Abstract

In this article, we examine the impact of board internationalization on real earnings management. Using the annual data of 2,899 Chinese listed non-financial firms with 16,638 firm-year observations over the period from 2008 to 2017 for empirical analysis, we find robust evidence that higher proportion of foreign directors on corporate boards reduces real earnings management. Results support the hypothesis that foreign directors increase boards’ effectiveness in monitoring the management and, consequently, lead to less earnings management by corporate executives. Our results are robust to alternative measures of board internationalization, instrumental variable analysis, and adding additional control variables. We further observe that foreign directors are more effective in reducing earnings management in firms with local directors with foreign experience and in Chinese provinces with developed institutional environment. Moreover, Chinese firms complement accrual and real activities–based earnings management, and board internationalization is effective in reducing both types of earnings management. Overall, our findings imply board internationalization improves the quality of reported earnings to outside shareholders.

Keywords

Introduction

Large corporate frauds, such as the Enron and Worldcom scandals, incorporating the fraudulent financial reporting have led to recognize the importance of corporate governance for financial reporting of firms. In this context, recent debate suggests that board members’ diversity, by increasing the board’s effectiveness, has significant influence on the quality of financial reporting and earnings management practices of firms. For example, the appointment of independent (Klein, 2002), female (Adams & Ferreira, 2009; Harakeh et al., 2019; Srinidhi et al., 2011), or experienced and more educated directors (Makaryanawati et al., 2016; Reeb & Zhao, 2013) at corporate boards can improve accounting disclosures quality and reduce earnings management. Another recent and noteworthy addition to this debate is whether and how the board internationalization affects the earnings management practices of firms. We add to this literature by examining how the presence of foreign directors on the boards of Chinese listed firms would affect the real earnings management practices of these firms.

The presence of foreign directors is expected to have either negative or positive association with the level of earnings management. Foreign directors can increase the board’s effectiveness in monitoring the management because of the reasons that they import foreign corporate governance experience, better understand international capital markets, and are more independent of the management and can critically scrutinize the managers for earnings management (Estélyi & Nisar, 2016; Miletkov et al., 2017; Oxelheim et al., 2013; Oxelheim & Randøy, 2003).

On the contrary, foreign directors can reduce the board’s effectiveness because of the reasons that they lack sufficient knowledge of local laws and regulations, have poor board meetings’ attendance, and have weak access to soft information about the firm, and their presence generates language issues in board meetings (Choi et al., 2007; Coval & Moskowitz, 2001; Hahn & Lasfer, 2016; Masulis et al., 2012).

A handful of recent studies have examined the impact of foreign directors at corporate boards on the level of earnings management and largely report the mixed results. For instance, some studies find that the presence of foreign directors increases board effectiveness and reduces earnings management and thus it is beneficial (Du et al., 2017), while others find that this presence reduces board’s effectiveness and increases earnings management and thus it is costly (Hooghiemstra et al., 2019).

One shortcoming of both of these studies is that they measure only accrual-based earnings management. However, managers can manage earnings through both the accounting accruals and real activities (Cohen et al., 2008; Zang, 2012). In accrual-based earnings management, managers use judgment in financial accounting to manipulate accruals (Healy & Wahlen, 1999), such as delaying asset write-offs or under-provisioning for bad debt expenses, to meet or beat certain earnings thresholds. On the contrary, in real activities–based earnings management, managers take actions regarding operational activities that deviate from normal business practices (Roychowdhury, 2006), such as the overproduction to reduce cost of goods sold, temporary increase in sales, or decrease in discretionary expenditures, with the purpose to meet certain earnings targets. Some studies have found that managers can use accrual-based and real activities–based earnings management as substitute for each other (Achleitner et al., 2014; Cohen et al., 2008; Zang, 2012). Thus, measuring the earnings management just with accruals can give misleading results if managers manipulate real activities for meeting earnings benchmarks; the findings of previous studies regarding the effect of board diversity on accruals-based earnings management may not hold after taking into account the extent of real activities–based earnings management. Therefore, in this study, our main measure of earnings management captures the level of earnings management through real activities. Besides, we use accrual-based earnings management for additional tests. Another reason to incorporate the real activities–based earnings management into analysis is that, unlike accrual-based earnings management where managers use accounting rules and manipulate earnings through accruals without real cash flow effects, real activities–based earnings management is achieved by manipulating the timing and scale of investments, operations, or financing transactions with real adverse economic effects (Kim & Sohn, 2013).

Focusing on Chinese context is ideal due to at least two factors. First, Chinese firms have incentives not only to manage earnings but to do so with real activities manipulation. China Securities Regulatory Commission (CSRC) has largely used an administrative governance approach to regulate China’s stock market (Pistor & Xu, 2005). CSRC relies on accounting numbers, especially return on equity ratio, to give approval for IPOs (e.g., initial public offerings), to assess a firm’s request for rights issue and to decide to de-list a public firm. This kind of regulatory approach provides strong incentives to listed firms to manage earnings to meet or beat earnings thresholds. Several studies have pointed out that Chinese firms are relying more on real activities manipulation to manage earnings as compared with accrual-based earnings management (Chen et al., 2008; Dong et al., 2020; Ho et al., 2015; Kuo et al., 2014; Szczesny et al., 2008). For instance, Chen et al. (2008) argue that “With rigid rule-based accounting standards, earnings management through accounting method choice and discretionary accruals is rare in China.” (p. 266) In the same vein, other studies have reported several instances of increase in real earnings management. They find that Chinese firms managed earnings more through real activities to meet regulation-imposed earnings threshold (Szczesny et al., 2008), after the share split reform in 2005–2007 (Kuo et al., 2014) and after the adoption of International Financial Reporting Standards (IFRS) in 2006 (Ho et al., 2015). In a more recent contribution, Dong et al. (2020) observe that real earnings management is getting more and more important for Chinese firms over recent years.

Second, China, despite rapid economic growth over the last four decades, is still an emerging economy which suffers from underdeveloped management practices (Syverson, 2011; Wen et al., 2020). The “Going Global Strategy” was formally initiated by the Chinese government in 1999 to encourage Chinese businesses to invest abroad. The pace of Chinese companies’ internationalization further accelerated with the announcement of “Belt and Road Initiative” by the President Xi Jinping in the year 2013 while visiting Kazakhstan and Indonesia. Chinese firms are taking the full advantage of these openness strategies. For example, Chinese outbound investments, especially after the financial crisis of 2008, have recorded a robust growth and the China ranked the second largest exporter of capital in the world in 2016 (United Nations Conference on Trade and Development [UNCTAD], 2017). As the openness urges financial and governance reforms to compete internationally (Ashraf, 2018; Ashraf et al., 2021), the Chinese firms are embracing the need to diversify corporate boards by appointing foreign directors with international exposures (Du et al., 2017). Moreover, Chinese government has devoted great effort to attract talent with foreign experience since the 1990s (Giannetti et al., 2015). For instance, government suggested talent promotion as national strategy in 2002. “The Thousand Talents Program,” which provides returnee talents with extraordinary benefits, including high salaries, housing allowances, jobs for spouses and schooling for children, was launched in 2008. Whether these programs are paying off in terms of improvement in the management of corporate sector is still a question to explore. In this backdrop, it is important to examine the impact of foreign directors on Chinese companies’ practices with very recent data.

For empirical analysis, we use the data of 2,899 Chinese A-share listed non-financial firms over the recent period from 2008 to 2017. The most critical empirical challenge was to collect the data of foreign directors at corporate boards. We hand-collected these data by searching the information about each director’s nationality either from the Wind database or published financial statements and websites of related companies. Following Roychowdhury (2006), we measure the level of real earnings management based on the abnormal levels of cash flows from operations, discretionary expenditures, and production costs. Board internationalization is mainly captured by the ratio of foreign directors to total directors on corporate board. Overall, our findings show that the board internationalization reduces real earnings management. Our results are robust to alternative measures of board internationalization, instrumental variable analysis, and adding additional control variables. We further observe that foreign directors are more effective in reducing earnings management in firms with local directors with foreign experience and in Chinese provinces with developed institutional environment. Moreover, Chinese firms complement accrual and real activities–based earnings management, and board internationalization is effective in reducing both types of earnings management.

Our study is different in various ways from a related paper by the Du et al. (2017). First, Du et al. (2017) use a sample of 11,529 firm-year observations of Chinese firms over the period 2004–2012. In contrast, our sample, which consists of 16,638 firm-year observations over the period 2008–2017 is much larger and more recent. Second, they examine the impact of presence of foreign directors on accrual-based earnings management, while we mainly investigate their impact on real earnings management. Third, we also examine that Chinese firms complement accrual and real earnings management, and the presence of foreign directors reduces both types of earnings management by firms.

We contribute to the existing literature in at least two ways: First, we complement the studies which examine the impact of board internationalization on firm performance (see, for example, Coval & Moskowitz, 2001; Hahn & Lasfer, 2016; Masulis et al., 2012; Miletkov et al., 2017; Oxelheim & Randøy, 2003; and others). Overall, these studies report mixed evidence. For instance, Oxelheim and Randøy (2003) report that Nordic or Swedish firms, which have outsider Anglo-American board members, display a significantly higher value as compared with the firms without such outsiders on board. Further in this regard, Miletkov et al. (2017) explore that the impact of foreign directors on firm performance depends on legal institutions and foreign directors have more strong positive effect on firm performance in the countries with lower quality legal institutions. On the contrary, Masulis et al. (2012) find that firms with foreign independent directors make better cross-border acquisitions; however, foreign directors have poor board meeting attendance records and are associated with a higher CEO compensation, a lower sensitivity of CEO turnover to performance, and a greater likelihood of intentional financial misreporting. Choi et al. (2007) and Hahn and Lasfer (2016) find that foreign directors have poor board meeting attendance record due to the geographic distance between their place of residence and corporate head quarters. Coval and Moskowitz (2001) show that foreign directors have weak access to information about on whose board they sit due to cutting off from local networks that provide valuable soft information. Hahn and Lasfer (2016) suggest that there is a trade-off between increased board diversity with foreign directors and reduced monitoring through fewer meetings. The combined effect of low meeting frequency and the presence of foreign directors is that internal corporate governance mechanism weakens, advisory role benefits of foreign directors reduce, and agency conflicts exacerbate significantly. We add to these studies by examining the impact of foreign directors on the level of earnings management in firms.

Second, our major contribution is to the literature which examines the role of foreign directors in controlling earnings management (Du et al., 2017; Hooghiemstra et al., 2019). These studies largely have measured accrual-based earnings management only and report mixed results. We add to this literature by examining the impact of foreign directors on both the accrual-based and real activities–based earnings management.

The study is organized as follows. The “Theoretical Framework and Hypotheses Development” section presents the theoretical background and the testable hypotheses for the study. The “Data Collection and Variables” section outlines the data collection procedures and variable definitions. The “Empirical Analysis and Results” section introduces empirical methodology and results. Final section concludes the study.

Theoretical Framework and Hypotheses Development

The agency problems arise in modern firms due to the separation of ownership and control (Jensen & Meckling, 1976); that is, self-interested managers, who manage and control the firm, can behave opportunistically and can try to maximize their own benefits at the expense of shareholders, who own the firm but do not participate in management. The board of directors (BoD), who usually are elected by shareholders, monitors the managers on behalf of shareholders and thus provides the corporate governance mechanism to reduce agency problems.

One key example of agency problems is the low-quality financial reporting where managers manage earnings to mislead shareholders or other investors. Earnings management is a practice where corporate managers present an overly positive view of a company’s business activities and financial position.

Corporate board diversity in terms of directors’ independence, gender, age, and education matters, and is the subject of recently heated academic debate. Diversity has both benefits and costs (Adams et al., 2015). On one hand, it may affect firm performance by improving the monitoring role of the board and providing more resources for decision making. As one main function of the board is to monitor self-interested managers (Fama & Jensen, 1983; Hart, 1995), a board with an adequate number of independent directors and having directors equipped with different skills and capabilities should be able to monitor managers optimally. On the other hand, diversity may raise decision-making costs and increase the likelihood of conflict and factions in teams. As such, empirical evidence is also inconclusive; although some studies report a positive effect of board diversity on firm performance, others predict a negative or no significant effect (Erhardt et al., 2003; Post & Byron, 2015; Tasheva & Hillman, 2019).

Recently expanding literature has also examined the impact of board diversity on earnings management practices of firms with inconclusive findings. For instance, one strand of the studies find that having more directors who are independent, female, or with financial expertise increases the quality of financial reporting by reducing the opportunistic earnings management activities by the managers (Cornett et al., 2009; Klein, 2002; Man & Wong, 2013; Saona et al., 2020). While another strand of studies report that the impact of corporate governance mechanisms on earnings management is not consistent across firms (Feng & Huang, 2020).

One potentially ignored area in this regard with scant research is how board diversity in terms of directors’ nationality affects earnings management practices of firms. Like other corporate governance attributes, the exact impact of board diversity in terms of directors’ nationality on corporate performance is difficult to predict.

The presence of foreign directors on board can increase, or decrease, the board’s overall effectiveness in monitoring the management, and thus the level of earnings management by the managers. It can help in curbing the earnings management by increasing the monitoring of management due to higher openness and independence among board members and by transferring the foreign best governance practices. Board members with same nationality often share same cultural values and thus might have strong preference for courtesy and politeness in discussions and issues handling. On the contrary, as foreign directors come from a totally different background, they are more independent from the national elites and their presence may encourage more openness and frankness in board discussions (Gregorič et al., 2017; Oehmichen et al., 2017; Oxelheim & Randøy, 2003). Furthermore, foreign directors reduce the level of cohesiveness in board, think more independently, and can easily promote cognitive conflict by raising controversial issues (Forbes & Milliken, 1999). Moreover, foreign directors who have learnt best corporate governance practices in other countries, especially with developed corporate governance frameworks, help in improving local corporate governance by transferring the knowledge about best corporate governance practices learnt in other countries (Iliev & Roth, 2018).

Besides open discussions and independence, in the context of emerging market economies such as China, foreign directors, with background and experience from countries with developed corporate governance mechanisms, may bring in ethic improvement and advanced management techniques. Adding such directors to boards, therefore, is likely to increase the boards’ effectiveness in monitoring the managers. Because of these effects, we expect a negative association between the presence of foreign directors and Chinese firms’ earnings management practices.

On the contrary, the presence of foreign directors on board can decrease the monitoring of management due to the foreign directors’ lack of knowledge of local laws and regulations and language issues (Hooghiemstra et al., 2019; Piekkari et al., 2015), and resultantly can lead to higher earnings management. Foreign directors’ may lack the knowledge of local laws, regulations, accounting rules, and governance styles. Financial reporting standards and governance styles entail rigorous technical details (Dhaliwal et al., 2010), which are necessary to understand the level of earnings management in general, and the extent of earnings management incorporating managers’ opportunistic behavior, in particular. And the lack of such detailed knowledge may lead to foreign directors’ inability to effectively monitor the management (Hooghiemstra et al., 2019). Consequently, the presence of foreign directors indeed can result in the higher level of earnings management.

Another issue with the presence of foreign directors is the language barrier. Language barrier can affect board discussions in two ways: First, it may be difficult for foreign directors to communicate and understand the other directors who are mostly speaking the Chinese language. Second, with the appointment of foreign director, the language of the board meeting might need to be changed to English instead of Chinese, which makes it difficult for Chinese-origin directors to communicate in non-native English language. Language barrier may lead to impoverished and silenced discussions. For example, Piekkari et al. (2015) argue that board members with a different language may find it difficult to contribute to board meetings and articulate disagreements. Resultantly, overall board effectiveness in monitoring the management might decrease and the level of earnings management might increase due to language barriers created by the presence of foreign directors.

Data Collection and Variables

Data Collection

In this study, the most critical empirical challenge was to collect the data of foreign directors at the boards of Chinese A-share listed companies. We started sample construction with all companies listed on Shanghai and Shenzhen stock markets. First, we hand-collected the data of nationalities of directors of these companies from their publicly disclosed resumes in firms’ annual reports and cross-check the data with Baidu (http://baikebaidu.com) and Sina (http://finance.sina.com.cn) to ensure the accuracy of the data. Next, we downloaded accounting and corporate governance data from China Stock Market and Accounting Research (CSMAR) database. Then, we appended both datasets together. Finally, we excluded firms in financial industry due to different financial regulations, eliminated firm-years without sufficient information to compute earnings management measures, and dropped the observations with missing necessary data. As a result, our final dataset included 16,638 firm-year observations for 2,899 companies over the period from 2008 to 2017. We winsorized firm-level continuous variables at 1% and 99% levels to eliminate outliers.

Variables

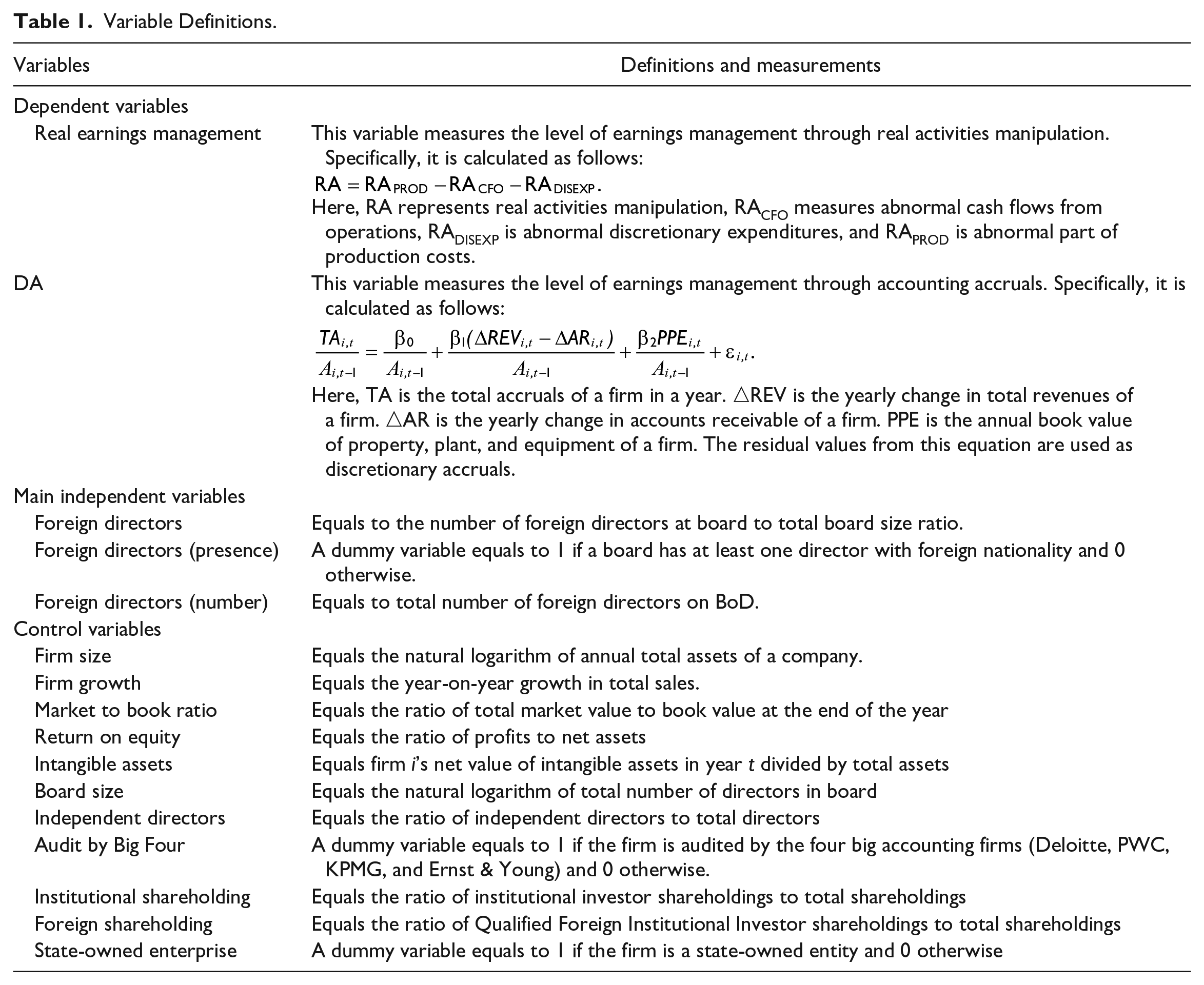

Dependent variables

Our main dependent variable is real earnings management. Following Roychowdhury (2006), we estimate the level of real earnings management based on the abnormal levels of cash flows from operations (RACFO), discretionary expenditures (RADISEXP), and production costs (RAPROD). For each firm-year, the abnormal level of RACFO, RADISEXP, and RAPROD is the difference between the actual value and the normal value, calculated as standardized residuals from the following three equations, respectively. These equations are estimated with cross-sectional ordinary least squares (OLS) regression model for each industry-year.

Here, the subscript t represents the year. △ shows the change from one year to the next. CFO denotes net cash flows from operations. DISEXP represents discretionary expenses and equals the sum of advertising expenses, R&D expenses and selling, and general and administrative expenses. PROD is the sum of cost of goods sold and the change in inventories. A is the total assets and S is the sales.

Next, we use RACFO, RADISEXP, and RAPROD variables to calculate the aggregate real earnings management variable. As at a given sales level, companies which tend to manage earnings upward can have abnormally higher production costs and abnormally lower cash flows from operations and discretionary expenses. Therefore, we calculate real activities–based earnings management as follows by combining the three variables:

Here, higher values of real earnings management variable represent higher real earnings management and vice versa.

Independent main variables

Following previous literature, we measure the extent of board’s internationalization, foreign directors, with the ratio of foreign directors on BoD. Specifically, it is calculated as the ratio of the number of foreign directors to total board size. This variable captures the impact of a higher proportion of foreign directors on the level of earnings management.

In addition, we use two alternative variables, foreign directors (presence) and foreign directors (number), to check the robustness of our findings. Foreign directors (presence) is a dummy variable equals 1 if a board has at least one director with foreign nationality and 0 otherwise. This variable captures the impact of the presence of a foreign director at board on the level of earnings management. Foreign directors (number) equals to the total number of foreign directors on BoD and captures the impact of higher absolute number of foreign directors on the level of earnings management.

Independent control variables

Following existing studies on corporate governance and earnings management (Du et al., 2017; Luo et al., 2017), we add several variables to control for other factors which can affect the level of earnings management in addition to board internationalization. Firm size is measured with the natural logarithm of year-end total asset of a firm. Firm growth is year-on-year growth rate of total sales. Market to book value ratio equals the ratio of total market value to book value at the end of the year. Return on equity is the ratio of profits to net assets. Intangible assets equals firm i’s net value of intangible assets in year t divided by total assets. Board size (Board size) equals the natural logarithm of total number of directors in board. Board independence (Independent directors) equals the ratio of independent directors to total directors. Audit by Big Four is a dummy variable equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding is the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding is the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise is a dummy variable equals to 1 if the firm is a state-owned entity and 0 otherwise.

Table 1 summarizes the definitions and measurements of all the variables.

Variable Definitions.

Empirical Analysis and Results

Empirical Model

We specify following pooled panel OLS model for empirical analysis.

Here, i and t subscripts represent firm and time, respectively. DV is dependent variable. We use real earnings management as main dependent variable. IV represents the main independent variable of interest which is the ratio of foreign directors at corporate boards. CV represents other control variables. We also include year and industry dummy variables to control for year and industry fixed effects. Heteroscedastic robust standard errors are used in analysis.

Empirical Results

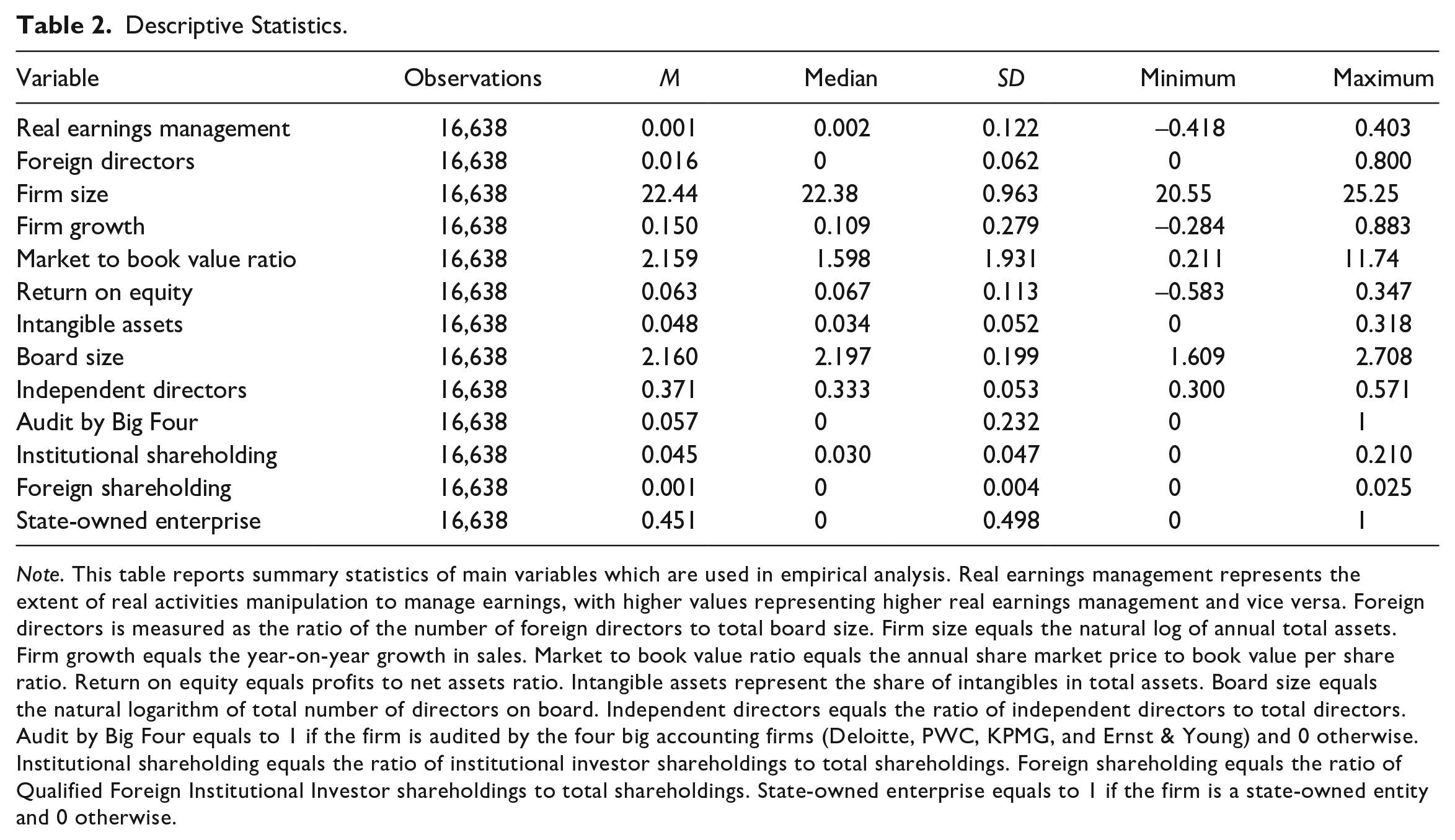

Descriptive statistics

Table 2 reports the descriptive statistics for main variables. The mean value of real earnings management equals 0.001 which is comparable with Cohen et al. (2008) who also found a 0.000 mean value. Similarly, the 0.017 mean value of the ratio of foreign directors on BoD indicates that on average, a board has 1.7% foreign directors at boards for sample companies. All these variables have considerable variation across mean values as shown by their standard deviations.

Descriptive Statistics.

Note. This table reports summary statistics of main variables which are used in empirical analysis. Real earnings management represents the extent of real activities manipulation to manage earnings, with higher values representing higher real earnings management and vice versa. Foreign directors is measured as the ratio of the number of foreign directors to total board size. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise.

Table 3 presents the Pearson correlations between each pair of variables. The coefficients of correlations between explanatory variables are not that high suggesting that multicollinearity would not be a concern in multivariate regression model. Bryman and Cramer (2001) suggests multicollinearity problem may exist when the correlation coefficients between independent variables are equal to .80 or higher.

Correlation Matrix.

Note. This table reports pairwise Pearson correlations between main variables. Real earnings management represents the extent of real activities manipulation to manage earnings, with higher values representing higher real earnings management and vice versa. Foreign directors is measured as the ratio of the number of foreign directors to total board size. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise.

Indicates significance at least 5%.

The correlation between board internationalization between real earnings manipulation is negatively significant providing some preliminary evidence that foreign directors are helpful in curbing real earnings management practices in China.

Multivariate regression results

To examine the impact of board internationalization on real earnings management, we estimate Equation 5 by using real earnings management as dependent variable. Results are reported in Table 4.

The Impact of Board Internationalization on Earnings Management—Main Results.

Note. This table reports pooled ordinary least squares (OLS) regression estimation results. Real earnings management is the dependent variable and represents the extent of real activities manipulation to manage earnings, with higher values representing higher real earnings management and vice versa. Foreign directors is measured as the ratio of the number of foreign directors to total board size. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise. The t statistics are in parentheses. FE = fixed effects.

**, and *** indicate significance at 10%, 5%, and 1%, respectively.

As shown, the ratio of foreign directors enters negative and significant with real earnings management in Model 1. Real earnings management remains negative and significant when we add other control variables in Model 2. These results suggest that the higher proportion of foreign directors on corporate boards boosts boards’ effectiveness in monitoring the management and consequently lowering the extent of real earnings management.

Results of control variables are also consistent with expectation. For instance, firms with higher growth rate (as shown by Firm growth and MtoB), profits, intangible assets, institutional ownership, and qualified foreign institutional ownership manage earnings less. On the contrary, state-owned enterprises (as shown by State-owned enterprise) manage earnings more. These results of control variables are consistent with previous studies, such as Arun et al. (2015) and Luo et al. (2017), and validate our empirical model.

Alternative Measures of Board Internationalization

To check the robustness of our findings, we utilize alternative measures of board internationalization that include the presence of foreign directors and the total number of foreign directors as main explanatory variables. As shown in Table 5, the higher number of foreign director and the presence of foreign directors on BoD reduce the level of firms’ real earnings management behavior.

The Impact of Board Internationalization on Earnings Management: Alternative Measures of Board Internationalization.

Note. This table reports pooled ordinary least squares (OLS) regression estimation results. Real earnings management is the dependent variable and represents the extent of real activities manipulation to manage earnings, with higher values representing higher real earnings management and vice versa. Foreign directors is measured as the ratio of the number of foreign directors to total board size. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise. The t statistics are in parentheses. FE = fixed effects.

**, and *** indicate significance at 10%, 5%, and 1%, respectively.

Overall, these results support our H1, while reject H2. Our results for the discretionary accruals are consistent with the study of Du et al. (2017) who found that the presence of foreign directors at the corporate boards of Chinese companies reduces accrual-based earnings management. We add that the presence and higher ratio of foreign directors at the corporate boards of Chinese firms also reduce the level of real activities manipulation by executives to manage earnings. However, our results are different from Hooghiemstra et al. (2019) who found that the presence of foreign directors at the boards of Nordic (i.e., Denmark, Finland, Norway, and Sweden) firms reduces board effectiveness and increases accrual-based earnings management. One likely reason is that foreign directors bring more benefits in emerging countries by transferring the expertise and experience learnt in countries with developed corporate governance system. However, in developed countries, such as the Nordic group, foreign directors might not be much better than local directors.

Alternative Empirical Specification: Change Analysis

To further confirm that our results are not biased due to endogeneity, we follow Wen et al. (2020) and perform change analysis to test whether appointing new foreign directors reduces real earnings management. In Table 6, the dependent variable Δreal earnings management stands for the change in real earnings management, calculated by the variation in real earnings management from the last year to this year. ΔForeign directors represents the variation in the proportion of foreign directors on BoD from year t – 1 to year t. The control variables are also measured by their changes. ΔForeign directors enters negative and significant showing that increase in the proportion of foreign directors at BoD leads to a decline in real earnings management. These findings again support our main results.

Testing the Effect of Foreigners on Earnings Management: Change Analysis.

Note. This table reports pooled ordinary least squares (OLS) regression estimation results. Δ shows that all variables are calculated as change from year t to t + 1. Real earnings management is the dependent variable and represents the extent of real activities manipulation to manage earnings, with higher values representing higher real earnings management and vice versa. Foreign directors is measured as the ratio of the number of foreign directors to total board size. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise. The t statistics are in parentheses. FE = fixed effects.

**, and *** indicate significance at 10%, 5%, and 1%, respectively.

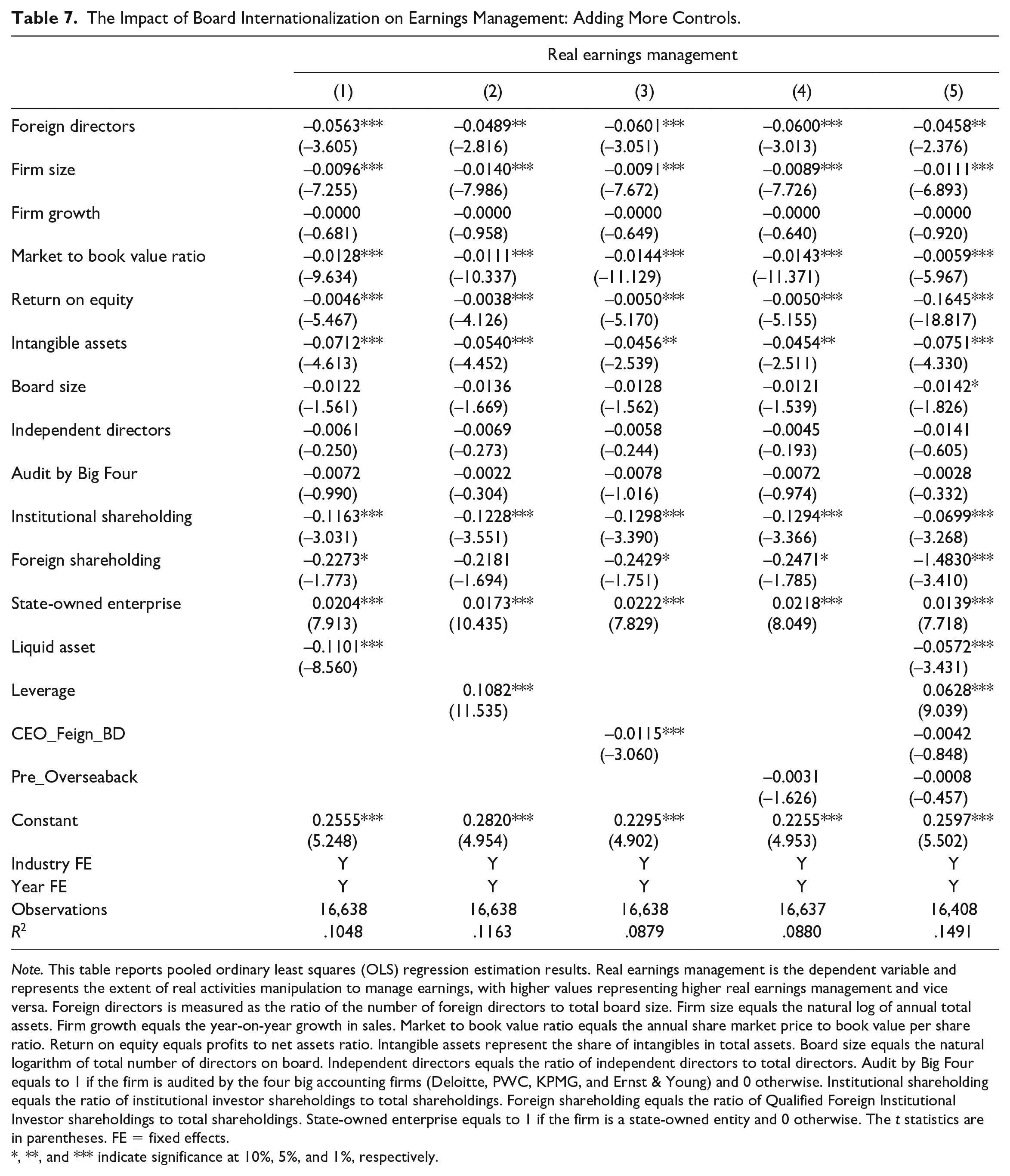

Additional Control Variables

Although we have added several control variables in the main model, to further mitigate the concern that our findings do not suffer from other omitted determinants of firms’ earnings management behavior, we further add more control variables. First, we add firm cash holdings represented with liquid assets and leverage ratio as controls in Models 1 and 2 in Table 7. Second, according to the Chinese Companies’ Law, a CEO can be a member of the BoD. As CEO manages the business and can influence all major corporate decisions, earnings management can decrease due to the foreign CEO who is also a director on the board of same company. In such a case, our proxies of board internationalization may just be capturing the impact of a foreign CEO on earnings management. To disentangle the impact of foreign CEO from foreign directors, we generate a dummy variable (CEO_Feign_BD), which equals 1 if a company has foreign CEO or general manager who is also an executive director and 0 otherwise, to control for foreign CEO’s effect. As shown in Model 3, the results of main variable of interest largely remain same as in Table 4 even after controlling for the effect of foreign CEO. In unreported results, we also dropped the observations with foreign CEO and observed that main results do not change.

The Impact of Board Internationalization on Earnings Management: Adding More Controls.

Note. This table reports pooled ordinary least squares (OLS) regression estimation results. Real earnings management is the dependent variable and represents the extent of real activities manipulation to manage earnings, with higher values representing higher real earnings management and vice versa. Foreign directors is measured as the ratio of the number of foreign directors to total board size. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise. The t statistics are in parentheses. FE = fixed effects.

*, **, and *** indicate significance at 10%, 5%, and 1%, respectively.

Finally, while some members of BoD do not have the foreign nationality, they may still have the foreign experience (e.g., studying or working abroad). Such overseas background may also influence their attitude toward earnings management. To control for this effect, we generate a dummy variable, Pre_Overseaback, which equals 1 if BoD includes other directors with foreign experience and 0 otherwise. As shown in Model 4, the results of main variables are largely intact.

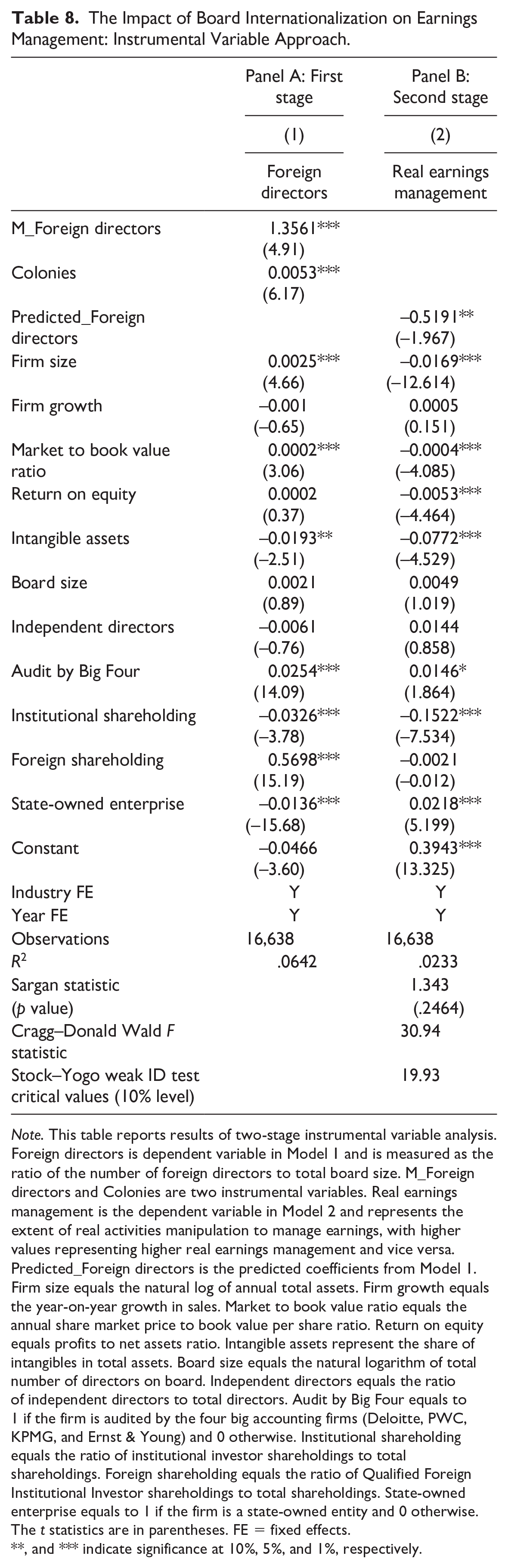

Instrumental Variable Approach

Although we conduct several tests to mitigate the concern of endogeneity, such as estimating the change analysis and adding additional variables in the baseline model, it is still possible that unobservable determinants affect our results. In this section, we use 2SLS instrumental variable approach with two instrumental variables. The first one is the industry-year median percentage of firms appointing directors with foreign nationality (M_Foreign directors). The other one is a dummy variable (Colonies), which equals 1 if a firm is located in a province having a leased territory established by Great Britain during the late Qing dynasty and 0 otherwise (Ang et al., 2014; Wen et al., 2020). Great Britain established leased territory in the following provinces: Fujian province, Hubei province, Jiangxi province, Jiangsu province, Guangdong province, Shandong province, Tianjin, and Shanghai. People living in these provinces have more chances to experience Western culture (Wen et al., 2020). Moreover, the early openness of these regions makes them more easily to attract foreign talents due to their Western-style lifestyles.

As shown in Table 8, the first-stage results in Panel A confirm that coefficients on both, M_Foreign directors and Colonies, are positively significant. In addition, the values of χ2 and F tests suggest that our instruments are valid. The results reported in Panel B still support our main findings.

The Impact of Board Internationalization on Earnings Management: Instrumental Variable Approach.

Note. This table reports results of two-stage instrumental variable analysis. Foreign directors is dependent variable in Model 1 and is measured as the ratio of the number of foreign directors to total board size. M_Foreign directors and Colonies are two instrumental variables. Real earnings management is the dependent variable in Model 2 and represents the extent of real activities manipulation to manage earnings, with higher values representing higher real earnings management and vice versa. Predicted_Foreign directors is the predicted coefficients from Model 1. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise. The t statistics are in parentheses. FE = fixed effects.

**, and *** indicate significance at 10%, 5%, and 1%, respectively.

Discussion

The Effect of Institutional Environment

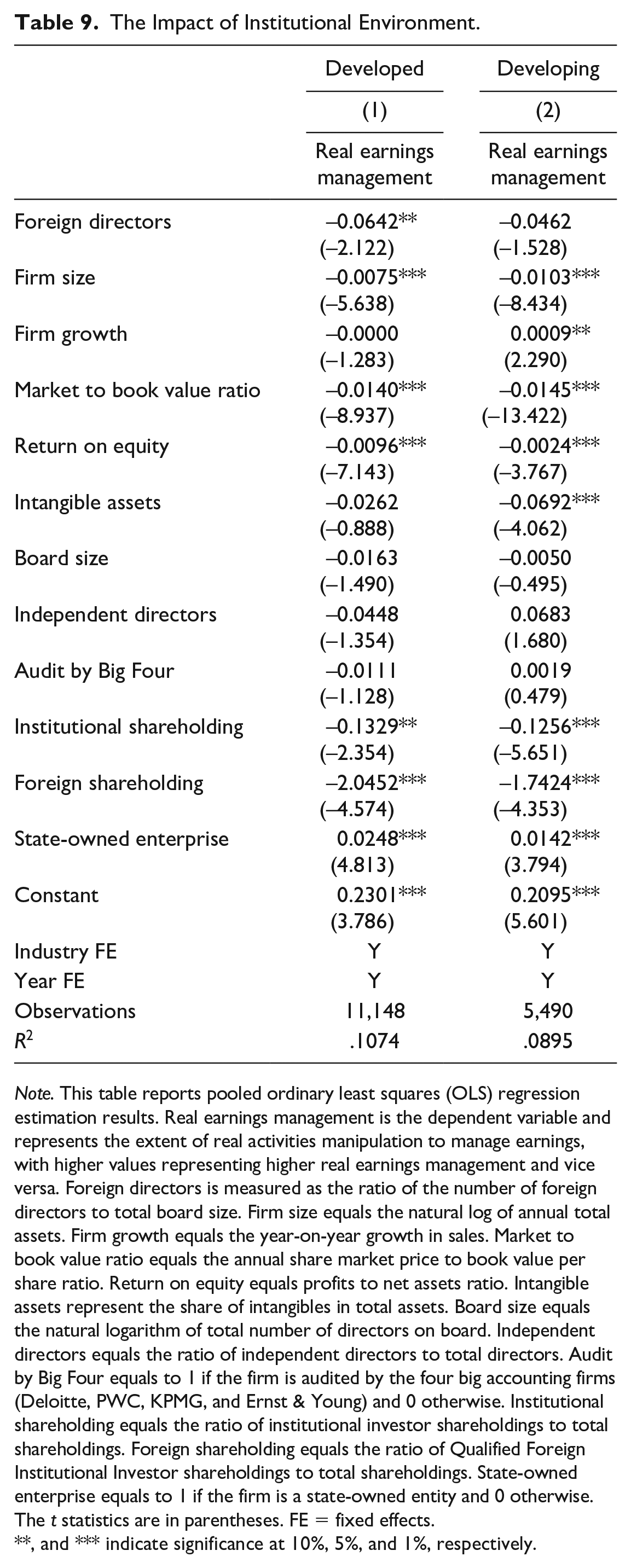

As discussed in the theoretical framework and hypothesis development section, culture and language barriers affect the efficiency of foreign directors’ monitor. Because, at first, it may be difficult for foreign directors to communicate and understand the other directors who are mostly speaking the Chinese language. Second, with the appointment of foreign director, the language of the board meeting might need to be changed to English instead of Chinese, which makes it difficult for Chinese-origin directors to communicate in non-native English language. Hence, foreign directors’ positive effect on curbing the earnings management by increasing the monitoring of management due to higher openness and independence among board members depends on the mitigation of language and culture barrier. Institutional environment affects such barrier. If a firm is located in a province which has the advanced education and is familiar with Western culture, then foreign directors can communicate more easily. We divide our sample into two subgroups based on firms’ location. If a firm is located in eastern coastal China, it is developed institutional environment subgroup, otherwise it is not developed institutional environment subgroup. We run a regression model on the two subgroups and report the results in Table 9. For developed institutional environment subgroup, the coefficients on Foreign directors in columns (1) and (3) are negative and significant. For not developed institutional environment subgroup, however, the coefficients on Foreign directors in columns (2) and (4) are not significant. Thus, the results suggest that the effect of foreign directors on earnings management is more pronounced in firms located in developed institutional environment, consistent with our prediction.

The Impact of Institutional Environment.

Note. This table reports pooled ordinary least squares (OLS) regression estimation results. Real earnings management is the dependent variable and represents the extent of real activities manipulation to manage earnings, with higher values representing higher real earnings management and vice versa. Foreign directors is measured as the ratio of the number of foreign directors to total board size. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise. The t statistics are in parentheses. FE = fixed effects.

**, and *** indicate significance at 10%, 5%, and 1%, respectively.

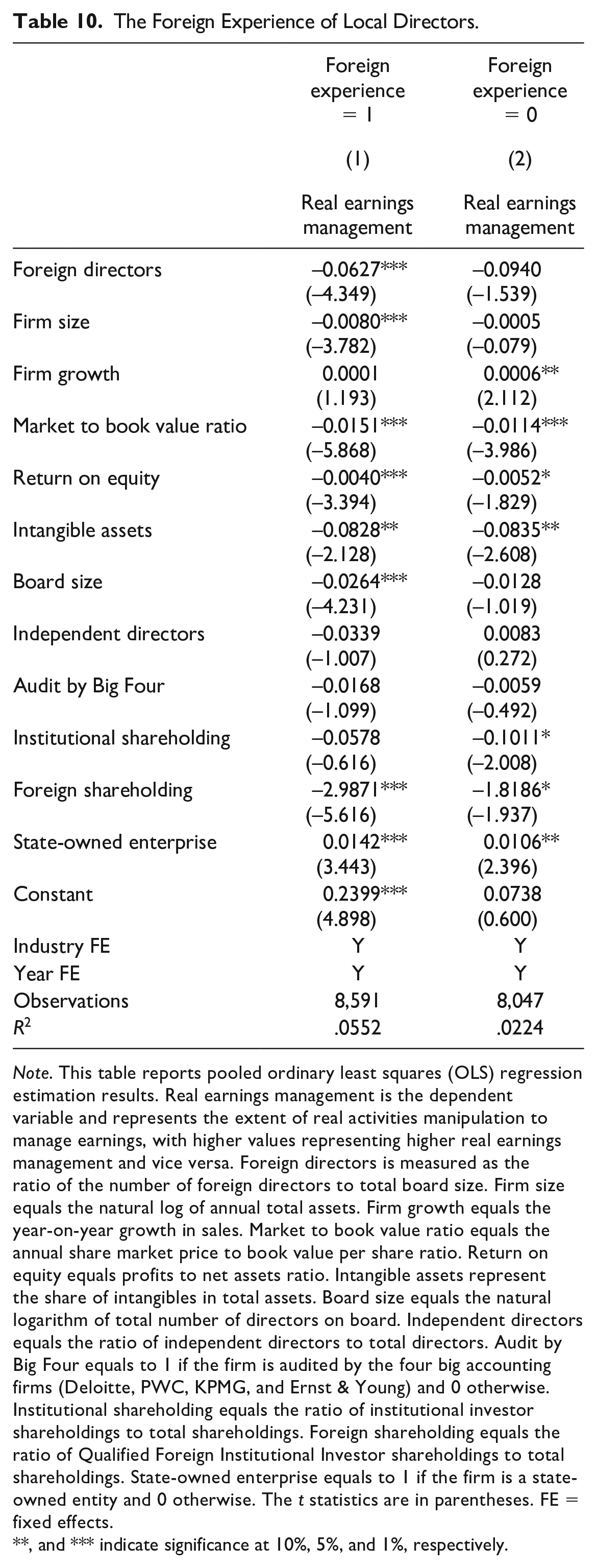

Foreign Experience of Other Directors

The foreign experience of some of local directors should also be considered (Oxelheim et al., 2013). Such experience may increase the effectiveness of foreign directors in improving corporate governance and hence curbing real earnings management practices. When more colleagues can communicate and understand foreign directors’ opinion, BoD effectiveness in monitoring the management would increase. We divide our sample into two subgroups based on other BoD members’ experience. If other BoD members have foreign experiences, it is foreign experience existence subgroup; otherwise, it is not foreign experiences existence subgroup. We run a regression model on the two subgroups and report the results in Table 10. For not foreign experience existence subgroup, the coefficients on foreign directors in columns (1) and (3) are not significant. For foreign experience existence subgroup, however, the coefficients on foreign directors in columns (2) and (4) are negative and significant. Thus, the results suggest that the effect of foreign directors on earnings management is more pronounced in firms, in which other BoD members have foreign experiences, consistent with our prediction.

The Foreign Experience of Local Directors.

Note. This table reports pooled ordinary least squares (OLS) regression estimation results. Real earnings management is the dependent variable and represents the extent of real activities manipulation to manage earnings, with higher values representing higher real earnings management and vice versa. Foreign directors is measured as the ratio of the number of foreign directors to total board size. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise. The t statistics are in parentheses. FE = fixed effects.

**, and *** indicate significance at 10%, 5%, and 1%, respectively.

Component Analysis

We follow Roychowdhury (2006) and measure aggregate real earnings management variable with three components, including the sales manipulation (RACFO), overproduction (RAPROD), and discretionary expenses manipulation (RADISEXP). To further shed light on the impact of board internationalization on real earnings management, we regress three categories one-by-one on board internationalization variable after adding other control variables. As shown in Table 11, foreign directors enter negative with RAPROD and positive with the both RACFO and RADISEXP (note RACFO and RADISEXP inversely measure earnings management). Coefficient of RADISEXP is not significant though. These results suggest that foreign directors have stronger effect in lowering earnings management through the manipulation of cash flows and production costs.

Real Earnings Management Component Analysis.

Note. This table reports pooled ordinary least squares (OLS) regression estimation results. RAPROD, RACFO, and RADISEXP are dependent variables in Models 1 to 3, respectively. RAPROD measures the level of abnormal production costs, with higher values representing higher earnings management and vice versa. RACFO measures the level of abnormal operating cash flows. RADISEXP measures the level of abnormal discretionary expenses. Higher values of both variables represent lower earnings management and vice versa. Foreign directors is measured as the ratio of the number of foreign directors to total board size. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise. The t statistics are in parentheses. FE = fixed effects.

*, **, and *** indicate significance at 10%, 5%, and 1%, respectively.

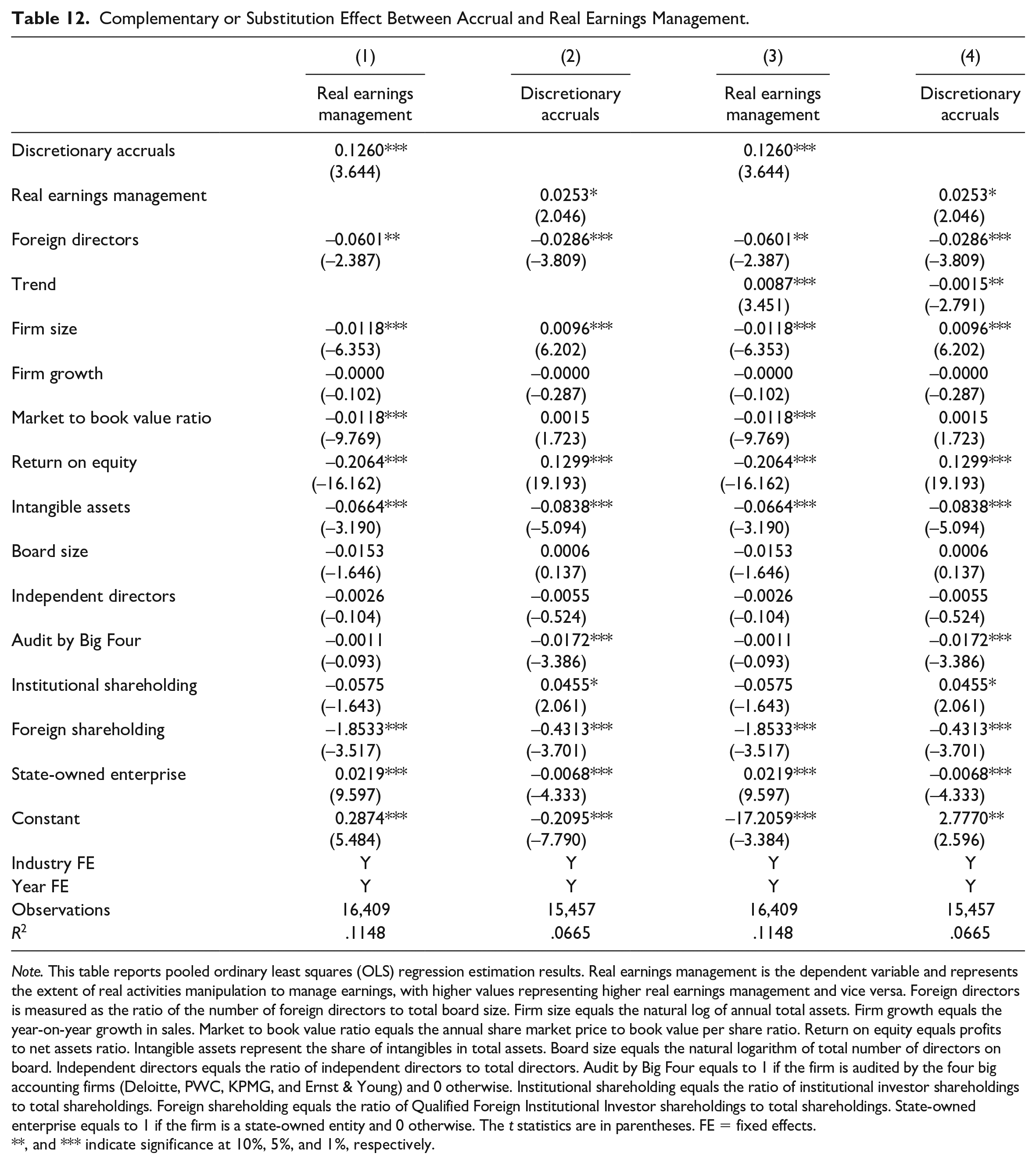

Complementary or Substitution Effect

Literature suggests that managers can substitute or complement discretionary accruals-based and real activities manipulation–based earnings management with each other (Kuo et al., 2014; Luo et al., 2017; Zang, 2012). A potential concern with our results is that firms might have decreased real earnings management by increasing accrual-based earnings management rather than due to the effect of board internationalization. To account for this concern, we calculate discretionary accrual-based earnings management variable and add it as control variable when regressing real earnings management on board internationalization.

We use modified Jones’s model (Dechow et al., 1995; Jones, 1991) to calculate discretionary accruals. The following cross-sectional regression equation is used for estimation.

Here, TA i,t denotes total accruals of firm i for year t, defined as income before extraordinary items minus cash flows from operating activities; Ai,t–1 is total assets of firm i at the beginning of year t; △REV i,t is the change in revenue of firm i between year t and year t – 1; △AR i,t is the change in accounts receivable of firm i between year t and year t – 1; and PPE i,t is the book value of property, plant, and equipment. The absolute residual values from Equation 6 are used as discretionary accruals.

As shown in Table 12 in Model 1, foreign directors variable still enters negative and significant after controlling for discretionary accruals-based earnings management. These results imply that our main results are not biased due to accrual-based earnings management. Accrual-based earnings management variable enters positive with real earnings management suggesting that Chinese firms complement both types of earnings management and are consistent with Kuo et al. (2014). Furthermore, we also observe in Model 2 that board internationalization also reduces the accrual-based earnings management.

Complementary or Substitution Effect Between Accrual and Real Earnings Management.

Note. This table reports pooled ordinary least squares (OLS) regression estimation results. Real earnings management is the dependent variable and represents the extent of real activities manipulation to manage earnings, with higher values representing higher real earnings management and vice versa. Foreign directors is measured as the ratio of the number of foreign directors to total board size. Firm size equals the natural log of annual total assets. Firm growth equals the year-on-year growth in sales. Market to book value ratio equals the annual share market price to book value per share ratio. Return on equity equals profits to net assets ratio. Intangible assets represent the share of intangibles in total assets. Board size equals the natural logarithm of total number of directors on board. Independent directors equals the ratio of independent directors to total directors. Audit by Big Four equals to 1 if the firm is audited by the four big accounting firms (Deloitte, PWC, KPMG, and Ernst & Young) and 0 otherwise. Institutional shareholding equals the ratio of institutional investor shareholdings to total shareholdings. Foreign shareholding equals the ratio of Qualified Foreign Institutional Investor shareholdings to total shareholdings. State-owned enterprise equals to 1 if the firm is a state-owned entity and 0 otherwise. The t statistics are in parentheses. FE = fixed effects.

**, and *** indicate significance at 10%, 5%, and 1%, respectively.

To check the trend of accrual and real activities–based earnings management over time, we introduce a time trend variable in the regressions in Models 3 and 4. Trend enters positive with real earnings management while negative with accruals-based earnings management suggesting that real earnings management is increasing over time while accrual based is going down. This later observation suggests that our focus on real earnings management is a right and timely choice.

Conclusion

This study examines the impact of board internationalization on real earnings management by corporate executives. We use the data of 2,899 Chinese listed non-financial firms with 16,638 firm-year observations over the period from 2008 to 2017. Board internationalization is measured with the ratio of foreign directors to total directors on the BoD. We find robust evidence that board internationalization reduces real earnings management. Our results support the hypothesis that the presence of foreign directors on corporate boards of Chinese companies increases board’s effectiveness in monitoring the management and, consequently, lead to less earnings management by corporate executives. Our results are robust to alternative measures of board internationalization, instrumental variable analysis, and adding additional control variables. We further observe that foreign directors are more effective in reducing earnings management in firms with some local directors with foreign experience and in Chinese provinces with developed institutional environment. Moreover, Chinese firms complement accrual- and real activities–based earnings management and board internationalization is effective in reducing both types of earnings management.

Overall, our results imply that the board diversification in terms of nationality is beneficial. It increases board’s effectiveness and reduces information asymmetries between shareholders and managers by insuring better quality financial disclosures. We support Chinese government’s reform efforts to attract foreign talent to improve management practices within China. Encouraging firms to hire foreign directors might enhance the effectiveness of corporate governance.

In China, corporate firms also have the board of supervisors in addition to the BoD. One limitation of our study is that we do not take into account the extent of internationalization of board of supervisors and is a promising area for future research.

Footnotes

Acknowledgements

We acknowledge the insightful comments from the editor and three anonymous reviewers and the participants of 2019 China Global Management Accounting Conference (Zhongnan University of Economic and Law, Wuhan, China) and various seminars at Jiangxi University of Finance and Economics (Nanchang, China) and East China Jiao Tong University (Nanchang, China) on earlier versions of this manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Ningyu Qian acknowledges the financial support from the Fundamental Research Funds for Central Universities (2021WKYXQN001, 2019kfyXJJS041). The usual disclaimer applies