Abstract

This study investigates the influence of ESG performance on aggressive tax planning (ATP) among A-share listed firms in China and hopes to unravel the moderating role of internal control between ESG performance and ATP. It utilizes the panel data and regression analysis to explore the effect between ESG performance and ATP in China during 2017 to 2022. The study incorporates the Huazheng ESG Rating Index to validate the current ESG performance of Chinese-listed firms and assess the potential influence of internal control on the effect between ESG performance and ATP. The study uniquely presents evidence from the perspective of listed companies in the biggest emerging country, China, indicating that ESG performance is positively linked to ATP. Moreover, this connection is moderated by an internal control mechanism. These unique findings contribute to the limited but expanding literature emphasizing the necessity and enhancements of ESG performance and corporate behavior regarding ATP in the Chinese context. More specifically, non-state-owned enterprises are more pronounced on the positive correlation between ESG performance and ATP than state-owned enterprises. The research results offer essential insights for stakeholders in ESG and ATP and investors, regulators, and policymakers in China.

Plain language summary

This study examines the effect of Environmental, Social, and Governance performance on aggressive tax planning among A-share listed firms in China and the moderating role of internal control. Using ordinary least squares and regression analysis on data from the Huazheng ESG Rating Index, the study finds a positive link between ESG performance and ATP, moderated by internal control mechanisms. This research insights are valuable for stakeholders, investors, regulators, and policymakers in China.

Introduction

Over the last 40 years of market reforms since the 1970s, the tax base in China has been significantly manipulated due to aggressive international tax planning (ATP), which artificially relocates profits to locations with little or reduced taxation (Shi, 2017). Along with a series of Chinese economic policies such as “Made in China 2025” and “One Belt, One Road” policy, China has primarily enhanced its influence in the international and domestic industries (Z. Chen et al., 2023). The internalization of Chinese technological companies such as Baidu, Alibaba, Tencent, and Huawei has continuously set up subsidiaries in tax havens like Hong Kong and the Cayman Islands, simulating the Netherlands and Luxembourg in Europe, Ireland, and the Caribbean for the companies in the United States (U.S.). These giant firms in China utilized ATP to minimize taxes and optimize profits during global operations (Christensen & Hearson, 2022), which may lead to ATP among listed companies in China. One current issue that requires investigation is the impact of ESG performance on the practice of ATP among the listed companies in China.

In the intricate landscape of global business, the Environmental, Social, and Governance (ESG) dimensions have become instrumental in delineating corporate ethos. The evolution of ESG is rooted in the principle of Corporate Social Responsibility (CSR), a doctrine propounded by the United Nations in 2004 and was later advanced through the Principles of Responsible Investment report (He et al., 2022; Meng & Zhang, 2023). This framework has oriented investors to consider ESG scores as a linchpin in their decision-making matrix, evaluating a firm's adherence to CSR beyond the traditional fiscal scope (Fonseca, 2020; T.-T. Li et al., 2021).

As the integration of CSR within corporate operations crystallizes, it unveils the dichotomy between ethical pursuits and financial stratagems, particularly in tax practices. In China, where ESG practices are burgeoning, only a sliver of A-share listed companies have attained commendation for their ESG endeavors, whereby out of approximately 4,000 listed companies in the A-share market with shares denominated in RMB, only 1,112 have released ESG reports (Wang, 2022). This embryonic stage of ESG development in China signals an opportune moment for empirical scrutiny into the nexus between ESG performance and ATP.

Tackling this conundrum, this research delves into the effect of ESG performance on ATP within the milieu of Chinese listed firms, a domain still nascent in academic exploration (Robert & Karie, 2016; Zhao et al., 2018). Utilizing the Huazheng ESG Rating Index, this study meticulously quantifies a firm's CSR engagement, drawing correlations to its tax avoidance behaviors. The research is poised to serve as a beacon for stakeholders, from policymakers to investors, navigating the murky waters of ATP amidst escalating ESG imperatives.

This study provides potential motivations and focal points about ESG performance and tax aggressiveness. First, the research recognizes that corporate ESG performance becomes more responsive to the tax burden as tax administration intensifies, leading to a significant decline in corporate ESG performance when the tax burden rises. Consequently, in the face of economic challenges and the imperative to balance financial considerations with sustainable development, the insights from this study can guide government authorities in prioritizing and implementing relevant ESG tax reduction policies to actively stimulate corporate motivation and enhance the willingness of enterprises to engage in ESG initiatives and disclosure. Second, this study underscores the continued need for stronger internal control mechanisms in most emerging economies, emphasizing the importance of internal controls in fostering sustainable development within Chinese firms and those of other developing countries.

To the best of the author's knowledge, the investigation into ESG performance and its relationship with ATP in China represents a pioneering or early contribution. Previous research has primarily focused on U.S. and European firms (Fonseca, 2020; Myhrberg & Harnesk, 2019). Notably, studies examining ESG performance and the adoption of tax planning strategies in developing nations have been gaining increasing attention. Thus, based on the aforementioned motivating factors, this study's primary purposes are to examine the effect of ESG performance on ATP in Chinese-listed companies and investigate whether ESG performance moderates the mutual relationship. This dual focus aims to provide a deep and novel understanding of the dynamics between ESG initiatives and tax affairs within the unique context of China's corporate landscape.

This study expects to add importance to the literature on ESG performance, tax aggressiveness, and internal control mechanisms. First, this research delves into the Chinese context, which remains a relatively unexplored area and offers valuable insights and similar reference to other emerging countries. Second, this research especially underscores the critical role of internal control in fostering sustainable development, which is initially used as the moderating role in this study, drawing attention to an often overlooked but increasingly important aspect among Chinese listed firms in future growth. Third, this study fills a critical gap by examining how the relationship between ESG performance and tax aggressiveness varies across different ownership structures, specifically state-owned and non-state-owned enterprises in China. This context remains under exploration in current literature.

Literature Review and Hypotheses Development

Agency Theory

Agency Theory highlights the contractual arrangement of the firm's owners (principals) and its managers (agents). This theory was developed by (Jensen & Meckling, 1976). Nevertheless, the divergent interests between these two parties can impact managerial strategies aimed at achieving corporate performance. Tax matters are one facet of this, as shareholders anticipate that managers will adhere to tax regulations, while managers might exploit tax regulation loopholes to reduce tax expenditures (Suparmun, 2018). Agency theory suggests that the management's decision to engage in corporate tax avoidance is motivated by self-interest in the relationship between ESG performance and tax aggressiveness.

ESG Performance and ATP

ESG, denoting Environmental (E), Social (S), and Governance (G), was initially introduced in the United Nations research report “Who Cares Wins” in 2004 (T.-T. Li et al., 2021). It acts as an extension of CSR, drawing interest from diverse stakeholders such as companies, investors, and governments. Numerous opportunities and challenges arise as the global economy and society continuously evolve. Notably in 2020, unforeseen and significant events unfolded, including the worldwide impact of COVID-19, where four financial crashes occurred in the U.S. stock market within two weeks, a locust outbreak in Africa, and the inclusion of Luckin Coffee in financial fraud cases. In response to these developments, the significance of ESG investing and performance has grown for both businesses and society (T.-T. Li et al., 2021).

Although ESG practices have been widely adopted for decades in industrialized countries such as America and Europe, developing countries still need improvement. This situation is mainly due to the limited popularity of ESG and the lack of extensive promotion of these practices by governments and companies (Boffo, 2020; Fonseca, 2020). ESG performance has become crucial for evaluating a company's non-financial performance and sustainability (Yoon et al., 2021). The Stakeholder Theory proposed by (Freeman et al., 2010) supposes that socially responsible companies may abstain from participating in ATP.

Some studies have investigated the relationship between ESG and ATP on an international scale. For example, Laguir et al. (2015) examined 24 publicly traded companies in France from 2003 to 2011, and the analysis concluded that a higher level of CSR is associated with decreased corporate tax aggressiveness. Zeng (2018) has conducted the first study to explore the reciprocal relationship between CSR and ATP across 35 countries characterized by weak governance. The results indicated that firms with higher CSR ratings typically participate in less tax evasion. Maas (2022) demonstrates a negative association between tax avoidance and ESG performance, suggesting that businesses with higher ESG performance are less likely to participate in tax aggressiveness. ESG performance has garnered increasing attention in China. ESG is an evaluation framework for assessing a company's comprehensive approach to sustainable development, including environmental conservation, commitment to social responsibilities, and effective corporate governance (Bai et al., 2022).

The primary objective of corporate managers is to generate wealth for the company while minimizing expenses, and it is inherent for them to fulfill the interests of shareholders. Reducing tax liability is a key economic goal of managerial efforts (D.-F. Huang et al., 2013). However, executing tax planning strategies may result in adverse consequences, such as the depletion of corporate human resources, political scrutiny, potential penalties, and consumer backlash (Yoon et al., 2021). Corporate sustainable decision-making has gained increased recognition, encouraging investors to seek sustainable investment opportunities. An essential tool for evaluating sustainability is the ESG performance ratings (Junius et al., 2020).

Prior research has delved into the adverse connection between ATP and ESG performance. Yoon et al. (2021) have examined Korean firms that demonstrate greater social responsibility and have a stronger inclination to avoid aggressive tax manipulation. They found that employing more ATP strategies can cause more significant damage to a company's social reputation. A positive correlation exists between tax transparency performance and higher ESG performance ratings (Munkejord & Vangdal, 2022). Moreover, Fonseca (2020) has indicated that highly socially responsible firms are inclined to steer clear of ATP. Environmentally conscious companies adopt a more moderate approach to taxation (Myhrberg & Harnesk, 2019).

However, improving ESG performance requires significant investment, potentially causing a short-term decrease in cash flow. Companies may cut operating costs to maintain normal operations. ATP can ease cash flow pressures and enhance short-term performance, making it a viable cost-cutting strategy (Zhang et al., 2021). Companies often prioritize economic benefits when enhancing ESG, sometimes creating a favorable illusion of performance at lower costs. They can achieve this through various methods like legal tax compliance or environmental efforts, but costs vary (Davis et al., 2016). Thus, they may prioritize cost-effective ESG investments over tax compliance, leading to aggressive tax avoidance. This strategy may be seen as rent-seeking to meet tax goals, as companies must fulfill social tasks to gain government resources. Based on the above analysis, it is inferred that there is a positive correlation between a company's ESG performance and its ATP behavior. In other words, the better a company's ESG performance, the more likely it is to engage in ATP. Therefore, the following hypothesis is formulated based on Agency Theory:

H1: There is a positive effect between ESG performance and ATP among Chinese listed firms.

ESG Performance, Internal Control, and ATP

Internal control, a fundamental component of corporate governance, plays an essential role in guiding corporate operations amid increasing uncertainty influenced by macro and micro-economic factors. Its key objectives include safeguarding corporate assets, supervising manufacturing and administration in compliance with legal requirements, ensuring the accuracy and integrity of financial reports, and improving overall business quality and efficiency (Zhang, 2020). Considering the potential of internal control to enhance overall corporate transparency, future studies may explore the link between disclosure policies and the effectiveness of internal control. Additionally, upcoming empirical investigations could focus on the impact of internal control effectiveness on adherence to these global standards for countries that have adopted international financial reporting standards. China also embraces this practice (Chalmers et al., 2018).

Previous studies have assessed Internal control as an explanatory and dependent variable, including the impact of corporate governance on internal control (Jiayao et al., 2023), the ESG performance and internal control (Harasheh & Provasi, 2022), and the influence of internal control on tax avoidance (Bimo et al., 2019). However, only a few studies have employed internal control as the moderating factor, such as Wenwu et al. (2023), who have investigated management equity and tax avoidance, and Hanwen Chen et al. (2020), who examined the internal control's moderating role in tax avoidance.

Under agency theory, managers might pursue ATP for short-term gains, risking regulatory and reputation issues (Jensen & Meckling, 1976). While ESG performance aims to curb ATP by promoting ethical practices, weak internal controls may enable managers to exploit ESG as a green washing tool while continuing ATP (Shakil, 2021). Strong internal controls could mitigate this by restricting managerial discretion, enhancing oversight, and ensuring ESG commitments translate into genuine governance improvements (Boulhaga et al., 2022). Thus, firms with robust internal controls are less likely to exhibit inappropriate ESG-ATP relationship, as a stricter monitoring prevents ESG performance from being misused to facilitate tax aggressiveness. As the firm grows and corporate governance becomes robust, this study explores whether internal control mechanism could enhance ESG performance and inhibit tax aggressive behavior among listed firms.

Few previous studies have utilized internal control as a moderator to investigate the relationships in studies related to ATP, especially within the context of China. This current research introduces internal control as a moderating factor in the associations between ATP behavior and ESG performance because it is assumed that this variable may influence these relationships. It is reasonable to suggest that internal control could impact the relationships between ESG performance and ATP. This rationale supports the hypothesis based on Agency Theory that presented as follows:

H2: Internal control weakened the positive relationship between ESG performance and ATP among Chinese listed firms (Figure 1).

The conceptual framework.

Research Methodology

Population and Sample

The study's population comprises A-share listed firms publicly traded on the Shanghai and Shenzhen Stock markets. The time scope is decided because of the advancement of digital technologies and the implementation of the Third Golden Tax Project in 2016, including big data and cloud computing, which may curb corporate tax avoidance tendencies (L. Su, 2023). Therefore, starting in 2017, this study aims to investigate the effects of a company’s tax planning after the Third Golden tax project has emerged. Moreover, the exclusion of S.T. firms is motivated by abnormal financial issues that could introduce extreme values, affecting the empirical analysis. Second, firms operating in the financial sector are also excluded to mitigate potential bias in reporting regulations (Jiang & Kim, 2022; Wenwu et al., 2023).

This study selects Chinese A-share listed companies as research samples, with a study period from 2017 to 2022. Data retrieved from the Chinese stock market and accounting research database (CSMAR) were filtered based on the following criteria:

(1) Due to missing data or late listing dates for some companies, samples with missing data were excluded;

(2) Considering the possibility of outliers and financial loss that might influence the results, special treatment (ST) and ST* type companies were excluded. After applying the criteria mentioned above, 2,137 listed companies from 2017 to 2022 were obtained, comprising 12,822 research samples. All variables undergo Winsorization at the 1st and 99th percentiles.

Measurement Scales

Dependent Variable-Aggressive Tax Planning

The main emphasis of this study is ATP, which acts as the dependent or explained variable. Previous studies typically utilized three measures to represent tax aggressiveness: RATE, BTD, and DD. RATE quantifies the difference between the applicable or statutory tax rate (STR) and the effective tax rate (ETR). In China, ETR is influenced by tax avoidance strategies and by statutory tax rates, which vary significantly across regions, industries, and corporate structures (Liu et al., 2022). Consequently, a low ETR may stem from preferential tax rates and tax avoidance activities. Even if two firms exhibit similar ETRs, their tax aggressiveness may differ due to variations in statutory tax rates. Thus, ETR does not solely reflect tax aggressiveness accurately. Conversely, RATE eliminates the impact of statutory tax rates, providing a more precise measure of tax aggressiveness (K. Su et al., 2019). The second measure, BTD, calculates pretax income minus taxable income, scaled by beginning total assets. The third measure, DD, represents the residual from regressing total book-tax differences on total accruals and firm fixed effects (Han et al., 2021).

Independent Variables-ESG Performance

ESG performance is one of the independent factors employed to assess a company's performance in corporate governance, social responsibility, and environmental protection in the current academia. Previous studies have commonly used aggregated and sub-dimension ESG performance ratings from various third-party rating agencies to evaluate ESG performance. In this study, the Huazheng ESG Rating Index is utilized to collect aggregated ESG performance ratings, which are widely utilized in Chinese ESG research, The ESG performance concept, introduced by Goldman Sachs in 2007, is internationally represented by systems like Sustainalytics, Thomson Reuters, and Dow Jones. However, these systems often fail to accurately measure the ESG performance of Chinese companies due to limited understanding of China's unique context.

In contrast, China's Huazheng ESG rating system, tailored to local conditions, incorporates corporate governance evaluation and rural revitalization data, making it more suitable for assessing the ESG performance of Chinese firms. The index is segmented into nine grades: C, CC, CCC, B, BB, BBB, A, AA, and AAA, each corresponding to values from one to nine. Higher ESG ratings indicate firms with better ESG performance (Jiang et al., 2024; Zhang et al., 2024; Zheng & Talib, 2024).

Moderating Variable- Internal Control

In this study, internal control is considered a crucial dimension of corporate governance and serves as a moderating variable to examine whether CEO attributes and ESG performance influence ATP. Internal control may also impact the alignment of interests between firm owners and managers regarding corporate activities, including ATP. The DIB internal control index, which was chosen for measurement in this study, was initially introduced in 2011 through collaborative research by Shenzhen DIB Company and Xiamen University, lending it high credibility. The index encompasses five internal control elements, providing a more objective and comprehensive assessment of effectiveness of various enterprises' internal control system. It can be applied to companies across different regions and industries, ensuring comparability between the enterprises (X. Li et al., 2018).

This study utilizes the DIB Internal Control Index to evaluate the quality of a firm's internal control. The index is scored on a scale from 0 to 1,000, with higher levels indicating more robust internal control. An index score of 0 signifies a significant internal control deficiency. The index value is normalized by dividing it by 1,000, where higher values represent superior internal control quality (H. Chang et al., 2020). In this study, IC is used to denote Internal control.

Control Variables

Based on prior studies, several additional variables have been included to control other possible determinants of a crash likelihood. This study considers firm size and leverage variables that account for potential influences or variations on the dependent variable.

Firstly, firm size is represented as SIZE and is calculated as the natural logarithm of total assets (W. Huang et al., 2018; Jin, 2021). Large companies often have more available resources to efficiently carry out tax planning and succeed in political lobbying campaigns to reduce their tax burden (K. Su et al., 2019). In addition, S. Chen et al. (2010) uncovered no significant correlation between firm size and ATP. Consequently, their study claimed that more tax aggressiveness positively correlates with firm size. Second, leverage is determined by dividing total debt by assets (Assidi et al., 2022).

Leverage (Lev), in this context, acts as a control variable to consider the influence of corporate financing decisions on tax aggressiveness or tax planning. A positive coefficient linked with leverage implies that high-leverage companies gain advantages from interest expense deductions compared to their counterparts. Conversely, a negative correlation between leverage and the effective tax rate would suggest that firms use long-term debt as an alternative to other tax planning strategies (Ogbeide, 2019). Furthermore, other key control variables, such as independent directors (Indep_director), might mitigate the motives of tax aggressiveness practices (James, 2020; Lanis et al., 2018). Different ownership structures (state-owned or non-state-owned enterprises), Firms with state-owned assets are subject to higher government oversight than private firms. Thus, private firms are more likely to engage in tax aggressiveness compared to state-owned enterprises (SOEs) (M.-L. Chang et al., 2019; Yuan et al., 2022); other firm-specific control variables, including board size (BS), revenue growth rate (Grow), equity concentration (Top1) are also considered to influence the ATP. Thus, this study controls those potential influences.

Models Specification

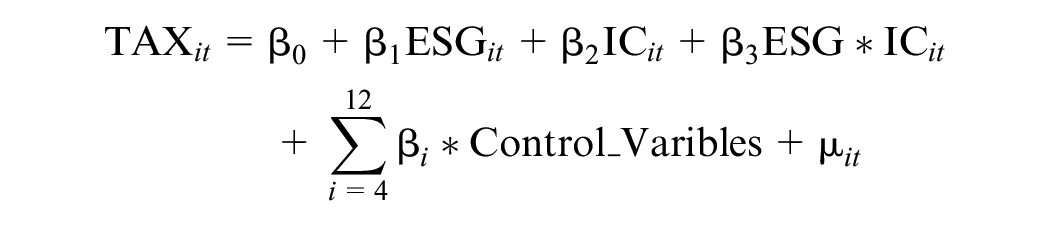

This study utilizes the following regression equation to investigate the influence of ESG performance on ATP (Represented as TAX). The nature of the data being panel data allows for applying panel data methods. Panel data entails the collection of observations over multiple periods. The general structure of the panel data model 1 can be delineated as follows:

Subsequently, this study investigates the impact of internal control on ESG performance concerning their influence on ATP behavior. The moderating variable of internal control (Represented as IC) and the corresponding interaction terms are collectively integrated into Model 2, as depicted below:

Empirical Analysis

Descriptive Statistics

The study takes the ATP of each company as the dependent variable and studies the impact of ESG performance on ATP. Additionally, variables such as financial leverage, firm size, proportion of independent directors, property rights, board size, revenue growth rate, and equity concentration that have been selected are controlled. The internal control is also chosen as a moderating variable for moderation on regression. Based on the selected variables, the research model is set as the following panel regression model:

The moderation effect model is as follows:

Where TAX represents ATP, ESG represents ESG performance, IC represents Internal Control Index, Indep_director represents independent directors, SOE represents property rights, BS represents board size, LEV represents financial leverage ratio, GROW represents revenue growth rate, SIZE represents firm size, and Top1 represents equity concentration. β0 represents the constant term, and β i represents the regression coefficients of each variable. Table 1 shows the descriptive statistical results of each variable:

Descriptive Statistics of Variables.

Table 1 shows that the standard deviation of ATP is 0.049, indicating that there is not much variation in ATP among the sample companies in this research. The standard deviation of ESG performance is 1.114, indicating a significant variation in ESG performance among different firms. The standard deviation of independent directors is 69.87, showing a considerable difference in independent directors among the companies. The mean value of property rights is 0.378, suggesting that there are relatively fewer samples of companies with specific property rights in the research sample from China. The standard deviation of board size is 1.64, indicating a significant difference in board sizes among the companies. The mean value of the revenue growth rate is 0.149, suggesting that the overall total assets of the research sample companies are experiencing positive growth. The standard deviation of firm size is 1.323, indicating a significant difference in firm sizes among the companies. The standard deviation of equity concentration is 14.48, showing a considerable difference in equity concentration among the companies.

Regression Results

Correlation

A correlation matrix was conducted between each independent variable and the dependent variable ATP, and the results are shown in Table 2.

Correlation Matrix.

Note. t statistics in parentheses, *p < .10, **p < .05, ***p < .01.

Table 2 shows that the correlation coefficient between ESG performance and ATP is .120, and it is significant, which indicates a positive correlation between ESG performance and ATP. Among the control variables, property rights, board size, firm size, and equity concentration have positive and significant correlation coefficients with ATP, which means that the property rights, board size, firm size, and equity concentration are positively correlated with ATP. On the other hand, the correlation coefficient between the financial leverage ratio and ATP is negative and significant, indicating a negative correlation between the financial leverage ratio and ATP. However, the independent directors' correlation coefficient is insignificant, suggesting a weaker correlation between independent directors and ATP.

Multi-Collinearity Test

Firstly, a multi-collinearity test was conducted for each variable, as shown in Table 3. From the multi-collinearity test results, it can be observed that the Variance Inflation Factor (VIF) for each variable is less than 10, indicating that there is no multi-collinearity among the variables (Maas, 2022; Wen et al., 2020).

Multi-Collinearity Test.

Baseline Regression Results

Firstly, the benchmark regression model is analyzed, and the results are shown in Table 4.

Baseline Regression Results.

Note. t statistics in parentheses, *p < .10, **p < .05, ***p < .01.

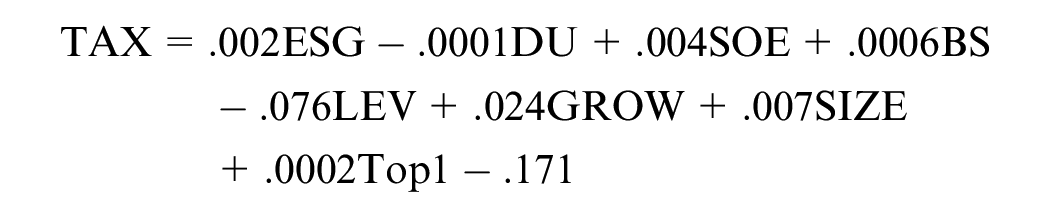

Based on the baseline regression results, the model passed the F-test at the 1% significance level, indicating that the overall regression model performs well with a goodness of fit of .1274, meaning that the variables collectively explain 12.74% of the variation in ATP. From the regression coefficients, the baseline regression equation can be derived:

The regression coefficient between ESG performance and ATP is .0024, and it has passed the t-test, indicating a positive correlation between them. For every unit increase in ESG performance, ATP will increase by .0024 units, meaning that an increase in ESG performance positively impacts ATP. Hence, this result rejects H1a (a negative correlation between ESG performance and ATP) and accepts H1b (a positive correlation between ESG performance and ATP).

Among the control variables, the regression coefficients for property rights, board size, ROA, revenue growth rate, and equity concentration are as follows: .0042, .0006, .0247, .0077, and .0002, respectively. These coefficients have also passed the t-test. The board size, ROA, firm size, and equity concentration contribute positively to ATP, with an increase of .0006, .0247, .0077, and .0002 units, respectively, for every one-unit increase in these variables.

However, the regression coefficient for the financial leverage ratio is −.0768, and it has also passed the t-test, which indicates that for every one-unit increase in the financial leverage ratio, ATP will decrease by .0768 units. On the other hand, the regression coefficient for the proportion of independent directors is insignificant, indicating that the influence of the proportion of independent directors on ATP is not significant.

Moderation Effect Regression

Further moderation effect regression has been conducted; the results are shown in Table 5.

Moderation Effect Regression.

Note. t statistics in parentheses, *p < .10, **p < .05, ***p < .01.

The moderation effect regression results show that the model has passed the F-test at the 1% significance level, indicating a good overall regression effect. The regression coefficient between ESG performance and ATP is .0621, and has passed the t-test. The regression coefficient between Internal Control and ATP is .1071, and has also passed the t-test. The regression coefficient for the interaction term between ESG performance and Internal Control is −.0095, and has also passed the t-test. This indicates a moderation effect of the Internal Control in the process of the ESG performance’s impact on ATP. In other words, the Internal Control weakens the positive effect of the ESG performance on ATP.

Heterogeneity Regression Results

This study categorizes the research sample into state-owned and non-state-owned entities for heterogeneity regression. The heterogeneity results are shown in Table 6.

Heterogeneity Regression Results.

Note. ***,**,* represent significance levels of 1%, 5%, and 10%, respectively. The values within parentheses indicate the T-statistic.

Based on the heterogeneous regression results for property rights mentioned above, all regressions passed the F-test at the 1% significance level, indicating a good overall regression effect. Looking at the results regarding ESG performance for state-owned enterprises, the regression coefficient between ESG performance and ATP is .0015. It has passed the t-test, which means that for state-owned enterprises, for every unit increase in ESG performance, the ATP will increase by .0015 units. For non-state-owned enterprises, the regression coefficient between the ESG performance and the ATP is .0028. It has also passed the t-test, which implies that for non-state-owned enterprises, for every unit increase in ESG performance, ATP will increase by .0028 units. In other words, both the state-owned and non-state-owned enterprises’ ESG performance positively impacts ATP, with the positive impact being more pronounced for non-state-owned enterprises.

Robustness Tests

The study finally conducts robustness regression through two methods: narrowing down the sample (using samples from the manufacturing industry), and excluding the research samples from 2020 to 2022 to eliminate the impact of the epidemic. The robustness regression results are shown in Table 7.

The Robustness Regression Results.

Note. ***,**,* represent significance levels of 1%, 5%, and 10%, respectively. The values within parentheses indicate the T-statistic.

The results of both robustness regressions show that the regression coefficients between ESG performance and ATP are positive and have passed the t-test, which indicates a positive correlation between ESG performance and ATP, which means that ESG performance has a positive impact on ATP. This is consistent with the earlier regression results and confirms the robustness of the regression results presented in this study.

Discussions and Conclusions

To date, empirical research on corporate tax aggressiveness is increasing, reflecting the academic research's attention on corporate tax aggressiveness. Based on the above regression results, the findings indicate a positive correlation between ESG performance and ATP based on Agency Theory; this study uncovers an unexpected result, contradicting most of the earlier studies that have suggested that ESG performance reduces tax avoidance, which mainly rely on Stakeholder theory (Jiang et al., 2024; Meng & Zhang, 2023; Yoon et al., 2021). These firms may project a socially responsible image that could encourage firms to engage in more tax aggressiveness driven by cosmetic actions and green washing.

To deal with the above similar problem, internal control could diminish the strong relationship between ESG performance and ATP due to its moderating influence, ensuring compliance with regulatory requirements, financial reporting accuracy, and ethical conduct. Hence, increasingly strong tax administration and corporate government mechanisms may contribute to corporate ESG performance and rationally manage the degree of tax behaviors.

Moreover, internal control could enhance corporate governance by increasing transparency and accountability of ESG performance and sustainable tax decisions. Furthermore, this study shows that non-state-owned firms are more inclined to adopt ATP when they perform better ESG. Based on the heterogeneity regression, SOEs in China face a unique set of regulatory pressures related to tax compliance and government expectations for sustainability; these firms are more likely to be scrutinized by the government and involved less in ATP than their private counterpart. As a result, SOEs are not immune to tax aggressiveness practices if they also believe such actions would enhance their profitability without undermining their social image. On the contrary, Non-state-owned enterprises have less government oversight and a higher focus on shareholder value and short-term gains, consistent with previous literature suggesting that non-state-owned firms might be more corporate tax aggressive (O. Z. Li et al., 2017).

This study aims to offer innovative contributions to the existing literature by exploring the impact of ESG on a firm's tax aggressiveness, with a particular focus on its role in internal control. The findings highlight the importance of collaboration between the government and enterprises to raise awareness of ESG performance and ATP while improving internal control practices among listed firms in China. Pursuing maximum ATP through enhanced ESG performance may be inappropriate and unethical.

First, to address these issues, the government should improve the quality of ESG information disclosure systems by developing scientifically sound frameworks aligned with domestic market laws and characteristics. Establishing transparent ESG practices and disclosure standards is crucial to prevent greenwashing, enhance transparency, and provide reliable data for regulators to evaluate firms' tax strategies in light of their ESG commitments. Enhanced financial and ESG performance disclosures also enable investors and regulators better to understand a company's tax behavior and operational status.

Second, from a corporate governance perspective, enterprises should encourage senior management and employees on ESG principles to involve them in implementation processes and regularly issue ESG reports to improve transparency. Strengthening internal control systems is equally vital, as high-quality internal control enhances shareholder value, mitigates tax avoidance risks rooted in poor governance, and curbs rent-seeking behavior by major shareholders. By fostering better ESG performance and mitigating risks from tax aggressiveness, this study enriches the research on internal control and the economic consequences of tax avoidance, addressing concerns about corporate losses caused by aggressive tax planning.

This study acknowledges several limitations that provide opportunities for future research. First, this study focuses solely on the effect of overall ESG performance on ATP. Future studies could explore the individual impacts of ESG dimensions on ATP to gain a more nuanced understanding. Second, using Huazheng ESG ratings in this study may introduce bias due to its nature as a third-party evaluation agency and its potential overemphasis on governance. Future research could consider alternative ESG rating systems to measure corporate ESG performance more comprehensively. Third, the sample in this study includes all non-financial and non-ST firms. To uncover industry-specific insights, future research could focus on specific industries, such as the supply chain or new energy electric vehicle sectors. Overall, this study aims to inspire further exploration of the relationship between ESG performance and tax aggressiveness in more specialized contexts.

Footnotes

Ethical Considerations

Not applicable

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data can be provided on reasonable request for academic purposes only.