Abstract

One of the most essential tools of poverty reduction would be the viable expansion of institutional credit facilities to large sections of the people who neither have adequate collateral nor credit history to secure a loan. In this backdrop, social collateral is popularized through the group lending programs to address the credit market problems. Microfinance through group lending is acting as a screening device; the joint liability mechanism creates incentives for internal monitoring. Hence, it has received a lot of attention from policy makers as well as academicians. It is playing an important role in delivering financial services to the “socially and economically excluded” poor, in general, and women, in particular. The group lending works with various dynamic incentives. One such kind is principle of progressive lending and it plays a vital role in sustaining the groups for the persistent delivery of microfinance services to its members. In progressive lending, a typical borrower receives very small amounts at first, which increases with good repayment conduct or it links new, larger loans to past repayment. This article explores possible theoretical and empirical relationship between progressive lending and its determinants in group lending approach. The primary survey was conducted in 10 villages covering 106 self-help groups and 318 members in Karnataka, India. The empirical results show the progressive lending amount rising up to 698% of the initial loan of the self-help groups.

Introduction

Asymmetries of information cause many problems in the credit markets, namely, adverse selection, moral hazard, and lack of enforcement. It is generally known that moral hazard, coupled with lack of collateral by the poor is the key reason why credit markets fail for them. The problem of moral hazard may arise when individuals engage in risk sharing under conditions such that their privately taken actions or behaviors affect the probability distribution of the outcome. These situations generally appear in a principal–agent relationship when actions taken by an agent are not Pareto optimal (Holmstrom, 1979).

The emergence of innovative group lending models in the field of microfinance is celebrated as a contractual innovation that has achieved the perceptible miracle of enabling previously unbankable or marginalized borrowers to lift themselves up by their own bootstraps by creating “social collateral” to replace the missing physical collateral that excluded them from access to more traditional forms of financial services, like credit, savings, and so on (Conning, 2000). Thus, the emergence of innovative joint liability microfinance models in the field of financial intermediation has created new hopes for the poor, who are otherwise unbankable from the perspectives of formal financial institutions.

One of the successful ways through which the financial services are being provided to the poor people in India is through microfinance groups (self-help groups [SHGs] or Grameen groups). These groups are essentially informal organizations of poor people from rural or urban areas. The groups are organized, owned, operated, and controlled by the members, based on solidarity, reciprocity, common interest, and resource pooling. People who are homogeneous with respect to social background, heritage, caste, or traditional occupation come together for a common cause to raise and manage their collective savings for the benefit of all the peers in the group. Microfinance group is a social design in which people participate by making themselves socially and economically accountable to each other. These group-based credit systems address the problems of screening, incentives, and enforcement by incorporating joint liability principle and peer monitoring. A group-based lending contract effectively makes a borrower’s neighbors co-obligator to loans, in the process mitigating problems created by informational asymmetries such as adverse selection, moral hazard, and enforcement (Morduch, 1999). Thus, in group lending contracts, the functions of screening, monitoring, and enforcement of repayments are, to a large extent, transferred from the financial institution to the group members. Varian (1990), Stiglitz (1990), and Besley and Coate (1995) viewed that several credit market failures that group-based lending have overcome are through the microfinance programs. The group-based lending mitigates the problem of adverse selection that in turn reduces the problem of credit rationing and brings the safe borrowers back to the credit market. The theoretical and empirical studies show that people try to investigate each other’s behavioral integrity and creditworthiness with the help of existing social networks before they try to prevent irresponsible and credit risky borrowers from joining the group.

The group-based lending methodologies will mitigate the problem of moral hazard. Soon after the members receives the loan, they have to monitor each other to make sure that every member has invested the loan in a safe project that will guarantee repayment by the peer. Members make use of their social ties and local networks to acquire the necessary information and create social sanctions and bring pressure on nonrepaying members. The peer pressure is a mechanism in the group lending that can be used in the process of mitigating moral hazard and enforcing prompt repayment (Stiglitz & Weiss, 1981). To secure future access, members are obliged to monitor each other. The social collateral (systems) or ties constitutes a powerful device to reinforce repayment among group members. The ability of the groups to harness social sanctions and make use of sanctions, including members to repay their installments, can be important mechanisms to sustain groups and improve the repayment performance of the microfinance lending. Distributing loans through groups of borrowers is assumed to result in lower transaction costs for the lender and the individual borrowers. The lender’s costs are minimized, as she or he is dealing with the group as a whole, rather than the individual within the group. Similarly, the group is responsible for distributing loans and collecting repayments. This will lead to reduction in the transaction costs to the individual borrowers. Thus, it is much clear that microfinance groups are having greater potentiality to mitigate market imperfection problems.

Furthermore, one important mechanism for securing high repayment rates in group lending programs involves exploiting “dynamic incentives” like “progressive lending” (Hulme & Mosley, 1996) by increasing loan sizes over time, conditional on repayment histories (Besley & Coate, 1995). Where, lending typically begins with small amounts and then increasing loan size upon satisfactory repayment. It is a key incentive for repayment in group lending where there is a promise of a new, additional larger amount of loan if the previous loan is successfully repaid. This approach is also called as “step lending” by the ACCION network (Morduch, 1999). Furthermore, in the microfinance context, the term progressive lending is also used when the disbursement of additional loans is made conditional on the entrepreneur having met easily verifiable conditions directly connected to the project. It is a unique feature of joint liability lending that has advantages over traditional lending methodologies (Egli, 2004).

There is less empirical evidence on the mechanism of progressive lending as a dynamic incentive in Indian microfinance group lending programs. Therefore, this article examines the nature and features of progressive lending as an incentive device and its association with the SHG member credit utilization. Furthermore, the article analyzes the factors that contribute to the progressive lending.

The article is organized as follows. The section titled “Introduction” introduces the research problem and study objectives. The section titled “Previous Research” gives a brief review on the progressive lending as an incentive and an enforcement mechanism in microfinance group lending. The section on “Survey Design and Data” describes the survey design and data source used in this study. In the section “Empirical Results,” the empirical results are presented, showing the factors influencing and its relative significance in determining the progressive lending. The section “Conclusion” concludes along with future research agenda.

Previous Research

Theoretical and empirical literature on group lending addresses the central problem of designing mechanisms in a way that borrowers have an incentive to repay their loans as well as an enforcement mechanism (Egli, 2004). In the world of microfinance, microcredit plays a unique role in fighting against poverty reduction. It seems to have a greater and more direct impact on the conditions of beneficiaries, given that it allows, by using a small amount of money, to foster economic activities for revenue generation. The approaches used to get the guaranteed repayment probably represent the most innovating and original facet of microcredit compared with conventional credit risk mitigation policies. Microcredit programs worldwide used the unconventional forms of guarantees. Poor people own only intangible assets like the sense of belonging to the same community and the reciprocal solidarity, and so on. Developing and transforming all these intangible assets into a social capital would ensure the collateral obligation of the loan and enforcement. Coherent with such an idea, the main risk-mitigating methodologies used are joint liability or group lending and dynamic incentives.

The “discovery” of group lending opened up promise of microfinancial services for the “financially and socially excluded” poor, in general and women in particular. It is by far the most celebrated microfinance innovation in the world. Today, it is just one element that makes microfinance different from the traditional banking. Within group lending, many mechanisms are practiced by the institutions to overcome information problems and improve efficiency. One among these mechanisms is “progressive lending.” It refers to the practice of promising larger and larger loans for groups and individuals in good standing (Armendariz & Morduch, 2005; Morduch, 1999). According to Hulme and Mosley (1996) “progressive lending is a practice of increasing the credit limit of borrowers by a proportion dependent on their previous repayment record” (p. 60).

Furthermore, Hulme and Mosley (1996) use a game theoretic approach to explain the progressive lending (see Figure 1). They visualize the relationship between utility-maximizing lender and borrower with a game in three stages that may or may not repeat themselves—initial agreement, implementation, and decision on whether and on what terms to grant repeat loan. They referred these three stages as Acts 1, 2, and 3, respectively. In the first stage, in Act 1, lender makes a loan of standard size of X at a standard interest rate r. In Stage 2, in Act 2, the borrower receives a return s on the project for which the loan is being used to finance and repays a proportion of this loan; in the event that repayment is not made in full, the lender either punishes this behavior by refusing to provide repeat finance or not. In the last stage, in Act 3, borrower does not repay the loan, but lender still provides a loan. This is because of the lender’s strategy of “lending into the recipient’s arrears” to pay back the arrears on the previous loan. Thus, progressive lending schemes expand the opportunity cost of nonrepayment and thereby discourage strategic default even further. However, it is obvious from the figure that the successive repayment of loan will enhance the size of loan through new loan contracts between the lender and borrowers and it further increases the loan cycles.

Incentive to repay and progressive lending: The game theoretic approach

According to Morduch (1999), progressive lending is the distinctive feature for leading microfinance programs like Grameen Bank, Banco-Sol, Bank Rakyat, Badan Kredit Desa, and FINCA Village Banks. The empirical result from these programs shows that progressive lending not only exists, but loans also seem to increase substantially over time. The study by Kevane and Wydick (2001) on Guatemala’s Fundacion para el Desarrollo Integral de Programas Socioeconomicos (FUNDAP) reports that the mean loan size increases from US$ 1,033 for the first loan to US$ 1,916 for the last loan. In addition, the field study by Robinson (2001) carefully describes the features of 18 loans in different countries and programs. Twelve of these projects show progressive lending, with amounts rising up to 200% of the initial loan (see Table 1).

Main Features of Several Microfinance Loans

Source: Egli (2004).

Progressive lending may also work as an enforcement mechanism in microfinance group lending programs (Egli, 2004). To date, a number of pioneering research studies in microfinance group lending elucidated peer pressure as an identical and a key enforcement mechanism. However, the research studies of Morduch (1999) and de Aghion and Morduch (2000) argue that group lending has become less prominent in some of the established microfinance programs, and individual lender–borrower contracts characterize the core component of microlending programs. Consequently, along with group pressure, dynamic incentives like progressive lending also witnessed its role as an enforcement device.

Survey Design and Data

The data were derived from a survey of 106 women SHGs and 318 women members in 10 villages in the state of Karnataka, India, between 2006 and 2007. Five of the villages were supported by the Sri Kshethra Dharmasthala Rural Development Project® (SKDRDP), Dharmasthala, and Dakshina Kannada, and the other five were supported by the Sanghamithra Rural Financial Services (SRFS), Mysore. The rationale behind the selection of SRFS is that it is the only not-for-profit company microfinance institution (MFI) registered under the Indian Companies Act, 1956, and has been working in the state for more than 10 years with wide experience in microfinance services in Karnataka. The SRFS also extends microfinancial services in neighboring states like Tamil Nadu and Andhra Pradesh. However, the motivation behind the selection of SKDRDP was that it is the largest (in terms of reaching the number of poor people and loan outstanding) nongovernmental organization (NGO) and MFI working in the field of microfinance in Karnataka.

To study the progressive lending in groups, a multistage random sampling technique was used in the selection of study units (SHGs and its members). Accordingly, at the first stage, the operational area of the SRFS, Mysore district and Dakshina Kannada district, from SKDRDP were selected. Selection of the study area was done keeping in view that it should satisfy the two criteria, namely, (a) cover (formed/linked to the MFI) the maximum number of SHGs and rural poor households and (b) the district should be the first operational area so that we have matured groups and members for the study. The second stage of sampling is the selection of taluks. The two taluks, namely, T. Narasipura and Belthangady from the SRFS and SKDRDP operational areas were selected by using the same criteria that were used for the selection of districts. The third stage of sampling covered the selection of villages. From each taluk, the village list was prepared with number of SHGs formed/linked to the MFI. Consequently, the top five villages having the largest number of SHGs and members were selected from each taluk. The fourth stage of sampling involved the selection of SHGs.

In each selected village, currently linked SHGs with MFI list was prepared. Accordingly, 25% of SHGs were selected randomly from each village. In all, 106 SHGs (53 SHGs from each taluk) were randomly selected from 10 villages. From each randomly selected SHGs, 25% of the member households were selected randomly. In total, 318 households, 159 households each from Belthangady and T. Narasipura taluk, were selected for the study. The sample of SHGs and members across MFIs/taluks and villages is presented in Table 2.

The Sample SHGs Across MFIs, Taluks, and Villages

Source: Primary survey.

Note: SHG = self-help group; MFI = microfinance institution; SRFS = Sanghamithra Rural Financial Services; SKDRDP = Sri Kshethra Dharmasthala Rural Development Project. Figures in parentheses denote percentage to the total number of sample SHGs in particular taluk.

Two interview schedules were prepared to collect the data from SHGs and its members. The data on basic details of the group, such as, age of the SHG and its size, number of loan cycles, rate of interest, and so on, were collected from the SHGs. Furthermore, data related to occupation, level of education, marital status, caste categories, number of loan cycles, loan utilization pattern, and so on were collected from the members. The study used a linear regression model to find out the determinants of progressive lending of groups to its members.

Empirical Results

Pattern of Progressive Lending: From SHGs to Its Members

The practice of repeat loans with higher doses of credit is followed by SHGs in their group lending thereby enticing prompt repayment. It is evident from Table 3 that across the loan cycles, the average loan amount is increasing; it shows that groups not only provide a continuing series of loans but also the size of the loan increases over the loan cycles. For the total sample, the mean loan size increases from Indian Rupees (Rs.) 17,560 for the first loan cycle to Rs. 1,22,640 for the sixth loan cycle. It indicates that these SHGs show progressive lending, with amounts rising up to 698% of the initial average loan. In addition, the per capita credit (PCC) accessed by the members in the total sample rose from Rs. 1,802 in the first loan cycle to Rs. 12,327 in the sixth loan cycle. It shows the member PCC amount accessed rising up to 684% of the initial loan. Nevertheless, these empirical results indicate that the progressive lending does not exists; loans seem to increase substantially over the period across the SHGs in India. It is under the progressive lending that the group tests the borrowers with small loans at the start to screen out the worst prospects before expanding the loan scale (Ghosh & Ray, 1999).

Progressive Lending (Rs.) in SHGs

Source: Primary survey.

Note: PCC denotes the per capita credit accessed by the member.

Furthermore, it is apparent from Table 3 that across the sample taluks, the average loan amount is higher in T. Narasipura taluk than Belthangady taluk. However, the PCC, up to fifth loan cycle, is higher in the groups of Belthangady taluk than in T. Narasipura. But, from the sixth loan cycle onwards, the PCC in both the study taluks is almost equal. Furthermore, the average number of members who accessed credit for the entire sample was found growing from 10.13 for first loan to 12.14 for sixth loan. Across the taluks, over the loan cycle, the groups in T. Narasipura taluk have served more number of members than the groups in Belthangady taluk (average number of members is 12.04 to 15.54 in T. Narasipura and 8.23 to 10.29 from the first loan cycle to sixth, respectively). The major reason for such difference across the taluks is that the size of the groups in T. Narasipura taluks are quiet large than that of Belthangady taluk.

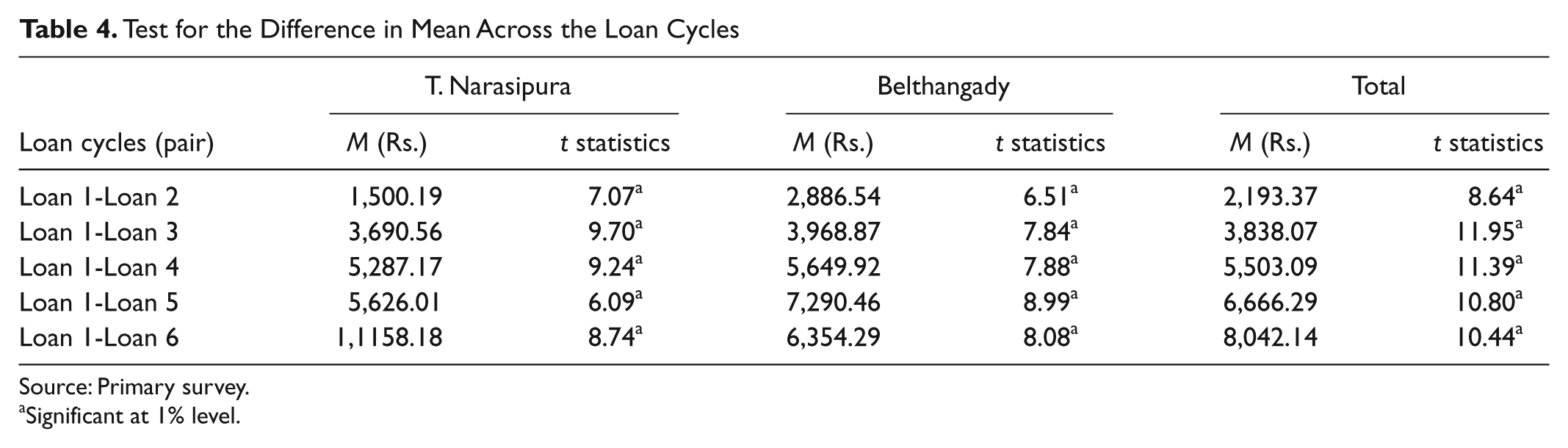

To examine whether or not there is any significant difference in the average loan lent by groups over various loan cycles, the paired-sample t test 1 for mean has been conducted. The result is given below in Table 4. The paired-sample t test tests the hypothesis that there is no difference in the mean of loan cycles across taluks and in the entire sample. The results indicate that the t statistics are significant and the mean of loan cycles differ across the loan cycles. In fact, the observed mean difference is higher in T. Narasipura taluk than in Belthangady taluk.

Test for the Difference in Mean Across the Loan Cycles

Source: Primary survey.

Significant at 1% level.

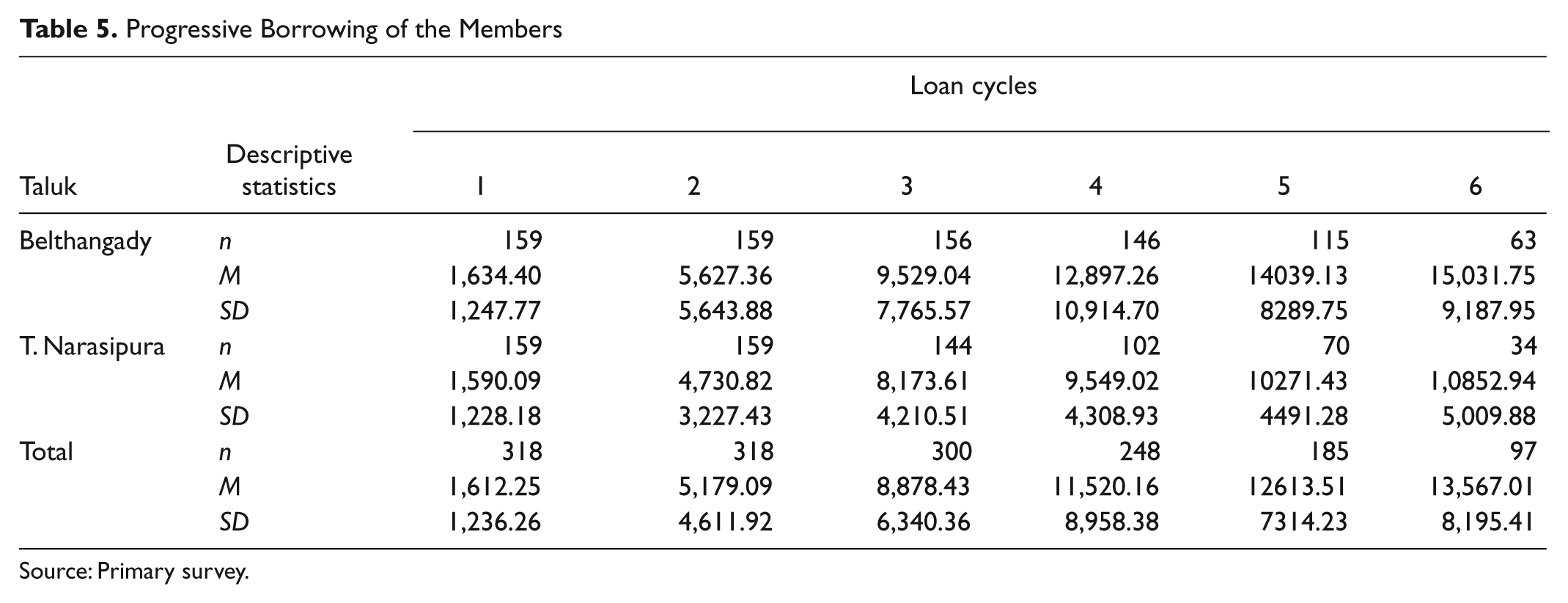

Pattern of Progressive Borrowing in SHG Members

The ultimate purpose of group lending methodology in microfinance is to provide timely and continuous credit to the members. The continuity of accessing credit is depending on the borrowers prompt repayment of past loan. Therefore, the progressive borrowing by the microfinance members from SHGs shows the effectiveness of dynamic incentives practiced in group lending. From Table 5, it is evident that in both the study taluks, the average borrowing of the member has increased over the first loan to sixth loan cycle. The empirical results in Table 5 clearly shows that SHGs are testing member’s creditworthiness with small loan amount and over the period, members are able to access larger amount of credit. Furthermore, repayment of previous loan is benefited through an incentive of greater loan credit in the current period. Thus, prompt repayment of credit directs progressive lending as a dynamic incentive for the members in microfinance lending.

Progressive Borrowing of the Members

Source: Primary survey.

Pattern of Loan Utilization Across Various Loan Cycles

The increased loan cycle not only depicts the pattern of progressive lending/borrowing but also represents where the credit has been utilized and its likely return to the investor. Generally, a borrower needs credit for many purposes, starting from small amount of money for the consumption requirements to a large amount for the productive needs. Theoretically, the initial steps in progressive borrowing will have a small amount that is generally used for consumption or emergency purposes. It is also evident from the table that the initial loan cycles are largely used for consumption purposes and later cycles are utilized on various income-generating activities, like, microenterprises, dairy, petty business, and so on.

The empirical results from Table 6 clearly illustrate that as the loan cycles increases with larger amounts, the utilization spreads across income-generating activities and housing purposes. It is found that poor people give more priority for the development of housing and buying the housing requirements. Furthermore, even some amount of investment is also found through investing on jewelry like gold and silver as a risk-baring or risk-mitigating factor for future.

Pattern of Loan Utilization Across Loan Cycles

Source: Primary survey.

Note: Bel = Belthangady taluk; T.N = T. Narasipura taluk; IGA = income-generating activity. The figures in parenthesis represent percentage to the total number of observation in particular categories of loan utilization.

Determinants of Progressive Lending

Theories based on sequential stage of group development are based on the identification of definite phases in the life cycle of the group. According to Tuckman (1965), each group will pass distinct stages of development like, forming, storming, norming, and performing. Thus, the age or the level of maturity of the group will play a dominating role in determining the progressive lending of the groups.

To test the relative importance of the factors that determine the progressive lending in groups, a log-linear regression model was estimated by using the ordinary least squares method. We found that the semilog functional form was better than the nonlog form to estimate the determinants of progressive lending in groups. To justify the semilog specification, we tested the distribution of residuals for normality. The validity of the t test and F test also depended on a normal distribution. In the normal probability (P-P) plot, we found that the residuals were more close to the normal probability curve in the case of semilogarithmic specification than the nonlogarithmic specification. Therefore, the results supports exercising regression method taking natural logarithm of average loan amount (total amount of loan divided by number of loan cycles considered as progressive lending) in the groups In this model, average loan amount in the group is the dependent variable, and age, size of the group, per capita savings (PCS), PCC accessed, and MFIs that is credit linked with groups are the explanatory variables. Description of independent variables and its expected signs is given in Table 7.

Description of Independent Variables

Note: mfi = microfinance institution; SKDRDP = Sri Kshethra Dharmasthala Rural Development Project; SHG = self-help group.

In analyzing the determinants of progressive lending SHGs, the age of the group is considered as an explanatory variable. The SHGs that exist for a long period with continued savings makes the group to increase its cycle or size of loans. It is expected that as compared with the Age 1, Age 2 and Age 3 groups are likely to positively influence on progressive lending of the SHGs. The PCC accessed by the member is considered as an explanatory variable in the model. It explains the reliability of SHGs in delivering credit services to the members in a more convinced manner. Thus, benefits to the members will keep the SHG alive and sustainable. It is expected that the PCC accessed by the member will positively influence the progressive lending of the SHGs. Generally, the microfinance groups depend on MFIs for financial requirements. Thus, MFI plays an important role in the availability of the credit. Group size is considered as an explanatory variable.

Most of the theoretical literature on group lending suggests that the group, which is too large or too small in size, may fail to achieve in increased size of loan. If the group is too big, then the strength of peer pressure and monitoring will be very weak due to information asymmetries and if it is extremely small in size, then there may be failure of “economies of scale” in its operation. Thus, in this model as compared with Group 1 (less than 10 members), Group 2 (10 to 15 members) and Group 3 (more than 15 members but less than 20) are likely to positively influence progressive lending of the SHGs.

The estimated equation is as follows.

The result indicates that there is positive association between the age of the SHGs and progressive lending. SHGs falling in Age Group 2 observed higher loan sizes by 0.1704 units compared with SHGs falling in Age Group 1. Similarly, Age 3 attained higher loan sizes by 0.3085 units as compared with SHGs falling in the Age Group 1. The coefficients of Age 2 and Age 3 are positive and statistically significant at 95% level, respectively. The coefficients of log of PCSs and log PCC accessed by the group member are positive and significant at 99% level. The size of the SHGs is positively associated with the loan size. While comparing the smallest group (Size 1), the progressive lending of Size 2 is comparatively higher at 0.2071 units and further, the Size 3 is still higher by 0.5739 units. Size 2 and Size 3 are statistically significant at 99% level, respectively. The R2 value is .61, which means 61% of the variations in progressive lending of the SHGs were explained by the included variables in the model.

Conclusion

Microfinance has evolved across the world into various operating forms and to a varying degree of success. One such form of microfinance has been the development of the SHG movement; it has become an increasingly utilized tool for providing credit access to the poor in India. The SHG lending approach accounted for strong repayment rate and continuous access to credit services even without collateral. The empirical studies argued that the ability of groups to self-select peer members mitigate adverse selection problems in credit market. Furthermore, it is argued that much of the screening of borrowers actually occur ex-post to group formation in the form of group expulsions. To date, to a great extent, the microfinance literature had discussed the group pressure as an enforcement device, rather than stressing the dynamic incentives like progressive lending.

The empirical result in this study reveals that the groups increased their loan sizes by many fold and it shows that they are following the dynamic incentives like progressive lending. The study indicates that the practice of principle of progressive lending has contributed in improving the loan size across the groups and regions. The supply of financial services through the SHGs to the poor is found to be efficient and sustainable. It has contributed in filling the gap between the relatively low cost but inaccessible formal banking sector, and the accessible, but high cost informal sector.

However, this article is limited in its approach and data to explore the dark side of progressive lending, such as—as compared with individual lending models—the group lending imposes significant costs to borrowers in managing the microfinance business. Here, the borrowers are held financially responsible for their screening mistake, by having no/small amount of future credit services. Furthermore, the lending institutions always may use the credible threat of refusing credit to the expelled members of groups. As a result, the critical poor would be declined to avail any benefit of microfinance even from the alternative lending institutions. Finally, to what extent progressive lending in microfinance has helped in meeting the capital requirements of member projects and its sustainability?

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.