Abstract

The current study examined the multifaceted effects of digital transformation on information disclosure and organisational efficiency in Chinese-listed companies. In this study technology adoption, digital strategy, process automation, transparency, and process innovation are used to understand the digital transformation to drive information disclosure towards organisational efficiency. A quantitative research design was utilised, employing a structured survey directed at senior executives, including directors, managers, chief information officers, and chief transformation officers. A nonprobability snowball sampling technique was employed to access a specialised population of experts. The research initially identified pertinent enterprises via the official information disclosure platform of the China Securities Regulatory Commission (CSRC). Five hundred questionnaires were disseminated through email and social media platforms from February 2023 to July 2023. Following the exclusion of incomplete and outlier responses, 300 completed questionnaires were analysed. The analysis was performed using a combination of PLS-SEM and artificial neural network (ANN) approaches. An ANN investigation was conducted to enhance the findings of PLS-SEM and improve predictive accuracy. The findings indicate a substantial positive correlation between digital transformation and increased information disclosure, along with enhanced organisational efficiency. Digital technologies enhance transparency and data-sharing systems, thereby improving decision-making processes. Moreover, research indicates that IT leadership within organisations is pivotal in facilitating successful digital transformation initiatives. These findings highlight the essential function of digital transformation in promoting corporate accountability and operational efficiency. Future research ought to investigate industry-specific impacts of digital transformation and incorporate longitudinal analyses to capture the evolving trends in digital adoption and corporate governance.

Keywords

Introduction

The saturation of markets that came with globalisation has created a demand for innovative manufacturing practices to gain a competitive edge (Keelson et al., 2024). The development of manufacturing companies through scientific and technological innovation is vital to becoming competitive (Wen et al., 2022). The globalised markets and technological innovations have created the circumstances for an industrial initiative to become more competitive, called Industry 4.0 (Klingenberg et al., 2022). Industry 4.0 creates value through the potential business practices that are made possible through the various technologies that it encompasses. The main technologies of Industry 4.0 are: Artificial Intelligence, Autonomous Robots, Augmented and Virtual Reality, Big Data, Cyber Physical Systems, Cloud Computing, and Digital Twin (Suleiman et al., 2022). However, gaining these advantages is a great challenge for companies that seek to utilise the potential of Industry 4.0. What companies have to overcome is the challenge of generating a profound understanding of the needs of such a transition towards a digitalised company (Adamik, 2019). J. Sudewa et al. (2023) states that even though innovative technologies possess great potential, prerequisites for these technologies need to be fulfilled through strategically transforming companies to become more digital.

The digital transformation (DT) concept, including innovative approaches, optimisation methods, and strategic adaptations, extends beyond adopting technology to involve rethinking organisational processes, strategies, and interactions (Alshammari, 2023). Therefore, DT has transformed global business operations. Specifically, China is a major player in DT by strategically employing digital technologies to enhance efficiency and gain a competitive edge in the contemporary era of rapid technological advancement (Brunetti et al., 2020). For example, artificial intelligence (AI), cloud computing, big data analytics, and the Internet of Things (IoT) are transforming Chinese corporate operational strategies through disruptive innovations to improve operational efficiency and effectiveness (Mangla et al., 2020).

However, there is less research on the relationship between DT and organisational efficiency in China, despite the country’s rapid expansion and high rates of DT, especially in the production sector. Furthermore, prior studies have emphasised the need to examine the impact of DT on organisational efficiency in various Chinese settings (L. Guo & Xu, 2021; Zhai et al., 2022). Furthermore, it is vital to comprehend the specific mechanisms through which DT impacts organisational efficiency (Lin & Xie, 2023). A proposed channel through which DT can influence organisational efficiency is information disclosure (Liu et al., 2022). Companies implement DT differently to account for respective goals and missions in accomplishing the vision of each organisation. The central theme of DT provides clients and stakeholders with extensive and relevant information and insights (Klos et al., 2021) as information dissemination could efficiently drive business outcomes (Daradkeh, 2021). Transparent annual reports, detailed product descriptions, and relevant information empower stakeholders to perform informed decisions about the respective involvement with the organisation (Monciardini et al., 2020).

Prior research has investigated the relationship between DT and the effectiveness of organisations in various settings. Sturesson and Groth (2018) conducted a study on the impact of DT on patient care in the medical field in Sweden, whereas Hess et al. (2016) explored the various approaches to formulating DT strategies in German enterprises across multiple industries. Nevertheless, the body of research on DT is typically limited in China, making it crucial to examine this idea within this specific context. The absence of sufficient study on this link is a practical challenge for organisations aiming to utilise technology to enhance operational efficiency while maintaining adherence to norms of information disclosure. How does the organisational ecosystem of enterprises undergo DT as a complete measure of “management and environment”? What is the driving force behind the process of DT in terms of improving efficiency and increasing information transparency? The study addresses these research questions. Thus, this study aimed to analyse the degree to which digital transformation enhances transparency and data-sharing mechanisms, and to ascertain how improved information disclosure affects operational effectiveness.

The contribution of this study can be summarised as follows, according to the aforementioned perspectives: as the DT landscape is dynamic, therefore, identification of integral elements in Chinese context by this study are helpful to improve information disclosure and stakeholder communication (Nicola & Maurizi, 2023). Moreover, organisations can create precise and targeted strategies by determining vital DT elements that disseminate high-quality information (Brunetti et al., 2020) and improve corporate efficiency and effectiveness. Further, to address the deficiency in research on DT, this study builds upon earlier research (Sohaib et al., 2019) by employing an artificial neural network (ANN) model with two or more hidden layers to enhance predictive accuracy (V.-H. Lee et al., 2020).

Literature Review and Hypotheses Development

Theoretical Support—Signalling Theory

Signalling Theory (Spence, 1978) elucidates how organisations communicate pertinent information to stakeholders to mitigate information asymmetry. Improved information disclosure within the framework of digital transformation (DT) is a sign of corporate credibility, openness, and effectiveness. Companies that effectively present data on digital platforms can boost confidence among consumers, investors, and regulatory authorities, so improving organisational effectiveness. Previous research have applied Signalling Theory in the framework of financial disclosure and corporate leadership. According to Connelly et al. (2011), companies with better disclosure policies build investor confidence and thus acquire competitive advantages. By reducing uncertainty among stakeholders, Jiang et al. (2024) examined how digital transparency in Chinese firms affected stock market performance. Nevertheless, these studies predominantly concentrate on financial disclosure rather than the overarching impact of digital transformation on organisational efficiency. This study expands Signalling Theory by illustrating how dimensions of digital transformation, including digital strategy, process automation, and transparency, serve as signals that enhance information disclosure and, consequently, organisational efficiency.

Digital Transformation (DT)

DT has altered conventional commercial and organisational operations and fostered a culture of innovation and change (Brunetti et al., 2020; Zhai et al., 2022) through relevant technology, which utilises advanced tools and systems to boost efficiency. In particular, cloud computing, big data analytics, AI, and the IoT have revolutionised the data landscape, thereby allowing organisations to acquire, retain, and analyse massive amounts of data efficiently (Rabah, 2018; T. Zhang et al., 2022). Thus, seamless technology integration optimises information disclosure while ensuring accuracy and reliability in information dissemination to stakeholders. In addition, technology adoption and process automation, which spur DT, are highly correlated with one another (Orji, 2019; Yu et al., 2022). Automating repetitive tasks in organisations reduces human errors and accelerates information disclosure while automated data collection and report generation enhance the speed of data acquisition and dissemination and improve data reliability and trustworthiness (Mosteanu & Faccia, 2020; Xie & Wang, 2023). The streamlined approach increases operational efficiency and stakeholder confidence when automation reinforces organisational commitments to accurate and reliable data to establish adequate trust and reliability.

DT requires an unambiguously defined digital strategy, which aligns technological investments with organisational goals and improves data management and disclosure processes (Dhamdhere, 2015; Xie & Wang, 2023). Organisational management requires strategic identification of relevant information types, optimal disclosure frequency, and optimal communication channels (Lin & Xie, 2023; Masur & Scharkow, 2016). Systematic information delivery reduces information overload while elevating stakeholder engagement (Mahdi et al., 2020; Xiao et al., 2024) when contemporary organisations could share large amounts of data with a variety of stakeholders, including the public, employees, investors, and partners (Susha et al., 2023). Furthermore, organisational transparency fosters accountability as companies disclosing accurate and reliable information would maintain high levels of reputation. Well-informed stakeholders would attract socially responsible investors and establish trust between organisations and stakeholders (Martínez-Peláez et al., 2023) through DTs and information transparency in spurring process innovation and new information disclosure strategies (Zreik, 2023). Blockchain technology also creates tamper-proof and immutable records to ensure data integrity, credibility, and security. Moreover, augmented reality reports and virtual shareholder meetings have created engaging and interactive stakeholder experiences (De Giovanni, 2023), wherein pioneering information disclosure strategies improve comprehension and present the organisation as technologically proficient and customer-centric (Mallinson & Shafi, 2022; Qi et al., 2024). Table 1 provides key definitions of DT.

Key Definitions.

Information Disclosure

Since the 1970s, industrialised countries have mandated the disclosure of firm environmental-related actions and information to the public as part of corporate social responsibility (CSR) (Tan & Li, 2023). The rise of environmental issues has garnered significant public interest, leading to a notable impact on consumer shopping habits. This shift in consumer behaviour has resulted in a greater inclination towards purchasing environmentally friendly items and a heightened need for the disclosure of environmental information (Song et al., 2023). In response to escalating environmental challenges, the Chinese government has mandated that companies divulge information pertaining to their environmental endeavours. As per the regulations outlined in the 2010 Guide of Environmental Information Disclosure of Listed Companies by the Shanghai and Shenzhen stock exchanges, all listed companies are required to fulfil their responsibility of disclosing environmental information.

Digital Transformation and Information Disclosure

DT has a major effect on information disclosure (Kraus et al., 2021) since, by concentrating on stakeholder communication data accuracy and dependability, technology integration and process automation greatly affect operational efficiency (Chowdhury et al., 2019). By easily including technology into current systems and automating procedures, companies simplify operations and improve performance (Asadov, 2023). Strategic sharing of pertinent data made possible by a well-crafted digital strategy helps companies to raise stakeholder involvement and confidence (Howell et al., 2023; Wei et al., 2024). DT has also increased transparency, accountability, and socially responsible investors (García-Sánchez et al., 2020; Wei et al., 2024) through process innovations that demonstrate organisational commitment to technological advancement while boosting relevant corporate images and reputation. In the digital age, proactive DT improves information disclosure and fosters a culture of trust, accountability, and sustainable growth. The current study hypothesised that:

Organisations could streamline information dissemination and ensure timely delivery through applicable digital technologies and platforms, including advanced communication tools, robust data management systems, and data-driven decision-making (Shrivastav & Bag, 2023). Information disclosure optimisation also improves organisational efficiency by increasing information accessibility. Additionally, advanced technologies, automation of critical processes, and effective information disclosure strategies could boost organisational decision-making and operational efficiency (Antoni et al., 2020). Decision-makers could perform wise and adaptable choices with swift and accurate data compared to the traditional laborious method.

DT provides leaders with real-time data to swiftly harness emerging opportunities and address encountered challenges. DT also streamlines and improves collaboration and organisational communication (Ziadlou, 2021). Transparently sharing relevant information across organisational levels would empower individuals to collaborate, proactively address challenges, and cooperate towards shared goals (Dagestani et al., 2024). Communication gaps and effort duplication reduction also optimise workforce efficiency and productivity. Furthermore, automating repetitive and monotonous tasks reduces human error, which allows employees to focus on more strategic and value-adding tasks (Kedziora & Hyrynsalmi, 2023). Automated data collection and reporting systems simultaneously decrease the need for manual data entry to ensure immediate access to accurate data. Moreover, information quality improves information disclosure and allows employees to focus on high-level tasks that significantly impact corporate growth (Koh et al., 2023).

DT improves customer service and satisfaction, which ensures businesses effectively and efficiently resolve customer issues. Real-time and accurate information assists customer service teams in delivering personalised and efficient service (Wirtz et al., 2023). High customer satisfaction could foster loyalty and advocacy for an organisation, which impacts business growth and success. DT also enhances information transparency and internal efficiency, which boosts investor and regulator confidence (Caputo et al., 2021; Jia et al., 2024). Concurrently, trust increases capital acquisition while reducing regulatory obligations to boost operational efficiency and industry competitiveness (Wang et al., 2021). DT also optimises information disclosure, wherein rapid data acquisition, optimised decision-making, seamless collaboration, automation of repetitive tasks, and improved customer service assist in achieving corporate goals (Thakker & Japee, 2023). Hence, DT and information disclosure are essential to long-term growth and prosperity in the ever-changing and technology-driven business environment. A hypothesis was proposed:

DT shapes the contemporary business environment (Sivarajah et al., 2020). As such, organisations must adapt and thrive in the digital age through information disclosure optimisation for high operational efficiency (Orrensalo et al., 2022). Optimising information disclosure involves strategic information dissemination management by employing relevant digital technologies and platforms to allow sending relevant and time-sensitive information instantaneously to the intended recipients (Jia et al., 2024; Morales et al., 2021). Optimisation also involves utilising sophisticated communication tools, resilient data management systems, automation processes, and data-driven decision-making procedures (Lazaroiu et al., 2022) while implementing effective strategies to increase information availability and accessibility (Lazaroiu et al., 2022).

Information disclosure assists decision-makers in performing informed and flexible choices with swift and accurate data (Ellili, 2022). The conventional data collection approach is time-consuming. Comparatively, DT allows leaders to access real-time data and leverage alternative opportunities while resolving challenges (Haleem et al., 2021). Successful DT projects also create a harmonious and effective collaborative environment, which enhances organisational communication channels (Martínez-Peláez et al., 2023). Furthermore, transparently disseminating relevant information throughout an organisation allows employees to actively participate in productive collaboration, proactively address obstacles, and cultivate cohesive efforts to achieve mutually agreed goals (Behar-Horenstein et al., 2021). Minimising communication gaps and reducing effort duplication also improve workforce efficiency and productivity.

Automation reduces the risk of human errors, thereby allowing workers to focus more on strategic and value-added tasks (Asif et al., 2024; Syed et al., 2020). Automated data collection and reporting systems decrease the need for laborious manual data entry while ensuring timely and accurate information. Meanwhile, information disclosure effectiveness depends on information quality (Aksoy et al., 2021) which allows employees to focus on high-level tasks with significant impacts on company growth. Additionally, DT efforts enhance customer service and satisfaction in organisations (Guzmán-Ortiz et al., 2020) to assist businesses in managing customer inquiries and concerns and ensuring unprecedented issue resolution speed. The latest and most accurate information also assists customer service teams in providing personalised and efficient services, wherein customer satisfaction fosters loyalty and advocacy to elevate organisational growth and success (I. Sudewa & Amberd, 2023). Furthermore, DT improves information transparency and internal efficiency that elevate investor and regulator trust. Organisaitonal trust could increase capital acquisition and reduce regulatory obligations in elevating operational efficiency and industry competitiveness for the company.

DT has improved organisational efficiency by optimising information disclosure (Patil et al., 2023). Rapid data acquisition, decision-making optimisation, seamless collaboration, task automation, and improved customer service would significantly impact organisational operational efficacy (Patil et al., 2023). Synthesising the factors would assist organisations in accomplishing respective goals accurately and efficiently through DTs and transparent information disclosure practices, especially for corporations seeking long-term growth and prosperity in current dynamic and technology-centric business environments. Accordingly, this study postulated that:

Table 2 shows the hypotheses tested in the results section (Figure 1).

Research Hypotheses.

Conceptual framework.

Methodology

Population and Sampling

The research design was based on the quantitative method to investigate the impacts of DT on information disclosure and organisational efficiency. The study focused on upper-level executives at Chinese domestic enterprises that are listed on the stock market. The specimens and data for this investigation were obtained from Chinese enterprises that are listed on the stock exchange. At first, the whole roster of company names was obtained by downloading from the information disclosure website (http://www.cninfo.com.cn/) designated by the China Securities Regulatory Commission (CSRC). The list was categorised based on service sectors and the magnitude of the company’s registered capital. The rationale for prioritising the service sector lies in its profound influence on both the worldwide economy and the economy of China. The Chinese economy is undergoing a transformation as digital technologies have an increasingly significant impact. This is particularly applicable in industries that include extensive interactions with customers, such as the service sector. In these industries, digital services facilitate stronger customer relationships and foster valuable interactions with customers (Wulf et al., 2017). As previously mentioned, the IT department plays a crucial role in any digital undertaking within a company. Among the members in that department, those at the managerial level are expected to have the highest level of knowledge about the firm’s current and past procedures and performance. Moreover, the primary individuals responsible for DT in a company are typically the chief information officer and chief transformation officer. Therefore, the survey carried out in this study was specifically targeted at and sent to directors, managers, chief information officers, and chief transformation officers of private service organisations operating in the service sector industry.

To maintain ethical standards, ethical approval was obtained from the research ethics committee of the University. Participants were asked to finish an anonymous online survey that examined organisational efficiency, information disclosure, and digital transformation. Before starting the questionnaire, informed consent was obtained electronically. Respondents were assured of their right to withdraw at any time, briefed on the goals of the study, and advised that their participation was entirely voluntary. With no sensitive or intrusive themes, the study carried little risk. Its non-collection of any identifying personal data guarantees rigorous confidentiality. Stored safely and used just for scholarly study were the data. While protecting participants’ rights and dignity, this ethical framework guaranteed that the advantages of the research, that is, helping to clarify digital governance and performance in Chinese companies, far exceeded any possible risks.

The survey incorporates the study objectives and identifies the specific persons it aims to target. This is essential to guarantee that the obtained data is unbiased. Every latent variable in the model, like digital transformation dimensions (technology adoption, digital strategy, process automation, transparency), information disclosure, organisational efficiency, was operationalised through several measurement items tailored from validated scales in the literature. Instruments were adopted from J.-S. Chen and Tsou (2007) and Gorla et al. (2010). A comprehensive Appendix 1 containing the complete questionnaire utilised in the study has been included, including item sources and measurement scales.

The present study employed this strategy to augment the sample size and ensure that it was exclusively comprised of experts. The technique of snowball sampling carries biases which include participant homogeneity and concentration among particular professional connections, yet our study implemented mitigation methods. The recruitment approach was enhanced through the use of LinkedIn, WhatsApp, and email combination as these platforms allowed access to professionals within various industries and organisations. Expert qualification standards enabled the selection team to include qualified participants exclusively. The research team conducted data quality checks by excluding both unanswered questions along with extremely abnormal replies that strayed far from typical patterns.

Furthermore, the volunteers rendered valuable assistance by disseminating the questionnaire among their coworkers, whom the researcher would have otherwise encountered difficulty in accessing. A total of about 500 questionnaires were distributed to executives and managers from February 2023 to July 2023. A sample of 300 completed questionnaires was retained for analysis after eliminating incomplete questionnaires and any data points that deviated significantly from the norm. The research utilised 300 participants as respondents to fulfil acceptable requirements for behavioural and management research statistical analysis. A power analysis through G*Power 3.1 determined the adequacy of this sample size based on a medium effect size (f2 = 0.15) and 0.05 significance level, and 0.80 power (Cohen, 1988). The research demands 88 to 153 participants for regression-based models containing three to six predictors (Hair et al., 2010). The 300 participants included in the study far surpass the prerequisite, which guarantees enough statistical power to identify meaningful relationships between variables.

Research papers about digital transformation, together with information disclosure and organisational efficiency, use sample sizes that are equivalent or smaller than what this study utilises. Numerous studies by Hayat et al. (2022) used constructs similar to this research while working with sample populations between 200 and 350, thus affirming the appropriate choice of the current study’s sample size. SEM and ANN modelling techniques need extensive data collections because they need bigger datasets to gain valuable generalising capability and model maintenance (Hair et al., 2019).

An ANN study was carried out to raise predictive accuracy and enhance PLS-SEM results. We performed analysis on obtained data points using an artificial neural network (ANN) model. The ANN consisted in two hidden layers and an output layer in addition to an input layer. X neurones found in the hidden layer were chosen by researchers using cross-valuation for best performance strength. Rectified Linear Units activation functions in the hidden layers allowed non-linear learning and efficiency gains; but, since softmax activation supports multi-class classification, the final output layer used softmax activation. By means of each hidden layer application, dropout regularisation with 0.2 strength served to prevent overfitting. Along with recall and the F1-score to gauge the model, the performance measures included accuracy and precision.

Data Analysis Method

This study used Partial Least Squares Structural Equation Modelling (PLS-SEM) method to estimate the hypotheses presented in Table 2. While to perform mediation analysis, the Preacher and Hayes approach was employed. Further, Non-compensatory artificial neural network (ANN) analysis utilises input, output, and hidden-layer deep-learning algorithms. The hidden layer connects input and output neurons (Lee et al., 2020) by acting as a black box similar to the brain (Hayat et al., 2020). This study measured predictive accuracy through the Root Mean Square Errors (RMSE) of trained and tested data (Lee et al., 2020) to understand outcome factors.

Results

Demographic Profile

The study respondents comprised 61% males and 39% females. All respondents were upper management in Chinese listed companies. The respondents were well-educated, with 75% possessing a graduate degree and the remaining 25% possessing a master’s degree in relevant fields. The respondents were categorised into three different age groups, namely 30 to 40 (15%), 40 to 50 (22%), and 50 to 60 (63%). Table 3 presents the demographic characteristics.

Demographic Characteristics.

Reliability and Validity

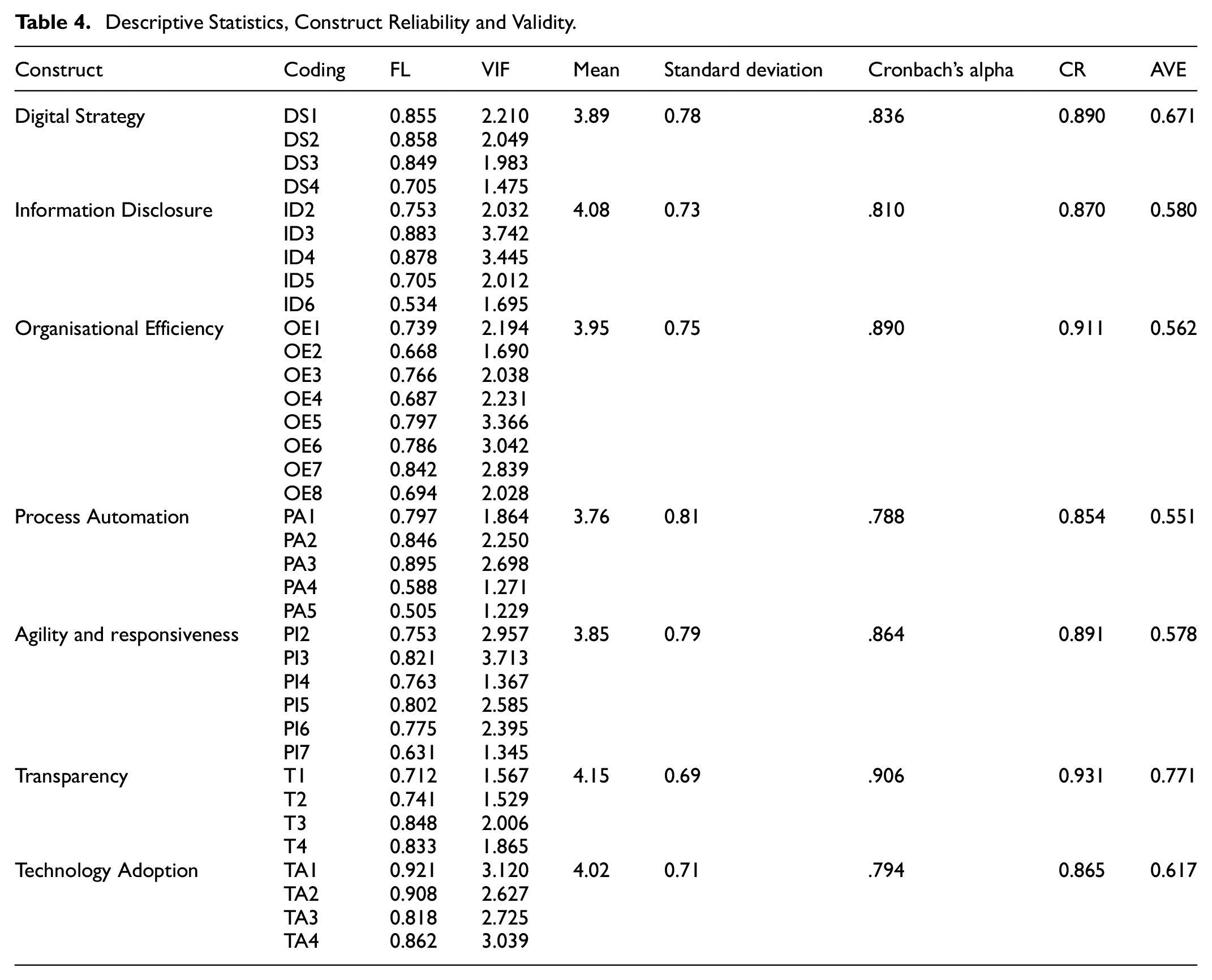

The reliability and validity of all the variables were tested. The Cronbach’s alpha values of all variables were above the threshold (0.70) value except for two items, which were the information disclosure item and the process innovation item. The factor loading (FL) of all the items was also above the threshold (0.5) value. Furthermore, the composite reliability (CR) of all items exceeded the threshold value of 0.70 (Hair, 2021). Concurrently, the variance inflation factor (VIF) was below the threshold value (3.3), which suggested no multicollinearity issue. Nonetheless, the average variance extracted (AVE) values of the two items were low and were deleted from the data. The detailed results are illustrated in Table 4. Meanwhile, the discriminant validity was evaluated through the Heterotrait-Monotrait (HTMT) ratio (Hair, 2021), as presented in Table 5.

Descriptive Statistics, Construct Reliability and Validity.

The HTMT Ratio.

Hypothesis Testing

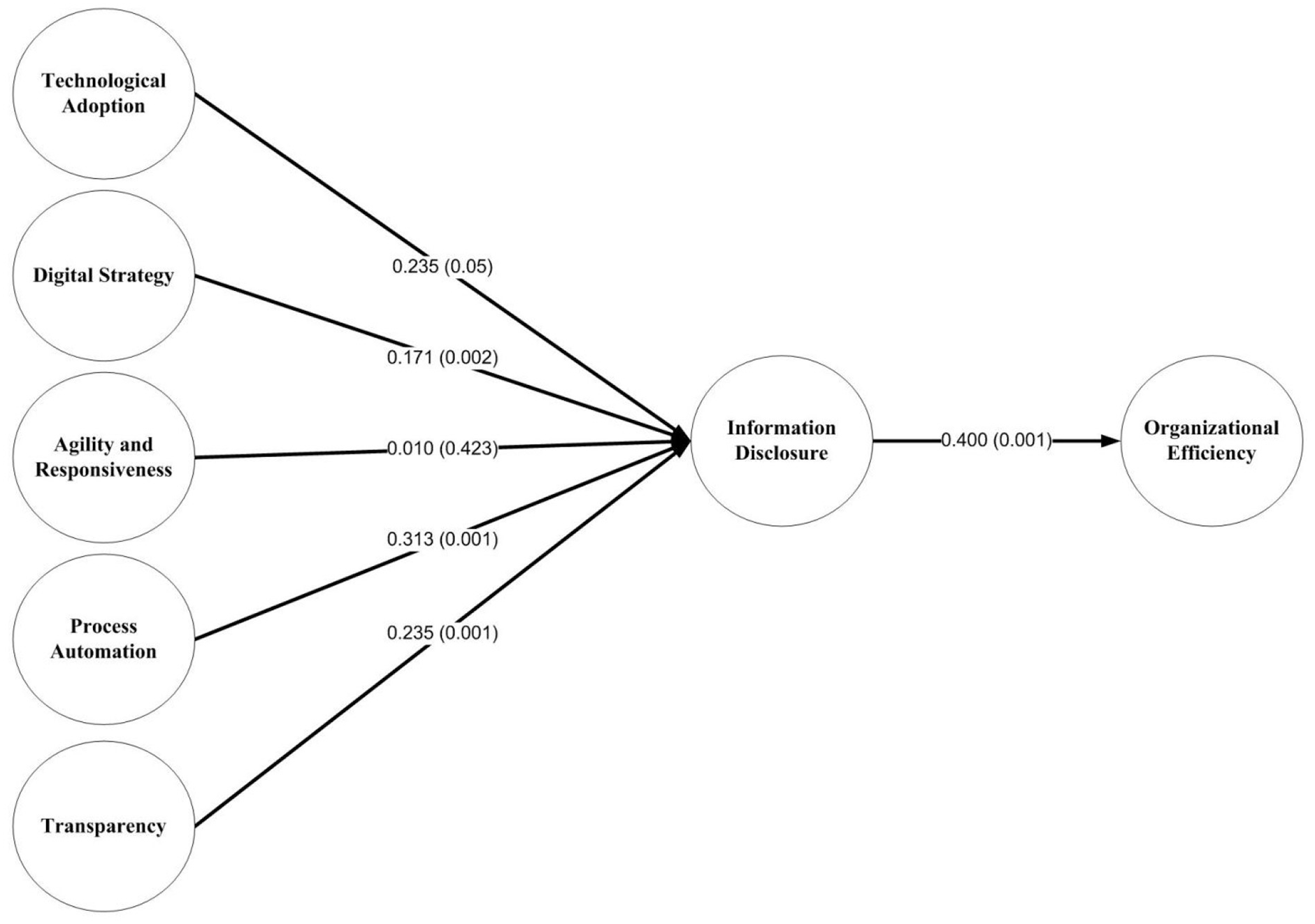

The proposed hypotheses were tested through the SmartPLS software. The results revealed that digital strategy positively and significantly impacted information disclosure (β = .171, t = 2.938, p < .05). Information disclosure positively and significantly impacted organisational efficiency (β = .400, t = 7.940, p < .05). Process automation also positively and significantly impacted information disclosure (β = .313, t = 4.154, p < .05). Nevertheless, process innovation did not significantly impact information disclosure (β = .010, t = 0.194, p > .05). Meanwhile, technology adoption positively and significantly impacted information disclosure (β = .073, t = 1.630, p = .05). Transparency positively and significantly impacted information disclosure (β = .235, t = 3.503, p < .05). Detailed findings are depicted in Table 6. Summarily, only one hypothesis was rejected based on the discovered p-value. Figure 2 shows the path diagram.

Hypothesis Testing.

Path diagram.

Mediation Analysis

The mediation analysis results demonstrated that information disclosure significantly mediated the relationship between process automation and organisational efficiency (β = .125, t = 3.213, p < .05). Nonetheless, information disclosure did not significantly mediate the relationship between technology adoption and organisational efficiency (β = .029, t = 1.528, p > .05). Similarly, information disclosure did not significantly mediate the relationship between process innovation and organisational efficiency (β = .004, t = 0.200, p .05). Nevertheless, information disclosure significantly mediated the relationship between digital strategy and organisational efficiency (β = .068, t = 2.572, p < .05). Information disclosure also significantly mediated the association between transparency and organisational efficiency. The findings are presented in Table 7. Summarily, two mediation hypotheses were rejected based on the p-value.

Mediation Analysis.

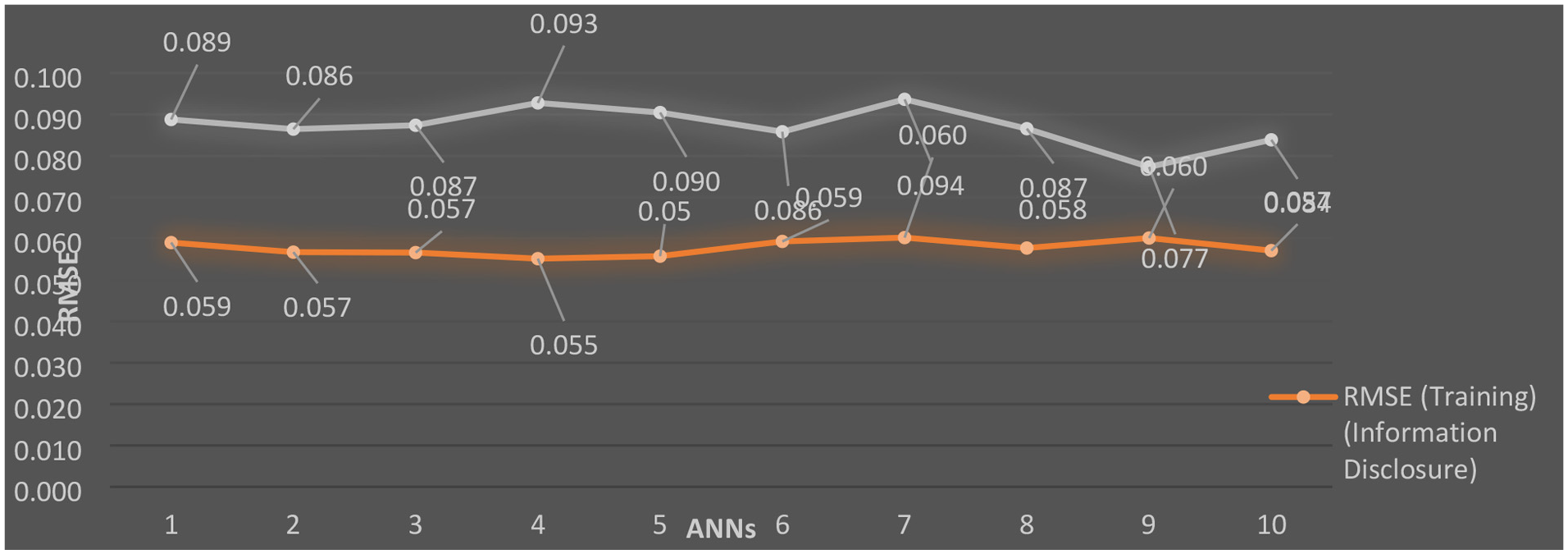

Artificial Neural Network Analysis

The multi-layer perception (MLP) artificial neural network (ANN) consisting of three layers, namely input, hidden, and output layers, was employed with forward-back propagation (FFBP; Lee et al., 2020). The tenfold ANN model in the SPSS neural network algorithm was utilised to address the over-fitting issue with 70% of the data for training and 30% for testing. The results revealed the high predictive accuracy of the RMSE value for training (RMSE = 0.058) and testing (RMSE = 0.087), which suggested a sufficient data fit and high predictive accuracy achieved by the ANN, as presented in Table 8 and Figure 3. A sensitivity analysis was also performed to evaluate the four dimensions of DT as exogenous constructs contributing to information disclosure (Hayat et al., 2020). The results illustrated in Table 9 demonstrated that transparency contributed the most to information disclosure, followed by process automation as the second most crucial dimension contributing to information disclosure. The remaining two dimensions also contribute to information disclosure. Process innovation showed no direct effect on disclosive transparency, possibly due to various plausible reasons. Process innovation shows potential to optimise operational efficiency inside businesses, while process automation directly enhances information delivery along with greater transparency. The measurement process for the process innovation construct likely did not adequately monitor its possible effects on information disclosure. Therefore, research should seek to reevaluate and modify existing measurement items to guarantee their proper alignment with the process innovation definition during digital transformation.

The RMSE for Training and Testing Processes.

The RMSE for training and testing processes.

Sensitivity Analysis.

Discussion

The current study demonstrated that technology adoption, digital strategy, process automation, and transparency significantly impacted information disclosure in the DT process. The substantial and noteworthy effect of digital strategy (β = .171, p = .002) on information disclosure corresponds with previous studies highlighting strategic digital initiatives as a catalyst for improved corporate transparency (Nylund et al., 2022). Process automation (β = .313, p = .001) significantly enhances information disclosure, corroborating the conclusions of K. Lee and Oh (2022), who posited that automation promotes efficient data management and minimises errors in disclosure procedures. Transparency (β = .235, p = .001) demonstrates a significant effect, corroborating previous research that emphasises the importance of transparency in promoting trust and accountability (Hassan et al., 2022). Nonetheless, agility and responsiveness (β = .010, p = .423) exhibited an insignificant correlation, contradicting prior research that highlighted its significance in real-time data management (Y. Guo et al., 2022). This discrepancy indicates that although agility is essential in various contexts, its influence on information disclosure in Chinese enterprises may be constrained by regulatory or cultural factors.

The mediation analysis highlights the indirect impacts of DT factors on organisational efficiency via information disclosure. Process automation (β = .125, p = .001), digital strategy (β = .068, p = .006), and transparency (β = .094, p = .001) significantly improve organisational efficiency through information disclosure. These findings substantiate the idea that improved disclosure mechanisms serve as a link between digital initiatives and overall organisational performance (Z. Zhang et al., 2023). The mediation effects of agility and responsiveness (β = .004, p = .065) and technology adoption (β = .029, p = .065) were negligible, suggesting that these elements may call for additional mechanisms, such corporate governance or regulatory policies, to completely maximise their benefits (X. Chen et al., 2020). The relative significance of the four dimensions in information disclosure results was also found by the ANN. The study found that information disclosure in DT would be much predicted by technology adoption, digital strategy, process automation, and transparency, so impacting the information distribution approach with stakeholders. Information disclosure was not much changed by agility or responsiveness (Morgan et al., 2023). To maximise information disclosure practices, companies should thus give other aspects top priority when developing DT projects. Furthermore, found to be greatly mediated by information disclosure was DT and organisational efficiency. Transparency, digital strategy, process automation, and technology adoption help to increase information disclosure and efficiency. Moreover, ANNs increased the analytical rigour of this study and corroborated the importance of the dimensions. Summarily, this study illuminated the complexity of DT and the corresponding significant effects on information disclosure and organisational efficiency. Organisations should employ a holistic approach to DT and leverage the pivotal dimensions to improve information disclosure and efficiency.

Study Implications

Theoretical Implications

This study enhances the existing literature on digital transformation by incorporating Signalling Theory into the framework of corporate information disclosure and efficiency. This study builds upon prior research by presenting empirical evidence of the mediating effect of information disclosure, thereby enhancing the understanding of how digital initiatives lead to performance enhancements. The current study significantly contributed to academia and practitioners in DT, information disclosure, and organisational management. The study assessed the multidimensionality of DT to challenge the unidimensional perspective. Researchers and practitioners must consider all aspects of DT when assessing relevant impacts on organisational outcomes. Technology adoption, digital strategy, process automation, and transparency significantly predicted information disclosure that assisted organisations in effectively allocating resources. Organisations could optimise information disclosure by prioritising the dimensions, as information disclosure is integral to DT and organisational efficiency.

The current study revealed that artificial neural networks (ANNs) have the ability to identify intricate connections in multidimensional concepts. This finding encourages future researchers to investigate DT and associated phenomena using sophisticated methodologies. The study provided insights on DT dimensions that are applicable to businesses from various sectors with distinct settings, regardless of industry. Corporations can enhance their communication strategy by comprehending the ways in which information disclosure enhances organisational efficiency and performance. Moreover, the research results could aid firms in making best judgements regarding DT. Organisations can achieve success in DT by aligning their plans with the most critical dimensions. Continual assessment and surveillance of the specified aspects and their consequent impact on information disclosure are necessary for DT. Companies should reassess and modify their DT strategy in order to maintain competitiveness. Furthermore, this study highlighted the significance of a multidimensional approach to DT, with a focus on prioritising dimensions, disclosing information, and utilising advanced analytical tools. This approach enables organisations to effectively traverse digital transition and optimise information disclosure and efficiency.

Practical Implications

The findings indicate that organisations ought to prioritise process automation, transparency, and digital strategy to augment information disclosure and enhance efficiency. Organisations ought to allocate resources toward digital instruments that optimise disclosure procedures and guarantee adherence to regulatory standards. Executives should cultivate a corporate culture that prioritises transparency, as this builds stakeholder trust and strengthens competitive advantage. For instance, this study demonstrates that digital strategies play an essential role in developing information disclosure systems that boost organisational efficiency. However, effective information disclosure depends on process automation combined with transparency. Therefore, managers should adopt automated reporting frameworks together with ERP solutions alongside AI analytics to remove human errors and maintain data precision. These technologies enable better regulatory compliance while establishing trust between investors and employees, and customers, which creates a positive corporate reputation that supports sustainable business expansion. The research results of this study demonstrated that process innovations failed to produce meaningful effects on information disclosure leading to the conclusion that internal efficiency-enhancing activities independently do not guarantee enhanced external reporting. Organisations need to implement formal communication systems and unified reporting methods during their innovation initiatives to fill the discovered knowledge gap. IR and ESG disclosure practices enable organisations to bridge their stakeholder-oriented transformations with innovation-driven developments.

The implications of our research are significant for policymaking. It is beneficial for a government to encourage the implementation of a DT policy, such as offering a platform for companies to adopt a DT plan. Like business innovation, the adoption of DT is expensive and presents challenges for a company. We contend that the adoption of DT enables a company to enhance its operational efficiency, a crucial factor for both the company’s future success and the economic progress of a nation. Although DT offers advantages to a company, such as cost savings and improved operational efficiency, there are numerous obstacles that a company must overcome in order to initiate the adoption process. Therefore, it is beneficial for an economy in the long run if a government offers a platform for companies to implement a DT strategy, which would reduce costs and make it easier to embrace DT.

Social Implications

Enhanced information disclosure practices, propelled by digital transformation, foster corporate accountability and ethical business conduct. Transparent organisations foster a more informed society, allowing investors, employees, and consumers to make informed decisions. These findings underscore the necessity for policies that promote digital disclosure mechanisms to enhance corporate governance and stakeholder engagement.

Economic Implications

Augmenting digital competencies and transparency practices can enhance financial performance and bolster investor confidence. Organisations with strong transparency protocols are more inclined to garner investments and maintain enduring growth. Policymakers ought to contemplate incentives for organisations implementing digital transformation strategies that enhance disclosure practices, thus promoting economic stability and market efficiency.

Conclusion

This paper explained the several aspects of DT and the related important consequences on organisational efficiency and information disclosure. Particularly, information disclosure with stakeholders in DT is much influenced by technology adoption, digital strategy, process automation, transparency, and process innovation inside DT. The most recent studies show that strong predictors of information disclosure practices are adoption of technology, application of digital strategies, automation of processes, and encouragement of transparency. Strategic inclusion of these aspects into digital transformation projects will help companies to improve organisational efficiency, transparency, and stakeholder communication. Process innovation did, however, not significantly influence information disclosure. This implies that companies should focus their DT efforts on components that more affect information disclosure instead of others. Therefore, this study found that the act of revealing information played a key role in connecting decision-making transparency and organisational effectiveness. The artificial neural networks (ANNs) also emphasised the significance of DT dimensions in relation to the disclosure of information. In summary, the study findings added to the existing information about DT and how it may help companies enhance communication, transparency, and efficiency. Thorough research and careful implementation would help companies thrive in the digital era.

Limitations and Future Directions

Initially, we get our findings exclusively from a single nation. It is preferable to investigate another developing market in order to confirm our conclusions. Furthermore, because of the vague and uncertain nature of DT adoption, our metrics may not accurately measure the impact of DT. This study proposes the utilisation of a survey method known as the Delphi methodology to gather evaluations from managers regarding a DT. We establish the viability and informativeness of the quantitative technique for analysing the influence of DT on a company’s performance. It would be optimal to measure the extent to which a company has adopted DT or the significant influence of a particular aspect of DT. We must devise a more effective measure to assess a company’s DT in the future.

Future research should investigate industry-specific differences in the relationship between digital transformation disclosure and efficiency to ascertain if particular sectors exhibit more pronounced effects. Furthermore, examining moderating variables such as the regulatory environment, corporate governance, or cultural influences may yield enhanced understanding of the contextual factors impacting these relationships. The inclusion of longitudinal data would facilitate the establishment of causality and enhance comprehension of the long-term effects of digital transformation on corporate performance.

Footnotes

Appendix

| Variable | Code | Item | Sources |

|---|---|---|---|

| Technology Adoption | TA1 | Our company has allocated a generous budget for purchasing information technology hardware. | J.-S. Chen and Tsou (2007) |

| TA2 | Our company has allocated a generous budget for purchasing information technology software. | ||

| TA3 | Our company has emphasised information technology staffing and training. | ||

| TA4 | Our company has embraced sophisticated Internet application | ||

| Digital Strategy | DS1 | Our information technology capability has supported business strategies that strengthen customer service. | J.-S. Chen and Tsou (2007) |

| DS2 | Our information technology projects have been implemented in compliance with business strategies. | ||

| DS3 | Our information technology applications have supported business strategies to improve process management. | ||

| DS4 | Our information technology applications have supported business strategies to improve product/service offerings. | ||

| Process Automation | PA1 | The adoption of new information technology systems and applications has enhanced employee empowerment. | J.-S. Chen and Tsou (2007) |

| PA2 | The adoption of new information technology systems and applications has enabled inter-department (cross-function) integration. | ||

| PA3 | The adoption of new information technology systems and applications has adjusted new business practices. | ||

| PA4 | The adoption of new information technology systems and applications has increased operations mobility. | ||

| PA5 | The adoption of new information technology systems and applications has helped managers make more timely decisions. | ||

| Process Innovation | PI1 | Our company has often offered new practices in customer service. | J.-S. Chen and Tsou (2007) |

| PI2 | Our company has often offered new practices in customer information inquiry and consultation. | ||

| PI3 | Our company has often offered new practices in selling products or services. | ||

| PI4 | Our company has often offered new practices in providing after-sale services. | ||

| PI5 | Our company has often offered new practices in developing new products or services. | ||

| PI6 | Our company has often offered new practices in promoting new products or services. | ||

| PI7 | Our company has often offered new practices in internal administration and operations. | ||

| Transparency | T1 | The company’s customer data management activities are clear to me. | Gorla et al. (2010) |

| T2 | The company’s customer data management activities are straightforward. | ||

| T3 | The company’s customer data management activities are easy to understand. | ||

| T4 | The company’s customer data management activities are transparent. | ||

| Information Disclosure | ID1 | Our information outputs are accurate. | Gorla et al. (2010) |

| ID2 | Our information outputs are complete. | ||

| ID3 | Our information outputs are useful for stakeholders. | ||

| ID4 | Hour information outputs are concise. | ||

| ID5 | Our information outputs are relevant to decision-making. | ||

| ID6 | Our information format is good in appearance as compared to others. | ||

| Organisational Efficiency | OE1 | Organisational efficiency is helpful to ensure high efficiency in the decision-making process. | Gorla et al. (2010) |

| OE2 | Organisational efficiency is helpful to ensure high efficiency in internal meetings and discussions. | ||

| OE3 | Organisational efficiency is helpful to ensure good coordination among the organisation’s functional areas. | ||

| OE4 | Organisational efficiency is helpful to provide a good evaluation of the annual budget. | ||

| OE5 | Organisational efficiency is helpful to provide a good evaluation of capital. | ||

| OE6 | Organisational efficiency is helpful to maximise the company’s profit margin. | ||

| OE7 | Organisational efficiency is helpful to maximise the company’s market share. | ||

| OE8 | Organisational efficiency is helpful to maximise the company’s strategic planning efficiency. |

Ethical Considerations

This study involved human participants and was conducted by institutional and international ethical research standards, including the principles outlined in the Declaration of Helsinki. Ethical approval for this research was obtained from the Research Ethics Committee of Capital University of Economics and Business.

Consent to Participate

Participants were informed of the purpose of the study, the voluntary nature of their participation, and their right to withdraw at any time without penalty. Informed consent was obtained before participation, and respondents were assured that all information would remain confidential and anonymous. The study involved minimal risk to participants, limited to the time spent completing a digital questionnaire. The research was designed to limit any risk of psychological, social, or legal harm to participants. Data were collected and stored securely, ensuring privacy protection. The potential benefits of this research, to both the academic community and practitioners in the digital transformation field, outweigh any minimal risks, as the findings can help guide policy and strategic improvements in organisational efficiency and transparency.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analysed during the current study.