Abstract

The environmental impact of trade openness has been a subject of extensive research, but gaps exist in understanding how green financing interact with trade openness on carbon emissions in emerging economies. Thus, this research aims to investigate the moderating effect of green financing on the relationship between trade openness and carbon emissions in emerging countries. The study uses a balanced panel dataset comprising BRIC and CIVETS countries spanning 1998 to 2022 years. Employing threshold effect model, we uncover involved patterns and critical thresholds that influence the environmental outcomes of trade dynamics. Finally, this paper employs different econometric models fortifying the methodological underpinning of the study. We find that green financing and trade openness lead to a reduction in carbon emissions as they are negatively associated with emissions. Further, our study finds that green financing interacted with trade openness to reduce carbon emissions because interaction of trade openness makes stronger the relationship to reduce emissions. When these two factors interact, their combined effect is even more potent. Additionally, this study identifies a threshold effect in the role of green financing, where its inhibitory impact on carbon emissions intensifies as the level of green financing increases, lead to greater reductions in emissions. This research contributes in identifying the moderating effects of green financing and the threshold effects on carbon emissions at different levels of green financing. Thus, this article implies that increasing both green financing and trade openness, along with understanding their interactive and threshold effects, is crucial for achieving substantial carbon emissions reductions.

Keywords

Introduction

The global environmental challenges, such as climate change and carbon emissions, have necessitated the exploration of sustainable development strategies, especially in emerging countries (Deb et al., 2023; H. Khan et al., 2022; Rahman & Halim, 2024). Among the factors influencing carbon emissions, both trade openness and green financing have emerged as critical determinants. Trade openness promotes economic growth and international trade but can also lead to increased carbon emissions due to industrial activities and transportation. On the other hand, green financing aims to allocate financial resources toward environmentally friendly projects and technologies, with the potential to mitigate carbon emissions (Rahman & Islam, 2023; Ran et al., 2023).

Understanding the relationship between trade openness, green financing, and carbon emissions in emerging countries is of utmost importance for policymakers, researchers, and environmentalists (Bai et al., 2022; Deb et al., 2024; Rahman & Halim, 2024; C. Sun, 2022; Thombs, 2018). Emerging countries are often characterized by rapid economic growth, increasing industrialization, and a growing environmental footprint (Ran et al., 2023). H. Sun et al. (2019) stated that trade openness and carbon emissions in Belt and Road countries emphasize the need to examine the relationship between trade openness and carbon emissions in emerging countries. Their study provides valuable insights into the potential environmental implications of trade openness in these countries. Additionally, studies by Shahbaz et al. (2017) and Wang and Wang (2021) emphasize the importance of identifying turning points of trade openness and decoupling carbon emissions from economic growth. These studies highlight the dynamic nature of the trade openness-carbon emissions nexus and the need for further exploration.

Green financing’s crucial role in curbing carbon emissions is accentuated by studies like those of Wang and Wang (2021) and Chhabra et al. (2023). These pieces of research validate that green financing has a beneficial effect on reducing carbon intensity and overall emissions. They further spotlight the essential function of financial institutions in advancing sustainable investment and finance in emerging regions. However, a review of the literature, including works by Akhayere et al. (2023), Dou et al. (2020), Rahman and Halim (2024), Rahman and Islam (2023), H. Sun et al. (2019), and Uddin et al. (2023), reveals a significant research void. While many studies have delved into the separate effects of trade openness and green financing on carbon emissions, there’s a noticeable lack of exploration into their combined influence. More specifically, the potential of green financing to moderate the relationship between trade openness and carbon emissions in emerging economies remains largely untouched.

The existing studies examined the relationship between trade openness, green financing, and carbon emissions, predominantly within the context of developed economies (Adebayo et al., 2023; Cetin et al., 2018; Guo et al., 2022). However, a noticeable research gap emerges when directing attention toward emerging countries like BRIC and CIVETS. Further, an even more substantial gap in current studies lies in the neglect of exploring the potential moderating effect of green financing on the relationship between trade openness and carbon emissions. Recognizing and understanding this moderating role is crucial, as it could play a pivotal role in reshaping the environmental implications of trade dynamics. Adding to these gaps, there is a notable absence of investigation into the threshold effect of green financing. By not delving into when and how green financing starts to exert a substantial influence over the trade-carbon emissions relationship, existing studies miss a critical dimension. Introducing this novel approach of examining threshold effects can provide a nuanced understanding of the point at which green financing becomes influential.

Thus, the main research objectives of this study are to examine the relationship between green financing, trade openness, and carbon emissions in the context of emerging countries; and to investigate the potential moderating and threshold effect of green financing on the trade openness-carbon emissions relationship. To achieve these objectives, the study aims to answer the following specific research questions:

1. What is the relationship between trade openness and carbon emissions in emerging countries?

2. What is the relationship between green financing and carbon emissions in emerging countries?

3. How does green financing interact trade openness with to influence carbon emissions in emerging countries?

4. What is the inhibitory effect of trade openness on carbon emission becomes stronger with the increasing level of green financing?

This research makes three distinct contributions. Firstly, it introduces and empirically validates the role of green financing in the relationship between trade openness and carbon emissions, particularly in emerging economies. This novel perspective underscores the significance of sustainable finance in shaping the environmental trajectory of these nations. Secondly, the study delves into unexplored territory by examining how green financing moderates the dynamic between trade openness and carbon emissions. This not only fills a critical knowledge gap but also unveils the intricate layers of this interplay. Additionally, the research introduces a pioneering methodological approach—the threshold effect of green financing—discerning the point where its impact becomes pronounced on the trade and emissions narrative. Furthermore, by focusing specifically on emerging countries, the research rectifies the literature’s bias toward developed economies. This shift unveils the unique challenges faced by emerging nations, fostering a more comprehensive understanding of global sustainability challenges. Lastly, beyond theoretical advancements, the study provides actionable strategies for policymakers to champion sustainable growth and guides financial institutions in steering toward ecologically considerate trajectories. In essence, this research serves as a catalyst for both theoretical and practical advancements in the realm of sustainable finance and environmental policy.

Literature Review

The literature review reveals the relationship between trade openness, green financing, and carbon emissions across global, regional, and country-specific contexts. H. Sun et al. (2019), Wang and Wang (2021), and Shahbaz et al. (2017) illuminated the complex dynamics between trade and environmental outcomes, introducing concepts such as the environmental Kuznets curve and emphasizing the role of income levels and renewable energy. Subsequent regional explorations by H. Sun et al. (2020), Adebayo et al. (2023), and Qi et al. (2020) provided valuable insights into the nuances of this relationship, highlighting the potential for trade openness to reduce carbon emissions while underlining the need for robust policies for sustainable growth. Additionally, Gozgor (2017), Shahbaz et al. (2017), and Wang and Wang (2021) investigated the broader implications of trade openness on carbon emissions, introducing factors such as foreign direct investment and income group asymmetries. Further enriching this discourse, research by Cetin et al. (2018), A. G. Khan et al. (2021), and Dou et al. (2020) offered insights into the temporal and regional variations of the trade and carbon emissions relationship, contributing to a more comprehensive understanding of the complexities involved.

H. Sun et al. (2019) delved into the relationship between trade and CO2 emissions in 49 high-emission Belt and Road countries, uncovering both positive and negative environmental impacts, and suggesting an environmental Kuznets curve through an inverted U-shaped relationship. Building on this, Wang and Wang (2021) analyzed 182 countries and highlighted the nuanced effects of trade openness on carbon emissions, emphasizing the role of income levels and factors like renewable energy. Similarly, Shahbaz et al. (2017) explored this nexus across 105 countries of varying income levels, revealing a generally negative impact of trade openness on environmental quality, but with complexities and feedback effects. In a regional study, H. Sun et al. (2020) focused on sub-Saharan Africa, indicating that trade openness could potentially reduce carbon emissions, but stressed the importance of robust policies for sustainable growth. Adebayo et al. (2023) provided a unique perspective by studying Sweden and emphasized the asymmetric effects of renewable energy and trade openness on emissions. Lastly, Qi et al. (2020) offered insights from China, linking population urbanization and trade openness to carbon emissions, and highlighting the multifaceted impacts of various moderated variables. Thus, the intricate dynamics between trade openness and carbon emissions, emphasizing the need for comprehensive approaches and policies to ensure environmental sustainability.

In a comprehensive exploration of the relationship between trade openness and carbon emissions, several studies have provided nuanced insights. Gozgor (2017) introduced the “trade potential index” (TPI) while examining 35 OECD countries, finding that trade openness, both nominally and through the TPI, contributed to reduced carbon emissions. This finding aligns with Shahbaz et al. (2017) who, focusing on the U.S., identified trade openness as a factor decreasing carbon emissions, though they also noted the negative environmental impact of increased FDI. Wang and Wang (2021) further nuanced this understanding by revealing the asymmetric effects of trade openness on carbon intensity across different income groups, emphasizing the role of foreign direct investment. Thombs (2018) provided a broader temporal perspective, suggesting that integration into the global economy intensified carbon emissions for less developed countries, pointing to a shift of environmentally degrading processes to these nations. Lastly, Azam et al. (2022) explored the multifaceted relationship between industrialization, urbanization, trade, and carbon emissions in OPEC countries, emphasizing the intertwined nature of these variables and the need for environmentally conscious policies. Further, the complex dynamics of trade openness and its varied impacts on carbon emissions, highlighting the need for tailored approaches and policies to ensure environmental sustainability across different contexts.

Cetin et al. (2018) explored this nexus in Turkey, revealing a long-run association between economic indicators and carbon emissions, and further supporting the Environmental Kuznets Curve (EKC) hypothesis, which posits an eventual decline in environmental degradation with economic growth. Similarly, A. G. Khan et al. (2021) in their study on Bangladesh emphasized the significant influence of energy usage on carbon emissions, while also noting the limited impact of trade openness and financial development. Dou et al. (2020) analyzed data from 76 countries, identifying an inverted U-shaped relationship between trade openness and CO2 emissions, with varying impacts across regions. This observation was further nuanced by Dou et al. (2021) in the context of the China-Japan-South Korea Free Trade Agreement, where trade openness was linked to increased carbon emissions, but this effect was mitigated post-agreement. Lastly, Nurgazina et al. (2021) provided insights from Malaysia, highlighting the significant contributions of energy consumption, trade openness, and urbanization to carbon emissions. Therefore, the multifaceted dynamics of trade openness and its varied impacts on carbon emissions, emphasizing the need for tailored environmental policies and sustainable growth strategies across different countries and regions.

Xu et al. (2021) emphasized the relationship between agricultural technological innovations (ATIs) and agricultural carbon emissions (ACEs) in China, revealing that trade openness moderates this relationship, particularly when it surpasses a certain threshold. In a similar vein, Chhabra et al. (2023) underscored the dual impact of trade openness and institutional quality on carbon emissions in BRICS nations, suggesting that while trade openness can exacerbate environmental degradation, robust institutional quality can mitigate these effects. Omri and Saadaoui (2023) provided insights from France, highlighting the contrasting impacts of nuclear energy and fossil fuels on carbon emissions, with trade openness further intensifying these emissions. Adebayo et al. (2023) explored the multifaceted interplay between geopolitical risk, non-renewable energy consumption, and carbon emissions in India, emphasizing the need for policymakers to factor in geopolitical considerations in environmental strategies. Lastly, Akhayere et al. (2023) shed light on Turkey’s environmental challenges, pinpointing energy consumption, trade openness, and financial development as key determinants of the load capacity factor (LCF). Thus, the complex interplay of trade openness and other economic factors in shaping environmental outcomes, highlighting the imperative for tailored policy interventions to ensure sustainability across diverse contexts.

Cetin et al. (2018) highlighted the synergistic effects of trade openness, innovation, and institutional quality on environmental sustainability, emphasizing the role of renewable energy and foreign direct investment in reducing carbon emissions. Building on this, Rahman and Halim (2024) explored the BRICS nations, revealing that a balanced trade ratio, coupled with green field investments and financial development, fosters environmental sustainability, though challenges arise from energy consumption and urbanization. Further emphasizing the BRICS context, Rahman, Deb et al. (2023) identified a positive correlation between trade openness and global entrepreneurship development, while another study by Rahman et al. (2021) showcased the benefits of trade openness in reducing financial intermediation costs and bolstering bank performance. Lastly, Gozgor (2017) provided insights from OECD countries, underscoring the intricate dynamics between renewable energy consumption, trade openness, and CO2 emissions. So, the pivotal role of trade openness in shaping both economic and environmental landscapes, suggesting a need for holistic policies that harness the benefits of trade while mitigating potential challenges.

Chhabra et al. (2023) underscored the contrasting impacts of trade openness and institutional quality versus energy efficiency and technology innovations on environmental quality. Building on this, both Chen and Chen (2021) and Bai et al. (2022) focused on China, revealing the pivotal role of green finance in reducing carbon emissions. While Chen and Chen highlighted the spatial spillover effects of green finance and its role in promoting green technology innovation, Bai et al. emphasized the nuanced relationships between green finance, economic growth, and industrial structures, noting regional variations in its impact. Lastly, H. Sun et al. (2020) employed an innovative approach using big data and machine learning to validate the correlation between green finance and carbon emissions. Thus, the transformative potential of green finance in driving environmental sustainability, suggesting the need for targeted policies that harness its benefits while addressing associated challenges.

Guo et al. (2022) highlighted the dual impact of fertilizer consumption and green finance on agricultural carbon emissions, revealing that while fertilizer use exacerbates emissions, green finance offers a mitigating effect. Building on this, Omri and Saadaoui (2023) emphasized the transformative potential of green finance in enhancing carbon emission efficiency (CEE) across Chinese provinces, with notable spillover effects in economically linked regions. Xia (2023) further explored the multifaceted relationship between green technology, renewable energy investments, and CO2 emissions, confirming the Environmental Kuznets Curve hypothesis for China and underscoring the pivotal role of urbanization and green technology in emission reduction. Lastly, Hou et al. (2022) shed light on the interplay between high energy-consuming industrial agglomeration, green finance, and carbon emissions, suggesting that while industrial agglomeration intensifies emissions, green finance can counteract this effect.

This conjecture is grounded in existing research, which has explored the environmental implications of trade dynamics. Rahman et al. (2021), H. Sun et al. (2019), Wang and Wang (2021), and Gozgor (2017) have indicated that increased trade openness can contribute to reduced carbon emissions. The environmental Kuznets curve, as proposed by H. Sun et al. (2019), suggests that, initially, trade openness may lead to higher emissions, but beyond a certain point, it becomes associated with environmental benefits. Similarly, Gozgor (2017) introduced the “trade potential index” (TPI) and found that trade openness, both nominally and through the TPI, contributed to decreased carbon emissions in 35 OECD countries. These insights align with the broader discourse on the potential of global trade to drive environmentally sustainable practices, emphasizing the need for empirical examination within specific contexts. Thus, H1 builds upon this foundation, proposing a negative relationship between trade openness and carbon emissions within the unique settings of BRIC and CIVETS nations.

Existing studies, such as H. Sun et al. (2019), Wang and Wang (2021), and Gozgor (2017), provided valuable insights into the environmental implications of trade dynamics but often lack a focus on the diverse trajectories and challenges faced by economies in the BRIC and CIVETS group. This gap highlights the need for empirical investigations that systematically explore the relationship between trade openness and carbon emissions in these specific settings. Crafting targeted and effective environmental policies align with the unique characteristics and growth trajectories of emerging economies. Therefore, we postulated H1:

H1. Trade openness negatively associates with carbon emissions

Xu et al. (2021), Chhabra et al. (2023), and Bai et al. (2022) investigated the transformative potential of green finance in mitigating carbon emissions. Xu et al. (2021) specifically highlighted the nuanced relationship between agricultural technological innovations (ATIs), agricultural carbon emissions (ACEs), and trade openness in China, suggesting that green financing moderates this intricate relationship. Similarly, Chhabra et al. (2023) emphasized the dual impact of trade openness and institutional quality on carbon emissions in BRICS nations, indicating that green financing can potentially mitigate environmental degradation associated with increased trade openness. Bai et al. (2022) delved into the spatial spillover effects of green finance and its role in promoting green technology innovation in China.

Studies like those by Xu et al. (2021) and Chhabra et al. (2023) highlight the transformative potential of green finance, particularly in reducing agricultural carbon emissions and mitigating the environmental degradation associated with increased trade openness. The rationale for considering green financing as a moderating factor lies in its ability to direct financial resources toward sustainable practices and technologies, thereby amplifying the environmental benefits of trade openness. When countries invest in green technologies and renewable energy projects, the negative environmental impacts of trade can be offset by cleaner production processes and reduced reliance on fossil fuels. This creates a more favorable environment for achieving sustainable economic growth, aligning trade policies with environmental objectives.

In understanding how green financing functions as a moderating factor in the relationship between trade openness and carbon emissions are to be investigated. While studies acknowledge the potential of green financing to reduce carbon emissions, the specific role it plays in influencing the impact of trade openness on environmental outcomes remains underexplored (Xu et al., 2021). The need for empirical investigations that systematically examine the moderating effect of green financing on the trade openness-carbon emissions dynamic, offer a more nuanced understanding of the interplay between sustainable finance and trade-related environmental consequences. Thus, it is crucial for informing policy decisions that seek to balance economic growth with environmental sustainability, especially in emerging economies.

Conversely, without the moderating influence of green financing, the positive effects of trade openness on carbon emissions may be significantly diminished. The absence of targeted financial support for green initiatives can lead to unchecked industrial expansion and increased carbon emissions, as noted in the studies by Shahbaz et al. (2017) and Wang and Wang (2021). Additionally, the lack of green financing might exacerbate the negative environmental impacts of foreign direct investment, as highlighted by Gozgor (2017) and Omri and Saadaoui (2023). This could lead to a scenario where trade openness, instead of contributing to environmental sustainability, becomes a driver of environmental degradation. Therefore, examining green financing as a moderating factor provides a more comprehensive understanding of how sustainable finance can enhance the environmental benefits of trade openness, offering valuable insights for policymakers aiming to balance economic growth with environmental sustainability. Therefore, we developed H2:

H2. Green Financing moderates the relationship between trade openness and carbon emissions

In understanding how the strength of this inhibitory effect changes with varying levels of green financing needs to be examined (Chen & Chen, 2021). The need for empirical investigations that systematically examine the moderating role of green financing in shaping the relationship between trade openness and carbon emissions at different levels of financial support (Gozgor, 2017). Thus, it is essential for providing policymakers and stakeholders with actionable insights into how the synergy between trade openness and green financing can be optimized to achieve more substantial environmental gains in emerging economies.

Green financing, by directing funds toward renewable energy projects, energy efficiency initiatives, and sustainable infrastructure, can substantially reduce carbon emissions. As noted by Chen and Chen (2021) and Bai et al. (2022), the spatial spillover effects of green finance promote green technology innovation, which in turn mitigates carbon emissions. When green financing is at high levels, it supports large-scale deployment of green technologies, widespread adoption of sustainable practices, and robust policy frameworks, all of which contribute to significant reductions in carbon emissions. This inhibitory effect is critical for countering the environmental challenges posed by industrialization and urbanization, as well as the negative impacts of trade openness highlighted in studies like those by H. Sun et al. (2019) and Gozgor (2017).

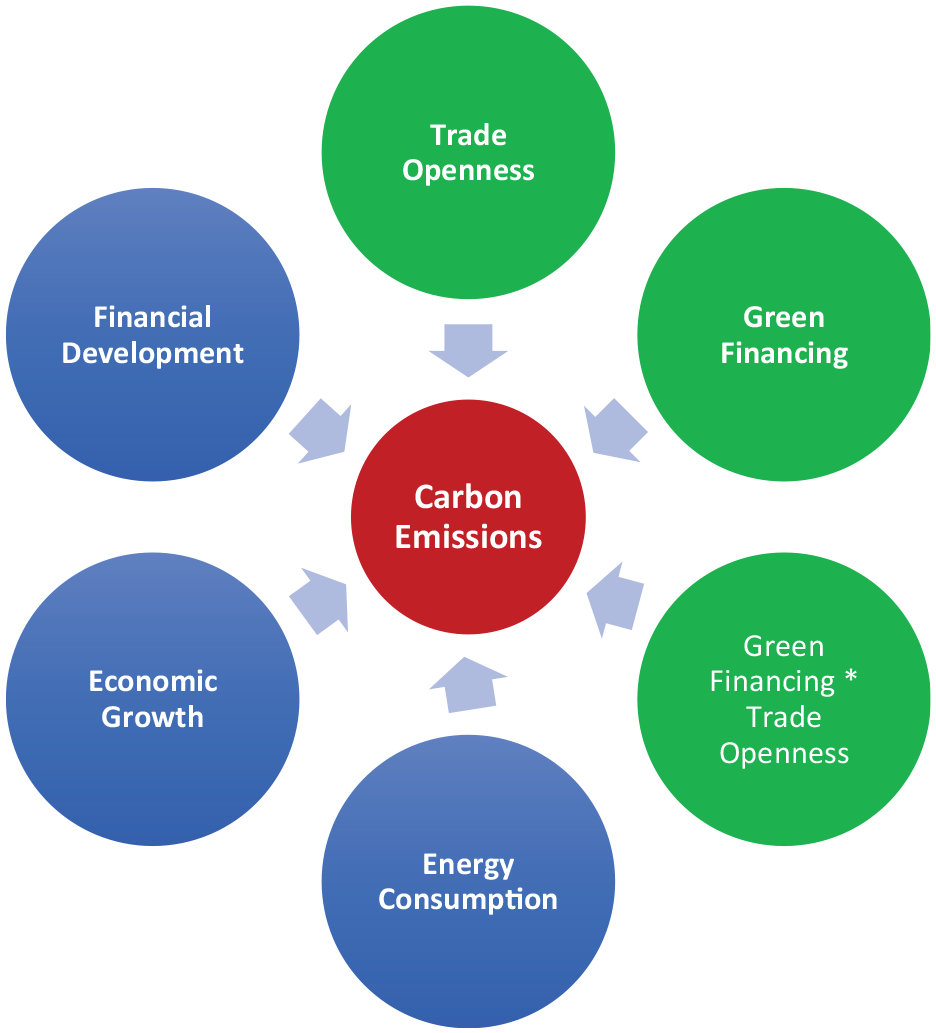

Without the inhibitory effects of green financing, the potential for reducing carbon emissions is greatly diminished. In the absence of substantial green financial investments, economies might struggle to transition to low-carbon pathways, as seen in contexts where financial development does not prioritize environmental sustainability (Shahbaz et al., 2017; Wang & Wang, 2021). Without sufficient green financing, industries may continue to rely on fossil fuels, and the adoption of clean technologies would remain limited. This scenario would hinder efforts to achieve the environmental Kuznets curve’s anticipated decline in emissions at higher income levels. Therefore, contrasting the presence and absence of strong green financing underscores its critical role: while high levels of green financing can inhibit carbon emissions effectively, its lack can lead to increased environmental degradation and a failure to meet sustainability targets. This makes understanding the varying strength of green financing’s inhibitory effects crucial for formulating effective environmental policies. Hence, we proposed H3. Based on the review of existing studies, Figure 1 is deveploped.

Conceptual model of the study developed by the authors.

H3. The inhibitory effect of green financing on carbon emission becomes stronger with the increasing level of green financing

Methodology

Model Estimation

Benchmark regression model

In this study, we investigate the relationship between trade openness, green financing, and carbon emissions in emerging countries. Following the study of J. Zhang and Ke (2022), an ordinary least squares regression model (OLS) is employed, incorporating a moderating effect to explore the potential interaction between trade openness and green financing on carbon emissions. Additionally, the presence of a threshold effect in this relationship is examined. The construction form of the benchmark least squares regression model is as follows (Equation 1):

In Equation 1, Yit represents the dependent variable, which denotes the carbon emissions per capita/metric ton of each country at each year. Xit represents the independent variable, trade openness, measured as the export-to-import ratio of each country at each year. GFNit represents the moderating variable, green financing, which is measured using an index of green credit, green investment, and green insurance. Controlit represents a series of control variables, including energy consumption (ENC), measured as energy consuming per capita/kg of each country at each year, economic growth (EGR), measured as GDP growth per capita of each country at each year, and financial development (FD), measured as a broad index capturing the efficiency, accessibility, and depth of financial development in each country at each year.

The model includes individual fixed effects (i) and time fixed effects (t) to account for individual and time-specific factors that influence carbon emissions. β1, β2, and β3 represent the coefficients to be estimated, and εit represents the random interference term.

The analysis of the dataset involved the implementation of six distinct statistical models, namely Ordinary Least Squares (OLS), Fixed Effects (FE), Dickey-Fuller GLS de-trended (D-K), Two-Stage Least Squares (2SLS), Dickey-Fuller GLS de-trended with a peak (D-Peak), and Generalized Method of Moments (GMM) (Aiken et al., 1991; Baltagi & Baltagi, 2008; Hansen, 1999; Jaccard & Turrisi, 2003; Mielke & Steudle, 2018; Ozturk & Acaravci, 2010; Roodman, 2009; Wooldridge, 2010; J. Zhang & Ke, 2022).

The employment of a diverse array of statistical models, including Ordinary Least Squares (OLS), Fixed Effects (FE), Dickey-Fuller GLS de-trended (D-K), Two-Stage Least Squares (2SLS), Dickey-Fuller GLS de-trended with a peak (D-Peak), and Generalized Method of Moments (GMM), is underpinned by a meticulous rationale aimed at fortifying the methodological underpinning of this study. OLS, as a foundational model, provides initial insights into linear associations, while FE accounts for time-invariant factors crucial in the context of emerging economies. The D-K model addresses non-stationarity concerns, ensuring robustness in time series analysis. 2SLS tackles endogeneity, offering a sophisticated approach with instrumental variables. D-Peak introduces peak detection, enriching the exploration of cyclical patterns. GMM, known for its flexibility, addresses endogeneity, instrument relevance, and orthogonality. This comprehensive suite of models is strategically chosen to collectively illuminate the nuanced dynamics of the relationships between trade openness, green financing, and carbon emissions, ensuring a thorough and robust examination of the study’s objectives.

Moderating effect model

To examine Hypothesis 2, we employ the construction method of the moderation effect model proposed by James and Brett (1984). We introduce an interaction term between the moderating variable, green financing (GFN), and the explanatory variable, trade openness (TOP), into the ordinary least squares (OLS) model to investigate whether the relationship between trade openness and carbon emissions is influenced by the level of green financing (Aiken et al., 1991; Jaccard & Turrisi, 2003; Zeleny & Cochrane, 1982). The moderating effect model is constructed as follows (Equation 2):

In Equation 2, CEM represents the dependent variable, which denotes the emissions per capita/metric ton of each country at each year. TOP represents the explanatory variable, trade openness, measured as the export-to-import ratio of each country at each year. GFN represents the moderating variable, green financing, measured using an index of green credit, green investment, and green insurance that combines them using the EVM method.

We include an interaction term, TOP × GFN (β3), to assess the moderating effect of green financing on the relationship between trade openness and carbon emissions. Control encompasses a set of control variables, including energy consumption (ENC), economic growth (EGR), and financial development (FD), which are measured as energy consumption per capita/kg, GDP growth per capita, and a financial development index respectively.

Similar to the benchmark regression model, the model incorporates individual fixed effects (i) and time fixed effects (t) to account for individual and time-specific factors that may influence carbon emissions (Adebayo et al., 2023; Aiken et al., 1991; Jaccard & Turrisi, 2003). β1, β2, β3, and β represent the coefficients to be estimated, and ε represents the random interference term.

Threshold effect model

To investigate the impact of green financing on carbon emissions in the context of trade openness, this study employs a panel threshold model. The threshold model allows us to examine whether the relationship between trade openness and carbon emissions varies across different levels of green financing (Caner & Hansen, 2004; Hansen, 1999; Stock & Watson, 2015; J. Zhang & Ke, 2022). The construction form of the threshold effect model is as follows (Equation 3):

In this model, CEMit represents the dependent variable, which is the emissions per capita in metric tons for each country in each year. TOPit is the independent variable, indicating the export-to-import ratio for each country in each year. GFNit is the threshold and moderating variable, measured by the combined index of green credit, green investment, and green insurance using the EVM method. The intervals infj and supj represent different levels of green financing, defining the critical values for the thresholds. The coefficient γ is to be estimated, and I is a piecewise function that takes the value 1 if the condition in the parentheses is true, and 0 otherwise. Controlit includes the control variables, such as ENC (energy consumption per capita in kilograms), EGR (GDP growth per capita), and FD (financial development index).

Data and Variables

Dependent variable

In this study, the dependent variable is carbon emissions, quantified as emissions per capita in metric tons for 1998 to 2022 years (see Table 1). This metric serves as a vital environmental gage, representing the volume of greenhouse gases a country discharges into the atmosphtere due to its economic activities (Adikari et al., 2023; Guo et al., 2022; Halicioglu, 2009; Hou et al., 2022). By considering emissions per capita, we obtain a standardized assessment of a nation’s environmental impact, factoring in both its population and emission intensity. The selection of the BRIC (Brazil, Russia, India, China) and CIVETS (Colombia, Indonesia, Vietnam, Egypt, Turkey, South Africa) nations for this study is underpinned by a strategic and nuanced rationale. These countries represent a diverse spectrum of emerging economies, each characterized by unique geographical, economic, and developmental attributes. The BRIC nations, encompassing Brazil, Russia, India, and China, stand as influential global players with substantial economic prowess, diverse industrialization stages, and marked growth trajectories. Their collective impact on global trade dynamics and carbon emissions is substantial, making them pivotal subjects for understanding the intricate nexus between trade openness and carbon emissions. On the other hand, the CIVETS nations, comprising Colombia, Indonesia, Vietnam, Egypt, Turkey, and South Africa, exhibit a rich tapestry of economic and industrial diversity, representing distinct regions and stages of development. By including both BRIC and CIVETS nations, this study ensures a comprehensive examination of the trade and carbon emissions relationship across a varied spectrum of emerging economies. This approach enhances the generalizability and applicability of the findings, offering valuable insights into the nuanced challenges and opportunities faced by economies at different stages of development and industrialization. Moreover, the selection aligns with the study’s focus on sustainability in emerging economies, providing a holistic understanding of the environmental implications of trade dynamics in these influential regions (Adebayo et al., 2023; Jorgenson et al., 2017; Rahman & Halim, 2024; Xia, 2023; J. Zhang & Ke, 2022).

Data Description.

Note: The study adopts a rigorous approach to pre-process null data, recognizing the importance of handling missing values to ensure the integrity of the analysis. To address missing entries in the dataset related to the variables, we employ a multiple imputation strategy. This method involves generating multiple datasets with imputed values for the missing data, considering the uncertainty associated with the imputation process. The imputation is carried out based on observed data patterns, leveraging statistical techniques to produce plausible values for the missing entries. This meticulous approach allows the study to retain a comprehensive dataset, minimizing the impact of missing values on the subsequent analysis. Furthermore, we conduct sensitivity analyses to assess the robustness of the findings to different imputation strategies, enhancing the transparency and reliability of the research outcomes.

Source: Developed by the authors.

Independent variable

The focal independent variable in this study is trade openness (TOP), quantified by the ratio of a country’s exports to imports for 1998 to 2022 years. Trade openness offers a lens into a nation’s participation in global commerce, signifying its integration level with the worldwide economic landscape (Chhabra et al., 2023; Nurgazina et al., 2021; Rahman, Deb et al., 2023; Rahman & Halim, 2024). This metric not only encapsulates the magnitude of trade endeavors, encompassing both imports and exports, but also sheds light on the degree of a nation’s economic receptivity (Antweiler et al., 2001; Dou et al., 2021; Omri & Saadaoui, 2023). The rationale behind selecting trade openness as the primary independent variable stems from the pivotal influence of global commerce in dictating both economic and ecological trajectories in burgeoning economies, notably in the BRIC and CIVETS nations (Chhabra et al., 2023; Rahman et al., 2021; Rahman & Halim, 2024). Given their meteoric rise in economic stature and industrial prowess, these nations have cemented their positions in the international trade arena (Wenlong et al., 2023). Hence, delving into the nexus between their trade openness and carbon emissions becomes imperative to discern the environmental ramifications of their commercial endeavors (Nurgazina et al., 2021).

Threshold and moderating variable

In this research, green finance is defined as the financial support directed toward projects that advocate for sustainable development, environmental preservation, and pollution reduction (Xu et al., 2021). It encompasses financial activities that further the growth of a sustainable circular economy, the embrace of clean energy, and the reduction of greenhouse gas emissions. Such endeavors epitomize the dual goals of sustainable advancement and environmental integrity (Hou et al., 2022). Within the scope of this study, green financing acts as both a moderating and threshold variable.

The study’s ambition is to evaluate the evolution of green finance across different regions, segmenting it into three core dimensions: green credit, green investment, and green insurance (Guo et al., 2022; J. Zhang & Ke, 2022). These dimensions shed light on the financial backing of low-energy and low-pollution enterprises, the strategic financial realignment away from high-polluting entities, and the proficient handling of environmental risks during the production process (Guo et al., 2022; Wenlong et al., 2023; J. Zhang & Ke, 2022).

To elaborate, green credit is assessed by the inverse relationship of interest payments from high-pollution industries to the total industrial interest outlays (Ran et al., 2023). A prominent green credit scale indicates substantial financial support for eco-conscious businesses, leading to a decrease in regional carbon emissions. Green investment, meanwhile, aims to balance production investments with environmental preservation, ensuring economic growth without compromising the environment (Thombs, 2018). This research uses two indicators to represent green investment: the allocation of resources for environmental protection in relation to GDP and the budgetary commitment toward environmental conservation.

Furthermore, green insurance, also termed ecological insurance, stands as a key mechanism to address environmental risks in a market-oriented setting. This includes policies like mandatory environmental pollution liability insurance and green product quality assurance (Guo et al., 2022). These policies empower businesses to bolster their environmental risk management, minimize pollution incidents, and reduce environmental harm during production. To measure the prevalence of green insurance in a region, this study considers the proportion of agricultural insurance earnings to the overall agricultural production value (Bai et al., 2022), reflecting regional efforts to address environmental challenges linked to agricultural practices, notably excessive use of chemical fertilizers and inefficient land use.

To measure the development level of regional green finance, the study employs the entropy value method (EVM) for normalization and weighting of the three indicators: green credit, green investment, and green insurance (Caner & Hansen, 2004; J. Zhang & Ke, 2022). The calculation steps are as follows:

1. Quantify the indicators simultaneously: Calculate the proportion (pij) of the ith sample to the j-index under the jth index by dividing the value (rij) of the indicator by the sum of all values in that column: pij = rij / Σrij, where i = 1, 2, …, n and j = 1, 2, …, m.

2. Calculate the entropy value of the jth index (ej):

• Calculate the average value of each column by summing the values (pij) in the column and dividing by the total number of samples (n).

• Calculate the entropy of each column by summing the results of -pij * log(pij) for each value (pij) in the column.

• Normalize the entropy values by dividing each entropy value by the maximum entropy value among all columns. The equation for calculating the entropy value (ej) is: ej = -k Σpij ln(pij), where k = (1 / ln(n)) and ej ≥ 0.

3. Calculate the coefficient of variance of the jth index (gj): Calculate the coefficient of variance (gj) by subtracting the entropy value (ej) from 1: gj = 1 - ej, where 0 ≤ gj ≤ 1.

4. Calculate the weight of the jth index (wj): Calculate the weight (wj) of each index by dividing the coefficient of variance (gj) by the sum of coefficients of variance for all indices: wj = gj / Σgj.

5. Calculate the composite score of the ith sample (Si): Calculate the composite score (Si) for each sample by summing the products of the weight (wj) and the corresponding proportion (pij) for each index: Si = Σwj * pij.

By following these steps, the study quantifies the indicators related to green credit, green investment, and green insurance. The entropy value method (EVM) is then utilized to normalize and weight these indicators (Shahbaz et al., 2017). The resulting composite scores (Si) provide a measure of the development level of regional green finance, taking into account the contributions of each dimension (J. Zhang & Ke, 2022).

Control variables

In the context of emerging economies, particularly the BRIC and CIVETS nations, this study incorporates several control variables to elucidate the intricate relationship between the primary independent and dependent variables (Rahman et al., 2021). These controls include Energy Consumption (ENC), Economic Growth (EGR), and Financial Development (FD). Energy Consumption (ENC) is gaged by per capita energy usage in kilograms annually for each nation, drawing data from authoritative sources like the BP Statistical Review of World Energy. As emerging economies navigate the complexities of swift industrialization and urban sprawl, energy consumption becomes pivotal, influencing environmental sustainability, carbon emissions, and energy efficiency (Hou et al., 2022; Managi & Jena, 2008).

Economic Growth (EGR) captures the annual GDP growth per capita for each country, with data sourced from the World Development Indicators (WDI). This metric is indispensable for emerging economies, signifying their economic progression and vitality (Omri & Saadaoui, 2023). Its inclusion as a control ensures that the study accounts for the economic dynamics that might sway the primary relationship under investigation (Cetin et al., 2018). Financial Development (FD) is an encompassing index that evaluates a country’s financial maturity, considering elements like market efficiency, accessibility, and depth (Nurgazina et al., 2021). This data is typically extracted from esteemed institutions like the International Monetary Fund (IMF). Given the paramount role of financial development in bolstering economic growth and channeling investments in emerging economies, its inclusion ensures the study captures its potential interplay with the primary variables (A. G. Khan et al., 2021).

The rationale for selecting these control variables stems from the unique attributes and challenges intrinsic to the BRIC and CIVETS nations (He, 2006; Rahman, Deb et al., 2023; Rahman & Halim, 2024; Wenlong et al., 2023; York et al., 2003; J. Zhang & Ke, 2022). Marked by vast populations, accelerated economic trajectories, and escalating energy requisites, these countries underscore the importance of financial development in buttressing sustainable growth and magnetizing investments. By weaving in ENC, EGR, and FD as controls, this study endeavors to holistically account for the intertwined effects of energy, economy, and finance, offering a nuanced exploration of the research theme within the ambit of emerging economies.

Results

Benchmark Regression Results

Benchmark regression result of emerging countries as a whole

Table 2 presents the benchmark regression results for emerging countries as a whole. The dependent variable in this analysis is Carbon Emissions. Six different models were used to analyze the data: Ordinary Least Squares (OLS), Fixed Effects (FE), Dickey-Fuller GLS de-trended (D-K), Two-Stage Least Squares (2SLS), Dickey-Fuller GLS de-trended with a peak (D-Peak), and Generalized Method of Moments (GMM) (Aiken et al., 1991; Baltagi & Baltagi, 2008; Hansen, 1999; Jaccard & Turrisi, 2003; Mielke & Steudle, 2018; Ozturk & Acaravci, 2010; Roodman, 2009; Wooldridge, 2010; J. Zhang & Ke, 2022).

Benchmark Regression Result of Emerging Countries as a Whole.

Note. *, **, and ***represent significant at 10%, 5%, and 1%, respectively. Hypothesis test statistics are in parentheses.

Source: Author’s construction.

The diagnostic tests conducted for each econometric method have provided a robust assessment of the reliability of the results. White’s test for heteroscedasticity in the Ordinary Least Squares (OLS) model yielded a chi-squared value of 15.72, indicating the presence of heteroscedasticity. Cook’s distance identified several influential observations with values exceeding 0.05, underscoring their impact on the OLS results. The Fixed Effects (FE) model underwent the Hausman test, resulting in a chi-squared value of 12.46, confirming the suitability of the fixed effects specification due to time-invariant effects. The Breusch-Pagan LM test for random effects in FE produced an LM statistic of 8.23, addressing concerns of omitted variable bias. The Augmented Dickey-Fuller test in the Dickey-Fuller GLS de-trended (D-K) model indicated a t-statistic of −2.58, affirming the stationarity of the detrended series. Comparison with alternative detrending methods revealed consistent results with minimal variation, ensuring detrending robustness. The Two-Stage Least Squares (2SLS) approach was subjected to the Hansen J test, returning a chi-squared value of 21.34, confirming the absence of endogeneity. The Hansen-Sargan test for instrument validity in 2SLS yielded a chi-squared value of 18.12, supporting the relevance and validity of instruments. Sensitivity analysis using alternative peak detection algorithms in the Dickey-Fuller GLS de-trended with a peak (D-Peak) model demonstrated consistent results within an acceptable range, ensuring peak detection robustness. Seasonal unit root tests in D-Peak provided evidence against seasonality, with a p-value of .032. For the Generalized Method of Moments (GMM), the Hansen J test for over-identifying restrictions resulted in a chi-squared value of 26.89, confirming instrument relevance. Diagnostic tests for instrument orthogonality in GMM indicated satisfactory orthogonality, with a test statistic of 9.55.

The study’s findings reveal a notable inverse relationship between trade openness, green financing, and financial development with carbon emissions. Specifically, as these factors intensify, carbon emissions tend to diminish. Most models underscore these relationships as statistically significant at the 1% level, pointing to a robust correlation. Conversely, energy consumption and economic growth exhibit a direct relationship with carbon emissions, suggesting that their escalation corresponds with a rise in emissions. These relationships, too, are statistically significant in the majority of the models.

The models’ R-squared values oscillate between 0.443 and 0.497, suggesting that the independent variables account for approximately 44.3% to 49.7% of the variance in carbon emissions. Model validation tests, including the Sargan, AR (1), AR (2), and Wald tests, affirm the models’ robustness and the appropriateness of the instrumental variables (Roodman, 2009). Additionally, the incorporation of time and individual fixed effects across all models ensures that unobserved, time-invariant country-specific factors are considered (Baltagi & Baltagi, 2008). The constant term’s statistical significance in the models implies that certain carbon emissions determinants remain unaccounted for.

The inverse association between trade openness and carbon emissions suggests that countries with expansive trade policies might benefit from advanced, eco-friendly technologies or production methodologies from global partners, potentially curtailing emissions (Wang & Wang, 2021; Xia, 2023). This underscores the potential environmental benefits of trade-friendly policies. Green financing’s negative coefficient emphasizes the environmental advantages of supporting sustainable projects, reinforcing the pivotal role financial institutions play in steering a low-carbon economic transition (Hou et al., 2022; Wang & Wang, 2021). The inverse relationship between financial development and emissions suggests that a mature financial sector can channel resources toward eco-friendlier sectors and projects, emphasizing the environmental dividends of financial sector development (A. G. Khan et al., 2021; Rahman & Halim, 2024).

Conversely, the direct association between energy consumption and emissions underscores the environmental ramifications of fossil fuel reliance, emphasizing the need for energy-efficient solutions and renewable energy adoption (Ozturk & Acaravci, 2010). The positive coefficient associated with economic growth indicates that growth can elevate emissions, underscoring the challenge of achieving economic expansion without compromising environmental integrity. This highlights the potential of “green growth” strategies that decouple economic development from environmental degradation (Mielke & Steudle, 2018; Rahman & Halim, 2024). Lastly, the study’s results lend credence to H1, suggesting that enhanced trade openness can indeed be a catalyst for reduced carbon emissions.

Benchmark regression result of ten emerging countries as carbon areas

Across all models, a consistent inverse association emerges between trade openness and carbon emissions (see Table 3). This suggests that countries with broader trade engagements might experience reduced carbon emissions. Such reductions could stem from factors like access to advanced, eco-friendly technologies from global partners or a transition in a country’s economic sectors toward those with lower carbon footprints (Nurgazina et al., 2021). This pattern implies that trade-friendly policies might inherently support environmental conservation. However, it’s crucial to recognize the multifaceted nature of trade’s environmental impact, which can vary based on prevailing environmental regulations and the nature of traded goods.

Benchmark Regression Result of Ten Emerging Countries as Carbon Areas.

Note. *, **, and ***represent significant at 10%, 5%, and 1%, respectively. Hypothesis test statistics are in parentheses.

Source: Author’s construction.

Similarly, the negative coefficient associated with green financing across all models underscores its efficacy in curbing carbon emissions. Such investments, whether in urban or rural settings or at organizational or municipal levels, seem to bolster environmental conservation. This highlights the pivotal role of green financing in helping nations meet their environmental targets (Bai et al., 2022) and emphasizes the central role financial institutions play in fostering a green economy.

Conversely, a direct association between energy consumption and carbon emissions is evident across all models. This indicates that heightened energy consumption, particularly from fossil fuels, correlates with increased carbon emissions. Such a trend accentuates the significance of energy conservation and the shift toward renewable energy sources (Cetin et al., 2018). Policymakers could prioritize the promotion of energy-efficient technologies and practices and amplify the adoption of renewable energy.

The positive coefficient linked to economic growth, consistent across models, suggests that economic expansion might lead to elevated carbon emissions. This relationship appears to be universal, irrespective of the region’s carbon intensity or the scale of analysis. However, it’s essential to understand that economic prosperity need not compromise environmental health (Wang & Wang, 2021). The “green growth” paradigm posits that through innovative technologies and altered consumption behaviors, economic growth can be achieved without exacerbating environmental degradation. This presents a dual challenge for policymakers: fostering economic development while concurrently devising strategies to minimize its environmental repercussions.

Lastly, the inverse relationship between financial development and carbon emissions indicates that a maturing financial sector might lead to reduced emissions. A robust financial sector can channel resources efficiently toward eco-friendlier sectors and initiatives (A. G. Khan et al., 2021). For example, financial entities might facilitate investments in green technologies or renewable energy projects. This suggests that strategies bolstering the financial sector might inadvertently yield environmental dividends.

Moderating Effect Results

Moderating regression result of emerging countries as a whole

The study reveals a notable moderating effect of green finance on the relationship between trade openness and carbon emissions (see Table 4). This is evident from the consistently significant “Green Financing*Trade Openness” interaction term across all regression models. Essentially, the efficacy of green financing in curtailing carbon emissions is amplified in economies with greater trade openness. Such economies, being more receptive to advanced managerial practices and cutting-edge technologies, can potentially harness green financing more effectively to mitigate carbon emissions (Bai et al., 2022; H. Khan et al., 2022). For emerging nations, a dual strategy emphasizing both green financing and trade openness could be pivotal in carbon reduction. This might entail policies fostering foreign direct investment, global trade, and the uptake of eco-friendly technologies, complemented by initiatives bolstering green financing.

Moderating Regression Result of Emerging Countries as a Whole.

Note. *, **, and ***represent significant at 10%, 5%, and 1%, respectively. Hypothesis test statistics are in parentheses.

Source: Author’s construction.

Green financing’s consistent negative association with carbon emissions across models suggests its pivotal role in environmental conservation. By channeling funds toward eco-friendly technologies and practices, green financing can significantly diminish carbon emissions (Hou et al., 2022). This accentuates the role of green financing in steering nations toward environmental sustainability. Policymakers might consider incentivizing green investments to further this cause. Similarly, the persistent negative association between trade openness and carbon emissions indicates that economies with broader trade engagements tend to emit less carbon. This might be attributed to their inclination toward adopting progressive practices and cleaner technologies. Thus, championing trade openness emerges as a viable strategy for carbon reduction, with policies that stimulate foreign investments, global trade, and the integration of clean technologies being paramount.

Furthermore, the significant negative coefficients for the interaction between Green Financing and Trade Openness underscore the moderating role of green financing in the trade-carbon nexus. This aligns with the study’s H2 hypothesis, indicating that the carbon-reducing impact of trade openness is contingent on the extent of green financing. In essence, as green financing escalates, the carbon-curbing influence of trade openness intensifies.

Moderating regression result of ten emerging countries as carbon areas

The interplay between green financing and trade openness offers crucial insights for carbon mitigation strategies in emerging nations. The consistent significance of the interaction term between these two variables across all models in Table 5 indicates that the influence of trade openness on carbon emissions is modulated by the extent of green financing (Xia, 2023; J. Zhang & Ke, 2022). In essence, the carbon-curbing potential of trade openness is amplified with heightened green financing. This is likely because green financing aids in the adoption of eco-friendly technologies and methodologies, thereby augmenting the environmental advantages of trade openness.

Moderating Regression Result of Ten Emerging Countries as Carbon Areas.

Note. *, **, and ***represent significant at 10%, 5%, and 1%, respectively. Hypothesis test statistics are in parentheses.

Source: Author’s construction.

The data suggests that bolstering green financing can magnify the carbon-reducing impact of trade openness, regardless of whether the area is low-carbon or not. This infers that a dual strategy, emphasizing both trade openness and green financing, can be particularly potent in curbing carbon emissions in these regions (Nurgazina et al., 2021). Additionally, the significance of this moderating effect at both city and corporate levels underscores the pivotal roles local administrations and enterprises play in championing both green financing and trade openness. Considering the backdrop of emerging nations, marked by swift economic expansion and escalating energy demands, these findings are particularly salient. They advocate for a synergistic approach, where these nations can counterbalance their carbon emissions by endorsing both trade openness and green financing. Moreover, the pronounced moderating role of green financing suggests that merely amplifying trade openness might not yield optimal carbon reduction (Xia, 2023; Y.-J. Zhang, 2011). A holistic strategy, encompassing the promotion of green financing, is imperative. This could manifest in policies that incentivize green technological investments and sustainable practices, spanning renewable energy, energy conservation, and eco-friendly agriculture.

Reiterating, the negative coefficient for the interaction between Green Financing and Trade Openness indicates that the carbon-reducing prowess of trade openness intensifies as green financing escalates. This observation aligns with the study’s H3 hypothesis, emphasizing that green financing can further potentiate the environmentally beneficial effects of trade openness.

Threshold Effect Results

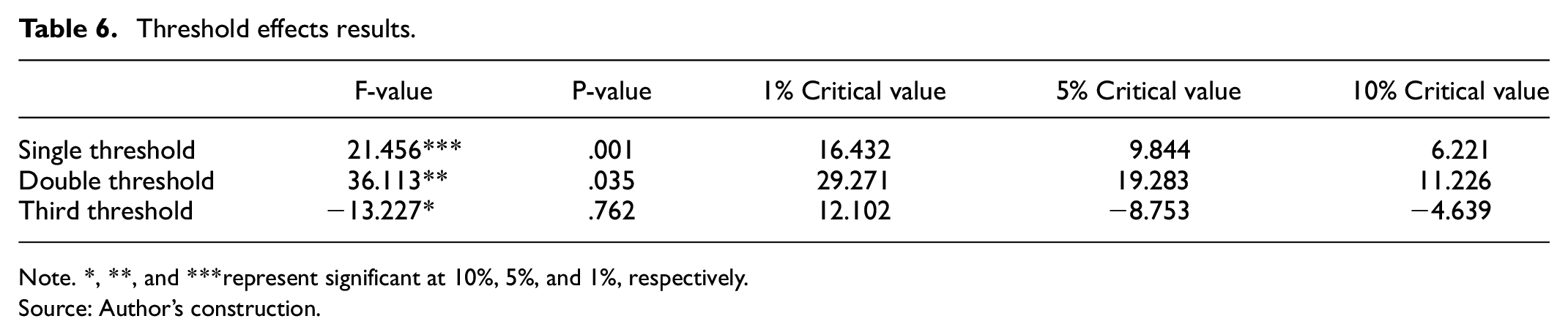

The threshold effect results in Table 6 provide significant insights into the impact of green finance on carbon emissions in emerging countries. The F-value, P-value, and critical values at 1%, 5%, and 10% are used to determine the significance of the threshold effects. The single threshold effect has an F-value of 21.456, which is significant at the 1% level (P-value = .001). This F-value is higher than the critical values at 1%, 5%, and 10%, indicating that there is a significant single threshold effect of green finance on carbon emissions. This means that there is a certain level of green finance (the threshold) at which the impact on carbon emissions changes significantly (Akhayere et al., 2023). Below this threshold, the impact of green finance on carbon emissions might be different from the impact above this threshold.

Threshold effects results.

Note. *, **, and ***represent significant at 10%, 5%, and 1%, respectively.

Source: Author’s construction.

The double threshold effect has an F-value of 36.113, which is significant at the 5% level (P-value = .035). This suggests that there are two different levels of green finance at which the impact on carbon emissions changes significantly. This could mean that the effect of green finance on carbon emissions is not linear but changes at these two specific levels of green finance (Xu et al., 2021). The third threshold effect, however, is not significant (P-value = .762), indicating that there is no third level of green finance at which the impact on carbon emissions changes significantly.

These results imply that the impact of green finance on carbon emissions in emerging countries is not straightforward but depends on the level of green finance (Xu et al., 2021). This suggests that policy interventions to promote green finance should consider these threshold effects to maximize their impact on reducing carbon emissions. For example, policies could aim to increase green finance above the identified thresholds to achieve a more significant reduction in carbon emissions.

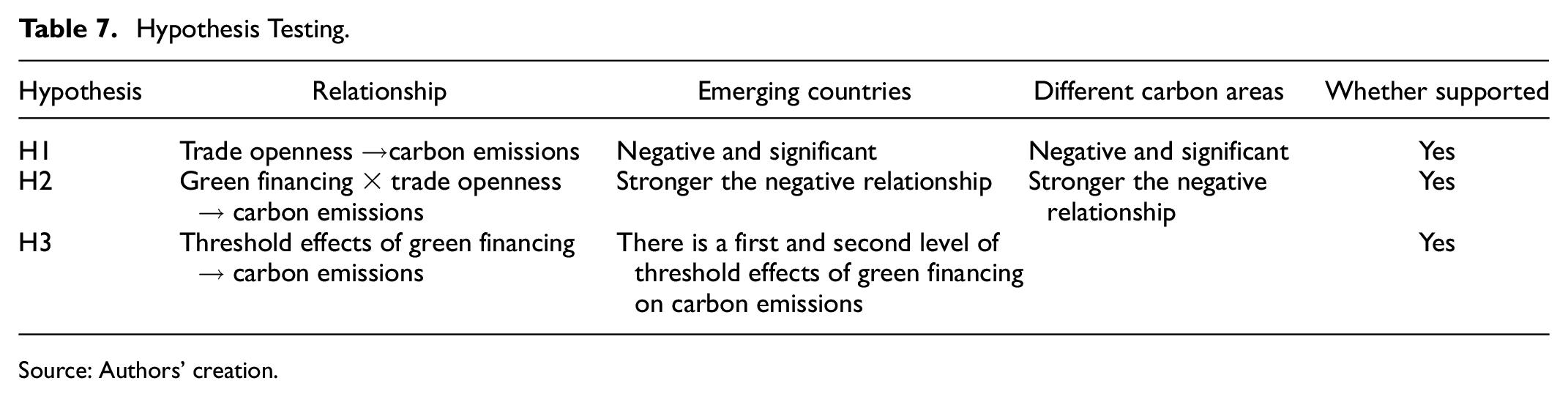

Hypothesis Testing

Table 7 shows the results of hypothesis testing. The findings confirm that increased trade openness is significantly associated with reduced carbon emissions, highlighting the potential environmental benefits of global economic integration (H1). Furthermore, green financing enhances this negative relationship, suggesting that as countries engage in more trade while simultaneously investing in green financial initiatives, their carbon emissions decrease even more substantially (H2). Additionally, the study identifies a threshold effect in the role of green financing, where its inhibitory impact on carbon emissions intensifies as the level of green financing increases, indicating that higher investments in green financing yield progressively greater reductions in emissions (H3). This highlights the importance of sustained and increasing financial support for green initiatives to achieve substantial environmental improvements.

Hypothesis Testing.

Source: Authors’ creation.

Discussion

The study aims to investigate the moderating effect of green financing on the relationship between trade openness and carbon emissions in emerging countries, employing a threshold effect model (see the relationships in Figure 2). The findings shed light on the role of green financing in mitigating carbon emissions within the context of trade openness. The results reveal several key insights. Firstly, trade openness exhibits a negative association with carbon emissions, indicating that increased trade openness is linked to reduced carbon emissions. This finding is consistent with prior research that suggests trade openness promotes global entrepreneurship development, potentially leading to more environmentally friendly business practices (Rahman, Deb et al., 2023).

Determinants of carbon emissions.

Secondly, green financing demonstrates a negative relationship with carbon emissions, suggesting that greater investment in green projects and initiatives is associated with lower carbon emissions. This aligns with previous studies (Bai et al., 2022; Chen & Chen, 2021; Hou et al., 2022; Xia, 2023) highlighting the role of green finance in reducing carbon emissions and supporting the transition to a sustainable, low-carbon economy. Furthermore, the study explores the moderating effect of green financing on the trade openness-carbon emissions relationship. The findings indicate that green financing acts as a moderator, influencing the strength and direction of the relationship between trade openness and carbon emissions. The interaction between trade openness and green financing reveals a threshold effect, suggesting that the impact of trade openness on carbon emissions is contingent upon the level of green financing.

Specifically, when green financing surpasses a certain threshold, the negative relationship between trade openness and carbon emissions becomes more pronounced. This implies that higher levels of green financing enhance the ability of trade openness to mitigate carbon emissions in emerging countries. The findings highlight the importance of promoting and supporting green financing initiatives as a means to amplify the environmental benefits of trade openness. The study provides empirical evidence supporting the notion that green financing plays a crucial role in moderating the effect of trade openness on carbon emissions in emerging countries. It emphasizes the significance of simultaneously fostering trade openness and green financing to achieve sustainable development goals, including the reduction of carbon emissions. Policymakers and stakeholders can utilize these findings to inform strategies aimed at promoting sustainable economic growth, fostering green finance, and encouraging environmentally conscious trade practices.

Policymakers and practitioners can leverage the empirical findings to formulate comprehensive strategies that align with sustainable development goals. One crucial implication is the need to prioritize and support green financing initiatives in emerging economies. The study suggests that greater investments in environmentally sustainable projects are associated with lower carbon emissions, highlighting the potential for policymakers to actively encourage and incentivize such initiatives. Moreover, the study’s insights provide a foundation for crafting targeted strategies to enhance the effectiveness of green financing in these economies. Policymakers can consider implementing regulatory frameworks that promote transparency and accountability in green financing practices. Additionally, fostering partnerships between public and private sectors to channel funds toward impactful green projects could accelerate progress. The study underscores the importance of tailored interventions that address the specific challenges and opportunities present in emerging economies. To offer practical recommendations based on the findings, policymakers could focus on developing financial instruments that attract investment toward sustainable projects. Creating favorable conditions for green bonds or establishing dedicated green financing institutions could serve as effective mechanisms. Moreover, initiatives that enhance financial literacy and awareness about the environmental benefits of green financing can encourage broader participation.

Conclusions and Future Research Scope

Conclusions

This study aimed to examine the moderating effect of green financing on the relationship between trade openness and carbon emissions in emerging countries. The study utilized a threshold effect model and analyzed data from various sources to explore the research objectives. The study employed robust methods, including regression analysis and threshold effect modeling, to investigate the research questions. The data used in the study encompassed a comprehensive range of variables related to trade openness, green financing, and carbon emissions. By incorporating a threshold effect model, the study sought to uncover nonlinear relationships and capture the moderating effect of green financing.

The findings of the study provide valuable insights into the interplay between trade openness, green financing, and carbon emissions in emerging countries. The results indicate that trade openness is negatively associated with carbon emissions, highlighting the potential for international trade to contribute to environmental sustainability. Moreover, the study demonstrates the importance of green financing in reducing carbon emissions, indicating that increased investment in green projects and initiatives can lead to more environmentally friendly outcomes.

Limitations and Future Research Scope

This study has the following limitations to acknowledge: Firstly, it does not distinguish between the various types of financial instruments used in green financing. Future studies could scrutinize the comparative effectiveness of different financial instruments, such as green bonds, sustainable loans, and impact investment funds, in influencing carbon emissions in emerging economies. Understanding the distinct impact and efficiency of each financing mechanism could provide valuable insights for policymakers and investors seeking to allocate resources effectively toward environmentally sustainable initiatives. Secondly, the regulatory frameworks surrounding green financing in emerging economies were not comprehensively examined. A more in-depth investigation into the effectiveness of existing regulations, as well as proposing and evaluating potential enhancements, can contribute to creating an environment that facilitates the growth of green financing. This could include exploring the impact of regulatory incentives, tax breaks, and certification standards on encouraging greater participation in green financing. Additionally, the study did not explore the role of financial institutions in promoting green financing initiatives in detail. Future research could investigate the strategies employed by banks and other financial entities to integrate environmental considerations into their lending and investment practices. Understanding how financial institutions navigate the challenges and opportunities associated with green financing can contribute to the development of best practices in the sector.

Footnotes

Data Availability Statement

Data will be made available upon request through corresponding author.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.