Abstract

This study seeks to identify core housing bubble predictors and empirically investigate a novel model for detecting housing bubbles in Malaysia. We engender new insights based on the extraction of real-time opinions of market players about housing bubble formation and collapse. We employ a practical approach using a comprehensive survey of opinions from relevant walks of life via the survey data analysis software, SmartPLS3. Results indicate that housing demand, economic growth outlook, and buyers’ expectations positively impact the housing bubble. This study’s present housing market condition, foreign investment, and government policies are otherwise insignificant. We found that the present housing condition, government policies, and economic growth outlook do not influence the impact of housing demand, buyers’ expectations, and foreign investment on the housing bubble. We employed a cross-sectional research design in this study to obtain our findings. This might have indirectly suppressed more robust findings, which may have been otherwise obtained in the case of a longitudinal study. We advocate that policymakers should not overlook the significant roles of housing demand, economic growth outlook, and buyers’ expectations of the housing bubble. We show that the present housing market condition has no significant moderating effect on the impact of buyers’ expectations, foreign investment, and housing demand on housing bubbles.

Introduction

The Great Recession (2007–2009) and its aftermath have planted serious financial crisis awareness among policymakers in many countries. According to IMF Global Financial Stability Report April 2008, this Great Recession may result in huge losses estimated at one trillion globally. What are the causes of this global financial crisis? To date, it is recognized that the main cause of the United States of America’s (USA) mortgage meltdown in the 2008 Financial Crisis was the housing bubble that occurred between 2001 and 2008 (Bianco, 2008). The surge of the financial crisis had led to tremendous losses in the global economy and global trade since WWII. This ultimately led to the global Great Recession. Studies have confirmed that continuous rising in housing prices and increasing the level of indebtedness are the two major players that led to the collapse of the financial systems (Banking crisis), which automatically caused the great recession (Kauko, 2014; Schularick & Taylor, 2012). Therefore, policymakers should not mainly focus on the ex-post strategies to curb the effect of the bubble or its collapse; instead, they should prioritize understanding the development of such bubbles and their occurrence in real time. This is because timely detection of the bubbles would help policymakers design more efficient macro-prudential actions, strategies, and measures to stop and curb any potential crisis and therefore ensure financial stability.

Most economic forecasters find it difficult, if not impossible, to identify leveraged bubbles. There is generally no consensus on a well-established definition of a bubble. In a way, the complexities in identifying bubbles force policymakers to resort to using a variety of factors and models. It is well understood that easy-to-interpret analytical frameworks are appropriate tools that could provide a significant and timely prediction of any potential bubble and crisis.

Given the complexities of identifying the housing bubble and policymakers’ preferences and priorities, we propose a survey approach whereby a comprehensive survey of opinions from relevant walks of life is conducted and analyzed using up-to-date survey data analysis software, SmartPLS3. However, to date, the housing bubble has no commonly accepted definition. Yet, other than recognizing past episodes of housing price booming-busting that resulted in the formation of a housing bubble like that of the 2006 subprime crisis bubble, it can be taken as a standard barometer. Thus, the crucial question is whether we should measure the disastrous effect of a busted housing bubble on the economy as a standard guide to monitoring the existence of a housing bubble. Or we use the rate of price hike and fall as a measure for the existence of a boom and bust of the housing bubble, based on a chosen bubble definition.

Housing bubble studies are scarce in the Malaysian context. Few studies have taken the initiative to investigate the causes of the housing bubble in Malaysia. Hussain et al. (2012) studied the housing market’s presence in the Malaysian context and argued that a housing bubble exists in Malaysia but only in five districts in Klang Valley, that is, Ampang, Batu, Kuala Lumpur, Petaling, and Setapak during 2005 to 2010. The limitation of Hussain et al. (2012) study is that the housing bubble was not clearly defined. Another shortcoming of Hussain et al. (2012) study is that they have not clearly defined the bubble’s magnitude and verified its existence. We attempt to bridge this gap in the literature by providing a model procedure to detect and ascertain the existence of a housing bubble.

Following the recommendations of Sarstedt et al. (2017) in employing the partial least square—structural equation modeling (PLS-SEM) technique, this study used the SmartPLS3 software to predict the direct impacts of present housing market conditions (PHMC), housing demands (HD), buyers’ expectations (BE), foreign investment (FI), government policies (GP), and economic growth outlook (EGO) on housing bubbles. The SmartPLS3 is a more appropriate statistical tool for estimating moderation models (Lowry & Gaskin, 2014). Therefore, it has been used to estimate the moderating effects of PHMC, GP, and EGO on the impacts of HD, BE, and FI on housing bubbles. The use of PLS-SEM is considered more appropriate in this study. This is because it has been explicated by Sarstedt et al. (2017) that PLS-SEM should be employed to predict and explain a defined crucial construct or when finding important predictors of a construct (Ringle et al., 2020). The SmartPLS3 has been used to analyze this study’s confirmatory and exploratory factor analysis. The demographics and descriptive statistics have been evaluated using the SPSS version 25.

Malaysian Housing Bubble Scenario

The Malaysian housing market has made many changes, especially in the past decade. Looking at Table 1 and Figure 1, we can conclude that the Malaysian House Price index has increased from 92.4 in 2009 Q1 to 193.5 in 2018 Q4. The housing prices increased from RM204,470 in 2009 to RM417,440 in 2018. This is an increase of 104.15% over 10 year only. This dramatic increase made housing prices less affordable, especially for M40 and B40 populations. But if we look at the changes over 12 month in the housing price index, we notice that the changes over 12 month show the existence of two scenarios. Based on Table 1 and Figure 2, the first scenario is between 2009 and 2012, when the house prices in Malaysia increased to their maximum by an average of 14.5% in Quarter 4 in 2012. The second scenario was between 2013 and 2018, where the change over 12 month then started decreasing over the year until it reached the minimum change of 1.6 in quarter 4 in 2018.

Malaysia Housing Price Index (MHPI) and All House Price Annual Change 2009—Q4 2018.

Source. NAPIC (2020).

Malaysia Housing Price Index (MHPI) quarterly trend Q1 2009−Q4 2018.

Malaysia Housing Price Index (MHPI): Annual percentage change Q1 2009−Q4 2018.

Table 1 shows that housing prices in Malaysia have a very strong average increase above two digits yearly between 2011 and 2013. The price index increase annually by 10.9%, 13.4%, and 11.2% in 2011, 2012, and 2013 respectively and an annual increase of 9.4%, 7.4%, 7.1%, and 6.5% in 2014, 2015, 2016, and 2017 respectively. This increase surpassed the average annual growth of 3.78% in these 7 year. During this period, banks were more relaxed in providing loans to house buyers, and they recorded high profits, thus expanding their growth to double-digit levels. The growing demand for housing in this period led developers to supply more units to make more profits. This steady completion among developers caused an oversupply of housing units. The Ministry of Finance (MOF) has announced that the oversupply of housing created approximately a 40% of new unsold residential units during the first half of 2017, compared to the first half of 2016. This phenomenon gradually led to a decline in housing prices until the housing market had an overhang in 2018 until today.

In the second phase of the scenario, the slow economic growth had significantly affected Malaysian purchasing power, making house prices unaffordable to many Malaysians. The firm regulations for foreigners to buy properties in Malaysia caused the housing demand to decrease again. The government increased the minimum investment requirement for foreigners from RM 250,000 to RM 500,000 in 2014 and then increased it again to RM one million from 2014 to 2019. In addition, the stagnant Malaysian House Price Index during the year 2018 (which was stable at around 193) and the decline of the overall demand for houses led the Malaysian government to give out many incentives to Malaysians, especially the lower income group and first-time homebuyers, such as stamp duty exemptions, deposit assistance, and low-interest rate loans. These measures and incentives are aimed at increasing the affordability of the M40 and B40 population to buy houses. Although the recent data shows some positive signs of housing demand recovery, it is still that these measures and incentives do not significantly stimulate the housing market.

Also, the government has implemented other measures, such as Rent-to-Own (RTO) financial scheme, lowering of the foreign ownership threshold fpm one million to only RM600,000, Youth Housing Scheme, and revising the Real Property Gains Tax (RPGT) could help the housing market to pick up and restore to normal condition. Another factor that has significantly affected the housing demand is the stagnation of the household’s income and, at the same time, the rise in the living cost. Data from the Department of Statistics (DOS, 2019) revealed that the median monthly income in Malaysia has grown only by 6.6% per annum since 2016. This is considerably low compared to the high cost of living, particularly in urban areas.

Literature Review

The housing bubble concept has received increased attention over the years (Holt, 2009; Joebges et al., 2015). In the wake of increased socio-economic, political, and technological advancements, several studies have investigated the phenomenon of the housing bubble to deepen insights into its association with price fluctuations and socio-economic growth (Hulse & Reynolds, 2018; Liao et al., 2015). Numerous attempts have been made to examine the housing bubble from housing affordability and demand perspective (Adi Maimun et al., 2018; Wetzstein, 2017), monetary policies (I. C. Tsai, 2015), mortgages and employment insecurities (Dotti Sani & Acciai, 2018), housing market conditions (Coskun & Jadevicius, 2017), housing boom and price (Blanco et al., 2016) and others. Nevertheless, the housing bubble phenomenon still poses significant socio-economic challenges that command attention concerning its significance to the wider economic growth across several developing countries (Coskun & Jadevicius, 2017; Dotti Sani & Acciai, 2018). Malaysia is one of the developing economies that have experienced the housing bubble impact and still struggles to deal with its challenges (Adi Maimun et al., 2018; Zainun et al., 2013). Consequently, to curb the growing challenges of the housing bubble in Malaysia, distinct approaches have also been employed to investigate and further propagate advancements in concepts associated with the housing bubble phenomenon (Adi Maimun et al., 2018).

Additionally, to deal with housing affordability and demand issues associated with the housing bubble, Adi Maimun et al. (2018) employed the Artificial Neural Network Model (ANN) to aid in forecasting housing demand in Malaysia. Zainun et al. (2013) also utilized the SmartPLS2 software to estimate and show that economic factors such as inflation rate, housing stuck, and Gross Domestic product are the most significant economic indicators of low-cost housing demand in Melaka, Malaysia. Amin et al. (2017) also employed the SmartPLS3 software to estimate and show that service quality, product choice, and Islamic policy are predictors of the Islamic home financing preference in Malaysia. In light of the constantly high housing demand in the Malaysian housing industry, Chai et al. (2015) used the SEM AMOS software to estimate and demonstrate that preventive measures are most influential for curbing housing delivery delays. Mohammed and Sulaiman (2018) also utilized the SmartPLS3 software to identify and exemplify that attitude, sense of attachment to a place, motive of bequest, perceived ability, and social influence positively influence households’ willingness to use a reverse mortgage in Malaysia. Khan et al. (2017) used the SmartPLS3 software to demonstrate further that neighborhood, economic, location, and structure factors influence first-time home buyers’ buying decisions for a new house. Likewise, Wan Rodi et al. (2019) employed the SmartPLS3 software to demonstrate that location, site, building engineering and services, and building appearance and design significantly impacted housing rental depreciation. These contributed to rental depreciation in the Golden Triangle Area of Kuala Lumpur, Malaysia.

While these studies mirror several significant findings that explicate the housing bubble undergirding, it is important to note that they respectively deal with rather narrow perspectives of housing bubble fundamentals, which in themselves do not holistically reflect wider socio-economic predictors of fluctuations and detections of the housing bubble phenomenon (Ab-Majid et al., 2017; Baqutaya et al., 2016; Lean & Smyth, 2013). Hence, we initiate deeper rigor that deepens knowledge on a much broader scope of the housing bubble concept by further investigating the roles of wider socio-economic predictors and how they aid in detecting the housing bubble in the Malaysian housing industry. Consequently, we empirically evaluate how housing demand, buyers’ expectations, market conditions, government policies, foreign investment, and economic growth outlook contribute toward housing bubble detection. Congruent with extant research (Adi Maimun et al., 2018; Wetzstein, 2017), housing demand significantly influences the housing bubble via constant price fluctuations in the housing market. Wetzstein (2017) argues that housing demand mirrors the rate of the need for adequate and affordable shelter by individuals in need of housing units. The demand for housing has also been argued to be a consequence of individuals wanting to move their houses to more comfortable locations or those desperately needing to relocate to escape disaster, conflict, or insatiability. Equally, a rapid increase in these situations fosters the upsurge in housing prices and housing shortages (Wan Rodi et al., 2019; Wetzstein, 2017).

Studies also argue that buyers’ expectations deal with the wants or needs associated with buyers’ preference for a defined housing unit (Khan et al., 2017). These preferences have been espoused to influence the housing bubble via an impact on house prices (Baqutaya et al., 2016). Preferences such as traffic congestion, housing location and accessibility, housing affordability, household type, housing value, and social class have been debated to be associated with buyers’ expectations (Baqutaya et al., 2016; Hou, 2017; Khan et al., 2017). Consequently, buyers deciding to buy housing units depends on the extent to which their housing expectations have been met (Khan et al., 2017; Wan Rodi et al., 2019). It is therefore argued that an increase in housing buyers’ expectations could result in a hike in price as the efforts to satisfy expectations might require more financial cost (Ab-Majid et al., 2017; Baqutaya et al., 2016). Moreover, it is plausible that a hike in housing prices could inspire higher investments by housing market investors, which might also cause a supply and, subsequently, less demand for houses. This could, thus, trigger a probable housing bubble bust (Hulse & Reynolds, 2018; Liao et al., 2015).

On the other hand, the housing market condition mirrors a mix of several factors capable of influencing the state of supply or demand of housing properties (Adi Maimun et al., 2018). These factors might include inflation rate, housing stuck, and Gross Domestic Product (Zainun et al., 2013). They may also be low-cost housing demand, service quality, product choice, government policies, housing delivery delay, attitude, sense of attachment to a place, motive of bequest, perceived ability, and social influence (Chai et al., 2015; Mohammed & Sulaiman, 2018). In the context of housing bubbles, studies indicate that market conditions have been arguably influenced by location and structure factors, building engineering and services, and building appearance and design (Khan et al., 2017; Wan Rodi et al., 2019). These factors tend to contribute toward an upward or downward slope in the demand or supply of housing properties. Congruently, high demand or supply or an excessive drop in the demand or supply of housing properties could trigger a housing bubble boom or bust (Glaeser et al., 2008; Nobili & Zollino, 2017).

Equally, government policies, foreign investments, and economic growth outlook have been argued to reflect a major precursor of the state of the housing bubble (Ab-Majid et al., 2017; Baqutaya et al., 2016; Joebges et al., 2015). Policies enacted by policymakers play a major role in influencing the power of property market agents and builders to exert strongholds on housing prices (Baqutaya et al., 2016; I. C. Tsai, 2015). A change or constant fluctuations in housing prices could result from unstable or ill-defined government policies enacted into law (Holt, 2009; I. C. Tsai, 2015). Likewise, property markets may face property returns shock in the wake of a shift in political power, thus, dampening the extent to which foreign investors invest in the property market industry (Antonakakis et al., 2018; Hulse & Reynolds, 2018). Ethics governing the property markets funding scheme ought to be given ample consideration as an excess of funding by the government may engender much supply of government-owned housing properties, hence, leaving less or no opportunities for foreign investments by exuberant investors (Hanudun et al., 2017; Mohammed & Sulaiman, 2018). Moreover, chances are that in the event of frequently changing policies or political instability, there could be dire cases of housing price shocks which can negatively trigger a housing bubble bust (Coskun & Jadevicius, 2017).

In light of the housing bubble, foreign investment could be a major source of increased revenue for an economy or a major factor that could strike a decline in the economy if left unchecked or less monitored (Hulse & Reynolds, 2018). Foreign investment could be explored as a remedy for housing markets with insufficient financial resources to meet the myriad choices enshrined in the demands of housing property buyers (Liao et al., 2015). However, a high rate of investment in the housing market could relay autonomy of fixing housing prices into the hands of probable investors who could influence housing prices to foster profit maximization (Hulse & Reynolds, 2018). Unchecked foreign investment could lead to an oversupply of housing properties (Wan, 2018; Wetzstein, 2017). In light of profit maximization, a high cost of housing properties could trigger a drop in housing demand, thus, fostering fluctuations in the housing bubble (Wan, 2018; Zainun et al., 2013).

Similarly, the economic growth outlook is yet to be given sufficient empirical attention to foster the prediction of housing bubble detection (Coskun & Jadevicius, 2017; Said & Majid, 2014). Studies advocate for an in-depth investigation into how the economic growth outlook could help detect the housing bubble phenomenon (Tokic, 2008; Yunus et al., 2012). This is important for policymakers to obtain informed decisions concerning possible housing price shocks (Holt, 2009). Economic growth outlook in the housing bubble context relates to the analytical forecast of the property market to determine, initiate favorable housing market conditions, and curb probable housing price shocks (Coskun & Jadevicius, 2017; Said & Majid, 2014). Debates of prior research indicate that an adequate forecast of property markets’ growth conditions could help account for or determine the housing bubble boom and project a plausible housing bubble bust (Tokic, 2008; Yunus et al., 2012).

Research Gap

Based on the review earlier, there are some limitations that previous researchers have not considered in their analysis. First, despite the fact that many researchers have studied past housing bubbles, there is still no agreement on how to define and recognize a bubble in the present. A potential area of focus is the creation of more precise and trustworthy methods for forecasting and spotting housing bubbles. This study developed a comprehensive model based on theoretical underpinning and apply the Structural Equation Modeling to predict the housing model. Second, researchers have identified various factors that can contribute to the formation of housing bubbles, such as low interest rates, lax lending standards, and speculative behavior. However, there may be other underlying factors such as buyers expectations, foreign investors, present housing market condition and government policies that have not been fully explored or understood. This study will look at these variables and understand how they contribute to the housing bubble. Third, governments and central banks may take various measures to mitigate the risks of housing bubbles, such as increasing interest rates, tightening lending standards, or implementing housing market regulations. However, there is still debate about the effectiveness of these policies in preventing or mitigating housing bubbles. This study provides a better understanding on how government policies prevents and/or contribute to the housing model. Fourth, while housing bubbles have been observed in many countries, most of the existing research has focused on specific regions or countries such as developed countries and China. This study focuses more on a developing country (Malaysia) and explore the Malaysian housing market conditions and how the bubble may occur in the Malaysian connect.

Conceptual Framework

A housing bubble develops when home prices rise quickly and uncontrollably without being supported by the market’s underlying fundamentals, such as housing demand, buyers’ expectation, foreign investors, government policies, present housing market condition, and the economic growth outlook (Bangura & Lee, 2022; Erdmann, 2022; I. C. Tsai & Lin, 2022). Speculation, which is often to blame for this rise in house prices, is encouraged by easy access to credit, cheap interest rates, and liberal lending guidelines. The concept of supply and demand is the foundation of the notion of a housing bubble. Prices may rise because of the supply of available houses not keeping up with the growth in demand for housing (Bayer et al., 2021). More individuals are interested in investing in real estate as prices rise, which drives up prices even more. This cycle may go on until prices rise to an unsustainable level, which would cause the housing market to fall (Azam Khan et al., 2023; Yildirim et al., 2022).

Housing bubbles and economic outlook may be related. Housing prices may rise because of increased demand for homes brought on by economic development. A housing bubble might develop, however, if this rise in house costs is not supported by underlying economic factors like growing earnings and population expansion (Aizenman et al., 2019; Guerrón-Quintana et al., 2020). During a housing bubble, house values increase fast, generally spurred by speculation and easy access to financing. This may result in a situation where the price of real estate separates from its underlying worth. Finally, the bubble bursts, property values plummet, and an economic slump follows. As it occurred during the 2008 financial crisis, the bursting of a housing bubble may sometimes have a big effect on the whole economy. When house values dropped, many homeowners found themselves owed more than their properties were worth (Tajani et al., 2019; Yip et al., 2021).

Governmental policies may significantly affect the development and deflation of housing bubbles. Loose monetary policy is one of the main ways that government policies may cause housing bubbles to develop. It is simpler for consumers to borrow money to buy a property when interest rates are low (Dyussupzhanova, 2022; Yu, 2022). Housing prices may rise because of the increased demand, producing a bubble. Government initiatives that support or promote house ownership, such as tax benefits or low-down payment requirements, may also raise housing demand and fuel a bubble. A housing bubble may also be fueled by measures that make it simpler for individuals to get mortgages, such as lowering lending rules. On the other hand, government actions may also assist avoid housing bubbles or lessen their damage (Cargill & Pingle, 2019; Jang et al., 2020; Kim & Lee, 2019).

Expectations and speculations of buyers may play a role in the development of housing bubbles. Buyers may be more inclined to pay more for houses than they otherwise would be if they anticipate that housing prices will continue to climb quickly. As a result, prices may grow further as sellers raise their asking prices to capitalize on the strong demand for property. Several things, such as how the housing market is covered in the media, how other buyers and investors behave, and government policies that support or promote homeownership, may affect buyers’ expectations (Shi et al., 2020; Tang et al., 2021). Buyers may think that purchasing a house is a wise investment and be more ready to pay high prices if media coverage highlights the concept that housing prices would grow forever. Similarly, if other purchasers and investors are engaged in speculative activity, such as purchasing properties primarily to flip them soon for a profit, this may create a self-fulfilling prophesy where prices continue to increase. Moreover, tax benefits and minimal down payment requirements are two examples of government measures that support homeownership and may influence purchasers’ perceptions that house ownership is a wise and secure investment. When more buyers join the market and raise demand, this may lead to a cycle of escalating prices (Bao & Hommes, 2019; Yang & Rehm, 2021).

In especially in locations where there is a considerable demand from international purchasers, foreign investment may contribute to the development of housing bubbles. When foreign investors buy houses in significant quantities, they may raise demand and prices, starting a cycle of rising prices and further investor demand. Several variables, including as currency rates, tax laws, and political and economic stability, may have an impact on foreign investment (Ahmed et al., 2021; Tavares, 2019; Zhang, 2019). For instance, international investors may be more inclined to invest in a country’s housing market if its economy is doing well and its political climate is stable. Like this, international investors may find it more advantageous to buy property in a country if exchange rates are in their favor. Several nations also have regulations that support foreign investment in their housing markets (Sabrina Abdul Latif et al., 2020; Saiz, 2019; Wong et al., 2019).

Housing bubbles may develop and collapse depending on the state of the housing market. A cycle where prices grow quickly, and purchasers may be ready to pay more than a home’s actual worth might result from a strong housing market, high demand, and little supply. This may lead to the development of a housing bubble. Like this, a poor housing market that has excessive supply and little demand may result in a cycle of falling prices, negative equity for homeowners, and a possible bubble collapse (Ayan & Eken, 2021; Kim & Lee, 2019; Levitin & Wachter, 2020). Many variables, including as the state of the economy, interest rates, governmental regulations, and demographic changes, have an impact on the state of the housing market. A robust housing market may be influenced by a healthy economy with low unemployment and high-income growth. On the other hand, a poor housing market might result from a weak economy with high unemployment and slow income growth. Like this, low loan rates may facilitate house purchases, resulting in more demand and a more robust housing market (C. F. Chen & Chiang, 2021; Coskun & Pitros, 2022; Özdemir Sarı, 2019).

Hypothesis Developments

Studies have indicated that housing bubble occurrence is due to several macroeconomic and microeconomics factors. The housing bubble occurs when there is a sharp increase in housing prices, followed by a sharp decline. The increase/decrease of housing prices is due to the increase/decrease of the demand and supply of housing units. Several factors contribute to the demand for houses increase/decrease, such as interest and mortgage rate, money supply, and exchange rate (Cheong et al., 2019; Rui, 2015). Rui (2015), Dotti Sani and Acciai (2018) argue that low mortgage rates motivate people to buy houses as the installment payment would be cheaper, and therefore they can afford to pay it. This increases the demand for houses and leads the prices to go up. If housing prices increase to high levels, buyers likely would not be able to afford to purchase houses, especially for the M40 and B40. And therefore, there would be a risk of the prices dropping sharply, and we would most likely experience a housing bubble. Therefore we hypothesize that

H1: There is a positive relationship between housing demand and the housing bubble

In addition, buyers’ expectations and behaviors play a crucial role in determining the demand for housing and therefore determining the housing price. Studies have revealed that several factors influence people to decide whether to buy a house or not. These factors are the housing location, construction quality, price, facilities, neighborhood, and legality (Ariyawansa, 2009, 2010). In Malaysia, the location and site of the house are one of the major factors influencing buyers’ intention to buy a house. Malaysian prefer to buy houses in big cities where most necessary facilities are available such as Train stations, Hospitals, Schools, and Shopping centers. This again led to the increasing demand for houses located in such environments, and therefore, this led to an increase in house prices (Ab-Majid et al., 2017; Baqutaya et al., 2016; Hou, 2017; Hulse & Reynolds, 2018; Khan et al., 2017; Liao et al., 2015; Wan Rodi et al., 2019). The significant increase in demand encourages developers to build more houses to maximize their profit. If supply surpasses demand, there will be a huge surplus in the market. This again will lead to a decrease in the prices. A sign of a housing bubble could appear. Thus we hypothesize that:

H2: Buyers’ expectation has a positive impact on the housing bubble

Housing demand and prices also are directly affected by foreign investors/buyers. Masron and Fereidouni (2012), Masron and Nor (2016) have revealed that investors and foreign buyers are not only interested in owning houses, but their main intention is to invest their capital in a profitable housing market. The increased demand for houses due to foreign investment will increase housing prices. Some studies have revealed that relaxing restrictions on foreign investors investing in the housing market could lead to a housing bubble (Liao et al., 2015; Wan, 2018; Wetzstein, 2017). This is because developers found it profitable to build high-class houses to sell to foreigners. Developers will compete to rip off the foreigners’ market share as much as possible. This will probably increase the high-end housing units in the market and the unsold units as the market may reach saturation level for foreign investment in housing. This scenario may again lead the prices to drop, signaling the housing bubble’s beginning. Therefore we hypothesize that

H3: There is a positive relationship between foreign investor buyers and the housing bubble

The expansion of the housing market and its performance significantly contribute to housing price determination. An increase in the buyers’ purchasing power ultimately expands the housing market, and thus the construction firm’s value will increase in the stock market. This will motivate more buyers to invest in real estate and buy more houses, increasing housing prices (Cheong et al., 2019). Again, an increase in construction firms’ value in the stock market also may lead developers to increase the housing supply due to the high margin of profit these firms generate. If the housing supply increase in such a way that surpasses the demand, then there will be many unsold units in the market, and again this could reverse the relationship (Adi Maimun et al., 2018; Glaeser et al., 2008; Khan et al., 2017; Nobili & Zollino, 2017; Wan Rodi et al., 2019). Another important aspect to notice is that market performance (condition) also could be a better moderator between buyers’ expectations, foreign investors, and housing prices. If housing demand is reduced due to higher prices (M40 and B40 cannot afford to buy houses at this price level), this could be corrected if the housing market performed well. A good performance of the housing market encourage investors (local and foreigners) to invest in real estate, and therefore the demand for the housing market increase again. Buyers’ and investors’ expectations will be strengthened as they expect higher profits in investing in real estate. There we hypothesize that:

H4a: Market condition (performance) has a positive impact on the housing bubble

H4b: Market conditions moderate the relationship between IVs (housing demand, buyers’ expectations, foreign investors) and the housing bubble

Economic growth probably is one of the most important factors in determining housing prices. It is well understood that economic growth translated into an increase in the population’s real income. As people’s average income increases, their affordability to buy houses increases. This motivates many to buy their first home and invest in the real estate market. Also, continuous positive economic growth would benefit companies in all sectors. Business boosts, and then many opportunities will be available to people in the job market (Coskun & Jadevicius, 2017; Holt, 2009; Said & Majid, 2014; Tokic, 2008; Yunus et al., 2012). Investment companies would also be encouraged to invest in the real estate market following the positive trend in the housing market. All of this will contribute to the increase in the housing demand, and therefore housing prices will rise to the highest level (Cheong et al., 2019; Hashim, 2010). This scenario again leads existing construction companies to increase their housing supply. Their capacity to build more houses increases as they can borrow more from banks and other financial institutions due to their stable financial situations. Developers continue to supply more houses until where the supply surpasses the demand. In this case, there will be an oversupply of houses in the market, which could lead to a sharp decline in housing prices and signal a possible housing bubble. In addition, economic growth also can play a significant role in strengthening the link between buyers’ expectations, foreign investments, and housing prices. A progressive, positive economic growth encourages investment in real estate. If the demand for housing is reduced due to low expectations and less foreign investment, this could be strengthened again if the country achieves higher economic growth. With sustained economic growth, buyers and investors build higher housing market expectations. This will significantly increase the demand for houses. There we hypothesize that:

H5a: Economic growth outlook has a positive impact on the housing bubble

H5b: Economic growth outlook moderate the relationship between IVs (housing demand, buyers’ expectation, foreign investors) and the housing bubble

The government may interfere in the housing market in policymakers notice that the housing market is not stable. The Malaysian government has designed various policies to stabilize the housing market. Again, sometimes enforcing too many regulations would make the housing market vulnerable (Zainun et al., 2013; Ab-Majid et al., 2017; Adi Maimun et al., 2018; Ariyawansa, 2009; Baqutaya et al., 2016; Cheong et al., 2019; Joebges et al., 2015; Stohldreier, 2012). Removing or reducing regulations that may hinder buyers’ ability to purchase houses could significantly help the housing market to expand. Some of the policies that government should consider avoiding are high mortgage rates and reducing the direct involvement of government agencies in building low-cost homes. If low-cost houses are not enough in the market for the B40 category, they may be forced to buy more expensive houses. This may lead to a total collapse of the financial system as those buyers will not be able to service their loans. This is what happened in the US housing bubble in 2001. We should notice that policies for low-cost housing should be carefully tailored and designed as this could significantly contribute to the decrease in house prices, leading to a possible housing bubble. This study further argues that government policies play an important role in moderating the link between housing demand and the housing bubble. If housing demand decreases due to buyers’ expectations and foreign investment, government policies should be placed to weaken that effect. Pro-housing growth policies increase buyers’ confidence and build a higher expectation among local and foreign buyers to purchase and invest in real estate. This would ultimately increase the demand for houses and thus strengthens the link between buyer expectations, foreign investment, and housing prices. There we hypothesize that:

H6a: Government policies have a positive impact on the housing bubble

H6b: Government policies moderate the relationship between IVs (housing demand, buyers’ expectation, foreign investors) and the housing bubble

Methodology

Sample Selection Procedure

We explore several unique factors in the respective survey to calculate the appropriate sample size. This approach rests on the authors’ initiative to initiate the decision regarding several unique factors. Consistent with extant research, the three most essential factors are the degree of confidence or risk, precision level, and the variability level in the measured attributes (Miaoulis & Michener, 1976). Therefore, we employ Krejcie and Morgan (1970) established formula to determine the sampling size for our study.

S = required sample size;

N = the population size;

d = the degree of accuracy or the level of precision expressed as a proportion (0.05);

X2 = the table value of chi-square for one degree of freedom at 95% confidence level (X2 = 1.962 = 3.841); and P = the population proportion or the degree of variability (assumed to be 0.50 since this would provide the maximum sample size)

Congruent with the above formula, the projected sample size mirrors a total of 384.

Research Method and Instrument

A positivist research method has been employed in this study. The positivist research is debated to mirror a type of quantitative data application and analysis and it is relevant for aiding researchers obtain objective insights via distinct avenues of scientific enquiry, such as the use of surveys, experiments and others (Y. Y. Chen et al., 2011; Schmierback, 2005). In this present study, the use of the quantitative research method would help to identify core housing bubble predictors and empirically investigate a novel model for detecting housing bubbles in Malaysia. By probing to obtain objective insights, new knowledge can be engendered based on the extraction and further statistical analysis of real-time opinions of market players about housing bubble formation and collapse. Consequently, the use of the quantitative technique of inquiry is used in this study, considering the rich opportunity to deploy statistical techniques that are key to unveil specific and objective insights (Gray, 2014; Mack, 2010).

This study employed questionnaires to investigate the determinants of the housing bubble in Malaysia. The questionnaire has been prepared in Bahasa Melayu, Chinese, and English. The questionnaire has been structured into seven sections. Section 1 relates to the “respondent’s profile.” Section 2 highlights “housing prices and demand” information. Section 3 elicits information on “house buyers' opinion of the current housing market scenario.”“Present housing market conditions” is addressed in Section 4. Section 5 addresses “government policies.” Section 6 deals with “foreign investors/buyers,” and “economic growth outlook” is examined in Section 7. The questionnaire is structured on a 5-point Likert scale ranging from strongly agree to disagree.

Population, Sample Size and Data Collection

Due to a cross-sectional study, data has been obtained from a one-round survey. Data originated from four Malaysian regions, which are known as the East coast region (Kelantan, Terengganu, and Pahang) region, the Southern region (Malacca and Johor), the Central region (Kuala Lumpur, Selangor, and Negeri Sembilan), and Northern region (Kedah, Penang, Perak, and Perlis). This study’s population comprises professional and nonprofessional individuals from the housing industry. To foster the obtaining of a stratified proportionate sampling of participants in this study, the Krejcie and Morgan (1970) determinant of sample size was employed. A total of 500 questionnaires were distributed, and only 382 questionnaires were collected from the respondents and also found useful for further statistical analysis. This outcome indicated a response rate of 76%.

The authors have handled the questionnaire distribution and collation processes. The authors ensured to be present all through the data collection and collation phase to provide further informed knowledge that can guide respondents in answering their respective questionnaires appropriately and adequately. To facilitate data accuracy and bias minimization, questionnaires were distributed to respondents and complimented by face-to-face interactions via local dialects. This helped to dispel possible issues of misunderstanding or miscommunication regarding the questions.

Ethical Consideration

This research has considered the ethical guidelines of doing surveys (Punch, 1998). The researchers have assured verbally to the respondents that their information will be kept confidential. Respondents have also been notified verbally that their participation is voluntary and that they may withdraw from participating in this research at any time without informing us. The researchers have verbally explained clearly the motive of the research to the respondents as well as guided the respondents on how to answer the questionnaire.

Additionally, the study considers the following to ensure that participants’ information is protected and their well-being is prioritized:

Limiting the Risk of Harm to Human Subjects: The study design focuses on collecting non-sensitive data related to housing market opinions, ensuring confidentiality through anonymized responses. Participants were informed of their right to withdraw at any time, which further reduces the risk of any potential harm.

Balancing Potential Benefits and Risks: The research aims to provide valuable insights into housing bubble predictors in Asian emerging economies, offering significant societal benefits such as informed policy-making and economic stability. The minimal risk to participants is greatly outweighed by these potential benefits, both to society and to the participants, who contribute to a greater understanding of market dynamics.

Obtaining Informed Consent: Informed consent was obtained verbally from all participants. Researchers clearly explained the study’s purpose, the voluntary nature of participation, the confidentiality of responses, and the right to withdraw at any time without consequence. This process ensured that participants were fully aware and agreed to the terms before participating.

Pilot Study and Questionnaire Reliability

A pilot test was done in Selangor state to ensure that all questionnaire items were well designed and constructed. Sixty random respondents were approached, and then data was collected. The initial results of Granbach’s Alpha value were very high (.864), indicating that the questionnaire items are all reliable. Most social science research uses an alpha level usually above or equal to .70 (Eisinga et al., 2013).

Questionnaire Validity

The study’s questionnaire was developed based on previous studies. Some items of the questionnaire were self-developed. This was important to more efficiently tap into the minds of participants and the questions were carefully structured to help them accurately share their own unbiased but objective opinions. To ensure the face and content validity of the instruments, our study thus, followed the position and debates of prior research (Y. Y. Chen et al., 2011; Cohen, Manion & Marion, 2002; Ogbeibu et al., 2018; Schmierback, 2005). We ensured experts’ opinions were solicited, and the questionnaire was examined by two experts on housing bubbles and one research methodology expert. The three experts examined the context and face validity of the measures employed in the instruments in the Malaysian, English, and Chinese languages. In light of their constructive feedback, the instruments were revised accordingly. Furthermore, this approach has helped to ensure the measurement items maintains very clear meaning in light of their respective constructs and that the results of the utilizing the measures are stable on conditions where stability is needed (Cohen et al., 2002; Trochim, 2006).

Empirical Findings and Discussion

A section of Table 2 shows the descriptive statistics, which highlight standard deviation (SD) and mean results. The mean results indicate that majority of the respondents disagree that economic growth outlook impact housing bubbles, compared to a majority who agree that buyers’ expectations impact housing bubbles. Likewise, the SD results are relatively close, suggesting less disparity between constructs. Hence, this indicates the normal data distribution, considering their even dispersion.

Sampling Design, Summary of Descriptive Statistics and Reliability and Validity of Measurement Model.

Note. Sample (N). CR = composite reliability; AVE = average variance extracted; VIF = variance inflation factor; QD = questionnaires distributed; QR = questionnaires returned.

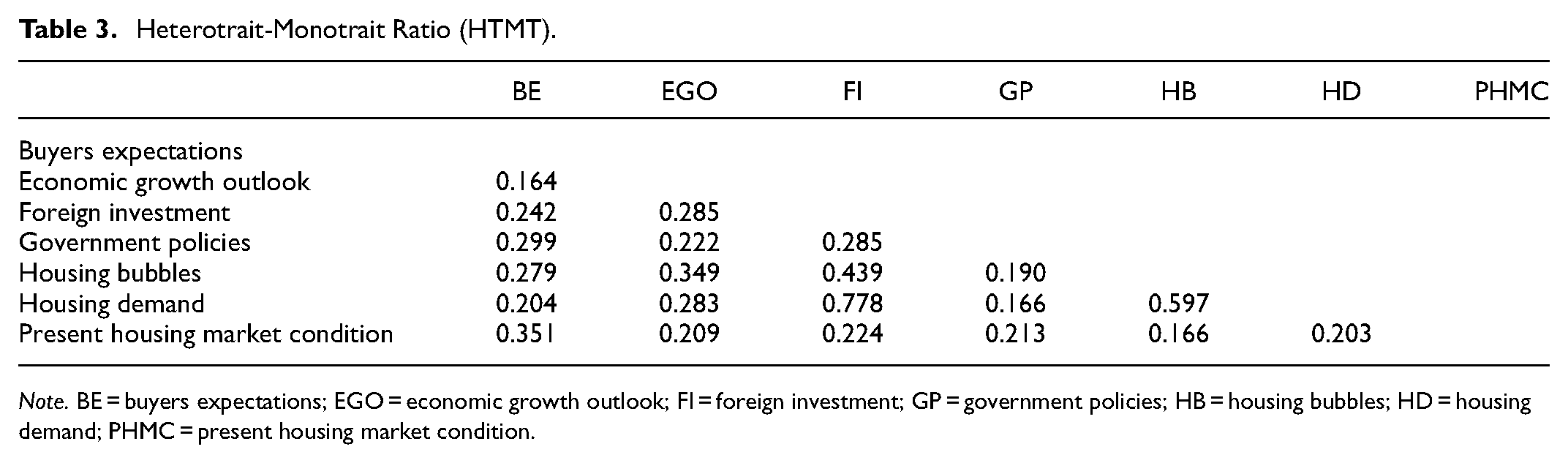

The measurement model is a point of departure (see Figure 3). Figure 3 shows that all the indicator items exceed 0.6, which is above the minimum of 0.5 (Awang, 2015; Hair et al., 2010). This indicates that all indicator items contribute strongly to their respective constructs. Likewise, Table 2 suggests that values for composite reliability (0.84–0.91) and the RhoA (0.84–0.93) confirm the internal consistency and reliability of all respective constructs (Henseler, 2017). Values for average variance extracted (AVE) suggest constructs’ convergent validity as all the values are above the minimum of 0.5 (Ringle et al., 2020). Also, the variance inflation factor (VIF) results confirm the measurement model’s construct validity due to a lack of multicollinearity (Ogbeibu et al., 2018). Equally, the Heterotrait-Monotrait Ratio (HTMT) has been espoused by Henseler (2017) as a higher boundary criterion for assessing the construct’s discriminant validity. Thus, Table 3 confirms this model’s constructs discriminant validity since all the values are lower than 0.850. It further suggests that all the constructs are independent (Henseler, 2017). Additionally, studies (Henseler, 2017; Nitzl et al., 2016) advocate that the standardized root mean square residual (SRMR) is currently the global goodness of fit measure for PLS path models. Thus, values 0.08 and below suggest that a model fits well (Hu & Bentler, 1999). Consequently, the SRMR value (0.053) of this study’s measurement (saturated) model is validated as a good fit.

Measurement model.

Heterotrait-Monotrait Ratio (HTMT).

Note. BE = buyers expectations; EGO = economic growth outlook; FI = foreign investment; GP = government policies; HB = housing bubbles; HD = housing demand; PHMC = present housing market condition.

Since the measurement model has fulfilled all the requirements of ascertaining a good fit, the structural model is consequently examined to determine the path models’ predictive relevance and significance. This includes estimating several measures such as the statistical significance, Q2,

Results of Figure 4 indicate that housing demand has the strongest positive and significant (

Structural model with t-statistics results.

Similarly, results from Figure 4 show that the economic growth outlook has the second strongest and most significant (

Figure 4 also highlights that foreign investment has the strongest negative (

The study conceptual framework.

Given the results in Figure 4, the present housing market condition is also exemplified to exercise no statistical significance (

Moreover, this study shows that buyers’ expectations have a significant positive (

Table 4 shows that economic growth outlook has no significant moderating effect on the impact of buyers’ expectations (

Moderating Effect.

Note. EGO = economic growth outlook; GP = government policies; PHMC = present housing market condition.

Equally, Table 4 indicates that government policies has no significant moderating effect on the impact of buyers’ expectations (

Furthermore, Table 4 reflect that present housing market condition has no significant moderating effect on the impact of buyers’ expectation (

Consequently, in the face of a price boom, banks and households are very likely to sign large mortgage contracts (Agnello et al., 2018). Nevertheless, in the event of a price bust, collaterals may likely be exceeded by loan value, which can generate instability for the economy’s financial system (Leszczyński & Olszewski, 2017; Li & Xu, 2016). In this wise, an unstable housing market condition may mirror strong delimiting effects on buyers’ expectations, housing demands, and foreign investments (Coskun & Jadevicius, 2017; I. C. Tsai, 2015; Wang, 2018). Exuberant individuals are, thus, very likely to become dissuaded from investing in the property markets (Holt, 2009; Hulse & Reynolds, 2018). It is also likely that this result may indicate that Malaysia presently has an unstable market condition. This, therefore, requires grave attention by Malaysian government policymakers to initiate a positive review of the property market’s economy.

Moreover, as an approach to further compliment this study’s overall model’s predictive relevance, the Q2 (0.226) result indicates that the predictive accuracy of housing bubbles as an endogenous construct in this study’s path model is acceptable. Additionally, the SRMR result of

Conclusion

The Malaysian economy has experienced several shifts over the years, partly due to constant fluctuations in the housing bubble. To pre-empt the housing bubble fluctuations, this study has developed a model procedure for housing bubble detection. This study’s results are of major importance as they would assist the Malaysian government in ascertaining probable housing bubble fluctuations by quickly exploring this study’s established predictors of the housing bubble phenomenon in the Malaysian housing market. Three major housing bubble detectors have been established in this study. Although quite unexpected, we find that only housing demand, economic growth outlook, and buyers’ expectations are significant predictors of the housing bubble. This indicates that the present housing market condition, foreign investment, and government policies are not housing bubble detectors as they are not significant predictors in our study.

In Malaysia, housing costs have significantly increased in recent years, especially in metropolitan areas. Many causes, such as quick economic expansion, low interest rates, and an expanding population, have contributed to this. As a result, more people are in need of homes, especially middle-class families and young professionals. A housing bubble may develop, though, if the demand for property is predominantly driven by speculators and investors rather than by individuals who truly wish to live there. This is due to the fact that rising prices as a result of rising demand spur greater speculation and investment, which raises prices even more. As the bubble eventually collapses, many investors and homeowners suffered considerable losses. In order to prevent the emergence of housing bubbles, it is crucial to make sure that real demand for housing is generated by individuals who truly want to live in the homes, as opposed to speculation and investment. This can be accomplished in a number of ways, such as making sure that there is an adequate supply of housing to meet demand, encouraging policies that encourage homeownership among those who actually want to live in the homes, and controlling the housing market to prevent excessive speculation and investment.

Moreover, we also found that the economic growth outlook has no significant moderating effect on the impact of buyers’ expectations, foreign investment, and housing demand on the detection of housing bubbles, respectively. Equally, government policies have no significant moderating effect on buyers’ expectations, foreign investment, and housing demand’s capability to predict housing bubbles. Further, we show evidence that the present housing market condition has no significant moderating effect on the impact of buyers’ expectations, foreign investment, and housing demand on housing bubbles. Consequently, the government should roll out suitable housing planning and policies especially during the period of high economic growth outlook that provide for the majority of the population as concentrating on affordable housing can reduce housing demand stress.

Policy Implication

Policy Implication

This study underpins previous theoretical positions by demonstrating that housing demand relays the strongest predictive and positive capability on the housing bubble. Therefore, policymakers should consider instituting policies that can guide stable rates of housing prices to maintain a continuous stream of demand by housing buyers. More strategies should be set in place to ensure an increase in housing buyers’ needs is satisfied to foster continued housing demand. Since foreign investment is not significant in predicting housing bubble, policies to control foreign investment such as price floor may not help in mitigating housing bubble Policymakers may also want to consider drafting initiatives tailored toward the provision of sufficient budget allocation that can foster the supply of more housing properties to tackle the problems of home ownership and availability to most of the public in light of the positive impact of housing demand especially in major urban areas. The policymaker should consider providing incentives for the developers to build more affordable housing. Likewise, since we show that the economic growth outlook is also a positive predictor of the housing bubble, policymakers need to institutionalize programs relevant to exploring and monitoring the economic growth condition of property markets. It is important to consider mitigating probable housing price shocks and bubble bursts by investigating the economic growth of the property markets. Consequently, control agencies could be set up to execute adequate monitoring of the housing price fluctuations and the rate of change in impact on the housing bubble. The government should also strengthen the advocacy against buyers’ expectations that predicting the housing bubble as the purchase of housing asset should provide for own staying instead of speculation.

Practical Implication

We complement prior insights by exemplifying buyers’ expectations positively impact the housing bubble. By ensuring that policies enforced in the property markets also benefit housing property buyers, policymakers may be able to detect the housing bubble much faster. Although this approach keeps policymakers in control, control could be deployed in ways that ensure that housing buyers’ concerns and expectations are met or exceeded. Given the results of this study, we advocate that policymakers may endeavor to redirect huge funds or higher focus from government policies, present housing market conditions, and foreign investments to more targeted and significant housing bubble detectors. This is because this study found that they exact no significant impact on the housing bubble and are, thus, not relevant housing bubble detectors. Instead, the major focus should be on the further development of significant housing bubble detectors like housing demand, economic growth outlook, and buyers’ expectations.

Limitations and Recommendations

We employed a cross-sectional research design in this study to obtain our findings. This might have indirectly suppressed more robust findings, which may have been otherwise obtained in the case of a longitudinal study. We implore other researchers to extend our findings by initiating and investigating longitudinal research. Likewise, we acknowledge that despite our applications of several approaches to deepen the insights into housing bubble detection, we have also obtained several insignificant results. We, therefore, call on extant research to replicate our model procedure for bubble detection across the Malaysian property markets and in other nations. This could aid foster comparability and generalizability of this study’s results across a wider context. To promote methodological validity and further results reliability, we advocate that future researchers should test our implied model across a range of other qualitative and quantitative methods. Future investigations could integrate more variables into our models should this study’s aims be extended and replicated across the Malaysian context.

In addition, housing bubbles can have differential impacts on different socioeconomic groups. For example, those who own homes during a bubble may experience significant wealth gains, while those who do not may face higher housing costs or exclusion from homeownership altogether. More research could be done to examine the distributional effects of housing bubbles.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by the Ministry of Higher Education, Malaysia, through the FRGS research grant reference FRGS/1/2016/SS08/UTAR/02/2)

Ethical approval

Informed consent was obtained verbally before participation. The consent was audio-recorded in the presence of an independent witness.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.