Abstract

The issue of overcapacity has been a widespread concern in the international community since the global financial crisis. For developing countries, adopting effective measures to alleviate overcapacity is crucial to overcome development bottlenecks and achieve the “dual-carbon” target on schedule. The integration of environmental, social, and governance (ESG) principles, which advocates for clean production and sustainable operation, reshapes the business philosophy of enterprises during their development process and profoundly influences enterprise behavior. It is worthwhile to explore how the ESG performance of Chinese enterprises affects capacity utilization (CU). Using data from 4,100 A-share listed companies over the period 2009 to 2022, the study employs a two-way fixed effects model for empirical analysis. The results of this study are as follows: (a) good ESG performance can enhance enterprises' CU; (b) ESG performance enhances CU by alleviating information asymmetry, improving green innovation capability, and strengthening internal control levels; and (c) the impact is more significant in non-state-owned, small, capital-intensive, and low-carbon industries. This study supports the global adoption of ESG practices and provides insights for addressing overcapacity issues in the context of global decarbonization.

Plain Language Summary

This study focuses on the relationship between ESG performance and capacity utilization (CU) from a green development perspective. This study can enrich the frontier of green finance as well as provide information for companies to realize environmental sustainability. The problem of overcapacity caused by the financial crisis has brought the issue of corporate sustainability to the forefront. The purpose of this paper is to analyze how companies can solve overcapacity through good ESG performance based on sustainable development orientation, and then provide new ideas for developing countries to solve the overcapacity problem in the context of global decarbonization. This paper aims to analyze how enterprises can solve overcapacity through good ESG performance based on sustainable development orientation, and then provide new ideas for developing countries to solve the overcapacity problem in the context of global decarbonization. The main innovation of this paper is to analyze the economic consequences of enterprises’ ESG performance on capacity utilization, which has certain policy implications for promoting enterprises’ sustainable development, overcoming resource and environmental constraints, and promoting society’s green development.

Keywords

Introduction

Overcapacity has been a longstanding issue in the global economy, particularly in China, where numerous industries are grappling with serious overcapacity problems amid rapid economic growth. Lin et al. (2010) argue that overcapacity not only causes resource waste but also undermines enterprise productivity and market competitiveness. In the context of China, Cheng et al. (2019) emphasize that inefficient capacity allocation is a key factor hindering the sustainable development of the country’s manufacturing sector. As the economy transforms and upgrades, traditional high-carbon industries are increasingly prone to generating excess capacity due to supply-demand imbalances, which in turn disrupt the stable growth of the national economy (Ge et al., 2024; Goel & Nelson, 2021). While some scholars suggest that technological advancements and global trade may gradually alleviate overcapacity, the issue remains a substantial challenge in China’s economy, particularly in low-tech and resource-intensive industries.

Environmental, social, and governance (ESG) performance is increasingly recognized as a critical indicator of corporate sustainability. In recent years, ESG has emerged as a central strategy for corporate development worldwide. According to De Falco et al. (2021), strong ESG performance can enhance enterprises’ green innovation capability and provide long-term financial benefits. Similarly, Zhao and Chen (2024) found that enterprises’ ESG performance is closely linked to its financial performance, with effective ESG management contributing to enhanced market competitiveness. However, despite these insights, there is a notable research gap concerning the specific effects of ESG performance on enterprises’ capacity utilization (CU) and its potential role in mitigating overcapacity. Most existing studies focus on the relationship between ESG and enterprise performance (Ahmad et al., 2021), but the exploration of how ESG can address overcapacity, particularly in large manufacturing nations like China, remains underexplored.

Overcapacity primarily results from the mismatch between production capacity and market demand. This issue is particularly prevalent in high-carbon industries, such as steel, cement, and coal, as well as low-tech industries. The rapid expansion of production capacity, coupled with a failure of demand to keep pace, has led to idle or inefficient use of production resources. In China, the overcapacity problem is particularly severe in traditional industries, where it has led to significant resource wastage and environmental pollution. These issues hinder the achievement of the country’s “dual-carbon” goals. While technological advancements and trade development have partially improved productivity, they have not fully resolved the overcapacity problem.

A more effective solution to overcapacity lies in improving CU. To increase CU, enterprises must not only enhance production efficiency through technological innovation but also address inefficient capacity by optimizing resource allocation, improving internal management, and strengthening market demand forecasting. Among these solutions, green technology innovation plays a crucial role. Green innovation helps enterprises optimize production processes, reduce resource consumption, and enhance CU, thereby reducing ineffective capacity.

Excess capacity, especially in high-carbon industries, poses a significant challenge to the dual-carbon goal. Not only does it lead to resource wastage, but it also contributes to higher carbon emissions, thus impeding the transition to a greener economy. One promising approach to addressing overcapacity is by improving ESG performance. By fostering green innovation and adopting low-carbon technologies, companies can better adjust their capacity structure, optimize resource allocation, and reduce excess capacity, particularly in high-carbon industries. This approach will enhance capacity utilization and support China’s green transformation and help achieve the “dual-carbon” goals.

This paper contributes in the following key aspects. (a) While existing research has focused on the relationship between enterprises’ ESG performance and financial performance or green innovation (De Falco et al., 2021; Raimo et al., 2021), there is limited exploration of how ESG performance directly influences enterprises’ CU. This study fills this gap by proposing a mechanism whereby ESG performance enhances CU through reducing information asymmetry, promoting green innovation, and optimizing internal controls. Raimo et al. (2021) highlighted that good ESG performance can reduce enterprises’ financing costs, while De Falco et al. (2021) found that ESG performance fosters innovation in green technologies. Despite these findings, there remains a lack of research on the specific impact of ESG performance on CU. (b) Through empirical analysis, this study identifies three key mechanisms by which ESG performance affects CU: mitigating information asymmetry, promoting green technological innovation, and optimizing internal controls. These mechanisms improve the efficiency of CU, thereby addressing the issue of overcapacity. Zhou et al. (2024) emphasize that green technological innovation is vital for promoting sustainable development, improving production efficiency, and reducing resource waste. Similarly, Chen et al. (2022) found that optimizing internal controls enhances CU and reduces resource waste, ultimately improving enterprise performance. This paper further investigates how ESG performance drives CU through these mechanisms. (c) The findings of this paper offer valuable insights for governments and enterprises on leveraging ESG policies to promote efficient resource allocation. Specifically, in China and other developing economies, ESG initiatives not only support the green transformation of enterprises but also help address the persistent challenge of overcapacity. Arvidsson and Dumay (2022) explored how ESG practices can support green transformation and sustainable development. Building on these studies, this paper underscores the practical importance of enhancing enterprise ESG performance, especially in solving overcapacity problems and promoting green development.

Literature Review

Economic Effect of ESG Performance

The concept of ESG has gained widespread recognition as a “universal language” for international communication and cooperation, owing to its inclusiveness and universality in promoting sustainable development. Furthermore, various market players, including the public, enterprises, financial institutions, and regulators in different countries, have maintained a high level of attention to ESG issues. Scholars have identified several benefits associated with strong ESG performance, including reduced corporate financing costs (Raimo et al., 2021), improved enterprise performance (Ahmad et al., 2021), greater foreign investment in listed enterprises (Tampakoudis & Anagnostopoulou, 2020), higher employment rates (Zhao & Chen, 2024), enhanced innovation output (De Falco et al., 2021), and the promotion of enterprises’ green transformation (Arvidsson & Dumay, 2022). Moreover, some scholars have examined business risk (Albuquerque et al., 2019; Abate et al., 2021), the quality of financial audits (Asante-Appiah, 2020), future stock returns (Deng & Cheng, 2019; Stotz, 2021), the extent of enterprises’ short-term debt and long-term use (Al Amosh et al., 2022), and other dimensions to analyze the economic impact of enterprises’ ESG performance. The existing literature has explored the economic impact of corporate ESG performance, offering valuable insights and lessons for this research. However, it has not yet addressed the impact of enterprise ESG on CU.

Factors Affecting Enterprises’ CU

Academic research on CU has concentrated on macro, industry and enterprise level studies. At the macro level, studies by Greenwood et al. (1988) and Gilchrist and Williams (2005) integrate investment, uncertainty, and capital utilization into the analysis of capacity within the framework of economic cycle theory. Industry-level models, such as those proposed by Manne (1961), Newsboy, and Whitt (1981), examine variations in industry-specific factors, illustrating how shifts in industry capacity correlate with demand fluctuations, the number of firms, capital intensity, and economies of scale in investment. In the case of China, scholars have focused on governmental factors to analyze the problem of CU. Jiang and Cao (2009) attribute overcapacity to incomplete marketization and excessive government intervention, arguing that policy subsidies create “excessive competition” resulting in overcapacity in industries such as iron and steel, cement, and photovoltaics (Geng et al., 2011). While these arguments can explain government overinvestment, they are inadequate for explaining enterprises’ underutilization of capacity. Enterprises, as independent decision-makers, are fully capable of adjusting their behavior in the medium- and long-term in response to government policies. This study argues that addressing CU requires a focus on the enterprise level to identify viable solutions for improvement. Existing literature on enterprise CU is largely confined to oligopolistic markets (Barham & Ware, 1993; Benoit & Krishna, 1987). This limitation has hindered efforts to elucidate the capacity underutilization observed among a significant proportion of enterprises. Given the increasing focus on green development, scholars have explored the link between environmental regulation and corporate CU. However, these studies have not reached a consensus. One such consequence is the negative impact. Environmental regulations have been shown to raise compliance costs, which are associated with reduced investment and increased capital holdings, ultimately leading to a decline in CU (Dale & Peter, 1990; Xie et al., 2023). Conversely, while environmental regulations may raise production costs initially, they can encourage enterprises to invest in innovations that offset these costs and improve CU over time (Zhu et al., 2021). Moreover, enterprise-level studies consider decision-making processes and view ESG performance as a key factor in green development. However, overlooking ESG concepts when analyzing the CU problem still presents a challenge in explaining why China continues to face overcapacity issues.

Research Hypothesis

ESG Performance and Enterprises’ CU

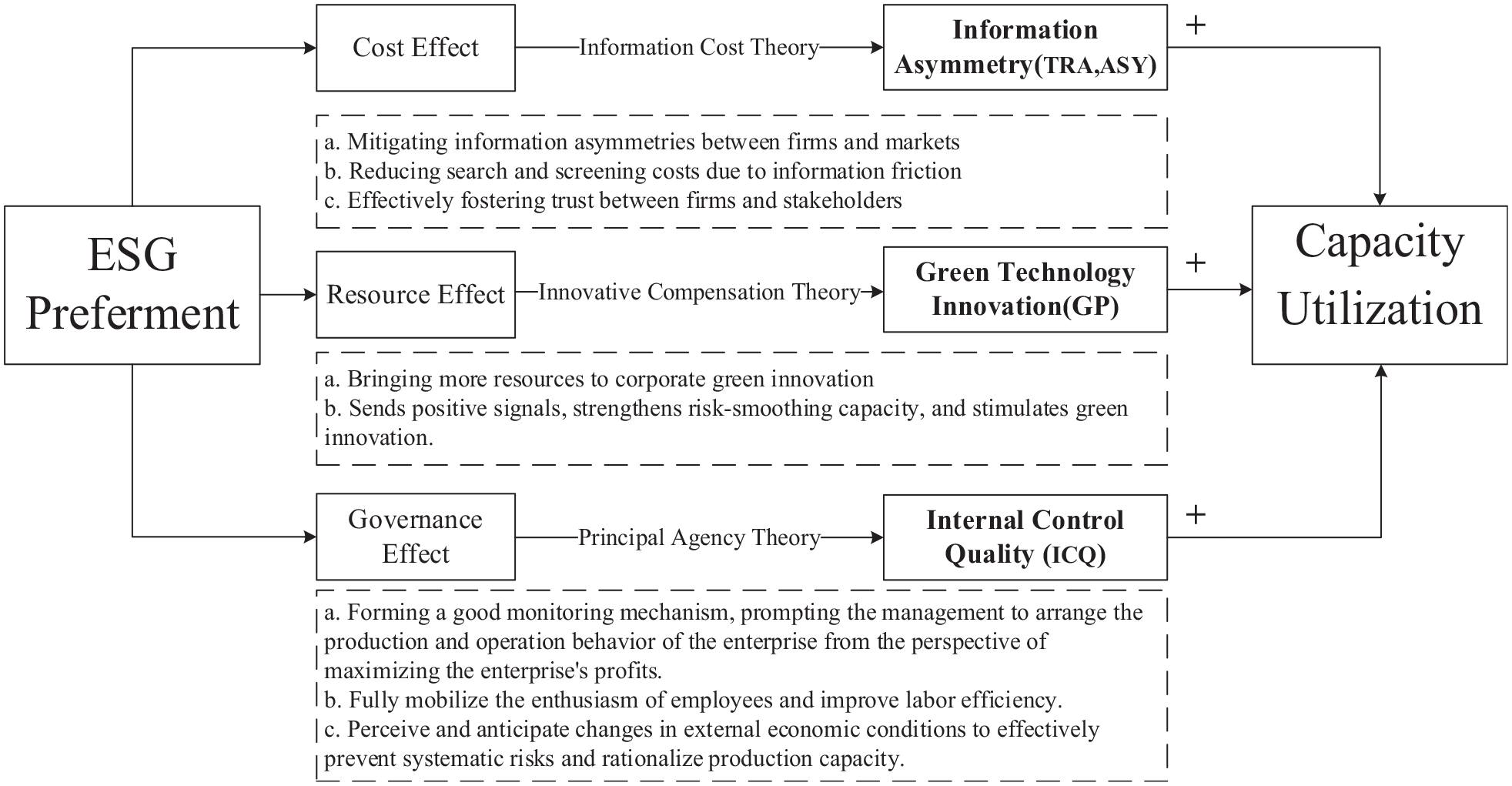

In the short term, superior ESG performance increases enterprises’ production costs and reduces the return on capital, thereby limiting the scale of industrial investment to some extent, assuming a constant level of technology (Garofalo & Malhotras, 1995). Additionally, commendable ESG performance elevates enterprises’ marginal cost of production, hinders investment in technological innovation, and consequently diminishes enterprises’ innovative capacity, which negatively impacts CU (Gray & Shadbegian, 2003). However, over the long term, an increase in ESG scores encourages industrial enterprises to invest more heavily in improvements to their production processes and technological innovation. This investment facilitates the alignment of enterprise production processes and technological capabilities with environmental regulatory requirements while simultaneously enhancing their technological innovation capacities. Therefore, the “innovation compensation effect” resulting from ESG disclosure will eventually offset the negative impact of the “cost effect” on CU (Du & Li, 2019). Moreover, an improvement in an enterprise’s ESG score elevates the environmental threshold for that enterprise, prompting a shift towards regions with less stringent environmental regulations. This shift facilitates inter-regional technology spillovers and further reinforces inter-regional capacity cooperation, thereby enhancing CU while promoting industrial upgrading in lagging regions. In conclusion, this paper proposes H1.

ESG Performance, Mitigating Information Asymmetries and Enterprises’ CU

In conjunction with globalization, resources are increasingly distributed among countries worldwide, and information is similarly undergoing a process of widespread dissemination. The extant literature indicates that information asymmetry is a significant determinant of enterprise CU. Information asymmetry increases the difficulty of enterprise financing (Li et al., 2023), weakens the growth and competitive abilities of enterprises, and potentially inhibits the improvement of enterprise CU. In the presence of substantial information asymmetry, enterprises may misrepresent product quality and conceal performance capabilities. To mitigate risk, partners may suppress product pricing, leading to adverse selection and elevating the risk of enterprise operation (Cage & Rouzet, 2015). To address this, enterprises seeking ESG ratings must disclose sustainability reports along with their financial statements. This provides more transparency, reducing information asymmetry between supply and demand, and enhancing trust between partners (Zheng et al., 2023). When buyers and sellers enter into contracts based on mutual trust, agency costs, as well as communication and negotiation costs, can be effectively reduced (Dan et al., 2011). This reduction can lead to lower product prices, greater competitiveness for the enterprise’s products, and improved CU. To maintain consistent information disclosure, enterprises will strive to enhance the quality of information disclosed, both preemptively and retrospectively. This effective information disclosure can reduce external information barriers, enhance the matching probability between the demand and supply sides of the transaction, improve the quality of transaction matching, and reduce inefficiencies in the entire transaction process (Chaney, 2014). As a result, this can positively impact the CU of enterprises. Finally, in the context of a deeply entrenched concept of sustainable development, enterprise ESG information will garner greater attention from analysts equipped with professional tools and capabilities (Baldini et al., 2018). The analysis and interpretation of ESG information by professional analysts can facilitate the transfer of more enterprise information to the trading market, assisting partners in understanding the operating risks and financial capabilities of export enterprises, thereby enabling them to avoid potential trading risks. Furthermore, it can strengthen the supervision of corporate ESG practices, reduce the possibility of ‘paper talk' in the process of improving ESG performance, and provide a guarantee for transactions based on the enterprise’s ESG performance by the partners. This, in turn, will promote the enhancement of the enterprise’s CU. Consequently, the implementation of ESG practices can enhance enterprise CU by mitigating information asymmetry. In conclusion, this paper proposes

ESG Performance, Improving Green Innovation Capability and Enterprises’ CU

In comparison to other forms of non-financial information disclosure, ESG disclosure possesses distinctive characteristics and can significantly influence the green innovation capacity of enterprises (Zhou et al., 2024). Green technological innovation can reduce the cost of raw material inputs, increase production capacity, and improve the input-output ratio when the production process is enhanced through green innovation (Chen et al., 2022). Signaling theory suggests that robust ESG performance communicates to society that a company values environmental protection, social responsibility, and corporate governance. This can, in turn, enhance investor confidence in the enterprise's long-term development, attract additional resources for its green innovation endeavors, and ultimately enhance the enterprise's green innovation capabilities, thereby improving its CU. In addition, the ESG concept emphasizes the importance of internal governance for sustainable corporate development. According to principal-agent theory, ESG disclosures lower information collection costs for external stakeholders, allowing for better supervision of management. This enhanced oversight motivates management to better coordinate green innovation efforts, improving CU through governance at both the strategic and operational levels. The implementation of effective ESG strategies can potentially influence enterprises to pursue green innovation. Therefore, enterprises must re-evaluate their resource allocation and leverage the pressure of ESG disclosure to drive green innovation (Liu et al., 2023), transforming green innovation into tangible outputs and subsequently optimizing resource utilization. In conclusion, this paper proposes H3.

ESG Performance, Optimizing Internal Control Levels and Enterprises’ CU

The implementation of effective ESG practices can facilitate the monitoring of managerial investment activities and enhance the efficacy of decision-making and management processes. Furthermore, the establishment of robust regulatory frameworks can encourage the optimization of production management procedures and improve the motivation of production personnel (Boulhaga et al., 2023). This, in turn, can lead to an increase in the enterprise’s CU. As enterprises seek to enhance their ESG performance, they will need to strengthen internal control measures to improve governance. This shift prompts accurate assessments of ESG performance, enabling targeted optimization and adjustment of internal control processes. Such actions help resolve internal control deficiencies and enhance effectiveness. The disclosure of ESG information reduces information asymmetry among internal enterprise stakeholders, curtails surplus management behaviors, ensures the accuracy of operating results and financial reports, and objectively evaluates the unique risks faced by enterprises, thereby improving the quality of internal control information (Fang & Chen, 2015). Enhanced internal control serves as an effective supervisory mechanism, mitigating the risk of opportunism and moral hazard under principal-agent arrangements. It also encourages management to organize production and operational activities with a focus on maximizing profits (Li et al., 2011). Moreover, internal control can fully mobilize employees’ motivation and enhance labor efficiency, thereby increasing the enterprise's CU through the implementation of a rational incentive structure. An effective incentive mechanism can stimulate employees’ enthusiasm, enhance labor efficiency, and ultimately improve the CU of the enterprise. Additionally, a well-designed incentive mechanism can effectively boost managerial performance, foster a comprehensive understanding of and response to external economic changes, and aid in the effective prevention of systemic risks, rationalization of production capacity allocation, and avoidance of excess capacity. In conclusion, this paper proposes

In light of the aforementioned analysis, this study presents a mechanism diagram illustrating the influence of ESG performance on enterprises’ CU, as shown in Figure 1. As depicted in Figure 1, strong ESG performance can enhance enterprises’ CU by mitigating information asymmetry, boosting green innovation capabilities, and optimizing internal control levels.

Diagram of the mechanism of action of ESG affecting CU.

Research Design and Methodology

Data Method

This study utilizes annual data from Chinese A-share listed companies for the period 2009 to 2022, excluding the following based on research criteria: (a) financial and insurance firms, due to their unique industry characteristics and operational nature; (b) *ST and **ST companies, as their irregular financial data could distort regression results; and (c) companies with missing data. Following screening, 35,692 data points from 4,100 companies were retained. Data for the study were gathered from the Cathay Pacific, Hua Zheng ESG rating, RESSET, CNRDS, Wind databases, and annual China Marketization Level Reports. Data aggregation and organization were done in Excel, with analysis conducted using Stata 17.0.

Model Specification

To investigate the impact of ESG performance on enterprises’ CU, this paper constructs the following equation (1):

Where, the following tables

To examine hypotheses 2 to 4, this paper draws on Jiang (2022) to empirically assess the mechanisms through which the causal relationship between ESG performance and enterprises’ CU. Specifically, this study utilizes information asymmetry as an exemplar to test hypothesis 2 and construct the following equation (2).

In equation (2), TRA represents the potential mediating variable, denoting the information asymmetry of the enterprise. The coefficient

Variables Definitions and Descriptions

Explanatory Variables (Esg)

The explanatory variable is ESG performance, measured as the average annual scores from the Huazheng ESG Rating Index. Commonly used ESG rating indexes include the Huazheng ESG rating, SynTao Green Finance ESG rating, and Bloomberg ESG disclosure score. This study selects the Huazheng ESG rating based on the number of companies included in the ESG score and its frequency of updates.

Explained Variables (CU)

The explanatory variable in this study is enterprises’ CU. Following Qu (2015), who applied the stochastic frontier production function method in empirical analysis, the ratio of actual output to frontier output is considered as CU. Given that listed companies do not disclose gross industrial output, this study uses proxies such as main business revenue, total assets, and the number of enterprises to construct the stochastic frontier production surface and calculate CU levels for listed enterprises. In addition, Zhao et al. (2015) the higher enterprise CU, the faster enterprise total asset turnover (ATO). Therefore, this study tests the robustness of ATO as an alternative indicator of enterprise CU.

Mediating Variables

Information Asymmetry Effect of Enterprises (TRA, ASY). First, the enterprise’s capacity to access external information (TRA) is gauged using the natural logarithm of the number of securities analysts tracking and publishing research reports in a given year, plus one (Yu, 2008). Second, the degree of outsiders’ access to information about enterprises (ASY) is assessed. Following the approach by Amihud et al. (1997), information asymmetry is measured using daily frequency trading data, where larger values indicate more pronounced information asymmetry.

Enterprises’ Green Innovation Effect (GP). Following the approach outlined in Qi et al. (2021), this paper uses the number of enterprise green patent applications to quantify green technology innovation. The number of green patent applications is chosen over green patent grants as it better reflects an enterprise’s technological innovation capacity for the current year, considering the potential lag in green patent grants.

Enterprise Internal Control Level Effect (ICQ). Building on the methodology proposed by Han et al. (2022), this study uses the internal control index of enterprises from the DIB internal control and risk management database, standardized by dividing by 1,000 for measurement purposes.

Control Variables

Referring to the study of Guo and Wu (2021), this paper selects control variables from both financial and enterprise governance aspects of the enterprise. Among them, enterprise size (Size), enterprise age (Age), enterprise gearing ratio (Lev), enterprise return on net assets (Roe), enterprise growth (GR), enterprise cash flow ratio (CF), and Tobin’s Q value (Tobinq) are selected as the control variables in the aspect of enterprise finance. The proportion of sole directors of the enterprise (Dud), whether the enterprise is Big 4 audited (Big4), audit opinion (Mao), and the proportion of shares held by the enterprise’s first largest shareholder (CR) are selected as control variables in terms of enterprise governance. The specific definitions of the variables used in the analysis are shown in Table 1.

Variable Definitions.

Results and Discussion

Descriptive Statistics

Table 2 summarizes the descriptive statistics for the main variables. The explanatory variable CU has a mean of 0.694, a standard deviation of 0.0812, with values ranging from a minimum of 0.0616 to a maximum of 0.916, reflecting the variability of CU across enterprises. In 2022, China’s industrial CU was 75.6%, which is in close agreement with the 69.4% reported in this study. Additionally, the descriptive statistics for the financial and governance control variables are consistent with those found in existing literature (Liu et al., 2022; Xiao et al., 2021).

Descriptive Statistics.

Regression Analysis

Main Hypotheses

Table 3 illustrates the regression results examining the impact of ESG performance on enterprises’ CU. Column (1) presents the regression outcomes without incorporating control variables, solely accounting for industry, city, and year fixed effects. Columns (2) and (3) depict the regression results after the inclusion of enterprise finance and enterprise governance control variables, respectively, while maintaining control for industry, city, and year fixed effects. It is evident that the regression coefficient of ESG in column (3) exhibits significance at the 1% level, signifying that enhanced ESG performance within the enterprise positively influences its CU. This finding substantiates

Results of Main Hypotheses.

Note. t-values in parentheses; standard errors adjusted based on enterprise-level robustness clustering, *p < 0.1. **p < 0.05. ***p < 0.01, the same applies to the following table.

Mediation Analysis

In the previous study, this paper establishes robust and reliable core findings through regression analysis of the benchmark model. The finding indicates that effective ESG performance contributes to the enhancement of enterprise’ CU. However, this conclusion stems solely from an empirical examination of the causal relationship between the two factors, offering no insights into the mechanism that operates between them. In this subsection, the paper draws on Jiang (2022) to empirically explore the causal pathway between enterprises’ ESG performance and their CU.

The specific test results are presented in Table 4. Columns (1) and (2) indicate that enterprise ESG performance alleviates enterprise information asymmetry. On the one hand, it promotes the ability of enterprises to obtain external information and reduces analysts’ prediction bias. On the other hand, it enables enterprises to dynamically grasp market changes and reverse-drive their production decisions, thereby reducing “cellar behaviors” in response to future changes in demand and enhancing their production capacity.

Results of Mechanism Analysis.

Note.*p < 0.1, **p < 0.05, ***p < 0.01.

Good ESG performance contributes to the improvement of enterprise CU through several mechanisms. First, by fostering green innovation, ESG performance enables enterprises to enhance their production processes, reduce raw material consumption, and increase production efficiency. This, in turn, improves CU while minimizing unnecessary capacity waste, thereby optimizing the use of existing resources (Chen et al., 2022). Second, strong ESG performance reduces information asymmetry within enterprises and strengthens the trust relationships between the enterprise, its supply chain, and the market. This increased transparency boosts the enterprise's competitiveness and market adaptability, facilitating better adjustments to production scales and resource allocation to prevent excess capacity (Zheng et al., 2023). Third, optimizing internal controls improves decision-making efficiency, mitigates the risk of over-expansion, and ensures that CU remains at a reasonable level (Li et al., 2023). Thus, good ESG performance does not directly contribute to overcapacity; rather, it enhances CU and prevents excess capacity through effective resource allocation, green innovation, and optimized internal management. The synergistic effects of green innovation, information transparency, and internal controls together maximize capacity use, reduce resource waste, and minimize environmental burdens.

Robustness Tests

To verify the robustness of the findings, this study replaces explanatory variables, error types, and individual fixed effects. Specifically, column (1) of Table 5 presents the regression results using ATO as the explanatory variable. In column (2), the explanatory variable is substituted with the median ESG score, calculated quarterly. Column (3) replaces cluster-robust standard errors clustered at the enterprise level with heteroskedasticity-robust standard errors. Finally, column (4) swaps city-level fixed effects with province-level fixed effects. The coefficients consistently pass the significance tests at both the 5% and 1% levels, regardless of the regression approach used. Therefore,

Results of Robustness Test.

Note. Standard errors in column (3) are heteroskedasticity robustness adjustments. *p < 0.1, **p < 0.05, ***p < 0.01.

Endogenous Analysis

In the baseline regression model, there may be an endogeneity problem between ESG performance and the enterprises’ CU. First, enterprises with high ESG ratings possess a distinct information advantage that may enable them to identify enterprises with elevated CU. Consequently, the relationship becomes entangled in mutual causality, suggesting that enterprises with higher CU enhance ESG scores, rather than ESG performance contributing to enterprises’ overcapacity problems. This situation leads to the endogeneity problem. Second, certain unobservable omitted variables might concurrently influence both ESG scores and the CU of enterprises. Third, the existence of ESG ratings for enterprises may not be entirely random but influenced by factors that also impact the enterprises’ overcapacity problem, introducing a selection bias. To mitigate these potential issues, this paper employs the instrumental variable method, Heckman two-stage model, and propensity score matching (PSM) method for individual tests.

Instrumental Variable Method

Drawing on Shi and Jiang (2023), this study uses the mean ESG performance of other listed enterprises in the same industry within the enterprise’s city (IVESG1) as an instrumental variable. In selecting instrumental variables, the ESG performance of other listed enterprises in the same industry located in the same district as the sample enterprises is relevant. These enterprises share similar institutional environments and are subject to the same industry policies, making them suitable for use as instrumental variables. It is unlikely that the ESG performance of other enterprises directly affects the CU of the target enterprise. Therefore, using their ESG performance as an instrumental variable is appropriate.

Following Wang and Xie (2022), this study re-examines the relationship between ESG performance and CU using the two-stage least squares (2SLS) method. The study uses the mean annual ESG score for the industry and the interaction term with Confucianism (Confu) culture (IVESG2) as instrumental variables. The industry’s ESG score correlates with enterprises’ ESG performance but does not directly affect their CU. A higher average ESG score for other listed enterprises in the same industry in the city suggests that enterprises in this region prioritize ESG management, which increases the likelihood of disclosing ESG information. Enterprises that disclose ESG information protect stakeholders’ rights and enhance their economic benefits. Additionally, Confucian culture encourages businesses to take on social responsibility, increasing the level of social awareness from an ethical standpoint (Zou & Li, 2022).

Table 6 presents the regression results of the IV-2SLS model. First, the correlation tests show that the instrumental variables are statistically significant, supporting their validity. Both IVESG1 and IVESG2 pass the 1% significance test, indicating that the instrumental variables are strongly correlated with the explanatory variables. Finally, as seen in columns (3) and (4) of Table 6, the regression coefficients of ESG are both 0.003 and pass the significance test at the 1% and 5% levels, confirming the reliability of the baseline regression results.

Results of 2SLS Method.

Note.*p < 0.1, **p < 0.05, ***p < 0.01.

Heckman Two-stage Model Test

Due to the non-mandatory nature of ESG disclosure, some enterprises may adopt significant ESG measures without disclosing strategic changes. This introduces an endogeneity problem stemming from sample selection bias. To address this, a Heckman two-stage model is used for testing. The Probit model estimates the Inverse Mills Ratio (IMR). The explanatory variable is DESG, which equals 1 when ESG exceeds the mean, and 0 otherwise. The exogenous instrumental variable used for analysis is IVESG1. IMR is included as a control variable in the benchmark regression model (1) to test for potential selectivity bias in the conclusions of the regression. The results in Table 7 show that the IMR coefficient is insignificant, indicating no significant self-selection bias in the sample. Additionally, the ESG performance coefficient is significantly positive at the 1% level, affirming the robustness of the conclusions.

Results of Heckman Two-stage Model and PSM Test.

Note. Columns (1) and (2) have z values in parentheses; columns (3) and (4) have t values in parentheses. *p < 0.1, **p < 0.05, ***p < 0.01.

PSM Method

This study uses the PSM method to mitigate potential endogeneity issues. The sample is divided into a high ESG group (treatment group) and a low ESG group (control group), based on the ESG mean of the same industry and city in the same year. A one-to-one matching method is used. The standardized deviation of all covariates after matching is below 10%, and most covariates show no significant differences post-matching. Following the regression on the matched sample, as shown in column (4) of Table 7, the coefficients of the independent variables are significantly positive at the 1% level, reinforcing the robustness of the conclusion.

Analysis of Heterogeneity

Enterprise-Level Heterogeneity Analysis

The impact of ESG performance on enterprises’ CU may vary significantly based on ownership structure. State-owned enterprises (SOEs) are subject to higher public scrutiny and more stringent environmental regulations. In contrast, non-SOEs enjoy greater flexibility in resource allocation, enabling them to invest more in projects aimed at enhancing CU. SOEs, however, operate in a more complex regulatory environment, which can influence their investment decisions. To understand the influence of ESG performance on CU, it is important to examine the differences between SOEs and non-SOEs. This requires an analysis of the heterogeneity associated with various ownership structures. Table 8 presents the results, where columns (1) and (2) show the regression outcomes for the original sample, divided into two sub-samples: SOEs and non-SOEs. Notably, ESG performance has a more significant impact on improving CU for non-SOEs. The government-enterprise linkage for SOEs provides them with additional policy support, tax incentives, and credit resources, reducing their perception of external competitive pressures. This diminished external pressure leads to a lack of motivation for SOEs to actively engage in ESG governance, limiting their ability to capitalize on their advantages in green transformation. As a result, the impact of ESG performance on improving CU for SOEs is relatively modest. In contrast, non-SOEs prioritize ESG not only to enhance economic efficiency but also to fulfill environmental and social responsibilities. The ESG practices of non-SOEs are more aligned with stakeholder interests, while those of SOEs are driven by national policy requirements. These differing motivations make the ESG performance of non-SOEs more effective in promoting their CU.

Results of Enterprise-Level Heterogeneity Analysis.

Note.*p < 0.1, **p < 0.05, ***p < 0.01.

Enterprise size is another significant variable influencing CU. Large enterprises have advantages in capital, talent, and technology, while small-scale enterprises are constrained by limited resources in their production and operational decisions. The implementation of effective ESG practices can help small-scale enterprises build positive relationships with stakeholders, enhancing their reputation and gaining support, which can lead to improved CU. Moreover, enhancing ESG standards can facilitate more efficient collaboration within and between enterprises, improve production and operational efficiency, and establish a virtuous cycle of internal and external resources. This improves the enterprise's ability to make informed business decisions and integrate resources effectively, leading to a notable increase in CU. The categorization is based on the mean value of total assets in the same industry. Large enterprises, with total assets above the industry mean, are denoted as 1, while smaller enterprises are marked as 0. The findings reveal that, in comparison to large enterprises, good ESG performance in small-scale enterprises contributes more significantly to improving CU. Generally, small enterprises are more prone to default than larger ones and are more likely to exit the market and prefer incremental investment. Additionally, small-scale enterprises often struggle to capitalize on economies of scale, such as accumulating capital and increasing capacity. However, their smaller size allows for a more flexible and efficient transformation process. As a result, the boost to CU is greater when small-scale enterprises achieve good ESG performance.

Industry-level Heterogeneity Analysis

To examine the relationship between ESG performance and CU across industries with different factor intensities, this study uses the classification framework from An et al. (2018). Industries are categorized based on their median capital per capita, with those exceeding the median classified as capital-intensive and those below the median as labor-intensive. The regression results in columns (1) and (2) of Table 9 show that ESG performance has a significantly positive impact in capital-intensive industries and a significantly negative impact in labor-intensive industries. This indicates that ESG performance has a stronger influence in capital-intensive industries. This can be explained by several factors: labor-intensive industries, often in low-end manufacturing sectors with high pollution, emissions, and low value-added outputs (e.g., textiles and metal products), typically have lower capitalization. Their longer production cycles and outdated processes may limit their ability to invest in ESG practices, thus reducing the impact of ESG on their CU. In contrast, capital-intensive enterprises, which usually make substantial early-stage investments, experience faster capital turnover and higher return cycles, allowing them to improve conditions, increase operational efficiency, and build a more positive enterprise image, thereby enhancing their CU.

Results of Industry-Level Heterogeneity Analysis.

Note.*p < 0.1, **p < 0.05, ***p < 0.01.

Do ESG ratings equally reflect the environmental performance of listed companies across different industry categories? Drawing from Haijun et al. (2023), this study categorizes sample enterprises into two groups: high-carbon and low-carbon enterprises. In particular, enterprises that are engaged in carbon-emitting priority sectors are classified as high-carbon enterprises, with a value of 1. Other sectors are designated as low-carbon enterprises, with a value of 0. For a detailed list of the specific sectors and the criteria used for their classification, refer to Appendix A. The results, presented in columns (3) and (4) of Table 9, show that the ESG coefficients for low-carbon industries are significantly positive at the 1% level, while the ESG coefficients for high-carbon industries are positive but not statistically significant. This suggests that CU in low-carbon industries is more responsive to ESG ratings, whereas high-carbon industries demonstrate lower sensitivity. This outcome underscores two key considerations: First, low-carbon industries inherently have lower carbon emissions, energy consumption, and pollution compared to high-carbon industries, resulting in better ESG ratings. Second, high-carbon industries, which are pivotal sectors in China and characterized by high pollution and energy consumption, still face significant challenges in achieving green and low-carbon transformations. Their current ESG performance lags behind societal expectations, making ESG ratings less impactful on the CU of high-carbon industries.

Discussion

Investigating the interplay between the development of ESG governance, the resolution of overcapacity, and their collective impact on economic development is of critical importance. This paper seeks to determine whether enhancing enterprises' ESG performance contributes to increased CU, thereby promoting high-quality economic growth. Addressing overcapacity could invigorates the economy and positions China to achieve its “double carbon” goals and advance its agenda for high-quality economic development. The development of ESG governance and the alleviation of overcapacity are essential for addressing resource and environmental challenges and act as catalysts for sustainable economic progress. However, existing literature offers limited insights into the synergistic effects of these dual factors, leaving their developmental trajectories unclear. To fill this gap, this study explores whether improving enterprises' ESG performance leads to enhanced CU and clarifies the mechanisms behind this relationship. The analysis yields compelling findings. As presented in Table 3, the results indicate that boosting enterprises' ESG performance indeed enhances CU, thereby supporting

Additionally, this study investigates the mechanisms through which ESG performance influences CU, expanding upon existing research in this area. Through a pathway analysis, it is revealed that ESG performance facilitates improved CU by mitigating information asymmetry, enhancing green innovation capabilities, and strengthening internal control measures. First, effective ESG performance can significantly alleviate information asymmetry between enterprises and the market, reduce search and screening costs associated with information friction, and foster mutual trust between enterprises and stakeholders (Zheng et al., 2023). This, in turn, enables enterprises to secure greater support from stakeholders, leading to positive development and improved CU. Second, green innovation generates spillover effects, which draw greater attention to sustainable development and help mitigate overcapacity issues (Liu et al., 2023). Third, the implementation of robust internal control measures has been shown to positively influence enterprise value by reducing operating costs, enhancing market influence, expanding market share, and ultimately improving CU.

In comparison to existing literature, this paper makes a novel contribution by examining the impact of ESG governance from the perspective of enterprise CU. By objectively assessing the policy implications of ESG governance, it offers new micro-level evidence and explores the economic ramifications of enterprise ESG performance on CU. This approach provides valuable insights for promoting sustainable development, addressing overcapacity, tackling resource and environmental constraints, and fostering high-quality enterprise development. Overall, the findings offer significant policy implications for advancing sustainable business practices and driving economic progress.

Conclusions and Policy Recommendations

Conclusions

With the development of China’s economy, overcapacity has emerged as a complex, global, long-term, and deeply rooted issue (Cao & Tang, 2021). In this context, effectively improving CU and resolving excess capacity have become urgent challenges. This paper theoretically analyzed the mechanism linking ESG performance to enterprise CU. The study, using data from A-share listed companies between 2009 and 2022, found that strong ESG performance improves CU. Specifically, holding all other factors constant, a one-unit increase in ESG performance corresponds to an average increase of 0.004 units in CU. This finding has been validated through a series of endogeneity tests and robustness analyses, confirming the validity of

Policy Recommendations

This paper underscores key insights on ESG for enterprise CU. First, enterprises should actively adopt the ESG development concept, as commendable ESG performance enhances productivity, reduces costs, alleviates financing constraints, releases excess capacity, and improves utilization rates. Enterprises should strengthen commitments to environmental protection, social responsibility, and governance optimization, integrating ESG principles into employee processes for market advantages. Enhanced ESG information disclosure is crucial for collaboration opportunities. Manufacturing enterprises, as change drivers, should lead domestic ESG practices. Second, analysts must intensify supervision and reporting of enterprise ESG behavior to guide resources to high-quality enterprises. Third, government departments should focus on policy guidance, refining systems, and promoting ESG information disclosure tailored to industries. Incentivizing comprehensive ESG engagement can drive proactive investment and contribute to China’s green transformation. Regulators should increase penalties for false ESG disclosure to enhance credibility and foster sustainable development.

Limitations of Research

This paper examines the impact of ESG performance on enterprise CU and its transmission mechanisms. However, there are certain limitations in the research process that require improvement. At the data level, the study relies on A-share listed enterprises, which represent a majority of enterprises but lack sufficient data from many micro, small, and medium-sized enterprises. The limited information disclosure from these enterprises poses a challenge. To address this, more comprehensive data collection through methods such as field visits, questionnaires, and enterprise interviews is needed to enhance the study’s depth and quality. In terms of research content, the impact of ESG performance on CU may vary across industries. Further refinement of the study is necessary for a more nuanced understanding of these industry-specific dynamics.

Footnotes

Appendix A

This paper refers to the eight industries with high carbon emissions that have been or will be included in China's carbon market as mentioned in the Notice of the General Office of the National Development and Reform Commission on Launching the Key Work of the National Carbon Emission Trading Market in 2016, including electric power, steel, cement, non-ferrous metals, petrochemical, paper making, building materials, chemical and aviation industries.

Acknowledgements

This manuscript has not been submitted to any journal for publication, nor is under review at another journal or other publishing venue.

Author Contribution

This paper is written by the three authors named in the title page. Tingwei Chen: Formal analysis, Investigation, Resources, Data curation, Visualization, Editing. Feng Yang: Literature, Methodology, software, Formal analysis, Investigation, Resources, Data curation, Writing original draft, Visualization. Zongbin Zhang: Conceptualizaiton, Writing-review & editing, Project administration, Funding acquistion, Supervision, Methodology.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Social Science Fund of China (Grant No.21BJL107).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Publisher’s Note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Data Availability Statement

Data sources are outlined above in the section variables, and will be available on demand.