Abstract

Our paper investigates how qualified foreign institutional investors (QFII) impact stock liquidity in the Chinese A-share market using data for 2005 to 2019. Contrary to previous findings, we find that QFII enhance stock liquidity. Specifically, QFII’s participation is negatively associated with the individual stock illiquidity and positively related to stock trading volume. Moreover, using a step-by-step procedure, we provide evidence that QFII raises stock liquidity by ameliorating information asymmetry. QFII will attract more market attention and improve firm disclosure quality. We address possible endogeneity with fixed effects and instrumental variables, and our findings are robust to self-selection bias, stock market shocks, and alternative explanatory variables.

Introduction

To enhance the efficiency of resource allocation in the capital market and improve the corporate governance of listed companies, China started to introduce foreign institutional investors several years ago. In 2002, the China Securities Regulatory Commission (CSRC) issued the Provisional Measures on the Administration of Domestic Securities Investments of Qualified Foreign Institutional Investors (QFII), allowing foreign qualified institutional investors (QFII) to convert foreign funds into RMB for direct investment in the A-share market. This regulation was published in December 1, 2002 by the China Securities Regulatory Commission (CSRC), when approved QFII were permitted to make their first trades in the A-share stock market on July 9, 2003. QFII are defined as overseas fund management firms, insurance companies, securities companies, and other asset management institutions approved by the CSRC to invest in China’s security market. QFII can exchange the host country’s currency into RMB and then invest in the Chinese market through a special account established in China. Since then, the QFII scheme has played a significant role in ameliorating the opening of China’s stock market to the outside world. In September 2019, China announced that it would abolish the investment quota restrictions on Qualified Foreign Institutional Investors (QFII) and Renminbi Qualified Foreign Institutional Investors (RQFII) to facilitate financial reforms and opening. With the continuous entry of foreign capital into the Chinese stock market, what QFII brings to the Chinese stock market has become a major focus of academia and the policy community.

Currently, with the rapid development of global financial markets, the influence of foreign institutional investors on the domestic stock market is becoming increasingly important and attracting more attention from scholars worldwide. However, there is still a heated debate on the impact of foreign institutional investors on the liquidity of the stock market. One stream of literature argues that foreign investors may have more information advantages for international markets (Ferreira & Matos, 2008; Maffett, 2012) or reduce the number of shares available to the public for trading (Brockman et al., 2009; Brockman & Yan, 2009; Rhee & Wang, 2009; Rubin, 2007). For these reasons, foreign investors, especially foreign institutional investors, will increase the information asymmetry of stocks, which will finally lead to a decline in stock liquidity. In contrast, other studies hold that foreign investors can diversify the types of shareholders for domestic companies and enhance the internal and external corporate governance of listed companies. Therefore, foreign investors will ultimately reduce information asymmetry and increase the liquidity of stocks (Vo, 2019; Wei, 2010). QFII’s investment has existed in China for approximately 20 years, and the ownership proportion of foreign institutional shareholders in listed companies is still increasing. However, what benefits can be reaped from QFII’s participation in China’s stock market remains controversial, especially for stock liquidity. In this paper, from the perspective of information asymmetry, we empirically study the causal relationship between QFII’s share holdings and stock liquidity in China in exploring the actual effect of QFII’s participation on stock trading liquidity.

Our research question is important for several reasons. First, although many articles (Deng et al., 2018; Ng et al., 2016) have surveyed the relationship between foreign investor ownership and stock liquidity around the world, most of these studies focus on countries or regions without capital controls. For quite a long time, China has controlled the inflow of foreign capital, leading to a very low shareholding proportion of foreign institutional investors in the A-share market. Therefore, it is necessary to study foreign institutional investors in China. On the one hand, such research can help us understand the role of foreign institutional investors under capital control; on the other hand, it further elucidates how foreign institutional investors affect the stock market under a low investment ratio. Second, there is dramatic differences between the QFII schemes of the Chinese market and of other emerging markets. Unlike many emerging economies wherein foreign institutional investors are permitted to hold more than 50% of the free-floating value of the equity market, China’s QFII scheme is restrictive: The total shares held by each (all) QFII in one listed company are not permitted to exceed 10% (20%) of the total outstanding shares of the company. China’s QFII scheme allows for an interesting case study of the relationship between foreign institutional participation and stock market liquidity in an environment characterized by low levels of foreign institutional ownership. This paper helps illustrate the role of foreign institutional investors under the restrictions of low shareholding. Third, liquidity is an important indicator of the efficiency of the stock market. Adequate liquidity helps investors complete purchasing or selling requests for stocks faster and is also an important guarantee for corporations seeking to raise listing financing and refinancing. A better understanding of the role of foreign institutional investors will help further develop and promote the efficiency of domestic financial markets.

In this paper, we mainly examine two issues. First, we investigate whether the participation of QFII in China’s A-share market can promote stock liquidity. Specifically, we examine whether the percentage of QFII’s share holdings is associated with higher stock liquidity. To test the above hypothesis, we use two indicators to measure the liquidity of stocks, the trading volume of stocks and the illiquidity ratio from Amihud (2002). Stock trading volume has been widely used as a measure of liquidity (Brockman & Yan, 2009; Ding et al., 2017). The greater the trading volume is, the better the liquidity level becomes. Following Chan et al. (2008), Lesmond (2005), and Hearn and Piesse (2013), we also use the illiquidity ratio as a measure of liquidity. This ratio is the absolute return divided by the trading volume, which can effectively measure the price impacts of the unit trading volume (in dollars) in the stock market. The higher the illiquidity ratio is, the lower the illiquidity level becomes. Second, this paper further discusses how QFII raises stock liquidity in China. We confirm that QFII advances stock liquidity through an information improvement channel using a step-by-step procedure. Market attention from financial analysts and the KV index are considered important indicators of the information environment and information disclosure quality of listed firms, respectively. The greater market attention from financial analysts becomes (more analysts and reports), the more investors in the market know about the given company, and the better the information environment of the company becomes (Chen et al., 2010; Hsieh et al., 2016; A. H. Huang et al., 2014; Nielsen, 2004). Ascioglu et al. (2005) and O. Kim and Verrecchia (2001) investigate the relationship between disclosure quality, returns, and trading volume. The authors believe that the lower the KV index is, the better the quality of information disclosure is. Therefore, we use analysts’ attention, report attention, and the KV index as measurements of information asymmetry. In the step-by-step regression, we first regress QFII’s ownership on the information asymmetry variable to test whether QFII’s ownership has a significant impact on information asymmetry. Then, we test whether the information asymmetry variable has a significant effect on stock liquidity when QFII’s shareholding and information asymmetry are controlled at the same time.

Using data on the Chinese A-share market for 2005 to 2019, this paper empirically finds that QFII in China’s A-share market can significantly increase the stock liquidity of listed companies. When QFII’s shareholding ratio increases by 1%, the illiquidity ratio of the stock will decrease by approximately 1%, and the logarithmic trading volume will likely increase by 2%. To further confirm whether QFII increases liquidity by improving the information asymmetry of listed companies, with a step-by-step regression test, we find that QFII’s ownership is negatively correlated with the information asymmetry level (analysts’ attention, report attention, and the KV index). After adding analysts’ attention, report attention, and the KV index to the baseline regression, we find evidence that information asymmetry level variables reduce stock liquidity, and they all significantly explain stock liquidity. These findings are consistent with the view that foreign institutional investors can reduce information asymmetry and then increase trading activity and liquidity.

In this paper, we use the fixed effect model, which can mitigate the omitted variables problem, to estimate our regression. We also adopt the 2SLS method to further alleviate possible reversal causality problems by taking lagged QFII’s ownership and the natural logarithmic distance between firms’ headquarters and Beijing as instrumental variables. The empirical results of the 2SLS regression remain the same as those of the fixed effect model. In addition, a Heckman two-step regression (Heckman, 1979) for QFII’s ownership and information asymmetry levels shows that our results are not affected by self-selection. Finally, when we employ the dummy variable of QFII’s shareholdings and the volume of QFII’s shareholdings as substitute measures of QFII’s participation or take the stock market shocks of 2007, 2008, and 2015 into account in the robustness test, the quantitative relation between QFII’s participation and liquidity remains the same.

Our contributions are as follows. First, this paper discusses how QFII affects liquidity in China’s stock market, extending the literature related to institutional investors. In previous studies, most of the research has focused on the impact of domestic institutional investors’ behavior on the financial market (Chiao et al., 2010; Impavido, 1998; Ng et al., 2016; Tan et al., 2008), while our paper focuses on foreign institutional investors. Second, there has been a long-standing debate about the impact of foreign institutional investors or QFIIs on liquidity, and our article provides new evidence on the debate over QFII’s impact on liquidity. Some literature suggests that foreign institutional investors’ adverse selection effect may lead to a decrease in liquidity (Brockman & Yan, 2009; Rhee & Wang, 2009; Wang et al., 2022). However, another type of literature argues that foreign investors have a positive effect on the liquidity of local stock markets (Amihud & Mendelson, 2012; Ding et al., 2017). Our research provides new evidence for this debate, indicating that foreign investors have a positive impact on the liquidity of local stock markets. In contrast to Wang et al. (2022), our study found that QFII has a positive impact on stock market liquidity, primarily due to attracting more market attention and improving firm disclosure quality, thereby ameliorating information asymmetry. Third, this article provides new evidence that foreign investors or QFII can increase liquidity through information channels. Ding et al. (2017) believe that the improvement in liquidity does not occur through the information friction channel, but rather the real friction channel. Compared with Ding et al. (2017), our evidence show that the information friction channel still works. QFII can promote liquidity through attracting more market attention and improving firm disclosure quality. Fourth, this paper further discusses the relation between QFII participation and liquidity under different information environments and information disclosure conditions, extending the research on information asymmetry (Albu & Albu, 2012; K. H. Chung et al., 2010; Frankel & Li, 2004; Kalay, 2015; L. Zhang & Ding, 2006).

The rest of the paper is structured as follows. Section “Literature Review” provides a literature review and our research hypotheses. Section “Hypothesis Development” explains the measurement of liquidity for individual stocks and develops the econometric design applied. Section “Econometric Design” describes the data source used and provides descriptive statistics for the studied variables. Section “Data” reports the empirical results. Section “Empirical Results” presents various robustness checks. The final section concludes.

Literature Review

The Determination of Stock Liquidity

Firstly, the liquidity of stocks is affected by market microstructure or trading systems such as market makers, exchange market manipulation rules, short selling mechanisms, margin trading systems. The theoretical analysis in Grossman and Miller (1988) suggest that market makers can resolve the problem of asynchronous trading orders between two parties, diversify price risks caused by delayed trading, reduce transaction costs, and improve stock liquidity. Cumming et al. (2011) construct foreign ownership and market manipulation indices to study the impact of exchange regulation on market liquidity. They found that the more effective the exchange regulation on market manipulation, the better the market liquidity. Schwartz (2021) argue that in a non-frictionless market, three factors matter: risk, return, and liquidity. Illiquidity is closely associated with price discovery being a noisy, dynamic process.

Secondly, the liquidity of stocks can be influenced by the behavior of institutional investors, controlling shareholders, and other investors. Moshirian et al. (2017) use intraday data from 39 markets over 15 years and show that liquidity commonality is driven by both market-level and firm-level factors. The correlated trading captured by domestic institutional ownership is positively related to liquidity commonality, whereas there is no such effect for foreign institutional ownership. Deng et al. (2018) identify a U-shaped relation between foreign institutional ownership and stock liquidity commonality. Li et al. (2022) employ five IVs for the 2SLS regression supporting the view that foreign investors significantly reduce stock liquidity uncertainty. They believe foreign investors introduce good governance practices and socially responsible philosophies to Chinese listed firms, reducing stock liquidity uncertainty.

Thirdly, the liquidity of stocks can be affected by characteristics of listed companies, such as ownership structure, information disclosure, and financial performance. Brockman and Yan (2009) investigate the impact of ownership concentration on the liquidity of stocks. Schoenfeld (2017) based on the research of index fund information disclosure, find that voluntary information disclosure of management is conducive to improving the liquidity of stocks.

Fourthly, the liquidity of stocks can be influenced by macroeconomic factors such as oil prices, monetary policy, and policy uncertainty. Chordia et al. (2005) argue that there is a connection between monetary liquidity and market liquidity. During a crisis, market liquidity may increase with the expansion of monetary policy. Q. Zhang and Wong (2022) use high frequency tick-by-tick intraday data and an innovative method to derive oil demand and supply shocks, and find evidence that oil shocks driven by demand lower stock liquidity, whereas oil supply shocks have the opposite effect. Q. Zhang and Wong (2023) provide strong empirical evidence that elevated oil price uncertainty has a significant and negative influence on stock liquidity. Mbanyele (2023) shows that economic policy uncertainty disproportionately contributes to stock illiquidity and the impact is mainly prominent for high risky companies, small firms and firms in competitive industries.

Foreign Institutional Investors and Stock Market

Foreign institutional investors can affect listed firms’ behavior such as governance, firm earnings management, cost of equity capital, voluntary disclosure, and so on. Aggarwal et al. (2011) suggest that international portfolio investment by institutional investors promotes good corporate governance practices around the world by analyzing portfolio holdings of institutions in companies from 23 countries during the period 2003 to 2008. W. Huang and Zhu (2015) find that Qualified Foreign Institutional Investors (QFII) have greater influence over the controlling state shareholders than local mutual funds and involving foreign institutional investors in corporate governance practices can significantly reduce expropriation by controlling shareholders in emerging markets using Brazil as a case study, Hillier and Loncan (2019) find that foreign ownership has a positive impact on the financing side by reducing cost of capital. J. B. Kim et al. (2019) find that Foreign institutional investors are likely to demand high-quality audits to mitigate the information asymmetry they face and facilitate their external monitoring when they invest overseas. Employing a large sample of 13,860 firms in 41 economies from 2000 to 2017, Gu et al. (2023) document that the ownership by foreign institutional investors (FIIs) is negatively associated with firms’ real earnings management (REM). Tsang et al. (2019) document that foreign institutional investments lead to improved voluntary disclosure, and their impact is larger than that of domestic institutional investors. J. Zhang et al. (2023) use an online support vector quantile regression to examine the impact of QFII on the volatility of China A-share stock market. They found that QFII have an unsystematic destabilizing effect during different financial stress times.

Moreover, foreign investors also have an impact on the liquidity of stocks of listed companies, yet there is still debate on the nature of this impact. Rhee and Wang (2009) find that overseas shareholders have information advantages in emerging markets, foreign ownership increases bid-ask spreads, reduces market depth, and has a negative effect on the liquidity of stocks. Similarly, the research of Brockman and Yan (2009) suggest that foreign ownership affects the shaping of a company’s information environment, exacerbates information asymmetry, and decreases the liquidity of stocks. However, Amihud and Mendelson (2012) argue that foreign ownership can diversify risks, enrich the ownership structure of listed companies, and increase the liquidity of stocks. Ding et al. (2017), using QFII to measure foreign ownership, find that foreign investors improve the liquidity of stocks in the trading process.

Hypothesis Development

How foreign institutional investors influence stock liquidity remains controversial. One stream of literature suggests that foreign institutional investors decrease stock supply or increase information asymmetry, thereby reducing stock liquidity. This research shows that foreign institutional shareholders have more professional international market information; more investment experience and better capabilities in collecting, processing, and analyzing information. Hence, foreign institutional investors are informed traders (Brockman & Yan, 2009) who make use of their advantages, which will increase information asymmetry in stock markets and finally reduce the liquidity of stocks. Ferreira and Matos (2008) find that foreign institutional shareholders have more investment and management experience with listed companies than local investors, and their research reports on local listed companies usually contain more information, which increases the information asymmetry of stocks. Kho et al. (2009) believe that due to their considerable resources and investment experience in the international capital market relative to local investors, foreign shareholders can better analyze the premium information of the local market, affording them information advantages.

In addition, studies also discuss imperfect competition caused by the large block transactions of foreign institutional shareholders. Rubin (2007), Brockman et al. (2009), Rhee and Wang (2009), and Tam et al. (2010) indicate that overseas institutional shareholders purchase a large volume of free-floating stocks in the market, lowering the stock supply and ultimately decreasing stock liquidity.

Contrary to the above context, other scholars hold that foreign institutional investors can improve the information situations of domestic listed companies by promoting stock price informativeness or corporate governance, thus reducing information asymmetry and increasing stock liquidity. Subrahmanyam (1991) believes that competitive behavior among informed traders will incorporate more information in the stock price, increasing the information efficiency of the stock. The improvement of information efficiency will increase the liquidity of the stock. Moreover, the introduction of foreign investment can ameliorate the governance and information disclosure quality of the company, which can diminish the potential risk or transactional costs (Gabaix et al., 2006). Hence, such investment positively influences liquidity. Boone and White (2015) find that the higher the proportion of foreign institutional ownership is, the lower the degree of information asymmetry becomes. This is the case because foreign institutional investors can strengthen the external regulatory environment, bolster external monitoring, and raise information disclosure quality.

Kalev et al. (2008) believe that foreign institutional shareholders are detached from local markets. Therefore, foreign institutional shareholders are at a disadvantage in obtaining information. Therefore, foreign institutional shareholders are more likely to become “noise traders,” acting as liquidity providers and improving stock liquidity.

Overall, this paper proposes two opposing hypotheses:

Hypothesis 1a: QFII reduces the stock liquidity of listed companies in China.

Hypothesis 1b: QFII enhances the stock liquidity of listed companies in China.

Generally, it is widely believed that more attention from analysts can accelerate the process of integrating information into stock prices and improve market efficiency. Givoly and Lakonishok (1979) found significant changes in stock prices and trading volumes within a certain time window after the release of analysts’ research reports, showing that the information mined by analysts can be reflected by market prices. Bushman et al. (2005) also find that the better the enforcement of laws restricting internal trading becomes, the greater the demand for the company’s information by external investors becomes; hence, the number of security analysts who act as the main information intermediaries will increase. This mechanism can finally improve the information efficiency of the market (Bushman et al., 2005). A. H. Huang et al. (2014) also note that analysts can disseminate information that is not reported directly. Therefore, when more analysts pay attention to a listed firm and publish more research reports, the company will enjoy a better information environment with a lower degree of information asymmetry.

Foreign institutional investors may strengthen the quality of information disclosure in at least three ways. First, foreign institutional investors can monitor earnings management by attracting market attention and exerting pressure on corporate managers to improve the quality of information disclosure (Boone & White, 2015; R. Chung et al., 2002; Dyck et al., 2019; Lel, 2019). Second, foreign institutional investors can influence stock prices through voting rights or holding or selling stocks. Thus, to maintain stock prices, corporate managers are encouraged to improve the quality of information disclosure and internal governance (Aggarwal et al., 2011; Chidambaran & Prabhala, 2003; Gulen & O’Brien, 2017). Third, foreign institutional investors can sue corporate managers for their harmful behaviors (Cheng et al., 2010). Under this legal threat, corporate managers will be more active in improving the quality of information disclosure (Pukthuanthong et al., 2017; Rayfield & Unsal, 2021).

To better explore the channel through which foreign institutional investors impact stock liquidity, we propose the following hypotheses on the information environment and information disclosure.

Hypothesis 2: QFII may improve stock liquidity by enhancing market attention and the quality of information disclosure in China, namely, by reducing firms’ information asymmetry.

Econometric Design

Following Brockman et al. (2009), Ding et al. (2017), and Rubin (2007), we build the following baseline regression model:

Our main independent variable,

where

In our baseline regression, we also control for firms’ ownership, financial, governance, and transaction characteristics. Ownership characteristic variables are as follows.

Firms’ financial indicators include asset size, leverage, and profitability.

Governance characteristics are measured with the following variables.

Transaction variables are as follows.

Data

Data Sources and Sample

The data for our main variables of QFII ownership, domestic institutional investor ownership, daily returns, daily trading volume, the ownership of the 10 largest shareholders, total assets, total liability, the daily stock price, floating shares, total shares, the daily turnover rate, and other basic data were all drawn from the CSMAR database. The data cover the period running from 2005 quarter 1 to 2019 quarter 4. The reason for using data up to 2019 is due to the official release of the “Provisions on the Administration of Domestic Securities and Futures Investment Funds by Foreign Institutional Investors,” by the People’s Bank of China in May 2020, which comprehensively lifted the investment quota restrictions on Qualified Foreign Institutional Investors (QFII). This was a significant structural policy impact, as the QFII were previously subject to quota management. We are concerned that this policy impact may lead to bias in the results, so we did not include data after 2019.

To eliminate the influence of external market shocks, we further remove data for 2007, 2008, and 2015. We also remove data with negative leverage. Before we estimate our regression, we first winsorize the nondummy data at the 5% level to remove the effect of outliers. Because QFII ownership shows uncontroversial minimum values, we do not winsorize QFII ownership. Our data has already been submitted to the journal.

Descriptive Statistics

The summary statistics of our main variables are reported in Table 1 and show that, on average, QFII holds approximately 1.566% of a firm’s outstanding shares. This value is slightly lower than the data cut off for 2012Q4 of 1.795% (Ding et al., 2017). Compared to many other emerging markets, this proportion is indeed very low. The Chinese stock market is relatively large in scale, and there are also many listed companies, which results in many companies that QFII does not hold shares in. Since this proportion of holdings is the average value of all companies, this will lead to a lower average value. In addition, in the Chinese market, whether it is retail investors, institutional investors, analysts, or listed companies themselves, they all attach great importance to QFII. The cultural and institutional environment in China is different from that of other general emerging markets. This high level of attention to QFII may be due to different cultural (Bashir & Yu, 2020) or institutional backgrounds (Bashir, 2021). Even though the holding proportion appears low, the information and attention brought by QFII can be higher than other general emerging markets.

Summary Statistics.

Note. This table presents summary statistics for QFII, liquidity measures Illiq and logTV, and firm characteristics. The sample covers the period of 2005 to 2019. Variable definitions are provided in Supplemental Appendix A.

Domestic institution investors (open-end funds, security, insurance, trust companies, and pension funds, etc.), in aggregate, hold approximately 4% of shares. The average illiquidity ratio is approximately 0.710. The mean log of the log trading volume is 15.56 per quarter.

Empirical Results

Preliminary Univariate Analysis

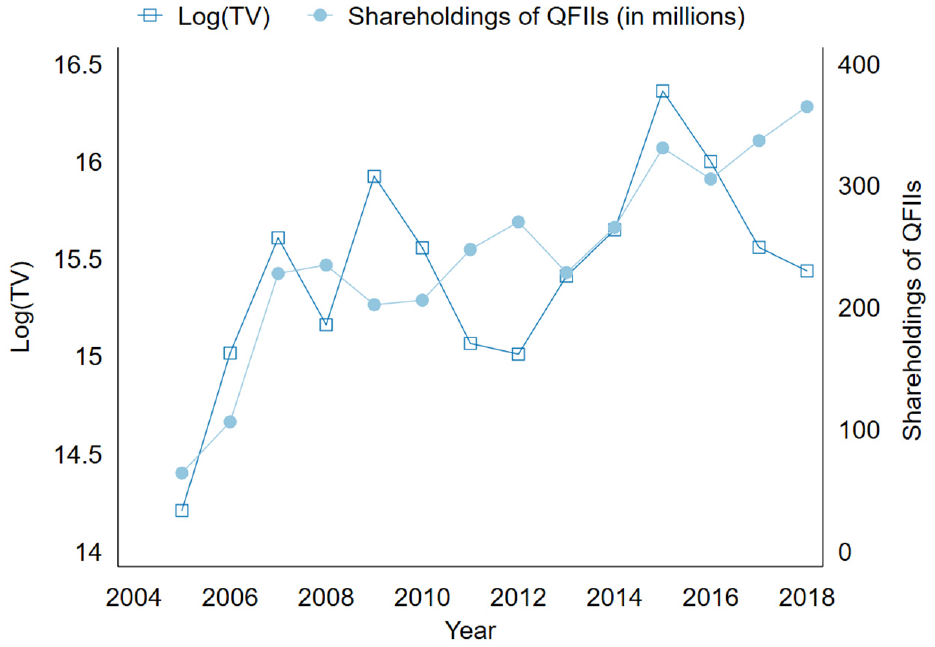

To provide a visual illustration of the dynamic relationship between liquidity and ownership, we first plot the total shareholdings of QFII (in millions) for each quarter and the two average quarterly liquidity measures, the illiquidity ratio and the logarithm of trading volume, as shown in Figure 1. The right vertical axis shows total shareholdings of QFII (in millions) for each quarter, and the left vertical axis shows liquidity for the sample period. The visual evidence provided in Figure 1 suggests a negative relationship between QFII holdings and market illiquidity over time. Figure 2 presents visual evidence of a positive relationship between QFII’s shareholdings and trading volume.

Shareholdings of QFII and illiquidity ratio.

Shareholdings of QFII and logarithm of trading volume.

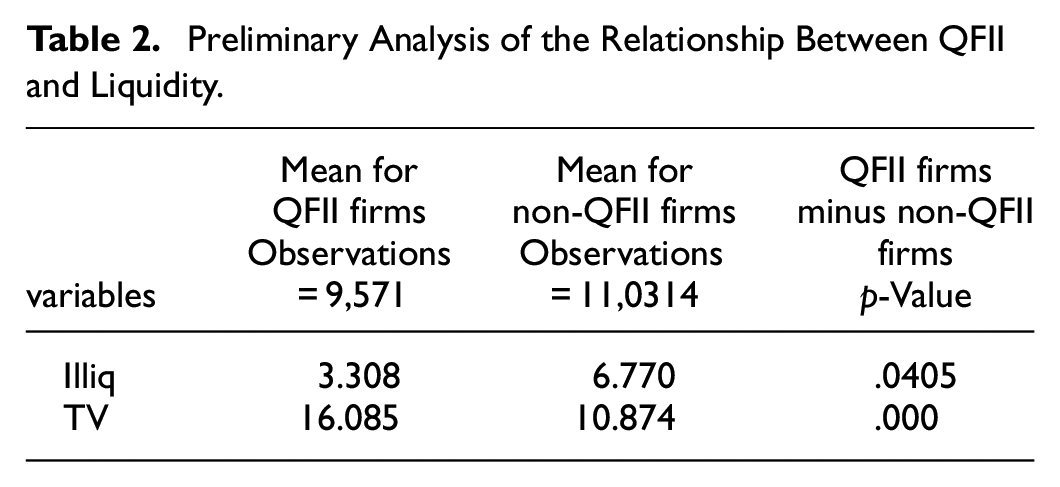

We perform preliminary univariate tests of the two liquidity measures, the illiquidity ratio, and trading volume between two subsamples of firms: those with QFII and those without QFII (non-QFII firms). We assume that if QFII participation increases liquidity, different average liquidity values should be found between the two subgroups. The evidence provided in Table 2 indeed suggests that this is the case. All differences are statistically significant at the 5% level, which means that on average, stocks with investment in QFII have more liquidity.

Preliminary Analysis of the Relationship Between QFII and Liquidity.

Foreign Institutional Investor Ownership and Stock Market Liquidity

Table 3 shows the regression results of model (1). Our focus is on the link between foreign institutional ownership and stock liquidity. The first two regressions presented in columns (1) and (2) show the regression results for QFII ownership with the Amihud illiquidity ratio applied as the dependent variable. The estimated coefficient of qualified foreign institutional investor ownership (

QFII Ownership and Stock Liquidity.

Note. This table reports regression estimates of models where the dependent variables are the illiquidity ratio (Illiq, Columns 1–3) and the natural logarithm of trading volume (logTV, Columns 4–6). All models include industry, year, and quarter fixed effects along with all time-varying control variables from Supplemental Appendix A. Robust standard errors are clustered at the firm level, and t-statistics are reported in parentheses. ***, **, and * indicate statistical significance at 1%, 5%, and 10%, respectively.

Columns (4) and (6) show the regression results obtained when using logTV as the dependent variable. The estimated coefficients of

The above evidence clearly supports the hypothesis that QFII ownership will enhance the stock liquidity of listed companies in China. Our estimation results are consistent with other previous studies (Ding et al., 2017; Vo, 2019; Wei, 2010). Ding et al. (2017) finds that foreign investor participation helps enhance the liquidity of affected stocks by promoting trade activities and price discovery. But they believe the improvement in liquidity does not occur through the information friction channel, but rather the real friction channel. Compared with Ding et al. (2017), in the following paper we will show that the information friction channel still works. Vo (2019) primarily examines the Vietnamese market and argues that foreign investors can mainly increase information efficiency in the Vietnamese stock market. Our research indicates that not only do foreign investors impact the liquidity of small emerging market, but they also influence the liquidity of large emerging market, such as China. Wei (2010) uses the 2003 US dividend tax cut as a natural experiment and finds that foreign investors can enhance market liquidity through information competition and greater liquidity trading. In following section in our paper, we will uncover that QFII in the Chinese market serves unique functions distinct from other countries—it can exert an influence on the external and internal governance of listed companies through attracting more market attention and improving firm disclosure quality. And that is why QFII can mitigate information asymmetry and improve liquidity, which is the main contribution of paper and the difference from Ding et al. (2017). Wang et al. (2022) also use the Amihud (2002) illiquidity ratio as a measure and their study find that QFII would reduce liquidity. However, their research used annual data and did not control enough variables.

QFII, Information Asymmetry, and Liquidity

To identify the detailed mechanism behind the relationship between stock liquidity and QFII’s ownership, we focus on information asymmetry. In the above section, we show that QFII will increase stock liquidity. Therefore, following Zhao et al. (2010), we use a step-by-step procedure to test whether QFII increases liquidity through information asymmetry. We build the following models:

The step-by-step procedure is divided into three steps. The first step involves testing whether coefficient

Analyst attention (logAnalyst) is defined as the natural logarithm of the number of registered analysts who write reports on a specific listed firm within a given period of time. Since analysts can collect, process and disseminate information to investors in the stock market (Gleason & Lee, 2003; A. H. Huang et al., 2014; Stickel, 1991), analysts are quite important to stocks’ information environments and market efficiency. The more analysts write reports on a stock, the better the information environment becomes and the lower information asymmetry for the stock becomes.

Report attention (logReport) is defined as the natural logarithm of the number of analysis reports focused on a specific stock written by registered analysts within a given period of time. Analysis reports serve as an important means for analysts to disseminate their views and information (Chen et al., 2010; Hsieh et al., 2016; A. H. Huang et al., 2014), and investors can receive information from these formal reports. If a listed firm attracts considerable market attention, an increasing number of research reports on this firm will likely appear. Therefore, similar to analyst attention, we believe that more formal reports on a stock indicate less information asymmetry.

Ascioglu et al. (2005) and O. Kim and Verrecchia (2001) investigate the relationship between disclosure quality, returns, and trading volume. The KV measure of firm disclosure is computed as 1,000,000 times the slope coefficient in the following ordinary least squares regression:

where

Table 4 shows the relationship between QFII ownership, analyst attention and liquidity. In columns 1 and 2, the estimated coefficients of

QFII, Analyst Attention, and Liquidity.

Note. This table shows that QFII ownership increases stock liquidity by relieving information asymmetry based on a step-by-step procedure. Columns 1 to 2 demonstrate the regression estimates of information asymmetry on QFII ownership from Equation 3. The dependent information asymmetry variable for Columns 1 to 2 is analysts’ attention (logAnalyst), which is measured by the natural logarithm of 1 plus the number of registered analysts who write reports on a specific stock within a given period of time. Columns 3 to 6 show regression estimates of liquidity on analysts’ attention (logAnalyst) and QFII ownership from Equation 4, where the dependent variables are the illiquidity ratio (Illiq, Columns 3–4) and the natural logarithm of trading volume (logTV, Columns 5–6). Variable definitions are given in Supplemental Appendix A. Robust standard errors are clustered at the firm level, and t-statistics are reported in parentheses. ***, **, and * indicate statistical significance at 1%, 5%, and 10%, respectively. All models include industry, year, and quarter fixed effects.

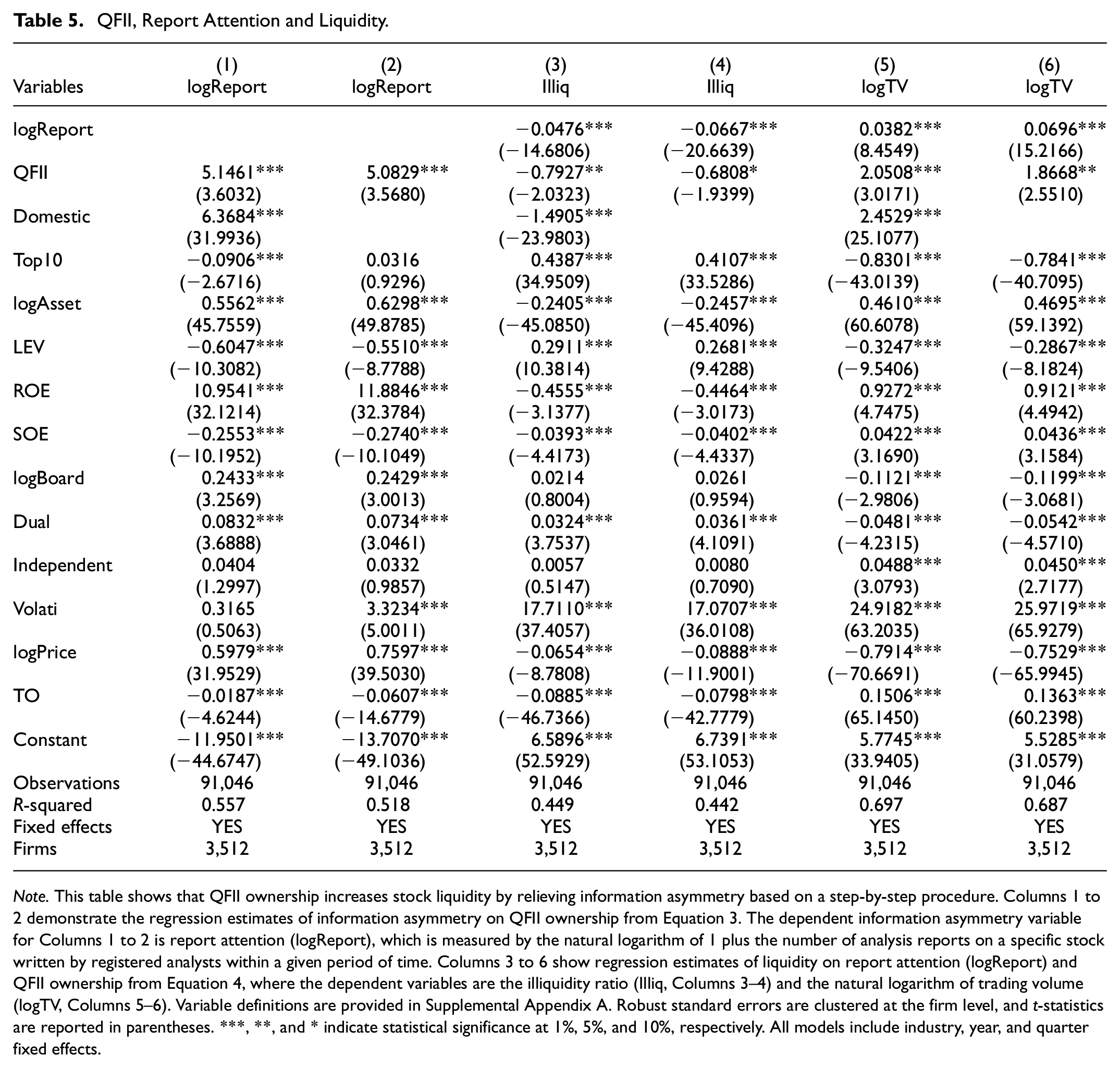

Table 5 presents the 2-step regression results for QFII ownership, reports attention, and liquidity. From the first two regressions applying logReport as the dependent variable shown in Table 5, the coefficient estimates of QFII are still significantly positive at the 1% confidence level, implying that QFII ownership can attract more report attention and reduce firms’ information asymmetry. Columns 3 and 4 show that logReport is negatively associated with the illiquidity ratio, as the coefficient estimates on logReport have a negative sign at the 1% level. From columns 5 and 6 applying logTV as the dependent variable, we also find that logReport increases stock liquidity, as the estimated coefficients on logReport are significantly positive at the 1% level. These results are consistent with those presented in Table 4 and confirm that QFII ownership enhances liquidity by relieving information asymmetry.

QFII, Report Attention and Liquidity.

Note. This table shows that QFII ownership increases stock liquidity by relieving information asymmetry based on a step-by-step procedure. Columns 1 to 2 demonstrate the regression estimates of information asymmetry on QFII ownership from Equation 3. The dependent information asymmetry variable for Columns 1 to 2 is report attention (logReport), which is measured by the natural logarithm of 1 plus the number of analysis reports on a specific stock written by registered analysts within a given period of time. Columns 3 to 6 show regression estimates of liquidity on report attention (logReport) and QFII ownership from Equation 4, where the dependent variables are the illiquidity ratio (Illiq, Columns 3–4) and the natural logarithm of trading volume (logTV, Columns 5–6). Variable definitions are provided in Supplemental Appendix A. Robust standard errors are clustered at the firm level, and t-statistics are reported in parentheses. ***, **, and * indicate statistical significance at 1%, 5%, and 10%, respectively. All models include industry, year, and quarter fixed effects.

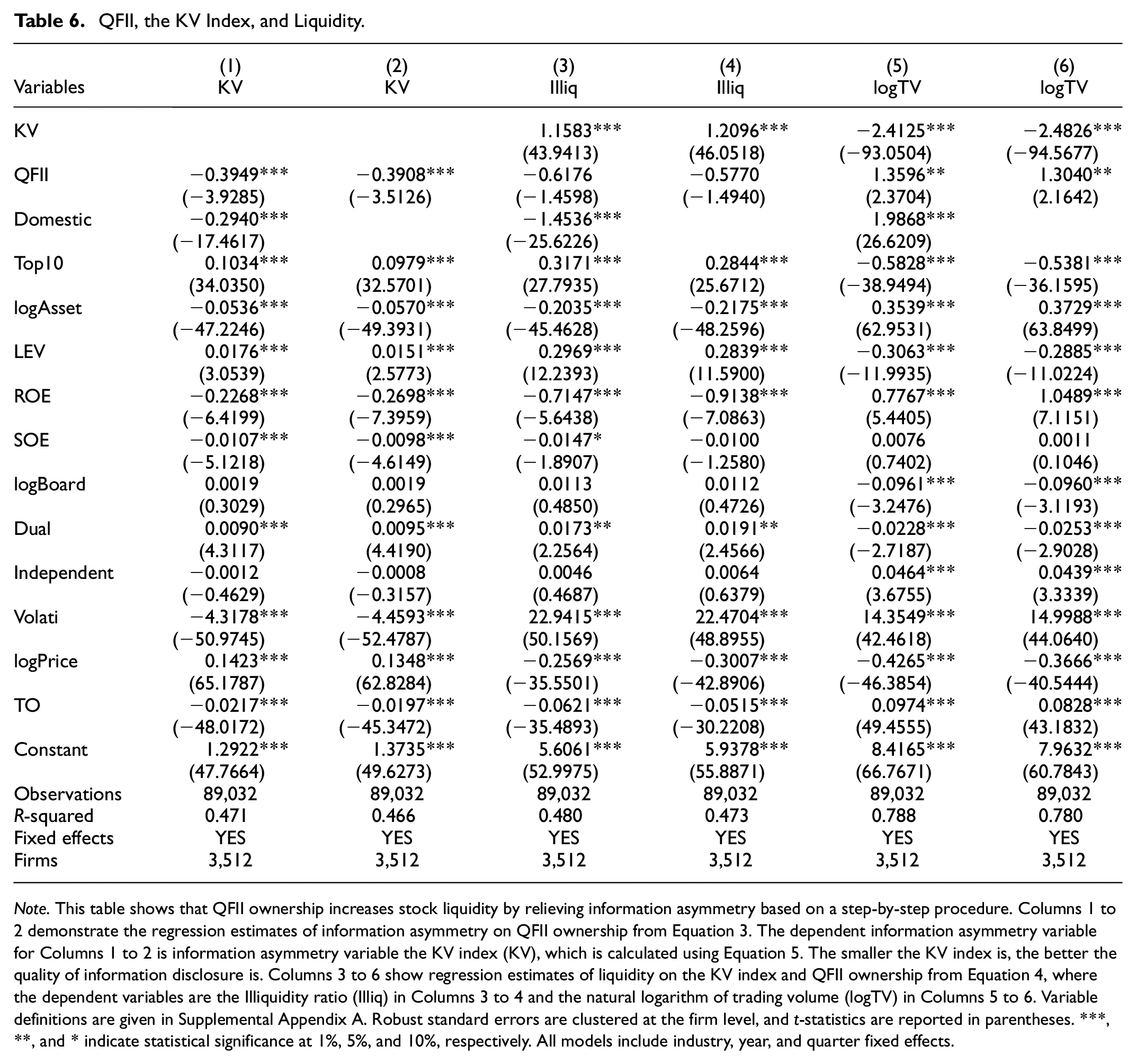

Table 6 presents the relation between QFII ownership, the KV index and liquidity. In columns 1 and 2, it is clear that QFII reduces the degree of information asymmetry, as the estimated coefficients of QFII with the KV index as the dependent variable are negatively significant at the 1% level. This evidence suggests that the higher the shareholding ratio of QFII is, the lower the KV index becomes (namely, the higher the quality of information disclosure becomes). In columns 3 to 6, we find that the KV index has a significantly positive effect on the illiquidity ratio and a significantly negative effect on logTV. These results are consistent with the results given Tables 5 and 6 and imply that low information asymmetry (a low KV index) leads to high stock liquidity.

QFII, the KV Index, and Liquidity.

Note. This table shows that QFII ownership increases stock liquidity by relieving information asymmetry based on a step-by-step procedure. Columns 1 to 2 demonstrate the regression estimates of information asymmetry on QFII ownership from Equation 3. The dependent information asymmetry variable for Columns 1 to 2 is information asymmetry variable the KV index (KV), which is calculated using Equation 5. The smaller the KV index is, the better the quality of information disclosure is. Columns 3 to 6 show regression estimates of liquidity on the KV index and QFII ownership from Equation 4, where the dependent variables are the Illiquidity ratio (Illiq) in Columns 3 to 4 and the natural logarithm of trading volume (logTV) in Columns 5 to 6. Variable definitions are given in Supplemental Appendix A. Robust standard errors are clustered at the firm level, and t-statistics are reported in parentheses. ***, **, and * indicate statistical significance at 1%, 5%, and 10%, respectively. All models include industry, year, and quarter fixed effects.

Overall, these findings show empirical support that QFII can increase analysts’ attention, report attention, and information disclosure quality and ultimately increase stock liquidity. From our step-by-step regression, we find that regardless of whether we use analysts’ attention, report attention, or the KV index as the measurement of information asymmetry, the QFII shareholding ratio is negatively associated with information asymmetry, namely, the QFII reduces the degree of information asymmetry. This is probably due to the increase in market attention and improvement in disclosure quality caused by QFII shareholding. When we add the information asymmetry variables to the regression equation, we find that the lower the degree of information asymmetry is, the higher the liquidity of the stock becomes (whether using the illiquidity ratio or the trading volume index). These results confirm our hypothesis that QFII can lead to an increase in stock liquidity through the improvement of information asymmetry.

Additional Robustness Test

Endogenous Problems and 2SLS

In research related to financial markets, endogenous problems may be serious. Another intrinsic explanation for the positive relationship between QFII ownership and liquidity is that QFII are more likely to choose stocks with better liquidity, which may lead to reverse causality problems. Therefore, in this section, we take lagged QFII ownership and the natural logarithmic distance between firms’ headquarters and Beijing as instrumental variables to mitigate concerns over reversal causality. We first compile the headquarter addresses of the listed firms from the CSMAR and use related Baidu programs to obtain the longitude and latitude coordinates of these addresses. Then, the longitude and latitude coordinates are used to calculate distances from Beijing. The longitude and latitude of Beijing used to calculate distance are 116.20 and 39.56, respectively.

A valid instrumental variable (IV) of QFII ownership must satisfy the following two conditions: (a) the IV should be correlated with QFII ownership; and (b) the IV should only affect liquidity through QFII ownership. The distance between firms’ headquarters and Beijing seems to be an appropriate candidate. Before 2019, if foreign institutional investors wanted to invest in the A-share market, they needed to obtain a sufficient investment quota approved by the relevant departments of the Chinese central government. Therefore, to obtain a sufficient quota, foreign institutional investors were obliged to apply to the China Securities Regulatory Commission and other relevant departments. Thus, many foreign institutional investors set up relevant offices or sent special personnel in Beijing to address this problem. In such institutional settings, the closer the headquarters of a listed company are to Beijing, the more convenient and likely it is for foreign institutional investors to conduct on-site research or surveys on these listed companies. Hence, short distances between firms’ headquarters and Beijing imply a higher likelihood of QFII investing in these companies. In addition, we also add lagged QFII ownership as another instrumental variable together with the distances between firms’ headquarters and Beijing.

Table 7 shows the 2SLS regression results of model (1), which takes lagged QFII ownership and the natural logarithmic distance between firms’ headquarters and Beijing as instrumental variables. The second-stage estimation results show that fitted value F_QFII from the first-stage regression is negatively related to the illiquidity ratio and significant at the 10% confidence level in columns (1) and (2). Fitted value F_QFII is also positively associated with trading volume logTV and still significant at the 1% confidence level in columns (3) and (4). These 2SLS regression results further address endogeneity concerns and confirm that QFII ownership can promote stock liquidity in China.

QFII Ownership and Stock Liquidity (2SLS Estimation).

Note. This table reports 2SLS regression estimates of models where the dependent variables are illiquidity ratio (Illiq, Columns 1–2) and the natural logarithm of trading volume (logTV, Columns 3–4). The instrumental variables in this table are lagged QFII ownership and natural logarithmic distances between firms’ headquarters and Beijing (MilesBJ). All models include industry, year, and quarter fixed effects along with all time-varying control variables from Supplemental Appendix A. Robust standard errors are clustered at the firm level, and t-statistics are reported in parentheses. ***, **, and * indicate statistical significance at 1%, 5%, and 10%, respectively.

Heckman Two-Step Regression for QFII and Information Asymmetry

While in Section “Data” we find that QFII’s ownership is negatively associated with the information asymmetry level, QFII may not reduce information asymmetry but only choose investment firms with a low degree of information asymmetry. In other words, QFII may be more likely to invest in firms with better information disclosure practices. To confirm that our results are robust and not affected by such self-selection, we use Heckman two-step regression to study the relationship between QFII and information asymmetry.

Table 8 presents the results of the Hackman two-step regression. From regression Hackman A, we find that the coefficient estimates on QFII with logAnalyst set as the dependent variable have a positive significant sign at the 1% level. In regression Hackman B, the estimated coefficients of QFII are positively significant at the 1% level when logReport is used as the dependent variable. From regression Hackman C, the coefficient estimates on QFII are negatively significant at the 5% level with the KV index set as the independent variable. The above results provide evidence that QFII ownership leads to a decrease in information asymmetry but not in self-selection.

QFII and Information Asymmetry.

Note. This table shows that QFII ownership relieves information asymmetry based on a Hackman two-step regression. Columns A, B, and C represent the Hackman two-step regression results obtained when the explained variables are logAnalyst, logReport, and the KV index, respectively. Variable definitions are provided in Supplemental Appendix A. The standard error uses a two-step variance estimator derived by Heckman, and t-statistics are reported in parentheses. ***, **, and * indicate statistical significance at 1%, 5%, and 10%, respectively. All models include industry, year, and quarter fixed effects.

Influence of the Market Shock

Liquidity and transaction costs are “two sides of one coin,” and a lower transaction cost always indicates higher market liquidity (Harris, 1990). When the stock market is greatly impacted by external forces, such as financial crises or policy shocks, the transaction cost tends to increase. As a result, the liquidity premium will increase as external shocks intensify. The Chinese stock market was not immune to the Global Financial Crisis of 2007 and 2008 and the major market shock of 2015, as most stocks encountered significant price crashes from these shocks. Therefore, in 2007, 2008, and 2015, market shocks definitely led to a decrease in stock liquidity in China. At the same time, to avoid market loss, QFII sold a large number of their shares actively or passively, which decreased QFII’s ownership significantly. Thus, there may be a positive relationship between QFII shareholding and liquidity for 2007, 2008, and 2015. However, this relationship is caused by external market shocks and is not driven by QFII themselves. Therefore, we initially remove data for 2007, 2008, and 2015 for our main regressions.

From our main regressions excluding data for 2007, 2008, and 2015, we verify that QFII increase stock liquidity. To confirm whether the influence of external market shocks affects our results, we further include data for 2007, 2008, and 2015 and then reestimate Equation 1 again.

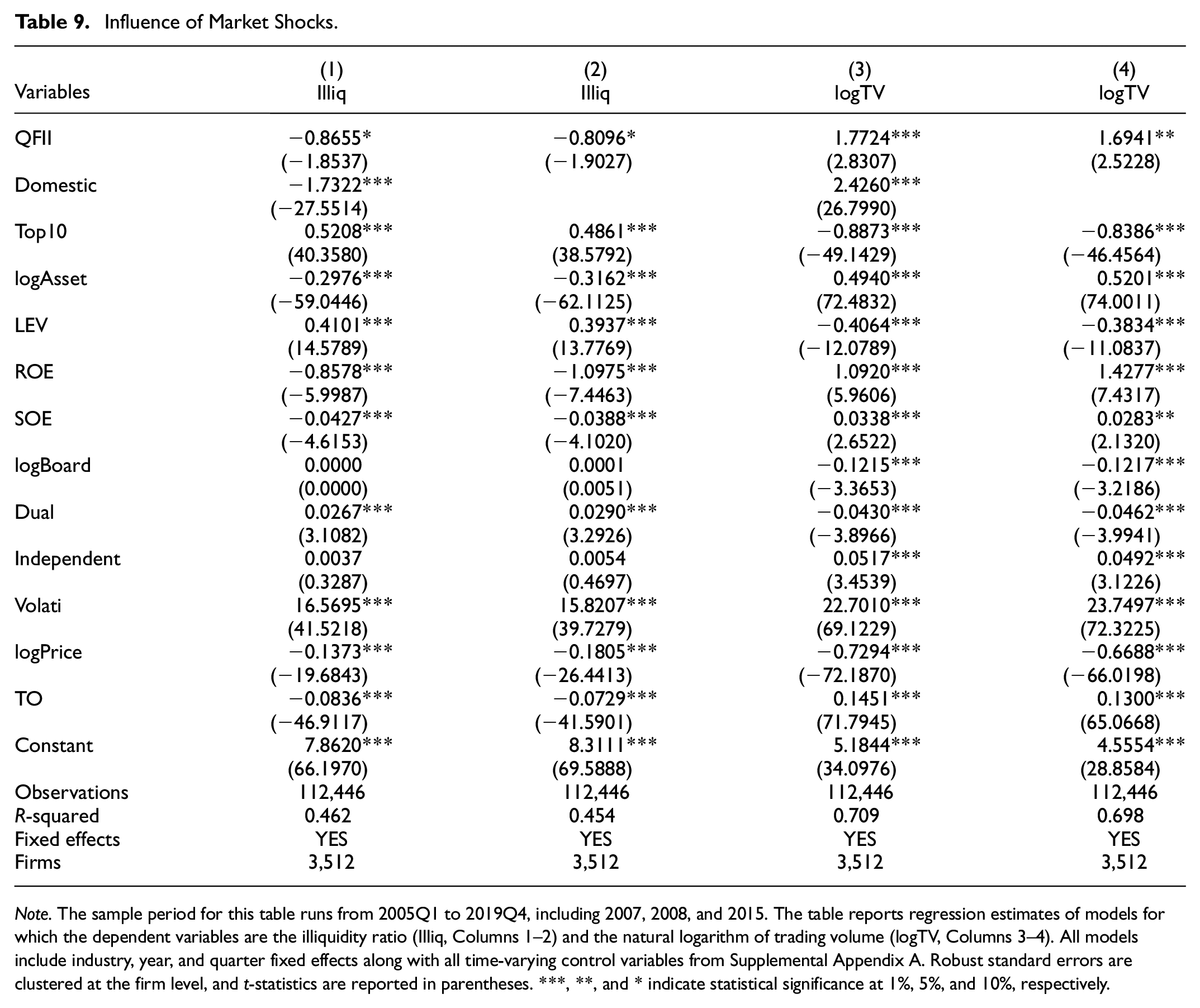

Table 9 gives the empirical results with significant market shocks. As shown in columns (1) and (2), the estimated coefficient of QFII is still significantly negative at the 10% level, and columns (3) and (4) show a significantly positive relation between QFII ownership and trading volume at the 1% level. These results indicate that our main findings are robust and are not affected by large market shocks.

Influence of Market Shocks.

Note. The sample period for this table runs from 2005Q1 to 2019Q4, including 2007, 2008, and 2015. The table reports regression estimates of models for which the dependent variables are the illiquidity ratio (Illiq, Columns 1–2) and the natural logarithm of trading volume (logTV, Columns 3–4). All models include industry, year, and quarter fixed effects along with all time-varying control variables from Supplemental Appendix A. Robust standard errors are clustered at the firm level, and t-statistics are reported in parentheses. ***, **, and * indicate statistical significance at 1%, 5%, and 10%, respectively.

Alternative Explanatory Variables

Table 1 shows that approximately 10% of the sample is composed of QFII firms, while the other 90% is composed of non-QFII firms. Since our analysis is based on the whole sample, there is a possibility that a small percentage of QFII firms in the sample might bias the estimated slope coefficient. For a robustness check, we re-estimate Equation 1 using a dummy variable (

QFII Dummy and Liquidity.

Note. This table reports regression estimates for the QFII dummy with dependent variables set as the illiquidity ratio (Illiq, Columns 1–2) and the natural logarithm of trading volume (logTV, Columns 3–4). All models include industry, year, and quarter fixed effects along with all time-varying control variables from Supplemental Appendix A. Robust standard errors are clustered at the firm level, and t-statistics are reported in parentheses. ***, **, and * indicate statistical significance at 1%, 5%, and 10%, respectively.

We also use the logarithm of QFII’s shareholdings (

QFII’s Shareholdings and Liquidity.

Note. This table reports regression estimates on QFII’s shareholdings with dependent variables set as the illiquidity ratio (Illiq, Columns 1–2) and the natural logarithm of trading volume (logTV, Columns 3–4). All models include industry, year, and quarter fixed effects along with all time-varying control variables from Supplemental Appendix A. Robust standard errors are clustered at the firm level, and t-statistics are reported in parentheses. ***, **, and * indicate statistical significance at 1%, 5%, and 10%, respectively.

Conclusion

In September 2019, China announced that it would abolish investment quota restrictions on QFII and RQFII to facilitate financial reforms and opening. With the continuous entry of foreign capital into the Chinese stock market, there have been many controversial debates on foreign capital’s influence, which has become a major focus in academia.

This paper employs a dataset for 2005 to 2019 to examine the limited participation of QFII in China’s A-share market and how these QFII impact stock liquidity in the Chinese market. Our empirical results reveal that greater foreign institutional participation is positively associated with stock market liquidity, namely, QFII’s ownership reduces the Amihud illiquidity index and increases trading volume. We also find that QFII enhances stock liquidity through an information improvement channel. An increase in QFII’s investment will attract more market attention, leading to more attention from analysts and in reports and then enhancing stock liquidity. In addition, an increase in QFII investment will strengthen the quality of information disclosure, increasing stock liquidity.

Our findings have some policy implications. First, the Chinese government should further accelerate the opening up of the financial market so that more foreign investors can participate in China’s A-share market. As foreign investors have some advantages in terms of collecting and processing unique private information, introducing more foreign investors into the A-share market can promote corporate information disclosure and improve the efficiency of the A-share market. Second, the Chinese government should continue to vigorously support institutional investors, optimize the structure of institutional investors, and guide overseas institutional capital into China’s A-share market. At present, the investment proportion of foreign institutional investors in the A-share market is still very low. Chinese regulators should appropriately relax restrictions on their investment proportion in the A-share market. For example, current regulatory requirements on shareholding ratios stipulate that individual QFII, RQFII, or other foreign investors are not allowed to hold more than 10% of the total shares of a single listed or listed company. Meanwhile, the total shares of company A and domestically listed shares held by all QFII, RQFII, and other foreign investors must not exceed 30% of the total shares of the company. We suggest raising these two ratios to 15% and 35%, respectively.

For listed companies, they should actively and proactively use QFII to improve their corporate governance and information disclosure quality, thus enhancing stock liquidity and market value. First, listed companies should have a deep understanding of QFII’s investment strategies and risk management methods, establish efficient investment cooperation mechanisms, jointly develop long-term investment plans, and timely adjust investment strategies according to market changes to enhance the company’s investment value and profitability. Second, listed companies should establish good relationships with QFII investors, actively seek cooperation, understand the investment preferences, and requirements of foreign investors through effective information communication and exchange mechanisms, and provide support for companies to adjust their business strategies according to market demand and better adapt to market changes. Third, with the Chinese government’s continued relaxation of investment restrictions on foreign capital in the A-share market and the push of foreign exchange supervision policies, listed companies should actively explore the use of QFII mechanisms to expand their overseas markets, establish brand images in overseas markets, and obtain more overseas investment opportunities, and cooperation resources. Fourth, listed companies should improve their governance and information disclosure levels, continuously improve investor relations management, strengthen the protection of shareholder rights and value creation, enhance the company’s value and reputation, and increase competitiveness in attracting QFII investments.

The entry of QFII is capable of improving the internal governance mechanisms of listed companies, enhancing the level of information disclosure, and subsequently improving the transparency, standardization, and market liquidity of the stock market. However, it is important to recognize that the current A-share market in China is mainly made up of retail investors, who are still relatively inexperienced, and the legal system is not yet fully developed. Thus, we should further investigate whether QFII can reduce market manipulation behavior, stock price crash risk (Bashir & Yu, 2020), or financial stability (Bashir, 2021) through its impact on corporate governance and market information. These topics are valuable research questions worthy of further investigation.

Footnotes

Appendix

Variable Definitions.

| Variable | Definition |

|---|---|

| Illiq | Amihud illiquidity ratio of the absolute return to dollar trading volume |

| logTV | the natural logarithm of trading volume in quarter t |

| QFII | The percentage ownership held by qualified foreign institutional investors in each quarter |

| MilesBJ | The natural logarithmic distances between firms’ headquarters and Beijing |

| QFIIdummy | Takes a value of 1 if a firm has QFII participation and 0 otherwise |

| logQFIIhold | The logarithm of QFII’s shareholdings in place |

| logAnalyst | The natural logarithm of the number of registered analysts who write reports on a specific listed firm within a given period of time |

| logReport | The natural logarithm of the number of analysis reports focused on a specific stock written by registered analysts within a given period of time |

| KV | Is computed as 10,00,000 times the slope coefficient in the following ordinary least squares regression |

| Domestic | The percentage ownership held by all domestic institutional investors at the end of quarter t |

| Top10 | The percentage ownership of the 10 largest shareholders at the end of quarter t |

| logAsset | The natural logarithm of total assets (in millions) of a firm at the end of quarter t |

| LEV | Total liability to total assets at the end of quarter t |

| ROE | The return on equity and stands for firm profitability at the end of quarter t |

| SOE | A dummy variable that equals 1 if a firm is a state-owned enterprise at the end of quarter t and 0 otherwise |

| logBoard | The natural logarithm of the number of board directors quarterly |

| Dual | Equals 1 if the board chairman and CEO are the same person; otherwise, it equals 0 |

| Independent | Equals 1 if the board has more than three independent directors; otherwise, it equals 0 |

| Volati | The stock return volatility level, which is calculated as the standard deviation of daily stock returns in quarter t |

| logPrice | The natural logarithm of the average stock price in quarter t |

| TO | The average daily turnover rate in quarter t |

| Age | The number of years since listing |

| GM | Gross Profit Margin, which is defined as revenue less cost of goods sold as a percent of total revenue |

| SGA | The natural logarithm of selling, general and administrative, and financial costs scaled by total assets |

| logSale | The natural logarithm of sales revenue |

| SGrowth | The sales growth rate |

Ethical Approval

Our study isn’t related to animal and human studies.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by The National Natural Science Foundation of China (No. 12271471), Ministry of Education Humanities and Social Sciences Research Youth Fund Western and Border Region Project (No. 22XJCZH007), Yunnan Fundamental Research Projects (Grant No. 202201AU070101), Scientific Research Foundation of Yunnan University of Finance and Economics (No. 2021D07 and No. 2022D10).

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.