Abstract

As the Digital Currency Electronic Payment (DCEP) pilot is implemented, identifying the factors that influence individuals’ attitudes and adoption of DCEP is paramount for its wider promotion. Grounded on the Push-Pull-Mooring model and Status Quo Bias theory, this paper proposes a predictive model of individuals’ intention to adopt DCEP, which was tested through a questionnaire survey of 395 individuals adopting DCEP and validated by a structural equation modeling (SEM) and back-propagation neural network (BPNN) analysis. The findings reveal that individuals’ attitudes toward DCEP are pivotal in determining their adoption. Specifically, perceived compatibility, subjective norms, network externalities, social self-image, perceived government policy, and perceived credibility have significant positive effects on attitudes, while perceived cost exerts negative influences. Additionally, subjective norms and perceived government policy positively reinforce perceived credibility. Furthermore, individual financial knowledge moderates the relationship between attitude and adoption intention. This study offers both theoretical insights and practical guidance to facilitate the progress of DCEP pilots and enhance their adoption.

Keywords

Introduction

Central Bank Digital Currency (CBDC) has great potential to promote financial inclusion, enhance payment efficiency, and reduce transaction costs and financial crime. CBDC is recognized as a new form of digital currency that can meet the payment and remittance needs of individuals in daily lives (Oh & Zhang, 2022). The digital economy has demonstrated strong resilience and vitality during the COVID-19 pandemic and has accelerated the adoption of contactless payments. However, mobile payments present concerns regarding security and data usage (Zhong & Chen, 2023), which has led individuals to place greater trust in CBDC than before.

Developing countries are actively researching and promoting CBDC, and the Digital Currency Electronic Payment (DCEP) launched by the People’s Bank of China (PBC) in April 2020 is an important CBDC project expected to serve as a model for other central banks (Xia et al., 2023). By the end of June 2023, DCEP transactions totaled 1.8 trillion yuan, with 16.5 billion yuan in circulation, 950 million transactions, and 120 million digital wallets, indicating a promising outlook for DCEP (Ministry of Commerce of the People’s Republic of China, 2023).

Undeniably, Alipay and WeChat Pay dominate China’s mobile payment market, a position reflected not only in market share but also in individuals’ awareness and habitual usage (Gong et al., 2020). This dominance can be explained through Status Quo Bias (SQB) theory, which highlights individuals’ tendency to maintain the current state despite better alternatives, driven by rational decision-making, cognitive biases, and psychological commitment. Such behavioral inertia poses a significant challenge for DCEP, as it cannot fully replace entrenched payment methods. Furthermore, individual acceptance of DCEP will depend on their functional understanding and psychological perception of this new payment system, a key focus of this study. The widespread adoption of CBDCs in developing nations is further complicated by their large informal economies, which create additional barriers compared to developed countries (Oh & Zhang, 2022).

Existing studies predominantly utilize the Technology Acceptance Model (TAM) and Unified Theory of Acceptance and Use of Technology (UTAUT) to delve into how perceived usefulness influence individuals’ willingness to adopt DCEP (Liu et al., 2021; Ma et al., 2023). This focus, from an individual’s perspective, is understandable. However, the introduction of DCEP is pivotal not only for individuals but also for fostering social stability and reshaping the financial architecture in China, which is characterized by a significant informal economy. Consequently, the government has a pressing need for widespread DCEP adoption to bolster the financial system’s transparency and fairness. Scholars highlight that widespread CBDC adoption faces hurdles in countries, particularly developing nations, with large informal economies (Oh & Zhang, 2022). Achieving universal DCEP adoption necessitates research that considers individuals transitioning between diverse payment methods. Prior research has examined individuals’ adoption intentions using the PPM and task technology fit (Xia et al., 2023) . It has also explored data privacy, substitution rewards, and inertia—categorized as push, pull, and mooring factors—while analyzing the impact of perceived security, switching costs, traditional payment habits, and perceived risks on the decision to switch payment methods (Loh et al., 2020; Mu & Lee, 2021; Wang et al., 2019).

Nevertheless, research on individuals’ adoption of DCEP can be further enhanced, particularly in the following areas. First, existing studies offer limited insights regarding the influence of individuals’ characteristics on DCEP adoption, focusing only on usage habits, perceived costs, and perceived risks. Thus, there is an urgent need to broaden research into individuals’ characteristics. Numerous studies indicate that individual traits influence technology adoption (Beerbaum et al., 2025; Palash et al., 2022), with a particular emphasis on individuals’ innovation inclinations. Additionally, this study examines the impact of individuals’ financial knowledge on DCEP adoption. Second, there is a lack of a robust theoretical framework to analyze the barriers to DCEP adoption. SQB theory illustrates individuals’ tendency to stick with an existing system despite the availability of potentially superior alternatives (Patre & Khan, 2025; Samuelson & Zeckhauser, 1988). In China, while mobile payment is prevalent, individual inertia and loyalty to existing platforms impede DCEP adoption. Therefore, this paper addresses the following research questions:

RQ1. How to promote individual adoption of DCEP platform?

RQ2. What is the complex psychological process behind identifying individuals’ adoption behavior?

In conclusion, this study conducts empirical analysis to assess the impact of individual intentions toward adopting DCEP, utilizing PPM and SQB to address limitations in current research. This aims to enrich theoretical literature, influence managerial practices, and promote broader adoption of DCEP. Specifically, the novelty of this study lies in two primary areas: Firstly, it integrates PPM and SQB to examine broader adoption of DCEP in China-a strategy that has received positive feedback in pilot areas but necessitates a more comprehensive analysis of individual adopting influences for nationwide implementation. Secondly, the study underscores the moderating effect of individuals’ financial knowledge on DCEP adoption and examines this transition from the perspective of individual characteristics, providing a more nuanced understanding of the factors driving individual adoption.

The findings of this article offer valuable insights for both theoretical and practical applications. Firstly, this study delivers a comprehensive analysis of variable relationships using the two-stage SEM-BPNN method. BPNN addresses SEM’s limitations, offering fresh insights into the factors influencing individuals’ decisions to adopt the DCEP. Secondly, by integrating the PPM with the SQB perspective, this study advances a deeper comprehension of individual acceptance and the adoption to DCEP, surpassing insights provided by the TAM and other models. Third, the final study results can provide DCEP operators with some improvements to focus on optimizing the individual experience and promoting individual adoption of DCEP.

The study is structured as follows: it begins by elucidating the theoretical foundation through a review of relevant literature on PPM and SQB. Research questions were developed within the PPM and SQB. Subsequent sections detail the findings and analyses. The conclusion summarizes the study, underscores its implications, and proposes directions for future research.

Theoretical Background

SQB

The SQB theory, proposed by Samuelson and Zeckhauser (1988), elucidates why individuals often maintain the status quo despite better alternatives. This theory has extensively informed research on individual decision-making, particularly in understanding brand loyalty (J. S. Wu et al., 2021) and resistance to mobile payment technologies (Gong et al., 2020; Lee & Li, 2024; Loh et al., 2020). In examining the factors that prompt individuals to adopt DCEP, the theory offers insightful perspectives into behavioral patterns.

SQB theory, which influences preferences for the status quo or existing information, encompasses three dimensions: rational decision-making, cognitive misperception, and psychological commitment (Samuelson & Zeckhauser, 1988). In rational decision-making, individuals evaluate the benefits and risks of alternative systems, potentially leading to the rejection of new technologies perceived as risky or costly (Lee & Li, 2024). In the digital economy, the efficiency benefits of crypto-currencies are often outweighed by their technological complexity, fostering inertia and hindering wider adoption. Cognitive misunderstandings arise when technological perceptions are skewed by personal values and beliefs, resulting in skepticism and distrust in the sharing economy (J. S. Wu et al., 2021). Furthermore, psychological commitment, driven by personal commitments and the sunk costs of time and effort, strengthens resistance to new technologies (Gong et al., 2020; Lee & Li, 2024), reinforcing inertia.

In summary, this paper utilizes two dimensions of SQB-perceived complexity and perceived trust-to investigate specific contexts. Additionally, this study explores individual adoption behaviors of DCEP within the Chinese context.

Push-Pull-Mooring (PPM) Model

The PPM, proposed by Heberle (1938) for population migration studies, aims to describe the reasons for relocating (Heberle, 1938). According to the original model, the push effect refers to the motivating factors prompting departure, while the pull effect involves factors attracting individuals to new residences (Moon, 1995). However, previous models lacked sufficient attention to individual and social factors; thus, Moon (1995) introduced “mooring” to more comprehensively interpret migration (Handarkho & Harjoseputro, 2019). According to the PPM, migration or switching behavior stems from the interaction of push and pull effects, potentially influenced by mooring effects (Liao et al., 2021). The concept of “moorings” emphasizes personal and social influences and can be effectively integrated with SQB elements (Handarkho & Harjoseputro, 2019).

The PPM has subsequently been applied widely to elucidate customer switching behavior, mirroring population migration phenomena (Moon, 1995). The PPM has been validated across various domains including smartphone branding, e-commerce services, education, and mobile payment (Chen et al., 2023; Choudhuri et al., 2022; Liao et al., 2021; Lisana, 2023; Wang et al., 2019). This study will apply the PPM to investigate individual behavior in adopting DCEP, as it closely resembles population migration.

Since the PPM does not prescribe specific elements for each factor, push, pull, and mooring effects must be identified based on the context’s characteristics (Moon, 1995). Therefore, this study identifies push, pull, and mooring effects driving or hindering DCEP adoption, reflecting the specific context of China.

Research Hypothesis

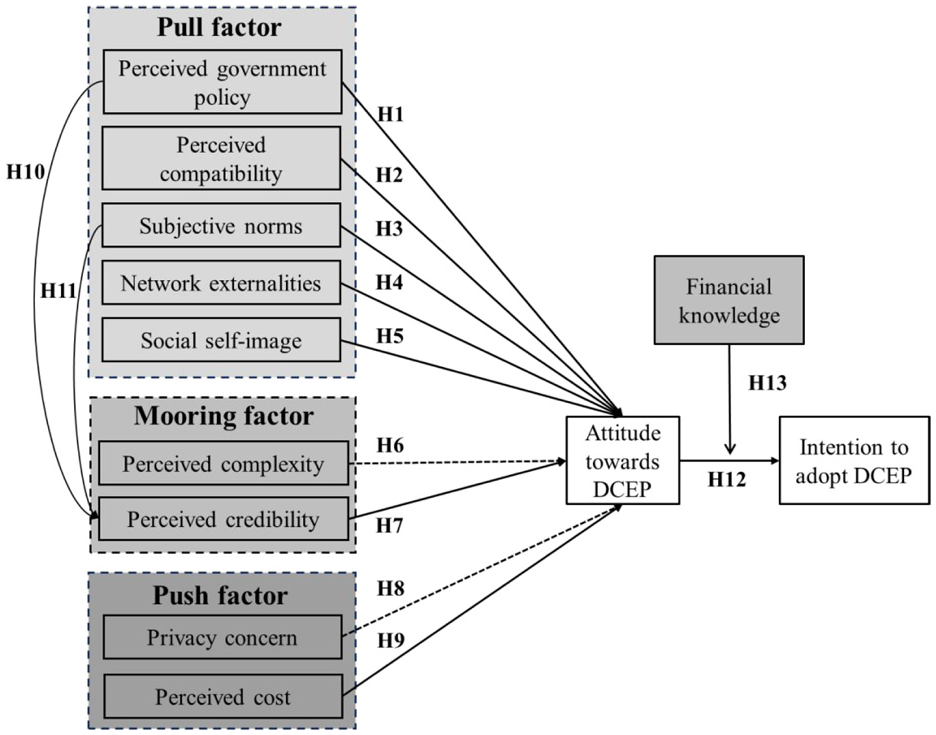

To systematically visualize the logical architecture of hypotheses and their theoretical grounding in the PPM model and SQB theory, a conceptual framework diagram of hypotheses is presented below (Figure 1), which categorizes hypotheses into four dimensions to clarify their roles in addressing research questions.

Conceptual framework of research hypotheses.

Pull Factors: Attractions of DCEP as a New System

The push effect refers to the driving factor that compels users to abandon the product they originally used (Wang et al., 2019). Since the DCEP is still in the pilot stage, government policy support will play an important role in prompting users to adopt for DCEP (Tronnier et al., 2023). The government can take supportive measures to promote and guide the diffusion of technological innovations; at the same time, the government can also set up relevant regulations that will hinder the adoption of a particular technological innovation. The government’s policy orientation directly affects individuals’ acceptance of new technologies (Qu et al., 2022), especially for the DCEP developed by PBC, where individuals’ willingness to adopt new technologies is more significantly affected by the government’s policy. The credibility of the government plays a positive role in motivating individuals to believe in the security of the DCEP (Xia et al., 2023). As a result, government policy support can significantly influence users’ attitudes toward DCEP. Based on the above arguments, we propose the following hypothesis:

H1: Perceived government policy positively influences individuals’ attitudes toward DCEP.

Perceived compatibility is defined as the degree to which an innovation is perceived to coexist with existing values, past experiences, and the needs of prospective adopters and is one of the five characteristics of Rogers’ diffusion of innovations theory (Alswaigh & Aloud, 2021). The concept of compatibility is widely used to verify the congruence between an innovation and the needs, values, and lifestyles of its potential users (Al-Okaily, 2023). Previous studies have verified that compatibility has a positive impact on consumer adoption of mobile payments (Al-Okaily, 2023; Fishbein & Ajzen, 1975). The design solution of the DCEP considers its convenience and security (Xia et al., 2023) and strongly aligns with the user’s lifestyle, values, and so on. Lifestyle, values, and so on. Based on the above arguments, we propose the following hypothesis:

H2: Perceived compatibility positively influences individuals’ attitudes toward DCEP.

Subjective norms are defined as the degree to which an individual is influenced by societal opinions in decision-making (Agárdi & Alt, 2024), forming a crucial element of both the theory of rational behavior and the theory of planned behavior. In scenarios where potential individuals encounter strong recommendations for a new technology, they are more inclined to adopt it (Kim & Kim, 2022; Schoefer et al., 2025). Previous study has employed subjective norms to confirm their impact on mobile payment adoption (Economides, 1996). DCEP’s security and traceability appeal particularly to Generation X, with older generations more influenced by subjective norms than younger ones (Kim & Kim, 2022). This study considers subjective norms to be important factors influencing users’ attitudes toward the DCEP and concludes that subjective norms can have a positive pull effect. Based on the above arguments, we propose the following hypothesis:

H3: Subjective norms positively influence individuals’ attitudes toward DCEP.

Network externalities refer to the increase in an individual’s valuation of a technological service as its user base grows (Zhang & Mao, 2020). When a potential user discovers that a large number of individuals in society are using a particular technology, especially when his friends and peers around him are using it. This widespread adoption enhances the potential user’s willingness to adopt (D. Wu et al., 2024), in which case the potential user is more likely to decide to try and adopt the technology. Users’ concerns about privacy and security issues may be reduced as a result of the externalities of the internet. According to some users of mobile payments, when more individuals in society start to use mobile payments, the government will take appropriate legislative measures to protect users’ privacy and security (Sirgy, 1985). Based on the above arguments, we propose the following hypothesis:

H4: Network externalities positively influence individuals’ attitudes toward DCEP.

Social self-image, a key psychological concept, represents the alignment between individuals’ perceptions of artifacts and their personal values and expectations (Zhang et al., 2023). This alignment influences individuals’ purchasing decisions and consumption experiences (Moore & Benbasat, 1991). Obtaining approval from peers when using a technology increases an individual’s willingness to continue its use. Based on the above arguments, we propose the following hypothesis:

H5: Social self-image positively influences individuals’ attitudes toward DCEP.

Mooring Factors: Inertia and Trust Anchors in SQB

According to the PPM, individual adoption behavior is influenced by a combination of push, pull, and mooring factors (Liao et al., 2021). The PPM is flexible regarding specific research elements; however, the mooring factor typically involves personal or social influences on individual adoption, as evidenced in numerous studies (Xia et al., 2023).

SQB refers to the tendency of users to favor the status quo and is usually classified into three dimensions: rational decision-making, cognitive misperception and psychological commitment (Samuelson & Zeckhauser, 1988). Through the previous analyses, this paper adopts two dimensions, namely, perceived complexity and perceived trust, and combines these two dimensions with the mooring factors in the PPM framework for the study. The relationship between the two dimensions for the attitude of the DCEP is specifically deduced below.

In rational decision-making, consumers evaluate the benefits and utility of alternative systems from a cognitive perspective (Nel & Boshoff, 2021), and users tend to abandon the use of a new system if its learning costs are too high. Systems that are easy to use are more likely to be adopted and accepted by consumers (Cham et al., 2021). Conversely, if the operating system and user interface of a mobile payment are too complex, the willingness of potential users to use it will decrease, which is particularly evident in Generation X (José Liébana-Cabanillas et al., 2014). The design philosophy of the DCEP includes simplicity, security, and portability, which are not only embodied in the technical aspects but also in its in-depth consideration of the user experience to reduce the learning cost for users and improve the user’s perception of the mobile payment system. Users’ learning costs and improve users’ attitudes toward DCEP. Based on the above arguments, we propose the following hypothesis:

H6: Perceived complexity negatively influences individuals’ attitudes toward DCEP.

Trust is the subjective belief that a mobile payment service service provider will always fulfill the promises and obligations it has made to provide consistent and quality service, regardless of the presence or supervision of the end user (Hamakhan, 2020). Initial trust is influenced by the quality of the payment system itself (Jain et al., 2023). The privacy of users’ information and the security of payments are also important causes of reduced trust (Sleiman et al., 2021). There is a positive relationship between individual consumers’ trust in information systems and behavioral intentions, and consumers’ trust is a determinant of their adoption of electronic transaction systems (Patil et al., 2020). Based on the above arguments, we propose the following hypothesis:

H7: Perceived credibility positively influences individuals’ attitudes toward DCEP.

Push Factors: Drivers for Abandoning Existing Payment Systems

In the process of using mobile payment applications, privacy risks can be a constraint that affects users’ continued use (Tronnier et al., 2023). In the process of using mobile payment applications, payment supply providers need to let users truthfully disclose their personal information for security reasons (Hu et al., 2023); this information disclosure behavior may potentially threaten users’ privacy. There is a general lack of understanding among users of mobile payment programs regarding the use of the private data they provide, and they may not be aware of how their personal information will be utilized. Privacy concerns further cause user resistance to payment technologies (Liu et al., 2021). The perceived effectiveness of privacy policies affects users’ trust and satisfaction with mobile payment processes (Li & Li, 2023). DCEP benefits from being a digital currency launched by PBC, and DCEP’s data are traceable and highly reliable; thus, users’ perceived effectiveness of privacy policies increases accordingly, which has a positive impact on users’ attitudes toward DCEP. Based on the above arguments, we propose the following hypothesis:

H8: Privacy concerns positively influence individuals’ attitudes toward DCEP.

Perceived cost is widely used in research in the field of mobile payments (Al-Okaily, 2023; Moon, 1995; Park et al., 2025) and are defined as the perceived financial loss acquired in the process of purchasing the product or service in question (Jean Pierre & Mombeuil, 2023). This includes the cost of purchasing the device, the overhead associated with using the mobile internet or data services, and the cost of applicable services (Ben Arfi et al., 2021). Several studies have confirmed that perceived costs have a negative impact on mobile payment acceptance (Chin et al., 2022), and some studies have identified perceived costs as one of the “mooring” factors (Moon, 1995; Rogers et al., 2019; Xia et al., 2023). However, this study does not consider that DCEP is different from the widely used mobile payment methods on the market today, as DCEP has the same utility as banknotes, and users are not charged any service or intermediary fees during the process of using DCEP (Oh & Zhang, 2022). This was also confirmed in the preliminary research, where the respondents generally agreed that the perceived cost of using DCEP was low; therefore, the perceived cost was defined as a “push” effect in this study. Based on the above arguments, we propose the following hypothesis:

H9: Perceived cost positively influences individuals’ attitudes toward DCEP.

Cross-Dimensional Relationships and Moderation

Perceived credibility essentially reflects users’ trust in the new payment system, and trust constitutes a core component of “psychological commitment” in SQB theory. When users’ trust in existing payment tools (such as Alipay and WeChat Pay) is not surpassed by the new system, an “Mooring Factors” emerges, hindering the adoption of DCEP (Loh et al., 2020; Mu & Lee, 2021). Therefore, this study also looks at other factors that have an impact on trust.

Government regulation in mobile payments is essential for building individual trust, exemplified by policies protecting individual property and privacy (Cheung et al., 2020). State security commitments can positively impact citizen adoption of mobile payments. DCEP, a digital currency backed by the central bank, benefits from strong state support, ensuring high security and reliability for individuals. National policy support for DCEP enhances individuals’ perceived trust. Based on the above arguments, we propose the following hypothesis:

H10: Perceived government policy positively influences perceived credibility.

In everyday life, individuals often tend to consider and highly regard the opinions of people around them, such as family and friends, to determine their thoughts on a particular technology or service (Lisana, 2021). When individuals are faced with indecisive situations, they tend to draw on external opinions and beliefs to justify their decisions (Ajzen, 1991). Individuals tend to draw on the opinions and experiences of people they know well to enhance the perceived security of mobile payments, with the ultimate goal of minimizing risk and uncertainty in the payment process (Lisana, 2021). Based on the above arguments, we propose the following hypothesis:

H11: Subjective norms positively influence perceived credibility.

Attitude refers to the degree to which a consumer tends to evaluate a behavior, either positively or negatively (Upadhyay et al., 2022). Existing studies have shown that attitudes toward a technology can significantly influence users’ adoption behavior (Iman et al., 2023; Mu & Lee, 2021). As a new technology, the attitudes of potential users toward DCEP are extremely important, and positive attitudes can promote consumers’ acceptance and adoption of DCEP, while negative attitudes can lead to consumer resistance and rejection of the technology. Based on the above arguments, we propose the following hypothesis:

H12: Individuals’ attitudes toward DCEP positively influence their intention to adopt DCEP.

Individuals with adequate financial knowledge better comprehend DCEP’s concept, operational logic, associated risks, and official protections (Kumari et al., 2023). Given DCEP’s innovation in the financial sector, individuals’ financial knowledge levels may influence their perceptions of its blockchain-based technology (Venkatesh & Davis, 2000). Thus, we hypothesize that financial knowledge moderates the relationship between potential individuals’ attitudes and their willingness to adopt DCEP.

H13: Individuals’ financial knowledge plays a moderating role between attitude and intention to adopt DCEP.

Combining the above hypotheses, this paper constructs a theoretical model, as shown in Figure 2.

Conceptual framework.

Research Methods

Measurement

The items of the study structure were revised and adapted from previous studies, and a seven-point Likert scale was used to rate all the items from 1 (Strongly Disagree) to 7 (Strongly Agree). Table 1 below shows the questionnaire items for each construct.

Variable Measures, Factor Loadings.

Data Collection and Respondent Profile

To ensure validity and reliability, this study conducted two rounds of pretesting. In the first round, an academician reviewed the questionnaire’s content and wording for accuracy. In the second round, 50 individuals adopting DCEP tested the revised questionnaire to verify its clarity.

Data collection was conducted via an online survey on the Credamo platform. Given the study’s focus on exploring individuals’ willingness to adopt DCEP, only respondents with DCEP experience were targeted. This criterion guided the data collection process. Since DCEP is in the pilot stage, the survey was distributed only in pilot regions using Credamo’s location filtering, with validation questions to confirm respondents’ DCEP usage. Of the 450 questionnaires collected, 55 were discarded due to incomplete responses, leaving 395 for analysis. The sample characteristics are detailed in Table 2.

Composition Distribution of the Sample (N = 395).

Method of Analysis

This study employs a two-step analytical approach using SEM and BPNN to validate hypotheses and identify factors influencing individuals’ willingness to adopt DCEPs. As SEM is limited to linear models, it may oversimplify the complexities in modeling individual adoption of DCEP. However, BPNN, with its nonlinear activation function, excels in handling nonlinear relationships and complex data patterns, yielding more accurate predictions. This study’s adoption of a two-stage SEM-BPNN approach enhances predictive analytics, offering a comprehensive understanding and a significant methodological contribution.

Results

Partial Least Squares-Structural Equation Modeling

Statistical software such as SPSS and Smart PLS were used to analyze the data in this study. Kurtosis and Skewness tests revealed that the data were approximately normally distributed. Since the data collected in this study were self-reported and cross-sectional, CMB may be an issue (Hair et al., 2022). To assess the possibility of CMB, this study utilized Harman’s one-factor test using SPSS. The results showed that one factor accounted for only 40.531% of the total variance explained, which is below the recommended threshold of 50% (Hair et al., 2022). This indicates that there’s no indication of CMB, and the validity and reliability of the data were verified.

The processed data were then analyzed in two stages. First, a measurement model was estimated to test the reliability and validity of the data in this study. Second, a structural model was estimated that tested the research hypotheses, and appropriate conclusions were drawn. These two approaches ensured that there were valid and reliable measurement properties between the study constructs.

Measurement Modeling

Reliability Analysis

In this study, Cronbach’s α coefficient and composite reliability (CR), which are usually used to measure the internal consistency of observed and latent variables, were used to measure the reliability of the questionnaire, as shown in Table 3. The Cronbach’s α coefficient and CR of the questionnaire used in this study were greater than 0.7, which indicated that the reliability of this study was acceptable.

Cronbach’s α, Composite Reliability (CR), Average Variance extracted (AVE) and Rho-A Values for the Construct.

Validity Analysis

To verify the validity of the modified measurement method, this article verifies it from two perspectives, convergent validity and discriminant validity. As shown in Table 1, Most of the factor loading coefficients are greater than 0.7. As shown in Table 4, the values of the AVE for all the constructs are greater than the threshold value of 0.5, which both indicate that the measurement model has good convergent validity.

Discriminant Validity (Fornell and Larcker).

Note. Bolded diagonal entries denote the square root of the average variance extracted (AVE) for each construct. Per the Fornell-Larcker criterion, discriminant validity holds if a construct’s AVE square root is larger than its correlations with all other constructs (off-diagonal values).

According to the Fornell–Larcker criterion, the square root of the AVE for each construct exceeds its correlations with other constructs in Table 4, confirming acceptable discriminant validity. Since HTMT does not apply to the relationship between lower-order component and higher-order component (Jain et al., 2023), it is not considered in this article.

Structural Modeling

The evaluation of the structural model focuses on testing its validity and assessing whether causality is established in the theory-building stage.

Validity Test

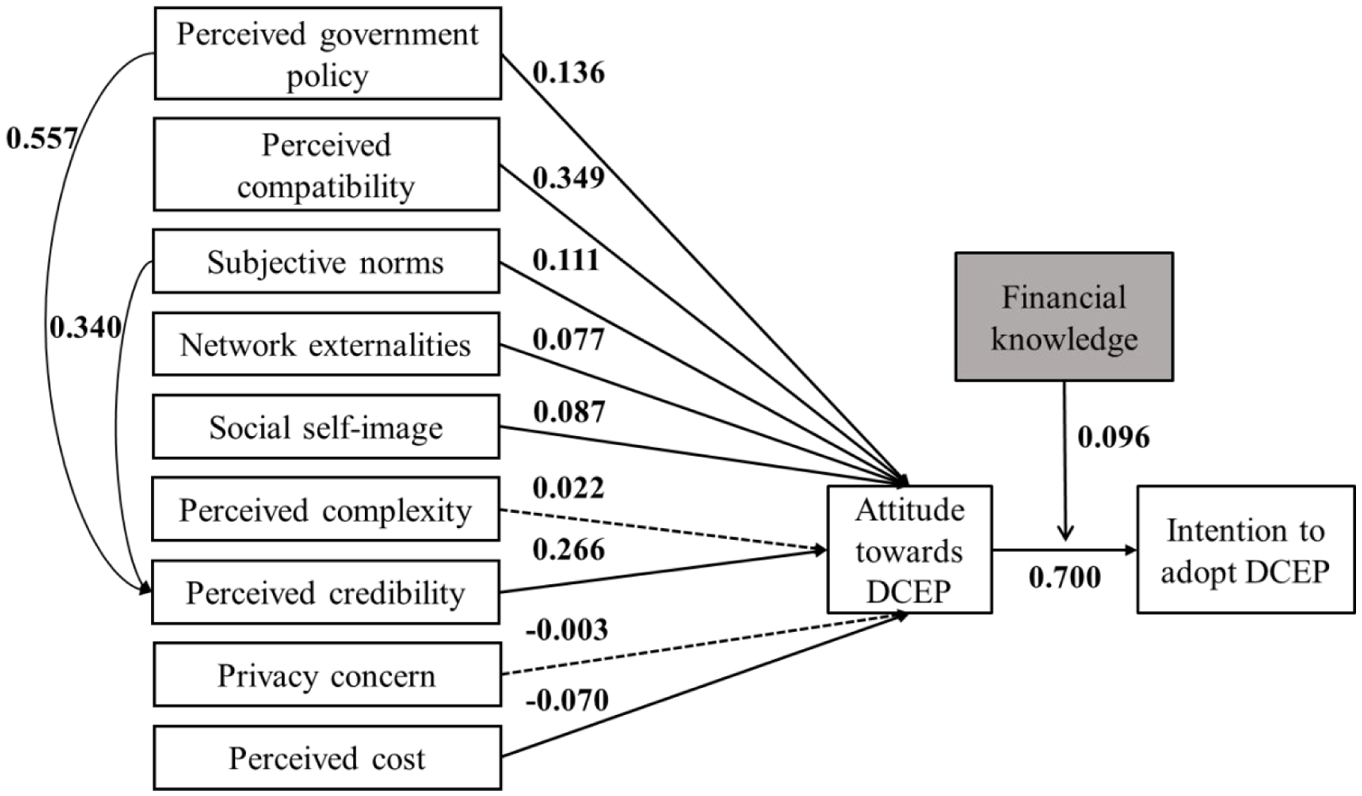

When the R2 value is greater than .26, the explanatory ability of the model is considered to be good (Reilly et al., 2007). As shown in the table, the R2 values of this paper are all satisfactory; thus, the model has good explanatory ability. The predictive relevance of the model is determined by the Q2 value, when the Q2 value is greater than 0, then it shows that the model has good predictive ability, as shown in Table 5, this model has a strong predictive ability. It has been shown that when the f2 value is greater than .01, the model has an acceptable path effect, and most of the path effect amounts are acceptable (Hagerty et al., 2020; Henseler et al., 2014; Rodrigues et al., 2020), as shown in Figure 3.

Predictive Power of Constructs.

Structural model results.

Overall Model Testing

The fitness of the predictive model is usually judged using the global criterion of goodness of fit (GoF); the baseline values of the GoF are .1, .25, and .36, which indicate a small, medium and high degree of model fitness, respectively; and the GoF value in this study is .69, which also indicates a high degree of fitness of the model.

Path Coefficients

The standardized root mean square residual (SRMR) is used to assess the goodness of fit, and the SRMR value in this article is .056 (<.08), which indicates that the model has a good fit. The RMS theta value is lower than .14 (Çakıt et al., 2020), and the NFI value ranges from 0 to 1, with values closer to 1 indicating a better model fit (Ding et al., 2023). The model in this paper has an RMS theta value of .129 and an NFI value of .796, which suggests that the quality of the model is within acceptable limits. Table 6 summarizes the empirical results of the hypotheses of this study, and the results are shown in Figure 3.

Hypothesis Testing (N = 395).

The results showed that the perceived government policy is positively related to the attitudes toward DCEP (β = .136, t = 2.626), supporting hypothesis H1. The perceived compatibility is positively related to the attitudes toward DCEP (β = .349, t = 7.171), supporting hypothesis H2. The subjective norms are positively correlated with the attitudes toward DCEP (β = .111, t = 1.975), supporting hypothesis H3. The network externalities are positively correlated with the attitudes toward DCEP (β = .077, t = 2.094), supporting hypothesis H4. The social self-image is positively correlated with the attitudes toward DCEP (β = .087, t = 2.014), supporting hypothesis H5. The perceived complexity had not a significant effect on the attitudes toward DCEP (β = .022, t = 799), rejecting hypothesis H6. The perceived credibility was positively correlated with the attitudes toward DCEP (β = 0.266, t = 4.407), supporting hypothesis H7. The privacy concern had not a significant effect on the attitudes toward DCEP (β = −.003, t = .075), rejecting hypothesis H8. The perceived cost is negatively related to the attitudes toward DCEP (β = −.07, t = 2.66), supporting hypothesis H9. The perceived government policy was positively correlated with the perceived credibility (β = .557, t = 7.03), supporting hypothesis H10. The subjective norms were positively correlated with the perceived credibility (β = .340, t = 5.212), supporting hypothesis H11. The individuals’ DCEP attitude is positively correlated with the Intention to adopt DCEP (β = .700, t = 14.206), supporting hypothesis H12. Financial knowledge plays a moderating role between the attitudes toward DCEP and the intention to adopt DCEP (β = .096, t = 2.851), supporting hypothesis H13.

BPNN

The BPNN was developed by Rumelhart et al. (1986) and can not only model the nonlinear relationship between variables but also has adaptive and self-learning capabilities. Scholars have adopted a two-stage SEM-BPNN approach based on survey data to forecast enterprise performance (Sun et al., 2022) and consumer purchase intention (Ding et al., 2023). To compensate for the lack of nonlinear analysis capability of SEM, this article introduces the paths that have significant influence on SEM as input neurons in neural network analysis, similar to Ding et al. (2023), and constructs a back-propagation neural network (BPNN) to explore the complex psychological paths of individuals’ willingness to adopt the DCEP.

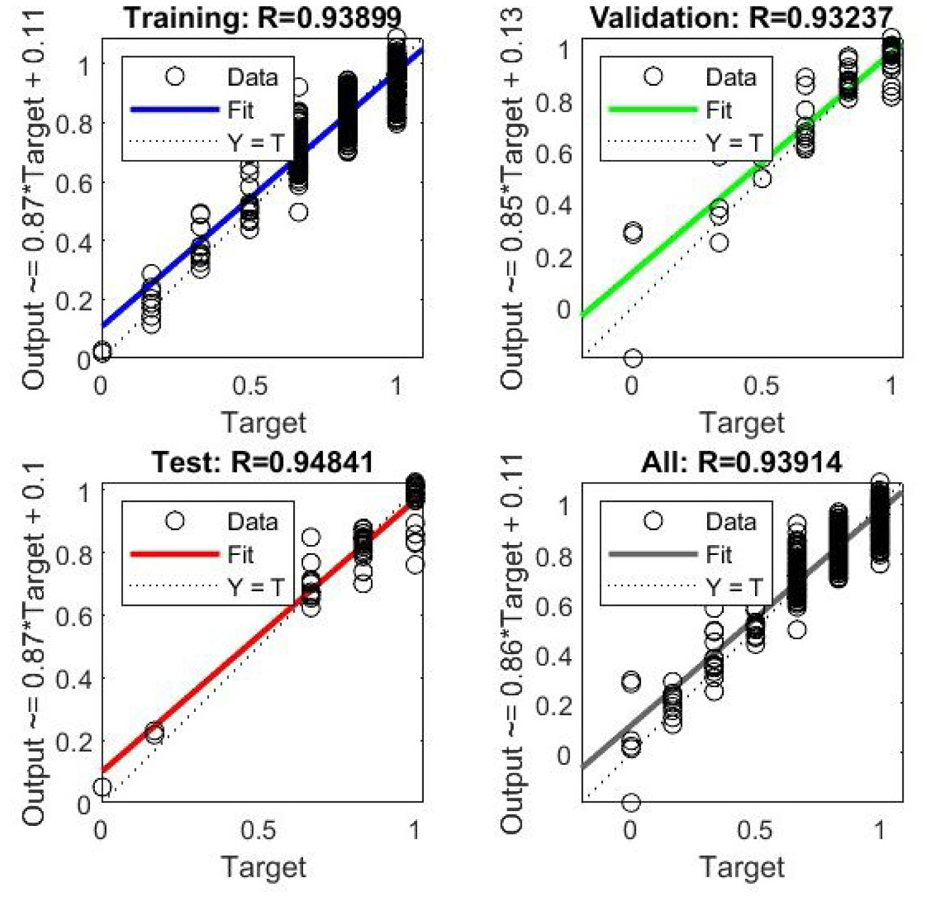

In this paper, the Monte–Carlo method is also introduced to adjust the parameters of the BPNN, and thousands of simulation experiments are carried out within a certain experimental range to obtain the optimal prediction model, which not only reduces the workload of manual parameter searches but also reduces the randomness and locality of manual parameter searches. Three hundred and ninety-five data points were collected through questionnaires, and before BPNN training, all the data were normalized; 80% of the data were randomly assigned for training, and 20% were used for testing and validating the optimal BPNN model established by the Monte–Carlo method. The final goodness of fit was acceptable, with an R value closer to 1 indicating a closer relationship between the predictions and the output data (the results are shown in Figure 4).

Goodness-of-fit of BPNN in different datasets.

The sum of squares due to error (SSE) and root mean square error (RMSE) were obtained from the training, testing, and validation processes, as shown in Table 7; the average SSE values were .8347 (SD = .2088), .5741 (SD = .0929), and .4366 (SD = .1222) for training, testing, and validation, respectively; and the average RMSE values were .0510 (SD = .0064), .1210 (SD = .0099), and .1035 (SD = .0147), respectively. The mean RMSE values of all three processes are relatively small, which suggests that the BPNN can calibrate the data well and has a higher level of predictive accuracy (G. Wu et al., 2022).

The Sum of Squared Error and RMSE for BPNN.

In this article, sensitivity analyses were also used to measure the importance of the variables. All the variables that produced significant effects in the SEM were entered into the BPNN and ranked according to the normalized importance of the neural network and SEM path coefficients (as shown in Table 8), in which perceived compatibility (PI) maintained the most important position in both stages of the analysis (SEM-BPNN); however, the five variables of perceived government policy (GP), social self-image (SSI), perceived cost (PEC), network externalities (NE), and subjective norms (SN), the order of importance of the six variables, changed dramatically in the BPNN. If only a single-stage SEM analysis is conducted, it is difficult to accurately explore the factors that influence individual’s adoption of DCEP, which is valuable when using a two-stage analysis (SEM-BPNN) in this study.

Sensitivity Analysis of Neural Networks.

Discussion

Conclusion

This study incorporates multiple theoretical perspectives into the PPM to provide empirical support for a clear understanding of individuals’ willingness to adopt DCEP. Based on the above results, it can be concluded that individuals’ attitudes toward DCEP are crucial prerequisites for their adoption of DCEP. In addition, variables such as perceived compatibility, subjective norms, network externalities, social self-image, perceived cost, perceived government policies, and trust significantly influence individuals’ Intention to adopt DCEP. Furthermore, individuals’ financial knowledge plays a positive moderating role between attitude and intention to adopt. This implies that individuals with more financial knowledge have more positive attitudes toward DCEP and are more likely to have the intention to adopt it, which is consistent with the findings of G. Wu et al. (2022).

Interestingly, when conducting SEM analyses, unlike the results of previous studies, this study found that the hypothesis that individuals’ perceived complexity negatively affects their attitudes toward DCEP does not hold. A reasonable explanation for this is that since mobile payment platforms are meant to provide convenient transaction services for financial transactions (Moon, 1995), most individuals in China alternate between using Alipay and WeChat, and the interfaces designed by major transaction platforms are very consistent. There is no high switching cost; therefore, individuals skilled in the use of mobile payments do not have a high level of perceived complexity.

Moreover, individuals’ perceptions of the effectiveness of privacy policies did not negatively affect their attitudes toward DCEP, which may be due to the Chinese government’s ongoing strict control over mobile payment platforms. Over the past few years, the Chinese government has taken a series of measures to protect individual privacy and data security, such as establishing the National Data Bureau to provide individuals with a more secure and reliable data environment, which has resulted in relatively high perceived effectiveness of privacy policies. In addition, the DCEP, as a representative of the central bank’s digital currencies, has been strongly supported and promoted by the government, which may further enhance individuals’ trust and recognition of it.

On this basis, the variables that showed a significant influence on the SEM analysis were introduced into the BPNN to analyze the nonlinear relationships between the independent variables and the dependent variable. The variable with the greatest influence on the SEM, perceived compatibility, remained in the first place in the BPNN. This finding suggested that what individuals are most concerned about should be the degree to which DCEP is compatible with their lifestyles and payment methods and the individuals’ sense of adoption of DCEP, which is consistent with the findings of Mombeuil (2024). Perceived government policies ranked 4th in terms of impact in SEM but rose to second place in BPNN, which may be due to the nonlinear nature of BPNN and higher prediction accuracy. The impact of government policies on individuals’ attitudes toward the adoption of DCEP is complex and affects not only individuals’ perception of trust but also their perceived costs, privacy, and security. These findings contrast with those of Qu et al. (2022) and underscore the practical significance of incorporating BPNN analysis. The impact of perceived cost changes from the penultimate position in SEM to the third position in BPNN, indicating that individuals are very concerned about the cost level of DCEP.

Therefore, to promote the adoption of DCEP by individuals, it is necessary to start from a number of aspects, including increasing individual awareness of DCEP, reducing the cost and complexity of their use, and accelerating inputs to increase the positive effects of network externalities. Moreover, the government needs to formulate appropriate policies to support the promotion and application of the DCEP.

Theoretical Contribution

The primary contributions of this study are as follows. First, the use of a two-stage analysis method, SEM-BPNN, for predictive analyses, which allows for a better understanding of the relationship between the variables and provides an important methodological contribution from a statistical perspective, further expands the research field of Ding et al. (2023). And BPNN analysis, which can compensate for the shortcomings of SEM analyses and provide a new perspective on understanding the factors influencing consumers’ adoption of DCEP.

Second, deepening the understanding of digital currency acceptance. Utilizing a combination of PPM and SQB perspectives, in contrast to TAM and UTAUT employed in prior studies (Ma et al., 2023), this research enhances our comprehension of consumer acceptance to the adopt of DCEP. This not only enriches the theoretical framework of digital currency acceptance but also provides novel perspectives and tools for future research.

Finally, revealing the consumer decision-making process. The results reveal the decision-making process of consumers adopting for DCEP, showing that consumers’ attitudes, perceived compatibility, subjective norms, network externalities, social self-images, perceived costs, perceived government policies and perceived credibility all influence their intention to adopt DCEP. This study provides new insights into understanding consumers’ decision-making mechanisms in the DCEP acceptance process.

Practical Implications

The comprehensive findings of this study yield significant practical value for policymakers, financial institutions, and technology developers seeking to promote the widespread adoption of DCEP.

First, achieving functional compatibility emerges as a critical prerequisite for user adoption. The DCEP interface should meticulously replicate the design logic and interaction patterns of mainstream payment platforms to minimize behavioral switching costs. By embedding payment functions within high-frequency transactional scenarios—while maintaining familiar operational workflows—developers can reduce cognitive load and accelerate habitual usage. This approach leverages existing user mental models to facilitate seamless migration from conventional payment tools.

Second, institutional trust-building requires strategically converting China’s sovereign credibility into tangible user perceptions. Policymakers should implement a multi-pronged trust architecture combining transparent policy communication, verifiable security features (e.g., blockchain-enabled transaction traceability), and robust privacy protections aligned with international standards. A phased incentive system proves particularly effective—allocating trial funds to overcome initial adoption inertia, followed by targeted subsidies to sustain engagement. This dual approach directly counteracts the psychological resistance mechanisms identified in SQB theory, transforming abstract national credit into daily transactional confidence.

Third, harnessing network effects demands demographic-specific strategies. For digitally native users, integrating DCEP with social platforms and fintech ecosystems can position it as both a payment tool and a vehicle for digital identity expression. Conversely, middle-aged adopters require emphasis on concrete benefits through trusted intermediaries; financial key opinion leaders (KOLs) should articulate DCEP’s unique value proposition, particularly its policy-backed stability advantages during economic volatility. This bifurcated approach ensures alignment with distinct generational motivations and media consumption patterns.

Fourth, regional implementation must account for socioeconomic disparities. In less developed regions with lower financial knowledge, campaigns should synergize basic monetary education with trust-building measures to overcome SQB-related cognitive barriers simultaneously. Contrastingly, first-tier city strategies should emphasize DCEP’s social signaling potential—collaborating with premium merchants to create exclusive membership tiers or luxury purchase benefits. Such initiatives satisfy higher-order psychological needs while leveraging urban consumers’ status-conscious behaviors.

Finally, we propose establishing an adaptive governance mechanism combining SEM for pathway monitoring with BPNN analytics. This system would dynamically optimize resource allocation when adoption metrics deviate from projected thresholds, creating a responsive feedback loop. Beyond immediate DCEP applications, this integrated methodology offers developing economies a replicable framework for CBDC deployment—particularly in markets where informal economic activity necessitates flexible policy instruments. Collectively, these implications bridge theoretical insights from behavioral economics with actionable fintech implementation strategies.

Research Limitations and Future Prospects

Despite its theoretical significance and practical value, this study on individual behavior when adopting DCEP has several limitations and suggests directions for future research. First, the interface research design only reveals concurrent relationships between variables. To ascertain causal relationships, future studies should consider causal inference designs or longitudinal approaches. Second, the use of a web-based questionnaire may introduce bias and subjectivity. Future research should employ diverse methods and larger sample sizes to enhance study accuracy and reliability. Finally, this study focuses on the conversion to DCEP and does not consider reverse conversions back to traditional mobile payments. Given the complexity of conversion processes, future research should explore reverse mobility to reassess the balance of factors influencing service choice, providing new practical insights.

Footnotes

Acknowledgements

We would like to express appreciation to the anonymous reviewers for their constructive feedback on an earlier draft of this article.

Ethical Considerations

The study was approved by the Institutional Review Committee of the School of Management, Guizhou University (Ethical Approval Number: GDGY2023007, Date: December 27, 2023). The research adheres to the ethical standards of the Declaration of Helsinki and relevant institutional guidelines. The committee confirmed that the experimental design ensures participant safety, privacy, and voluntary engagement, with no foreseeable harm or conflicts of interest.

Consent to Participate

Participants provided electronic informed consent via the Credamo platform before engaging in the online experiment. They were explicitly informed of the study’s purpose, procedures, and their right to withdraw at any time without penalty. Consent was confirmed by checking a digital “Informed Consent” box and providing a signature. All data were anonymized and stored confidentially, with no personal identifiers linked to the results.

Author Contributions

XG, YZ, MW, and XJ involved in conceptualization and methodology. XG and YZ involved in data analysis, writing—original draft preparation, and translation. XG and MW involved in writing—review & editing, supervision, and final review.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Humanities and Social Sciences Research Program of Guizhou University (Grant No. GDYB2023011), the Guizhou Provincial Graduate Research Fund Project (Grant No. 2024YJSKYJJ100), the Special Project on Ideological and Political Education for Postgraduate Students of Guizhou University (Grant No. GDZX2024034), and the Guizhou University Laboratory for Collaborative Innovation in Digital Transformation and Governance (Grant No. GLSZ202415).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting the findings of this study can be obtained from the corresponding author upon reasonable request.