Abstract

China’s cross-border mergers and acquisitions (M&A) activities have shown a remarkable increase during the past few decades of rapid economic growth. This paper proposes that the development of High-Speed Railway (HSR) serves as a key factor driving the surge in cross-city M&A activities. Using the staggered differences-in-differences (DID) model, we find that HSR services significantly promote cross-region M&A activities by reducing information asymmetry. Specifically, the results show that the introduction of HSR services leads to a 43.7% increase in cross-region M&A activities in HSR cities. This study provides practical recommendations to enhance capital allocation efficiency in developing economies.

Plain language summary

In recent decades, China has seen a huge rise in companies buying or merging with other companies across different regions. This paper explores how High-Speed Rail (HSR) has contributed to this increase. We found that HSR plays a major role in boosting these cross-region business deals by making information about companies more accessible and reducing confusion. Specifically, our findings show that adding HSR services has led to a 43.7% rise in such business activities in cities with HSR. Our study offers practical advice on how to improve the efficiency of investments in developing economies.

Keywords

Introduction

Merger and acquisition (M&A) is a significant device for capital allocation between regions, which theoretically can not only reshape individual production units’ performance, but also account for aggregate productivity growth (Bartelsman et al., 2013; Braguinsky et al., 2015; David, 2021). Exploring the determinants of M&A has been a prominent field in economic and financial studies for decades (D. Chen et al., 2022; Hyun & Kim, 2010; Pablo, 2009; Rossi & Volpin, 2004; Stahl & Voigt, 2008; B. Yang et al., 2019). Compared to developed countries, China’s financial system is still underdeveloped, and capital misallocation is widespread in the economic growth process. In the past decades, China has experienced a stunning increase in M&A activities, which have facilitated improvements in the quality of economic growth (Heater et al., 2021; Liu et al., 2017). Thirty years ago, there were only 214 M&A deals with a total value of 8.6 billion U.S. dollars in mainland China. By 2016, the M&A volumes reached 8,065 deals worth $757.06 billion U.S. dollars, while expenditures on M&A from 2014 to 2016 averaged about 5.5% of GDP. The rapid development of M&A in China has prompted scholars to explore the stories behind the phenomenon. However, so far, academia has shed limited light on Chinese M&A activities (Ahlstrom et al., 2014; Lebedev et al., 2015; Zhu & Zhu, 2016).

Along with the phenomenal increase in M&A activities, China’s transport infrastructure has been in a mode of rapid development. We hypothesize there might be a relationship between the development of transport infrastructure and M&A activities. In fact, this topic is closely related to the “home bias” issue in M&A literature. It is a preference of acquirers to select target companies that are geographically close or located in the same country or region during M&A, which is well observed across various countries. One of the main reasons why bidder firms prefer local target firms is that the transaction costs of searching and processing information in M&A deals increase with geographic distance (Coval & Moskowitz, 2001; Ellwanger & Boschma, 2015; Sun et al., 2021). With the development of globalization, digitalization, and information communication technology (ICT), some scholars assert that spatial distance plays a negligible role in economic activities (Cairncross, 1997; Tranos & Nijkamp, 2013). However, this view has long been questioned in academia and practice (Ragozzino, 2009; Takhteyev et al., 2012). Contrary to this view, Goldenberg and Levy (2009) even argue that the friction of spatial distance on economic activities has increased with the ICT revolution. In recent years, the development of HSR, which does not reduce geographical distance between cities, has greatly reshaped the economic geography of China (Baum-Snow et al., 2017; Diao, 2018; Zheng & Kahn, 2013). By decreasing travel time between interconnected cities, HSR has significant potential to reduce the transaction costs associated with information search and processing in M&A, thereby further facilitating cross-city M&A activities.

Cross-city merger and acquisition is an economic activity with high uncertainty. Both acquiring and target firms engage in frequent offline communication to mitigate this uncertainty Bathelt and Henn (2021). As the geographical distance between the parties increases, M&A uncertainty intensifies. Insufficient information exchange or distorted information leads to significant information asymmetry, resulting in M&A transaction failures (Uysal et al., 2008). Cross-city M&A involves multiple stages, including research, valuation, negotiation, adjustment, contract signing, and execution. These stages require obtaining both hard information (such as financial data, product details, company bylaws, external ratings, business plans, and loan guarantees) and soft information (such as founder characteristics, corporate culture, social capital, and management traits). Moreover, acquirers often rely on face-to-face interactions to uncover concealed soft information about the target firm (e.g., legal disputes, organizational culture, employee quality, government support, or contingent liabilities).

The geographical distance limits the information exchange between the two sides of an M&A transaction. Cai et al. (2016) highlighted that transportation infrastructure development can mitigate the negative impact of geographical distance on information interaction. HSR improves connectivity and accessibility between cities, and compresses the geographical distance between enterprises in the time dimension. Building on this foundation, HSR promotes on-site visits by managers from both acquiring and target firms, facilitating face-to-face communication between them. During due diligence, HSR enables acquirers to conduct more detailed on-site inspections of the target firm, enhancing the depth and breadth of their information acquisition. The advent of HSR strengthens acquirers’ supervision of the target firm through on-site visits, which effectively reduces monitoring costs. Overall, the establishment of HSR networks enhances regional accessibility, reduces the time cost of face-to-face interactions, and mitigates information asymmetry across regions. Consequently, HSR could significantly lower transaction costs in cross-city M&As and facilitate cross-region M&A transactions.

We collect all cross-region M&A cases from 2000 to 2016, where participants could be either listed firms or not. Geographic proximity has been used as a proxy for information asymmetry in earlier empirical M&A studies (Cai et al., 2016; Kang & Kim, 2008; Uysal et al., 2008). However, this indicator is time-invariant and closely related to other distance-related confounding factors in M&A transactions. As we analyzed above, this proxy does not effectively isolate the role of information asymmetry. We propose that the opening of HSR services is a good proxy for measuring the impact of information asymmetry on M&A transactions, because HSR services can decrease information asymmetry among cities with HSR access and are not correlated with confounding factors. The opening times for HSR services in different cities vary, so this paper uses the staggered DID method to isolate the role of information asymmetry in M&A transactions.

Our empirical results show that HSR services significantly boost cross-region M&A activities in China. Specifically, we found that a city’s cross-region M&A activities increased by 43.7% after it was connected to the HSR network. For a city pair, the number of M&A deals between them increased by 5.1% after they were interconnected by HSR lines. In addition, we observe that following the opening of HSR services in a city, the number of M&A deals where local firms target outside firms increased by 39.1%, while the number of M&A deals where firms are targeted by non-local bidders increased by 29.6%. The baseline results remain stable after accounting for potential systematic differences between HSR cities and non-HSR cities. We also conducted a test of parallel trends in pre-treatment periods to ensure the internal validity of the staggered DID analyses. The results of the parallel trend hypothesis are consistent with descriptive evidence. That is, in the absence of HSR services, the difference in cross-region M&A activities between HSR cities and non-HSR cities is small over time. Whereas the number of cross-region M&A transactions in HSR cities significantly outnumbers that in non-HSR cities 2 years after the opening of HSR services. Placebo tests confirm that the surge in cross-region M&A deals occurs between HSR cities, rather than between HSR cities and non-HSR cities, and is not the result of random events.

The results of instrumental variable (IV) regression show a strong causal relationship between HSR services and cross-regional M&A activities. Additionally, we find that the impact of HSR services diminishes with increasing distance between cities and is more pronounced for adjacent cities and cities within the same province after they are interconnected by HSR lines. Using multiple variables as proxies for information asymmetry, the mechanism tests indicate that HSR exerts positive impacts on cross-region M&A activities by alleviating information asymmetry.

M&A research typically focuses on large-scale transactions or those involving publicly traded companies. As a result, a large number of M&A deals (e.g., deals involving private bidders or targets, small targets, or deals without a deal value) are excluded from most M&A studies due to insufficient data for analysis. Netter et al. (2011) conclude that common data used in M&A studies oversample larger deals and deals involving only public firms, leading some inferences in prior research to be incomplete and misleading. For instance, they find that when the sample is limited to large listed companies acquiring other large listed companies, the acquirer’s announced return rate is negative, whereas in larger samples, the return is positive and significant.

Our study contributes to two broad strands of literature. First, existing M&A research has revealed the significant negative role of geographical distance in M&A activities, while few studies have examined the factors that either exacerbate or mitigate the impact of geographic proximity in M&A transactions, with the exception of two studies. Ascani (2018) recently showed that bidders in cross-border M&As can offset information disadvantages by selectively acquiring targets based on their profitability. Similarly, Chakrabarti and Mitchell (2013) found that firms can partially overcome distance constraints through direct, contextual, and vicarious learning. We complement this literature by exploring whether HSR can promote inter-city M&A activities by reducing spatial and temporal distances between cities.

Besides, prior M&A research typically focuses on large-scale transactions or those involving only publicly traded companies. However, listed companies account for only a very small proportion of all M&A deals (Erel et al., 2012; Netter et al., 2011), which inadvertently creates a heavily biased sample of M&A deals. For instance, scholars find that when the sample is limited to large listed companies acquiring other large listed companies, the acquirer’s announced return rate is negative, whereas in larger samples, the return is positive and significant. This paper adds new and robust evidence to M&A research by incorporating data from both private and public firms.

The literature suggests that the role of geographic proximity in M&A transactions is related to information asymmetry. However, geographic proximity is also intertwined with other factors related to distance, such as cultural proximity, linguistic proximity, and institutional proximity. Isolating the effect of information asymmetry from these other factors is challenging. We explore the impact of information asymmetry on cross-region M&A activities by leveraging variations in the opening times of HSR services and employing a staggered difference-in-differences model. The opening of HSR services can potentially reduce information asymmetry between regions while having a minimal impact on other factors related to geographic proximity.

Second, this paper enriches the literature on the various economic impacts of HSR services. Extant studies mainly evaluate the effects of HSR on competition between transport modes, regional innovation capacity and technological productivity, the tourism market, and the real estate market (Albalate & Fageda, 2016; Coppola et al., 2020; Zheng & Kahn, 2013), as well as employment (Duranton & Turner, 2012), economic development, and urban expansion (Diao, 2018; Long et al., 2018). Few studies have explored the impact of HSR on capital reallocation from the perspective of M&A activities. Our study highlights the role of developing transportation infrastructure in boosting the efficiency of capital allocation.

The rest of the paper is organized as follows: Section 2 provides the background for our study. Section 3 reviews related literature and develops hypotheses. Section 4 discusses the sample selection procedure and empirical design. Section 5 presents the empirical results. Section 6 concludes.

Background

The expansion of the HSR network marks a historic revolution in the Chinese trans-regional transportation system. HSR is considered one of the most significant breakthroughs in transport technology in the second half of the 20th century (Campos & de Rus, 2009), making substantial progress in areas such as speed, comfort, and punctuality (Ureña et al., 2009). In the first two decades of the 21st century, China rapidly developed the largest-scale HSR network in the world. By 2017, China’s HSR network had a running mileage of 22,000 km, connecting 188 out of 292 Chinese cities. The large-scale HSR network in China operates over 4,000 pairs of high-speed trains each day, becoming a mature transportation system widely accepted by the general public. Given its substantial improvement in city accessibility, many studies find that passenger traffic between cities increases significantly after the introduction of HSR services (Vickerman, 2018). To date, the China Rail High-Speed (CRH) train service has transported more than 10 billion passengers, with a total passenger turnover of over 3.34 trillion passenger kilometers, both ranking first in the world.

According to passenger onboard surveys, more frequent trips by both repeat and new customers account for the growth in overall trip-making with HSR services (Lawrence et al., 2019). HSR services attract business and leisure travelers, and onboard surveys reveal that business trips typically make up between 40 and 60 percent of total travelers (Lawrence et al., 2019). The induced growth in cross-region trips through HSR services is thought to reduce the negative effect of physical distance on cross-regional information asymmetry. Recent studies suggest HSR services enable more frequent site visits and face-to-face interactions between HSR cities (D. Chen et al., 2022; Dong et al., 2020; Wang et al., 2022; Xiong et al., 2021; Xu, 2019), thereby reducing information asymmetry. Essentially, information-sensitive professionals (such as monitors, top managers, senior auditors, innovators, fund managers, and scientists) far from their focal firms now experience reduced travel time and enhanced travel time reliability with the opening of HSR services between HSR cities. M&A transactions involve a large amount of information-based synergies, which especially rely on soft-information production and transmission (Coff, 1999; Kang & Kim, 2008; Uysal et al., 2008). Unlike hard information, which is tangible and can be easily coded, verified, transmitted, and interpreted, soft information is difficult to codify, identify, and transfer over distance. Examples of soft information include the value of intellectual assets, corporate culture, managerial skills, moods, and feelings about the future. The importance of soft information transmission demands intensive face-to-face interactions between acquirers and targets in social, civic, and business contexts. This feature of soft information highlights the role of accessibility between the acquirer and the target in an M&A transaction, enhancing information-based synergies. Therefore, these arguments suggest that we should see more M&A transactions between HSR cities after the opening of HSR services in China.

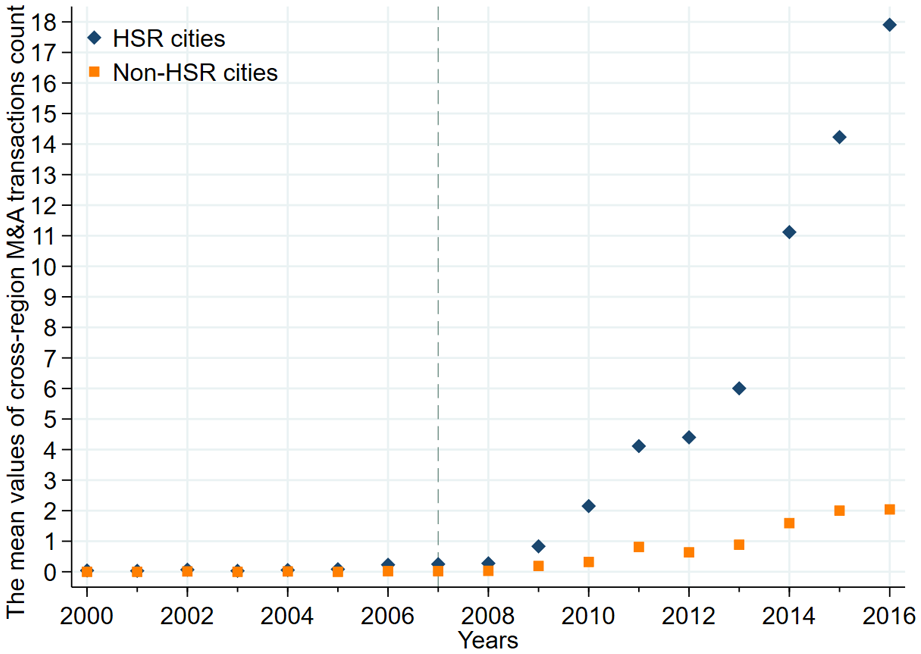

In 1991, there were only 214 M&A deals with a value of 8.6 billion dollars in mainland China. Over the past few decades, China’s M&A market has experienced a notable expansion both in number and scale. In 2016, the M&A volume in mainland China surged to a new record of 8,065 deals worth $757.06 billion. However, most M&A cases tend to be localized (e.g., confined within a province, county, or city) rather than cross-regional due to a variety of reasons (Wei & Boyreau-Debray, 2004). As described by Qian and Xu (1993), China can be treated as a case of de facto federalism where each region is considered an autonomous economic entity. Specifically, China has marked regional differences in many aspects, such as economic growth, industrial structure, policy formulation, local languages, and cultural norms. In addition, the long distances between regions present barriers to cross-region interactions and travel, leading to information asymmetry. Information asymmetry makes it difficult for cross-region M&A to be successful. In this context, has the development of HSR systems in China facilitated cross-region M&A activities? Our data (see Figure 1) show that before 2008, when HSR services made their debut in China, there were few and slowly increasing cross-region M&A transactions. However, the number of cross-region M&A transactions began rapidly increasing after 2008 and exceeded 1,500 by 2016. The dramatic shift in the growth pattern of cross-regional M&A deals in China suggests that high-speed transportation could potentially alleviate information asymmetry between regions.

The trends of M&A cases in HSR cities and non-HSR cities.

Related Literature and Hypothesis Development

The Role of Spatial Distance in Financial Activities

The finance literature has documented that spatial distance matters in a range of business activities. Evidence shows that firms and private investors prefer nearby investments over remote ones due to better information availability (Cashman & Deli, 2009; Coval & Moskowitz, 2001; Dvořák, 2005; Hau, 2001; Ivković & Weisbenner, 2005; Malloy, 2005; Massa & Simonov, 2006; Teo, 2009). For instance, Coval and Moskowitz (2001) find that US mutual funds strongly prefer local stocks to remote stocks, generating higher abnormal returns on local investments. They argue that local investors have significant information advantages regarding local stocks compared to remote stocks. Similarly, using individual investors’ data from 1991 to 1996, Ivković and Weisbenner (2005) find that households show a strong preference for local assets. They also find that the average annualized return on local assets is 3.2% higher than on non-local assets for an average household, and the returns are even larger for local stocks not in the S&P 500 index, suggesting that local investors can leverage local information. The study by Bodnaruk (2009) shows that when individual investors move away from a company in their portfolio, they sell more shares of this company compared to investors who do not move, and they abnormally increase their holdings in companies closer to their new location. Additionally, the strong bias in favor of startups located in close proximity is a well-documented characteristic of venture capital investment, and information asymmetries matter for the success of such investments (Cumming & Dai, 2010).

The existing literature has examined the determinants of M&A activities, including firm characteristics (Aktas et al., 2013), deal characteristics (Savor & Lu, 2009), financial market development (Jongwanich et al., 2013), institutional environments (Cornaggia et al., 2015), and financial crises (Wan & Yiu, 2009). Among them, extensive theoretical works highlight the vital role of geographic proximity in M&A activities (Chakrabarti & Mitchell, 2013; Kang & Kim, 2008; Uysal et al., 2008). Boschma et al. (2016) demonstrated that the likelihood of completing an M&A increases with geographic proximity. Scholars around the world have observed a preference for geographically proximate targets (Chakrabarti & Mitchell, 2013; Kang & Kim, 2008). Uysal et al. (2008) found that U.S. bidders achieve higher returns when targeting local firms, attributing this to information advantages from being geographically close.

Previous studies suggest that the role of geographic proximity in M&A activities is closely related to information asymmetry between regions. Research indicates that greater geographic distance between regions leads to increased levels of information asymmetry (X. Yang et al., 2025). Scholars have found that many factors, alone or in combination, have important influences on information asymmetry, including geographic distance, overall market conditions, media coverage, regulatory environment, and the broader social structure (Asongu et al., 2019; Doan et al., 2022; Nam et al., 2020). There is an extensive theoretical literature unveiling the role of information asymmetry in M&A transactions (Fishman, 1988; Hirshleifer & Png, 1989; P. R. Milgrom, 1981; P. Milgrom & Weber, 1982; Povel & Singh, 2006). There are also empirical studies that find information asymmetry significantly affects various aspects of M&A activities, such as relative deal size, closure time, target selection, the likelihood of (and time to) completion, valuation of the target, and announcement returns (Bick et al., 2017; Borochin & Cu, 2018; Martin & Shalev, 2017; McNichols & Stubben, 2015). However, it’s difficult to capture the differences and dynamics of information asymmetry. Scholars, as a compromise, use the geographical proximity between the acquiring firm and the target company as a measure of information asymmetry. For instance, Uysal et al. (2008) explored the role of information asymmetries in M&A activities by differentiating M&A transactions based on the distances between acquiring and target firms.

However, information asymmetry is not the only benefit arising from geographic proximity (Uysal et al., 2008). Geographical proximity is probably tied to cultural proximity, institutional proximity, political proximity, administrative proximity, a shared labor pool, similarity of language, etc. These distance-related factors have been proven to be important in M&A activities (Angwin, 2001; Lee et al., 2014; Malhotra et al., 2016; Nielsen & Nielsen, 2011). Due to the time-invariant feature of geographical distance, it’s difficult to disentangle the role of information asymmetries from other factors that also arise from geographical proximity. These factors could possibly lead to overestimating the effect of information asymmetries in M&A transactions.

HSR and M&A Transactions

There are at least two reasons why HSR affects cross-regional M&A. First, a large number of studies have demonstrated the positive effect of HSR services in reducing travel time. The development of the HSR network represents a significant advancement in the Chinese interregional transport system. In terms of speed, bullet trains are three to six times faster than traditional trains, so unlike other modes of transportation (such as traditional railways, aviation, and road systems), they greatly reduce inter-regional travel time. For instance, HSR services greatly reduce the travel time between cities like Beijing and Shanghai, which can be completed in 4 hr by HSR versus 19 hr by traditional train. Shaw et al. (2014) demonstrate that the introduction of HSR in China significantly shortened the average travel time between cities in China, encompassing both time spent in transit and time spent outside of transit. Likewise, analyzing individual passenger data, Z. Chen and Haynes (2017) conclude that HSR services lead to more than a 50% reduction in average travel time.

Travel time is of great significance to M&A activities. During the M&A transaction process, a large number of cross-regional trips are required for identifying potential targets, due diligence, negotiation, value assessment, and post-event monitoring (Bruner & Perella, 2004; Harvey & Lusch, 1998). Desirable targets are frequently situated far from the bidder firm’s current location, placing bidder firms at an informational disadvantage when assessing the value of these distant targets (Conner & Prahalad, 1996; Montgomery & Wernerfelt, 1988). When participants encounter a high level of information asymmetry, the probability of successfully completing cross-regional M&A transactions tends to decrease significantly (Coates et al., 2019).

Second, many studies show that cross-city passenger traffic in China increases significantly after the introduction of HSR services (D. Chen et al., 2022; Dong et al., 2020; Wang et al., 2022; Xiong et al., 2021; Xu, 2019), although there is some displacement of passengers from other transport modes (Lin, 2017; Vickerman, 2018). For example, Ollivier et al. (2014) found that HSR services have led to an increase in business travel. A survey conducted by Lawrence et al. (2019) on HSR development in China found that the HSR system generates more than 850 million business trips annually. The companies surveyed in the study reported that HSR services have become an essential mode of their business travel and that information and communication technology alternatives (such as video and teleconference) cannot replace face-to-face meetings. The increase in inter-regional travel brought about by the opening of HSR will greatly reduce the degree of information asymmetry between regions, thus facilitating cross-regional M&A transactions.

In fact, the role of HSR in cross-regional M&A transactions is closely related to the competition between different transport modes. Compared to other transport modes, bullet trains have significant advantages, such as punctuality in various weather conditions, high frequency, large capacity, low ticket fares, and low pollution (Campos & de Rus, 2009; Diao, 2018; Ke et al., 2017). Scholars have found that HSR has a crowding-out effect on other intercity transportation modes (Albalate et al., 2017; Park & Ha, 2006). For example, Martin and Nombela (2007) found that in Spain, HSR attracts travelers away from planes and buses on long-haul routes. Behrens and Pels (2012) reported that after the development of HSR, two airlines exited the market and another two significantly reduced their service frequency. Cascetta et al. (2015) observed that in Italy, the demand for HSR increased at the expense of air and automobile modes. Wang et al. (2018) provided statistics showing that between 2007 and 2014, among 277 city pairs with both HSR services and direct flight routes, 16 city pairs suspended all civil aviation flights after the introduction of HSR services. Furthermore, 60 city pairs saw the growth rate of civil aviation passenger traffic shift from positive to negative, and 109 city pairs experienced a slight decrease in the growth of civil aviation passenger traffic. In China, Lin et al. (2021) analyzed traffic data from 2009 to 2016 from monitoring stations on over 4,000 national roads or highway segments parallel to HSR lines. They found that HSR connections led to a 20.5% log-point reduction in the number of passenger vehicles on these roads.

The rapid development of a large-scale HSR system in China provides an ideal setting to distinguish the role of information asymmetry in M&A activities from other confounding factors. That is, HSR can reduce information asymmetry between acquirers and targets by enabling frequent and convenient face-to-face interactions while other dimensions of proximity at the regional level remain unchanged. Recently, numerous studies on HSR have found that the dramatic reduction in travel time brought by HSR services can significantly decrease information asymmetries in organizations and many businesses (Dong et al., 2020; Gumpert et al., 2022; Wang et al., 2022). Meanwhile, proximities across a range of factors are highly unlikely to change (at least in the short term) when HSR services are introduced. This paper specifically concentrates on one type of M&A: cross-city M&A. Compared to local M&A transactions, the problem of information asymmetry is more severe in cross-regional M&A deals. Thus, a large number of researchers have reported that local M&A transactions far outnumber cross-border M&A transactions (Campa & Hernando, 2006; Grote & Umber, 2008). If HSR can actually reduce information asymmetry in M&A activities, we expect that the emergence of HSR services in China will exert a positive impact on cross-regional M&A activities. Based on the above arguments, we predict our hypothesis as follows:

Hypotheses 1: The opening of HSR services facilitates M&A activities among HSR cities.

Data and Methodology

Data Source

This study utilizes the PEdata database to gather information on 6,354 cross-region M&A deals involving both public and private companies in China from 2000 to 2016. The PEdata database contains detailed information on participants in each transaction. We then identify the cities where the participants are located by searching their names on the official websites, such as the PEdata database official site (https://zdb.pedaily.cn/company), Unified Social Credit Code Query of National Organization (https://www.cods.org.cn), China Government Procurement Service Information Platform (http://www.ccgp.gov.cn), National Enterprise Credit Information Publicity System (http://gsxt.gdgs.gov.cn), Qichacha website (https://www.qcc.com), and Aiqicha website (https://aiqicha.baidu.com).

We manually collect HSR data from the China Railway Passenger Train Schedule, a printed book issued by the China Railway Administration, which lists the dates when each city began offering HSR passenger service. The China City Statistical Yearbook, covering the years 2000 to 2016, is also used as a data source, providing information on various city characteristics that serve as controls in the study. The innovation index data is taken from the Report on the Innovation Capability of Chinese Cities and Industries 2017. Additionally, the study manually compiles historical data on Chinese railway stations from a 1961 map available on Wikipedia.

Empirical Strategy and Research Design

Our research design, following Dong et al. (2020), focuses on analyzing the impact of HSR services at both the city and city-pair levels. We investigate whether the introduction of HSR services leads to an increase in cross-region M&A activities for individual cities and city pairs. Additionally, we conduct a range of robustness checks and heterogeneous analyses to explore the mechanisms underlying this relationship.

The Difference-in-Differences (DID) model is a robust technique for evaluating the effects of interventions in observational studies by comparing changes in outcomes between treatment and control groups. However, when treatments (e.g., policy changes) are implemented at different times across various units, the traditional DID model may be inadequate for analyzing staggered treatments and can produce misleading estimates of the treatment effect. In our study, the timing of HSR service openings varies across cities. To address this, we use a multi-period DID model, as recommended in prior research (Beck et al., 2010; Biasi & Sarsons, 2022; Cantoni & Pons, 2021; Cao et al., 2022; Guriev et al., 2021). This approach provides greater flexibility in selecting control groups, allowing us to include both “not-yet treated cities” and “never-treated cities” as controls.

Empirical Results

Descriptive Evidence

Table A2 in Appendix presents the descriptive statistics of key variables. The mean and the median values of M&A at the city level are 0.45 and 0.86, respectively, implying that cross-region M&A transactions are not well developed in China. While the maximum and minimum values of M&A at the city level are 6.26 and 0.00, respectively, suggesting that M&A varies immensely among cities. The statistics for M&A at the city-pair level present similar characteristics. The variances of M&A at the city level and city-pair level are larger than the mean values, which means that different cities may have significant differences in the number of cross-region M&A transactions.

The study uses data from 188 out of 292 Chinese cities that were connected to the HSR network before 2017. The samples are divided into two groups: HSR cities and non-HSR cities. Figure 1 illustrates the trends of cross-region M&A transactions in both groups before and after the introduction of HSR service in China. The figure shows that before 2008, cross-region M&A transactions were few in number and grew slowly in both HSR cities and non-HSR cities, with little difference in the number of transactions between the two groups. However, after 2008, the scale of cross-region M&A transactions in HSR cities began to climb rapidly and kept a high-speed growth, while the growth in non-HSR cities was very slow. This suggests that HSR services might have a significant impact on cross-region M&A transactions in HSR cities.

Baseline Results

City-Level Baseline Results

In Table 1, the impact of HSR services on cross-region M&A activities is assessed using Equation 1. The regression in Column 1 includes city and year fixed effects. Column 2 includes additional time-varying city-specific characteristics such as GDP per capita, population, industrial structure, government behavior, and innovation capacity. Column 3 includes the development of ICT, measured by the number of internet terminals and mobile phones. The final column controls for the availability of other modes of transportation, such as highways and airports.

HSR and Cross-Region M&A Transactions: Baseline Regression Results at the City Level.

Note. All regressions presented include a constant. The t-values of the results are reported in parentheses, and statistical significance is indicated by * (p-value < .1), ** (p-value < .05), and *** (p-value < .01). Additionally, all regressions controls for factors such as population, the proportion of the secondary industry, innovation index, city and year fixed effects. Same hereinafter.

Table 1 shows that the HSR dummy, a variable indicating the presence of HSR services, enters positively and is significant at the 1% level in all 4 regressions. For example, the results in Column 4 suggest that HSR services lead to a 39.1% increase in cross-region M&A activities in HSR cities, which is considered a large economic increase. These results indicate that firms located in cities with HSR services engage in more cross-region M&A activities than those in cities without HSR services after the opening of HSR services, supporting hypothesis 1. In addition, we observe that following the opening of HSR services in a city, the number of M&A deals where local firms targeting outside firms increased by 39.1%, while the number of M&A deals where firms targeted by non-local bidders increased by 29.6% (see Table A3 in the Appendix). This means that HSR services not only promote enterprises to invest in other places but also promote enterprises from other places to invest in local areas. The findings suggest that the HSR network plays an important role in the development of cross-region M&A transactions and also imply that reducing information asymmetries can facilitate M&A transactions.

Citypair-Level Baseline Results

In this section, the impact of HSR services on a specific city-pair is explored using stepwise regressions. Table 2 shows that the coefficients of HSR dummies are all positive, significant, and close in all regressions. The results indicate that HSR services significantly boost cross-region M&A activities for a city-pair. Specifically, the number of M&A deals realized by companies from the two cities in a city-pair increases significantly when the two cities are connected by the HSR network. These city-pair-level baseline results are consistent with the city-level baseline results, providing further support for the conclusion that HSR services play a positive role in promoting cross-region M&A activities.

HSR and Cross-Region M&A Transactions: Baseline Regression Results at the Citypair Level.

Note. CP FEs refers to citypair fixed effects. Same hereinafter.

(p-value <0.1), **(p-value <0.05), and ***(p-value <0.01).

Robust Tests

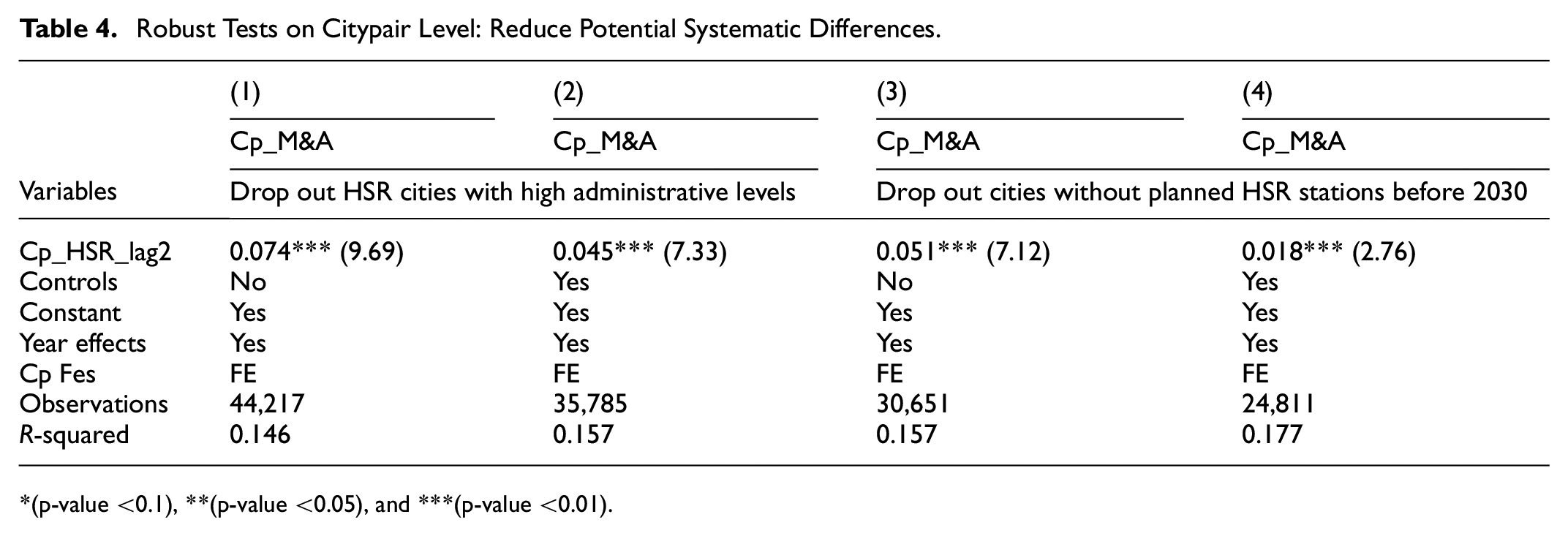

Reduce Potential Systematic Differences Between HSR Cities and non-hSR Cities

It is possible that there are systematic differences between HSR cities and non-HSR cities that may lead to biased estimation results. For example, many HSR cities have higher administrative status, such as four major cities (Beijing, Shanghai, Tianjin, and Chongqing), 23 capital cities of provinces, and 15 sub-provincial cities. These cities typically have a larger pool of skilled labor, more capital, and higher levels of technology (Dong et al., 2020). They are also likely to be different from other prefecture-level cities in terms of economic scale, transportation location, and development level. Additionally, there may be certain city characteristics correlated with M&A transactions but are not observable to researchers, which may also lead to bias in the estimation results.

To reduce potential systematic differences between HSR cities and non-HSR cities, two strategies are used:

Dropping HSR cities with high administrative levels from the treatment group, including four major cities (Beijing, Shanghai, Tianjin, and Chongqing), 23 provincial capital cities, and 15 sub-provincial cities.

Deleting sample cities that had no planned HSR stations before 2030 according to the latest version of the Medium and Long-term Railway Plan approved by the State Council. This ensures that the sample includes cities that have been connected to the HSR network and those that will be connected before 2030. This strategy greatly reduces the systematic differences between HSR cities and non-HSR cities in the remaining samples.

Tables 3 and 4 report the results of robust tests at the city level and the city-pair level after excluding special samples. It can be found that the coefficients of all HSR dummies are significant at the 1% significance level. This finding indicates that potential systematic differences between HSR cities and non-HSR cities had little effect on the baseline analysis.

Robust Tests on City Level: Reduce Potential Systematic Differences.

(p-value <0.1), **(p-value <0.05), and ***(p-value <0.01).

Robust Tests on Citypair Level: Reduce Potential Systematic Differences.

(p-value <0.1), **(p-value <0.05), and ***(p-value <0.01).

Examine HSR’s Impact Across Varying Economic Growth Rates

During the sample period of this study, China’s economy developed very rapidly, and M&A activities are closely linked to economic growth. Therefore, there is concern that the rise in cross-city M&A activities is mainly due to China’s rapid economic development. To address this concern, we grouped cities according to their GDP growth rates and analyzed the impact of HSR on cross-city M&A activities.

Specifically, the cities are divided into four groups based on their annual GDP growth rates during the sample period. We further examine whether the positive impact of HSR on cross-city M&A activities holds true across cities with varying economic growth rates. The results are reported in Table 5. The coefficients of HSR remain significantly positive in all quartiles. Our regression results confirm that the positive impact of HSR on cross-city M&A activities is robust across cities with different GDP growth rates. The results suggest that the observed relationship is not merely a reflection of overall economic growth but rather an intrinsic effect of improved transportation infrastructure.

Robust Tests: Examine HSR’s Impact Across Varying Economic Growth Rates.

Note. Q1 = cities with the lowest 25% GDP growth rates; Q2 = cities with GDP growth rates between the 25th and 50th percentiles; Q3 = cities with GDP growth rates between the 50th and 75th percentiles; Q4 = cities with the highest 25% GDP growth rates.

(p-value <0.1), **(p-value <0.05), and ***(p-value <0.01).

Parallel Trend Assumption

The parallel trends assumption is a key prerequisite for DID analysis, and violation of this assumption leads to biased estimation. The connotation of this hypothesis is that in the absence of treatment, the difference between the treatment and control groups is constant over time (Abadie, 2005; Angrist & Pischke, 2008). In fact, since the counterfactual outcome of the treatment group cannot be observed, the post-treatment effect cannot be tested. To ensure the validity of the results, researchers typically check if the parallel trends assumption holds before treatment. Following the work of Beck et al. (2010), we use Equation 2 to test for the parallel pre-trend assumption and observe the dynamic effects of HSR services on the outcome of interest:

where “Ds” correspond to 1 year, j years,…, before or after the opening of HSR services.

The dynamic effect of HSR services on intercity co-developed patents.

Figure 2 shows that the difference in cross-region M&A transactions between HSR cities and non-HSR cities did not precede the introduction of HSR services. As shown, the coefficients

IV Regressions

HSR routes are unlikely to be randomly selected by the Chinese central government (Dong et al., 2020), but are likely associated with unobservable factors (geographical conditions, environmental protection, construction cost, connecting with the existing railway network, etc.) of HSR layout. These unobservable factors could introduce hidden bias into our causal estimation. We rely on the instrumental variables (IV) strategy, a common econometric solution to address endogeneity problems in transport literature (Redding & Turner, 2015), to mitigate potential bias.

Specifically, this study uses the 1961 Chinese railway route map to construct an instrumental variable (IV). The IV (rail1961_i) equals one if city i was connected to the 1961 railway network, and zero otherwise. It is a commonly used instrumental variable in China’s HSR economic research to address the problem of non-random allocation of HSR routes (Baum-Snow et al., 2017; Diao, 2018; Zheng & Kahn, 2013). To be a valid instrument, this IV must predict recent M&A activities only through its influence on the location and configuration of the modern HSR network, conditional on control variables. The layout of HSR must account for connections with the existing railway network, which results in a high correlation between the layout of high-speed rail and historical railway lines. In other words, historical railway lines can effectively predict the current HSR layout.

The railway network of China before 1962 served as a means for shipping raw materials and manufactured goods according to the national and provincial plans rather than facilitating M&A activities between cities. The market now plays a central role in the Chinese economy, and economic activities would have had ample time to relocate since 1962. The railway layout of China before the 1960s was the product of a complex series of historical events. Given the variety of actors and motives behind the construction of the pre-1962 railway network, it is plausible that much of the rail network was constructed without regard to its impact on post-2000 M&A activities between cities, conditional on our base controls. Thus, this instrument is closely correlated with the likelihood that a city is connected by HSR but is unlikely to be correlated with the city’s recent M&A activities.

In summary, this IV can serve as a good instrument for predicting the layout of high-speed rail lines. At the same time, the railway tracks in 1961 are unlikely to affect current cross-city M&A transactions through factors other than the railway system itself. Following Churchill et al. (2023) and Wossen et al. (2022), we employ the Control Function Approach developed by D’Haultfœuille et al. (2024) to test the exclusion restriction of this IV. The p-value of this test is .003, indicating that there are no concerns about our instrument violating the exclusion restriction. Overall, the historical IV is one of the best methods currently available for identifying the causality between transportation infrastructure and economic activities (Redding & Turner, 2015).

The results of the IV regression are reported in Table 6. Following Diao (2018) and Zheng and Kahn (2013), we employ a logit model to predict the probability of cities being connected to the HSR network from 2007 to 2016, using the IV and a series of time-varying city characteristics in the first-stage regression. Column 1 shows that the instrumental variable is significant and positive at the 1% level, confirming that the IV is a strong predictor of HSR treatment. The F-value is greater than 10 in the first-stage regression, and the Wald F statistic is greater than the Stock-Yogo critical value of 16.38 in the second stage, indicating that the selected IV is valid and not weak. In the second stage, the predicted probability is integrated into Equation 1. The coefficient of HSR connection in Column 2 is positive and significant at the 1% level, confirming the robustness of our baseline estimation.

Robustness Test: City-Level Instrument Variable Regressions.

Note. The validity test refers to the exclusion restriction test in D’Haultfœuille et al. (2024), with p-value reported in parenthesis.

(p-value <0.1), **(p-value <0.05), and ***(p-value <0.01).

Placebo Test 1

To examine whether the baseline results are the outcome of random events, we conduct a placebo test, following methods used in previous studies (Chetty et al., 2008; Ferrara et al., 2012; Li et al., 2016). This test involves randomly assigning HSR services to cities and then performing baseline regressions using “virtual” HSR dummies. This procedure is repeated 1,000 times to enhance the identification power of the placebo test and to gather the estimated coefficients of the “virtual” HSR dummies. Given the random nature of data generation, it is expected that the “virtual” HSR services will produce insignificant estimates with a magnitude near zero.

The results of the placebo test are presented in Figure 3. It shows that the distribution of the estimated effects of the “virtual” HSR dummies is centered around zero, confirming that there is no impact from the randomly assigned HSR services. Additionally, the real effect of HSR services, as derived from Column 4 of Table 1 (indicated by the red vertical line), is clearly situated outside the range of coefficients estimated by the placebo tests. In conclusion, Figure 3 suggests that the positive effect of HSR services on cross-region M&A transactions is not a result of random events.

The result of placebo test 1.

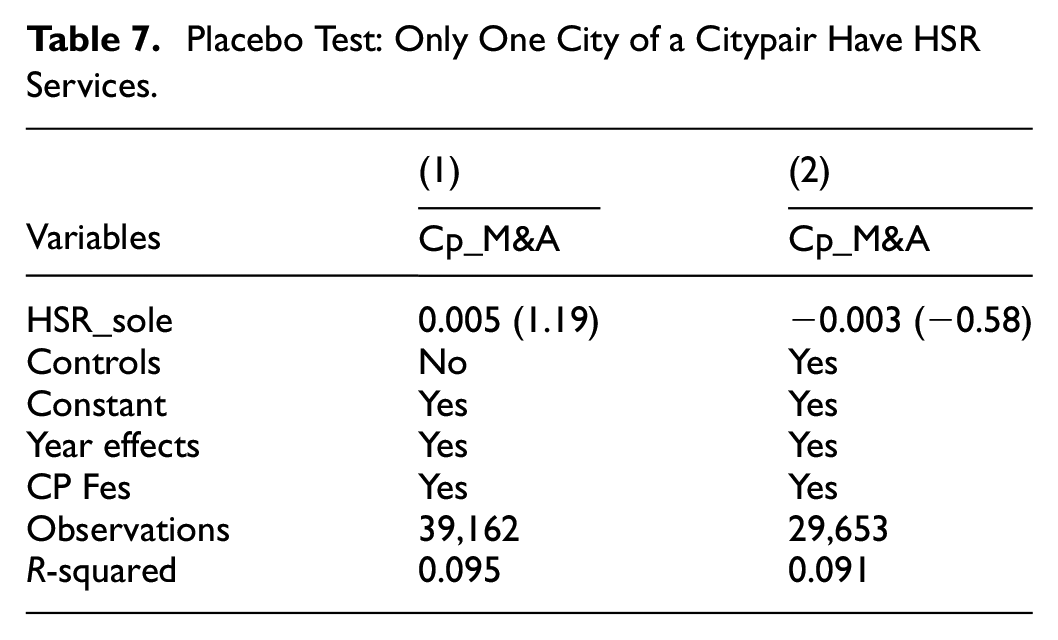

Placebo Test 2

To further investigate the causal relationship between HSR services and cross-region M&A transactions, we designed a second placebo test using the citypair structure. For a given citypair, there are three possible scenarios: (1) neither of the two cities has an HSR station; (2) only one city has an HSR station; (3) both cities are connected by HSR lines. The baseline results have demonstrated that the opening of HSR service leads to an increase in cross-region M&A transactions of HSR cities. However, if only one city of a certain citypair has HSR services, it should not have a significant impact on the cross-region M&A transactions for that citypair. To test this hypothesis, we introduced a new dummy variable, HSR_sole, into the benchmark model. The variable HSR_sole is set to 1 when only one city in a citypair has HSR services and 0 otherwise.

Table 7 presents the results of the placebo test. The coefficients for the HSR_sole variable are not statistically significant, which suggests that when only one side of a citypair opens HSR services, it does not lead to a significant increase in cross-region M&A activities for that citypair. Considering these results in conjunction with the baseline results, we can conclude that HSR networks promote cross-region M&A activities among HSR cities, but not between HSR cities and non-HSR cities. Thus, this test further verifies the robustness of the causal relationship between HSR services and cross-region M&A activities.

Placebo Test: Only One City of a Citypair Have HSR Services.

Mechanism Tests

In this section, we explore whether alleviating information asymmetry plays an important role in how HSR affects cross-city M&As. Following the literature, we adopted the following proxies to measure the degree of information asymmetry. The first proxy is the weighted average travel time (WATT), a widely used accessibility indicator (Gutiérrez et al., 1996; Vickerman et al., 1999; Wang et al., 2018). WATT calculates the average travel time between one city and all others, weighted by the mass of destinations (measured by the square root of GDP in this study). The formula is given by

where

The second proxy for information asymmetry is the variation in railway passenger traffic (VRPT) for each city. First, as a medium for information dissemination, passengers can bring new market information, business opportunities, and technologies to different cities, reducing information differences caused by geographical isolation. Second, the network of contacts established by passengers through social interaction and interpersonal communication promotes information sharing and exchange, thereby alleviating information asymmetry. In addition, changes in passenger consumption and production behaviors encourage local producers to understand the market information of other regions and adjust their products and services. As passenger flow increases, the transparency of different cities improves. Information such as price, quality, and service that travelers learn through actual experience reduces market distortion and uncertainty. Finally, passenger flow promotes the diffusion of technology and business models. The combined effect of these factors enables passenger flow between cities to effectively alleviate information asymmetry between markets to some extent. This proxy is the variation in railway passenger flow. This study uses the volume of railway passengers in each city in 1999 as the benchmark. The variation in passenger numbers is obtained by subtracting the volume in other years from this benchmark value. This variation reflects the change in passenger volume brought by the HSR connection. Many studies have found that inter-city business and leisure travel increased significantly after the opening of HSR services (Bonnafous, 1987; Rietveld et al., 2001; Yin et al., 2015).

The third indicator of information asymmetry across regions is innovation, measured by the number of patent applications per 10,000 people. If there is no information asymmetry between regions, each region can obtain information from other markets (e.g., new technologies, new knowledge, market demand information) and there is no technological distance between enterprises. Assuming other conditions are similar, the innovation performance of each region will tend toward the optimal value. In our study, some regions (e.g., Beijing, Shanghai, Shenzhen) have very high per capita innovation output and are generally considered to have smoother communication with each other. Conversely, cities that find it difficult to obtain and exchange information typically have low per capita innovation output.

Consistent with the studies of Hayes (2009) and Kenny, D. A. (1986), we propose the following two-stage mediation model to investigate whether alleviating information asymmetry plays a mediating role in the process of HSR promoting cross-city M&As:

Where

The results of the intermediary effect are reported in Table 7. The coefficients in Columns (1), (3), and (5) are all positive at the 1% significance level. The results in Column (1) indicate that HSR has reduced the weighted average travel time between HSR cities. The results in Column (2) show that HSR has led to increased railway passenger flow in HSR cities, while the results in Column (5) demonstrate that HSR has promoted the per capita innovation output of HSR cities. With these three variables used to measure the degree of alleviation of information asymmetry, the results consistently show that HSR has reduced the degree of information asymmetry between HSR cities.

Columns (2), (4), and (6) represent the estimated impacts of the reduction of information asymmetry on HSR and cross-city M&As. The coefficients of the three information asymmetry proxy variables in Columns (2), (4), and (6) are all positive at the 1% significance level. The estimations indicate that the reduction of information asymmetry positively affects cross-city M&As between HSR cities. Combined with the results in Columns (1), (3), and (5), we find that HSR can reduce the degree of information asymmetry in HSR cities, thereby affecting cross-city M&A activities.

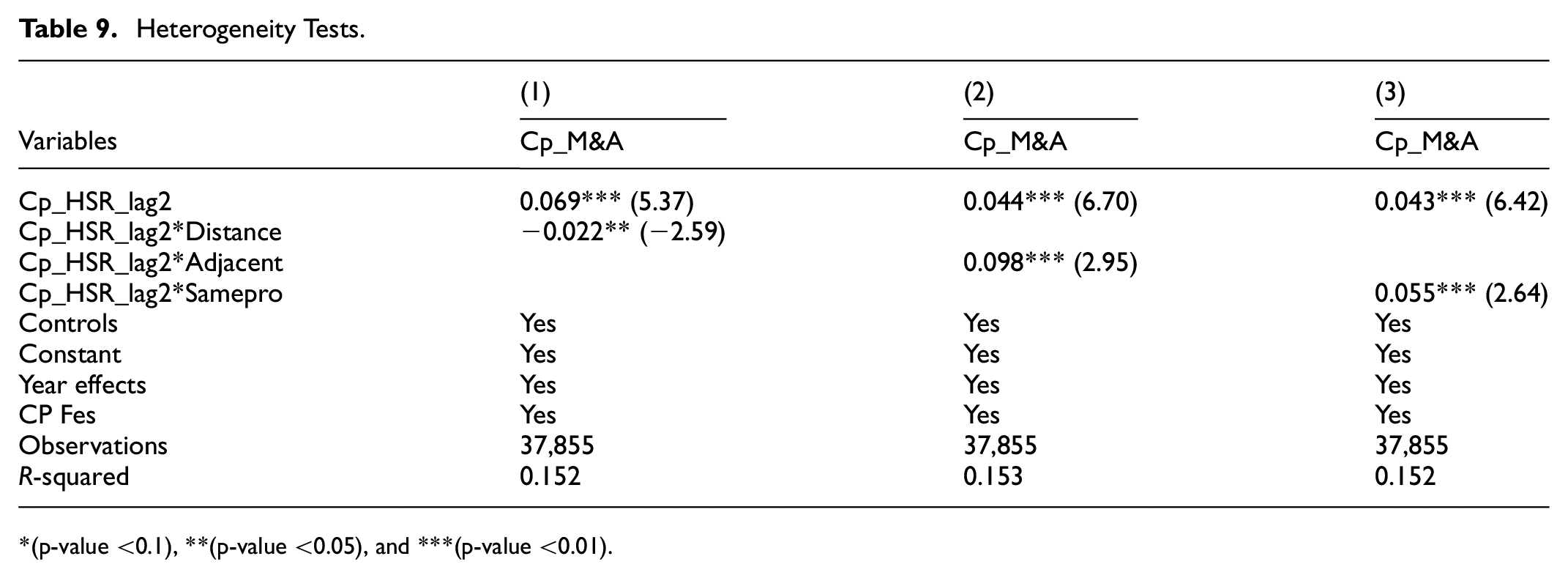

Heterogeneity Tests

This subsection tests hypothesis two, which examines the role of HSR in reducing information asymmetry by considering various inferences. The empirical results are reported in Table 9. As previously established, the evidence suggests that HSR services can significantly promote cross-region M&A transactions involving HSR cities. We propose that the mechanism behind this effect is that HSR can reduce information asymmetry between cities. If this is true, the following inferences should hold. The first inference is that if HSR services can promote cross-region M&A activities by reducing information asymmetry, then the effect of HSR should decrease with increasing distance. The second column of Table 8 shows that the coefficient of the HSR dummy variable is positive, but the coefficient of the interaction between the HSR dummy variable and the distance between the two cities of a city pair is negative and statistically significant. These results suggest that the positive effect of HSR on cross-region M&A activities decreases with increasing distance, which is consistent with the information asymmetry channel.

Mechanism Tests.

Note. For the sake of readability of the results, this article takes the inverse value of WATT. That is, the larger the value of WATT, VRPT, and Innovation, the lower the degree of information asymmetry.

(p-value <0.1), **(p-value <0.05), and ***(p-value <0.01).

Next, we focus on two types of cities: neighboring cities and cities within the same province. These cities share similar cultural and institutional environments, dialects, and other factors that are important for M&A activities. These proximities are key factors in M&A activities. HSR services can hardly affect these factors but can reduce information asymmetry by facilitating face-to-face interactions between these cities. Therefore, we expect HSR services to have a pronounced impact on cross-region M&A activities in these cities after they are interconnected by HSR routes. In this analysis, we introduced two dummy variables: Adjacent and Samepro. The variable Adjacent is equal to 1 if two cities are adjacent to each other and 0 otherwise. The variable Samepro is equal to 1 if both cities are located in the same province and 0 otherwise. Column 3 of Table 9 shows that the coefficient estimate for the interaction between the HSR dummy variable and the Adjacent dummy variable is positive and statistically significant at the 1% level, indicating that adjacent cities experienced a significantly higher increase in cross-region M&A activities compared to non-adjacent cities. Similarly, in column 4, we find a positive, significant, and economically substantial coefficient for the interaction term between the HSR dummy variable and the Samepro proxy, which further supports that HSR services have a greater impact on cities in the same province compared to those not in the same province. As expected, hypothesis 2 is supported by the evidence.

Heterogeneity Tests.

(p-value <0.1), **(p-value <0.05), and ***(p-value <0.01).

Conclusion

This study investigates the role of HSR development in promoting cross-city M&A in China. Our findings show that the introduction of HSR services significantly improves cross-city M&A activities by 43.7% in HSR cities. After the two cities were interconnected through HSR lines, the number of M&A transactions between them increased by 5.1%. After employing various robustness checks, including reducing systematic differences, conducting placebo tests, and performing IV regressions, our findings consistently support the positive impact of HSR services on cross-region M&A activities. Further analysis shows that HSR plays a key role in reducing information asymmetry, thereby facilitating cross-regional capital reallocation.

Our study contributes to the literature by addressing the gap in understanding the impact of transportation infrastructure on M&A activities. We provide new and robust empirical evidence using a staggered DID approach, highlighting HSR’s role in M&A transactions by reducing information asymmetry. This research also expands the scope of M&A studies by including both private and public firm data, offering a more comprehensive analysis of M&A dynamics in developing economies.

This study can help policymakers recognize the importance of transportation infrastructure in emerging economies, such as HSR, in enhancing regional connectivity and market efficiency. By investing in HSR networks, governments can reduce transaction costs and information barriers, thus fostering a more efficient allocation of capital across regions. This can lead to increased economic growth and development, particularly in underdeveloped areas. In addition, this study suggests that the government should carefully plan the layout of HSR routes to coordinate regional economic development.

This study has some limitations. First, the analysis is limited to the impact of HSR on M&A activities within China. Future research could extend this framework to other countries with different transportation infrastructures to validate the generalizability of our findings. Second, while we control for various factors, there may still be unobserved variables influencing M&A activities. Future studies could incorporate more granular data, such as firm-level characteristics and industry-specific factors, to provide a deeper understanding of the mechanisms driving M&A decisions. Third, with regard to the measurement of information asymmetry, the lack of proper theory and data makes it difficult to fully capture the dynamic changes in regional information asymmetry. As a result, proxy variables may not fully reflect the actual situation. In this study, we used multiple variables to proxy information asymmetry; however, these variables cannot show the full picture and only observe changes from a certain dimension. We hope that future studies will have access to comprehensive data and employ sophisticated research designs to better address this issue. Fourth, another limitation of our study is the choice of the research period, specifically the years 2000-2016. This period was selected primarily due to data availability and the authors’ time constraints. Considering the potential for diminishing marginal effects, the impact of HSR may weaken in the future. We acknowledge that the economic environment and policy changes during this specific timeframe may influence our results. To enhance the robustness and generalizability of our findings, future research should consider extending the timeframe to include more recent years. By doing so, researchers can verify whether the observed patterns and conclusions hold true in different economic conditions and over a longer period, providing a more comprehensive understanding of the role of transportation infrastructure in alleviating information asymmetry across regions.

Footnotes

Appendix

Pearson Correlation Coefficient Matrix of Citypair-Level Variables.

| Variables | Cp_M&A | Cp_HSR_lag2 | Cp_Rgdp | Cp_Population | Cp_Structure | Cp_Government |

|---|---|---|---|---|---|---|

| Cp_M&A | 1 | |||||

| Cp_HSR_lag2 | 0.279*** | 1 | ||||

| Cp_Rgdp | 0.248*** | 0.401*** | 1 | |||

| Cp_Population | 0.108*** | 0.177*** | 0.008* | 1 | ||

| Cp_Structure | −0.159*** | −0.074*** | 0.113*** | −0.256*** | 1 | |

| Cp_Government | 0.134*** | 0.210*** | 0.346*** | 0.065*** | −0.075*** | 1 |

| Cp_Internet | 0.245*** | 0.390*** | 0.721*** | 0.475*** | −0.186*** | 0.312*** |

| Cp_Information | 0.232*** | 0.367*** | 0.843*** | −0.082*** | 0.027*** | 0.285*** |

| Cp_Highway | 0.087*** | 0.174*** | 0.325*** | 0.348*** | −0.009* | 0.164*** |

| Cp_Airport | 0.119*** | 0.081*** | 0.211*** | 0.194*** | −0.191*** | 0.064*** |

| Cp_Innovation | 0.305*** | 0.461*** | 0.740*** | 0.406*** | −0.277*** | 0.348*** |

| Variables | Cp_Internet | Cp_Information | Cp_Highway | Cp_Airport | Cp_Innovation | |

| Cp_Internet | 1 | |||||

| Cp_Information | 0.706*** | 1 | ||||

| Cp_Road | 0.373*** | 0.368*** | 1 | |||

| Cp_Airport | 0.241*** | 0.169*** | 0.109*** | 1 | ||

| Cp_Innovation | 0.883*** | 0.714*** | 0.382*** | 0.256*** | 1 |

Notes. The statistical significance is indicated by * (p-value <0.1), ** (p-value <0.05), and *** (p-value <0.01).

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the National Social Science Fund of China (24XJL007).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data used to support the findings of this study are available from the corresponding author upon request