). In the weekly meeting, an MFI keeps track of the reciprocity expectations among the participants, which builds long-lasting trust with its clients. Perceived community support, enjoyment, and informativeness make three characteristics that have an impact on reciprocity norms (Hani et al., 2021). In the context of this study, an MFI with positive reciprocal actions, such as high-perceived microenterprises support, enjoyment, and informativeness, creates psychological ties that encourage microentrepreneurs to maintain relationships, influence their decision-making, and set expectations of reciprocation. These psychological ties may increase LR performance. In accordance with SET, microentrepreneurs who receive encouragement and inspiration from MFI to continue and develop their businesses to break the cycle of poverty and create value in their microbusinesses will feel obligated to repay their loans more effectively as a way of returning the favor.

According to empirical studies, enduring MFI-client relationships minimize danger of loan default, resulting in higher payback performance. More specifically, Cornée and Szafarz (2014) reported that reciprocity can generate better repayment performance. However, they identified reciprocity based on economic benefits rather than social or relational benefits. According to Voss et al. (2019), B2B models have neglected reciprocity. MFIs and policymakers should also enhance reciprocity norms by being sensitive to the needs of impoverished microentrepreneurs by offering advantageous loan terms such as fair interest rates, loan sizes, and flexible repayment schedules that consider their sales cycles. According to Cornée and Szafarz (2014), inspired borrowers drastically reduce their default risk in response to favorable borrowing terms. In addition, reciprocity should be enhanced by empowering microenterprises with valuable business information. According to Voss et al. (2019), quality information exchange (based on reciprocity) is essential for enduring B2B connections, which are crucial for better LR. In light of the discussion above, the resulting proposition is put forth:

H2: Business reciprocity has a positive and significant effect on LR

Moderating Role of Strategic Intent on LR

Strategic intent is a management approach that highlights the spirit of achievement by inspiring people and their enterprises to meet predetermined goals (Hamel & Prahalad, 2005). It is consistent, and it gradually allocates resources to get the competitive advantage it seeks (Johnson & Sohi, 2001). This study defines strategic intent as a microenterprise’s clarity of purpose, growth goals, and commitment to long-term business development. Microenterprises with high strategic intent are more likely to value respectful and reciprocal relationships with MFIs, viewing them as strategic partners. Based on SET (Blau, 1964), such relationships can significantly enhance LR, as they align with the enterprise’s long-term goals, strengthening the positive impact of relationship quality on LR.

In contrast, microenterprises with low strategic intent are typically short-term or subsistence-focused, prioritizing immediate needs over long-term growth. Their decisions are driven by factors like ease of access or low interest rates rather than relationship quality. According to SET (Blau, 1964), even if they experience respect and reciprocity from MFIs, it may not significantly improve LR due to their limited or opportunistic outlook, leading to a weaker or negligible impact of relationship quality on LR. Mahdzan et al. (2017) found a significant impact of competitive advantage (an outcome of strategic intent) on consumer behavior. Based on this discussion, strategic intent is expected to influence LR behavior by moderating the relationship between business respect, reciprocity, and LR. Accordingly, the following hypotheses are tested:

H3: The association between business respect and LR is moderated by strategic intent

H4: The association between business reciprocity and LR is moderated by strategic intent

Figure 1 illustrates the research’s conceptual model.

Proposed conceptual model.

Methodology

Study Design, Population, and Sample

The study used a cross-sectional approach to determine the association between the variables. However, this approach can limit the ability to make inferences about causality or long-term trends (Hair et al., 2019). While this design cannot prove causality, it can suggest patterns of associations that can be tested in future research. Hence, building on the current study, future research using longitudinal design may help mitigate this limitation. The research was conducted among microenterprises that receive loans from MFIs in the regions of Mwanza, Arusha, and Dar es Salaam. Tanzania’s microbusinesses are concentrated in these regions (Kasoga & Tegambwage, 2021). Specifically, the unit of inquiry was the individual microenterprise owners (microentrepreneurs) who met the inclusion criteria of having been MFI clients for at least 3 years, and therefore responsible for repayment decisions. Previous studies on relationship quality in the microfinance field have used participants with at least 3 years’ experience (Hani et al., 2021). According to Berger and Udell (2002), the significance of enduring relationships is especially severe in MFI-microbusiness relationships, which lack collateral. Due to a lack of collateral, MFIs rely on credit relationships with customers to mitigate issues of moral-hazard and adverse-selection (Brand & Gerschick, 2000). Microenterprises, on the other hand, need to create enduring relationship with MFIs (by borrowing and repaying their loans promptly) in order to receive progressively larger loans in the future (which are needed to finance their business in order to achieve their strategic objectives). Successful MFIs establish long-term relationships with clients as a way of providing sustainable or profitable financial services to poor microentrepreneurs (Brand & Gerschick, 2000). According to this scholar, MFIs typically break even on a client only after the fourth or fifth loan.

Using a convenience sampling technique, 900 questionnaires (300 for each of the three cities) were personally administered by the researchers to microenterprise owners. This sampling technique yields several inherent benefits, including being cost-effective and less time-consuming (Hair et al., 2019). However, since convenience sampling may introduce selection bias, affecting the extent to which the results can be generalized to other settings (Hair et al., 2019). Thus, this study employed a large sample size and regression analysis to control for confounding variables such as age, gender, education, and business type to suggest relationships that can be tested in future research using random sampling methods. A total of 603 questionnaires were filled out and returned, which is a 67% response rate. Prior empirical research on the microfinance industry has used sample sizes of 500 or more. For example, in a Tanzanian research on excessive debt among MFI clients, Kasoga and Tegambwage (2021) employed a sample size of 535 borrowers. Schicks (2013) employed a sample size of 531 micro-borrowers when assessing the signs of excessive debt among MFI clients in Ghana. While assessing repayment incentives and excessive debt among MFI clients in Bolivia, Gonzalez (2008) employed a sample size of 959.

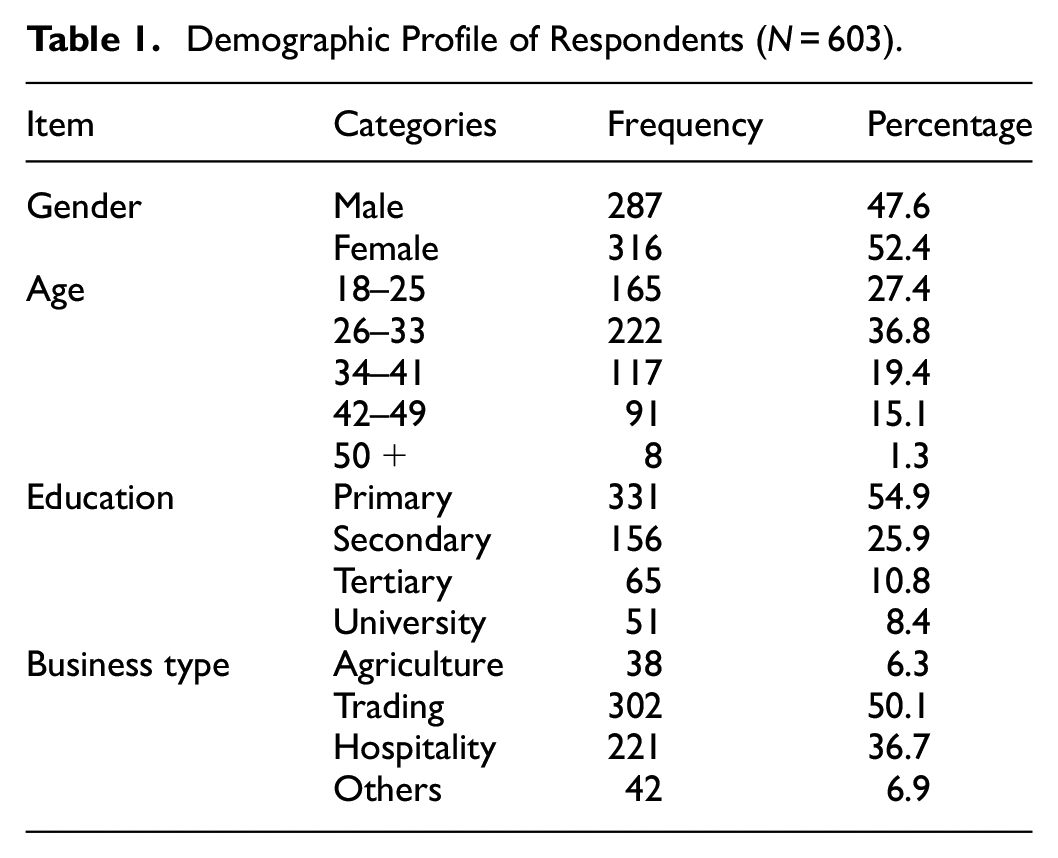

As indicated in Table 1, there were 287 males (47.6%) and 316 females (52.4%), showing a balanced dataset distribution by gender. The bulk of responses (36.8%) were made by microentrepreneurs with an age range of 26 to 33 years who had attained a basic primary education (54.9%) and were self-employed in retail trading (50.1%).

Demographic Profile of Respondents (N = 603).

Data Collection and Analysis

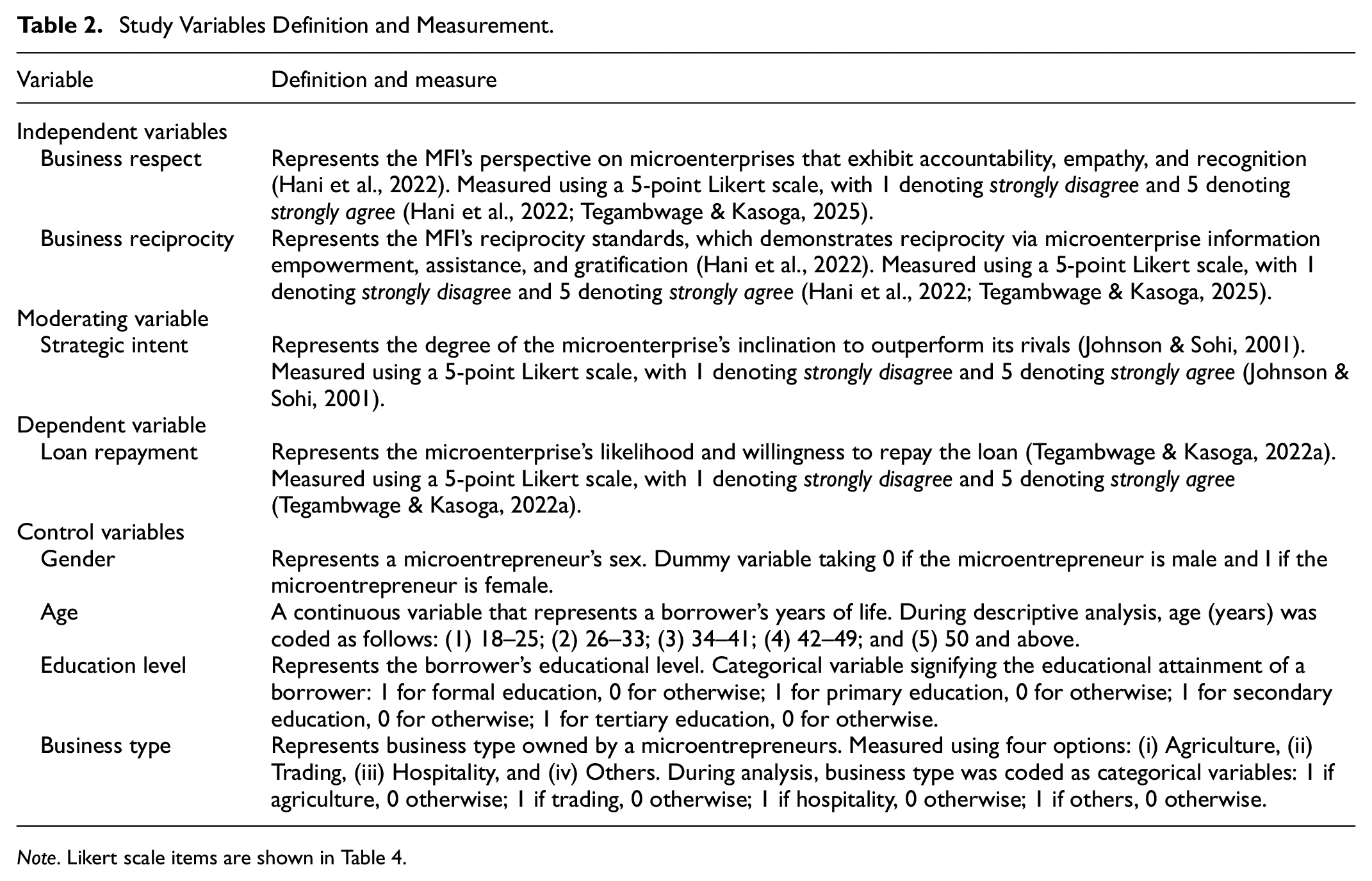

With the aid of qualified research assistants, a standardized questionnaire was used by the researchers to gather data from each participant individually. Cronbach’s α coefficient was used to verify the data collecting instrument’s reliability, making sure that all research variables possessed α coefficient above the .70 level (Hair et al., 2019). Four sections made up the questionnaire, looking at the respondent’s demographic attributes (control variables), LR (a dependent variable), business respect and reciprocity (independent variables), and strategic intent (moderating variable) respectively. Study variables’ definition and measurement are presented in Table 2. The questionnaires were taken from previous research and adapted to the study’s viewpoint. LR items were adapted from Tegambwage and Kasoga (2022a), while business respect and reciprocity items were adapted from Hani et al. (2022). Each response was given a grade on a Likert scale of 1 to 5, with grade 1 denoting severe disagreement and grade 5 denoting strong agreement.

Study Variables Definition and Measurement.

Note. Likert scale items are shown in Table 4.

In a pre-test phase, a panel of five experts (two academics and three marketing experts) validated the questionnaires to enhance the scale items’ face validity and clarity. Three business respect items: BRES7 (Members of the MFI community respond to my suggestions right away), BRES8 (My fellow MFI community members respond right away when I ask inquiries or express concerns), and BRES9 (When I have a difficulty, I can get assistance from the MFI) were removed because they address B2C rather than B2B relationships. Likewise, two business reciprocity items: BREC4 (The knowledge offered by the MFI in the community meeting is beneficial to me) and BREC5 (The knowledge offered by the MFI community is useful to me) were also removed because they address B2C rather than B2B relationships. Two strategic intent items: SI3 (My firm seeks competitive dominance) and SI4 (My firm systematically builds competitive advantage) were removed because they were relatively similar to another item: SI1 (My enterprise reorganizes its resources to get a competitive). Moreover, one loan repayment item: LR3 (“The probability I would repay my loan is high”) was removed because it was relatively similar to another item: LR2 (I am quite willing to pay back my loan). Table 3 presents the summary of the study variables and their corresponding number of items.

Summary of Study Variables and Items After Expert Validation.

Following expert validation, a pilot test involving 30 microentrepreneurs was conducted to evaluate the conceptual model’s dimensionality and nomological chain and the research metrics’ internal consistency (Podsakoff et al., 2003). It is worth noting the difference between the current study and Hani et al.’s (2021) and (2022) studies in that, although these previous studies identified the dimensions of business relationships between microenterprises and MFIs (such as respect and reciprocity), they did not investigate their impact on LR.

The questionnaire was available in Swahili and English for respondents. The researchers carefully laid out the objectives of the study for the respondents before requesting their permission to participate. The confidentiality of the respondents’ identities was guaranteed. Additionally, participants could stop taking the survey whenever they wanted.

Combinations of procedural and statistical approaches were used to alleviate the common method bias (CMB). To reduce common methodological bias in the gathering of data and to ensure uniformity in analysis of data, the questionnaire items were procedurally reverse-coded (Podsakoff et al., 2003). CMB’s absence was statistically confirmed using Harman’s single-factor test (Podsakoff et al., 2003). A four-factor explanation of 75.13% of the variance was found following factor analysis of the four focus components; with 27.13% of the variation being explained by factor one. CMB is unlikely to exist because no distinct component appeared, and factor one could not account for the bulk of the variance (Lindell & Whitney, 2001).

The direct relationships between dependent and independent variables were analyzed using the multiple regression approach using the statistical package for social sciences (SPSS), version 20 software. The moderator’s and predictors’ interaction was used to assess the moderating effects and determine if the interaction term’s regression coefficient was significant (Baron & Kenny, 1986). Classical regression assumptions, such as normality, multicollinearity, and autocorrelation, were examined to guarantee objective coefficient estimates, accurate standard errors, and legitimate hypothesis testing (Field, 2009).

Results

Descriptive Statistics

Table 3 displays means and standard deviations (SD). The average ratings for both business respect and reciprocity are 2.26 and 2.44, respectively, indicating that microbusiness owners in Tanzania believe their relationships with MFIs to be of inferior quality. Likewise, the strategic intent received a mean score of 2.41, suggesting low strategic determination among Tanzanian microenterprises. Similarly, the LR construct had a 2.56 mean score, suggesting that Tanzanian MFI clients have a low willingness to repay their loan. This is likely due to low perceived relationship quality and low switching barriers between MFIs (Kasoga & Tegambwage, 2021; Mbuya & Tegambwage, 2022). The low levels of perceived relationship quality in the study setting suggest that MFIs in Tanzania have not adequately embraced relationship quality from a B2B standpoint. This could be one of the causes of LR problems among microenterprises because the success of the microfinance model relies on relational elements due to a lack of collateral.

The descriptive statistics support Hani et al.’s (2022) claim that emerging markets like Africa have not sufficiently embraced relationship quality from a B2B perspective. The results for kurtosis and skewness fell within acceptable bounds (Table 4), hence there is no reason to be concerned about a non-normal distribution in the data set (Hair et al., 2019).

Descriptive Statistics.

Reliability and Validity of the Measures

As summarized in Table 5, the measures met all requirements for evaluation, demonstrating strong convergent validity and reliability. As recommended by Hair et al. (2019), the Bartlett’s test and the Kaiser-Meyer-Olkin (KMO) test were conducted to assess the data’s suitability for factor analysis. The KMO value exceeding 0.5 and a significant Bartlett’s test (p < .001) in Table 5 confirmed the data’s suitability for factor analysis (Hair et al., 2019). Each independent variable exceeds the 0.50 cutoff for factor loading and .70 for reliability tests: Composite reliability (CR) and Cronbach’s alpha (α; Hair et al., 2019), suggesting that the indicators as a whole fairly evaluate each concept. The average variance extracted (AVE) and CR were used to evaluate convergent validity (Henseller et al., 2015). All AVE and CR in Table 5 surpass 0.50 and .70 respectively, confirming the presence of convergent validity (Hair et al., 2019).

Measures’ Reliability and Validity.

Note. KMO = 0.528; Bartlett’s test of sphericity χ2(6) = 495.991***. BREC = business reciprocity; BRES = business respect; SI = strategic intent; LR = loan repayment.

p < .001.

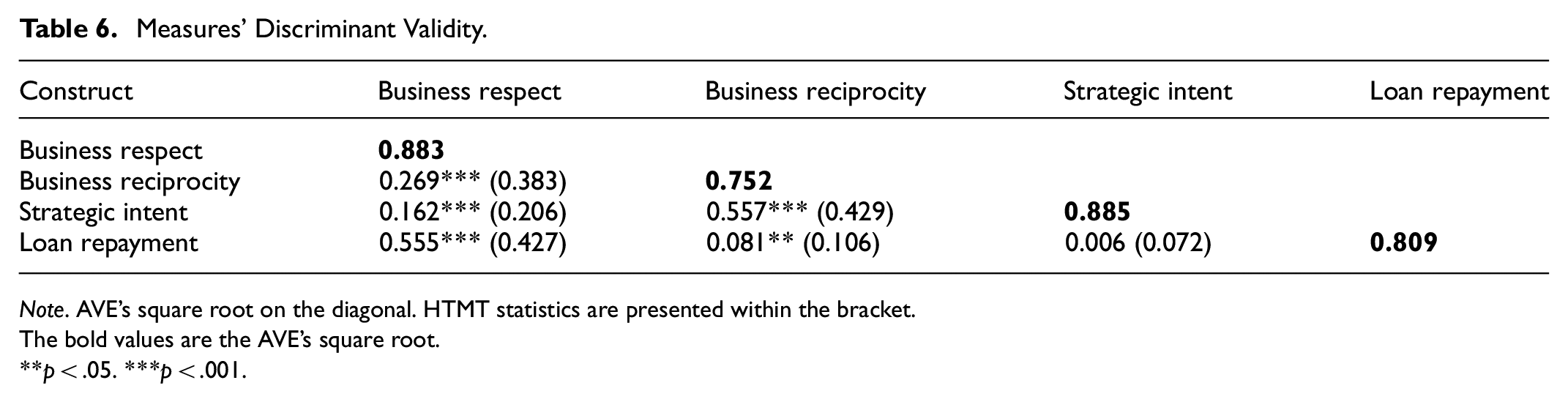

The Fornell and Larcker (1981) method was used to evaluate the measures’ discriminant validity. Table 6 demonstrates discriminant validity as the square root of AVE for each construct was higher than the equivalent correlation coefficients (Fornell & Larcker, 1981). The Heterotrait-Monotrait (HTMT) values are also shown in brackets in Table 6, falling within the 0.85 limit. The constructs’ discriminant validity is therefore considered to be high (Hair et al., 2019). Thus, each construct’s indicators have little correlation with the other constructs in the model.

Measures’ Discriminant Validity.

Note. AVE’s square root on the diagonal. HTMT statistics are presented within the bracket.

The bold values are the AVE’s square root.

p < .05. ***p < .001.

By using pre-existing measurements and ensuring anonymity of respondents, potential CMB was minimized (Podsakoff et al., 2003). Further proof that CMB did not seriously jeopardize the results is provided by Table 6, which reveals the absence of unusually strong associations (r > .80) across the variables (Podsakoff et al., 2003). The degree of multicollinearity between the explanatory variables was assessed using the variance inflation factor (VIF) for each of them. Compared to the standard cut-off threshold of 10, the VIF values vary from 1.862 to 4.388 as shown in Table 7, indicating that there is no substantial correlation between the components (Hair et al., 2019). Furthermore, Table 7’s Durbin-Watson values fell between 1.5 and 2.5, suggesting that there was no serial correlation between the research variables across time (Field, 2009).

Results of the Multiple Regression Analysis.

Note. R = .773; R2 = .597; Adjusted R2 = .590; Durbin-Watson = 1.622; F-value = 127.432***. Dependent variable: Loan repayment.

p < .05. ***p < .001.

Multiple Regression Analysis and Hypotheses Testing

Before conducting the multiple regression analysis, the normality, multicollinearity, and autocorrelation tests were among the traditional regression assumptions that were examined and found satisfactory (Tables 4 and 7), as discussed earlier. Hence, the regression analysis was appropriate for hypothesis testing. The findings in Table 7 show that business respect (β = .064, p < .05) and reciprocity (β = .100, p < .001) positively and significantly influence LR, supporting H1 and H2. With regards to the moderating effects of strategic intent, the interaction terms: Business respect*Strategic intent and Business reciprocity*Strategic intent positively and significantly influence LR (β = .492, p < .001 and β = .486, p < .001, respectively), supporting H3 and H4. These findings imply that strategic intent moderates the connection between business respect, reciprocity, and LR. In addition, coefficients of determination (R2) show the proportion of the predictor variable’s variance that can be attributed to an endogenous component. The cutoff value for R2 should, according to Falk and Miller (1992), be greater than 10%. Thus, LR can be satisfactorily explained by our suggested model, which provides an explanation for 59.0% of the variance in LR (adjusted R2 = .590). This means that the remaining portion of the variance in LR (41.0%) is explained by other variables, including loan factors such as interest rates (Churchill & Halpern, 2001; Makorere, 2014), loan size (Muhammad et al., 2019), and loan tenure (Endris, 2022; Kiros, 2023; Muhammad et al., 2019).

Robustness Checks

Robustness tests were carried out to certify the results. With the microentrepreneur’s sociodemographic characteristics (gender, age, education level, and business type) acting as control factors, a multiple regression approach was used to ascertain the capability of business reciprocity, respect, and strategic intent to predict LR. The findings (Table 7) indicate that females had a substantial impact on LR (β = .455, p < .001), whereas males had no significant impact (β = .480, p > .05). Tegambwage and Kasoga (2022a), who found that female considerably and favorably affects LR, corroborate this finding. Likewise, Table 7 indicates that business type: agriculture (β = .345, p < .001), trading (β = .350, p < .001), and hospitality (β = .111, p < .05) significantly influence LR. However, other business types (β = .038, p > .05) do not significantly influence LR. Thus, to enhance LR in Tanzania, MFIs should grant loans to microenterprises engaging in agriculture, trading, and hospitality businesses. Although insignificant, the positive relationships between LR and age (β = .095, p > .05) and education: primary (β = .432, p > .05), secondary (β = .111, p > .05), tertiary (β = .121, p > .05), and university (β = .055, p > .05), imply a direct connection between them. The findings corroborate previous research (Endris, 2022; Kassegn & Endris, 2022), which documented positive relationships between age, education level, and LR. The conclusion that business respect, reciprocity, and strategic intent influence LR is thus proven to be resilient in the presence of socio-demographic factors.

Discussion

The goal of this research was to investigate the moderating power of strategic intent between business respect, reciprocity, and LR. The results showed that LR is influenced by business respect, demonstrating that respectful interaction between an MFI and microentrepreneurs helps to create lasting bonds and boosts LR. The results are supported by SET (Blau, 1964) in that microentrepreneurs who are respected by the MFI have an obligation to reciprocate by repaying their loans promptly. The results are also in line with Cornée et al. (2012), who show that enduring ties between lenders and borrowers lessen the repayment problem. According to Berger and Udell (2002), the importance of enduring relationships is especially severe in small businesses, which are frequently characterized by opacity of informational and collateral-related challenges. Hani et al. (2022) point out that business respect enhances perceived relationship quality and is the key to a microentrepreneur’s success. Thus, an MFI with adequate respect for the microentrepreneur will foster robust relationships with them and, in turn, enhance LR.

The findings also showed that business reciprocity has a positive and significant influence on LR. The findings align with SET and earlier research, such as Cornée and Szafarz (2014), who found that reciprocity, can generate better repayment performance. The findings are not consistent with that of Tegambwage and Kasoga (2022a) which discovered that commitment, trust, and satisfaction do not significantly influence LR in the B2C context in Tanzania. This suggests that the influence of relational factors on LR tends to be significant in a B2B context than a B2C context. Thus, managers of MFIs in Tanzania should focus on building and practicing effective relationship marketing strategies (through enhancing business respect and reciprocity) to build robust relationships with microenterprises in order to enhance LR. In addition, the study found that business reciprocity has a stronger effect on LR than business respect. This could be due to the fact that reciprocity creates a mutual obligation and a sense of moral duty to repay, while respect mainly fosters positive feelings and trust without necessarily generating the same level of commitment or desire to return the favor. The emotional bond, the expectation of mutual benefits, and the psychological need to reciprocate are all strong drivers for LR when reciprocity is at play. Thus, reciprocity fosters a stronger obligation to repay loans than mere respect.

With regards to the moderation power of strategic intent between respect, reciprocity, and LR, the findings indicate that strategic intent moderates the relationships between the aforementioned variables. Specifically, the findings show that strategic intent moderates the links between business respect, reciprocity, and LR. This implies that strategic intent strengthens the effects of B2B relational factors on LR. Although firms with high strategic intent are more disciplined in repayment (as evidenced by a significant positive effect of strategic intent on LR), the interaction effects of strategic intent and business respect, and reciprocity suggest that when firms have high strategic intent and feel respected and valued, they create stronger relationships with MFI, increasing the likelihood of repaying their loans to reciprocate the goodwill. These findings are in line with SET, in that constructive actions by one company will lead to constructive actions by the other company through reciprocity norms. According to SET, relational norms force the partner to do reciprocal behavior. Hence, microenterprises with favorable relationship quality with MFI (through business respect and reciprocity) coupled with strong strategic intent repay their loans promptly to ensure steady flow of capital (by acquiring subsequent larger loans from the MFI) to achieve their desired strategic objectives. Thus, MFIs and policymakers in developing countries like Tanzania should focus on enhancing strategic intent among microenterprises (e.g., through relevant business skills training programs) in order to enhance LR, which, as mentioned earlier, is essential for poverty alleviation and sustainability of MFIs (Tegambwage, 2023).

It is worth noting that the study findings are likely influenced by a combination of cultural, regulatory, and economic factors. Cultural values may influence relational factors like respect and reciprocity that encourage microenterprises to prioritize relationships and repayment (Hani et al., 2022). Repayment can also be affected by economic difficulties or weak regulatory enforcement (Kasoga & Tegambwage, 2021). While the regulatory framework may offer some guidance, its shortcomings in the microfinance sector, especially in developing countries like Tanzania, often lead to a greater dependence on the quality of MFI-microenterprise relationships (Hani et al., 2021). Therefore, understanding how these factors interact is essential for strengthening MFI-microenterprise relationships and improving loan repayment behavior among microenterprises in developing economies like Tanzania, where microfinance often relies on group lending models and strong community networks (Tegambwage, 2023).

Since this study was conducted in Tanzania, it opens an opportunity for cross-cultural validation in different countries to foster generalizability. While Tanzania shares many commonalities with other developing countries in the way microfinance operates, such as the importance of relational elements due to a lack of collateral (Hani et al., 2021), there are also significant contextual differences. The unique social, economic, legal, and infrastructural challenges faced by microenterprises in Tanzania shape the dynamics of LR in ways that may differ from other countries such as Bangladesh, India, and Kenya where microfinance is widely used. Thus, MFIs need to implement more tailored strategies to improve repayment rates.

Conclusion

The goal of this research was to investigate the moderating power of strategic intent between business respect, reciprocity, and LR. According to the findings, LR is influenced by business respect and reciprocity, with reciprocity exerting a stronger effect. However, there were low levels of perceived relationship quality in the study setting, suggesting that MFIs in Tanzania have not adequately embraced relationship quality from a B2B standpoint. This contributes LR challenges among microenterprises, as the success of the microfinance model in developing countries like Tanzania depends heavily on relationship-based factors, given the absence of tangible collateral (Hani et al., 2021). As a result, the sustainability of MFIs could suffer, leading to failure to alleviate poverty. Therefore, business relational factors of respect and reciprocity play a crucial role in enhancing LR by microentrepreneurs. With regards to the moderating effects of strategic intent, the findings indicate significant moderating effects of strategic intent between business respect, reciprocity, and LR. This suggests that strategic intent strengthens the effects of business respect and reciprocity on LR.

This research’s conclusions have important theoretical and practical inferences. Drawing on SET, this study extends microfinance research by proposing a LR framework, linking LR with business respect, reciprocity, and strategic intent. This improves our understanding of the theory in the context of microfinance as well as its scope of applicability in the B2B context. Previous research (Hani et al., 2021, 2022; Tegambwage & Kasoga, 2025) have proposed reciprocity and respect as essential components of MFI-microenterprise relationship quality but did not establish their roles in enhancing LR. This is, to our knowledge, the first study to empirically show the link between business respect, reciprocity, strategic intent, and LR, extending prior research (Hani et al., 2021, 2022; Tegambwage & Kasoga, 2025).

From a practical perspective, the findings of this study imply that fostering positive MFI-microenterprise relationships characterized by respect and reciprocity, alongside enhancing the strategic intent of microenterprises, is essential for improving LR in developing countries like Tanzania. This, in turn, supports the sustainability of MFIs, contributes to poverty alleviation, and promotes overall socio-economic development (Tegambwage, 2023). MFIs should treat microenterprises as valued partners by respecting their goals and perspectives, while also promoting reciprocity through supportive loan terms, such as fair interest rates, adequate loan amounts, and flexible repayment aligned with business cycles. Favorable terms can significantly reduce default risk (Cornée & Szafarz, 2014). Additionally, enhancing microenterprises’ strategic intent through business training and sharing valuable information can strengthen reciprocity norms and foster long-term relationships, which are key to improving LR in developing economies like Tanzania (Voss et al., 2019).

With regard to social implications, the study can inform microfinance regulations in developing countries like Tanzania by encouraging the use of reciprocity norms when setting interest rates. This could enhance financial inclusion for trustworthy microentrepreneurs, improving access to fair and consistent loans. Implementing relationship marketing strategies that foster respect, reciprocity, and strategic intent can help MFIs achieve both social and financial goals, especially in developing economies like Tanzania.

This study has some limitations, just like any other research project. First, the study was carried out in Tanzania, a particular developing country. Hence, it creates a chance for the study to be repeated in other countries to foster generalizability. Second, this study covered the microfinance sector. Since the socioeconomic structure between MFI and typical bank clients differs (Hani et al., 2021), the similar study may be repeated in future banking sector research. Third, the study employed convenience sampling which may introduce selection bias, affecting the extent to which the results can be generalized to other settings (Hair et al., 2019). Future research using random sampling methods may help mitigate this limitation. Fourth, this research employed a cross-sectional design. Additional information on the link between relational elements and LR can be provided via longitudinal study in the future. Finally, the findings of this study indicate low levels of “lender-borrower” relationship quality, suggesting inadequate embracement of relationship aspects in the study settings. Future research should explore how cultural, regulatory, and economic factors affect MFIs’ ability to implement effective relationship marketing strategies in developing countries. Understanding these dynamics is key to strengthening MFI-microenterprise relationships and improving LR behaviors.

Footnotes

Acknowledgements

The authors sincerely thank the Editor of this Journal for initiating the desk review and coordinating a rigorous blind peer review process. The authors also extend gratitude to the anonymous reviewers for their valuable and constructive feedback, which contributed to the revision, enhancement, and refinement of the paper. Additionally, the authors appreciate the support of colleagues and assistant researchers who played a crucial role in completing this work.

Ethical Considerations

During data collection, participants were informed about the purpose of the study. Participation in this study was voluntary and confidentiality of respondents was observed. The committee approval number (for animal and human studies) is not applicable.

Authors Contributions

A.G.T. conceptualized the introduction, reviewed the literature, discussed the findings and wrote the conclusion. P.S.K. collected the data, analyzed the data, and proofread the paper. All authors read and approved the final manuscript.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Available upon request.