Abstract

Good ESG and enterprise innovation performance are significant drivers of high-quality economic development. Utilizing data from A-share listed companies in Shanghai and Shenzhen from 2009 to 2022, this paper employs regression analysis to explore the impact of ESG performance on enterprise innovation performance and its multiple mechanisms. The research findings indicate that ESG performance significantly enhances enterprise innovation performance, with the E (Environmental) dimension having the greatest promotional effect, followed by the G (Governance) dimension, and the S (Social) dimension coming last. These conclusions remain valid after a series of robustness checks. Regarding mechanisms, ESG performance primarily promotes enterprise innovation by improving internal control quality, alleviating financing constraints, and increasing government R&D subsidies. Heterogeneity tests reveal that the impact of ESG performance on enterprise innovation performance is more pronounced in non-state-owned enterprises, high-innovation-performance enterprises, non-heavy-pollution enterprises, growing enterprises, and central and western regions enterprises. This paper further enriches the research on the economic consequences of ESG performance and provides insights for enterprises to adopt ESG principles and actively enhance their innovation performance.

Keywords

Introduction

Since the 21st century, the continuous advancement of science and technology has brought tremendous convenience to people’s lives. However, societal issues such as climate change, energy crises, and environmental pollution have concurrently emerged. These challenges interact and collectively shape human survival and development, placing sustainable development at the forefront of global concern. In 2004, the UN Global Compact introduced the Environmental, Social, and Governance (ESG) framework to the public. Defined by the initials “Environmental,”“Social,” and “Governance,” ESG represents an investment philosophy and corporate evaluation criterion that focuses on a company’s performance in environmental stewardship, social responsibility, and governance practices. It serves as a response to pressing societal issues and as a guiding investment philosophy crucial in promoting social, environmental, and sustainable development. This framework encourages investors to pursue economic efficiency while assuming social responsibilities, prioritizing environmental protection and corporate governance to achieve a fairer, greener, and more sustainable future. ESG performance is a comprehensive assessment derived from rating a company’s effective actions in environmental, social, and governance domains, reflecting the tangible outcomes of its ESG-related investments and initiatives. With increasing attention from both academic and practical spheres, research on the value effects of ESG performance has emerged as a prominent area of inquiry (Sandberg et al., 2023; Tampakoudis & Anagnostopoulou, 2020; Zheng & Bu, 2024).

In recent years, remarkable progress has been achieved in China’s innovation-driven development. Within this context, enterprises are recognized as key entities in deeply implementing the innovation-driven development strategy. Enterprise innovation not only maintains competitive advantages, enhances corporate reputation, and boosts operational performance (Liao, 2018; Peng & Tao, 2022; S. Wang et al., 2022) but also further improves total factor productivity and drives high-quality development (Liang & Zhang, 2024; Xiao et al., 2022). Enterprise innovation performance (EIP), measured by the outcomes and effectiveness of a firm’s innovative activities, is considered a critical indicator for evaluating its creative capabilities and the efficiency of its innovation initiatives (Prajogo & Ahmed, 2006). Therefore, investigating strategies to enhance EIP carries significant research and practical implications.

With the extensive attention given to the relationship between ESG performance and EIP in the academic community, many studies have been conducted on this relationship. Generally speaking, many scholars have affirmed that ESG performance has a positive impact on EIP (X. Sun & Xiong, 2025; Wu et al., 2024; H. Zhang et al., 2024), and it has been found that factors such as the supply chain relationship stability (L. Ren et al., 2025) and employees’ organizational identification (Wu et al., 2024) are important mechanisms through which ESG performance affects EIP. Factors such as firm age, property rights nature, and technological level can significantly moderate their relationship (Wan et al., 2024; C. Zhang & Jin, 2022). However, three areas still need to be expanded in the existing research. Firstly, the existing literature has paid more attention to external moderating factors such as firm size (Feng et al., 2025) and institutional environment (M. Wang et al., 2024) or exploring the indirect impacts of ESG performance on corporate value (Qian, 2024; W. Tan et al., 2024), corporate performance (Zheng & Bu, 2024), and corporate downside risk (Lin & Li, 2024) through the mediating effect of enterprise innovation. Nevertheless, a systematic explanation for how ESG performance affects EIP has not been formed. This leads to a lack of pertinence when enterprises formulate strategies and policies, making it difficult for them to effectively drive the improvement of EIP through ESG practices. Secondly, most studies regard ESG as an overall concept, ignoring the differential impacts of the environmental, social, and governance dimensions on EIP. The heterogeneous effects of these internal elements have not been fully revealed, which limits the in-depth understanding of the impact of ESG performance on EIP. Thirdly, some studies focus on specific industries such as new energy (M. Wang et al., 2024), manufacturing (Shan et al., 2025), and traditional energy (M. Ren et al., 2024). Although they have deepened the impact analysis within the industry context, the generalizability of the research conclusions is limited. Transferring these conclusions to other industries, such as service and traditional manufacturing, is difficult, creating a theoretical gap for cross-industry comparisons.

Given this, this study takes Chinese listed companies on the Shanghai and Shenzhen A-share markets as the research objects. Based on theories such as stakeholder and resource-based theories, it attempts to deconstruct the mechanism through which ESG performance affects EIP from a dual perspective. On the one hand, starting from the governance effect, it examines how ESG performance promotes EIP by enhancing internal control (IC). On the other hand, from the perspective of the resource effect, it analyzes how ESG performance affects EIP by alleviating financing constraints (FC) and increasing government R&D subsidies (GRDS). At the same time, this paper further explores the heterogeneous impacts of the three dimensions (environmental, social, and governance) of ESG performance on EIP, aiming to break through the limitations of the holistic nature of existing research. The research contributions of this paper are reflected in the following aspects. Theoretically, it expands the research on the micro-mechanisms of the relationship between ESG performance and EIP and enriches the analytical framework for cross-dimensional comparisons. At the practical level, it provides decision-making references for enterprises to implement ESG strategies in a differentiated manner and helps them systematically improve EIP by actively practicing the ESG concept, thus achieving the integration of the goal of high-quality corporate development.

Theoretical Foundation and Hypothesis Development

ESG Performance and EIP

Corporate ESG practices fundamentally represent a strategic choice for achieving sustainable development by aligning the demands of multiple stakeholders. Previous studies have found that good ESG performance can effectively reduce a company’s debt costs (Mathath et al., 2024), thereby decreasing the risk of default (Atif & Ali, 2021). ESG advantages can also enhance corporate value by reducing information asymmetry among investors and agency costs (Yu et al., 2018). As posited by stakeholder theory, enterprises balance the economic and social interests of shareholders, employees, governments, communities, and other stakeholders (Freeman, 2010). This balance fosters stable internal and external operational environments and supports corporate innovation by integrating resources and relationship networks. Regarding environmental responsibility, enterprises’ proactive engagement in resource conservation and environmental protection enhances managers’ ecological awareness, prompting optimized resource allocation and increased investment in green technology R&D and sustainable solutions. These actions establish a technical foundation for innovation activities while mitigating environmental risks (Y. Tan & Zhu, 2022; Velte & Stawinoga, 2020). In social responsibility, active fulfillment of social obligations strengthens employees’ emotional commitment to the organization, stimulates their innovative motivation, and attracts and retains top talent for innovation initiatives (Mbanyele et al., 2022; T. Zhang et al., 2024). A strong social responsibility profile attracts high-skilled personnel and access to diverse innovation resources through deepened collaboration with external stakeholders, cultivating human capital and network advantages for innovation (Bereskin et al., 2016; Paruzel et al., 2023; Tamimi & Sebastianelli, 2017). From a corporate governance perspective, a robust structure reduces information asymmetry between management and shareholders and curbs opportunistic behavior, creating an endogenous incentive mechanism that prioritizes long-term value creation. This encourages managers to embrace innovation risks and resist short-term performance pressures that might otherwise reduce R&D investments, thus ensuring scientific rigor and sustainability of innovation decisions. Rooted in dynamic capability theory, corporate ESG practices are fundamentally strategic choices that drive improvements in innovation performance by cultivating dynamic capabilities such as environmental sensing, resource reconfiguration, and organizational process optimization. The development and strengthening of these capabilities transform heterogeneous resources, including green technology reserves, reputation capital, and institutional advantages developed through ESG practices, into tangible innovation outcomes. Based on this theoretical logic, the following hypotheses are proposed:

The Mediating Role of IC

Institutional theory posits that an organization’s institutional arrangements must align with internal and external environments to achieve effectiveness. IC is a mechanism through which enterprises aiming to achieve operational objectives formulate systems, procedures, and methods to restrict, regulate, and manage internal economic activities. As a core institutional framework within enterprises, improving the quality of IC is contingent on the institutional environment fostered by ESG practices. Internally, the transparent governance and accountability culture advocated by ESG provides a values-based foundation for IC, reducing resistance to its implementation. Externally, firms with strong ESG performance are more likely to obtain governmental policy support, investor trust, and recognition from social oversight (Hao & Wu, 2024; Meng et al., 2023). This institutional support minimizes external costs associated with IC operations, enabling a greater focus on risk control and resource optimization. High-quality IC influences corporate innovation performance through three mechanisms. First, given the long cycles and high uncertainty inherent in innovation activities, the risk assessment and monitoring mechanisms within IC systems can track innovation progress in real time, promptly identify technical bottlenecks or resource allocation issues, and adjust strategies to ensure innovation projects proceed as planned (Chan et al., 2021). Second, by designing appropriate incentive and oversight mechanisms, IC alleviates myopic behavior arising from principal-agent problems, preventing managers from reducing R&D investments in pursuit of short-term profits (W. Li et al., 2011). Third, standardized information disclosure under IC reduces information asymmetry between internal and external stakeholders, enhancing investor confidence in the firm’s innovative potential and indirectly improving the financing environment for innovation activities (Skaife et al., 2013; Zhou et al., 2024), thereby promoting enterprise innovation performance (EIP). Based on this reasoning, the following hypothesis is proposed:

The Mediating Role of FC

FC refers to situations where enterprises encounter difficulties in obtaining funds, face high costs, or are limited in the scale of financing due to factors such as information asymmetry, credit risks, or market imperfections. The Resource-Based Theory views financing capability as a core competence for enterprises to acquire critical external resources, and ESG performance enhances this capability through signaling theory mechanisms: the disclosure of non-financial information on environmental management, social responsibility fulfillment, and corporate governance serves as a signal to the market about a firm’s high operational transparency and strong risk management capabilities (Nie et al., 2023). This signaling advantage reduces investors’ information collection costs and assessment risks, alleviating FC (Banerjee et al., 2020). From a governance perspective, the corporate governance dimension within ESG is closely associated with internal governance quality. A sound governance structure strengthens investor confidence in a firm’s long-term value by curbing managerial self-interest and improving resource utilization efficiency, making investors more willing to provide financial support for innovation activities (Hao & Wu, 2024). The impact of alleviated FC on EIP manifests itself in two ways. First, it directly ensures the continuity of R&D investments, preventing innovation project interruptions due to capital shortages. Second, it indirectly enhances the firm’s attractiveness to innovative talent: stable funding sources enable enterprises to offer competitive compensation and R&D conditions, reducing the loss of core personnel. Based on this, the following hypothesis is proposed:

The Mediating Role of GRDS

GRDS denotes the resource support provided by the government in the form of fiscal funds, tax incentives, and other means to eligible enterprises to promote their technological research and development, product innovation, and other innovative activities. Within the institutional theory framework, governments, as key institutional providers and resource allocators, significantly influence corporate innovation behavior through their policy orientations. Firms with strong ESG performance align with governmental goals of promoting sustainable development and public welfare by fulfilling environmental, social, and governance responsibilities, thereby gaining institutional preference in allocating GRDS (X. Zhang et al., 2023). Signaling theory further explains this process: ESG performance, as a non-financial signal, reduces information asymmetry between enterprises and governments, enabling governments to more accurately identify firms’ potential in green innovation, livelihood technologies, and other domains. It minimizes the screening costs of resource allocation (Luo & Wu, 2022) and increases the likelihood of enterprises receiving GRDS.

The promotion of EIP by GRDS is manifested in two aspects. First, it directly increases financial and resource support for R&D investment, technology acquisition, and innovative talent cultivation (Y. Zhang et al., 2023), enabling enterprises to expand the scale and improve the quality of innovation activities, thereby boosting innovative outputs and directly enhancing EIP (Xu & Xiao, 2024). Second, it acts as a leverage effect by facilitating industry-university-research collaborations to build innovation ecosystems, reducing innovation risks and enhancing innovative capabilities (Bronzini & Piselli, 2016). Based on the above, the following hypothesis is proposed:

Research Design

Sample Selection and Data Source

Annual data of Chinese A-share listed companies from 2009 to 2022 are selected as the analytical sample. HuaZheng ESG Ratings are employed to measure ESG performance because, within the ESG evaluation framework for Chinese listed companies, this rating system demonstrates outstanding advantages in constructing multi-dimensional indicators compared to other ESG ratings. It establishes a dynamically updated evaluation mechanism and develops a differentiated indicator system by deeply integrating China’s local market characteristics. Its evaluation scope has extended to all industrial sectors, showing significant advantages over international mainstream standards regarding data update frequency, indicator localization adaptability, and industry coverage completeness. The year 2009 is chosen as the starting point of the sample period due to the earliest availability of HuaZheng ESG rating data dating back to 2009.

Data are sourced from three databases: financial and ESG data of listed companies are obtained from Wind Information; corporate patent data are retrieved from the China National Research Data Service Platform (CNRDS); and data on the governance structure of listed companies are collected from the China Stock Market and Accounting Research Database (CSMAR). Additionally, a rigorous data screening process is implemented to construct the sample. Specifically, first, financial and insurance companies are excluded because their financial statement structures and business models differ significantly from those of other industries, potentially leading to biased research results. Second, listed companies labeled as “ST” or “*ST” are removed, as these firms typically face severe financial distress or operational issues, whose data may exert abnormal influences on research outcomes. Finally, listed companies with severe missing data in key variables (such as ESG scores and corporate patent data) are excluded to ensure data integrity and reliability. After screening, a final panel dataset consisting of 17,444 observations from 1,246 listed companies over 14 years is obtained. To mitigate the interference of extreme values, all continuous variables except ESG scores are winsorized at the 1% level.

Variable Measurement

The Explained Variable

This paper’s explained variable is EIP, primarily measured by indicators such as the number of patent applications, patent grants, and new product sales revenue. Given that the number of patent applications more directly and timely reflects the effectiveness of corporate innovation, this paper employs the number of patent applications to assess EIP. Additionally, considering that some firms have zero annual patent applications and this indicator exhibits right-skewed distribution, the natural logarithm of (the number of patent applications + 1) is used to measure EIP. In robustness checks, this paper also utilizes the number of patent grants and invention patent applications as measures of EIP.

The Explanatory Variable

ESG performance, as determined by the HuaZheng ESG rating, is the explanatory variable in this study. HuaZheng has conducted corporate ESG assessments longer than other third-party ESG rating organizations, and its rating encompasses all A-share listed firms. It has three dimensions: governance, social, and environmental, and is based on the realities of China’s capital market. From “C” to “AAA,” which correspond to scores of 1 to 9, companies are given a rating. A higher score indicates better ESG performance. Furthermore, this study considers using Bloomberg’s ESG rating for robustness assessments.

The Mediating Variables

Three mediating variables are identified in this paper: IC, FC, and GRDS. The Dibo IC Index for Chinese Listed Companies specifically quantifies IC. The index value is increased by one to quantify IC, and the natural logarithm is then calculated. The SA index developed by Hadlock and Pierce (2010), which is based on two exogenous variables—firm size and firm age—is the main tool used to measure FC. Higher final processed values indicate greater FC, which is measured in this paper using the absolute value of the SA index. GRDS is measured as the ratio of GRDS to total corporate assets, with 1 added to this ratio and the natural logarithm taken to quantify GRDS.

The Control Variables

Corporate innovation success is affected by several variables, including capital flow and business size. The following factors are chosen as control variables in this article to more thoroughly examine the relationship between ESG performance and EIP: firm size (SIZE), return on assets (ROA), debt-to-asset ratio (LEV), duality of CEO and COB (DUAL), firm growth (GROWTH), top shareholder concentration (TOP1), cash flow ratio (CF), and ownership nature of the enterprise (SOE). Furthermore, corporate innovation capabilities have changed significantly due to China’s recent rapid economic expansion, and firms in different industries have varying innovation capabilities. Consequently, this study uses year and industry as control variables in the regression analysis to guarantee the precision and scientific validity of the research findings. Table 1 lists the precise meanings of every variable used in this work.

Variable Definitions.

Source. Authors own work.

Empirical Model

Based on the preceding analysis, regression analysis is employed to construct the following models to test the direct impact of ESG performance on EIP and the underlying mechanisms. The choice of regression analysis as the empirical method is guided by three key considerations. First, the nature of the research question: this study aims to explore the effect of corporate ESG performance on EIP, a relationship involving multiple variables. Regression analysis effectively controls for interference from other variables, enabling the identification of the independent association between ESG performance and EIP, which is well-suited for testing the research hypotheses. Second, data suitability: the study constructs a 14-year panel dataset comprising 1,246 listed companies and 17,444 observations. The fixed effects model can capture both temporal and industrial variations simultaneously, addressing unobserved individual heterogeneity and enhancing the accuracy of estimation results. Third, methodological prevalence: regression analysis is widely used in this research field (Bagh et al., 2024; Broadstock et al., 2021), with a mature framework and easily interpretable results, ensuring the scientific validity of findings. Additionally, robustness and endogeneity tests are conducted to guarantee the reliability and validity of the research outcomes.

In these models, Model (1) examines the direct impact of ESG performance on EIP, while Models (2) and (3) test the underlying mechanisms through which ESG performance influences EIP. In these models, ESG represents ESG performance, Apply denotes EIP, Control signifies control variables, ∑Yeari,t accounts for year effects, ∑Industryi,t captures industry effects, and ε represents the random error term.

Empirical Results

Descriptive Statistics

SPSS statistical software is used to perform descriptive statistics on the data, as indicated in Table 2. The findings show that the explanatory variable, ESG performance, has a mean value of 4.051, with a minimum value of 1.000 and a maximum value of 8.000. It suggests considerable variation in ESG performance among different companies and room for improvement in ESG performance levels. The main cause of this discrepancy is that, despite recent increases in corporate involvement and policy support, as well as a growing interest in ESG, China’s ESG development is still in its infancy and confronts many obstacles. It is in contrast to developed nations like the US and Europe. The mean value of the dependent variable, EIP, is 2.635, with a standard deviation of 1.961, and the mean leans toward the minimum value, indicating that the EIP of the sampled companies is relatively low and there is potential for improvement.

Descriptive Statistics.

Source. Authors own work.

Correlation Analysis

In the correlation analysis results presented in Table 3, the primary variables in this paper are significantly correlated, providing preliminary validation of the proposed research hypotheses.

Correlation Analysis.

Source. Authors own work.

p < .05. ***p < .01.

Baseline Regression Analyses

Results for ESG Performance and EIP

This research uses regression analysis to look at how ESG performance affects EIP. Table 4 presents the results of the tests assessing this impact. As indicated in Column (1), the regression initially only includes the explanatory variable and controls for year and industry. The findings show that ESG performance significantly improves EIP (β = .462, p < .01). The calculated coefficient for ESG performance on EIP is 0.195, which is significant at the 1% level when controlling variables are added, as seen in Column (2). It demonstrates that ESG performance significantly enhances EIP, supporting Hypothesis H1. Additionally, the regression results in Columns (3) to (5) show that good E, S, and G performance all contribute to improved EIP, validating Hypotheses H1a, H1b, and H1c. Specifically, EIP benefits most from E, which G and S follow.

ESG Performance and EIP.

Source. Authors own work.

p < .1. **p < .05. ***p < .01.

The reasons are as follows: Firstly, under China’s “Dual Carbon” goals, stakeholders have placed higher demands on corporate environmental performance. To reduce pollution and enhance resource utilization, corporations must increase investments in innovation, engaging in green technological innovation and product development, thereby directly promoting EIP. Secondly, effective corporate governance structures ensure alignment between innovation direction and strategic objectives, supporting innovation activities through scientific decision-making and risk management. They also optimize resource allocation and capital investment, providing necessary resources for innovation. Lastly, while fulfilling social responsibility enhances corporate image and reputation, this enhancement is more evident in social image and brand value rather than direct EIP. In summary, among the ESG dimensions, the environmental dimension promotes EIP the most due to direct environmental pressures stimulating innovation vitality and driving green technology development. Corporate governance supports innovation through improved decision-making, resource allocation, and capital investment. While corporate social responsibility positively affects EIP, it is relatively smaller and more evident in long-term social benefits.

Results for the Mediating Effect Test

Table 5 shows the findings of the mediation effect test for IC, FC and GRDS. In particular, Column (1) indicates that, at the 1% significance level, the estimated coefficient of ESG performance on EIP is 0.195. At the 1% level, Column (2) shows that ESG performance significantly improves IC. The calculated coefficients for ESG performance and IC, respectively, are 0.186 and 0.043, both significant at the 1% level, when both are considered independent variables in predicting EIP, as shown in Column (3). These results imply that IC mediates the association between EIP and ESG performance to some extent, suggesting that EIP is promoted by ESG performance through improved IC. In addition, this study employed the same methodology to examine the mediating effects of FC and GRDS. The results, as presented in Table 5, demonstrate that both FC and GRDS have served as mediators.

Results of the Mediation Effect Test.

Source. Authors own work.

p < .1. **p < .05. ***p < .01.

Endogeneity Checks

The Instrumental Variable Method

Enhancing enterprise innovation capability may improve ESG performance, which has strongly influenced EIP in prior studies. As a result, the effect of ESG performance on EIP can have an endogenous problem of reverse causality. This work uses the instrumental variable (IV) method for robustness testing to overcome this. We choose the average ESG score of other businesses in the same sector and region (ESG_IV) as the IV for two-stage least squares (2SLS) regression by Long and Zhang’s methodology (Long & Zhang, 2023). The following justifies this decision: Previous research has demonstrated that peer effects are present in ESG performance (Z. Li & Li, 2023). Companies in the same industry and province often face similar geographical, cultural, policy, and market environments, and they may adjust their ESG performance based on the ESG performance of other companies.

Regarding homogeneity, there is no concrete proof that EIP is directly impacted by the ESG performance of other businesses operating in the same sector and region. Therefore, the IV ESG_IV satisfies the homogeneity and relevance conditions. The IV estimation results are shown in Columns 1 to 2 of Table 6. First, the first-stage regression findings are shown in Column (1), which validates the relevance assumption of ESG_IV as an IV by demonstrating that it significantly improves corporate ESG performance (β = .065, p < .01). Secondly, Column (2) presents the results of the second-stage regression, showing that ESG performance still positively affects EIP at the 1% level, indicating that the research conclusions remain valid after addressing potential endogeneity issues. Finally, tests for weak IV, over-identification, and non-identification were conducted. The results indicate no issues with weak IV, over-identification, or non-identification, confirming the robustness of the baseline regression.

Result of Endogeneity Checks.

Source. Authors own work.

p < .01.

PSM Method

This paper uses the PSM method for robustness testing to mitigate potential sample selection issues that may arise due to firms with better ESG performance inherently having stronger innovation capabilities. First, all firms are split into groups with high and low ESG scores based on their average ESG performance. Next, propensity scores are calculated using the control variables in this paper as covariates in a Probit regression. Finally, firms are matched between the high and low ESG score groups based on their propensity scores using various matching techniques, including kernel matching. Finally, regression is carried out using the matched samples based on Model (1). The findings in Columns (3) to (6) of Table 6 show that the estimated coefficients for ESG performance are significantly positive at the 1% level, indicating that ESG performance still significantly impacts EIP even after sample selection bias is somewhat mitigated. Thus, Hypothesis H1 is further confirmed.

Robustness Checks

Lag Test

Considering that the impact of ESG performance on EIP may not manifest immediately, a lagged effect is hypothesized. First, enterprises must make long-term investments and efforts in ESG practices to develop favorable ESG performance. These investments typically require time to generate returns, influencing EIP. Second, market and societal recognition of a firm’s ESG performance often unfolds over time, affecting the innovation ecosystem and access to innovation resources. The dependent variable, EIP, is lagged by 1 to 3 periods in the regression analysis to address this potential lag. As shown in Columns (1) to (3) of Table 7, ESG performance remains a significantly positive predictor of EIP even after these lags. This result confirms that ESG performance exerts a long-term influence on EIP, underscoring the importance of accounting for temporal dynamics in the relationship between ESG and EIP.

Result of Robustness Checks.

Source. Authors own work.

p < .05. ***p < .01.

Alternative Measurements of the Key Variables

Firstly, alternative measurements for the explanatory variable, ESG performance, are adopted, utilizing the Bloomberg ESG scores (ESG1). Simultaneously, the measurement methods for the dependent variable, EIP, are replaced, employing the number of patent grants (Apply1) and patent applications for inventions (Apply2). The test results, as presented in Columns (4) to (6) of Table 7, demonstrate consistency with the previous findings, thus reinforcing the main research conclusions of this paper.

Subsample Regression

Subsample analyses were conducted to test the hypotheses and mitigate the confounding effects of external factors on EIP. At the policy level, in September 2018, China’s Ministry of Finance, State Taxation Administration, and Ministry of Science and Technology jointly promulgated the “Notice on Increasing the Pre-Tax Additional Deduction Ratio for R&D Expenses.” This regulatory measure stimulated firms to augment research and development investments and foster innovation. The sample period was truncated to 2009 to 2017 to isolate the policy’s impact on EIP. The corresponding regression results are reported in Column (7) of Table 7. From an industrial perspective, technological innovation represents the cornerstone of competitiveness for high-tech enterprises. In these firms, innovation metrics such as R&D intensity and patent production typically surpass those of traditional industries by substantial margins. As a result, EIP in high-tech sectors may be more strongly influenced by internal determinants, including technical capabilities and R&D expenditures, rather than ESG performance. All high-tech enterprise observations were excluded from the analysis to address this potential endogeneity, leaving only non-high-tech enterprises in the subsample. The findings of this analysis are presented in Column (8) of Table 7. Across both subsample specifications, the empirical results align with the primary analysis, validating the robustness of the study’s conclusions.

Heterogeneity Analysis

Property Rights Heterogeneity Test

The nature of enterprise property rights may lead to heterogeneity in the impact of ESG performance on EIP (Husted & Sousa-Filho, 2019). In China, state-owned enterprises (SOEs), compared to non-state-owned enterprises (NSOEs), enjoy advantages in policy support and resource acquisition, rendering the incentive effect of ESG performance on enterprise innovation activities relatively limited. Conversely, NSOEs often face less policy support, fiercer market competition, and FC. As such, they are more motivated to engage in innovative activities when fulfilling ESG responsibilities to gain market competitiveness and advance corporate development. EIP is, therefore, more likely to be improved by NSOEs performing well in ESG. To do grouped regression tests on the relationship between ESG performance and EIP, this study separates the sample businesses into SOEs and NSOEs based on the type of corporate ownership. Columns (1) to (2) of Table 8 display the test results accordingly. The findings indicate that EIP is significantly improved by ESG performance in both SOEs (β = .134, p < .01) and NSOEs (β = .266, p < .01). Nonetheless, it is clear from comparing the estimation coefficients that NSOEs are more affected by ESG performance in terms of EIP. To further test whether there are significant differences in the coefficients between the groups after grouped regression, this study conducted a seemingly unrelated regression (SUR) test. The test results indicate a p-value of .000 for the difference test of regression coefficients between groups, suggesting a significant difference in coefficients between the groups.

Results of Heterogeneity Test.

Source. Authors own work.

p < .01.

Levels of EIP Heterogeneity Test

EIP is often influenced by factors such as a firm’s innovation level and available innovation resources. To further explore the relationship between ESG performance and EIP under various conditions, this study categorizes firms into high-innovation-performance and low-innovation-performance firms based on the median of EIP. It employs Model (1) for grouped regression analysis. Columns (3) to (4) of Table 8 display the regression findings. The findings show that, at the 1% level, there is a strong positive association between ESG performance and EIP for high-innovation-performance firms but not for low-innovation-performance firms. Using a seemingly unrelated regression (SUR) technique, additional tests for group differences in coefficients produce a p-value of .018 and an F-value of 5.65, which are significant at the 5% level, indicating that the two groups differ significantly. This further illustrates how high-innovation-performance enterprises are more likely to experience the positive effects of ESG performance on EIP. This may be attributed to the combined effects of high-innovation-performance firms’ resource and capability advantages, brand reputation and image, social responsibility and mission, as well as stakeholders’ expectations and pressures, which collectively drive these firms to actively explore and practice the integration of ESG and EIP.

Industry Environmental Sensitivity Heterogeneity Test

Industrial activities of corporations constitute a major source of environmental pollution. Firstly, heavily polluting corporations often face more government regulations, media scrutiny, and stakeholder pressure. To meet the demands of multiple stakeholders, these corporations may invest in ESG to some extent, thereby diminishing the impact of ESG performance on EIP. Besides, in the context of the “Dual Carbon” goals, heavily polluting corporations typically have higher carbon emissions and greater risks, leading investors to demand higher returns to compensate for potential risk losses. Conversely, corporations with lower carbon emissions are more favored by investors. Thus, the ESG performance of non-heavily polluting corporations is more likely to attract investors’ attention and recognition, which aids in alleviating capital constraints, obtaining external resources, and enhancing EIP. Therefore, this study reexamines the relationship between ESG performance and EIP and divides sample corporations into heavily polluting and non-heavily polluting corporations based on their industry codes, as per the Guidance on the Industry Classification of Listed Companies, which was updated by the China Securities Regulatory Commission in 2012. The results, as shown in Columns (5) to (6) of Table 8, demonstrate that the regression coefficients of ESG performance are favorably significant at the 1% level for both substantially polluting and non-heavily polluting businesses. However, compared to firms that pollute heavily, the regression coefficient for non-polluting corporations is greater. Additionally, the seemingly unrelated regression (SUR) test results show significant differences between the two groups. The above analysis suggests that compared to heavily polluting corporations, the impact of ESG performance on EIP is more significant for non-heavily polluting corporations.

Life Cycle Heterogeneity Test

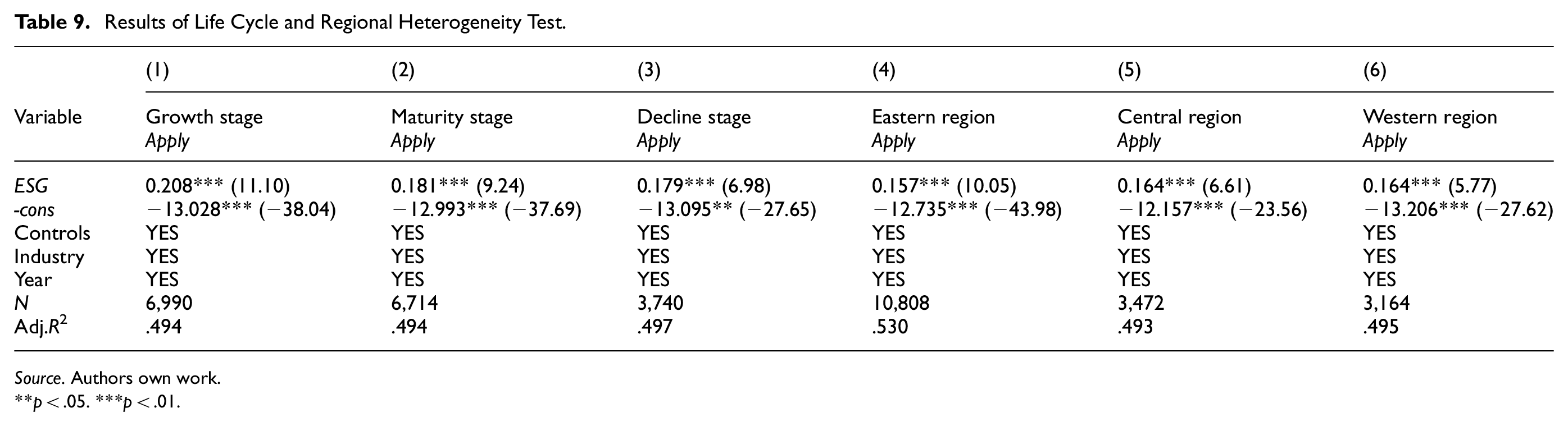

According to the corporate life cycle theory, different stages of a corporation’s development exhibit differentiated characteristics regarding strategic objectives, resource allocation, risk tolerance, and market environment. Consequently, do these various stages of development have varied effects on EIP due to ESG performance? Therefore, this study follows Dickinson’s approach and classifies the development stages of corporations based on their cash flow patterns. Specifically, the corporate life cycle is divided into three stages: growth, maturity, and decline, according to the positive and negative combinations of net cash flow from operating, investing, and financing activities (Dickinson, 2011). Among the 17,444 samples in this study, there are 6,990 samples in the growth stage, 6,714 in the maturity stage, and 3,740 in the decline stage. The growth and maturity stage samples account for 78.56% of the total, indicating a favorable development trend for listed corporations in China.

The regression results of the relationship between ESG performance and EIP at various phases of development are shown in Columns (1) to (3) of Table 9. Across all stages of company development, it is clear that ESG performance significantly improves EIP at the 1% level. It is possible by comparing the regression coefficients that the growth stage has the biggest coefficient, followed by the maturity stage, and the decline stage has the smallest coefficient. This suggests that the influence of ESG performance on EIP is highest during the growth stage and progressively lessens as the company moves through its life cycle. The potential explanation is that businesses with strong ESG performance have a higher chance of luring partners and investors when they grow, as they are perceived as having long-term potential and social responsibility. These investors and partners may bring more resources and opportunities to the corporation, promoting innovation. In the maturity stage, while the corporation has established a stable market position and customer base, it must also cope with intense market competition and a constantly changing market environment. At this stage, the impact of ESG performance on EIP remains significant but may slightly weaken. When a corporation is in the decline stage, it faces challenges such as declining market share and weakened profitability. Firstly, resources may become limited and must be prioritized for basic operations and survival. Therefore, the corporation may be unable to allocate sufficient resources to focus on ESG factors and innovation activities. Besides, innovation becomes more difficult during the decline stage, as the corporation’s capability may be somewhat constrained. Due to changes in the market environment and competitive pressures, it may be challenging for the corporation to identify new business opportunities and potential market demands, making it difficult to develop competitive, innovative products or services.

Results of Life Cycle and Regional Heterogeneity Test.

Source. Authors own work.

p < .05. ***p < .01.

Regional Heterogeneity Test

Given the disparities in regional economic development levels, ESG performance exerts varying degrees of influence on EIP. In this study, the entire nation is partitioned into three major economic regions: the eastern, central, and western regions. Regression models are constructed for the sample data of each region separately, and the regression results are presented in Columns (4) to (6) of Table 9. Findings reveal that the regression coefficients of ESG performance on EIP in the eastern, central, and western regions are all significantly positive, indicating the universal promoting effect of ESG performance on EIP. However, upon closer examination, the regression coefficients in the central and western regions are identical and significantly larger than those in the eastern region. This suggests that ESG performance has a more pronounced enhancing effect on EIP in the central and western regions. The relatively smaller coefficient in the eastern region implies that the marginal impact of ESG may be constrained or diluted by other factors in this area. This phenomenon is likely attributed to regional economic and market maturity differences. Compared with the central and western regions, the eastern region is more economically developed and has a higher level of marketization. Corporate innovation in the eastern region may rely more heavily on traditional factors such as technology, capital, and talent, rendering the marginal contribution of ESG relatively limited. In contrast, in the central and western regions, where the economic development level is lower, policy preferences, such as green financial support and the Western Development Program, may amplify the positive effects of ESG. Additionally, the reputation enhancement and resource acquisition brought about by ESG can be more readily transformed into drivers of innovation, thus exerting a stronger promoting effect on EIP.

Concluding Remarks

Conclusions and Discussion

ESG, as a concept promoting greener and more sustainable development for enterprises, has facilitated diverse growth aspects. This paper employs data from Shanghai and Shenzhen A-share listed companies from 2009 to 2022 to investigate the impact of ESG performance on EIP. The research reveals that ESG performance has a significant positive effect on EIP. Mechanism tests further demonstrate that IC, FC, and GRDS are intermediary factors between the two. After applying various robust testing methods, the conclusions remain valid. Further insights show that the enhancing effect of ESG performance on EIP is more pronounced when the enterprise is non-state-owned, a high-innovation-performance enterprise, a non-heavy-pollution enterprise, or an enterprise in its life cycle growth stage.

Implications for Theory and Practice

This study has the following theoretical significance: Firstly, this research enriches the studies on the effects of ESG performance. The impact of ESG performance on businesses, including financial performance and corporate tax evasion, has been the main subject of previous research (Jiang et al., 2024). This study focuses on EIP and shows how EIP and ESG performance are related. In contrast to earlier studies (H. Sun et al., 2024; Wu et al., 2024), this study investigates the effect on EIP from three dimensions: E (Environment), S (Social), and G (Governance), echoing scholars’ calls for examining the influence on EIP from various dimensions (J. Li et al., 2023; M. Ren et al., 2024). Secondly, from both governance and resource effects, this study analyzes the underlying mechanisms through which ESG performance affects EIP, considering IC, FC, and GRDS. It offers factual information that helps scholars and companies better grasp the elements boosting EIP.

The practical implications of this paper are as follows at the enterprise level: Enterprises should tailor strategies to their specific characteristics to enhance the promotional effect of ESG performance on EIP. First, they must prioritize the collaborative development of ESG dimensions, with particular emphasis on the E (Environmental) dimension, and optimize key strategies according to distinct organizational attributes. Non-state-owned enterprises should strengthen corporate governance structures by enhancing transparency in information disclosure. This approach signals standardized operations to the market and alleviates information asymmetry in financing, thus facilitating easier access to external capital for innovation. Heavily polluting enterprises, in turn, should increase investments in green technology R&D, proactively fulfill environmental responsibilities, and align with government policies promoting green and low-carbon development. Such actions reduce resource consumption and pollution while increasing the likelihood of securing GRDS by matching policy priorities. Second, ESG implementation pathways must be adjusted based on the enterprise lifecycle and innovation maturity. Growth-stage enterprises can integrate ESG development with upgrades to internal control systems. These enterprises can ensure stable innovation resource allocation by establishing standardized decision-making processes and risk-monitoring mechanisms. Meanwhile, enterprises with high innovation performance should intensify social responsibility practices to attract top-tier talent. They should also deepen collaborations with universities and research institutions to build industry-university-research collaborative innovation networks, thereby amplifying the positive effects of ESG performance on EIP through these partnerships. Enterprises in the central and western regions should fully utilize the advantages of national policies and play a role in promoting the effect of ESG performance on EIP. Additionally, enterprises must recognize the long-term strategic value of ESG performance, moving beyond the view of environmental protection and social responsibility as mere additional costs. Proactive disclosure of ESG-related information is essential, as is full utilization of ESG’s governance and resource effects. By doing so, enterprises can construct a more solid resource and institutional foundation for innovation activities. Embedding ESG into core strategies enables firms to create a sustainable framework that enhances innovation capabilities and long-term value.

The following actions are recommended at the governmental level: Governments should establish differentiated policy frameworks to guide enterprises in enhancing their ESG performance. First, when improving ESG rating systems and information disclosure regulations, attention must be paid to industry and enterprise-type disparities. Assessment dimensions tailored to micro, small, and medium-sized enterprises should be incorporated into ESG rating indicator systems to address the inherent financing disadvantages faced by non-state-owned enterprises. This approach will guide financial institutions to integrate ESG performance into credit approval criteria, alleviating financing constraints for non-state-owned enterprises. Stricter environmental responsibility assessment indicators should be formulated for heavily polluting industries to incentivize enterprises to increase investments in environmental technology innovation. Meanwhile, preferential support in R&D subsidy allocation should be provided to heavily polluting enterprises that proactively pursue green transformation. Second, governments must develop differentiated incentive and penalty mechanisms linked to ESG performance. Enterprise ESG performance results should be directly associated with policy resources such as GRDS and tax incentives. For example, enterprises in the growth stage with excellent ESG performance could receive additional support in allocating innovation funds. In contrast, those with poor ESG performance might face measures such as increased tax burdens. Third, pilot programs for ESG practices should be launched using typical samples such as non-state-owned and growth-stage enterprises. Replicable best practices derived from these pilots can be summarized and disseminated through policy briefings and other means to encourage more enterprises to convert ESG advantages into innovation drivers. By tailoring policies to address specific challenges and leveraging successful examples, governments can effectively promote the integration of ESG performance and innovation capacity across diverse enterprise contexts.

Limitations and Future Research Suggestions

Firstly, the conclusions of this study are based on data from Chinese enterprises, revealing the positive impact of ESG performance on EIP; however, their generalizability may be limited by regional differences. The commonalities in global ESG trends and innovation drivers may endow the findings with some applicability in other regions, particularly regarding the mechanisms through which ESG promotes innovation by alleviating FC, enhancing IC, and securing GRDS. Nevertheless, disparities in institutional environments, stages of economic development, cultural values, and data quality may reduce the general applicability of these conclusions. For example, ESG regulatory systems in developed countries are more mature, whereas developing countries may prioritize short-term economic gains. Future research could further validate the generalizability of these conclusions through cross-national comparisons and regional heterogeneity analyses, providing more comprehensive theoretical support for global ESG practices.

Secondly, the boundary conditions require further exploration and analysis. This research examines how IC, FC, and GRDS influence ESG performance and EIP. However, it does not explore the boundary conditions within these mechanisms. Boundary conditions, including corporate governance levels and corporate digital transformation, may mitigate the effect of ESG performance on EIP. Future studies can explore these topics further to give firms more focused managerial insights.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.