Abstract

Environmental concerns garner global attention, with firms in developing nations responsible for addressing these issues effectively. Environmental disclosure is a prominent aspect of this responsibility, which has become crucial to corporate practice in these nations. This study explores directors’ foreign experience’s influence on a firm’s environmental information disclosure. Data from listed firms in China, a developing country, are employed for this analysis. Using an empirical model, we investigate the proposed hypotheses. The results indicate a trend among firms to favor directors with foreign experience, given their apparent inclination toward environmental information disclosure. However, it’s been observed that corporate governance tends to weaken the positive correlation between hiring directors with foreign experience and environmental information disclosure. This positive association is particularly evident in firms with weak financing constraints, those subjected to strict environmental regulations, and state-owned enterprises. Our study offers valuable insights for managers and decision-makers in developing countries, particularly regarding managing corporate social responsibility and facilitating green transitions in response to environmental regulations. It aids top-tier management in bolstering their internal strategies to optimize their contribution to environmental sustainability. This study, therefore, presents a valuable exploration into the role of directors with foreign experience in influencing firms’ environmental information disclosure.

Introduction

The accelerated pace of the global economy has been accompanied by escalating environmental deterioration. China has been actively involved in global environmental changes, governance, and international cooperation to combat this. Following the implementation of the Paris Agreement in 2016, the Chinese government has ramped up its efforts to address climate change on both international and domestic fronts. China’s 14th Five-Year Plan for National Economic and Social Development posits a peak in carbon dioxide emissions by 2030 and aims to achieve carbon neutrality by 2060. China has made substantial progress in pursuing these goals, with CO2 emissions per unit of GDP dropping by 48.4% compared to 2005 levels, surpassing the international commitment of a 40%–45% reduction.

As major carbon dioxide emitters, firms are pivotal in realizing the “dual carbon” goal. The Chinese government perceives high-quality environmental disclosure as critical for promoting modern environmental governance and laying the groundwork to curtail global warming. Since 2003, China has revised the “Regulations on Firm Environmental Information Disclosure” four times, progressively enhancing disclosure measures and escalating regulatory intensity. These revised regulations play an instrumental role in ensuring that firms disclose environmental information in a timely and comprehensive manner, fulfilling their environmental protection duties, diminishing the release of hazardous gases like CO2, and mitigating global warming.

Given the crucial role of firms as the main consumers of natural resources, they bear significant responsibility for environmental protection. However, their willingness to provide environmental protection information often falls short. Consequently, amplifying firms’ environmental protection information disclosure is critical in China’s environmental governance mechanism.

Numerous factors shape a firm environmental information disclosure strategy formulation and implementation process. Previous studies (Huang & Kung, 2010; Sun et al., 2019; Xue et al., 2021; Zhan, 2021) have identified government regulatory requirements, public policy pressure, and credit pressure as key catalysts for enhancing firm environmental information disclosure governance. Other factors such as corporate size (Ismail et al., 2018; Kumar, 2021), profitability (Ardi & Yulianto, 2020), and a host of inherent factors also play a role. However, existing research tends to focus more on policy and economic factors, with less emphasis on internal relationships and individual director characteristics.

As corporate stewards, directors play a significant role in environmental disclosure, the green transition, and social responsibility. Following the 2008 launch of the “Overseas High-level Talent Introduction Plan” by the central government, a surge of talented individuals with overseas experience returned to China, sparking a “returnee director fever” among listed firms. The question arises whether these returnee directors, as a valuable component of a firm’s human capital, can significantly enhance firm value and governance. Directors’ characteristics influence not only their personal preferences and career development (Schoar & Zuo, 2016) but also various firm decision-making behaviors (Quan et al., 2023), such as innovation (Quan et al., 2023; Sunder et al., 2017), tax avoidance behavior (Wen et al., 2020), and social responsibility (Islam et al., 2021). Earlier studies have demonstrated that executives’ educational background (Knezović & Drkić, 2020; Wu et al., 2017) and life and work experiences (Mahrinasari et al., 2021; Schoar & Zuo, 2016) influence their decision-making, including matters related to firm green governance disclosure. Therefore, this study explores the role of directors’ overseas experience in firm environmental disclosure, aiming to bridge the gap in related research.

As the world’s largest emerging economy, China presents a fitting context for this study. Firstly, China’s economic progress has lured numerous returnee talents over the past two decades. Recognizing that rapid economic growth poses major environmental challenges, the Chinese government has focused on managing environmental issues alongside economic expansion. Secondly, directors with foreign experience, although in short supply, play an integral role in Chinese firms. Previous studies (Cao et al., 2019; Giannetti et al., 2015) using Chinese data have found that firms with foreign-experienced directors perform better and can mitigate the risk of the stock price collapse, although this negative association is more pronounced in firms with serious agency problems, weak corporate governance, and low information transparency.

This study investigates the relationship between directors with foreign experience and firms’ environmental information disclosure using data from Chinese firms from 2010 to 2020. The findings reveal a significant positive relationship between directors with foreign experience and firms’ environmental disclosure. It suggests that directors with foreign experience can bolster a firm’s environmental protection behavior and enhance environmental information disclosure. Further, it was found that corporate governance dilutes the positive relationship between directors with foreign experience and firms’ environmental information disclosure. The positive association is only discernible in firms with weak financing constraints, strict environmental regulations, and state-owned firms. These findings withstand a series of robustness checks.

This study offers several key contributions to the existing literature. Firstly, it presents a novel perspective on the specific influence of director characteristics on firms, specifically examining the association between directors with foreign experience and environmental information disclosure. This study enriches research concerning environmental protection behavior by considering directors’ foreign experience influencing firms’ environmental information disclosure. Both external elements such as environmental regulation (Katarzyna et al., 2020), geographical location (Q. Li et al., 2023), and legal environment (Liu & Liu, 2022), and internal aspects, including firm size, firm image, corporate governance, and development opportunities (Samara et al., 2018) impact environmental protection behavior. Yet, there has been limited investigation into the relationship between directors with foreign experience and firms’ environmental information disclosure. The findings of this study fill a significant lacuna in environment-related literature, particularly pertinent to China, a country grappling with substantial environmental challenges and economic development.

Secondly, this study introduces another determinant influencing a firm’s environmental information disclosure - the characteristics of directors at the strategic decision-making level. Existing research (Gao et al., 2020) has indicated that CEOs’ military experience can imprint environmental values, subsequently motivating increased investment in environmental protection. However, within China’s unique economic system and cultural context, diverse factors influence firm policies and decisions related to environmental protection. This study probes the influence of directors’ foreign experience at the strategic decision-making level. More so than management, directors have the motivation and capacity to disclose environment-related information, given their role in curbing self-serving management behaviors, protecting stakeholders (Giannetti et al., 2015), and reducing information asymmetry with stakeholders (Kwak et al., 2012). Furthermore, this study contributes to the accounting literature by highlighting a unique “people” factor—the director’s foreign experience—within the Chinese context. Foreign experience can instill advanced corporate governance theories into directors, fostering diversified thinking and shaping decisions related to environmental protection.

Lastly, evidence concerning directors’ early life and career experiences and their influence on management decisions and policy preferences is multifaceted. While some research posits that directors who have experienced adversity are risk-averse and opt for more cautious decisions (S. Zhang, 2021), other studies suggest that early adversity experiences engender confidence in directors and a tendency to underestimate risks (Hu et al., 2017). The empirical findings of this study offer additional evidence to support these varied perspectives and to explore this contentious issue further.

The rest of this paper is structured as follows. The next section presents the context of directors’ foreign experience and firms’ environmental information disclosure and develops hypotheses. The third section details the research design, including data sources, model configuration, and definitions of key variables. The fourth section discloses the regression results and analyses them. The fifth section delves into the differential impacts of firm financing constraints, environmental regulations, and ownership heterogeneity on the association between directors with foreign experience and environmental information disclosure. The paper concludes with a summary of the study’s findings.

Literature Review and Hypothesis Development

Literature Review

As green governance practices deepen within firms, it has become increasingly evident that numerous internal and external factors influence the implementation of environmental disclosure. These factors are pivotal in green corporate governance and social responsibility (Nureen et al., 2023). Consequently, researchers globally have delved into the determinants of firms’ environmental disclosures. A review of their findings reveals that government regulatory requirements (Huang & Kung, 2010; Sun et al., 2019), public policy pressure (Huang & Kung, 2010; Xue et al., 2021), dispersed firm ownership (Brammer & Pavelin, 2006), board independence (Gerged, 2021; Okere et al., 2021), “China Famous Brand” status (Zeng et al., 2012), firm size (Ismail et al., 2018; Kumar, 2021), profitability (Ardi & Yulianto, 2020), media coverage (Solikhah & Maulina, 2021), institutional ownership (Y. Li et al., 2022; Tarkhouni et al., 2020), and green credit (Zhan, 2021) are all positively correlated with the quality of environmental information disclosure.

Conversely, separation of control rights and cash flow rights (Zeng et al., 2012), financial leverage (Ismail et al., 2018; Kumar, 2021), CEOs with legal backgrounds (Lewis et al., 2014), executives with military experience (Chen et al., 2021), CEO duality (Caputo et al., 2021), highly politically connected executives (Y. Li et al., 2022), and air quality (C. Y. Wang et al., 2021) all show negative correlations with the quality of environmental information disclosure.

The landscape of international talent migration has evolved significantly in recent years (Harrington & Seabrooke, 2020). Early literature characterized the movement of highly trained individuals from developing to developed countries as a “brain drain,” a term coined about the United States attracting global talent (Bhagwati & Hamada, 1974). Yet, many professionals return to their home countries after studying or working abroad (Roberts & Beamish, 2017; Waddell & Fontenla, 2015). Scholars have since turned their attention to studying the impact of this foreign experience on firms. A wealth of studies has found that returning overseas talents significantly contribute to the economic and social development of their home countries, particularly in emerging economies like China, in sectors such as science and technology (Quan et al., 2023; Wen et al., 2020).

Research reveals that directors with overseas study or work experience often bring back considerable international knowledge or management expertise. Firms guided by boards or executives with foreign experience frequently adopt the governance characteristics and practices of foreign firms (Iliev & Roth, 2018), show a reduced propensity for tax evasion (Wen et al., 2020), display higher investment efficiency (Dai et al., 2018), bear a lower risk of collapse (Cao et al., 2019), exhibit heightened innovation enthusiasm (Quan et al., 2023), and often have higher firm valuations (Giannetti et al., 2015). The unique operational style that directors’ overseas experiences confer can assist firms in making more informed and forward-looking decisions, generating a positive spillover effect on firm development and management. Crucially, the foreign experience of executives or directors can effectively promote corporate social responsibility (Xu & Hou, 2021), facilitating sustainable firm development. Thus, the foreign experience of executives or directors holds significant positive implications for firms and suggests a potentially positive impact on a firm’s environmental disclosures.

Hypothesis Development

Informed by the Upper Echelons Theory (Hambrick & Mason, 1984), it is posited that directors’ values bear considerable influence on strategic decisions and, consequently, overall firm decision-making. The board of directors, as the foremost corporate governance mechanism, carries two essential functions: supervising (monitoring function) and advising managers (advisory function) (Fama & Jensen, 1983). Directors’ characteristics substantially influence these functions (Adams et al., 2010). In our globalized era, it is increasingly common for firm directors to possess foreign experience. Prior studies have demonstrated that board members’ foreign experience significantly affects various aspects of corporate operations, including corporate social responsibility (CSR) commitment (Islam et al., 2021), business risk (Cao et al., 2019), tax avoidance capability (Wen et al., 2020), and firm performance (Giannetti et al., 2015). Psychological and physiological studies further underscore that directors’ risk preferences, thinking patterns, and policy preferences are largely determined by their past experiences (Cronqvist & Yu, 2017; Schoar & Zuo, 2016). Given the significant role of information disclosure in firm decision-making, it follows that directors with foreign experience can effectively monitor managers and encourage environmental information disclosure.

Agency theory provides a lens through which to view managers’ tendencies to accrue additional benefits and power, often at the expense of shareholders (Karpoff, 2021). The agency issue between shareholders and managers becomes more critical when the manager holds a considerable power level (Filatotchev et al., 2022). This principal-agent problem is especially acute in Chinese firms with concentrated shareholding structures and weak internal governance. In such instances, controlling shareholders and managers are incentivized to conceal adverse information for personal gain, thereby impeding environmental information disclosure. Yet, directors who have pursued further education in developed countries—characterized by better legal systems, higher investor protection mechanisms, and stricter disclosure requirements—are likely to possess stronger perceptions of information disclosure, leading to a higher commitment to environmental information disclosure (Islam et al., 2021). Thus, directors with foreign experience are likely more inclined to monitor managers and disclose environmental information.

Drawing from imprinting theory, it can be argued that directors’ foreign experiences “imprint” upon them, particularly during sensitive periods of cognitive structure and value formation (Quan et al., 2023). This imprinting manifests in two forms of environmental information disclosure: “cognitive imprinting” and “competence imprinting.” Cognitive imprinting largely stems from exposure to foreign systems, cultures, and laws. In contrast, competence imprinting is driven by knowledge gained about environmental information disclosure and corporate governance mechanisms in developed countries. As such, directors with foreign experience are likely more proactive in monitoring managers to disclose environmental information (Dixon-Fowler et al., 2017) and more willing to disclose such information.

Moreover, directors with foreign experience tend to be more cost-sensitive and reputation-conscious and are typically more motivated to perform their duties. Reputation theory suggests that these directors may be more concerned about their firm’s information disclosure reputation and, therefore, will monitor managers to enhance environmental information disclosure (Muttakin et al., 2018). Further, environmental information disclosure correlates with the share value of listed firms (Shroff et al., 2017). Directors with foreign experience, who are often more aware of the importance of CSR to firm success (J. Zhang et al., 2018), are likely to advise managers to be more socially responsible and enhance environmental disclosure. Thus, they play a crucial role in formulating an environmental protection vision for the firm (Jędrych et al., 2022; Klimek & Jędrych, 2020) and enhancing its value and reputation.

Given these considerations, this paper’s first hypothesis explores whether directors’ foreign experience significantly impacts firms’ environmental information disclosure.

The Moderating Role of Corporate Governance

Corporate governance, defined as an institutional arrangement that distributes control and residual claims among firm participants (Bacq & Aguilera, 2022), comes into play due to the separation of ownership and management and the establishment of a principal-agent relationship. Inadequate internal corporate governance can foster unethical behaviors within firms (Su & Song, 2022). When internal governance mechanisms falter due to poor governance and the predominance of short-term, opportunistic managerial behaviors, alternative mechanisms may emerge, such as reputation, government relations, or self-regulatory mechanisms (Yiu et al., 2019). Conversely, effective corporate governance can reduce costs, eradicate firm earnings management, boost social responsibility commitments, and foster a sustainable development system (Q. Wang et al., 2021). Consequently, under effective internal governance, the impact of alternative mechanisms, including the directors’ foreign experience considered in this study, is diminished. As such, corporate governance can substitute for directors’ foreign experience, positively influencing firms’ environmental information disclosure.

Firstly, corporate governance can supplant the monitoring effect exerted by directors’ foreign experience. Based on the agency theory, managers may hide adverse information for personal benefits, and corporate governance mechanisms can alleviate these agency problems, substituting for directors’ foreign experiences (Shahzad et al., 2016). Factors like concentrated shareholding structures (Abdallah & Ismail, 2017), more effective boards of directors (Tibiletti et al., 2001), and a higher proportion of independent directors (Tibiletti et al., 2001) can effectively curtail managerial agency behavior. Furthermore, internal monitoring governance mechanisms can contain managerial behavior through specific regulations. Effective corporate governance mechanisms can monitor and discipline agents’ behavior, mitigating conflict between agents and principals (Panda & Leepsa, 2017). As a result, such firms are likely to increase their investment in environmental projects, thereby enhancing firm competitiveness and social responsibility. These investments provide long-term benefits to firms and improve their image. Therefore, the impact of appointing directors with foreign experience on a firm’s environmental disclosure may not be significant in firms with strong governance.

Secondly, corporate governance can substitute for the imprinting effect of directors’ foreign experience. Imprinting theory suggests that directors’ foreign “cognitive imprint” and “competence imprint” bolster environmental disclosure, but effective corporate governance can have a similar effect. Environmental information disclosure is vital to corporate governance (Z. Li et al., 2022). Sound corporate governance encourages management to exhibit greater diligence and responsibility, align management’s goals with those of the firm’s owners, curtail management’s short-term decisions, and promote consideration of the firm’s production operations and the quality of environmental information disclosure from a long-term perspective (M. C. Wang, 2016). Consequently, managers are more likely to prioritize the firm’s long-term value and avoid short-sighted behavior (Pande & Ansari, 2014). Thus, well-governed firms engage in voluntary public disclosure of environmental information to project positive signals to external stakeholders, establish a green firm image, and enhance firm value. This implies that well-governed firms may not need to promote their environmental disclosure behavior through the imprinting effect of directors with foreign experience.

In summary, corporate governance and directors’ foreign experience can similarly affect environmental information disclosure via alternative pathways, suggesting a possible substitution relationship between corporate governance and directors’ foreign experience. Hence, the study proposes the following hypothesis:

Materials and Methods

This section provides detailed information on the construction of the sample and data sources, model specifications, and crucial research variables.

Sample Selection

This study employs data from A-share listed firms on the Shanghai Stock Exchange (SHSE) and the Shenzhen Stock Exchange (SZSE) from 2010 to 2020. The selection of 2010 as introducing a series of environmental protection policies influences the starting point. The validity of data and the standards for annual reports guided the exclusion of the following cases: (1) firms operating in financial industries, such as banks, insurance companies, and investment trusts, due to their unique accounting and reporting requirements and distinct capital structures compared to other firms; (2) firm-year observations of firms with Special Treatment (ST); (3) firm-year observations with incomplete data; (4) firm-year observations with mandatory disclosure requirements. After these exclusions, 12,846 firm-year observations were compiled for analysis.

Data about directors’ foreign experience was sourced from the China Stock Market Accounting Research (CSMAR) system and the Chinese Research Data Services Platform (CNRDS). Manual data collection from www.baidu.com was conducted for missing values related to directors’ foreign experience. Moreover, data concerning the firms’ internal control was extracted from the DIB database. All other data utilized in this study were obtained from the CSMAR system, a leading financial data service provider in China.

Measurement of the Dependent Variable

This study designates the disclosure of environment-related information in a firm’s Corporate Social Responsibility (CSR) report as the dependent variable. It is a binary variable, assigned the value of 1 if a firm discloses environmental information in its CSR report and 0 otherwise. To bolster the robustness of the findings, the environmental responsibility score from Hexun.com is employed to gage the extent of firms’ environmental information disclosure, with higher scores denoting substantial environmental investment and increased transparency in disclosure.

Hexun.com is a credible platform for assessing the social responsibility reports of listed firms. It estimates the environmental responsibility of firms via a professional content-scoring system. This score incorporates various factors such as environmental awareness, environmental management system certification, investment in environmental protection, the number of emission types, and energy-saving measures.

Measurement of Independent Variable

The independent variable in this study is operationalized using two measures. The first measure is a binary variable, assigned a value of 1 if a firm has at least one director with foreign experience and 0 otherwise. In this study, directors with foreign experience are characterized as individuals with either educational or professional exposure outside mainland China.

The second measure of the independent variable is the ratio of directors with foreign experience (i.e., with an education, work history, or both outside of China) to the total number of directors on the firm’s board. It should be noted that individuals who have worked for a foreign branch of a Chinese company or were employed by a Chinese branch of a foreign company or joint venture are not included in this measure. This exclusion ensures that the foreign experience signifies exposure to a foreign environment.

Measurement of Moderating Variable

This study posits that directors with foreign experience can serve as an internal monitoring mechanism, thereby enhancing environmental information disclosure, especially in companies with weaker corporate governance structures. In this study, we utilize earnings management as a gage of corporate governance, positing that higher earnings management indicates subpar corporate governance.

To operationalize this, we use the mean value of earnings management as a benchmark to categorize firms for group regressions. If a firm’s earnings management exceeds the average, it is classified within the “weak corporate governance” group, and conversely, firms with earnings management below the average are considered to have “strong corporate governance.”

Control Variables

In alignment with previous research (Giannetti et al., 2015), we incorporate a variety of control variables in our analysis. These include the natural logarithm of the book value of total assets (Size), firm age calculated as the current year minus the listing year plus one (Age), the ratio of net income to total assets (ROA), the growth rate of operating income measured as the ratio of the change in operating income to the previous period’s operating income (Growth), and the ratio of total debts to total assets (Lev).

We also consider ownership structure (Top1 and MH), the proportion of independent directors on a firm’s board (BDI), whether the roles of chairman and general manager are held by the same individual (DUAL), the quality of internal control (IC), and the ratio of market price to book value (PB).

Moreover, our model includes year and industry fixed effects for temporal and sectoral variations. The industry fixed effects are determined based on the coding provided by the China Securities Regulatory Commission (CSRC). We use the two-digit industry code for manufacturing firms, while a one-digit code is used for other industries.

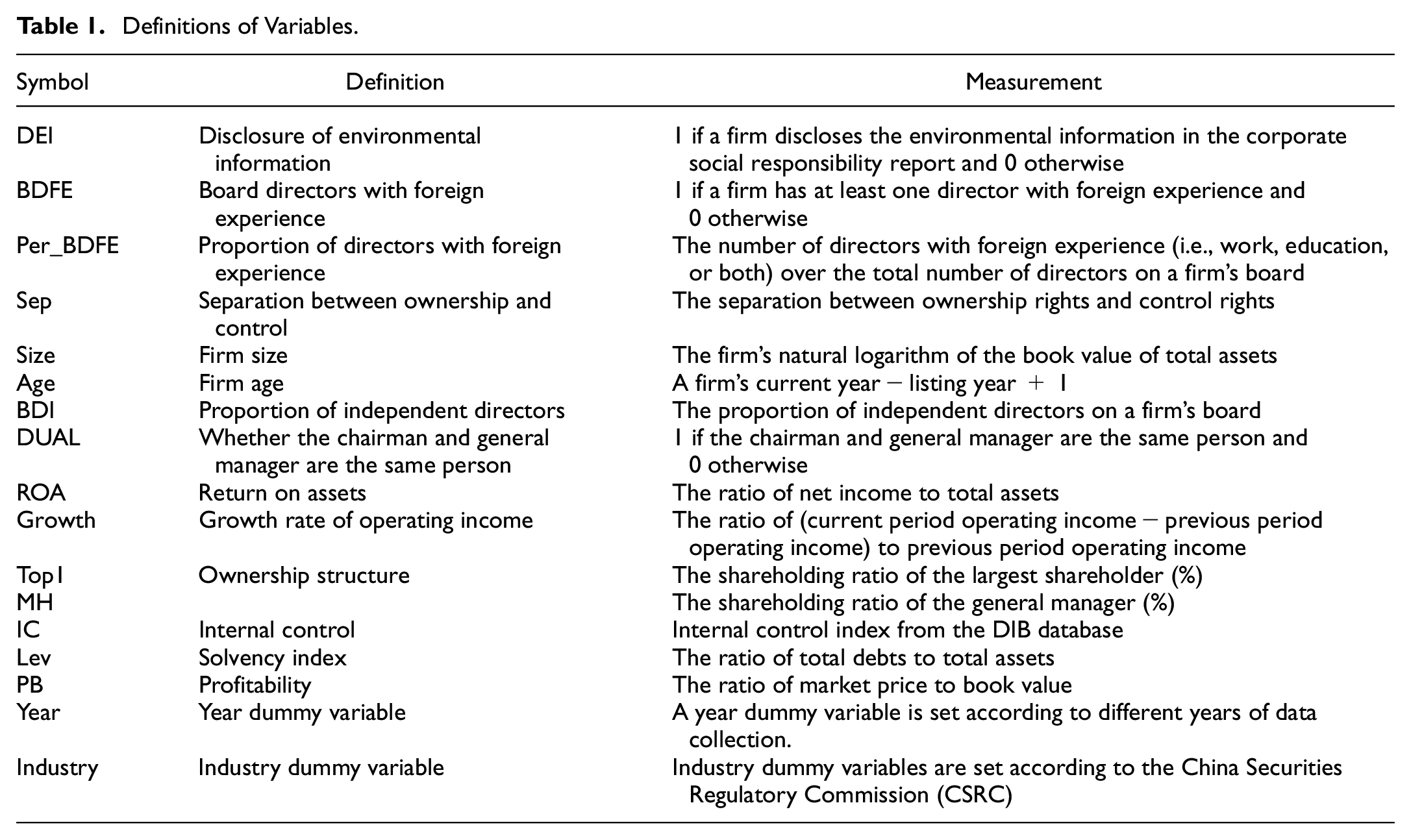

Table 1 provides comprehensive definitions for each variable. To mitigate the influence of extreme values, we winsorize all continuous variables at the 1% level on both ends of the distribution.

Definitions of Variables.

Empirical Model

To explore the relationship between directors’ foreign experience and firms’ environmental information disclosure, we employ a logistic regression model as delineated in Model (1):

Additionally, to analyze the moderating influence of corporate governance on the above relationship, we construct the following regression model, Model (2):

Given that the dependent variable is discrete (i.e., whether a firm discloses environmental information or not), it is necessary to employ an appropriate model to accommodate this type of outcome. Utilizing a standard linear regression could produce estimated probabilities outside the [0,1] interval and would assume the residuals follow a normal distribution, which is not the case here.

To rectify these issues and ensure the predicted values of the dependent variable lie within [0,1], we employ the logistic regression model, also known as the logit model. This non-linear approach establishes a “link function” between the independent and dependent variables, considering the binary nature of the dependent variable. It effectively models the log odds of the dependent variable equaling “1.”

In this research, “environmental information disclosure” (the dependent variable) is a binary outcome, which, if estimated with a standard linear model, would lead to inconsistent estimation and implausible predicted values. Therefore, we use the logit model for its estimation. The primary independent variable—“directors with overseas experience”—is also binary, but this does not impede the estimation results.

Results

Descriptive Statistics

Table 2 presents the summary statistics for the study’s variables of interest. The mean value for environmental information disclosure (CSR) is 0.324, with a standard deviation of 0.468. This suggests that only around 32.4% of listed firms disclose environmental information. Using the environmental responsibility score as a measure of environmental disclosure, we find a mean value of 2.05 with a standard deviation of 5.408. This indicates a substantial divergence in the levels of environmental disclosure among different firms, which implies a need for Chinese-listed firms to enhance their environmental protection information disclosure.

Descriptive Statistics.

Note. All variables as previously defined.

Regarding directors with foreign experience (BDFE), we find a mean value of 0.54 and a standard deviation of 0.498. This reveals that over half of the firms employ directors with foreign experience. However, these individuals represent a relatively small portion of the board members, with a mean ratio of 0.106, equating to nearly 11%.

Lastly, the mean of Sep, a measure of corporate governance issues, is 0.493. This indicates that less than half of the firms have severe corporate governance concerns.

Correlation Analysis

Table 3 presents the Pearson correlation coefficients for the principal variables in this study. The findings reveal a significant positive correlation at the 1% level between our main variable of interest, that is, whether a firm has at least one director with foreign experience (BDFE), and firms’ disclosure of environmental information (CSR and Environ_score). These preliminary results provide initial validation for the study’s first hypothesis.

Correlation Analysis.

Note. All variables as previously defined.

Denotes significance at the 1% level. **Denotes significance at the 5% level. *Denotes significance at the 10% level.

In addition, there’s a significant positive correlation at the 1% level between the proportion of directors with foreign experience on a board (Per_BDFE) and the firm’s environmental information disclosure. Notably, all correlations between the independent variables are relatively low, suggesting limited multicollinearity concerns within our analysis.

Main Results

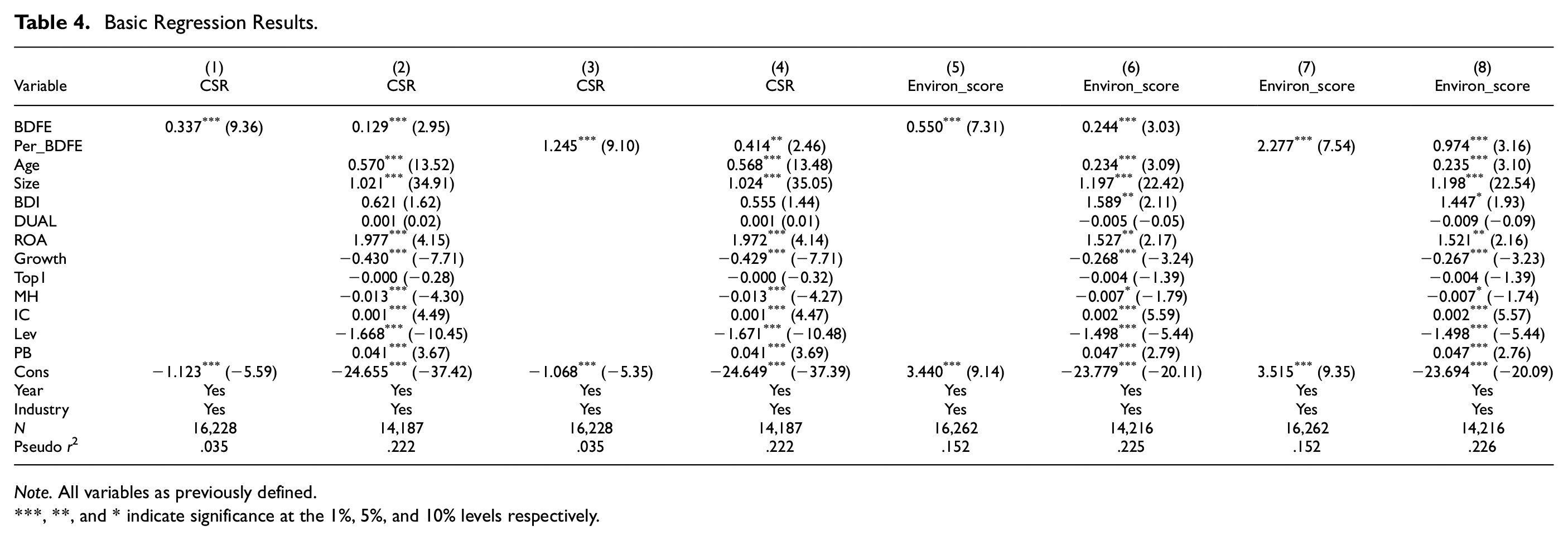

Table 4 presents the regression analysis on the relationship between directors with foreign experience and firms’ environmental information disclosure. Using CSR as a measure of environmental disclosures, Columns (1) and (3) show that both the coefficients for the presence of at least one director with foreign experience (BDFE) and the proportion of directors with foreign experience on a board (Per_BDFE) are statistically positive at the 1% level. Additionally, when control variables are incorporated (Columns (2) and (4)), the coefficients for BDFE and Per_BDFE retain their significance at the 1% and 5% levels, respectively.

Basic Regression Results.

Note. All variables as previously defined.

, **, and * indicate significance at the 1%, 5%, and 10% levels respectively.

Similar results are obtained when using Environ_score as the measurement for environmental disclosures. With or without control variables, the coefficients for BDFE and Per_BDFE remain statistically positive at the 1% level. The findings imply that firms employing directors with foreign experience are more likely to disclose environmental information, supporting our first hypothesis.

Directors with foreign experience, influenced by the external environment of developed countries, exhibit enhanced perceptions toward information disclosure. They tend to be more independent, professional, future-oriented, and environmentally aware (Emmanuel et al., 2018), driving them to oversee environmental managerial disclosure (Slater & Dixon-Fowler, 2009). Further, the foreign experience of directors leaves an “imprint” that continuously influences their decision-making upon returning to their home country (Nishida, 1999). Also, reputation theory posits that these directors are more reputation-conscious, thus, more motivated to fulfill their supervisory functions impartially and objectively. Consequently, integrating directors with foreign experience prompts firms to disclose environmental information more actively, underscoring the relevance of corporate governance research.

In line with previous literature (Giannetti et al., 2015), control variable coefficients display expected trends. Variables depicting firm complexity, such as larger firm size (Size), firm age (Age), a higher net income to total asset ratio (ROA), better internal control (IC), and a higher market price to book value ratio (PB), are positively correlated with environmental information disclosure. In contrast, variables reflecting business risks, such as the ratio of current to previous operating income (Growth) and the total debts to total assets ratio (Lev), show a negative association with environmental information disclosure.

Table 5 delineates the regression results concerning the moderating role of corporate governance on the connection between directors’ foreign experience and environmental information disclosure. Our sample is divided into firms with strong and weak corporate governance based on whether their earnings management is above or below the yearly mean. The coefficients for BDFE and Per_BDFE are significantly positive only within the weak corporate governance group, irrespective of the environmental disclosure measure used. This suggests corporate governance mitigates the positive correlation between directors’ foreign experience and firms’ environmental information disclosure. Thus, these directors are more crucial in promoting environmental information disclosure in firms with weaker corporate governance.

Results for Moderating Effects of Corporate Governance.

Note. All variables as previously defined.

, **, and * indicate significance at the 1%, 5%, and 10% levels respectively.

Hence, directors with foreign experience serve a governance role, especially within firms exhibiting weaker corporate governance. This study contributes to the literature on the influence of directors’ characteristics on corporate governance. It also extends the Upper Echelons Theory (Hambrick & Mason, 1984) by suggesting that the presence of foreign-experienced directors can help firms optimize their governance system, enhance information disclosure levels, and reduce information asymmetry.

Robustness Test

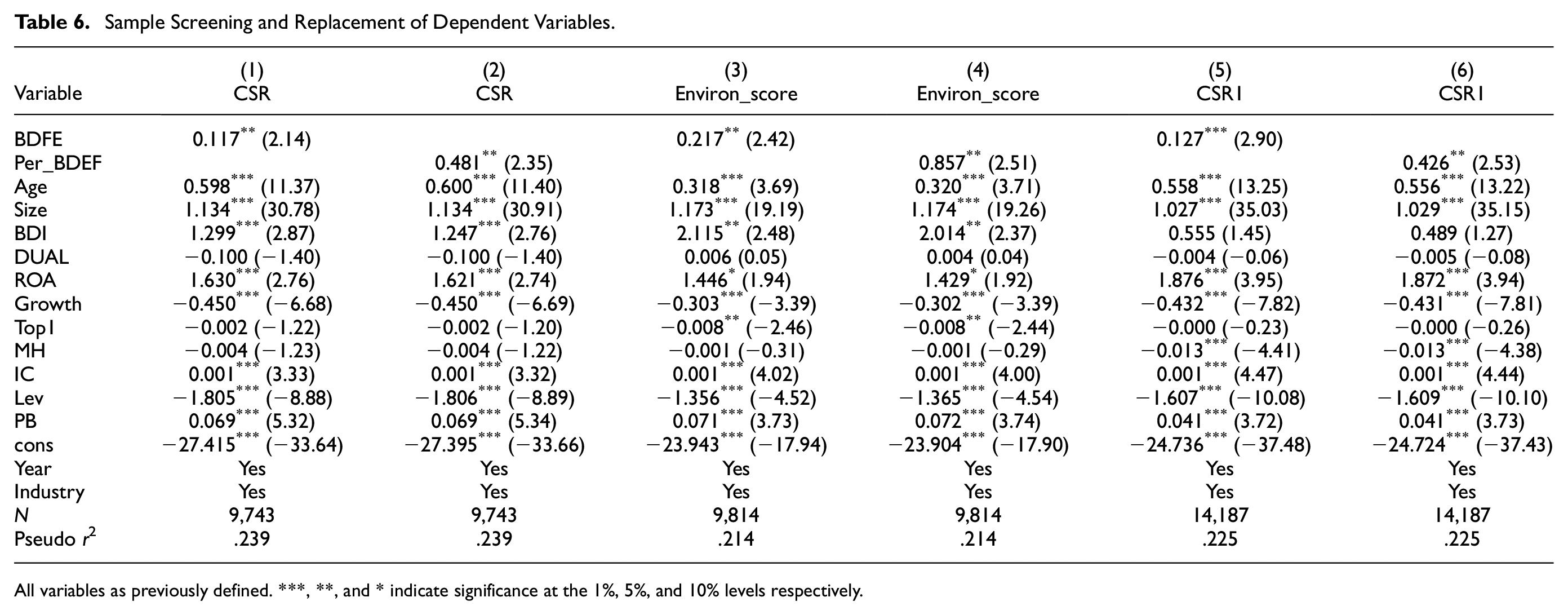

Given that heavily polluting industries in China are under more stringent environmental regulations, these rules may influence firms’ environmental information disclosure. To address this concern, this study excludes heavily polluting industries from the sample and performs a robustness check. Based on the Classified Management List of Environmental Protection Verification Industries of Listed Firms, we extract a sample of 4,941 from 16 heavily polluting industries, including thermal power, iron and steel, cement, electrolytic aluminum, coal, metallurgy, chemical, petrochemical, building materials, papermaking, brewing, pharmaceutical, fermentation, textile, tanning, and mining. The findings, shown in columns (1) to (4) of Table 6, indicate that the coefficients of the presence of at least one director with foreign experience (BDFE) and the proportion of directors with foreign experience on a board (Per_BDFE) remain statistically positive at the 5% level. This suggests that directors with foreign experience continue to facilitate firms’ environmental information disclosure, even after the exclusion of firms facing stricter environmental regulations.

Sample Screening and Replacement of Dependent Variables.

All variables as previously defined. ***, **, and * indicate significance at the 1%, 5%, and 10% levels respectively.

Since environmental information is disclosed across various reports such as CSR, financial, and environmental reports, this study focuses on information disclosed in the CSR report due to its environmental richness compared to the other reports. For the robustness check, the study integrates the environmental information from the CSR and environmental reports to create a new variable. The results are presented in columns (5) and (6) of Table 6. The coefficients of BDFE and Per_BDFE continue to show significant positivity at the 1% and 5% levels, respectively.

We further conduct a logistic regression robustness test with the subsamples of different director categories: those with foreign work experience (OSW), foreign education experience (OSE), both foreign work and education experience (OS), the proportion of directors with foreign work experience (POW), foreign education experience (POE), and both foreign work and education experience (POS). The findings are exhibited in Table 7. When environmental disclosures are measured by CSR, Columns (1) to (3) show that the OSW, OSE, and OS coefficients are statistically positive at 1%, 5%, and 1%, respectively. Similarly, the POW, POE, and POS coefficients in Columns (4) to (6) are significantly positive at 5%, 5%, and 1%, respectively. When environmental disclosures are measured by Environ_score, the OSW, OSE, and OS coefficients in Columns (7) to (9) remain statistically positive at 5%, 1%, and 1%, respectively, as do the POW, POE, and POS coefficients in Columns (10) to (12) at 5%, 1%, and 1%.

Alternative Measure Results of the Independent Variable.

Note. All variables as previously defined.

, **, and * indicate significance at the 1%, 5%, and 10% levels respectively.

The coefficients of OSW, OSE, and OS are 0.071, 0.065, and 0.142 (0.103, 0.181, and 0.272, respectively), suggesting that firms’ environmental information disclosure increases with the number of directors possessing foreign experience. Further, directors with work and education experience abroad are more inclined to disclose environmental information than those with just one type of foreign experience. The coefficient of POS (1.155/2.247) is higher than that of POE (0.438/1.439) or POW (0.493/0.752), indicating that directors with foreign work experience possess superior professional judgment and management ability (Yuan & Wen, 2018), and an understanding of environmental protection.

Conversely, directors with foreign education are likely to uphold higher ethical standards and a stronger sense of social responsibility (Cho et al., 2017). They also show a greater understanding and judgment in formulating environmental protection systems. Therefore, directors with foreign experience can catalyze firms to disclose environmental information.

Solution of Endogenous Issues

Propensity Score Matching (PSM) Method

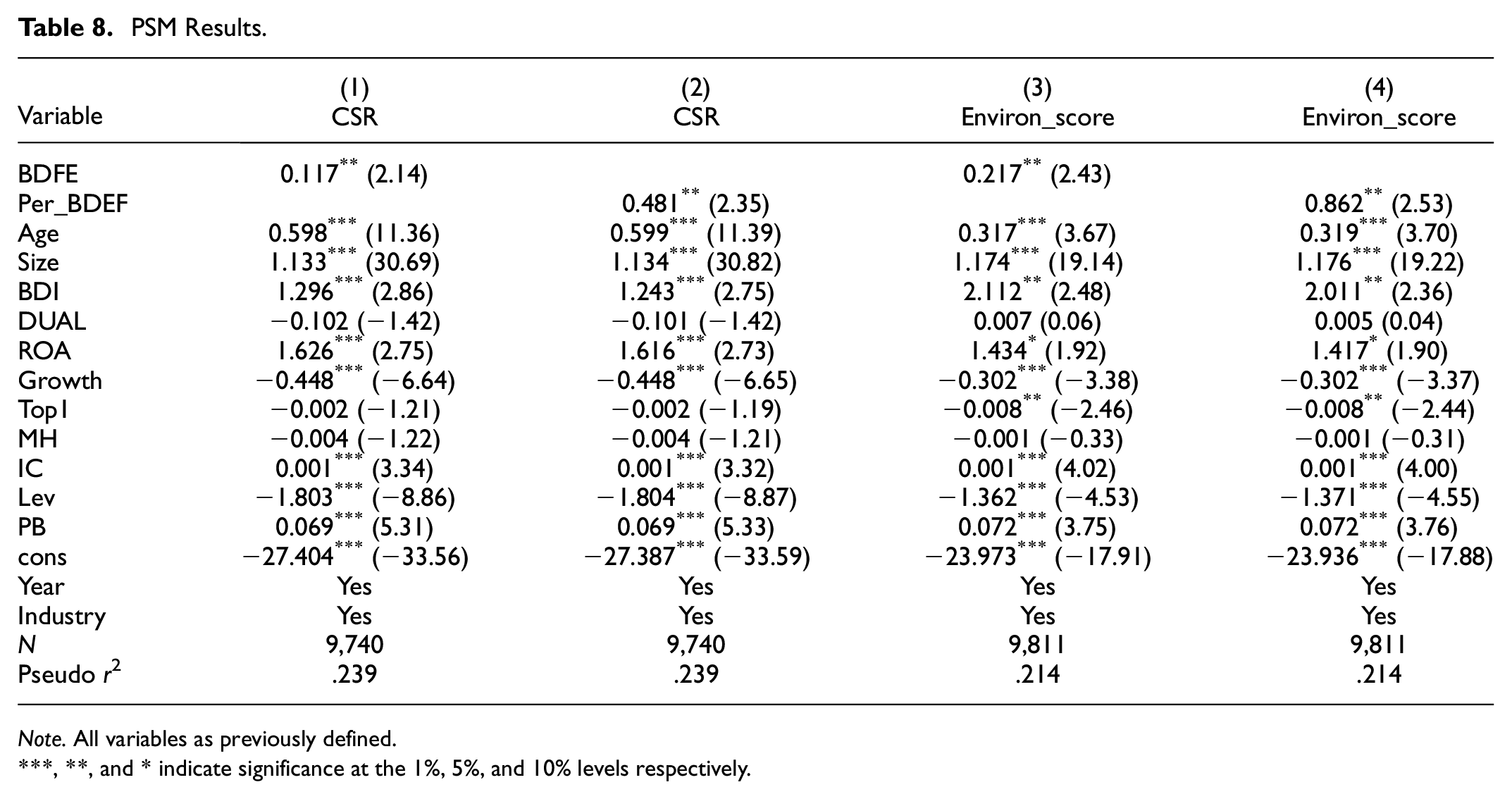

Thus far, this study has not considered any potential endogeneity problems, such as the correlated omitted variable bias that may occur in the regression. Instead, this study addresses this issue using a propensity score matching sample. Specifically, this study utilizes a logit model to regress the indicator variable of directors with foreign experience on control variables in the model (1). It estimates a firm’s propensity score with at least a director with foreign experience. Next, this study matches each treatment firm (foreign experience = 1) with a control firm (foreign experience = 0) with the closest propensity score. This study requires the caliper to be 0.01 and performs the matching with replacement. Then this study runs the regression with the matched sample and reports the results in Table 8. Both coefficients of whether a firm has at least one director with foreign experience (BDFE) and the proportion of directors with foreign experience on a board (Per_BDFE) are statistically positive at the 5% level. Thus, the finding is robust to the potential endogeneity concerns.

PSM Results.

Note. All variables as previously defined.

, **, and * indicate significance at the 1%, 5%, and 10% levels respectively.

Heckman Selection Model

Self-selection bias is likely to occur in this study. Firms with certain characteristics might be more likely to hire directors with foreign experience and disclose environmental information. The hiring decision is not a random choice, introducing self-selection bias. To mitigate this potential issue, this study employs the Heckman selection model. In the first stage, this study calculates the Inverse Mills Ratio (IMR) coefficient by including variables such as Size, Age, Growth, ROA, Lev, BDI, DUAL, Top1, MH, IC, BS, SOE, and the industry and year fixed effect. Besides, following Quan et al. (2023), this study utilizes the average proportion of directors with foreign experience (MPer_BDFE) in a board as the instrumental variable that satisfies Heckman’s exogenous variable requirement model. Firms in the same industry will likely have similar incentives for hiring directors with foreign experience. Therefore, the average industry-level variable is positively associated with BDFE but is less likely to affect firms’ environmental information disclosure.

The results of Heckman’s selection model are listed in Table 9. Column (1) shows the first stage regression results. IMR generated from the first stage is included in the second stage. Columns (2) to (5) show that after controlling the IMR, the coefficients of BDFE and Per_BDFE are statistically positive at the 5% level at least. Accordingly, the results are robust to the potential endogeneity concerns.

Heckman Results.

Note. All variables as previously defined.

, **, and * indicate significance at the 1%, 5%, and 10% levels respectively.

Instrumental Variable Estimations

The foreign experience of directors likely affects the disclosure of environmental information. At the same time, firms may be motivated to hire directors with foreign experience to improve their environmental disclosure. Therefore, there may exist an endogeneity issue. This study employs the instrumental variable method to solve the possible endogeneity problem.

Based on previous studies (Giannetti et al., 2015; Quan et al., 2023), this study utilizes the attracting highly-skilled talent policy (TalentPolicy) as the instrumental variable in the regression. TalentPolicy is a dummy variable that equals 1 if there is a policy in the province where the firm is located that encourages the return of highly-skilled talents before 2000 and 0 otherwise. Introducing provincial policies should positively affect directors with foreign experience but are less likely to influence environmental information disclosure directly. The second instrumental variable is the index of investor protection (Stakeprotect), obtained from the Investor Protection Research Center of Beijing Technology and Business University.

The instrumental variable passes the weak instrumental variable test and override test. Therefore, the two-stage regression method is employed. The regression results of the first stage are shown in columns (1) and (3) of Table 10. The results of the second stage are shown in columns (2) and (4) of Table 10. In the first stage, the coefficients of TalentPolicy and Stakeprotect are statistically positive at 1% with BDFE and Per_BDFE. In the second stage, the coefficients of BDFE and Per_BDFE are both significantly positive at 1% levels. The results of the robustness checks lend further support to the hypotheses of this study.

Results of the Instrumental Variable Method.

Note. All variables as previously defined.

, **, and * indicate significance at the 1%, 5%, and 10% levels respectively.

Further Research

Financing Constraints (SA)

There are characteristics of a long cycle, high risk, and slow income generation for environmental investments (Shahzad et al., 2016), making financing constraints common for Chinese listed firms. Firms with strong financing constraints have a prominent “crowding out effect” of investments, reducing environmental investments. Conversely, firms with weak financing constraints have more environmental protection investments. To maximize the value of environmental investments, environmental disclosure is an important medium to convey firms’ excellent development concepts and prospects to the stakeholders and attract potential investors (de Gooyert et al., 2017).

In this study, the financing constraint (SA) variable proposed by Hadlock and Pierce (Hadlock & Pierce, 2010) measures firms’ degree of financing constraint. Firms with greater than the median of SA are the group with weak financing constraints, and those with less than the median of SA are the group with strong financing constraints. The specific calculation formula is as follows.

Where

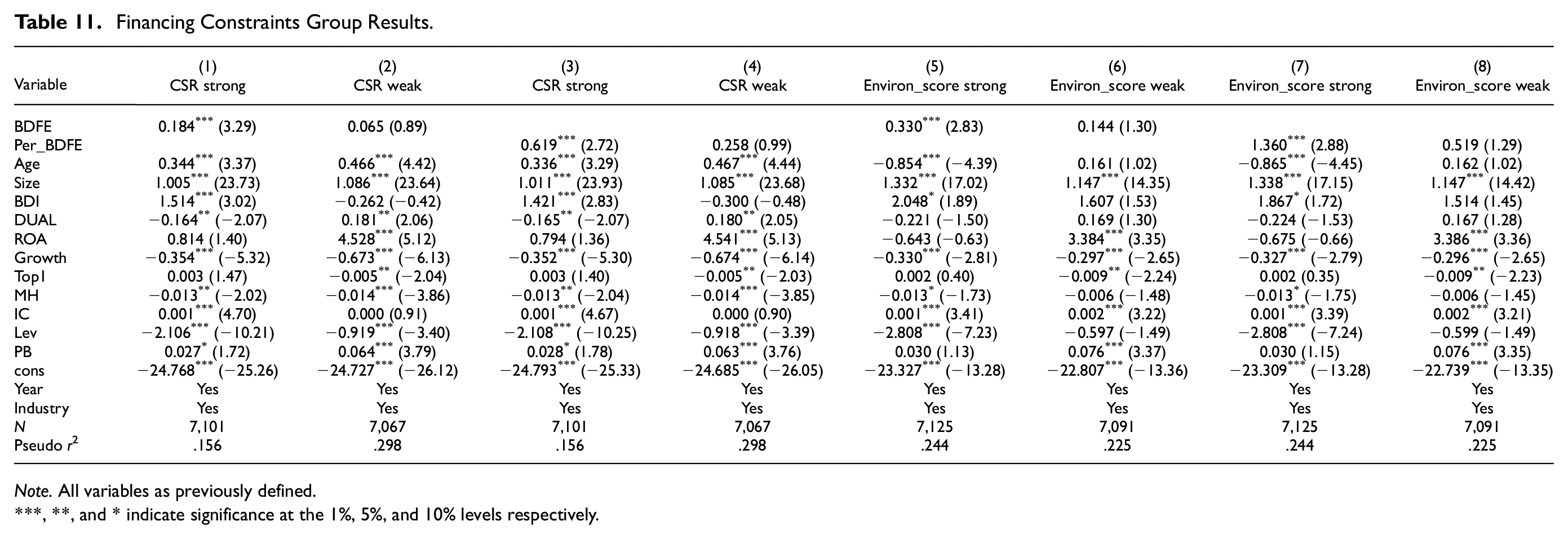

Table 11 shows the regression results based on the grouping of financing constraints. Columns (1) to (3) and (5) to (7) show the strong financing constraint group’s regression results of environmental information disclosure associated with BDFE and Per_BDFE. The results show that there is a significantly positive association between environmental information disclosure and directors with foreign experience and the proportion of directors with foreign experience on a board at the 1% levels, respectively. The results suggest that strong financing constraints weaken the positive relationship between directors’ foreign experience and firms’ environmental information disclosure. Firms must prioritize their operation over environmental protection investments (Andersen, 2016), reducing their willingness to disclose environmental information.

Financing Constraints Group Results.

Note. All variables as previously defined.

, **, and * indicate significance at the 1%, 5%, and 10% levels respectively.

However, columns (2) to (4) and (6) to (8) present insignificant results of environmental information disclosure associated with BDFE and Per_BDFE for weak financing constraint groups. A firm with weak financing constraints has resources for normal operation, combined with the foreign experience of directors, improving firms’ environmental protection consciousness and optimizing corporate governance. As a result, firms input more resources into environmental protection and increase the willingness to disclose environmental information accordingly.

Environmental Regulation

Environmental protection is attributed to public goods, while environmental pollution has negative externalities (Ling et al., 2018). Environmental regulation refers to the institutional arrangement of the government to regulate the failure of the market mechanism in environmental externalities. The environmental expenditures of firms are mainly the costs incurred in response to environmental regulations. The stronger the environmental regulation, the more resources the firm devotes to environmental protection. Directors with foreign experience are more inclined to disclose environmental protection information.

This study uses the method of Ren et al. (2020) to calculate the comprehensive index of environmental regulation based on industrial wastewater discharge per unit output value, industrial SO2 discharge per unit output value, and industrial soot discharge per unit output value. The comprehensive index of environmental regulation increases with the pollution discharge. The specific measurement methods of the comprehensive index of environmental regulation are as follows.

Firstly, industrial wastewater discharge per unit output value, industrial SO2 discharge per unit output value, and industrial soot discharge per unit output value of each city are standardized, as shown in model (4).

where

This study calculates the environmental regulation intensity of city i as shown in model (6).

Following M. C. Wang (2016), each city’s calculated environmental regulation intensity is grouped according to the median. The group greater than the median is the group with weak environmental regulation, and the group less than the median is the group with strong environmental regulation. The regression results are shown in Table 12. Columns (1) to (3) and (5) to (7) show regression results for the strong environmental regulation group. Columns (2) to (4) and (6) to (8) present regression results for the weak environmental regulation group. Results show that for the group with strong environmental regulation, whether the firm has at least a director with foreign experience and the proportion of directors with foreign experience on a board are significantly and positively associated with environmental information disclosure at 5% levels at least. However, there is almost an insignificant relationship (except column (6)) between environmental information disclosure and BDFE/Per_BDFE for the group with weak environmental regulation. The results indicate that environmental regulation enhances the positive association between directors’ foreign experience and firms’ environmental information disclosure.

Environmental Regulation Sub-Group Results.

Note. All variables as previously defined.

, **, and * indicate significance at the 1%, 5%, and 10% levels respectively.

Moreover, environmental regulation can improve environmental quality (Tanaka, 2014). Improving environmental quality is conducive to enhancing the willingness of firms to disclose environmental information. In the group with strong environmental regulation, the firm spends more resources on environmental protection activities to achieve environmental regulation requirements. Therefore, directors with foreign experience have better environmental awareness to explore the related environmental protection opportunities (Masulis et al., 2012) and have more willing to disclose environmental information (de Gooyert et al., 2017).

Grouping Regression of Ownership

Chinese firms are divided into state-owned and non-state-owned firms according to whether the ultimate controller is the government. Non-state-owned firms pay more attention to maximizing economic benefits and are far less capable of obtaining resources than state-owned firms. State-owned firms are subject to higher government intervention and stricter supervision (Chi, 2021). The economic decisions of state-owned firms reflect the government’s will, including environmental governance and protection. Therefore, state-owned firms must inevitably assume more environmental protection responsibilities and increase their investment (Tang & Li, 2013).

An interesting issue is how directors’ foreign experience affects firms’ environmental information disclosure under different ownerships differently. This study divides the samples into state-owned and non-state-owned groups for the regression. The regression results are shown in Table 13. Columns (1) to (3) and (5) to (7) are the state-owned group, and Columns (2) to (4) and (6) to (8) are the non-state-owned group. In the state-owned firm group, whether the firm has at least a director with foreign experience and the proportion of directors with foreign experience on a board are significantly and positively associated with disclosing environmental information at a 5% level at least. However, the non-state-owned group has an insignificant association with them.

Grouped Ownership Results.

Note. All variables as previously defined.

, **, and * indicate significance at the 1%, 5%, and 10% levels respectively.

The findings show that state-owned firms, on the one hand, are under the pressure of environmental protection and strict environmental supervision imposed by the government and public (Anton et al., 2004) and have a stronger impetus to implement environmental protection. On the other hand, state-owned firms with political resources and financing advantages are more capable of environmental investment. Therefore, directors with foreign experience can further improve the environmental awareness of state-owned firms and fulfill the environmental protection of social responsibilities. Furthermore, introducing directors with foreign experience can promote environmental protection information disclosure.

Conclusions and Discussions

The concept of sustainable development in firms originates from the Triple Bottom Line (TBL) theory proposed by Elkington (1998). While corporations have undoubtedly spurred economic growth, their activities have led to significant environmental challenges. Thus, the call for businesses to shoulder responsibility for their environmental footprints has intensified. Firms’ environmental disclosure policies can influence their financial performance (CFP) and operational decision-making related to the environment (Ardi & Yulianto, 2020; Kumar, 2021; Sun et al., 2019). Previous studies have concentrated on stable long-term characteristics such as firm size, profitability, and government regulatory requirements - factors that businesses cannot alter quickly or at all. This paper, in contrast, pivots to board-level executive characteristics, offering a practical approach for substantive changes in firm environmental information disclosure.

In the Chinese context, the “returnees fever” phenomenon underscores the demand for directors with foreign experience who play pivotal roles in Chinese firms. Earlier research (Giannetti et al., 2015) suggests that these firms tend to perform better. This study’s key findings include (1) a strong positive association between foreign-experienced directors and firm environmental disclosure, implying such directors can enhance a company’s environmental stewardship and promote disclosure; (2) a moderating effect of corporate governance on this positive relationship; and (3) a correlation between environmental information disclosure and directors with foreign experience, noticeable only in firms with weak financing constraints, stringent environmental regulations, and state ownership.

This study enriches our understanding of corporate governance and sustainable development under China’s “dual carbon” framework. By identifying gaps in the current literature, we pave the way for further research. More focused studies are needed considering corporations’ pivotal role in managing limited global resources and promoting sustainability. Our analysis offers valuable insights for academia, practitioners, and policymakers, helping firms adjust their executive structures to foster sustainability-related practices.

Potential areas for future research include exploring international experiences further and enhancing sustainability theory. The relationship between top management characteristics and sustainability issues, like environmental disclosure, warrants a more profound exploration. Also, research should address the interplay between firm behavior and societal sustainability. While sustainable development includes economic, social, and environmental dimensions, most studies focus on only one or two aspects, typically neglecting the social aspect. Future research should thus integrate sociology and management studies.

Another potential direction is clarifying the theoretical framework of corporate management and environmental disclosure. Future research should delve deeper into organizational characteristics, semi-structured sustainable development models, social responsibility infrastructure, and the balance of cooperation and competition. Furthermore, an international comparison would provide invaluable insights into the relationship between corporate internal governance structures and environmental disclosure.

However, this research has limitations. Firstly, it may be more relevant to developing countries due to the talent flow to developing countries, where advanced management concepts are learned and later applied in developing countries. Secondly, the research is subject to government policy as different countries have varied requirements for environmental information disclosure.

This research suggests several policy implications. Firstly, the foreign experience of directors can enhance environmental disclosure. Chinese firms should respond actively to the national policy of “importing high-level talents from overseas,” enhancing their executive team diversity. Secondly, due to China’s unique social background and dominant state-owned economic system, the introduction of overseas talents and environmental governance should be adapted to local conditions, not merely imitating foreign models. Finally, while foreign experience positively impacts environmental disclosure, it’s not a panacea and shouldn’t be pursued unthinkingly. An appropriate tracking mechanism is needed to monitor the specific effects on different firms and to make timely adjustments to the management structure.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Zhejiang Office of Philosophy and Social Science, Grant/ Award Number: 23NDJC154YB. “Study on the Course Module Design and Teaching Model Reform for Training Excellent Accounting Talents under the Convergence of ‘Dual Carbon’ Goals and Digital Economy”—a Graduate Teaching Reform Project of the Zhejiang Province’s 14th Five-Year Plan.

Informed Consent Statement

“Not applicable.” for studies not involving humans.

Data Availability Statement

The data supporting this study’s findings are available from the corresponding author upon reasonable request.