Abstract

This study provides a comprehensive synthesis of empirical research on the Balanced Scorecard (BSC), examining the interrelationships among its four core dimensions. By employing a meta-analytic approach, the study quantifies the strength and direction of these relationships and evaluates the consistency of effect sizes across prior research. The analysis integrates findings from a broad dataset to uncover patterns that clarify how learning and growth, internal processes, customer satisfaction, and financial performance interact to drive organizational success. The results highlight the pivotal role of learning and growth in enhancing overall performance, while internal process improvements and customer satisfaction emerge as key contributors to financial health. These findings reinforce the BSC’s value as a holistic performance management framework, demonstrating that optimizing each dimension produces synergistic benefits across the organization. The study offers evidence-based insights for both scholars and practitioners, emphasizing the strategic importance of understanding these interdependencies to improve decision-making and performance management.

Plain Language Summary

Why was the study done? Many companies use the Balanced Scorecard (BSC) as a tool to measure and improve performance. However, while it’s widely used, not much research has explored how the four key areas of the BSC—learning and growth, internal processes, customer, and financial—work together to affect a company’s overall success. What did the researchers do? The researchers analyzed data from 134 studies, which included more than 700,000 observations, to better understand how the four areas of the Balanced Scorecard are connected, and how they impact a company’s financial outcomes. They used a statistical approach called meta-analysis to uncover patterns in the data. What did the researchers find? The study found that the four areas of the BSC are closely linked. Improving learning and growth had a strong positive effect on overall performance. Additionally, better internal processes were found to be closely related to improved customer satisfaction, both of which help drive financial success. What do the findings mean? The research shows that the Balanced Scorecard is a powerful tool for managing and improving performance. By focusing on all four areas—learning, internal processes, customer experience, and financial health—companies can create stronger, more interconnected systems that lead to better decision-making and better overall results.

Keywords

Introduction

The Balanced Scorecard (BSC) is a strategic management framework that integrates financial and non-financial performance indicators (Kaplan & Norton, 1996). While its four dimensions—learning and growth, internal processes, customer satisfaction, and financial performance—provide a holistic view of organizational effectiveness, a lack of clarity regarding the interdependencies among these dimensions presents a significant challenge. Prior research often isolates these dimensions or yields mixed findings, particularly regarding how improvements in leading indicators influence financial outcomes. Understanding these interrelationships is critical for strategic management. Despite the recognized importance of the BSC as a strategic management tool, a comprehensive understanding of the intricate interdependencies among its four dimensions remains underdeveloped in the existing literature. This gap hinders organizations’ ability to fully leverage the BSC’s synergistic benefits for achieving strategic objectives.

The theoretical foundations of the BSC—rooted in the resource-based view (RBV; Barney, 1991), dynamic capabilities theory, and organizational learning theory (Garvin, 1993)—offer important insights but fail to fully explain the interactions between leading and lagging indicators within the BSC framework. The RBV emphasizes internal capabilities, such as human capital and knowledge sharing, as key sources of competitive advantage (Barney, 1991). However, it does not explicitly account for how these capabilities translate into firm performance through the interconnections between BSC dimensions. Similarly, dynamic capabilities theory describes how firms adapt through innovation and reconfiguration of resources, yet empirical studies often overlook the full pathway from internal learning to process improvement, customer satisfaction, and financial returns (Teece et al., 1997). Organizational learning theory (Garvin, 1993) further highlights the role of knowledge acquisition and dissemination in driving competitive advantage but does not fully integrate how these learning processes interact with financial outcomes. For instance, while business planning, marketing, or return on investment (ROI) are commonly examined as components of organizational learning, their integration with lagging indicators, such as profitability or shareholder value, remains underexplored.

This study addresses these theoretical limitations by framing the BSC as a causal model in which leading indicators influence one another through a cascading process, ultimately shaping financial performance. Specifically, it aims to provide empirical support for this cascading relationship, demonstrating how factors such as employee motivation contribute to innovation, which in turn enhances customer satisfaction and drives financial outcomes. By employing a meta-analytic framework, this study not only validates these relationships statistically but also identifies the strongest links and areas of inconsistency, highlighting the need for further investigation.

While the BSC has been widely adopted in practice, empirical research on its effectiveness remains inconclusive. The Balanced Scorecard has gained significant practitioner acceptance, with 29% of companies adopting it in 2018 (Rigby & Bilodeau, 2009). More recent data indicate a substantial increase in usage, as a 2GC (2021) survey reported that BSC adoption at the executive level rose from 44% in 2019 to 88% in 2020, with 71% of private-sector organizations across 21 countries incorporating the framework. Additionally, the term BSC was used in over 4,660 articles in 2018 and 475 articles in public and private health services institutions (Asiaei & Bontis, 2019). However, empirical evidence regarding how BSC leading factors relate to firm performance remains inconclusive. For instance, O’Sullivan and Abela (2007) provided strong evidence that improvements in non-financial indicators, such as employee training or innovation, eventually lead to financial performance gains, while Capelo and Dias (2009) found benefits beyond the use of financial measures alone. The interactions among BSC leading factors and their impact on lagging factors have not been verified in a comprehensive framework. Various theories and models have been adopted to support BSC effectiveness, such as organizational learning, human relations theory, and dynamic capability theory (Teece et al., 1997).

Several meta-analyses have attempted to synthesize the aggregated effect sizes of previous BSC empirical studies, yet they have largely failed to reconcile conflicting findings regarding the interdependencies among BSC dimensions. For instance, Mio et al. (2022) synthesized 65 articles published between 2000 and 2020 on sustainable BSC (SBSC) and identified key determinants of SBSC, but their focus was primarily on environmental and social performance, leaving the traditional four-dimensional framework under examined. Tawse and Tabesh (2023) synthesized previous BSC studies and recommended strategic refinements such as (1) integrating a strategy map with the BSC, (2) securing top management team (TMT) support for BSC adoption, and (3) enhancing board participation and horizontal communication. However, their study did not address whether these refinements resolve inconsistencies in how financial and non-financial perspectives interact within the BSC framework. Similarly, Kumar et al. (2024) conducted a bibliometric analysis of 1,294 BSC-related studies over 30 years, concluding that leading indicators positively influence firm performance. Yet, they did not fully account for contradictory findings on whether these leading indicators consistently drive lagging performance outcomes across different organizational contexts. Furthermore, Hinojosa and Mauricio (2021) found no relationship between firm ownership and the structure of BSC’s strategic dimensions, further illustrating the inconsistencies in how firms implement and benefit from BSC. While these studies provide valuable insights into various aspects of BSC, they collectively fail to resolve the discrepancies in empirical findings regarding the interdependencies among BSC dimensions. This gap underscores the need for further investigation to clarify how these dimensions interact and influence each other in practice.

By integrating theoretical perspectives with empirical evidence, this study contributes to a more comprehensive understanding of BSC functionality, particularly regarding the transformation of intangible assets, such as employee knowledge and innovation, into tangible financial metrics like profit growth and return on equity (ROE). This refined perspective offers practical implications for organizations seeking to optimize strategy execution and enhance long-term performance through a more integrated and dynamic application of the BSC framework.

Theoretical Foundation and Hypothesis Development

Theoretical Foundation of BSC

Kaplan (2009) argued that BSC was not original for adopting non-performance measures to evaluate a firm’s performance. For example, GE has used the following indicators to measure its divisional performance: (1) profitability, (2) market share, (3) productivity, (4) product leadership, (5) public responsibility, (6) personal development, (7) employee attitude, and (8) balance between short-range and long-term objectives. These indicators have covered the dimensions in the four pillars of BSC. Simon (1944) was one of the leading scholars to introduce the term of scorecard into the performance management discussions. Drucker (1954) argued that every employee should have performance objectives that strongly aligned to the company strategies, even though Drucker did not provide a clear description of how to internalize the concept of the top-level strategy to middle level managers and front line employees. In the mid-1960s, Anthony (1965) proposed a comprehensive framework of planning and control system, which encompassed both financial and non-financial indicators in the categories of strategic planning, managements control, and operational control. In the 1970s and 1980s, the Japanese management style has received a great attention on its long-term orientation from the aspects of continuous improvement, zero-defect, quality control, cycle time reduction, and quick customer responsiveness. Porter (1992) also echoed such an argument. Thus many authors (Howell et al., 1987; Kaplan, 1992) have argued to incorporate non-financial accounting and control system.

In 1992, Kaplan and Norton developed BSC framework with one lagging pillar (financial performance) and three leading pillars (customer satisfaction, internal process improvement, and learning and growth). This BSC framework is crucial for firms as it provides a comprehensive system for measuring performance beyond just financial metrics. It helps align firm activities with the strategic objectives across four different pillars. This BSC approach can enable better decision-making and long-term success by focusing on various aspects of organizational performance.

Hypothesis Development

Interrelationship Between Learning and Growth (LG) and Continuous Improvement/Innovation (CII)

The dynamic link between LG and CII is grounded in the theories of learning organizations (Garvin, 1993) and knowledge management (Nonaka & Takeuchi, 1995). Kaplan and Norton (1996) highlighted that as individuals and organizations acquire knowledge and develop skills, they foster a culture of innovation and adaptability. Learning drives problem-solving, creativity, and adaptability (Crossan & Apaydin, 2010), with continuous improvement emerging as a natural extension of this process. The synergistic interaction between LG and CII forms a cycle that propels firms to thrive in competitive and evolving landscapes.

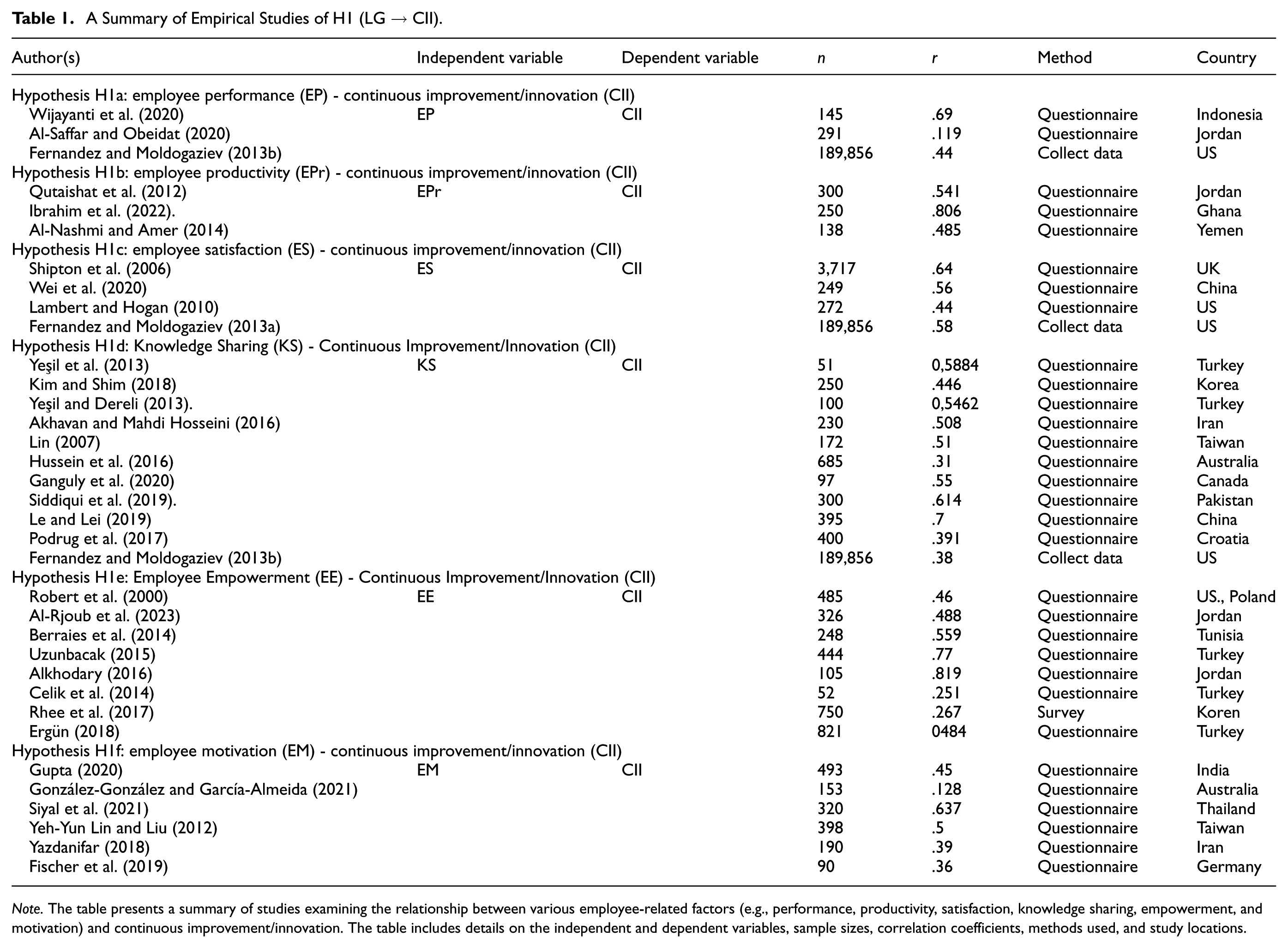

This study identifies six key indicators of LG: employee performance, productivity, satisfaction, knowledge sharing, empowerment, and motivation. Previous empirical research supports these as critical drivers of CII. Enhanced employee performance positively correlates with innovation capacity, as motivated and committed employees improve individual and organizational outcomes (Wijayanti et al., 2020). Similarly, increased productivity fosters creativity and readiness for innovation (Ibrahim et al., 2022; Qutaishat et al., 2012). Employee satisfaction also plays a crucial role, with studies emphasizing that satisfied employees, enjoying conducive work conditions, are more likely to contribute to CII (Shipton et al., 2006; Wei et al., 2020).

Knowledge sharing is another vital component. Studies have consistently demonstrated its positive impact on innovation capabilities, as collaborative environments encourage employees to share insights that enhance organizational adaptability (Lin, 2007; Siddiqui et al., 2019). Employee empowerment also significantly influences innovation, with empowered individuals contributing energy and initiative to the innovation process (Alkhodary, 2016; Berraies et al., 2014). Lastly, both intrinsic and extrinsic motivations are critical in driving employees to tackle challenges and actively participate in organizational innovation (Fischer et al., 2019; Yeh-Yun Lin & Liu, 2012). LG and CII form an interdependent relationship, where continuous learning cultivates innovation, and innovation sustains growth. By fostering a culture of learning, knowledge sharing, and empowerment, organizations can create a robust foundation for continuous improvement and sustained competitiveness.

Based on the above statements, the following hypotheses were developed:

Interrelationships Between LG and Customer Satisfaction (CS)

The relationship between LG within a firm and CS highlights the critical role of an adaptable and forward-thinking corporate culture (Kaplan & Norton, 1996). Continuous learning enhances employee skills, empowering the workforce to meet evolving customer expectations. Firms that foster learning cultures develop customer-centric approaches, enabling them to tailor their offerings and deliver high-quality, reliable services. This adaptability ensures better customer experiences and builds trust in the firm’s capabilities. Moreover, learning-oriented cultures increase employee engagement and enthusiasm, which positively influences CS through professional growth and commitment.

Based on a comprehensive review, five key LG factors—employee performance, satisfaction, knowledge sharing, empowerment, and motivation—emerge as significant contributors to enhancing CS. Competent employees with robust knowledge and expertise improve customer communication and problem-solving, directly impacting satisfaction (Abbasi & Alvi, 2013; Alkhamis, 2018; Söderlund (2018)). Higher levels of customer engagement also foster proactive service delivery and strengthened relationships.

Employee satisfaction plays a crucial role in CS, as satisfied employees are more likely to approach tasks enthusiastically and adopt customer-oriented behaviors. This alignment results in better service quality, effective communication of customer needs, and improved customer experiences (Chi & Gursoy, 2009; Evanschitzky et al., 2011). Satisfied employees often act as brand ambassadors, further enhancing organizational reputation and customer loyalty.

Knowledge sharing among employees is another key driver of CS. By exchanging insights and expertise, employees develop a deeper understanding of customer needs, enabling them to provide accurate and helpful information. This knowledge transfer fosters better responsiveness, problem resolution, and customer trust (Michna, 2018; Sari & Marwan, 2023).

Employee empowerment also significantly impacts CS. Empowered employees, given autonomy and authority Self-Determination Theory (SDT; Deci & Ryan, 1985; Ryan & Deci, 2000), feel a sense of ownership and responsibility. This empowerment enables quicker decision-making, personalized service, and proactive problem-solving, leading to improved customer interactions (Pandey et al., 2016; Zeglat et al., 2014).

Lastly, employee motivation is a critical determinant of CS. Motivated employees demonstrate higher levels of engagement and enthusiasm, going beyond basic expectations to deliver exceptional service (SDT; Deci & Ryan, 1985; Ryan & Deci, 2000). This commitment enhances customer interactions and fosters positive experiences, ultimately boosting satisfaction (Awan et al., 2014; Ahmad et al., 2012). Fostering LG through targeted employee development strategies strengthens CS, creating a synergistic relationship that benefits both the organization and its customers.

Based on the above statements, the following hypotheses were developed:

Interralationships Between CS and Financial Performance (FP)

CS is a crucial factor in a firm’s FP. It increases brand loyalty, leads to repeat purchases, and reduces the likelihood of switching to competitors. Firms with a strong reputation and CS can differentiate themselves from competitors, which can improve market performance. Additionally, firms with better customer relationship management can achieve higher levels of CS, which in turn promotes FP. Furthermore, satisfied customers are more likely to provide constructive feedback, which can guide improvements in products, services, and overall operation performance. In essence, CS creates a positive cycle that influences various aspects of a firm’s performance, including revenue generation, cost reduction, market positioning, and employee satisfaction, ultimately promoting FP.

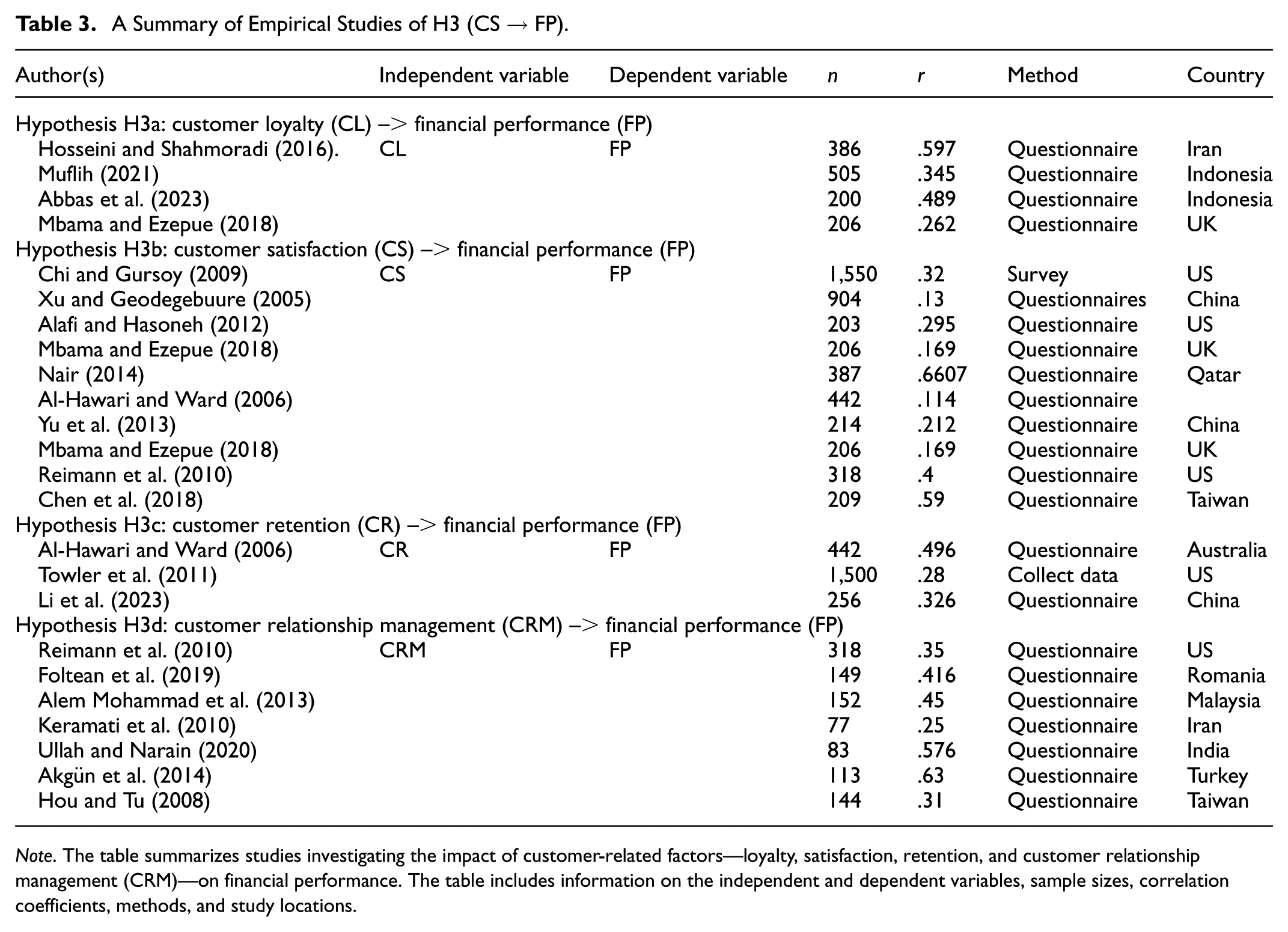

Based on a review of previous literature, this study identifies customer loyalty, CS, customer retention, and customer relationship management as four major factors of CS that enhance firm performance (Tables 1 and 2). Table 3 shows a summary of previous studies regarding the influence of CS on FP. For the influence of customer loyalty on FP, previous studies from Hosseini and Shahmoradi (2016), Mbama and Ezepue (2018), Muflih (2021) and Abbas et al. (2023) all supported this influential path. A long relationship between customer and a brand plays a vital role to business performance. The customer loyalty not only increases the FP of an organization, but also in a lower cost maintain a regular customer is lower than costs which a firm spent to get a new one.

A Summary of Empirical Studies of H1 (LG → CII).

Note. The table presents a summary of studies examining the relationship between various employee-related factors (e.g., performance, productivity, satisfaction, knowledge sharing, empowerment, and motivation) and continuous improvement/innovation. The table includes details on the independent and dependent variables, sample sizes, correlation coefficients, methods used, and study locations.

A Summary of Empirical Studies of H2 (LG → CS).

Note. The table presents a summary of studies examining the relationship between various employee-related factors (e.g., performance, satisfaction, knowledge sharing, empowerment, and motivation) and customer satisfaction. The table includes details on the independent and dependent variables, sample sizes, correlation coefficients, methods used, and study locations.

A Summary of Empirical Studies of H3 (CS → FP).

Note. The table summarizes studies investigating the impact of customer-related factors—loyalty, satisfaction, retention, and customer relationship management (CRM)—on financial performance. The table includes information on the independent and dependent variables, sample sizes, correlation coefficients, methods, and study locations.

For the influence of custmer satisfaction on FP, previous studies from Al-Hawari and Ward (2006), Xu and Geodegebuure (2005), Reimann et al. (2010), Chi and Gursoy (2009), Alafi and Hasoneh (2012), Yu et al. (2013), Nair (2014), Mbama and Ezepue (2018, 2018, 2018), and Chen et al. (2018) all supported this influential path. The benefits from this factor were investigated and reported that CS leading to increase the investment’s effectiveness through the measure of finance. For the influence of customer retention on FP, previous studies from Al-Hawari and Ward (2006), Towler et al. (2011), and Li et al. (2023 ) all supported this influential path. A positive correlation between customer retention and FP was found. Understanding the consequence of customer retention can help management concern more about the marketing strategy to attention the return rate of customer. For the influence of customer relationship management on FP, previous studies from Reimann et al. (2010), Foltean et al. (2019), Alem Mohammad et al. (2013), Keramati et al. (2010), Ullah and Narain (2020), Akgun et al. (2014), and Hou and Tu (2008) all supported this influential path. These investigations highlighted that there is a positive link between customer relationship management and a firm’s FP. The customer relationship management improved the differentiated level of finance, which was belonged to the company’s strategy.

Based on the above statements, the following hypotheses were developed:

Interrelationship Between CII and Fp

Continuous improvement and innovation are crucial for a firm’s FP within the strategic framework of BSC. These practices, such as total quality management (TQM; Deming, 1986), resource-based view (RBV; Barney, 1991), and customer relationship management (Berry, 1983), can significantly improve product quality, reduce operating costs, and promote company image. By refining working processes and workflows, these practices can enhance employee skills and capabilities, leading to increased efficiency, cost reduction, and streamlined processes. Innovation-driven enhancement in internal business processes can directly influence FP, allowing firms to introduce novel solutions to ensure competitiveness. Continuous improvement can also foster innovation to meet customer needs and expectations, resulting in higher customer loyalty and FP. Thus, integrating continuous improvement and innovation through employee capabilities can promote competitive advantage, cultivate customer loyalty, and enhance customer relationships, all of which serve as catalysts for FP.

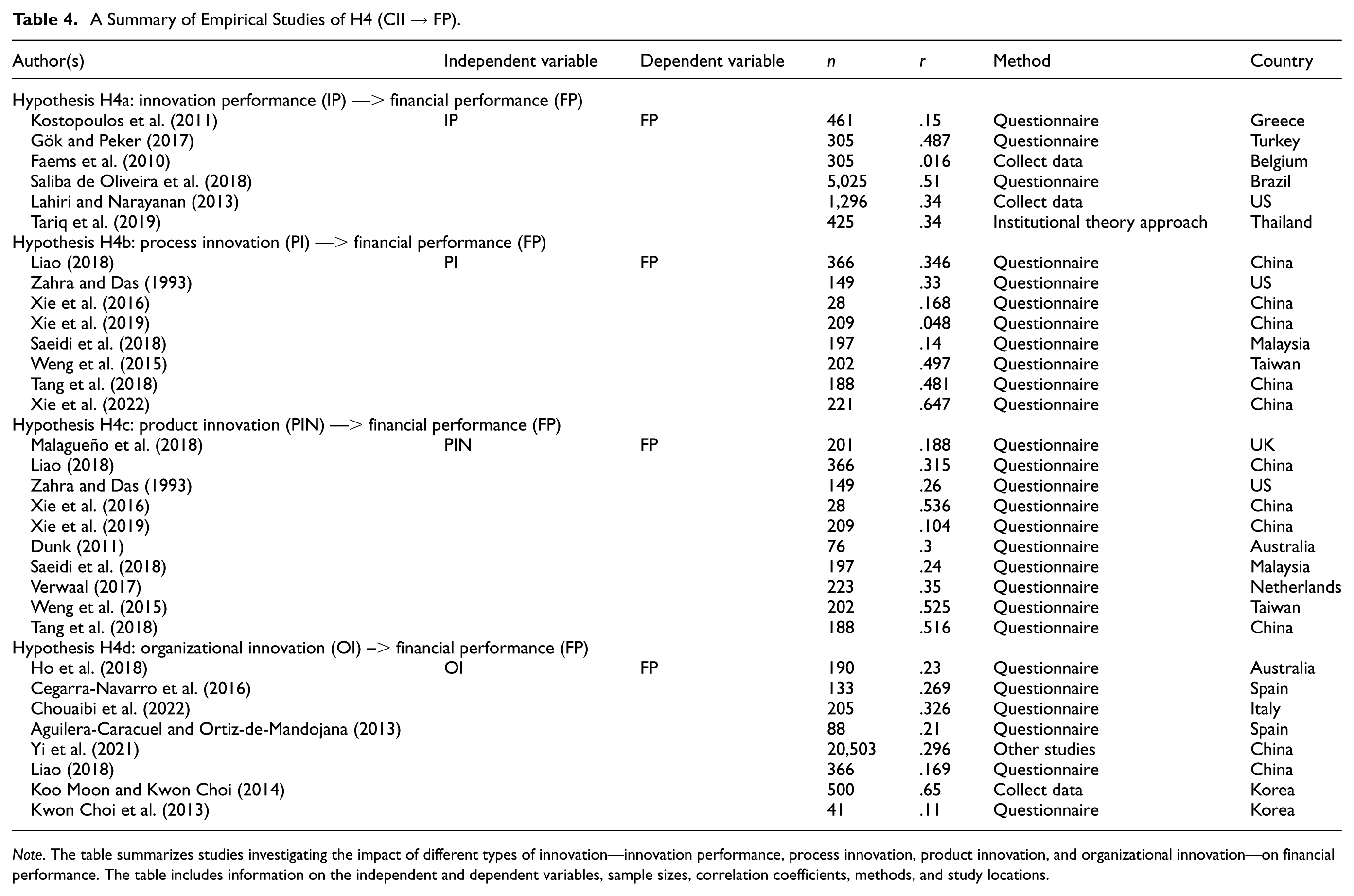

Based on a summary of previous studies, this study identifies process innovation, product innovation, organizational innovation, and innovation performance as four major factors of continuous improvement innovation. Table 4 shows a summary of previous studies regarding the influence of CII on a firm’s FP. For the influence of innovation performance, Kostopoulos et al. (2011), Gök and Peker (2017), Faems et al. (2010). Saliba de Oliveira et al. (2018), Lahiri and Narayanan (2013), and Tariq et al. (2019) all commented that innovation performance can promote FP. Thus innovations may result in recruiting more new customers, increasing sales, cost savings, and stakeholder confidence. Continuous innovation is essential for a firm’s long-term viability and competitive sustainability. For the influence of process innovation, Liao (2018), Zahra and Das (1993), Xie et al. (2016, 2019), Saeidi et al. (2018), Weng et al. (2015), Tang et al. (2018), and Xie et al. (2022) all argued for the influence of CII on FP. Process innovation, which involves streamlining workflows, reducing bottlenecks, improving production techniques, and optimizing procedures, is crucial for product quality improvement, operating efficiency, CS, and a firm’s FP. For the influence of product innovation, Malagueño et al. (2018), Liao (2018), Zahra and Das (1993), Xie et al. (2016, 2019), Dunk (2011), Saeidi et al. (2018), Verwaal (2017), Weng et al. (2015), and Tang et al. (2018) all endorsed its influence on FP. Product innovation is a key driver of promoting market differentiation, enhancing customer value and brand perception, which are all critical for a firm’s revenue growth, long-term sustainability, and profitability.

A Summary of Empirical Studies of H4 (CII → FP).

Note. The table summarizes studies investigating the impact of different types of innovation—innovation performance, process innovation, product innovation, and organizational innovation—on financial performance. The table includes information on the independent and dependent variables, sample sizes, correlation coefficients, methods, and study locations.

For the influence of organizational innovation, Ho et al. (2018), Cegarra-Navarro et al. (2016), Chouaibi et al. (2022), Aguilera-Caracuel and Ortiz-de-Mandojana (2013), Yi et al. (2021), Liao (2018), Koo Moon and Kwon Choi (2014), and Kwon Choi et al. (2013) all argued for its influence on FP. Organizational innovation involves implementing internal practices, processes, and structures to promote efficiency, flexibility, and adaptability. It can proactively respond to environmental changes, transform company culture, management style, and competitive leads, boosting employee productivity and FP.

Based on the above statements, the following hypotheses were developed:

Interrelationship Between LG and Fp

LG are crucial for an organization’s strategic framework and FP. The resource-based view (RBV; Barney, 1991) suggests that a firm’s unique capabilities and resources provide a competitive advantage. Learning becomes a dynamic capability that enables the acquisition, assimilation, and application of knowledge, enhancing its resource base and influencing financial outcomes. The learning organization theory, developed by Senge (1990), emphasizes the importance of fostering a culture of continuous learning within an organization. A learning organization is better equipped to navigate business complexities, innovate, and respond to market changes effectively, enhancing resilience and positively impacting FP. The human capital theory suggests that investments in employee learning and development can lead to a skilled and productive workforce, improving overall productivity and efficiency. The innovation diffusion theory explains how learning and growth facilitate the adoption of innovative practices, leading to product/service differentiation and increased market share, positively impacting FP.

Table 5 shows a summary of previous studies regarding the influence of learning and growth on a firm’s FP. For the influence of employee productivity on FP, Ismanto (2018), Tunio et al. (2021), and Hajdari et al. (2023) all supported for such an influential path. Employee productivity is a cornerstone of financial success. A productive workforce enhances operational efficiency, reduces costs, and increases output, leading to higher revenue generation, improved FP, and market competitiveness. For the influence of employee satisfaction on FP, Banker et al. (2000), Shafique and Ahmad (2022), Chi and Gursoy (2009), and Eren et al. (2013) all supported for such an influenced path. Employee satisfaction is a catalyst for financial success. Satisfied employees are more engaged and committed, leading to lower turnover rates and increased impact the bottom line and fostering a positive corporate image that can attract both customers and investors. For the influence of knowledge sharing on FP, Chen et al. (2018), Wang et al. (2014), Son et al. (2020), and Younis and Adel (2020) all supported for such an influential path. Knowledge sharing is a strategic asset that significantly impacts FP by enhancing innovation, problem-solving, and organizational intelligence. This collective knowledge helps a company adapt to market changes, make informed decisions, and ultimately improve financial outcomes. For the influence of employee empowerment on Kaya Özbağ and Gündüz Çekmecelioğlu (2022), Berraies et al. (2014), Yin et al. (2019), Tiong et al. (2017), and Afram et al. (2022) all supported for such an influential path. Employee empowerment is crucial for financial success, as it fosters ownership, initiative, and creativity, leading to improved operational efficiency and FP. This autonomy streamlines processes, accelerates decision-making, and fosters innovative problem-solving. For the influence of employee motivation on FP Dimba and K’Obonyo (2009), Ferguson and Reio (2010), Kundu and Gahlawat (2018), and Dar et al. (2014) all supported for such an influential path. Employee motivation is crucial for achieving financial goals, as motivated employees show higher commitment and effort, enhancing individual and team performance, productivity, and fostering a positive work environment, ultimately improving output quality and quantity.

A Summary of Empirical Studies of H5 (LG → FP).

Note. The table summarizes empirical studies examining the relationship between employee factors (e.g., productivity, satisfaction, knowledge sharing, empowerment, and motivation) and financial performance (FP). Each hypothesis is associated with studies detailing the sample size, correlation coefficient, research method, and country of the research.

As employee motivation fosters a culture of continuous improvement, it becomes a powerful force in driving a firm’s financial success.

Based on the above statements, the following hypotheses were developed:

Interrelationship Between CII and Cs

Continuous improvement and innovation significantly impact FP and CS. Product innovation addresses customer needs and preferences, leading to new products and services that exceed satisfaction. Firms with higher innovation performance stay ahead of market trends, offering innovative solutions that enhance CS and loyalty. Process innovation improves internal operations, fostering quicker transactions, reduced errors, and enhanced service quality. Innovative products provide unique features and enhance customer values, further elevating satisfaction. Organizational innovation, involving changes in structure, culture, and management practices, indirectly contributes to CS. Firms with a higher customer orientation culture provide excellent customer service, demonstrating responsiveness and adaptability. Overall, innovation plays a pivotal role in enhancing CS and trust.

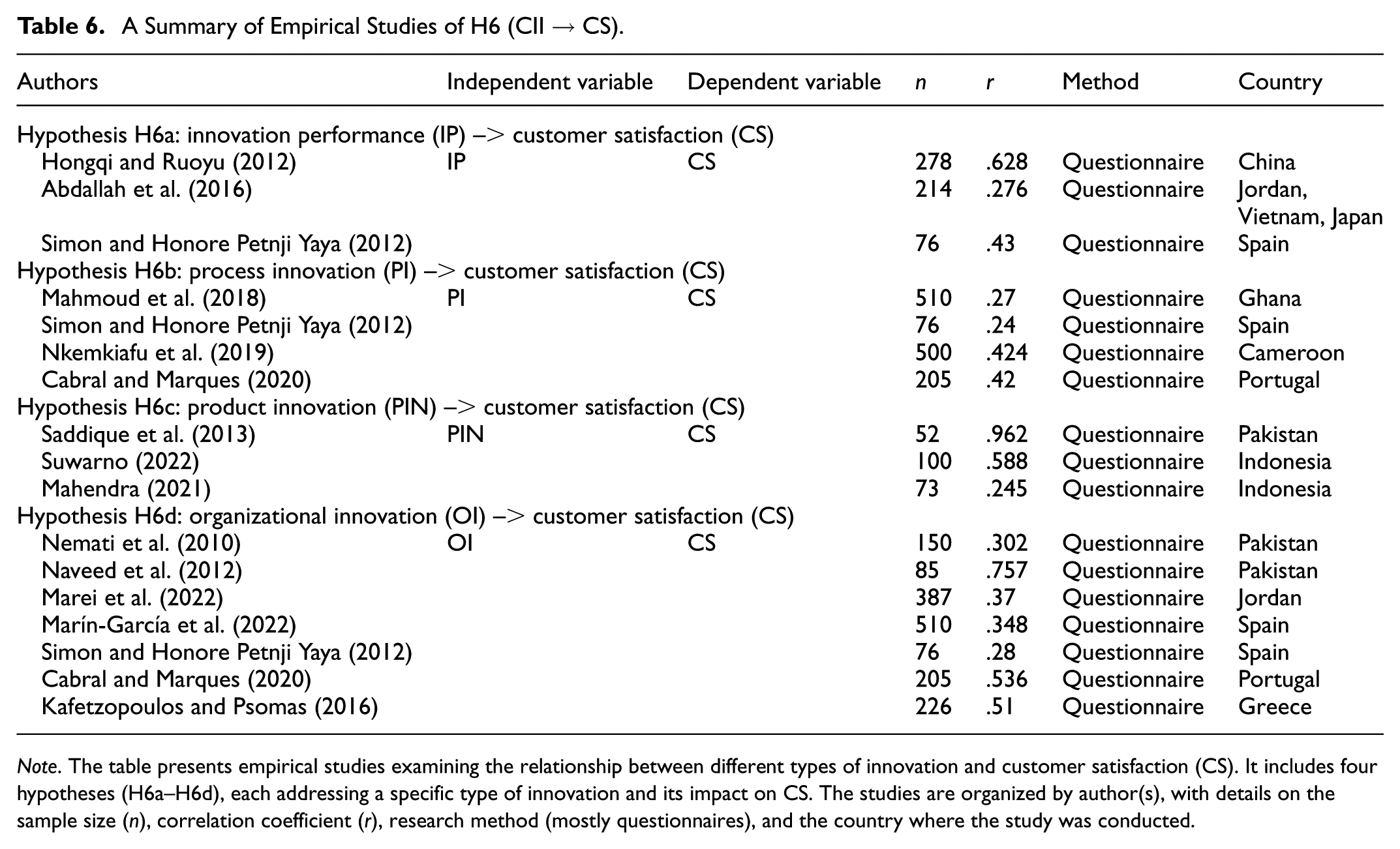

Table 6 shows a summary of previous studies that have shown the significant impact of continuous CII on CS. For the influence of innovation performance, Hongqi and Ruoyu (2012), Simon and Honore Petnji Yaya (2012), and Abdallah et al. (2016) all argued for its influence on CS. Innovation performance, which involves improving products, processes, and organizations, can lead to heightened customer experiences and trust. Novel solutions, streamlined processes, and responsiveness can earn customer trust. Firms need to create a path through innovation where customer contentment becomes intrinsic to their identity and success. For the influence of process innovation, Mahmoud et al. (2018), Simon and Honore Petnji Yaya (2012), Nkemkiafu et al. (2019), and Cabral and Marques (2020) all argued for its influence on CS. Process innovation revolutionizes how tasks are accomplished, enhancing efficiency and leading to quicker, error-free services. This leads to a satisfied customer base. For the influence of product innovation, Saddique et al. (2013), Suwarno (2022), and Mahendra (2021) all recognized its influence on CS. Product innovation, on the other hand, meets evolving needs with novel features, improved functionality, and cutting-edge design. A continual cycle of product innovation establishes a brand as forward-thinking, fostering loyalty and staying ahead of competitors. For the influence of organizational innovation, Nemati et al. (2010), Naveed et al. (2012), Marei et al. (2022), Marín-García et al. (2022), Simon and Honore Petnji Yaya (2012), Cabral and Marques (2020), and Kafetzopoulos and Psomas (2016) all argued for its influence on CS. Organizational innovation, encompassing changes in structure, culture, and management approaches, is pivotal in shaping CS. A responsive and adaptive organizational structure can swiftly address customer needs, providing personalized solutions. A culture that values innovation and customer-centricity can foster trust, contributing significantly to CS. The organizational framework becomes a catalyst for enhanced service quality and customer loyalty.

A Summary of Empirical Studies of H6 (CII → CS).

Note. The table presents empirical studies examining the relationship between different types of innovation and customer satisfaction (CS). It includes four hypotheses (H6a–H6d), each addressing a specific type of innovation and its impact on CS. The studies are organized by author(s), with details on the sample size (n), correlation coefficient (r), research method (mostly questionnaires), and the country where the study was conducted.

Based on the above statements, the following hypotheses were developed:

Research Design and Methodology

Research Framework

This study aims to synthesize empirical findings from prior research on the Balanced Scorecard (BSC) published between 1993 and 2023. Specifically, it examines the interrelationships among leading indicators—LG, CII, and CS—and the lagging indicator—FP. Guided by the literature review and hypothesis development, the research framework is illustrated in Figure 1. In total, four primary hypotheses and 28 sub-hypotheses have been developed to comprehensively capture these relationships.

The research framework.

Meta-Analytic Approach

A meta-analytic approach is employed to evaluate the proposed research model. Meta-analysis is a rigorous statistical method that integrates and synthesizes quantitative findings from multiple independent studies, enabling the estimation of overall effect sizes and the identification of underlying patterns (Lipsey & Wilson, 2001). This approach offers several advantages, notably increasing statistical power, enhancing generalizability, resolving inconsistencies, and mitigating the risk of publication bias.

By combining effect sizes from diverse studies, meta-analysis improves accuracy and supports the detection of variations attributable to study context, sample characteristics, or methodological differences. Furthermore, it enables the exploration of potential moderating variables, offering a nuanced understanding of performance relationships within the BSC framework.

Literature Search Strategy and Inclusion Criteria

A systematic search strategy was designed to identify relevant empirical studies. Database searches were conducted across ProQuest, JSTOR, Sage, Emerald, ScienceDirect, Frontiers, ResearchGate, and Springer. Keywords such as “Balanced Scorecard,”“Learning and Growth,”“Continuous Improvement,”“Innovation,”“Customer Satisfaction,” and “Financial Performance” were used in various combinations to maximize coverage.

To reduce sampling bias, this search process adhered to the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) guidelines (Moher et al., 2009), ensuring transparency and explicability.

Inclusion criteria:

Empirical studies published between 1993 and 2023.

Studies employing quantitative methods and reporting sample sizes.

Studies providing statistical effect sizes, such as correlation coefficients (r) or standardized regression coefficients (β), relevant to the hypothesized relationships within the BSC framework.

Exclusion criteria:

Qualitative studies and theoretical frameworks without empirical testing.

Studies lacking statistical information necessary for meta-analytic calculations.

Duplicated studies across databases.

The initial search yielded 1,523 articles. After screening titles, abstracts, full texts, and applying the inclusion criteria, 134 empirical studies were retained for analysis. These studies collectively represented a cumulative sample of 721,826 observations. The studies included are presented in Table 7.

The Studies Included in the Meta-Analysis.

Note. The table lists studies alphabetically by author(s), detailing independent and dependent variables, hypothesis codes, sample sizes, and the focus of each study. It examines relationships between employee factors (e.g., knowledge sharing, innovation performance) and organizational outcomes like customer satisfaction and financial performance.

Journals are in order: (1) Administration & Society, (2) African Journal of Business Management, (3) Asian Journal of Business Research, (4) Asian Social Science, (5) Jurnal Ilmiah Akuntansi, (6) Australian Journal of Business and Management Research, (7) British Journal of Economics, Management & Trade, (8) Budapest International Research & Critics Institute-Journal, (9) Business Management, (10) Business Management and Strategy, (11) Business Strategy and the Environment, (12) Business: Theory and Practice, (13) Criminal Justice Policy Review, (14) Economic Analysis and Policy, (15) Economic research, (16) Emerging Science Journal, (17) Engineering Economics, (18) Engineering, Technology & Applied Science Research, (19) Environmental Science and Pollution Research, (20) EuroMed Journal, (21) European Journal of Innovation Management, (22) European Journal of Social Sciences, (23) European Journal of Work and Organizational Psychology, (24) European Management Journal, (25) European Scientific Journal, (26) Frontiers, (27) Global Journal of HRM, (28) HRM Journal, (29) Transactions on Engineering Management, (30) In The Annual International Conference of The British Academy of Management (BAM), (31) Industrial Management & Data Systems, (32) Industrial Marketing Management, (33) Innovative Marketing, (34) Intangible Capital, (35) International Conference on Applied Business and Management, (36) International journal of bank marketing, (37) International Journal of Business and Management, (38) International Journal of Business Innovation and Research, (39) International Journal of Business Performance Management, (40) International Journal of Contemporary Hospitality Management, (41) International Journal of Customer Relationship Marketing and Management, (42) International Journal of Economics, Business and Management Research, (43) International Journal of Electronic Customer Relationship Management, (44) International Journal of Hospitality & Tourism Administration, (45) International Journal of Hospitality Management, (46) International Journal of Humanities and Social Science, (47) International Journal of Innovation Management, (48) International Journal of Innovation Studies, (49) International Journal of Manpower, (50) International Journal of Production Economics, (51) International Journal of Science, Technology & Management, (52) International Journal of Service Science, Management, Engineering, and Technology, (53) International Journal of Social Sciences and Humanities Research, (54) International Review of Management and Marketing, (55) Jurnal Ilmiah Ilmu Pendidikan, (56) Journal of Applied Psychology, (57) Journal of Business research, (58) Journal of Business Studies Quarterly, (59) Journal of Cleaner. Production, (60) Journal of Entrepreneurship and Innovation Management, (61) Journal of Financial Services Marketing, (62) Journal of Forensic Psychology, (63) Journal of Hospitality, and Tourism Technology, (64) Journal of Innovation & Knowledge, (65) Journal of Innovation Management, (66) Journal of International Social Research, (67) Journal of Knowledge Management, (68) Journal of Management & Organization, (69) Journal of Management Development, (70) Journal of Managerial Studies and Research, (71) Journal of Marketing Development & Competitiveness, (72) Journal of Product Innovation Management, (73) Journal of Public Administration Research and Theory, (74) Journal of Public Affairs, (75) Journal of Service Research, (76) Journal of the Academy of marketing science, (77) Journal of Workplace Learning, (78) Journal of world business, (79) Knowledge and Process Management, (80) Knowledge Management Research & Practice, (81) Management and Administrative Sciences Review, (82) Management Decision, (83) Management Science Letters, (84) Management Science Letters, (85) Manufacturing Industry, (86) Marketing Intelligence & Planning, (87) Munich Personal RePEc Archive, (88) Organization & Environment, (89) Pakistan Journal of Commerce and Social Sciences (PJCSS), (90) Personnel Review, (91) Procedia-Social and Behavioral Sciences, (92) Production and Operations Management, (93) Retailing and Consumer Services, (94) Review of Managerial Science, (95) Sage Open, (96) Science International, (97) Small Business Economics, (98) Social Behavior and Personality, (99) Strategic Management Journal, (100) Sustainability, (101) Technology Analysis & Strategic Management, (102) The British Accounting Review, (103) The Journal of Hospitality Financial Management, (104) The University of Texas at Dallas, (105) Uncertain Supply Chain Management, (106) Verslas.

Variable Coding and Data Extraction

Data extraction and coding are carried out using the Comprehensive Meta-Analysis (CMA) software package. Following the procedures recommended by Miao et al. (2018), each study is carefully reviewed to extract consistent variables and effect sizes. To ensure accuracy and minimize researcher bias, a multi-stage coding process is implemented. Initially, the corresponding author and subject-matter junior professors independently coded the variables, effect sizes, and study characteristics. Subsequently, the subject-matter professors cross-verified the coding results for accuracy and consistency with the definitions used in the original studies. Classification of LG, CII, and CS as leading indicators and FP as a lagging indicator followed the conceptual framework established by Kaplan and Norton (1996). Any discrepancies are resolved through collaborative discussion to ensure high inter-coder reliability.

In the event of discrepancies between the corresponding author and subject-relevant professors regarding the inclusion or exclusion of literature, a consensus-based approach is employed. Disagreements are resolved through discussions between the authors and the subject-relevant professors, and, if necessary, a third independent reviewer is consulted to ensure that all studies adhered to the methodological standards and criteria set for the meta-analysis.

Handling of Publication Bias

To address potential publication bias, the literature search included gray literature and unpublished works to reduce the likelihood of over-representing studies with significant results. In addition, statistical tests for publication bias were conducted using funnel plot analysis and Egger’s regression test (Borenstein et al., 2009). These analyses reveal no significant publication bias, supporting the robustness of the meta-analytic findings.

Analytic Techniques

The correlation coefficients (r) are used as the primary effect size in this study. Those studies presented in standardized coefficients (β) are transformed to r for further analysis. Following Peterson and Brown (2005), the following formula is adopted for this transformation.

where:

β = the beta coefficient from multiple regression analyses, λ equals 1 when β is non-negative and 0 when β is negative

Lipsey and Wilson (2001) developed the following Q-statistic formula to verify the homogeneity of the effect size distribution. Q-statistic is also named as the Cochran’s heterogeneity statistics.

where:

- ESi = individual effect size

- (ESj)− = weight mean effect size of each group

- Wi = weight for each effect size

The analysis of Q-statistic is justified that, under 95% of confidence interval, if Q-statistic (Lipsey & Wilson, 2001) is higher than χ2 (χ2 with n-1 degree of freedom, n = number of studies), then the null-hypothesis of homogeneity should be rejected. In this case, the heterogeneity between variance would exist. In other words, the variations in effect size may be due to true effect rather than sampling errors. I2 statistic was developed by J. P. T. Higgins and Thompson (2002) to improve possible errors from sampling error (number of studies included), with the following formula:

where:

- I2 is the I-squared statistic

- Q is Cochran’s heterogeneity statistic

- df is the degrees of freedom

According to Lipsey and Wilson (2001), I2 values are between 0 and 1. An I2 value of 0 indicated no observed heterogeneity among studies, 25% indicates low heterogeneity, 50% indicates moderate heterogeneity, and 75% indicates high heterogeneity among the studies in the meta-analysis which represents a substantial difference in the true effects being studied.

Results

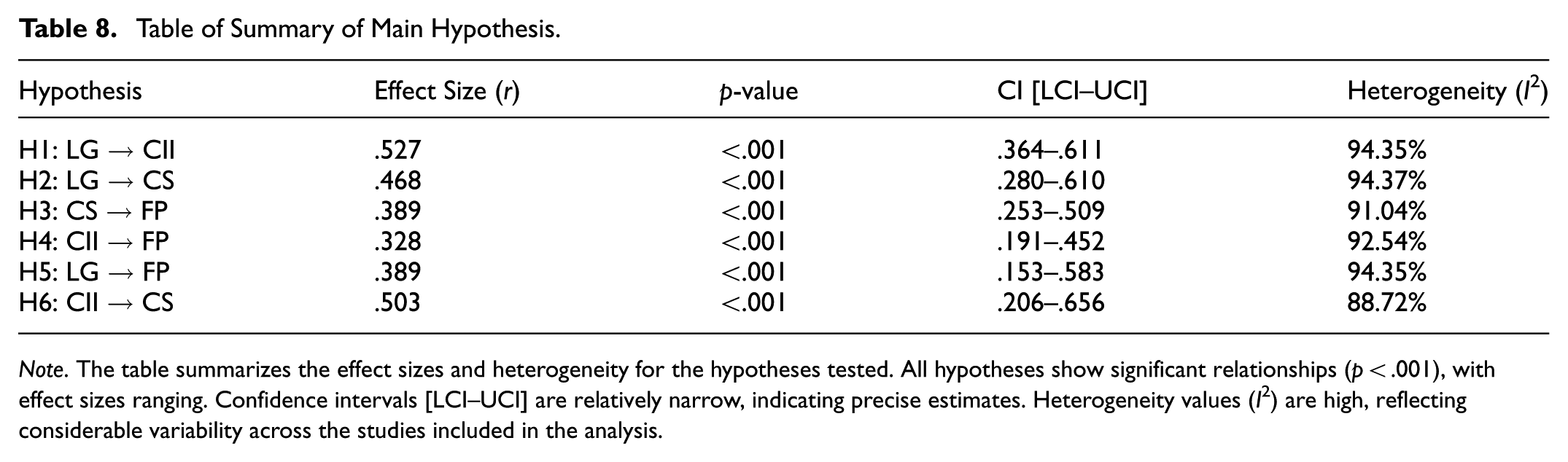

To enhance clarity, Table 8 provides a high-level summary of the main hypotheses (H1–H6), presenting the pooled effect size (r), 95% confidence interval, overall p-value, and heterogeneity (I2). The results presented in Table 9 offers a detailed examination of the main effects across 28 sub-hypotheses.

Table of Summary of Main Hypothesis.

Note. The table summarizes the effect sizes and heterogeneity for the hypotheses tested. All hypotheses show significant relationships (p < .001), with effect sizes ranging. Confidence intervals [LCI–UCI] are relatively narrow, indicating precise estimates. Heterogeneity values (I2) are high, reflecting considerable variability across the studies included in the analysis.

Summary of Hypotheses.

Note. The table presents the meta-analysis results, showing statistically significant effect sizes (p he table presents the meta-analysis results, show [LCI and UCI] are narrow, supporting robust findings. Heterogeneity, indicated by high Q-statistics and I2 values, reflects considerable variability across studies. Egger’s regression tests reveal no significant publication bias for most hypotheses (p > .05), ensuring the reliability of the results.

Employee performance exhibits a strong and significant relationship with both CII (r = .441, p < .001) and CS (r = .523, p < .001), with high heterogeneity across studies (I2 > 96%). This finding aligns with the resource-based view (RBV; Barney, 1991), which emphasizes the role of valuable, rare, and inimitable resources—such as high-performing employees—in fostering innovation and creating superior customer experiences. In practical terms, organizations that prioritize employee performance management—through training, clear KPIs, and recognition systems—can expect downstream improvements in process innovation and customer engagement.

Similarly, employee productivity shows strong associations with CII (r = .650, p < .001) and FP (r = .382, p < .001). Productivity improvements enhance internal efficiency and reduce operational costs, which aligns with TQM (Deming, 1986) principles emphasizing process optimization. Managers should view productivity not only as an operational metric but also as a precursor to financial gains and sustained process improvements.

Employee Satisfaction significantly affects CII (r = .573, p < .001), CS (r = .316, p < .001), and FP (r = .209, p < .001), confirming its central role in both internal and external outcomes. This supports the Human Relations Theory, which posits that satisfied employees are more engaged, collaborative, and committed. Practically, fostering a positive work environment—via fair compensation, work-life balance policies, and open communication—can directly enhance innovation capacity, customer service quality, and financial stability.

Knowledge sharing emerges as a critical mechanism, positively impacting CII (r = .506, p < .001), CS (r = .516, p < .001), and FP (r = .454, p < .001). This finding is consistent with Knowledge-Based View (KBV) and Dynamic Capabilities Theory (Teece et al., 1997), which stress the importance of knowledge dissemination in building innovation capability and organizational adaptability. Encouraging cross-departmental collaboration, knowledge platforms, and team learning routines can strengthen these effects in practice.

The analysis further shows that Employee Empowerment significantly influences CII (r = .547, p < .001), CS (r = .375, p < .001), and FP (r = .391, p < .001). Empowerment fosters autonomy, ownership, and innovation, which is strongly supported by Organizational Learning Theory (Garvin, 1993). Practically, decentralizing decision-making and providing employees with authority and resources to experiment can lead to meaningful process improvements and better customer outcomes.

Likewise, Employee Motivation demonstrates strong positive relationships with CII (r = .430, p < .001), CS (r = .609, p < .001), and FP (r = .512, p < .001). Drawing from SDT (Deci & Ryan, 1985; Ryan & Deci, 2000), motivated employees exhibit greater intrinsic engagement, driving both creative efforts and customer-focused behaviors. Managers should implement reward systems and career development programs that nurture intrinsic and extrinsic motivation to amplify organizational performance.

In the customer dimension, Customer Loyalty, Customer Satisfaction, Customer Retention, and Customer Relationship Management (CRM; Alem Mohammad et al., 2013) each display significant positive effects on FP. Specifically, customer loyalty (r = .434, p < .001), CS (r = .321, p < .001), customer retention (r .370, p < .001), and CRM (r = .432, p < .001) confirm the foundational assumption in Relationship Marketing Theory that long-term, trust-based customer relationships drive profitability. In practice, businesses should consistently invest in personalized customer experiences, loyalty programs, and CRM systems to reinforce customer ties and financial outcomes.

Turning to internal processes, innovation performance, process innovation, product innovation, and organizational innovation all show significant impacts on FP and CS. Innovation performance contributes positively to FP (r = .319, p < .001) and CS (r = .459, p < .001), supporting the Dynamic Capabilities Theory (Teece et al., 1997) view that firms’ ability to innovate consistently enhances both market positioning and operational success. Process Innovation improves FP (r = .356, p < .001) and CS (r = .352, p < .001), underscoring the relevance of Lean Management and continuous improvement frameworks.

Product Innovation displays a strong effect on FP (r = .329, p < .001) and especially on CS (r = .745, p < .001), highlighting its role in differentiating offerings and satisfying evolving customer needs. Organizational Innovation also significantly supports FP (r = .306, p < .001) and CS (r = .456, p < .001), echoing the relevance of adaptive structures and cultures in fostering long-term competitive advantage.

Collectively, these findings reaffirm the BSC’s holistic approach, where human capital development, process optimization, customer relationship management, and innovation efforts are intricately linked to financial success. The high heterogeneity across effect sizes (I2 > 90%) suggests that industry, organizational culture, and market dynamics moderate these relationships—an important consideration for practitioners tailoring BSC implementation to their specific contexts.

To assess the robustness of the meta-analytic findings against potential publication bias, Rosenthal’s (1979) Fail-Safe N test and Egger’s regression test (Egger et al., 1997) were conducted. The results of the Fail-Safe N analysis revealed that several hypotheses, notably H1c (176 studies), H1a (125 studies), H1d (78 studies), and H1e (31 studies), exhibited strong resistance to publication bias. These high values suggest that a substantial number of unpublished null-effect studies would be required to nullify the observed effects (p > .05), thus affirming the stability and reliability of these findings (Rosenthal, 1979).

Furthermore, Egger’s regression intercept tests yielded non-significant p-values (p > .05) across all pathways, indicating no evidence of significant funnel plot asymmetry or small-study effects (Egger et al., 1997). This strengthens confidence in the meta-analytic results and suggests the absence of systematic publication bias.

Nevertheless, several hypotheses—such as those with Fail-Safe N values ranging between approximately 11 to 20 studies—warrant cautious interpretation, as these findings are moderately vulnerable to potential publication bias. Despite this, the combined evidence from Rosenthal’s Fail-Safe N and Egger’s regression tests supports the overall robustness and validity of the meta-analytic conclusions.

Conclusion

This meta-analysis systematically synthesizes empirical evidence from 134 studies (N = 721,826) to clarify the interrelationships among the four Balanced Scorecard (BSC) dimensions: LG, internal processes (CII), CS, and FP. The findings highlight the significant role of contextual factors in shaping these interdependencies, as evidenced by substantial heterogeneity (I2 > 90%). This variation underscores the importance of industry characteristics, organizational culture, and external market conditions in moderating the effects of BSC dimensions on firm performance. Therefore, practitioners should prioritize investments in employee development and strategically integrate innovation metrics into their BSC framework to drive customer satisfaction and financial performance.

The analysis reveals robust associations between key variables. Employee performance exhibits a strong positive relationship with customer satisfaction (r = .523, p < .001), indicating that firms prioritizing employee engagement, skill development, and motivation are likely to see corresponding improvements in customer perceptions and loyalty. Given this, managers should invest in targeted training programs and empowerment initiatives to strengthen this link. Similarly, innovation performance demonstrates a moderate yet significant connection to financial outcomes (r = .319, p < .01), confirming that organizations fostering continuous improvement and creativity can achieve long-term financial gains. This reinforces the need for organizations to integrate innovation performance metrics into their strategic decision-making processes, ensuring that both process and product innovation efforts align with broader financial objectives.

Further robustness analyses confirm the absence of publication bias, supporting the generalizability of these findings. By resolving inconsistencies in the literature and identifying key causal pathways between non-financial and financial metrics, this study provides a clearer theoretical and empirical foundation for BSC implementation. The findings emphasize that learning and growth serve as the cornerstone of the BSC framework, driving improvements in internal processes, customer satisfaction, and financial outcomes. Organizations that recognize this foundational role and strategically invest in human capital, process efficiencies, and customer-centric innovations are more likely to gain a sustainable competitive advantage.

Academic Implications

This study makes several key contributions to strategic management theory. Firstly, it consolidates fragmented empirical evidence to offer a more integrated understanding of BSC dynamics. The findings align with and extend existing theoretical frameworks, including the resource-based view, dynamic capabilities, and organizational learning theories. The identification of learning and growth as a foundational pillar underscores the role of human capital in driving operational effectiveness and customer satisfaction, reinforcing human capital theory. The observed mediation effects of internal process improvements and innovation on financial performance provide empirical support for the dynamic capabilities framework, highlighting the importance of adaptability and continuous improvement in achieving long-term financial success.

Additionally, the results demonstrate that customer satisfaction is a critical mediator linking non-financial initiatives to financial performance, further validating service-dominant logic. By empirically quantifying these relationships, the study strengthens the theoretical underpinnings of performance measurement and strategic alignment within organizations. Future research should extend these insights by exploring how industry lifecycle stages, firm size, and national cultural contexts influence the strength of these relationships. Longitudinal studies that track the evolution of BSC interdependencies over time would also enhance theoretical development by capturing the dynamic nature of these constructs.

Managerial Implications

The findings offer actionable recommendations for practitioners seeking to optimize BSC implementation. Organizations should strategically align employee development programs with corporate objectives, ensuring that training initiatives directly contribute to innovation, process efficiency, and customer satisfaction. For example, firms emphasizing innovation should prioritize creativity-focused training and cross-functional collaboration to cultivate a workforce capable of driving product and process improvements. Employee empowerment initiatives, such as decentralized decision-making and knowledge-sharing platforms, can further enhance organizational agility, and responsiveness to market demands.

To improve internal processes and innovation performance, companies should adopt lean management principles and integrate real-time customer feedback into continuous improvement cycles. Innovation metrics should be embedded in performance evaluations to sustain a culture of experimentation and refinement. Firms must also recognize that a one-size-fits-all approach to BSC implementation is ineffective. Instead, managers should tailor performance indicators to industry-specific challenges, ensuring that BSC metrics reflect the unique operational constraints and strategic priorities of their organization. Engaging key stakeholders during the BSC design phase can enhance commitment and facilitate smoother execution.

Finally, organizations should leverage dynamic monitoring systems to track BSC dimensions in real time. Implementing data-driven dashboards that provide insights into employee satisfaction, innovation progress, customer feedback, and financial performance can enable proactive decision-making. For example, a decline in employee satisfaction scores may serve as an early warning signal for future customer retention issues, prompting preemptive interventions to mitigate negative outcomes. By adopting an integrated approach to performance measurement, firms can maximize the strategic value of the BSC framework.

Limitations and Future Research Directions

While this study provides valuable insights into BSC interdependencies, several limitations warrant consideration. The reliance on a meta-analytic approach, while effective for synthesizing empirical findings, is inherently subject to heterogeneity, and potential overgeneralization. Despite controlling for variance using I2 and Q-statistics, residual variability suggests that unexamined moderators, such as firm size, regulatory environments, and national culture, may influence BSC dynamics. Although we did not conduct formal moderator analyses in this study, future research should explore these contextual moderators through meta-regression or subgroup analyses to better account for the observed heterogeneity and refine our understanding of the BSC framework’s applicability across different settings.

Additionally, the reliance on secondary data limits causal inference. While the study identifies significant associations between BSC dimensions, the directionality and mechanisms of these relationships remain partially speculative. Mixed-methods approaches that combine meta-analytic techniques with qualitative case studies or experimental research could provide deeper insights into the causal mechanisms underlying BSC effectiveness.

Another limitation is the relatively narrow focus on commonly studied BSC indicators. Certain sub-dimensions, such as the role of organizational innovation in fostering learning cultures or the impact of digital transformation on BSC performance metrics, remain underexplored. Expanding the range of indicators included in future meta-analyses and incorporating emerging performance measures—such as sustainability metrics or digital capabilities—would enhance the comprehensiveness of BSC research.

Finally, the sample of studies included in this meta-analysis is predominantly drawn from corporate settings, with limited representation from non-profit organizations, government agencies, and emerging markets. Future research should explore how BSC dynamics operate in these underrepresented sectors, as well as how digital transformation and artificial intelligence-driven analytics influence the implementation and effectiveness of the BSC framework in contemporary organizations. Conducting longitudinal studies that capture the evolution of BSC relationships over time would further refine its applicability in dynamic business environments.

Footnotes

Ethical Considerations

This study is a meta-analysis that synthesizes findings from previously published empirical studies related to the Balanced Scorecard. It did not involve the collection of primary data from human participants. Therefore, direct ethics review and approval for this study were not required. However, the original studies included in this meta-analysis would have adhered to the ethical guidelines relevant to their respective contexts and data collection methods.

Consent to Participate

This research is a meta-analysis and did not involve direct interaction or data collection from human participants. Informed consent was obtained in the primary studies included in this synthesis, as applicable to their research designs and data collection methods.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting the findings of this manuscript are publicly accessible through established academic databases, including Science Direct, Elsevier, Taylor & Francis, JSTOR, Emerald, Springer, Sage, and Google Scholar. Scholars and researchers are encouraged to access these databases for further exploration or verification.