Abstract

Even though previous studies have investigated the effect of environmental regulation policy on stock price crash risk, little is known about how the firm-specific environmental punishment would impact stock price crash risks. By applying difference-in-difference method with manually collected firm-specific environmental punishment data for the listed firms in China, our study finds that the implemented environmental punishment leads to larger stock price crash risk accumulation of the punished firms. This effect can be mitigated by better information disclosure behavior, higher media reputation, healthy fundamentals, and optimal capital structure. Our study also finds the consecutive punishment effect only exists in a long period. Our work is among the first to rigorously analyze the effect of firm-specific environmental punishment on firm’s stock price crash risk. This research provides relevant policy suggestions on the environmental punishment practice.

Keywords

Introduction

Since the financial crisis in 2008, stock market crashes have been common, such as the “high cut” in the share price of a listed firm named Softcontrol in early 2011 and the continued decline. Therefore, it is important to study the impact factors of stock price crash risk.

There is a long history of theoretical research on the stock price crash risk. Black (1976), based on the efficient market theory, attempted to explain the formation mechanism of stock crash risk with the hypothesis of financial leverage effect. Thereafter, Pindyck (1984) proposed the volatility feedback hypothesis under the efficient market framework, pointing out that an increase in stock price volatility raises the risk premium of investors, amplifies the negative returns from bad news, and leads to a negatively skewed distribution of stock market returns. In addition to efficient market theory, scholars have begun to provide new entry points for stock price crash risk from both information asymmetry and investors’ imperfect rationality perspectives (Blanchard & Watson, 1983; L. Jin & Myers, 2006).

On the empirical side, based on the information asymmetry perspective, scholars have studied the impact of management, accounting soundness, and other factors on stock price crash risk (L. Jin & Myers, 2006; Hotton et al., 2009). From the perspective of behavioral finance, scholars have given the assumption of imperfect rationality to investors and explained the existence of stock price crash risk from two perspectives: stock price bubble hypothesis and heterogeneous belief hypothesis (Blanchard & Watson, 1983; Hong & Stein, 2003).

Given the above background, we address several research questions as follows: (1) Will the environmental punishment increase or decrease firm’s accumulated stock price crash risk? (2) If the effect significantly exists, is there any factor accelerating or mitigating it? (3) What is the effect of recidivism (in terms of firm’s environmental violation) on stock price crash risk?

According to data from the Chinese Environmental Protection Bureau, environmental pollution incidents have occurred frequently in recent years. Through manually collected environmental punishment data published by the Institute of Public and Environmental Affairs (IPE, https://www.ipe.org.cn/index.html) and the provincial environmental protection bureaus, we find that the number of listed firms being environmentally punished is increasing dramatically (defined as Number of firms, as shown in Figure 1), and the frequency of environmental punishments is also increasing (defined as Number of EPPs, as shown in Figure 1). The number of punished firms rose from 65 in 2013 to 391 in 2016 and dropped in 2017. Since the number of listed firms is changing over time, we further analyze the ratio of being punished listed firms over the total number of listed firms (defined as Prop of firms, as shown in Figure 1). The trend of Prop of firms over time is consistent with that of Number of firms and Number of EPPs.

Distribution of punished firms and environmental protection punishments (EPPs) by year.

Theoretically, in information asymmetry theory, due to information asymmetry, company managers are conditioned to hide bad news about the company for their own benefit (Akerlof, 1978; Balakrishnan & Koza, 1993; Rosser, 2003). According to signaling theory, firms or governments disclose information to the outside world, which conveys information to investors, who make decisions based on the information (Karasek & Bryant, 2012; Taj, 2016). Based on bad news hiding theory, corporate managers have an incentive to release positive information, hide negative news, or delay the disclosure of negative news (F. Jiang et al., 2020; Lee et al., 2021). As suggested in stakeholder theory, the attention of external stakeholders to the firm has an impact on the value of the firm (Freeman et al., 2010). After that, this paper investigates the mechanism of the effect of environmental punishments on the stock price crash risk based on these four theories in the theoretical framework and literature review sections.

However, there is a limited number of literatures exploring whether the environmental punishment, which is the implemented punishment on a specific firm, would affect the specific firm’s stock price crash risk. The focus of some recent work is to examine the impact of the national or environmental policy enforcement on stock price crash risk (Yildiz & Karan, 2020; X. Zhang et al., 2021), which cannot identify how the accumulated stock price crash risks are different for the firms punished and those not punished. Our current work tries to fill this gap with the firm-level environmental punishment evidence, which can evaluate the impact of environmental regulations and the related environmental policies from a different perspective. It is recognized that firm level evidence can better reveal the internal mechanism of the policy effect with corporate heterogeneities considered (D. Zhang & Vigne, 2021). In the above context, we intend to study the impact of environmental punishments on the accumulation of stock price crash risk, and its mechanism.

Our contributions are as follows. First, in this paper, we seek to depart from existing studies by providing new insights on the potential effects of environmental protection punishments, and thereby extending, as well as making a number of new contributions to the extant literature. First, we advance the broad literature on environmental enforcement and regulations (Heyes & Kapur, 2011; Z. Jiang et al., 2018; Tarui & Polasky, 2005). We study the impact of environmental punishments received by individual firms on their accumulated stock price crash risk using the difference-in-difference (DID) method with multiple time periods instead of the event study method (Zeng et al., 2021). The findings can tell the differences in accumulated stock price crash risk between the punished firms and non-punished firms under the same environmental policy or enforcement strength with fewer endogeneity concerns.

Second, we innovatively examine the accumulation of stock price crash risk of firms under environmental punishment. Small negative events may not significantly increase the risk of stock price crash of the firm, but it is the accumulated risks that may aggravate the stock price crash of the firm. The traditional crash risk measures cannot clearly describe this kind of accumulation (J. Chen et al., 2001). Dynamic panel data models may be favored since there are lagged key variable used (Elhorst, 2012). By referring commonly used event windows used in literature (Pandey & Kumari, 2021), we calculate the crash risk changes in this window to analyze the cumulative effect of environmental enforcement on the risk of stock price crash.

Third, we complement the literature on stock price crash risk (Hutton et al., 2009; Kim et al., 2011). Our findings suggest that environmental punishments received by firms change their accumulated stock price crash risks, while this effect is impacted by documented factors of stock price crash risk such as information transparency and quality of information disclosure, corporate media reputation, and so on.

Fourth, our findings provide further support on the environmental regulation practice. We innovatively find that consecutive punishment within a short period of time cannot have a desired effect on environmental enforcement, which provides a reference for the effective use of relevant government enforcement powers.

Background

On February 22, 2021, the Fifth Session of the United Nations Environment Conference was held online with the theme of “Enhancing Conservation of Nature and Realizing Sustainable Development.” The conference strongly advocates green and low-carbon production and lifestyle and encourages all economies to seek new opportunities from green development. The United Nations Environment Program (UNEP) has proposed three actions for the Earth at peace with nature in terms of climate action, nature action, and chemicals and pollution prevention action.

China is the world’s largest developing country and the largest economy in transition. Over the past 40 years, along with China’s rapid economic development, China itself has faced increasingly serious environmental crises, including the major water pollution of the Songhua River in Jilin, China, on November 13, 2005, when a benzene plant exploded, affecting the lives of millions of people living along the river, and the water pollution of 96,000 mu of water in Baiyangdian, Hebei, China, in February and March 2006, which caused serious environmental and environmental problems. In February and March 2006, water pollution occurred in the 96,000-acre Baiyangdian waters in Hebei, China, causing a serious environmental and ecological disaster. In addition to water pollution, China’s air quality has also been very poor for some time, with the 2015 to 2016 Beijing haze event among others being the most impressive. All these events show that although China has experienced rapid economic growth over the past 40 years, the environmental cost behind its high growth is also very high.

The increasingly prominent ecological problems have attracted the attention of the Chinese government. In order to combat environmental pollution, China has invested a lot of human and financial resources, and the total investment in environmental pollution control in China reached RMB 1,063.89 billion in 2020 alone, accounting for about 1.0% of the gross domestic product (GDP) and 2.0% of the total investment in fixed assets of the whole society. By region, except for four regions in China, including Tibet, Qinghai, Hainan, and Ningxia, the total investment in environmental pollution control in the remaining 27 regions exceeded RMB 10 billion.

In addition to the investment in human and financial resources, China has also made significant improvements at the legislative level. In December 2016 China enacted the Environmental Protection Tax Law, the first law in China that specifically reflects a green tax system, and its introduction is of great significance to China in building a green fiscal and taxation system, regulating the pollution management behavior of emitters, and establishing a green production and consumption system.

China has done a lot of work on the system construction related to environmental punishment. In 2003, the former State Environmental Protection Administration issued the “Announcement on Enterprise Environmental Information Disclosure,” which required listed heavy polluting enterprises to disclose environmental information; in 2008, the “Measures for Environmental Information Disclosure” was published, which required heavy polluting enterprises to disclose the emission methods, emission concentrations and exceedances of major emissions, etc. In 2014, the new Environmental Protection Law proposed to comprehensively strengthen information disclosure and public participation. In 2015, the former Ministry of Environmental Protection issued the Measures for Environmental Information Disclosure by Enterprises and Institutions, which clarified the way of disclosing environmental information, increased the penalties for enterprises that discharge pollutants, and provided corresponding incentives for enterprises’ environmental protection behavior.

China has established and implemented a central ecological environmental protection inspection system since 2015 and completed the first round of inspections in 2018 and carried out “look-back” to 20 provinces (regions). The second round of inspectors was launched in 2019 and the task was fully completed by June 2022. In 2021, the Ministry of Ecology and Environment issued the “Reform Program of Environmental Information Disclosure System According to Law,” which clearly pointed out that environmental information disclosure according to law is an important enterprise environmental management system, and moreover, a fundamental element of the ecological civilization system.

In the above context, China has done a lot of work on environmental punishments, and the environmental information disclosure system is increasingly perfect. Then leads to the research question of this paper, what is the effect of environmental punishment? How did capital markets react?

Theoretical Framework

Information Asymmetry Theory

Economic theory usually assumes that both sides of a market transaction have completed information, however, in real economic activities, economic actors in most cases not only do not have complete information, but also have very limited ability to discover information, which makes their decision-making behavior face a lot of uncertainty, which is in direct conflict with the assumption of complete information in traditional economic theory. The theory of information asymmetry is a new development of modern economic theory, which is based on filling the loopholes of traditional economic theory.

The theory of information asymmetry was developed by three American economists, that is, G. Akerlof, M. Spence, and J. E. Stigliz. According to the theory of information asymmetry, in market economic activities, there are differences in the knowledge of information among various categories of people. Those who have more adequate information are often in a more advantageous position, while those who are poorly informed are in a more disadvantageous position (Akerlof, 1978; Balakrishnan & Koza, 1993; Rosser, 2003).

Information asymmetry is a drawback of the market economy. To reduce the harm that information asymmetry produces in the economy, the government should play a strong role in the market system. The Institute of Public and Environmental Affairs (IPE) is a public interest environmental research institute registered in Beijing. Since its establishment in June 2006, IPE has been dedicated to collecting, organizing and analyzing public environmental information from government and enterprises, building an environmental information database, integrating environmental data to serve green procurement, green finance and government environmental decision-making, leveraging the combined efforts of enterprises, government, public interest organizations and research institutions to transform a large number of enterprises into environmental protection, and promoting environmental information disclosure and the improvement of environmental governance mechanisms.

Information asymmetry theory suggests that the information asymmetry between listed companies and investors provides the prerequisite for management’s opportunism. When the information opacity of listed companies is high, management has a stronger incentive to hide negative information about the company, but the ability and space to hide negative news within the company is not endless, and when management cannot continue to hide bad news, the concentrated release of bad news will cause a significant negative reaction in the market, leading investors to make negative value judgments and investment decisions, resulting in a plunge and crash in stock prices.

Based on information asymmetry theory, L. Jin and Myers (2006) studied the influence of national information environment on the risk of stock price crash of listed companies and found that when the quality of information environment in a certain country is low, that is, the degree of information asymmetry is high, the risk of future stock price crash of local listed companies is significantly higher. Hutton et al. (2009) conducted a study from the perspective of micro corporate financial information and found that when the quality of surplus information of listed companies is low, their stock price crash risk will be significantly higher, which verifies the information asymmetry formation mechanism of stock price crash from the perspective of micro enterprises.

Signaling Theory

Signaling theory is a branch of economics that studies how people use information to make decisions (Connelly et al., 2011; Riley, 2001; Spence, 1973). It is based on the idea that people use signals to convey information about themselves and their intentions. The theory has been used to explain a wide range of phenomena, including the behavior of firms in competitive markets, the formation of social networks, and the dynamics of political campaigns.

Signaling theory refers to the transmission of information through observable behaviors, and screening model refers to the screening of true information in different ways.

Signaling theory suggests that external stakeholders will make decisions based on information about the firm in order to mitigate adverse selection under information asymmetry. In the case of environmental punishments, the government promptly discloses information about corporate environmental violations, which is a policy signal, and this can alleviate information asymmetry and is an important channel for investors to obtain information (Aydinoğlu & Krishna, 2011; Jervis, 2017; Yarhi-Milo et al., 2016). More importantly, environmental punishments have an important impact on capital market activity (Karpoff et al., 2005), and Karpoff’s study, based on data from a sample of environmental punishments disclosed in the Wall Street Journal, found that the average fine was $13.2 million between 1980 and 2000, and that the cost of violations reduces the market value of companies. This shows that environmental punishments can serve as an effective signal that provides an important reference for investors’ risk perception of a firm.

The Screening model suggests that investors who do not have private information need to screen the information, which entails a cost (Yabushita, 1983). The release of information on environmental punishments by the government can have an informational effect and can effectively screen for problems in corporate disclosure and problems related to corporate environmental pollution. Therefore, when a listed company is subject to environmental punishments, it sends “bad news” to the market about problems in corporate disclosure and corporate social responsibility, causing a negative market reaction (Dasgupta et al., 2001; Konar & Cohen, 1997). At the same time, stakeholders of listed companies adjust their expectations about the future risks of the company, re-judge the value of the company, and react accordingly (Liu,2012; Travlos, 1987).

Bad News Hoarding Theory

The majority of the stock price crash risk literature is based on bad news hoarding theory (Hutton et al., 2009). The Bad news hoarding theory proposed by L. Jin and Myers (2006) suggests that the less transparent a firm’s information is, the more likely it is that management will disclose good news and bad news asymmetrically, allowing bad news to accumulate within the firm. However, there is a limit to the amount of bad news that insiders are willing and able to absorb successfully, and when the accumulated amount of bad news exceeds the manager’s ability to hoard it, the bad news will be instantly released in large quantities thus causing the stock price to crash and bringing a huge shock to the capital market. Or investors may be fooled by false financial information, leading to a “bubble” in the stock price. Once investors have the true picture of the company’s operations, the stock price will crash.

L. Jin and Myers (2006) found that managers often conceal and hoard bad news due to a combination of factors such as compensation plans and careers due to opaque information, and Hutton et al. (2009) showed that when company insiders have stronger incentives and better access to hide negative information about the value of the company, the news is more likely to accumulate within the company. Piotroskiet et al. (2015) argue that managers are motivated by political incentives to reduce the disclosure of bad news during the window of important political events. Graham et al. (2005) find that managers are more likely to delay the disclosure of bad information than good news. Hu and Wang (2018) find that political connections can influence stock price crashes by influencing the speed at which bad news travels. Some scholars have also found that managers usually hide and hoard bad news, but leak or publicly disclose good news to outside investors in a timely manner, or even over-disclose good news (Ball, 2009; Bao et al., 2019; Kothari et al., 2009; Moradi et al., 2021).

Environmental punishments enhance information transparency and optimize the information environment of the market in which firms are located, which helps investors to grasp the true business situation of firms. At the same time, the instantaneous release of a large amount of hoarded negative information may have a negative impact on the capital market and cause a stock price crash.

Stakeholder Theory

Stakeholder theory is a theory of organizational management and business ethics that addresses morals and values in managing an organization. It holds that organizations are accountable to all their stakeholders, not just their shareholders. Stakeholders include anyone who is affected by the actions of the organization, such as employees, customers, suppliers, the local community, and the natural environment. The theory suggests that organizations should take into account the interests of all stakeholders when making decisions (Melé, 2009; Stieb, 2009).

In terms of environmental protection, the concern of internal stakeholders such as shareholders for environmental protection issues is increasingly influenced by external stakeholders, and the importance of environmental protection and related decisions are no longer solely determined by internal stakeholders such as shareholders. External stakeholders influence internal stakeholders’ awareness of environmental protection and the importance of environmental protection, mainly through indirect means such as social opinion, and thus influence corporate environmental behavior (Porter & van der Linde, 1995). For example, if a firm’s direct emission of pollutants to the outside is perceived by external stakeholders, the firm may make some environmental behaviors, such as green technology and green products, in response to social opinion.

In addition, as government environmental regulation increases, if a company fails to take positive environmental responses to meet the requirements, it will receive severe sanctions, such as revocation of production and operation licenses, suspension of production, and production restrictions. For example, in the melamine case of Sanlu Group Co., Ltd. was severely punished for not responding positively to environmental protection, and some of its executives were sentenced to prison and the company was banned.

Empirical Literature Review and Hypothesis Development

Environmental Regulation and Stock Price Crash Risk

As China’s stock market belongs to an emerging market and the system still needs to be improved, the stock prices of listed companies are likely to deviate from the market average level in the short term due to the impact of “bad news.” The existing literature on stock price crash risk about China is developed from two aspects. The first is the internal factor of the firm, includes board characteristics (Jebran et al., 2022), CEO characteristics (Shahab et al., 2020; J. Xu & Zou, 2019), institutional investor (F. Li & Jiang, 2022), etc. The second is the external factor, includes tax (S. Chen et al., 2022), confucianism (Jebran, Chen, Ye, & Wang, 2019), geographical factors (X. Jin et al., 2022), etc. Few studies have studied the influencing factors of stock price crash risk from the perspective of environmental regulation, especially environmental punishment. Some scholars have studied the impact of green credit policies on the risk of stock price crash from the perspective of environmental regulation (Shao et al., 2022; W. Zhang et al., 2022). This paper studies the impact of environmental punishments on the risk of stock price crash, which complements the relevant literature.

Existing environmental regulation literature examines the impact of environmental regulation on firm’s innovation performance (Z. Jiang et al., 2018), technological change (Tarui & Polasky, 2005), R&D activities (Heyes & Kapur, 2011), and so on. There are also studies that have found environmental regulation may directly hurt the value of the polluting firms, and the long-term effect may be positive (Khanna & Damon, 1999; Ramiah et al., 2013; Sam & Zhang, 2020). Only a few recent works pay attention on how environmental regulation would affect stock price crash risk. Yildiz and Karan (2020) study how the country-level environmental regulation performance would impact the stock price crash risk of renewable energy firms, and find that there is a nonlinear correlation between a country’s environmental performance and the stock price crash risk of firms. Another research is about China’s new environmental inspector program. With city-level enforcement data, X. Zhang et al. (2021) find the program increases the information transparency of firms in the inspector region, and reduces the stock price crash risk.

All the above research on environmental regulation mainly focuses on the role of the “event” of environmental regulation policy change or implementation initiative. To best of our knowledge, there is no existing literature directly examining how environmental punishments received by individual firms would affect their stock price crash risks.

Intuitively, the environmentally punished firms are seldom with good environmental performance. The environmental punishments received by individual firms can be interpreted as the negative events where the firms are unwilling to disclose. The negative events would cause negative emotions which can influence investors’ decisions, and finally affect stock prices, resulting a huge market loss (Kaplanski & Levy, 2010). Relatedly, the negative impact of adverse environmental incidents on market value has been confirmed in countries like the United States (Hamilton, 1995) and China (X. He & Liu, 2018). As a result, we would expect the environmental punishments received by firms may disturb their stock prices. Even though the environmental enforcement may have deterrent effect (X. Zhang et al., 2021), the punished firm and its manager may gamble on no further regulations and sophisticatedly hide information in a more confidential way. This may lead to higher accumulated stock price crash risk. When one firm is punished, the other non-punished firm may also be deterred by the regulation action and improve their environmental performance voluntarily, and its accumulated stock price crash risk may be lower.

According to Information asymmetry theory, more information about environmental punishments disclosed by the government represents more negative information hidden by the firm, higher information asymmetry between investors and firms, and higher risk of potential stock price crash (Caputo et al., 2016; Nikolaou et al., 2013). According to signaling theory, environmental punishments transmit negative information about the company to the market and stakeholders of listed companies adjust their expectations about the future risks of the company, which in turn affects the capital market (Lorraine et al., 2004). According to bad news hoarding theory, the instantaneous release of a large amount of negative information hoarded by a company after the disclosure of environmental punishments negatively affects the capital market and causes a stock price crash (Kothari et al., 2009; Piotroski et al., 2015). According to stakeholder theory, with the rising concern of external stakeholders about environmental protection, environmental punishments disclosing negative environmental information about a firm may have a negative impact on firm value if the firm does not take environmental actions (Freeman & Reed, 1983; Freeman et al., 2021).

Accordingly, we formulate our first hypothesis as follows:

H1: Compared with the non-punished firms, the environmentally punished firms’ stock price crash risk accumulations may be increased significantly.

The Role of Information Opacity and Quality

According to the information asymmetry theory, the improvement of firm’s information disclosure quality can reduce the stock price crash risk by alleviating the degree of asymmetry of market information (Brown & Hillegeist, 2007; S. Li et al., 2020). Opaque financial reports are more likely to have the risk of stock price crash (Hutton et al., 2009).

According to the signaling theory, disclosure of negative or positive information of enterprises can convey news to investors. Investors are informed of some negative news about enterprises before they are punished for environmental punishments. Therefore, the punishment effect will be partially dispersed (Connelly et al., 2011). In addition, enterprises can also release positive news through the media to enhance corporate reputation, which will also offset some of the negative impact of environmental punishments (Ahern & Sosyura, 2014).

According to the bad news hoarding theory, media can play another role in information disclosure, and disclose the hidden negative news of the enterprise. With the increasing emphasis on environmental pollution in China, X. D. Xu et al. (2016) find that disclosure of environmental violations by Chinese companies can lead to a punitive decline in the related stock market, and media coverage can exacerbate this effect. Meanwhile, media’s report on firm’s positive information will enhance its market value (Ahern & Sosyura, 2014).

According to the stakeholder theory, the disclosure of positive information by the media or the increase of information transparency can improve the corporate image, and the observation of this phenomenon by external stakeholders will enhance the evaluation of the enterprise (Stieb, 2009). Therefore, the negative impact of environmental penalties on enterprises will be weakened.

Given the above argument, we formulate our second hypothesis as follows:

H2: Environmentally punished firm with higher quality of information disclosure, higher information transparency, or higher media reputation may have lower stock price crash risk accumulation.

The Role of Corporate Fundamentals and Capital Structure

The fundamentals of a firm are factors affecting its market performance and potential risk. Even though the negative information disclosed through environmental regulations may increase the stock price crash risk, the good fundamentals may mitigate this effect since they may indicate firm’s potential to survive during the regulation period and finally improve its environmental performance.

According to signal theory, good financial indicators of enterprises will convey positive information to investors and have a positive impact on enterprise value. According to the bad news hoarding theory, financial indicator information disclosure can improve the level of external supervision, restrain the possibility of hoarding bad news, and contribute to the long-term stable development of enterprises. Dang et al. (2018) study the impact of debt maturity structure on the risk of stock price crash, and find that compared with long-term debt, short-term debt can play a more supervisory role, enhance the disclosure of management information, inhibit the possibility of hoarding bad news, and reduce the risk of stock price crash. Capital structure plays an important role in maintain the stability of the stock price (Andres et al., 2014). Accordingly, we formulate our third hypothesis as follows:

H3: Environmentally punished firm with better fundamentals or better capital structure will have lower stock price crash risk accumulation.

Research Design

Sample Selection and Data Source

We choose the time from 2013 to 2017 for our main study. The starting year is 2013, because after the new government came to power in 2013, China launched a campaign to protect the environment intensively. In November 2012, the 18th National Congress of the Communist Party of China (CPC) pointed out that ecological progress should be given high priority. The ending year is chosen to be 2017 instead of 2019, because we want to use the latest data in 2018 and 2019 to study the potential effect of consecutive punishments.

The data on environmental punishments comes from the Institute of Public and Environmental Affairs (IPE, https://www.ipe.org.cn/index.html), following Cai et al. (2020) and Ma et al. (2021), including a total of 1,664 observations of daily environmental punishments from 2013 to 2017. The distribution of these observations across different categories is shown in Table A1 in Appendix 2 (see Supplemental Material). Table A2 in Appendix 2 (see Supplemental Material) shows the stock code, punished date, and reasons for environmental punishments for some sample. Table A3 in Appendix 2 (see Supplemental Material) shows the year-quarter and industry distribution of the entire sample.

Firm-level financial data and firm’s characteristic data are all from the China Stock Market and Accounting Research (CSMAR) database (https://data.csmar.com). Following L. Jin and Myer (2006) and Hutton et al. (2009), we have eliminated some samples following the criteria: (1) the samples with trading days less than 30 in each quarter are excluded to estimate the stock price crash risk index; (2) finance firm samples are excluded; (3) samples with negative net assets are excluded; (4) samples with missing control variables are excluded. To avoid the influence of extremes, continuous variables are subjected to 1% winsorize tailing. The following table shows the steps of elimination and the consequent number of observations after each step (Table 1).

Sample Elimination Steps.

Variable Definition

Independent Variable: Environmental Punishment

We use the environmental punishment data for individual firms, which is obtained by the following method. First, we collect the names of all the listed firms in China from CSMAR database. Second, we search for environmental announcements for each listed firm in IPE database. IPE collects all environmental notices of government inspections and environmental regulation from different cities, different provinces, or the central government. When we enter one firm name into the IPE database’s search bar, we will find all the environmental inspections and events for the firm and its subsidiaries, including “Environmental Protection Verification,”“Monetary Penalty,”“Tuning Within a Time Limit,”“Environmental Credit Rating,”“Production Suspension,” and others. We sort out the environmental punishment samples quarterly. We set a dummy variable

Dependent Variable: Stock Price Crash Risk Measures

Based on daily idiosyncratic rate of return, we calculated negative return skewness coefficient

First, we calculate the firm-level daily rate of return

Second, we calculate

Here n is the number of days in quarter t of a given year. A larger

Finally, we calculate

Here

Small negative events may not significantly increase the risk of stock price crash of the firm, but it is the accumulated risks that may aggravate the stock price crash of the firm. The two crash risk measures above cannot clearly describe this kind of accumulation. By referring to the method of event study, we select the event window and calculate the crash risk changes in this window to analyze the cumulative effect of environmental enforcement on the risk of stock price crash.

We do empirically find the insignificant impact of environmental punishment received by firms on their stock price crash risk (shown in Table A4 of Appendix 2 [see Supplemental Material]). This result further confirms our above argument since we consider the impact of environmental punishment would gradually affect firm’s stock crash risk, in terms of increasing the accumulated risks.

We provide a revised measurement of stock price crash risk accumulation, which uses the difference between the

Here

Control Variables

Following Callen and Fang (2013), Jebran, Chen, & Zhu (2019), Jebran et al. (2020), Kim et al. (2011), Shahab et al. (2020), Z. Zhang et al. (2022), we select the variables of asset liability ratio (LEV), firm size (SIZE), return on equity (ROE), book-to-market ratio (B/M), market return (RET), market volatility (SIGMA), turnover rate (TURNOVER), corporate information transparency (OPAQUE), corporate governance structure (TOP10), board size (BOARD), board independence (IND), dual position of CEO and chairman (CEO) as control variables. The detailed definitions of the variables are in Table A5 of Appendix 2 (see Supplemental Material).

In addition, we use the individual firm dummy variable (

The samples are divided into two groups, high information transparency and low information transparency, based on whether the firm’s modified Jones coefficient is greater than the average value.

Empirical Model

We try to examine the impact of exogenous environmental punishment on the accumulation of stock price crash risk, and the difference-in-difference (DID) method with multiple periods is a common tool to evaluate the effectiveness of policies. Therefore, we apply this method to estimate the impact of environmental punishment received by firms on their stock price crash risks. We conduct the DID with multiple time periods analysis within the panel data fixed effect model as in formula (6):

Here

Empirical Results and Discussion

Data Descriptive Statistics

Data descriptive statistics are shown in Table 2, and Pearson correlation statistics are shown in Table A6 of Appendix 2 (see Supplemental Material). The average number of punishments received by each firm is about 3. The average values of ΔNCSKEW and ΔDUVOL are about 0.04 and 0.04. The average values of Δ3NCSKEW and Δ3DUVOL are about 0.06 and 0.05, and the average values of Δ5NCSKEW and Δ5DUVOL are about 0.06 and 0.05.

Descriptive Statistics.

Considering that the information disclosure evaluation index provided by authoritative institutions usually has good impartiality and objectivity, we adopt the rating of the information disclosure quality of listed firms by Shenzhen Stock Exchange as the measurement of the information disclosure quality, which can reflect the overall information disclosure quality of the firm comprehensively. The samples are divided into excellent, good, qualified, and unqualified for subsample description, where excellent or good disclosure quality is considered as High Disclosure Quality, qualified or unqualified disclosure quality is considered as Low Disclosure Quality. Table A7 in Appendix 2 (see Supplemental Material) shows the descriptive statistics for sub-samples. We further conduct the mean and median test in Table A7 in Appendix 2 (see Supplemental Material). The results shows that the risk of stock price crash of firms with low information disclosure quality is significantly higher than that of firms with high information disclosure quality.

Results Analysis

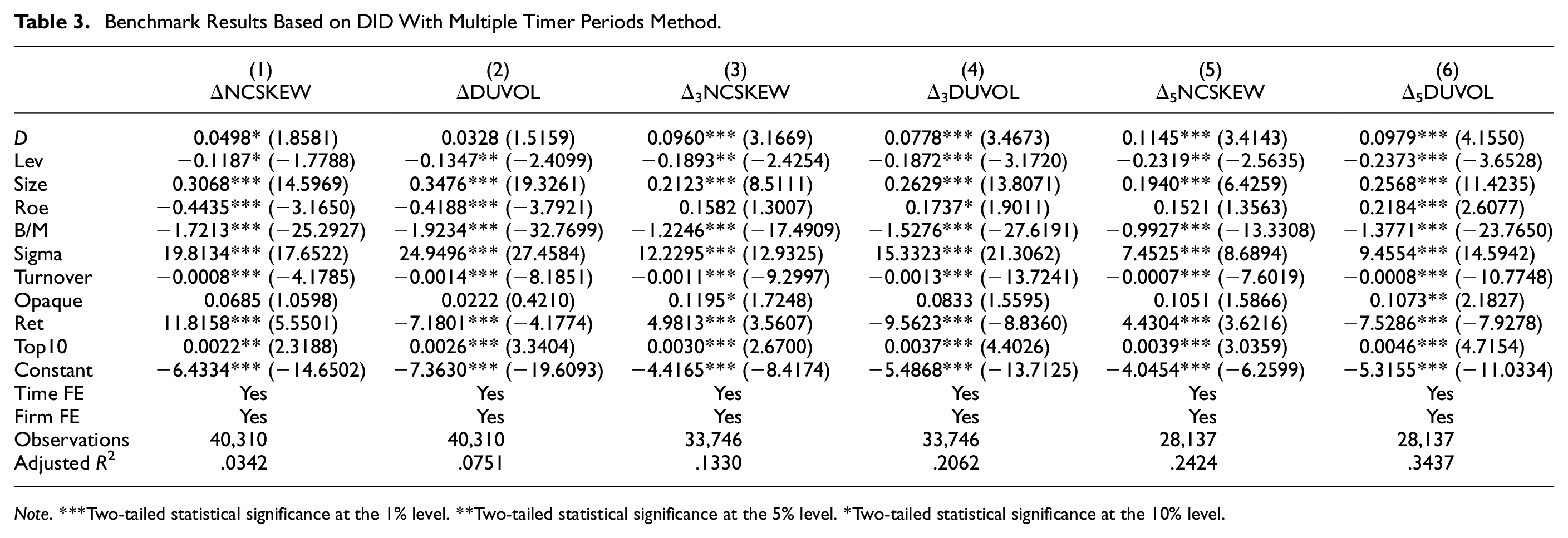

We use the panel data fixed effect model (6) to conduct DID analysis. The results are shown in Table 3. After including the control variables, year-quarter fixed effect and firm fixed effect, the coefficient of

Benchmark Results Based on DID With Multiple Timer Periods Method.

Note. ***Two-tailed statistical significance at the 1% level. **Two-tailed statistical significance at the 5% level. *Two-tailed statistical significance at the 10% level.

To apply the DID with multiple time periods method, we need to conduct a parallel trend test. The parallel trend test results are in Figure A1 of Appendix 3 (see Supplemental Material). These results indicate that we pass the parallel trend test.

Robustness Check

Replacing the Independent Variable

In the main analysis, we have investigated how the environmental punishment as an event would impact crash risk. As a robustness check, we replace the independent variable with the number of punishments received by one firm to further explore the impact of environmental punishment. The new independent variable is named as PUNISH it , which records the number of punishments received by firm i in quarter t. We only focus the firms received non-zero punishment. There are a large number of firms received 0 punishment. Including these firms into analysis would bring nonmeaningful issue to identification. The summary statistics for is PUNISH it as follows (Table 4). The regression results can be found in Table A8 in Appendix 2 (see Supplemental Material). From columns (3) to (6), we can see that our main findings still hold.

The Summary Statistics for PUNISH.

Replacing the Dependent Variable

In the main text, this paper uses the stock price crash risk index after the event minus the event before to define the dependent variable. Here, this paper uses the stock price crash risk index before the event minus the current period of the event to redefine the dependent variable as a robustness test. We replaced the dependent variable as follows:

Here

The regression results can be found in Table A9 in Appendix 2 (see Supplemental Material). We can see that our main findings still hold.

Placebo Test

We conduct the Placebo test to show whether our DID analysis is robust. We conduct one regression for the three-period-ahead and another regression for the three period-lag as a robustness check. The results can be found in Table A10 in Appendix 2 (see Supplemental Material). The Placebo test results indicate that, no matter three-period-ahead or three-period-lag, the term D in any specification is no longer significant. This indicates the impact of environmental punishment on crash risk is not affected by other unobserved factors.

Random-Effect Panel Data Analysis

In the main analysis, we applied the fixed-effect panel data analysis. As a robustness, we conduct a random-effect panel data analysis. The results are in Table A11 in Appendix 2 (see Supplemental Material). The findings in our main analysis still hold.

Generalised Least Square Regression

We conduct Generalised Least Square (GLS) regression as a robustness check to revisit our analysis in the main context. The results can be found in Table A12 in Appendix 2 (see Supplemental Material), which indicates that our findings in the main analysis still hold.

Lagged One Period Independent Variable

The main text study shows that the independent variable of the current period has a significant impact on the dependent variable. To test for endogeneity, this paper refers to Banerjee and Duflo (2003) and carries out regression with the independent variable lagged by one period. If the coefficient of the one-period lagged independent variable is still significant, it indicates that the main conclusion is valid. Therefore, we re-conduct the analysis with a one-period-lagged independent variable. The results are in Table A13 in Appendix 2 (see Supplemental Material), which indicates our main findings still hold.

Heckman Selection Model

To deal with the potential endogeneity due to self-selection, we use Heckman selection model to examine the impact of environmental punishment on crash risk. The results are in Table A14 in Appendix 2 (see Supplemental Material), which indicates our main findings still hold.

Two-Stage Least Squares Regression

It is possible that the financial performance or other bad news accumulation induces the firms to violate the environmental protection regulations, resulting in the environmental punishment. Therefore, the main analysis may suffer from endogeneity due to mutual causality. In order to deal with this potential problem, we use one-period-lagged independent variable as the instrumental variable and conduct the two-stage squares regression. The results are in Table A15 in Appendix 2 (see Supplemental Material), which indicates our main findings still hold.

The Impact of the Chinese Stock Market Crisis

In the first half of 2015, Chinese investors’ enthusiasm for investment was high, the stock price valuation was on the high side, and the upward pressure on the stock price increased. From June to July 2015, the stock price plummeted for four consecutive weeks, until the stock market crisis initially subsided at the end of August 2015. In addition, at the beginning of 2016, China’s A-share market experienced another crisis. From January 4 to January 29, 2016, lasting for 21 trading days, Shanghai stock exchange Composite Index fell from 3,539 to 2,638. To eliminate the potential impact of this stock market crisis in our results, we remove the samples in 2015, and the first quarter of 2016 to do the analysis again and the results are in Table A16 in Appendix 2 (see Supplemental Material), which indicates our main findings still hold.

Clustering at the Firm and Time Levels

To get more rigorous results, we further cluster at both the firm and time levels to conduct our analysis and the results are shown in Table A17 in Appendix 2 (see Supplemental Material). With ΔNCSKEW and ΔDUVOL as dependent variables separately, neither coefficient of interaction term

PSM-DID Analysis

Since the punished firms are not randomly assigned, the influence of other factors may exist in the treated group and the control group, leading to some endogeneity problem. Therefore, we further apply propensity score matching (PSM) method to match similar control variables. To enhance the robustness, one-to-one nearest neighbor matching and one-to-three nearest neighbor matching are used separately. The results are shown in Panel A and Panel B of Table A18 in Appendix 2 (see Supplemental Material). The coefficient of

Additional Analyses

On Possible Internal Mechanism

The Role of Information Disclosure Quality

We examine the impact of information disclosure quality on our main results. The information disclosure quality index (SCORE) based on the “information disclosure evaluation” section on the website of Shenzhen stock exchange can measure the degree of information asymmetry of listed firms.

The information disclosure quality is divided into four grades: excellent, good, qualified, and unqualified by SCORE. We generate three dummies: Excellent

i,t

, Good

i,t

, and Qualified

i,t

. If the information disclosure quality is excellent (good or qualified) in a given year, the value of the corresponding dummy Excellent

i,t

(Good

i,t

or Qualified

i,t

) is 1, otherwise, it is 0. Then we generate three interaction terms:

The results are in Table 5. The coefficients for

Results for Internal Mechanism Discussion: Information Disclosure Quality.

Note. ***Two-tailed statistical significance at the 1% level. **Two-tailed statistical significance at the 5% level. *Two-tailed statistical significance at the 10% level.

The Role of Information Transparency

In this section, we verify H2. Following Hutton et al. (2009), we construct the firm’s information transparency index (OPAQUE) based on earnings management. Then, the sample is divided into high information transparency sample (above average of OPAQUE) and low information transparency sample (below average of OPAQUE).

The results are in Table 6. For the sample with high information transparency, the coefficients for

Results for Internal Mechanism Discussion: Information Transparency.

Note. ***Two-tailed statistical significance at the 1% level. **Two-tailed statistical significance at the 5% level. *Two-tailed statistical significance at the 10% level.

The Role of Media Reputation

In this part, we further verify H2, examine the role of media reputation with a created reputation index. We collect the media report data of all listed firms in CNKI (China National Knowledge Infrastructure, https://www.cnki.net/), the full-text database of Major Chinese Newspapers, and manually sort all the reports into three categories: positive, negative, and neutral. We define a reputation index as a positive reporting tendency of all newspapers. The index is SLANT i,t , and calculated as SLANT i,t = (the number of positive reports − the number of negative reports)/ (1 + the number of positive reports + the number of negative reports) × 100%.

The sample with SLANT

i,t

above average is considered as high reputation sample, and the sample with SLANT

i,t

below or equal to average is considered as low reputation sample. The empirical results are in Table A32 in Appendix 2 (see Supplemental Material). Consider the high reputation sample. The coefficient of

The Role of Corporate Fundamentals

In this section, we verify H3. Firstly, we set up a series of fundamental indicators to examine the different impacts of environmental punishment on the stock price crash risks under different fundamentals. We extracted the first principal component of some financial ratio indicators (asset growth, current debt ratio, cash ratio, EPS, liquidity ratio, quick ratio, asset turnover) to conduct the fundamental analysis. The results are in Table A33 in Appendix 2 (see Supplemental Material). The coefficient of

The Role of Corporate Capital Structure

In this part, we further verify H2. We examine whether the differences of corporate capital structure would affect our findings. The moderate increase of corporate asset liability ratio is conducive to the increase of firm’s value. Therefore, we classify the asset liability ratio in the following ways: if the asset liability ratio is higher than the third quartile or lower than the quarter quantile, it means that the asset liability ratio is too high or too low, indicating that the firm deviates from the optimal capital structure; otherwise, the asset liability ratio is moderate, which means that the firm is close to the optimal capital structure. The results are in Table A35 in Appendix 2 (see Supplemental Material). For sample with high or low asset liability ratio, the impact of environmental punishment on their short-term or long-term development is not significant, but there is a significantly negative impact in the long-term. For sample with moderate asset liability ratio, environmental punishment has no significant impact on their short-term or long-term development. This finding verifies H3.

The Consecutive Environmental Punishment Effect

In our environmental punishment data collected from 2013 to 2017, there are many consecutive punishment cases in some given quarter as shown in Table A36 in Appendix 2 (see Supplemental Material). About half of the firms have been punished consecutively within a given quarter, and the maximum number of consecutive punishments for each of these firms is 10 within a given quarter. Motivated by this observation, we further analyze the impact of consecutive punishment effects on the stock price crash risk accumulation.

We construct a dummy variable

With this new dummy variable, we can construct a triple interaction term

We set dummy variable

Results for Discussing Consecutive Punishment Effect in a Given Quarter.

Note. ***Two-tailed statistical significance at the 1% level. **Two-tailed statistical significance at the 5% level.

In addition, we find that 160 (about 26%) of the 606 punished firms in 2013 to 2017 were punished again in 2018 to 2019. Based on this observation, we conduct another analysis.

We constructed a dummy variable

Results for Discussing Consecutive Punishment Effect at Long Intervals.

Note. **Two-tailed statistical significance at the 5% level. *Two-tailed statistical significance at the 10% level.

Summary and Conclusion

We thoroughly investigate the impact of environmental punishments received by firms on their stock price crash risks, using DID with multiple time periods and PSM-DID methods. We find that after being environmentally punished, compared with the non-punished firms, the punished firm’s stock price crash risk accumulation is increased significantly. Our main findings are robust under various checks. We provide some explanations from the perspective of firm’s fundamentals, information transparency, information disclosure quality to better understand the internal mechanism of our findings. We further analyze the potentially consecutive punishment effect and find that consecutive environmental punishment at long intervals may reveal more negative information, and therefore increasing the stock price crash risk accumulation. However, this effect was not significant at short punishment intervals.

Our work contributes to the literature. First, we advance the understanding about relationship between the crash risk and the firm-level environmental punishment instead of the environmental policies as a whole, which is not well explored in the environmental regulation literature while important for both firms and policy makers. Second, we innovatively suggest revised crash risk measures which can better fit the non-yearly data while still sensitively capture the changes in crash risks. Third, we rigorously verified the impact of a new factor, namely the firm-level environmental punishment, on the crash risk in China, which expand the crash risk literature in the context of emerging economies. Finally, our findings indicate one interesting impact of environmental punishment’s impact on crash risk, namely the consecutive effect, which provide a reference for the effective use of relevant government enforcement powers.

According to our empirical findings, we have the following policy implications in terms of the effective implementation of environmental enforcement. First, the increasing intensity of environmental administrative punishment does have some deterrent effect on environmental violations. The government should balance the environmental punishment and the development of firms to achieve sustainable and stable growth. Second, the improvement of firm’s information transparency and firm’s information disclosure quality may reduce the accumulation risk of stock price crash, and improve the public and investors’ cognition of firms. The government should try to force firms to improve their information disclosure policies to mitigate the risk of stock price crash. Third, the government should implement heavier punishment on those incorrigible firms, such as cumulative punishments, suspend production, or even shut down factories. Only by establishing the rigidity of law enforcement can we possibly eliminate the inertia of firms in performing their duties. Finally, this paper show that the effect of consecutive punishments in a short period of time is not significant, indicating that environmental protection cannot be achieved overnight. Therefore, the government should try to design a long-term environmental enforcement system which would gradually reduce the pollution without fundamentally hurting the economic development.

The limitations and future research directions of our current study are as follows. First, the existing literature on the accumulation of stock crash risk is relatively small, and most of it is about the study of stock crash risk. Due to the limitation of time and space, this paper only analyzes from the perspective of environmental penalties. In the future, we may further analyze from the perspective of internal corporate governance, policy perspective (e.g., green credit policy, etc.), and external factors (e.g., media, analyst evaluation, etc.) to continuously improve this part of the research.

Second, we have studied the potential mechanism of environmental punishments received by firms affecting their stock price crash risks, but there are still some other possible transmission mechanisms, such as credit channels and environmental protection expenditure channels. The corporate credit and environmental protection expenditure channels may be a topic worthy of further study, if more complete micro data including corporate credit costs and corporate environmental protection expenditure data can be obtained.

Finally, the influencing factors of stock price crash risk have been the focus of research, and relatively little literature is to focus on both the economic consequences of stock price crash risk and hedging measures. Will audit committees provide more effective oversight of financial reporting after a stock price crash event? Do firms improve their internal governance and internal controls? This can all be further studied in the future.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440231199871 – Supplemental material for The Effect of Firm-Specific Environmental Punishment on Stock Price Crash Risk: Evidence From China

Supplemental material, sj-docx-1-sgo-10.1177_21582440231199871 for The Effect of Firm-Specific Environmental Punishment on Stock Price Crash Risk: Evidence From China by Minghui Li, Chaohai Shen and Mengyao Wen in SAGE Open

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (grant numbers 72003067, 72173045); the Shanghai Municipal Foundation for Philosophy and Social Science (grant number 2018ECK007); the China Postdoctoral Science Foundation (grant numbers 2016M600292, 2017T100280); Pujiang Talent Program (grant number 18PJC033); and the Shanghai M&A Financial Research Institute Science Foundation.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.