Abstract

Value Added Tax is widely used and prominent since it generates significant economic revenue and is very simple to administer. Consumers who purchase various goods and services are subject to a standard consumption tax called VAT, which is gradually collected. Economic growth is necessary for a country to be sustainable in the long run. VAT has been recognized as an essential global tax instrument that fosters economic growth. The study examines the customers’ perception of financial, economic, and social perspectives of VAT in sustainable economic development. This study employed a mixed-methods design, incorporating both quantitative and qualitative methodologies. The data was obtained from 315 respondents in Saudi Arabia via a structured, self-administered questionnaire. Descriptive analysis, correlation analysis, reliability analysis, regression analysis, and ANOVA were employed to analyze the data in SPSS. The study results showed that all factors substantially impacted customers’ perception, and customers perceive that the revenue generated from VAT significantly contributes to a country’s financial, social and economic development. The advice presented would be helpful to scholars and policymakers who are examining the implications of VAT and how to improve compliance.

Keywords

Introduction

A broad approach is necessary for assessing VAT in the context of sustainable economic development. How customers perceive VAT significantly impacts how they feel about it and how they behave, which can affect how effective it is at fostering sustainable economic growth. Value Added Taxes are the name for consumption taxes (VAT). Lower-income families are more likely to spend a sizable portion of their income. Regressive VATs are those that are calculated against current income and are applied without any other policy changes. In terms of lifetime income, a VAT is less regressive than one based on current income. Individuals may be dissuaded from working, saving, investing, or coming up with new ideas when marginal tax rates are high, but tax preferences can influence the distribution of economic resources. Tax cuts might produce more large deficits, limiting economic growth. Tax reform will substantially affect development if it has significant positive incentive (substitution) impacts that increase saving, investing, and working; minor or adverse income effects, including clever targeting of tax cuts; and minor or adverse income effects.

On January 31, 2017, Saudi Arabia accepted the Gulf Cooperation Council’s VAT and excise tax accord. The Kingdom of Saudi Arabia adopted a 5% value-added tax on January 1, 2018. In Saudi Arabia, the General Authority of Zakat & Tax administers and enforces this tax. The social goal is establishing tax justice by exempting some income earners from paying for necessities (Alavuotunki et al., 2019). Administrative goals include simplifying tax law so taxpayers can adopt it quickly and contribute to better tax performance. These goals have arisen and are compatible with most countries’ tax reform efforts (Al-Abdali Iman et al., 2019).

The Kingdom of Saudi Arabia imposed a value-added tax (VAT) of 5% standard on January 1, 2018. VAT is a form of indirect tax levied on every product and service. VAT levies most services and products, excluding zero-rated supplies and specific exemptions. Organizations that reach certain revenue thresholds must enroll for value-added tax (VAT) and adhere to the associated reporting and payment responsibilities. The General Authority of Zakat and Tax (GAZT) is Saudi Arabia’s tax authority responsible for administering taxes such as the value-added tax (VAT), the corporate income tax, and Zakat.

Before the recent global COVID-19 outbreak, the VAT imposed by Saudi Arabia on all goods and services was 5%. However, the country has since increased this sum and enacted a 15% VAT beginning in July 2020. As of July 1, 2020, the government raised the regular VAT rate to 15%. “Effective from July 1st, 2020, Saudi Arabia tripled its value-added tax (VAT) to 15%, as part of financial reforms intended to support the fiscal imbalance between public revenues and expenditures caused by the negative impact of the coronavirus crisis (www.arabnews.com).”

To calculate VAT, we need to multiply the gross value of the supply by the VAT rate, that is, 15%. The gross value and 15% VAT will be added to find the total amount payable. For example, if the gross value is SAR 500, the final value after VAT will be SAR 575 (SAR 500 + 75 VAT). Table 1 presents a few countries’ standard VAT rates and reduced rates.

World VAT Rates 2024.

The value-added tax (VAT) has several potential advantages, including preventing a cascade of indirect taxes, potential improvement in tax compliance compared to other types of taxation, and simple adaptability to international commerce. The value-added tax, or VAT, has been referred to as a “money machine” in an empirical macro study conducted by Keen and Lockwood (2010). The VAT has helped governments generate more income than they otherwise would have.

Rationale of the Study

The value-added tax (VAT) is a form of consumption tax that directly impacts individuals who engage in consuming activities. Gaining insight into customers’ perceptions of VAT’s financial, economic, and social repercussions is essential for informing tax policy decisions and fostering sustainable economic growth. The impact of tax reform on growth will be greater if the change has significant positive incentive (substitution) effects that boost work, saving, and investment; minor or adverse income effects, including smart targeting of tax cuts; and minor or adverse income effects. Tax policy has a variety of impacts on economic growth. Taxation is used to achieve particular social objectives, such as the redistribution of wealth and, as a result, a reduction in disparities. In other words, taxation is utilized as an instrument (Musgrave, 2008).

As a result of the fact that taxation in any economy is a complex component because its effects are felt across the board in all areas of the economy, any study on the topic is of considerable value. One of the most significant improvements to the public financial system in any nation is the implementation of VAT (Shakkour et al., 2021). This study is of great significance in the sense that it has the potential to give an insight into the impact that the VAT on consumable goods has on the payers from three significant dimensions: financial, economic, and social.

Problem Statement

The value-added tax (VAT) is a widely utilized taxing method governments implement to generate fiscal income and facilitate sustainable economic growth. This study investigates how customers perceive the influence of value-added tax (VAT) on sustainable economic development’s financial, economic, and social aspects. The primary concern revolves around acquiring a comprehensive understanding of the impact of value added tax (VAT) on individuals and businesses and the extent to which it facilitates or obstructs the attainment of sustainable economic development objectives.

VAT is a significant component of modern tax systems worldwide, contributing to government revenue and economic stability. However, there needs to be more understanding of how customers perceive the implementation of VAT in terms of its financial, economic, and social impacts on sustainable economic development. This research addresses this gap by examining customers’ perceptions of VAT implementation and its implications from three broad perspectives: financial, economic, and social. The study examines the customers’ perception of the financial burden of VAT on their household budgets and purchasing power, its impact on public services and infrastructure development, the role of VAT in economic growth, investment attractiveness, and business competitiveness. The study also analyzes the customers’ perception of the equity and fairness of VAT implementation in society, particularly concerning its impact on different income groups and vulnerable populations. It explores the customer’s awareness of the social welfare initiatives funded by VAT revenue and their contribution to poverty alleviation and social development. However, customers also believe that an increase in taxes somewhere affects their financial planning, household budgets and their spending.

Objectives of the Study

The following goals are taken into consideration when conducting this study:

To explore customer awareness and comprehension regarding the concept and operation of value-added tax (VAT).

To analyze the elements of financial perspectives of VAT and its impact on sustainable economic development.

To study the elements of economic perspectives of the VAT and its impact on sustainable economic growth.

To examine the elements of social perspectives of VAT and its impact on sustainable economic development.

Research Gaps

This study takes valuable insights from the available literature review in the existing field. It provides dimensions for understanding the payer’s views on VAT’s financial, economic, and social perspectives in sustainable economic development. The present literature study has analyzed the financial, economic, and social dimensions of value-added tax (VAT) within the framework of sustainable economic development. Although a considerable body of research has been conducted, it is imperative to acknowledge the presence of significant gaps in the existing literature that necessitate future investigation. By addressing these gaps, a comprehensive comprehension of the correlation between value added tax (VAT) and sustainable development can be achieved, offering valuable insights for informing future policy decisions and academic study.

Incorporating consumer perspectives about the financial, economic, and social aspects of value-added tax (VAT) is crucial in formulating tax policies that facilitate sustainable economic growth. The extant body of literature places significant emphasis on comprehending consumer viewpoints, yet it is essential to acknowledge the presence of considerable research gaps in this domain. By addressing these gaps, the present study mainly focuses on exploring customers’ opinions on three significant dimensions of VAT.

The present study aims to investigate the following research questions:

Q1. What is the extent of customer awareness and comprehension regarding the concept and operation of value-added tax (VAT)?

Q2. What is customers’ perception regarding the financial implications of value added tax (VAT) on their finances, including factors such as augmented consumer prices, income distribution, and the overall tax burden?

Q3. What are the economic consequences of value added tax (VAT) as seen by consumers? How does it impact consumer behavior, business operations, and investments?

Q4. To what extent do customers see the impact of value added tax (VAT) on social welfare?

The paper is divided into the following sections: The first is the introduction; Section 2 discusses the literature review, followed by the development of hypotheses derived from the current literature. Section 3 presents the research methodology. Section 4 presents the results and testing of the hypothesis. Section 5 presents the discussions. Section 6 presents the study’s implications, and Section 7 concludes the study.

Literature Review and Hypotheses Development

VAT and Economic Development

The relationship between VAT and economic growth in both industrialized and developing countries has been studied empirically by numerous researchers. According to Unegbu and Iretin (2011) investigation, VAT significantly affects economic growth. The main goals of the VAT were to increase the government’s income base and make money available for development projects that would hasten economic growth (Adereti et al., 2011). Hassan (2015) and Inimino et al. (2018) assert that VAT contributes to economic growth.

Both wealthy and developing countries have been quite concerned about global economic growth. The increased tax revenue from implementing VAT will allow governments to invest more in technological advancements and spur economic growth (Bansal & Alfardan, 2020). According to Lipsey (1986), economic growth is the steady rise in a country’s total output. Economic growth is an increase in the value of the commodities and services an economy generates (Al-Faki, 2006). Economic growth is when a nation’s national revenue or output of goods and services increases (Osammonyi, 2005). From research conducted between 2003 and 2012, Jalata (2014) determined that VAT considerably aided economic growth in the country. This finding aligns with many experts’ opinions that VAT contributes to increased economic growth and industry productivity (Ayoub & Mukherjee, 2019; Demi et al., 2021; Inimino et al., 2018; Lan et al., 2020; Ma et al., 2022; Nasiru et al., 2016). Basalat et al. (2023) conducted a study to investigate the influence of corporate governance on the financial performance of publicly traded firms on the Amman and Palestine stock exchanges. Based on its findings, the study suggests that codes are subject to ongoing evaluation and that corporations must adhere to corporate governance practices via legislation and laws. This would encourage corporations to demonstrate a more significant commitment to such practices.

Some studies primarily focused on determining the customer’s perception of VAT in the growth and development of economies. The study conducted by Al-Hadrami and Almoosa (2019) investigated customers’ perspectives and awareness of the value-added tax (VAT) in the Kingdom of Bahrain. The study’s findings suggest that the participants neither have a favorable nor unfavorable view toward VAT (Al-Hadrami & Almoosa, 2019). Another study by Almutairi and Naser (2021) investigated individuals’ perceptions of implementing the Value Added Tax (VAT) in Kuwait. The analysis findings revealed a positive correlation between the level of support for implementing VAT and the perceived economic benefits associated with its implementation (Almutairi & Naser, 2021). The study conducted by Chigbu and Ali (2014) examined the correlation between value-added tax (VAT) and economic development in the context of Nigeria. This study used the Engle and Granger cointegration approach to analyze a dataset from 1994 to 2012. The findings of this research demonstrate a positive relationship between the value-added tax (VAT) and economic growth, as measured by actual gross domestic product (GDP). According to Chigbu and Ali (2014), the findings indicate a need for both long-term and short-term correlation between VAT and GDP.

Financial Perspectives of VAT

Extensive research has been conducted on the financial implications of value added tax (VAT). Scholars have frequently prioritized examining the immediate financial consequences for customers. Nevertheless, the value-added tax (VAT) is also commended for its efficacy in generating income and its capacity to mitigate tax fraud, hence offering advantageous fiscal outcomes for governments (Keen & Lockwood, 2010).

Bogari (2020) looked into the social and economic effects of enacting a value-added tax in the Kingdom of Saudi Arabia. The results show that implementing the value-added tax increases the nation’s financial resources. However, such an effort would be strenuous and have negative social consequences. The introduction of a VAT has little impact on the overall level of prices; instead, the growth of credit programs and pay raises are responsible for the current price increase (Al-Mursi, 2004). To pinpoint some of the issues associated with introducing the VAT, Ahmed (2005) looked at the factors underlying its adoption. The fact that an adequately implemented VAT has no adverse effects on revenue or price is noteworthy. One of the study’s most significant findings is that the development of public revenues and the effectiveness of tax collection determine how well a VAT is implemented. A positive and robust relationship exists between VAT and gross domestic product (Kalas & Milenkovic, 2017). The research conducted by Jabarin et al. (2019) examines the impact of macroeconomic variables on the returns of the Amman Stock Exchange and the Palestine Stock Exchange. According to the key findings, political events and macroeconomic factors substantially affect the returns of the stock markets in Amman and Palestine.

Ahmad et al. (2013) state that direct taxes should be raised rather than indirect taxes to encourage economic growth. According to Bird (2005), the value-added tax (VAT) is the “money machine” tax that both developed and developing countries need to enact for their governments to be able to raise enough revenue. Between 1995 and 2015, Simionescu and Albu (2016) analyzed how the standard VAT rate affected GDP growth in Central and Eastern European nations. The study’s results demonstrated that the increase in the VAT rate was beneficial to the economy. A Value Added Statement (VAS) can function as a mechanism to stimulate corporate governance through the provision of accountability and transparency concerning the generation and distribution of value within a company (Abdel Naser et al., 2004). Chan et al. (2017) studied the impact of public expenditure performance on productivity development in 115 countries with a VAT system. We can derive the following hypothesis from prior discussions.

H1: Financial perspectives of VAT significantly impact sustainable economic development.

Economic Perspectives of VAT

Hamid (2010) assessed how the VAT affected the achievement of economic and social objectives in the Syrian Arab Republic. According to the study, VAT favored investment and produced a sizable financial return for the state budget. The impact of VAT on tax revenue and inequality was investigated in this study. According to this study, the VAT increased total government revenues, which increased spending on essential public services for low-income families. Oladipupo and Izedonmi (2008) claim that the extent of taxpayers’ non-compliance with the VAT may be due to their ignorance of the numerous tax regulations. As a result, the public’s perception of VAT issues has frequently been unfavorable, which has led to low revenue generation to support economic growth.

From an economic perspective, the Value Added Tax (VAT) is pivotal in fostering sustainable economic development. According to the research conducted by Burgess and Stern (1993), value-added tax (VAT) systems can enhance investment and promote economic growth by reducing the tax wedge and strengthening the overall business climate. The proponents assert that when well executed, the Value Added Tax (VAT) can enhance economic efficiency and foster competitiveness. Nevertheless, it is worth noting that Value Added Tax (VAT) can influence consumer behavior, influencing consumption and savings patterns. These effects potentially have implications for the overall trajectory of long-term economic growth, as highlighted by Feldstein (1978).

Alavuotunki et al. (2019) examine how installing the value-added tax has affected inequality and tax revenue using recently made public macro data. Contrary to an earlier study, the results indicate that the VAT’s effects on revenues have not been sound. The data show that while implementing the VAT did not change consumption disparity, it did increase income-based inequality. According to Omesi and Nzor (2015), taxation is the “life wire” of any nation, and a country’s degree of growth may often be directly correlated to the amount of money it receives through taxation. Nour and Allae (2003) conducted a study to investigate the comprehension of the implications of economic value added (EVA) as a metric for assessing the success of Jordanian industrial companies. The study found that EVA is contingent upon the accuracy of financial statements and provided several crucial recommendations for such companies.

According to research by Nasiru et al. (2016), value-added tax has been linked to increased productivity. The significance of VAT revenue and its role in driving economic expansion is also highlighted in their recommendations. To determine the urgency of the Nigerian economy’s systemic transformation and the connection between the two, Adegbie et al. (2016) assessed the impact of value-added tax on the country’s economy from its inception to the present. It was shown that VAT and GDP were positively correlated.

This study investigates the impact of VAT receipts on the performance of the industrial sector (Omodero & Eriabie, 2022). The research uses Pairwise Granger Causality Tests, which reveal positive and robust causation effects of local VAT returns and aggregate VAT collection on industrial output. Szarowska (2013) used regression analysis on annual panel data for EU-24 member states from 1995 to 2010 and concluded that consumption taxes contributed positively to GDP growth. Using time series data from 1985 to 2016, Ayoub and Mukherjee (2019) examined the impact of China’s VAT on the country’s economic growth and discovered a statistically significant positive link. We can derive the following hypothesis from prior discussions.

H2: Economic perspectives of VAT substantially impact sustainable economic development.

Social Perspectives of VAT

According to Musgrave (2008), taxation is used to achieve particular social objectives, such as the redistribution of wealth and, as a result, a reduction in disparities. In other words, taxation is utilized as an instrument. In all countries worldwide, but especially in Western countries, taxation is a fundamental source and pillar of revenue creation (Azubike, 2009). Value-added tax (VAT), according to

Aguolu (2000) is a sensible idea that has reduced the tax burden on taxpayers, reduced the incidence of tax evasion, and ensured the collection of funds to support economic growth. Before the recent global COVID-19 outbreak, the VAT imposed by Saudi Arabia on all goods and services was 5%. However, the country has since increased this sum and enacted a 15% VAT beginning in July 2020. As of July 1, 2020, the government raised the regular VAT rate to 15%. The primary justification for increasing this rate is to enhance income because economic activity has declined, and health costs have increased (Sarwar et al., 2021).

Value-added tax (VAT) may give rise to societal ramifications. Torgler (2005) conducted a study that investigated the correlation between tax morale and compliance with value added tax (VAT) regulations. The research revealed how individuals perceive equity within the tax system, which might impact their compliance with value added tax (VAT) requirements. The maintenance of social cohesion relies on the imperative of establishing a perception of equity within the VAT system.

The value-added tax (VAT), an indirect form of taxation, has emerged as one of the most important revenue generators in many nations (Aasness et al., 2002; Weber, 2012). The governments of all countries will work arduously to increase the tax revenues they receive because of the significance of taxes in terms of generating income for the government to use for a variety of purposes, its capacity to influence consumption patterns, which in turn results in the expansion of the economy, its capacity to exert influence on economic variables, and its capacity to influence consumption patterns (Asaolu et al., 2018). Adhikari (2020) highlights that implementing VAT has a varying production effect based on the nation’s wealth level, citing certain unique features of emerging countries, including the propensity for tax evasion. Wadesango (2020) showed that various factors, including human characteristics, VAT technical requirements, and environmental factors, such as the advanced nation’s economic, political, and socioeconomic situation, impacted VAT compliance.

Owolabi and Okwu (2011) assessed the impact of VAT on the expansion of the Lagos State economy from 2001 to 2005. Each development indicator (infrastructure, environmental management, education sector, youth and social welfare, agriculture, healthcare, and transportation) was examined to see how it affected Lagos State’s VAT receipts during the study period. They concluded that during the study period, VAT revenue favored the growth of the various economic sectors in Lagos State. We can derive the following hypothesis from prior discussions.

H3: Social perspectives of VAT significantly impact sustainable economic development.

However, the present study used three new dimensions to explore the customers’ perception toward VAT; in addition to this, we also referred to the Theory of Planned Behavior (TPB) to understand customers’ perceptions and intentions toward value-added tax (VAT) in the context of sustainable economic development. TPB examines the relationship between attitudes, subjective norms, perceived behavioral control, and behavioral intentions. Perceptions of one’s desirability to carry out a behavior are referred to as attitudes toward doing that behavior (Ajzen, 1987). According to Ajzen (1991), the subjective norm in TPB refers to an individual’s perception of social pressure to perform or refrain from performing a behavior. The ability to carry out a target behavior is reflected in perceived behavioral control (Ajzen, 1987). In this case, it could help understand how customers’ attitudes, societal norms, and perceived control influence their support or opposition toward VAT and its role in sustainable economic development. Utilizing the Theory of Planned Behavior (TPB) for examining customers’ perceptions of the financial, economic, and social perspectives of value-added tax (VAT) in sustainable economic development can provide a robust framework for understanding and analyzing their attitudes and intentions regarding VAT. Understanding customers’ attitudes toward VAT can shed light on their perceptions of its effectiveness in sustainable economic development. Subjective norms encompass the perceived social pressures and norms surrounding VAT. This includes how customers perceive the expectations and opinions of others (e.g., peers, family, and society) regarding VAT and its role in economic sustainability. Perceived behavioral control refers to customers’ perceived ease or difficulty in performing a behavior related to VAT, such as complying with VAT regulations or understanding its economic impact.

Methodology

The Conceptual Framework

This study explores the multifaceted impacts of implementing value-added tax (VAT) on customers’ perceptions within Saudi Arabia’s economic landscape. The introduction of VAT represents a significant fiscal policy shift in the Kingdom, aiming to diversify revenue sources and bolster sustainable economic development. Through a comprehensive examination of financial, economic, and social dimensions, this research provides a nuanced understanding of how VAT implementation influences customers’ perceptions and its broader implications for the Saudi Arabian economy. Examining the financial, social, and economic perspectives of VAT is significant for customers because it helps them understand the impact of the tax on their personal finances, social equity considerations, economic efficiency, consumer behavior, and policy implications—such significance motivated researcher to choose three broad explanatory variables for the examination.

This study employed one dependent and three independent variables in its investigation. Three independent variables, the financial perspectives of VAT (FP), the economic perspective of VAT (EP), and the social perspectives of VAT (SP), were used to develop the conceptual framework and examine their impacts on a dependent variable, economic development (ED). The study considered twenty to two dimensions under these independent and dependent variables to examine customers’ perceptions of the financial, economic, and social perspectives of value-added tax (VAT) in sustainable economic development. The financial perspectives of VAT consist of five dimensions, the economic perspectives of VAT six dimensions, the social perspective five dimensions, and economic development six dimensions. The conceptual framework of the study is presented in Figure 1:

Proposed conceptual framework on the financial, economic, and social perspectives of VAT on sustainable economic development.

Data Collection and Sampling

The present study is empirical and quantitative. A mixed-method approach consisting of primary and secondary sources was used to collect the data for this investigation. The primary data was collected through a structured, self-administered questionnaire. The questionnaire used in the study has been provided as Supplemental Material. The study was conducted using a cross-sectional questionnaire survey method among Saudi residents. The available literature was thoroughly reviewed to explore the significant variables used in the previous studies that helped design the questionnaire.

The present study aims to gather data from customers in Saudi Arabia, who were the prime respondents. For gathering the data, we used convenience sampling, a non-probability sampling method, to choose individuals who are readily available or accessible. An online questionnaire was created using Google Docs, and the link was shared via various social media platforms among colleagues, friends, and known persons with a request to share further. The questionnaire was floated for 3 months, and we got 315 filled online questionnaires from the respondents. Hair et al. (2014) state that when the population is unknown, the minimal sample size for the investigation is five times the number of indicators. There were 22 indicators in this study. Hence, a minimum sample size of 110 respondents was required. The study had 315 participants, which exceeded the needed minimum sample size.

The generalizability of this research provides contextual relevance and focuses on Saudi Arabia and its implementation of VAT. The generalizability of findings would primarily apply to similar contexts where VAT policies are being implemented or considered. The sample used in the study is diverse and representative of various demographic groups, regions, and socioeconomic backgrounds within Saudi Arabia, which makes the findings more generalizable. The methodology used to conduct the research, including the sampling techniques, data collection methods, and statistical analysis, would influence the generalizability of findings. Rigorous methodology that accounts for potential biases and limitations increases the likelihood of generalizability. The research findings may affect policy-making and sustainable economic development in Saudi Arabia.

There were two parts to the questionnaire. In the first part, the demographic information of the respondents was gathered. The second part contained twenty-two statement-based questions, allocated under the three constructs, related to the familiarity of financial, economic, and social perspectives of VAT and its impact on economic development. The responses were measured using a five-point Likert scale, with one being strongly disagreed and five strongly agree. The information was gathered utilizing an online survey through Google Forms, with brief study details and the survey link, shared among available contacts with a request to share further. One of the popular non-probability sampling methods for these kinds of studies, the convenience sampling approach, was utilized to gather the data.

A pilot test was conducted on the pre-designed questionnaire. To get input on the questionnaire’s design, 50 respondents participated in a pilot test of the questionnaire. All questions from the original, extensively tested version of the survey were included in the final, fully functional version of the survey questionnaire. Three hundred fifteen respondents across Saudi Arabia participated in a questionnaire-based online survey, which provided valuable insight for the analyses of the study. All the participants gave their informed consent to participate in the study. The respondents were informed of the data’s confidentiality in the questionnaire, and it was assured that the information would only be utilized for analysis. However, ethics approval was not required for this study because it aimed to use a quantitative technique to evaluate different aspects of the customer’s perception of VAT.

The study explores the residents’ opinions on the social, economic, and financial aspects of value-added tax on economic development. The questionnaire was designed to keep in view the customers’ behavioral aspects related to the VAT they pay in their daily purchases. Five out of 22 questions measured the financial perspectives of the VAT, six questions measured the economic aspects, five questions measured the social elements, and six questions were based on economic measurements.

Data Analysis

Statistical package for social sciences (SPSS) was used to examine the primary data gathered from the respondents. Three independent factors and one dependent variable were compared in this study. The variables’ mean, minimum and maximum values and standard deviations were examined using descriptive statistics. The demographic characteristics of the samples were also analyzed as frequency and percentage. Cronbach Alpha was used to assess the validity of the study’s scale, and correlation analysis was done to determine how the variables related to one another. With the help of regression models and analysis of variance, the proposed hypotheses were examined.

Results

Demographic Profile of the Respondents

The demographic profile of the responders is shown in Table 2. The characteristics of the population in the table represent the age, gender, educational level, and professions of respondents.

Demographic Profile.

Descriptive Statistics of the Variables

Considering the minimum and maximum values, mean, standard deviation, and other data in Table 3, it is reasonable to conclude that all three variables based on customer’s perception of VAT play an essential role in economic development. On the other hand, the influence of economic perspectives is the most significant of all variables, followed by social and financial perspectives of value-added tax.

Descriptive statistics of the variables.

Reliability Test

The internal consistency of the constructs employed in the study was examined using the reliability analysis (Cronbach’s alpha). The internal consistency reliability of the scales should be measured using Cronbach’s alpha if the study is based on a Likert-type scale (Gliem & Gliem, 2003). Estimates of the variance in scores of various variables that can be attributed to chance or random errors make up reliability (Selltiz et al., 1976). A coefficient of more than or equal to 0.5 is typically regarded as satisfactory and a sign of construct dependability (Nunally, 1978). SPSS was used to compute the reliability measure. The dependability of each construct and its interpretations is summarized in Table 3. Cronbach’s alpha indicates internal consistency and reliability, ranging from .811 to .872. This suggests that the data was highly consistent and reliable internally, as the Cronbach alpha values in Table 4 below are more significant than .7 (Sekaran, 2003).

Reliability Analysis.

Correlation Analysis

The correlation between the dependent and independent variables is shown in Table 5. The Pearson correlation coefficient is commonly utilized for comparing test results (Beanland et al., 1999). A correlation coefficient of less than .7 is considered favorable (Litwin, 1995). The correlation analysis revealed that financial perspectives of VAT (r (315) = .48, p = .05), economic perspectives (r (315) = .63, p = .05), social perspectives (r (315) = .64, p = .05), and economic development were significantly correlated.

Correlation Analysis of the Variables.

Correlation is significant at the .01 level (two-tailed).

Regression Analysis

This study uses regression models, as regression analysis is predominantly employed to investigate the association between a dependent variable and one or more independent variables. The current study comprises a single dependent variable and three independent factors. This approach is appropriate for straightforward models that involve a solitary outcome variable. Multiple regression allows us to analyze how several independent variables influence a single dependent variable. Social sciences and business research often use this to predict outcomes based on multiple factors (Hair et al., 2014).

Considering the correlation analysis’s findings, a high level of correlation coefficients was observed. So, we adopted bivariate regression analysis because there was a strong possibility of multicollinearity and a significant requirement to investigate individual regression coefficients. The overview of the linear regression model emphasizes the importance of the overall research model in reaching the intended outcome (Hair et al., 2014).

The regression model specification used in this study is as follows:

Where:

SED = Sustainable economic development.

β1 FP = Financial perspectives.

β2 EP = Economic perspectives.

β3 SP = Social perspectives.

β0: Intercept (constant term).

β1: (i = 1, 2, 3) Slope (coefficient of the independent variables).

ε: Error term (residuals).

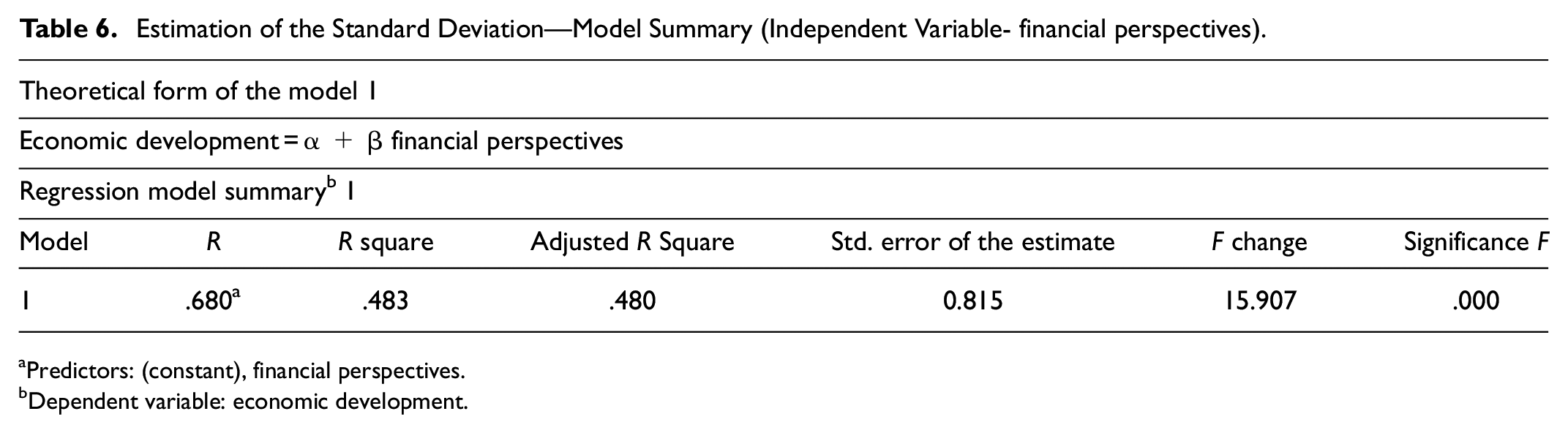

Table 6 displays the summary estimation for the standard deviation model. The first independent variable, financial perspectives, significantly predicts economic development. The F, p, and R2 values demonstrate the regression model’s statistical validity. The regression model has 68% explanatory power. Financial perspectives significantly influence economic development at the 5% limit for p-value.

Estimation of the Standard Deviation—Model Summary (Independent Variable- financial perspectives).

Predictors: (constant), financial perspectives.

Dependent variable: economic development.

Table 7 displays the summary estimation for the standard deviation model. The second independent variable, economic perspectives, significantly predicts economic development. The F, p, and R2 values demonstrate the regression model’s statistical validity. The regression model has 68% explanatory power. Economic perspectives significantly influence economic development at the 5% limit for p-value.

Estimation of the Standard Deviation—Model Summary (Independent Variable—Economic Perspectives).

Predictors: (constant), economic perspectives.

Dependent variable: economic development.

Table 8 displays the summary estimation for the standard deviation model. The third independent variable, social perspectives, significantly predicts economic development. The F, p, and R2 values demonstrate the regression model’s statistical validity. The regression model has 71% explanatory power. Social perspectives significantly influence economic development at the 5% limit for p-value.

Estimation of the Standard Deviation—Model Summary (Independent Variable—Social Perspectives).

Predictors: (constant), social perspectives.

Dependent variable: economic development.

Testing of Hypotheses

There were substantial collective impacts between the variables, financial perspectives, economic perspectives, and social perspectives, according to the regression results (R2 = .688, F(3, 315) = 175.099, p = .000). Customers’ awareness and comprehension regarding the concept and operation of value added tax (VAT) can vary significantly depending on factors such as their level of education, exposure to business transactions, and the transparency of government communication about taxation policies. Many customers understand that VAT is a consumption tax levied on the value added to goods and services at each stage of production or distribution. They may comprehend that the end consumer ultimately bears it. Customers are generally aware that VAT is included in the prices of goods and services they purchase, although they might only sometimes recognize the specific amount of VAT being charged. However, the customers also believe that implementing value-added tax (VAT) represents a significant policy shift aimed at diversifying revenue sources, promoting fiscal sustainability, and fostering economic development.

The relationships between dependent and independent variables were examined by analyzing the predictors individually. The regression results indicated that “financial perspectives” were a significant predictor in the model (R2 = .483, F(1, 314) = 15.907, p = .000); thus, H1 was accepted. In addition, in the model, “economic perspectives” (R2 = .553, F(1, 314) = 18.340, p = .000) was a significant predictor in the model; thus, H2 was accepted, and “social perspectives” (R2 = .686, F(1, 314) = 85.131, p = .000) was found to be a significant predictor in the model; thus, H3 was accepted. An overview of the hypothesis testing is given in Table 9:

Results of Hypotheses Testing.

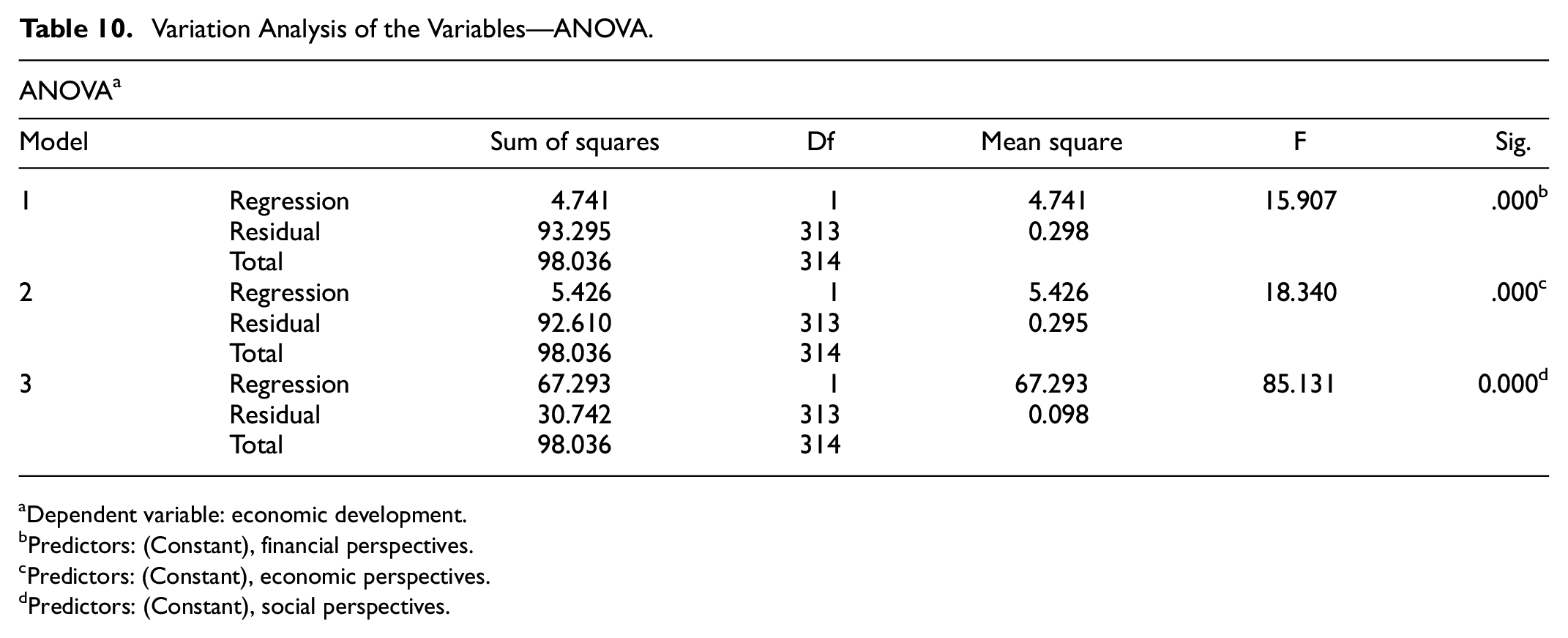

The three regression predictor model ANOVAs are shown in Table 10, and the regression model coefficients are shown in Table 11. The relationship between the models across all variables was evaluated using an ANOVA model. The ANOVA can assist in determining if the means of independent variables differ significantly. The significance value for the regression models, as shown in Table 9, is 0.000, less than 0.05. This means that the models are statistically significant (Hair et al., 2014).

Variation Analysis of the Variables—ANOVA.

Dependent variable: economic development.

Predictors: (Constant), financial perspectives.

Predictors: (Constant), economic perspectives.

Predictors: (Constant), social perspectives.

Coefficients Regression Models.

Economic development.

Table 10 provides the values of the regression coefficients for each of the three variables. The figures indicate that the first predictor has the most significant impact on economic development (β = .273, t = 3.988, p < .05), followed by the impact of the second predictor (β = .231, t = 4.282, p < .05), and third predictor (β = .150, t = 3.017, p < .05) respectively. This analysis indicates that people believe that in a nation’s economic development, the economic and financial perspectives of the value-added tax have a significant contribution compared to the social perspectives.

Discussions

This study evaluated the effects of financial, economic, and social perspectives of VAT on sustainable economic development and analyzed the payers’ perspectives on these dimensions. Based on the findings of the study, these variables have a substantial impact on the economic development of a nation. These findings are consistent with the views of many experts who believe that VAT helps to increase economic growth and industry productivity (Ayoub & Mukherjee, 2019; Demi et al., 2021; Inimino et al., 2018; Lan et al., 2020; Ma et al., 2022; Nasiru et al., 2016). VAT impacts economic growth since it helps pay for various government requirements (Illyas & Siddiqi, 2010). According to a descriptive statistics study, all three variables substantially impact the growth and development of an economy. According to descriptive statistics, the mean value of each variable is close to the fourth Likert scale point. As a result, it appears that all variables are at levels of “agree.” The most significant economic development-related standard deviation is 0.799, which pertains to the economic perspectives of VAT.

In contrast, social perspectives had a minor standard deviation, 0.505. The study of Cronbach’s alpha revealed that the internal consistency and reliability of the data were excellent. The correlation study found that the variables had a concrete and positive relationship. According to regression results, all three regression models significantly impact economic development and are deemed significant.

The study analysis reveals that payers believe that VAT implementation may be straightforward for several reasons and provide various financial, economic and social benefits in economic development. The primary objectives of the VAT were to enhance the government’s revenue base and make funds available for development programs that would accelerate economic growth (Adereti et al., 2011). VAT compliance is one of the most significant improvements of any country’s public financial system (Shakkour et al., 2021). A consistent tax rate helps simplify exports and imports because it applies to a larger population. VAT systems can generate substantial amounts of revenue. According to Adereti et al. (2011), the primary objective of adopting a VAT system is to broaden the government’s income base so that more money may be allocated to various developmental projects to speed up the economic growth rate. In Jordan’s retail sector, the study Alshira'h (2024) investigated the relationship between government trust, VAT compliance costs, and VAT compliance. It revealed that trust in the government was found to have a statistically significant positive association with VAT compliance, whereas expenses related to VAT compliance were not. The study Gimba and Anyanwu (2023) investigated the effect of federally collected tax revenue on Nigeria’s economic development and indicates that the revenue generated from value-added tax, petroleum profits tax, and corporation income tax significantly and positively influences Nigeria’s long-term economic growth.

The number of taxable goods and services directly relates to the tax income produced by VAT. A logical idea known as VAT has helped taxpayers pay less taxes, stop tax evasion, and ensure that money is collected to support economic growth (Aguolu, 2000). Taxation is utilized to achieve specific social goals, such as wealth redistribution and reducing inequities (Musgrave, 2008). As a result of the government’s implementation of VAT on various goods and services, taxes are more extensive. The value-added tax and institutional quality are acknowledged elements that influence the link between government expenditure and economic development (Chan et al., 2017; Khan et al., 2024). This may result in a significant tax revenue stream that the government can use to pay for public services. The main goal of a tax system is to raise enough money to pay for the government’s essential expenditures, and taxation is frequently acknowledged as the most efficient means of improving the capabilities of the public sector and paying off debt (Okoye & Ezejiofor, 2014). An econometric model of VAT’s fiscal implications on Romania’s construction sector business performance from 2010 to 2021 was proposed by Badiu (Cazacu) et al. (2024) and shows that financial independence and solvency promote excessive taxation in rising markets and developing countries like Romania, connected with macroeconomic evolution. The data also show that tax pressure might hinder company sustainability, affecting consumers. The study by Ojo and Shittu (2023) evaluates Nigerian SME VAT compliance. It examines how Taxpayer Perception and Attitudes (TPA), Organizational Characteristics (OC), Tax Compliance Cost (TCC), VAT Implementation Efficacy (VIE), income, profit, staff, consumers, and SME size affect VAT compliance among Nigerian SMEs. The results show that TPA, OC, TCC, and VIE affect VAT compliance. The study found that revenue positively but not significantly affects VAT compliance.

A VAT is a consumption-based tax. VAT has a substantial impact on economic growth (Unegbu & Iretin, 2011). Jalata (2014) determined, based on studies undertaken between 2003 and 2012 that the value-added tax contributed significantly to the country’s economic growth. The share of money spent by poorer households is higher. Therefore, a value-added tax is regressive if measured relative to current income and applied without additional policy modifications. According to Oghuma (2017), VAT is a consumption tax evaluated and paid for at each level in the consumption chain. Taxes fund the government’s traditional duties of law enforcement, general administration, and social and infrastructure development to boost a nation’s economy. Many countries have adopted value-added tax, a consumption tax (Alan, 2003). The study of Adefolake and Omodero (2022) employs time series data spanning the years 2000 to 2021 to assess the influence of tax revenue on the economic expansion of Nigeria, and findings indicate that both PPT and VAT have a substantial and positive impact on GDP. It also demonstrates that CIT has a significant and adverse effect on GDP. Focusing on blockchain technology in the value-added tax (VAT), the study conducted by Setyowati et al. (2023) examined strategic considerations associated with the integration of blockchain technology into the value-added tax (VAT) system of Indonesia. The results of the study indicate that environmental and organizational factors should be considered when integrating blockchain technology into Indonesia’s VAT system: support from foreign governments and partners; advantages, data security, smart contract coding, architecture, permissions, and shared infrastructure; and organizational readiness, support from higher authorities, and technological advancements.

More significant tax revenue from implementing VAT will allow governments to invest more in technical breakthroughs, promoting economic growth (Bansal & Alfardan, 2020). A value-added tax is less regressive compared to lifetime income. Specific tax preferences can affect how economic resources are distributed, while high marginal tax rates can discourage work, saving, investing, and innovation. Tax cuts, however, have the potential to slow down economic growth in the long run through increasing deficits. Furthermore, the findings of Alsughayer (2021) are supported by the positive and significant influence of revenue and profit on VAT compliance, which suggests that SMEs profit more and comply with VAT the more sales they create. The research conducted by Almousa and Adeem (2023) empirically investigated the perception of value-added tax (VAT) in Saudi Arabia and indicated that a majority of the participants in the sample had VAT knowledge, its favorable impact on tax revenues, and agreed that its proper implementation is crucial. The study of Al Farsi et al. (2020) reveals that the level of correlation between knowledge that value-added tax applies to banking services and the extent to which value-added tax can assist in addressing the budget imbalance in the economy is the weakest. Furthermore, the research emphasized critical variables such as consumer knowledge, understanding, perception, and awareness regarding value-added tax. The study by Faheem and Alzoubi (2019) evaluates and reviews the literature on VAT’s influence in the UAE and finds that because VAT taxes consumption rather than income, the VAT system will encourage tax compliance, savings and investment and improves economic efficiency and fairness.

Implications of the Study

The argument that higher consumption taxes encourage economic growth by discouraging spending and promoting saving is one of the main arguments that favor taxing consumption rather than income. The research proves that financial, social, and economic perspectives of VAT have significant implications for sustainable economic growth. The above findings are essential for all stakeholders directly and indirectly related to VAT. The findings significantly affect how taxpayers, policymakers, and tax authorities interpret VAT’s financial, social, and economic impact on sustainable economic development and how they should be analyzed and used. The current study will add valuable information to the knowledge base of the payers to understand these perspectives and enhance their views on the contribution of VAT to sustainable economic development.

Understanding how customers see VAT can help policymakers create more effective and acceptable tax laws. Through consumer perception of VAT in the context of sustainable development, policymakers may find ways the tax system can support environmentally friendly and socially responsible economic operations. VAT perception affects customer spending and saving. VAT may be a significant government revenue stream. Perceptions can explain VAT’s effects on income and social fairness. Positive VAT perceptions can boost a nation’s product competitiveness. Findings suggest tax system education for consumers. Customers may accept VAT and its role in supporting government services if they understand how it works. In conclusion, understanding consumer VAT views in sustainable economic development is essential for creating efficient taxation policies, distributing the tax burden fairly, and encouraging economic growth and social well-being.

Numerous studies have been conducted on customers’ perceptions of VAT implantations. The present study also takes valuable insights from the available literature. Also, it provides a new direction for VAT implementation and customers’perception of three new broad areas: financial, social and economic perspectives of VAT. We have designed twenty-two new dimensions to explore the customer’s perception of the implementation of VAT and its connection with sustainable economic development. The conceptual frameworks used in this study are entirely different from the previous studies and established theories or frameworks in financial, social, and economic perspectives to analyze customers’ perceptions of VAT implementation. The present study is likely more current than previous studies, reflecting the most recent data, policies, and societal attitudes toward VAT implementation in Saudi Arabia. The previous study also employed regression models and descriptive statistics to examine the data, so we also used this method. The present study might have a broader or narrower scope than previous studies, focusing on different aspects or objectives related to VAT implementation and its impact on sustainable economic development. The present study may aim to contribute new insights, perspectives, or empirical evidence to the existing body of literature on the topic, distinguishing itself from previous studies regarding its contributions to knowledge.

Conclusion and Recommendations

VAT systems have the potential to generate significant revenue and contribute to economic development. Implementing VAT may be straightforward and significant from a financial and economic point of view. This is because, in a VAT system, a consistent tax percentage applies to a larger population, which helps simplify exports and imports. The number of items and services subject to the tax determines the quantity of tax income generated by VAT. Because the government imposes VAT on a wide range of products and services, the scope of taxes is broader, and hence, there is a considerable possibility of generating high revenue. Subsequently, this can produce a significant tax income for governments to spend on public services, leading to a nation’s social, financial and economic growth and development.

This study investigated the payers’ viewpoints on financial, economic, and social perspectives of VAT and its influence on economic development. Some important implications may be drawn from the study’s findings and analysis. Based on the descriptive analysis, it is evident that all three perspectives significantly impact economic development. This also signifies that payers’ believe that tax revenue generated from VAT leads to the economic development of a nation. A considerable correlation between the financial, economic, and social views of VAT and its function in economic development was discovered, per the findings of the correlation analysis. The results of regression models concluded that all three variables significantly influence economic development. The analytical evidence revealed that people believe that VAT is widely adopted and well-liked since it generates substantial economic revenue and is very simple to administer. Since VAT is based on consumption, it encourages people to save and invest, another economic growth and development instrument.

There are a few limitations associated with this study. Firstly, the study considers only three essential dimensions of VAT: financial, economic, and social perspectives. In contrast, other dimensions that could influence economic development have yet to be considered. Second, the individual residents were targeted for their opinions about the influence of VAT on sustainable economic development. The opinions of the owners of the firms and corporate professionals might be different. Future research should consider a few more dimensions of VAT that could also influence economic development. One more limitation was associated with the sample size. However, the researchers were able to get a significant 315 responses, but future studies could be done with a larger sample size. VAT encourages investment by replacing distortionary taxes and generating more revenue for the government. Academicians, researchers, and policymakers researching the consequences of VAT and how to increase compliance will find the study’s findings helpful.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440241290342 – Supplemental material for Examining the Customers’ Perception Toward the Implementation of Value-added Tax in Saudi Arabia: A Financial, Economic, and Social Perspectives in Sustainable Economic Development

Supplemental material, sj-docx-1-sgo-10.1177_21582440241290342 for Examining the Customers’ Perception Toward the Implementation of Value-added Tax in Saudi Arabia: A Financial, Economic, and Social Perspectives in Sustainable Economic Development by Hamad Alhumoudi and Amar Johri in SAGE Open

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data will be made available on request from the corresponding author.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.