Abstract

This study aims to investigate the impact of shared auditors on the selection of M&A targets and analyze the moderating effects of the signing auditor’s gender and partner characteristics. In M&A transactions, shared audit firms or auditors are believed to contribute to information symmetry, which may influence the selection of target companies. However, there is a lack of systematic research on the specific role of shared auditors in M&A, particularly regarding the effects of their gender and partner characteristics. Based on data from Chinese listed companies between 2010 and 2020, this study uses a matched sample control group and the Probit regression model to evaluate the impact of shared auditors, their gender, and partner characteristics on M&A decisions. The findings reveal a positive effect of shared auditors on target selection in M&A. Specifically, female auditors demonstrate a significant positive moderating effect in M&A decisions, possibly due to their cautious approach and ability to build strong client relationships. In contrast, the background characteristics of partners have no significant impact on M&A decisions. Additionally, supplementary tests show that this relationship is not entirely dependent on macro-level monetary policies or economic policy uncertainty. The positive effect of shared auditors on target selection remains significant. This study provides empirical evidence for the role of shared auditors in M&A transactions, particularly highlighting the potential value of auditor gender. These findings offer important insights for both corporate M&A strategies and the consideration of gender diversity within the auditing profession.

Introduction

In Merger and Acquisition (M&A), information asymmetry is a significant issue that makes it challenging for the acquiring party to fully evaluate the resources and capabilities of potential target companies, thus affecting the success of the transaction (Capron & Shen, 2007). Acquirers often rely on audit firms to obtain information about target companies, especially when time and cost are limited (Y. Cai et al., 2016; T. Chen et al., 2012; Dhaliwal et al., 2016). Therefore, how to reduce information asymmetry through audit firms to help acquirers make more informed decisions has become a key issue in M&A research. Existing literature has shown that shared auditors can reduce transaction premiums, and target companies with shared auditors are more likely to become acquisition targets or facilitate friendly acquisitions (Bedford et al., 2022; Y. Cai et al., 2016; Chahine et al., 2018; Chircop et al., 2018; Dhaliwal et al., 2016). Additionally, studies suggest that female auditors, due to their risk-averse tendencies, are more likely to adopt cautious auditing approaches and issue going-concern opinions (Hao et al., 2021; Hardies et al., 2016). The role of partners in the audit process also cannot be overlooked, as there are significant differences in performance among different partners, and early career experiences have a substantial impact on their professional skepticism (Gul et al., 2013; He et al., 2018).

Problem Statement

There is limited research on the specific role of shared auditors in the selection of target companies and how auditor gender and partner background influence the M&A process. One reason for this is the lack of data, as few jurisdictions require the disclosure of audit partner names in audit reports (Burke et al., 2020; Chu et al., 2022; Laurion et al., 2017; Lennox & Wu, 2018). How the individual characteristics of auditors influence target company selection remains underexplored. In particular, whether factors such as audit partner background and gender among shared auditors affect target selection deserves further study.

Research Objectives

The aim of this study is to fill this research gap by exploring the impact of shared auditors on target selection in M&A transactions, within a unique context, and analyzing how the gender of signing auditors and the characteristics of partners moderate this impact. Specifically, the research objectives are: (1) to assess the influence of shared audit firms on the selection of M&A targets; (2) to examine the positive moderating effect of female auditors on the success rate of M&A transactions; and (3) to analyze the role of audit partners’ backgrounds in the completion of M&A deals. To achieve these objectives, this study controls for relevant factors and excludes cases involving the same signing auditors, focusing on the impact of shared audit firms at the company level.

For several reasons, first, prior research has shown that shared auditors improve transparency through information sharing, reducing information asymmetry and enhancing the credibility and accuracy of financial reports (J. Z. Chen et al., 2019; J. Chen et al., 2022; Hu et al., 2022). This increased transparency raises the likelihood that targets will accept acquisition proposals and lowers the uncertainty risks in M&A transactions. Additionally, shared auditors facilitate friendly acquisitions, reduce acquisition premiums, and increase cumulative abnormal returns (Bedford et al., 2022; Dhaliwal et al., 2016). This increased transparency raises the likelihood that targets will accept acquisition proposals and lowers the uncertainty risks in M&A transactions. Additionally, shared auditors facilitate friendly acquisitions, reduce acquisition premiums, and increase cumulative abnormal returns (J. Z. Chen et al., 2020).

Second, research suggests that female auditors tend to be more diligent, detail-oriented, and responsible when managing conflicts of interest (Abed & Al-badainah, 2013; Alderman, 2017). They are inclined to adopt a democratic leadership style and improve audit quality through deeper communication and collaboration (Trinidad & Normore, 2005). Additionally, female auditors are more likely to issue going-concern opinions (Hardies et al., 2016), making them more cautious in the audit process. This reduces information asymmetry in M&A transactions and increases audit effort, thereby enhancing the reliability of financial reports. These factors collectively contribute to the success of M&A transactions.

Third, the background of audit partners may have a positive moderating effect on the success of M&A transactions, as there are significant differences in the performance of individual partners, and early career experience helps shape their professional skepticism, which may influence their assessment of M&A deals (Gul et al., 2013; He et al., 2018). Furthermore, research shows that when partners retain their position after changing audit firms, audit fee pressure is reduced, and selecting younger partners may lower fees and facilitate deal completion (Cao & Feng, 2022). However, research on this topic is still limited due to the non-disclosure of partner names in certain jurisdictions (Laurion et al., 2017; Lennox & Wu, 2018)

Testable Hypotheses

Based on the existing literature and research objectives, this study proposes the following testable hypotheses: (1) Companies that share audit firms are more likely to be selected as acquisition targets; (2) Shared female auditors have a significant positive moderating effect on M&A decisions; (3) The partner characteristics of auditor have a significant moderating impact on M&A decisions. By testing these hypotheses, this study aims to explore the role of shared auditors in M&A decisions and the moderating effects of their gender and background characteristics.

Using a sample of 468 data points from the Chinese market between 2010 and 2020, we found that 11.54% of companies selected firms with which they shared auditors as their acquisition targets. By applying sample matching guidelines from the Guidelines for the Industry Classification of Listed Companies (2012) and data from A-share listed companies, we selected companies with similar industry and size characteristics as the matched group. After pairing, the resulting study sample consisted of 885 samples (468 treated samples and 417 matched samples). We employed a Probit regression model to evaluate the effect of shared auditors and the moderating role of shared auditors’ gender and partner characteristics on M&A decisions. We generally find a positive effect of shared auditors on the choice of acquisition targets. Specifically, female auditors demonstrated a significant positive moderating effect in M&A decisions, likely due to their greater caution and ability to build strong relationships with clients. In contrast, the background characteristics of audit partners had no significant impact on M&A decisions. These findings suggest that the gender characteristics of auditors and the backgrounds of partners positively contribute to M&A decision-making, increasing the likelihood of success.

In additional tests, we examined the effects of macro-level monetary policy and economic policy uncertainty. Monetary expansion and economic uncertainty may adversely affect emerging market economies, thereby hindering M&A activity. Considering these factors provides a more comprehensive understanding of the drivers of M&A activity during the sample period. To explore whether the positive impact of shared auditors on target selection can be explained by these two variables, we extended our main tests on partner turnover. By controlling for the Federal Reserve (Fed) policy and Economic Policy Uncertainty (EPU) in the model, we further introduced interaction terms for Fed (EPU) with bidder females, target females, and shared auditors. The regression results showed that the relationship between shared auditors and target selection in M&A transactions does not entirely rely on macro-level monetary policy and economic policy uncertainty. The positive impact of shared auditors on the choice of acquisition targets remained significant. The results remained robust even when alternative measures of shared auditors were used.

This study provides empirical evidence on how companies can leverage the role of shared auditors in M&A transactions, especially highlighting the potential value of auditor gender. The findings offer significant insights for addressing gender diversity issues in the auditing profession and for making informed auditor selection decisions in M&A processes. Specifically, this study makes several important contributions to the existing literature. First, prior research has shown that the selection of target companies is influenced by internal factors and institutional contexts (Ahern et al., 2015; Alimov, 2015; Bettinazzi et al., 2018; Erel et al., 2012; Gomes, 2019; Li & Zhang, 2020; Maas et al., 2018), and that shared auditors facilitate friendly acquisitions between acquirers and targets (Bedford et al., 2022; Dhaliwal et al., 2016). By introducing the factors of auditor gender and partner characteristics, this study enriches the research on audit teams and shared auditors, offering a new perspective on the information transfer function of auditing. It not only extends the application of audit theory but also provides a theoretical basis for understanding the role of auditors in complex transactions, particularly in M&A environments characterized by information complexity and decision-making challenges.

Second, this study provides important insights into the impact of auditor gender characteristics on information transfer. It offers a new theoretical perspective for understanding the relationship between auditors’ individual traits and information transfer, with particular attention to the impact of gender diversity. Female auditors possess advantages in moral sensitivity, risk aversion, and audit rigor, which may enhance the credibility and transparency of financial reports during the M&A process, thereby increasing the likelihood of a successful transaction.

From a practical perspective, the significance of our research lies in the dynamics of audit relationship networks and M&A activity. Organizations may consider establishing closer shared auditor mechanisms to improve the effectiveness of information transfer in M&A transactions. Companies can strategically utilize shared auditors, particularly by leveraging the strengths of female auditors, to improve audit quality, reduce information asymmetry, and enhance the success rate of mergers and acquisitions.

The remainder are as follows: Section 2 provides a comprehensive overview of the literature pertaining to shared auditors and auditor attributes, subsequently outlining the formulated hypotheses. Section 3 encompasses the dataset details and introduces the empirical model. Empirical findings are presented in Section 4, while the study’s conclusions are deliberated in Section 5.

Theoretical Framework and Hypotheses Development

Shared Auditors and M&A Target Select

Due to information asymmetry, the acquirers may face difficulties in assessing the capabilities of potential targets (Capron & Shen, 2007). Selecting the right target is an essential factor in the success of M&A. Research has indicated that target-related risk is one of the sources of risk in M&A transactions (Bruyland & de Maeseneire, 2016).

In emerging markets, a company’s size and the market environment can have an impact on the growth strategy decisions. Specifically, larger companies tend to prefer growth through M&A, and cross-border bank mergers often yield significant value creation (Kayo et al., 2010; Williams & Liao, 2008). However, evaluating potential targets can be difficult due to factors such as asymmetric information and the interpretation of information. One way to facilitate understanding between firms and increase the likelihood of successful mergers is to have similar ownership structures (Bettinazzi et al., 2018). Institutional context factors such as accounting disclosure quality (Erel et al., 2012), labor market regulations (Alimov, 2015), Cultural proximity (Ahern et al., 2015), the strength of anti-director rights (Maas et al., 2018), higher CSR scores (Gomes, 2019), and the shareholders’ social network (Li & Zhang, 2020) also play a role in target selection.

Recent research on “shared auditors” stated that shared auditors can have an information sharing effect. The behavior of two firms hiring an audit firm jointly is referred to as “shared auditor” (T. Chen et al., 2012). This increased transparency increases the likelihood of the target accepting the M&A offer, as it avoids the risk of rejecting a potentially beneficial offer due to a lack of information. Also, shared auditors facilitate acquisitions and lower transaction premiums, allowing the acquisition to generate positive market returns (Dhaliwal et al., 2016). Previous studies have shown that firms employing the same auditor have similar financial reporting patterns (Robert Knechel et al., 2015). Due to time and cost constraints, the acquirer will typically ask the audit firm if there is a potential acquisition target that matches it (Y. Cai et al., 2016). Shared auditors facilitate friendly acquisitions, reduce acquisition premiums, and increase total cumulative abnormal returns for acquirers (Bedford et al., 2022). Hiring the same audit firm, office, and team leads to higher comparable returns, with the individual auditor style having an even stronger impact (J. Z. Chen et al., 2020).

Moreover, shared auditors between banks and borrowers result in lower interest rates for borrowers and improved audit quality for both parties, with lenders benefiting from more accurate loan loss provisions (Aguir et al., 2022; Francis & Wang, 2021; Ton, 2022). Similarly, shared auditors can also provide benefits to the supply chain. And shared auditors can reduce the likelihood of accounting restatements, moderate expectations, decrease supplier cost stickiness, increase supplier RSI, and mitigate the negative impact of inefficient investment through non-audit services, particularly tax-related services (C. Cai et al., 2019). Shared auditors offer advantageous contributions within the supply chain context, encompassing enhanced audit service efficiency and accuracy, bolstered credibility of financial reports, and mitigation of financial fraud risks (J. Z. Chen et al., 2019; J. Chen et al., 2022; Hu et al., 2022).

The selection of appropriate targets in M&A is crucial for achieving successful outcomes, yet it is often hindered by information asymmetry, which complicates the acquirer’s ability to assess potential targets effectively. Research indicates that shared auditors can significantly alleviate these challenges by enhancing transparency and fostering better communication between acquirer and target firms. This collaborative relationship not only reduces misunderstandings and mistrust but also facilitates informed decision-making during the target selection process.

Previous studies have shown that firms utilizing shared auditors experience smoother acquisitions, including favorable terms such as reduced premiums and positive market responses post-announcement. Given the importance of these dynamics, it is hypothesized that shared auditors positively influence the selection of M&A targets, ultimately increasing the likelihood of successful acquisitions. This understanding underscores the strategic role of auditor collaboration in navigating the complexities of M&A, providing valuable insights into the mechanisms that drive effective target selection. Based on this, our first hypothesis is as follows:

H1: It is highly probable that a company has the same audit firm with the acquirer can become the real target.

The Moderating Effect of Auditor’s Characteristics on Target Selection

DeFond and Francis (2005) suggest that future research should shift focus from the firm level to the individual auditor level in order to gain deeper insights into auditor behavior. This shift is particularly valuable in China, where the mandatory disclosure of individual auditor information offers a unique opportunity to study personal auditor characteristics and their impact on audit outcomes. Individual attributes such as risk preference, experience, specialized knowledge, and incentives play a significant role in shaping audit judgments and decisions, particularly in complex settings like M&A. A key part of our analysis focuses on how the characteristics of individual auditors, such as gender and professional background, can influence the audit process and outcomes.

Gender

Gender has emerged as an important characteristic in auditing, influencing auditors’ judgments and decision-making processes (Chung & Kallapur, 2003). Research indicates that female auditors tend to be more diligent and cautious compared to their male counterparts (Abed & Al-badainah, 2013; Bernardi & Arnold, 1997; Hardies et al., 2010). Their preference for risk aversion and democratic leadership styles (Chin & Chi, 2008; Hao et al., 2021; Jones et al., 2019; Trinidad & Normore, 2005) positions them as more meticulous and ethical in their professional practice, which translates into increased audit investment and, consequently, higher audit fees (Hao et al., 2021; Ittonen & Peni, 2012; Lee et al., 2019). These findings are reinforced by studies showing that female auditors are more likely to address conflicts of interest with greater responsibility (Alderman, 2017; Schubert, 2006), further strengthening the quality of their audit services.

Additionally, workplace gender discrimination has been shown to pressure female auditors to outperform their male colleagues to succeed professionally (Hardies et al., 2021; Lennox & Wu, 2018). These gender-based differences could have significant implications for M&A transactions. The professional prudence and ethical behavior exhibited by female auditors may not only enhance the quality of audit reports but could also affect key decisions in M&A, such as target selection. Gender differences between the auditors of the acquirer and target may therefore influence the dynamics and outcomes of these transactions, especially when gender-specific attributes are fully considered.

PCAOB Rule 3211, which mandates the disclosure of the audit partner’s name, has triggered research into the role of individual auditors in shaping audit quality (Burke et al., 2020; Chu et al., 2022; Gul et al., 2013; Hardies et al., 2015, 2016; Hou et al., 2019). These studies suggest that auditors bring their own specialized knowledge, experience, and incentives into the audit process, and that their individual decisions leave a lasting imprint on the audit reports. This becomes particularly relevant when gender is considered as a key variable in determining audit quality and effectiveness.

While research has demonstrated the positive effects of female auditors’ ethical conduct and risk-averse tendencies, the impact of gender on audit quality can yield conflicting results, particularly in the presence of workplace gender discrimination. In China, where audit regulations mandate the disclosure of both junior (engagement) and senior (review) auditors, research has begun to explore the influence of individual auditors, including the moderating effects of gender (Cameran et al., 2020). These dynamics become especially relevant in M&A contexts, where shared auditors between the acquirer and target could shape target selection and deal success.

The practice of shared auditing is particularly important in this context. The involvement of shared auditors may encourage more rational and responsible decision-making, which aligns closely with the prudent and ethical behavior of female auditors. Therefore, in the M&A process, the professional competence of female auditors combined with the advantages of shared auditors can effectively enhance the success rate of transactions and the rationality of target selection.

Research indicates that female auditors typically demonstrate higher diligence and risk aversion, making them more meticulous and cautious in the audit process, which in turn improves audit quality. This high-quality auditing not only provides the acquirer with accurate financial information but also reduces information asymmetry, facilitating more effective target selection. In summary, the unique qualities of female auditors significantly impact the success of mergers and acquisitions and the selection of targets.

Building on these insights, we hypothesize that the role of shared auditors in M&A transactions may be moderated by the gender of the auditors. Specifically, the presence of female auditors could strengthen the influence of shared auditors on the success of M&A, given the higher levels of diligence, prudence, and ethical behavior typically associated with female auditors. We thus propose the following hypotheses:

H2: The role of the shared auditor is stronger when all four signing auditors are female.

H2a: The role of the shared auditor is stronger if both auditors of the bidder are female.

H2b: The role of the shared auditor is stronger if both auditors of the target are female.

Partner Background

Several studies have demonstrated that individual audit partners can have a significant impact on audit outcomes, with notable variations in performance across different auditors. For example, Gul et al. (2013) found that partner-specific characteristics can lead to differences in audit quality. Early career experiences have also been shown to influence professional skepticism, shaping auditors’ judgments and decision-making processes (He et al., 2018). These variations emphasize the importance of examining auditors at the individual level, rather than focusing solely on the firm level.

Although there has been growing interest in studying individual auditor characteristics, research has been somewhat limited due to the lack of mandatory disclosure of audit partners’ names in some countries (Laurion et al., 2017; Lennox & Wu, 2018). This lack of transparency has made it difficult to fully explore the impact of specific partners on audit quality. However, recent regulatory changes, such as the mandatory disclosure of audit partners in certain regions, have allowed researchers to delve deeper into the influence of individual auditors on the audit process. For instance, the mandatory disclosure of auditor names in China has provided a unique opportunity to investigate how specific auditor characteristics affect audit outcomes and financial reporting quality.

Research has also highlighted the differences between junior and senior audit partners. Firms tend to favor selecting junior partners, who generally charge lower fees, especially following a change in audit firms (Cao & Feng, 2022). However, this preference for junior partners can lead to reduced pressure to maintain audit quality. Senior partners, with their greater experience and expertise, tend to uphold higher auditing standards, and provide more rigorous assessments, which can be critical in contexts such as M&A.

The role of individual auditor characteristics, such as experience, is particularly relevant in M&A transactions, where audit quality, and reliability are essential for accurate financial reporting and due diligence. While prior studies have highlighted the positive influence of senior audit partners on audit quality, the specific implications of auditors’ backgrounds on M&A decisions remain relatively underexplored. This gap in the literature suggests a need for further investigation into how individual auditors, particularly senior partners, influence M&A outcomes.

Building on the existing literature, this study aims to explore how the status of signing auditors (whether junior or senior) affects M&A transactions. Specifically, we categorize auditors into two subgroups—junior and senior partners—and propose that senior partners play a more significant role in facilitating successful M&A transactions due to their higher levels of expertise and professional skepticism. Accordingly, we propose the following hypotheses:

H3: Three-quarters of the signing auditors are partners, so there is a stronger role for shared auditors.

H3a: The role of the shared auditor is stronger if two signing auditors of the acquirer are partners.

H3b: The role of the shared auditor is stronger if two signing auditors of the target are partners.

The conceptual framework in Figure 1 illustrates the underlying assumptions and variables that guide our hypothesis testing and help to understand the relationships among the different components of this study.

Conceptual framework.

Sample Selection, Measures, and Research Design

Sample and Data

Population and Sampling Procedures

The study focuses on M&A transactions of China A-share listed companies from 2010 to 2020. To ensure comprehensive data coverage in our database, we selected 2010 as the starting year, which is 2 years after the China Securities Regulatory Commission (CSRC) requirement for names disclosure in 2008. We exclude financial firms and failed deals. For multiple acquisitions completed by the same bidder in the same year, only the first acquisition is retained.

The number of M&A events from 2010 to 2020 is 770, and it is reduced to 468 samples due to missing data on the auditor’s gender and partner background, as shown in Table 1. We utilized the winsorization at the 1% and 99% for all continuous variables. The financial data, audit firm and auditor information were collected from CSMAR, and any missing values are manually searched for and supplemented.

Sample Selection.

Note. The source of observation is all from CSMAR.

Data Generation and Coding

We employed a matching approach to construct a control group, employing industry and size criteria, using the 468 M&A events derived from the preceding data processing as the matched sample. Following the previous studies (Bodnaruk et al., 2009; Capron & Shen, 2007), Guidelines for the Industry Classification of Listed Companies (2012) and data from A-share listed companies are used to select companies with similar industry and size characteristics (within 10% above and below total asset size, with a 1:1 ratio) as the matched group. During the matching process, some companies were not successfully matched due to the limited availability of suitable control firms with similar industry and size characteristics. After pairing, the resulting study sample consisted of 885 samples (468 treated samples and 417 matched samples). The data processing and regression analysis are conducted using STATA 17.0 statistical program. Table 2 shows the specific information of matched samples and total samples.

Real Samples and Matched Samples.

Measurement

Dependent Variables

Target selection (TS). In this paper, TS is defined as whether a company is the real target or not. The real target equals 1 if a company is the real target of the M&A transaction; and 0 otherwise. We define the real target as the company that is acquired in an M&A deal.

Independent Variables

Same audit firms but different signing auditors (sharedauditor). The variable equals 1 if the acquirer and the target share the same audit firm but do not share the signing auditor; and 0 otherwise.

Moderator Variables

The study employs the following indicator variables to measure the impact of gender differences and partner background on M&A decisions:

Female auditors (Female). Chinese regulatory mandates necessitate the inclusion of two individual auditors’ signatures on each audit report—one junior (engagement) auditor and one senior (review) auditor (MOF, 1995a, 1995b). Accordingly, for both sides of M&A, there are four auditors. The indicator variable takes the value of 1 if four signing auditors on each side of the M&A are all female; and 0 otherwise. Partner Signing Auditors (Partner). The indicator variable takes the value of 1 if three-of-four signing auditors on each side of the M&A are partners; and 0 otherwise. The bidder’s signing auditor gender (Bidder_Female). The indicator variable takes the value of 1 if two signing auditors of the bidder are all female; and 0 otherwise. The target’s signing auditor gender (Target_Female). The indicator variable takes the value of 1 if two signing auditors of the target are all female; and 0 otherwise. Partner background of the bidder (Bidder_Partner). The indicator variable takes the value of 1 if two signing auditors of the bidder are all partners; and 0 otherwise. Partner background of the target (Target_ Partner), the indicator variable takes the value of 1 if two signing auditors of the target are all partners; and 0 otherwise.

Control Variables

This study controls for two main factors that may influence M&A decisions, target characteristics, and shareholding structure (Y. Cai et al., 2016). The data are selected from the year before the first M&A announcement.

Target Characteristics. Controls represent the characteristics that are associated with the same audit firms and the same signing auditors. All variables are taken from the year preceding the M&A announcement date. To account for target characteristics, we included the natural logarithm of the target’s assets (SIZE), leverage (LEV), which is measured as the total liabilities to total assets ratio, and sales growth (GROWTH; Ashbaugh-Skaife et al., 2008; Y. Cai et al., 2016; Capron & Shen, 2007; Dhaliwal et al., 2016; Gaur et al., 2013). Additionally, we included operating cash flow (OCF) divided by the total assets. In addition to the financial condition, we also control for shareholding ratios of the largest shareholders (LSR). We also control whether the acquisition is paid with stock (PAY) because managers may have different incentives to make stock-based versus cash-based acquisitions (Erickson & Wang, 1999). In terms of profitability, this paper uses return on equity (ROE) to measure profitability (Capron & Shen, 2007). Asset quality is a function of M&A cost, which ultimately determines whether a company can become an M&A target. To capture asset quality, we include two variables: the book to market ratio (BM) and the price to earnings ratio (PER; Y. Cai et al., 2016). Additionally, a company’s governance structure can have an impact on M&A transactions (Capron & Shen, 2007), which we capture through three variables: board size (SCALE), independent directors’ proportion (IND), and duality (DUAL). In particular, SCALE is the number of board members of the targets. IND is the ratio of the number of independent directors to the sum of board members. DUAL is measured as the dualling of the chairman and CEO of the target. We also include stock volatility (STD), which reflects the uncertainty of a company’s prospects. Generally, higher stock volatility indicates a higher risk of uncertainty and a lower possibility of becoming an M&A target. In this study, we use the standard deviation of monthly stock returns (Kang & Kim, 2008). Finally, we include the competitive intensity of the product market (HHI). Also, we control for industrial effect, and year effect. The variables and definitions are listed in Appendix A.

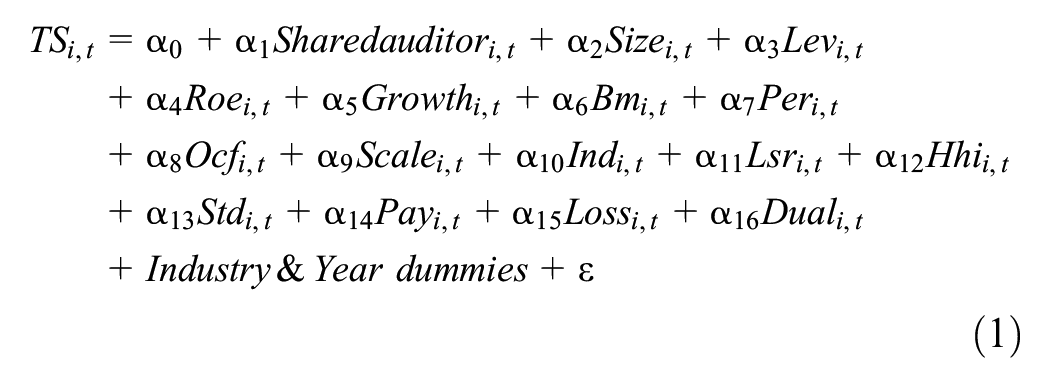

Model Specification

This study examines the effect of the independent variable “Shared Auditors” (excluding the same signing auditors) and the moderating variables of signing auditors’ gender and partnership on the dependent variable. Existing literature indicates that the Probit model provides more robust estimation results in similar research contexts (Dhaliwal et al., 2016). In the binary choice model of this study, both the independent and dependent variables, particularly the specific characteristics of the auditors, exhibit a normal distribution. Therefore, the Probit model is a better choice for explaining the role these characteristics play in M&A decision-making.

This study uses target selection as the dependent variable, with the specific characteristics of auditors (such as gender and partnership) as independent variables. Control variables are determined based on existing research and include firm-level factors such as company size, financial leverage, and return on equity. We estimated the Probit regression model and gradually validated each hypothesis through the following three models:

Where, TSi,t indicates the real target or not, Sharedauditori,t represents the shared auditor, and α0 is the intercept term.

Where, TSi,t indicates the real target or not, Sharedauditori,t represents the shared auditor, and Femalei,t(Bidder_Femalei,t or Target_Femalei,t) indicates that the auditors are all female (either the bidder’ auditors is female or the target’ auditors is all female). This model tests the hypothesis that gender serves as a moderating variable, specifically whether female auditors enhance the effect of shared auditors.

Where, TSi,t indicates the real target or not, Sharedauditori,t represents the shared auditor, and Partneri,t (Bidder_partneri,t or Target_partneri,t) indicates that the auditors are all partners (either the bidder’s partners or the target’s partners). This model tests whether the status of auditors as partners further enhances the impact of shared auditors on M&A transactions.

The effect of Sharedauditor is examined through the coefficient α1. If α1 is significantly positive (or negative), it indicates a positive (or negative) impact on target selection. Based on the hypothesis, we predict that the coefficient of Sharedauditor in the equation is expected to be positive, and the coefficients of the gender interaction term and the partner interaction term are also expected to be positive. This indicates the validity of the hypothesis, suggesting that shared auditors have a positive impact on the selection of M&A targets, and that female auditors (partnership) have a positive moderating effect in the role of shared auditors.

Empirical Results

Descriptive Statistics

In Table 3, the trends in M&A activities from 2010 to 2020 are presented. Over this period, the number of M&A deals increased steadily and peaked in 2015 with 62 cases. This growth can be attributed to the relaxed policy restrictions on M&A and the introduction of various measures aimed at reducing the cost of M&A. Although there was a dip in M&A events in 2017, the overall trend remained positive. The sample size consists of 468 deals and it is estimated that the sample of shared auditors represents 11.54% of the M&A events. As indicated by this percentage, the phenomenon of sharing audit firms is relatively common. The number of same audit firms is 83 (9.38%) among the 885 total samples. In the treated sample, the proportion is higher than the proportion after matching. This suggests that the same audit firm and signing auditor can increase the likelihood of M&A occurring to some extent. Overall, the data in Table 3 shows a clear trend of increasing M&A activity and suggests the importance of shared audit firms.

Sample Distribution by Year.

Note. The distribution of matched and treated samples is shown in this table. All variables are defined in Appendix A.

Table 4 provides descriptive statistics of the sample. TS’s mean value is 0.529, indicating that the overall sample had an average 52.9% chance of being an M&A target. The proportion of Sharedauditor is 9.38% of the full sample. Regarding the auditor’s gender, the mean value of Female is 0.227, indicating that there is a 22.7% chance of having all female signing auditors. In terms of Partner, the mean value is 0.310, indicating that there is a higher percentage of partners. After dividing the bidder and target subgroups, the gender of the bidder and the target is roughly the same, but there is a higher percentage of partner auditors on the target. For the control variables, the means and medians generally followed a normal distribution.

Full Sample Descriptive Statistics.

Note. The full sample descriptive statistics are presented in this table. All variables are defined in Appendix A.

Table 5 demonstrates the Pearson correlation matrix. The correlation coefficient between target selection (TS) and the same audit firm (Sharedauditor) is .078 (p < .01). This highlights a notable positive correlation between employing the same audit firm and the process of target selection. Hypothesis 1 is supported initially. It should be noted that the other variables’ coefficients in the matrix are almost all below 0.3, indicating that there are weak correlations between the other variables included in the analysis.

Correlation Coefficients.

Note. This table reports the correlation matrix.

, **, ***p < .1, p < .05, p < .01, respectively. The variables are defined in Appendix A.

Regression Results

Test of Shared Auditor and Gender Moderator Variable on Target Selection

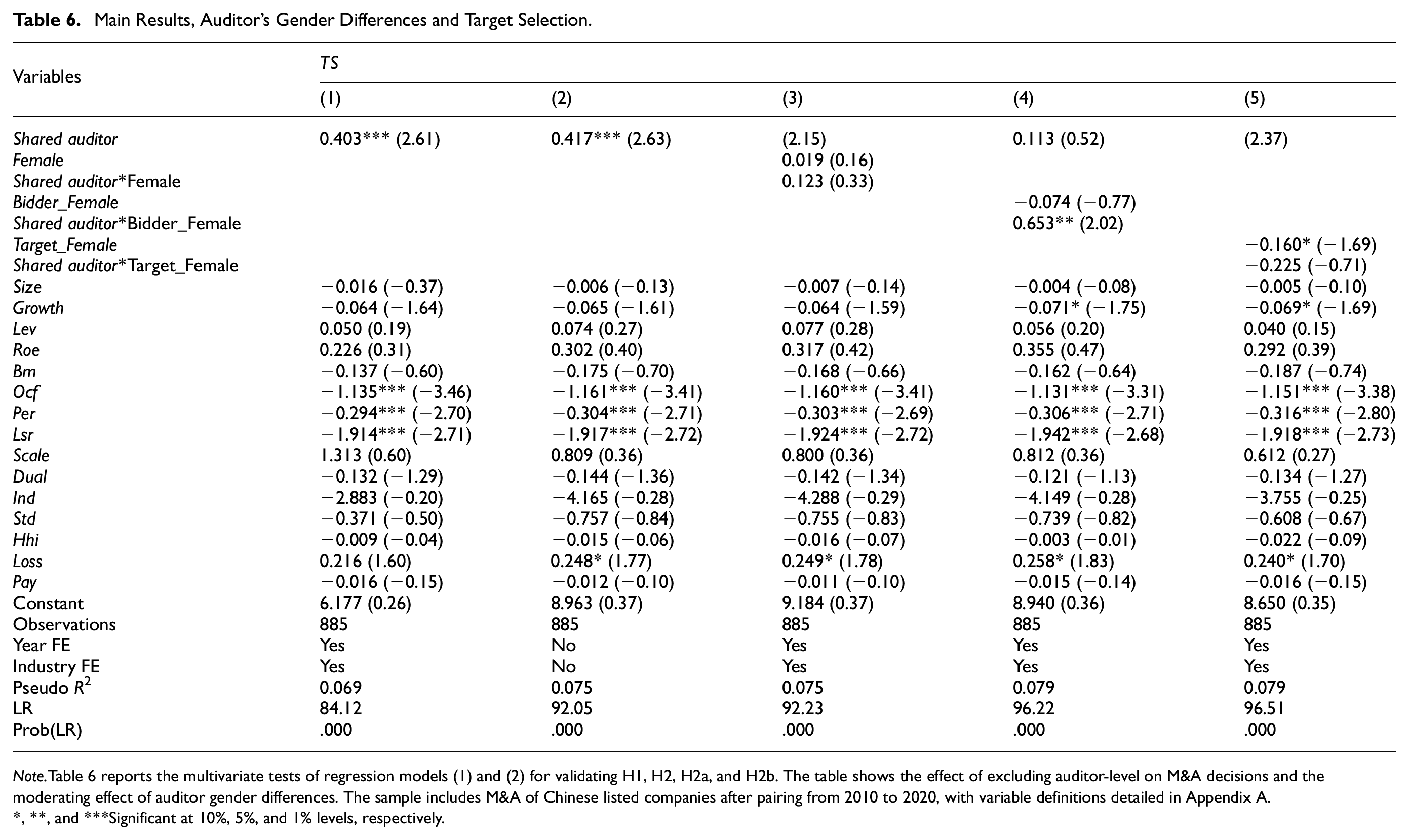

The empirical results presented in Table 6 offer several insights into the relationship between shared auditors and M&A target selection, as well as the moderating role of gender. In Column (1), the positive and significant coefficient of the shared auditor indicates that targets sharing auditors with the acquirer are more likely to be selected for M&A. In Column (2), after controlling for industry and year effects, the significance of the coefficient remains robust. The regression coefficient (z-value) for shared auditor (Sharedauditor) after controlling for industry and year is 0.417 (2.63), a significantly positive (+) value. It posits that the likelihood of a target being selected for M&A increases if it shares its auditor with the acquirer, supporting hypothesis 1 that a shared auditor may be a factor that influences target selection. This finding aligns with previous studies that highlight the role of shared auditors in facilitating information transparency (Bedford et al., 2023; Dhaliwal et al., 2016). Specifically, it supports the argument that shared auditors can promote greater understanding between firms and reduce transaction risks (J. Z. Chen et al., 2020), which in turn increases the likelihood of successful M&A transactions.

Main Results, Auditor’s Gender Differences and Target Selection.

Note. Table 6 reports the multivariate tests of regression models (1) and (2) for validating H1, H2, H2a, and H2b. The table shows the effect of excluding auditor-level on M&A decisions and the moderating effect of auditor gender differences. The sample includes M&A of Chinese listed companies after pairing from 2010 to 2020, with variable definitions detailed in Appendix A.

, **, and ***Significant at 10%, 5%, and 1% levels, respectively.

Columns (3), (4), and (5) in Table 6 show outcomes subsequent to incorporating Female, Bidder_Female and Target_Female as moderating variables, respectively. Column (3) displays a positive but not significant (+) value for Shared auditor*Female. We then decompose Female into two variables (Bidder_Female and Target_Female) to separately test the effects of Bidder’s gender and Target’s gender. We observe a significantly positive(+) moderating effect (Coeff. = 0.653, z = 2.02) of Shared auditor*Bidder_Female in Column (4). This supports hypothesis 2a, which states that the moderating effect of female auditors is stronger on the influence of the shared auditor on target selection. It is consistent with prior studies suggesting that female auditors tend to be more diligent, risk-averse, and ethical in their professional judgments, which enhances the quality of financial reporting, and decision-making (Hao et al., 2021; Hardies et al., 2010). The findings in Column (5) do not show a significant effect for the moderating role of Shared auditor*Target_Female, which is inconsistent with the expectation that female auditors at the target firm would also influence M&A outcomes. This discrepancy suggests that the influence of female auditors may vary depending on whether they are associated with the acquirer or the target. One possible explanation is that the risk-averse behavior and enhanced scrutiny attributed to female auditors may be more impactful on the decision-making side (i.e., the bidder) than on the target side.

In summary, this support for Hypothesis 1 and 2a. Shared auditors enhance M&A success, and female auditors in acquirer firms further amplify this effect, suggesting a gender influence in these transactions. While the shared auditor effect is confirmed, the gender moderation results suggest that the influence of female auditors may be more pronounced for the acquirer’s decision-making process.

Test of Shared Auditor and Partner Moderator Variable on Target Selection

The findings presented in Table 7 indicate that the inclusion of partner background variables (Partner, Bidder_partner, and Target_partner) as moderators in the shared auditor effect on M&A target selection yields non-significant results. This contradicts hypotheses 3, 3a, and 3b, which predicted that partner background would strengthen the influence of shared auditors on M&A decisions. These results are inconsistent with prior studies that suggest individual auditor characteristics, particularly partner status, can influence audit outcomes and decision-making processes (Burke et al., 2020; Hardies et al., 2016). Prior research has highlighted the importance of audit partners’ expertise, experience, and decision-making style in shaping financial reporting quality (Cameran et al., 2020; J. Z. Chen et al., 2020).

Partner Background and Target Selection.

Note. Table 7 reports the multivariate tests used to validate regression model (3) for H3, H3a, and H3b. The table shows the moderating effect of auditor partner’s background. The sample includes post-pairing M&A of Chinese listed companies from 2010 to 2020. All variables are defined in Appendix A.

, **, and ***Significant at the 10%, 5%, and 1% levels, respectively.

However, our findings suggest otherwise. One potential explanation for this discrepancy could be that the overall influence of shared auditors is strong enough to render the moderating effect of partner background negligible in the context of M&A. Alternatively, it may be that other factors, such as firm-level processes or organizational dynamics, overshadow the role of individual partners. This suggests that the impact of shared auditors on M&A target selection is more likely a firm-level effect rather than an individual auditor-level effect. While prior studies emphasize the significance of auditor partners in various auditing contexts, this study does not find support for the moderating effect of partner background on the shared auditor influence in M&A decisions. Further research could explore other individual characteristics or specific conditions.

Additional Tests

The escalation in Economic Policy Uncertainty has become a worldwide trend, noted since the global financial crisis and the subsequent Eurozone crisis. In response to these crises, advanced economies’ central banks like the Federal Reserve, European Central Bank, Bank of Japan, and Bank of England have instituted a series of quantitative easing measures. Nevertheless, the unilateral expansion of the Fed could potentially distort exchange rates, leading to the depreciation of the dollar and influencing capital and trade flows (Dedola et al., 2021). These monetary strategies contribute to heightened economic uncertainty (Baker et al., 2016; Campello et al., 2022) and foster economic protectionism (Born et al., 2019; Caldara et al., 2020). Adding to these developments, the UK’s referendum has sparked a significant surge in global uncertainty (Campello et al., 2022).

Research indicates that economic uncertainty leads to short-term output contraction (Baker et al., 2016). A robust connection exists between financial conditions in the US and global markets. Yet, the implementation of several rounds of quantitative easing might engender a cascade of detrimental consequences, especially impactful on emerging market economies. These repercussions encompass protectionist measures, asset market inflations, and excessive leveraging of both households and firms (Aizenman et al., 2017; Iacoviello & Navarro, 2019). The subprime crisis saw an unusual co-movement between equities in advanced economies and emerging market economies, with emerging market economies exhibiting a longer horizon of 6 months (Cortes et al., 2022). This suggests that the economic policies of developed countries in response to crises can cause international capital flows and economic uncertainty, which is more pronounced in developing economies. While monetary expansion may promote mergers and acquisitions during this period, increasing uncertainty may reduce the likelihood of such transactions.

We acknowledge that economic uncertainty impacts corporate decisions, including M&A activities. Additionally, as economic protectionism increases globally, it is crucial to explore its impact on M&A transactions. Monetary expansion and economic uncertainty may generate adverse effects on emerging market economies and subsequently impede M&A activities. Therefore, studying these factors in conjunction with monetary expansion provides a more comprehensive understanding of the driving forces behind M&A activity over the sample period. To identify the factors that influence monetary expansion and economic uncertainty, we introduce two macroeconomic variables as linear regressors: Fed’s balance-sheet size (Fed; Cortes et al., 2022) and Global economic policy uncertainty (EPU; Baker et al., 2016). Fed is defined as the natural logarithm of the ratio of the central bank assets to the gross domestic product (GDP) for the U.S. The measurement of EPU involves computing the logarithm of the relative occurrence of newspaper articles containing a combination of the terms related to economy (E), policy (P), and uncertainty (U) within a specific country. The use of these two macroeconomic variables as linear regressors in our analysis helps us understand the impact of monetary expansion and economic uncertainty. This section examines whether the positive impact of shared auditors on target selection can be explained by the two variables mentioned above.

Model (4) controls for Fed (EPU) based on Model (1), and the results are shown in column (1) of Table 8. The coefficient remains significantly positive, indicating that the main analysis remains significant after controlling for Fed.

The Effect of Monetary Expansions and Economic Policy Uncertainty.

Note. To investigate the potential impact of monetary expansion and economic policy asymmetries on the results of the main analysis, we conducted additional analyses, which are discussed in this table. Specifically, we examined how Fed (EPU) may influence the outcomes of the study. The sample includes post-pairing M&A of Chinese listed companies from 2010 to 2020, with variable definitions detailed in Appendix A.

and ***Significant at the 10%, and 1% levels, respectively.

We add an interaction term of Fed(EPU)* Sharedauditor to Model (5), and an interaction term of Fed(EPU) * Bidder_Female * Sharedauditor and Fed(EPU) * Target_Female * Sharedauditor to Model (6) and Model (7).

Column (2) in Table 8 shows that Fed*sharedauditor has no significant impact on target selection (Coeff. = −0.382, z = −0.51). However, when considering Bidder_Female, we find that Fed*Bidder_Female also has no significant impact on target selection in column (3; Coeff. = 0.075, z = 0.15). Similarly, Fed*Bidder_Female*Sharedauditor on target selection is also not entirely significant (Coeff. = 0.241, z = 1.88). When considering Target_Female, the results in column (4) still indicate insignificance. We also considered the impact of economic policy uncertainty on target selection. We found that even after controlling for EPU, shared auditors still have a significant positive impact on target selection. Moreover, the interaction terms in columns (6), (7), and (8) do not exhibit a significant impact on the correlation between shared auditors and target selection.

The regression results reveal that the connection between shared auditors and target selection in M&A transactions does not depend exclusively on the impact of macro-level monetary and economic policy uncertainty.

Robustness Test

To further check the stability of the findings, we conducted a robustness test by using alternative measures of shared auditors. The model considers “shared auditors” based on the data from 1 year prior to the announcement. To ensure the reliability of this measurement, this study also uses “shared auditor within the 3 years before the M&A.”Table 9 shows that both shared auditors (Sharedauditor_3) and target selection (TS) remain significant (p < .01). In conclusion, even after replacing the main dependent variable (Sharedauditor_3), our findings remain robust and unchanged. This provides more reliable evidence for understanding the relationship between auditor characteristics and merger and acquisition decisions.

Redefinition of the Independent Variable.

Note. Robustness tests are reported in Table 9. The table shows the effect of shared auditor (Sharedauditor_3) on target selection over a 3-year period, with variable definitions detailed in Appendix A.

Significant at the 5%, levels.

Conclusions

Our sample observational data is derived from mainland China. This study provides evidence of the positive impact of shared auditors, along with auditor gender and partner characteristics, on M&A decision-making. It reveals the role of audit information transfer in M&A transactions and offers practical references for companies in selecting audit teams during M&A. Using data from the Chinese market between 2010 and 2020, we successfully validated Hypothesis 1: shared auditors have a positive influence on the selection of M&A targets. Consistent with previous research, employing the same audit firm as the acquirer increases the likelihood of successful mergers, especially when involving the same audit firm, office, or team (J. Z. Chen et al., 2020). Information shared through shared auditors enhances transparency, which increases the likelihood of target companies accepting acquisition proposals and reduces uncertainty risks in M&A transactions.

In the gender hypothesis, we support H2a. And the conclusion rejects hypotheses 3, 3a, and 3b. This positive moderating effect is particularly pronounced when the auditor is female, aligning with the notion that female auditors are more cautious and better at establishing good relationships with clients, significantly improving M&A success rates. This further validates the critical role of shared auditors in information transfer. Although the partner characteristics of auditors do not have a significant impact on M&A decision-making, their positive contribution to enhancing M&A success rates still exists in certain cases. Female auditors tend to be more detail-oriented and responsible when managing conflicts of interest (Abed & Al-badainah, 2013; Alderman, 2017). These traits make them more cautious in the auditing process, thereby reducing information asymmetry in M&A.

Shared auditors enhance M&A success, and female auditors in acquirer firms further amplify this effect. The gender moderation results indicate that the moderating effect of female auditors is stronger on the influence of shared auditors on target selection. This is consistent with prior studies suggesting that female auditors tend to be more diligent, risk-averse, and ethical in their professional judgments, which enhances the quality of financial reporting, and decision-making (Hao et al., 2021; Hardies et al., 2010). As for partner background, the impact of shared auditors on M&A target selection is more likely a firm-level effect rather than an individual auditor-level effect. While prior studies emphasize the significance of auditor partners in various auditing contexts, this study does not find support for the moderating effect of partner background on the influence of shared auditors in M&A decisions. This deviation from the existing literature highlights the need for further exploration of the complexities of auditor characteristics and their impact on M&A outcomes.

Our results have several contributions and implications. First, this study offers significant insights into the impact of auditor gender characteristics on information transfer. It provides a new theoretical perspective for understanding the relationship between individual auditor characteristics and information transfer, particularly concerning the effects of gender diversity. Furthermore, we systematically explored the performance of auditor gender factors in M&A transactions, revealing that the unique advantages of female auditors offer new insights into M&A decision-making. From a practical perspective, companies should pay more attention to the gender diversity of their audit teams, especially the contributions of female auditors in M&A transactions. Female auditors exhibit greater caution and heightened risk awareness, helping companies make more robust decisions in M&A transactions (Abed & Al-badainah, 2013; Bernardi & Arnold, 1997; Huang et al., 2015; Ittonen & Peni, 2012; Palvia et al., 2015; Peni et al., 2010). Therefore, when selecting audit teams, companies should consider gender diversity, particularly in high-risk M&A transactions, as the involvement of female auditors may lead to more favorable M&A outcomes. Companies can optimize the M&A decision-making process and outcomes through a gender-balanced and diversified audit team configuration, better addressing complex transactional environments. During M&A processes, companies should consider the positive role of shared auditors, especially when M&A involves complex financial and information transfer. Shared auditors can help companies better evaluate acquisition targets and reduce information asymmetry through effective information transfer and risk identification, which is particularly important for companies involved in complex financial and information disclosure. It is advisable for companies to prioritize collaboration with partners that have shared auditors during M&A.

Second, our study provides new evidence supporting the role of shared auditors in M&A transactions, particularly in institutional environments similar to China’s M&A market. This research not only expands the application scenarios of audit theory but also provides a theoretical basis for understanding the role of auditors in complex transactions, especially in information-complex and decision-challenging M&A environments. Previous studies have confirmed that shared auditing has a series of impacts during M&A processes (Bedford et al., 2022; Y. Cai et al., 2016; Chahine et al., 2018; T. Chen et al., 2012; J. Z. Chen et al., 2020; Chircop et al., 2018; Dhaliwal et al., 2016), particularly concerning the completion of mergers and the selection of target companies (Bedford et al., 2022; Dhaliwal et al., 2016). Specifically, our results are consistent with previous studies that emphasize the importance of audit networks in promoting information sharing and resource acquisition (Aguir et al., 2022; C. Cai et al., 2019; J. Z. Chen et al., 2019; J. Chen et al., 2022; Francis & Wang, 2021; Hu et al., 2022; Ton, 2022).

Additionally, the significance of our research lies in the dynamics of audit relationship networks and M&A activities. Social organizations might consider establishing closer shared auditor mechanisms to improve the effectiveness of information transfer in M&A transactions. Companies could also implement strategies that encourage and support the professional development of female auditors, thereby increasing the gender diversity of audit teams and promoting the efficient transfer of audit information. The findings offer valuable references for policymakers and regulatory agencies. In promoting gender diversity policies within companies and constructing audit teams, policymakers may consider guiding companies to enhance the diversity of their audit teams, particularly achieving gender balance, to further promote the stability, and success of corporate M&A transactions.

The findings may have limited generalizability due to variations in regulatory and institutional contexts across different countries and regions. Additionally, the effectiveness of shared auditors may be impacted by differences in auditor quality and independence, which can vary across firms and industries. These limitations highlight the need for future research that employs a multi-method, multi-level approach to capture the complex and dynamic nature of M&A transactions and the role of shared auditors. To address these limitations, future research could investigate the underlying mechanisms that explain the impact of shared auditors on target selection in M&A, and explore the influence of other auditor characteristics, such as experience, expertise, and industry specialization. Moreover, the scope of investigation could be expanded to include other types of corporate transactions, such as joint ventures, strategic alliances, and divestitures, and consider the impact of cultural norms, values, and institutional frameworks on the use and effectiveness of shared auditors in corporate transactions. Overall, there are several promising avenues for future research that can deepen our understanding of the role and impact of shared auditors in corporate transactions. By addressing these limitations and expanding the scope of investigation, future research can offer valuable insights that can inform and improve M&A decision-making processes.

Footnotes

Appendix

| Variables | Definitions |

|---|---|

| Dependent variables | |

| TS | The real target equals 1 if a company is the real target of the M&A transaction; 0 otherwise. We define the real target as the company that is acquired in an M&A deal. |

| Independent variables | |

| Sharedauditor | The variable equals 1 if the acquirer and the target share the same audit firm but do not share the signing auditor; 0 otherwise. |

| Moderator variables | |

| Female | The indicator variable takes the value of 1 if four signing auditors on each side of the M&A are all female; 0 otherwise. |

| Partner | The indicator variable takes the value of 1 if three-of-four signing auditors on each side of the M&A are partners; 0 otherwise. |

| Bidder_Female | The indicator variable takes the value of 1 if two signing auditors of the bidder are all female; 0 otherwise. |

| Target_Female | The indicator variable takes the value of 1 if two signing auditors of the target are all female; 0 otherwise. |

| Bidder_Partner | The indicator variable takes the value of 1 if two signing auditors of the bidder are all partners; 0 otherwise. |

| Target_Partner | The indicator variable takes the value of 1 if two signing auditors of the target are all partner; 0 otherwise. |

| Additional tests | |

| Fed | The natural logarithm of the ratio of the central bank assets to the gross domestic product (GDP) for the United States. |

| EPU | The natural logarithm of the relative frequency of newspaper articles in a given country that contain a combination of three terms related to the economy (E), policy (P), and uncertainty (U). |

| Target characteristics | |

| Size | The natural log of total assets. |

| Lev | Total liabilities are divided by the total assets of the target. |

| Growth | Current year operating income minus prior year operating income to prior year operating income. |

| Ocf | Operating cash flow to the prior year’s total assets. |

| Roe | The ratio of the net income to the target’s equity. |

| Lsr | The shareholding ratio of largest shareholder. |

| Bm | The book value of the target’s equity to the market value. |

| Per | The ratio of the actual and potential target’s share price to earnings per share. |

| Shareholding structure | |

| Scale | The number of board members of the target. |

| Dual | The indicator equals 1 if there is a duality of chairman of the board and CEO of the target; 0 otherwise. |

| Ind | The indicator of the proportion of independent directors on a board of directors of a target company to the total number of board members. |

| Std | The standard deviation of monthly stock returns of the target. |

| Hhi | HHI=∑(Xi/X) 2, X=ΣXi, Xi is the operating revenue of firm i in the industry of the target. |

| Pay | The indicator variable equals 1 if the acquirer uses stock as a method of payment; and 0 otherwise. |

| Loss | The indicator variable equals 1 if the acquirer’s net profit>0; and 0 otherwise. |

| Robustness tests | |

| Sharedauditor_3 | The variable equals 1 if the acquirer and the target share the same audit firm but do not share the signing auditor within 3 years before the announcement; 0 otherwise. |

| Dummy variables | |

| Industry | Based on Guidelines for the Industry Classification of Listed Companies (2012). |

| Year | M&A transactions took place from 2010 to 2020, with 10 years of dummy variables set. |

Note. All accounting variables are derived from data of the preceding year and the variables related to M&A are as of the acquisition announcement year. The source of observations is all from CSMAR.

Acknowledgements

Special thanks to the reviewers for valuable comments.

Ethical Considerations

This research did not involve human or animal participants.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by the Scientific Research Program for Higher Education Institutions of Hebei Provincial Department of Education (Grant No. QN2025869).

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

All data are publicly available from the sources identified in this paper.