Abstract

This study aims to investigate the impact of shared auditors and same signing auditors on audit quality in M&A transactions. Existing research suggests that shared auditors in M&A transactions are considered to enhance information symmetry, thereby improving transaction quality. However, there is a lack of systematic research on how shared auditors influence audit quality in M&A, particularly regarding the interaction with same signing auditors. Using a sample of 1,083 M&A transactions from the Chinese market between 2004 and 2020, we analyze the impact of shared auditors and the same signing auditors on audit quality during the M&A process. The findings indicate that both shared auditors and same signing auditors contribute to improved audit quality in M&A. Further analysis reveals that this enhancement effect is more pronounced in M&A across industries and provinces. Moreover, the impact on audit quality is stronger when the bidder is larger, non-state-owned, or not audited by the Big 4 audit firms. This study provides empirical evidence on the roles of auditors at both the firm and individual levels in improving audit quality, highlighting the potential value of shared auditors. The conclusions offer recommendations for enhancing audit quality and make informed choices regarding auditors.

Plain language summary

This study examines the impact of shared audit firms or signing auditors on audit quality in mergers and acquisitions (M&A). Auditors play a vital role in ensuring the reliability of financial information, which is essential for the success of M&A transactions. Analyzing data from over 1083 M&A deals in China between 2004 and 2020, the study finds that when companies use the same audit frms or signing auditors, audit quality improves. This effect is more pronounced in cross-industry or cross-regional transactions. The positive impact is especially significant for larger companies, non-state-owned enterprises, and those not audited by the Big 4 firms. These results suggest that shared auditors enhance access to reliable financial information, which reduces risks in M&A. The study offers practical guidance for businesses on how to strategically select auditors to improve both audit quality and M&A outcomes.

Introduction

Given the strategic imperative for expanding industry scale and capturing market share, Mergers and Acquisitions (M&A) have emerged as the preferred external growth strategy for listed companies. However, due to incomplete information disclosure, acquirers often face information opacity and low credibility in target’s financial reports. According to information asymmetry theory, uneven information distribution between transaction parties can hinder the transaction process. Informal systems and various information networks play a vital role in addressing this issue (Peng & Luo, 2000).

Recent studies highlight the role of social networks, particularly shared auditors, in M&A decision-making (Bedford et al., 2023; Y. Cai et al., 2016; Chahine et al., 2018; Chircop et al., 2018; Dhaliwal et al., 2016). Shared auditors is a term used when two firms select the same audit firm (T. Chen et al., 2012). When borrowers and lenders in lending relationships share the same auditor office, the audit quality is improved (Ton, 2023). The utilization of professional auditors and functioning within industries characterized by greater homogeneity is linked to enhanced audit quality (Sun et al., 2020). Moreover, common signing auditors contribute to greater financial statement comparability by applying consistent accounting standards and professional judgment (Jiu et al., 2020). They also increase information transparency, fostering better comparability across companies (Livne et al., 2024). In addition, the professional judgment of individual signing auditors also contributes positively to audit quality and consistency.

While prior research on shared auditors in M&A has focused on post-merger performance and M&A premiums, their impact on audit quality remains underexplored. This study aims to: (1) analyze the role of shared auditors and same signing auditors in enhancing audit quality, particularly for bidder in M&A; (2) examine the differential impact of shared auditors in cross-industry and cross-province transactions; and (3) investigate how the characteristics of the acquirer, such as firm size, ownership, or engagement with a “Big 4” audit firm, moderate the impact of shared auditors on audit quality.

For several reasons, first, social networks facilitate information sharing, reducing the high costs and low transparency of M&A (Baxamusa et al., 2024; T. Chen et al., 2012; Peng & Luo, 2000). Augmenting information exchange between the involved entities is deemed a critical approach to heighten the efficacy and advantages of M&A (L. Li et al., 2018). The moderate involvement of third-party intermediaries has a positive impact on M&A (Ahn et al., 2010; Bi & Wang, 2018; Cukurova, 2012; de Sousa Barros et al., 2020; Dhaliwal et al., 2016; Golubov et al., 2012). Firms with the same auditor exhibit similar financial reporting patterns, lowering transaction premiums and improving market returns (Bedford et al., 2023; Y. Cai et al., 2016; Dhaliwal et al., 2016; Robert Knechel et al., 2015).

Second, financial reports must be independently audited in compliance. The junior (engagement) auditor and the senior (review) auditor should both sign and seal the audit report, as Audit Standards No. 1501 and No. 1121 issued by the Department of Treasury. In China, disclosing signing auditors’ identities highlights their unique approaches, improving financial statement comparability (Jiu et al., 2020; L. Li et al., 2018). The personal methods employed by auditors play a noteworthy role in enhancing the comparability of financial statement consistency (J. Z. Chen et al., 2020; Jiu et al., 2020).

Third, industry-specific mergers benefit from faster information flow, lower costs, and specialized auditors (Dunn et al., 2000; Solomon et al., 1999). Cross-industry mergers face greater information challenges, where shared auditors mitigate asymmetry (Bathelt & Henn, 2021; Luypaert & Van Caneghem, 2014). While geographic proximity aids communication, shared auditors are crucial when distance hinders information flow (Ciobanu, 2016; Z. Jin et al., 2021). For state-owned enterprises (SOEs), mergers are often policy-driven, and shared auditors facilitate collaboration by mitigating information barriers (Gu et al., 2020). Larger firms tend to hire high-quality auditors (T. Chen et al., 2012) and set higher expectations for targets (Dhaliwal et al., 2016). While Big 4 auditors ensure independence and quality, non-Big 4 firms may better align with client needs (Jain & Agarwalla, 2022). Thus, challenges in information sharing arise from decentralized structures, cross-industry regulations, regional differences, and the scale of firms, with larger audit firms typically being more effective.

Overall, based on M&A data from China’s A-share market from 2004 to 2020, we analyze the impact of shared auditors and the same signing auditors on audit quality during the M&A process. We find empirical evidence that is largely consistent with most hypotheses, with the effect being more pronounced for same signing auditors. To further explore the role of shared auditors and same signing auditors in different scenarios, we conducted heterogeneity tests on five factors: (1) industry differences, (2) regional differences, (3) ownership, (4) relative size, and (5) audit firm size. We argue that the effect is more significant in cross-industry, cross-province, larger acquirer, non-SOEs and non-Big 4, where the role of the shared auditor and the same signing auditor in enhancing audit quality.

The study provides valuable additions to existing literature by focusing on the impact of same signing auditors and supplements the relevant literature on the impact of shared auditors (Ai et al., 2020; Bedford et al., 2023; Y. Cai et al., 2016; Chircop et al., 2018; Dhaliwal et al., 2016; Sun et al., 2020). Regardless of whether it involves shared auditors or same signing auditors, both can generate knowledge spillovers based on M&A. In addition, it expands the related research on the heterogeneous effects of shared auditors and same-signing auditors on audit quality, reflected in aspects such as industry, region, relative size, firm nature, and Big 4 accounting firms (Cao & Pham, 2021; Chahine et al., 2018; J. Z. Chen et al., 2020; Jiu et al., 2020; Tong et al., 2022).

The remaining sections include: Section 2 provides the existing literature concerning shared auditors and same signing auditors, and presents the hypotheses. Section 3 presents the data and outlines the empirical model employed. Section 4 presents the empirical analysis. Section 5 offers the conclusions.

Theoretical Framework and Hypotheses Development

Social networks refer to the relationships between various actors is affected by influencing the preferences and decisions (Granovetter, 1985). Information asymmetry theory highlights the uneven distribution of information, which can hinder M&A success, while social networks bridge these gaps to aid decision-making. Transaction cost economics further reveals the complexity of M&A, emphasizing the importance of efficient information flow (Williamson, 1975).

For audit firms, access to additional firm-level expertise. Shared auditors, interlocked directors, and advisors are key in transferring information (Burris, 2005; Y. Cai et al., 2016; C. Cai et al., 2019; Chiu et al., 2013; Cukurova, 2012; Dhaliwal et al., 2016). Auditing, as an external social network, promotes sustainability in economic systems. Shared auditors refer to two or more firms jointly hiring an audit firm for different purposes (T. Chen et al., 2012). Research shows that shared auditors contribute significantly across supply chains (C. Cai et al., 2019; T. Chen et al., 2012), M&A (Y. Cai et al., 2016; Dhaliwal et al., 2016), competitor relationships (Aobdia, 2015), banks and borrowers (Francis & Wang, 2021), investment and financing relationships (Cao & Pham, 2021; Sun et al., 2020) and Strategic alliances (Baxamusa et al., 2024). By facilitating private information exchange, shared auditors reduce transaction frictions and enhance M&A decision-making, particularly in high-risk or cross-border transactions (Y. Cai et al., 2016; C. Cai et al., 2019; T. Chen et al., 2012; Chircop et al., 2018; Francis et al., 2009). Additionally, they help lower acquisition premiums, improve market reactions, and increase asset returns (Bedford et al., 2023; Chircop et al., 2018).

For the signing auditor, in accordance with PCAOB Rule 3211, audit firms must reveal the audit partner’s name (Burke et al., 2020). The junior (engagement) auditor and the senior (review) auditor should both sign and seal the audit report, as Audit Standards No. 1501 and No. 1121 issued by the Department of Treasury. Individual auditors significantly influence audit quality and outcomes (Carey & Simnett, 2006; R. Chen et al., 2009; Chi & Chin, 2011; DeFond & Francis, 2005; Gul et al., 2013; Lennox et al., 2014). In China, signing auditors’ identities are publicly available, making their professional judgment and audit styles more visible (Jiu et al., 2020; L. Li et al., 2018). Notably, individual auditors significantly contribute to enhancing the comparability of client firms’ earnings and ameliorating financial statement comparability (J. Z. Chen et al., 2020; Jiu et al., 2020). Audit quality also improves when borrowers and lenders share the same audit office (Ton, 2023).

Overall, firm-level auditing prioritizes resource integration over individual professional judgment. Shared auditors promote information sharing through industry expertise and firm-wide coordination, ensuring consistent audit services and improving audit quality. In M&A, they strengthen mutual trust and financial reporting consistency. Same signing auditors further enhance information flow and risk control. This paper argues that auditor knowledge spillovers and information-sharing mechanisms improve audit quality, as reflected in higher audit fees and lower discretionary accruals.

Thus, the hypotheses can be formulated as follows:

H1: Audit quality is higher for shared auditors than for non-shared auditors.

H2: Audit quality is higher for same signing auditors than for non-same signing auditors.

In M&A decision-making, acquirers evaluate the target’s industry, resources, and market dynamics, aligning with the resource-based theory, which emphasizes resource heterogeneity. Successful mergers often rely on the integration of these diverse resources, making a comprehensive evaluation of both parties’ resource compatibility a critical factor.

When the acquirer and the target operate in related industries (e.g., upstream or downstream enterprises or direct competitors), shared market environments, business connections, and aligned credit policies reduce communication costs and mitigate information asymmetry (Betton et al., 2009). Auditors with industry expertise improve audit quality and financial reporting (Dunn et al., 2000; Solomon et al., 1999). And acquirers often select industry-expert auditors to better assess targets and enhance post-merger performance (Cui & Chi-Moon Leung, 2020; Dhaliwal et al., 2016). In regional economic integration, industry relevance strengthens synergies in resources, technology, and markets (Wilson & Pholo Bala, 2019). The characteristics of the industry significantly affect the policy implications in M&A decision-making (Shen et al., 2023).

However, cross-industry M&A presents greater integration challenges due to differences in industry scale and structure (Hu, 2024). Acquirers may lack understanding of the target’s industry, increasing information asymmetry (Luypaert & Van Caneghem, 2014). External mechanisms, such as improved geographical proximity, reduce information barriers between companies from different industries, thereby facilitating more efficient cross-industry M&A and increasing the frequency (Ahern & Harford, 2014; Z. Jin et al., 2021). Shared auditors play a crucial role in such transactions by helping acquirers grasp industry dynamics, business processes, information systems, and internal controls, thereby enhancing audit quality and mitigating information asymmetry challenges in cross-industry M&A.

Based on this, the following hypothesis is proposed:

H3: Shared auditors and same signing auditors play a more significant role in improving audit quality in unrelated-industry mergers.

Geographical proximity between acquirers and targets facilitates access to operational and developmental information, reducing information asymmetry (Ciobanu, 2016; Croci et al., 2023; Z. Jin et al., 2021; Kengelbach et al., 2010; C. Li et al., 2022). This advantage is evident in local supply chains, where firms often engage the same audit firm’s branch to oversee both parties within the same province or municipality. Proximity also enhances M&A returns by providing informational advantages (Uysal et al., 2008).

However, cross-industry or cross-regional M&A increases information acquisition challenges, leading to higher consulting costs and risks of overpayment (Bathelt & Henn, 2021; Bick et al., 2017; C. Li et al., 2022; Reddy & Fabian, 2020). Under these circumstances, rely more on external networks, with shared auditors playing a key intermediary role. Cross-regional M&A are more driven by local factors, such as product diversification and the degree of globalization (J. Wu et al., 2024). Through their professional audit activities, shared auditors can access accurate information about the potential target’s operational circumstances and future development. This information intermediary function is especially critical when the geographical distance between the acquirer and the target is greater.

Therefore, we hypothesize that in cross-province M&A, the role of shared auditors and same-signing auditors becomes more significant in improving the quality of audits. They help bridge the information gap that arises due to the geographical and industry distance between the acquirer and target, thereby contributing to a more informed and transparent M&A process. Based on the above analysis, this paper proposes the following hypothesis:

H4: Shared auditors and same signing auditors play a more significant role in improving audit quality in cross-province mergers.

The performance of SOEs in M&A is closely tied to the unique policy support, resource advantages, and market credibility, which make them less sensitive to external market constraints. Despite the transfer of operational authority, the government still uses SOEs to implement its policies (X. Jin et al., 2022). This allows SOEs to mitigate some negative effects of high corporate social responsibility (CSR) on M&A outcomes (Feng et al., 2024; Zou & Ma, 2024). However, SOEs are relatively weaker in resource reorganization capabilities and innovation drive, limiting their ability to fully capitalize on M&A opportunities (Wang et al., 2024). Local SOEs focus on policy goals, while central SOEs prioritize control over state-owned capital (Del Bo et al., 2017), with M&A decisions often driven by government objectives rather than maximizing corporate value (Gu et al., 2020).

In contrast, non-SOEs, lacking political background advantages, prioritize external legitimacy to improve their image and competitiveness. For example, they tend to adopt measures such as high-quality environmental information disclosure and green M&A (Feng et al., 2024; He et al., 2024). Non-SOEs also show greater flexibility and adaptability in M&A, particularly in technological innovation. This difference is evident in shared audit relationships, where government intervention in SOEs weakens auditors’ role in communication, while non-SOEs, with less government interference, are more likely to use shared auditors to reduce information asymmetry.

Based on this, this paper proposes a hypothesis:

H5: Shared auditors and same signing auditors play a more significant role in improving audit quality within non-SOE bidders.

In M&A, the relative size of the acquirer and the target has a significant impact on the decision-making, execution, and outcomes of the deal. Larger acquirers typically dominate the transactions and set higher expectations for targets (Qiao et al., 2023). In contrast, smaller and medium-sized acquirers, constrained by their resources and capabilities, focus more on cost control and risk management by selecting smaller or relatively simpler targets, thus reducing the complexity and potential costs of post-merger integration (J. Wu et al., 2024). And, larger clients are more likely to choose high-quality audit firms (T. Chen et al., 2012; Danos & Eichenseher, 1986; Healy & Lys, 1986; Johnson & Lys, 1990; Reynolds & Francis, 2000). When the acquirer is significantly larger than the target, it exercises greater control over the target, often prompting the target to engage the same auditor as the acquirer (Dhaliwal et al., 2016). This simplifies access to the target’s information and reduces audit and integration costs.

Larger acquirers tend to rely on external intermediaries, such as shared auditors, to obtain critical information about targets. They are better able to integrate the target’s resources, achieve higher synergies, and enhance post-merger innovation and strategic goals (Qiao et al., 2023; Wang et al., 2022). Shared auditors help mitigate information asymmetry, act as communication bridges, and enhance M&A efficiency, especially in complex transactions involving large firms.

Thus, larger acquirers demonstrate a stronger need for information collection and control, with shared auditors playing a crucial role in reducing uncertainties, optimizing resource integration, and achieving strategic and innovation goals. Based on this, we propose the following hypothesis:

H6: Shared auditors and same signing auditors play a more significant role in improving audit quality in larger bidders.

The Big 4 audit firms are renowned for their high standards and independence in auditing, leading to better audit quality and reduced earnings management (Jain & Agarwalla, 2022; Lopes, 2018). As key players in external governance, the Big 4 demonstrate greater independence and professional competence in environments characterized by information asymmetry (Zhang et al., 2024). Their expertise and resources are particularly important in complex industries. In M&A, the Big 4 enhance audit outcomes with their specialized M&A auditing expertise (Gal-Or et al., 2022). Also, the Big 4 primarily serve larger clients with more complex transaction structures and maintain a stable leadership position in high-end markets (Kitto, 2024).

In contrast, non-Big 4 firms face greater challenges due to limited resources and reputational constraints but are motivated to improve audit quality and meet client needs. Non-Big 4 firms place a stronger emphasis on building client relationships and improving service quality to strengthen their market position (Gal-Or et al., 2022). In competitive markets, they often attract clients by offering cost-effective services while optimizing cost structures through shared resources and expertise (Kitto, 2024).

In M&A, non-Big 4 firms use shared auditors as intermediaries to compensate for weaker brand effects and market share. These relationships promote information transparency and resource integration, supporting clients with focused informational needs. We expect the intermediary role of shared auditors or signing auditors is more evident in non-Big 4 firms. Based on this, we propose the following hypothesis:

H7: Shared auditors and same signing auditors play a more significant role in improving audit quality with non-Big 4 audit firm.

Sample Selection, Measures, and Research Design

Sample Selection

This study selects completed M&A in the Chinese A-share listed company listed in Shanghai Stock Exchange (SSE) and Shenzhen Stock Exchange (SZSE) from 2004 to 2020. M&A are characterized by the successful transfer of control or ownership rights between the bidder and the target. We exclude financial firms and failed deals. For multiple acquisitions completed by the same bidder in the same year, only the first acquisition is retained.

This procedure left us with 1,083 M&A transactions. To address potential outliers, all continuous variables are winsorized at 1% and 99%. Financial data, audit firm information and auditor information were sourced from the China Stock Market and Accounting Research (CSMAR) database, the missing data are manually searched and supplemented. The categorization of a company’s industry was determined by adhering to Guidelines for the Industry Classification of Listed Companies (2012).

Variable Definitions

Dependent Variables

Our main analysis investigates the impact of shared auditors on audit quality. Specifically, we use two audit quality proxies. The first proxy is AUDITFEE, the natural logarithm of total audit fees of the bidder, reflecting the effort and complexity involved in the audit process. As noted by Francis (2004), in most cases, high audit fees still serve as a signal of more resources being allocated by the audit firm, thereby improving audit quality (Doyle et al., 2007). Unified auditing, rather than reducing audit fees, actually tends to increase them (Y. N. Wu & Edwin Cheng, 2008). Higher audit fees are generally associated with better audit quality due to increased resources allocated to high-risk engagements.

The second proxy, |DA|, quantifies the absolute magnitude of discretionary accruals of the bidder calculated using the Modified Jones model, as described by Dechow et al. (1995).

Here, TACCi,t represents the total accruals of firm i in year t, scaled by the lagged total assets (Ai,t−1). The absolute value (|DA|) serves as the second proxy for audit quality. Lower |DA| values indicate higher audit quality. The model is specified as:

Where,

TACCi,t = Accounting earnings- Cash Flow from Operating activities

DAi,t = Discretionary accruals

Ai,t -1 = Lagged total assets (total asset in year t-1)

ΔREVi,t = Change in the revenues of company i from year t-1 to year t

ΔRECi,t = Change in the net receivables of company i from year t-1 to year t

PPEi,t = Property, plant, and equipment of company i at the end of year t

εi,t = Errors in company i in the year t

Independent Variables

Shared auditors (SHARE). Shared auditors refer to audit firms that provide auditing services simultaneously to both the acquirer and the target involved in an M&A. According to Y. Cai et al. (2016) and Dhaliwal et al. (2016), the variable is assigned a value of 1 if the acquirer and the target are audited by the same audit firm within the 2 years preceding the first announcement of the M&A; 0 otherwise.

Same signing auditors (SAMESIGN). The variable represents a stricter condition where the acquirer and target not only share the same audit firm but also have identical signing auditors listed in audit reports. This variable is coded as 1 if the individual signing auditors disclosed for both firms are the same within the 2 years preceding the first announcement of the M&A; 0 otherwise.

Moderator Variables

Industry differences (SI). The variable equals 1 when Shared auditor = 1 and the common auditors are from related industries; 0 otherwise (Faccio & Masulis, 2005; Megginson et al., 2004).

Region differences (SP). The variable equals 1 when Shared auditor = 1 and the common auditors are from the same province; 0 otherwise (Portes & Rey, 2005).

Firm nature (SOE). The variable equals 1 when the acquirer is a state-owned enterprise; 0 otherwise.

Relative size (RS). The ratio of the market value of the target’s equity is divided by the acquirer’s equity (Hayward & Hambrick, 1997; Lee & Kocher, 2011).

Audit Firm size (BIG4). The variable equals 1 when the audit firms are from “big 4”; 0 otherwise (Xie et al., 2013).

Control Variables

According to T. Chen et al. (2012) and Y. Cai et al. (2016), we control for two main factors that may affect the M&A decision, target characteristics and shareholding structure. The data are selected from the last fiscal year of M&A.

Controls represent the characteristics that are associated with the shared auditor and the same signing auditor. With respect to deal characteristics, we control for the acquirer’s size (SIZE) that the natural logarithm of the total assets of the real and potential targets 1 year prior to the date of the first announcement of the acquisition was used to measure the size of the company (Y. Cai et al., 2016; Dhaliwal et al., 2016). We also control for leverage (LEV) measured as total liabilities divided by total assets (Capron & Shen, 2007) and sales growth (GROWTH; Ashbaugh-Skaife et al., 2008; Gaur et al., 2013). We also control for whether the acquisition is financed with stock (PAY) because managers may have different incentives to make stock-based versus cash-based acquisitions (Erickson & Wang, 1999). We control for Big 4 audit firms(BIG) of the acquirer because they play an important role in facilitating M&A (Xie et al., 2013) and some prior research suggests that Big 4 auditors provide higher financial reporting quality (Khurana & Raman, 2004). We also control inventory (INVENTORY) scaled by lagged assets. We also control for shareholding ratios of the largest shareholders (LSR). We also keep track of the total shareholder equity to share ratio (NAVPS; T. Chen et al., 2012). In terms of profitability, this study measures profitability using return on equity (ROE), which is defined as the ratio of the target’s net income to the target’s equity (Capron & Shen, 2007). In addition, we use return on assets (ROA) to determine profitability (Bodnaruk et al., 2009). Asset quality is a function of M&A cost, which ultimately determines whether a company is the real target. To assess asset quality, we use the book-to-market ratio (BM) and the price-to-earnings ratio (PER; Y. Cai et al., 2016). The price-to-earnings ratio (PER) is taken as the ratio of share price to earnings per share of the target 1 year before the first announcement date. Also, we included industry dummies and year dummies to control for industrial effect and the effect of time-related contemporaneous correlation. The variables and measurements are listed in Appendix 1.

Research Design

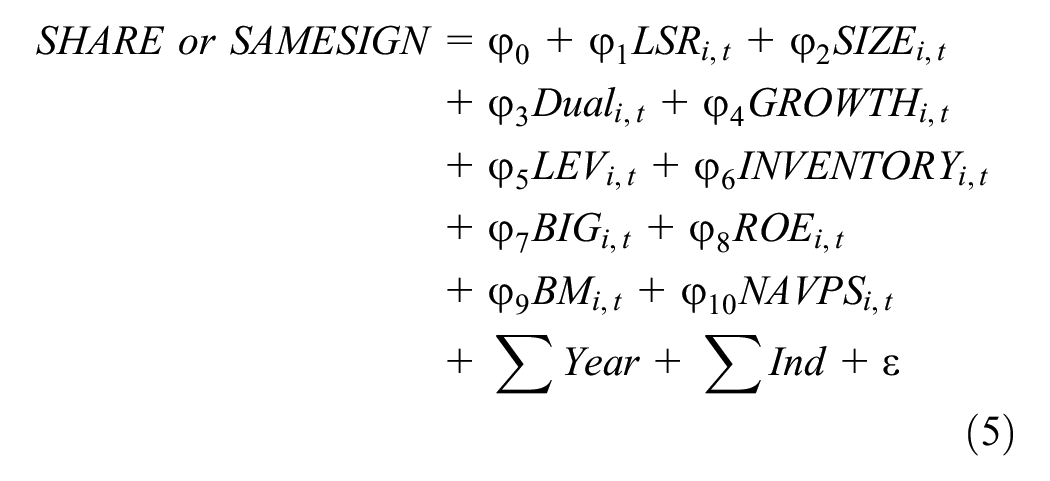

We refer to previous research on the factors influencing audit fees and discretionary accruals. We design the model as follows.

Model (3) evaluates the correlation between audit fees and SHARE (SAMESIGN). We use the coefficient α1 to verify the relationship between audit fees and shared auditor and same signing auditors. If α1 is significantly positive, it indicates that the acquirer’s audit fees are higher and the audit quality is higher with shares auditors or same signing auditors. Otherwise, it indicates that the bidder’s audit fees are lower and the audit quality is lower.

Model (4) is used to measure the association between |DA| and SHARE (SAMESIGN), and we verify the relationship by observing the coefficient β1. If β1 is significantly negative, it indicates that the acquirer has less earning management behavior and higher audit quality with shares auditors or same signing auditors. Conversely, it indicates that the acquirer has more earning management behavior and has no effect on audit quality.

These variables inherently have binary attributes, and dummy variables can accurately reflect their characteristics. Additionally, due to data availability constraints, we are unable to obtain more detailed continuous or categorical data, making dummy variables a feasible alternative. Nevertheless, existing literature indicates that similar binary measurement methods effectively capture the core impact of these variables (T. Chen et al., 2012; Lopes, 2018).

Empirical Results

Descriptive Statistics

Full Sample Descriptive Statistics

In Table 1. The mean value of AUDITFEE (|DA|) is 13.894 (0.087). SHARE accounts for 19.2% of the total sample, while SAMESIGN accounts for 5.4%. The mean value of SOE is 25.7%, suggesting that the sample contains more non-SOEs. The mean value for Industry differences (SI) and Region differences (SP) are 0.200 and 0.366, respectively, indicating that the sample contains more cross-industry and cross-region M&A. As the market and industry become more saturated, companies must choose to seek opportunities in unrelated industries and exotic markets in order to achieve further growth. The mean value of relative size (RS) is −1.913, indicating that the acquirer is smaller. The average of BIG4 is 0.022, indicating that M&A employing big 4 auditors accounts for only 2.2% of the M&A sample and the sample size is small.

Full Sample Descriptive Statistics.

Note. The table displays the full sample descriptive statistics. Detailed definition of variables is in Appendix 1.

Subsample Difference Statistics

We performed a T-test analysis to compare the means of two groups of audit firms, divided based on whether they are shared by two firms. Our findings are presented in Table 2. The findings reveal a significant positive correlation between shared auditors and audit fees. Specifically, the mean value of AUDITFEE is 14.014 for audit firms with shared auditors, compared to 13.866 for firms without shared auditors. Moreover, our results indicate that acquirers tend to exhibit lower mean discretionary accruals when they share auditors. Specifically, discretionary accruals’ mean value is 0.083 for acquirers with shared auditors, compared to 0.088 for those without shared auditors. This finding is consistent with theoretical expectations, providing preliminary support for hypotheses H1 and H2. In addition, the shared auditor group demonstrates notably higher values for same signing auditors (SAMESIGN), region (SP), and audit firm size (BIG4) compared to the non-shared auditor group.

Sub-Sample Difference Statistics.

Note. This table presents T-test result.

Significance levels are represented by *, **, and ***, indicating 10%, 5%, and 1%, respectively. Further explanation of variables is in the note of Appendix 1.

Correlation Analysis

The results of the Person and Spearman correlation analyses conducted between the dependent variable (AUDITFEE), independent variables (shared auditor and same signing auditors), moderating variables (firm nature, relative size, audit firm size, industry, and region), and control variables. In Table 3, The findings reveal that the coefficient between audit fees (AUDITFEE) and shared auditors (SHARE) is .0501 (p < .1), indicating a significant positive relationship. This suggests that companies with shared auditors tend to allocate higher audit fees to improve audit quality. Moreover, the correlation coefficient between discretionary accruals (|DA|) and shared auditors (SHARE) is −.0159 (p < .1), suggesting a significant negative relationship between these two variables. This finding implies that shared auditors can reduce acquirer’s discretionary accruals behavior, increase audit fees and improve financial statement audit quality. Hypothesis 1 is confirmed.

Correlation Matrix.

Note. The table displays the correlation matrix.

The *, **, and *** symbols indicate significance levels of 10%, 5%, and 1%, respectively. Further explanation of variables can be found in Appendix 1.

Similarly, the correlation coefficient between audit fees (AUDITFEE) and same signing auditors (SAMESIGN) is .0305 (p < .05), revealing a significant positive relationship. This indicates that the presence of same signing auditors can help to enhance audit quality. However, the correlation coefficient between discretionary accruals (|DA|) and same signing auditors (SAMESIGN) is −.0100, which is not significant. The audit quality, represented by audit fees, improves to some extent in the case of the same signing auditor, and Hypothesis 2 is confirmed.

Additionally, audit fees (AUDITFEE), industry (SI), firm nature (SOE), audit firm size (BIG4), and relative size (RS) demonstrate a significant positive relationship with audit fees. On the other hand, discretionary accruals (|DA|) exhibit a significant positive relationship with firm nature (SOE) and relative size (RS).

Regression Results

Table 4 illustrates the correlation between audit fees and shared auditors (same signing auditors) in M&A. The results indicate a significant positive coefficient of .2236 (p < .01) connecting shared auditors (SHARE) and audit fees (AUDITFEE). However, this also results in increased fees to account for the shared auditor’s increased workload and the overlap of audits. Shared auditors play a crucial role as information brokers. As such, the findings confirm Hypothesis 1. Furthermore, our regression analysis also uncovers a positive coefficient of .3161 (p < .01) between same signing auditors (SAMESIGN) and audit fees (AUDITFEE), indicating that same signing auditors have a favorable impact on audit fees, particularly at the team level, where information is more likely to be shared. The findings confirm Hypothesis 2.

Estimates of SHARE and SAMESIGN on AUDITFEE.

Note. The table displays the result of SHARE (or SAMESIGN) and AUDITFEE.

The *, **, and *** indicate significance levels of 10%, 5%, and 1%, respectively. Further explanation of variables can be found in Appendix 1.

A regression analysis was performed to examine the impact of shared auditors and same signing auditors on another proxy variable for audit quality, |DA|, as presented in Table 5. The results indicate a significant negative coefficient of −.0574 (p < .01) between SHARE and |DA|, suggesting that the use of shared auditors has a significant adverse impact on discretionary accruals. The findings confirm Hypothesis 1. Moreover, the regression analysis also presents a negative coefficient of −.0320 (p < .01) between same signing auditors (SAMESIGN) and audit quality (|DA|), indicating that the experience and expertise of professional auditors at the team level of same signing auditors can be leveraged to reduce financial statement discretionary accruals and improve audit quality. Hypothesis 2 is verified.

Estimates of SHARE and SAMESIGN on |DA|.

Note. The table displays the result of SHARE (or SAMESIGN) and |DA|.

The * and *** symbols indicate significance levels of 10% and 1%, respectively. Further explanation of variables can be found in Appendix 1.

Additional Analysis

Drawing on prior research, this study identifies five factors potentially affecting information sharing: firm nature, industry and regional differences, relative size, and audit firm size. We aim to examine how these factors may contribute to variations in the impact of our primary findings.

Firstly, the acquirer’s firm nature may influence the ease of information sharing due to differences in organizational structures and cultures. For example, decentralized firms may struggle more with information sharing compared to centralized ones. Secondly, industry differences, such as regulations and competitive dynamics, can affect information sharing. Thirdly, regional differences introduce challenges due to distinct cultural norms, legal frameworks, and market conditions. Fourthly, relative size between the acquirer and target impacts information sharing, with larger firms often requiring and facing more challenges in sharing information. Lastly, audit firm size influences the process, as larger audit firms typically possess more resources and expertise, enabling them to facilitate smoother information sharing compared to smaller firms.

By considering these factors, this analysis may help firms and regulators to better evaluate the potential benefits and challenges of auditor sharing arrangements and team audit work in M&A across different contexts.

Moderating Effect on Audit Fees

Moderating Effect of Industry Differences on the Relationship Between SHARE(SAMESIGN) and AUDITFEE

This study divided the sample into two subsamples based on whether the two firms were in the same industry and conducted separate regression analyses for each subsample. As shown in Table 6, when the acquirer and target are from unrelated industries, a significant positive moderating effect on the relationship between shared auditors and audit fees is observed (Coeff. = .2759, p < .01). Likewise, when the two firm operates in unrelated industries, a positive moderating effect is evident between same signing auditors and audit fees (Coeff. = .3073, p < .05). These results suggest that differing industry contexts increase the information acquisition challenge for the acquirer Thus, both the audit firm and auditor team have a stronger impact in cross-industry M&A. The findings are consistent with Hypothesis 3.

Further Tests Grouping by Industry Differences (AUDITFEE).

Note. The table displays the heterogeneity analysis of SHARE (or SAMESIGN) and AUDITFEE grouping by industry differences.

Significance levels are represented by ** and ***, corresponding to significance at 5% and 1% levels, respectively. Further elaboration of variable definitions can be located in Appendix 1.

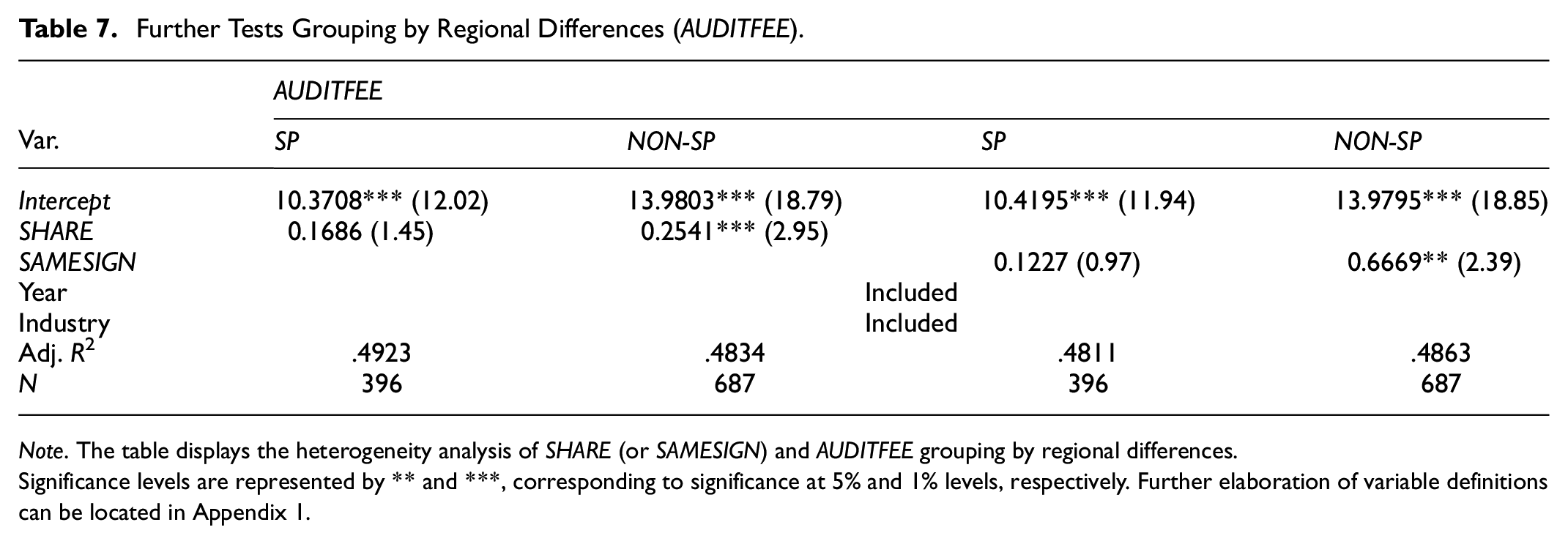

Moderating Effect of Regional Differences on the Relationship Between SHARE(SAMESIGN) and AUDITFEE

Firms in the same region often hire the same branch of an audit firm to reduce costs and improve information access, strengthening the “information sharing” effect. To examine regional differences, the sample was divided into same-province and cross-province groups. In Table 7, the coefficients of AUDITFEE and SHARE for the same-province group are not significant. However, for the cross-province group, the coefficients of AUDITFEE and SHARE are significantly positive (Coeff. = .2541, p < .01), indicating a stronger knowledge-sharing impact. Similarly, the coefficients of AUDITFEE and SAMESIGN are not significant in the same province group but are significantly positive in the different province groups (Coeff. = .6669, p < .05). The results provide support for Hypothesis 4.

Further Tests Grouping by Regional Differences (AUDITFEE).

Note. The table displays the heterogeneity analysis of SHARE (or SAMESIGN) and AUDITFEE grouping by regional differences.

Significance levels are represented by ** and ***, corresponding to significance at 5% and 1% levels, respectively. Further elaboration of variable definitions can be located in Appendix 1.

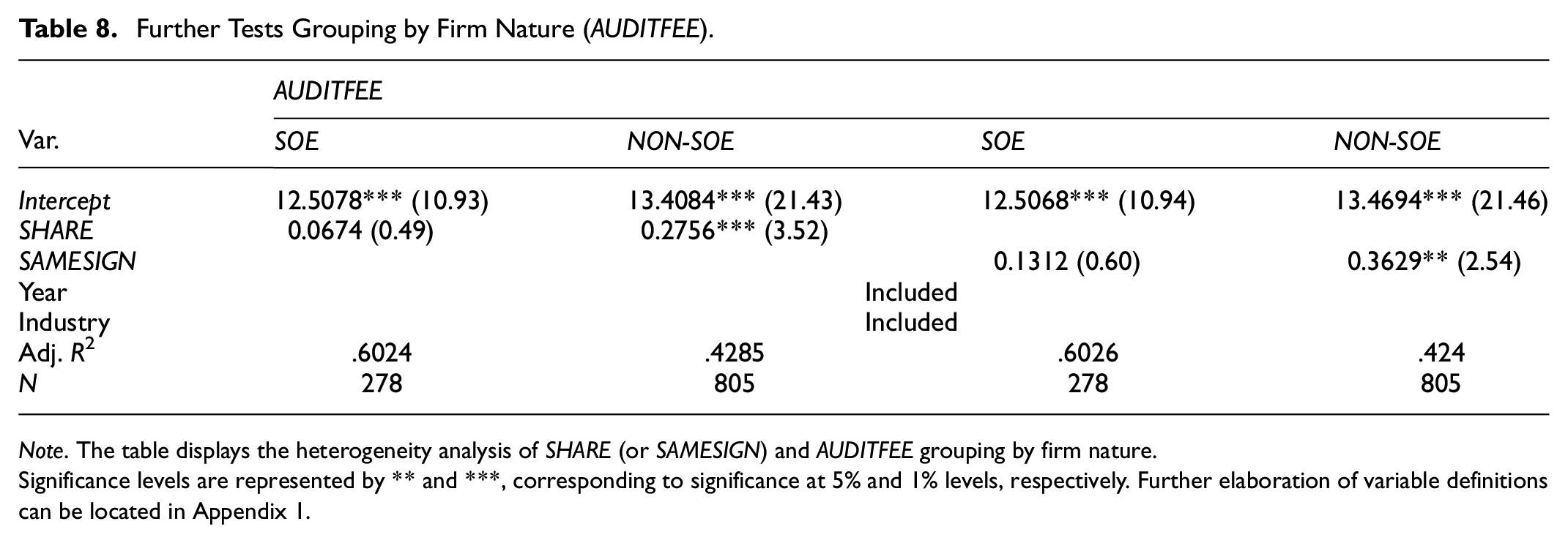

Moderating Effect of Ownership on the Relationship Between SHARE(SAMESIGN) and AUDITFEE

The sample was divided into two subgroups to examine the effect of adding the factor of whether the acquirer is SOEs or non-SOEs, as shown in Table 8. Specifically, when the acquirer is SOEs, the coefficients of AUDITFEE and SHARE are not significant. However, when the acquirer is non-SOEs, AUDITFEE and SHARE are significantly positively related (Coeff. = .2756, p < .01). Regarding the association between AUDITFEE and SAMESIGN, the coefficients are insignificant for SOEs. However, in the case of non-SOEs, AUDITFEE and SAMESIGN show a significant positive relationship (Coeff. = .3629, p < .05). The results confirm Hypothesis 5. These results confirm Hypothesis 5, indicating that the acquirer’s nature moderates the relationship between shared auditors and audit quality in non-SOEs.

Further Tests Grouping by Firm Nature (AUDITFEE).

Note. The table displays the heterogeneity analysis of SHARE (or SAMESIGN) and AUDITFEE grouping by firm nature.

Significance levels are represented by ** and ***, corresponding to significance at 5% and 1% levels, respectively. Further elaboration of variable definitions can be located in Appendix 1.

Moderating Effect of Relative Size on the Relationship Between SHARE(SAMESIGN) and AUDITFEE

As the acquirer’s size increases, so does business complexity, motivating the audit firm to gather and cross-check more information, thus investing more in the audit process. This additional effort often focuses on the acquirer to prevent disguised financial reporting. On the flip side, the target’s shareholders may also be driven to disclose more to improve their financial clarity. To explore this, we segment the dataset into two groups based on the median relative size: larger acquirers and smaller acquirers. Table 9 shows a significant positive moderating effect of shared auditors on audit quality for larger acquirers (Coeff. = .2318, p < .05), implying a more pronounced role played by shared auditors. A similar effect is observed for same signing auditors (Coeff. = .3237, p < .05), highlighting the more pronounced role played by same signing auditors. Thus, there is a clear preference for larger acquirers, where the moderating effect is stronger. The findings confirm Hypothesis 6.

Further Tests Grouping by Relative Size (AUDITFEE).

Note. The table displays the heterogeneity analysis of SHARE (or SAMESIGN) and AUDITFEE grouping by relative size.

Significance levels are represented by ** and ***, corresponding to significance at 5% and 1% levels, respectively. Further elaboration of variable definitions can be located in Appendix 1.

Moderating Effect of Audit Firm Size on the Relationship Between SHARE(SAMESIGN) and AUDITFEE

This section delves into the examination of the moderating impact of audit firm size by categorizing shared auditors as either “Big 4” or “non-Big 4,” as outlined in Table 10. Results indicate a significant positive correlation between AUDITFEE and SHARE for non-Big 4 audit firms (Coeff. = .1887, p < .01), indicating a stronger moderating effect. Similarly, for the relationship between audit fees (AUDITFEE) and same signing auditors (SAMESIGN), a similar moderating effect is observed for non-Big 4 (Coeff. = .3131, p < .01), where the role of the signing auditor is more pronounced. The analysis supports Hypothesis 7.

Further Tests Grouping by Audit Firm Size (AUDITFEE).

Note. The table displays the heterogeneity analysis of SHARE (or SAMESIGN) and AUDITFEE grouping by audit firm size.

Significance levels are represented by ***, corresponding to significance at 1% levels. Further elaboration of variable definitions can be located in Appendix 1.

Moderating Effect on Absolute Value of Discretionary Accruals

Moderating Effect of Industry Differences on the Relationship Between SHARE(SAMESIGN) and |DA|

We also investigate the moderating effect of shared auditors on the absolute value of discretionary accruals (|DA|) by dividing the M&A into related and unrelated industry categories.

In Table 11, there is a significant positive moderating effect of shared auditors (SHARE) on discretionary accruals (|DA|) in unrelated industries (NON-SI, Coeff. = −.0709, p < .01). Likewise, for the relationship between discretionary accruals (|DA|) and same signing auditors (SAMESIGN), a significant positive moderating effect is observed in unrelated industries (Coeff. = −.0383, p < .01). This supports Hypothesis 3. Due to higher information asymmetry in unrelated industries, shared and signing auditors need more time and experience to improve audit work, reducing discretionary accruals, and enhancing audit quality.

Further Tests Grouping by Industry Differences (|DA|).

Note. The table displays the heterogeneity analysis of SHARE (or SAMESIGN) and |DA| grouping by industry differences.

Significance levels are represented by ***, corresponding to significance at 1% levels. Further elaboration of variable definitions can be located in Appendix 1.

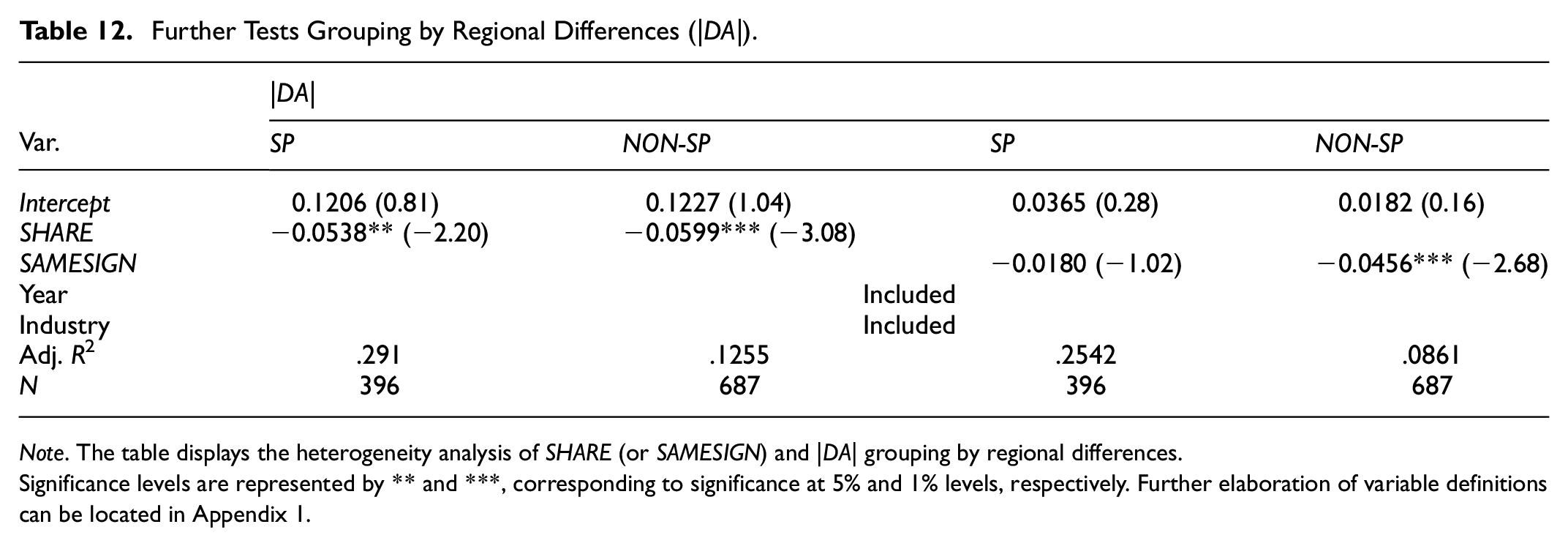

Moderating Effect of Regional Differences on the Relationship Between SHARE(SAMESIGN) and |DA|

Accordingly, this study incorporates the distance factor and divides the sample by province. Table 12 shows that the coefficients of |DA| and SHARE are significantly negative for the cross provinces group (Coeff. = −.0599, p < .01), indicating that shared auditors enhance information sharing and reduce discretionary behavior in cross-province transactions. For SAMESIGN, the coefficients of discretionary accruals (|DA|) and SAMESIGN in the cross provinces group show a significant positive coefficient (Coeff. = −.0456, p < .05), suggesting a stronger moderating effect of same-signing auditors when the acquirer and target are in different provinces. These results support Hypothesis 4.

Further Tests Grouping by Regional Differences (|DA|).

Note. The table displays the heterogeneity analysis of SHARE (or SAMESIGN) and |DA| grouping by regional differences.

Significance levels are represented by ** and ***, corresponding to significance at 5% and 1% levels, respectively. Further elaboration of variable definitions can be located in Appendix 1.

Moderating Effect of Ownership on the Relationship Between SHARE(SAMESIGN) and |DA|

The sample was divided into SOE and NON-SOE subsets. In Table 13, for NON-SOEs, the coefficients of discretionary accruals (|DA|) and shared auditors (SHARE) are significantly negative (Coeff. = −.0778, p < .01). Similarly, the coefficients of discretionary accruals (|DA|) and same signing auditors (SAMESIGN) for NON-SOEs are significantly negative (Coeff. = −.0502, p < .01). The moderating effect of shared auditors and same signing auditors is more pronounced for NON-SOEs. The findings confirm Hypothesis 5.

Further Tests Grouping by Firm Nature (|DA|).

Note. The table displays the heterogeneity analysis of SHARE (or SAMESIGN) and |DA| grouping by firm nature.

Significance levels are represented by ***, corresponding to significance at 1% levels. Further elaboration of variable definitions can be located in Appendix 1.

Moderating Effect of Relative Size on the Relationship Between SHARE(SAMESIGN) and |DA|

We divided the sample into two subsample sets based on the relative sizes. A larger acquirer is defined when the relative size is larger than the median, while a smaller acquirer is defined otherwise. In Table 14, the relationship between discretionary accruals (|DA|) and shared auditors (SHARE) shows a significant negative moderating effect for larger acquirers (Coeff. = −.0833, p < .01), while the coefficients are not significant for smaller acquirers. Similarly, a significant moderating effect is observed between discretionary accruals (|DA|) and same signing auditors (SAMESIGN) for larger acquirers (Coeff. = −.0695, p < .01). Both the audit firm and auditor team levels show a stronger moderating effect for larger acquirers, confirming Hypothesis 6.

Further Tests Grouping by Relative Size (|DA|).

Note. The table displays the heterogeneity analysis of SHARE (or SAMESIGN) and |DA| grouping by relative size.

Significance levels are represented by ** and ***, corresponding to significance at 5% and 1% levels, respectively. Further elaboration of variable definitions can be located in Appendix 1.

Moderating Effect of Audit Firm Size on the Relationship Between SHARE(SAMESIGN) and |DA|

As demonstrated in Table 15, when both parties employ non-big 4 audit firms, there is a significant negative correlation between discretionary accruals (|DA|) and shared auditors (SHARE; Coeff. = −.0653, p < .01). However, this correlation is not significant when both parties hire Big 4 firms. This indicates a stronger moderating effect of shared auditors on discretionary accruals with non-Big 4 firms. Similarly, a significant moderating effect is found for same signing auditors (SAMESIGN), when the signing auditor is non-Big 4 (Coeff. = −.0765, p < .05). The findings are consistent with Hypothesis 7.

Further Tests Grouping by Audit Firm Size (|DA|).

Note. The table displays the heterogeneity analysis of SHARE (or SAMESIGN) and |DA| grouping by audit firm size.

Significance levels are denoted by ** and ***, corresponding to significance at 5% and 1% levels, respectively. Elaborated definitions of variables are provided in the Appendix 1.

Robustness Tests

We further conducted robustness tests in three ways. We run the endogeneity test based on the propensity score matching method. Then, we used different key variables of shared auditors and same signing auditors to test the stability of the results. And also, this study carried out the regression to retest the model by using an alternative variable of audit quality.

Endogeneity Test

To overcome the endogenous problem, this study employed the propensity score matching method (PSM). First, taking SHARE (or SAMESIGN) as the independent variable and taking the largest shareholding’s ratio (LSR), dual position (Dual), company size (SIZE), sales growth rate (GROWTH), inventory to total assets (INVENTORY), asset to liability ratio (LEV), big 4 (BIG), return on equity (ROE), net asset value per share (NAVPS), book to market ratio (BM), the same year (YEAR), the same industry (INDUSTRY) as covariates. To calculate the propensity score, Model (4) was established. Subsequently, the nearest neighbor matching method was applied. The SHARE samples were matched 1:1. 207 samples of SHARE matched 184 samples, total of 390 samples. 57 samples of SAMESIGN matched 53 samples, total of 110 samples. Third, AUDITFEE and |DA| were utilized as the dependent variable, and SHARE was utilized as the independent variable. In Table 16, SHARE and SAMESIGN with AUDITFEE were significantly and positively correlated (p < .01), respectively. SHARE and SAMESIGN with |DA| were significantly negatively correlated (p < .01), respectively. The findings confirmed the persistence of the research conclusions.

Robustness Tests Using PSM Method.

Note. The table displays the results of SHARE (SAMESIGN) and AUDITFEE (or |DA|) using PSM method.

**and ***Denote the significance at 5% and 1% level, respectively. Further elaboration of variable definitions can be located in Appendix 1.

Alternative Measures of Shared Auditors and Same Signing Auditor

This section uses shared auditors for the 3 years prior to the M&A to improve the reliability of the data. After replacing the proxy of shared auditors, as shown in Table 17, SHARE and SAMESIGN with AUDITFEE are significant at the 1% level. SHARE and SAMESIGN with |DA| are significant at the 5% and 10% level, respectively, with no change in the regression results. In summary, the findings are robust after replacing the key independent variable.

Robustness Tests Using Other Measures of SHARE and SAMESIGN.

Note. The table displays the results of SHARE (or SAMESIGN) and AUDITFEE (|DA|) by replacing the independent variable.

*, **, and ***Denote the significance at 10%, 5%, and 1% level, respectively. Further elaboration of variable definitions can be located in Appendix 1.

Alternative Measures of Audit Quality

We employed two alternative measures to evaluate audit quality. The first measure is based on the calculation of the modified Jones model as described by Kothari et al. (2005). Specifically, we used the absolute value of discretionary accruals as a proxy, denoted as absDA, instead of using |DA| in this model. The modified Jones model of Kothari et al. (2005) is based on the modified Jones model of Dechow et al. (1995) by further considering the return on assets (ROA).

Where,

TACCi,t (Total accruals) = Accounting earnings-CFO

Ai,t- 1 = Lagged total assets (total asset in year t-1)

ΔREVi,t = Change in the revenues of company i from year t-1 to year t

ΔRECi,t = Change in the net receivables of company i from year t-1 to year t

PPEi,t = Property, plant, and equipment of company i at the end of year t

ROAi,t- 1 = Return On Assets of company i at the end of year t-1

εi,t = Errors in company i in the year t

As an alternative gauge of audit quality, we adopt a metric, the duration in days of the audit report, to signify audit delay or efficiency.

Table 18 presents regression results showing a significant positive relationship between shared auditors and audit quality. The coefficient for shared auditors (SHARE) with discretionary accruals (absDA) is −.0331 (p < .01), and for same signing auditors (SAMESIGN), it is −.0138 (p < .1), indicating that both reduce discretionary accruals, thereby improving audit quality. Similarly, the coefficient for SHARE with audit efficiency (lag) is −2.7199 (p < .1), and for SAMESIGN, it is −4.1652 (p < .05), suggesting both increase audit lag, further reinforcing audit quality. The findings remain robust after substituting the key dependent variables (absDA and lag).

Robustness Tests Using Other Measures of Audit Quality.

Note. The table displays the results of SHARE (or SAMESIGN) and absDA (or lag) by replacing the independent variable.

*, **, and *** denote the significance at 10%, 5%, and 1% level, respectively. Further definition of variables is in the note of Appendix 1.

Conclusions

This research investigates the impact of shared auditors and same signing auditors on audit quality, based on M&A data from the Chinese A-share market spanning from 2004 to 2020. The result suggests that both shared auditors and same signing auditors enhance audit quality, with the effect being stronger at the individual auditor level. Shared auditors facilitate alignment between M&A parties and reduce uncertainties, a role more prominently reflected in same signing auditors. These findings remain robust across different model specifications and adjustments.

Heterogeneity tests reveal that this effect is more pronounced in cross-industry, cross-province, larger acquirer, non-SOEs, and non-Big 4. First, industry differences. Cross-industry M&A often face significant challenges due to differences in business practices and accounting techniques, making information acquisition more difficult. Second, regional differences. Greater geographical distances make information exchange between companies more challenging, making external networks particularly advantageous for information sharing. Third, ownership. M&A decisions by SOEs are often influenced by government policy objectives. Auditors can act as communication channels to reduce barriers. Fourth, relative size. Larger companies typically have higher expectations for targets and tend to gather information through external networks. Lastly, audit firm size. Non-Big 4 audit firms, due to their relatively weaker independence, are often more inclined to follow client directives and facilitate information sharing between the parties involved.

From a theoretical perspective, by examining the roles of shared auditors and same signing auditors in different business, industry, and regional contexts, it further enhances the existing literature on the role of auditors in complex corporate transactions (Ai et al., 2020; Bedford et al., 2023; Y. Cai et al., 2016; Chircop et al., 2018; Dhaliwal et al., 2016; Sun et al., 2020). Secondly, the study reveals how shared auditors and same signing auditors enhance audit quality in M&A through knowledge spillover effects, especially in M&A involving larger acquirers and non-SOEs. This finding provides an important supplement to the theoretical model of information sharing and decision-making in M&A (Cao & Pham, 2021; Chahine et al., 2018; J. Z. Chen et al., 2020; Jiu et al., 2020; Tong et al., 2022). The knowledge-sharing mechanism across businesses and industries helps deepen the understanding of the auditor network effect in M&A. Lastly, this study further emphasizes the unique importance of shared auditors and same signing auditors in specific contexts, highlighting the strategic role of shared auditors in M&A, especially in cases requiring cross-regional and cross-industry coordination (Jiu et al., 2020; Tong et al., 2022). It also emphasizes the interaction between the role of auditors and acquirer size (or audit firm size). These findings offer new insights into the relationship between auditor independence and audit quality in auditing theory (J. Z. Chen et al., 2020; Dhaliwal et al., 2016), while also contributing to the theory on the relationship between policy-driven M&A decisions and audit quality (Gu et al., 2020).

From a practical perspective, the findings guide companies in selecting audit services for mergers, suggesting that shared auditors with industry expertise and regional networks improve information-sharing efficiency and decision-making quality. This study also highlights the proactive role of non-Big 4 audit firms in information sharing and knowledge spillovers due to their flexibility in meeting client needs, offering practical insights for small and medium-sized audit firms to strengthen competitiveness. Additionally, the findings provide empirical evidence for policymakers on the role of auditors as information bridges, aiding the optimization of M&A regulations and improving audit quality in the industry.

The following suggestions are derived from this study. Firstly, it may be beneficial to consider using the same audit firm or signing auditor as the acquirer to enhance audit quality, during M&A. Secondly, to effectively utilize information resources, priority may be given to using shared auditors in cross-industry and cross-regional M&A to maximize the benefits of information sharing. Thirdly, shared auditors could be prioritized when the acquirer is larger in scale, non-SOEs, or audited by a non-Big 4 firm. Additionally, the improvement in audit quality or information quality for the acquirer may trigger a series of chain reactions, benefiting the target and leading to a significant enhancement in overall efficiency. Lastly, the government should promote market-oriented M&A and foster the development of market intermediaries to support the healthy growth of the M&A market.

This paper has some limitations. First, the study focuses on China’s A-share market, with a limited sample size due to the scarcity of listed company data. This limits the generalizability of the findings to unlisted companies and other countries. Future research could include unlisted companies and cross-national comparisons to improve external validity. Second, the study assumes a common interest between the acquirer and target, but conflicts of interest are unexplored. Future research could examine shared auditors’ behavior in such cases. Third, while the effects of shared and same signing auditors were explored, the role of social relationship networks between audit firms remains unexamined. Future research could investigate how these networks and their characteristics affect M&A and audit quality.

Footnotes

Appendix

Variable Definitions.

| Variables | Definitions |

|---|---|

| Dependent variables | |

| AUDITFEE | Natural logarithm of total audit fee of the audit report. |

| |DA| | Absolute values of discretionary accruals from modified Jones model (1995). |

| Independent variables | |

| SHARE | Indicator variable takes the value of 1 if both sides of M&A are engaged in the same audit firm within the 2 years preceding the first announcement of the M&A; 0 otherwise. |

| SAMESIGN | Indicator variable takes the value of 1 if the acquirer and the target of M&A are engaged in the same audit firm and have the same signing auditors within the 2 years preceding the first announcement of the M&A; 0 otherwise. |

| Moderator variables | |

| SI | Indicator variable equals 1 if shared auditor = 1 and the common auditors are from related industries; 0 otherwise. |

| SP | Indicator variable equals 1 if shared auditor = 1 and the common auditors are from same province; 0 otherwise. |

| BIG4 | Indicator variable equals 1 if shared auditor = 1 and the common auditors are from the “Big 4”; 0 otherwise. |

| SOE | Indicator variable equals 1 if the acquirer is state-owned enterprises; 0 otherwise. |

| RS | Natural log of the ratio of the market value of target’s equity is divided by the acquirer’s equity. |

| Control variables | |

| SIZE | Natural log of total assets. |

| LEV | Total liabilities are divided by total assets of the target. |

| GROWTH | Current year operating income minus prior year operating income is divided by prior year operating income. |

| INVENTORY | The ratio of net inventory to total assets. |

| ROE | The ratio of the net income to the target’s equity. |

| ROA | The ratio of the net income to assets of the target. |

| BM | The book value of the target’s equity is divided by the market value of the target’s equity. |

| BIG | Indicator variable takes the value of 1 if the audit firm of the acquirer is from the Big 4; 0 otherwise. |

| NAVPS | Net asset value per share. The ratio of the net asset value to the number of outstanding shares. |

| LSR | Shareholding ratio of largest shareholder. |

| PAY | Indicator variable equals 1 if the acquirer uses stock as a method of payment; 0 otherwise. |

| Dummy variables | |

| Industry | Guidelines for Industry Classification of Listed Companies (2012). |

| Year | M&A took place from 2004 to 2020, with 16 years of dummy variables set. |

Note. All accounting variables are derived from data of the preceding year and the variables related to M&A are as of the acquisition announcement year. The source of observations is all from CSMAR.

Acknowledgements

Special thanks to the reviewers for valuable comments.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by the Scientific Research Program for Higher Education Institutions of Hebei Provincial Department of Education (Grant No. QN2025869).

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethical Approval

This research did not involve human or animal participants, and thus, ethical approval was not required.

Data Availability Statement

All data are publicly available from the sources identified in the article.