Abstract

This study examined the impact of renewable energy adoption on the attractiveness of Asian emerging economies to Foreign Direct Investment (FDI) amidst 2020s global economic upheavals. Utilising an Autoregressive Distributed Lag (ARDL) cointegration bounds testing approach to analyse data from 1971 to 2020, the findings revealed a significant positive correlation between renewable energy use and long-term FDI inflows, particularly in Indonesia and Malaysia. Furthermore, the analysis has shed light on the positive impact of rising real per capita income on FDI attractiveness in Malaysia and the Philippines, suggesting a multifaceted economic landscape influencing investment trends. This research has distinguished itself by demonstrating how renewable energy initiatives, alongside economic indicators, have significantly attracted FDI in Asian emerging markets. It has highlighted the ASEAN 4 countries, especially Indonesia and Malaysia, with their rich renewable energy resources and supportive policies, increasingly favoured by global investors. This study’s contribution has been novel in its focussed analysis of the interplay between renewable energy adoption and FDI attractiveness, offering insightful implications for policymakers and investors.

Plain language summary

This research looked into how using more renewable energy, like solar or wind power, can make Asian developing countries more appealing for foreign investments, especially during the economic challenges of the 2020s. By studying data from 1971 to 2020, it was found that countries using more renewable energy, especially Indonesia and Malaysia, tend to attract more long-term foreign investments. The study also found that the income level of people in a country and how open a country is to international trade play big roles in attracting foreign investment. This work stands out for showing that efforts in renewable energy, along with economic factors, make Asian emerging markets, particularly some ASEAN countries like Indonesia and Malaysia, more attractive to international investors. This research is unique in closely examining how adopting renewable energy affects a country’s ability to attract foreign investment, providing valuable insights for both policymakers and investors.

Introduction

In an in-depth analysis of global economic dynamics, recent findings by the International Monetary Fund (IMF) highlighted a substantial 3.5% contraction in the global Gross Domestic Product (GDP) for the year 2020, IMF (2021). This downturn was chiefly attributed to the disruptive ramifications of the COVID-19 pandemic. Despite these challenges, projections initially pointed towards a robust recovery, with anticipated global economic growth rates of 5.8% in 2021, 4.4% in 2022, and 4% in 2023. However, the persistent emergence of new COVID-19 variants underscored the complex challenges of global economic recovery, particularly affecting emerging markets and developing economies. This situation has raised critical concerns regarding long-term economic stability and growth, motivating an exploration into effective avenues for recovery, with a keen focus on the role of Foreign Direct Investment (FDI).

Expanding upon the Exogenous Growth Theory, which was pioneered by influential economists such as Swan (1956) and Romer (1994), it has been widely believed that FDI inflows have been crucial for the economic expansion of domestic economies given that FDI is not only a channel for importing valuable technology and expertise but has also played a pivotal role in spurring job creation, enhancing export capabilities, and contributing to global value chain spillovers in host countries (Ali & Hussain, 2017; Carkovic & Ross Eric, 2002; Dritsaki & Stiakakis, 2014). Moreover, the World Bank (2018) has emphasised the broader impacts of FDI, such as improving workforce skills, boosting productivity, stimulating local business growth, and creating better-paying job opportunities in developing nations. This multifaceted contribution of FDI has underscored its significance as a catalyst for socioeconomic development and global integration in the contemporary economic landscape.

In an environment characterised by such economic volatility, policymakers across the globe have been ardently focussing on leveraging Foreign Direct Investment (FDI) to rejuvenate their ailing economies. Recognising the transformative power of FDI in spurring economic progress within host countries, governments have been strategising to attract more foreign investment (Goh et al., 2020). Nevertheless, the pervasive impact of the pandemic has significantly disrupted the flow of FDI, resulting in a substantial worldwide contraction of 42%. According to the United Nations Conference on Trade and Development (UNCTAD, 2021), this has led to a marked decrease in global FDI inflows, plummeting from US$1.5 trillion in 2019 to approximately US$859 billion in 2020. This scenario has propelled policymakers across the globe to ardently focus on leveraging FDI as a pivotal strategy for economic rejuvenation, acknowledging its transformative power in spurring economic progress within host countries.

Conversely, there has been a significant shift towards renewable energy in the evolving landscape of energy sources, encompassing solar, wind, geothermal, hydro, and biomass. These sources offer environmentally sustainable alternatives to conventional finite and depletable energy sources like natural gas, oil, coal, or nuclear power. Notably, renewable energy has become increasingly cost-effective, offering an economically viable option for power generation. This situation has been evidenced by the 62% surge in global renewable power capacity in 2020, culminating in a total worldwide renewable energy capacity of 163 GW. The International Renewable Energy Agency (IRENA) projected that integrating renewable energy in 2021 could save approximately US$55 billion in global energy production expenses for 2022, surpassing the cost-effectiveness of even the least expensive fossil fuels. This shift is aligned with the investment motives that J. Dunning and Lundan (2008) identified, positioning renewable energy resources as strategic assets that could attract FDI. The integration of renewable energy is poised to address environmental sustainability concerns and catalyse economic strategies to attract FDI for more sustainable and long-term growth.

Implementing the Carbon Border Adjustment Mechanism (CBAM) in 2023, aimed at reducing carbon dioxide emissions by taxing imports of fossil fuels such as oil, coal, and gas, has been another critical development in the global energy landscape. This policy move has been anticipated to have far-reaching implications for multinational enterprises (MNEs) looking to minimise production costs or expand their export capabilities. Besides, the World Bank’s Global Competitiveness Survey (2017/2018) reported that 51% of surveyed Multinational Enterprise (MNE) executives cited that cost reduction was the primary motivation of MNEs for outward investment. Hence, countries with abundant renewable energy sources may have an advantage in attracting inbound FDI.

Extensive research has delved into the various factors influencing Foreign Direct Investment (FDI), presenting a range of perspectives on its key drivers. Economic indicators have been prominent. The study by Cevis and Camurdan (2007) emphasised the role of inflation, interest rates, and trade openness. Complementing this view, Kumari and Sharma (2017) underscored the importance of market size. Furthermore, Saini and Singhania (2018) highlighted economic growth, trade openness, and gross fixed capital formation, while Asongu et al. (2018) and Suleiman et al. (2013) pointed to market size and infrastructure availability as critical in attracting FDI. Despite these insights, the specific impact of renewable energy sources on FDI inflows has remained a relatively unexplored domain, presenting a unique opportunity for this study.

Given that Asia’s developing countries emerged as the only region to experience FDI growth in 2020 (ASEAN Investment Report, 2021) and considering the rising prominence of renewable energy as the most cost-effective energy source (IRENA, 2021). This paper has investigated the hypothesis that countries emphasising renewable energy investments may become increasingly attractive to efficiency-seeking MNEs, potentially leading to a surge in FDI inflows. To this end, the study employed the Autoregressive Distributed Lag (ARDL) cointegration bounds testing technique, allowing for a nuanced understanding of the interplay between renewable energy and FDI. This approach has contributed significantly to the ongoing academic and policy discussions, offering insights into the primary drivers influencing FDI inflows and providing a basis for informed policy-making and strategic planning.

The remainder of this paper is structured as follows: Section 2 provides an in-depth review of the theoretical background and empirical evidence from previous literature. Section 3 details the methodology and data sources utilised in this research. Section 4 presents the key findings from the analysis, followed by Section 5, which discusses the policy implications of the findings. Finally, Section 6 concludes the paper with a synthesis of remarks and suggests avenues for future research, aiming to enrich further the discourse on the nexus between renewable energy and FDI.

Background of the Study

The following sections explore two pivotal aspects shaping the economic and environmental landscapes of the ASEAN 4 countries: Indonesia, Malaysia, the Philippines, and Thailand. The analysis is twofold, beginning with a comprehensive assessment of renewable energy advancements while examining foreign direct investment (FDI) inflows. These elements are crucial for understanding the region’s trajectory towards sustainable development and global integration.

Comprehensive Analysis of Renewable Energy Progress in the ASEAN 4 Countries: Indonesia, Malaysia, Philippines, and Thailand

In Southeast Asia, a region traditionally driven by industrial growth, population increases, and escalating reliance on electrical technologies, there has been a significant surge in electricity demand, with more than a 6% annual increase witnessed in the past two decades (International Energy Agency (IEA), 2020). Key nations in Southeast Asia such as Indonesia, Thailand, and Malaysia, which collectively account for more than 60% of the region’s electricity consumption, have spearheaded a shift towards renewable energy. This transition is evidenced by the ASEAN region’s target to integrate 23% of renewable energy into its energy mix by 2025, diverging from its historical coal-dominated generation (IRENA, 2017). Various initiatives and policy incentives have been implemented to support this commitment, boosting domestic and international renewable energy investments. Indonesia, for instance, aims to increase its renewable energy share to 23% by 2025 and 31% by 2050 (IRENA, 2017). In parallel, Thailand and Malaysia have laid out comprehensive renewable energy adoption plans, with Thailand aiming for a 29% contribution of renewable energy to its total electricity generation by 2037 and Malaysia targeting 31% renewable energy in its installed capacity by 2025, with a further goal of 40% by 2035 (The Edge, 2021). Additionally, the Philippines strives for a 50% renewable share in electricity generation by 2030, equivalent to approximately 15.3 GW (France-Presse, 2011). These initiatives, as depicted in Figure 1, indicate a growing reliance on renewable energy sources across these nations, with the Philippines leading in renewable energy percentages and the other countries showing a clear upward trend.

Share of energy from renewable sources of the ASEAN 4 countries.

Renewable Energy Policies in Indonesia, Thailand, Malaysia, and the Philippines

Southeast Asia is undergoing a significant transition towards renewable energy as part of its efforts to achieve global climate goals and support sustainable economic development. This section provides an overview of the renewable energy policies in Indonesia, Thailand, Malaysia, and the Philippines, focussing on the distinctive approaches, key policies, and progress each country has made in advancing renewable energy adoption.

Indonesia

Indonesia is implementing comprehensive renewable energy policies aiming to increase the share of renewables in its energy mix to 23% by 2025. The focus is on geothermal, hydro, solar, and biomass energy. The Just Energy Transition Partnership (JETP) was launched with a $20 billion investment plan to support clean energy projects, involving significant contributions from international partners (IEA, 2023a; The Diplomat, 2023). The country is also enhancing its grid infrastructure to integrate renewable energy sources and reduce transmission and distribution losses (McKinsey & Company, 2023). Recent legislative changes and market liberalisation have further spurred the growth of renewable energy in Indonesia, attracting private sector investment and improving the regulatory framework to facilitate these investments. Indonesia is also focussing on extending electricity access to rural and remote areas through small-scale, off-grid solutions like solar panels and micro-hydro plants. Overall, these efforts highlight Indonesia’s commitment to leveraging its renewable energy potential to reduce emissions and enhance energy security.

Thailand

Thailand is accelerating its renewable energy transition with the goal of increasing the share of renewables in its power generation mix to 51% by 2037, up from 20% in 2023. This shift is part of the revised Power Development Plan (PDP) for 2024 to 2037, which also aims to reduce reliance on natural gas from 57% to 41% and coal from 20% to 7%. The additional renewable power will predominantly come from solar energy, supplemented by wind, biomass, biogas, floating solar panels, waste-to-energy projects, mini-hydropower plants, geothermal power, and imported renewable electricity from neighbouring countries (Turner, 2024). The Thai government has launched its largest feed-in tariff programme to date, aiming to double wind and solar capacity by 2030. Additionally, Thailand plans to auction 3.67 GW of renewable capacity later this year, building on the 5 GW of renewables already planned for procurement (Connor, 2023). The country’s focus on renewables is part of a broader strategy to achieve net-zero greenhouse gas emissions by 2065 and carbon neutrality by 2050. To meet these goals, the PDP includes measures to replace a portion of gas fuel with hydrogen, aiming for a 20% hydrogen mix between 2035 and 2037 (IEA, 2023b).

Malaysia

Malaysia has set ambitious targets to increase the share of renewables in its power mix to 70% by 2050, as part of its broader commitment to achieving net-zero emissions by the same year. Key initiatives include the Large Scale Solar (LSS) programme and the establishment of a renewable energy exchange. The country is focussing on solar energy, grid infrastructure improvements, and energy storage technologies. Policy incentives and regulatory reforms are in place to create a conducive investment environment for renewable energy projects (Anisa & Amirulddin, 2023; IRENA, 2023; MIDA, 2023; W. Rajah et al., 2024; The Edge, 2023). Solar energy is set to play a predominant role in Malaysia’s renewable energy strategy, with substantial investments aimed at boosting solar PV capacity. The country expects to see significant reductions in emissions and cost savings of between USD 9 billion and USD 13 billion annually by 2050, thanks to avoided energy, climate, and health costs (IRENA, 2023). Malaysia’s approach includes the lifting of the ban on renewable energy exports, which is expected to further boost the local renewables sector and benefit neighbouring countries (The Edge, 2023). The government is also promoting the development of a robust renewable energy industry value chain and encouraging private sector investment through various incentives, such as corporate income tax holidays, enhanced deductions, and preferential tax rates (Anisa & Amirulddin, 2023).

The Philippines

The Philippines aims to achieve a 35% renewable energy share in its power generation mix by 2030 and 50% by 2040. Significant policy reforms have been enacted, including amendments to the Renewable Energy Act that allow full foreign ownership of renewable energy projects. The Green Energy Auction Programme (GEAP) and other initiatives are boosting renewable capacity, with a focus on solar and wind power. The National Renewable Energy Programme (NREP) outlines strategic targets for various renewable sources, aiming to increase geothermal, hydropower, wind, and biomass capacities (ASEAN Briefing, 2023; Department of Energy, 2023; Enerdata, 2023). The DOE has launched the Green Energy Auction Programme to boost renewable energy capacity, targeting the installation of nearly 2 GW of new solar capacity in 2024 (pv magazine, 2024). The Philippines is heavily focussing on solar energy, expecting significant investments in both solar PV installations and battery storage systems. This expansion is part of a broader goal to install 15 GW of clean energy by 2030 (pv magazine, 2024). Additionally, the liberalised energy market and recent legislative reforms have made the Philippines an attractive destination for renewable energy investments, further supported by various government incentives and regulatory changes (ASEAN Briefing, 2023).

FDI Inflows to the ASEAN 4 Countries

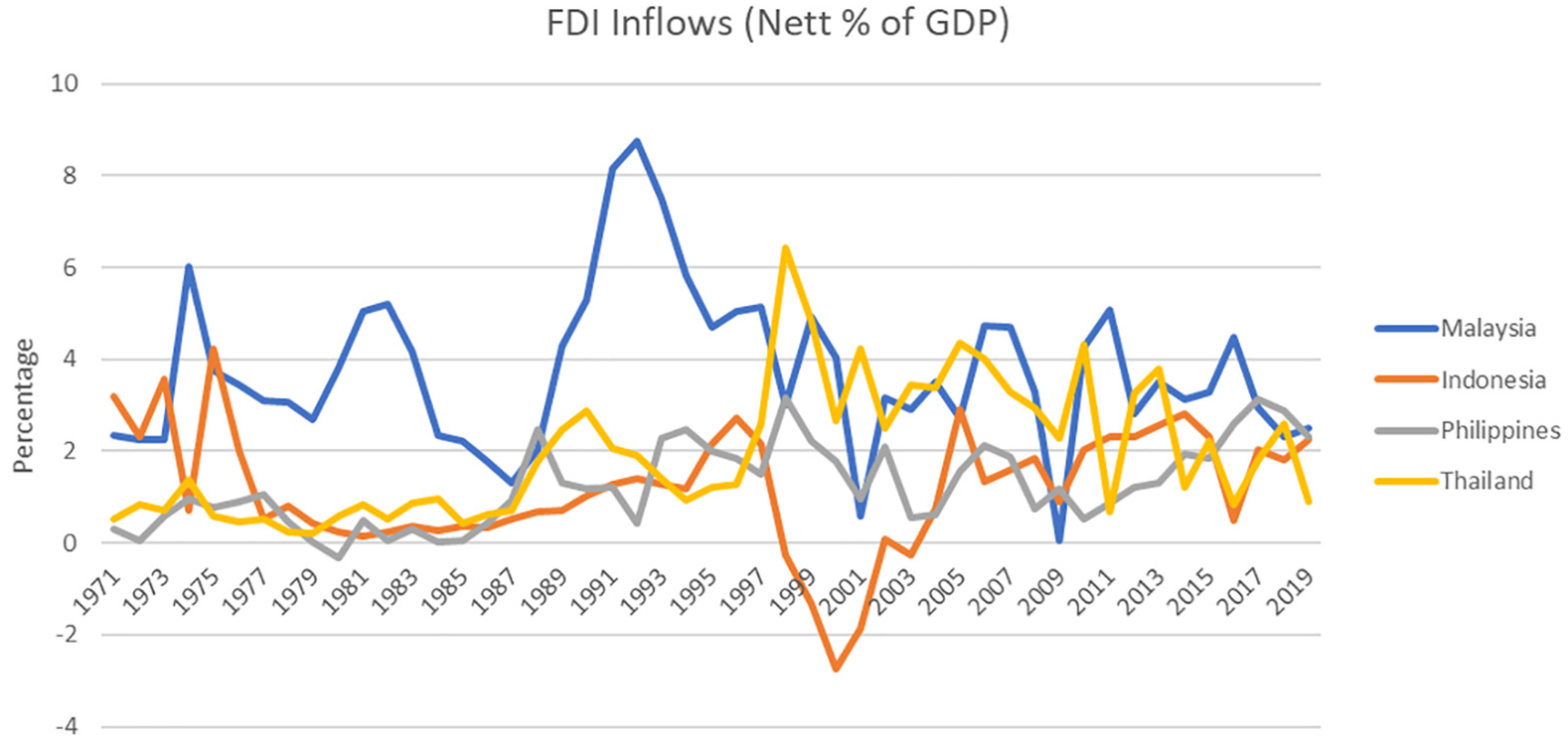

Before the COVID-19 crisis, as shown in Figure 2, ASEAN countries saw significant growth in Foreign Direct Investment (FDI), with a 5% increase in inflows in 2019, reaching US$156 billion. Substantial investments in nations such as Singapore, Indonesia, and Vietnam mainly drove this growth. Singapore experienced a notable 16% increase from the previous year, attracting US$92 billion. This surge has highlighted the ASEAN region’s growing attractiveness as an investment destination, supported by favourable policies, a strategic location, and burgeoning markets. However, 2020s COVID-19 pandemic led to considerable economic challenges, causing a sharp 31% decline in ASEAN’s FDI inflows to US$107 billion. This downturn mirrored broader global economic disruptions, including lockdowns, supply chain issues, and heightened uncertainties. Each country within the ASEAN 4 (Indonesia, Malaysia, Thailand, and the Philippines) faced different levels of FDI reductions. Thailand experienced the most significant drop, primarily due to a major deal involving a Thai investor group’s acquisition of Tesco’s Southeast Asian business. This period underscored the importance of adaptive strategies in ASEAN for enhancing economic resilience, diversifying investment sources, and creating environments conducive to sustainable FDI, particularly in the post-pandemic recovery stage (UNCTAD, 2021).

FDI inflows (Nett % of GDP) of the ASEAN 4 countries.

Literature Review

The following section presents the theoretical background of this study, followed by relevant empirical evidence.

Theoretical Background - Eclectic Paradigm

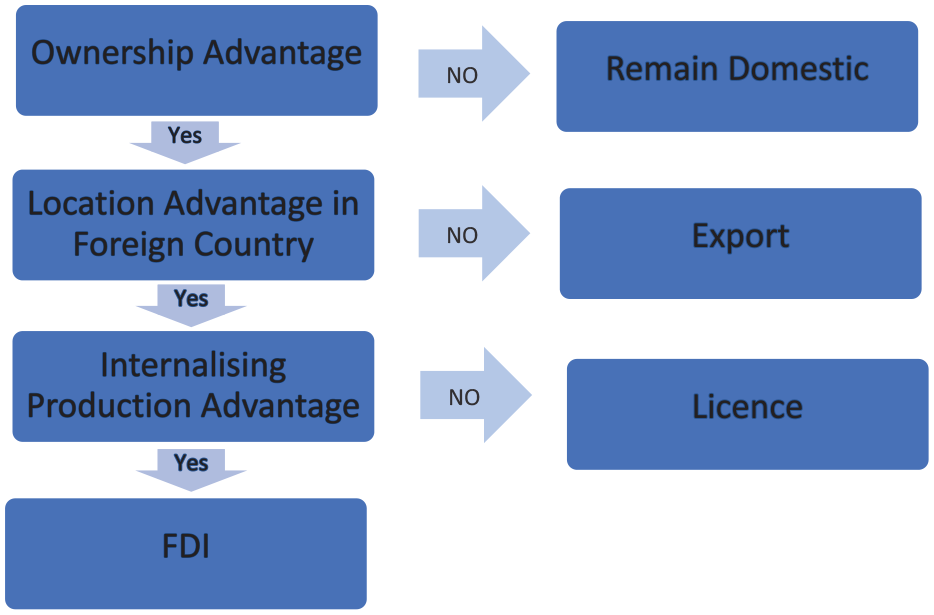

John Dunning’s Eclectic Paradigm, introduced in 1980 (J. H. Dunning, 1980), has long been a cornerstone in understanding foreign direct investment (FDI), particularly in the context of renewable energy-rich countries. This paradigm offers a multifaceted view of FDI decision-making by integrating the OLI (Ownership, Location, and Internalisation) framework. However, the global economic landscape has undergone seismic shifts since its inception, especially with digital technology and globalisation. These shifts have necessitated a critical re-examination of the paradigm’s applicability in today’s interconnected and digitally driven world, particularly in addressing the rapidly changing dynamics of international business and investment strategies.

As the paradigm defines, ownership advantages are pivotal in endowing firms with a competitive edge in foreign markets. Traditionally, this referred to tangible assets and proprietary technologies. However, in today’s digitised and knowledge-based economy, ownership extends to digital assets, innovative capabilities, and brand equity. This evolution compels a broader and more dynamic interpretation of ownership advantages. It underscores the importance of intellectual capital and the strategic management of digital resources, which are increasingly crucial for gaining a competitive advantage in global markets.

The concept of location advantages, initially centred around physical and economic factors, has also been evolving. While traditional elements such as geographical proximity, natural resources, and labour costs remain relevant, the digital era has introduced new factors like digital infrastructure, connectivity, and data accessibility. In renewable energy, location advantages also encompass environmental policies, sustainable practices, and green technology innovations. These shifts highlight the need for a more holistic approach to evaluating location advantages that balance traditional economic considerations with modern environmental and digital priorities.

Internalisation, the process of managing cross-border operations, has gained new dimensions with the rise of global supply chains and digital platforms. Decision-making processes now involve cost-benefit analyses and strategic considerations of supply chain resilience, technological integration, and global market dynamics. In the renewable energy sector, this could mean navigating complex international regulations and adapting to diverse energy markets. The traditional view of internalisation, focussed primarily on cost efficiencies, must now account for these broader strategic considerations, emphasising agility, adaptability, and long-term sustainability in a globally interconnected landscape.

In summary, Figure 3 elucidates the strategic decision-making process of a multinational enterprise (MNE) based on the Eclectic Paradigm when contemplating overseas investment. The model posits that an MNE will commit to international investment if it possesses three principal advantages: ownership, location in the foreign country, and internalisation of production. Without these concurrent advantages, the company is more inclined to remain domestic, concentrating on domestic operations or merely exporting its products. Conversely, if there is a lack of internalisation advantage in production, the MNE might consider alternative strategies, such as franchising, by selling its licence overseas. This decision-making framework assists MNEs in assessing the most feasible strategy for international expansion, tailored to their unique strengths and market dynamics. In addition, while Dunning’s Eclectic Paradigm lays a foundational framework for understanding FDI, the ongoing transformations in digital technology, global supply chains, and environmental sustainability call for an updated approach to the paradigm. This new perspective should incorporate the evolving nature of ownership in the digital age, the expanding definition of location advantages in a connected world, and the complex strategic considerations in internalisation decisions. As such, the intersection of FDI and renewable energy sources has become a vibrant field for ongoing research and policy development.

The eclectic paradigm.

Numerical Foundation Underlying the Theoretical Principles

J. Dunning and Lundan (2008) highlighted that MNEs were motivated primarily by what they perceived to be in the interests of their direct stakeholders, who must be reimbursed for their contributions to the production process by an amount at least equal to the opportunity cost of the resources and capabilities they provided (maximisation of profits). Their argument can be expressed as:

Where

Where r is the maximum income a firm can earn through reinvesting profits earned in years 1 and 2, assuming that the owner’s investment stake does not change independently of the profits made, however, with an appreciation or depreciation of property values or changes in the future earning capacity of the firm, Equation 2 would need to be modified as follows:

And

The formula to achieve the objectives of wealth-maximising firms, assuming a 3-year period, is as follows:

Where NPV is the net present value of the expected income of a firm at time t = 3, Y is the net expected income of a firm in times 1, 2 and 3, and r is the opportunity cost of K invested in a firm to earn that income.

Therefore, the profit maximisation of a firm with foreign direct investment (FDI) would be subject to the following condition:

Where fp is the profit due to an MNE’s activity, f indicates the foreign affiliate, and r is the other producing units of the MNE. However, due to differences in the perceptions of MNE’s decision-makers towards incentive structures and risk-taking, some firms may place a higher value on the risk-spreading opportunities or cultural sensitivities of FDI than others. This situation suggests that some firms may produce outside their national boundaries as part of a coherent and coordinated global asset-exploiting-and-seeking competitive strategy rather than simply earning profits on a specific FDI.

Accordingly, J. Dunning and Lundan (2008) indicated four main reasons motivating firms to engage in FDI, summarised in Table 1.

The Four Main Motivations for FDI (J. Dunning and Lundan, 2008).

Literature Review

The extensive literature regarding Foreign Direct Investment (FDI) inflows has traditionally centred around various economic and socio-political factors. Studies such as those by Ang (2008) and Choong and Lam (2010) have underscored the importance of GDP growth, financial development, and trade openness in driving FDI, particularly in Malaysia’s Electronic and Electrical (E&E) sector. This focus on economic growth and trade openness as pivotal drivers is a recurring theme. Tang et al. (2014) further correlated these factors with FDI inflows, emphasising sector-specific nuances in the E&E sector. This situation has highlighted the multifaceted nature of FDI determinants, showcasing their diverse impacts across sectors and economic contexts.

In parallel, the existing literature has revealed a stark contrast in FDI determinants between developed and developing countries. Research by Saini and Singhania (2018) and Antonakakis and Tondl (2015) highlighted distinctive factors driving FDI inflows in these regions. In developed countries, traditional aspects like GDP growth and trade openness play a significant role, while in developing countries, domestic investment and efficiency levels are more influential. This distinction is pivotal for tailoring policy formulation and investment strategies to different economic settings. It underscores that a country’s attractiveness to foreign investors depends on its economic size or growth prospects, business environment, and operational efficiency.

More recently, there has been an increasing focus on the role of broader socioeconomic factors in influencing FDI. The studies by Kapuria and Singh (2019) and Immurana (2021) have expanded the research scope to include variables such as corruption control, life expectancy, and health indicators. This shift towards integrating socioeconomic factors has indicated a recognition of the complex interplay between the economic and social determinants of FDI. Sharma and Kautish (2020) introduced the concept of asymmetry in the relationships between macroeconomic determinants and FDI in India, suggesting nonlinear impacts of economic factors on FDI, thus adding complexity and necessitating more sophisticated analytical approaches.

Moreover, Wahyudi and Palupi (2023) highlighted the reciprocal relationship between energy consumption and Foreign Direct Investment (FDI) within OECD nations. In contrast, Dang and Nguyen (2021) and Kurtović et al. (2020) identified factors such as economic growth, GDP per capita, urbanisation, the engagement of foreign businesses in the service sector, and service industry employment levels as crucial determinants for FDI location preferences. These insights aligned with the observations of Camarero et al. (2019), who underlined the significance of economic potential, competitive edge, regional agglomerations, and productive capacities in choosing Spanish territories for FDI. Additionally, Alrubaiat (2024) pointed out that in Jordan, factors such as the gross domestic product, worker compensation, and the extent of the industrial market boosted FDI inflows. In contrast, political instability and high taxes deterred them.

However, despite this extensive research, there remains a notable gap in understanding the impact of environmental sustainability, particularly the role of renewable energy, on FDI inflows. In an era increasingly focussed on environmental concerns, the extent to which a country’s energy policies and practices, especially the adoption of renewable energy, influence FDI decisions is a critical yet underexplored area. This gap is particularly relevant in the global shift towards sustainable development and climate change mitigation. Investigating this area could offer significant insights, bridging the gap between environmental sustainability and economic investment decisions and potentially revolutionising the understanding of FDI determinants in the contemporary global context. In summary, while existing literature has extensively explored the economic and socio-political determinants of FDI, the influence of environmental factors, particularly the adoption of renewable energy, remains underexplored. This situation presents a significant opportunity for future research to contribute to a more holistic understanding of FDI dynamics, integrating economic, social, and environmental perspectives.

Data and Methodology

The current study adopted the autoregressive distributed lag (ARDL) bounds testing approach for its analysis, a method first introduced by Pesaran et al. (2001). This approach was meticulously selected to investigate the interactions between foreign direct investment (FDI) inflows and renewable energy, in the short and long term, within the framework of the ASEAN 4 countries. The ARDL approach was particularly advantageous for this research owing to its adaptability in analysing small sample sizes, its capacity to manage variables of differing degrees of integration, and its precision in delineating immediate and sustained connections. Consequently, the research model developed for this study was established as follows:

Where FDI represents the net inflows of foreign direct investment (nett FDI inflows (% of the GDP)), RNEW represents the share of energy from renewable sources, RGDPC is the real GDP per capita, and TO represents trade openness (Trade (% of the GDP)). The ARDL bounds testing cointegration model is shown below:

The selection of the optimum lag from the above ARDL model was based on the Akaike Information Criterion (AIC) and the Schwarz Bayesian Criterion (SBC). Each variable is as previously defined; in addition, β1, β2, β3, and β4 are the vectors of the long-run parameters to be estimated. While

The implementation of the ARDL Bounds testing analysis was executed through a sequential approach, adhering to the protocol suggested by Pesaran et al. (2001). This protocol was critical in ensuring that the ARDL models excluded any I(2) variables known to compromise F-statistics’ validity in cointegration tests. The Augmented Dickey-Fuller (ADF) and Philips-Perron (PP) unit root tests were applied to verify the stationarity of the variables, confirming that each variable was classified as either I(0) or I(1). The results of the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test further reinforced these findings, which corroborated the outcomes of the ADF and PP tests.

Subsequently, the error correction model was executed within the framework of the ARDL model to identify the optimal lags for the ARDL model. As Pesaran et al. (2001) suggested, ARDL cointegration bounds testing was conducted to detect cointegrating variables. A comparison was made with the critical values provided by Narayan (2005), considering the sample size comprised fewer than 100 observations, to assess the statistical significance of the obtained F-statistics.

Following the ARDL model, the long-run model was estimated based on the following restrictions:

The short-run Error-Correction Model (ECM) was estimated based on the following:

Additionally, the estimation was thoroughly examined for serial correlation and diagnostic stability tests, including CUSUM and CUSUM of Squares. To ensure the robustness of the findings, the variable “net FDI inflows (US$)” was employed as a stand-in for FDI inflows. This strategy was chosen to assess the effect of the ratio of energy obtained from renewable sources on the scale of FDI inflows into the ASEAN 4 countries.

Data

The present research concentrated on four specific nations within the Association of Southeast Asian Nations (ASEAN) region: Indonesia, Malaysia, the Philippines, and Thailand, commonly called the ASEAN 4 countries. The study’s examination was centred on yearly data from 1971 to 2020. The study utilised Net FDI inflows (% of GDP) with data sourced from the World Bank’s World Development Indicators (WDI) to gauge the extent of Foreign Direct Investment (FDI) inflows for the selected countries. The representation of renewable energy usage (RNEW) was approximated by the proportion of renewable energy consumption, with data extracted from the World Energy Outlook (WEO) database. Additionally, the present study considered the real gross domestic product per capita (RGDPC) and trade openness (TO), which measure the combined value of goods and services, exports and imports as a percentage of the gross domestic product. Data sets for these variables were also obtained from the World Development Indicators (WDI). Table 2 provides an overview of the statistical characteristics of these datasets.

Summary Statistics.

Note. FDI represents the Nett FDI inflows (% of GDP), RNEW represents the share of energy from renewable sources, RGDPC refers to the real GDP per capita, and TO represents trade openness.

Empirical Results

This section presents the findings of the empirical investigation, structured into five key areas. These include the Stationarity Test (4.1), Model Specification and Cointegration Analysis (4.2), Long-run Estimates and Short-run Dynamics (4.3), Robustness Check (4.4), and an examination of the Influence of Renewable Energy Policies on Attracting Foreign Direct Investment (4.5). Each subsection provides detailed insights and analyses pertinent to the study’s objectives.

Stationarity Test

Building on the foundational insights provided by Pesaran et al. (2001), the initial analysis recognised the challenges posed by I(2) variables in cointegration testing, particularly their impact on the accuracy of F-statistics calculations. Consequently, the study thoroughly examined each variable’s stationarity, utilising the Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) unit root tests. This two-pronged approach was designed to enhance the robustness of the preliminary findings. Additionally, the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test was employed as a supplementary measure, offering a contrasting perspective by testing the null hypothesis of stationarity instead of detecting the presence of a unit root. The combined results of these tests, as presented in Table 3, indicated that all variables under study were either integrated at order 0 (I(0)) or order 1 (I(1)), with no instances of I(2) integration observed. This alignment of results from the ADF, PP, and KPSS tests laid strong groundwork for the subsequent application of ARDL bounds testing.

ADF and PP Unit Root Test Results.

Note. FDI represents Net FDI inflows as a percentage of the GDP (% of GDP), RNEW represents the proportion of energy sourced from renewable sources, RGDPC signifies the real GDP per capita, and TO stands for trade openness. The coefficients shown are the T-statistics derived from the Eviews software application. In the Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) tests, the null hypothesis posits the existence of a unit root, while in the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test, the null hypothesis assumes stationarity. The test equation included both constant and trend terms, and the ADF test equation employed the SIC (Schwarz Information Criterion) to determine the optimal lag order. The significance levels are denoted by ***, **, and *, representing the 1%, 5%, and 10% significance levels, respectively.

Model Specification and Cointegration Analysis

Equation 8 reflects the model’s specifications, intricately derived through a general-to-specific approach, as Pesaran et al. (2001) advocated. To discern the presence of long-run cointegration, bounds testing F-statistics were utilised, adhering to Narayan’s (2005) guidelines for small samples. The criterion is clear: exceeding the upper bound critical value signals cointegration. Table 4 illustrates that this criterion was met across all countries in the sample, rejecting the null hypothesis of no cointegration between foreign direct investment (FDI) inflows and the share of renewable energy at the 1% significance level. This noteworthy finding corroborated the preset study’s theoretical framework, positing a robust long-term linkage between renewable energy and FDI, especially in their current cost-effectiveness. Additionally, this study employed the Breusch-Godfrey serial correlation LM statistics up to the fourth order, ensuring the robustness and adequacy of the model specification.

Long-Run Cointegration and Serial Correlation LM Test (Dependent Variable: FDI inflows (% of GDP)).

Note. The cointegration test statistics were contrasted with the critical thresholds outlined in Narayan (2005) study, focussing on sample sizes below 100 observations. Serial (1) and Serial (2) represent the Breusch-Godfrey LM test statistics without serial correction. The values in parentheses represent the corresponding p-values. The significance levels are denoted by *, **, and ***, indicating the 10%, 5%, and 1% significance levels, respectively.

Long-Run Estimates and Short-Run Dynamics

The analysis, as depicted in Table 5, unveiled a nuanced relationship between renewable energy and FDI in the ASEAN 4 countries. A notable divergence emerged: Indonesia and Malaysia exhibited a positive and significant correlation between renewable energy usage and FDI. This trend was conspicuously absent in the Philippines and Thailand. This differentiation underscored the heterogeneity among these economies. Furthermore, the role of per capita income (RGDPC) in attracting FDI, particularly in Malaysia and the Philippines, aligned with the market-seeking motivations of multinational enterprises, as theorised by J. Dunning and Lundan (2008). Additionally, trade openness emerged as a consistent and vital determinant of FDI across all selected countries, resonating with the Eclectic Paradigm’s principles.

ADRL Estimation Results (Dependent Variable: FDI Inflows (% of GDP)).

Note. FDI represents the Net Foreign Direct Investment Inflows as a percentage of the Gross Domestic Product (GDP; % of GDP). RNEW signifies the proportion of energy derived from renewable sources. RGDPC refers to the real GDP per capita, and TO stands for trade openness. The coefficients presented are the T-statistics obtained using the Eviews software application, with a maximum lag length of four considered. The urbanisation rate of Singapore was excluded from the model due to Singapore’s already high level of urbanisation. The optimal lag structure for the ARDL model was determined using the Akaike Information Criterion (AIC). The significance levels are denoted by ***, **, and *, indicating the statistical significance at the 1%, 5%, and 10% thresholds, respectively.

The second section details the short-term dynamics, presenting a different picture. In the short run, the impact of renewable energy on FDI within the ASEAN 4 countries was minimal. However, the considerable effect of real per capita income on FDI in Indonesia aligned with the results reported by Saini and Singhania (2018) and Antonakakis and Tondl (2015), underscoring the critical importance of a country’s economic robustness in attracting investments from multinational corporations. This situation was particularly evident in Indonesia’s increased net FDI in 2019, coinciding with a rise in per capita income. At the same time, trade openness notably influenced FDI in Malaysia and Thailand in the short term, aligning with the findings of Tang et al. (2014). This outcome underscored the significance of open trade policies for drawing foreign investment, particularly in critical sectors such as automotive and electronics. Finally, the error correction term’s negative and statistically significant coefficient (ECTt−1) underscored the rapid adjustment towards long-term equilibrium.

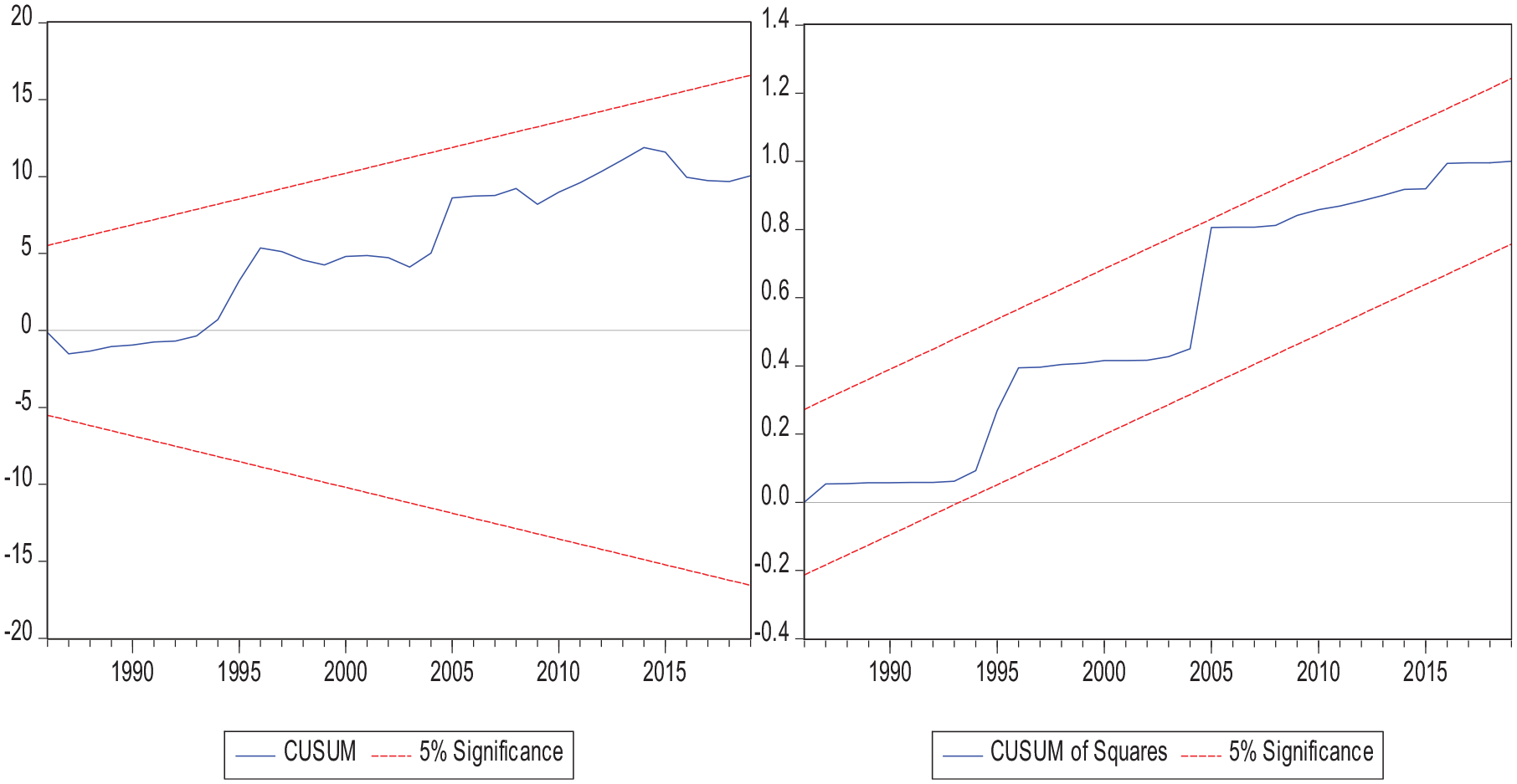

The present study’s findings highlighted a clear positive correlation between a high proportion of renewable energy and FDI inflows in Indonesia and Malaysia. This outcome suggested an emerging trend wherein renewable energy attractiveness has played a significant role in investment decisions in these countries. The crucial role of per capita income in Malaysia and the Philippines and the universal influence of trade openness across the ASEAN 4 nations were notable. These findings validated the theoretical propositions in this study’s earlier sections and suggested a nuanced understanding of FDI determinants in these economies. Moreover, the stability of the model’s residuals, as confirmed by the CUSUM and CUSUM of Squares tests (Figure 4, 5, 6 and 7) within the 5% confidence interval, underscored the robustness of this study’s estimations.

Indonesia – stability testing – CUSUM and CUSUM of squares tests.

Malaysia – stability testing – CUSUM and CUSUM of squares tests.

Philippines – stability testing – CUSUM and CUSUM of squares tests.

Thailand – stability testing – CUSUM and CUSUM of squares tests.

Robustness Check

The present study initiated a comprehensive re-evaluation to validate the analytical model’s robustness and dependability. This process involved a methodological refinement where the conventional metric – FDI inflows were substituted as a percentage of GDP – with a more granular and direct metric, namely Net FDI Inflows in US$. This strategic shift in measurement was pivotal in elucidating the influence of renewable energy utilisation on Foreign Direct Investment within the ASEAN 4 nations. This empirical investigation, detailed in Tables 6 and 7, unequivocally corroborated a sustained, long-term cointegrative relationship across the countries studied. This finding was pivotal, as it reinforced this study’s preliminary conclusions and delineated a consistent and statistically significant interrelation between renewable energy adoption and FDI inflows. Notably, Table 6 reveals a significant long-term influence of renewable energy on FDI in Indonesia and Malaysia. Conversely, this relationship was not statistically significant in the Philippines and Thailand. These nuanced outcomes align with the previous findings in Tables 4 and 5, augmenting the present research’s integrity and reliability.

Long-Run Cointegration and Serial Correlation LM Test – Robustness Checks (Dependent Variable: Nett FDI Inflows (US$)).

Note. The cointegration test statistics were assessed by comparing them to the critical values documented in Narayan (2005) study for datasets with fewer than 100 observations. Serial (1) and Serial (2) refer to the Breusch-Godfrey LM test statistics without serial correction. The values inside parentheses represent the p-values, while *, **, and *** signify statistical significance at the 10%, 5%, and 1% confidence levels, respectively.

ADRL Estimation Results -Robustness Checks (Dependent Variable: Nett FDI Inflows (US$)).

Note. FDI corresponds to Net FDI inflows in US$, RNEW indicates the proportion of energy derived from renewable sources, RGDPC signifies the real GDP per capita, and TO stands for trade openness. The coefficients presented are the T-statistics acquired through the Eviews software application. This study employed a maximum lag length of four for the analysis. The urbanisation rate of Singapore was omitted from the model because Singapore is already a highly urbanised country. The optimal lag structure for the ARDL model was selected based on the Akaike Information Criterion (AIC). Significance levels are denoted by ***, **, and *, representing the 1%, 5%, and 10% significance levels, respectively.

Impact of Renewable Energy Policies on Foreign Investment Attraction

The gathered empirical evidence underscored renewable energy initiatives’ significant long-term positive influence on Foreign Direct Investment (FDI) in Indonesia and Malaysia. This correlation resonated with the global movement towards green energy investment, notably in emerging markets. The analysis further dissected the renewable energy strategies of both nations, shedding light on their success in garnering the attention of foreign investors. This success indicated a broader trend in which progressive energy policies have increasingly been a marker of a country’s overall investment potential.

In Malaysia, the evolution of renewable energy (RE) policies, tracing back to the 1980s, has positioned the country as a progressive hub for RE investment (Rajah et al., 2022). Early adoption of solar photovoltaic systems and the Small Renewable Energy Power (SREP) programme in 1999 has been foundational in establishing a comprehensive RE infrastructure in the country. Additionally, initiatives like the Biogen Full Scale Model and fiscal incentives since 2000 have played pivotal roles in amplifying investor interest by reducing financial risks and demonstrating government backing. A solid regulatory framework, including the Feed-in Tariff system, has created a stable and predictable investment climate. Malaysia’s concerted efforts in these areas have highlighted the importance of governmental foresight and strategic planning in attracting FDI. Malaysia’s RE policy encompasses a strategic vision to bolster energy security and socioeconomic development through sustainable measures. The emphasis on human capital investment, research, innovation, advocacy programmes, and legal frameworks such as the RE Law and RE Fund have fortified investor confidence. The long-term goals for 2050, focussing on environmental conservation and competitive RE generation costs, align with global sustainability targets, further endorsing Malaysia as a lucrative destination for RE investment. This strategic approach has underlined how multifaceted policies, beyond just economic incentives, can make a country an attractive destination for foreign investment.

Indonesia’s RE sector has become a focal point for FDI, backed by a comprehensive legal framework and evolving energy policies that provide clarity and legal safeguards for investors (East Asia Forum, 2023). The government’s commitment, as evidenced in the National Determined Contributions for COP26 and renewable energy bill, aims to increase the share of renewable energy and reduce fossil fuel dependency by 2050. The country’s vast potential in geothermal, solar, and wind energy, significant investment targets, and policies favouring full foreign ownership have marked Indonesia as a promising market for transformative RE investments. Indonesia’s approach has demonstrated a clear understanding of the global shift towards sustainable energy and its potential economic benefits. Moreover, Indonesia’s strategic implementation of policies, such as the renewable energy bill and the National Determined Contributions, aligns with international environmental goals and showcases the country’s readiness to adapt to global energy trends. This adaptive approach is crucial for countries looking to attract FDI, as it signals resource availability and a commitment to long-term environmental and economic sustainability. Indonesia’s focus on harnessing its geothermal, solar, and wind energy potential has also highlighted the importance of leveraging natural resources sustainably to attract foreign investments.

The lack of a similar positive trend in the Philippines and Thailand can be attributed to various factors, including less favourable renewable energy policies and infrastructural challenges (Bertheau et al., 2020; Lopez, 2023; Sirasoontorn & Koomsup, 2017). Policy fragmentation and instability in Thailand have impeded FDI in the RE sector. Despite having laws and renewable energy plans since 1992, the slow progress has been attributed to fragmented responsibilities among various agencies and conflicting interests of state-owned enterprises, especially in the solar power sector. Similarly, in the Philippines, despite the Renewable Energy Act of 2008, the transition to renewable energy has faced setbacks, with a decline in the reliance on renewable energy sources and challenges in implementing policies like FiT and GEAP. These contrasting outcomes in the Philippines and Thailand have highlighted the complexity of implementing renewable energy policies effectively. In Thailand, the lack of a unified vision and conflicting interests among different governmental bodies have created an environment of uncertainty, discouraging FDI. The Philippines, facing similar issues, has also illustrated how the gap between policy formulation and practical implementation can result in missed opportunities for attracting foreign investments. These cases have underscored the importance of establishing renewable energy policies and ensuring their cohesive implementation and adaptation to changing market dynamics.

In summary, Indonesia and Malaysia’s success in attracting FDI in the renewable energy sector has been a testament to their long-term policy commitments, comprehensive frameworks, and untapped renewable energy resources. These countries have established a stable investment climate, fostering investor confidence. In contrast, the Philippines and Thailand have faced challenges due to policy fragmentation and regulatory issues, leading to an unfavourable environment for attracting FDI in the renewable energy sector. This analysis has underscored the pivotal role of coherent, supportive renewable energy policies in attracting foreign investment, highlighting the effective strategies of Malaysia and Indonesia and the impediments faced by the Philippines and Thailand. It also has underscored the importance of addressing policy fragmentation and regulatory hurdles to unlock the potential for renewable energy investment in emerging markets.

Conclusion

This comprehensive study has underscored the significant correlation between the adoption of renewable energy and the enhancement of Foreign Direct Investment (FDI) inflows, with a particular focus on the ASEAN economies of Indonesia and Malaysia. Through the meticulous application of the Autoregressive Distributed Lag (ARDL) model, initially introduced by Pesaran et al. (2001), the findings supported and extended the insights of Parab et al. (2020), illustrating that well-orchestrated renewable energy strategies are highly attractive to international investors, particularly in sectors focussed on sustainability. Furthermore, the analysis has shed light on the positive impact of rising real per capita income on FDI attractiveness in Malaysia and the Philippines, suggesting a multifaceted economic landscape influencing investment trends.

This research’s implications are profound and actionable for stakeholders within the ASEAN region. The apparent association between renewable energy adoption and FDI inflows, especially in Indonesia and Malaysia, has underscored the tangible economic and environmental benefits of shifting towards more sustainable energy sources. This relationship is emblematic of the successful implementation of comprehensive renewable energy strategies, which include legislative support, financial incentives, and a strong emphasis on innovation (IEA, 2021). Such frameworks serve as a blueprint for attracting long-term foreign investments and a guideline for other ASEAN nations aiming to enhance their appeal to green energy investments.

In addition to highlighting the critical role of trade openness and the effectiveness of regional free trade policies in driving FDI – a notion reinforced by UNCTAD (2021) through Singapore’s success – the research has emphasised the importance of public awareness, education, and structured administrative and financial frameworks in fostering the growth of renewable energy projects. These elements are crucial for creating a conducive environment for the adoption and expansion of renewable energy, aligning with the International Energy Agency’s recommendations (IEA, 2021) and supported by various studies, including those by Papathanasiou (2022) and reflected in the Asian Development Outlook (2019).

The present study also suggests strategic pathways for ASEAN countries to attract more FDI, focussing on developing green financing mechanisms and investment incentives tailored to renewable energy projects. Emphasising the importance of initiatives like the ASEAN Catalytic Green Finance Facility and the role of green bonds and low-interest loans, it points to a substantial opportunity for growth in green finance – a critical component for meeting the extensive investment needs of the region’s sustainable development agenda.

In conclusion, the research advocates for enhanced regional cooperation and the pursuit of a unified regional grid for renewable energy, a strategy that promises to bolster energy security and create a stable and cooperative investment environment. By aligning with the visions outlined in the ASEAN Renewable Energy Outlook, this approach underscores the indispensable role of renewable energy in securing the region’s developmental and economic future, positioning ASEAN as a leader in sustainable growth and an attractive hub for foreign investment in the green economy.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project received funding from the Universiti Malaya Partnership Grant (MG026-2022). Additional support was provided by Universitas Sebelas Maret under the 2024 International Research Collaboration scheme, contract number 194.2/UN27.22/PT.01.03/2024.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analysed during the current study.