Abstract

This research examines how shared auditors and signing auditors influence the decision-making process in M&A. Using a comprehensive sample of Chinese A-share market M&A transactions from 2004 to 2020, we analyze how sharing the same audit firm or signing auditor influences the likelihood of completing an acquisition. The regression results reveal that firms with common auditors are more likely to achieve successful acquisitions. The effect is particularly pronounced for large acquirers, non-state-owned enterprises, cross-industry M&As, cross-province M&As, and those involving non-Big 4 audit firms. These findings are robust to various model specifications and adjustments. This paper extends the literature by demonstrating the dual-level (firm-level and individual-level) role of auditors as information intermediaries in M&A transactions. The results suggest that organizations and audit teams should consider the potential benefits of shared auditors in enhancing the quality and success of M&A deals.

Introduction

Companies increasingly adopt Mergers and Acquisitions (M&A) as a strategic approach to resource allocation, expansion, and risk distribution. The acquirer needs to conduct due diligence to identify any material adverse events that could negatively impact the acquisition (Wangerin, 2019). Failure in any part of the process can lead to a failed M&A (Renneboog & Vansteenkiste, 2019). However, M&A transactions are inherently complex and challenging, with information asymmetry often preventing acquirers from fully assessing the resources and capabilities of potential targets (Capron & Shen, 2007). In particular, risks arising from the target company can significantly impact the success of the acquisition (Bruyland & de Maeseneire, 2016; Dhaliwal et al., 2016). As an external organization, an audit firm provides an independent evaluation of a company’s financial situation, thus reducing information asymmetry in M&A.

The term “shared auditor” refers to the situation where two companies employ the same audit firm (T. Chen et al., 2012). Acquirers often turn to audit firms for information on potential targets due to time and cost constraints (Y. Cai et al., 2016; T. Chen et al., 2012; Dhaliwal et al., 2016). Although substantial research has focused on the role of shared auditors at the audit firm level, it is equally important to explore the unique contributions of individual auditors, particularly in contexts where high information demand exists, such as cross-industry or cross-regional acquisitions, or when large firms acquire smaller ones.

Information asymmetry in M&A often leads to a strategic game between the bidder and the target. Committee (2001) contributed significantly to the understanding of this issue by demonstrating that buyers and sellers possess different levels of information, with sellers typically having more detailed knowledge about the product than buyers. Hansen (1987) pioneered the idea that a target company will only accept an acquisition offer if the offer price exceeds its actual value. Information asymmetry can also impact various facets of the M&A process, including the method of payment, valuation discrepancies, and bargaining power (Luypaert & Van Caneghem, 2014; Mantecon, 2008; Raman et al., 2013). The role of social networks in facilitating information sharing has gained significant attention, with shared auditors playing a key role in reducing uncertainty and information asymmetry during the M&A process (Y. Cai et al., 2016).

Existing literature underscores the critical role that shared auditors play in transmitting information across various networks, including supply chains (C. Cai et al., 2019; J. Chen et al., 2022; Hu et al., 2022, 2023), in M&A (Y. Cai et al., 2016; Dhaliwal et al., 2016), in competitive relationships (Aobdia, Lin, & Petacchi, 2015), in banks and borrowers (Aguir et al., 2022; Francis & Wang, 2021; Ton, 2023), and in auditing networks (Bills et al., 2020; Cao & Pham, 2021; Jiu et al., 2020). Sun et al. (2020) found that the positive outcomes of information sharing outweigh the negative effects of “lowballing” as evidenced by improved audit quality and increased audit costs. Aobdia (2015) introduced the perspective of information spillover, suggesting that when companies share auditors with their competitors, there could be a risk of information leakage.

Audit firms, as external entities, play an essential role in enhancing the accuracy and effectiveness of corporate decision-making by facilitating information sharing and reducing information asymmetry. Despite M&A being one of the primary ways for companies to expand their business, they also pose significant risks to the acquirer. Previous research highlights the importance of audit intermediaries in the M&A process. Typically, the acquirer conducts due diligence to identify any potential issues that could negatively impact the transaction. However, due to the high level of information opacity, this process can often be costly and challenging. Research on shared auditors suggests that jointly hiring an audit firm can facilitate acquisitions, reduce transaction premiums, provide valuable information, and lead to positive market returns (Bedford et al., 2023; Y. Cai et al., 2016; Chahine et al., 2018; Chircop et al., 2018; Dhaliwal et al., 2016).

There has been growing scholarly interest in the individual roles of signing auditors in recent years. Empirical research has demonstrated that signing auditors, through their distinctive professional judgments and audit methodologies, significantly influence the comparability of corporate financial statements (J. Z. Chen et al., 2020; Jiu et al., 2020). Within the context of M&A, shared signing auditors can substantially mitigate information asymmetry, thereby enhancing the quality and success rate of transactions, particularly in environments characterized by high uncertainty (C. Cai et al., 2019; Dhaliwal et al., 2016). Moreover, Bedford et al. (2023) provide evidence that shared audit partners not only increase the likelihood of favorable acquisitions but are also associated with lower acquisition premiums and higher acquirer returns.

In the auditing process, signing auditors frequently serve as information intermediaries through confidential exchanges with senior management (Hassanzadeh Mohassel et al., 2024). Such interactions enable auditors to acquire critical financial and operational data about clients, which is often controlled by audit partners (Ferguson et al., 2019). The information exchanged within these covert networks enhances transaction transparency and contributes to improved audit quality (Causholli et al., 2021; Sun et al., 2020). The expertise of signing auditors is intrinsically linked to their individual knowledge and experience (Chi & Chin, 2011). Research also indicates that variations in audit quality among auditors are influenced by factors such as educational background, experience with large firms, professional rank, and political affiliations (Gul et al., 2013). For example, signing auditors affiliated with the Communist Party have been shown to reduce earnings management, with this effect being more pronounced in smaller audit firms (Hou et al., 2023).

In the context of M&A, most studies have focused on the role of shared audit firms, with less attention given to the impact of individual auditors’ social networks on target selection (Bedford et al., 2023; Y. Cai et al., 2016). This study contributes to the literature by examining the influence of both shared auditors and shared signing auditors on M&A decision-making. Employing the same audit firm and auditors is a cost-effective strategy to enhance the due diligence process and improve M&A outcomes. These findings align with earlier research that identifies shared audit partners as pivotal channels for information dissemination, extending beyond the firm or office level (Bills et al., 2020; J. Z. Chen et al., 2020). Through direct interactions within the firm, shared auditors are more likely to accumulate and effectively transmit pertinent knowledge to both acquirers and target companies, thereby refining the audit process for the newly merged entity.

This research investigates the influence of shared auditors, considering both firm-level and individual auditor-level perspectives, on the selection of acquisition targets within the Chinese market. We propose that the impact will be more significant when both the audit firm and the signing auditor are shared. Additionally, we conduct a heterogeneity analysis to further understand the characteristics of these effects. Given that information asymmetry conditions necessitate the role of external information intermediaries, we anticipate that the influence of shared auditors will be particularly pronounced in situations where there is a high demand for information, such as when the acquirer and target belong to different regions, or when there is a considerable size difference between the firms.

The disclosure of auditor information in certain countries provides a unique context for exploring the role of individual auditors within the audit market. Consequently, this study seeks to bridge the existing research gap by examining the varying impacts of shared auditors at both the firm and individual auditor levels on M&A target selection. Using a comprehensive sample of 1,083 Chinese acquisitions from 2004 to 2020, where 19.21% involve the same audit firm and 5.36% share the same signing auditor, we analyze how these factors influence the likelihood of completing an acquisition. Through a matched sample methodology (Bodnaruk et al., 2009; Capron & Shen, 2007), the M&A samples are paired 1:1. For each actual target, a control group is set, consisting of companies with similar industry classification codes and similar size (total asset size within ±10%). The paired sample of 2,025 is used to test whether an acquisition occurs between the potential acquirer and the target company. If an acquisition occurs, the variable equals 1; otherwise, it equals 0.

The probit regression results reveal that firms sharing the same audit firm or signing auditor are more likely to achieve successful acquisitions. Shared auditors are more effective at aligning clients involved in M&A transactions and minimizing uncertainties that could otherwise disrupt the process. The analysis shows that the influence is mainly attributed to shared signing auditors, which aligns with previous studies. These results remain consistent across different model specifications and adjustments.

To further understand how shared auditors and same signing auditors affect different scenarios, we conduct heterogeneity tests based on (1) industry differences, (2) region differences, (3) ownership, (4) relative size, and (5) audit firm size.

First, industry differences. Cross-industry M&A is often challenging due to differences in business practices and accounting techniques, making information access more difficult. Consistent with expectations, the findings indicate that shared auditors and same signing auditors play an important role in facilitating M&A, especially in cross-industry transactions. Second, regional differences. Greater geographical separation makes it more challenging for businesses to exchange information, so sharing information through an external network becomes advantageous. The results suggest a stronger impact of shared auditors across regions. Third, Ownership. In China, state-owned enterprises (SOEs) often make M&A decisions influenced by government policy goals rather than solely maximizing corporate value (Gu et al., 2020). In such cases, shared auditors can serve as communication channels to reduce barriers. Our findings confirm this, showing a significant positive moderating effect when the acquirer is a non-state-owned enterprise. Fourth, relative size. Larger firms tend to have higher requirements for targets in M&A and prefer to gather information through external networks to obtain more accurate insights. The findings suggest that the effects of both the audit firm and the audit team are more significant when the acquiring company is larger. Finally, audit firm size. Non-Big 4 auditors, being less independent, are often more inclined to follow client directions and facilitate information sharing between both sides of the transaction. The comparison shows that the moderating effect is stronger when a non-Big 4 audit firm is involved.

This research contributes to the existing literature in several ways. Firstly, it extends the study of “information sharing” (Capron & Shen, 2007; Chahine et al., 2018; Knechel et al., 2015; Marquardt & Zur, 2015) by exploring how these mechanisms operate not only through “interlocking directors” and “shared advisors” but also at the auditor level in M&A transactions (Y. Cai et al., 2016; Ishii & Xuan, 2014; Rousseau & Stroup, 2015; Stuart & Yim, 2010). This enriches the academic literature on the influence of external information intermediaries in capital markets.

Secondly, our study complements existing research by extending the investigation into the impact of shared auditors, both at the firm and individual auditor level (Kachelmeier, 2010; Mala & Chand, 2015). While studies at the auditor level are limited due to data availability primarily in countries like China, Taiwan, and Australia, our research offers fresh perspectives by providing new data and insights through a survey focused on individual auditors. This work fills a gap in the literature concerning the impact of individual auditors (Al-Dhamari & Chandren, 2018; Burke et al., 2020; Carey & Simnett, 2006; C. Chen et al., 2008; S. Chen et al., 2010; Chi & Chin, 2011; Ittonen & Peni, 2012). By conducting this survey, we offer new perspectives and valuable data on information sharing in emerging markets, particularly within the context of M&A (J. Z. Chen et al., 2020; Jiu et al., 2020; Nelson et al., 2005).

Lastly, this study explores the role of shared auditors under different conditions, enhancing our understanding of how external information intermediaries, such as audit social networks, influence market transactions and information transmission mechanisms. The findings provide valuable insights for policymakers and investors.

This paper is structured as follows: Section 2 outlines the research hypotheses. Section 3 discusses the research methodology, Section 4 presents the estimation results, and Section 5 concludes with a summary.

Theoretical Framework and Hypotheses Development

Shared Auditors and Target Selection

Based on signaling theory (Akerlof, 1970), information asymmetry in M&A processes prompts acquirers to rely on publicly available quality signals to evaluate target companies, such as the reputation of venture capitalists or underwriters (Ragozzino & Blevins, 2016; Ragozzino & Reuer, 2007) and investor assessments (Chatterjee et al., 2012). Additionally, similar ownership structures can facilitate mutual understanding between companies, thereby increasing the probability of a merger (Bettinazzi et al., 2020). While information gathering and analysis are critical steps in the M&A process (Trichterborn et al., 2016), existing research has rarely explored the role of external institutions in information transmission. The opacity of information increases transaction costs, especially during information gathering and due diligence (Bruner, 2004). Information asymmetry exacerbates this issue, making it more challenging to assess the resources and capabilities of target companies (Capron & Shen, 2007). Research suggests that acquirers, by obtaining more information about target companies, can gain greater confidence in their capabilities, which in turn makes them more willing to increase their offers (Marquardt & Zur, 2015).

To address information asymmetry, acquirers often choose to work with companies they have existing relationships with, such as alliance partners (Porrini, 2004; Zaheer et al., 2010), nearby companies (Chakrabarti & Mitchell, 2013), or companies connected through shared customers, auditors, managers, or directors (Y. Cai et al., 2016; Dhaliwal et al., 2016; Ishii & Xuan, 2014). Recent research indicates that when two companies engage the same audit firm, this arrangement can lead to an “information sharing” effect (T. Chen et al., 2012). Existing literature demonstrates that shared auditors contribute to various aspects of M&A by enhancing audit quality and efficiency through facilitated knowledge exchange (Causholli et al., 2021; Duh et al., 2020). This knowledge sharing primarily stems from the interaction and relationships between auditors (Hassanzadeh Mohassel et al., 2024). By enhancing the professional knowledge sharing within the audit team, shared auditors are better positioned to identify and address risks of material misstatements in financial reports. The communication and knowledge transfer among shared auditors enable acquirers to better ensure the quality of M&A transactions (Y. Cai et al., 2016). Moreover, companies that hire M&A expert auditors are more likely to avoid misstatements and achieve better audit outcomes in M&A (Gal-Or et al., 2022).

In China’s auditing system, the Ministry of Finance requires auditors to sign audit reports (MOF, 1995a). This requirement has been widely studied and proven to significantly impact audit outcomes (S. Chen et al., 2010; Gul et al., 2013; He et al., 2017). However, information asymmetry not only affects the completion of M&A transactions but can also impact the realization of expected value (Chahine et al., 2018). Before finalizing a merger or acquisition, acquirers typically evaluate multiple potential targets. Due to constraints of time and cost, acquirers may directly inquire with audit firms about suitable acquisition targets, thereby gaining additional relevant information (Y. Cai et al., 2016). Furthermore, companies that share auditors often exhibit greater similarity in their financial reporting, which helps reduce information asymmetry (Knechel et al., 2015). The presence of shared auditors can help target companies in better understanding the true intentions of the acquirer, thereby increasing the likelihood of accepting a merger proposal (Bedford et al., 2023; Dhaliwal et al., 2016).

Sharing one audit firm or signing auditor enhances the transparency and credibility of exchanged information, with the auditor’s reliability, objectivity, and independence playing a crucial role. When auditors maintain independence and provide objective opinions, acquirers are better positioned to accurately evaluate the financial condition of the target, thereby mitigating the risks associated with information asymmetry. Although companies may sometimes prefer to choose different audit firms to ensure diversity and independent verification of information, sharing the same audit firm or signing auditor can still improve the reliability and transparency of the information, increasing the likelihood that the target will be chosen as an acquisition target.

Thus, leveraging a shared auditor is expected to enhance communication between both parties in an M&A, leading to more informed target selection. The involvement of a shared auditor in the M&A process not only facilitates effective communication but also significantly enhances the attractiveness of the target company as a potential acquisition. The consistency and transparency offered by a shared auditor allow the acquirer to gain a clearer understanding of the target company’s financial standing, which directly reduces uncertainty and risk during due diligence. Additionally, a shared auditor ensures the accuracy and reliability of financial data, providing the acquirer with a solid foundation for confident investment decisions. Therefore, a target company that shares the same auditor with the acquirer is likely to experience a significant increase in its competitiveness, making it more attractive option for the acquirer’s preferred target. In summary, the presence of a shared auditor creates a more trustworthy and efficient environment for both parties in an M&A, which significantly enhances the target selection process. In this context, companies that employ the same audit firm as the acquirer are more likely to be selected as the final acquisition target. Given the above considerations, our hypothesis is that:

Same Signing Auditors and Target Selection

Audit firms and signing auditors possess a certain degree of flexibility in the audit process. As knowledge-intensive service providers, audit firms benefit from the social information networks formed by individual auditors, which facilitate information sharing. This requires a robust firm-level framework as well as increased reliance on professional judgment at the individual level (Hambrick, 2007). Auditors are expected to apply their best professional judgment throughout the audit process (Mala & Chand, 2015). The experience of signing auditors influences every stage of the audit process, from accepting the engagement to planning, executing, and determining the type of audit report (Borkus et al., 2022; Gul et al., 2013; Hassanzadeh Mohassel et al., 2024; Jiu et al., 2020; Kusumawati & Syamsuddin, 2018).

Signing auditors act as information intermediaries during the audit process. They frequently engage in private discussions with senior management (Hassanzadeh Mohassel et al., 2024). If a client is considering buying or selling assets, the audit firm’s client network might become aware of this information. Therefore, within the invisible network created by auditors, opportunities for information sharing are greater (Causholli et al., 2021; Sun et al., 2020). Research also shows that individual auditors play a significant role in the comparability of a client’s earnings (J. Z. Chen et al., 2020).

According to Rule 3211 of the Public Company Accounting Oversight Board (PCAOB), as of January 31, 2017, registered public audit firms must disclose the names of auditors on each audit report. This requirement has been extensively studied and proven that signing auditors significantly affect audit outcomes (S. Chen et al., 2010; Gul et al., 2013; He et al., 2017). Additionally, Chinese regulations require that each audit report includes the signatures of two auditors: a junior (engagement) auditor and a senior (review) auditor (MOF, 1995a, 1995b). These two auditors function like business partners, playing a vital role in establishing client trust and confidence in financial reports (Gul et al., 2013). If an audit failure occurs, the individual signing auditors are subject to sanctions (S. Chen et al., 2010; Gul et al., 2013). Furthermore, Chinese accounting standards are converging with International Financial Reporting Standards (IFRS). Under the principles-based system, regulatory bodies have set broad accounting guidelines, granting auditors greater discretion in applying these principles (Kothari et al., 2010). Globally, only a limited number of countries require auditors’ names to be disclosed. Comparative studies of signing auditor names provide a research context, including countries such as Australia (Carey & Simnett, 2006), Taiwan (C. Chen et al., 2008; Chi & Chin, 2011), China (S. Chen et al., 2010), Finland and Sweden (Ittonen & Peni, 2012), and Malaysia (Al-Dhamari & Chandren, 2018).

Several studies have shown that shared signing auditors significantly impact company performance. J. Z. Chen et al. (2020) found that companies sharing the same signing auditor exhibit higher earnings comparability compared to those using different auditors. This study highlights that individual auditors demonstrate unique audit styles in applying accounting standards and professional judgment, maintaining consistency across different audit tasks. Similarly, Jiu et al. (2020) further validated this conclusion, noting that companies sharing signing auditors have incremental advantages in financial statement comparability, especially in environments where auditor identities are disclosed, such as China. These studies collectively emphasize the influence of individual auditors’ styles on the comparability of financial reports, offering practical insights for market participants and policymakers.

In the context of selecting target companies during M&A, research has predominantly focused on the role of shared audit firms. For instance, C. Cai et al. (2019) found that M&A transactions involving shared auditors yield significantly higher announcement returns compared to those without shared auditors, especially in scenarios with high pre-acquisition uncertainty. This suggests that shared auditors play a key role in reducing information asymmetry, thereby facilitating better capital allocation and enhancing the quality of M&A transactions. Dhaliwal et al. (2016) further support this perspective, noting that shared auditors are linked to higher transaction completion rates and improved event returns for acquirers. Additionally, Bedford et al. (2023) observed that shared audit partners increase the likelihood of friendly acquisitions, which are associated with lower acquisition premiums and higher cumulative abnormal returns for acquirers in Australian M&A cases.

Prior research has established that shared signing auditors enhance the comparability of financial statements and improve M&A transaction quality by mitigating information asymmetry. However, most studies have focused on the broader impact of shared auditors on M&A outcomes, with less emphasis on the specific role of shared signing auditors in the target selection process. Previous research has demonstrated the crucial role of shared signing auditors in facilitating information transmission. In M&A, the influence of shared signing auditors extends beyond the audit firm to individual auditors. In the Chinese M&A market, where signing auditor data is publicly available, sharing the same signing auditor allows acquirers to gain clearer insights into target company information, simplifying the selection of appropriate acquisition targets. Consequently, this study hypothesizes that companies sharing the same signing auditor with the acquirer are more likely to be selected as the final target due to the provision of clearer and more consistent financial information.

Given the above considerations, our hypothesis is as follows:

Sample Selection, Measures, and Research Design

Sample Selection

This study conducts a comprehensive examination of M&A involving China A-share listed companies from 2004 to 2020. Financial institutions and failed transactions are excluded, resulting in a final sample of 1083 M&A events where both parties are listed companies. To mitigate the influence of extreme outliers, continuous variables are winsorized at the 1% and 99% levels. Financial data, as well as information about audit firms and auditors, are obtained from CSMAR, with any missing data manually retrieved and added. Details of the sample construction process are outlined in Table 1.

Sample Selection.

Note. The source of observation is all from CSMAR.

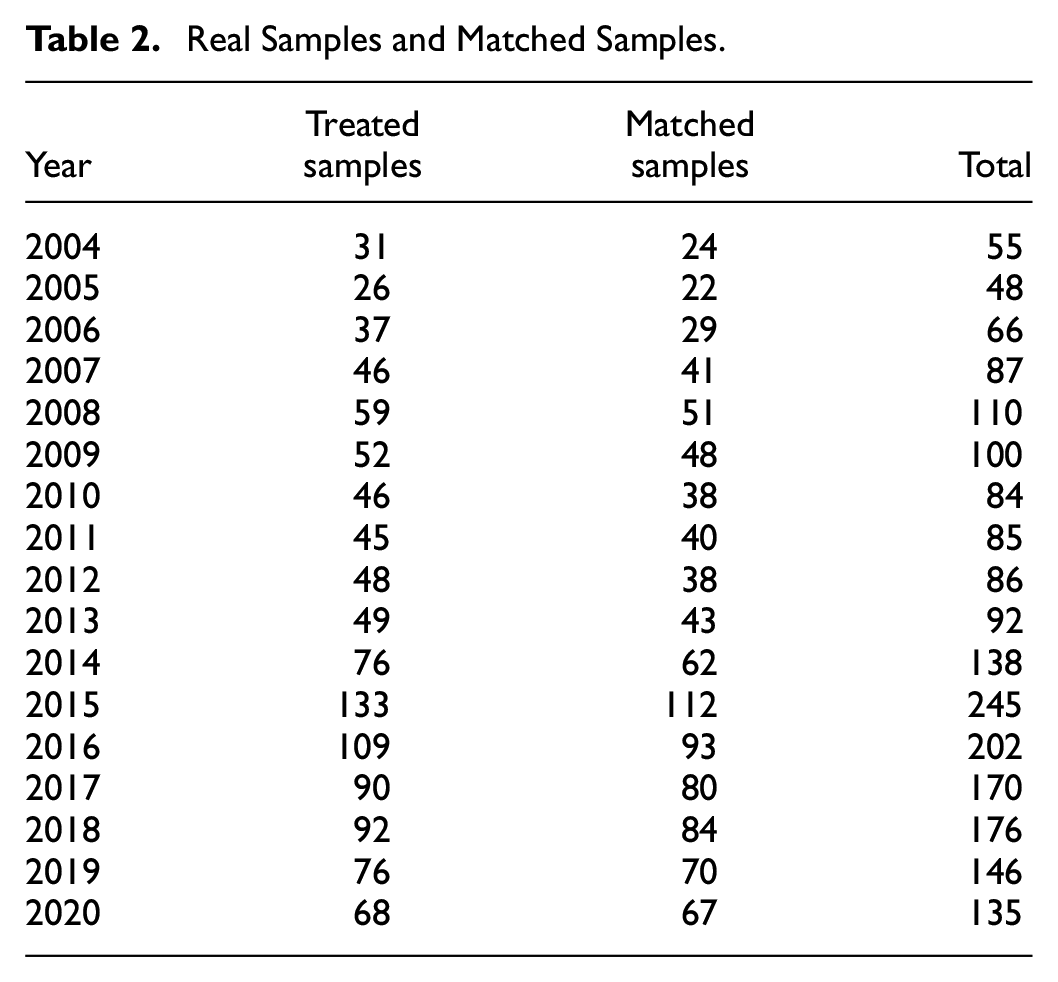

We employed the matched sample methodology (Bodnaruk et al., 2009; Capron & Shen, 2007) to study the likelihood of two companies participating in M&A. For each actual target company, we identified potential targets as those within the same industry classification code, similar in size (within 10% above and below total asset size, with a 1:1 ratio), to create a control group. Ultimately, 942 matched samples and 2,025 total samples are obtained. Data processing and regression analysis were conducted using STATA 17.0 statistical software. Table 2 shows the specific information of matched samples and total samples.

Real Samples and Matched Samples.

Variable Definitions

Dependent Variable

Real or Potential Targets Firm (TS)

TS is defined as whether a company is the real target or not. Firms that are the actual target are assigned a value of 1, and 0 otherwise.

Independent Variables

Same Audit Firms (Samefirm)

A binary variable identifies whether the acquirer and target share the same audit firm in the fiscal year immediately preceding the M&A announcement. It takes a value of 1 if both companies use the same audit firm, and 0 otherwise (Y. Cai et al., 2016).

Same Signing Auditors (Sameauditor)

A binary variable equals 1 if the acquirer and the target share one or two signing auditors in the latest fiscal year before the M&A announcement date, and 0 otherwise.

Moderator Variables

Industry Differences (SI)

The variable equals 1 when Shared auditor = 1 and the common auditors are from related industries; 0 otherwise (Faccio & Masulis, 2005; Megginson et al., 2004).

Region Differences (SP)

The variable equals 1 when Shared auditor = 1 and the common auditors are from the same province; 0 otherwise (Portes & Rey, 2005).

Firm Nature (SOE)

The variable equals 1 when the acquirer is a state-owned enterprise; 0 otherwise.

Relative Size (RS)

The ratio of the target’s market value of equity to that of the acquirer’s equity (Hayward & Hambrick, 1997; Lee & Kocher, 2011).

Audit Firm size (BIG4)

The variable equals 1 when the audit firms are from “big 4”; 0 otherwise (Xie et al., 2013).

Control Variables

This study considers for two main factors that may impact M&A decisions, target characteristics and shareholding structure (Y. Cai et al., 2016). The data are selected from the year before the first M&A announcement.

Target Characteristics

Controls represent the characteristics that are associated with the same audit firms and signing auditors. It also accounts for the natural logarithm of the target’s assets (SIZE) (Y. Cai et al., 2016; Dhaliwal et al., 2016). This study incorporates a control variable for leverage, measured as the ratio of total liabilities to total assets (LEV) (Capron & Shen, 2007) and a growth metric defined as the ratio of current sales to those from the same period in the previous year (GROWTH) (Ashbaugh-Skaife et al., 2008; Gaur et al., 2013). Additionally, operating cash flow (OCF) as a percentage of total assets from the prior year is included. The model also controls for the shareholding ratios of the largest shareholders (LSR). We also control whether the acquisition is paid with stock (PAY) because managers may have different incentives to make stock-based versus cash-based acquisitions (Erickson & Wang, 1999). In terms of profitability, this paper uses return on equity (ROE) to measure profitability (Capron & Shen, 2007). Asset quality is a function of M&A cost, which ultimately determines the likelihood of a company becoming an acquisition target. To assess asset quality, we incorporate two financial metrics: the book to market ratio (BM) and the price to earnings ratio (PER) (Y. Cai et al., 2016). The governance structure of a company directly affects the ease of M&A transactions (Capron & Shen, 2007). It is examined through the board size (SCALE) and the independent directors’ proportion (IND). In particular, SCALE reflects the number of board members, while IND represents the percentage of independent directors. Stock volatility (STD) indicates the uncertainty of a company’s prospects. It measures how much a company’s stock price fluctuates over a given period. Higher stock volatility indicates a higher level of risk and uncertainty, which can decrease the likelihood of the company being targeted for a merger or acquisition. The standard deviation of the target companies’ monthly stock returns is used as a measure of stock volatility (Kang & Kim, 2008). HHI is also employed to assess the competitive intensity of the product market. Also, we control for industrial effect, and year effect. The variables and their definitions can be found in Appendix A.

Research Design

Based on the existing related literature (Dhaliwal et al., 2016), this study adopts the target selection as the dependent variable, and the same audit firm and the same signing auditor as the independent variables. The control variables are determined based on existing research findings, and a Probit regression model (1) is established.

The impact of Samefirm and Sameauditor is explored through the coefficient α1(γ1). If α1(γ1) is significantly positive (negative), it indicates a positive (negative) effect on the target selection.

In model (1), TS is the target selection, Samefirm is the independent variable, and α0 is the intercept term.

In model (2), TS is the target selection, Sameauditor is the independent variable, and γ0 is the intercept term.

Empirical Results

Descriptive Statistics

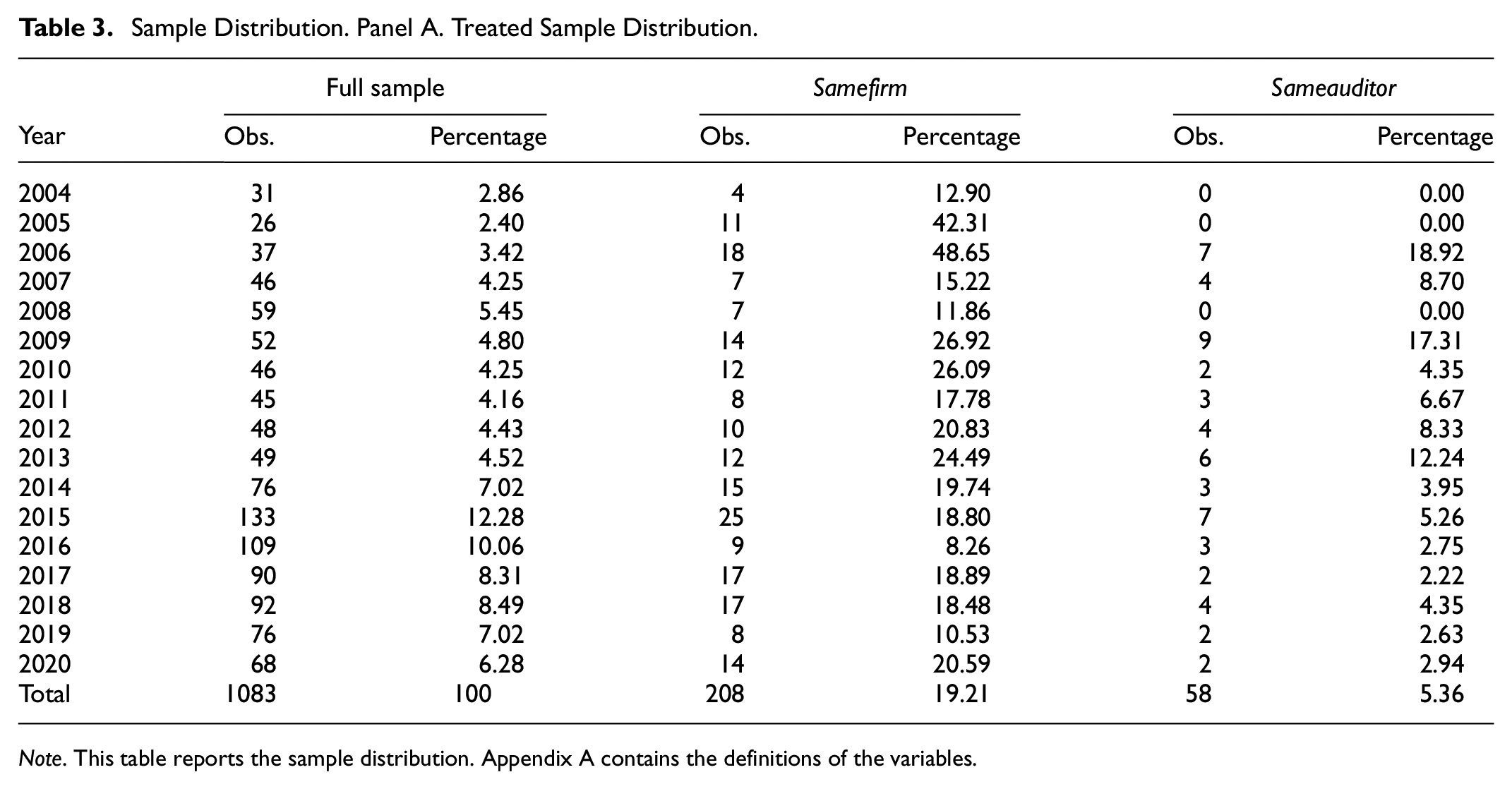

In Table 3, Panel A, it can be observed that the number of M&A increased steadily from 2004 to 2020, with a peak in 2015. This growth can be attributed to the liberalization of policy restrictions in 2014 and the introduction of various regulatory guidelines aimed at reducing the costs associated with M&A activities. Despite a slight dip in the number of M&A events in 2017, the overall trend remained positive. The sample size includes 1,083 deals and it is estimated that the sample of the same audit firm represents 19.21% of the total M&A events and the same signing auditor account for 5.36%. As indicated by this percentage, the phenomenon of shared audit firms is fairly common.

Sample Distribution. Panel A. Treated Sample Distribution.

Note. This table reports the sample distribution. Appendix A contains the definitions of the variables.

Table 4, Panel B presents the treated and matched samples. Among the 2025 total samples, 290 (14.32%) share the same audit firm, while 78 (3.85%) share the same signing auditor. The proportions of both shared audit firms and signing auditors are higher in the actual sample than in the matched sample. This suggests that having the same audit firm or signing auditor may somewhat increase the likelihood of an M&A happening.

Sample Distribution. Panel B. Full Sample Distribution.

Note. The distribution of matched and treated samples is shown in Table 1, Panel B. Appendix A contains the definitions of the variables.

Table 5 provides the descriptive statistics analysis. The analysis reveals that the average target selection (TS) value is 0.535, suggesting that there was a 53.5% likelihood of a company being chosen as an M&A target. The proportion of Samefirm is 14.3% of the whole sample, whereas Sameauditor is 3.5%. Based on the key control variables, it can be observed that the acquirer tends to prefer companies with higher growth rates when selecting targets, as the mean value of growth rate (Growth) is 34.8%, surpassing the median. Additionally, the mean value of the target’s price-earnings ratio (PER) is 58.708, compared to a median of 24.758, indicating that target companies are generally overvalued, which implies a higher M&A risk. Regarding corporate governance, the mean levels of independent directors (IND) and dual positions (DUAL) are higher than the median, implying that the acquirer is more likely to select companies with better corporate governance as targets. This is a positive sign as better corporate governance can lead to more efficient decision-making and better long-term performance. In terms of product market competition (HHI), the mean is higher, indicating that the target’s product market competition intensity is higher. This suggests that the acquirer prefers to target firms with high market competition intensity, which could indicate a desire to gain a stronger foothold in a competitive market. Overall, these key control variables provide insights into the acquirer’s preferences and strategies when selecting merger targets.

Descriptive Statistics.

Note. The full sample descriptive statistics are presented in this table. Appendix A contains the definitions of the variables.

Table 6 displays the correlation matrix. The correlation coefficient between target selection (TS) and shared auditors (Samefirm) is .1495 (p < .01), reflecting a significant positive association between shared auditors and target selection, supporting Hypothesis 1. Similarly, the correlation coefficient between target selection (TS) and same signing auditors (Sameauditor) is .1078 (p < .01), suggesting a significant positive link between same signing auditors and M&A target selection, supporting Hypothesis 2.

Correlation Matrix.

Note. This table reports the correlation matrix. *, **, *** indicate p < .1, p < .05, p < .01, respectively. The variables are defined in Appendix A.

The target’s firm size (SIZE) and sales growth rate (GROWTH) are both significantly and negatively correlated with target selection (TS) (coeff. = −.0427, p < .01; coeff. = −.0553, p < .01, respectively). Moreover, OCF, ROE, LSR, BM, SCALE, and IND all exhibit significant negative correlations with M&A target selection (TS), indicating that the target frequently has average assets and a more average sales growth rate and profitability. The data supports the observation that M&A tends to “merge small with large.” The target’s leverage (LEV) is also significantly negatively correlated with target selection (TS) (coeff. = −.0420, p < .01), suggesting that bidders prefer targets with low debt levels. Dual is significantly and negatively correlated with M&A target selection (TS), indicating that the bidder is more likely to select targets with a better corporate governance environment. The correlation coefficient between net profit (LOSS) and M&A target selection (TS) is .0558 (p < .05), indicating that acquirers prefer to select profitable companies as targets.

In conclusion, M&A transactions often require companies to “swallow the huge with the tiny” to overcome internal obstacles and advance independently. The correlation coefficients of the remaining variables are all below .3.

Multivariate Tests

Table 7 presents the Probit regression results. The regression coefficient for shared auditors (Samefirm) and target selection (TS) is 0.4845 (p < .01), indicating a significant positive impact of shared auditors on target selection. This finding supports Hypothesis 1. Moreover, the regression coefficient for same signing auditors (Sameauditor) and target selection (TS) is 0.7447 (p < .01), demonstrating a significant positive impact of same signing auditors on target selection. This result supports Hypothesis 2, indicating that same signing auditors can further increase the likelihood of a firm being selected as a target, in addition to the beneficial effects of shared auditors on target selection at the firm level.

Estimates of SHARE and SAMESIGN on TS.

Note. The table presents the results from the probit regression analysis, which investigates the effects of having the same audit firm (Samefirm) and signing auditors (Sameauditor) on target selection (TS). For each target, we define the pool of potential target firms as those of similar size (within 10% of market capitalization) in the same standard industry classification. Columns (1) presents the findings for Hypothesis 1, while Column (2) displays the results for Hypothesis 2. The results are presented with and without controlling for year and industry variables. Z-statistics are used to indicate the level of significance, with *** denoting p < .01 and * denoting p < .1. Definitions of the variables used in this analysis can be found in Appendix A.

Heterogeneity Tests

We attempt to condense five factors from the literature that may have a moderate influence.

Industry Differences

Mergers within the same industry are facilitated by stronger business ties, homogeneous market environments, and shared information technology and credit policies, resulting in faster information flow and lower communication costs (Betton et al., 2009). Auditors with industry expertise make more accurate audit decisions, which improves customers’ financial reporting quality (Dunn et al., 2000; Solomon et al., 1999). Furthermore, acquirers are more inclined to engage auditors with industry-specific expertise when acquiring companies within the same industry, as managerial ability tends to have a more significant positive impact on long-term performance in such scenarios (Cui & Chi-Moon Leung, 2020; Dhaliwal et al., 2016).

Cross-industry M&A, on the other hand, can be challenging in terms of information access. However, external audits can be instrumental in addressing information asymmetry (Luypaert & Van Caneghem, 2014). This study investigates the influence of shared auditors and same signing auditors on target selection in M&A, dividing the sample into same-industry and cross-industry sub-groups. The regression results presented in Table 8, Panel A, demonstrate that both shared auditors and same signing auditors have a significant positive moderating effect on target selection in cross-industry M&A (Coeff. = .1971, p < .01; Coeff. = .4354, p < .01). This indicates that auditors with industry expertise have a more pronounced positive impact on target selection in cross-industry transactions, likely due to the substantial differences in business practices and accounting methods across industries. Overall, these findings highlight the important role that shared auditors and same signing auditors play in facilitating M&A, particularly in cross-industry deals.

Heterogeneity Tests. Panel A. The Effect of Industry Differences.

Note. The industry heterogeneity test is provided in Table 8, Panel A. Z-statistics: ***p < .01, *p < .1. The variables are defined in Appendix A.

Region Differences

Geographical proximity facilitates information exchange between acquirers and targets about each other’s operational circumstances and future development (Ciobanu, 2016; Croci et al., 2024; Z. Jin et al., 2021; Kengelbach et al., 2010). There is less information asymmetry when the acquirer and potential target are close by and in the same region (Z. Jin et al., 2021; Li et al., 2022). Firms tend to choose local firms due to their close proximity. The supply chain often opts to engage a single audit firm branch office to oversee the company when the supplier and client are situated within the same province or municipality.

When the acquirer and the potential target are in different industries or regions, access to information becomes more limited, forcing the acquirer to incur high consulting and search fees while also facing the risk of being overcharged (Bathelt & Henn, 2021; Bick et al., 2017; Li et al., 2022; Reddy & Fabian, 2020). In order to find potential M&A targets, the acquirer will rely more on external relationships. Meanwhile, greater separation makes it more challenging for the two businesses to exchange information. It would be advantageous to share information via an outside information network.

In this subsection, we divided the entire sample into two subgroups based on whether the two firms are located in the same region. Table 9, Panel B displays the regression results for the moderating effects on Samefirm and Sameauditor, respectively. For the relationship between the target (TS) and the shared auditor (Samefirm), when the two firms are located in different regions (NON-SP, Coeff. = .1395, p < .01). In this scenario, the role of the shared auditor becomes more pronounced. This demonstrates how the acquirer’s access to information becomes increasingly constrained as geographic distance increases. Additionally, there is a problem with operational and cultural integration, which makes the acquisition more challenging and highlights the beneficial role of shared auditors. For the relationship between the target (TS) and the Same signing auditors (Sameauditor), when the two parties are located in different regions (NON-SP, Coeff. = .3185, p < .05), they also show a significant positive moderating effect. It appears that there is a clear tendency to have a stronger impact across regions. The advantages of auditors working in different jurisdictions are increasingly obvious.

Heterogeneity Tests. Panel B. The Effect of the Region Differences.

Note. Region heterogeneity test is provided in Table 9, Panel B. Z-statistics: ***p < .01, **p < .05. The variables are defined in Appendix A.

Ownership

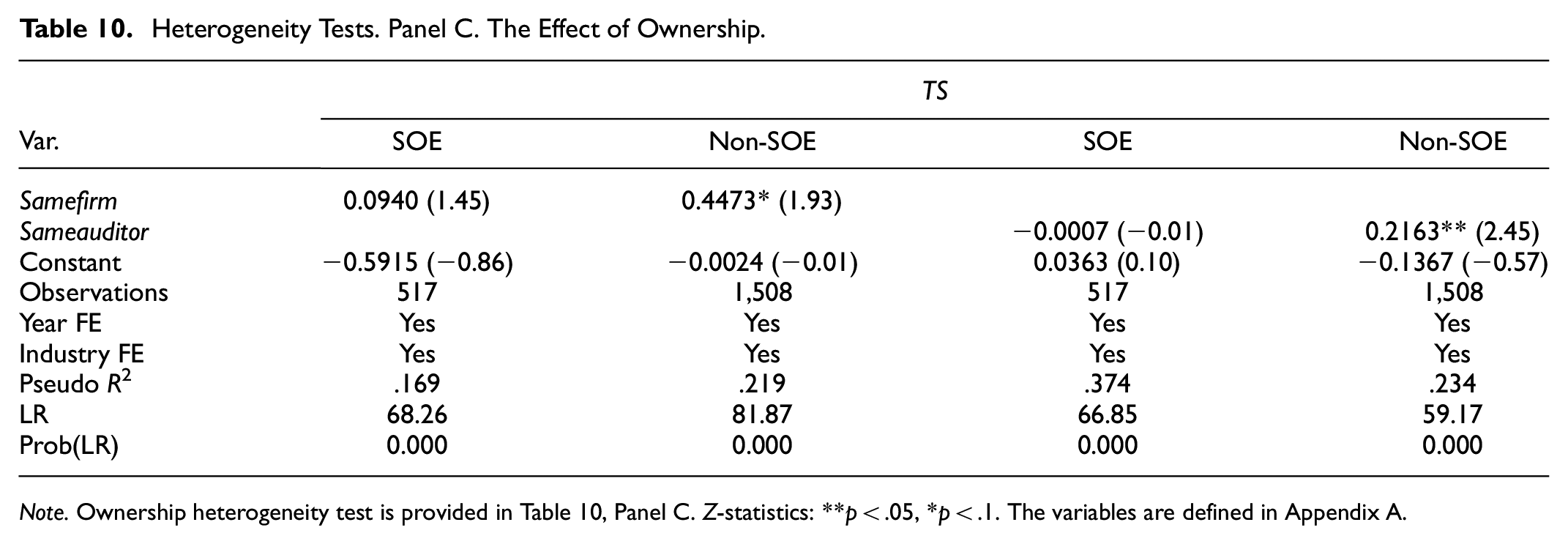

State-owned enterprises (SOEs) have often been targets of takeovers under privatization policies (Del Bo et al., 2017). While the Chinese government supports SOEs at the policy level, it also retains ultimate decision-making authority over major economic decisions, including M&A. Although operational and management authority may be transferred to the enterprises, the government still uses SOEs as a tool for implementing its policies (X. Jin et al., 2022). This dual role is particularly evident in M&A activities: the government encourages local SOEs to engage in M&A to fulfill policy obligations or achieve political progress, while central SOEs are often driven by the goal of strengthening control over state-owned capital (Del Bo et al., 2017). Consequently, when the acquirer is a state-owned company, the M&A decision is likely influenced more by government policy objectives than by the aim of maximizing corporate value (Gu et al., 2020). In such cases, a shared auditor can play a crucial role by acting as a communication channel, helping to reduce barriers and facilitate clearer understanding between the involved parties.

The regression results are shown in Table 10, Panel C. In the sample, the relationship between target selection and shared auditor shows a significant positive moderating effect when the acquirer is non-SOE (Coeff. = .4473, p < .1). This suggests that non-SOEs typically aim to maximize their interests in such transactions. The relationship between target selection and same signing auditors also shows a significant positive moderating effect when the acquirer is non-SOE (Coeff. = .2163, p < .05). Also shows a significant positive moderating effect.

Heterogeneity Tests. Panel C. The Effect of Ownership.

Note. Ownership heterogeneity test is provided in Table 10, Panel C. Z-statistics: **p < .05, *p < .1. The variables are defined in Appendix A.

Relative Size

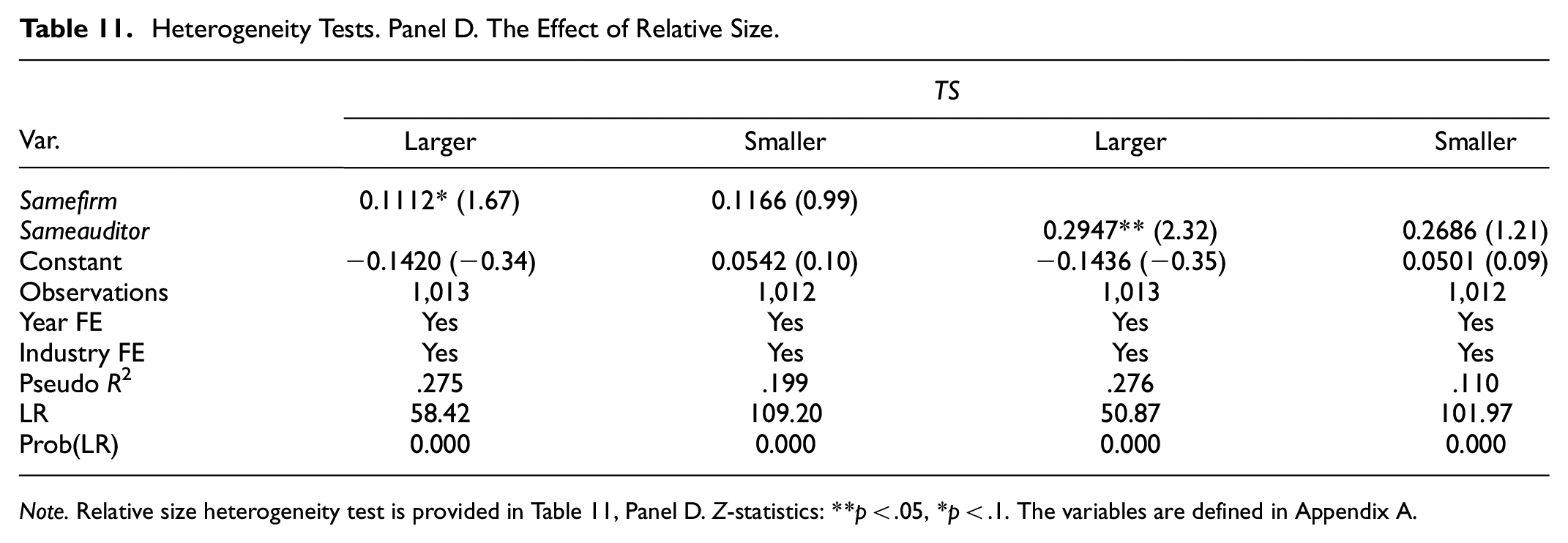

Customer size and auditor selection have a significant positive correlation. Greater client size increases the likelihood that they will select an excellent audit firm (T. Chen et al., 2012; Danos & Eichenseher, 1986; Healy & Lys, 1986; Johnson & Lys, 1990; Reynolds & Francis, 2000). Additionally, when the acquirer is significantly larger than the target, it exercises greater control over the target, possibly prompting the target to engage the same auditor to facilitate better access to its information(Dhaliwal et al., 2016). Based on this, we posit that larger firms have higher expectations for targets in M&A transactions and often prefer to gather detailed insights about their targets through external networks. This approach not only helps in obtaining more accurate inside information but also supports the realization of economies of scale in M&A activities.

We divided the sample into two subgroups based on the relative sizes of the acquirer and target. If the acquirer’s size exceeds the median, it is classified as a larger acquirer, and if below, as a smaller acquirer. The regression results are presented in Table 11, Panel D. When the acquirer is a large enterprise (Coeff. = .1112, p < .1), there is a significant positive moderating effect on the relationship between the target (TS) and the shared auditor (Samefirm). This shows that when the scale of the acquirer is large, the acquirer has stronger control and is more willing to understand the target through sharing the audit relationship. In the relationship between the target (TS) and the same signing auditors (Sameauditor), when the acquirer is a large enterprise (Coeff. = .2947, p < .05), it also shows a significant positive moderating effect. Thus, both the audit firm and the audit team tend to favor larger acquirers.

Heterogeneity Tests. Panel D. The Effect of Relative Size.

Note. Relative size heterogeneity test is provided in Table 11, Panel D. Z-statistics: **p < .05, *p < .1. The variables are defined in Appendix A.

Audit Firm Size

The Big 4 audit firms are renowned for their high standards and independence in auditing, leading to better audit quality and reduced earnings management (Jain & Agarwalla, 2023; Lopes, 2018). This study investigates how the size of the audit firm influences the effects of shared audit firms or signing auditors. Table 12, Panel E compares results between Big 4 and non-Big 4 firms. For Big 4 firms, the impact of shared auditors on the relationship between TS and Samefirm is insignificant. In contrast, for non-Big 4 firms, the effect of shared auditors on TS and Samefirm is more pronounced (Coeff. = .1519, p < .05). Non-Big 4 auditors in China, being less independent than Big 4 firms, may be more inclined to follow client directives and gather information, as well as collect validation data due to the transparency of shareholders’ financial information. Consequently, bidders often prefer non-Big 4 firms due to the easier information collection process. Similarly, the relationship between TS and Sameauditor shows a significant positive effect when the audit firm is a non-Big 4 firm (Coeff. = .1491, p < .1), indicating a stronger moderating effect in this context.

Heterogeneity Tests. Panel E. The Effect of Audit Firm Size.

Note. Audit firm size heterogeneity test is provided in Table 12, Panel E. Z-statistics: **p < .05, *p < .1. The variables are defined in Appendix A.

Robustness Tests

We conducted robustness tests in two ways. First, we assessed the stability of findings by applying alternative variables of shared auditors and same signing auditors. Second, we carried out the regression using a newly matched sample.

Alternative Measures

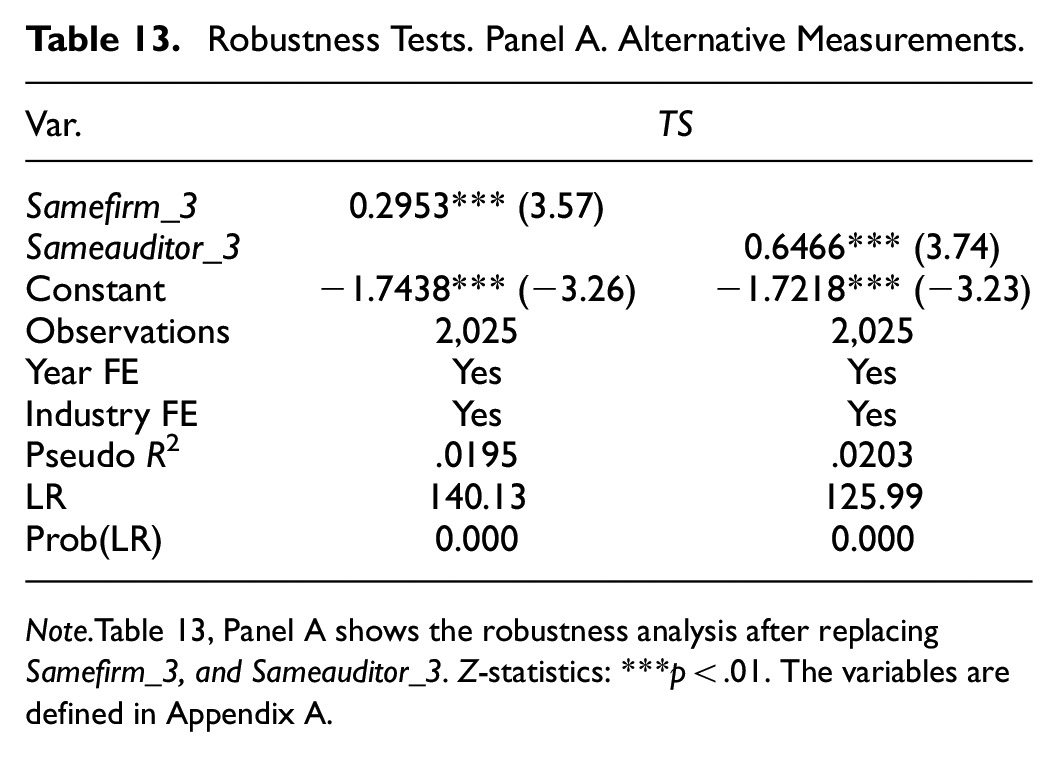

The model measures “same audit firm” and “same signing auditors” based on the data from 1 year before the M&A announcement. This study also uses “the same audit firm or the same signing auditor within 3 years before the M&A” as a proxy indicator. As demonstrated in Table 13, Panel A, Samefirm_3 (Sameauditor_3) and target selection (TS) are significant at 1% after replacing the independent variable, and the regression results are unchanged. To sum up, after replacing the key dependent variable, the previous research conclusions have not changed and the conclusions are robust.

Robustness Tests. Panel A. Alternative Measurements.

Note.Table 13, Panel A shows the robustness analysis after replacing Samefirm_3, and Sameauditor_3. Z-statistics: ***p < .01. The variables are defined in Appendix A.

Alternative Matching Technique

The matched sample of 1083 M&A samples is constructed using the same criteria of industry and size. Considering the possibility of sample selectivity bias for samples constructed according to this criterion, a new matching method is adopted in this paper. The matching criteria remain the same, but the ratio is 1:2 to collect samples (the final sample is 3,125, of which 1,083 are treatment samples and 2,042 are matched groups). As shown in Table 14, Panel B, Samefirm (Sameauditor) is significantly correlated with TS (Coeff. = .5028, p < .01; Coeff. = .7112, p < .01) after the newly matched samples are selected for testing.

Robustness Tests. Panel B. A Newly Matched Sample.

Note. Table 14, Panel B shows the robustness analysis with the newly matched sample. Z-statistics: ***p < .01. The variables are defined in Appendix A.

Conclusions

This study explores how shared auditors and same signing auditors influence M&A decision-making, particularly in target selection, and examines how this impact varies across different contexts. The use of shared auditors and same signing auditors by the acquiring firm is positively linked to the successful completion of M&A deals. Additionally, the impact varies across different acquirer types and M&A characteristics. Specifically, the effect is stronger for large acquirers, state-owned acquirers, cross-industry M&A, cross-province M&A, and non-Big 4 audit firms. The results remain robust after controlling for potential confounding variables through sample adjustment and employment period replacement.

The finding may have several theoretical contributions and implications for audit firms and M&A market. Firstly, we try to expand the research on “information sharing” (Capron & Shen, 2007; Chahine et al., 2018; Knechel et al., 2015; Marquardt & Zur, 2015), by highlighting the vital role of auditors as intermediaries in M&A. The mechanisms of “information sharing” not only manifest in areas such as “interlocking directors” and “shared advisors” but also at the level of auditors involved in M&A (Y. Cai et al., 2016; Ishii & Xuan, 2014; Rousseau & Stroup, 2015; Stuart & Yim, 2010). Our research demonstrates that auditors, whether at the audit firm or individual level, significantly impact the success rate of M&A transactions, especially in complex scenarios such as large-scale acquisitions, cross-industry, and cross-province deals. This underscores the importance of strategic auditor selection in M&A activities and suggests that both audit firms and regulatory bodies should monitor the benefits of shared auditing carefully.

Secondly, our research extends the investigation on individual auditors (Bedford et al., 2023; J. Z. Chen et al., 2020; Kachelmeier, 2010; Mala & Chand, 2015). While studies on individual auditors have been limited due to data constraints, particularly in countries like China, Taiwan, and Australia, our study provides new insights through a comprehensive survey that fills a gap in the literature by providing new insights into the impact of individual auditors(Al-Dhamari & Chandren, 2018; Burke et al., 2020; J. Z. Chen et al., 2020; Chi & Chin, 2011; Jiu et al., 2020). Our research suggests that to fully leverage the potential of shared auditors in future M&A transactions, firms should consider engaging auditors with relevant industry experience 1 to 2 years prior to the transaction.

Moreover, the implications for audit firms and the M&A market are multifaceted. To support the sustainable development of the M&A market, it is recommended that audit firms establish robust social and informational networks. Strengthening these networks will enable audit firms to play a more proactive role in M&A transactions, thereby enhancing overall market quality and success rates. However, while pursuing these network benefits, it is essential to mitigate potential risks of homogenization within the audit industry to maintain the independence and diversity of audit opinions.

This paper has several limitations. Firstly, the small sample size due to limited audit firm data restricts the applicability of the findings to unlisted companies. Future research could address this by including a larger number of unlisted companies to enhance the generalizability of the results. Secondly, the study assumes that the acquirer and target share common interests, but it does not address how shared auditors might behave in situations with conflicting interests. Future studies could investigate how shared auditors handle conflicts of interest. Lastly, while this study focuses on the effects of shared auditors and same signing auditors, it does not explore the impact of social relationship networks between audit firms. Future research could examine how various social connections and networks influence M&A outcomes, with a particular emphasis on information sharing.

Footnotes

Appendix A. Variable Definitions

| Variables | Definitions |

|---|---|

| Dependent variables | |

| TS | The indicator variable equals 1 if the company is the real target of M&A; 0 otherwise. |

| Independent variables | |

| Samefirm | The indicator variable equals 1 if the acquirer and the target hire the same audit firm; 0 otherwise. |

| Sameauditor | The indicator variable equals 1 if the acquirer and the target have the same one or two signing auditors; 0 otherwise. |

| Moderator variables | |

| SI | The indicator variable equals 1 if shared auditor = 1 and the shared auditors are from related industries; 0 otherwise. |

| SP | The indicator variable equals 1 if shared auditor = 1 and the shared auditors are from the same province; 0 otherwise. |

| BIG4 | The indicator variable equals 1 if shared auditor = 1 and the shared auditors are from the “Big 4”; 0 otherwise. |

| SOE | The indicator variable equals 1 if the acquirer is a state-owned enterprise; 0 otherwise. |

| RS | The ratio of the target’s market value to the acquirer’s market value. |

| Target characteristics | |

| SIZE | The natural log of total assets. |

| LEV | Total liabilities are divided by the total assets of the target. |

| GROWTH | Current year operating income minus prior year operating income to prior year operating income. |

| OCF | Operating cash flow to the prior year’s total assets. |

| ROE | The ratio of the net income to the target’s equity. |

| LSR | The shareholding ratio of the largest shareholder. |

| BM | The book value of the target’s equity to the market value. |

| PER | The ratio of the actual and potential target’s share price to earnings per share. |

| Shareholding structure | |

| SCALE | The number of board members of the target. |

| IND | The indicator of the proportion of independent directors on a board of directors of a target company to the total number of board members. |

| STD | The standard deviation of monthly stock returns of the target. |

| HHI | HHI = ∑(Xi/X)2, X = ΣXi, Xi is the operating revenue of firm i in the industry of the target. |

| PAY | The indicator variable equals 1 if the acquirer uses stock as a method of payment, and 0 otherwise. |

| LOSS | The indicator variable equals 1 if the acquirer’s net profit > 0, and 0 otherwise. |

| Robustness tests | |

| Samefirm_3 | The indicator variable equals 1 if the acquirer and the target hire the same audit firm within 3 years before the announcement, and 0 otherwise. |

| Samefirm_Sameauditor_3 | The indicator variable equals 1 if the acquirer and the target have the same one or two signing auditors within 3 years before the announcement; 0 otherwise. |

| Dummy variables | |

| Industry | Based on Guidelines for the Industry Classification of Listed Companies (2012). |

| Year | M&A transactions took place from 2010 to 2020, with 10 years of dummy variables set. |

Note. All accounting variables are derived from data of the preceding year and the variables related to M&A are as of the acquisition announcement year. The source of observations is all from CSMAR.

Acknowledgements

Special thanks to the reviewers for valuable comments.

Data Availability Statement included at the end of the article

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by The Project of Scientific Research and Development Program of Hebei University of Economics and Business, “Logical Mechanism and Practical Path of Digital-Realistic Integration Driving the Development of New Quality Productivity” (Grant No. 2024YB05); This study was supported by the Scientific Research Program for Higher Education Institutions of Hebei Provincial Department of Education (Grant No. QN2025869).

Ethics Statement

This research did not involve human or animal participants.

Data Availability Statement

All data are publicly available from the sources identified in the article.