Abstract

This study uses a two-way fixed-effect model to analyze the impact of ESG performance on corporate value based on the quarterly data of Chinese A-share listed sports companies from 2018 to 2022. The results prove that (1) The ESG performance of sports enterprises positively affects corporate value: the higher the ESG score is, the higher the corporate value is. (2) Mechanism analysis shows that financing constraints play a partially mediating role in the relationship between ESG performance and corporate value. (3) Heterogeneity analysis shows that corporate political relations will weaken the facilitating effect of ESG performance on corporate value. The stronger the political relations are, the weaker the facilitating effect of ESG performance on corporate value. Compared with that during the bear market, the performance of ESG in the bull market has a greater facilitating effect on corporate value. Compared with sports service enterprises, sports goods enterprises’ ESG performance has a stronger facilitating effect on corporate value.

Plain Language Summary

Research question: This paper provide an in-depth discussion of the impact of sports enterprises’ ESG (environment, social responsibility and corporate governance) performance on corporate value. Research methods: This study uses a two-way fixed-effect model to analyze the impact of ESG performance on corporate value based on the quarterly data of Chinese A-share listed sports companies from 2018 to 2022. Results and findings: The results prove that (1) The ESG performance of sports enterprises positively affects corporate value: the higher the ESG score is, the higher the corporate value is. (2) Mechanism analysis shows that financing constraints play a partially mediating role in the relationship between ESG performance and corporate value. (3) Heterogeneity analysis shows that corporate political relations will weaken the facilitating effect of ESG performance on corporate value. The stronger the political relations are, the weaker the facilitating effect of ESG performance on corporate value. Compared with that during the bear market, the performance of ESG in the bull market has a greater facilitating effect on corporate value. Compared with sports service enterprises, sports goods enterprises’ ESG performance has a stronger facilitating effect on corporate value. Implications: It is helpful for relevant enterprises to clarify the positive influence of ESG performance on corporate value to stimulate the internal motivation of sports enterprises to fulfil their ESG responsibilities while boosting the sustainable development of sports enterprises and the green and coordinated development of the sports industry. Limitations: The overall data is relatively less, and the research methods need to be enriched.

Introduction

The Chinese government has included developing a green economy and improving social equality in its 14th Five-Year Plan and proposed targets of a 2030 “carbon peak” and 2060 “carbon neutral” status. In this context, the direction and goal of enterprises is to achieve higher quality, more efficient, more equitable and more sustainable development. ESG (environment, social responsibility and corporate governance) is a new sustainable development concept on how to coordinate the development of the environment, social responsibility and corporate governance in the world, first proposed by the United Nations Environment Program in 2004. ESG advocates that enterprises should pay attention to environmental protection, social responsibility and corporate governance responsibility while operating; urges listed companies to set an example in green development, social responsibility and effective governance; conveys the development concept of pursuing the unity of economic value and social value; and is an important starting point for achieving high-quality economic development and sustainable enterprise development. The concept of environment, social responsibility and corporate governance has been gradually accepted and valued. ESG has become three important indicators used to measure the level of green and sustainable development of enterprises in the international community. In recent years, all sectors of domestic society have paid close attention to the ESG performance of enterprises, and relevant policies and regulations have been constantly improved and introduced. In 2018, the China Securities Regulatory Commission (CSRC) issued a new version of the Code on the Governance of Listed Companies, which presented the latest provisions on the three aspects of the environment, social responsibility and corporate governance of listed companies, aiming to advocate the ESG concept, promote the practice and development of ESG, and thereby promote the sustainable development of the Chinese economy.

As a green and sunrise industry, the sports industry is an important force promoting Chinese economic transformation and upgrading. The sustainable development of relevant enterprises has thus become an important aspect of China’s efforts to develop an ecological civilization and promote high-quality economic development. Currently, the relevant government departments in China actively advocate the concept of ESG; ask sports enterprises to implement green development, assume social responsibility and improve corporate governance; and guide the listed sports companies to constantly improve ESG performance. At the same time, some enterprises are actively promoting the development of ESG practice, constantly increasing green input and taking the initiative to shoulder social responsibilities while optimizing corporate governance. For example, in 2021, ERKE donated 50 million yuan to the areas affected by a heavy rainstorm disaster in Zhengzhou, Henan Province, making this company, which had been out of public view, an object of heated debate among the people, and many people placed orders to buy products from ERKE to show their support, setting off a flurry of “wild consumption.” Can ESG performance of sports enterprises enhance their corporate value? To date, studies have been inconclusive, which is one of the gap for this study. Most scholars believe that ESG performance has a positive impact on enterprise value and that ESG performance can improve enterprise business performance (Brogi & Lagasio, 2019; Peiris & Evans, 2010) or market valuation (Albuquerque et al., 2019; Cajias et al., 2014; Ferrell et al., 2016; Gao & Zhang, 2015; Ghoul et al., 2017). Some scholars, in contrast, consider ESG initiatives as a waste of resources and a tool used by managers to extract private benefits from shareholders (Barnea & Rubin, 2010; Buchanan et al., 2018; Garcia & Orsato, 2020; Groening & Kanuri, 2013). Still other scholars believe that ESG performance has no significant impact on enterprise value (Atan et al., 2018; Humphrey et al., 2012). Moreover, the current ESG related research mostly involves listed companies in all industries, with few focusing on a single industry. In the field of sports, scholars have studied the impact of environmental protection (Y. Li & Zhao, 2008), social responsibility (Liang & Zhao, 2008) and corporate governance (Zhang, 2018) on sports enterprises separately. However, there is still a gap in the research on the impact of ESG performance on the corporate value of sports enterprises.

Based on the above analysis, we applied a two-way fixed-effect model to analyze the impact of ESG performance on corporate value based on the quarterly data of Chinese A-share listed sports companies from 2018 to 2022. Furthermore, we analyzed the functional mechanism of the effect of enterprise ESG performance on enterprise value from the perspective of financing constraints. In addition, we discussed the influence of the heterogeneity of political relationships, market situations and business focuses on the relationship between enterprise ESG performance and enterprise value. The marginal contribution of this paper includes three aspects: (1) It expands the scope of ESG and enterprise value research to sports field, and it provides proof for ESG to promote enterprise value. Therefore, this paper is a beneficial supplement to ESG studies. (2) This paper explores the functional mechanism of the impact of sports ESG performance on corporate value from the perspective of financing constraints to provide ideas for alleviating the financing constraints of sports enterprises. (3) Based on the situation of China, market situation and sports industry characteristics, the paper considers the impact of political relations, market situation and business focuses on the relationship between enterprise ESG performance and enterprise value. It helps to clarify the impact of ESG performance of companies with different political relations, different market conditions and different business focuses on enterprise value.

Research Overview and Research Hypothesis

Research Overview

At present, the related research in the field of sports mainly focuses on the single dimension of environment, social responsibility and corporate governance.

In terms of the environmental dimension, most studies explore the relationship between sports and the environment. The relationship between sports and natural environment is bidirectional. Specifically, sports affects the natural environment and is influenced by the natural environment (Brian et al., 2020). Since the 1990s, sports management scholars have mainly discussed the impact of sports industry on the environment from the perspectives of sports sustainability (Chard & Mallen, 2012; Kellison & Hong, 2015; Mallen et al., 2010), corporate social responsibility (Casper et al., 2012; Inoue & Kent, 2012a, 2012b) and the influence of sports industry on environmental behavior (Casper et al., 2017; Kellison & Kim, 2014; McCullough, 2013). In recent years, the impact of the environment on sports has been gradually increased, mainly including the impact of climate change on sports (Dingle & Stewart, 2018; Orr & Inoue, 2019) and the adaptive behavior of athletes, organizations and fans to the environment (Orr & Schneider, 2018). However, there are still few studies on the environmental responsibility of sports enterprises, especially the empirical studies on the value and benefit of the environmental responsibility of sports enterprises. Relevant research has mainly focused on the environmental behavior of professional sports organizations. For example, Sylvia et al. (2013) explored institutional forces affecting environmental sustainability in professional sport teams and leagues in North America. Pfahl (2010) considered strategic and efficiency elements of the adoption of environmentally oriented CSR in sport organizations and concluded that these types of CSR practices can have both economic and legitimacy benefits for sport organizations. Brian et al. (2021) examined the environmental attitudes and the corresponding environmental initiative preferences of external stakeholders of sports organizations.

There are rich literature on sports social responsibility, and the theoretical research involves the comprehensive motivation, content dimensions, prominent problems and causes, cultivation path and the impact of corporate social responsibility on corporate value (Kathy, 2010). In addition, the empirical study is mainly to verify the impact of sports enterprises’ social responsibility on corporate performance or corporate value. For example, Johannes and Matthias (2022) analyzed the relationship between perceived CSR and perceived organizational performance in professional sports organizations, and found that employee CSR awareness was positively correlated with perceived organizational performance when controlling for age, gender, income, education, sports discipline, and organizational level. Babiak and Wolfe (2009) tracked the financial performance of enterprises that practice social responsibility, and found that enterprises with long-term social responsibility have better financial performance, but not obvious in the short term.

The research of sports corporate governance mainly focuses on professional sports clubs, especially focusing on the corporate governance research of professional football clubs. Related research not only involves the current situation, problems and suggestions of club governance (Amaury et al., 2010; Michie & Oughton, 2005), but also the relevant research has been deep into the impact of the governance structure and governance mechanism on the club’s financial performance. For example, Dimitropoulos and Tsagkanos (2012) analyzed the impact of corporate governance quality (namely board size, board independence, managerial ownership, institutional ownership, and CEO duality) on the profitability and viability of European Union’s football clubs over the period 2005 to 2009. Empirical results documented that corporate governance quality leads to greater levels of profitability and viability. Bell et al. (2013) examined the impact of the departure of English football club managers on the value of the club stock. Malagila et al. (2021) investigated the relationship between the corporate structure of football clubs and financial performance and non-financial performance. However, due to the low degree of marketization of China’s sports industry and the few listed companies in the sports industry, there are few research on corporate governance in China’s sports industry. Only Zhang (2018) studied the current governance status and the relationship between corporate internal governance and performance of small and medium-sized sports companies in China

In general, the current research mainly focuses on the single dimension of environment, society and corporate governance, and the research objects are mainly focused on professional sports clubs, and rarely involve other types of sports enterprises in the sports industry. In addition, most of the relevant empirical studies are foreign data, and the empirical studies of Chinese sports enterprises are relatively lacking. This paper provides an in-depth discussion of the impact of sports enterprises’ ESG (environment, social responsibility and corporate governance) performance on corporate value based on the data of China’s A-share sports listed companies. It provides a new and comprehensive lens on environment, social responsibility and corporate governance problem for sports enterprises, and it expands the research scope of ESG to sports enterprises.

Research Hypothesis

ESG Performance and Corporate Value

Resource dependence theory emphasizes that the survival of organizations depends on their ability to draw resources from the surrounding environment, and the construction of organizational competitive advantage relies on the core resources held by stakeholders (L. L. Gu et al., 2020). Signal transfer theory contents that good environmental, social and governance performance of enterprises sends positive signals to stakeholders, which can help ease the degree of information asymmetry between stakeholders and business managers, thus improving corporate reputation and gaining the trust of the public (Z. B. Li et al., 2022). Together, resource dependence theory and signal transfer theory indicate that, good corporate ESG performance plays a role in transmitting positive enterprise information, which can improve corporate reputation and gain the trust of stakeholders. Furthermore, good ESG performance can help an enterprise obtain the key strategic resources of stakeholders, overcome the constraints of limited resources, realize competitive advantages and improve corporate value (Ferrell et al., 2016; Gao & Zhang, 2015; Lins et al., 2017; Malik, 2015).

The stakeholders of the enterprise include its shareholders, creditors, employees, upstream and downstream supplier, customers, government, natural environment, etc. For enterprise managers, enterprises actively undertake environmental, social responsibility and improve corporate governance can not only improve the legitimacy of the enterprise, but also harvest environmental prevention measures, environmental technology, improved production technology and good corporate governance system and other valuable resources (Miles & Covin, 2000). It helps to reduce the probability of environmental and social responsibility accidents and eliminate the negative impact of such accidents on the value of enterprises, such as corporate reputation damage, legal sanctions and brain drain (Peloza, 2006). For the investors, participation in ESG activities sends positive corporate signals to investors, reduces the degree of information asymmetry between investors and enterprise managers, and enhances investor confidence (Z. B. Li et al., 2022), which is conducive to obtaining investors’ financial resources. For the government, good ESG performance provides support for relevant policies, which helps enterprises establish good relations with the government to obtain the support of government resources (Z. B. Li et al., 2022). For the supplier, the good ESG performance of the enterprise also signals good current business performance to suppliers (Wang & Yang, 2022), which helps the enterprise to gain the trust of the suppliers to improve the enterprise’s ability to borrow from the suppliers. At the same time, the enterprise improves its reputation and stimulates the enthusiasm and efficiency of employees through good ESG performance, injecting high-quality human capital into the enterprise innovation (Wang & Yang, 2022). In addition, good corporate ESG performance helps to win the trust and support of consumers and improve customer satisfaction (Amel-Zadeh & Serafeim, 2018; Pérez & del Bosque, 2015; Walsh & Bartikowski, 2013) and customer loyalty (Ramlugun & Raboute, 2015). All these benefits provide valuable resources for enterprises to obtain competitive advantages, which is conducive to expanding the operating income and profit of enterprises and improving enterprise value.

The above theoretical research shows that enterprise ESG performance is means by which enterprises can engage in sustainable development while taking into account all stakeholders, which is helpful to gain the trust and resource support of all stakeholders, reduce enterprise risks, and thereby enhance corporate value (Ferrell et al., 2016; Lins et al., 2017; Malik, 2015). Based on the above analysis, the following hypothesis is proposed:

Hypothesis 1: The ESG performance of sports enterprises promotes corporate value; the better the ESG performance, the higher the corporate value.

The Mediating Role of Financing Constraints

Based on signal transfer theory, positive ESG performance sends positive enterprise signals to stakeholders, which can reduce the degree of information asymmetry between investors and enterprise managers, ease investors’ concerns about the enterprise’s future operations, and enhance investors’ willingness to ease the financing constraints of enterprises (Ghoul et al., 2011; L. L. Gu et al., 2020). First, ESG performance information can compensate for the defects of reflecting incomplete information in a company’s financial reports, improve enterprise information transparency, and reduce the degree of information asymmetry between other stakeholders and enterprise managers (Z. B. Li et al., 2022). This transparency enables investors to comprehensively and systematically consider the financial and nonfinancial performance of enterprises, helps creditors to gain a more comprehensive understanding of the business conditions of the enterprise, helps the enterprise to gain trust and recognition from investors, and enhances investors’ investment willingness (Qian et al., 2017). Second, the enterprise ESG performance conveys to creditors a positive enterprise signal about higher corporate social responsibility consciousness, strong sustainable development ability and an effective corporate governance mechanism. These impressions help enterprises to develop a good reputation, enhance investor trust, improve credit ratings, reduce investors’ risk perception, and their required necessary remuneration rate (Albarrak et al., 2019; Z. B. Li et al., 2022), and increase the allocation of credit funds from creditors (Zhang, 2018). Third, good ESG performance is compliant with relevant government policies, helping enterprises establish good government–enterprise relations and obtain high-quality resources and opportunities (S. Li & Xie, 2014), prompting banks and other institutions to increase the supply of credit funds for enterprises, and improving enterprise external financing capacity.

Based on resource dependence theory, enterprises with strong financing constraints are more likely to fall into financial distress, are more likely to suffer setbacks in market competition and experience a decline in enterprise value (Q. Gu & Zhai, 2011; Qiu et al., 2020). Specifically, the higher the degree of financing constraints is, the smaller the intensity and scale of enterprise R&D investment will be. Enterprises cannot obtain sufficient capital resources to make optimal investment decisions, which can hinder the sustainable development of enterprises (Q. Gu & Zhai, 2011). The easing of financing constraints can help enterprises obtain financial resource support from investors and thus improve the competitiveness of enterprises and enhance corporate value (L. L. Gu et al., 2020).

Based on the above analysis, the following hypothesis is proposed:

Hypothesis 2: The ESG performance of sports enterprises promotes corporate value by reducing corporate financing constraints.

The Impact of Political Relations, Market Conditions, and Business Focus

The Impact of Political Relations

On the one hand, the political relationship of enterprises has the function of transmitting enterprise quality signals to stakeholders (Hu, 2006). Entrepreneurs’ political identities, such as deputies to the National People’s Congress and CPPCC members, show that enterprises have considerable economic strength and scale or that the corresponding enterprises have contributed to economic development and have been recognized by society and the government. This status helps to alleviate the degree of information asymmetry between stakeholders and business managers and improve corporate reputation. The value effect of ESG performance is mainly realized in the process of reducing the information asymmetry between enterprises and investors and delivering positive signals to investors (Wang & Yang, 2022) Therefore, compared with enterprises without political relations, the positive information transmission effect of the ESG performance of enterprises with political relations is reduced, and the positive effect of ESG on corporate value is weakened.

On the other hand, the ESG performance of enterprises with strong political relations is mandatory (Wang & Yang, 2022). In the view of stakeholders, enterprises with strong political relations undertake environmental and social responsibilities actively and may only be compliant with relevant policies, so they are more accustomed and less sensitive to enterprise ESG performance. As a result, the market responds less to the ESG performance of enterprises with political relations, which weakens the positive effect of ESG on corporate value. Thus, this paper expects that political relationships will weaken the positive effect of ESG on enterprise value; that is, when enterprise political relationships are stronger, the positive effect of enterprise ESG performance on enterprise value is reduced. Based on the above analysis, the following hypothesis is proposed:

Hypothesis 3: political relationships will weaken the positive effect of ESG on enterprise value.

The Impact of Market Conditions

Investors have different investment sentiments in bull and bear markets. Related studies show that investment sentiment in bull markets is generally higher than that in bear markets (Liu, 2020), and investors may have a greater tendency to buy in the former (S. Luo, 2017). Based on this concept, this paper proposes that compared with a bear market, investors’ investment sentiment is higher and they are more sensitive to corporate ESG performance in a bull market. This leads to the enhanced effect of ESG performance on corporate value. Based on the above analysis, the following hypothesis is proposed:

Hypothesis 4: compared with a bear market, ESG performance has a greater impact on corporate value in a bull market.

The Impact of Business Focus

The sports industry includes both sports goods and sports service enterprises. Analyzing the difference in ESG performance on enterprise value in companies with different business focuses can shed light on the role of ESG in sports enterprises with different attributes.

On the one hand, due to the differences in product production mode and product characteristics, compared with sports goods enterprises, sports service enterprises can pass enterprise information on to stakeholders in the process of product production to reduce the degree of information asymmetry with stakeholders. First, from the perspective of product production mode, the product production of sports service enterprises requires cooperating with stakeholders (Such as the government, the media, consumers, etc.). For every sporting competition at least two sport organizations must cooperate and agree on certain aspects (rules, place, date, time etc.) (Breitbarth et al., 2015). Therefore, sports service enterprises can pass on enterprise information to stakeholders in the process of product production, which is helpful to gain the trust and resource support of stakeholders, while sports goods enterprises have strong independence in product production. Second, from the perspective of product characteristics, sports events and other sports service products have a strong eye-catching effect, which often attracts more media reports and helps to strengthen stakeholders’ understanding of enterprises. Based on this, this paper proposes that, compared with sports goods enterprises, sports service enterprises can better transmit enterprise information to consumers in the product production process, which weakens the information transmission effect of ESG performance and thereby reduces its value increasing effect.

On the other hand, sports events have unique requirements for the environment (Smith & Westerbeek, 2007). Sports event organizers have an incentive to improve the environment to reduce the impact of environmental problems on the event and promote the smooth development of the event (Brian et al., 2020). For example, hockey is affected by the water environment, and freshwater shortages can hinder their outdoor practice activities, so the National Hockey League (NHL) has developed and implemented NHL indicators that focus on reducing water use at team facilities (Sylvia et al., 2013). Furthermore, sporting events focus large numbers of people in a limited space for a relatively short period of time, which may pose a risk to the natural environment in which they operate (Sylvia et al., 2013). Therefore, the event organizer has the responsibility to improve the possible environmental breaking problems of the relevant events. Currently, many sports organizations and venues are now implementing environmental initiatives, especially the super bowl, the Olympics and World Cup football championships and other big events have environmental plans or guidelines, including planting trees, stadium recycling initiative and environmental guidelines for suppliers and contractors to offset the audience carbon emissions, food waste and other production waste (Mallen et al., 2011; Paquette et al., 2011). In general, holding sports events not only need to have a good ecological environment condition, but also may have an impact on the local environment and society. Therefore, sports event service enterprises have the motivation and the responsibility to undertake the environmental and social responsibilities, resulting in the low sensitivity of the stakeholders to the ESG performance of sports service enterprises. The environmental protection and social performance of sports event service enterprises may be considered to be the compliance with the relevant competition rules to meet the environmental standards of holding the event, or to make up for the environmental and social problems caused by the event, thus reducing the value effect of ESG performance of sports service enterprises.

Based on the above analysis, this paper expects that, compared with sports goods enterprises, the information of sports service enterprises is more easily transmitted to stakeholders in the product production process, and the stakeholders are less sensitive to the ESG performance of the sports service enterprises. As a result, the information transmission effect of ESG performance of sports service enterprises is weakened, thus weakening the effect of ESG performance of sports service enterprises in promoting enterprise value. Based on the above analysis, the following hypothesis is proposed:

Hypothesis 5: Compared with sports service enterprises, sports goods enterprises’ ESG performance has a stronger facilitating effect on corporate value.

Research Design

Sample Selection and Data Processing

This paper selects the data of Shanghai and Shenzhen A-share listed sports companies or companies related to sports products and sports services from the first quarter of 2018 to the second quarter of 2022 as the research sample. The ESG data of the company come from the Wind database. The political relationship and business content data were compiled manually by checking the companies’ annual reports. The other data are from the CSMAR database. The sample data were chosen from the first quarter of 2018 because the Wind database began to give ESG scores for A-share listed companies beginning in the first quarter of 2018. Finally, 729 observations of 49 A-share listed companies were obtained.

Variables

Corporate Value

Modigliani and Miller (1958) proposed enterprise value as early as the 1950s, defining it as the present value of the cash flow realized by enterprises in the future. Enterprise value can be composed of three parts: standard value, customer value and social value (Yan, 2022). Based on relevant research (Z. Li, 2006), this paper uses Tobin’s Q to measure corporate value. Tobin’s Q represents the ratio of the market value of an enterprise to the enterprise replacement cost. This variable is used to measure the investment value of an enterprise and represents the market evaluation of investors on the growth potential of the enterprise. A high Tobin’s Q means that investors are optimistic about the company and are willing to invest in the company (Z. Li, 2006). The calculation method is as follows:

ESG Performance

According to relevant studies (Deckop et al., 2006; Z. B. Li et al., 2022; Shiu & Yang, 2017), enterprise ESG performance is generally measured by the ESG score and the ESG score mainly originated from the KLD database and Thomson Reuters ASSET4 database. Therefore, this paper uses the ESG score to measure ESG performance. Meanwhile, consider the availability of the data, The ESG score comes from the Wind database. The Wind database is the leading financial database in China, in which the ESG data content of Chinese sports enterprises is relatively complete. In addition, the Wind ESG index system consists of 3 dimensions, 25 issues and more than 300 indicators, among them, environmental indicators include environmental management system, green business objectives, green products, etc.; social indicators include social responsibility system, business activities and social contribution, etc.; corporate governance indicators include governance structure, operational risks, external sanctions, etc.

Corporate Political Relations

In the literature, the following three methods are used to measure corporate political relations: (1) the shareholding ratio of the government in the enterprise (Adhikari et al., 2006); (2) whether the directors and shareholders of the enterprise have channels through which to contact the main leaders of the country (Adhikari et al., 2006; Johnson & Mitton, 2003); and (3) whether the senior executive of the enterprise is a member of the NPC or CPPCC or has served in government departments (Fan et al., 2007; D. L. Luo & Huang, 2008).

In research on the Chinese market, the third of these methods is basically used. This paper also uses the third method, and referring to the research of D. L. Luo and Huang (2008), three indicators are used to measure the political relationship of enterprises. The first is the political relations dummy variable (D

Corporate Financing Constraints

Referring to the study of Z. B. Li et al. (2022), the

Control Variables

To avoid the influence of other variables on the research results, a series of control variables were added by reference to the relevant literature (Cheng et al., 2017), including company size (

Definition of the Main Variables.

Descriptive Statistics

Table 2 presents the descriptive statistics for the main variables. As shown in the table, the minimum and maximum data of

Descriptive Statistics of the Main Variables.

Model Design

To test the hypothesis 1, the following regression model is established:

To test the hypothesis 2, the following regression models are established:

To test the hypothesis 3, the following regression model is established:

To test the hypothesis 4, this paper draws on the practice of Lu et al. (2022) and divides the market into bull and bear markets according to whether the annual yield of the Shanghai Composite Index is greater than 0. The virtual variable (

If

To test the hypothesis 5, this paper divides the companies into sports services and sports goods companies according to the different business focuses of the sample companies. Model (1) is again used for group regression.

Empirical Results and Discussion

ESG Performance and Corporate Value

Table 3 presents the regression results of Model (1), with only regression coefficients for key variables. As shown in the table, Column 2 indicates the regression results of

ESG Score and Corporate Value.

Note. Data in parentheses are the standard error. “YES” means that control variables, individual fixed effect or time fixed effect is added to the model. Similarly hereinafter.

*, ***, and *** represent significance at the 10%, 5%, and 1% levels, respectively

The conclusion is consistent with the relevant studies (Ferrell et al., 2016; Gao & Zhang, 2015; Lins et al., 2017; Malik, 2015). Enterprises can improve their reputation and gain the trust of stakeholders to obtain the key strategic resources of stakeholders by delivering positive information through positive ESG performance to bring competitive advantage to the enterprise and improve the enterprise value. It is helpful for relevant enterprises to clarify the positive influence of ESG performance on corporate value to stimulate the internal motivation of sports enterprises to fulfil their ESG responsibilities while boosting the sustainable development of sports enterprises and the green and coordinated development of the sports industry. Moreover, this study has contributed to the sports industry perspective and Chinese data for the study of ESG and enterprise value, and it is a useful supplement to the related research.

Mechanistic Analysis of the Impact of ESG Performance on Corporate Value in the Context of Financing Constraints

The regression results are shown in Table 4, giving only the regression coefficients for the key variables to save space. Column (1) of Table 4 gives the regression results of Model (2). The

Regression Results of the Mediation Variable.

Note. ** and *** indicate significance levels of 5% and 1%.

The conclusion is consistent with the relevant studies (Wang & Yang, 2022). Enterprises can improve their reputation and gain the trust of stakeholders to obtain the key strategic resources of stakeholders by delivering positive information through positive ESG performance to ease corporate financing constraints and improve the enterprise value. This suggests that money will be more willing to go to companies with higher ESG scores. Relevant departments can guide the flow of capital to high-quality investment targets with high ESG scores by regulating enterprise ESG disclosure, help investors to explore the investment opportunities and comprehensive value of the sports industry, and prevent major risks. It will also promote the high-quality development and sustainable development of the sports industry.

Heterogeneity Analysis of the Impact of ESG Performance on Corporate Value

Heterogeneity Analysis of Political Relations

Table 5 presents the regression results for Model (5), with only regression coefficients for key variables. Column (1) indicates that when using dummy variable (D

Influence of Political Relations on the Relationship Between ESG and Corporate Value.

Note. *, **, and *** indicate significance levels of 10%, 5%, and 1%, respectively.

In the Chinese context, relationships are crucial. The development level of China’s sports industry market is relatively low, and the political relationship of senior executives of sports enterprises is strong. This paper found that the existence of political relations will weaken the positive effect of ESG performance on corporate value, because political relations, like ESG performance, send a positive signal. This paper will help the world to strengthen the understanding of Chinese sports enterprises and contribute Chinese experience to relevant theoretical research.

Heterogeneity Analysis of Market Conditions

Table 6 presents the regression results for Model (6), with only regression coefficients for key variables. The results show that the coefficient of the cross term was significantly greater than 0, indicating that ESG performance promoted enterprise value more in the bull market than in the bear market. For companies, the value effect of corporate ESG performance will be greater in a bull market, because investors’ investment sentiment is higher and they are more sensitive to corporate ESG performance in a bull market. It will help enterprises to adjust their ESG plans in time and maximize the value effect of enterprise ESG.

Impact of Market Conditions on the Relationship Between ESG Performance and Corporate Value.

Note. * indicate significance levels of 10%.

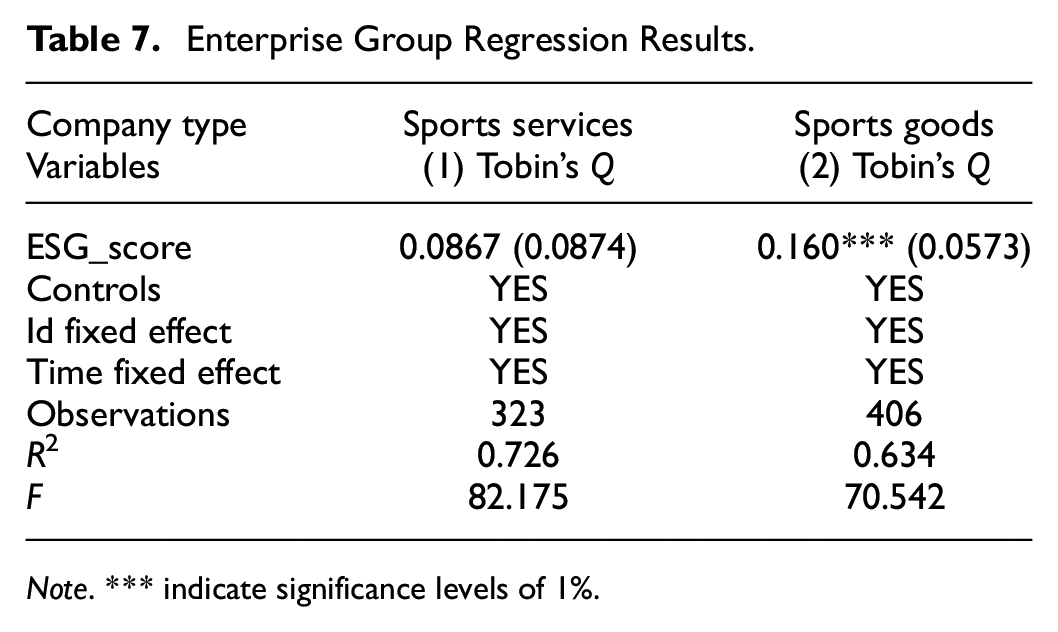

Heterogeneity Analysis of Business Focus

The regression results are shown in Table 7. Column (1) indicates companies whose business is sports services, and Column (2) indicates companies whose business is sporting goods. Compared with the regression results of Columns (1) and (2), for sports service companies, the coefficient of

Enterprise Group Regression Results.

Note. *** indicate significance levels of 1%.

Sports enterprises have both sports goods enterprises and sports service enterprises. Compared with sports goods enterprises, the information of sports service enterprises is more easily transmitted to stakeholders in the product production process, and the stakeholders are less sensitive to the ESG performance of the sports service enterprises. As a result, the information transmission effect of ESG performance of sports service enterprises is weakened, thus weakening the effect of ESG performance of sports service enterprises in promoting enterprise value. Our conclusion can help different business content enterprises to introduce appropriate ESG plans to maximize the value effect of ESG and improve the enterprise value. Moreover, it provides a unique perspective on sports and enriches the theoretical knowledge for ESG related research.

Robust Tests

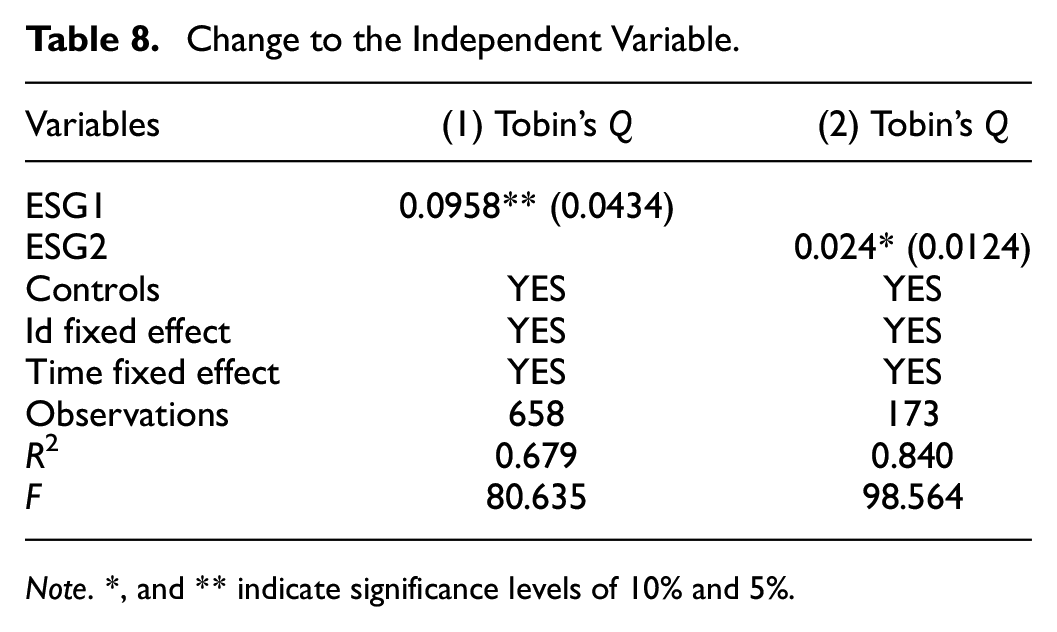

Changes to the Independent Variable

The Wind database gives an alternative method of scoring the ESG performance of listed companies. The company ESG performance ratings are in the form of “AAA, AA, A, BBB, BB, B, CCC, CC, C.” AAA indicates the highest rating, and C indicates the lowest rating. This paper quantifies this rating by assigning the highest rating “AAA” a score of 9. “AA” is assigned a score of 8. In turn, the lowest rating “C” is assigned a score of 1. The ESG rating is represented by the symbol

Change to the Independent Variable.

Note. *, and ** indicate significance levels of 10% and 5%.

Second, to test whether the impact of ESG performance on enterprise value has different results due to database selection, the Bloomberg ESG score is used, and the ESG score is represented by the symbol

Instrumental Variables Test

In this paper, the previous ESG score was used as the instrumental variable of the current ESG score, and the two-stage least squares (

Instrumental Variables.

Conclusion

In this study, we applied a two-way fixed-effect model to analyze the impact of ESG performance on corporate value based on the quarterly data of Chinese A-share listed sports companies from 2018 to 2022. Furthermore, we analyzed the functional mechanism of the effect of enterprise ESG performance on enterprise value from the perspective of financing constraints. In addition, we discussed the influence of the heterogeneity of political relationships, market situations and business focuses on the relationship between enterprise ESG performance and enterprise value.

Based on these analyses, we found that the ESG performance of sports enterprises positively affects corporate value: the higher the ESG score is, the higher the corporate value. Enterprises will obtain resource support from investors, consumers, employees, suppliers, governments and other stakeholders to improve enterprise competitiveness and enhance enterprise value through active ESG performance. Furthermore, Mechanism analysis shows that financing constraints play a partially mediating role in the relationship between ESG performance and value firms. On the one hand, ESG performance directly promotes corporate value. Besides, ESG performance reduces the financing constraints of enterprises, and lower financing constraints improve corporate value. In addition, the heterogeneity analysis shows that corporate political relationships weaken the facilitating effect of ESG performance on corporate value. The stronger the political relationship is, the weaker the facilitating effect of ESG performance on corporate value. Compared with a bear market, ESG performance in a bull market has a greater facilitating effect on corporate value. Compared with sports service enterprises, sports goods enterprises’ ESG performance has a stronger facilitating effect on corporate value.

This paper is a beneficial supplement to current inconclusive ESG studies by using data from Chinese sports companies. Specifically, the funding of this paper provides proof for ESG to promote enterprise value, which is consistent with some studies (Albuquerque et al., 2019; Brogi & Lagasio, 2019; Cajias et al., 2014; Ferrell et al., 2016; Gao & Zhang, 2015; Ghoul et al., 2017; Peiris & Evans, 2010). Besides, it expands the research scope of ESG to sports field. Furthermore, it provides new perspectives of financing constraints, political relations and business focus to enrich the research of ESG and enterprise value.

The findings of this paper provide directions for the related stakeholders. Enterprises should not only see the short-term costs of ESG practices, but should pay more attention to the long-term benefits brought by ESG, and actively implement ESG practices to promote the high-quality development of enterprises and the sustainable development of the sports industry. Relevant departments can guide the flow of capital to high-quality investment targets with high ESG scores by improving ESG service system and standardizing enterprise ESG disclosure, help investors to explore the investment opportunities and comprehensive value of the sports industry, and prevent major risks, which will also promote the high-quality development and sustainable development of the sports industry. Long-term investors should pay more attention to the environmental, social and governance performance of enterprises, and establish the ESG investment concept.

Future research should enrich the related enterprise data and expand the research methods, such as FGD and case study, to study the impact of ESG performance on enterprise anti-risk ability, enterprise attention and other aspects, as well as the heterogeneous research on national culture, enterprise nature, information disclosure, etc., in order to continuously enrich the relevant research on ESG and enterprise value of sports enterprises, and to obtain more scientific research conclusions.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets used and/or analyzed during the current study are available from the corresponding author on reasonable request.