Abstract

With the growing complexity of innovation, numerous patentees with patents needed for corporate innovation can act as a forest of thorns for companies, often referred to as “Patent Thickets.” These thickets increase the patenting transaction costs and depreciate the company’s market value. However, few studies have examined the mechanism of patent thickets’s impact on firms’ market value in the Chinese context. Based on the patent and market value data of 419 high-tech enterprises in China, this study finds that patent thickets reduce the market value of a company. However, firms with more patent assets can better protect themselves from the depreciation caused by patent thickets by building up their R&D resources, enabling them to generate more of their patented assets internally. This reduces the costs of purchasing patents from outside sources and can enhance the firm’s market value. This study suggests that to mitigate the negative impact of the patent thickets on firms’ market value, firms must build up their R&D inventories. By doing so, they can acquire more patents in-house, thereby protecting their patent rights.

Introduction

The technologies and products of electronic equipment manufacturing industries have become increasingly complex due to the development of artificial intelligence, industrial integration, and penetration (Benalcazar et al., 2017; Entezarkheir, 2019; Zhang et al., 2019). The manufacturer’s production and innovation processes may require multiple patented technologies owned by other entities. Under these conditions, a single manufacturer must pay multiple patent licensing fees to other entities to obtain these rights (Haejun, 2016). These patents are like “forests” that companies must “walk through” to achieve their innovation and product innovation goals. As a result, this phenomenon has been defined by scholars as the “Patent Thickets” (Shapiro, 2000; Teece et al., 2014). Patent thickets can lead to higher barriers to patented technologies and increase the likelihood of extortion by patent licensors. This discourages innovation and raises costs for firms, leading to the “tragedy of the anti-commons” and the emergence of “Patent Trolls” (Heller & Eisenberg, 1998; Yuan & Hou, 2024).

Existing literature has shown that patent thickets reduce the market values of software, computer, and biology enterprises in the U.S. and some European countries (Goode & Chao, 2022). A study by the UK Intellectual Property Office (2013) indicates that high-tech firms tend to avoid investing in R&D in areas with heavy patent thickets, which can negatively impact their growth and performance. Patent thickets have triggered significant overlapping of intellectual property rights, and in a fragmented technology market, firms have increased the cost of acquiring patents, which reduces firm performance (Entezarkheir, 2019; Ziedonis, 2004). However, current research has paid little attention to the factors that can mitigate the negative impact of patent thickets on firms’ market value. Despite the lack of systematic research, studies still show that if enterprises focus on applying, maintaining, and utilizing patents, they will ultimately improve their technological competitiveness and earn higher profits (Luo & Zor, 2023). Accumulating a certain amount of R&D stock promotes more patent production, and holding a certain number of patents can effectively increase enterprise market values. Chinese high-tech enterprises started relatively late compared to other countries; thus, foreign or a few large enterprises often hold essential technology patents. Consequently, Chinese enterprises face substantial patent barriers when entering those markets. For example, the semiconductor industry’s core technology patents are monopolized by giant foreign entities. Therefore, Chinese enterprises that want to break through the patent thickets to engage in technological innovation and market expansion must invest considerable resources and incur high costs, which limits the extent to which their market values can be enhanced (Li & Yuan, 2023). The impact of patent thickets on the market value of Chinese high-tech firms has garnered research attention. China’s patent law has been reformed four times (1992, 2000, 2008, and 2020), and enterprises’ awareness of patent protection has been gradually strengthened. By holding a substantial portfolio of patent assets, an enterprise can enhance its competitiveness, increasing its market value. For example, the unlocking technology patents of bicycle-sharing firms like Mobike and OFO led to multiple lawsuits, negatively impacting their market value. In comparison, in the U.S.-China trade war involving intellectual property issues, ZTE and Huawei performed strongly. Consequently, in patent thickets, enterprises can effectively acquire patent resources, reduce their R&D cost and risk, and enhance their market value (Hall et al., 2021). Given the constraints of patent thicket environments, coordinating patent attribution and benefit distribution among enterprises can be beneficial (Rai & Price, 2021).

In summary, the research questions we endeavored to answer are as follows: (1) Do patent thickets negatively affect firms’ market value in the Chinese context? (2) can firms holding patent assets mitigate this adverse effect? (3) Can the synergistic allocation of firms’ patent assets and R&D stock overcome the external constraints of patent thickets and help increase their market value? Existing studies do not explain or analyze whether patent thicket characteristics affect the market values of Chinese high-tech companies. Few studies examine the mechanism through which patent thickets impact enterprise market value. Clarifying which factors influence the mechanism through which patent thickets impact enterprise market values can reveal a path Chinese high-tech enterprises can follow in dealing with patent thickets and improving their market value effectively. Studying China’s patent thickets at the enterprise level is a new perspective that expands the theory of patent thickets research and provides new opportunities for additional research.

The remainder of this study is organized as follows. The second part is a literature review. The third part is the research design, including the sources of research data and the research methodology introduction. The fourth section describes the data in terms of empirical results and discussion. Additionally, the impact of patent thickets on the market value of Chinese high-tech enterprises, the mechanism of the role of patent assets, and the mechanism of the synergy between patent assets and R&D stock are also tested and analyzed. Finally, the fifth section provides a short conclusion with implications for theory and practice.

Literature Review

Patent Thickets and Firm Market Value

Scholars have begun focusing on the danger patent thickets impose on firms’ market values in emerging technologies (Yuan & Li, 2020). For example, Sanderson and Simons (2014) found evidence that the patent thicket problem exists in the U.S. LED manufacturing industry. Scholars in fields such as biology, nanotechnology, and software in the U.S. and Europe have shown that some patent owners have become patent knockers, creating severe fragmentation of patent rights (Gątkowski et al., 2020). According to the UK Intellectual Property Office (2013), high-tech enterprises tend not to invest in R&D within technology areas with serious patent thickets, which may negatively affect growth in their market value. Entezarkheir (2016) used manufacturing patent data to conclude that patent thickets trigger numerous overlapping intellectual property interests. In a fragmented technology market, enterprises begin producing more internal patents to circumvent external patentee-patented technologies, increasing patent costs. Thus, patent thickets reduce a firm’s market value. Because of the increasing number of internal patents, high-tech enterprises possess patent assets, which gives them certain advantages over other patent owners in negotiation, litigation, product production, and innovation. Thus, patent thickets’ negative impact on enterprise market value is weakened (Syed, 2020).

Previous researchers have comprehensively studied the level of patent thickets formation and their harm to enterprise market values. However, scholars have also not considered whether a difference exists in the degree to which patent thickets affect the market values of U.S. enterprises differently compared to those in other countries, such as China. The patent designs of individual emerging technology enterprises are very balanced in the U.S. and Europe; the negative effect of patent thickets on firms’ market value shows slight variation (Entezarkheir, 2016; Ziedonis, 2004). However, patent resource distribution in China’s high-tech enterprises is unbalanced, triggering market failures and deflating enterprise market values (Luo & Zor, 2023). For example, incomplete statistics indicate that over 100 high-tech manufacturing enterprises in Shenzhen have closed, most concentrated in patent-intensive downstream packaging and application industries. Resource allocation theory suggests enterprises adjust the allocation of required resources so that the resources can focus on the core value of the enterprise and improve its competitiveness (Wang et al., 2023). Patents are considered significant intangible resources necessary for enterprises to compete effectively (Chávez & Lara, 2020). However, firms will inevitably disrupt their resource allocation to acquire patents in a fragmented patent market. This will cause firms to allocate more costs, workforce, and resources to searching for infringement of their technology, negotiating with patentees, litigating, and increasing the resources invested in acquiring external patents (Amore & Mastrogiorgio, 2022; Yuan & Hou, 2023). Thus, the patent thickets problem has become a significant constraint to developing high-tech enterprises in China. It causes misallocation of resources, increases redundancy costs, and relatively depreciates the enterprise’s market value. Additionally, the imbalance in patent resource allocation caused by patent thickets inevitably leads to overlapping product patent license fees, which pressures the production costs of high-tech enterprises (Cass, 2015; Niwa, 2018). Therefore, Hypothesis 1 is proposed:

Inhibiting Role of Patent Assets

Resource allocation theory suggests that the process of allocating resources can result in a mismatch of resources. This leads to market failure and requires direct intervention or regulation by firms or the government (Zeng et al., 2021). Studies have shown that high-tech enterprises use patent strategies, including patent acquisition strategies, to reach patent transaction agreements with external holders of complementary patents (Lee et al., 2018). These strategies may also increase their patent assets or reduce patent costs by concentrating on the patents they need to improve their product manufacturing and operational efficiency. Such strategies thus affect their market values (Jell et al., 2016). Some scholars have begun studying how patent thickets indirectly affect an enterprise’s market value through patent holdings. For example, Entezarkheir (2016) examined a sample of manufacturing enterprises in the U.S. from 1976 to 2002. The study found that fragmentation of patent rights reduced high-tech enterprises’ market values. Still, holding more patents could suppress this negative effect. High-tech firms have also formed patent pools or negotiated patent licenses to cut the cost of acquiring patents from other rights holders and improve efficiency.

Rational resource allocation can reduce transaction costs, improve capital utilization efficiency, facilitate enterprise growth, and help enterprises form unique competitive capabilities. Effective allocation of resources is believed to play a key role in maintaining unique enterprise competitive advantages and allows firms to achieve good performance (Wang et al., 2023). Existing research has overlooked the potential to explore the corrective effect that intangible resources can have on imbalanced resource allocation, leading to declining enterprise performance. This study proposes that enterprise patent assets are essential and unlimited enterprise resources. According to prior research, holding certain patents can mitigate the negative effect patent thickets have on enterprise market values, slow the patent thicket formation caused by the imbalanced allocation of patent resources in China’s high-tech enterprises, and effectively help enterprises compete to improve their market value. Therefore, Hypothesis 2 is proposed:

Inhibiting Role of R&D Stock

Previous research on how patent assets impact enterprise market value and resource allocation focuses on the impact of individual firm resource allocation (Zeng et al., 2021). However, the synergistic allocation and interaction of dual resources and their impact on enterprise market values have been ignored (Kiselev et al., 2020). Enterprises can obtain patents from diverse sources, such as patent transactions, patent licenses, and R&D (Haejun, 2016). Patents obtained through legal means are often of low quality and easily invalidated through patent litigation, while patents produced by an enterprise’s R&D output are more substantial and less easily invalidated (Choi & Gerlach, 2013). R&D stock comprises the R&D resources and capabilities enterprises accumulate over time, including the knowledge and experience of R&D personnel, R&D equipment, and existing technological reserves. These resources and capabilities provide an essential foundation for firms’ innovative activities. Having rich R&D stock means companies have more specialized R&D staff and advanced analytical tools (Jeon & Jung, 2024). R&D stock allows firms to carve new paths through patent thickets (Entezarkheir, 2019), as they can utilize their abundant R&D stock to develop alternative technological solutions and reduce their reliance on existing external resources. For example, when facing communications patent thickets, enterprises with large R&D stocks in the communications field can explore new communication protocols or technological implementations based on their research foundations. This helps them break through the technological barriers formed by patent thickets.

These enterprises can develop their R&D and patent strategies based on their specific situations to cope with patent thickets. They can cross-license patents with other patent owners to avoid constraints and improve their patent litigation and negotiation positions. Developing their own patents will allow them to form patent portfolios in line with their characteristic strategies, avoid redundant resources, and improve knowledge exchange and acquisition (Haejun, 2016; Jell et al., 2016). The stronger an enterprise’s R&D capital, the more patents it will acquire. Additionally, the higher the quality of its patents, the stronger a firm will cope with competitive risks. The greater the number of other enterprises a firm has direct contact with, the lower its cost of dealing with risks, while the easier it is to obtain complementary skills from different enterprises, the more inclined a company is to adopt an offensive patent strategy. Moreover, an enterprise that simultaneously shares patents and joins a patent pool is more likely to form a defensive patent strategy with other patent owners (Lee et al., 2018; Niwa, 2018). Weaker R&D enterprises have less patent output and rely more on external resources to obtain complementary patents, leading them to adopt more single-patent strategies. Additionally, firms can better integrate internal resources for collaborative innovation when they have rich R&D stock and numerous patents (Jain, 2023). For example, enterprises can improve and combine existing patents using their R&D inventories and develop more competitive new technologies or products. Similarly, R&D personnel can apply their existing R&D experience and equipment to probe deeply and expand their firm’s patented technology to realize a 1 + 1 > 2 effect.

In summary, the study of dual resource allocation on enterprise performance enriches the theory of resource diversification, provides additional pathways for enterprises to increase market value, and optimizes the allocation of enterprise resources. Rational dual resource allocation helps enterprises increase their market value and guarantees sustainable development. As seen from the above analysis, the synergy of a firm’s patent assets and R&D stock enables the acquisition of patents through internal corporate R&D, thereby reducing the resource costs associated with external patent search and acquisition. Additionally, external technical barriers and patent litigation risks are reduced. Thus, the negative effect of patent thickets on the enterprise’s market value is effectively suppressed. Therefore, Hypothesis 3 is proposed:

Overall, Figure 1 illustrates this study’s theoretical framework. It is the theoretical model of how patent thickets influence enterprise market value.

Theoretical model of the influence of patent thickets on enterprise market value.

Research Design

Research Methodology

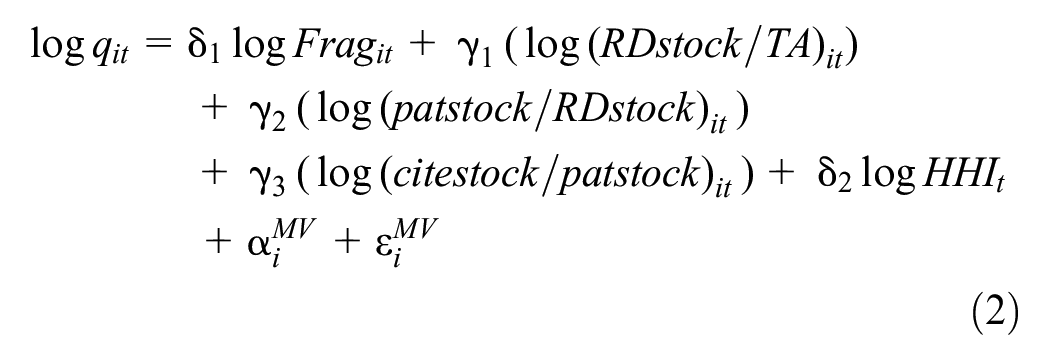

Since the sample is panel data, the patent dispersion index is included in the regression model as a measure of patent thickets. This index is used as an independent variable to control for its effect on the dependent variable. Furthermore, RDstock/TA, citestock/patstock, patstock/RDstock, and HHI are included as control variables in the regression model. These variables may also interact with the dependent variable, considering the potential negative impact relationship between patent thickets and firms’ market value. There may be a dampening effect on firms’ patent assets and R&D stock, and this negative relationship may turn positive. These variables show a nonlinear relationship with each other. To reduce the error between the variable data and the interference caused by different value intervals on the regression analysis and to ensure the distribution of variable data approximates a normal distribution, this study will apply a logarithmic transformation to the regression model of each variable. To reduce the error between the variable data and the interference of different value intervals on the regression analysis so that the distribution of variable data tends to be normal, therefore, this paper will use a regression model of each variable that is logarithmic. The dependent and independent variables have a nonlinear relationship with the control variables. To avoid multicollinearity between the variables, we draw on the study of Ziedonis (2004) to empirically analyze the regression coefficients of the variables using the nonlinear least squares (NLS) method. The differences in regression coefficients were further compared to verify the research hypotheses. To assess how corporate patent assets might mitigate the negative impacts of patent thickets on a company’s market value and to explore the synergistic effects between patent assets and R&D stock, our model will include interaction terms. Specifically, these terms will involve the patent dispersion index interacting with patent assets, as well as the patent dispersion index interacting with both patent assets and R&D stock. Estimating the coefficients of the interaction terms allows precise quantification of the magnitude and direction of synergistic effects. It avoids merely summing the independent effects of the variables while ignoring the possible mutual reinforcement or weakening of their relationships. The interaction between the three variables allows a more comprehensive study to analyze their synergistic effects.

Based on data availability, this study focuses on the data from 419 high-tech enterprises in China from 2009 to 2017. Referring to Hall et al. (2005), Bloom et al. (2013), Griliches (1981), and Entezarkheir (2019), Equation 1 is adopted as the study’s empirical econometric model:

In Equation 1, the log of Tobin’s Q (log(q)) is the dependent variable. Qi,t is the market value of enterprise i in year t, and the logarithm of the patent fragmentation index (log(frag)), which is defined in the next section, represents the patent fragmentation value of firm i in year t. RDstock/TA, patstock/RDstock, citestock/patstock, and log(HHI) are control variables, α is the constant term, and ε is the error term. Firms’ patent assets are measured as log(Grants), and firm R&D stock is defined in Section 3.2. An interaction term is also added to estimate the inhibitory effects of firms’ patent assets and R&D stock on the impact patent thickets have on firm market value: Log(frag) × log(Grants) and log(frag) × log(Grants) ×log(RDstock) are added as interaction terms.

To avoid multicollinearity among the variables in the regression model, log values are used for the dependent variable, Tobin’s Q, and the independent variable, frag. Because a nonlinear relationship exists between the dependent, independent, and control variables, this study follows Ziedonis (2004) and adopts nonlinear regression (NLS) to estimate the coefficients in Equation 1. This enables measuring the patent fragmentation index’s marginal effect on market value to evaluate its degree and direction. To ensure the validity of the empirical research findings and avoid pseudo-regressions, the variable settings are changed in a robustness text. NLS and time-fixed effects regression methods are used to determine whether the regression results remain significant. The robustness test model is given in Equation 2:

Variable Descriptions and Definitions

Dependent Variable

The dependent variable, firm market value, is measured using Tobin’s Q. Relative to other financial performance indicators like return on assets, Tobin’s Q is more sensitive to market responses and captures a firm’s economic value (Bloom et al., 2013; Entezarkheir, 2019; Griliches, 1981; Hall et al., 2005).

Independent Variable

Shapiro (2000) systematically formulated the patent thickets theory. Therefore, this study identifies the patent thicket characteristics of high-tech companies using the following three aspects of Shapiro’s definition of patent thickets. They have (1) a high number of patents; (2) their patent assets refer to numerous other patents, which represent the follow-up innovation of the referenced patents and form a complementary relationship; and (3) the enterprise patent references are owned by multiple patentees, meaning that complementary patents are dispersed. Therefore, combining Shapiro’s (2000) study on the characteristics of patent thickets and referring to the patent fragmentation index proposed by Ziedonis (2004), we measure the density of patent thickets, as shown in Equation 3.

Cite indicates the number of patents cited by a high-tech enterprise. The fraction’s numerator in Equation 2 shows the number of patents of other patentees quoted by firm i in year t, while the denominator indicates the total number of patents that firm i quotes in year t. This ratio is then squared, summed across all j patentees, and subtracted from one to measure fragit. If firm i quotes only the patents of one patentee, the numerator and denominator are equal, which makes the indicator equal to zero. This indicates that the required complementary patents in the high-tech field are concentrated in the hands of one patentee. The lower the value, the more comprehensive the patent rights of that high-tech enterprise in the technology field. The larger the value, the more scattered the patent rights, and the more serious the patent thickets. In this case, the patents held by a high-tech enterprise are unlikely to cover the entire industrial chain.

Control Variables

Based on Hall et al. (2005), the perpetual inventory method calculates an enterprise’s patent and patent citation stock. The total number of granted patents for both inventions and utility models is used to measure enterprise patent assets. The stock of patent assets, INTAstockit, equals the number of patents granted in the previous period discounted to the current period plus the number of patents granted in the current period, as shown in Equation 4:

The stock of patent citations is the number of patents cited in the previous period discounted to the current period plus the number of patents cited in the current period, where δ equals 15%. Referring to Entezarkheir’s (2019) main approach, R&D intensity (RDstock/TA), patent cumulative intensity (patstock/RDstock), and patent citation intensity (citestock/patstock) indicators are used as the main control variables. In addition, the logarithm of the firm’s Herfindahl index (log(HHI)) is included as a control variable. The descriptions of the main variables are shown in Table 1.

Variable Descriptions.

Data Sources

The study sample is drawn from listed companies involved in China’s computer, communication, and other electronic equipment manufacturing industries. A secondary technical classification of the manufacturing industry published by the Securities and Futures Commission in 2012 includes 419 companies on the Science and Technology Board, Main Board, Growth Enterprise Market, and Small and Medium Size Board and excludes ST companies. The Chinese patent system is unlike the U.S. one in that no available database specializes in patent citations. Consequently, obtaining the patent citation data of Chinese companies, especially information about specifically cited patent owners, is complex and the biggest obstacle to studying the patent thickets of Chinese companies. The data for this study were obtained from the Derwent Patent Database, the largest patent database in the world; it includes not only all countries’ patent data but also patent citation data. Since there is a lag between patent grants and patent citations, and the Chinese patent system stipulates that the minimum period from patent application to grant is 2 to 3 years, data from 2009 to 2017 are used in this study. To measure each year’s patent thicket indicators, thousands of observations for the 419 enterprises were collected over nearly 10 years, and each enterprise was mined using patent text mining. Because no specialized database exists for patent citations by the patentee, to calculate the patent fragmentation index (frag) and measure patent thicket density, patent text mining must be used to extract patent citation information from the sample firms’ patent literature, patent text mining methods can identify valuable patent information by analyzing the content of a large number of patent documents. For example, mining the text of a patentee cited in an enterprise’s patent literature can identify the name of the patentee, specific patent information cited by the patentee, and other information to clarify the enterprise’s citations by other patentees (Li & Yuan, 2023; Yuan & Li, 2020). Each company’s patent fragmentation index and patent citation stock were individually measured using the perpetual inventory method and based on the number of patents of all patent owners cited by the company each year. Financial, R&D, and Herfindahl index data were collected from the Cathay Capital (CSMAR) database. The empirical analysis was conducted using Stata 17.0.

Notes: Stata 17.0 is a powerful statistical analysis software. It provides a wealth of data analysis, management, and visualization tools that can be used in academic research, business analysis, government decision-making, and many other fields. It has a wealth of analytical methods, including descriptive statistics, NLS regression analysis, panel data analysis, elasticity analysis, least squares, and other statistical analysis methods needed for this paper. It also has powerful data management functions to import, clean, organize, and convert data, such as for merging multi-source data, processing missing values, and other operations. It can generate high-quality charts and graphs, including line graphs, quantile graphs, etc., which are needed for this study (https://www.stata.com/).

Empirical Results

Descriptive Statistics

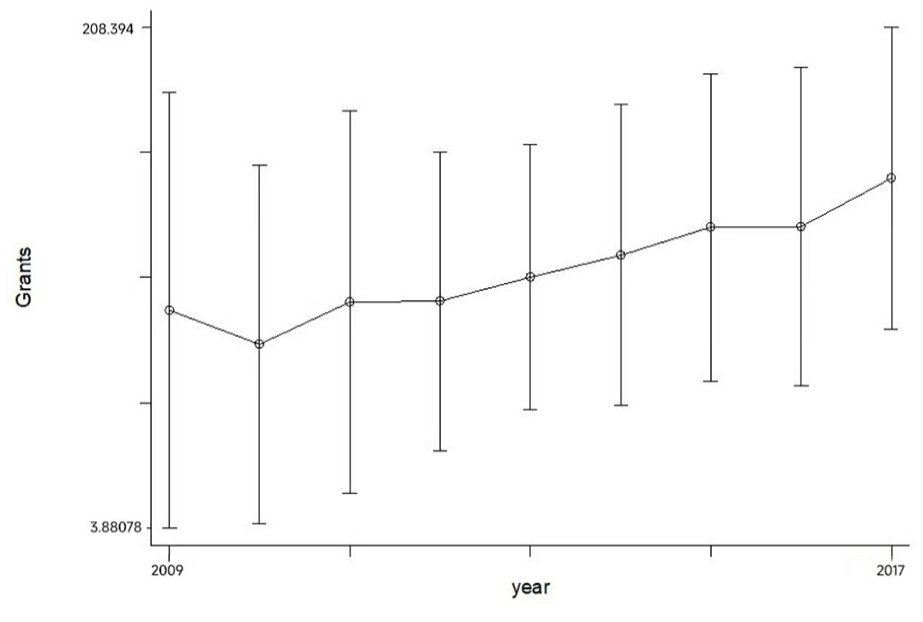

Table 2 reports the descriptive statistics. Due to the late development of China’s patent system and lagging and missing patent data values, 2009 to 2017 was used as the study period. The sample includes 1,125 observations. The statistics show that the maximum and minimum values of frag are 1 and 0.5, respectively, indicating that different patent owners hold many complementary patents. Thus, patent fragmentation is quite apparent, and patent thickets are very dense. The average number of patents granted over the years is shown in Figure 2. From 2009 to 2017, the average number of patents granted in China increased, with more than 200 being granted yearly.

Descriptive Statistics.

Trend of average patents granted (2009–2017).

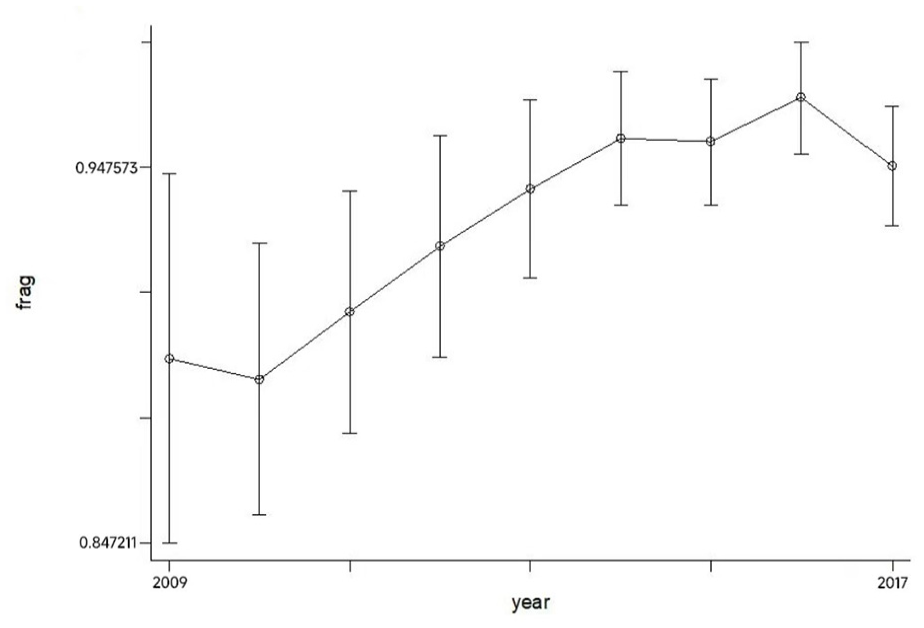

Stata 17.0 was used to carve out the evolution of the sample enterprises’ average frag from 2009 to 2017 to study the trend of patent thicket changes, as shown in Figure 3. The figure shows an upward trend in the sample enterprises’ patent frag; the rate rises increasingly yearly, with a maximum average value close to 0.9.

Trend of average patent fragmentation index (2009–2017).

The increase in frag reflects several factors. The rapid development of high-tech enterprises in China, the increase in the awareness of intellectual property protection, and the recognition by enterprises that patents are vital intangible assets have led firms to realize that they must have more patents for their patent strategy or R&D design to be competitive. The increase in the number of complementary patents indicates a trend of technology fragmentation in the industrial chain. Consequently, any enterprise will struggle to obtain a concentration of patents in a given technology, let alone all of them. A single patent owner only enjoys the right to use a patent without the ownership. Moreover, the realization of products and technological innovations is too dependent on patent rights cooperation. Patent thickets tend to be dense, and enterprises that compete in a dense patent thickets environment face the risk of marketization and encounter patent risks such as litigation, licensing, patent negotiation, and technology mergers and acquisitions.

Empirical Results

Patent Thickets and Firm Market Value

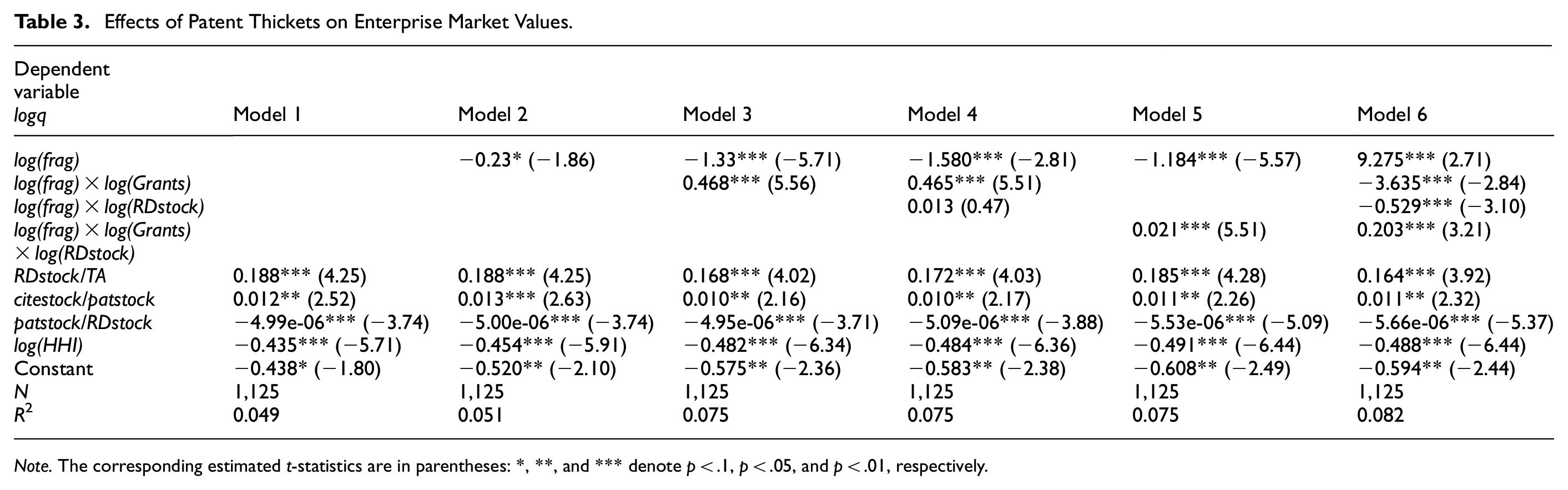

This study uses NLS, as proposed by Ziedonis (2004), to analyze the mechanisms through which patent thickets influence enterprise market value from 2009 to 2017. The regression coefficients are estimated using Equation 1, and the results are shown in Table 3. Hierarchical regression is adopted to avoid model collinearity and mutual interferences by other variables. First, after the explanatory variable log(frag) is added to Model (2), as shown in Column 3 of Table 3, its regression coefficient is −0.236 (p < .1), indicating that patent thickets hurt enterprise market value. Tobin’s Q decreases by 23% for every 1% expansion in patent thickets. This indicates that the denser patent thickets are, the lower an enterprise’s market value. This finding supports Hypothesis 1. In the long run, firms tend not to invest or innovate technologically in patented thickets-intensive technology areas because they will encounter obstacles from multiple patent owners, which affects their market value. Consequently, they prefer market-based competitive means, such as price wars and mergers and acquisitions, to avoid patent risks, indicating that the results for H1 also support the findings of the UK Intellectual Property Office (2013).

Effects of Patent Thickets on Enterprise Market Values.

Note. The corresponding estimated t-statistics are in parentheses: *, **, and *** denote p < .1, p < .05, and p < .01, respectively.

The Inhibitory Effect of Firm Patent Assets and R&D Stock

The results of the test for the inhibitory effects of firms’ patent assets and R&D stock are presented in Table 3. In Models (3) and (5) in Table 3, the log(frag) × log(Grants) and log(frag) × log(Grants) × log(RDstock) interaction terms are all positive and significant at the 1% level. In Model (3), the coefficient of log(frag) is −1.337 (p < .01), and that of the interaction term log(frag)xlog(Grants) is 0.468 (p < .1), showing that the inhibitory effect of patent assets plays a significant role. The more patents an enterprise owns, the more complementary patents it requires, which increases its patent fragmentation index. Holding a larger number of patents allows an enterprise to carry out subsequent innovations and guards against patent risks. Market competition can solve the patent thickets problem and enhance the market value of companies through patent behaviors. Instead of employing more commercialization means, such as mergers and acquisitions, market transactions, and price reductions, enterprises pay more attention to patent strategy and technological innovation. This is consistent with the conclusion reached by Entezarkheir (2016), thus supporting H2.

The regression results of Model (5) in Table 3 show that the regression coefficient of log(frag) is −1.184 (p < .01), while that of the interaction term log(frag) × log(Grants)× log(RDstock) is 0.021 (p < .01). These results indicate that enterprise R&D strength has a promotion effect on patent output. Patents produced through R&D do not incur additional costs and are more easily utilized by enterprises than patents from other sources. This is conducive to concentrating enterprises’ complementary patents while avoiding dormant and invalid patents. This allows enterprises to pay more attention to R&D, which is fundamental for coping with patent thickets. The regression results thus support H3.

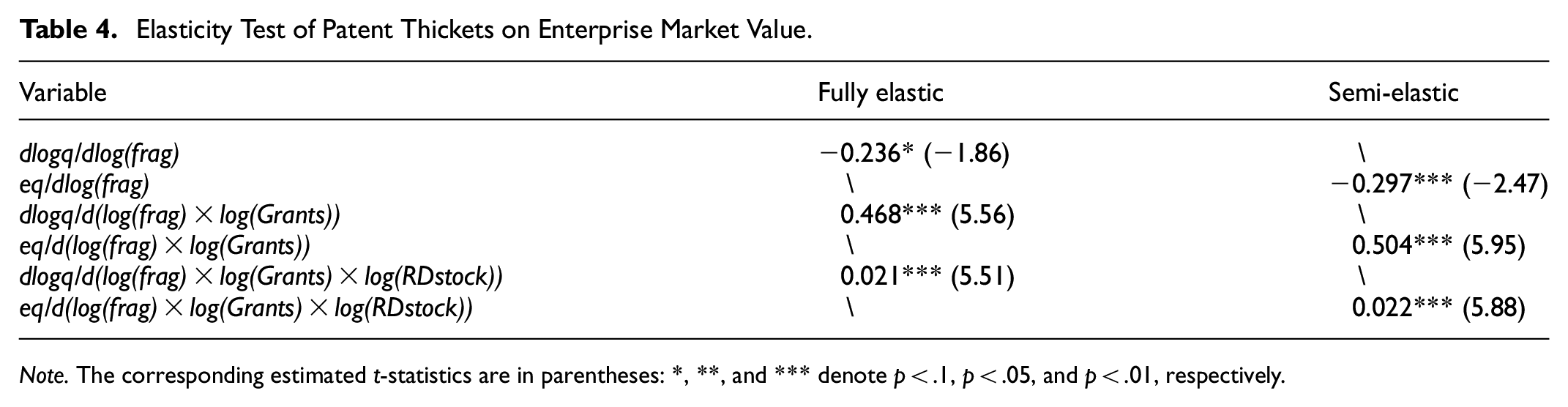

Stata 17.0 is used to measure the semi-elasticity coefficients of log(frag) × log(Grants) and log(frag) ×log(Grants) × log(RDstock) and analyze their direct marginal effects on market value. Table 4 reports the direct marginal effects on market value. The direction and significance levels of the semi-elasticity coefficients are consistent with the findings in Table 4.

Elasticity Test of Patent Thickets on Enterprise Market Value.

Note. The corresponding estimated t-statistics are in parentheses: *, **, and *** denote p < .1, p < .05, and p < .01, respectively.

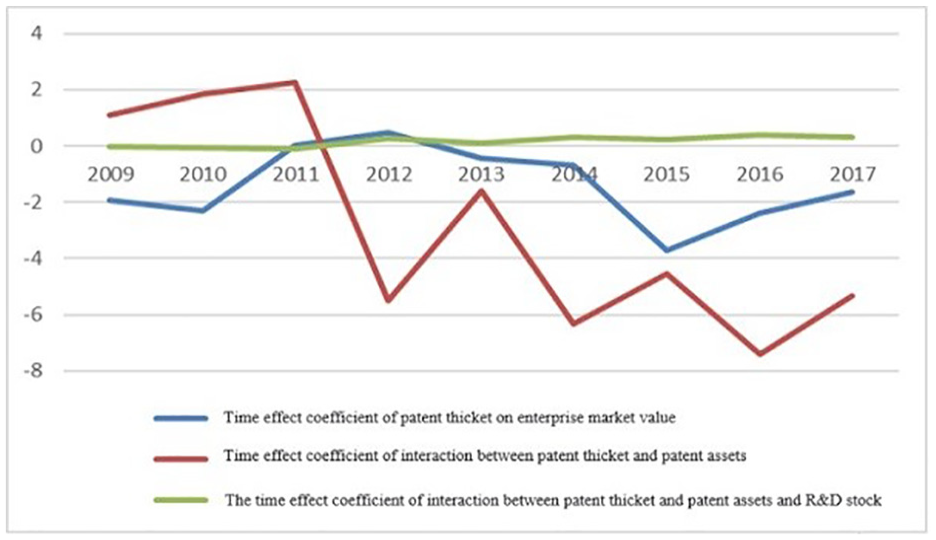

Since China’s patent system started after those in Western countries, enterprises have experienced a certain lag and time effect between applying for patents and using them to compete in the market. Therefore, the impact of patent thickets on enterprises in China differs from that in the U.S. The U.S. accumulated numerous patents earlier, and its market transformation and commercialization using an R&D system is more mature. Many complementary and basic patents exist; patent thickets have an obviously negative influence, while their impact on enterprises in China is relatively slow. To observe the time trend of patent thickets’ impact on firm market values and the inhibitory effect of patent assets and R&D stock, Stata 17.0 is used to depict the time trends of the regression coefficients of log(frag), log(frag) × log(Grants), and log(frag) × log(Grants)× log(RDstock). The graph is shown in Figure 4.

Time effect of patent thickets on market value of enterprises.

Figure 4 shows a significant time effect in patent thickets. The coefficient change interval is negative, indicating that as time passes, patent thickets gradually have a more negative influence on enterprise market value. The coefficient values become increasingly smaller, indicating that the impact patent thickets have in impairing enterprise market values is becoming more prominent every year. Moreover, the marginal negative effect also increases. The more it increases, the more prominent the influence of patent thickets on enterprise development in China. The coefficient of the joint influence of patent assets and R&D stock on the patent fragmentation index is positive with an upward trend. This confirms that enterprises must engage in effective R&D, develop more patents to cope with patent thickets and improve their development. The roles of patents and R&D will become increasingly crucial for future enterprise development.

Robustness Tests and Further Analysis

Robustness Tests

To ensure the research findings are reliable, we employ multiple regression methods, including NLS and panel fixed effects, and then compare the results. The variables in the model are first adjusted according to Equation 4 and then tested using NLS. The Hausman test is performed to reduce the endogeneity problem in the panel data and to consider the individual differences in the data. The result is a rejection of the original hypothesis. Therefore, a more suitable fixed effects model is considered under the same conditions. The robustness test results are presented in Tables 5 and 6. The regression results show that the coefficient of log(frag) is negative and significant at the 1% level. The log(frag) ×log(Grants) and log(frag) × log(Grants) × log(RDstock) interaction coefficients are positive and significant at the 1% level. Consequently, the results in Tables 5 and 6 support the three theoretical hypotheses, indicating that the research findings are valid and reliable.

Robustness Tests.

Note.*, **, and *** denote p < .1, p < .05, and p < .01, respectively.

Robustness Test Using the Modified Regression Method.

Note.*, **, and *** denote p < .1, p < .05, and p < .01, respectively.

Further Analysis

Quantile regression is employed to more clearly analyze the differences in how patent thickets impact the various market value levels of China’s high-tech enterprises and the intrinsic logical relationship between patent assets, patent thickets, and enterprise market value. This study argues that in a patent-intensive environment, the inhibitory effect of patent assets on patent thickets and firm market value is more significant for firms in the middle and high market value quantiles. Different enterprise market-value quantiles reflect the differences in patent thicket impact; thus, each quantile’s market value can provide a comprehensive picture of how the potential and strength of an enterprise’s market value are distributed. Quantiles reflect the marginal impact of patent thickets at different market value levels. Table 7 and Figure 5 show that the quantile regression results based on bootstrap standard errors and the coefficients of log(frag) move from the low to high ends of the conditional distribution, first increasing and then gradually decreasing, showing a relatively complex inverted U-shaped curve. Figure 5 shows that the coefficient of log(frag) is −1.159 in the 0.2 quantile and peaks at −2.038 in the 0.5 quantile; after the 0.6 quantile, it begins to shrink. A possible explanation is that firms at higher tertile points deliver more favorable news to the market, attracting more investors and being bullish about the future; at the same time, they are subject to patent thickets and experience more patent risk. However, patent thickets have a critical mass effect as the role of patent asset protection increases. When the tertile point breaks through a particular value and further increases, enterprises will inevitably increase the protective effect of patents to maintain their competitive advantage and alleviate the constraints imposed by patent thickets. This will alleviate the negative impact of patent thickets.

Quartile Regression Results Based on Patent Assets.

Note.*, **, and *** denote p < .1, p < .05, and p < .01, respectively.

Quartile regression results graph.

Discussion

In this study, patent thickets are considered the result of an imbalance in the allocation of resources to corporate technological innovation. From an enterprise’s internal point of view, if its patents or R&D stock are insufficient, and it does not hold all required patents, innovations will fail, or products will not be produced smoothly, thus wasting the enterprise’s R&D resources. Also, the business will incur additional costs, reducing its market value. Table 7 and Figure 5 show that firms in the middle and higher market value quantiles can amplify this negative effect better. Previous studies (Entezarkheir, 2016; Hsu et al., 2022) and Table 3 support the conclusion that patent thickets lower firm market value. Table 3 and Figure 4 show that the negative effect of China’s patent thickets on enterprise market value is more evident than that of U.S. patent thickets. In the future, the four reforms of China’s patent law may produce a “blowout” in patent volume.

As important intangible resources, patents can effectively promote enterprise market values. At the same time, patent thickets may lead to a mismatch of innovation resources, creating a “tragedy of the anti-commons” (Heller & Eisenberg, 1998). Resource allocation theory suggests that organizations must optimize their resource allocations to maintain sustained competitiveness (Wang et al., 2023). However, few studies have addressed the synergistic allocation of the two resources. Moreover, little research has explored whether the allocation of intangible resources, such as patent assets and R&D stock, can correct the resource mismatch formed by China’s patent thickets and increase the market values of Chinese high-tech enterprises (Kiselev et al., 2020). This study’s empirical results show that the interaction coefficients of log(frag) × log(Grants) and log(frag) × log(Grants) ×log(RDstock) are positive and significant at the 1% level. This suggests that holding a certain amount of patent assets can correct the resource mismatch caused by patent thickets; this is driven by enterprises having a certain scale of R&D stock. Moreover, the allocation of these two kinds of enterprise intangible resources should be synergistically optimized.

This unique finding distinguishes this study from previous literature. Further analysis shows that the interaction coefficient of log(frag) × log(Grants) is positive for firms in the middle and high market-value quantiles. It is larger than firms in the low market-value quantiles and significant at the 1% level. This suggests that the higher a firm’s market value, the more critical it is to hold and optimize its patent asset allocation. This is likely due to the economies of scale that develop as a business increases its cash flow. As cash flow increases, firms invest more resources in innovation, produce more patents, have greater demand for patents, and increase the efficiency with which they use patents. As companies acquire more patents, patent protection improves, helping them cope with patent thickets. This is another unique finding of this study.

Conclusions and Managerial Implications

Conclusions

This study examines how patent thickets impact the market values of high-tech enterprises in China. We further investigate the inhibitory effect of firms’ patent assets and R&D stock on the negative impact patent thickets have on high-tech firms’ market values. The study’s innovations and theoretical and practical contributions are as follows. First, previous studies have focused on how patent thickets impact enterprise market values in the U.S. and Europe, while few studies consider Chinese high-tech enterprises (Entezarkheir, 2019; Ziedonis, 2004). To fill this gap, this study explores the patent thickets of Chinese high-tech enterprises. The empirical analysis shows that patent thickets also negatively affect the market values of Chinese high-tech enterprises; this result is significant at the 1% level, supporting Ziedonis’s (2004) findings. However, over time, this negative effect has become more potent than that in the U.S., likely due to the four reforms of China’s patent law and the “blowout” phenomenon of patent volume. As necessary intangible resources, patents can effectively increase firm market value. However, patent thickets may lead to a mismatch of innovation resources, forming a “tragedy of the anti-commons” (Heller & Eisenberg, 1998).

Second, few previous studies have dealt with inhibiting the effects of patent thickets (Paik & Zhu, 2016). This study adds patent assets to study the inhibition of patent thickets. Resource allocation theory suggests that the effective allocation of a firm’s resources can produce sustained development and improve firm performance (Wang et al., 2023). However, the impact of intangible resource allocation has been ignored. Patents are considered critical unlimited enterprise resources, which raises the question: Can Chinese high-tech enterprises holding patent assets correct the imbalance in patent resource allocation formed by patent thickets that lead to a loss in enterprise market value? One innovation of this study is its integration of patent thickets, patent assets, and the market value of Chinese high-tech firms into one framework. The study shows that the more patents an enterprise holds, the more it can suppress the negative influence of patent thickets. In addition, having more patents helps the firm cope with patent thickets, improves its position for patent negotiation in competition, helps it develop patent designs, and improves its performance. For example, Mobike, OFO, and other shared bicycle companies were caught in multiple lawsuits regarding locking technology patents, which affected their enterprise market values. In comparison, the performances of ZTE and Huawei in the U.S.-China trade war involving patent infringement are steady; notably, these Chinese high-tech enterprises have large volumes of patent assets.

Third, resource allocation theory studies have focused more on single-asset allocation and neglected dual-asset allocation’s synergistic effect (Kiselev et al., 2020). Furthermore, all previous studies on inhibiting patent thickets were conducted from a single-factor perspective. Patent assets can be acquired through various channels, including legal aspects like purchases, licensing, and transfers, or by firms conducting R&D and applying for patents for their technological achievements (Entezarkheir, 2017; Niwa, 2018). A firm’s R&D stock is a fundamental factor in patent acquisition (Lee et al., 2018). Another innovation of this study is using the interaction of corporate patent assets with R&D stock to study their inhibitory effect on patent thickets’ negative impact on enterprise market value. This innovation reveals the factors that can drive internal corrections of the imbalance in resource allocation caused by the patent thickets of China’s high-tech enterprises, as well as the factors that drive the acquisition of patent assets. This study uses the joint effect of patent assets and R&D stock on patent thickets to study their two-factor inhibition of patent thickets. Companies with strong R&D have more patent assets, enabling them to fight patent thickets and increase their market value.

Managerial Implications

The study findings have the following implications for managers. First, enterprises should effectively focus on complementary patents that meet the required characteristics. They should systematically integrate and innovate products and technologies and adopt diversified technology models. Firms should vigorously apply technology penetration to manufacturing, finance, commerce, industry, and other fields for future technology integration.

Second, firms should concentrate on the patent design of key technologies in their industrial chain. They should concentrate these patents in the hands of the enterprises themselves and respond to patent thickets using patent strategies to establish the technology industry as a complete chain, making coverage of individual enterprise patent rights more complete. In addition to acquiring patents through legal channels, firms should focus on improving their R&D levels to produce more patents. Avoiding paying additional fees for patents reduces costs and improves enterprise innovation and competitiveness.

Third, to minimize the risk of patent thickets, companies could introduce ex-ante dispute settlement mechanisms while negotiating for patent acquisitions, such as in patent purchases. Relevant settlement mechanisms can also be negotiated and established when patent risks like infringement, product income, and patent commercialization emerge. These include ex-ante patent licensing, measures for allocating the achievements and benefits obtained through cooperative R&D, and patent sharing. Relying on the dual incentive measures of technology promotion and market pulling can jointly cope with the influence of increasingly prominent patent thickets on enterprises in China.

Limitations and Future Research

One limitation of this study is that the research sample is composed of 419 high-tech enterprises in China. This negative effect of patent thickets is evident in China in traditional manufacturing industries; however, the results of patent thickets studies in other fields or countries may vary. For example, enterprises in developed countries may, by virtue of a large number of patents in core technology areas, form technical standards and extend the period of market exclusivity through the patent thickets strategy. In this way, they consolidate their high-end position in the global industrial chain, reap high profits and promote industrial upgrading instead. Qualcomm, a U.S. company, dominates the thickets of communication technology patents and participates in standard-setting, creating patent barriers that, in turn, enhance the company’s market value. The patent thickets built around Humira by pharmaceutical giant ABBV.US have shielded it from biosimilar competition in the U.S. market for two decades, generating more than $200 billion in cumulative revenues. In some emerging technology areas such as generative artificial intelligence, gene editing, etc., although the negative effect of the patent thickets may not be very obvious, the formation of patent barriers will significantly increase the innovation threshold of the latecomers. Enterprises will make it more difficult to obtain subsequent patents to avoid infringing on others’ patents, which may discourage some small businesses or start-ups from innovating. Therefore, the generalizability of the conclusions and policy recommendations to other enterprises may be limited; in the future, research could be conducted on a sample of different industries or regions of the country to enhance the broader relevance of the patent thickets Study. Besides, This study explores the two regulating mechanisms through which patent thickets affect enterprise market values. Future research should explore mediating mechanisms and other regulating factors to help China’s high-tech enterprises cope with patent thickets in a more targeted way. In addition, the patent thicket index in this study is based solely on the patent fragmentation index proposed by Ziedonis (2004); additional patent thicket indexes should be developed in the future.

Footnotes

Acknowledgements

The author is grateful to the insightful comments suggested by the editor and the anonymous reviewers.

Ethical Considerations

Ethical approval does not apply to this article. Because this article does not contain any research involving humans or animals.

Author Contributions

Kai Luo: Conceived the study, collected data, analyzed results, wrote the initial draft, revised the manuscript. Jia Ren: Contributed to text revision, wrote the draft, analyzed results, revised the manuscript. Yibo Wang: Formatting revisions, suggested revisions. Jun Wan: Suggested revisions, supervised the study.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by National Natural Science Foundation of China: Grant no. 71902151 and The Humanities and Social Sciences Project of Hubei Provincial Education Department: Grant no. 23Q104 and Hubei Provincial Social Science Foundation: Grant no. HBSKJJ20243278.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The original contributions presented in the study are included in the article, further inquiries can be directed to the corresponding author.