Abstract

Investing in green total factor productivity is the key to realizing high-quality economic development in China. Can green finance effectively enhance green total factor productivity and promote high-quality economic development? Based on the panel data of 30 provinces in China from 2010 to 2020, this study empirically examines the direct, indirect, nonlinear, and spatial effects of green finance on green total factor productivity by using the two-way fixed effects model, the mechanism test model, the threshold effect model, and the dynamic spatial Durbin model. The results show that (1) green finance can directly promote green total factor productivity, specifically a 1% increase in the standard deviation of green finance increases green total factor productivity by 2.98% relative to the mean; (2) substantial green technological innovation, industrial structure supererogation, and industrial structure rationalization are important mechanisms for green finance to enhance green total factor productivity; (3) when the economic development level and urbanization level are used as threshold variables, the impact of green finance on green total factor productivity has a nonlinear characteristic of increasing “marginal effect”; (4) there is a significant positive spatial spillover effect of green finance on green total factor productivity, which is dominated by the short-run spatial effect; (5) the effects of green finance on the enhancement of green total factor productivity are more obvious in the eastern regions (2.0580), the high marketization level regions (0.7866), and the weak environmental protection enforcement strength regions (0.7699). This study reveals the internal logic of the role of green finance in green total factor productivity growth and provides empirical support for green finance to promote high-quality economic development. Therefore, local governments should actively promote the development of green finance, and at the same time take into account the differences in the economic development stage and urbanization process of each region and formulate differentiated green finance development policies.

Plain language summary

Investing in green total factor productivity is the key to realizing high-quality economic development in China. Can green finance effectively enhance green total factor productivity and promote high-quality economic development? Based on the panel data of 30 provinces in China from 2010 to 2020, this study empirically examines the effects of green finance on green total factor productivity and its mechanism of action by using various econometric models. The results show that (1) green finance can directly promote green total factor productivity and this conclusion still holds after a series of robustness tests such as instrumental variables approach and exclusion of contemporaneous policy effects; (2) substantial green technological innovation, industrial structure supererogation, and industrial structure rationalization are important mechanisms for green finance to enhance green total factor productivity; (3) when the economic development level and urbanization level are used as threshold variables, the impact of green finance on green total factor productivity has a nonlinear characteristic of increasing “marginal effect”; (4) there is a significant positive spatial spillover effect of green finance on green total factor productivity, which is dominated by the short-run spatial effect; (5) the effects of green finance on the enhancement of green total factor productivity are more obvious in the eastern regions, the high marketization level regions, and the weak environmental protection enforcement strength regions. This study reveals the internal logic of the role of green finance in green total factor productivity growth and provides empirical support for green finance to promote high-quality economic development.

Keywords

Introduction

At present, China’s economy has shifted from the stage of high-speed growth to the stage of high-quality development, and the issues of environmental pollution and waste of resources have become important factors restricting the high-quality development of China’s economy. In this context, how to realize green and sustainable development has attracted great attention from the Chinese government. The Fifth Plenary Session of the 18th Communist Party of China (CPC) Central Committee for the first time put green development as one of the five development concepts and elevated green development to the national development strategy level. The report of the 20th CPC National Congress clearly puts forward “promoting green development and harmonious coexistence between human beings with nature,” which further establishes the important status and strategic significance of green development. Since entering the new century, green total factor productivity has received increasing attention in the process of transformation from crude economic development to high-quality economic development. Green total factor productivity is an important indicator for measuring green sustainable development capacity in the new era, which is based on total factor productivity and further takes into account environmental protection factors (Tian & Pang, 2022). Therefore, under the dual constraints of resources and the environment, focusing on enhancing green total factor productivity is a key initiative to promote a comprehensive green transformation of socio-economic development and to facilitate high-quality economic development.

In recent years, with the in-depth implementation of the concept of green and low-carbon development, China’s green finance has been developing rapidly. According to the Global Green Finance Development Report (2022) released by the International Institute of Green Finance (IIGF) Central University of Finance and Economics, China’s green finance development index in 2021 ranked fourth out of 55 countries in the world, topping the list of developing countries. Relevant data from the former China Banking and Insurance Regulatory Commission (CBIRC) shows that by the end of 2022, the balance of green credit of 21 major domestic banks will be RMB 20.6 trillion, a year-on-year increase of 33.8%, which can support the saving of more than 600 million tons of standard coal and the emission reduction of more than 1 billion tons of carbon dioxide equivalent per year. In the same year, the new issuance scale of green bonds in China amounted to RMB 874.658 billion, a year-on-year increase of 44%, effectively broadening the investment and financing channels for green projects. In October 2023, the Central Financial Work Conference explicitly took “green finance” as one of the five articles for building a financial powerhouse, once again clarifying the important role of green finance in promoting the high-quality development of green and low-carbon industries. It can be seen that green finance, which is aimed at improving the environment and combating climate change, is gradually becoming one of the key factors in promoting green total factor productivity.

Existing studies have mainly examined environmental regulation (Cheng & Kong, 2022; He et al., 2021; Tian & Feng, 2022; Zheng et al., 2023), financial agglomeration (X. Li et al., 2023; Xie et al., 2021), technological innovation (C. Chen et al., 2018; Wang et al., 2021; X. Zhao et al., 2022), fiscal decentralization (Song et al., 2018; X. Zhan et al., 2022), and resource mismatch (Hao et al., 2020) on green total factor productivity. In addition, there are some studies focusing on the effects of green finance on green total factor productivity (Lee & Lee, 2022; Shi & Shi, 2022; K. Xu & Zhao, 2023; H. Zhang et al., 2022), which provide useful empirical references for this research. However, the above studies do not provide a unified analytical framework to comprehensively reveal the direct, indirect, non-linear and spatial effects of green finance on green total factor productivity. Hence, this paper attempts to construct a complete framework to examine the environmental-economic dual effects of green finance in depth and answer the following three questions: does green finance effectively enhance green total factor productivity? If this effect exists, what are the influencing mechanisms of green finance on green total factor productivity? Is there a nonlinear relationship and spatial spillover effects on the impact of green finance on green total factor productivity? Clarifying the above issues has important theoretical and practical significance for understanding the economic growth and environmental governance effects of green finance, promoting finance to better serve green development, and thus promoting China’s high-quality economic development.

In view of this, this research combines the connotation and realistic characteristics of green finance to construct a theoretical analysis framework of the impact of green finance on green total factor productivity. The panel data of 30 provinces in China from 2010 to 2020 is selected to investigate the direct effect, indirect effect, nonlinear effect, and spatial effect of green finance on green total factor productivity. The marginal contributions of this study are mainly as follows. Firstly, this study examines the two indirect transmission mechanisms of green technological innovation and industrial structure upgrading. This adds new empirical evidence and explanations to the study of the impact mechanism of green finance on green total factor productivity. Secondly, this study also reveals the nonlinear effect of green finance on green total factor productivity and verifies the threshold effect of the economic development level and urbanization level between green finance and green total factor productivity. This deepens the research on the effect of green finance in the established literature to a certain extent. Thirdly, considering the spatial dependence of green finance and green total factor productivity, this study further explores the spatial spillover effect of green finance on green total factor productivity. It enriches the discussion on the spatial effects of green finance in existing studies. Finally, the heterogeneity of the impact of green finance on green total factor productivity is revealed based on the differences between different regional characteristics, different marketization levels, and different environmental protection enforcement strengths. This provides a new research perspective for the literature on green finance and green total factor productivity.

The remainder of the study is organized as follows. Section 2 is the theoretical framework and research hypotheses. Section 3 presents the research design, which mainly introduces the model setting, variable measurement, data sources, and descriptive statistics results. Section 4 shows the empirical results and analysis, which empirically examines the effects of green finance on green total factor productivity and its functioning mechanism in a multi-dimensional way. Section 5 summarizes the conclusions and research contributions and proposes relevant policy implications, as well as discusses research limitations and future research directions.

Theoretical Framework and Research Hypotheses

This study demonstrates the impact of green finance on green total factor productivity from the multi-dimensional perspectives of direct effects, indirect effects, nonlinear effects, and spatial spillover effects.

Figure 1 illustrates the theoretical framework of green finance on green total factor productivity.

Theoretical framework of green finance on green total factor productivity.

Direct Effects of Green Finance on Green Total Factor Productivity

Green finance, as a new financial model supporting sustainable development (R. Y. Liu et al., 2019), can directly enhance green total factor productivity and promote high-quality economic development. First, green finance has a financial support effect. On one hand, green finance policies require commercial banks to consider environmental risk factors when making credit decisions, offer loan products for environmentally friendly projects, lower the loan threshold for green enterprises, expand financing channels, and increase financial support for them (H. Zhang et al., 2022). On the other hand, reducing the credit lines of high energy-consuming and high-polluting enterprises could increase their financing costs and limit their access to funds (X. Xu & Li, 2020). Second, green finance has a resource allocation effect. Green finance can facilitate the redirection of capital from non-green industries to green industries, compelling them to undergo green transformation and upgrading (Lee & Lee, 2022), reducing energy consumption and pollution emissions. Third, green finance has a signaling effect. According to signaling theory, green financial policy can serve as a signal for the development of a green economy (H. Zhan, 2021). As the primary recipients of this signal, commercial banks and potential investors may increase credit investment in green enterprises while strictly controlling the credit scale of high energy-consuming and high-polluting enterprises. This can help the economy develop in a green, low-carbon, and sustainable manner. Focusing on the effects of financial support, resource allocation, and signaling in green finance can further stimulate the development of green, low-carbon transformation and promote sustainable economic growth. Therefore, we propose the following hypothesis.

Indirect Effects of Green Finance on Green Total Factor Productivity

Regarding the indirect impact mechanism of green finance on green total factor productivity, this study will explore it in depth from the perspectives of green technology innovation and industrial structure upgrading. Green technological innovation refers to activities that aim to reduce environmental burdens or achieve sustainable development (OECD, 2009). The role of green finance in promoting green technological innovation is mainly reflected in three aspects. First, green finance can broaden the financing channels for enterprises’ green technological innovation. As green technology innovation has the characteristics of high investment, high risk, long cycle, and high uncertainty (Weber & Neuhoff, 2010), the traditional financial services model makes it difficult to meet the financial support required by enterprises’ green innovation activities. Green finance offers various financing channels for enterprises’ green innovation activities by building a multi-level green financial market system based mainly on green loans and green bonds, supplemented by other green financial instruments. Second, green finance can reduce the financing cost of enterprise green technology innovation. Green finance policies strengthen financial institutions’ scrutiny of corporate environmental performance, improve the quality of corporate environmental information disclosure (Liu et al., 2022), and reduce the information asymmetry between financial institutions and enterprises (Jin et al., 2024; X. Li et al., 2023), thereby reducing the cost of debt financing required for corporate green innovation activities. Third, green finance can stimulate the endogenous motivation of enterprise green technology innovation. According to Porter’s hypothesis, appropriate environmental regulation can create an innovation compensating effect, encouraging firms to engage in green technological innovation and thus offset the costs of environmental regulation. And green financial policy as a kind of environmental regulation means (X. K. hang & Ge, 2021), is conducive to forcing enterprises to choose green innovation strategy and stimulate their green innovation motivation.

Green technological innovation is an important factor in enhancing green total factor productivity. Through green technology innovation, companies improve their resource use efficiency, reduce pollution emissions at the source, and play an important role in promoting the green transformation of the economy. Meanwhile, scholars have investigated the role of green technology innovation in promoting green total factor productivity from various perspectives. At the macro-city level, X. Zhao et al. (2022) found that green technological innovation has a significant positive impact on green total factor productivity by empirically examining panel data from 263 Chinese cities. At the micro-enterprise level, Wu et al. (2022) showed that green technological innovation can also significantly contribute to the enhancement of enterprises’ green total factor productivity, especially in non-state-owned enterprises and heavily polluting enterprises. Hence, the following hypotheses are proposed.

Besides promoting green technological innovation, green finance also contributes to green total factor productivity by facilitating industrial structural upgrading. From a theoretical perspective, green finance primarily drives industrial structure upgrading through two main aspects. First, green finance can promote the industrial structure supererogation. On the one hand, green finance directs financial resources toward green and low-carbon industries, encouraging the market to phase out high-energy-consuming and high-polluting industries and promoting the transition to a greener industry (W. Wang & Li, 2022; K. Zhao et al., 2024). In turn, it can facilitate the transformation of the industrial structure from the primary and secondary industries to the tertiary industry, and achieve the industrial structure supererogation. On the other hand, as the concept of green development gradually gains popularity, green finance stimulates more green investment demand from social capital, encouraging social capital to invest in green industries (K. Zhang et al., 2023). This provides important support for the evolution of the industrial structure and subsequently drives the industrial structure supererogation. Second, green finance can facilitate the industrial structure rationalization. From one perspective, green finance reduces certification and transaction costs through the use of financial science and technology, effectively enhancing the efficiency of factor allocation between the green industry and other industries. This strengthens inter-industry coordination, contributing to the industrial structure rationalization. From another perspective, green finance provides capital support to the green industry (R. Li & Luo, 2024), enabling it to achieve economies of scale and attracting resources such as commodities and technology to cluster in non-green industries (C. J. Liu et al., 2023). This further guides the effective allocation of resources among industries and then pushes forward the industrial structure rationalization.

Industrial structure upgrading also plays an important role in enhancing green total factor productivity. According to the theory of structural dividend hypothesis, industrial structure upgrading can transfer production factors from low-end industries to high-end industries by optimizing factor allocation (Timmer & Szirmai, 2000). Thereby, it can stimulate regional economic growth and improve production efficiency, thus generating the structural dividend effect. Concurrently, in the process of reallocating production factors, they are concentrated on green and low-carbon industries, thereby enhancing environmental quality and generating a green dividend effect. The research of S. Li (2021) pointed out that industrial structure optimization and upgrading help promote the growth of green total factor productivity, especially the industrial structure supererogation plays a more important role in this process. Furthermore, T. Ma and Cao (2022) discovered from a spatial effect perspective that industrial structure upgrading has a positive spatial spillover effect on the enhancement of green total factor productivity. This leads to the following hypothesis.

Nonlinear Effects of Green Finance on Green Total Factor Productivity

Economic development is the premise and foundation of financial development (Kenen et al., 1960). And green finance, as an important part of the financial industry, its effect is bound to be affected by the regional economic development level. Existing research has indicated that at higher economic development levels, green finance’s role in promoting high-quality economic development is significantly enhanced (Yu & Fan, 2022). At the same time, green total factor productivity is one of the key indicators of high-quality economic development. As a result, the enhancing effect of green finance on green total factor productivity should also be influenced by the economic development level. In one regard, at the lower economic development level, the overall development of the financial industry is relatively lagging, the green financial market system is imperfect, and financial institutions mainly aim at economic benefits. This leads to a relatively single green financial product category and service model, which can not effectively bring into play the driving effect of green finance on green total factor productivity. In another regard, when entering a higher stage of economic development, the service level of the financial industry has been comprehensively upgraded, and the supply structure of the green financial market has become more and more perfect. Financial institutions pay more attention to the organic combination of economic and environmental benefits, and constantly innovate and optimize green financial products and services, thereby facilitating green finance to enhance green total factor productivity. Thus, the impact of green finance on green total factor productivity may have a nonlinear characteristic of the economic development level, leading to the following hypothesis.

Urbanization has an essential role to play in promoting the development of the financial sector, and the effects of green finance may also be affected by the urbanization level. For example, Yan and Tan (2023) find that the impact of green finance on carbon emission performance has a nonlinear effect across different urbanization levels. Therefore, the effect of green finance on green total factor productivity is equally affected by the urbanization level. During the early stages of urbanization, economic factors are dispersed, limiting the potential for the development of high-tech enterprises focused on environmental protection and new energy. As a result, the demand for green finance markets is low, which hinders the ability of green finance to enhance overall green productivity. As urbanization levels increase, the agglomeration of talents, technology, capital, and other factors accelerates, continuously stimulating the development of green enterprises. This increases their demand for green finance and strengthens the effect of green finance on the improvement of green total factor productivity. In addition, at the beginning of the urbanization process, government support for green financial policies is insufficient, and the degree of participation in the green financial market is low. In the middle and late stages of urbanization, the incentive mechanism for green financial policies is more sound, and the scale of the green financial market has been effectively expanded. Therefore, the effect of green finance on green total factor productivity may have a nonlinear characteristic of the urbanization level, resulting in the following hypothesis.

Spatial Spillover Effects of Green Finance on Green Total Factor Productivity

According to the first law of geography, there is a certain correlation in the spatial distribution of anything, and the closer the distance the stronger the spatial correlation (Anselin, 1988). Then, the impact of green finance on green total factor productivity may also have spatial spillover effects, and its spatial mechanism of action is mainly reflected in the following three aspects. The first is the demonstration effects. Regions with better implementation effects of green financial policies will have a positive demonstration effect on surrounding areas, strengthening inter-regional green financial exchanges and cooperation, and promoting continuous learning and imitation of local green financial policies in surrounding areas. In turn, this will improve the green total factor productivity of the surrounding regions. The second is the competition effects. As a result of the significant disparities in green financial development among different regions in China, coupled with the pronounced spatial agglomeration trend (Lv et al., 2021), competition in green financial markets among local and surrounding regions has been constantly intensifying. The resulting pressure on regions has been to step up their efforts to innovate green financial products, continuously strengthen the construction of their green financial market systems, and ultimately improve the overall level of green financial development within the region. At this time, the improvement of the green financial development level in the neighboring regions can help to enhance the green total factor productivity of the region. The third is the technology spillover effects. Existing research has shown that green finance has a significant spatial spillover effect on green technology innovation (Y. Huang et al., 2022), which helps spread advanced green technology to neighboring regions and promotes the improvement of green total factor productivity in neighboring regions. Consequently, the following hypothesis is proposed.

Research Design

Economic Model

To examine the direct effects of green finance on green total factor productivity (Hypothesis 1), this study constructs the model as follows:

where

In addition to testing the direct transmission mechanism of green finance on green total factor productivity (Hypothesis 2a and Hypothesis 2b). According to the previous theoretical analysis, this study also needs to further verify the two indirect mechanisms of green technological innovation and industrial structure upgrading. Considering that the mediation effect model based on the three-step approach suffers from the problem of “Bad controls” (Angrist & Pischke, 2009). Therefore, this study draws on Baron (2022), Y. Chen et al. (2020), and J. Li et al. (2019) to construct two mechanism testing models as follows:

where

Furthermore, to identify the nonlinear effects of green finance on green total factor productivity (Hypothesis 3a and Hypothesis 3b). In this study, the economic development level and urbanization level are taken as the threshold variables respectively to establish the panel threshold model proposed by Hansen (1999), and the specific model is set as follows:

where

Finally, to further discuss the spatial spillover effects of green finance on green total factor productivity (Hypothesis 4). This study further extends the equation into a spatial econometric model by adding spatial lag terms for green total factor productivity, green finance, and control variables. Meanwhile, considering that the explained variable green total factor productivity has a certain serial correlation. Accordingly, the green total factor productivity with one period lag is also included in the model to construct the dynamic spatial Durbin model, and the specific model is set as follows:

where

Variables Selection

Explained Variable: Green Total Factor Productivity

Green total factor productivity (GTFP), as the residual value after removing factor inputs, is an important indicator of sustainable economic development. However, since the output indicator system of green total factor productivity contains both desired outputs of economic outputs and non-desired outputs of industrial pollutants. This makes the traditional DEA model not applicable. Therefore, this study adopts the SBM-GML model that considers non-desired outputs to measure green total factor productivity. Referring to J. Wang and Guo (2023) the specific calculation steps are as follows: (1) calculating the domain-wide production possibility set; (2) solving for the SBM directional distance function; and (3) constructing the GML index. Meanwhile, this study is based on the setup of the SBM-GML model, which uses capital inputs, labor inputs, and energy inputs as input indicators, and desired outputs of economic outputs and non-desired outputs of industrial pollutants as output indicators (see Table A1).

Explanatory Variable: Green Finance

Following the ideas of Lee and Lee (2022) and X. Chen and Chen (2021) this study selects indicators from five dimensions, including green credit, green securities, green insurance, green investment, and carbon finance (see Table A2). On this basis, we use weighted TOPSIS model to measure the green finance development level (GF) of each province in China. The specific measurement steps are as follows: (1) standardizing the evaluation indexes; (2) constructing a weighting matrix; (3) determining the positive ideal solution and the negative ideal solution; (4) Calculating the Euclidean distance to the positive and negative ideal solutions for each evaluation metric; and (5) measuring the green finance development level (GF). The results of the green finance measurements are shown in Figure 2.

Spatial distribution of green finance development level in China from 2010 to 2020: (a) 2010, (b) 2015, and (c) 2020.

Control Variables

In order to more comprehensively analyze the impact of green finance on green total factor productivity. This study refers to the existing literature and controls for the following variables: the economic development level (lnPGDP), infrastructure development (INF), trade openness (TRADE), energy structure (ES), population density (lnPOP), the financial development level (FD), the foreign direct investment (FDI), and the informatization level (INL). The specific definitions are shown in Table 1.

Variable Definition.

Data Source and Descriptive Statistics

This study uses the panel data of 30 provinces in China from 2010 to 2020 as the research sample. There are three main sources of sample data. The first is the various national and local statistical yearbooks. They included the China Statistical Yearbook, the China Industrial Statistical Yearbook, the China Environmental Statistical Yearbook, the China Insurance Yearbook, the China Economic Census Yearbook, and the statistical yearbooks of each province, respectively. The second is an integrated Macro and Micro database. Including CSMAR database, Wind database, Choice Financial Terminal, and China Research Data Service Platform (CNRDS), respectively. The third is the bank’s social responsibility report. Including the social responsibility reports of the Industrial and Commercial Bank of China (ICBC), Agricultural Bank of China (ABC), Bank of China (BOC), China Construction Bank (CCB), and Bank of Communications (BOCOM), respectively. It should be noted that the economic variables in this paper are all based on the year 2000 and deflated using the corresponding deflators to eliminate the effects of price fluctuations and inflation. Besides, Tibet, Hong Kong, Macao, and Taiwan were not included in the study sample because of serious missing data. The results of descriptive statistics for the main variables are presented in Table 2.

Descriptive Statistics.

Empirical Results and Analysis

Baseline Regression Results

The baseline regression results of direct effects are detailed in Table 3. Columns (1) to (3) show the estimation results of the pooled ordinary least squares, the individual fixed effects, and bidirectional fixed effects models without control variables, respectively. The findings suggest that the coefficients of green finance (GF) are all significantly positive at the 5% level. In columns (4) to (6), after including control variables, the coefficients of green finance (GF) decrease to 0.4230, 0.8503, and 0.5445, respectively. Except the pooled ordinary least squares model, all models are significantly positive at the 5% level, indicating that green finance has a significant positive effect on green total factor productivity. That is, green finance can directly enhance green total factor productivity, which is consistent with the findings of Lee and Lee (2022). In terms of economic significance, a 1% increase in the standard deviation of green finance raises green total factor productivity by 2.98% relative to the mean. Therefore, Hypothesis 1 is verified.

Results of the Baseline Regression.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Robustness Check

Instrumental Variable Estimation

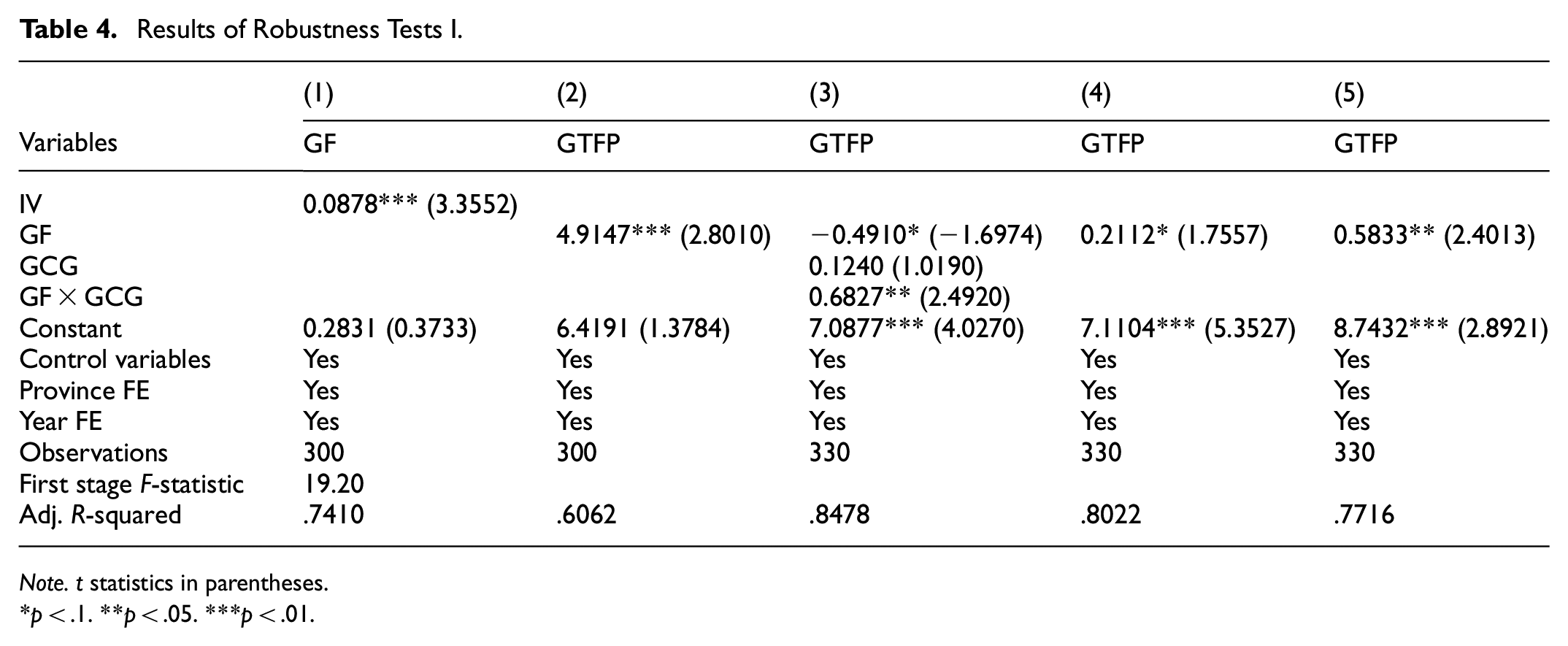

The endogenous issues may skew GF coefficient estimates, necessitating address. Drawing on C. J. Liu et al. (2023), this study uses the interaction between bank outlets per 10,000 people and lagged green finance development as an instrumental variable (IV). More bank branches facilitate credit access, and are often in developed regions prioritizing environmental protection, thus correlating with green finance. Yet, branches per capita are exogenous to green total factor productivity. Lagged green finance positively correlates with current levels but limitedly impacts current productivity (Hu et al., 2023; Lee et al., 2024), satisfying correlation and exogenous assumptions. The results of the two-stage regression of instrumental variables are shown in columns (1) and (2) of Table 4. The first stage of estimation shows that the coefficient of the instrumental variable (IV) is significantly positive at the 1% level, which validates the hypothesis of correlation between the instrumental variable (IV) and green finance (GF). Meanwhile, the F-statistic is 19.20 > 10, indicating that there is no problem with weak instrumental variables. The second stage of estimation reveals that the coefficient of green finance (GF) is also significantly positive at the 1% level, which further confirms that the findings of this study still hold after mitigating potential endogeneity issues.

Results of Robustness Tests I.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Exogenous Policy Impact Test

In 2012, China Banking Regulatory Commission (CBRC) issued a policy “Green Credit Guidelines (GCG).” The GCG policy aims to strengthen environmental risk management and promote the green transformation of the economy by clarifying the responsibilities of banking and financial institutions with regard to green credit. Theoretically, the launch of the GCG policy significantly strengthens the effect of green finance on green total factor productivity. Therefore, this study try to reveal the impact effect of the GCG policy. Referring to Lee and Lee (2022), this study adds an interaction term between green finance and the GCG policy dummy variable (assigned a value of 0 before the GCG policy is published and a value of 1 after the GCG policy is published; GF × GCG) in the baseline regression model, and the results are shown in column (3) of Table 4. The results show that the coefficient of the interaction term of green finance and GCG policy dummy variable (GF × GCG) is 0.6827 and passes the 5% significance level test, indicating that the issuance of “Green Credit Guidelines (GCG)” further enhances the effect of green finance on green total factor productivity, which is consistent with theoretical expectations.

Additional Robustness Tests

Besides, this study carries out robustness tests on the baseline regression results in the following six areas. First, green total factor productivity is re-measured using the EBM-GML model with the replacement of the explanatory variables (see column (4) in Table 4). Second, the green finance development level is re-measured by replacing the core explanatory variables with the indicator construction of Lee and Lee (2022; see column (5) in Table 4). Third, the impact of green finance on green total factor productivity is re-examined using a GMM model (see column (1) in Table 5). Fourth, all variables are indented by the first and last 5% to exclude anomalous data (see column (2) in Table 5). Fifth, environmental regulation is added to the baseline model as a control variable to exclude its potential impact on green total factor productivity and green finance (see column (3) in Table 5). Sixth, the quantile regression model is used to examine the marginal effect of green finance on green total factor productivity (see columns (4)–(6) in Table 5). The results of all the above robustness tests consistently demonstrate that green finance has a significant effect on the enhancement of green total factor productivity.

Results of Robustness Tests II.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Impact Mechanism Analysis

Impact Mechanism: Green Technology Innovation

The theoretical analysis mentioned earlier emphasizes that green technological innovation is an important mechanism for green finance to affect green total factor productivity. Therefore, the aim here is to verify whether this mechanism holds. Considering that green patents can directly and objectively reflect the output level of regional green innovation activities (Han et al., 2023), this study adopts the number of green patents granted to measure the green technology innovation level. Further, green patents can be subdivided into green utility model patents and green invention patents. Green utility model patents have a lower technology level and a shorter R&D cycle, thus representing a strategic innovation for companies. Green invention patents have the characteristics of high technological content, complex R&D process, and strict authorization criteria, reflecting substantial innovation activities of enterprises. To deeply examine the specific path of green finance to promote green technological innovation, this study divides green technological innovation into two dimensions: strategic green technological innovation and substantive green technological innovation. The natural logarithm of the number of green utility model patents granted is used to denote strategic green technology innovation (lnGTI1), and the natural logarithm of the number of green invention patents granted is used to denote substantive green technology innovation (lnGTI2).

Based on equations and to empirically test the green technology innovation as a mechanism of action. On the one hand, the impact of green finance on green technology innovation is examined, and the regression results are shown in columns (2) and (4) of Table 6. The coefficient of green finance (GF) on strategic green technology innovation (lnGTI1) is not significant, indicating that green finance fails to enhance green total factor productivity by promoting strategic green technology innovation; the coefficient of the green finance (GF) on substantive green technological innovation (lnGTI2) is significantly positive, suggesting that green finance can promote substantive green technological innovation, which in turn enhances green total factor productivity. On the other hand, the interaction term between green finance and strategic green technology innovation (GF × lnGTI1) and the interaction term between green finance and substantive green technology innovation (GF × lnGTI2) are included in the baseline model, and the regression results are shown in columns (3) and (5) of Table 6. The coefficient of the interaction term between green finance and strategic green technological innovation (GF × lnGTI1) is not significant, while the coefficient of the interaction term between green finance and substantial green technological innovation (GF × lnGTI2) is significantly positive. This indicates that the effect of green finance on enhancing green total factor productivity is more evident in groups with higher levels of substantial green technological innovation. A possible explanation is that the low technical difficulty of strategic green technology innovation is not an enhancement of firms’ real green technology innovation capability (Liu et al., 2022), which cannot effectively drive the growth of green total factor productivity. In contrast, substantial green technological innovation can reduce energy consumption and pollution emissions to a certain extent, which is an important driving force for green total factor productivity. As a result, the Hypothesis 2a is partially confirmed.

Results of the Green Technology Innovation Mechanism Test.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Impact Mechanism: Industrial Structural Adjustment

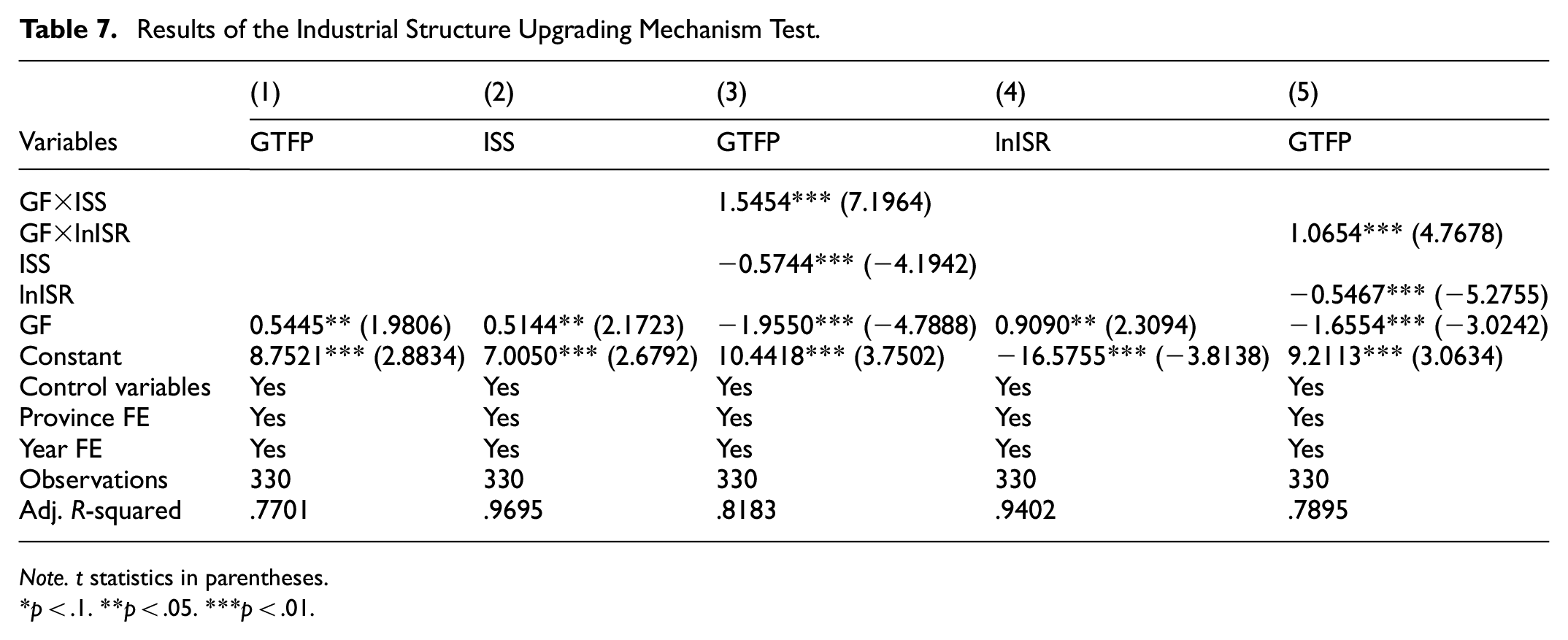

The second mechanism that this study focuses on is the ability of green finance to promote industrial structural upgrading, which in turn enhances green total factor productivity. Regarding the measure of industrial structure upgrading, this study mainly measures it from two dimensions: industrial structure supererogation and industrial structure rationalization. Industrial structure supererogation emphasizes the evolution process of industries from low-end to high-end (D. Ma & Zhu, 2022), thus we adopt the ratio of tertiary industry output value to secondary industry output value as a proxy variable for industrial structure supererogation (ISS); industrial structure rationalization refers to the quality of inter-industry aggregation, which reflects the degree of coordination among industries (Gan et al., 2011). The Theil index (TL) is a good indicator to measure industrial structure rationalization by considering the relative importance of industries and avoiding the calculation of absolute value. However, considering that the TL index is an inverse indicator, this study finally uses the natural logarithm of the inverse of the TL index as a proxy variable for industrial structure rationalization (lnISR).

Based on equations and to empirically test the industrial structure upgrading as a mechanism of action. On the one hand, the impact of green finance on industrial structure upgrading is examined, and the regression results are shown in columns (2) and (4) of Table 7. The coefficient of green finance (GF) on industrial structure supererogation (ISS) is significantly positive, indicating that green finance can enhance green total factor productivity by promoting industrial structure supererogation; The coefficient of green finance (GF) on industrial structure rationalization (lnISR) is significantly positive, suggesting that green finance can improve green total factor productivity by facilitating industrial structure rationalization. On the other hand, the interaction term between green finance and industrial structure supererogation (GF × ISS) and the interaction term between green finance and industrial structure rationalization (GF × lnISR) are included in the baseline model, and the regression results are shown in columns (3) and (5) of Table 7. The coefficient of the interaction term between green finance and industrial structure supererogation (GF × ISS) is significantly positive, indicating that the enhancing effect of green finance on green total factor productivity is stronger in the group with higher industrial structure supererogation; the coefficient of the interaction term between green finance and industrial structure rationalization (GF × lnISR) is significantly positive, showing that the enhancement effect of green finance on green total factor productivity is more obvious in the group with higher industrial structure rationalization. All the above results are in line with theoretical expectations and Hypothesis 2b is supported.

Results of the Industrial Structure Upgrading Mechanism Test.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Nonlinear Effects Analysis

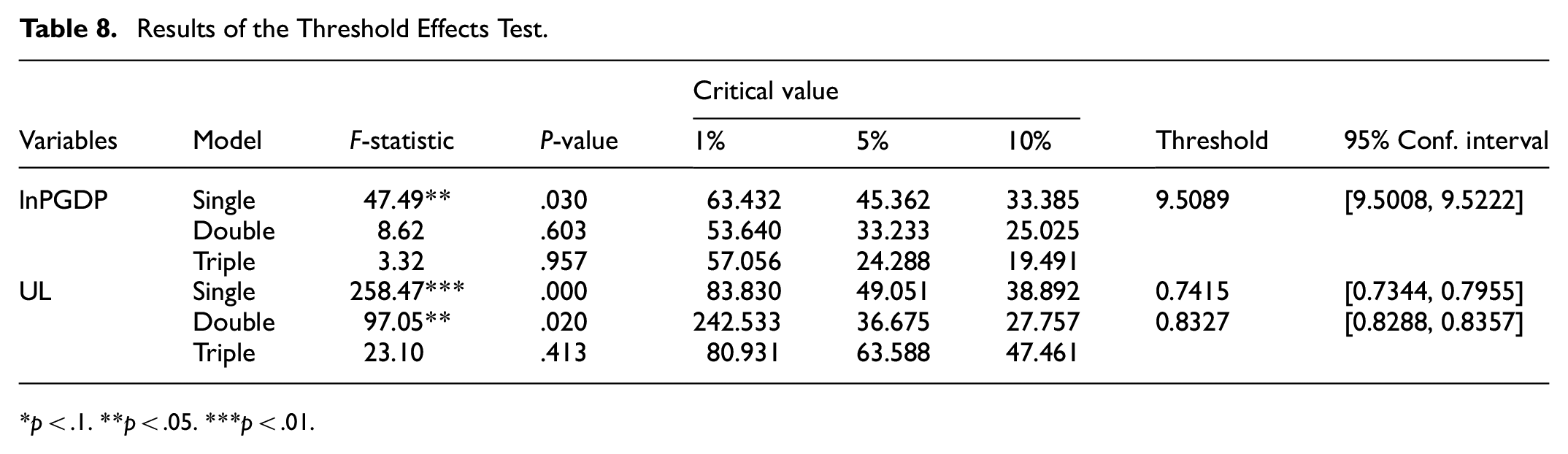

To further analyze the nonlinear effects of green finance on green total factor productivity, this study takes the economic development level (lnPGDP) and urbanization level (UL) as threshold variables for threshold estimation, respectively. Following the existing literature, the economic development level is expressed in terms of the natural logarithm of GDP per capita; the urbanization level is expressed in terms of the share of urban population in the total population. First, the threshold effect is tested and the threshold value with its number is determined by Bootstrap sampling 300 times, which is shown in Table 8. In particular, when the economic development level (lnPGDP) is used as the threshold variable, the number of threshold values is one, the threshold value is 9.5089, and it passes the 5% significance level test. This indicates that there is a single threshold effect of economic development level between green finance and green total factor productivity. When urbanization level (UL) is used as the threshold variable, the number of threshold values is two, the threshold values are 0.7415 and 0.8327, and both of them passed the 5% significance level test. This shows that there is a double threshold effect of urbanization level between green finance and green total factor productivity. It can be seen that the effects of green finance on green total factor productivity will be characterized by nonlinear dynamic changes according to the different regional economic development levels and urbanization levels. Therefore, this study constructs a single-threshold model and a double-threshold model to examine the effects of green finance on green total factor productivity with the changes in the economic development level and urbanization level of the region, respectively.

Results of the Threshold Effects Test.

p < .1. **p < .05. ***p < .01.

Table 9 presents the results of the threshold model regression. Column (1) shows the impact of green finance on green total factor productivity with the economic development level as the threshold variable. The results show that when the economic development level (lnPGDP) is less than or equal to the threshold value of 9.5089, green finance is unable to exert a significant impact on green total factor productivity; When the economic development level (lnPGDP) crosses the threshold, the coefficient of green finance (GF) increases to 1.4733 and is significant at the 1% level, indicating that green finance has a significant effect on green total factor productivity at that stage. Hence, it is evident that the enhancing effect of green finance on green total factor productivity increases with the increase in the level of economic development, and Hypothesis 3a is tested. Column (2) denotes the impact of green finance on green total factor productivity with urbanization level as the threshold variable. The findings reveal that the coefficient of green finance (GF) is significantly negative at the 1% level when the urbanization level (UL) is less than or equal to the first weighted threshold of 0.7415, suggesting that at this point green finance loses its positive effect on green total factor productivity; When the urbanization level (UL) is located between the first and second thresholds, the coefficient of green finance (GF) is significant and increases to 3.4199 at the 1% level, indicating that the effect of green finance on green total factor productivity turns from negative to positive; When the urbanization level (UL) crosses the second threshold of 0.8327, the coefficient of green finance (GF) is significant at the 1% level and increases again to 5.3719, meaning that at this point, the role of green finance in enhancing green total factor productivity is further strengthened. Therefore, it can be seen that the effect of green finance on the enhancement of green total factor productivity increases with the increase in the urbanization level, and Hypothesis 3b is proved.

Results of the Threshold Model Regression.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Spatial Spillover Effects Analysis

Spatial Autocorrelation Analysis

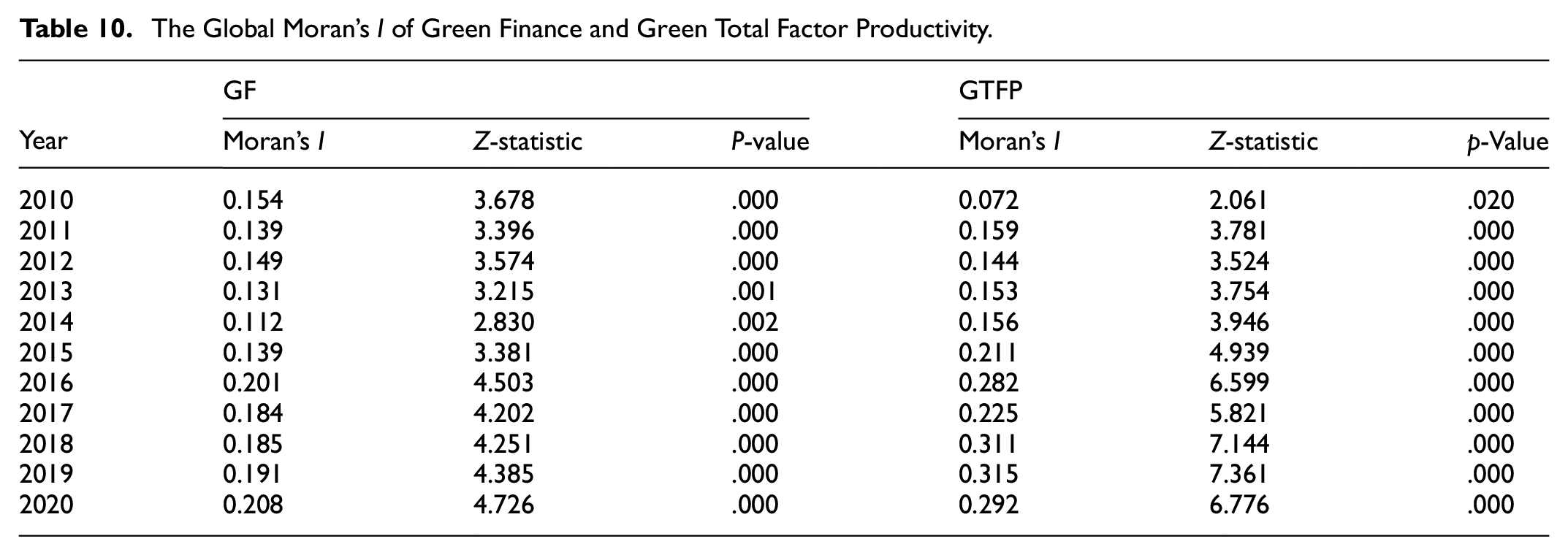

Before conducting a spatial econometric analysis, the spatial relevance of the variables of interest needs to be examined. For this purpose, this study uses Moran’s I to test the spatial autocorrelation of green finance (GF) and green total factor productivity (GTFP), respectively. Table 10 reports the global Moran’s I of green finance and green total factor productivity. The results show that the global Moran’s I of green finance and green total factor productivity are both positive, between 0.112 and 0.208 and 0.072 and 0.315, and both pass the 5% significance level test. This shows that green finance and green total factor productivity have a significant spatial positive correlation.

The Global Moran’s I of Green Finance and Green Total Factor Productivity.

Spatial Regression Results Analysis

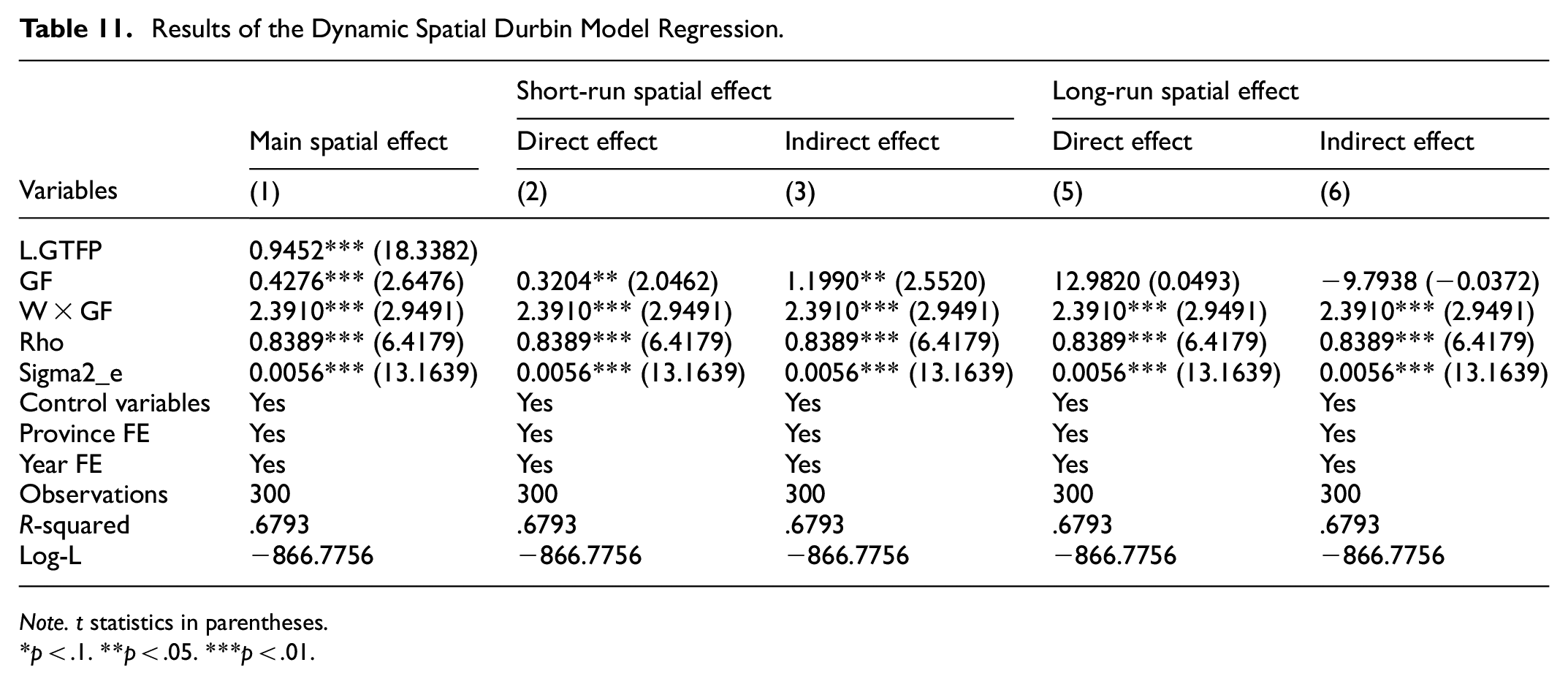

Table 11 displays the results of the dynamic spatial Durbin model regression. Column (1) shows the main spatial effect results, and the coefficient of green total factor productivity lagged one period (L.GTFP) is significantly positive at the 1% level. It demonstrates that the green total factor productivity of each province has obvious time dependence, which further validates the rationality of the dynamic model established in this study. The coefficient of green finance (GF) is significantly positive, which again validates the role of green finance in enhancing green total factor productivity. The coefficient of the spatial lag term of green finance (W × GF) is significantly positive at the 1% level, indicating that the development of green finance in the neighboring regions has a positive impact on the improvement of green total factor productivity in the region. It is initially proved that there is a spatial spillover effect of green finance on green total factor productivity. In addition, the spatial autoregression coefficient (Rho) is also significantly positive, consistent with the results of the previous spatial autocorrelation analysis.

Results of the Dynamic Spatial Durbin Model Regression.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

However, due to the presence of spatial lag terms in the dynamic spatial Durbin model, the point estimation method used has significant errors and cannot directly reflect the degree of influence of green finance on green total factor productivity. Therefore, this study draws on Lesage and Pace (2009) to decompose the coefficients of green financial effects on green total factor productivity into direct, indirect (spatial spillover), and total effects by partial differentiation. Meanwhile, the dynamic spatial Durbin model further divides the three effects into short-run and long-run spatial effects (short-run and long-run spatial effects correspond to different time scales, respectively, with short-run effects focusing on immediate relationships between variables and long-run effects focusing on long-run relationships between variables.), and the decomposition results are shown in columns (2) to (5) of Table 11. From the perspective of short-run spatial effects, the direct and indirect effects of green finance on green total factor productivity are 0.3204 and 1.1990, respectively, and all of them pass the 5% significance level test. This suggests that green finance can not only effectively enhance the green total factor productivity of the region, but also drive the growth of green total factor productivity in neighboring regions, with significant spatial spillover effects. From the perspective of long-run spatial effects, the direct and indirect effects of green finance on green total factor productivity are not significant. Possible reasons for this may include that the current development of green finance is still in its early stages, with incomplete policy and institutional systems and immature market operation systems. A long-run mechanism for green finance development has not yet been formed, thus the long-run spatial effects are not significant. In summary, green finance has a positive spatial spillover effect on green total factor productivity, and the short-run spatial effect is dominant. Thus, Hypothesis 4 is further verified.

Heterogeneous Effects Analysis

Regional Characteristics

Due to significant differences in resource endowments and economic development among various regions, both green finance and green total factor productivity exhibit distinct regional heterogeneity characteristics. Therefore, the impact of green finance on green total factor productivity is also likely to vary across regions and needs to be discussed in depth. For this reason, the entire sample is divided into two groups: the eastern and the midwest regions, according to the classification standard of the National Bureau of Statistics (NBS) of China. The results of the subgroup regressions are shown in columns (1) and (2) of Table 12. The findings show that the coefficient of green finance (GF) is significantly positive in the eastern region but significantly negative in the midwest region; the p-value for the test of difference in coefficients between groups is .000, which is significant at a 1% level. This means that green finance has a more pronounced role in enhancing green total factor productivity in the eastern region than in the midwest region. The possible reason is that the eastern region of China is more economically developed, and its financial market system is more complete, which makes the overall level of green financial development higher (Lv et al., 2021). Consequently, it is more conducive to green finance to play a more effective. In contrast, the midwest region has insufficient support for the development of green finance due to its weak economic foundation and the lagging development of the financial industry as a whole. As a result, green finance fails to have a positive effect on green total factor productivity.

Results of the Heterogeneity Effects Test.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Marketization Level

Differences in the marketization level of regions may have an impact on the effectiveness of green finance in promoting green total factor productivity enhancement. To quantify this effect, this study uses the marketization index compiled by Wang et al. (2021) as a measure of the regional marketization level, with larger values of the index indicating a higher marketization level. Then, we divide the full sample into the high marketization level group (H-ML) and low marketization level group (L-ML), according to the median of the annual marketization index. The group regression results are shown in columns (3) and (4) of Table 12. It is easy to see that the coefficient of green finance (GF) is significantly positive in the high marketization level group but not significant in the low marketization level group; the p-value of the test of difference of coefficients between groups is .088, which is significant at a 10% level. As a result, it can be seen that green finance has a stronger effect on the enhancement of green total factor productivity in regions with high marketization levels, which is consistent with the findings of Zhou and Chen (2023). The possible reason is that compared with regions with a higher marketization level, regions with a lower marketization level have less mature market mechanisms, and the local government has a greater degree of intervention in bank credit investment as well as the management of enterprises (X. L. Huang et al., 2023). This leads to the lower effectiveness of green finance policy implementation, which in turn weakens the effect of green finance on it.

Environmental Protection Enforcement Strength

The area of environmental protection enforcement strength is an important factor affecting the effectiveness of environmental regulation policies (Cui et al., 2023). The effects of green finance as an environmental regulatory policy on green total factor productivity may also be affected by environmental protection enforcement strength in the region. We measure the environmental protection enforcement strength of the region by the amount of sewage fee of each province. According to the median amount of annual sewage fee settlement into the reservoir, the whole sample is divided into the strong environmental protection strength group (S-EPES) and the weak environmental protection strength group (W-EPES). The grouping regression results are shown in columns (5) and (6) of Table 12. Thus, it is clear that the coefficient of green finance (GF) is significantly positive in areas with weak environmental protection enforcement strength, but not significant in areas with strong environmental protection enforcement strength; the p-value for the test of difference in coefficients between groups is .019, which is significant at a 5% level. This suggests that in regions with weak local environmental protection enforcement strength, green finance has become a powerful complement to environmental protection enforcement and can effectively contribute to green total factor productivity, similar to the findings of Cui et al. (2023); whereas in areas with strong local environmental protection enforcement strength, green finance has failed to play a catalytic role in greening total factor productivity. Possible reason may be that regions with strong environmental protection enforcement strength have a more robust environmental monitoring and warning system, and have strict control standards for pollutant emissions. Their comprehensive environmental governance has achieved significant results, making it difficult for green finance to demonstrate a significant improvement in green total factor productivity.

Conclusions and Policy Implications

Conclusions

This study focuses on the dual effects of green finance on the environment and the economy, utilizing panel data from 30 provinces in China from 2010 to 2020. Through the comprehensive application of various econometric models, the study empirically examines the impact of green finance on green total factor productivity and its underlying mechanisms from multiple dimensions. The main conclusions are as follows. First, green finance significantly promotes green total factor productivity. Second, green finance can increase green total factor productivity by promoting substantial green technological innovation, industrial structural supererogation, and industrial structural rationalization. Thirdly, the impact of green finance on green total factor productivity has a single-threshold effect on the economic development level and a double-threshold effect on the urbanization level, with a nonlinear characteristic of increasing “marginal effects.” Fourth, there is a significant positive spatial spillover effect of the impact of green finance on green total factor productivity, which is dominated by short-run spatial effects. Fifth, the role of green finance in enhancing green total factor productivity is more pronounced in the eastern regions, the high marketization level regions, and the weak environmental protection enforcement strength regions.

Policy Implications

The findings of this study also imply the following policy implications. In the first place, it is steadily promoting the high-quality development of green finance. The development of green finance plays an important role in promoting the enhancement of green total factor productivity, and it is necessary to increase support for green finance through multiple channels and continuously promote the innovation of green financial products and services. In turn, enhancing the quality and efficiency of green financial services, maximizing the positive role of green finance in the overall green transformation of economic and social development. In the second place, it should accelerate the construction of a regional green financial market integration and cooperation system. Combined with the previous conclusions, it can be seen that there is a significant positive spatial spillover effect of green finance on green total factor productivity, but only dominated by short-run spatial effect. Therefore, it is necessary to build a platform for the integration of green financial services, establish a mechanism for the interoperability and sharing of green financial information, and deepen inter-regional cooperation in green financial regulation. Thereby, a long-term mechanism for the spatial spillover effect of green finance will form. In the third place, it is important to strengthen the effective path of green finance to enhance green total factor productivity. Focusing on the growth mechanism of green finance to promote green total factor productivity, gives full play to the direct effects of green finance, such as the financial support effect, resource allocation effect, and signaling effect. And we should continue to strengthen the two indirect paths, namely green technological innovation and industrial structure upgrading, which together help to enhance green total factor productivity. In the fourth place, it is important to formulate and implement differentiated green financial policies. The conclusion of this study shows that the effect of green finance on green total factor productivity varies greatly for provinces with different economic development levels and urbanization levels. At the same time, the impact of green finance on green total factor productivity also differs in terms of regional characteristics, the marketization level, and the environmental protection enforcement strength. This means that comprehensive consideration should be given to the stage of economic development, urbanization, and regional characteristics of each province, as well as differences in their marketization levels and environmental protection enforcement strengths. On this basis, we should also formulate a targeted green financial services catalog to improve the precision of green financial support for green and low-carbon industries. Then, the problems of inadequate implementation of green financial policies and insufficient participation by financial institutions will be effectively solved.

Footnotes

Appendix A

Evaluation Index System of Green Finance.

| First-level index | Second-level index | Attribute | Weight |

|---|---|---|---|

| Green credit | Total amount of green credit | + | 0.225 |

| Ratio of interest expenditure in energy-intensive industries | − | 0.225 | |

| Green securities | Ratio of the market value of environmental protection enterprises | + | 0.125 |

| Ratio of the market value of high energy-consuming industries | − | 0.125 | |

| Green insurance | Ratio of agricultural insurance scale | + | 0.075 |

| Agricultural insurance loss ratio | + | 0.075 | |

| Green investment | Ratio of public expenditure on energy conservation and environmental protection | + | 0.050 |

| Ratio of investment in environmental pollution control | + | 0.050 | |

| Carbon finance | Intensity of carbon emission loans | − | 0.050 |

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is partly supported by Liao Ning Revitalization Talents Program (XLYC2410051) and the Youth Program of National Social Science Foundation of China (No.21CJY026).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data for this study can be obtained by contacting the authors.